luder - a contingency model - james l. chan

TRANSCRIPT

99

A CONTINGENCY MODEL OF GOVERNMENTAL ACCOUNTING INNOVATIONS IN THE POLITICAL-ADMINISTRATIVE ENVIRONMENT

Klaus G. Lüder ________________________________________________________________________

ABSTRACT This paper proposes a comprehensive contingency model of introducing accounting innovations in the public sector. Based on a comparative study of the United States, Canada, and several European countries, the model consists of four modules: stimuli, social structural variables about information users, structural variables describing the politico-administrative system, and implementation barriers. Whether a more informative accounting system is introduced depends on the specific combination of favorable and unfavorable conditions in these modules. Favorable conditions exist in Canada, Denmark, Sweden, the United States at the federal level, and those states that adopted GAAP. Conditions unfavorable to innovations prevail in Germany and France, and to a lesser extent in the United Kingdom and the European Community. _______________________ Research in Governmental and Nonprofit Accounting, Vol. 7, pages 99-127. Copyright © 1992 by JAI Press Inc. All rights of reproduction in any form reserved. ISBN: 1-55938-418-2

100

I. REVIEW OF THE LITERATURE

A. A Classification of Recent Research The first attempts to analyze and explain the similarities and differences between various public sector accounting systems in the light of the politico-administrative factors that condition them are found in the Anglo-Saxon literature on the subject from about the mid 1970s [e.g., Zimmerman, 1977]. The object of this research was primarily to investigate the causes and deciding factors responsible for the decision by the states and local governments in the United States to abide by governmental Generally Accepted Accounting Principles (GAAP) in preparing their annual financial reports [e.g., Baber and Sen, 1984; Evans and Patton, 1987; Ingram, 1983, 1984]. These principles, initially codified by the National Council on Governmental Accounting (NCGA), are now set by the Governmental Accounting Standards Board (GASB). The hypothesized influence of the conditioning factors was analyzed in subsequent research on the basis of various theoretical approaches, research methods and subjects. This body of literature may therefore be classified accordingly. 1. Theoretical Orientation

On the basis of theoretical approach, the studies may be approximately subdivided into (1) those that are influenced by political science, more particularly the economic theory of politics (public choice) or comparative political science, and (2) those that are predominantly oriented towards behavior theory. The two approaches cannot of course be separated with absolute precision, since they share certain basic assumptions. In particular they both adopt methodological individualism, emphasizing individual behavior as conditioned by specific inclinations (i.e., maximization of utility) and situations (i.e., social and/or institutional factors).

Those studies that draw their inspiration from political economy [e.g., Chan and Rubin, 1987] are based on traditional neoclassical principles of explanation. Starting from classical behavioral assumptions such as utility maximization and limited rationality of the individual, this approach uses market mechanisms for coordination to achieve equilibrium. Analysis of coordination via the “market” is not confined to a price system of supply and demand for public services. It also takes social forms of coordination, for example, the “market for electoral votes,” into consideration. The principles of self-interest and the assumption of rational behavior are both taken as applicable to the state. That is, it is assumed that the protagonists in the fields of politics, government and administration pursue a form of self-interest [e.g., Buchanan, 1967; Chan and Rubin, 1987; Downs, 1957; Niskanen, 1971]. The possibility of being able to pursue one’s self-interest presupposes a discretionary margin in decision-making, which, as an endogenous variable, can be accounted for on the basis of asymmetrical distribution of information between the participants. If the restrictive classical assumption of complete information is abandoned, information itself becomes the subject of investigation, and so does the government financial accounting system.

101

One line of research concerns how information influences individuals’ decision-making processes. Other studies investigate how institutional arrangements (i.e., the political system and regulations) and changes to them shape the government’s information instruments such as its financial accounting system, and vice versa. Typical research questions are: How, why, and to what extent are accounting systems affected by politico-administrative structures and processes? Are there any interactions between socioeconomic institutions and the government’s financial reporting practices? If so, which interactions are significant? One consequence of such interactions is the further development of the government’s accounting system [Ingram, 1984, pp. 127-131]. The hypotheses based on such an approach are logically predicted on institutional factors of influence.

Approaches that tend to be oriented towards behavior theory [Chan, 1989; Evans and Patton, 1987] address not so much the institutional factors of influence as the individual ones. Institutional factors are, of course, not ignored. But their influence is regarded as being peripheral or restricting on individual behavior. This line of research analyzes the configuration of individuals, their interests, situations and behavior. If we take the public accounts as the subject of inquiry, this means formulating hypotheses to explain what motivates individuals to demand information and to promote the development of particular accounting systems. The motivations are based on their interest as, for example, voters, taxpayers, recipients of services, or members of parliament. 2. Research Methods Some studies test hypotheses by means of statistical or econometric techniques [Baber and Sen, 1984; Evans and Patton, 1987], while others examine the plausibility of hypotheses through a series of case studies of particular situations. The precision and accuracy of econometric methods undoubtedly contribute to their popular use in empirical studies. However, the nature of the data they use can often lead to questionable results. Statistical methods have minimum requirement for standardization of the subject of the investigation, especially as regards the quantification of variables. In view of the often purely qualitative nature of the variables to be tested, this requirement is not always assured. Exactitude of method does not exclude the possibility that a mathematical-statistical reshaping of the data will remain insignificant from the empirical point of view. Case studies, on the contrary, due to their flexibility, make it possible to describe a given situation closer to reality. The causal hypotheses underlying case studies are, however, not susceptible to statistical tests, although they could still meet plausibility tests.

102

B. Literature Analysis

This section analyzes a number of common themes and variables suggested in recent literature, followed by some concerns about research methods used. 1. Themes and Variables

Political Competition. Political competition promotes the use of GAAP in government. This is one of the most frequently made assertions in the literature concerning the relationship between institutional conditions and innovations in governmental accounting [Baber and Sen, 1984; Evans and Patton, 1987; Ingram, 1984; and numerous recent conferences not available for quotation]. Surprisingly, despite the varying interpretations and measurements of this ambiguous concept, most of the studies show positive correlations between political competition and the adoption of GAAP.

The fundamental common assumption shared by these studies is that there exists a “market” consisting of exchange relationships between voters, interest groups, politicians, and administrators. In this “market for votes,” politicians and parties are subject to a process of competition which, in order to maximize the number of votes, obliges them to satisfy the voters’ needs. “Political competition” can assume several forms: the competition for electoral success between parties; competition within a party for nomination as a candidate; competition for the support of interest groups; or competition in the search for coalition partners.

Evans and Patton [1987, p. 137] expressed the relationship between political competition and the adoption of GAAP as follows: “the greater is the political competition, the weaker is the politician’s position relative to the interest groups and, therefore, the better will be the monitoring information he must provide to obtain their support.” Other studies posit that governments that are subject to “competitive pressures” have a stronger incentive to show that they have fulfilled their election promises—for example, distribution of budgetary resources over several policy areas, the repayment of debts, the soundness of the budgetary management. This line of thinking introduces public opinion as an influence on public sector accounting.

The connection between political competition and application of the GAAP generally corresponds to agency theory and it is done by marginal analysis [Baber and Sen, 1984]. In an agency model, the initial situation is characterized by the asymmetrical distribution of information between the principals (e.g., the voters) and their agents (e.g., elected politicians). This asymmetry is reduced by setting up a monitoring system, such as a system of financial reporting, which facilitates a posteriori control to ensure ensuring that the promises have been kept. Among the measures is the promise of better information resulting from the adoption of G AAP. It is commonly assumed that GAAP-based financial information is better and more economical to produce by virtue of standardization.

103

If the starting situation involves a high degree of political competition, for example, in a “neck to neck” race between the incumbent and opposition in an election, use of the GAAP (or, as appropriate, the promise to use it) increases the likelihood of an electoral victory for its advocate. This is because, at the margin, when other things (e.g., political preferences) are equal, an improvement in the starting situation will be achieved by compliance with GAAP. From this abstract description of the situation, we may derive the proposition: ceteris paribus, the intensity of political competition promotes the use of the GAAP.

Moving from this proposition to an empirically testable hypothesis creates considerable problems. On the one hand, the effect of the use or nonuse of the GAAP on specific voting decisions, in comparison with other factors that may have a decisive effect on election results, cannot be isolated and operationalized. On the other hand, suitable measurable surrogates must be found for unobservable political competition. To the extent, therefore, that a statistical test to measure the correlation between political competition and use of the GAAP was carried out in empirical research, the results appear to be questionable, at least from the methodological point of view.

The Method for Selecting Accounting Officials. Alternatively, one might argue that the further development of public sector accounting is influenced by the way accounting officers are selected—by election or appointment [Ingram, 1984]. According to this view, an elected “monitoring agent” is directly subject to the competitive pressure of election and thus has a greater incentive, as compared with appointed (and in some cases tenured) public officials, to improve the accounting and reporting system. In addition, Ingram [1984, p. 17] comments, without any further justification, that “personal attributes (e.g., professional experience and training) may differ between elected and appointed administrators, and thus the extent of accounting disclosure may be affected by the administrative selection process itself.” If the accounting officers are more efficiently recruited in the political market, rather than by appointment, Ingram’s hypothesis acquires some plausibility from the extensive analyses of the economic theory of bureaucracy and the literature on public choice. Of course, in this specific expression the hypothesis is hardly capable of empirically testing. There also exists evidence to the contrary, that is, some jurisdictions that comply with GAAP have appointed accounting officials.

Size. Another hypothesis that is similarly based on the monitoring agent theory postulate is that use of the GAAP is more likely as the size of the government increases [Baber, 1983; quoted by Evans and Patton, 1987]. Size is measured by the population in absolute terms or population density. The hypothesis goes as follows: the more populous the area governed, the higher the government’s tax and other revenues tend to be, and the greater the amount of resources that may be badly managed. As the population increases, so does the number of persons who have an interest in the establishment of control systems. Monitoring costs as a proportion of the agency costs can be reduced in individual cases by standardized procedures (through the use of the GAAP). “Thus, cities with greater population are predicted to produce better reporting / more auditing because more resources are at stake” [Evans and Patton, 1987, p. 136]. This prediction, inspired by agency theory, is partly supported by empirical evidence from U.S. municipalities for

104

the period from 1981 to 1984. Ironically, the Federal Government in the U.S., the largest of all in terms of the number of people under its jurisdiction, does not have a GAAP-based accounting system.

Capital Market and Rating Agency Influences. Another hypothesis suggests that the capital market generates incentives for GAAP adoption [Evans and Patton, 1987; Ingram 1984]. This is based on a policy statement issued in 1980 by Standard and Poor, one of the largest American rating agencies, that nonuse of the GAAP would count as a negative factor in assessing the creditworthiness of a government. The capital (more specifically, bond) market, according to this hypothesis, rewards the use of the GAAP as evidence of qualified financial management by granting borrowers lower interest rates. Ingram [1984] concludes from this that the incentive to adopt the GAAP must be high, especially in the case of governments that are heavily burdened with debt, provided that the savings on interest costs are greater than the cost of modifying the accounting system. This line of argument appears to be perfectly plausible in the case of the American situation on account of the system of bond rating of government debt. As financial reports are only one of several sources of information in arriving at a rating, the impact of the quality of information in these reports can be overridden by other factors (such as taxing capacity). Furthermore, this hypothesis has limited application in the international context, as government debts are not rated in all countries.

Financial Reports as a Signaling and Monitoring Tool. The hypotheses advanced

in the research work analyzed so far are largely based on presumed individual attitudes. The accounting system, taken as a given and shaped by institutional conditions, is included in the analysis as a datum. The system of institutions provides the framework within which individuals are led to make conceptual changes to the public sector accounting system and financial reports. The institutional factors condition the attitudes of participants and those who are directly affected towards a definite reshaping of the accounting system. They also determine the demand for and the supply of financial information. In terms of agency theory, to quote Baber and Sen [1984, p. 92], “We view the political market as a nexus of contracting relationships between interest groups (principals) and public officials (public agents) and assume that the contracting parties are rational self-interested individuals.” In such a model, the public officials as agents “signal the principals, who in turn “monitor” the politicians. “Accounting practices evolve under the influence of politicians’ attempts to maximize the benefits of office and voters’ attempts to constrain the politicians’ abilities to act to their detriment” [Ingram, 1984, p. 127].

105

Users’ Socioeconomic Status. More recently, it is no longer assumed that individuals have identical demands for information, as they are not identical in the socioeconomic attributes relevant for predicting their demand for government financial information. The principal’s (e.g., voter’s) demand for information is related to one’s socioeconomic status (SES) [Chan, 1989, p. 8]. As early as 1960, Downs [1960] posited that individuals find it easier to grasp the costs of state services than the benefit they derived from them—thus resulting in a kind of fiscal illusion. It is argued that the rising tax burden that accompanies a higher income is more acutely perceived than any increases in social service. This effect is reinforced by the fact that individuals whose incomes and tax burdens are rising ultimately become “net contributors” in respect to public services, whereas individuals with lower incomes and lower tax obligations are “net beneficiaries.” For this reason, the level of demand for information goes up as one’s socioeconomic status rises. It is therefore hypothesized that as one’s SES improves, so does one’s awareness of costs of government (i.e., government revenue and debt) increase relative to one’s awareness of benefits of government (i.e., government expenditure). This line of reasoning leads to the following propositions about demand for specific information. “[Members of the public] of lower SES have greater demand for expenditure information. [Those] of higher SES have greater demand for information about revenues and liabilities” [Chan, 1989, p. 8].

Cost is a relevant consideration in the use of information, as it is in the adoption of GAAP. Demand for information is limited by the marginal benefit of additional information compared with the marginal cost of acquiring and evaluating information. The time needed to evaluate information is seen as an essential cost component. This leads to the complementary hypothesis that as socioeconomic status rises increased demands are made as regards the quality of the information. “Individuals of higher SES enjoy a higher cost-benefit ratio in investing their time in this activity on two accounts: (1) their higher educational level reduces the costs of analysis and evaluation; and (2) as they bear higher per capita tax burdens they have greater economic incentives to find tax savings or how their tax dollars are spent” [Chan, 1989, p. 12].

Professionalism. The existence of signaling incentives, which lead to the “voluntary” provision of financial information by the executive branch and the legislature, does not at first seem plausible because of the additional monitoring possibilities that are bound up with them. The fact that the signaling effects that stem from voluntary conformity with a system of rules such as the GAAP may be perfectly rational may, however, be explained in terms of the agency theory. In an initial situation that is characterized by intense political competition, for example, there is a need to demonstrate the qualifications and the quality of public management in order to increase the likelihood of reelection. One way of achieving that is to make use of an accounting system that is oriented towards the GAAP in order to signal a certain level of professionalism [Evans and Patton, 1984; Ingram, 1984] Various topics were raised as test variables for such signaling incentives, for example, recourse to standard-setting bodies as advisers, the demands made on the account staff as regards qualifications and even the level of their salaries [Evans and Patton, 1984]. This latter approach rests on the assumption that governments that wish to indicate the level of professionalism of their financial management for the purpose of obtaining highly qualified staff (e.g., auditors),

106

must offer substantial financial incentives. In general, hypotheses that are formulated in this way exclude the possibility of their being clearly and neatly distinguished from others, such as, for example, the influence of political competition on use of the GAAP, so that the presumed influence of signaling incentives as compared with other influences cannot be singled out.

C. Comments

Inasmuch as an attempt is made in these studies to test the hypotheses with statistical procedures, reservations may be raised in at least three respects:

1. The relationship between use of the GAAP as a dependent variable and the above-mentioned independent variables are not monocausal but multicausal. The independent variables may have an additional, mutual effect on each other. So it is conceivable (but so far barely demonstrated by the statistical tests) that, for example, the level and the growth of indebtedness, and the effect of professional organizations, do not favor the use of GAAP in isolation of each other but rather through a kind of synergy. Moreover, it is also conceivable that, as the growth of debt comes increasingly to be seen as “desperate,” the need for competent advise from professional organizations will rise and become institutionalized. In the former case, instead of the usual simple regression, multiple regressions would have to be carried out. In the latter case, multicollinearity, which is statistically relevant, occurs. The doubtfulness of the statistical results of the studies being evaluated as regards multicausality and multicollinearity may presumably be applicable to an even higher degree in the concept of political competition, which is frequently tested as if it were an independent variable. If the use of GAAP is to be explained as dependent variable (with a decisive influence on election results), the existence of political competition (however defined and measured) as the only (independent) explanatory factor is probably not enough. Since the results of an election are decided by a “package” of political measures, it is doubtful that the use or nonuse of the GAAP would have such a decisive impact. As hypotheses are usually formulated independently of each other, their tests also tend to look for monocausal connections. The multicollinearity can be detected by observing correlation matrices. Multiple regression analysis, however, is only rarely carried out.

107

2. The variables in the above-mentioned hypotheses are frequently difficult to measure directly. It is thus necessary to operationalize them by means of observable and measurable proxy variables. Valid surrogates are essential to avoid mistaken interpretation. Two examples may illustrate this point. “Interest costs of state debt” operationalize the capital market’s rewards for the use of GAAP. On the other hand, salary of accountancy staff (used in Evans and Patton 1987, p. 131) is not an adequate reliable indicator of staff qualification, as salary is determined by many factors other than qualification. No account is taken, in this assumption, of other factors that also help to determine salary levels. In some cases other variables influence both use of the GAAP and salary levels. In such cases there is an apparent correlation, but it is only apparent.

Probably the most serious objection to statistical tests concerns the use of regression analysis. Regression analysis, in contrast to other multivariate methods (e.g., discrimination or contingency analysis), requires a metrical measurement of both dependent and independent variables. Of course, account may be taken of only nominally measured variables, by breaking them down into binary variables, but this is only applicable in the case of independent variables. This, however, is exactly what is not the case in the studies we are concerned with here: the use of a binarily defined dependent variable (use or non-use of GAAP). It is no more than the classification of a nominally measured, quantitative expression of qualities, for which it is only possible to calculate degrees of frequency, with which the categories of characteristics known as “use” and “nonuse” are filled out. For this same reason the forms taken by the characteristics in question can also not be subjected to the requisite accounting transformations without which a regression analysis is devoid of meaning.

3. It also seems questionable whether the use or nonuse of the GAAP can really be conceived of as a binary variable at all. The extensive body of rules within which the GAAP are codified, with their numerous, intrinsic margins for maneuver on the basis of electoral legislation, ultimately does not make for any hard and fast decision as to when, in a particular case, it can be assumed that there is use or nonuse of the GAAP.

The present state of empirical research into the relationships between institutional conditions and the shaping of public accounting is characterized by the “incongruity” which Helmut Klages [1977] similarly found to exist in the case of organizational contingency theory, between “highly developed empirical instruments and manifold findings, on the one hand, and contradictory theoretical elements, on the other” [Kieser and Kubicek, 1983, p. 353, with reference to Klages, 1977, p. 61]. In this case, as in that of organizational contingency theory, this seems to be not least the consequence of a dominant paradigm of empirical social science research in the United States.

108

II. A CONTINGENCY MODEL OF GOVERNMENTAL ACCOUNTING INNOVATIONS

A. Overview and Assumptions

This section proposes a model that explains the transition from traditional

government accounting to a more informative system. A more informative system performs two functions: it supplies comprehensive and reliable information on public finance, and it provides a basis for improved financial control of government activities. The transition assumes a specific starting point and final state for the public sector accounting system. The task of the model is to explain the innovation process that connects these two points. Unlike previous efforts that singled out individual background conditions, a conceptual overview is provided that would explain the process of innovation (or its absence) as fully as possible. Due to its high degree of complexity, the model currently may not be statistically testable.

The model seeks to integrate ideas from the literature as described earlier, along with observations made about the governmental accounting systems in Canada, the United States (the federal government and several states), and several European countries, including Denmark, France, Germany, Sweden, the United Kingdom, and the European Community. Interviews were conducted with knowledgeable persons to ascertain practices as well as innovations being contemplated or underway, if any. The politico-administrative environment in terms of the variables encompassed in the model was documented [Lüder , 1989; Lüder , et al., 1989]. After the model was described, these countries were compared along the various dimensions of the model on the basis of the empirical observations made in the empirical phase of the study (henceforth the “Comparative Study”) in 1987-1988.

The structure of the model is similar to models of organizational contingency theory, extended, however, by behavioral components [Khandwalla, 1977, p. 270; Kieser and Kubicek, 1983, p. 355; Schreyogg, 1985]. Such a model can include both institutional background conditions and collective behavior as determinants of the innovation process. The contextual variables describing institutional conditions may be classified, according to their functions in the innovation process, into three categories:

1. Stimuli [Simon, 1981, p. 126]: events that occur at the initial stage of the

innovation process and create a need for improved information on the part of the users of accounting information and increase the producers’ readiness to supply such information.

2. Structural Variables: characteristics of the social and politico-administrative systems that influence the basic attitudes of users and producers of information towards the idea of a more informative form of public sector accounting.

3. Implementation Barriers: environmental conditions that inhibit the process of implementation, thus hindering, and in extreme cases preventing, the creation of a more informative accounting system which is in principle desirable.

109

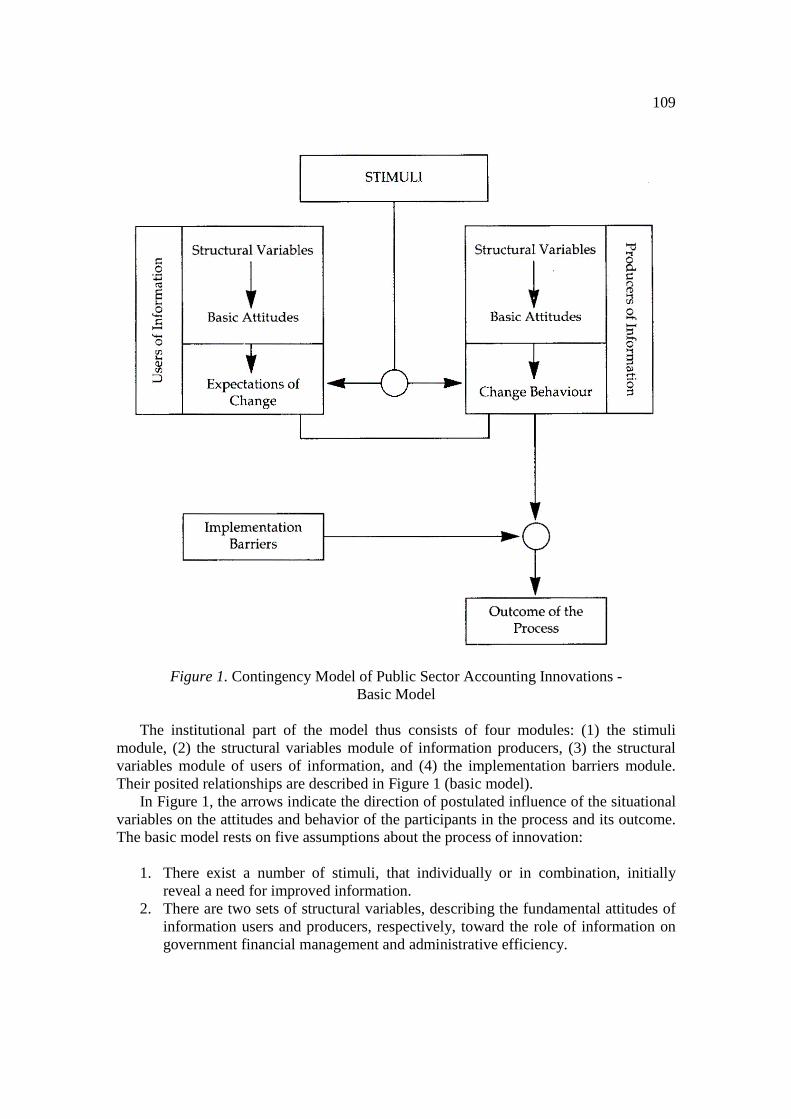

Figure 1. Contingency Model of Public Sector Accounting Innovations - Basic Model

The institutional part of the model thus consists of four modules: (1) the stimuli

module, (2) the structural variables module of information producers, (3) the structural variables module of users of information, and (4) the implementation barriers module. Their posited relationships are described in Figure 1 (basic model).

In Figure 1, the arrows indicate the direction of postulated influence of the situational variables on the attitudes and behavior of the participants in the process and its outcome. The basic model rests on five assumptions about the process of innovation:

1. There exist a number of stimuli, that individually or in combination, initially reveal a need for improved information.

2. There are two sets of structural variables, describing the fundamental attitudes of information users and producers, respectively, toward the role of information on government financial management and administrative efficiency.

110

3. Information users’ expectations of change are influenced by their basic attitudes and by the stimuli that exist in the starting situation. The information producers’ willingness to make changes is similarly affected by these two factors, and the effects of the information users’ expectations of change.

4. The setting off of the process of innovation does not necessarily require the existence of a stimulus. Basic attitudes (that have been changed) can also raise the level of willingness to make change in such a way that the decision to do so is taken.

5. The decision to innovate is dependent not only of the information producer’s willingness to change, but also the implementation barrier. Two extreme cases are conceivable. In the first case, if all the factors affecting implementation are neutral to the changes, the innovation decision is determined by the degree of willingness to accept change. In the second case, if all the factors affecting implementation inhibit change, a high degree of willingness to accept is required, or change may not be achievable at all.

In each case the complex of relationships between the specific form assumed by

public sector accounting and the factors that affect it cannot be traced back like a monocausal concatenation of effects. Rather one must start from the assumption that a specific constellation of background conditions collectively affect the public sector accounting system (multicausal relationship).

As mentioned earlier, the specification of the basic model draws on the results of a number of empirical studies, primarily on the Comparative Study. However, the model has some speculative features, too, as the empirical relevance of the environmental conditions and their relationships with the accounting system are not definitely settled. Moreover, the model may not contain all conceivable and relevant independent variables. The contingency model therefore should be understood and interpreted as a first attempt to describe a complex innovation process by a set of hypotheses.

B. Description of the Model

The institutional part of the specific form of the model consists of the same four modules as the basic model. The components of the individual modules, the relationships between them and their effects on the results of the innovation process are set out in Figure 2. This section examines the institutional modules. It assumes, as does organizational contingency theory, that the specific configurations or institutional components influence the attitudes and behavior of the participants m public life, politics and administration. The mechanism by which this influence is exerted and its strength are not, however, examined in detail.

111

Figure 2. Contingency Model of Public Sector Accounting Innovations –

Detailed Model

112

1. Stimuli

Fiscal Stress. Financial difficulty arises when the increase in and/or the absolute level of public debt are considered to be no longer sustainable in terms of interest burden, interest rate or creditworthiness. In such a situation, comprehensive disclosure of the financial situation as well as financial management takes on enhanced importance. At the same time, however, the shortcomings of traditional public sector accounting systems are borne more strongly upon the consciousness of the participants, prompting demands for a more informative accounting system.

Research results have confirmed that financial problems serve to trigger reforms of public sector accounting systems. They regularly played a role in the case of governments that carried out conceptual changes to their accounting systems during the 1980s. This was true of Canada, Sweden, Denmark, the states of the United States, the Canadian provinces, and also Great Britain (which primarily reformed its internal accounting system to ensure better financial management of government departments and agencies). More recently, the budget deficits of the U.S. Government have, partially at least, contributed to the urgency of improving the federal Governments’ accounting system [Carpenter and Feroz, 1990; GAO, 1989].

Financial Scandal. The term “financial scandal” refers to cases of negligent or deliberate waste in financial management by the public authorities with serious financial consequences for the taxpayers. In some cases such practices are connected to deliberate misleading information on the financial situation. Depending on a government’s fiscal situation, and the scale and the timing of its revelation, a financial scandal may result in a situation of fiscal stress. Regardless of that, however, financial scandals draw the attention of the public and of those who are immediately involved, to shortcomings in the accounting system. This may trigger a reshaping of the system to make it more informative. For example, the poor quality of the fiscal information revealed in New York City’s financial crisis helped to create an atmosphere conducive to the establishment of the Governmental Accounting Standards Board.

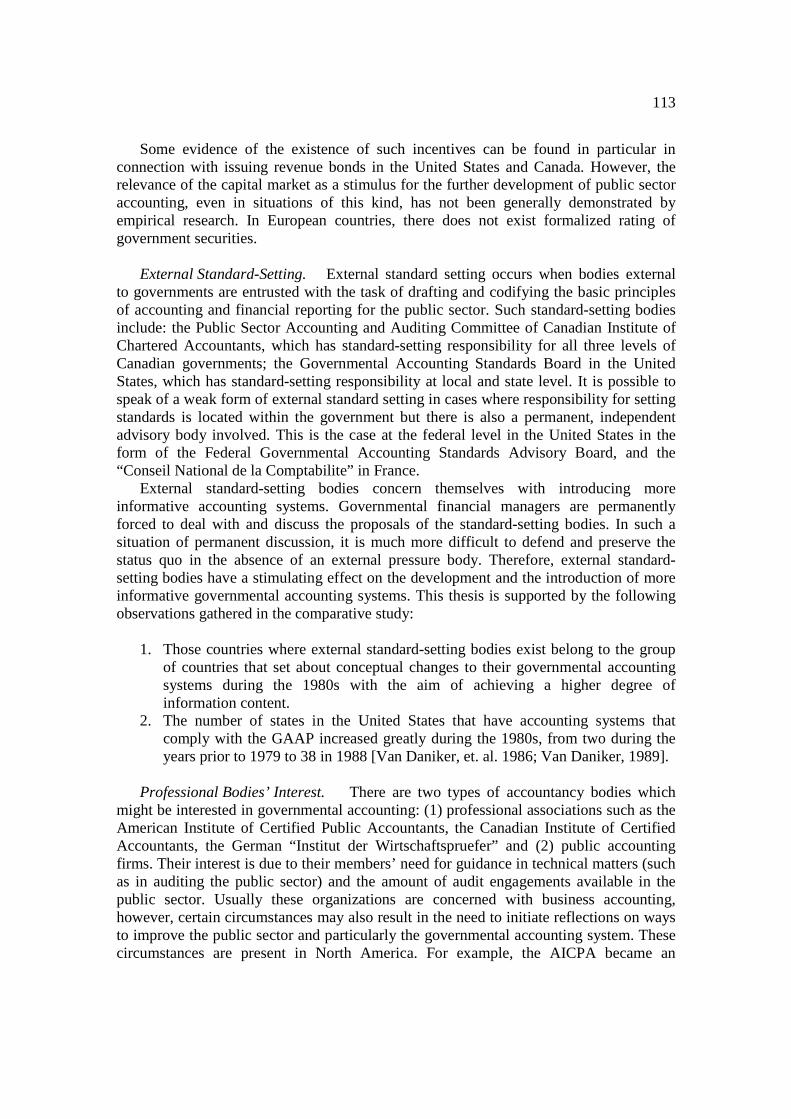

Capital Market. The capital market can be the source of incentives to create a more informative system of governmental accounting and financial reporting. However, this possibility rests on two premises: (1) bond issues are subject to formalized ratings; (2) the issue conditions, in particular the rate of interest, depend on the results of such ratings. The rating agencies mainly make use of annual reports, along with economic background data (such as expected tax revenues), as their sources of information. The other factor that affects the rating is the quality of the information in a government’s annual report. If the generally accepted principles of accounting are not observed in describing the financial situation, the rating may be lower. This potential risk acts as a sanction for the distortion or concealment of information. It constitutes an incentive for the government in question to convert to GAAP, provided that the expected benefits exceed the costs.

113

Some evidence of the existence of such incentives can be found in particular in connection with issuing revenue bonds in the United States and Canada. However, the relevance of the capital market as a stimulus for the further development of public sector accounting, even in situations of this kind, has not been generally demonstrated by empirical research. In European countries, there does not exist formalized rating of government securities.

External Standard-Setting. External standard setting occurs when bodies external

to governments are entrusted with the task of drafting and codifying the basic principles of accounting and financial reporting for the public sector. Such standard-setting bodies include: the Public Sector Accounting and Auditing Committee of Canadian Institute of Chartered Accountants, which has standard-setting responsibility for all three levels of Canadian governments; the Governmental Accounting Standards Board in the United States, which has standard-setting responsibility at local and state level. It is possible to speak of a weak form of external standard setting in cases where responsibility for setting standards is located within the government but there is also a permanent, independent advisory body involved. This is the case at the federal level in the United States in the form of the Federal Governmental Accounting Standards Advisory Board, and the “Conseil National de la Comptabilite” in France.

External standard-setting bodies concern themselves with introducing more informative accounting systems. Governmental financial managers are permanently forced to deal with and discuss the proposals of the standard-setting bodies. In such a situation of permanent discussion, it is much more difficult to defend and preserve the status quo in the absence of an external pressure body. Therefore, external standard-setting bodies have a stimulating effect on the development and the introduction of more informative governmental accounting systems. This thesis is supported by the following observations gathered in the comparative study:

1. Those countries where external standard-setting bodies exist belong to the group

of countries that set about conceptual changes to their governmental accounting systems during the 1980s with the aim of achieving a higher degree of information content.

2. The number of states in the United States that have accounting systems that comply with the GAAP increased greatly during the 1980s, from two during the years prior to 1979 to 38 in 1988 [Van Daniker, et. al. 1986; Van Daniker, 1989].

Professional Bodies’ Interest. There are two types of accountancy bodies which

might be interested in governmental accounting: (1) professional associations such as the American Institute of Certified Public Accountants, the Canadian Institute of Certified Accountants, the German “Institut der Wirtschaftspruefer” and (2) public accounting firms. Their interest is due to their members’ need for guidance in technical matters (such as in auditing the public sector) and the amount of audit engagements available in the public sector. Usually these organizations are concerned with business accounting, however, certain circumstances may also result in the need to initiate reflections on ways to improve the public sector and particularly the governmental accounting system. These circumstances are present in North America. For example, the AICPA became an

114

instrumental force in creating the GASB in part to protect its interests and that of the Financial Accounting Standards Board. If there is an interest of professional organizations in the public sector, a strong interest in the application of private-sector accounting in the public sector can be presumed as well. Proposals are frequently put forward for discussion at meetings of professional associations and within auditing firms [e.g., Arthur Anderson & Co., 1986]. In contrast, in the countries of Continental Europe covered by the comparative study, professional interest in public sector accounting is weak. Government and private-sector accountants do not belong to the same professional associations. Furthermore, there is also relatively little business potential for accounting firms in public sector audit engagements. 2. Social Structure Variables

Socioeconomic Status. Chan and Rubin [1987] introduced the notion of “socioeconomic status” (SES) as a means of explaining the influence of economic and social background conditions on the information content of public sector financial reports. Socioeconomic status is reflected by many variables, such as income and education levels. It is argued that voters’ SES influence their tax burden and public services received. As one’s SES rises, so does his share of the tax burden; however, SES is negatively correlated with the amount of public services received. Thus it is argued that higher SES individuals have a greater interest in disclosure of the public sector financial management. Socioeconomic status is therefore related to the basic attitude of information users toward more informative forms of public sector financial reporting. So far, this hypothesis has not been tested empirically; nor was it possible to obtain evidence of its validity during the comparative study.

Political Culture. “Political culture” in this context is to be understood as “patterns of political behavior” in which social value concepts are expressed. Political culture influences the basic attitudes of information users regarding the disclosure of information on public sector financial management, and thus also on their view of the need for a more informative accounting system. Political culture is revealed by the degree of openness and the participation by the citizenry in public decision-making processes. The more the political culture is open and disposed towards public participation, the greater the information users’ expectations of financial information from the public sector. Active participants in the political system prefer comprehensive information on the government’s financial management. An indication of the degree of openness and participation in political decision-making processes is the importance of referenda and other consultative procedures based on direct democracy (in particular, the direct election of the holders of the highest administrative offices).

115

To the extent that a relative high degree of openness and participation may be assumed in the countries included in the comparative study (Sweden, Switzerland, some states in the United States), innovation in the direction of a more informative system of governmental accounting may also be observed. 3. Structural Variables of the Politico-Administrative System

Staff Training and Recruitment. The training of administrative, especially accounting staff, and the recruitment of persons for top fiscal positions (e.g., financial controller, auditor) are factors that influence the basic attitudes (i.e., readiness to accept change) of these information producers to the further development of public sector accounting. Government accountants and auditors in different countries have rather diverse professional training and backgrounds. The United States and Canada have a large number of private-sector accounting specialists on their staffs in the public sector. This is due partly to formal legal requirements and partly to the customary practice of emphasizing the possession of professional accounting credentials, such as the CPA in the United States and the CA in Canada, for high level government accounting and auditing positions. On the other hand, in Germany, for example, the appointment to the position of the President of the Court of Auditors (federal and state) requires an education in law, but no education and practice as an accountant is required. The administrative staff in accounting and auditing in French government receive specialty training in public sector accounting. Whereas in some other countries (Germany, the United Kingdom) many governmental accounting staff have not had any accounting education at all and do get on-the-job training only.

Specialist training or qualifications as accountants, which cover knowledge and experience of private-sector accounting, give reason to expect a more positive basic attitude to the introduction of a more informative system. Such systems are regarded by some as more strongly oriented toward the private-sector approach. Those only trained in traditional public-sector accounting, on the other hand, often lack the incentive for suggesting innovations. A positive attitude toward improvements in governmental accounting does not only positively affect the accounting staff’s willingness to implement changes but it even gives rise to initiating ideas for a more informative accounting system.

From the comparative study, it can be seen that in those countries with a form of staff training and recruitment that is strongly oriented towards the private-sector, as in the United States and Canada, further development of the public-sector system in the direction of a more informative type of accounting was observed.

116

Administrative Culture. Administrative culture is apart of the political culture. To the extent that the political culture is open and encourages participation, that will also be the case for administrative culture. Administrative culture has an effect on the basic attitude of administrative staff to openness and popular participation in the public policy process. In an open administrative culture, information producers themselves have a positive basic attitude to the idea of a more informative governmental accounting and financial reporting system.

Political Competition. The term “political competition” has two distinct meanings.

The first is in the sense of competition in the “market for votes”; and the second refers to the competition between decision-making bodies (the executive and legislative branches of government) and the electorate. The first meaning is adopted in the above-mentioned American studies. The second meaning, however, seems to be more appropriate in the institutional module of a contingency model of governmental accounting. In both cases, however, the supposed connection between political competition and the form of accounting is rooted in agency theory considerations. Stronger political competition between users of information (i.e., the electorate and the legislature) and producers of information (i.e., executive) enables the former to assert their information interests more easily and thus to bring about a reduction in the asymmetrical distribution of information between users and producers.

Political competition in tendency causes an endeavor and readiness to achieve a more informative system of governmental accounting given the interest of users in additional or improved information. Under the institutional approach the strength of competition between producers and users of information is thought to be determined by the degree of symmetry in the distribution of power between the legislative, the executive branch, and electorate. A high degree of political competition may thus be assumed if the degree of division of power between the legislature and the executive is relatively symmetrical, for example, there exist extensive checks and balances. This criterion is supplemented by the extent to which elements of direct democracy are present in the political decision-making process. This situation is, for example, found in American federal and state governments. In contrast, there is a low degree of political competition if the division of power between the legislature and the executive is relatively asymmetrical and plebiscite-like aspects are entirely or mainly absent. France and the European Community (EC) can be named as examples for governments with a low degree of political competition. Figure 3 represents an attempt to binarily classify governments in terms of the degree of political competition.

It is hypothesized that vigorous political competition leads to information producers’ positive basic attitude toward the introduction of a more informative governmental accounting system, whereas weak political competition is correlated with a negative basic attitude. This hypothesis is largely borne out by the two extreme examples mentioned earlier, namely the United States and France. Political competition also acts as a mechanism whereby users of information are able to exert influence over producers of information.

117

Division of power between legislature and executive

Plebiscite-like aspects present yes no

Definitely symmetrical

of political

Slightly asymmetrical

High degree competition

Low degree of

Definitely asymmetrical

political competition

Figure 3. Political Competition

4. Implementation Barriers

Organizational Characteristics. The decentralization of responsibility for changes of accounting practices in the government seem to be an important organizational implementation barrier. In a government with several organizational units exercising responsibility for the development of accounting procedures, there exists the risk that strongly diversified—and nonuniform—accounting systems will develop. Furthermore, those organizational units may have different ideas of what and how to change and thus get into conflict with each other. This was and still is the case at the Federal level in the United States: each agency, within the overall framework of the General Accounting Office’s responsibility for issuing guidelines, is answerable for its own accounting. Even the GAO’s authority to issue guidelines exists only on paper—it cannot be insisted on in face of the opposition of the executive branch:”... fragmentation of financial management functions has hindered development of a governmentwide financial reporting system” [Arthur Andersen & Co., 1986]. For this reason there has long been a call for the creation of the post of Chief Financial Officer, who would be responsible for the development of the conceptual bases for the federal accounting system and at the same time would have full powers to ensure their implementation.

118

Legal System. The legal systems of the countries included in the Comparative Study come either under the Roman-Germanic tradition or the English tradition. In the Roman-Germanic tradition—or civil law countries—a comprehensive and detailed system of statute law has been developed, whereas in the countries with English legal tradition—the common law countries—the statute law is limited in quantity and predominantly of the common law type. A country’s legal tradition is also reflected in the extent of legal codification of the regulations for public sector accounting. In the countries with Roman-Germanic traditions, such as France and Germany, public sector accounting principles and procedures are laid down in details by law. On the other hand, in countries belonging to the English tradition such as the United Kingdom, the United States and Canada, there are only general legal prescriptions for the keeping of public sector accounts. The legal system thus influences the flexibility of the public sector accounting system. The tendency is for the system to be less flexible in countries that belong to the Roman-Germanic tradition than in countries with English legal tradition. As a result of its built-in inflexibility, the legal system of civil law countries offers greater impediment to changes to the public sector accounting system than the legal system of common law countries.

Qualification of Accountancy Staff. As described earlier, the accountancy staffs of

some countries are dominated by individuals trained in private or public sector accounting, while in others the positions are occupied by nonspecialists, that is, not professional accountants or auditors, who learn specific accounting techniques on the job. The lack of certain general skills in the accounting field may create implementation barriers which cannot be eliminated in the short term and which may in certain circumstances mean that attempts to introduce more informative accounting will fail. This danger exists, for example, when accountancy techniques must be fundamentally altered in connection with the introduction of new accounting concepts (e.g., cameralistics, double-entry bookkeeping) and the accountancy staff lack the knowledge needed for the implementation of such new techniques.

Size of Jurisdiction. The size of a jurisdiction is expressed in terms of the

population size and the number and size of government agencies, which are positively correlated. Understood in this sense, as the size of jurisdiction increases, technical and administrative problems of implementing a new accounting and financial reporting system multiply and cost of implementation rises. This may be an additional reason why innovations are more frequently seen in the smaller territorial units (smaller countries, such as Denmark, Sweden, and the member states of larger countries with federal constitutions) than in the larger ones.

119

III. SITUATIONAL PATTERNS The environmental factors in a particular entity affecting accounting reforms may be

described by a combination of the various manifestations of the institutional modules of the contingency model. For simplicity, it is assumed that each module exhibits just two different manifestations, one which is favorable (+) and the other one which is unfavorable (-) to accounting reforms. Since the model contains four modules a total of 16 (= 24) different patterns of environmental conditions can be derived which are differently favorable to the implementation of a more informative governmental accounting and financial reporting system. The two extreme patterns are characterized by only favorable manifestations and by only unfavorable manifestations of all the modules, respectively.

As each of the modules contains a set of variables, the following operational definitions of “favorable” and “unfavorable” are used.

• The stimulus module is favorable if at least one stimulus is present. • The module of the social structural variables is favorable if the following

conditions can be assumed to exist: a strong political competition; and either a relatively high socioeconomic status, or an “open” type of political culture, or both.

• The module of structural variables of the politico-administrative system is “favorable” if at the least either the contents of staff training are predominantly influenced by private-sector accounting, or the administrative culture may be regarded as open and the degree of political competition may be considered high. Here varying weights are attributed to the module components, mainly because political competition is effective only in conjunction with information users’ expectations of change.

• The implementation barriers module is “favorable” if such barriers do not exist. In Figure 4, the governmental accounting system of each of the jurisdictions included

in the comparative study is assigned to the situation pattern it best fits. This assignment is based on either (1) the evidence of the respective politico-administrative background conditions as they were observed during the empirical investigations carried out in 1987 and 1988, or (2) if at that time an innovation process had already been initiated, the evidence of the politico-administrative situation existing prior to the commencement of the innovation process. As far as component states (U.S. states and Canadian provinces) of federations are concerned, the assignment is on a summary basis. The certainly observable differences between the politico-administrative settings of the states of a federation are neglected since the very broad classificatory approach does not seem to be sensitive to those differences. The overall assessment of a specific situational pattern as “favorable” or “unfavorable” to the implementation of a more informative governmental accounting and financial reporting system may best be characterized, in the words of Khandwalla [1977, p. 279], as an assessment “on the basis of research results and/or informed speculation.”

1

20

Mo

dul

e

S I

JUR

ISD

ICT

ION

G

N

C

AN

(F

eder

al

&

Pro

vin

cial

G

vts.

)

D

DK

E

C

F

S

UK

U

SA

(F

eder

al

Gvt

.)

US

A

(Sta

te

Gvt

s.)

(+

) X

X

X

X

X

X

X

S

timul

i

(-)

X

X

So

cial

Str

uct

ura

l (+

)

X1

X

X

V

aria

bles

(-

)

X

X

X

X

X

X

S

truc

tura

l Var

iabl

es o

f (+

) X

X

X

X

X

P

olit

ico-

Ad

min

istr

ativ

e

S

yste

m

(-)

X

X

X

X

Impl

emen

tatio

n

(+)

X

X

X

X

B

arrie

rs

(-)

X

X

X

X2

X

(+)

X

X

X

X

X

Ove

rall

Ass

essm

ent

(-)

X

X

X

X

Note

s:

(+

): F

avo

rab

le to

th

e im

plem

enta

tion

of

a m

ore

info

rmat

ive

pub

lic s

ecto

r ac

coun

ting

syst

em

(--)

: U

nfa

vora

ble

C

AN

= C

anad

a; D

= G

erm

any;

DK

= D

enm

ark;

EC

= E

uro

pea

n C

om

mu

nity

; F

= F

ran

ce; S

= S

wed

en;

UK

= U

nite

d

Kin

gdo

m;

US

A =

Un

ited

Sta

tes

of A

mer

ica

1 Th

e E

C f

aces

a p

artic

ular

situ

atio

n: in

the

case

of

fin

anci

al p

robl

ems

(whi

ch w

as u

nd

er c

onsi

der

atio

n

her

e) t

he

user

s of

fin

anci

al in

form

atio

n

(mem

ber

co

unt

ries

) ar

e ab

le t

o co

nsi

der

ably

influ

ence

th

e b

ehav

ior

of t

he

pro

du

cers

of t

he

info

rmat

ion

(C

om

mis

sion

).

2 Rel

ativ

ely

slig

ht

impl

emen

tatio

n b

arri

ers

(onl

y “q

ual

ifica

tion

s,”

may

be

size

).

F

igu

re 4

. C

lass

ifica

tion

of J

uris

dict

ions

121

On the basis of the situation patterns observed for the various jurisdictions, the following hypotheses are proposed:

1. The politico-administrative background conditions for the introduction of a more

informative system of governmental accounting are comparatively favorable in Canada, Denmark, Sweden, and the United States. In these countries, one may most readily expect innovations to have occurred, or will occur, in the system of public sector accounting.

2. The politico-administrative background conditions observed in Germany and France are comparatively unfavorable to the introduction of a more informative governmental accounting system. In the case of the EC (due to the stimulus and the influence of the users of information) and the United Kingdom (thanks to the presence of a stimulus and feeble implementation barriers) this is true only within certain restrictions. In all of those jurisdictions but particularly in France and Germany, innovations in governmental accounting and financial reporting are rather unlikely.

IV. EMPIRICAL OBSERVATIONS OF THE

RELATIONSHIPS BETWEEN THE NATIONAL SITUATIONAL PATTERNS AND THE STATE OF THE

ART IN GOVERNMENTAL ACCOUNTING As to the state of the art in governmental accounting and financial reporting the jurisdiction that were included in the comparative study may be classified as “rather progressive” and “rather rooted in the tradition.” “Rather progressive” entities are those which, during the 1980s, planned fundamental changes to their systems of governmental accounting and—in the meantime—at least initiated the implementation of these changes. In contrast, those entities that kept their systems of governmental accounting largely unchanged during the period in question, or carried out merely procedural (but not conceptual) changes, are classified as “rather rooted in tradition.” The entities that were examined are assigned, as far as feasible, accordingly. In this way it can be established whether there are any common features that distinguish the entities in the two categories, in relation to the politico-administrative background conditions, and if so which.

A. Progressive Units The “rather progressive” units include the Scandinavian countries of Denmark and Sweden, Canada, some Canadian provinces (in particular Alberta and British Columbia) and those states in the United States that have adopted the GAAP. The characteristics of governmental accounting systems used in these entities are:

122

• Replacing the concept of net monetary debt with concept of net total debt or a near-net-total-debt approach.

• Expanding the recipients of government financial reports beyond Members of Parliament, in particular with the objective of making more and better information on the public financial management available to the general public.

• Making annual financial reports more “user-friendly” by means of improving their explanatory notes, producing summary reports, or otherwise improving the accessibility for those who do not belong to either the legislature or the executive branch of government.

As far as the politico-administrative background conditions are concerned, it is remarkable that the smaller territorial units that are covered by the comparative study are the progressive ones. The North American entities enjoy background conditions that are conducive to changes in the system of their public sector accounting. Using the notion of the contingency model described above, those conditions include:

• a relative strong political competition (with elements of direct democracy, competition between the executive branch and Parliament particularly on the state level of the United States);

• considerable influence exercised by external standard-setting bodies (i.e., the GASB in the United States and the CICA’s Public Sector Accounting and Auditing Committee in Canada);

• accountancy staff trained in the techniques of private sector accounting; • the existence of capital market incentives to produce informative financial

statements; and • a flexible legal system.

In the Scandinavian countries, the connection between the politico-administrative

background conditions and the form of the public-sector accounting system is not so unambiguous. Both Denmark and Sweden are characterized in general by a particular orientation of the political process towards disclosure, with, as a consequence, specific attitudes on the part of politicians, administrators, and the public to the supply and demand for information. That means that the citizenry expect fundamentally candid information on the financial and economic situation of the state, and government agencies are fundamentally disposed to supply such information. In addition, in the first half of the 1980s, both Denmark and Sweden experienced critical financial situations, with rapid rises in the level of state indebtedness (by about 300% in Denmark between 1980 and 1985 and by more than 270% in Sweden). It may be assumed that this resulted in pressure on the government and administration to ensure administrative efficiency and to demonstrate sound financial management to the public. The device for being able to do that is an appropriate accounting and financial reporting system, for whose reshaping certain factors favorable to implementation existed: DP support for the system of public accounts and a legal system that was not too restrictive (this latter factor was even truer of Sweden than of Denmark). In contrast to the North American territorial units, Denmark and Sweden have built up and developed their management accounting systems ahead of, or at least in parallel with, their external systems. The reason for that may

123

presumably be found in the external drive to improve governmental efficiency and the given economic and financial situation of the state.

B. Traditional Units

Germany, the United States at the federal level, and France may be considered “rather rooted in tradition.” Their governmental accounting systems are:

• based on the net monetary debt concept or a near-monetary-debt approach; • primarily, or exclusively, Parliament-oriented, and relatively user-unfriendly as

regards explanatory notes to the annual reports and the availability of the revenue and expenditure accounts to the general public.

In respect to the politico-administrative background conditions, almost the only thing

these three units have in common is their large population. The federal government in the United States faces comparatively favorable

institutional factors for the further development of its accounting system:

• there is a high level of political competition between the executive branch and the Congress;

• public sector accountancy staff are usually familiar with private-sector concepts and practice; and

• the growth of public debt points to a problematic financial situation and the need for demonstrating sound financial management.

The fact that there has, nevertheless, not yet been any fundamental change of the

government’s accounting practice may presumably be attributed to the existence of divergent values and attitudes as well as to the aggravating presence of implementation barriers:

• There exist different conceptions of the ideal situation in terms of supply of information between the legislature and the executive branch. The legislature is unable or unwilling so far to assert its more far-reaching conception.

124

• Pressure from the public to improve the information situation (e.g., as manifested in particular in the views expressed by professional organizations) is evidently not strong enough.

• The large number of diverse accounting practices in the huge federal government organization (i.e., degree of disharmonization) impedes the introduction of a more developed and uniform accounting system.

It is hypothesized that the relative inflexibility of the accounting system at the federal

level in the United States is primarily due to values, attitudes, and implementation barriers, rather than structural background conditions. This is confirmed by the fact that numerous proposals for improving the federal government’s accounting system have been suggested and as many meetings on this subject have been held. Thus, a lack of proposals and initiatives cannot be the reason for the present state of the art.

The situation has to be judged differently in the case of Germany and France: the combination of weak structural factors that promote change and the presence of factors inhibiting implementation create a context which is unfavorable for the further development of their governmental accounting systems. These two countries are characterized by the following:

• A low degree of political competition (No elements of direct democracy. An

absence of competition between Parliament and the executive branch. The French constitution strongly emphasizes the role of the President. In Germany, the government and Parliamentary majority are closely identified with one party).

• Professional organizations having little influence on the governmental accounting system (with the sole exception in France via the Conseil National de la Comptabilite).

• Public-sector accounting staff having no or only limited experience of the concepts and practices of private sector accounting.

• No problematic financial situation. • No capital market incentives. • Relatively comprehensive and detailed legal prescriptions of governmental

accounting systems (which in Germany are largely harmonized due to the Budgetary Principles Act).

• A lack of promotion by accounting professionals.

C. Special Cases

The United Kingdom and the EC occupy a rather special position—they cannot be assigned to either the “rather progressive” or “rather rooted in tradition” categories without some qualification.

125

In the United Kingdom, while it is true that its governmental accounting system is inclined to be “rooted in tradition,” in the 1980s, however, great efforts were clearly made to develop and improve the management accounting system through the Financial Management Initiative. Similar to Denmark and Sweden, though to a lesser degree, the general economic situation and the situation of the government finance in the United Kingdom coincided with the appearance of a catalyst (in the person of Margaret Thatcher) to precipitate an initiative in favor of more effective, efficient, and economic administration and the creation of the necessary instruments to achieve that end. The fact that this initiative did not extend to the external system, unlike what happened in the Scandinavian countries, may be attributed to the following causes:

• The problem is purely one of time. The reform of the management system had

priority. It may however be assumed that if the initiative had been spread out over a longer period of time a start would also have been made on the reform of the external accounting system. There is some evidence to support this interpretation.

• The restructuring of the external governmental accounting system rates lower in the hierarchy of priorities in the United Kingdom than in the Scandinavian countries due to a lower “openness” and “citizen-orientation” of British politics and government.

• The strength of the institutional factors promoting change in the United Kingdom is not great.

The EC, as a supranational entity, launched some early initiatives towards the end of

the 1980s with a view to creating a management accounting system for the commission and made its own external accounting accessible to the public. More comprehensive conceptual changes did not, however, accompany these initiatives. The cause of the changes that took place was probably a temporarily critical financial situation in the EC in the mid 1980s and sharper criticism from the member states about the sound financial management aspect of the expenditure of Community resources by EC agencies. The changes that took place in the accounting system and in the accounts created the instrumental preconditions for improving the administrative efficiency and for demonstrating sound financial management. Fundamentally, however, the politico-administrative background conditions for the further development of the external accounting system are rather unfavorable:

• There is certainly political competition between Parliament on the one hand and

the Council and/or the Commission on the other. But the European Parliament is of course even less able than the French one to influence the supply of information from the executive branch.

• There is no significant influence by professional organizations and even the element of state debt or capital market incentives as factors precipitating change is absent.

126

• If those factors that are neutral as regards implementation are compared with those that inhibit it, the latter predominate, as reflected in the inflexibility of the legal system and the professional background of accountancy staff.

EDITORS’ NOTE This paper is based, in part, upon the “Comparative Government Accounting Study” recently completed by Professor Klaus G. Lüder and his associates at the Postgraduate School of Administrative Sciences in Speyer, Germany. The Study’s interim summary report is available in English, while the country studies cited in the References are in German only. Readers who wish to obtain copies of these publications may write to Professor Klaus G. Lüder , c/o James L. Chan at the University of Illinois at Chicago. Readers interested in “comparative international governmental accounting research” (CIGAR) and the biennial CIGAR conference series may similarly communicate with James Chan, who will put them in touch with the appropriate parties.

REFERENCES Arthur Andersen & Co., Sound Financial Reporting in the U.S. Government [Arthur Andersen & Co.,

1986]. Baber, W.R., “Toward Understanding the Role of Auditing in the Public Sector,” Journal of Accounting

and Economics 5 [1983], pp. 213-227. Baber, W.R., and P.K. Sen, “The Role of Generally Accepted Reporting Methods in The Public Sector:

An Empirical Test,” Journal of Accounting and Public Policy 3 [Summer 1984], pp. 91-106. Buchanan, J.M., Public Finance in A Democratic Process [University of North Carolina Press, 1967]. Carpenter, V.L., and E. Feroz, “Fiscal Stress and State Government’s Financial Reporting Practice: A

Cross Case Analysis,” paper presented to the Annual Conference of the American Accounting Association in Toronto, August 9-11,1990.

Chan, J.L., “The Economics and Politics of Governmental Financial Information: Issues for Research,” paper presented to the second CIGAR Conference in Speyer, April 3-4,1989.

Chan, J. L., and M.A. Rubin, “The Role of Information in A Democracy and in Government Operations,” Research in Governmental and Nonprofit Accounting 3, Part B [1987], pp. 3-27.

Downs, A., An Economic Theory of Democracy [Harper and Row, 1957]. Downs, A., “Why the Government’s Budget Is Too Small in a Democracy,” World Politics [July 1960],

pp. 541-563. Evans J.H., III and J.M. Patton, “Signaling and Monitoring in Public-sector Accounting,” Journal of

Accounting Research 25 [Supplement 1987], pp. 130-158. Governmental Accounting Standards Board, “Measurement Focus and Basis of Accounting—

Governmental Fund Operating Statements,” Proposed Statement of Governmental Accounting Concepts, [rev. ed.], Governmental Accounting Standards Series, No. 062-A [1989].

Ingram, R.W., “The Importance of State Accounting Practices for Credit Decisions,” Journal of Accounting and Public Policy 2 [Spring 1983], pp. 5-19.

127

________ “Economic Incentives and the Choice of State Government Accounting Practice,” Journal of Accounting Research [1984], pp. 26-134.

Ingram, R.W., and E.A. Wilson, “Governmental Capital Market Research in Accounting: A Review,” Research in Governmental and Nonprofit Accounting 3, Part B [1987], pp. 111-126.

Khandwalla, P. N., Design of Organizations [Harcourt, Brace, Jovanovich, 1977]. Kieser, A., and H. Kubicek, Organisation, 2nd ed. [Berlin: De Gruyter, 1983]. Lüder , K.G., “Comparative Government Accounting Study: Interim Summary Report,” rev. ed. [Speyer:

Speyerer Forschungsberichte, No. 76,1989]. Lüder , K.G., et al., “Vergleichende Analyse offentlicher Rechnungs systeme—Landerberichte.” [Speyer:

Speyerer Forschungsberichte, No. 73,1989]: Bd. 1: U.S.A. Bd. 2: Kanada Bd. 3: Frankreich und Grob Britannien Bd. 4: Danemark Bd. 5: Schweden Bd. 6: Kommission der Europaischen Gemeinschaften

Niskanen, W., Bureaucracy and Representative Government [Aldine-Atherton, 1971]. Simon, H.A., Entscheidungsverhalten in Organisationen [Landsberg am Lech: Verlag Moderne Industrie,

1981], German translation of Administrative Behavior, 3rd ed. U.S. General Accounting Office, Proposed Framework for Establishing Federal Government Accounting

Standards, Exposure Draft [U.S. General Accounting Office, Washington, DC: May 1989]. Van Daniker, R.P., “Governmental Accounting in the U.S.—State Orientation,” paper presented to the

second CIGAR Conference in Speyer, April 3-4, 1989. Van Daniker, R.P., et al., State Comptrollers—Technical Activities and Functions [National Association

of State Auditors, Comptrollers and Treasurers, 1986]. Van Daniker, R.P., and T. Criswell, State Comptrollers—Technical Activities and Functions [National

Association of State Auditors, Comptrollers and Treasurers, 1989]. Zimmerman, J.L., “The Municipal Accounting Maze: An Analysis of Political Incentives,” Journal of

Accounting Research 15 [Supplement 1977], pp. 107-144.