luck bias and skill performance of individual mutual funds*

TRANSCRIPT

1

Luck Bias and Skill Performance of Individual Mutual Funds*

MARTIN ROHLEDER and MARCO WILKENS

University of Augsburg

Abstract. This is the first study measuring luck bias and skill performance of individual

funds. We show that luck and bad luck balance within the cross-section, such that market

level performance is virtually unbiased. Many individual funds, however, suffer greatly from

luck bias resulting in significant rank changes. In performance persistence tests, we show that

skill is persistent and that our luck-bias-corrected skill alpha discriminates more effectively

between future outperformers and underperformers than standard alpha does. Further, skill-

High-minus-Low portfolios consistently outperform standard-High-minus-Low portfolios by up

to 0.9 % p. a. Thereby we deliver economically valuable contributions to the discussion on

luck versus skill.

JEL Classification: G11, G12

Keywords: Mutual fund performance, luck bias, reverse survivorship bias, survivorship bias,

luck versus skill, performance persistence.

______________

* We are grateful for helpful comments and suggestions by Dominik Schulte, Ludwig von la Hausse, … We are

responsible for any remaining errors. Corresponding author: [email protected].

2

1. Introduction

A recent strand of research struggles with the question if there is significant investment skill

among mutual fund managers, which part of the measured performance is effectively based on

managers' skill and which part is due to mere luck. Unfortunately, there is no easy answer to

this question because the level of skill of individual funds is unobservable. Hence, the related

literature is majorly depending on bootstrap or simulation approaches and on assumptions

about the distribution of skill within the cross-section of mutual funds. Among this research

there is consensus that, due to the zero-sum game nature of the capital market, the average

skill level is zero which in turn leads to zero market level alpha before costs (e.g., Kosowski et

al, 2006; Fama and French, 2010). However, none of the existing studies provide reliable

estimates of the magnitude of skill performance or of the bias in mutual fund performance

induced by luck, especially not on an individual fund level.

Closing this gap, this is the first study estimating luck bias and skill performance of

individual funds in the U.S. domestic equity fund market. Specifically, we develop different

sets of fund-specific dummy variables to disentangle luck and skill in the estimated residuals

of standard performance measures. The first set of dummy variables is based directly on the

recently established concept of reverse survivorship bias by Linnainamaa (2013) which covers

a particular part of luck bias: bad luck resulting in disappearance. The dummies therefore

represent the last two years of a fund's existence due to the fact that there exists a

correlation between model residuals and disappearance making disappearance itself an

omitted variable disguising skill. In addition, this design also covers any actions by the fund

family occurring immediately before a fund's disappearance that disguise the investment

ability of the manager. In this context, anecdotal evidence suggests that fund families shift

bad assets into or strip good assets from disappearing funds, respectively, to enhance the

performance of their remaining funds. In the following, we refer to such actions as \Monkey

Business".

The second set of dummy variables is based on outlier identification methods analogue

to Chan and Lakonishok (1992) and Martin and Simin (2003) who both estimate robust

CAPM betas in the U.S. stock market. This way, these dummies cover lucky and unlucky

events experienced by a fund independent of survival and disappearance which has not been

considered before in the existing research on luck and skill in mutual fund performance.

Overall, both sets of dummies are based on readily available information such that our

methodology is easy to implement by academics and by investors alike. Thereby, we deliver

valuable contributions to the discussion on luck versus skill in general and to the concept of

reverse survivorship bias in particular.

3

Our results indicate that about 10 % of non-survivors indeed disappear due to bad

luck biasing market level performance downwards by up to 0.29 % p. a. However, this is a

distinctly lower estimate for reverse survivorship bias than reported by Linnainmaa (2013).

Furthermore, correcting realized performance for luck and bad luck independent of

disappearance uncovers a significant upward bias in realized performance by up to

0.25 % p. a. This overestimation of market level performance emerges because there is no

mechanism punishing good luck in a similar fashion as disappearance punishes bad luck.

Seemingly, funds on average experience more lucky events than unlucky events while they

survive. Using both corrections combined in a full luck-bias-correction model, the effects

eventually offset each other. Our final market level estimates of luck bias are therefore very

close to zero and economically irrelevant which \reverses" the reverse survivorship bias

established by Linnainmaa (2013).

On an individual fund level, however, our analysis shows that performance can be

severely biased and that fund rankings change considerably after correcting for individual

luck bias. This is documented by rank correlations below 70 % between uncorrected alphas

and our skill alphas. Moreover, our analysis of the distribution of alpha in the cross-section

shows that estimated alpha underestimates the width of the distribution as skill alpha has

fatter tails. Consequentially, there are more skilled but also more truly unskilled funds in the

market than suggested by standard measures. Our results regarding the distributions of

estimated alphas and skill alphas thereby closely correspond to the existing research on luck

versus skill. Our results rationalize and confirm most of their findings, thereby further

contributing to this strand of literature.

To analyze whether skill is persistent and to confirm that our results are not mere

statistical artifacts, we test for the predictive power of our luck-bias-corrected skill

performance measures using performance persistence analysis. The results on these tests show

that rank correlations between ranking and holding periods are consistently higher when

using skill alpha in the ranking period. Furthermore, we show that investing in a skill alpha

based High-minus-Low portfolio yields a premium that is up to 0.9 % p.a. higher than that of

a standard alpha based High-minus-Low portfolio. These results are robust for different

combinations of ranking and holding period lengths. This proves that our measures of skill

alpha discriminate more effectively between future outperformers and future underperformers.

Overall, our study thereby adds significant economic value for academics and for investors.

The rest of the paper is organized as follows. Section 2 motivates our study by

providing the theoretical background, summarizing the related literature and describing in

more detail the contribution of this paper. Section 3 describes our approach to correcting

individual estimated performance for luck bias and formulates five distinct research

4

hypotheses. Section 4 introduces the dataset and describes the methodology used in our

empirical analysis. Section 5 reports results as well as interpretations thereof. Section 6

concludes.

2. Motivation and Literature Overview

Research in the field of mutual fund performance has been determined to measure investment

ability for purposes of manager gratuity and to find sustainable superior performance for

future investment. In the process, many biases in performance measurement have been

identified and eliminated by the use of less biased data and more sophisticated methods.

However, performance measurement still struggles with the question which part of the

measured performance is effectively based on the managers' skill and which part is only due

to luck. To motivate our own study on luck versus skill, in this section we first give a

theoretical background and definition of the luck bias in measured performance. Then we

summarize the existing literature on the topic of luck and skill as well as on the related topic

of reverse survivorship bias. Last, we describe to what extent our approach deviates from that

literature and how we contribute to the research on luck and skill in general and on reverse

survivorship bias in particular.

Theoretically, each individual fund j has a specific unknown level of skill represented

by its skill alpha ®j

skill which is assumed to be constant over time. In addition, fund j

experiences in each period t a specific and also unknown true shock "jt with limTj → ∞

E("jt) = 0.

Abnormal return in each period rjt

a can thus formally be represented by:

rjt

a = ®j

skill + "jt. (1)

In limited time, however, a fund's performance might be biased by an overweight of positive

shocks, interpreted as luck, or an overweight of negative shocks, interpreted as bad luck, such

that E("jt) ≠ 0. With ®j

skill and "jt unknown in limited time, the best estimator for skill alpha

is \realized" or \estimated" alpha ®j which is calculated from the returns observed up to the

actual date. Realized performance is therefore not necessarily constant over time and certainly

subject to investors' learning (Linnainmaa, 2013). Fitting a regression like the CAPM to return

observations yields estimated shocks "jt with E("jt) = 0 by construction. Abnormal return rjt

a can

thus alternatively be represented as in Equation 2 where ERjt is the return of fund j in excess of

the risk free rate and ERMt is the market excess return.

rjt

a = ERjt { ¯j ERMt = ®j + "jt (2)

5

Combining both representations in Equation 3 reveals that realized alpha equals skill alpha in

all cases where E("jt) = 0.

®j = t = 1

Tj (rjt

a { "jt)

Tj =

t = 1Tj (®j + "jt)

Tj = ®j

skill + E("jt)

(3)

This is per se true in unlimited time or if positive and negative true shocks "jt coincidentally

balance over limited time. In most cases, however, realized performance will be biased by

E("jt) ≠ 0. Ultimately, luck bias or luck alpha ®j

luck can be represented as:

®j

luck = ®j

skill { ®j = {E("jt). (4)

In practical research, on the other hand, the identification of luck and skill is a great

challenge. One popular approach is analyzing performance persistence to discover repeat

outperformers among mutual funds (e.g. Grinblatt and Titman, 1992; Hendricks et al., 1993;

Brown and Goetzmann, 1995; Elton et al., 1996; Carhart, 1997). In summary, evidence

against performance persistence outweighs. Specifically, most studies find outperformance to

persist at best on the short run. Underperformance, on the other hand, seems to be persistent

over longer horizons. This is consistent with a majority of fund managers possessing no skill,

and only very few managers showing levels of skill that allow them to repeatedly outperform.

However, there is also criticism regarding the adequacy of performance persistence analyses.

The methodology is based on short-term performance measures and results may largely be

based on noise (Fama and French, 2010). Furthermore, the possibility that luck may also

persist (Kosowski et al., 2006) is not recognized but could (partly) explain short-term

persistence in mutual fund performance.

Therefore, several recent studies follow another approach which is based on

assumptions about the nature of true alpha. In a pioneering work for the U.S. equity fund

market, Kosowski et al. (2006) use a bootstrap methodology to identify those alphas created

by skill in the cross-section of realized alphas. Assuming true alpha to be zero, they generate

a distribution of alphas that is based exclusively on sampling variation and compare it to the

distribution of realized alphas. The authors find far more positive and significant alphas than

could be expected from luck alone and conclude that there exists a minority of fund managers

with significant investment skill. Moreover, the authors use the bootstrap to uncover which of

the positive realized alphas are due to luck and which are due to skill. They do not, however,

provide estimates for the magnitude of skill performance. Also, the bootstrap allows inferences

only on alphas in the tails of the cross-section, but not at its center.

Using the Kosowski et al. (2006) methodology, Cuthbertson et al. (2008) report

basically identical results for the UK equity fund market. Layfield and Stevenson (2011)

6

apply the same method to U.S. REITs finding only one manager with significant skill among

a vast majority of unskilled ones. Barras et al. (2010) additionally apply the false discovery

rate by Storey (2002) to estimate fractions of unskilled funds, zero-alpha funds, and skilled

funds in the U.S. equity fund market. They find that, over a long horizon, the majority of

funds (75.4 %) show zero alpha while the proportion of skilled funds is insignificant (0.6 %).

A considerable fraction of managers (24 %) have inferior skill. Sastry (2011) uses a

hierarchical Bayesian model and a mixture-of-normals alpha-distribution to distinguish skill

from luck in the U.S. fund market. He finds that the resulting estimates for alpha exhibit

strong predictability across the entire population of funds, not only in the tails. Also, the

distribution of alpha is fat tailed and the standard deviation of true alpha is underestimated

by the realized performance. Finally, Fama and French (2010) use a differently designed

bootstrap methodology to distinguish between luck and skill in the cross-section of U.S.

equity funds. They show that only very few managers possess enough skill to enhance

expected returns. However, all of these papers also do not provide direct estimates of luck

bias or skill performance on an individual fund level.

Based on the Fama and French (2010) methodology, Linnainmaa (2013) introduces

the concept of reverse survivorship bias which covers a specific part of luck bias: bad luck

resulting in disappearance. Following the argumentation of the paper, reverse survivorship

bias arises if otherwise skilled funds disappear due to bad luck and thus their estimated

alphas do not get a chance to recover towards their true alphas. Consequentially, market level

management skill is understated by the use of survivor-bias-free data. More specifically,

Linnainmaa defines reverse survivorship bias as the difference between estimated alpha and

true alpha. His approach to measuring reverse survivorship bias in the mean is based on a

comparison of two market level aggregations: fund-by-fund (FbF) and fund-of-funds (FoF).

FbF estimates individual alphas over time and averages them cross-sectionally. FoF

calculates monthly average returns and estimates alpha from the resulting time series.

Linnainmaa states that \both methods should yield consistent estimates of the average

alpha", such that any difference is due to the time series of non-survivors being \sometimes

cut short due to more negative than positive errors". In conclusion, the difference between

FoF and FbF performance equals reverse survivorship bias. Linnainmaa reports that the

cross-section of U.S. equity funds is significantly biased by approximately 0.49 % to 0.62 %

p. a. together with a considerable change in the shape of the alpha-distribution. Compared to

recent estimates of annualized survivorship bias of up to 1.5 % p. a. (e.g., Carhart, 2002;

Rohleder et al., 2011), this is also economically relevant. Linnainmaa, too, does not present

measures of reverse survivorship bias and skill performance of individual funds.

We deliver a valuable contribution to this strand of research by being the first to

disentangle luck and skill on an individual fund level to obtain estimates of luck bias and skill

7

performance for every fund. More specifically, our approach corrects performance measures

using information derived from the estimated shocks "jt about the true shocks "jt. Using

accordingly designed fund-specific dummy variables we are able to show that there is

significant luck bias on an individual fund level. Moreover, we find empirical evidence for

Monkey Business by fund families during the time approaching disappearance. As a result,

our estimated skill alpha ®j

skill is a superior measure of the true skill alpha ®j

skill compared to

standard alpha. To show the economic value of our contribution we extensively test for

performance persistence showing that our skill alpha is a better predictor of future performance

than standard alpha. Moreover, our approach is based on readily available data and easy to

implement such that it is of interest for academics and for investors. Furthermore, our

methodology allows measuring each fund's level of skill on a continuous scale between {∞ and

+∞ which is a significant advancement over recent studies using binomial (skill, no skill) or

trinomial scales (positive skill, zero-skill, negative skill), respectively. A detailed description of

this methodology is given in Chapter 3.

Using our findings on the skill performance of individual funds, we also contribute to

the topic of reverse survivorship bias by delivering a realistic estimate of the magnitude of

reverse survivorship bias. Moreover, we correct for erroneous calculations in Linnainmaa

(2013) as, in contrast to the author's assumption, FoF and FbF market level aggregation

yield consistent estimates only if all funds have the same number of observations and cover

the same time period. By definition, survivor-bias-free data as used in both his and our

studies satisfy neither condition. The difference between FoF alpha and FbF alpha then arises

from the relative overweight of short-living funds in the FbF approach. This means that

unlucky disappearances are present in both FbF and FoF such that both suffer from the bias.

Even more importantly, the time series of many funds are short due to reasons besides bad

luck. In this context Rohleder et al. (2011) show that non-survivors consistently

underperform survivors during their last four years. Thus, the difference is majorly due to

inferior skill and therefore does not represent reverse survivorship bias.

Finally, we also contribute to market level performance measurement in general by

using a new \meta-bootstrap" that allows consistent significance levels for FoF and FbF

alphas. Specifically, the method corrects for the fact that FoF generally overestimates

diversification between the funds and FbF underestimates inter-fund-dependencies. More

importantly, the meta-bootstrap thereby allows realistic significance levels for estimates of

market level alpha biases like survivorship bias, reverse survivorship bias and luck bias. A

detailed description of the meta-bootstrap is given in Chapter 4.

8

3. Measuring Skill Performance and Research Hypotheses

In this section we first define \skill" and \luck". We then develop and describe in detail our

approach to correcting the estimated performance of individual funds for luck bias. This part

further divides into two separate corrections using different sources of information and

borrowing from different strands of literature. In the process of describing our methodology,

we formulate five distinct research hypotheses for our empirical analysis.

We define skill and luck as follows: On the one hand, a manager's skill creates

sustainable performance by using long-term strategies and developing repeatable investment

ideas. On the other hand, the dictionary definition of luck reads \events that are beyond

control and seem subject to chance".1 In the mutual fund context, such events can be

established by exceptionally high or exceptionally low returns that occur rarely, do not match

the general long-term strategy or character of the fund, cannot be predicted and therefore

cannot be replicated on purpose. In addition, we also consider actions or influences disguising

the true skill of the manager as (bad) luck. Such influences are, for example, fund families

doing \Monkey Business" with designated graveyard funds. Anecdotal evidence suggests that

they might engage in asset stripping, shift bad assets from other family funds into the

disappearing fund or, more generally, deviate from the stated long-term investment objective

because \no one really cares anymore".

Regarding individual fund performance, our baseline performance measure is the

standard Carhart (1997) 4-factor model as it is the widest spread model to date and risk

factors are readily available over long horizons to everyone, including investors, from Kenneth

French's online data library. In the following, we refer to the uncorrected Carhart alpha as

the realized alpha ®j of the fund. It is represented by

ERjt = ®j + ¯1j ERMt + ¯2j SMBt + ¯3j HMLt + ¯4j MOMt + "jt (5)

where SMBt is the return on a zero-investment portfolio capturing the size effect, HMLt is

the return on a zero-investment portfolio capturing the value effect (Fama and French, 1993),

and MOMt is the return on a zero-investment portfolio capturing the momentum effect (e.g.,

Jegadeesh and Titman, 1993).

Our approach to correcting realized performance for luck bias is based on adding

dummy variables to the baseline model. In general, our luck-correction-model can thus be

represented by Equation 6a where Dj is the matrix of fund-specific dummy variables and @j is

the corresponding vector of coefficients.

1 http://www.collinsdictionary.com, 13.09.2012.

9

ERjt = ®j

skill + ¯1j ERMt + ¯2j SMBt + ¯3j HMLt + ¯4j MOMt + @j Dj + "jt (6a)

The fund's abnormal return can therefore be represented as in Equation 6b. Consequentially,

after the luck bias correction, E(®j

luck + "jt) is a more realistic estimator for E("jt) ≠ 0 such

that, ultimately, ®j

skill is a better estimator for the true skill performance ®j

skill.

rjt

a = ®j

skill + @j Dj + "jt = ®j

skill + ®j

luck + "jt (6b)

Our first specific luck-correction is based on the concept of reverse survivorship bias.

According to Linnainmaa (2013) it is caused by \the correlation between the performance-

evaluation regression's error term and survival" which arises \due to more negative than

positive errors". Disappearance can thus be regarded as an omitted variable. Therefore,

estimated performance is systematically biased by a temporary downward level shift, a

negative luck alpha, caused by bad luck during the time approaching disappearance. To

correct for this temporary level shift, we construct fund-specific dummy variables that equal 1

when the fund approaches disappearance and 0 while it survives. This methodology closely

relates to Grundy and Martin (2001) who estimate stock alphas for different timeframes

within a stock's time series using chronologically disjoint dummy variables instead of a global

constant. In contrast to Grundy and Martin, however, we do use a global constant capturing

the fund-specific ®j

skill plus an additional timeframe-specific constant ®j

luck captured by the

dummies and representing the correlation between the fund's error terms and disappearance,

hence the reverse survivorship bias.

To constitute the timeframe \approaching disappearance" we refer to results from

previous studies analyzing the determinants of fund disappearance. For U.S. equity funds,

Rohleder et al. (2011) show that non-survivors significantly underperform in the last four

years before they disappear, implying that underperformance of non-survivors is systematic in

general. However, the highest underperformance on average occurs in the second to last year

(Tj{2yr). Moreover, the probit analysis in Rohleder et al. (2011) shows, that the impact of

returns on disappearance is economically significant during the last two years. These results

are consistent with comparable studies by Brown and Goetzmann (1995) and Zhao (2005) as

well as with results for U.K. equity funds by Blake and Timmermann (1998). We interpret

these results such that it takes approximately one year (Tj{1yr) to execute the dissolving of

the fund after the decision thereto is made based on severe underperformance in year Tj{2yr.

Consequentially, we use two dummies: Decision which is 1 in each month of year Tj{2yr, and

Execution which is 1 in each month of year Tj{1yr. Negative and significant dummy-deltas

thus imply that underperformance is (at least partly) due to bad luck or Monkey Business

while positive or insignificant dummy-deltas suggest that underperformance is due to inferior

10

skill. In the following, we refer to the first luck-correction-model represented by Equation 7 as

\D&E".

ERjt = ®j

skill + ¯1j ERMt + ¯2j SMBt + ¯3j HMLt + ¯4j MOMt

+ @1j Decisionjt + @2j Executionjt + "jt

(7)

Research Hypothesis 1: When exclusively using the D&E correction, we will find

more individual funds with negative than positive deltas as well as negative market

level deltas. As a consequence, the market level skill performance of U.S. equity fund

managers will be higher than their realized performance, implying a positive luck bias {

or in this case: reverse survivorship bias.

However, thus far the dummies only capture luck in the errors of disappeared funds because

there are no timeframes approaching disappearance for survivors. This is unsatisfying because

the skill performance of non-survivors does not yield the possibility of identifying superior

future investments and is therefore only of academic interest. To add economic value for

investors, our second correction considers luck independent of disappearance. We therefore

follow approaches used by Chan and Lakonishok (1992) as well as Martin and Simin (2003)

to estimating robust CAPM-betas in the U.S. stock market by identifying outliers in stock

returns. Closely matching the dictionary definition of luck, outliers are defined as

observations that are numerically distant from the rest of the data (Barnett and Lewis, 1994).

They occur very rarely, seemingly by chance and are thus not systematic. Moreover, following

Cook (1977) an outlier is an observation which is highly influential to the outcome of a linear

regression. Consequentially, outliers disguise the true sustainable long-term character of the

data, in our case the investment skill of the fund.

In contrast to Martin and Simin (2003), however, we apply outlier identification only

to the baseline model errors instead of excess returns in order to identify the influences that

are in addition to the long-term character of the fund which is represented by its model

returns. Moreover, we do not reject (remove data points) or winsorize identified outliers (alter

data by cutting the errors down to a certain value). Instead, we use the mean shifting outlier

model-approach from Cook and Weisberg (1982) which involves the creation of dummies,

thereby maintaining the information about luck included in the outliers. More specifically, we

apply Cook's Distance (Cook, 1977) to the error terms of the baseline model. Cook's Distance

measures the effect of eliminating each observation separately from the data to identify those

with the highest influence, or leverage, on the regression outcome. With the outliers identified

by this method, we construct two new dummy variables. The first dummy equals 1 in all

cases of positive outliers and is therefore titled Luck. The second dummy equals 1 in all case

11

of negative outliers and is therefore titled BadLuck. By construction, Luck delta is always

positive and BadLuck delta is always negative. Thus, if Luck delta is higher than the

absolute of BadLuck delta, this can be interpreted as the respective fund experiencing more

lucky true shocks than unlucky true shocks during the sample period, and vice versa. In the

following, we refer to our second luck-correction-model represented in Equation 8 as \L&B".

ERjt = ®j

skill + ¯1j ERMt + ¯2j SMBt + ¯3j HMLt + ¯4j MOMt

+ @3j Luckjt + @4j BadLuckjt + "jt. (8)

Our expectations regarding L&B correction results are also based on Linnainmaa (2013) but

this time we argue against it. Because lucky survival of otherwise inferior funds is not

punished in a similar fashion as bad luck is sometimes punished by disappearance, there

should be slightly more lucky true shocks in the errors of survivors. Consequentially, the

performance of survivors should be systematically overstated by luck bias.

Research Hypothesis 2: When exclusively using the L&B correction, we will find

more lucky events per fund than unlucky events. On market level, there will be a higher

Luck delta. As a result, market level skill performance will be lower than realized

performance. Ultimately, we will find a negative luck bias contradicting Linnainmaa's

reverse survivorship bias.

In our final correction model, we use both pairs of dummies to consider both sources of

information: correlations between error terms and disappearance as well as outliers over the

whole survival period. The dummies are not mutually exclusive, meaning that L&B outliers

can also occur during the D&E periods. This could decrease the significance of the deltas in

these particular cases. However, the model should be very effective in using the available

information to disentangle the performance created by a manager's skill from luck. In the

following, we refer to the luck-correction-model represented in Equation 9 as the \full model".

ERjt = ®j

skill + ¯1j ERMt + ¯2j SMBt + ¯3j HMLt + ¯4j MOMt

+ @1j Decisionjt + @2j Executionjt + @3j Luckjt + @4j BadLuckjt + "jt. (9)

Research Hypothesis 3: When using the full model, we will see that both

corrections (partly) offset each other such that the resulting market level performance is

between the results of D&E and L&B. We will further find the resulting luck bias to be

very small and economically irrelevant.

Thus far, the stated research hypotheses only refer to market level skill performance and luck

bias while the great strength of our paper compared to the existing literature is the possibility

of estimating skill performance on individual fund level. Unfortunately, it is unpractical to

discuss individual performance of nearly 4,000 funds in one paper. We therefore compare fund

12

rankings based on different performance estimates to analyze if individual funds suffer

significantly from luck bias. Moreover, the related literature regularly analyzes distributions of

different performance estimates in the cross-section of funds to gain ideas on the proportion of

skilled funds compared to unskilled funds. We also conduct such an analysis to compare our

findings to those in the related literature.

Research Hypothesis 4: There is significant impact of luck bias on the performance

estimates of individual funds. Specifically, we will find significant changes in fund

rankings and in the shape of the alpha distribution when correcting estimated alpha for

luck bias.

In summary, we expect our corrected measure of skill performance to capture the long-term

sustainable character of funds better than standard performance measures. If this is true and

not just a statistical artifact, skill performance should be a better predictor of future

performance than realized performance. Moreover, we expect significant rank changes when

using our correction models. Therefore, we analyze performance persistence based on skill

performance and compare it to measures of performance persistence based on standard

performance to add economic value to our findings.

Research Hypothesis 5: We will find a higher degree of performance persistence

when using skill alpha to rank the funds during the ranking period. Specifically, there

will be higher rank correlations between ranking and holding periods and,

consequentially, higher returns to investment strategies based on skill performance.

4. Data and Methodology

In Part A. of this section, we describe our dataset, which data sources we use, our data

selection procedure, and how we treat certain data problems. We also present summary

statistics on our final dataset. In Part B. we describe the methodology used in our empirical

analysis. The part divides into descriptions of our approaches to analyzing Monkey Business,

of measuring market level performance including the meta-bootstrap, and of our approach to

analyzing performance persistence.

A. DATA

We use market excess returns, the Fama and French (1993) equity risk factors, the

momentum factor, and returns on the one-month U.S. Treasury bill from the Kenneth R.

French data library. We obtain mutual fund data from the CRSP survivor-bias-free mutual

fund database. Our dataset covers the time period from 01/1993 through 03/2013. We limit

13

our dataset to actively managed funds consistently classified as U.S. non-sector domestic

equity funds by CRSP objective codes. We eliminate funds with missing return values as well

as those without any size or expense ratio data. For funds with fragmentary TNA, we apply a

missing values approach based on Rohleder et al. (2011) which is further described in the

Appendix. Different share classes of a fund are combined on portfolio level using CRSP

portfolio numbers and manually matched fund names.2 As we estimate performance measures

for individual funds and due to our special methodology it is of crucial importance that our

regression estimates are reasonably reliable. Therefore, we exclude all funds with less than 48

months of returns. This introduces some survivorship bias to the sample. Our results

therefore underestimate survivorship bias to some extent. Our final sample contains a total of

3,802 funds of which 2,213 are end-of-sample survivors and the remaining 1,589 funds are

non-survivors.

[Insert Table I and Figure 1 here.]

Table I shows summary statistics for the survivor-bias-free dataset with 484,492 monthly

observations and for the survivor-biased sub-sample with 314,189 monthly observations. The

industry size at the end of our sample period equals almost 3.4 trillion USD. Figure 1 shows

the development of the survivor-bias-free sample in terms of industry size and the number of

funds over the sample period. Survivors are generally larger than non-survivors. Within the

groups, however, the median size is distinctly lower than the mean such that the industry

consists of a large number of small and medium funds and a small number of exceptionally

large funds. Regarding returns, survivors show higher returns in general, which is not very

surprising (e.g., Carhart et al., 2002). Also, value-weighted returns are lower than equal-

weighted returns suggesting that smaller funds have lower returns on average (e.g., Rohleder

et al., 2011). Expense ratios are slightly lower for survivors and with value-weighting. The

equal-weighted fund age in our dataset is just above 100 months. Value-weighted, however,

the average fund age is around 200 months which suggests that large funds also survive over

longer periods than smaller funds (e.g., Rohleder et al., 2011).

B. METHODOLOGY

B.1. Monkey Business

In the following, we describe our method of testing our idea of fund families doing monkey

business with designated graveyard funds. Specifically, we test for all 1,589 non-survivors in

2 Share class returns and expense ratios are value-weighted within the fund. Fund size is the aggregate of all

share classes. The investment objective is determined by the largest share class. Fund age is determined by the

oldest share class.

14

our sample whether the Carhart factor betas differ significantly between the periods

approaching disappearance compared to their baseline-betas. Therefore, we extend Equation 7

by interaction terms between the Carhart factors and the D&E dummies. A similar approach

is used in Grundy and Martin (2001) to construct beta-momentum portfolios. Equation 10

can thus be used to estimate baseline betas ¯j

Base plus additional timeframe-specific

disappearance betas ¯j

Deci and ¯j

Exec. If the timeframe-specific betas are significant, this can be

interpreted as funds differing from their stated long-term objective when approaching

disappearance which is an indication of monkey business.

ERjt = ®j

+ @1j Decisionjt + @2j Executionjt

+ ¯1j

Base ERMt + ¯1j

Deci Decisionjt×ERMt + ¯1j

Exec Executionjt×ERMt

+ ¯2j

Base SMBt + ¯2j

Deci Decisionjt×SMBt + ¯2j

Exec Executionjt×SMBt

+ ¯3j

Base HMLt + ¯3j

Deci Decisionjt×HMLt + ¯3j

Exec Executionjt×HMLt

+ ¯4j

Base MOMt + ¯4j

Deci Decisionjt×MOMt + ¯4j

Exec Executionjt×MOMt + "jt

(10)

B.2. Market Level Performance

On the market level, we present results for fund-by-fund aggregation and fund-of-funds

aggregation because both have advantages and disadvantages with respect to different aspects

of our empirical analysis. On the one hand, statistics on dummy deltas are best documented

by FbF as these occur exclusively on the individual fund level. On the other hand, FoF is the

generally more accurate measure of market level performance as it weights funds correctly

regarding their time series lengths. Furthermore, with FoF it is possible to value-weight fund

returns by the correct beginning of month size without inducing forward-looking bias.

However, it is not a straight-forward exercise to calculate luck-corrected FoF measures

because the dummy variables are specific to individual funds which makes it impossible to

apply Equations 7, 8, and 9 directly to FoF time series. Therefore, we first estimate corrected

models for individual funds in order to generate corrected returns ER ^

jt

corr for each fund as

represented in Equation 11. These corrected returns can then be aggregated in the respective

FoF portfolios such that skill performance can be estimated using the standard Carhart

model.

ER ^

jt

corr = ERjt { @j Dj

= ®j

skill + ¯1j ERMt + ¯2j SMBt + ¯3j HMLt + ¯4j MOMt + "jt

(11)

15

B.3. Market Level Significance { Meta-Bootstrap

As stated in section 2, FbF and FoF yield consistent estimates of market level performance

under conditions of a balanced panel. However, even then both measures yield very different

estimates of the corresponding standard deviations; hence measures of statistical significance

are ambiguous and depend directly on the aggregation method. On the one hand, this

discrepancy obviously results from unjustified portfolio diversification leading to an

understatement of the FoF standard deviation. On the other hand, individual fund alphas are

counter-evidently treated as independent in the FbF aggregation, leading to an overstatement

of the standard deviation (e.g., Kosowski et al., 2006). These problems are even more

pronounced when comparing market level estimates to calculate alpha biases like survivorship

bias, reverse survivorship bias and luck bias.

Therefore, we use a meta-bootstrap that allows us to calculate test statistics for single

market level measures that are consistent for both aggregation methods. Moreover, it allows

us to calculate test statistics for the differences between single market level measures like,

e.g., survivorship bias, reverse survivorship bias, and luck bias. In contrast to a standard

bootstrap, where single observations (returns or residuals) are drawn with replacement from a

fund, the meta-bootstrap draws with replacement entire fund time series from the dataset,

thereby creating artificial cross-sections of funds. For FbF, this approach yields the same

result as drawing individual alphas from the cross-section. However, our approach

additionally enables us to calculate the corresponding FoF alpha for each randomly drawn

sample. Moreover, we sample real funds, thereby preserving time series characteristics like

autocorrelation as well as cross-correlations between funds. Moreover, the funds in our

bootstrap are weighted by their actual time series length and by their actual size in the case

of value-weighted results such that the problem of under- or oversampling can be avoided

(Fama and French, 2010). As a consequence, our drawings closely represent the structure of

the actual cross-section of funds. Ultimately, the meta-bootstrap yields connected samples

with paired FbF and FoF observations.

Specifically, the meta-bootstrap in our empirical analysis works as follows: In each of

100 replications, we randomly draw with replacement 3,802 out of the 3,802 funds of our

survivor-bias-free dataset or 2,213 out of the 2,213 funds of our survivor-biased dataset,

respectively. For these randomly drawn funds, we estimate realized and corrected individual

alphas as well as the equal-weighted and value-weighted FoF time series of monthly average

(corrected) returns. Then the aggregate FbF and FoF alphas are estimated as described

above.

16

To draw inferences on the significance of single market level measures, we calculate t-

statistics from mean meta-bootstrapped alpha (®{ b) divided by the corresponding standard

deviation of bootstrapped alphas (s®b).

tb = ®{ b

s®b (12)

T-statistics for estimates of survivorship bias are calculated based on the test for differences

between the means of two unconnected samples, hence as the difference between the means of

survivor-biased and survivor-bias-free alphas divided by the square root of added variances.

tb = ®{ SB

b – ®{ SBfree

b

s®SB

b 2 + s®SBfree

b 2 (13)

T-statistics for estimates of reverse survivorship bias and luck bias are calculated based on

the test for differences in the means of two connected samples, hence from mean and

standard deviation of the differences between paired skill and realized alphas. In either case,

two-sided p-values (pb) are calculated as the corresponding quantiles of Student's t-

distribution with 100 degrees of freedom.

tb = ®j

b,skill – ®j

b |||||

s(®j b,skill – ®j

b) (14)

B.4. Performance Persistence

As our measures of skill performance aim at identifying the sustainable character of a fund,

we are interested in the long-term persistence of our measures despite the general assumption

that performance persists at best on the short run (e.g., Brown and Goetzmann, 1995;

Carhart, 1997). To test this, we estimate Spearman's rho (½) and Kendall's tau (¿) rank

correlations between different ranking periods and the following holding periods. Then we

compare rank correlations based on skill alpha to rank correlations based on realized alpha to

test whether skill alpha discriminates better between future out- and underperformers. For

this test, we exclusively use the L&B-correction to calculate skill alpha because D&E

dummies, by nature, do not cover the ranking period of such a test and require knowledge of

future information. More specifically, we calculate L&B and realized alphas for growing long-

term ranking periods starting in January of 1993 and ending in March of each year from 2003

through 2009, respectively. Then we calculate the respective L&B and realized holding period

alphas over the following 48 months and compare the respective ranks. We chose these sub-

period definitions to ensure maximum use of our sample period. Moreover, separating ranking

17

and holding periods between March and April reduces truncation by end-of-calendar-year

window dressing. L&B dummies are calculated specifically for each sub-period to avoid

forward-looking bias. We require funds to have at least 48 monthly observations during either

period to ensure that estimation results are reasonably reliable and represent the long-term

character of the fund. Further, to test whether these results are of economic value we

separately calculate realized alphas of equal-weighed \High" (best 20 %) and \Low" portfolios

(worst 20 %) for all 48-month holding periods.

We are aware of the fact that the requirement of 48 months survival during the

holding periods potentially induces look-ahead survivorship bias to our performance

persistence tests due to the use of future knowledge (e.g., ter Horst et al., 2001). However,

both realized and L&B alpha suffer equally from the bias such that performance persistence

in general might be overstated but the difference between realized and L&B rankings remains

unbiased. However, to test for robustness of our results, we calculate correlations based on

realized alphas for holding periods of 12 months, thereby substantially reducing look-ahead

bias at the expense of noisier holding period alphas. Accordingly, we extend the ranking

periods until March 2012 for this part of the test. In a further step, we eliminate look-ahead

bias completely by showing realized performance of High and Low portfolios over 48-month

holding periods dropping the requirement of survival. In addition, we also calculate

cumulative alphas and time series alphas of yearly rebalanced High and Low portfolios to add

further robustness to our results and to gain further insight into the short-term persistence of

our skill alpha.

5. Empirical Results

This section reports results from our empirical analysis. It is organized based on the order of

the research hypotheses we formulate in section 2. Therefore, we first present results on

Monkey Business and market level performance, survivorship bias and luck bias. Then we

present results on individual fund level. Finally, we present the results regarding performance

persistence.

A. MARKET LEVEL PERFORMANCE AND LUCK BIAS

A.1. Monkey Business

Before testing our Research Hypothesis 1 that there exists a positive reverse survivorship

bias, we test for evidence of Monkey Business. In that context, Table II reports average factor

loadings and the number of funds with significant interaction-betas calculated by Equation

18

10. The results clearly show that during the time approaching disappearance, factor betas

differ significantly for a considerable number of funds. This is especially the case for HML

where baseline beta is slightly positive suggesting a tendency to investing in value stocks.

Interaction-betas, on the other hand, are distinctly negative for a large number of funds such

that total betas are also negative, which is more consistent with a growth strategy. The

results in the last column show, that the majority of funds with significant changes in factor

loadings are also the ones with significant corrections regarding realized alpha. Overall, we

therefore consider our assumption confirmed that some fund families do Monkey Business

with designated graveyard funds.

[Insert Table II here.]

A.2. Reverse Survivorship Bias { D&E Correction

After confirming that Monkey Business plays a role in disguising skill when approaching

disappearance we now test whether our Research Hypothesis 1 holds that some funds

disappear due to bad luck biasing market level estimated performance downwards. In that

context, Panel a. of Table III reports estimates of market level net-of-fee performance. As a

first finding, all equal-weighted survivor-bias-free performance measures are negative and

statistically significant which is in line with the general perception that active fund

management on average does not add value for investors. Survivor-biased performance is also

negative but statistically insignificant, also in line with general perception. Value-weighted

results are negative but generally closer to zero and therefore also insignificant. For further

insight, realized performance serves as a reference point to which corrected skill performance

measures can be compared. The D&E results clearly indicate higher skill alpha compared to

realized alpha. Moreover, we observe more individual funds with a positive and significant

alpha and fewer funds with a negative and significant alpha when correcting for bad luck.

The FbF standard deviation of corrected alphas (≈ 1 % p.a.) is higher than that of realized

alphas (0.86 % p.a.) which is in accordance with findings by Sastry (2011) who reports that

realized performance underestimates standard deviation. Linnainmaa finds a standard

deviation of true alpha that is even higher than ours (2.1 % p.a.). Fama and French (2010)

report an annual standard deviation of true alpha in the range from 1.25 % to 1.5 %. Panel b.

of Table III reports gross-of-fee performance. The relations between the alphas are basically

the same.

[Insert Table III here.]

Further, the FbF results show that D&E dummy deltas are negative on average. We also

obtain more negative and significant than positive and significant individual dummy deltas.

19

The frequencies of negative and significant deltas are roughly 10 % with 157 (Execution) and

164 (Decision) out of 1,589 disappeared funds. We interpret these 10 % such that we are not

catching a systematic effect and that these funds are the ones disappearing because they were

unlucky. Figure 2 visualizes this finding by showing how our survivor-bias-free sample divides

into survivors and different non-survivor groups over time. Non-survivors in general are

displayed as the cumulative number of funds disappearing prior to a respective date.

Unskilled non-survivors are defined by having positive or insignificant D&E dummy deltas.

Unlucky non-survivors are those with negative and significant D&E dummy deltas and are

displayed as the difference between the dotted and dashed lines in the right graph. The figure

shows that the number of unlucky non-survivors is only a small fraction of the total non-

survivors, suggesting that reverse survivorship bias is small.

[Insert Figure 2 here.]

Table IV shows estimates of the different alpha biases corresponding to the performance

measures presented in Table III. Specifically, we present estimates of survivorship bias as a

reference for reverse survivorship bias. The results show that equal-weighted survivorship bias

is significant with approx. 0.7 % p.a. As expected, this is lower than recent estimates of up to

1.5 % p.a. due to our selection criteria (e.g. Carhart et al, 2002; Rohleder et al., 2011). Value-

weighted survivorship bias is about half as high with 0.33 % p.a. which is expected because

non-survivors are relatively smaller than survivors. Moreover, value-weighted results also

account for the fact that money outflows from underperforming funds might show up as

inflows to outperforming funds.

[Insert Table IV here.]

Our estimate of reverse survivorship bias (D&E luck bias) is positive and significant as

predicted. However, the annualized reverse survivorship bias with 0.2884 % p.a. (FbF) is less

than half in magnitude compared to the 0.62 % p.a. estimated by Linnainmaa (2013). Value-

weighted, FoF reverse survivorship bias is in fact very small with less than 4 basis points p.a.

such that it is economically irrelevant. These findings on the one hand confirm our Research

Hypothesis 1 by showing a positive and significant reverse survivorship. On the other hand,

they prove that Linnainamaa overestimates its economic significance. Also, it supports our

previous findings that only a small fraction of up to 10 % disappears due to bad luck such

that reverse survivorship bias is in general very small.

A.2. Luck Bias Independent of Disappearance { L&B Correction

Pursuing Research Hypothesis 2, we discuss in this sub-section the results for performance

corrected for lucky and unlucky events unrelated to disappearance. Specifically, we

20

exclusively use the outlier-based dummies Luck and BadLuck. Equal-weighted results in

Table III show that average L&B corrected performance is lower than realized performance.

FbF-statistics on dummy deltas rationalize this discovery because the average Luck delta is

higher (+4.36 %) than the average BadLuck delta (-4.21 %) in absolute terms. Also, the

number of lucky events per fund is higher with 3.55 than the average number of unlucky

events per fund (3.20). This confirms our Research Hypothesis 2 and supports the prediction

that funds experience more lucky than unlucky events while surviving because there is no

mechanism punishing luck in a similar fashion as disappearance punishes bad luck.

The corresponding estimates for luck bias in Table IV show that the bias is negative

and significant in case of equal-weighting with values of -0.1810 % p.a. (FbF) and -0.2505 %

p.a. (FoF). This strongly contradicts Linnainmaa's prediction that luck generally biases

market level estimated performance downwards. Value-weighted L&B luck bias is also

negative but statistically insignificant and economically irrelevant with -0.0876 % p.a. Gross-

of-fee results for L&B alphas and alpha biases are basically the same as the net-of-fee results.

Overall, our new L&B approach delivers valuable insight on luck of funds independent of

disappearance previously undocumented by the related literature.

A.3. Complete Correction using All Available Information { Full Correction

Pursuing Research Hypothesis 3, we combine the previous corrections by using all four

dummy variables. Table III shows that both effects offset each other such that \Full" skill

alpha is between the D&E and L&B alphas. In case of FbF, skill performance is a bit higher

than realized performance. Both numbers of significant positive and negative alpha funds

increase, thereby confirming Sastry's (2011) finding of a fat-tailed true alpha-distribution.

Average dummy deltas remain as above, such that Execution and Decision deltas are both

negative. Also, Luck delta is higher in absolute terms than BadLuck delta and we document

more lucky events than unlucky events per fund. For equal-weighted FoF, skill performance is

a bit lower than realized performance. The same is true for value-weighting. This confirms

our expectations formulated in Research Hypothesis 3.

Finally, the results in Table IV show that \full" luck bias is very small, economically

irrelevant, and statistically insignificant except for the equal-weighted FoF case. Here, luck

bias is slightly significant and negative with an annualized value of -0.1247 % p.a., thereby

also contradicting Linnainmaa (2013) and ultimately \reversing" reverse survivorship bias.

Gross-of-fee results for alphas and alpha biases are basically the same as the net-of-fee results.

Overall, the results in this sub-section indicate that luck and bad luck more or less

balance within the cross-section of funds. Therefore, there is no economically significant luck

21

bias in market level realized performance measures such that the standard Carhart model is a

good estimator for market level skill performance.

B. INDIVIDUAL FUND PERFORMANCE

B.1. Rank Correlations between Realized and Skill Performance

Besides the fact that average market level performance is not biased by luck, the results in

the previous section indicate that individual funds might indeed be significantly biased by

luck because dummy deltas are significant for considerable numbers of funds and the

frequencies of significant alphas increase. Being the key strength of our paper compared to

the related literature, our luck bias corrections allow us to analyze the actual skill

performance of individual funds. As it is unpractical to present results for 3,802 individual

funds, our Research Hypothesis 4 states that fund rankings change significantly when using

skill performance measures. Therefore, Table V reports correlation coefficients between

individual realized and corrected performance estimates. Specifically, it shows standard

correlations as well as Spearman's rho (½) and Kendall's tau (¿) rank correlations. The later

not only considers that ranks are different but also the distance between the ranks, thereby

giving higher weight to larger rank changes. In general, the results show that both corrections

significantly change the ranks of individual funds. Moreover, the correction by D&E causes

higher rank changes (¿) supporting our finding that some funds disappear due to bad luck.

Overall, these rank changes confirm our hypothesis that individual performance is

significantly affected by luck. Results on net and gross returns are basically the same.

[Insert Table V here.]

B.2. Distribution of Individual Alphas

Another way of testing Research Hypothesis 4 regarding the impact of luck bias on the

performance of individual funds is to compare distributions of different alpha estimates in the

cross-section of funds. This also resembles the existing literature on luck and skill, where the

distribution of realized alpha in the cross-section of funds is regularly compared to

hypothetical true-alpha distributions based on different assumptions, bootstraps and

simulations (e.g., Kosowski et al., 2006; Fama and French, 2010; Sastry, 2011). Specifically,

we compare fractions of funds performing above and below certain levels of annualized alpha

measured by our different realized and skill models. In Table VI, \All" counts all funds

regardless of the significance of alpha while \**" counts only funds where alpha is statistically

significant based on a Newey and West (1987) HAC-consistent p-value of at least 5 %. Panel

a. shows results for net-of-fee returns. The numbers on all alphas indicate that the majority of

22

funds (63-69 %) show negative performance, irrespective of the measure. However, there are

also at least 30 % of funds with a positive alpha.

[Insert Table VI here.]

Looking at the significant-only alphas shows that the fractions of funds above certain levels

reduce dramatically such that only 1.95 % of all funds significantly exceed a realized alpha of

1 % p.a. Correcting alpha with D&E leads to an upward shift which is in accordance with

Linnainmaa's prediction of funds disappearing due to bad luck. Moreover, it leads to a wider

alpha-distribution which is also visible in Table III where D&E alpha shows a larger standard

deviation. The L&B correction leads to a downward shift combined with slight narrowing of

the alpha distribution due to the elimination of outliers in the errors (see also the standard

deviation Table III). Looking at the full model reveals that the level of the distribution is

comparable to the realized alpha distribution but with slightly fatter tails. This is in

accordance with Kosowski et al. (2006), Fama and French (2010), and Sastry (2011) who

report that the true alpha distribution is wider and has fatter tails than the distribution of

estimated alpha. Moreover, we find a considerable fraction of 17 % of funds with a significant

and negative performance and a very large fraction of 79 % with zero skill. These numbers

closely correspond to respective fractions of 24 % and 75 % reportet by Barras et al. (2010).

However we also find that 4.10 % of funds deliver a positive and significant alpha above 1 %

p.a. which is in line with findings of Kosowski et al. (2006).

Panel b. of Table VI reports gross-of-fee performance fractions. Generally, the results

are the same as above but, as expected, with an upward shift of the distribution. The

distributions are now more or less centered on zero with a slightly higher weight above.

Bearing in mind that our sample slightly suffers from survivorship bias due to the 48 months

survival criterion this further confirms that the mutual fund market as a whole is a zero sum

game before costs. Overall, the tests in this section confirm our Research Hypothesis 4 that

luck bias significantly affects individual performance measures. Moreover, using our new

approach to correcting individual fund performance for luck bias, we deliver a valuable

contribution to the related literature by confirming many of their findings which were based

on hypothetical assumptions about the nature of true alpha.

C. PERFORMANCE PERSISTENCE

In the previous sections of our empirical study, we document that while luck and bad luck

balance within the cross-section of mutual funds, individual fund performance is significantly

suffering from luck bias. This leads to changes in fund rankings and in the distribution of

alpha. To verify the economic implications of our findings, in this sub-section we extensively

23

test whether the predictive power of our corrected skill performance measures is higher than

that of standard performance measures. Specifically, our Research Hypothesis 5 states that

measures of performance persistence based on skill performance should be higher than those

based on realized performance if our corrected measures better approximate the long-term

investment skill of individual managers. To test our hypothesis we conduct performance

persistence analyses using L&B skill performance in comparison to analogous analyses using

standard realized performance.

Panel a. of Table VII shows rank correlations between growing long-term ranking

periods and long-term 48-month holding periods. As a first finding, all correlations are

positive, many even significant. The results for net-of-fee performance further indicate that

rank correlations based on skill alphas are higher than those based on realized alphas in the

majority of sub-periods. Overall, we consider these results prove that our L&B corrected skill

alpha is better in measuring sustainable long-term manager skill as it is a better predictor of

future performance than the standard realized alpha. In case of gross-of-fee performance,

correlations are slightly lower and for few sub-periods correlations are higher for realized

ranking alphas. This could be due to persistent differences in fees which will show in net-

returns but not in gross-returns. However, investors observe net-returns rather than gross-

returns. As both are only slightly different, we focus on net-of-fee results in the following.

[Insert Table VII. here.]

Now, to test if these results are also economically relevant, Panel b. of Table VII reports

realized 48-month holding period performance of equal-weighted \High" and \Low" portfolios

for the ranking and holding periods in Panel a. Net return results clearly indicate that High

portfolios always outperform Low portfolios creating a positive High-Low return. Moreover,

L&B-High portfolios always outperform realized-High portfolios while L&B-Low portfolios

always underperform realized-Low portfolios. The premium to a zero-investment L&B-High-

minus-Low portfolio is therefore up to 0.6 % p.a. higher than the premium to a realized High-

minus-Low portfolio. This means that L&B skill alpha more effectively discriminates between

future outperformers and future underperformance. Our approach thus adds significant

economic value.

To check for any impact of look-ahead bias, Panel c. of Table VII shows correlations

based on realized alphas for much shorter 12-month holding periods, thereby accepting noisier

holding period alphas. Net-of-fee results show that rank correlations are still positive and

comparable in magnitude to the results in Panel a. in 9 out of 10 sub-periods. Moreover, L&B

ranking alphas show higher rank correlations than realized ranking alphas in 8 out of 10 sub-

periods. This means that our general persistence results are not systematically overstated by

24

look-ahead bias. Furthermore, it means that our L&B correction is better in predicting short-

term as well as long-term performance compared to the standard model.

In a fashion similar to Panel b., Panel d. of Table VII shows realized alphas of High

and Low portfolios. Net-of-fee results clearly show that the L&B-High portfolio outperforms

in 6 out of 7 sub-periods and the L&B-Low portfolio underperforms in all sub-periods.

Moreover, the premium to L&B-High-minus-Low portfolios is up to 0.9 % p.a. higher than

the premium to realized-High-minus-Low portfolios. In addition, the last two columns of

Panel d. show the cumulative alpha and the time series alpha of yearly rebalanced High and

Low portfolios. In both columns, the L&B-High portfolio outperforms the realized-High

portfolio and the L&B-Low portfolio underperforms the realized-Low portfolio. This leads to

premiums to the L&B-High-minus-Low portfolio of 0.7 % (cumulative alpha) and 0.4 % p.a.

(time series alpha), respectively, over the corresponding realized-High-minus-Low portfolios.

Overall, the results of our extensive performance persistence tests show that our

approach to correcting measured performance for luck bias is not just a statistical artifact.

We confirm our Research Hypothesis 5 that L&B skill alpha has higher predictive power for

future performance and discriminates more effectively between future outperformers and

future underperformers. This adds significant economic value for academics and for investors

because our approach is easy to implement and the information used is readily available.

Moreover, in results not reported in the paper (Table VIII is available from the authors upon

request) we continue testing Research Hypothesis 5 using much shorter 48-month ranking

periods thereby testing the predictive power of short-term L&B alpha. The results clearly

confirm our above findings with the exception that correlations are now sometimes negative

suggesting that long-term past performance in general predicts future performance better

than short-term past performance.

6. Conclusion

Despite constantly improving datasets and methods used to measure mutual fund

performance, research still struggles with the question which part of the measured

performance is effectively due to the managers' investment skill and which part is due to

luck. We deliver a valuable contribution to answering this question by being the first to

measure luck bias and skill performance separately for individual funds. In the process, we

also contribute to the very recent topic of reverse survivorship bias by Linnainamaa (2013).

Our results clearly show that, while insignificant on the aggregate market level, luck bias

significantly truncates measured performance of individual funds thereby altering fund

rankings and understating the width of the alpha distribution in the cross-section of funds.

25

Using performance persistence tests, we prove that our luck bias corrected skill performance

measures are not just statistical artifacts. Our skill alpha shows consistently higher predictive

power than standard estimated alpha creating premiums to skill alpha based High-minus-Low

portfolios that are up to 0.9 % p.a. higher than those to standard alpha based High-minus-

Low portfolios. As our methodology is easy to implement and based on readily available data,

our findings add significant economic value for academics and for investors.

26

References

Barnett, V. and Lewis, T. (1994) Outliers in Statistical Data. John Wiley & Sons., 3rd edition.

Barras, L., Scaillet, O., and Wermers, R. (2010) False Discoveries in Mutual Fund

Performance: Measuring Luck in Estimated Alphas. Journal of Finance 65, 179-216.

Blake, D. and Timmermann, A. (1998) Mutual Fund Performance: Evidence from the UK.

European Finance Review 2, 57-77.

Brown, S. J. and Goetzmann, W. N. (1995) Performance Persistence. Journal of Finance

50, 679-698.

Carhart, M. M. (1997) On Persistence in Mutual Fund Performance. Journal of Finance 52,

57-82.

Carhart, M. M., Carpenter, J. N., Lynch, A. W., and Musto, D. K. (2002) Mutual fund

survivorship. Review of Financial Studies 15, 1439-1463.

Chan, L. K. C. and Lakonishok, J. (1992) Robust Measurement of Beta Risk. Journal of

Financial and Quantitative Analysis 27, 265-282.

Collins English Dictionary Online (2012), http://www.collinsdictionary.com, 13.09.2012.

Cook, R. D. (1977) Detection of Influential Observations in Linear Regressions.

Technometrics 19, 15-18.

Cook, R. D. and Weisberg, S. (1982) Residuals and Influences in Regressions. New York,

Chapman and Hall.

Cuthbertson, K., Nitzsche, D., and O’Sullivan, N. (2008) UK mutual fund performance: Skill

or Luck? Journal of Empirical Finance 15, 613-634.

Elton, E. J., Gruber, M. J., and Blake, C. R. (1996) The persistence of risk-adjusted mutual

fund performance. Journal of Business 69, 133-157.

Fama, E. F., and French, K. R. (1993) Common risk factors in the returns on stocks and

bonds. Journal of Financial Economics 33, 3-56.

Fama, E. F., and French, K. R. (2010) Luck versus Skill in the Cross-Section of Mutual Fund

Returns. Journal of Finance 65, 1915-1947.

Grinblatt, M. and Titman, S. (1992) The Persistence of Mutual Fund Performance. Journal

of Finance 47, 1977-1984.

Grundy, B. D. and Martin, J. S. (2001) Unterstanding the Nature of the Risk and the Source

of the Rewards to Momentum Investing. Review of Financial Studies 14, 29-78.

27

Hendricks, D., Patel, J., and Zeckhauser, R. (1993) Hot Hands in Mutual Funds: Short-Run

Persistence of Relative Performance, 1979-1988. Journal of Finance 48, 93-130.

Jegadeesh, N. and Titman, S. (1993) Returns to Buying Winners and Selling Losers:

Implications for Stock Market Efficiency. Journal of Finance 58, 65-91.

Kacperczyk, M., Sialm, C., and Zheng, L. (2008) Unobserved Actions of Mutual Funds.

Review of Financial Studies 21, 2379-2416.

Kosowski, R., Timmermann, A., Wermers, R., and White, H. (2006) Can individual Fund

“Stars” Really Pick Stocks? New Evidence from a Bootstrap Analysis. Journal of Finance

61, 2551-2595.

Layfield, L. and Stevenson, S. (2011) Separating Skill from Luck in REIT Mutual Funds.

Working Paper, University of Reading.

Linnainmaa, J. T. (2013) Reverse Survivorship Bias. Journal of Finance 68, 789-813.

Martin, R. D. and Simin, T. T. (2003) Outlier-Restistant Estimates of Beta. Financial

Analysts Journal, September/October, 56-69.

Newey, W. K. and West, K. D. (1988) A simple, positive semi-definite, heteroskedasticity and

autocorrelation consistent covariance matrix. Econometrica 55, 703-708.

Rohleder, M., Scholz, H., and Wilkens, M. (2011) Survivorship Bias and Mutual Fund

Performance: Relevance, Significance, and Methodical Differences. Review of Finance 15,

441-473.

Sastry, R. (2011) The Cross-Section of Investing Skill. Working Paper, Columbia Business

School.

Storey, J. D. (2002) A direct approach to false discovery rates. Journal of the Royal

Statistical Society B 64, 479-498.

ter Horst, J. R., Nijman, T. E, and Verbeek, M. (2001) Eliminating look-ahead Bias in

evaluating persisence in mutual fund performance. Journal of Empirical Finance 8, 345-373.

Zhao, X. (2005) Exit Decisions in the U.S. Mutual Fund Industry. Journal of Business 78,

1365-1401.

28

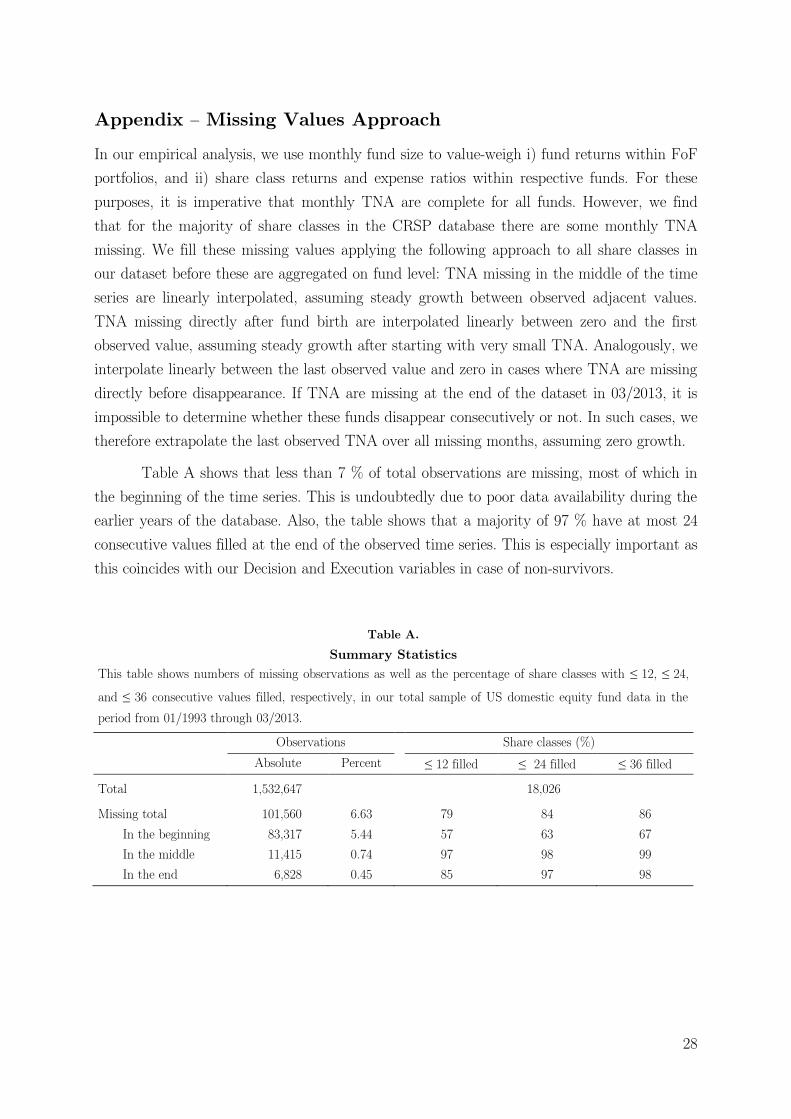

Appendix { Missing Values Approach

In our empirical analysis, we use monthly fund size to value-weigh i) fund returns within FoF

portfolios, and ii) share class returns and expense ratios within respective funds. For these

purposes, it is imperative that monthly TNA are complete for all funds. However, we find

that for the majority of share classes in the CRSP database there are some monthly TNA

missing. We fill these missing values applying the following approach to all share classes in

our dataset before these are aggregated on fund level: TNA missing in the middle of the time

series are linearly interpolated, assuming steady growth between observed adjacent values.

TNA missing directly after fund birth are interpolated linearly between zero and the first

observed value, assuming steady growth after starting with very small TNA. Analogously, we

interpolate linearly between the last observed value and zero in cases where TNA are missing

directly before disappearance. If TNA are missing at the end of the dataset in 03/2013, it is

impossible to determine whether these funds disappear consecutively or not. In such cases, we

therefore extrapolate the last observed TNA over all missing months, assuming zero growth.

Table A shows that less than 7 % of total observations are missing, most of which in

the beginning of the time series. This is undoubtedly due to poor data availability during the

earlier years of the database. Also, the table shows that a majority of 97 % have at most 24

consecutive values filled at the end of the observed time series. This is especially important as

this coincides with our Decision and Execution variables in case of non-survivors.

Table A.

Summary Statistics

This table shows numbers of missing observations as well as the percentage of share classes with ≤ 12, ≤ 24,

and ≤ 36 consecutive values filled, respectively, in our total sample of US domestic equity fund data in the

period from 01/1993 through 03/2013.

Observations

Share classes (%)

Absolute Percent ≤ 12 filled ≤ 24 filled ≤ 36 filled

Total 1,532,647

18,026

Missing total 101,560 6.63 79 84 86

In the beginning 83,317 5.44 57 63 67

In the middle 11,415 0.74 97 98 99

In the end 6,828 0.45 85 97 98

29

Figures and Tables Figure 1

Industry Development

This figure shows the development of the survivor-bias-free sample of US equity funds in the period from

01/1993 through 03/2013. The left graph shows industry size in Mio. USD. The right graph shows number of

funds. To be counted, funds have to survive at least 48 months within the sample period.

Figure 2

Survivors, Unskilled and Unlucky Non-Survivors

This figure shows how the survivor-bias-free sample of US equity funds divides into survivors and different

non-survivor groups over time in the period from 01/1993 through 03/2013. Non-survivors in general are the

cumulative number of funds disappeared prior to a respective date. Unskilled non-survivors are those with

positive or insignificant D&E dummy deltas based on Newey and West (1987) HAC-consistent p-Values

≤ 5 %. Unlucky Non-Survivors are the differential between Total Non-Survivors and Unskilled Non-Survivors

and are those funds with negative and significant dummy deltas. Total funds are the cumulative number of

all non-survivors plus the actual number of survivors (differential between the solid and the dashed lines).

0

1000000

2000000

3000000

4000000

Indust

ry S

ize

(Mio

USD

)

1997m1 2001m1 2005m2 2009m21993m1 2013m3Date

500

1000

1500

2000

2500

3000

Num

ber

of Funds

1997m1 2001m1 2005m2 2009m21993m1 2013m3Date

0

1000

2000

3000

4000

Num

ber

of Funds

1997m1 2001m1 2005m2 2009m21993m1 2013m3Date

Non-Survivors Total Funds

0

1000

2000

3000

4000

Num

ber

of Funds