low-cost carriers will continue to outperform but network airlines

TRANSCRIPT

January 19, 2012

Research Report: Sector update

Davy on Airlines

Low-cost carriers will continue to outperform but network airlines will struggle

www.davy.ie Bloomberg: DAVY<GO> Research: +353 1 6148997 Institutional Equity Sales: +353 1 6792816 Davy Research

g

Stephen Furlong [email protected] / +353 1 6148924

Joshua Goldman, PhD [email protected] / +353 1 6148997

Low-cost carriers (LCCs) are preferred play in a weak eurozone environment

• We see real pricing power for market leaders Ryanair and easyJet. As we look into Q1 and Q2, capacity conditions appear beneficial for both airlines and competitive pressures are benign.

• We expect further cost benefits for Ryanair as capacity is reallocated to favourable airport locations.

• easyJet should gain from 'easy' comparables and from the group's strategy overview to be presented at its capital markets day on January 31st.

• Cash returns are a key feature in 2012: easyJet will provide a 11.5% dividend yield; Ryanair has c.€1bn pre-capex free cash flow, which allows for significant returns to shareholders.

Network airlines face many challenges due to uncontrollable cost increases; premium traffic the biggest risk

• The network airlines are experiencing slowing volumes and declines in load factors. Although supply is adjusting somewhat to suppressed demand, it is difficult to envisage a scenario in which there is pricing power.

• Leading indicators (freight and manufacturing PMIs) suggest that premium traffic could turn negative.

• With large cost increases (fuel and taxes), 2012 is shaping up to be a very challenging year for the network airlines.

Valuation multiples low but earnings momentum key

• Having made some adjustments to our forecasts (upwards in the case of Ryanair and downwards for Lufthansa), we are now 10-15% below consensus for the networks and at or above consensus for the LCCs.

• Our top picks remain Ryanair and easyJet based on profit growth and cash returns to shareholders. We are increasing our price target for Ryanair to €5.

• We are downgrading Aer Lingus to 'neutral' and expect the networks to 'underperform' until the macro environment improves. For balance sheet and valuations reasons, we retain Lufthansa's rating as 'neutral'.

Please refer to important disclosures at the end of this report.

J&E Davy, trading as Davy, is regulated by the Central Bank of Ireland. Davy is a member of the Irish Stock Exchange, the London Stock Exchange and Euronext. For branches in the UK, Davy is authorised by the Central Bank of Ireland and subject to limited regulation by the Financial Services Authority. Details about the extent of our regulation by the Financial Services Authority are available from us on request. All prices are as of close of January 17th. All authors are Research Analysts unless otherwise stated. For the attention of US clients of Davy Securities, this third-party research report has been produced by our affiliate, J & E Davy.

Calendar of upcoming events

January 26th

easyJet Q1 IMS

January 30th

Ryanair Q3 results

January 31st

easyJet capital markets day

February 28th

Aer Lingus FY results

February 29th

IAG FY results

March 7th

Air France-KLM FY results

March 15th

Lufthansa FY results

Ratings Aer Lingus Neutral (19/01/12) Previous Outperform (23/04/10) Air France-KLM Underperform (19/01/12) Previous Neutral (09/09/11) easyJet Outperform (22/07/11) Previous Neutral (19/04/11) IAG Underperform (19/01/12) Previous Neutral (09/09/11) Lufthansa Neutral (09/09/11) Previous Outperform (21/03/11) Ryanair Outperform (07/12/09) Previous Neutral (02/11/09)

For full details of current and previous ratings see www.davy.ie/ratings.

Price targets

Aer Lingus 0.75c 19/01/12

Previous 100c 09/09/11

Air France-KLM 380c 19/01/12

Previous 700c 09/09/11

easyJet (£) 475p 05/08/11

Previous 350p 19/04/11

IAG 140c/115p 19/01/12

Previous 230c/200p 09/09/11

Lufthansa 900c 19/01/12

Previous 1200c 09/09/11

Ryanair 500c 19/01/12

Previous 450c 19/04/11

Research Report: Davy on Airlines January 19, 2012

2 Davy Research

Contents

Key themes for 2012 3

Current estimates 5

Capacity update 6 Intra-EU capacity remains below peak and should help support yields; in

contrast, to/from EU is showing steady growth 6 Q1 planned capacity for the network airlines has been adjusted downwards,

but is it enough? 7

Early indicators signal upcoming weakness in premium traffic; potential significant impact on earnings 9

Rise in uncontrollable costs will prove challenging for network airlines 12 Fuel remains stubbornly high, even as network airlines' operating profit declines 12 Effects of the UK APD 16 EU ETS has greater impact on the network airlines 16

Second wave of consolidation should benefit specific players 17

Stock views 20 Valuations are low but earnings at risk for networks; LCCs remain attractive 20 easyJet – special dividends and business focus 24 Ryanair – cash machine to be further illustrated in 2012 26 Aer Lingus – needs to break out from 'value trap' in 2012 28 IAG – constrained by capex and cash flow 30 Lufthansa – challenges ahead in current environment 33 Air France-KLM – needs to deliver on turnaround plan 37 Announces ambitious turnaround plan 37 Scenario analysis – rights issue likely if plan not delivered 39

Appendix 1: Price to book 42

Appendix 2: Price/peak EPS 44

Appendix 3: Cyclically adjusted P/E 45

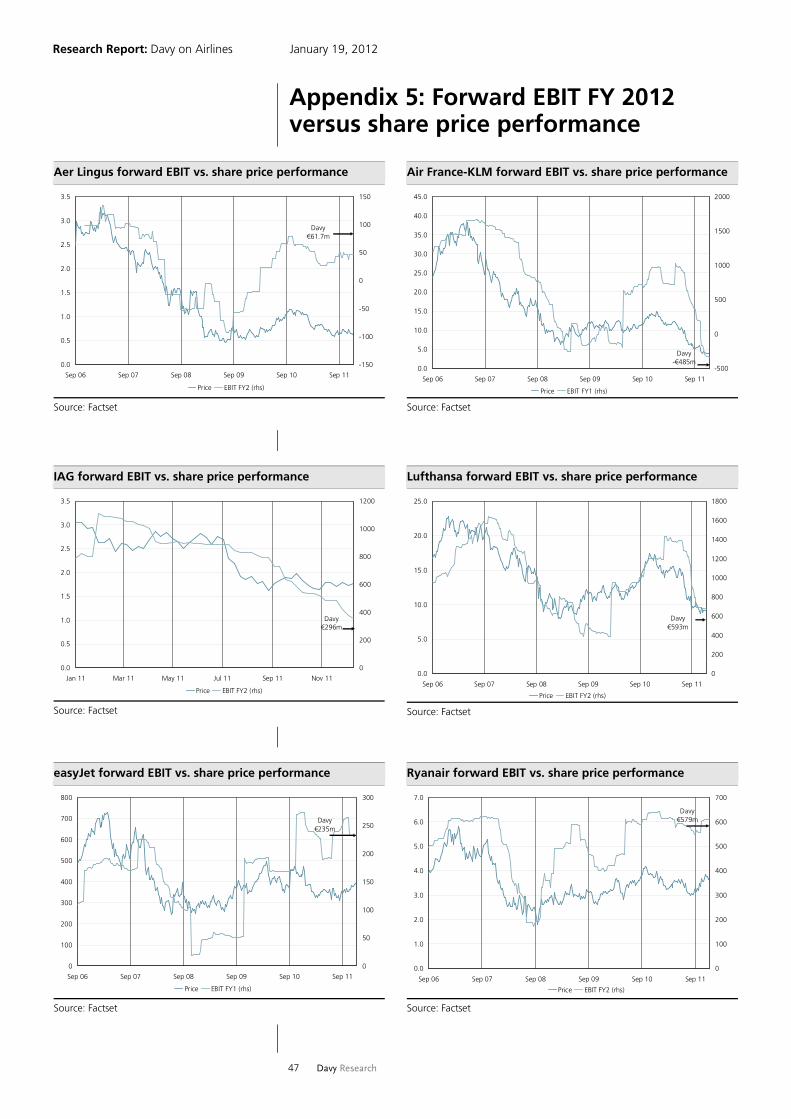

Appendix 4: Forward EBIT FY 2011 versus share price performance 46

Appendix 5: Forward EBIT FY 2012 versus share price performance 47

Appendix 6: EV/sales 48

Appendix 7: IATA summary forecasts 49

Appendix 8: Sector valuations and company analysis 50

Important disclosures 58

Research Report: Davy on Airlines January 19, 2012

3 Davy Research

Key themes for 2012 Capacity is decelerating, but further cuts are needed given PMI signals and freight volume declines

Capacity, which had grown in 2011, is adjusting downwards. The capacity data for December show an increase of 0.2% in the number of flights to/from Europe and a rise of 2% in offered seats. Within Europe, flight operations and seats have decreased by 2% and 0.4% respectively.

Long-haul traffic is more reliant on global GDP growth. All the major European airlines have signalled decelerating capacity growth but no contraction as of yet. Such contraction may be required if the economic picture continues to worsen.

Signals of a sharp slowdown in premium travel are evident in the Purchasing Managers Index (PMI) of business confidence, averaged across major economies. Business confidence has been a good early warning indicator of movement in premium travel growth, leading changes by up to six months.

The two main low-cost airlines have either flat capacity growth (easyJet) or negative capacity growth (Ryanair) this winter. We would expect further consolidation, particularly in short haul, as weaker network airlines, smaller LCCs and tour operators contract operations.

Air freight volumes, which tend to be a leading indicator of air passenger volumes, continue to show mid-single-digit declines that began in June.

In the freight market, we are witnessing capacity reductions by some express/cargo airlines on the Asia-Europe trade lane.

Operating leverage works in both directions; some uncontrollable costs rising

Companies, particularly those in the airline industry, are facing the challenge of pushing through higher input costs to end-users. IAG commented on this as follows: "the challenge and opportunity of recovery though revenue remains, but should take at least another 12 months". This is likely to make 2012 a challenging year, particularly as economic conditions worsen and the fuel price remains at elevated levels.

– Unwinding of fuel hedges is still likely to lead to double-digit increases in yoy fuel costs.

– In addition, other parties in the value chain (notably governments) are still raising taxes (e.g. the recent c.8% increase in air passenger duty (APD) tax in the UK and the introduction of an EU emissions tax scheme (ETS) for all airlines operating in/out of Europe in 2012).

– Charges at some regulated airports and some route charges are increasing.

In the absence of further revenue recovery, comparables may become more difficult.

Key themes for 2012 Further cuts in capacity are required

Uncontrollable costs are rising

Second wave of consolidation is starting

Contraction of long-haul European growth may be required if the economic situation worsens

Capacity is falling: negative intra-Europe but only decelerating growth on long haul

Signals of a sharp slowdown in premium travel are evident in the Purchasing Managers Index (PMI) of business confidence

We would expect further consolidation, particularly in short haul, as weaker network airlines, smaller LCCs and tour operators contract operations

Cost pressures Fuel remaining at elevated levels

Government taxes – APD, EU ETS

Regulated airports, route charges

Interest cost pressures as negative free cash flow resumes

Research Report: Davy on Airlines January 19, 2012

4 Davy Research

The focus on capital expenditure reductions through deferral and capacity and cost reductions will be needed to bolster balance sheets and prevent negative free cash flow positions. Most companies' balance sheets are healthy, but we note that Air France-KLM has presented a plan to rapidly reduce debt.

Second wave of consolidation starting

Downward pressure on revenues in 2008 led to quicker consolidation in the marketplace towards the stronger players. After a pause and as revenue pressure resumes, we expect a second wave of consolidation.

Recent examples are the negotiations regarding the sale of bmi; other potential sales include TAP and Aer Lingus' government stake. After Qatar Airways' recent acquisition of a 35% stake in Cargolux, it will be interesting to see if the Gulf carriers combine organic with acquisitive growth (e.g. the proposed 29.2% stake in Air Berlin by Etihad).

Latest consolidation moves AMR bankruptcy

Etihad stake in Air Berlin

Qatar stake in Cargolux

Bmi sale to IAG; bmibaby likely closed

Lan Chile/TAM merger

Research Report: Davy on Airlines January 19, 2012

5 Davy Research

Current estimates Our current forecasts are provided in the table below and include changes to our estimates for Ryanair and Lufthansa. We have adjusted numbers upwards in the case of the former and downwards in the case of the latter. Broadly, our estimates are at or above consensus for the LCCs and below for the networks (which reflects our current view). We assume oil prices at current levels of c.$110 per barrel. Clearly, the largest sensitivities for the airlines are the euro/dollar or sterling/dollar cost of fuel and yield development; we map out the sensitivities to these below.

Table 1: Operating profit estimates and consensus 2012

Operating profit old (€/£m)

Operating profit current (€/£m)

Change Operating profit consensus (€/£m)

% above/below consensus

Lufthansa 800 593 -26% 686 -13.5%

Ryanair 550 579 5% 567 2.1%

easyJet 235 235 0% 235 0.3%

Aer Lingus 62 62 0% 53 15.5%

IAG 296 296 0% 331 -10.5%

Air France-KLM -485 -485 0% -280 -73.2%

Source: Davy; Reuters; Bloomberg

Table 4: Fuel hedging positions

Airline Hedging guidance

Air France-KLM 52% FY2012 guiding €7.2bn, c.€800m increase

IAG 53% hedged for FY2012; +/-$10/MT = +/-€33m cost approx

Lufthansa 67% hedged in FY2012 above>$104 enjoy relative cost advantage

Ryanair 73% hedged FY2013 at $990PMT

easyJet 73% hedged FY2012 at $956/MT; 48% FY2013 at $979PMT

Aer Lingus 47% of FY12 at $975MT

Source: Davy

The direction of estimates is upwards for the LCCs (we upgrade Ryanair) and downwards for the networks (we downgrade Lufthansa)

We are at or above consensus for LCCs and below for networks

Table 2: FY 2012 profit sensitivity to 1% yield movement

Operating profit (€/£m) Currently +/- 1% yield

Change Percentage

Ryanair 579.4 543.5 -35.9 -6.2%

easyJet 235.2 206.4 -28.8 -12.2%

IAG 296.2 151.6 -144.7 -48.8%

Lufthansa 593.2 345.0 -248.2 -41.8%

Air France KLM -485.0 -669.4 -184.4 -38.0%

Aer Lingus 61.7 50.1 -11.6 -18.8%

Source: Davy

Table 3: FY 2012 profit sensitivity to $5 change in oil per barrel ($50 per tonne)

Operating profit (€/£m)

Currently +/- $5 ($50 PMT)

Change Percentage

Ryanair 579.4 602.9 23.5 4.1%

easyJet 235.2 243.8 8.6 3.7%

IAG 296.2 461.2 165.0 55.7%

Lufthansa 593.2 718.2 125.0 21.1%

Air France KLM -485.0 -263.0 222.0 45.8%

Aer Lingus 61.7 66.4 4.7 7.6%

Source: Davy

Research Report: Davy on Airlines January 19, 2012

6 Davy Research

Capacity update Current levels of intra-European capacity are below 2008 peak levels (as is capacity in the US domestic market). On the other hand, inter-continental EU traffic is above peak levels. Planned intra-European capacity growth is benign and in our opinion should help to support higher yields. A similar scenario has occurred in the US domestic market. Given the potential outbound demand weakness in Europe, the planned European long-haul capacity growth will have to be supported by demand from outside Europe. We also have concerns about premium traffic, which has shown slowing growth. Leading indicators suggest that it could turn negative, which would have a significant impact on the operating profits of the network airlines. Intra-EU capacity remains below peak and should help support yields; in contrast, to/from EU is showing steady growth

Intra-European capacity in 2011 is 2% down from the 2008 peak as the network airlines have significantly reduced capacity due to the economic downturn and intense competition from the LCCs. The below-peak levels of intra-EU capacity create a beneficial environment for the LCCs. As we have previously outlined in previous research notes, there has been a structural decrease in US domestic capacity that has helped to support yield increases in the US. The US Air Transport Association statistics reported that domestic average fares were up 9.3% year-to-date to November 2011 compared to the same period last year. The slowdown, and indeed contraction, in EU capacity, driven by the key players (Ryanair and easyJet), is likely to lead to a similar situation to that of the domestic US market. Intercontinental European capacity in 2011 was 12% above the 2008 peak. This was helped by the consistent growth in capacity to/from the Middle East and the rebound in capacity to/from Asia Pacific. The capacity to/from US/Canada is still below peak levels, which have likely been helped by the joint venture consolidation on the transatlantic (over 75% of northern transatlantic capacity is controlled by the three alliances with anti-trust immunity).

Capacity is below peak in intra-European and US domestic markets

The below-peak levels of intra-EU capacity create a beneficial environment for the LCCs

Research Report: Davy on Airlines January 19, 2012

7 Davy Research

Q1 planned capacity for the network airlines has been adjusted downwards, but is it enough?

Given the stubbornly high fuel prices and the challenging economic outlook in Europe, many of the European carriers have lowered their planned capacity growth (as is evident in the following chart). The planned capacity growth by region reinforces our view. The LCCs should benefit from negative intra-European capacity

growth in Q1 and low growth in Q2. The picture is more negative for European network airlines. To keep

load factor stable, assuming challenging GDP conditions in Europe for H1, demand from outside the EU will need to be robust in order to handle the planned intercontinental increase in capacity.

We note the limited capacity growth on the Europe to North America route in H1 and believe that this may more closely match demand (assuming that the US continues to show low-single-digit GDP growth).

Intercontinental European capacity in 2011 was 12% above the 2008 peak

From SRS Analyser database, it is clear that intra-European capacity is favourable. On long haul, inbound demand needs to be strong to fill planned capacity.

Figure 1: Regional capacity data (millon seats)

-

200

400

600

800

1,000

1,200

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Within EU To/From EU USA domestic

Source: OAG; Davy

Figure 2: December European intercontinental capacity trends (millon seats)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011USA/Canada to from Western Europe Western Europe to/from Asia PacificWestern Europe to/from Middle East

Source: OAG; Davy

Research Report: Davy on Airlines January 19, 2012

8 Davy Research

Figure 3: Capacity growth by market – Q1 2012

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Europe tooutside Europe

Europe toAfrica

Europe to Asia Intra-Europe Europe toMiddle East

Europe to N.America

Europe to S.America

Current analysis From September Davy on Airlines Source: SRS Analyser; Davy

Figure 4: Capacity growth by market – Q2 2012

0%

2%

4%

6%

8%

10%

12%

Europe tooutside Europe

Europe to Africa Europe to Asia Intra-Europe Europe toMiddle East

Europe to N.America

Europe to S.America

Source: SRS Analyser; Davy

Research Report: Davy on Airlines January 19, 2012

9 Davy Research

Early indicators signal upcoming weakness in premium traffic; potential significant impact on earnings

In previous downturns, freight and manufacturing PMIs were leading indicators of premium volume. Both of these are showing negative trends, which suggests that premium traffic will soon turn negative. Using reported historical data, we estimate the potential impact of changes in premium traffic volumes on the operating profit of the three network airlines.

Table 7: Impact of premium traffic volume changes on Lufthansa's operating profit

Premium traffic volume Operating profit (2012) Δ from base case

5% 781 32%

1% 633 7%

Base case 593 0%

-1% 555 -6%

-5% 407 -31%

Source: Davy

Leading indicators suggest premium weakness

Leading indicators suggest premium weakness

Impact of declining premium volumes would be large

Figure 5: Manufacturing PMI suggests premium declines

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Apr

07

Aug

07

Dec

07

Apr

08

Aug

08

Dec

08

Apr

09

Aug

09

Dec

09

Apr

10

Aug

10

Dec

10

Apr

11

Aug

11

30

35

40

45

50

55

60

65

Premium volumes (IATA) JP Morgan Global Manufacturing PMI [50= No change] (rhs)

6 month lag between PMI >50 and growth in premium volumes

c. 3 month lag between PMI <50 and decline in premium volumes

October 49.9 November 49.7December 50.8

Source: IATA; Davy

Figure 6: Air freight suggests premium declines

-30%

-20%

-10%

0%

10%

20%

30%

40%

Apr

07

Aug

07

Dec

07

Apr

08

Aug

08

Dec

08

Apr

09

Aug

09

Dec

09

Apr

10

Aug

10

Dec

10

Apr

11

Aug

11

Premium volumes (yoy) Freight (yoy)

c. 3 month lag between air freight turning

negative and decline in premium volumes

c. 2 month lag between air freight turning positive and increase in premium

volumes

Air freight has been negative since May

Source: IATA; Davy

Table 5: Impact of premium traffic volume changes on Air France-KLM's operating profit

Premium traffic volume

Operating profit (2012)

Δ from base case

5% -319 34%

1% -448 8%

Base case -485 0%

-1% -522 -8%

-5% -651 -34%

Source: Davy

Table 6: Impact of premium traffic volume changes on IAG's operating profit

Premium traffic volume

Operating profit (2012) Δ from base case

5% 434 47%

1% 324 9%

Base case 296 0%

-1% 267 -10%

-5% 146 -51%

Source: Davy

Research Report: Davy on Airlines January 19, 2012

10 Davy Research

International Air Transport Association (IATA) remains cautious

In early December, industry body IATA revised down its 2012 industry outlook. For 2011, profitability remains weak but unchanged at $6.9bn for a net margin of 1.2%. Looking ahead to 2012, IATA downgraded its central forecast for airline profits from $4.9bn to $3.5bn for a net margin of 0.6%. It also provides a downside case in the event of a second banking crisis with losses of $8.3bn. Its central view is that both passenger and cargo yields will remain flat in 2012. Its fuel assumption is $99 per barrel. European carriers are expected to deliver losses of $600m, hit by the weakness of their home market economies and further increases in passenger taxes. IATA indicates that historically the airline industry has seen profit turn into loss whenever global GDP growth falls below 2%. IATA forecasts are shown in Appendix 7. The IATA forecasts by region and traffic assumptions showing supply exceeding demand are provided in the following tables.

Table 8: IATA forecasts by region

EBIT margin % revenues Net profits

Industry profits (US$bn) 2007 2008 2009 2010 2011F 2012F 2012F* 2007 2008 2009 2010 2011F 2012F 2012F*

Global 3.9 -1.6 0.4 4 2.2 1.4 0.5 14.7 -16 -4.6 15.8 6.9 3.5 -8.3

Regions

North America 5.5 -1.8 1.2 4.7 3.2 2.4 0.3 5.5 -9.6 -2.7 4.1 2 1.7 -1.8

Europe 4 0.1 -2.2 1.9 1.2 0.3 -1.7 6.4 0 -4.3 1.9 1 -0.6 -4.4

Asia-Pacific 2.9 -4.7 2.8 6 2.4 2.1 0.2 3 -4.7 2.6 8 3.3 2.1 -1.1

Middle East 0 1 -1.5 3.6 2 1.6 -0.4 -0.1 -0.3 -0.6 0.9 0.4 0.3 -0.4

Latin America 2 2.3 2.8 5 2 1.8 -0.1 0.1 -1.4 0.5 0.9 0.2 0.1 -0.4

Africa 1 -0.9 -1.2 1.6 0.8 0.3 -0.6 -0.2 -0.1 -0.1 0.1 0 -0.1 -0.2

* Banking crisis Source: Davy; IATA

Table 9: IATA forecasts – traffic volumes and capacity

Traffic volumes Capacity

Annual average growth rates %

2006 2007 2008 2009 2010 2011F 2012F 2012F* 2006 2007 2008 2009 2010 2011F 2012F 2012F*

Global 5.3 6 0.7 -4.3 10.4 4.2 2.9 -1.3 4.1 5.8 1.1 -3.5 5.2 6 3.1 0

Regions

North America 2.7 3.5 -2.4 -6.3 9.9 2 2.2 -1 0.5 3.2 -2.8 -5.6 3.9 3.4 2 -0.5

Europe 4.9 2.1 0.9 -7.7 5 7.5 2.5 -3.7 3.9 3.5 2.9 -5.4 1.5 9.2 2.9 -0.1

Asia-Pacific 7.5 7.8 -0.2 -2.2 12.6 2.1 2 -0.2 6.7 6.9 0.6 -4.8 5.8 4.6 2.9 0.1

Middle East 11.8 16.4 3.6 9.5 20 7.9 5.7 4.5 12.6 14.5 4.7 11.1 15.8 10.8 5.8 4.8

Latin America -3.4 9.9 3.3 0 14.5 10.6 8.5 2.3 1.6 6.9 3.2 1.4 9.6 8 8.3 3.3

Africa 7 4.5 5.1 -5.4 15 0.8 3.5 0.3 1.8 5.8 7.2 -1.5 9.5 2.9 3.7 0.7

* Banking crisis Source: Davy; IATA

IATA is pointing to softer profits with margins wafer thin

IATA indicates that historically the

airline industry has seen profit turn into loss whenever global GDP growth falls below 2%

Research Report: Davy on Airlines January 19, 2012

11 Davy Research

It is clear from the IATA data that passenger and freight volumes have dropped. Freight markets have contracted some 4% compared to January. Although passenger markets have shown some growth relative to the start of 2011 – about 2% – the trend has been soft and volatile. Further passenger loads have fallen, showing that passenger demand is outpacing airlines' ability to adjust capacity accordingly. In terms of premium traffic, it declined substantially in October – consistent with weaker trade and confidence indicators.

It is clear from the IATA data that passenger and freight volumes have dropped

Figure 7: Premium/economy traffic growth

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

Nov-06 May-07 Nov-07 May-08 Nov-08 May-09 Nov-09 May-10 Nov-10 May-11 Nov-11

% g

row

th y

oy

First/Business Economy Source: Davy; IATA

Figure 8: Passenger/freight traffic

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Jan-03 Sep-03 May-04 Jan-05 Sep-05 May-06 Jan-07 Sep-07 May-08 Jan-09 Sep-09 May-10 Jan-11 Sep-11

Passenger Traffic growth (yoy) Freight growth (yoy)

Freight growth consistently negative

SARS impact

Still growth in passenger nos

Impact of volcanic ash

Source: Davy; IATA

Research Report: Davy on Airlines January 19, 2012

12 Davy Research

Rise in uncontrollable costs will prove challenging for network airlines Airlines face many uncontrollable cost increases (fuel, the APD and the EU ETS). Through various initiatives, the LCCs have demonstrated an ability to pay for higher fuel costs in weaker economic conditions. On the other hand, the network airlines are slower to adjust capacity and face significant challenges this year. Through fuel surcharges, the network airlines try to pass through fuel price increases; however, this only works in a robust economic environment. It appears that we are currently experiencing the twin evils of a weaker economic environment and stubbornly high oil prices. In particular, we feel that the combination of the APD and the EU ETS will make it very difficult for IAG to continue to increase yields to recoup the increase in fuel costs.

Fuel remains stubbornly high, even as network airlines' operating profit declines

Fuel prices remain stubbornly high in euro and sterling terms. This could prove very challenging for the network airlines. As hedges roll over, we estimate that there will still be double-digit percentage unit fuel increases for most of the airlines. This could squeeze network airlines' profits for perhaps a more prolonged period of time than during the 2008/2009 cycle. However, the impact on profits is likely to be less severe if supply is corrected.

Table 10: FY 2012 unit fuel cost increase (yoy)

Aer Lingus 13%

Air France-KLM 9%

IAG 14%

Lufthansa 11%

easyJet 19%

Ryanair 10%

Source: Davy

Profits could be squeezed for longer than during the 2008/2009 cycle for the network airlines

Figure 9: Jet kerosene ($) per metric tonne

600

700

800

900

1000

1100

1200

Dec 2009 Mar 2010 Jun 2010 Sep 2010 Dec 2010 Mar 2011 Jun 2011 Sep 2011 Dec 2011

-10%

Source: Davy; Bloomberg

Figure 10: Jet kerosene (£) per metric tonne

375

425

475

525

575

625

675

725

Dec 2009 Mar 2010 Jun 2010 Sep 2010 Dec 2010 Mar 2011 Jun 2011 Sep 2011 Dec 2011

-4%

Source: Davy; Bloomberg

Research Report: Davy on Airlines January 19, 2012

13 Davy Research

During the 2008/2009 economic downturn, the airline industry was helped significantly by the rapid decrease in the price of fuel. Brent crude peaked at $145/barrel on July 14th 2008 and was trading in the mid-$60-70 range by December. In contrast, there has not been any significant decrease in oil prices over the last couple of months. This implies that there could be a very significant impact on operating profits. As the network airlines continue to try to pass on the cost of fuel, the elasticity of demand will likely be reached and load factors or yield will fall (as has been seen in previous cycles). In the last cycle, fuel prices had already begun to fall, placing only a temporary squeeze on airlines' operating profit; this time, however, fuel is not falling. On top of this, the airlines also have to pass on APD and EU ETS costs. Early indicators already point to deteriorating premium traffic and intercontinental economy volume growth. The operating profits of the network airlines started to decline in Q3 relative to the previous year (Q3 IAG -31%, Lufthansa -27%, Air France-KLM -31%). We have seen falling volumes and declines in load factors (see below). Although supply is adjusting somewhat to suppressed demand, it is difficult to envisage a scenario in which the networks have pricing power.

Adding new capacity in a lower demand environment limits pricing power and the ability to pass on higher costs such as fuel

Figure 11: Jet kerosene (€) per metric tonne

375

425

475

525

575

625

675

725

775

825

875

Dec 2009 Mar 2010 Jun 2010 Sep 2010 Dec 2010 Mar 2011 Jun 2011 Sep 2011 Dec 2011

2%

Source: Davy; Bloomberg

Figure 12: Rebased currency impact on jet kerosene

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

Dec 09 Mar 10 Jun 10 Sep 10 Dec 10 Mar 11 Jun 11 Sep 11 Dec 11

Jet Kerosene pmt ($) Jet Kerosense pmt (€) Jet Kerosense pmt (£ ) Source: Davy; Bloomberg

Research Report: Davy on Airlines January 19, 2012

14 Davy Research

Figure 13: Association of European Airlines – supply versus demand

-20

-10

0

10

20

30

2004 2005 2006 2007 2008 2009 2010 2011

Demand exceeding supply

Supply adjusting to suppressed demand

Source: Association of European Airlines; Davy

During the 2008/2009 cycle, oil eventually decreased, offering some relief. However, this has not occurred in the current scenario, placing continued pressure on the network airlines' profits. The network airlines may lose a year (perhaps even longer) in paying for oil in this economic environment.

Figure 14: In the last oil spike, sustained yield increase by BA had a toll on load factor

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Q1 2007 Q3 2007 Q1 2008 Q3 2008 Q1 2009 Q3 2009 Q1 2010 Q3 2010

-5

-4

-3

-2

-1

0

1

2

3

Yield (lfs) Change in load factor (rhs)

• Sustained yield increases begins• Load factor starts to drop• Brent crude makes a sustained break above $100/bbl

Source: Davy; BA

Figure 15: In the last oil spike, sustained yield increase by Air France-KLM had a toll on load factor

-3

-2

-1

0

1

2

3

4

Q4 2010Q2 2010Q4 2009Q2 2009Q4 2008Q2 2008Q4 2007Q2 2007

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Change in load factor (rhs) Yield (lhs)

LF 75.5%

Continued yield increases

Source: Davy; Air France-KLM

Research Report: Davy on Airlines January 19, 2012

15 Davy Research

Figure 18: BA operating income versus Brent

FY H2 2009FY H1 2009FY H2 2008FY H1 2008FY H2 2007FY H1 2007

0

20

40

60

80

100

120

140

BA (£, rhs) Brent Crude ($, lhs)

Source: Davy; Bloomberg

Figure 16: Air France-KLM operating income versus Brent

-100

0

100

200

300

400

500

600

700

800

Q3 2008Q2 2008Q1 2008Q4 2007Q3 2007Q2 2007Q1 2007Q4 2006Q3 2006Q2 2006

0

20

40

60

80

100

120

140

160

AF KL M Op income (€, rhs ) Brent Crude ($, lhs )

Source: Davy; Bloomberg

Figure 17: Lufthansa operating income versus Brent

0

100

200

300

400

500

600

Q3 2008Q2 2008Q1 2008Q4 2007Q3 2007Q2 2007Q1 2007Q4 2006Q3 2006Q2 2006

0

20

40

60

80

100

120

140

160

L ufthansa Op income (€, rhs ) B rent Crude ($, lhs )

Source: Davy; Bloomberg

Research Report: Davy on Airlines January 19, 2012

16 Davy Research

Effects of the UK APD

The UK APD is due to increase as of April 2012 (rates shown below). Assuming that demand levels stay constant, we have estimated the potential gains airlines could have made if, instead of the tax increase, they had increased yields by the same amount. We have performed this analysis on the airlines that have a significant proportion of their overall passengers departing from the UK.

Table 11: Increase in UK APD

Miles from UK Reduced rate (in lowest class of travel)*

Standard rate (in other than lowest class of travel)*

Band A (0-2000) £12 (£13) £24 (£26)

Band B (2001-4000) £60 (£65) £120 (£130)

Band C (4001-6000) £75 (£82) £150 (£164)

Band D (over 6000) £85 (£93) £170 (£186)

*Bracketed rates apply from April 2012 Source: HM Treasury

IAG is the airline that is most significantly affected by the increase in APD due to the proportion of its passengers that fly standard (i.e. premium) and the proportion of its passengers that fly long haul. Obviously, Ryanair and easyJet are only short-haul, low-cost economy.

Table 12: Impact of UK APD on airlines' profits – full-year run rate

Impact of APD increase 2012 (£m) As a proportion of FY2012E earnings

Ryanair 23.0 6%

easyJet 24.6 15%

IAG 52.5 40%

Source: Davy; company reports; HM Treasury

EU ETS has greater impact on the network airlines

The aviation industry has been included in the EU ETS as of 2012, having to surrender allowances for 2012 carbon emissions by April 2013. Any emissions in excess of the allotted carbon allowances can be purchased in the open market. IATA estimates that the annual industry-wide cost of the ETS will be c.€900m this year and will rise to €2.8bn by 2020. Based on company comments, estimates of the impact on the airlines under coverage are provided below. In order to recoup any of this cost, many airlines are adding surcharges.

Ryanair announced the introduction of a €0.25 levy to cover the cost of the carbon permits needed.

Lufthansa has said that it will add the costs of the EU ETS to its existing fuel surcharges. It will need to buy c.35% of permits in 2012 from the market.

Delta, American Airlines and US Airways have all added a $3 surcharge each way on flights between Europe and the US.

Networks will bear the brunt of tax increases

Table 13: EU ETS cost

easyJet £10.5m

IAG €90m

Lufthansa €130m

Ryanair €19m

Source: Davy; company reports

Research Report: Davy on Airlines January 19, 2012

17 Davy Research

Second wave of consolidation should benefit specific players We believe that a second wave of consolidation is underway as revenue pressure resumes (this aspect is dealt with in more detail later in this report in our discussion of each airline). Greater consolidation is part of the wider theme that necessitates the need for industry right-sizing in order to safeguard profitability. If IAG receives regulatory approval to purchase bmi with its 56

Heathrow slots, it will increase its dominant position from the current c.44% control of Heathrow slots to c.53%. As stated in our previous issue of Davy on Airlines ("Virtual airline mergers; implications of the consolidation of the North Atlantic", issued October 4th 2011), hub dominance is a long-term positive.

Etihad has taken a 29.2% equity stake in Air Berlin, which gives Etihad increased access to European airports (most notably German airports, which currently have restricted access). The deal gives Etihad access through Air Berlin to Berlin, with rival Emirates restricted to the four German cities of Hamburg, Frankfurt, Munich and Dusseldorf (Emirates has been pushing for landing slots in Berlin and Stuttgart).

Given the tough operating environment, further consolidation in the form of strategic partnerships or take-out could occur. Potential targets are Aer Lingus and TAP.

The CDS spreads for European airlines below (notably SAS) imply some form of further consolidation.

More consolidation is part of the wider theme that necessitates the need for industry right-sizing in order to safeguard profitability

Figure 19: Airlines CDS spreads

0

200

400

600

800

1000

1200

1400

1600

1800

Jan 10 Apr 10 Jul 10 Oct 10 Jan 11 Apr 11 Jul 11 Oct 11

SAS Societe Air France Lufthansa British Airways

Source: Davy; Bloomberg

Research Report: Davy on Airlines January 19, 2012

18 Davy Research

Middle East airlines moving into Europe

The recent move by Etihad to take a 29.2% stake in Air Berlin shows that Middle Eastern airlines continue to find ways into Europe. The Middle Eastern Airlines, dubbed by some the 'Super Connectors', have a business model that focuses on using new, large, lower unit-cost aircraft to service connecting traffic via the Middle East. This can make sense for European traffic heading to the East, especially to South East Asia. The Middle Eastern hubs will act as a gateway to Asia, the Middle East, the Indian subcontinent and Australia.

Figure 20: Etihad and Air Berlin route map

Source: SRS Analyser; Davy *Legend: Light grey is Air Berlin; dark grey is Etihad

The Middle Eastern Airlines have thus far placed a significant number of routes into Europe in order to capture transfer traffic. For example, Emirates recently launched a daily service to Dublin. Qatar, Etihad and Emirates fly over 640 operations per week from Western Europe to the Middle East, including 120 services per week from Germany.

Figure 21: Routes by Qatar, Emirates and Etihad to Western Europe

Source: SRS Analyser

Research Report: Davy on Airlines January 19, 2012

19 Davy Research

Qatar, Etihad and Emirates have very strong order books for wide-body aircraft, which will likely lead to a trebling of their fleet size. We would expect this to continue to put pressure on the European network airlines' routes to the East. When the orders are delivered, this will result in a fleet size that is 30% larger than the estimated wide-body fleet size of the three major European network airlines combined.

Middle Eastern airlines' fleet size is likely to triple in size and could be at least 30% larger than the European network fleet size

Table 14: Boeing aircraft for airlines in Middle East

Order In service Options

777 787 747 777 747 777 787 747

Emirates 92 5 94 9 20 0 10

Qatar 14 30 0 28 0 1 30 0

Etihad 12 41 0 8 0 7 25 0

Total 118 71 5 130 9 28 55 10

Source: Davy; Bloomberg; company

Table 15: Airbus aircraft for airlines in Middle East

Airbus Order In service Options

A380 A350 A380 A340 A330 A300 A380 A350

Qatar 10 80 0 4 29 3 3 0

Emirates 72 70 16 18 27 0 0 20

Etihad 10 25 0 11 22 2 5 10

Total 92 175 16 33 78 5 8 30

Source: Davy; Bloomberg; company

Research Report: Davy on Airlines January 19, 2012

20 Davy Research

Stock views Valuations are low but earnings at risk for networks; LCCs remain attractive

While we look at absolute and relative valuations for the airlines, earnings momentum remains key. As we have already outlined, we still see this as vulnerable for the networks. Our price targets and ratings are provided in Table 18. We examine various valuation methodologies, including DCF valuation, forward P/E, EV/EBITDAR and replacement value for the LCCs and forward EV/EBITDAR, P/E, replacement value and SOTP for the networks. In some cases, given the macro uncertainty, we apply discounts to our price targets. Our over-riding view is that the LCCs are sector relative outperformers and that the networks are sector relative underperformers. We believe the networks will continue to struggle in the current macro environment. However, it is worth pointing out that the leading networks (particularly IAG and Air France-KLM) have multiple upside over the medium term if and when they deliver on their business plans in a more favourable macro environment.

Table 16: Network peer comparison (€m)

Aer Lingus Air France-KLM IAG Lufthansa

2011 2012 2013 2011 2012 2013 2011 2012 2013 2011 2012 2013

Market cap 338.9 338.9 338.9 1344.3 1344.3 1344.3 3511.9 3511.9 3511.9 4383.5 4383.5 4383.5

Net balance sheet debt -376.3 -486.4 -557.9 6549.6 6758.9 6483.4 860.2 1291.4 2017.8 1517.3 1778.5 1860.7

Off-balance sheet 349.0 357.9 367.0 5895.7 6072.6 6254.7 2793.0 2876.8 2963.1 1396.4 1382.4 1368.6

Pension liability 0.0 0.0 0.0 0 0 0 2976.2 2777.8 2579.4 2371.0 2389.2 2189.2

Adjusted EV 311.6 210.4 148.0 13789.7 13975.8 14132.4 10341.3 10657.9 11272.1 9668.2 9933.5 9802.0

Revenue 1298.0 1362.2 1398.5 24325.3 25116.6 26207.3 16426.6 17356.0 18247.8 29562.8 30829.1 32543.4

EBITDAR 184.9 203.0 216.7 2150.5 2043.7 2653.2 1877.5 1756.8 1952.5 2565.6 2473.6 2647.5

P/E 7.8 6.0 5.0 -1.8 -2.1 -6.3 10.6 24.7 16.4 11.0 17.0 11.2

EV/sales 0.2 0.2 0.1 0.6 0.6 0.5 0.6 0.6 0.6 0.3 0.3 0.3

EV/EBITDAR 1.7 1.0 0.7 6.4 6.8 5.3 5.5 `6.1 5.8 3.8 4.0 3.7

Price/book 0.4 0.4 0.4 0.2 0.2 0.2 0.7 0.7 0.7 0.5 0.5 0.4

Net debt/EBITDAR -0.15 -0.63 -0.88 5.8 6.3 4.8 1.9 2.4 2.6 1.1 1.3 1.2

Net debt/capital -2.9% -14.3% -21.1% 52.0% 53.9% 54.1% 31.1% 34.1% 38.1% 16.0% 17.1% 17.3%

Free cash flow 56.0 110.1 71.5 -488.6 -209.3 275.5 34.8 -431.2 -726.3 78.7 -261.1 -82.3

Source: Davy

Stocks' ranking of preference LCCs (Ryanair and easyJet) preferred

Aer Lingus – very cheap but still waiting for value crystallisation

Lufthansa – exposed but low valuation and good balance sheet

IAG – sound strategy but big 2012 headwinds

Air France-KLM – strained balance sheet

Our over-riding view is that the LCCs are sector relative outperformers and that the networks are sector relative underperformers

Research Report: Davy on Airlines January 19, 2012

21 Davy Research

Table 17: LCC peer comparison

easyJet (£m) Ryanair (€m)

2011 2012 2013 2011 2012 2013

Market cap 1732 1732 1732 5713.6 5713.6 5713.6

Net balance sheet debt -100.0 113.2 77.6 150.0 -540.1 -1430.4

Off-balance sheet 763 571.2 591.528 616.9 601.0 534.4

Pension liability 0.0 0.0 0.0 0.0 0.0 0.0

Adjusted EV 2395.3 2416.7 2401.4 6366.5 5660.5 4703.6

Revenue 3452.0 3780.5 4009.8 4274.1 4680.1 5068.5

EBITDAR 468.0 424.8 449.6 996.7 993.8 1063.6

P/E 7.8 10.7 9.7 12.3 12.1 10.3

EV/sales 0.7 0.6 0.6 1.5 1.2 0.9

EV/EBITDAR 5.1 5.7 5.3 6.4 5.7 4.4

Price/book 1.0 1.0 1.0 1.7 1.5 1.3

Net debt/EBITDAR 1.4 1.6 1.5 0.8 0.1 -0.8

Net debt/capital 23.6% 24.4% 22.8% 16.2% 1.3% -21.8%

Free cash flow -57.0 -213.2 35.6 558.8 690.1 890.4

Source: Davy

Table 18: Ratings and price targets

Rating Price target

Airline Old New Old New

Aer Lingus Outperform Neutral €1.00 €0.75

Air France-KLM Neutral Underperform €7 €3.8

easyJet Outperform Outperform £4.75 £4.75

IAG Neutral Underperform 230c/200p 140c/115p

Lufthansa Neutral Neutral €12 €9

Ryanair Outperform Outperform €4.5 €5.0

Source: Davy

Table 19: Valuation methods and price targets

easyJet (£) Ryanair (€) Aer Lingus (€) Lufthansa (€) Air France-KLM (€) IAG (€)

DCF 4.1 5.4 - - - -

Forward P/E/mid cycle 5.0 4.5 - - - 1.27

EV/EBITDAR 4 5.0 1.4 9.2 - 1.60

Replacement value 5.9 3.5 1.8 7.2 5.3 0.7

SOTP - - - 11.6 - -

Current stock price 4.04 3.87 0.64 9.6 4.5 1.89

Undiscounted stock price 4.73 4.60 1.50 9.3 n/a 1.43

Discount for economic/ pension/liquidity uncertainty

0.0% 0.0% 50.0% 0.0% n/a 5.0%

Price target 4.75 5.0 0.75 9.0 3.8 1.4

% change 18% 29% 17% -6% -16% -26%

Source: Davy

Research Report: Davy on Airlines January 19, 2012

22 Davy Research

Table 20: 2012 EV/EBITDAR

Valuation multiples 2012 (£/€) Ryanair easyJet IAG Air France KLM

Lufthansa Aer Lingus

EBITDAR 993.8 424.8 1757 2043.7 2474 203.0

Multiple 7.5 6 5.5 4.0 4.0 3.0

Enterprise value 7454 2549 9662 8175 9894 609

Deduct adjusted net debt 60.9 684.4 4168 12831 3160.9 -128.5

Deduct pension liability 0 0 2778 0 2389.2 0

Minorities 0 0 0 0 0 0

Add investments 103 0 483 853 668 0

Market value 7496 1864 3200 -3804 5013 737

Shares (m) 1480.2 433 2051 300 460.5 530

Per share value 5.06 4.31 1.56 n/a 10.89 1.39

Current price 3.87 4.04 1.89 4.50 9.6 0.64

Current EV/EBITDAR multiple 6.4 5.7 6.1 6.8 4.0 1.01

Source: Davy

The following scatter graphs for our 2012 numbers clearly show the LCCs at a valuation premium. However, the operating and financial positions are superior and in most cases justify an even higher premium. Earnings momentum remains positive for the LCCs and negative for the networks.

LCCs' operating and financial positions are superior and in most cases justify an even higher premium

Figure 22: EV/EBITDAR compared to EBITDAR margins

Ryanair

Ryanair ex potential div

easyJet

easyJet ex special div

Lufthansa

Air France KLMIAG

Aer LingusAverage

0%

5%

10%

15%

20%

25%

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

EV/EBITDAR 2012E

EBIT

DA

R m

argi

n 20

12E

Favourable

Unfavourable

Source: Davy

Figure 23: EV/IC compared to ROIC

Average

Aer Lingus

IAG

Air France KLM

Lufthansa

easyJet ex special div

easyJet

Ryanair ex potential div

Ryanair

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4

EV/IC 2012F

ROIC

201

2F

Favourable

Unfavourable

Source: Davy

Research Report: Davy on Airlines January 19, 2012

23 Davy Research

We examine each of the airlines separately in the pages that follow.

Figure 24: Price/book compared to ROE

RyanairRyanair ex potential

diveasyJeteasyJet ex special

div

Lufthansa

Air France KLM

IAG

Aer Lingus

Average

-15%

-10%

-5%

0%

5%

10%

15%

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

Price/Book 2012F

ROE

2012

F

Favourable

Unfavourable

Source: Davy

Figure 25: Operating margin compared to EV/Sales

RyanairRyanair ex potential

div

easyJeteasyJet ex special div

Lufthansa

Air France KLM

IAG

Aer Lingus Average

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4EV/Sales 2012F

Op

Mar

gin

2012

F

Favourable

Unfavourable

Source: Davy

Research Report: Davy on Airlines January 19, 2012

24 Davy Research

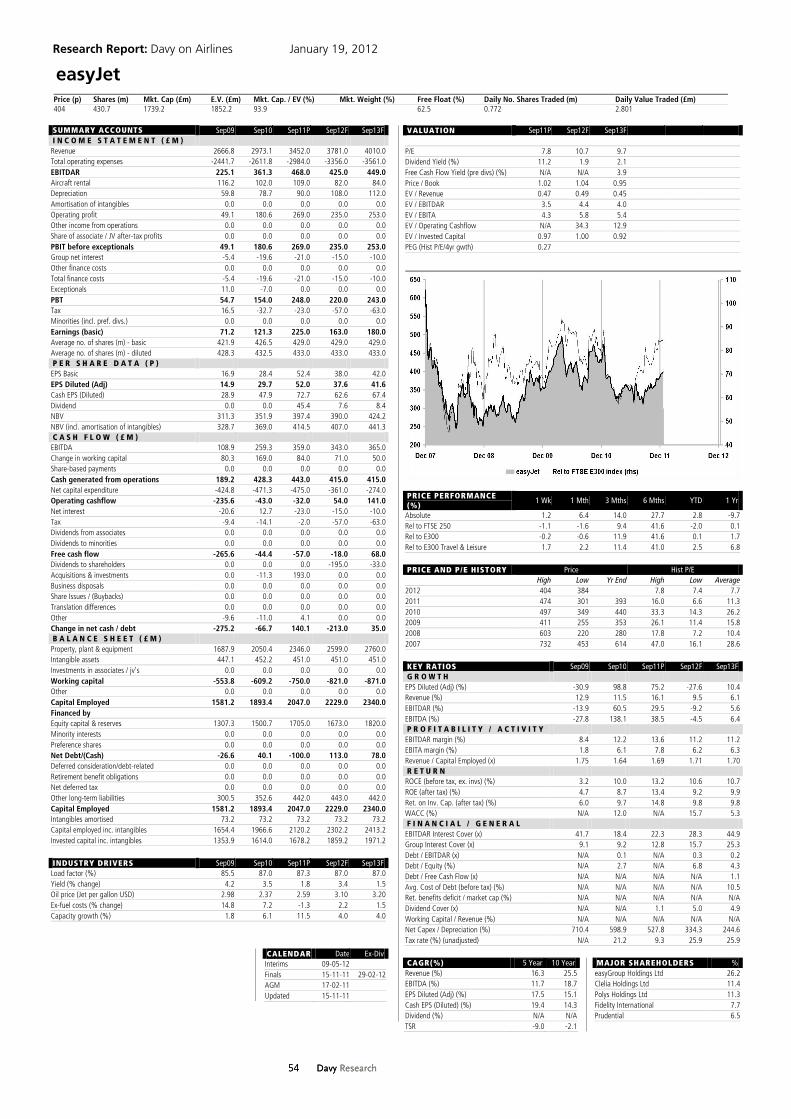

easyJet – special dividends and business focus

Next catalyst – Q1 IMS January 26th; capital markets day January 31st While easyJet has some cost headwinds into 2012, we see it as a sector outperformer due to the following factors: wasyJet generates £400m in free cash flow (pre-capex). As capex slows,

we believe that this will be returned to shareholders in the form of special dividends similar to the £150m being paid in March 2012. Taken together with the ordinary dividend, total cash returns of £195m or 45.4p per share will be paid on March 23rd 2012 to those shareholders on the register at the close of business on March 2nd with an ex-dividend date of February 29th.

Slower capacity growth has the added benefit of allowing more active management of fares. This will help to offset increasing costs, enhancing margins and returns. Capacity for the first half of the year will be flat with growth of around 4% for the full year. The Q1 IMS statement should be helped by easy comparables – there was double- digit growth in capacity last winter with significant capacity investments (e.g. +32% in France). The CEO has bedded down strategy and has implemented fee and charges increases. Ancillary revenues should grow significantly for the next three quarters.

easyJet is well placed to attract business and consumer traffic down-trading from network airlines in a difficult environment. Its business offering is enhanced by the launch of its 'Flexi-fare' product. easyJet's goal is to drive an additional contribution of £100m from passengers travelling on business through delivering improvements in product and distribution. Yields could be helped with even limited penetration in 'Flexi-fares'. Yields should also be aided by the fact that 84% of easyJet's airports are slot constrained, e.g. Milan, Paris, Gatwick, Geneva, Lisbon.

Table 21: Potential flexi-fare penetration

Flexi-fare penetration 0% 0.5% 1.0% 1.5% 2.0% 5.0% 10.0%

Average fare (£) 50 50.8 51.5 52.3 53 57.5 65

Increase from base fare 0.0% 1.5% 3.0% 4.5% 6.0% 15.0% 30.0%

Absolute incremental (£m) 0 42 84 126 168 420 840

Source: Davy

The capital markets day will allow members of easyJet's senior management team to present the group's strategy overview and implementation. Recent results from easyJet have been positive, with higher unit revenue helped by the maturing of capacity investments and the optimisation of fees and charges offsetting unit cost rises. For FY2011, ROCE at 12.7% was above its medium-term target.

easyJet positive catalysts

Cash returns – 11.5% dividend yield paid in March

CEO embedded strategy to illustrate at capital markets day

Higher fees and charges leading to strong ancillaries

Flat capacity – easy Q1 comps

Potential business traffic revenue kicker

Research Report: Davy on Airlines January 19, 2012

25 Davy Research

easyJet's last comment in November indicated that forward bookings were in line with last year and that 45% of winter seats were booked; first-half unit revenue per seat at constant currency is expected to be up by mid-single-digits. Costs per seat are expected to grow 2-3% for the full year and by 4% in H1, driven by price increases at regulated airports (costs creep is something to watch out for at easyJet) and investments in new revenue streams. The fuel headwind is £220m (currently marking to market, this may be c.£4m higher). The Q1 load performance continues to be very positive – the December number (stripping out weather) was one percentage point above that of last year. We expect easyJet to be positive on the revenue front for FY2012, albeit H1 is loss-making (we assume £219.2m) and H2 profitable (we assume £439.2m). Cost comps leave FY2012 PBT slightly below last year (£220.2m versus £248m). A strong winter implies upward bias for forecasts, albeit the summer will be key to easyJet's forecasts. We continue to rate easyJet 'outperform' with a £4.75 price target, supported by its special dividend, and trading at two-thirds of its replacement value.

Figure 26: easyJet profit bridge

0

50

100

150

200

250

300

350

400

450

FY 11 PBT Unit costs Vol/ yield uplift Ancillary EU ETS Fuel costs FY12 PBT Consensus

£248m -£47m

£100m

£105m -£10.5m -£176.5m

£220m £213m

Source: Davy

Research Report: Davy on Airlines January 19, 2012

26 Davy Research

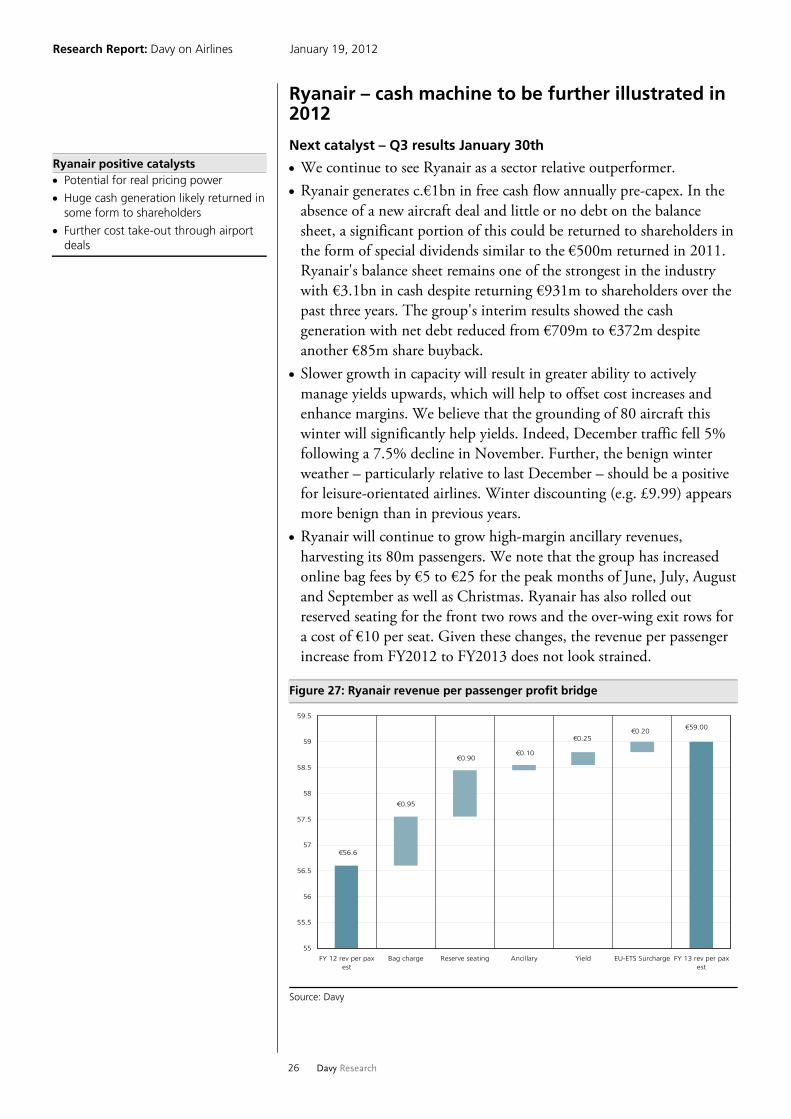

Ryanair – cash machine to be further illustrated in 2012

Next catalyst – Q3 results January 30th

We continue to see Ryanair as a sector relative outperformer. Ryanair generates c.€1bn in free cash flow annually pre-capex. In the

absence of a new aircraft deal and little or no debt on the balance sheet, a significant portion of this could be returned to shareholders in the form of special dividends similar to the €500m returned in 2011. Ryanair's balance sheet remains one of the strongest in the industry with €3.1bn in cash despite returning €931m to shareholders over the past three years. The group's interim results showed the cash generation with net debt reduced from €709m to €372m despite another €85m share buyback.

Slower growth in capacity will result in greater ability to actively manage yields upwards, which will help to offset cost increases and enhance margins. We believe that the grounding of 80 aircraft this winter will significantly help yields. Indeed, December traffic fell 5% following a 7.5% decline in November. Further, the benign winter weather – particularly relative to last December – should be a positive for leisure-orientated airlines. Winter discounting (e.g. £9.99) appears more benign than in previous years.

Ryanair will continue to grow high-margin ancillary revenues, harvesting its 80m passengers. We note that the group has increased online bag fees by €5 to €25 for the peak months of June, July, August and September as well as Christmas. Ryanair has also rolled out reserved seating for the front two rows and the over-wing exit rows for a cost of €10 per seat. Given these changes, the revenue per passenger increase from FY2012 to FY2013 does not look strained.

Ryanair positive catalysts Potential for real pricing power

Huge cash generation likely returned in some form to shareholders

Further cost take-out through airport deals

Figure 27: Ryanair revenue per passenger profit bridge

55

55.5

56

56.5

57

57.5

58

58.5

59

59.5

FY 12 rev per paxest

Bag charge Reserve seating Ancillary Yield EU-ETS Surcharge FY 13 rev per paxest

€56.6

€0.95

€0.90€0.10

€0.25

€59.00€0.20

Source: Davy

Research Report: Davy on Airlines January 19, 2012

27 Davy Research

We see little aggressive discounting in short haul, which is not surprising given that Ryanair leads the market. Overall – based on the limited level of winter discounting, benign weather, trading down and capacity discipline – we are moving up our estimates by slightly over 5% from net income of €443m to €467m for FY2012, pushing up our FY2013 estimates by similar amounts to €473.9m (or 32c). This assumes yields approaching the c.16.5% yoy increases achieved in Q2. This would imply only very modest losses in Q3 (-€2.5m) and the loss in Q4 curtailed to c.€74m. Ryanair's market-leading position in the low-cost sector – it now has 50 bases – and its industry-leading low costs leave it very well placed. With the competitive environment very weak, airport opportunities are abundant — look for example at recent base deals at Wroclaw, Palma, Baden-Baden, Manchester, Billund and Paphos. These bases imply a strong level of revenue as we head into the summer schedule. The positive unit revenue performance shows the benefits of the Southwest-type model of slowing growth and rising unit revenue, even in a weak European economic environment. It has also delivered a stellar cost performance (unit costs ex-fuel, sector length adjusted flat in the last six months). Recent airport deals are likely to further illustrate the cost leadership of the business model. With a business whose DNA is built for a recession, we reiterate our 'outperform' rating. With positive earnings momentum, we are raising our price target to €5 (from €4.5).

We are moving up our estimates by slightly over 5% from net income of €443m to €467m for FY2012, pushing up our FY2013 estimates by similar amounts to €474.9m (or 32c)

We reiterate our 'outperform' rating and raise our price target to €5 (from €4.5)

Figure 28: Ryanair profit bridge

0

100

200

300

400

500

600

700

800

FY2012e netincome

Volume uplift Ancillaries Yield Fuel Unit costs FY2013e netincome

Consensus

€467m

€22m

-€160m€173m

-€61.2m

€474m

€34m

€472m

Source: Davy

Research Report: Davy on Airlines January 19, 2012

28 Davy Research

Aer Lingus – needs to break out from 'value trap' in 2012

Next catalyst – full-year results February 28th Aer Lingus has always looked cheap on valuation metrics but, for a variety of reasons (liquidity, economic, pensions), has failed to perform from a share price perspective. The Q3 results were strong, and Aer Lingus provided guidance that the full-year 2011 operating result (before exceptional items) would be at the upper end of the range of market expectations. At that time, we adjusted our FY results – raising operating profit upwards to €45m. Management indicated that it was too early to provide detailed guidance for 2012. It stated that the primary factors likely to influence trading performance are an expected slowdown in yield growth momentum, low-single-digit passenger volume increases and higher fuel costs. Two strategic issues discussed at the airline's investor day in September remain unresolved: the multi-employer pension deficit, which has clearly increased

significantly since the €400m actuarial deficit valuation in March; ownership structure. Management indicated that it is bound by the IPO prospectus on the former and therefore has no obligation to increase contributions – any change would require shareholder approval. The trustees continue to look for a solution. In relation to the shareholder structure, management continues to see a priority to expand the free float. We continue to believe that management has done an excellent job in repositioning the business as a network airline with a lower-cost structure. However, legacy issues – chief among which is the pension fund – will need to be resolved, but that should clear the path to potentially selling the government's 25% stake. The granting by the UK Court of Appeal of a stay on the investigation by the UK Office of Fair Trading into Ryanair's minority shareholding in Aer Lingus clearly delays any decision here. It is not clear whether there will be any trade buyer interest as the two leading candidates, IAG and Etihad (through investments in bmi and Air Berlin), appear to be looking elsewhere. A potential trade investor would almost certainly not take any pension deficit exposure and is likely to be largely interested in the transatlantic business and the Heathrow slots. We believe that restrictions on Heathrow slots should be removed, and we are in agreement with the Report of the Review Group on State Assets and Liabilities (April 2011) that "Heathrow slots would be deployed to their optimal use in the absence of restrictions" and "it is not plausible that Dublin-Heathrow would be under-served should slot allocation be left to market forces". Other global gateways such as Dubai are in many cases usurping Heathrow anyhow.

What Aer Lingus needs to do to break out from 'value trap' Remove pension risk as an issue

Increase liquidity

Use excess cash for special dividend

Consider strategic partnership

Research Report: Davy on Airlines January 19, 2012

29 Davy Research

We also note the passing in November of a resolution for a capital allocation – we believe some of Aer Lingus' excess cash should be used for special dividends. We do not see the Aer Lingus shares outperforming without a resolution of the pension issue and are sceptical of it gaining a trade buyer in 2012. Pending more clarity on both of these issues, we reduce our rating to 'neutral' and our price target to €0.75. The catalyst for a change in the airline's rating would be news on liquidity, a trade buyer and pension and/or dividend payments. There is value in Aer Lingus, but a logjam has to be cleared in order to crystallise this value.

We reduce our rating to 'neutral' and our price target to €0.75

Figure 29: Aer Lingus profit bridge

0

10

20

30

40

50

60

70

FY2011e opresult

Unit costs Greenfield Fuel Underlyingyield / vol

Ancillary FY2012e opresult

Consensus

€45m

€17m

-€6m

€-37m

€26m€44m

€17m €62m

Source: Davy

Research Report: Davy on Airlines January 19, 2012

30 Davy Research

IAG – constrained by capex and cash flow

Next catalyst – full-year results February 29th We have short-term concerns regarding IAG and see it as a sector underperformer in the current environment. We are changing its rating from 'neutral' to 'underperform' for the following reasons: IAG has c.10% premium traffic (c.45% of passenger revenue). This is

clearly exposed to any downturn. Premium traffic tends to lag business confidence (PMIs) by three to six months. The gap between its premium and non-premium volumes continues to narrow. Of its corporate contracted revenue, banking, professional and other services (e.g. telcos) represents 63%. These sectors are under pressure.

On the transatlantic, where it leads and has 31% of its traffic exposure, the majority point-of-sale is Europe (55% of long-haul point-of-sale is UK/Spain/rest of Europe). Further, IAG's North American partner in the revenue-sharing joint venture is in bankruptcy. While the American bankruptcy will not have any direct financial effects and should result in a leaner airline, consumer sentiment is unlikely to be positive.

We believe the increase in UK APD, which is due to occur in April 2012, should have a significant impact on IAG and make it more difficult to recoup fuel costs. We estimate that the APD increase will account for c.40% of FY2012 profits (if the tax was instead a yield increase, it would raise profits by c.40%).

Further earnings pressure could come from industrial relations problems in Iberia (pilots are out of contract and there were two strikes over the Christmas period and more in January related to the creation of Iberia Express).

Potential acquisitions such as bmi will take time to embed and enhance value. In Latin America, the creation of LATAM (merger of TAM and LAN Chile) could potentially see LAN Chile leave the oneworld alliance for Star. IAG probably also needs to expand its exposure to higher growth emerging markets (it has expressed interest in TAP), including Asia.

While net debt to capital is relatively low (c.31.1%), a high level of capital expenditure to renew the long-haul fleet should see this rise, and we expect IAG to be free cash flow negative in 2012 and 2013. While the recovery plan is on track, the pension deficit remains at c. £2.5bn with a review due in March 2012.

We believe that IAG and its management team are visionary and have ambitious targets. This could result in material profit and, as such, improved stock performance in the coming years in a better economic environment. The problem, however, is that we continue to see a "risk-off" trade for the networks. IAG's targets are set very far into the future, and it faces significant short-term challenges that are likely to result in lower profits in 2012 and further downside risk to estimates.

IAG long-term story but short-term challenges Cost headwinds in 2012

Negative free cash flow in 2012-2013

Complete and restructure bmi

Iberia competitive and industrial relations position challenging

Premium traffic at risk

Pension review in 2012

Research Report: Davy on Airlines January 19, 2012

31 Davy Research

At its inaugural capital markets day (November 11th), IAG indicated the following: It is targeting an operating profit improvement of c.€1.5bn in 2015

(assuming oil up to the $120 per barrel range), achieved through an increase from €400m to €450m in annual synergy targets from year-five, structural profit improvements of €400m and organic growth of €150m. Its goal is to deliver a 12% return on capital employed by 2015.

Specific areas of financial benefit include the creation of Iberia Express (at least €100m) and hub improvements at Madrid Barajas (at least €100m).

From a 2010 base, the company expects the optimisation of the transatlantic joint business with American Airlines to deliver at least €150m.

It is planning a capital expenditure programme of €1.1bn in 2011, €1.6bn in 2012, €2.0bn in 2013, €1.35bn in 2014 and €1.6bn in 2015 with a target of free cash generation in aggregate between 2012 and 2015.

There will be cost efficiency gains of c.€250m from the introduction of new aircraft into the fleet.

It is looking for an organic capacity growth rate of 2.5% per annum up to 2015.

It expects EU emissions trading costs of €90m in year one of the scheme at current carbon prices.

For FY2012, the company expects c.14% growth in unit fuel costs and unit costs ex-fuel to be flat. It plans to grow capacity by 2.5%.

Since the capital markets day, IAG has announced that it has reached a binding agreement with Lufthansa to sell bmi. The specifics of this deal include: a gross price of £172.5m with a significant reduction if Lufthansa does

not opt to sell bmibaby before completion; IAG's Heathrow slot portfolio to increase by up to 56 additional slot

pairs – BA currently has c.44% of Heathrow slots; earnings per share (EPS) to be accretive by 2014 at the latest and

IAG's 2015 operating profit target to increase by more than €100m with a consequent increase in EPS;

restructuring costs spread over three years and significantly lower in total than bmi's current annual losses;

deal subject to competition clearance; We think that this could be a great deal for IAG in the longer term if it can turn bmi around – IAG sees significant room for unit cost reduction and unit revenue improvement. In our previous issue of Davy on Airlines ("Virtual airline mergers; implications of the consolidation of the North Atlantic", issued October 4th), we outlined that home hub dominance is a positive long-term structural benefit bought for little cost

We found 18 routes, or 5%, of route overlap between BA and bmi. We expect the deal to be approved but with a small number of slot remedies.

Research Report: Davy on Airlines January 19, 2012

32 Davy Research

and remarkably without the pension deficits. However, the regulator may look at slot remedies to approve the deal, and bmi will not be easy to right-size given that it is perpetually loss-making. We rate IAG 'underperform' and reduce our price target to 140c/115p. In addition to more positive macro indicators, catalysts for a change in IAG's rating and for market sentiment improvement are as follows: greater clarity on the downside risk to premium (the airline currently

defines long haul premium as 'stable'); indications that Iberia Express can be a success; deliverability on targets, particularly as we get closer to its 2015 goals.

Figure 31: BA/IAG premium versus non-premium traffic growth

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

May-96

Feb-97

Nov-97

Aug-98

May-99

Feb-00

Nov-00

Aug-01

May-02

Feb-03

Nov-03

Aug-04

May-05

Feb-06

Nov-06

Aug-07

May-08

Feb-09

Nov-09

Aug-10

May-11

Premium volume growth Non-premium volume growth Source: Davy

We rate IAG a sector underperformer and reduce our price target to 140c/115p

Figure 30: IAG profit bridge

-100

0

100

200

300

400

500

600

700

FY2011e opresult

EU-ETS Yieldincrease

ATI

Yieldincreasemerger

Unit costs MENA/Japan

Vol uplift Fuel Vol uplift FY2012e opresult

Consensus

€459m -€90m€62m

€48m €26m

€8m -€673m

€356m

€100m

€331m

€296m

Source: Davy

Research Report: Davy on Airlines January 19, 2012

33 Davy Research

Lufthansa – challenges ahead in current environment

Next catalyst – full-year results March 15th Lufthansa is guiding operating profit "at the upper end of the three-digit-million euro range" for 2011. It reiterated this guidance at its Q3 results on October 27th after issuing a profit warning ahead of its September investor day. This was due to weaker-than-expected booking trends, particularly in intercontinental economy. Premium business had yet to see significant weakness.

Figure 32: Valuation is influenced by uncertainty and external events

Source: Lufthansa

In the short term, Lufthansa faces a number of cyclical and structural challenges. Our concerns, relating principally to weakness in cargo and potential weakness in the premium business, have caused us to lower our estimates. We are lowering Q4 FY2011 yields to 1.5% (previously 2.5%) and assume yield growth of 1.3% in 2012 and 1.1% in FY2013 (previously 1.1%) and a 5% decline in cargo revenue (previously flat). We now assume operating profit of €683m in FY2011 (previous €800m) but have also lowered FY2012 to €563m (previously €800m) and FY2013 to €769m (previously €1,114m). We assume that bmi is sold in Q1 2012 and adjust our 2012 operating profit to take this into account. Despite the removal of the loss-making subsidiary, pressure on the revenue line is likely to lead to a negative growth year for operating profits. Our numbers are now 10-15% below consensus. The specific issues facing the airline are: Normally representing some 25% of operating income, Lufthansa is

exposed to declining air cargo. The night-time flying ban at its hub at Frankfurt Main will also suppress profits (c.€50m in FY2012; court review in mid-March). Some restructuring of this business is likely, and we note likely restructuring at its Jade Cargo JV.

Lufthansa – challenges in 2012 Cargo weakness and night-time flying

ban at Frankfurt

Premium traffic risk

Potential long-term competition increase – Middle East, Frankfurt expansion

Continues to restructure passenger subsidiaries

Research Report: Davy on Airlines January 19, 2012

34 Davy Research

With almost 50% of long-haul passengers exposed to the premium end of the business, Lufthansa faces a potential decline in this high- yielding traffic. Winter capacity has been reduced to 4% (from 12% originally) and 3% next summer (the original plan was 9%). Despite the obvious monitoring of the market environment and utilising its flexibility as appropriate, we expect its premium share to fall back a number of percentage points in a cyclical downturn. Even in a more stable macro environment, the premium share should structurally fall as Lufthansa adds proportionally more economy seats with larger aircraft.

The proposed investment of a 29.2% stake by Etihad in Air Berlin highlights the potential for increased competition by the Gulf carriers over time. We see them as major threats to yields on long-haul Asian traffic.

The removal of loss-making subsidiary bmi is a positive, albeit the sale price is likely "clearly negative" if bmibaby is not sold pre-deal. The retention of the pension obligations of bmi (estimated to be £180m) is surprising.

The new runway at Frankfurt Main represents a medium-term growth opportunity for Lufthansa but will cause it to allocate capacity in the short term to protect its slot position here. We may see increased competitor and slot take-up in the summer schedules.

Based on these factors and the current uncertain macro environment, we see Lufthansa's share price struggling in 2012. For valuation and balance sheet reasons, we are retaining its rating as 'neutral'; in an uncertain economic environment, it will likely outperform other networks. Catalysts to change our recommendation could come from the following: further cost restructuring plans – as always, we expect Lufthansa's

Climb programme to reach its €1bn target by end-2012. There have been some indications of a potential further cost plan, including closer integration of subsidiaries, which could be announced in 2012.

significant improvement in the cargo market; successful restructuring of subsidiaries, including Austrian. We see the Lufthansa group as a robust aviation business model with a strong management team that is focused on the following: finding solutions to loss-making entities and accelerated management

cost initiatives (e.g. bmi); gaining strong market positions and significant leadership in Aviation

Services (e.g. MRO); ensuring a strong financial profile with a robust liquidity position. It

has 67% of its fleet unencumbered with a book value of €11.8bn. However, with earnings momentum still negative and the stock affected by uncertainty and external factors, we reduce our price target to €9.

Research Report: Davy on Airlines January 19, 2012

35 Davy Research

Table 22: Lufthansa passenger group forecasts

Passenger business -operating profit (€m)

Lufthansa Passenger

Airlines

Swiss bmi Austrian Germanwings SN Brussels Other Total

FY2013 251 200 0 -70 -50 0 0 331 FY

FY2012 193 200 0 -100 -50 0 0 243 FY

FY2011 291 300 -250 -70 -50 0 0 221 FY

3m -234 17 -63 -64 -44 0 -3 -391 Q1

6m -100 104 -120 -64 -46 0 -13 -239 H1

9m 161 244 -154 -34 -23 0 -25 169 Q1-Q3

FY2010 382 298 -145 -66 -39 0 6 436 FY

3m -236 1 -45 -66 -34 0 7 -373 Q1

6m -203 54 -93 -70 -39 0 9 -342 H1

9m 158 194 -90 -47 -11 0 14 218 Q1-Q3

FY2009 -107 93 -78 -31 24 0 91 -8 FY

Source: Davy; OAG Worldwide

We retain Lufthansa's rating as 'neutral but reduce our price target to €9

Figure 33: Lufthansa profit bridge

0

100

200

300

400

500

600

700

800

FY2011eop result

Japan Fuel costs Fuelsurchage

Underlyingyield / vol

Costsavings

EU ETS Cargonight

flying ban

bmi sale Non-paxbusiness

FY2012e op result

Consensus

€683m

€65m -€677m

€338m

€123m

€51m -€30m

€250m -€80m

€593m

€689m

-€130m

Source: Davy

Research Report: Davy on Airlines January 19, 2012

36 Davy Research

Table 23: Lufthansa operating forecasts (€m)

Passenger transportation

Logistics MRO IT Services Catering Service and financial

companies

Segment total

Reconciliation Group

2013F Total revenue 25,857.3 2,851.0 4,290.6 626.3 2,377.2 - 36,002.4 -3, 459.0 32,543.4 Operating result 331 171 257 21 83 -94 769 769.3 Operating margin 1.3% 6.0% 6.0% 3.3% 3.5% n/a 2.1% 2.4% 2012F Total revenue 24,355.5 2,851.0 4,165.6 608.1 2,308.0 - 34,288.1 -3,459.0 30,829.1 Operating result 244 100 250 20 81 -101 593 593.1 Operating margin 1.0% 3.5% 6.0% 3.3% 3.5% n/a 1.7% 1.9% 2011F Total revenue 23,031.4 2,962.0 4,124.4 596.1 2,308.0 - 33,021.8 -3,459.0 29,562.8 Operating result 221 207 247 18 83 -94 683 682.9 Operating margin 1.0% 7.0% 6.0% 3.0% 3.6% n/a 2.1% 0.0% 2.3% 556 2010A Total revenue 20,912.0 2,795.0 4,018.0 595 2,249.0 - 30,569.0 -3,245.0 27,324.0 EBITDA 2,610.0 445 412 45 174 3686 -1,128.0 2,558.0 EBITDA margin 12% 16% 1% 8% 8% 12% 9% Operating result 436 310 268 10 76 -226 874 2 876 Operating margin 2.1% 11.1% 6.7% 1.7% 3.4% n/a 2.9% -0.1% 3.2% 664 2009A Total revenue 16,798.0 1,951.0 3,963.0 605 2,102.0 - 25,419.0 -3,136.0 22,283.0 EBITDA 1,430.0 -28 436 54 120 2012 1,605.0 EBITDA margin 8.5% -1.4% 11.0% 8.9% 5.7% 7.9% 7.2% Operating result -8 -171 316 16 72 -134 91 39 130 Operating margin -0.05% -8.8% 8.0% 2.6% 3.4% n/a 0.4% -1.2% 0.6% 2008 Total revenue 18,393.0 2,907.0 3,717.0 657 2,325.0 - 27,999.0 -3,129.0 24,870.0 EBITDA 1,948.0 323 425 78 166 46 2,986.0 -343 2,643.0 EBITDA margin 10.6% 11.1% 11.4% 11.9% 7.1% 10.7% 10.6% Operating result 722 164 299 40 70 69 1364 -10 1,354.0 Operating margin 3.9% 5.6% 8.0% 6.1% 3.0% n/a 4.9% 0.3% 5.4% 2007 Total revenue 15,956.0 2,736.0 3,571.0 679 2,396.0 - 25,338.0 -2,918.0 22,420.0 EBITDA 2,047.0 299 406 39 167 232 3,190.0 -608 2,582.0 EBITDA margin 12.8% 10.9% 11.4% 5.7% 7.0% 12.6% 11.5% Operating result 826 136 293 23 100 53 1431 -53 1,378.0 Operating margin 5.2% 5.0% 8.2% 3.4% 4.2% n/a 5.6% 1.8% 6.1% 2006 Total revenue 13,475.0 2,845.0 3,415.0 652 2,278.0 - 22,665.0 -2,816.0 19,849.0 EBITDA 1,485.0 276 352 90 168 2,371.0 -475 1,896.0 EBITDA margin 11.0% 9.7% 10.3% 13.8% 7.4% 10.5% 16.9% 9.6% Operating result 409 82 248 49 50 52 890 -45 845 Operating margin 3.0% 2.9% 7.3% 7.5% 2.2% n/a 3.9% 1.6% 4.3% 2005 Total revenue 12,047.0 2,752.0 3,121.0 635 2,215.0 - 20,770.0 -2,705.0 18,065.0 EBITDA 1,381.0 284 364 99 17 2,145.0 -170.5 1,974.50 EBITDA margin 11.5% 10.3% 11.7% 15.6% 0.8% 10.3% 6.3% 10.9% Operating result 135 108 258 63 5 54 623 -46 577 Operating margin 1.1% 3.9% 8.3% 9.9% 0.2% n/a 3.0% 1.7% 3.2% 2004 Total revenue 11,207.0 2,469.0 3,060.0 628 2,334.0 - 19,698.0 -2,733.0 16,965.0 EBITDA 939 166 328 104 53 1,590.0 -94.8 1,495.20 EBITDA margin 8.4% 6.7% 10.7% 16.6% 2.3% 8.1% 3.5% 8.8% Operating result 265 34 205 40 -167 0 377 6 383 Operating margin 2.4% 1.4% 6.7% 6.4% -7.2% n/a 1.9% -0.2% 2.3% 2003 Total revenue 10,208.0 2,161.0 2,852.0 611 2,667.0 - 18,499.0 -2,542.0 15,957.0 EBITDA -157 177 310 95 217 642 541 1,183.0 EBITDA margin -1.5% 8.2% 10.9% 15.5% 8.1% 3.5% -21.3% 7.4% Operating result 45 -16 157 39 -215 - 10 26 36 Operating margin 0.4% -0.7% 5.5% 6.4% -8.1% n/a 0.1% -1.0% 0.2% 2002 Total revenue 10,461.2 2,350.5 2,808.3 557.4 3,075.8 - 19,253.2 -2,282.2 16,971.0 EBITDA 2,437.3 758 297.2 87.7 334.4 3,914.6 -1,986.4 1,928.2 EBITDA margin 23% 32% 11% 16% 11% 20% 87% 11% Operating result 477.6 122.5 176.4 37.1 -93.8 - 719.8 -1.8 718 Operating margin 4.6% 5.2% 6.3% 6.7% -3.0% n/a 3.7% 0.1% 4.2% 2001 Total revenue 10,632.5 2,437.6 2,834.8 478.1 2,515.4 - 18,898.4 -2,208.4 16,690.0 EBITDA 835.5 182.6 233.3 77 -223.5 1,104.9 635.7 1,740.6 EBITDA margin 7.9% 7.5% 8.2% 16.1% -8.9% 5.8% -28.8% 10.4% Operating result 31.7 41.5 130.3 19.6 -212.3 - 10.8 17.2 28 Operating margin 0.3% 1.7% 4.6% 4.1% -8.4% n/a 0.1% -0.8% 0.2%

Source: Davy

Research Report: Davy on Airlines January 19, 2012

37 Davy Research

Air France-KLM – needs to deliver on turnaround plan