lupin - ic - business...

TRANSCRIPT

1January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 1

LupinInitiating Coverage

Stock Info

ACCUMULATEPrice Rs979

Target Price Rs1,112

Investment Period 12 Months

Sector Pharmaceutical

Market Cap (Rs cr) 8,261

Beta 0.4

52 Week High / Low 1020 / 518

Avg Daily Volume 54564

Face Value (Rs) 10

BSE Sensex 15,412

Nifty 4,580

Shareholding Pattern (%)

Promoters 50.4

MF / Banks / Indian FIs 26.1

FII / NRIs / OCBs 13.9

Indian Public / Others 9.6

Abs. 3m 1yr 3yr

Sensex (%) 29.8 4.7 36.2

Lupin (%) 30.7 32.0 100.2

BSE Code 500257

NSE Code LUPIN

Reuters Code LUPN.BO

Bloomberg Code LPC@IN

Source: Company, Angel Research

Key Financials (Consolidated)Y/E March (Rs cr) FY2008 FY2009 FY2010E FY2011E

Net Sales 2,706 3,776 4,596 5,094

% chg 34.4 39.5 21.7 10.8

Net Profit 408.3 501.5 635.4 704.8

% chg 32.3 22.8 26.7 10.9

EPS (Rs) 49.7 60.6 71.6 79.4

EBITDA Margin (%) 16.1 17.2 18.5 18.7

P/E (x) 19.7 16.2 13.7 12.3

RoE (%) 37.9 37.1 34.6 28.0

RoCE (%) 25.4 25.0 26.7 24.1

P/BV (x) 6.3 5.7 3.9 3.1

EV/Sales (x) 3.3 2.5 2.1 1.9

EV/EBITDA (x) 14.0 12.4 10.4 9.1

All guns (geographies) blazingLupin is one of the best plays in the generic space given its strong execution capabilities,improving financial performance and diversifying business model. Lupin registered stellar growthin Top-line and Bottom-line during FY2006-09. Going ahead, we expect Lupin to extend itsrobust growth albeit on a high base and clock 16.2% and 18.5% CAGR in Top-line andBottom-line respectively, over FY2009-11E. At Rs979, the stock is trading at 13.7x FY2010Eand 12.3x FY2011E Earnings, which is at 17-35% discount to its larger peers, which we believeis unwarranted. However, owing to the Mandideep issue, we have valued Lupin at 14x(Mid-cap multiple) FY2011E Earnings. But, we believe that Lupin has the potential to getre-rated once uncertainty over Mandideep gets cleared. We recommend an Accumulate onthe stock, with a Target Price of Rs1,112.

To register growth across geographies: In the US, Lupin has a value-based productpipeline. To mitigate volatilities in price erosion in the pure Vanilla Generic Segment, Lupin hasalso built a formidable presence in the Branded Generic Segment. Going ahead, we estimateLupin to register 22.2% CAGR in the US markets over FY2009-11E to Rs1,768.8cr. In theIndian market, we expect its Domestic Formulation sales to post a CAGR of 17.0% overFY2009-11E to Rs1,562.1cr. In Japan, we believe that Lupin is probably the best placed Indiancompany to benefit from the expected break-out there. Hence, we expect Lupin to register astrong 21.7% CAGR in the Japanese market over FY2009-11E to Rs655.5cr. In Europe, weexpect Lupin to post a CAGR of 37.3% to Rs201.9cr over FY2009-11E albeit on a low base.

Strong Balance Sheet: Lupin has one of the better Balance Sheets in the Pharma Sectorwith Net Debt/Equity of 0.8x (including FCCBs) and RoCE of 25.0% as on FY2009 given thescale up in the last four years (Top-line up 3x, Bottom-line up 5x). Moreover, with its balanceFCCBs of US $61mn also likely to get converted to equity and increasing operating cash flow,we expect Lupin's Net Debt/Equity to decline to 0.3x in FY2011E.

Mandideep overhang on stock persists: Management expects re-inspection of the facilityby US FDA to be completed in the near term and seeks to resolve the matter. Lupin sellsCephalosporin products in the US from this facility. However, furtther adverse action by theUS FDA may lead to marketshare erosion for non-Ceph products as witnessed by other players.

Sushant Dalmia

Tel: 022 - 4040 3800 Ext: 320

E-mail: [email protected]

Sarabjit Kour Nangra

Tel: 022 - 4040 3800 Ext: 343

E-mail: [email protected]

2January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 2

Lupin

Pharmaceutical

Company Background

Lupin, established in 1968, is primarily engaged in the manufacture and global distribution ofactive pharmaceutical ingredients (APIs) and finished dosages. Over the years, Lupin has movedup the value chain and successfully transformed from being an Intermediaries and API player to arobust Formulation player. As of FY2009, Formulations accounted for 81% of its Total Salesincreasing from 51% in FY2006. Moreover, the company has gained recognition as the world'slargest manufacturer of Anti-TB drugs. Besides, the company also has significant presence in theCephalosporin, Cardiovascular (Prils and Statins), Diabetology, Asthama and NSAIDs TherapySegments. Further, Revenue contribution from Exports has also increased to 66% in FY2009 from50% in FY2006.

Source: Company, Angel Research

Exhibit 1: Sales Break-up (%, FY2009)

Formulation Sales constituted81% of FY2009 Total Salesincreasing from 51% in FY2006

81

19

Formulation APIUS Japan Europe

India Other Markets API & CRAMS

31

12

3

29

6

19

The US, where the company has developed a robust branded and generic business, forms thelargest overseas market for Lupin. In CY2003, Lupin entered the US market with the launch ofCefuroxime Axetil. The company set the ball rolling with the introduction of its first brand Suprax in2004, while its Generic business gained momentum in 2005. As a result, Lupin managed to growits Revenue in the US market by almost 5 times in the last three years to US $273mn. Thus, theUS contributed almost one-third to the company's Net Sales as in FY2009. Further, the company'spresence in the Branded Generic space (US $74m sales) has also been a key differentiator amongstthe second-tier Indian generic companies targeting the US market.

Lupin now aspires to replicate its success in the US markets in other advanced markets as wellincluding the Europe, Japan and Australia. In accordance with the same, during the last two years,Lupin fast tracked its growth trajectory in the mentioned markets through six acquisitions. As aresult, the company managed to gain access to Japan, Germany, Australia, South Africa, thePhilippines region as well as the CRAMS space. While acquisition of Kyowa catapulted thecompany to rank among the Top-ten generic pharma companies in Japan.

Lupin's Revenues grew byalmost 5x in the US marketsduring the last 3 years andcontributed almost one-thirdto the company's Total NetSales in FY2009

3January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 3

Lupin

Pharmaceutical

To expand its foot-print in the global market, Lupin has prudently adopted the inorganic growthroute. In line with this, over the last two years, the company made small acquisitions acrossgeographies prominent among these being the acquisition of Kyowa in the growing Japanesemarket. We believe that Lupin's strategy to acquire relatively smaller companies to get a footholdin new geographies is paying off compared to its larger peers, who made bigger ticket sizeacquisitions. Till-date, Lupin has incurred Rs4,52.2cr towards its various acquisitions done in thelast two years with majority being spent for acquiring Kyowa in Japan.

We believe Lupin's strategy toacquire relatively smallercompanies to get a foothold innew geographies is paying offcompared to its larger peers,who made bigger ticket-sizeacquisitions

Source: Company, Angel Research. Note: * Sales are from the respective date of completion of acquisition till March2009

Exhibit 2: Acquisitions done over the last two years

Lupin is also scouting for acquisitions in the GCC, Latin America and Japan regions to be fundedthrough internal accruals.

Lupin's Domestic Formulation business has recorded robust growth over the last few years evensurpassing Industry. The company has also widened its product basket to include a mix of brandedand value-added generics apart from foraying into newer Therapeutic Segments such asGynaecology, Oncology and Wound Management. Simultaneously, the company has also focusedon garnering marketshare in the Anti-Asthma, Cardiovascular, Diabetes and other ChronicSegments, while maintaining its dominant position in the Anti-TB and Anti-Infective Segments.Lupin forayed into the CRAMS Segment with the acquisition of Novodigm.

The company's manufacturing facilities are approved by international regulatory agencies such asthe US FDA, UK MHRA, TGA Australia, WHO and MCC South Africa. Lupin incurs 6-7% of Salestowards R&D expenditure and has an intellectual pool of over 500 scientists focused on NCE andNDDS programmes.

Company Key Benefits Acquisition FY2009 Stake (%)Cost (Rs cr) Sales (Rs cr)

Kyowa Access to one of the rapid growing 2,48.2 4,36.8 100.0generic market Japan.

Novodigm Access to CRAMS space 37.3 67.6 100.0Hormosan Access to Germany with a rich portfolio 31.1 17.4 100.0Pharma* on the CNS SegmentGeneric Health Access to Australia market 20.4 n.a. 36.7Pharma Access to South Africa with a leadership 90.1 91.9 60.0Dynamics* position in CVS Segment.Multicare Access to Philippines region 25.0 1.4 51.0Pharma*

4January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 4

Lupin

Pharmaceutical

Source: Company, Angel Research

Exhibit 3: Infrastructure Fact-setAPI & Intermediaries Product/Segment Approved byTarapur, India Rifampicin, Lovastatin US FDA, WHOMandideep, India Cephalosporins, Prils WHO, US FDA, UK MKRAAnkleshwar, India Ethambutol Intermediates WHOVadodara, India CRAMSFormulationsKyowa, Japan NA MOH (Japan)Goa, India Non- Cephalosporin Oral

Finished Dosage US FDA, UK MHRAAurangabad, India Anti -TB, Lisinopril WHOMandideep, India Cephalosporins, Prils WHO, US FDA, UK MKRAJ&K, India Oral Finished DosageIndore, India NA Approvals in Pipeline

5January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 5

Lupin

Pharmaceutical

Investment Arguments

To register growth across geographies

Lupin registered stellar growth during FY2006-09 with its Formulation Sales in the US and Indiaposting 74.2% CAGR to Rs1,184.6cr and 22.9% to Rs1, 141.2cr, respectively.

To expand its foot-print in the global markets, Lupin has prudently adopted the inorganic growthroute, and over the last two years made small acquisitions across geographies. We expect Lupinto register 16.2% and 18.5% CAGR in Top-line and Bottom-line respectively, over FY2009-11E.

In the US, Lupin has a value-based product pipeline and has built a formidable presence in theBranded Generic Segment. Going ahead, we estimate the company to register 22.2% CAGR inthe US markets over FY2009-11E to Rs1,768.8cr. In the Indian market too, we expect itsDomestic Formulation sales to post a CAGR of 17.0% over FY2009-11E to Rs1,562.1cr. In theJapanese Generics market, we believe that Lupin is probably the best placed Indian company tobenefit from the expected break-out there. Hence, we expect Lupin to register a strong 21.7%CAGR in the Japanese market over FY2009-11E to Rs655.5cr. In Europe, Lupin aspires toreplicate its success of the US market. We expect Lupin to post a CAGR of 37.3% to Rs201.9cr inEurope over FY2009-11E albeit on a low base.

US Market: The key growth driver

Lupin's US business grew 5x during FY2006-09 to register Sales of US $273mn, and is currentlythe largest Indian company in terms of prescription. The company's Revenue per product standsat US $11, which is the highest among its Indian peers in the US markets.

We expect Lupin to register16.2% and 18.5% CAGRin Top-line and Bottom-linerespectively, over FY2009-11E

We estimate the company toregister 22.2% CAGR in theUS markets over FY2009-11E

Source: Company, Angel Research

Exhibit 4: Sales Break-up

Lupin has also been successful in garnering marketshare in competitive products. In fact, Lupin isthe fastest growing generic company in the US and the Ninth largest generic player in the US byprescription.

0

50

100

150

200

250

300

350

400

450

FY2006 FY2007 FY2008 FY2009 FY2010E FY2011E

US Branded US Generic

51

178

273

345

385

CAGR 48%

78

US

$(M

n)

6January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 6

Lupin

Pharmaceutical

Source: Company Reports, Angel Research

Exhibit 5: Market Prescription Share (Dec 2008)

Management expects to file25-30 ANDAs in the US everyyear going forward

23.1

12.5

7.8 7.7

3.9 3.8 3.6 3.4 3.0 2.5 2.1 2.1 2.1 1.9 1.6

0.0

5.0

10.0

15.0

20.0

25.0

Teva

/Ba

rr

Myl

an

Sa

nd

oz

Wa

tso

n

Ma

llin

ckro

dt

Ap

ote

x

Co

rp

Qu

alit

est

Gre

en

sto

ne

Act

avi

sU

S

Lu

pin

DR

L

Pa

r

Ra

nb

axy KV

Le

nn

ett

%

Lupin's success in the US market can be attributed to vertical integration, differentiated productportfolio and strong supply channels. Notably, Lupin has a well-differentiated, value-basedproduct pipeline with a clear focus on controlled release, exclusive and unique FTF Para IV andother niche filings. Till date, Lupin has filed around 90 ANDAs with most of them being potentiallylow competition products/Para IV challenges. In FY2009, Lupin filed 28 ANDAs (after sluggishfilings in FY2008) with 5FTFs of which 2 are potential exclusive FTF opportunities. Managementexpects to file 25-30 ANDAs every year going forward.

Source: Company, Angel Research. Note: For Ranbaxy figures are CY ending.

Exhibit 6: Comparative ANDA filings

Going ahead, we estimate the company to register 22.2% CAGR in the US markets overFY2009-11E to Rs1,768.8cr.

Generic Business: Gaining marketshare

In FY2009, Lupin registered 35.6% yoy surge in its US Generic business to US $199mn Sales.This was a remarkable performance as the company managed to achieve these sales from mere22 products. Moreover, Lupin currently holds Top 3 position, in terms of marketshare, for 18 of itsproducts. In FY2009, Lupin also expanded its product portfolio with the launch of Ramiprilcapsules, Divalproex DR tablets, Cefadroxil suspension/capsules and Levetiracetam tablets.

Lupin holds the Top 3 positionin terms of marketshare for 18of its products in the USmarket

2224

4548

37

2628 28

6 6

13 12

33

19 20

13

1815

11

28

0

10

20

30

40

50

60

FY2005 FY2006 FY2007 FY2008 FY2009

Sun Ranbaxy Dr Reddy’s Lupin

Ramp-up in

FY2009

7January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 7

Lupin

Pharmaceutical

We believe that Lupin has been able to capitalise on its strong backward integration initiatives andstrong supply chain to garner marketshare in an already genericised market. Pertinently,marketshare of Cefprozil OS increased from 46% in FY2008 to 66% in FY2009 while CefprozilTabs witnessed an increase in marketshare by 9% to 39%. In case of Lisnopril tablets and HCTZtablets, the company was able to increase marketshare by 6-7%. Ramipril capsule was ablecapture 45% marketshare in the first year of its launch.

We believe Lupin would continue its strong show on the Generic front by growing at a CAGRof 19.3% over FY2009-11E to Rs1,223.9cr on back of new product launches.

Para IVs to contribute from FY2012

In the past few years, Lupin has been targeting FTF opportunities in the US. In FY2009, thecompany filed 5 FTFs of which 2 are exclusive FTF opportunities for the generic version of FortametER (Metformin ER) and Antara (Fenofibrate tablets). We believe that the company could have apotential FTF status for the generic version of Niacin, Renagel and Fosrenol. On other Para IVopportunities, Lupin arrived at a successful settlement on Effexor XR with Wyeth, the innovator,and will launch the product by June 2011. In case of Clarinex, Lupin has entered into a settlementwith Schering-Plough and will launch the generic version of the product by July 2012.

In FY2009, the company filedfor 5 FTF of which 2 areexclusive FTF opportunitiesfor the generic version ofFortamet ER (Metformin ER)and Antara (Fenofibratetablets)

Source: Company, Angel Research

Exhibit 7: Key Products - Marketshare (%)

FY2008 FY2009

34

23

46

3033

41

29

45

34

66

3944

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Lisn

opril

Tabs

Lisn

opril

HC

TZ

Tabs

Ram

ipril

Cap

s

Cef

adro

xil O

S

Cef

proz

ilO

S

Cef

proz

ilTa

bs

Mel

oxic

amTa

bs

8January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 8

Lupin

Pharmaceutical

Exhibit 8: Para IV opportunitiesBrand Generic Innovator Sales in US Comment

($ mn, 2008)PotentialFTFsAntara Fenobirate Oscient 70 Lupin is the exclusive FTF holder. The

company could enjoy 6 months exclusivity ifit successfully invalidates the patent. Patentis scheduled to expire in August 2020

Niacin Niaspan Abbott 786 Lupin has been sued by the Innovator. Webelieve it has an FTF status as no othercompany has been sued. Patent isscheduled to expire in Sept 2013

Renagel Sevelamer Genzyme 678 Lupin seems to have the FTF status as it isHydrochloride the first generic company to get sued by the

Innovator. Lupin could be able to enjoy thesix months exclusivity if it successfully invalidate the existing patent. Impax is othergeneric player which has been sued postLupin. Patent is scheduled to expire inAugust 2013

Fosrenol Lanthanum Shire 86 Natco (tie-up with Lupin) has been suedCarbonate along with Barr and Mylan. Patent is

scheduled to expire in Oct 2018.We believeNatco alongwith Lupin could be the FTFholder and enjoy the six month exclusivity ifit successfully invalidates the patent.

Other Para IVsCymbalta Duloxetine Eli Lilly 2,253 Lupin has been sued along with 7 other

generic players. Patent is scheduled toexpire in June 2013.

Namenda Memantine Forest 949 Lupin has been sued by the innovator. Teva,hydrochloride Sun Orchid, Apotex and Wockhardt have

also been sued. Patent is scheduled toexpire in April 2015.

Combivir Lamivudine GSK Pharma 290 Lupin has been sued along with Teva. Thepatent is scheduled to expire in CY2012.

SettledEffexor Venlafaxine Wyeth 3,010 Lupin has settled with Wyeth to launch the

product in June 2011. Wyeth has alsosettled with Teva and Impax.

Clarinex Desloratadine Schering 329 Lupin has been able to settle the law suitPlough with the Innovator and plans to launch the

product by July 2012. Schering Plough hassettled with more than 10 generic players.

Source: Company Reports, Angel Research

9January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 9

Lupin

Pharmaceutical

Branded Generic: The key differentiator

To mitigate volatilities in price erosion in the pure Vanilla Generic Segment, Lupin entered theBranded Generic Segment in the US. Lupin is among the few Indian companies to have successfullypenetrated the highly competitive US Branded market. In FY2009, Lupin's Branded Sales spiked134.9% to US $74mn on the back of the continuous strong showing by Suprax and launch ofAeroChamber in alliance with Forest Laboratories.

Suprax

The company re-launched Suprax, a pediatric anti-infective, in FY2004 by licensing it from Fujisawasince its US partner (Wyeth) had stopped promoting the drug since 2003. Since Suprax is anoff-patent drug, the threat of generic competitors remains high. Therefore, Lupin launched doublestrength Suprax suspension and tablets, which will not only help it increase marketshare in theUS $450mn Antibiotic market, but also reduce possibility of generic competition to some extent.Further, Lupin also extended Suprax to the adolescent and teenage population as well. Hence,the company has been able to move around 50% of volumes to other dosage forms from theoriginal 100mg suspension. The Suprax basket now comprises oral suspension of 100mg/5ml,200mg/5ml and 400mg tablets. To reduce its dependence on Suprax, which is likely to facecompetition from FY2011E, and leverage it existing field force of 60 personnel, Lupin plans to sellmore branded products in the market.

AeroChamber

In FY2009, Lupin entered into a strategic alliance with Forest Labs to promote AeroChamber Plusin the US market. As per the agreement, Lupin would use it existing field force to promoteAeroChamber among the pediatricians.

AllerNaze

In 1QFY2010, Lupin announced acquisition of worldwide rights of the intra-nasal steroid (INS)product, AllerNaze (triamcinolone acetonide, USP) Nasal Spray, 50mcg, from CollegiumPharmaceutical, Inc. AllerNaze is an aqueous based intranasal steroid indicated for the once dailytreatment of nasal symptoms associated with both Seasonal Allergic Rhinitis (SAR) and PerennialAllergic Rhinitis (PAR) in adults and children twelve years of age and older. In the US, SAR is themost common allergic disease and is increasing in prevalence. Approximately 40 million Americanssuffer from this condition. The product will compete in the approximately $2.5bn a year US marketfor INS products for the treatment of allergic rhinitis.

Exhibit 9: Global Sales of Intra Nasal SteroidsInnovator Brand Molecule US $mnSchering Plough Nasonex Mometasone 1,198Sanofi Aventis Nasacort AQ Triamcinolone acetonide 337AstraZeneca Rhinocort Aqua Budesonide 322

Source: Company, Angel Research

Lupin has been able to movearound 50% of volumes toother dosage forms from theoriginal 100mg suspension

10January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 10

Lupin

Pharmaceutical

The US FDA has already approved AllerNaze. The safety and efficacy of AllerNaze in both SARand PAR have been well established in 14 controlled clinical trials involving almost 1,200 subjects.The studies assessed safety and effectiveness of AllerNaze in treating the symptoms (runny nose,nasal itching, sneezing and nasal congestion) in patients with allergic rhinitis.

We believe that in case of AllerNaze Lupin will closely compete with Sanofi Aventis's Nasacort AQspray (same molecule), which recorded global Sales of US $337mn in CY2008 with the UScontributing around 72% of Sales. Previously indicated for the treatment of the nasal symptoms ofseasonal and perennial allergic rhinitis in adults and children six years of age and older, NasacortAQ received additional approval for the seasonal and annual treatment of children between 2 - 5years of age from the FDA in September 2008. However, in November 2008, Sanofi Aventissettled the patent litigation with Barr, where in Barr granted license to sell a generic triamcinoloneacetonide in the US as early as June 2011. Lupin expects to launch the molecule in 2HFY2010 inthe US and later in the other parts of the world. We believe that the move is positive as it will helpthe company reduce its dependence on Suprax within the Branded Generic space and leverageits existing field force in US. The company also plans to increase its field-force to 100 from thecurrent 60 by end FY2010.

This deal (financial details are awaited) signifies Lupin's growing presence in the global markets.However, Lupin has capitalised the upfront payment made to Collegium Pharmaceutical and alsoplans to capitalise any future milestone payments. We have factored in AllerNaze sales in the USFY2011E onwards and expect it to register Sales of US $27.6mn and healthy OPM of 35%. Weexpect the Branded Generic segment to grow at a CAGR of 29.6% to Rs544.8cr as the companywidens its branded product basket.

Oral Contraceptive and Ophthalmology Segments to be new focus areas

In FY2009, the company entered the high-barrier Oral Contraceptive (OC) space in the US withthe filing of 7 OC ANDAs and associated DMFs. The generic OC market is estimated at US $3bnand is growing in low teens with limited competition (Teva (through Barr), Watson are the currentgeneric players in the market). Recently, Warner Chilcott announced that it has received two ParaIV certification from Lupin for generic version of its oral contraceptives, Loestrin 24 FE and FemconFE. Loestrin 24 FE has Annual Sales of US $197.2mn (patent expires in July 2014) while FemconFE clocked US $45.8mn (patent expires in April 2019). Lupin also proposed to target theOphthalmology space for future growth in the US markets.

Japan: Early mover advantage

Japan is a US $65bn market of which generic comprises 5% in value terms. The Japanesegovernment has been taking aggressive measures to boost its generic market. Over the last twoyears, the government of Japan has ushered in a series of reforms on the back of which thecountry's generic market is expected to register 30% growth in volume terms and touch US $6.5bnin value terms by CY2012E.

Warner Chilcott announcedthat it has received two ParaIV certification from Lupin forgeneric version of Warner'soral contraceptives, Loestrin24 FE and Femcon FE

11January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 11

Lupin

Pharmaceutical

Kyowa is the seventh largestplayer in the generic space inJapan

Lupin forayed into the Japanese market with the acquisition of Kyowa Pharmaceutical in October2007. Kyowa is the seventh largest player in the generic space in Japan with a rich portfolio inPsychiatric and Neurological Therapeutic Segments as well as in CVS, Respiratory, Allergic andDigestive System. Kyowa, which has sales force of 55, recorded a turnover of US $95mn inFY2009, up 21% as against the industry growth rate of 13%. Kyowa launched 10 products inFY2009 and is now market leader in Risperidone, in volume terms.

We believe that Lupin is probably the best placed Indian company to benefit from the expectedbreak-out in the Japanese generics market. Additionally, Lupin expects to back-end productionfrom Japan to India within the next two years. The company is also looking at in-licensing and APIsourcing avenues for the Japanese market. Notably, Lupin managed to expand its Gross Marginin Japan by 5% in FY2009. Going ahead, in FY2010E, Lupin plans to launch 5-6 products inJapan. Overall, we expect Lupin to register a CAGR of 21.7% over FY2009-11E to Rs655.5cr inJapan.

Europe: Building blocks

Lupin aspires to replicate its successful foray in the US market in the European market as well.The company's product portfolio for Europe includes products in the Anti-Infective, CVS and CNSSegments. Lupin launched Lisnopril in the UK in FY2008, which now commands marketshare of15%. Cefpodoxime Proxetil tablets were launched in France in FY2008, which now commands65% marketshare. The company is also looking at launching several new products and has astrong pipeline of 22 MAAs, and received approval for Trandolapril and Perindopril tablets in FY2009.

Lupin acquired Hormosan Pharma, Germany in FY2009. This was the company's first acquisitionin the European market. Hormosan specialises in the supply of pharmaceutical products for theCNS Segments, develops and markets a range of generics in the European market. Lupin throughHormosan has successfully won the AOK bid for one product, viz. Setraline in all the five regionsof Germany.

The company's total filings across the EU market stands at 54. Going forward, the companyintends to have close to 15 filings every year in the EU. We expect Lupin to post a CAGR of 37.3%over FY2009-11E on account of the low base to Rs201.9cr.

Lupin's total filings across theEU market stands at 54. Goingforward, the company intendsto have close to 15 filingsevery year in the EU

We believe that Lupin is thebest-placed Indian company tobenefit from the expectedbreak-out in the Japanesegeneric space

Source: Company, Angel Research. Note: * Sales are from the respective date of completion of acquisition

Exhibit 10: Sales Trend in Japan

0

100

200

300

400

500

600

700

FY2008*

Rs

cr

132

442

558

656

FY2009 FY2010E FY2011E

12January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 12

Lupin

Pharmaceutical

Source: Company, Angel Research

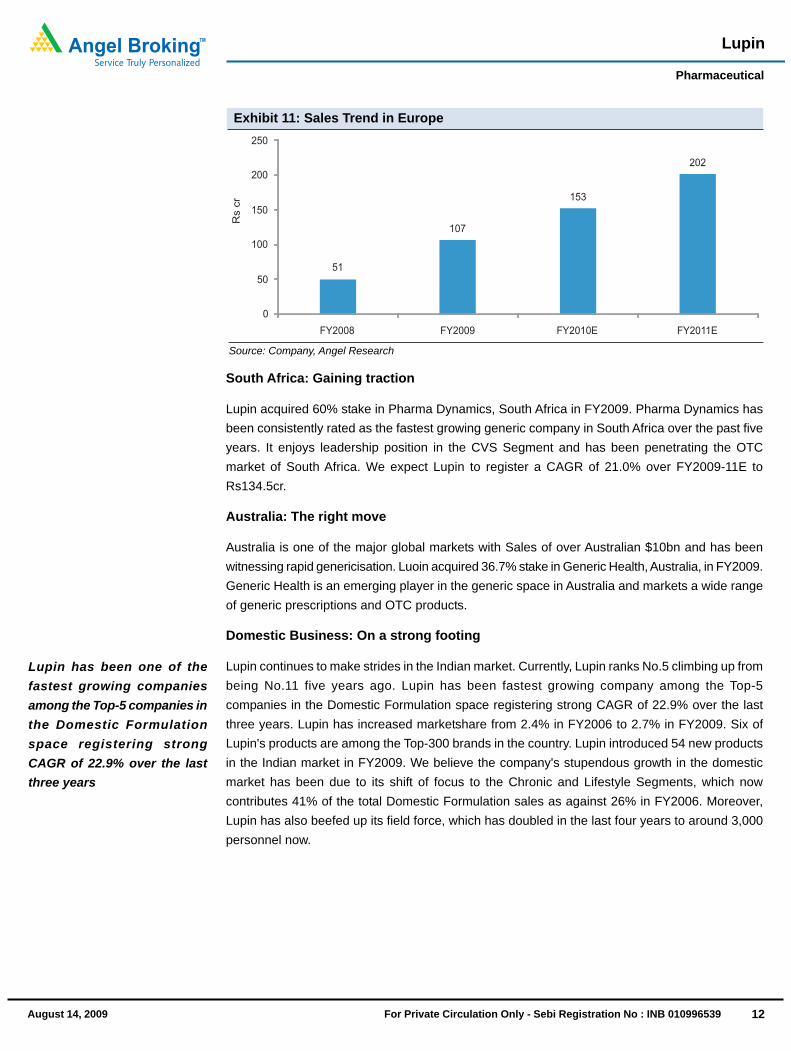

Exhibit 11: Sales Trend in Europe

South Africa: Gaining traction

Lupin acquired 60% stake in Pharma Dynamics, South Africa in FY2009. Pharma Dynamics hasbeen consistently rated as the fastest growing generic company in South Africa over the past fiveyears. It enjoys leadership position in the CVS Segment and has been penetrating the OTCmarket of South Africa. We expect Lupin to register a CAGR of 21.0% over FY2009-11E toRs134.5cr.

Australia: The right move

Australia is one of the major global markets with Sales of over Australian $10bn and has beenwitnessing rapid genericisation. Luoin acquired 36.7% stake in Generic Health, Australia, in FY2009.Generic Health is an emerging player in the generic space in Australia and markets a wide rangeof generic prescriptions and OTC products.

Domestic Business: On a strong footing

Lupin continues to make strides in the Indian market. Currently, Lupin ranks No.5 climbing up frombeing No.11 five years ago. Lupin has been fastest growing company among the Top-5companies in the Domestic Formulation space registering strong CAGR of 22.9% over the lastthree years. Lupin has increased marketshare from 2.4% in FY2006 to 2.7% in FY2009. Six ofLupin's products are among the Top-300 brands in the country. Lupin introduced 54 new productsin the Indian market in FY2009. We believe the company's stupendous growth in the domesticmarket has been due to its shift of focus to the Chronic and Lifestyle Segments, which nowcontributes 41% of the total Domestic Formulation sales as against 26% in FY2006. Moreover,Lupin has also beefed up its field force, which has doubled in the last four years to around 3,000personnel now.

Lupin has been one of thefastest growing companiesamong the Top-5 companies inthe Domestic Formulationspace registering strongCAGR of 22.9% over the lastthree years

250

51

107

153

202

0

50

100

150

200

FY2008 FY2009 FY2010E FY2011E

Rs

cr

13January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 13

Lupin

Pharmaceutical

Source: Company, Angel Research

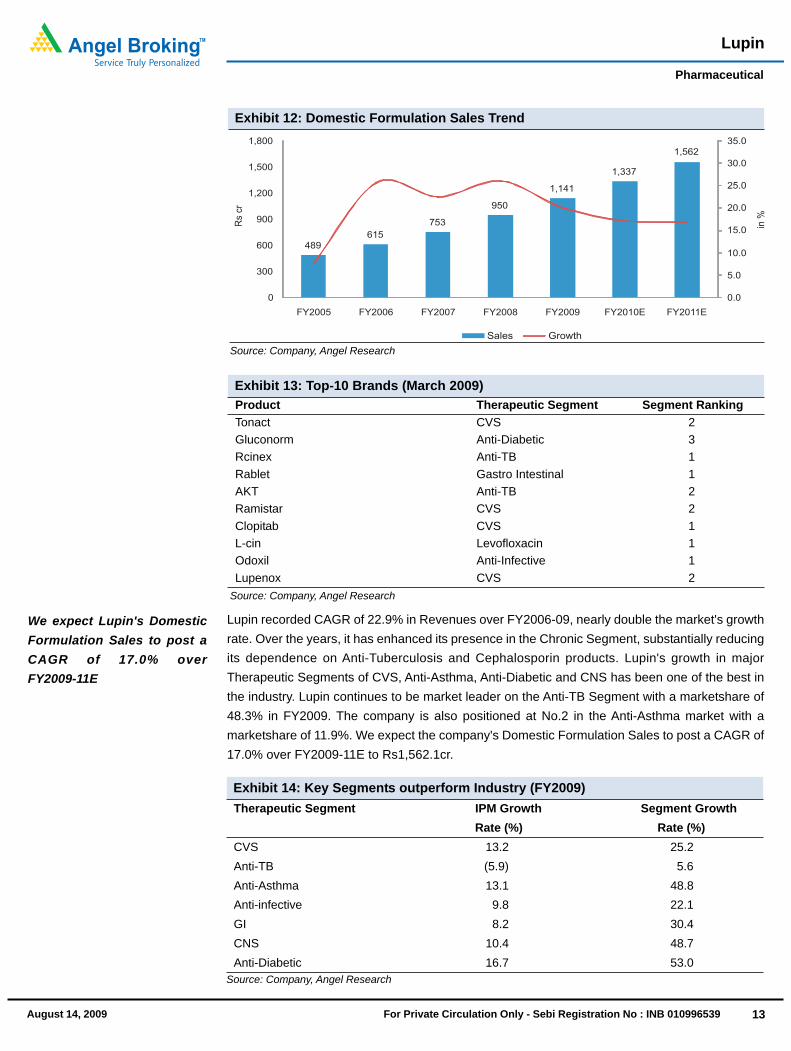

Exhibit 12: Domestic Formulation Sales Trend

Lupin recorded CAGR of 22.9% in Revenues over FY2006-09, nearly double the market's growthrate. Over the years, it has enhanced its presence in the Chronic Segment, substantially reducingits dependence on Anti-Tuberculosis and Cephalosporin products. Lupin's growth in majorTherapeutic Segments of CVS, Anti-Asthma, Anti-Diabetic and CNS has been one of the best inthe industry. Lupin continues to be market leader on the Anti-TB Segment with a marketshare of48.3% in FY2009. The company is also positioned at No.2 in the Anti-Asthma market with amarketshare of 11.9%. We expect the company's Domestic Formulation Sales to post a CAGR of17.0% over FY2009-11E to Rs1,562.1cr.

We expect Lupin's DomesticFormulation Sales to post aCAGR of 17.0% overFY2009-11E

Source: Company, Angel Research

Exhibit 13: Top-10 Brands (March 2009)Product Therapeutic Segment Segment RankingTonact CVS 2Gluconorm Anti-Diabetic 3Rcinex Anti-TB 1Rablet Gastro Intestinal 1AKT Anti-TB 2Ramistar CVS 2Clopitab CVS 1L-cin Levofloxacin 1Odoxil Anti-Infective 1Lupenox CVS 2

Source: Company, Angel Research

Exhibit 14: Key Segments outperform Industry (FY2009)Therapeutic Segment IPM Growth Segment Growth

Rate (%) Rate (%)CVS 13.2 25.2Anti-TB (5.9) 5.6Anti-Asthma 13.1 48.8Anti-infective 9.8 22.1GI 8.2 30.4CNS 10.4 48.7Anti-Diabetic 16.7 53.0

Sales Growth

489

615

753

950

1,141

1,337

1,562

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

0

300

600

900

1,200

1,500

1,800

FY2005 FY2006 FY2007 FY2008 FY2009 FY2010E FY2011E

in%

Rs

cr

14January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 14

Lupin

Pharmaceutical

Near-term Overhang

Mandideep facility under US FDA scanner

In November 2008, US FDA had issued 15 inspectional observations (483s) to the company'sMandideep facility post which the company has responded to 8 observations satisfactorily.However, in May 2008, Lupin received a warning letter from the US FDA. We believe that the USFDA warning letter was a negative in spite of Lupin responding on four occasions post theobservations in November 2008. We believe that the warning letter will result in no further productapprovals from the facility. However, the company has only one product pending approval fromthe unit. Lupin sells Cephalosporin products from this facility. In FY2009, Cephalosporin productscontributed 10-12% to the company's overall Top-line and 13-15% to the Bottom-line.

Lupin believes that the US FDA letter seeks additional documentation and explanation as its initialresponses were inadequate. However, we remain cautious as any further adverse action by USFDA may lead to loss of marketshare for non-Ceph products as was witnessed by other playersunder the US FDA scanner.

In case of Mandideep, webelieve any further adverseaction by the US FDA Lupinmay register loss ofmarketshare in its non-Cephproducts as was witnessed byother players

Source: Company, Angel Research

Exhibit 15: Indian Pharmacos under US FDA quagmire

483Observation

WarningLetter

ProductRecalls,

Seizure of

products

ImportAlert

Seizureand Banon Plant

Lupin

Sun Pharma

Ranbaxy

Loss of Market Share in products not covered by the alert

Management has indicated that there can be nearterm pressure on distributed products

Management confident of resolution

Incre

ais

ng

Ris

kLevel

15January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 15

Lupin

Pharmaceutical

Europe Anti-trust Investigations

Lupin is facing anti-trust investigations by the European Union (EU) regulator for delaying its entryinto the market of generic versions of its cardio vascular drug, Perindopril. In April 2007, Lupin hadsold the patent rights and other related intellectual property for the generic version of Perindoprilto French drug maker Les Laboratories Servier for Rs112.7cr (Euro 20mn). Hence, the EU startedinvestigation for hindering the launch of Perindopril. Regulators suspect that Servier entered intodeals with generic rivals Krka, Lupin, Matrix, Niche Generics Ltd and Teva to hold back cheaperversions. However, the Regulator has stressed that the ongoing investigation does not indicatethat the companies have violated the rules.

Management believes that in their settlement with Servier they had obtained the permission tolaunch the drug as and when the genericisation happens and is confident of its stance. In fact,Lupin is currently in the midst of launching Perindopril in many of the EU countries. We believethat any adverse outcome on this front could lead to one-time penalty for the company.

Lupin is also in the midst oflaunching Perindopril in manyof the EU countries

16January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 16

Lupin

Pharmaceutical

Financials: Growth Momentum to continue

Top-line to register strong growth

During FY2006-09, Lupin posted 30.6% CAGR in Net Sales largely driven by growth in its ExportFormulation Sales. The company's Export Formulation Sales registered CAGR of 85.8% duringthe mentioned period primarily driven by its US business. We believe Lupin is one of the fewIndian pharma companies to scale up in the US market in a short time span. Pertinently, thecompany's US Sales registered robust 75.2% CAGR to US $273mn in FY2009. The primary driverfor strong show in the US has been the success of its branded product, Suprax, and aggressiveincrease in marketshare in other Generic products. We expect the company's US Sales to record22.2% CAGR over FY2009-11E on the back of new launches.

The company has also started building up a formidable presence in Europe post the acquisition ofHormosan in Germany. Going forward, we expect Europe to grow by 37.5% over FY2009-11E.

Lupin entered Japan with the acquisition of Kyowa in FY2008. Going ahead, we expect the Japanmarket for the company to grow by 21.7% over FY2009-11E.

The company has also been able to scale up its Domestic Formulation business posting a CAGRof 22.9% over FY2006-09 to Rs1,141.2cr out-pacing the industry growth rate.

During FY2006-09, Lupinposted 30.6% CAGR in NetSales largely driven by growthin its Export Formulation Sales

Going ahead, we expect the company to maintain its growth over FY2009-11E primarily driven byits Exports Segment. We expect the company's overall Net Sales to register a CAGR of 16.2%over FY2009-11E to Rs5,094cr.

Sales Growth to be consistent compared to larger peers

We expect the company's Top-line to register more consistent growth than its larger peers onaccount of having a formidable presence in the US market (both in the Generic and Brandedbusinesses), increasing marketshare on the Domestic front and diversifying across geographiespredominantly in Japan and Europe.

Source: Company, Angel Research

Exhibit 16: Sales Break-up

0

1,000

2,000

3,000

4,000

5,000

6,000

FY2006 FY2007 FY2008 FY2009 FY2010E FY2011E

US Japan Europe India Other Markets API & CRAMS

CAGR 24.5%

2,014

2,706

3,776

4,596

5,094

1,695

Rs

cr

17January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 17

Lupin

Pharmaceutical

Source: Company, Angel Research. Note: For Ranbaxy figures are CY ending.

Exhibit 17: Sales Growth across companiesWe estimate the company toregister more consistentgrowth in Top-line than itslarger peers

We expect Lupin OPM toexpand going forward by100-150bp over FY2009-11E onback of increasingcontribution from ExportMarket and Formulationsegment

Source: Company, Angel Research. Note: Core Operating Profit excludes Other Operating Income and Other Incomea

Exhibit 18: Margins to expand

To register higher Margins than most larger peers

We estimate Lupin to register higher OPMs compared to its larger peers (except Sun Pharma) onthe back of its vertical integration, exposure to high-Margin Branded generic business in the USand increasing proportion of Chronic sales within its Domestic Formulation Segment.

Core Operating Margins to expand by 100-150bp over FY2009-11E

We estimate OPM to expand by 100-150bp over FY2009-11E on the back of increasingcontribution from Exports and Formulation Segment. We expect Lupin's Core Operating Profit toregister a CAGR of 21.2% over FY2009-11E to Rs952.6cr.On the Bottom-line front, we expect thecompany's Earnings to register a CAGR of 18.5% over FY2009-11E to Rs704.8cr.

(50)

0

50

100

150

200

FY2007 FY2008 FY2009 FY2010E FY2011E

Ranbaxy Sun Pharma Dr Reddy Lupin

%

224292

436

648

850

953

173

309408

502

635705

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

0

200

400

600

800

1,000

1,200

FY2006 FY2007 FY2008 FY2009 FY2010E FY2011E

Core Operating Profit Net Profit Core Operating margin Net Margin

%Rs

cr

18January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 18

Lupin

Pharmaceutical

Capital Efficiency

Lupin has been expanding its presence through both organic and inorganic route. In the last threeyears, Lupin incurred capex to the tune of Rs750.3cr towards building up capacities and incurredRs423.7cr towards acquisitions. Lupin incurred capex of Rs339cr during FY2009 of whichsignificant investment was made in the OC SEZ in Indore. The company has guided for capex ofRs450cr to be incurred in FY2010E. Pertinently, Lupin is also scouting for acquisitions in the GCC,Latin America and Japan regions to be funded through internal accruals.

Source: Company, Angel Research. Note: For Ranbaxy figures are CY ending.

Exhibit 19: OPM, NPM across companiesSecond in terms ofProfitability Margins

Lupin plans to incur capex ofRs450cr in FY2010E

Source: Company, Angel Research

Exhibit 20: Capex, Acquistion and FCF

12

9

31

4

32

47

44

3233

24

1720

1719

1516 17 19 19

0.0

10.0

20.0

30.0

40.0

50.0

FY2007 FY2008 FY2009 FY2010E FY2011E

Ranbaxy Sun Pharma Dr Reddy Lupin

In%

812

3

38

4443

30 32

15

9 1012

15 1513 14 14

0.0

10.0

20.0

30.0

40.0

50.0

FY2007 FY2008 FY2009 FY2010E FY2011E

Ranbaxy Sun Pharma Dr Reddy Lupin

In%

83

177234

339

450400

0

(5)

272

157

496

(269)

(82)

42

276

(400)

(300)

(200)

(100)

0

100

200

300

400

500

FY2006 FY2007 FY2008 FY2009 FY2010E FY2011E

Capex Acquistion Free Cash Flow

Rs

cr

19January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 19

Lupin

Pharmaceutical

FCCBs in the money

Lupin had issued FCCBs of US $100mn at a conversion price of Rs567/ share in FY2006, whichmatures in FY2011E. We believe that Lupin is the only pharma company whose FCCBs havebeen in the money post the issuance. Around 40% of the company’s FCCBs has been convertedinto equity. We have taken the balance FCCBs as part of equity for our estimates.

Till date, around 40% of thecompany’s US $100mn FCCBshas been converted intoequity

Source: Company, Angel Research; Note: FY2010 onwards we have considered FCCB as part of equity

Exhibit 21: Efficiency ParametersParameter FY2006 FY2007 FY2008 FY2009 FY2010E FY2011ELeverage Ratio (x)Net Debt/Equity 0.7 0.6 0.7 0.8 0.4 0.3Net Debt/ Ebitda 2.0 1.6 2.1 1.8 1.1 0.8Return Ratio (%)RoCE 19.5 23.4 25.4 25.0 26.7 24.1RoE 31.1 41.2 37.9 37.1 34.6 28.0Margins (%)Core Operating Margins 13.2 14.5 16.1 17.2 18.5 18.7Net Margins 10.2 15.3 15.1 13.3 13.8 13.8

20January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 20

Lupin

Pharmaceutical

Concerns

Competition expected in Suprax

Nectar Lifesciences and Orchid Chemicals are the two Indian companies that have filed a DMFsfor Cefixime (Suprax) and could launch the product towards the latter part of FY2010 or earlyFY2011. We do not expect significant loss of marketshare for Lupin since the company's producthas developed strong brand equity. Further, the company has also been able to move about 50%of volume to other dosage form from the original 100mg suspensions, which are unlikely to facegeneric competition in the near future. In its bid to reduce it dependence on Suprax and theassociated field-force costs (60 MR), Lupin is planning other branded product launches in the USthrough marketing alliances or in-licensing. For instance, in 2008, Lupin entered into a marketingtie-up with Forest Labs for its AeroChamber Plus range of products. It also plans to launch AllerNazein 2HFY2010 for which it proposes to leverage its Suprax field force.

Vulnerable to DPCO

Despite rising contribution from Exports, the Domestic market will continue to contribute a majorchunk to the company's overall Net Sales going ahead. This, we believe, makes it vulnerable toany change in the DPCO.

Foreign currency risks

Exports constitute 66% of the company Revenues. Hence, any significant appreciation in theRupee could adversely affect the company's Margins.

Price Erosion on the API front

Higher-than-anticipated price erosion in the company's generic API business, which contributesaround 19% of its Sales, could impact its Profitability.

Nectar Lifesciences andOrchid Chemicals are the twoIndian companies that havefiled DMFs for Cefixime andcould launch the product inlate FY2010 or in early FY2011

21January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 21

Lupin

Pharmaceutical

Outlook and Valuation

Lupin has moved up the value chain and transformed from being a pure API player to a robustFormulations player. Lupin has tapped high-Margin Regulated markets as well. It is also amongthe few Pharma companies that have managed to grow its Top-line by 30.6% and Bottom-line by42.6% over FY2006-09 driven by its US business. In the US, Lupin has differentiated itself bybuilding a formidable presence in the Branded Generic space. We believe Lupin will continue togain traction in the US markets while simultaneously scaling up its business in other geographies,viz. Japan and Europe. On the Domestic Formulations front we expect Lupin to gain marketshareas it expands its Chronic Product portfolio. We believe Lupin, a second tier Pharma company, hasthe potential to get re-rated hereon once uncertainty over its Mandideep facility gets cleared.Overall, we expect Lupin's Top-line and Bottom-line to post CAGR of 16.2% and 18.5%respectively, over FY2009-11E

On the valuation front, over the last four years, Lupin has traded in the 7-16x PE band averagingaround 11x in the mentioned period. On the EV/EBITDA front, the stock has been trading in therange of 5-12x and at an average 9x during April 2005 - March 2009. On the EV/Sales front, thestock has been trading in the range of 0.8-2.2x and at an average of 1.4x.

95% of the time in the last fouryears Lupin has traded in therange of 8x-15.5x

Source: Company, Angel Research

Exhibit 22: One-Year Forward PE Band

We believe Lupin has thepotential to get re-rated onceuncertainty over its Mandideepfacility clears

Source: Company, Angel Research

Exhibit 23: One-Year Forward EV/EBITDAOn the EV/EBITDA front, thestock has been trading in therange of 5-12x and at anaverage of 9x during April 2005- March 2009

Mean PE One Year Fwd PE 1+ Std Dev 1-Std dev 2+ Std dev 2- Std dev

4

8

12

16

20

1-A

pr-0

5

1-Ju

n-05

1-A

ug-0

5

1-O

ct-0

5

1-D

ec-0

5

1-Fe

b-06

1-A

pr-0

6

1-Ju

n-06

1-A

ug-0

6

1-O

ct-0

6

1-D

ec-0

6

1-Fe

b-07

1-A

pr-0

7

1-Ju

n-07

1-A

ug-0

7

1-O

ct-0

7

1-D

ec-0

7

1-Fe

b-08

1-A

pr-0

8

1-Ju

n-08

1-A

ug-0

8

1-O

ct-0

8

1-D

ec-0

8

1-Fe

b-09

0

2,000

4,000

6,000

8,000

10,000

12,000

Apr-

05

Aug

-05

Dec-0

5

Apr-

06

Aug

-06

Dec-0

6

Apr-

07

Aug

-07

Dec-0

7

Apr-

08

Aug

-08

Dec-0

8

Apr-

09

EV

(Rs

cr)

3x

6x

9x

12x

22January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 22

Lupin

Pharmaceutical

Source: Company, Angel Research.

Exhibit 24: One-Year Forward EV/SalesOn the EV/Sales front, thestock has been trading in therange of 0.8-2.2x and at anaverage of 1.4x forward salesover the last 4 years

Lupin is currently trading at a 17-35% discount compared to its larger peers, which we believe isunwarranted given the scale up in its business in the last four years. We also estimate thecompany to register a CAGR of 16.2% in Top-line and 18.5% in Bottom-line over FY2009-11E,which we believe is among the best in the Industry. However, we have assigned a Target Multipleof 14x to Lupin (in line with the Mid-cap multiple) as we believe the Mandideep issue will continueto be an overhang on the stock and delay the imminent re-rating of the stock. We recommend anAccumulate on the stock, with a Target Price of Rs1,112.

0

2,000

4,000

6,000

8,000

10,000

Ap

r-0

5

Au

g-0

5

De

c-0

5

Ap

r-0

6

Au

g-0

6

De

c-0

6

Ap

r-0

7

Au

g-0

7

De

c-0

7

Ap

r-0

8

Au

g-0

8

De

c-0

8

Ap

r-0

9

EV

(Rs

cr)

0.5x

1.5x

1.5x

2.0x

Source: Bloomberg, Angel Research; Note * M-cap in US $mn, ** M-cap in Euro Mn, For Ranbaxy figures are CYending.

Exhibit 25: Comparative ValuationCompanies M-cap P/E (x) EV/EBITDA (x)

(Rs cr) FY2009 FY2010E FY2011E FY2009 FY2010E FY2011EIndian Large CapRanbaxy 12,449 - - 72.4 61.4 261.7 62.0Sun Pharma 25,329 14.4 19.6 16.6 13.0 16.5 13.4Dr Reddy’s 13,510 - 19.6 14.9 8.9 9.8 7.6Cipla 21,934 28.6 21.3 19.0 23.1 21.4 18.8Average 13.7 17.1 25.7 22.8 54.9 21.5Indian Mid CapLupin 8,261 16.2 13.7 12.3 12.4 10.4 9.1Cadila Healthcare 6,039 19.9 13.6 12.3 9.1 7.1 6.3Aurobindo Pharma 3,565 12.3 8.5 6.7 11.5 7.7 5.8Average 16.7 12.7 11.3 11.1 8.7 7.6Global PeersTeva* 47,434 18.4 15.5 11.7 na na naMylan* 4,027 21.5 12.1 9.5 8.7 7.1 6.6Watson* 3,643 9.6 11.0 9.8 7.5 7.8 7.3Average 18.1 15.0 11.4 8.1 7.4 7.0Stada** 1,035 8.5 9.7 8.6 6.6 6.8 6.5

23January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 23

Lupin

Pharmaceutical

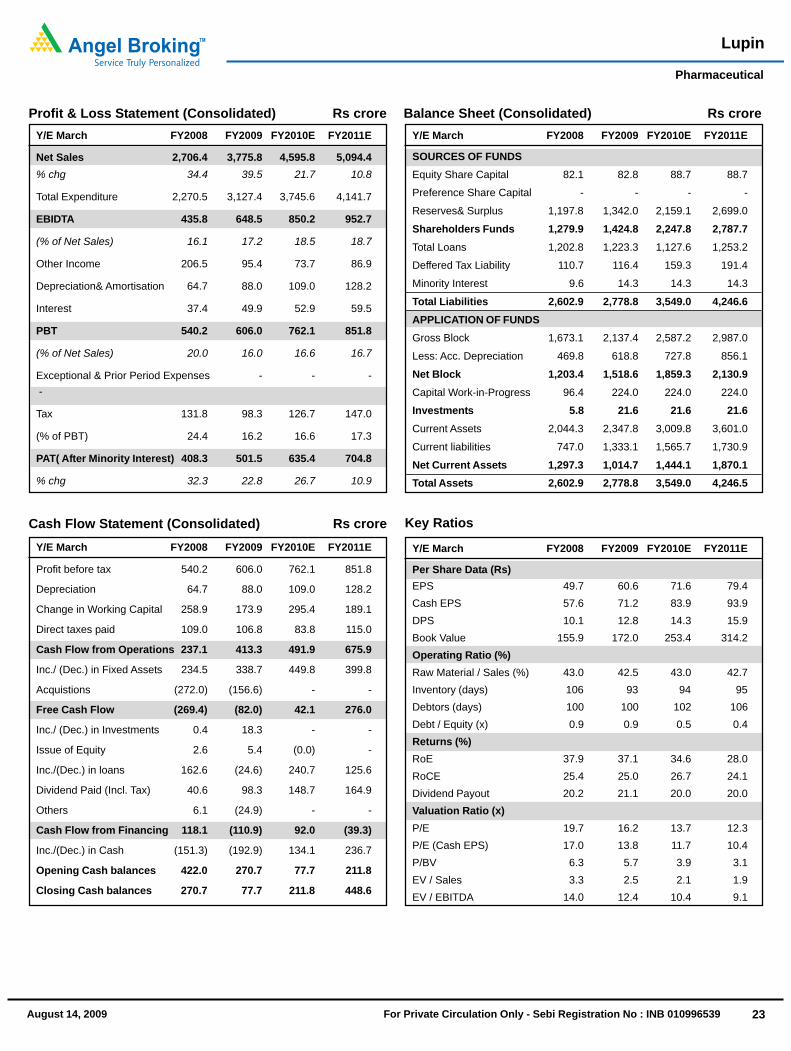

Profit & Loss Statement (Consolidated) Rs croreY/E March FY2008 FY2009 FY2010E FY2011E

Net Sales 2,706.4 3,775.8 4,595.8 5,094.4% chg 34.4 39.5 21.7 10.8

Total Expenditure 2,270.5 3,127.4 3,745.6 4,141.7

EBIDTA 435.8 648.5 850.2 952.7

(% of Net Sales) 16.1 17.2 18.5 18.7

Other Income 206.5 95.4 73.7 86.9

Depreciation& Amortisation 64.7 88.0 109.0 128.2

Interest 37.4 49.9 52.9 59.5

PBT 540.2 606.0 762.1 851.8

(% of Net Sales) 20.0 16.0 16.6 16.7

Exceptional & Prior Period Expenses - - - -

Tax 131.8 98.3 126.7 147.0

(% of PBT) 24.4 16.2 16.6 17.3

PAT( After Minority Interest) 408.3 501.5 635.4 704.8

% chg 32.3 22.8 26.7 10.9

Y/E March FY2008 FY2009 FY2010E FY2011E

SOURCES OF FUNDSEquity Share Capital 82.1 82.8 88.7 88.7

Preference Share Capital - - - -

Reserves& Surplus 1,197.8 1,342.0 2,159.1 2,699.0

Shareholders Funds 1,279.9 1,424.8 2,247.8 2,787.7Total Loans 1,202.8 1,223.3 1,127.6 1,253.2

Deffered Tax Liability 110.7 116.4 159.3 191.4

Minority Interest 9.6 14.3 14.3 14.3

Total Liabilities 2,602.9 2,778.8 3,549.0 4,246.6APPLICATION OF FUNDSGross Block 1,673.1 2,137.4 2,587.2 2,987.0

Less: Acc. Depreciation 469.8 618.8 727.8 856.1

Net Block 1,203.4 1,518.6 1,859.3 2,130.9Capital Work-in-Progress 96.4 224.0 224.0 224.0

Investments 5.8 21.6 21.6 21.6Current Assets 2,044.3 2,347.8 3,009.8 3,601.0

Current liabilities 747.0 1,333.1 1,565.7 1,730.9

Net Current Assets 1,297.3 1,014.7 1,444.1 1,870.1Total Assets 2,602.9 2,778.8 3,549.0 4,246.5

Balance Sheet (Consolidated) Rs crore

Cash Flow Statement (Consolidated) Rs croreY/E March FY2008 FY2009 FY2010E FY2011E

Profit before tax 540.2 606.0 762.1 851.8

Depreciation 64.7 88.0 109.0 128.2

Change in Working Capital 258.9 173.9 295.4 189.1

Direct taxes paid 109.0 106.8 83.8 115.0

Cash Flow from Operations 237.1 413.3 491.9 675.9

Inc./ (Dec.) in Fixed Assets 234.5 338.7 449.8 399.8

Acquistions (272.0) (156.6) - -

Free Cash Flow (269.4) (82.0) 42.1 276.0

Inc./ (Dec.) in Investments 0.4 18.3 - -

Issue of Equity 2.6 5.4 (0.0) -

Inc./(Dec.) in loans 162.6 (24.6) 240.7 125.6

Dividend Paid (Incl. Tax) 40.6 98.3 148.7 164.9

Others 6.1 (24.9) - -

Cash Flow from Financing 118.1 (110.9) 92.0 (39.3)

Inc./(Dec.) in Cash (151.3) (192.9) 134.1 236.7

Opening Cash balances 422.0 270.7 77.7 211.8

Closing Cash balances 270.7 77.7 211.8 448.6

Key Ratios

Y/E March FY2008 FY2009 FY2010E FY2011E

Per Share Data (Rs)EPS 49.7 60.6 71.6 79.4Cash EPS 57.6 71.2 83.9 93.9DPS 10.1 12.8 14.3 15.9Book Value 155.9 172.0 253.4 314.2Operating Ratio (%)Raw Material / Sales (%) 43.0 42.5 43.0 42.7Inventory (days) 106 93 94 95Debtors (days) 100 100 102 106Debt / Equity (x) 0.9 0.9 0.5 0.4Returns (%)RoE 37.9 37.1 34.6 28.0RoCE 25.4 25.0 26.7 24.1Dividend Payout 20.2 21.1 20.0 20.0Valuation Ratio (x)P/E 19.7 16.2 13.7 12.3P/E (Cash EPS) 17.0 13.8 11.7 10.4P/BV 6.3 5.7 3.9 3.1EV / Sales 3.3 2.5 2.1 1.9EV / EBITDA 14.0 12.4 10.4 9.1

24January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 24

Lupin

PharmaceuticalFund Management & Investment Advisory ( 022 - 3952 4568)P. Phani Sekhar Fund Manager - (PMS) [email protected] Bhamre Head - Derivatives and Investment Advisory [email protected] Mehta AVP - Investment Advisory [email protected] Team ( 022 - 3952 4568)Hitesh Agrawal Head - Research [email protected] Kour Nangra VP-Research, Pharmaceutical [email protected] Agrawal VP-Research, Banking [email protected] Jajoo Automobile [email protected] Shah IT, Telecom [email protected] Pareek Oil & Gas [email protected] Solanki Power, Mid-cap [email protected] Kanani Infrastructure, Real Estate [email protected] Shah FMCG , Media [email protected] Bambha Capital Goods, Engineering [email protected] Dalmia Pharmaceutical [email protected] Desai Logistics [email protected] Bariya Fertiliser, Mid-cap [email protected] Nadkarni Retail [email protected] Vora Research Associate (Oil & Gas) [email protected] Waghmare Research Associate (Metals & Mining, Cement) [email protected] Srinivasan Research Associate (Power, Mid-cap) [email protected] Mate Research Associate (Infra, Real Estate) [email protected] Gaunekar Research Associate (Automobile) [email protected] Agrawal Jr. Derivative Analyst [email protected] Bagaria PMS [email protected] Wagle Chief Technical Analyst [email protected] Joshi AVP Technical Advisory Services [email protected] Ail Manager - Technical Advisory Services [email protected] Jagtap Sr. Technical Analyst [email protected] Sanghvi Sr. Technical Analyst [email protected] Vasudeo Technical Analyst [email protected] Dayma Technical Analyst [email protected] Padhye AVP Mutual Fund [email protected] Rathod Research Associate (MF) [email protected] Jangid Research Associate (MF) [email protected] Research TeamAmar Singh Research Head (Commodities) [email protected] P Sr. Technical Analyst [email protected] Gupta Sr. Technical Analyst [email protected] Patki Sr. Technical Analyst [email protected] Chauhan Technical Analyst abhishek [email protected] Research Team (Fundamentals)Badruddin Sr. Research Analyst (Agri) [email protected] Walia Research Analyst ( Base Metals, Energy Complex) [email protected] Narvekar Research Analyst ( Agri) vedika.narvekar @angeltrade.comNalini Rao Research Analyst (Agri) [email protected] Shetty Research Editor [email protected] Adhyaru Assistant Research Editor [email protected] Patil Production [email protected] Patel Production [email protected]

Research & Investment Advisory: Acme Plaza, 3rd Floor ‘A’ wing, M.V. Road, Opp Sangam Cinema, Andheri (E), Mumbai - 400 059

Buy (Upside > 15%) Accumulate (Upside upto 15%) Neutral (5 to -5%)Reduce (Downside upto 15%) Sell (Downside > 15%)

Ratings (Returns) :

DisclaimerThis document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any other person. Persons into whosepossession this document may come are required to observe these restrictions.Opinion expressed is our current opinion as of the date appearing on this material only. While we endeavor to update on a reasonable basis the information discussed in this material, there maybe regulatory, compliance, or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and may besubject to change without notice. Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true and are for general guidance only.While every effort is made to ensure the accuracy and completeness of information contained, the company takes no guarantee and assumes no liability for any errors or omissions of theinformation. No one can use the information as the basis for any claim, demand or cause of action.Recipients of this material should rely on their own investigations and take their own professional advice. Each recipient of this document should make such investigations as it deemsnecessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult theirown advisors to determine the merits and risks of such an investment. Price and value of the investments referred to in this material may go up or down. Past performance is not a guide forfuture performance. Certain transactions - futures, options and other derivatives as well as non-investment grade securities - involve substantial risks and are not suitable for all investors.Reports based on technical analysis centers on studying charts of a stock's price movement and trading volume, as opposed to focusing on a company's fundamentals and as such, may notmatch with a report on a company's fundamentals.We do not undertake to advise you as to any change of our views expressed in this document. While we would endeavor to update the information herein on a reasonable basis, Angel Broking,its subsidiaries and associated companies, their directors and employees are under no obligation to update or keep the information current. Also there may be regulatory, compliance, or otherreasons that may prevent Angel Broking and affiliates from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and may besubject to change without notice. Angel Broking Limited and affiliates, including the analyst who has issued this report, may, on the date of this report, and from time to time, have long or shortpositions in, and buy or sell the securities of the companies mentioned herein or engage in any other transaction involving such securities and earn brokerage or compensation or act asadvisor or have other potential conflict of interest with respect to company/ies mentioned herein or inconsistent with any recommendation and related information and opinions.Angel Broking Limited and affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction tothe companies referred to in this report, as on the date of this report or in the past.

25January 30, 2008 For Private Circulation Only - Sebi Registration No : INB 010996539August 14, 2009 For Private Circulation Only - Sebi Registration No : INB 010996539 25

Lupin

Pharmaceutical

Central Support & Registered Office:G-1, Akruti Trade Centre, Road No. 7, MIDC Marol, Andheri (E), Mumbai - 400 093 Tel : 2835 8800 / 3083 7700

Regional Offices:

Private Client Group Offices: Sub - Broker Marketing:

Branch Offices:

Corporate & Marketing Office : 612, Acme Plaza, M.V. Road, Opp Sangam Cinema, Andheri (E), Mumbai - 400 059 Tel : (022) 3952 7100 / 4000 3600NRI Helpdesk : e-mail : [email protected] Tel : (022) 4000 3622 / 4026 2700Investment Advisory Helpdesk : e-mail : [email protected] Tel : (022) 3958 4000Commodities : e-mail : [email protected] Tel : (022) 3081 7400PMS : e-mail : [email protected] Tel: (022) 3953 2800Feedback : e-mail : [email protected] Tel : (022) 2835 5000

Ahmedabad - Tel: (079) 3941 3940

Bengaluru - Tel: (080) 3941 3940

Chennai - Tel: (044) 3941 3940

Hyderabad - Tel: (040) 3941 3940

Coimbatore - Tel: (0422) 3941 394

Cochin - Tel: (0484) 3941 394

Indore - Tel: (0731) 3941 394

Jaipur - Tel: (0141) 3941 394

Kanpur - Tel: (0512) 3941 394

Kolkata - Tel: (033) 3941 3940

Lucknow - Tel: (0522) 3941 394

Ludhiana - Tel: (0161) 3941 394

Mumbai (Powai) - Tel: (022)3952 6500

Pune - Tel: (020) 3941 3940

New Delhi - Tel: (011) 3941 3940

Nagpur - Tel: (0712) 3941 394

Nashik - Tel: (0253) 3941 394

Mumbai (Goregoan) Tel: (022) 2879 0411-15

Surat - Tel: (0261) 3941 394

Rajkot - Tel :(0281) 3941 394

Visakhapatnam - Tel :(0891) 3941 394

Ahmedabad (C. G. Road) - Tel: (079) 3982 9934 Surat - Tel: (0261) 3071 600 Rajkot (Race course) - Tel: (0281) 2490 847 Powai - Tel: (022) 3952 6500

Andheri (W) - Tel: (022) 2635 2345 / 6668 0021

Bandra (W) - Tel: (022) 2655 5560 / 70

Andheri (Lokhandwala) - Tel: (022) 2639 2626

Bandra (W) - Tel: (022) 6643 2694 - 99

Borivali (W) - Tel: (022) 3952 4787

Borivali (Punjabi Lane) - Tel: (022) 3951 5700.

Chembur - (Basant) - Tel:(022) 022) 6156 1111 / 01

Kalbadevi - Tel: (022) 2243 5599 / 2242 5599

Kandivali (W) - Tel: (022) 2867 3800/2867 7032

Chembur - Tel: (022) 6703 0210 / 11 /12

Fort - Tel: (022) 3958 1887

Ghatkopar (E) - Tel: (022) 3955 8400/2510 1525

Malad (E) - Tel: (022) 2880 4440

Kandivali - Tel: (022) 4245 1300

Malad (Natraj Market) - Tel:(022) 28803453 / 24

Masjid Bander - Tel: (022) 2345 5130 /1 / 8 / 42 /28

Mulund (W) - Tel: (022) 2562 2282

Nerul - Tel: (022) 2771 9012 - 17

Sion - Tel: (022) 3952 7891

Powai (E) - Tel: (022) 3952 5887

Thane (W) - Tel: (022) 2539 0786 / 0650 / 1

Vashi - Tel: (022) 2765 4749 / 2251

Vile Parle (W) - Tel: (022) 2610 2894 / 95

Wadala - Tel: (022) 2414 0607 / 08

Agra - Tel: (0562) 4037200

Ahmedabad (Kalupur) - Tel: (079) 3041 4000 / 01

Ahmedabad (Maninagar) - Tel: (079) 3981 7430 / 1

Ajmer - Tel: (0145) 3941 394

Alwar - Tel: (0144) 3941 394 / 99833 60006

Ahmeda. (Bapu Nagar) - Tel : (079) 3091 6900 - 02

Ahmeda. (Gurukul) - Tel: (079) 3011 0800 / 01

Ahmedabad (C. G. Road) - Tel: (079) 4021 4023

Ahmedabad (Sabarmati) - Tel : (079) 3091 6100 / 01

Ahmedabad (Satellite) - Tel: (079) 4000 1000

Ahmedabad (Shahibaug) -Tel: (079)3091 6800 / 01

Amreli - Tel: (02792) 228 800/231039-42

Anand - Tel : (02692) 398 400 / 3

Amritsar - Tel: (0183) 3941 394

Ankleshwar - Tel: (02646) 398 200

Baroda - Tel: (0265) 6635 100 / 2226 103

Baroda (Akota) - Tel: (0265) 2355 258 / 6499 286

Baroda (Manjalpur) - Tel: (0265) 6454280-3

Bhavnagar - Tel: (0278) 3941 394

Bengaluru - Tel: (080) 4072 0800 - 29

Ahmeda. (Ramdevnagar) - Tel : (079) 4024 3842 / 43

Bhavnagar (Shastrinagar)- Mobile: 92275 32302

Indore - Tel: (0731) 4238 600

Gandhinagar - Tel: (079) 4010 1010 - 31

Gajuwaka - Tel: (0891) 3987 100 - 30

Faridabad - Tel: (0129) 3984 000

Gandhidham - Tel: (02836) 237 135

Gondal - Tel: (02825) 398 200

Ghaziabad - Tel: (0120) 3980 800

Gurgaon - Tel: (0124) 3050 700

Himatnagar - Tel: (02772) 241 008 / 241 346

Hyderabad - A S Rao Nagar Tel: (040) 4222 2070-5

Hubli - Tel: (0836) 4267 500 - 22

Indore - Tel: (0731) 3049 400

Bhopal - Tel :(0755) 3941 394

Bikaner - Tel: (0151) 3941 394 / 98281 03988

Chandigarh - Tel: (0172) 3092 700

Deesa - Mobile: 97250 01160

Erode - Tel: (0424) 3982 600

Bhilwara - (01482) 398 350

Jamnagar (Cross Word) - Tel: (0288) 2751 118

Jamnagar(Indraprashta) - Tel: (0288) 3941 394

Jodhpur - Tel: (0291) 3941 394 / 99280 24321

Junagadh - Tel : (0285) 3941 3940

Keshod - Tel: (02871) 234 027 / 233 967

Kolkata (N. S. Rd) - Tel: (033) 3982 5050

Kolkata (P. A. Shah Rd) - Tel: (033) 3001 5100

Mehsana - Tel: (02762) 645 291 / 92

Kota - Tel : (0744) 3941 394

Mansarovar - Tel:(0141) 3057 700/99836 74600

Mysore - Tel: (0821) 4004 200 - 30

Nadiad - Tel : (0268) - 2527 230 / 34

Jamnagar (Moti Khawdi) - Tel: (0288) 2846 026

Jamnagar(Madhav Plaza) - Tel: (0288) 2665 708

Jalgaon - Tel: (0257) 2234 832

Kolhapur - Tel: (0231) 6632 000

Madurai Tel: (0452) 3941 394

Mangalore - Tel: (0824) 3982 140

Nagaur - Tel: (01582) 244 648

New Delhi (Nehru Place) - Tel: (011) 3982 0900

New Delhi (Preet Vihar) - Tel: (011) 4310 6400

Palanpur - Tel: (02742) 308 060 - 63

Patel Nagar - Tel : (011) 45030 600

Patan - Tel: (02766) 222 306

Porbandar - Tel : (0286) 3941 394

Noida - Tel : (0120) 4639 900 / 1 / 9

New Delhi (Bhikaji Cama) - Tel: (011) 41659711

New Delhi (Lawrence Rd.) - Tel: (011) 3262 8699 / 8799

New Delhi (Pitampura) - Tel: (011) 4751 8100

Porbandar (Kuber Life Style) - Mob.-98242 53737

Nashik - Tel: (0253) 3011 500 / 1 / 11

Jaipur - (Rajapark) Tel: (0141) 3057 900 / 99833 40004

Pune (Aundh) - Tel: (020) 4104 1900

Pune (Camp) - Tel: (020) 3092 1800

Pune - Tel: (020) 6620 6591 / 6620 6595

Rajamundhry - Tel: (0883) 3941 394

Rajkot (Ardella) Tel.: (0281) 2926 568

Rajkot (University Rd.) - Tel: (0281) 2331 418

Rajkot - (Bhakti Nagar) Tel: (0281) 2361 935

Rajkot - (Indira circle) Tel : 99258 84848

Rajkot (Orbit Plaza) - Tel: (0281) 3983 485

Rajkot (Pedak Rd) - Tel: (0281) 3985 100

Rajkot (Ring Road)- Mobile: 99245 99393

Rajkot (Star Chambers) - Tel : (0281)3981 200

Rajkot - (Star Chambers) - Tel : (0281) 2225 401-3

Salem - Tel: (0427) 3941 394

Surat (Ring Road) - Tel : (0261) 3071 600

Surendranagar - Tel : (02752) 223305

Secunderabad - Tel : (040) 3093 2600

Surat (Mahidharpura) - Tel: (0261) 3092 900

Surat - (Parle Point) - Tel : (0261) 3091 400

Pune - Tel : (020) 3093 4400 / 3052 3217

Udaipur - (0294) 3941 394

Valsad - Tel - (02632) 645 344 / 45

Vapi - Tel: (0260) 3941 394

Varachha - (0261) 3091 500

Vijayawada - Tel :(0866) 3984 600

Warangal - Tel: (0870) 3982 200

Varanasi - Tel: (0542) 2221 129, 3058 066

Tirupur - (0421) 4302 800