lowland investment company - alliance trust word - lwi james henderson describes his reasons for...

TRANSCRIPT

Stock in focus: Velocys

James Henderson describes his reasons for investing in Velocys We run a long list in the Lowland portfolio of around 110 holdings, comprising of large, medium and small-cap positions. The relatively long list is needed because of the smaller companies. They are much higher risk so we must be prudent and diversify, hence only around 1/3 of the portfolio’s value is in 60 small-cap positions. The outcomes these smaller companies are aiming for are usually ground-breaking, and if they achieve them the impact will certainly be felt in the portfolio’s performance. Velocys is one such example, daring to develop technology that, in one application, uses landfill rubbish to power airline jets, and in another, could seriously reduce the amount of carbon pumped into our frail environment. Harnessing a process Velocys’ technology is doing nothing new. The business is based on a chemical reactor design called Fischer-Tropsch and the catalyst that makes it work. Its purpose is to turn a feedstock of petrochemicals, namely methane, into intermediate fuels such as low sulphur transport fuel, as well as feedstock for lubricants, premium waxes and paraffins, in a process called ‘gas-to-liquid’ (GtL). The process is nothing new – the technology has existed since the 1920s; Shell and Sasol have been using it for years.

What is different about Velocys? Where it differs is the dramatically smaller scale at which the process can become economically viable. Velocys has a range of patents that protect the design of its micro-channel reactor and the highly active catalyst used to optimise it. To give an idea of scale, Shell and Sasol’s process is commercially viable at a minimum of 15,000 barrels of oil equivalent per day (b/d), whereas the Velocys micro-reactor offers viability at 1,500 b/d, opening up a significant new end market. Revenues come from licensing the design (they don’t actually make the reactors), selling the catalyst and its subsequent re-loadings. A key element of their unique selling proposition (USP) is feedstock that is very cheap - in some cases a negative cost (i.e. they are paid to take it) - but also an end product that is usually very high quality. By some estimates these premium products could generate revenue in the region of 180-200% the cost of Brent crude (Source: Canaccord Genuity). Source: courtesy of Velocys Waste not, want not At the moment, revenues for Velocys come from a variety of sources such as: alternative energy suppliers who benefit from public subsidies; waste companies looking to monetise their waste gases; and speciality chemical companies who wish to use gas-based feedstock rather than the more expensive oil based. Projects thus far have been largely focused on waste or biomass, for example their admission into the GreenSky project - a consortium led by Solena Fuels to build a facility to convert landfill waste into jet fuel for British Airways.

Lowland Investment Company

Lowland Investment Company (continued)

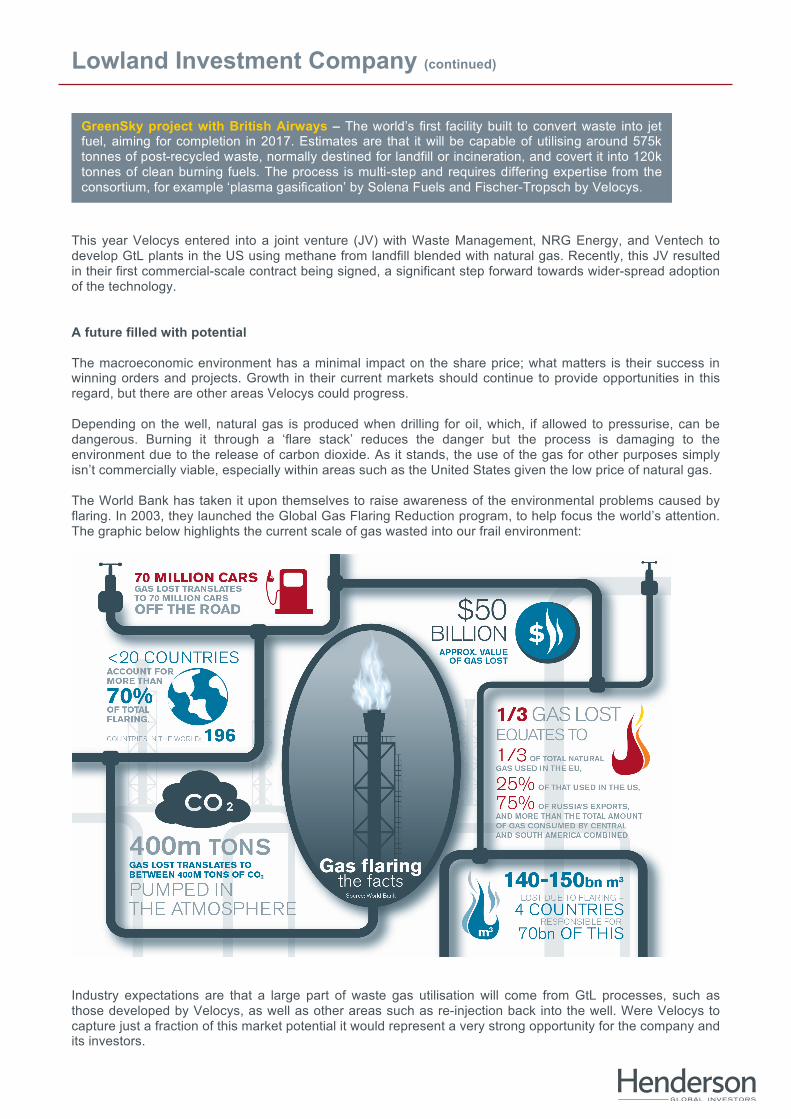

This year Velocys entered into a joint venture (JV) with Waste Management, NRG Energy, and Ventech to develop GtL plants in the US using methane from landfill blended with natural gas. Recently, this JV resulted in their first commercial-scale contract being signed, a significant step forward towards wider-spread adoption of the technology. A future filled with potential The macroeconomic environment has a minimal impact on the share price; what matters is their success in winning orders and projects. Growth in their current markets should continue to provide opportunities in this regard, but there are other areas Velocys could progress. Depending on the well, natural gas is produced when drilling for oil, which, if allowed to pressurise, can be dangerous. Burning it through a ‘flare stack’ reduces the danger but the process is damaging to the environment due to the release of carbon dioxide. As it stands, the use of the gas for other purposes simply isn’t commercially viable, especially within areas such as the United States given the low price of natural gas. The World Bank has taken it upon themselves to raise awareness of the environmental problems caused by flaring. In 2003, they launched the Global Gas Flaring Reduction program, to help focus the world’s attention. The graphic below highlights the current scale of gas wasted into our frail environment:

Industry expectations are that a large part of waste gas utilisation will come from GtL processes, such as those developed by Velocys, as well as other areas such as re-injection back into the well. Were Velocys to capture just a fraction of this market potential it would represent a very strong opportunity for the company and its investors.

GreenSky project with British Airways – The world’s first facility built to convert waste into jet fuel, aiming for completion in 2017. Estimates are that it will be capable of utilising around 575k tonnes of post-recycled waste, normally destined for landfill or incineration, and covert it into 120k tonnes of clean burning fuels. The process is multi-step and requires differing expertise from the consortium, for example ‘plasma gasification’ by Solena Fuels and Fischer-Tropsch by Velocys.

Lowland Investment Company (continued)

Before investing in an investment trust referred to in this document, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser. Telephone calls may be recorded and monitored. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell or purchase any investment. It does not form part of any contract for the sale or purchase of any investment. Issued in the UK by Henderson Global Investors. Henderson Global Investors is the name under which Henderson Global Investors Limited (reg. no. 906355), Henderson Fund Management Limited (reg. no. 2607112), Henderson Investment Funds Limited (reg. no. 2678531), Henderson Investment Management Limited (reg. no. 1795354), Henderson Alternative Investment Advisor Limited (reg. no. 962757), Henderson Equity Partners Limited (reg. no.2606646), Gartmore Investment Limited (reg. no. 1508030), (each incorporated and registered in England and Wales with registered office at 201 Bishopsgate, London EC2M 3AE) are authorised and regulated by the Financial Conduct Authority to provide investment products and services. Ref: 34V