long run competitive equilibrium. one price monopoly versus perfect competition

TRANSCRIPT

LONG RUN COMPETITIVE EQUILIBRIUM

One Price Monopoly Versus Perfect Competition

Price Discrimination Prices and Output

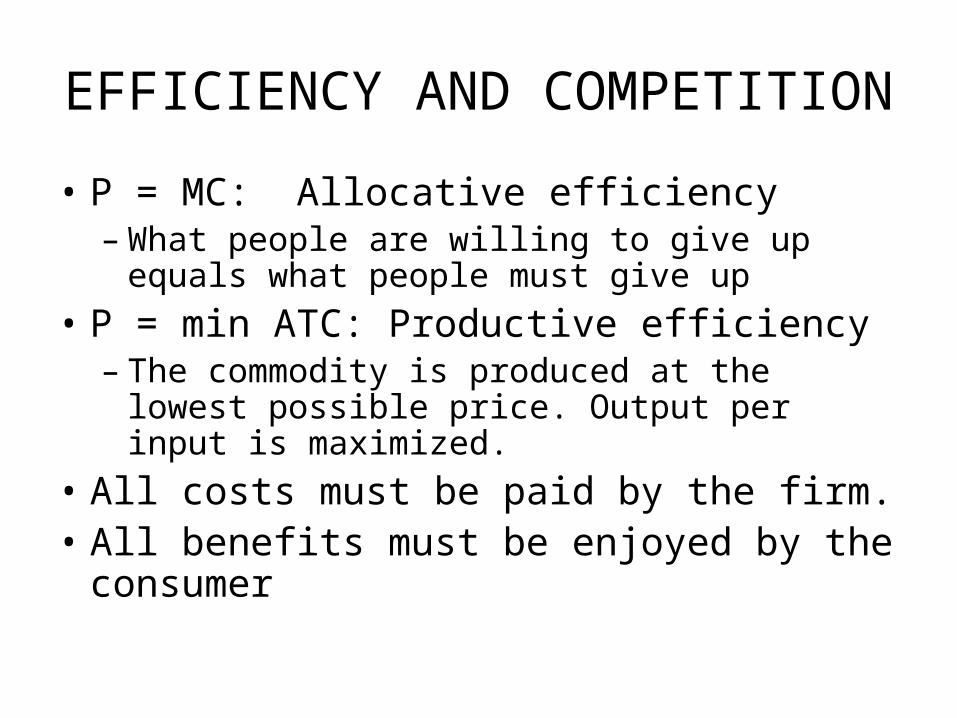

EFFICIENCY AND COMPETITION

• P = MC: Allocative efficiency– What people are willing to give up equals

what people must give up

• P = min ATC: Productive efficiency– The commodity is produced at the lowest

possible price. Output per input is maximized.

• All costs must be paid by the firm.• All benefits must be enjoyed by the

consumer

Monopoly in Long-run Equilibrium

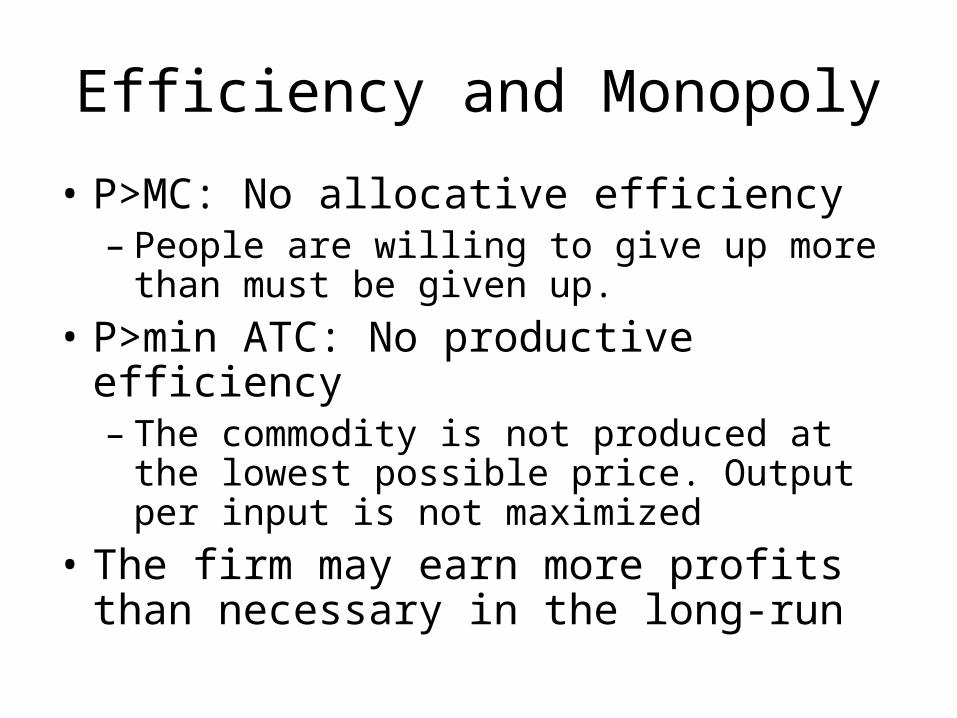

Efficiency and Monopoly

• P>MC: No allocative efficiency– People are willing to give up more than must

be given up.

• P>min ATC: No productive efficiency– The commodity is not produced at the lowest

possible price. Output per input is not maximized

• The firm may earn more profits than necessary in the long-run

Monopolistic competition in short-run equilibrium

Efficiency and Monopolistic Competition in the short-run

• P>MC: No allocative efficiency– People are willing to give up more than must

be given up.

• P>min ATC: No productive efficiency– The commodity is not produced at the lowest

possible price. Output per input is not maximized

• BUT the profits will not persist in the long-run

Monopolistic competition in Long-run Equilibrium

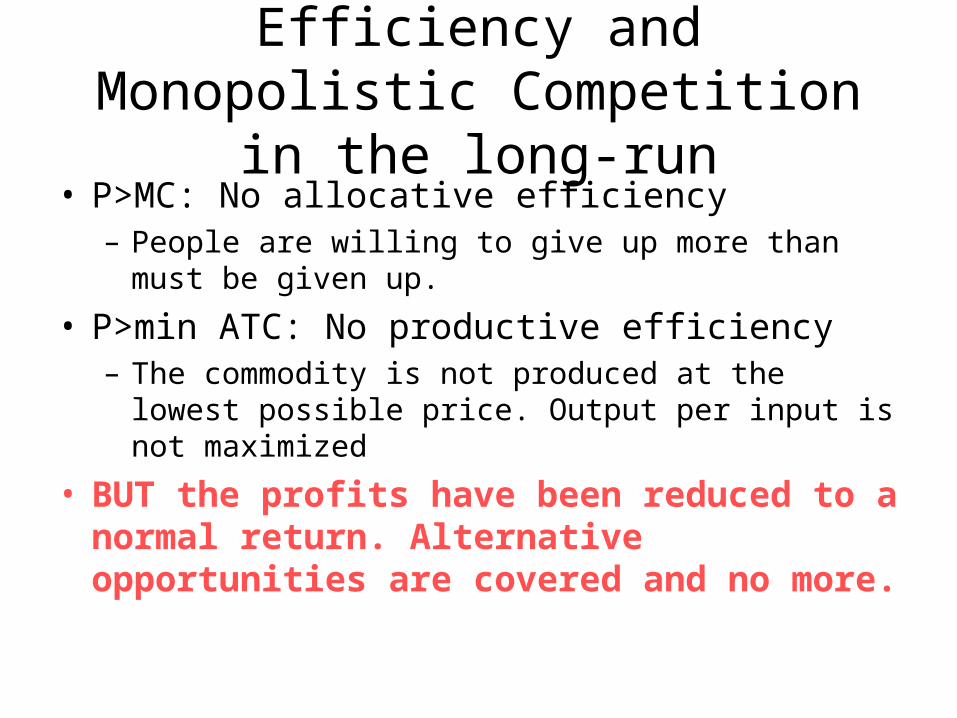

Efficiency and Monopolistic Competition in the long-run

• P>MC: No allocative efficiency– People are willing to give up more than must be given

up.

• P>min ATC: No productive efficiency– The commodity is not produced at the lowest possible

price. Output per input is not maximized

• BUT the profits have been reduced to a normal return. Alternative opportunities are covered and no more.

NO DEAD WEIGHT LOSS IN PERFECT COMPETION

QUANTITY

PRICE

S= SUM OF MC’s

D

Q

P

CS

PS

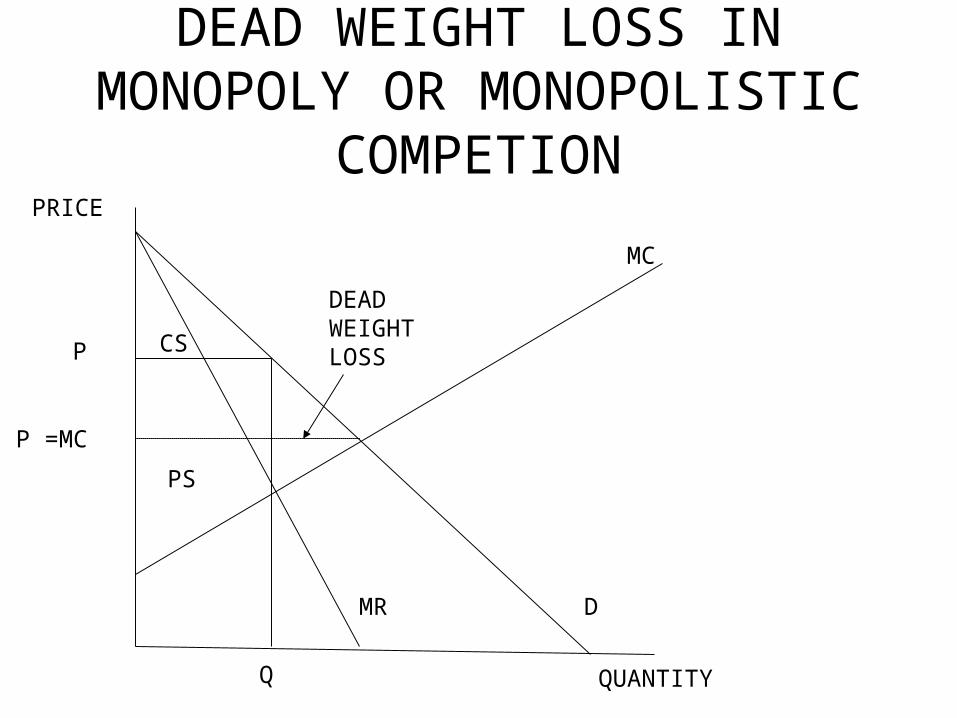

DEAD WEIGHT LOSS IN MONOPOLY OR MONOPOLISTIC

COMPETION

QUANTITY

PRICE

MC

D

Q

CS

PS

MR

P

DEAD WEIGHT LOSS

P =MC

Dead Weight Loss In Monopolistic Competition with Close Substitutes

QUANTITY

PRICE

MC

D

Q

CS

PS

MR

P

DEAD WEIGHT LOSS

P=mc

Monopolistic Competition and Perfect Competition

• In monopolistic competition, products may have very close substitutes.

• The closer the substitute the more elastic the demand curve. (The less the firm can raise price without customers going to the substitute.)

• The price set by the firm maybe very close to the MC and the deadweight loss may be small– (Consumer surplus is small, because the benefit from

a Louis’s pizza is very little more than the benefit from a Wheel pizza, for most consumers.)

How bad is monopolistic competition?

• If each firm has very close substitutes, the price charged by the monopolistically competitive firm will be very close to the price which equates price and marginal cost.

• Firms often compete by introducing products which are similar to successful products of competitors

Circumstances of Monopolistic Competition

• Each firm has excess capacity, and would like to sell more at the price they have set.

• Each firm wants to shift its demand curve out.

• Each firm wants to make its demand curve more inelastic – They want to be able to raise their price and

lose fewer customers.

Dynamics of Monopolistic Competition

• Firms want a larger demand for their product. If their demand shifts out, their profits will rise.

• Firms want a more inelastic demand curve. If they can raise the price with only a small decline in quantity sold, their profits will rise

Dynamic Monopolistic competition

• Firms ADVERTISE.– They hope to increase demand – shift the demand

curve out.– They hope to create brand name loyalty – Only Nike

shoes will due, no matter what they cost.• Firms DEVELOP more appealing products.

– Low fat subway sandwiches– Blueberry messenger systems– Running shoes with air cushions in them– If Elton John or Ashley MacIsaac are not longer hot,

perhaps Avril or David Matthews will have a big market.

Advertising and Product Development

• Both add to the costs of the firms

• If successful, they add to the revenues of the firms

• Firms must balance the addition to costs against the anticipated addition to revenues

Workings of Capitalism

• If there is entry to an industry, excess profits will be competed away.

• Competition in the music, book, and film industry as well as in fast foods and running shoes takes the form of developing new products and advertising them.

• P > MC but variety is the spice of life.

Drug Companies

• Even here, firms have the incentive to develop new products which may be useful.

• If one drug is highly successful and profitable, other firms may develop similar products that do not infringe on patents, if possible.– There are many drugs that lower cholesterol.

• (But I’m not sure we achieve the best possible results.)