logistics augmentation to the freight-truck-pavement interaction pilot study: final report · ·...

TRANSCRIPT

January 2014Research Report: UCPRC-RR-2014-02

Logistics Augmentation to the Freight-

Truck-Pavement Interaction Pilot Study:

Final Report

Authors:Nadia Viljoen, Quintin van Heerden, Lorina Popescu, Livison Mashoko,

Esbeth van Dyk, and Wilna Bean

Work Conducted Under Partnered Pavement Research Program (PPRC) Strategic Plan

Element 4.44: Pilot Study Investigating the Interaction and Effects for State Highway Pavements, Trucks,

Freight, and Logistics

PREPARED FOR: California Department of Transportation

Division of Transportation Planning (DOTP)

Office of Materials and Infrastructure

PREPARED BY:

CSIR

University of Pretoria

University of California

Pavement Research Center UC Berkeley

(This page blank)

UCPRC-RR-2014-02 i

DOCUMENT RETRIEVAL PAGE Research Report No.:

UCPRC-RR-2014-02

Title: Logistics Augmentation to the Freight-Truck-Pavement Interaction Pilot Study: Final Report Authors: Nadia Viljoen, Quintin van Heerden, Livison Mashoko, Esbeth van Dyk, and Wilna Bean Caltrans Technical Lead: Nerie Rose Agacer-Solis and Bill Nokes Prepared for: Caltrans Division of Transportation Planning

FHWA No.: CA142482C

Date Work Submitted:

January 2014

Date:January 2014

Strategic Plan Element No.: 4.44

Status: Stage 6, final version

Version No.:Final

Abstract: The objectives of this logistics augmentation to the Freight-Truck-Pavement interaction pilot study are: (1) to provide a basic understanding to Caltrans of private-sector decision making in road-freight transportation; (2) to identify and describe the comprehensive set of interactions between the efficiency and efficacy of road-freight transportation and the capacity, performance and regulation of road infrastructure in the state and recommend which of these interactions warrant more in-depth assessment on a statewide scale to quantify the overall economic and efficiency impact road infrastructure decisions have on the economy of California; and (3) to illustrate the value of direct interactions and consultations with private companies in exploring private sector decision making and the interdependence of these decisions on public sector actions. Conclusions: By using desktop studies, qualitative analysis, and case studies, this study has shown that road infrastructure and

regulation, as managed by Caltrans, have a marked impact on supply chain operations and strategies. Given the critical role that supply chains play in the economic well-being of and quality of life in California and the

dependence of these supply chains on road infrastructure and regulation, it is imperative that the public sector (Caltrans) and the private sector engage in the planning and construction of road infrastructure as well in the drafting and implementation of policy.

This pilot study has shown that road infrastructure and regulations have a direct effect on supply chain vulnerability, and that design and private companies need to consider these elements in their decision making.

Recommendations: Recognize that supply chain vulnerability and design are different for each economic goods movement-dependent

sector and therefore a blanket approach to the treatment of sectors will not suffice, and In order for this study to be comprehensive enough to form part of Caltrans’ routine decision making regarding road

infrastructure and regulation, expand the study’s scope to cover all goods movement-dependent sectors and deepen the study by conducting representative case studies of each sector.

Keywords: public sector, private sector, road-freight transportation, logistics, road infrastructure Proposals for Implementation: Publish this final report to provide the client with information to support planning and decision making regarding logistics, goods movement, and road infrastructure and regulation.

ii UCPRC-RR-2014-02

Related Documents: W.J.vdM. Steyn, N. Viljoen, L. Popescu, and L. du Plessis . 2012. Freight-Truck-Pavement Interaction, Logistics,

and Economics: Final Phase 1 Report (Tasks 1–6). Research Report prepared for Caltrans Division of Transportation Planning. (UCPRC-RR-2012-06)

W.J.vdM. Steyn. 2013. Freight-Truck-Pavement Interaction, Logistics, and Economics: Final Phase 1 Report (Tasks 7–8). Research Report prepared for Caltrans Division of Transportation Planning. (UCPRC-RR-2013-08)

W.J.vdM Steyn, and L. du Plessis. Freight-Truck-Pavement Interaction, Logistics, and Economics: Final Phase 1 Report (Tasks 9–11). (UCPRC-RR-2014-01)

W.J.vdM. Steyn, L. du Plessis, N. Viljoen, Q. van Heerden, L. Mashoko, E. van Dyk, and L. Popescu. 2014. Prepared for Caltrans Division of Transportation Planning. (UCPRC-SR-2014-01)Freight-Truck-Pavement Interaction, Logistics, & Economics: Final Executive Summary Report. Summary Report

Signatures N. Viljoen First Author

Nerie Rose Agacer-Solis

Bill Nokes Technical Reviewers

W.J.vdM. Steyn John T. Harvey Principal Investigators

Nerie Rose Agacer-Solis

Bill Nokes Caltrans Technical Leads

T. Joe Holland Caltrans Contract Manager

UCPRC-RR-2014-02 iii

TABLE OF CONTENTS

LIST OF FIGURES .............................................................................................................................................. ix

LIST OF TABLES ................................................................................................................................................ xi

DISCLAIMER STATEMENT ........................................................................................................................... xii

PROJECT OBJECTIVES ................................................................................................................................. xiii

EXECUTIVE SUMMARY ................................................................................................................................. xv

SECTION 1: BACKGROUND INVESTIGATION AND LITERATURE STUDY ...................................... xv

SECTION 2: CASE STUDY RESEARCH REGARDING THE INTERSECTION OF SUPPLY CHAINS

AND ROAD INFRASTRUCTURE AND REGULATION .................................................................. xvii

CONCLUSIONS AND WAY FORWARD .................................................................................................. xxiii

LIST OF ABBREVIATIONS ........................................................................................................................... xxv

SECTION 1: BACKGROUND INVESTIGATION AND LITERATURE STUDY

1 INTRODUCTION .......................................................................................................................................... 1

1.1 Background to the Logistics Augmentation Study ................................................................................... 3

1.2 The Interface Between the Public and Private Sector in Road Freight Systems ...................................... 3

1.3 Objectives of the Logistics Augmentation Study ...................................................................................... 5

1.4 Scope of the Logistics Augmentation Study ............................................................................................. 5

2 TASKS L1 – L4 SUMMARY ......................................................................................................................... 7

2.1 Task L1: Background Investigation and Project Inception Workshops .................................................... 7

2.2 Task L2: Literature Survey and Fieldwork Preparation ............................................................................ 7

2.3 Task L3: Operational Investigation (Fieldwork) ....................................................................................... 8

2.4 Task L4: Information Analysis and Progress Evaluation .......................................................................... 8

3 OVERVIEW OF CALIFORNIA FREIGHT TRANSPORTATION ......................................................... 11

3.1 Freight Trends in California .................................................................................................................... 11

3.1.1 Drivers of Growth in Freight Transportation ...................................................................................... 11

3.1.2 Current Freight Flows and Priority Corridors .................................................................................... 13

3.2 Freight Transportation Infrastructure in California ................................................................................. 17

3.2.1 Rail ..................................................................................................................................................... 17

3.2.2 Road ................................................................................................................................................... 18

3.2.3 Airports .............................................................................................................................................. 19

3.2.4 Ports ................................................................................................................................................... 20

3.3 Rail-Road Intermodal Systems ............................................................................................................... 21

iv UCPRC-RR-2014-02

3.3.1 Long-Haul Intermodal Shipments ...................................................................................................... 21

3.3.2 Short-Haul Intermodal Shipments ...................................................................................................... 22

4 PUBLIC SECTOR PERSPECTIVE ........................................................................................................... 23

4.1 Role of the Public Sector in Road Freight Systems ................................................................................ 23

4.2 Public Sector Decision Making .............................................................................................................. 26

4.3 Strategic Plans Impacting Road-Freight in California ............................................................................ 28

4.3.1 California Transportation Plan 2025 [7] ............................................................................................ 29

4.3.2 Goods Movement Action Plan [15] ................................................................................................... 31

4.3.3 California State Rail Plan 2007-08 to 2017-18 [9] ............................................................................ 31

4.3.4 SJV Interregional Goods Movement Plan [16] .................................................................................. 32

4.3.5 Central Coast California Commercial Flows Study [17] ................................................................... 33

4.3.6 Regional Transportation Plans ........................................................................................................... 34

4.3.7 Merced County Overall Work Program [23] ..................................................................................... 38

4.3.8 Colusa County Overall Work Program [24] ...................................................................................... 38

4.4 Decision Support for Freight Planning ................................................................................................... 38

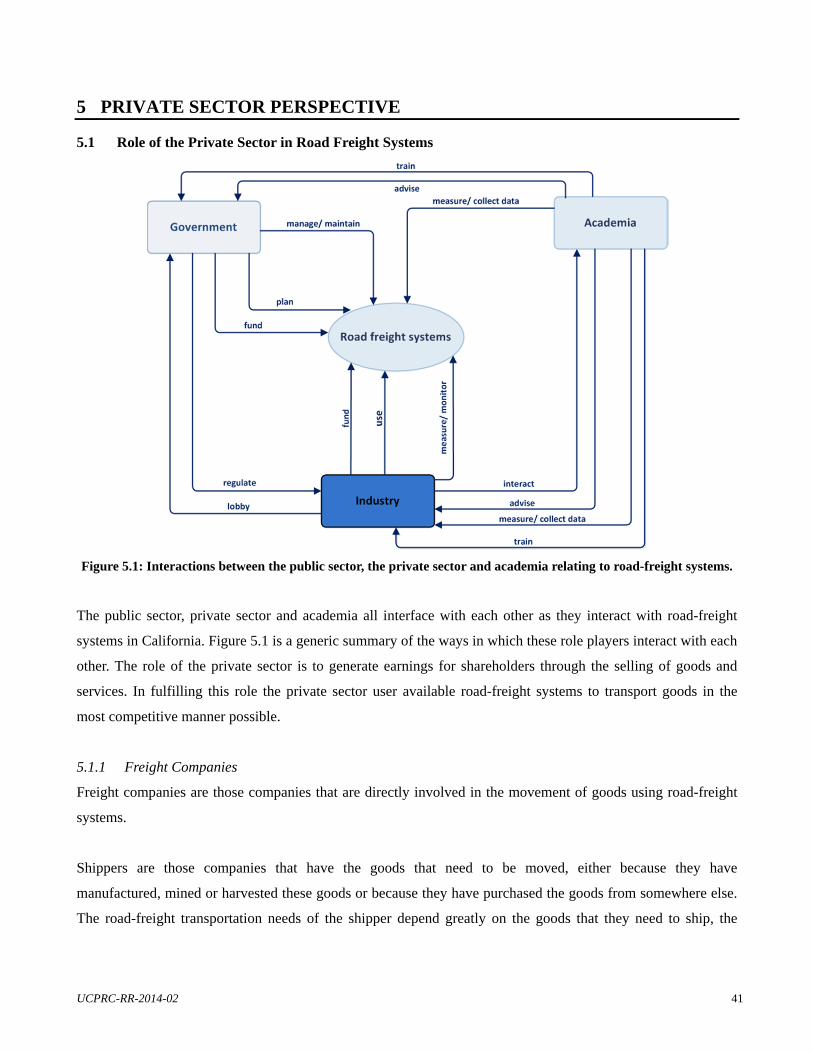

5 PRIVATE SECTOR PERSPECTIVE ......................................................................................................... 41

5.1 Role of the Private Sector in Road Freight Systems ............................................................................... 41

5.1.1 Freight Companies ............................................................................................................................. 41

5.1.2 Support Services ................................................................................................................................ 42

5.1.3 Industry Associations ......................................................................................................................... 42

5.2 Private Sector Decision Making ............................................................................................................. 43

5.3 Emergent Logistics Practices .................................................................................................................. 45

5.3.1 Outsourcing Trends ............................................................................................................................ 45

5.3.2 Intermodal Transport .......................................................................................................................... 46

5.3.3 Inventory-Pull Systems ...................................................................................................................... 47

5.4 Trucking Industry Trends ........................................................................................................................ 49

6 INTERDEPENDENCE OF PUBLIC AND PRIVATE DECISIONS ....................................................... 51

6.1 Interaction Between Public and Private Decision Making ..................................................................... 51

6.2 Success Factors for Public-Private Interaction in Freight Systems ........................................................ 52

UCPRC-RR-2014-02 v

SECTION 2: CASE STUDY RESEARCH REGARDING THE INTERSECTION OF SUPPLY CHAINS AND ROAD INFRASTRUCTURE AND REGULATION

7 TASK L3: OPERATIONAL INVESTIGATION ....................................................................................... 55

7.1 Rationale for the Operational Investigation ............................................................................................ 55

7.2 The Case Study Research Method .......................................................................................................... 56

7.3 Case Study 1: Operational Investigation of Company A ........................................................................ 57

7.3.1 Day 1, May 15, 2013 – Understanding the Organization and its Scope of Business ......................... 57

7.3.2 Day 2, May 16, 2013 – Understanding the Interface between Transport and the Processing Plant(s)58

7.3.3 Day 3, May 17, 2013 – Understanding the Road Transport Function ................................................ 58

7.4 Summary of Findings: Company A ........................................................................................................ 59

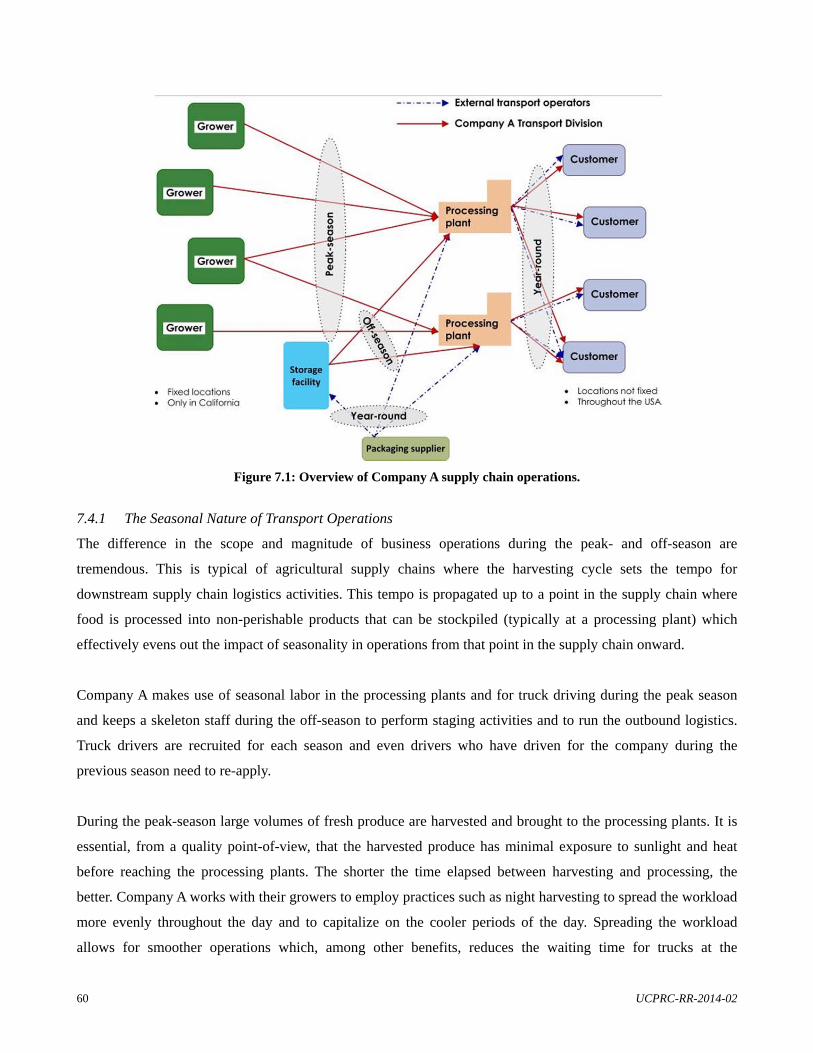

7.4.1 The Seasonal Nature of Transport Operations ................................................................................... 60

7.4.2 The Interface between Inbound and Outbound Logistics and the Facilities ...................................... 61

7.4.3 Reverse Logistics ............................................................................................................................... 63

7.4.4 Driver Recruitment, Regulation, Training and Management ............................................................. 63

7.4.5 From the Driver’s Perspective ............................................................................................................ 64

7.4.6 Fleet Management .............................................................................................................................. 66

7.4.7 Public-Private Interaction ................................................................................................................... 66

7.5 Business Decisions Affected by Road Infrastructure and Regulation: Company A ............................... 67

7.5.1 Strategic Decisions ............................................................................................................................. 67

7.5.2 Operational and Tactical Decisions .................................................................................................... 68

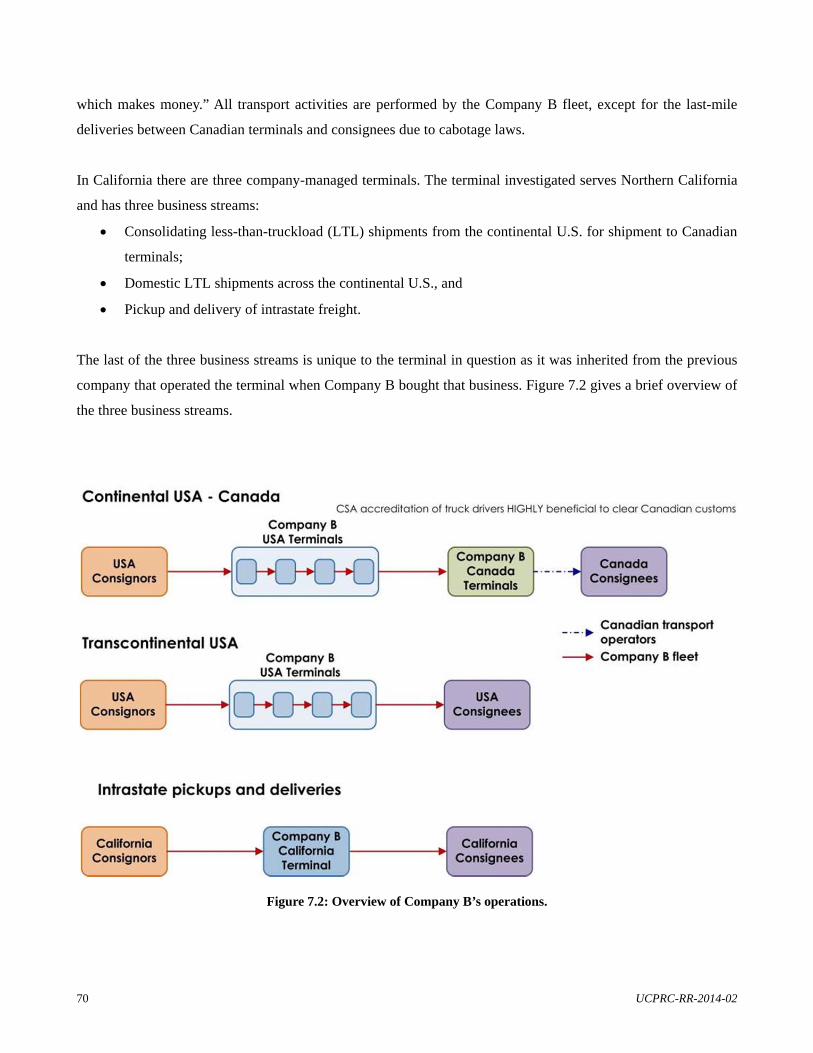

7.6 Case Study 2: Operational Investigation of Company B ........................................................................ 68

7.6.1 Day 1, May 21, 2013 – Understanding the Organization and its Scope of Business ......................... 68

7.6.2 Day 2, May 22, 2013 – Observing Shipments from Pickup to Delivery ........................................... 69

7.7 Summary of Findings: Company B ........................................................................................................ 69

7.7.1 The Role of Less-than-Truckload Shipping in the Supply Chain ...................................................... 72

7.7.2 Cycles in Less-than-Truckload Shipping ........................................................................................... 72

7.7.3 Driver Management ........................................................................................................................... 73

7.7.4 Crossing the Canadian Border ........................................................................................................... 74

7.7.5 From the Driver’s Perspective ............................................................................................................ 75

7.7.6 Fleet Management .............................................................................................................................. 76

7.7.7 Inspections and Freeway Restrictions ................................................................................................ 77

7.7.8 The Image of Trucking ....................................................................................................................... 78

7.7.9 Triple Trailers and Truck Lanes ......................................................................................................... 78

7.8 Business Decisions Affected by Road Infrastructure and Regulation: Company B ............................... 79

vi UCPRC-RR-2014-02

7.8.1 Strategic Decisions ............................................................................................................................. 79

7.8.2 Operational and Tactical Decisions .................................................................................................... 79

7.9 Congruency of Findings with the San Joaquin Valley Interregional Goods Movement Plan ................. 79

7.10 Lessons Learned and Recommendations for Future Case Studies ......................................................... 80

7.10.1 Executive Support ....................................................................................................................... 80

7.10.2 Privacy and Confidentiality Protocols ........................................................................................ 81

7.10.3 A Flexible Plan of Action ............................................................................................................ 81

7.10.4 Exploring Topics through Conversation ..................................................................................... 81

7.10.5 Recording Notes .......................................................................................................................... 82

8 SUPPLY CHAIN DESIGN AND VULNERABILITY ............................................................................... 83

8.1 The Role of Transport Infrastructure in Supply Chain Management ...................................................... 83

8.2 Supply Chain Risk and Vulnerability ..................................................................................................... 84

8.2.1 Supply Chain Risk and Vulnerability in California ............................................................................ 86

8.3 General Risks in the Agriculture, Forestry and Fishing sector ............................................................... 87

8.3.1 Weather-Related Hazards ................................................................................................................... 89

8.3.2 Natural Disasters ................................................................................................................................ 89

8.3.3 Biological and Environmental Hazards.............................................................................................. 90

8.3.4 Market-Related Hazards ..................................................................................................................... 90

8.3.5 Logistics and Infrastructure Hazards ................................................................................................. 91

8.3.6 Managerial and Operational Hazards ................................................................................................. 92

8.3.7 Public Policy and Institutional Hazards ............................................................................................. 92

8.3.8 Political Risks .................................................................................................................................... 92

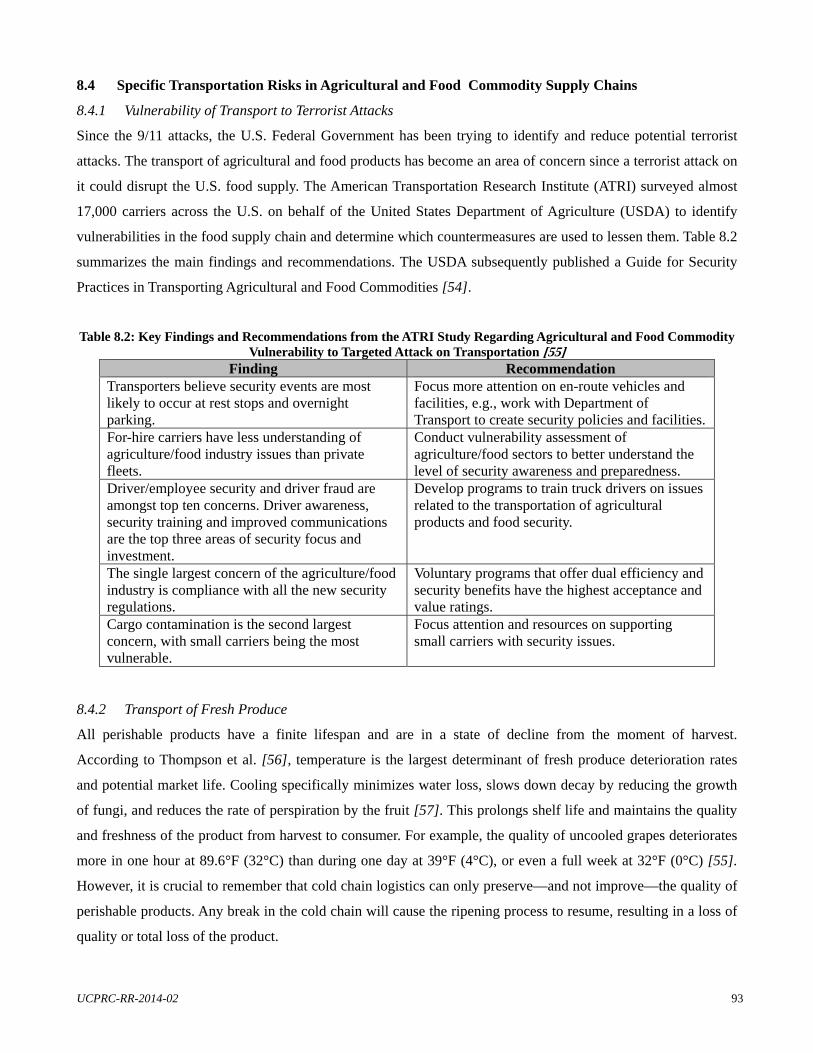

8.4 Specific Transportation Risks in Agricultural and Food Commodity Supply Chains ........................... 93

8.4.1 Vulnerability of Transport to Terrorist Attacks .................................................................................. 93

8.4.2 Transport of Fresh Produce ................................................................................................................ 93

8.5 General Risks in the Transport and Warehousing Sector ........................................................................ 94

8.5.1 The Role of Third-Party Logistics in the Supply Chain ..................................................................... 94

8.5.2 Transport Infrastructure ...................................................................................................................... 96

8.5.3 Communications Infrastructure .......................................................................................................... 97

8.5.4 Economic Volatility ............................................................................................................................ 97

8.5.5 Environmental Regulation ................................................................................................................. 98

8.5.6 Geopolitical Unrest ............................................................................................................................ 98

8.6 Supply Chain Network Design ............................................................................................................... 99

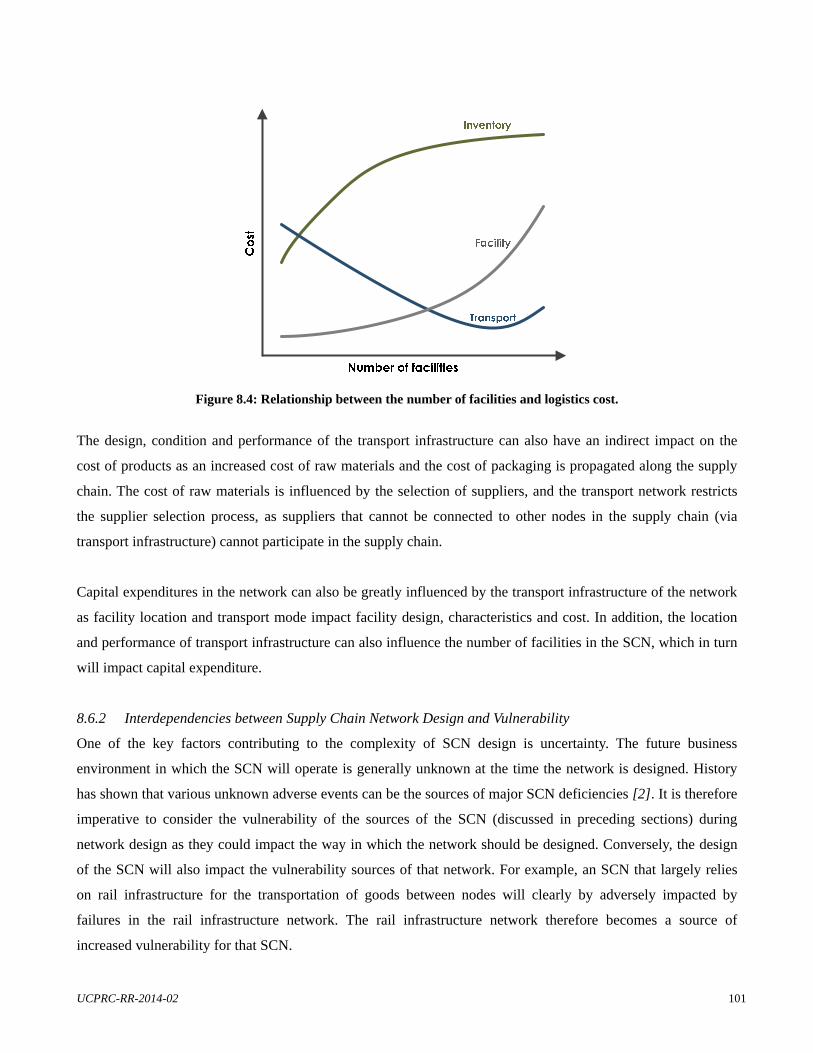

8.6.1 Impact of Infrastructure on Supply Chain Network Design ............................................................. 100

UCPRC-RR-2014-02 vii

8.6.2 Interdependencies between Supply Chain Network Design and Vulnerability ................................ 101

9 THE SPREAD OF ECONOMIC SECTORS IN CALIFORNIA AND IMPLICATIONS FOR ROAD

INFRASTRUCTURE AND REGULATION ............................................................................................ 103

9.1 The Value and Spatial Spread of Goods-Movement Dependent Sectors in California ......................... 103

10 CONCLUSION AND WAY FORWARD ................................................................................................... 107

10.1 Implications of the Findings of the Logistics Augmentation Pilot Study for Caltrans ......................... 107

10.2 Expanding the Scope and Depth of the Logistics Augmentation Pilot Study ....................................... 108

10.2.1 Expanding the Scope of the Study ............................................................................................ 108

10.2.2 Developing Representative Case Study Ensembles .................................................................. 108

10.3 Complex Network Analysis to Analyze Supply Chain Vulnerability Drivers in the Californian Road

Freight Network .................................................................................................................................... 109

REFERENCES ................................................................................................................................................... 110

TECHNICAL APPENDICES ........................................................................................................................... 115

APPENDIX A: SUMMARY TABLES OF FREIGHT FLOW ANALYSES ................................................. 115

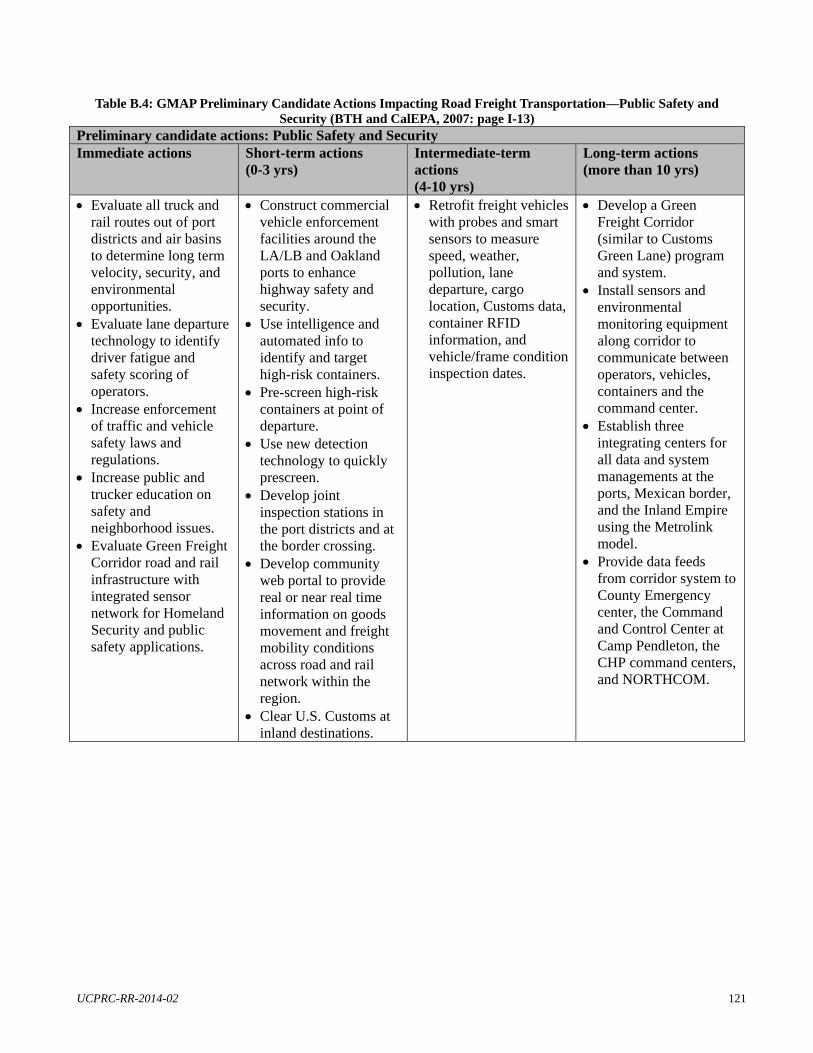

APPENDIX B: PRELIMINARY GMAP ACTIONS AFFECTING ROAD FREIGHT

TRANSPORTATION .................................................................................................................................. 117

APPENDIX C: SHORT DESCRIPTIONS OF PUBLIC-PRIVATE INTERACTION CASE STUDIES . 122

APPENDIX D: INTERVIEW QUESTIONS PREPARED FOR TASK L3 ................................................. 124

APPENDIX E: PRIVACY AND CONFIDENTIALITY PROTOCOLS ...................................................... 130

APPENDIX F: ECONOMIC CONTRIBUTION OF CALIFORNIAN COUNTIES ................................. 134

APPENDIX G: PRELIMINARY SECTOR SEGMENTATION .................................................................. 143

APPENDIX H: POTENTIAL PARTICIPANTS FOR FUTURE CASE STUDIES .................................... 154

viii UCPRC-RR-2014-02

UCPRC-RR-2014-02 ix

LIST OF FIGURES

Figure 3.1: California projected population growth 2010 – 2060, percent change [10]. ...................................... 12

Figure 3.2: Estimated freight flows within California and through California in 2011 [11]. ............................... 13

Figure 3.3: Estimated freight flows into and out of California in 2011 [11]. ........................................................ 14

Figure 3.4: National truck freight flows to and from California in 2007 [12]. ..................................................... 14

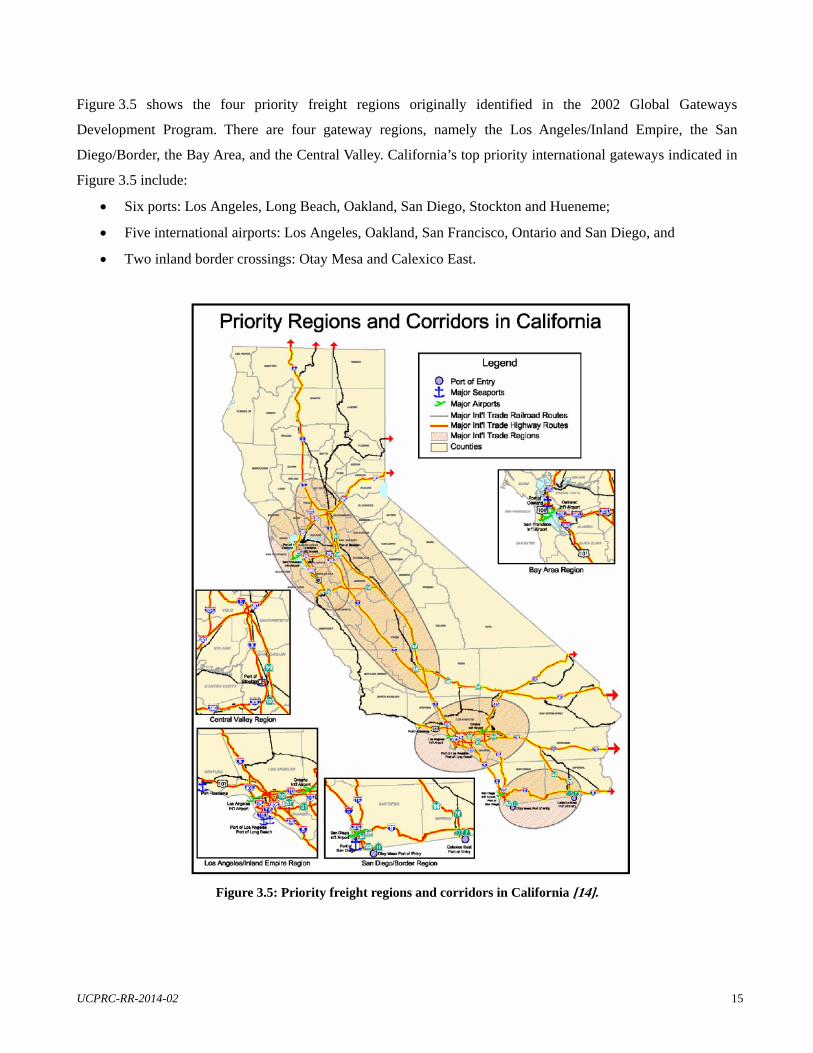

Figure 3.5: Priority freight regions and corridors in California [14]. ................................................................... 15

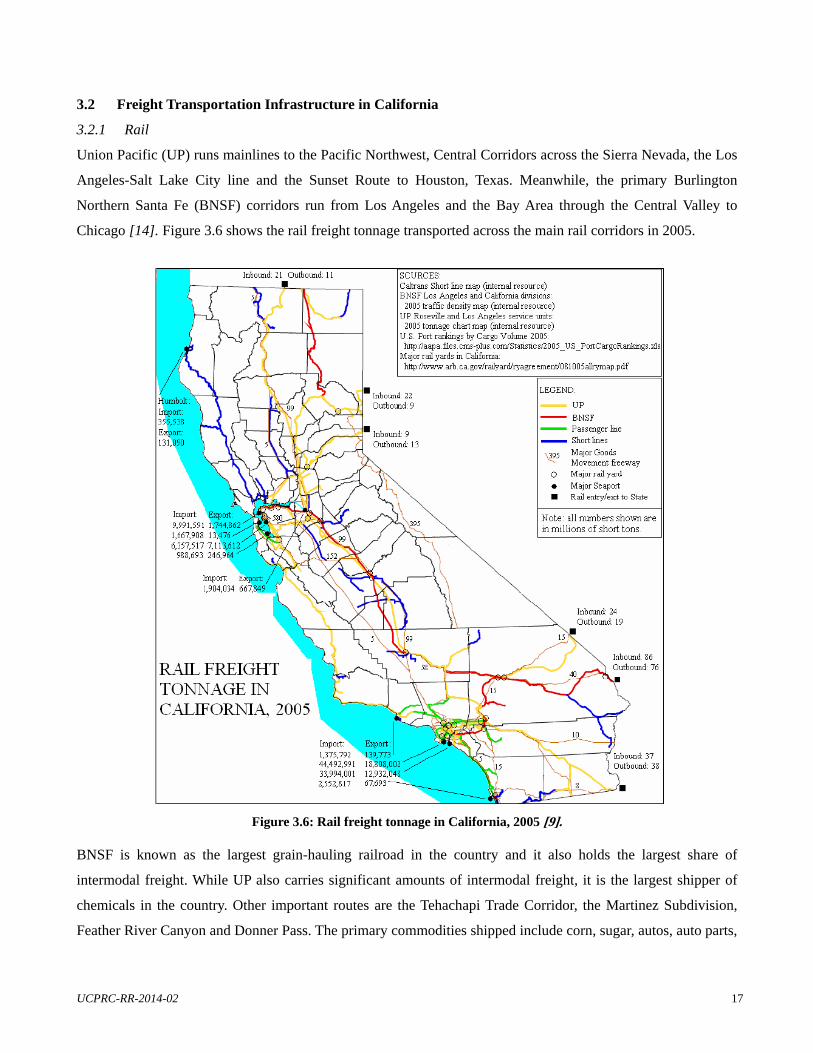

Figure 3.6: Rail freight tonnage in California, 2005 [9]. ...................................................................................... 17

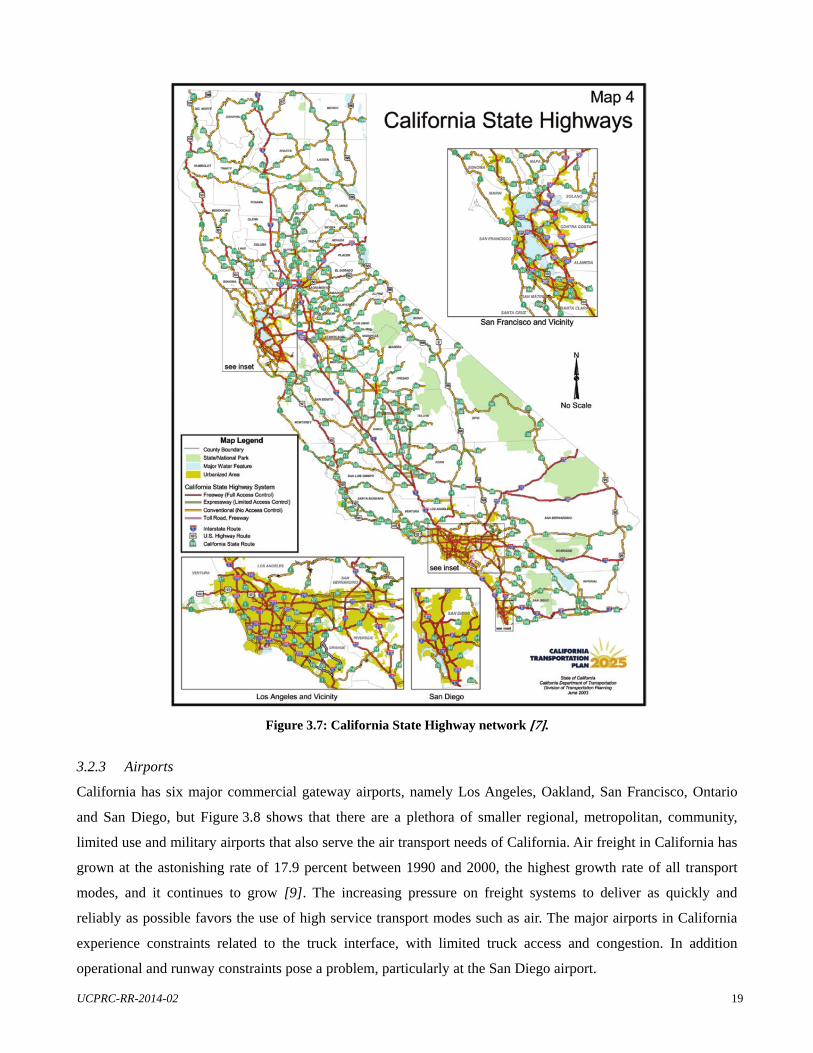

Figure 3.7: California State Highway network [7]. .............................................................................................. 19

Figure 3.8: California public use and military airports [7]. .................................................................................. 20

Figure 3.9: California seaports [7]. ....................................................................................................................... 21

Figure 4.1: Interactions between the public sector, the private sector and academia relating to road-freight

systems. ................................................................................................................................................. 23

Figure 4.2: Vision, goals and policies of the California Transportation Plan 2025 [7]. ........................................ 30

Figure 4.3: California Regional Transportation Planning Agencies (RTPAs) and Metropolitan Planning

Organizations (MPOs) [7]. ................................................................................................................... 34

Figure 5.1: Interactions between the public sector, the private sector and academia relating to road-freight

systems. ................................................................................................................................................. 41

Figure 7.1: Overview of Company A supply chain operations. ............................................................................ 60

Figure 7.2: Overview of Company B’s operations. ............................................................................................... 70

Figure 8.1: Typology of supply chain risk sources. ............................................................................................... 85

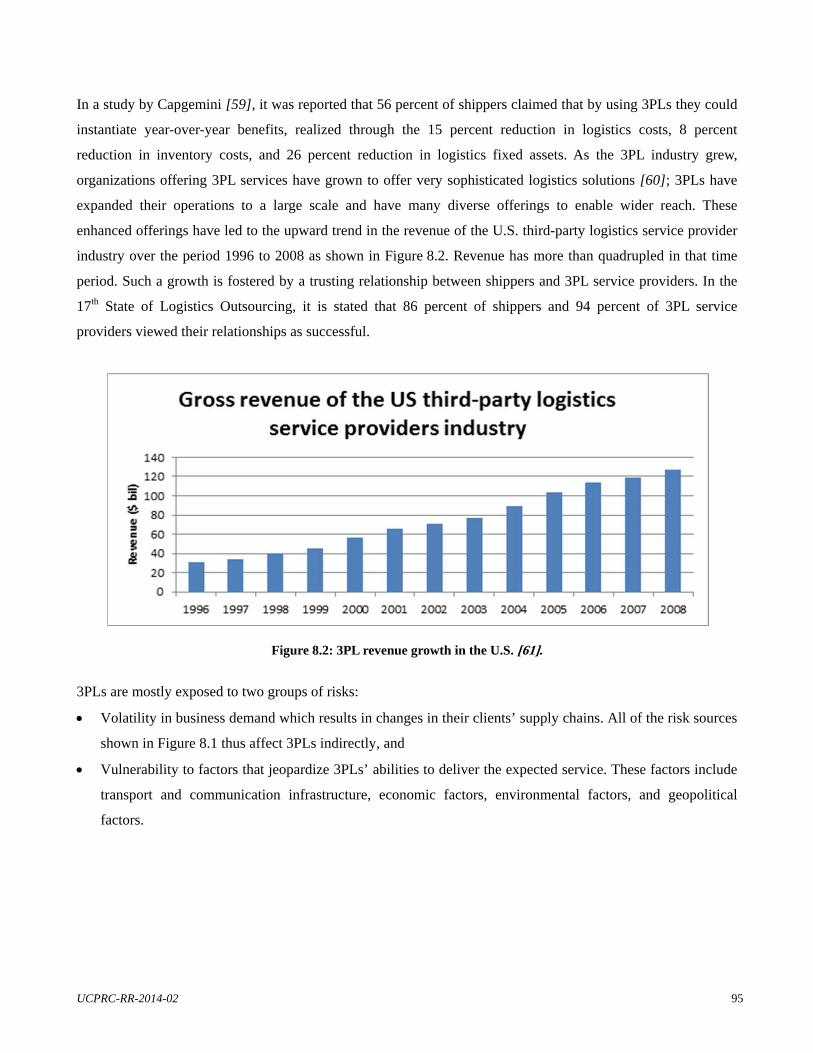

Figure 8.2: 3PL revenue growth in the U.S. [61]. ................................................................................................. 95

Figure 8.3: Typology of supply chain value drivers. ........................................................................................... 100

Figure 8.4: Relationship between the number of facilities and logistics cost. .................................................... 101

Figure 9.1: Economic contribution of the 58 Californian counties in terms of the 10 goods movement dependent

sectors. ................................................................................................................................................. 105

Figure 9.2: Economic contribution of Los Angeles and Orange counties by sector. .......................................... 106

Figure A.1: Summary analysis of all estimated exports originating from or travelling through California in 2011

(Center for Transportation Analysis, 2013). ......................................................................................... 115

Figure A.2: Summary analysis of all estimated imports destined for or travelling through California in 2011

(Center for Transportation Analysis, 2013). ......................................................................................... 116

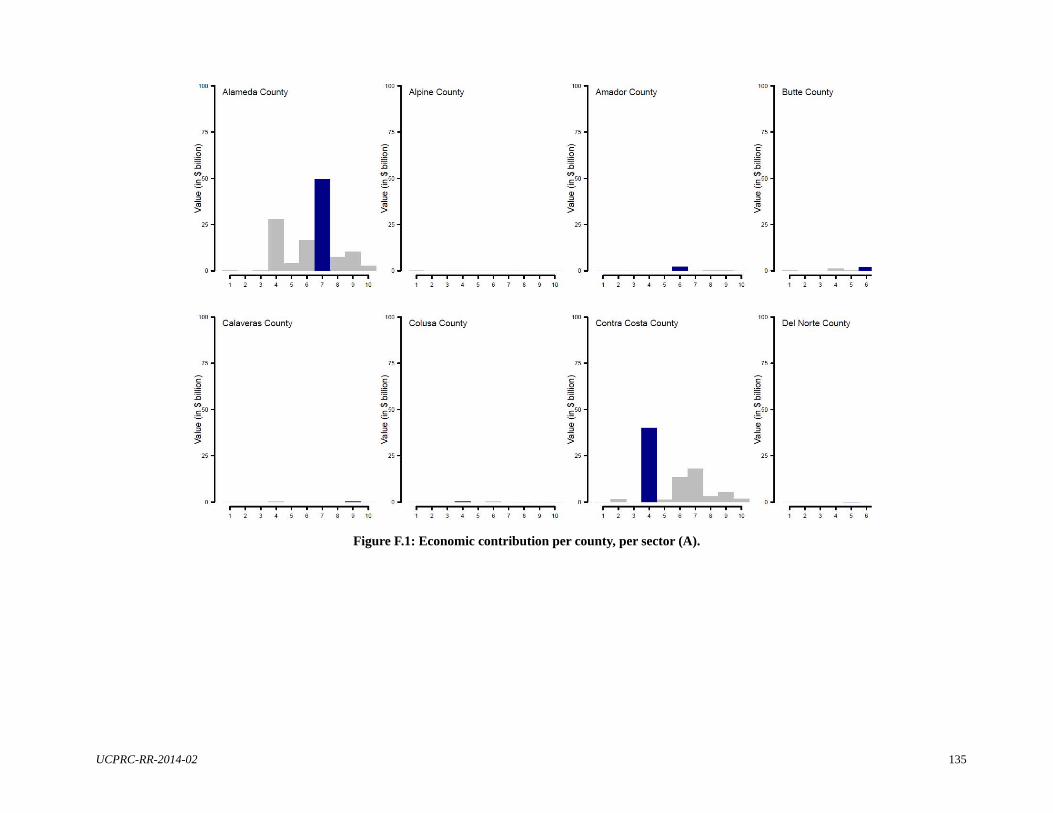

Figure F.1: Economic contribution per county, per sector (A). ........................................................................... 135

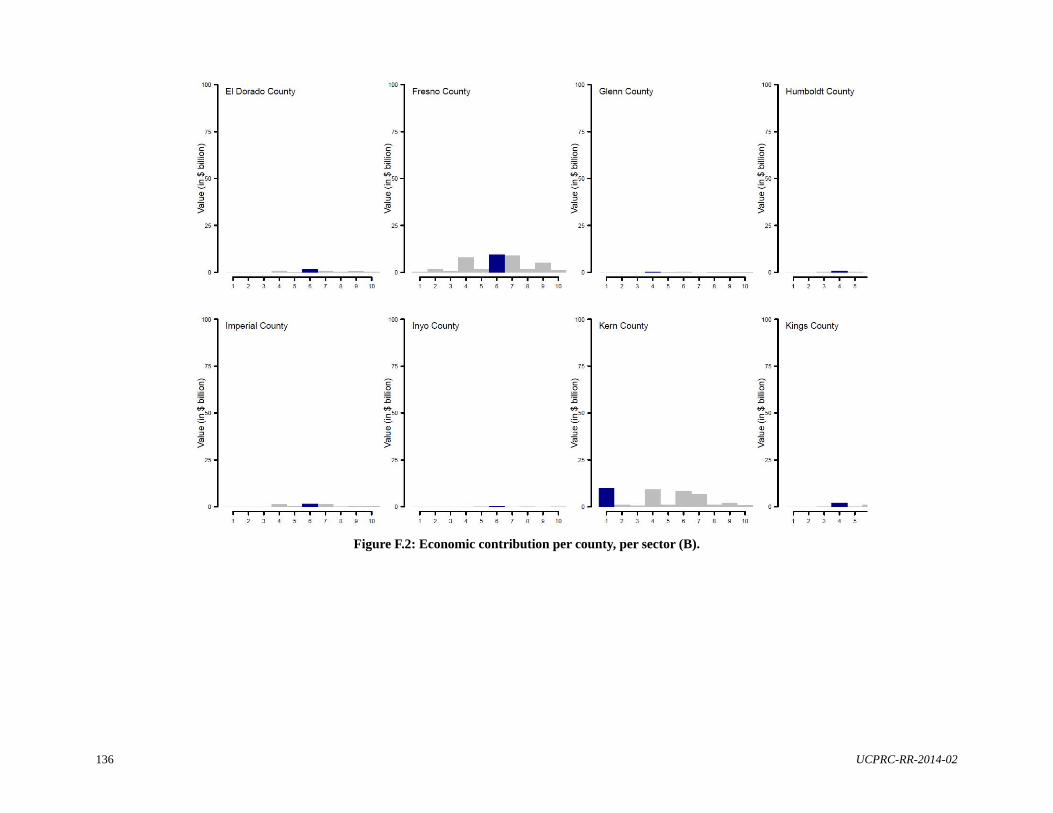

Figure F.2: Economic contribution per county, per sector (B). ........................................................................... 136

Figure F.3: Economic contribution per county, per sector (C). ........................................................................... 137

Figure F.4: Economic contribution per county, per sector (D). ........................................................................... 138

x UCPRC-RR-2014-02

Figure F.5: Economic contribution per county, per sector (E). ........................................................................... 139

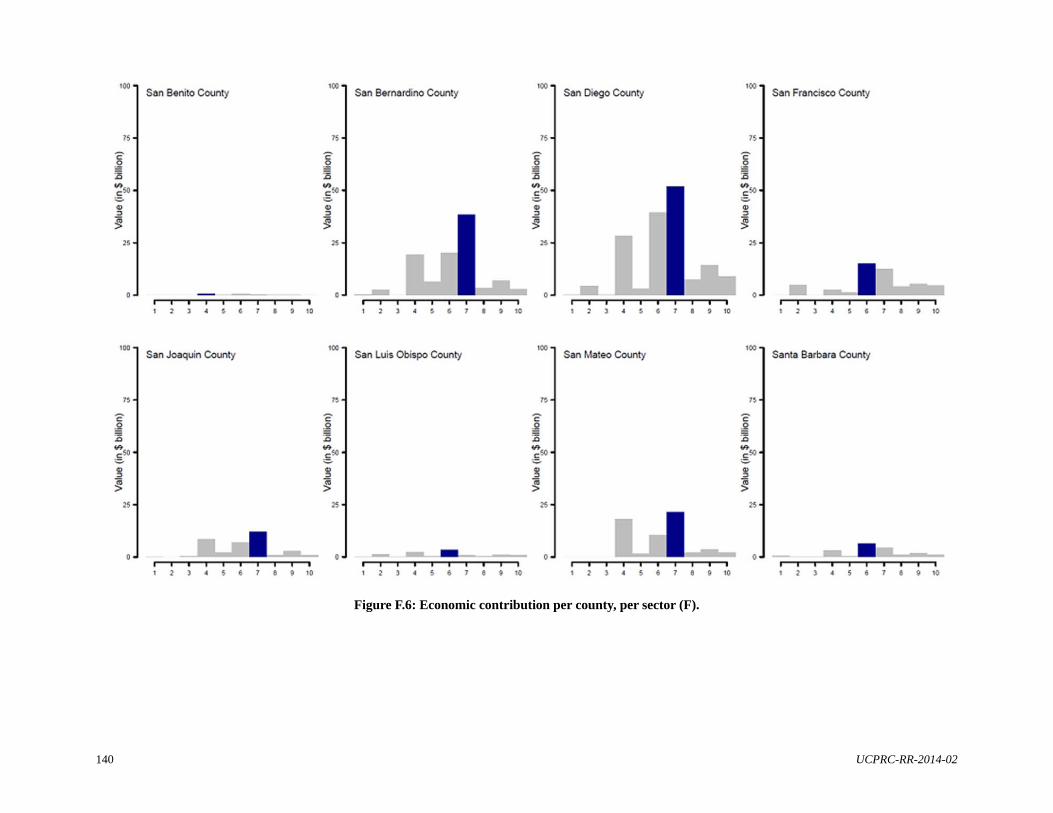

Figure F.6: Economic contribution per county, per sector (F). ........................................................................... 140

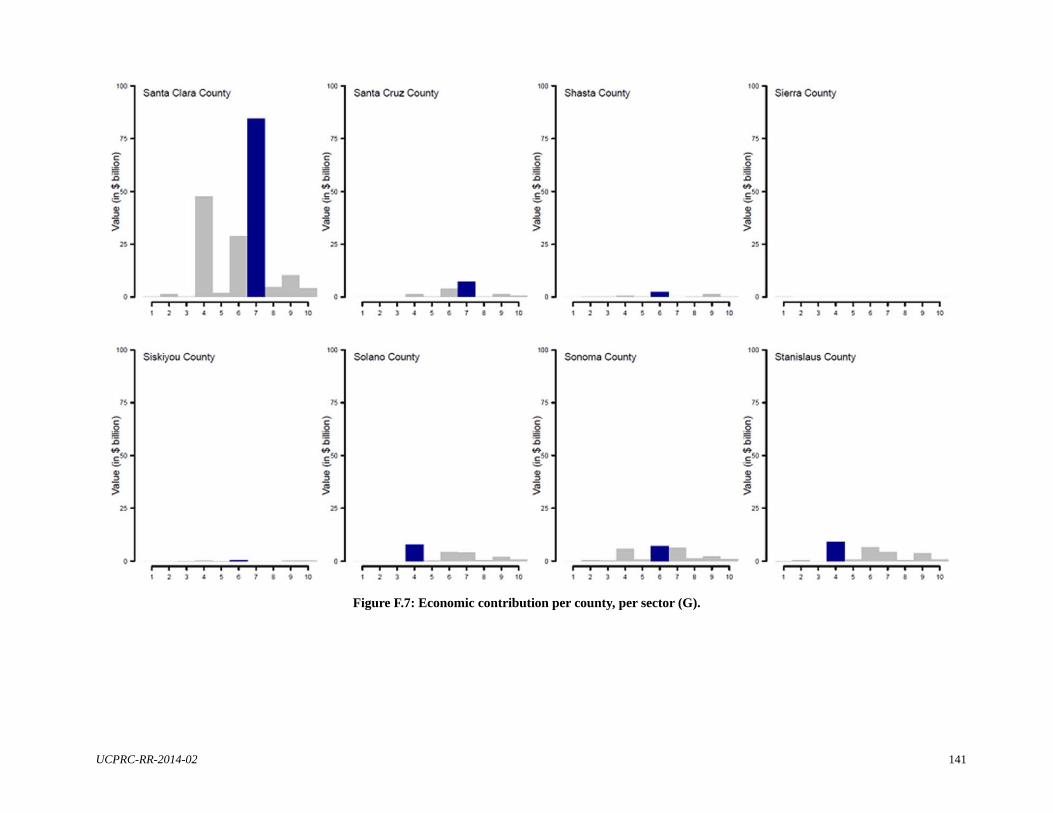

Figure F.7: Economic contribution per county, per sector (G). ........................................................................... 141

Figure F.8: Economic contribution per county, per sector (H). ........................................................................... 142

Figure G.1: List of prominent utility companies in California. ........................................................................... 145

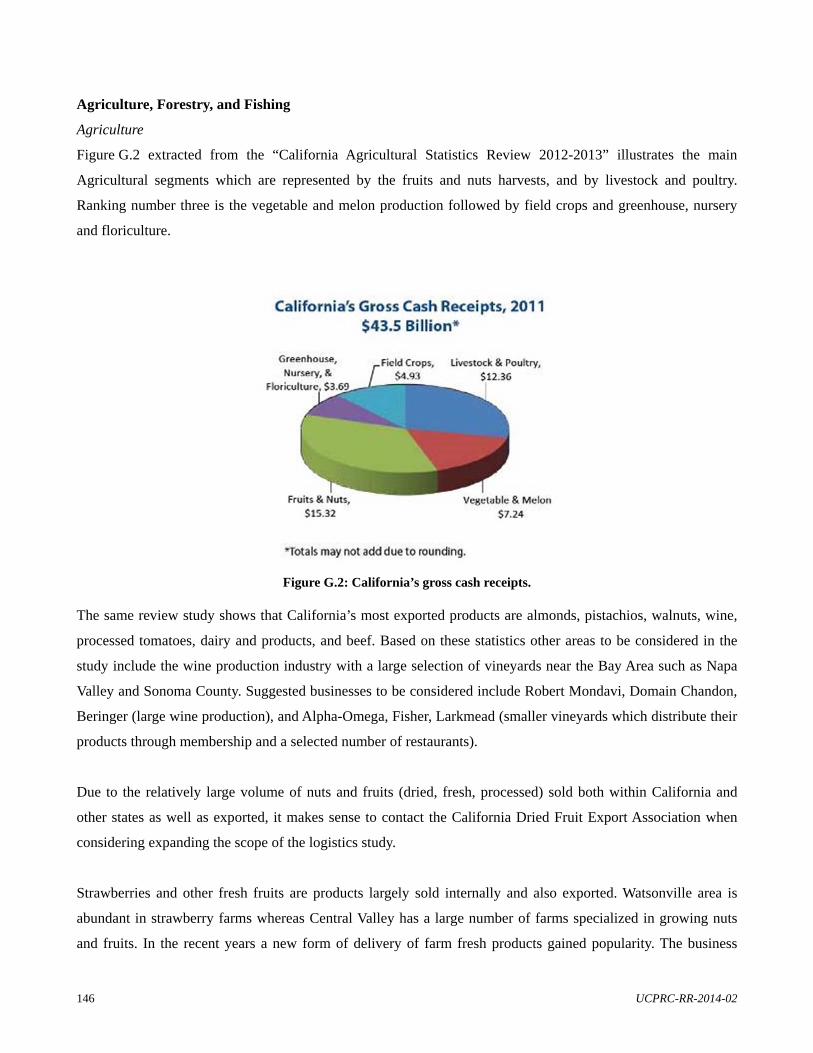

Figure G.2: California’s gross cash receipts. ....................................................................................................... 146

Figure G.3: Wood harvested in California by industry sector. ............................................................................ 148

UCPRC-RR-2014-02 xi

LIST OF TABLES

Table 1.1: Key Differences in Public and Private Sector Freight Decision Making [6] ......................................... 4

Table 1.2: Task Description for Project ................................................................................................................... 6

Table 4.1: Federal Level Public Sector Role Players [7] ...................................................................................... 24

Table 4.2: State-Level Public Sector Role Players [7] .......................................................................................... 25

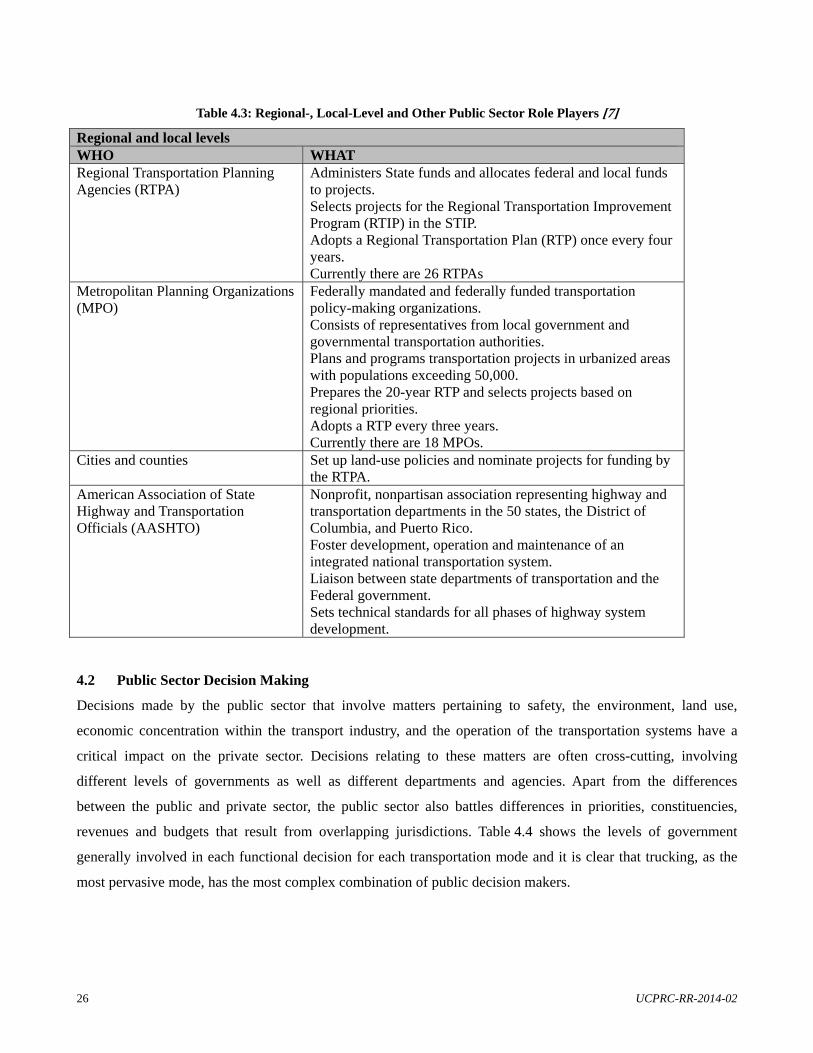

Table 4.3: Regional-, Local-Level and Other Public Sector Role Players [7] ...................................................... 26

Table 4.4: Primary Government Level of Responsibility by Function and Mode [6] .......................................... 27

Table 5.1: The States in Which the Top 40 3PL Providers in North America Are Headquartered [29] ................ 46

Table 6.1: Key Differences in Public and Private Sector Freight Decision Making [6] ....................................... 51

Table 6.2: Timeframe and Hierarchy of Decision Making in Public Sector [6] ................................................... 51

Table 7.1: Different Levels of Business Decisions Investigated During Operational Investigation ..................... 55

Table 8.1: Categories of Major Hazards Facing Agricultural Supply Chains (adapted from [52]) ...................... 88

Table 8.2: Key Findings and Recommendations from the ATRI Study Regarding Agricultural and Food

Commodity Vulnerability to Targeted Attack on Transportation [55] .................................................. 93

Table B.1: GMAP Preliminary Candidate Actions Impacting Road Freight Transportation— Infrastructure

and Operations (BTH and CalEPA, 2007: page I-6) ............................................................................ 117

Table B.2: GMAP Preliminary Candidate Actions Impacting Road Freight Transportation—Public Health

and Environmental Mitigation (BTH and CalEPA, 2007: page I-7 – I-10) .......................................... 118

Table B.3: GMAP Preliminary Candidate Actions Impacting Road Freight Transportation—Community

Impact Mitigation and Workforce Development (BTH and CalEPA, 2007: page I-11 – I-12) ........... 120

Table B.4: GMAP Preliminary Candidate Actions Impacting Road Freight Transportation—Public Safety

and Security (BTH and CalEPA, 2007: page I-13) ............................................................................. 121

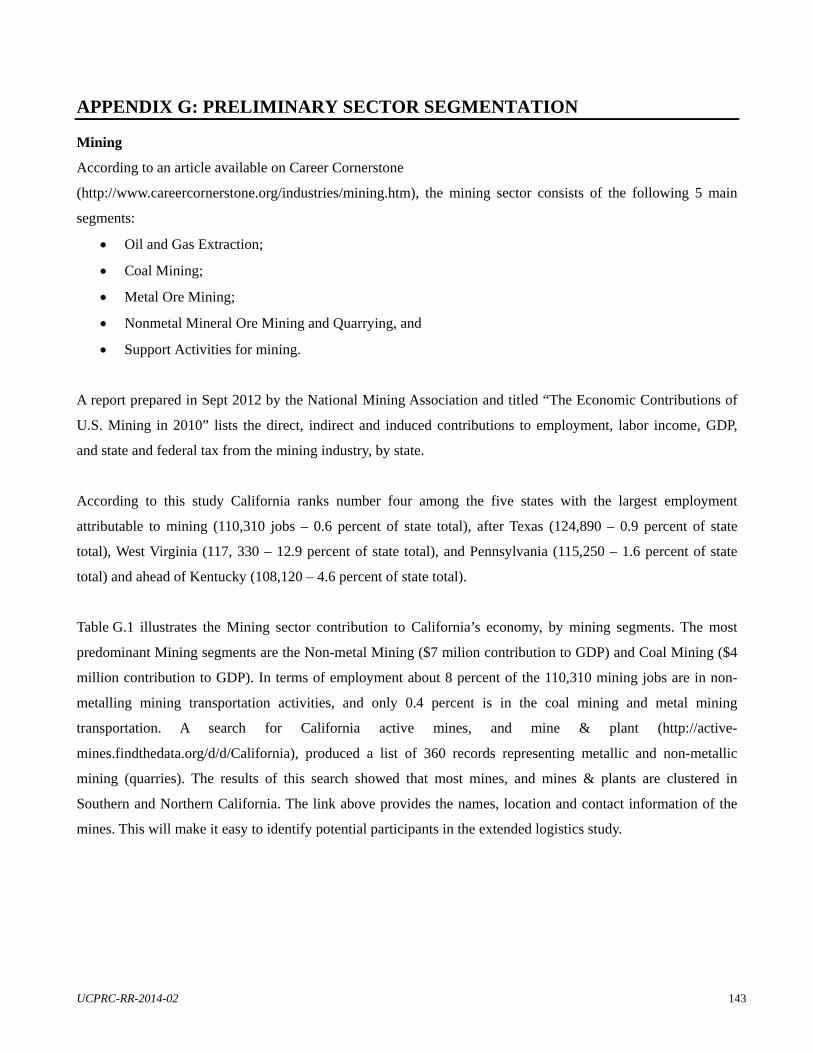

Table G.1: Mining Contribution to the Californian Economy ............................................................................ 144

xii UCPRC-RR-2014-02

DISCLAIMER STATEMENT

This document is disseminated in the interest of information exchange. The contents of this report reflect the

views of the authors who are responsible for the facts and accuracy of the data presented herein. The contents do

not necessarily reflect the official views or policies of the State of California or the Federal Highway

Administration. This publication does not constitute a standard, specification or regulation. This report does not

constitute an endorsement by the Department of any product described herein.

For individuals with sensory disabilities, this document is available in alternate formats. For information, call

(916) 654-8899, TTY 711, or write to California Department of Transportation, Division of Research,

Innovation and System Information, MS-83, P.O. Box 942873, Sacramento, CA 94273-0001.

ACKNOWLEDGMENTS

The authors gratefully acknowledge the comments and input of all the organizations contacted for information

in this project. The authors are especially grateful to the following individuals:

Caltrans technical advisors to the project team: Al Arana (DOTP Office of System Planning), Joanne

McDermott (DOTP Office of Freight Planning);

DOTP Economic Analysis Branch staff: Rose Agacer, Barry Padilla, Seunggeun Paek, and Austin

Hicks.

Division of Transport Planning: Doug MacIvor

DRISI Office of Materials and Infrastructure: Joe Holland and Bill Nokes

UCPRC-RR-2014-02 xiii

PROJECT OBJECTIVES

The objectives of the logistics augmentation study are to:

Provide a basic understanding to Caltrans of private sector decision making in road-freight

transportation;

Identify and describe the comprehensive set of interactions between the efficiency and efficacy of road-

freight transportation and the capacity, performance and regulation of road infrastructure in the state and

recommend which of these interactions warrant more in-depth assessment on a statewide scale to

quantify the overall economic and efficiency impacts that road infrastructure decisions have on the

economy of California, and

Illustrate the value of direct interactions and consultations with private companies in exploring private

sector decision making and the interdependence of these decisions on public sector actions.

The objectives of this report are to summarize the activities and findings of Task L1, Background study and

project inception workshops, and Task L2, Literature review and fieldwork preparation of this study, and to

provide guidance regarding Task L3, Operational investigation (Fieldwork).

xiv UCPRC-RR-2014-02

(This page blank.)

UCPRC-RR-2014-02 xv

EXECUTIVE SUMMARY

The efficient movement of goods within an economy is a crucial lever to competitiveness. Road freight is the

predominant freight transportation mechanism in California, with 78 percent of communities connected

exclusively by road and 88 percent of manufactured goods being transported by truck. The efficiency of road-

freight transportation depends on the capacity and performance of publicly owned and managed road networks

as well on as the capacity and performance of privately owned truck fleets. Growing freight volumes and

increasing demands on freight transportation systems to be reliable, cost efficient, time efficient, flexible and

adaptable have highlighted the importance of the interdependence between the public and private sector in

providing the population with the essential freight systems it requires. Despite the importance of this

interdependence between the public and private sector in road-freight transportation, the divergent decision-

making styles of the two parties hamper collaboration. In essence, the differences between these two parties

arise from the fundamentally different roles they play. The purpose of this logistics augmentation pilot study is

to identify and examine those interdependencies that have particular bearing on road-freight transportation in

California.

SECTION 1: BACKGROUND INVESTIGATION AND LITERATURE STUDY

Overview of California Freight Transportation

Freight transport is the cornerstone of California’s economy, and with 40 percent of freight entering and exiting

the U.S. through California’s sea, land and air gateways, the state’s freight systems are critical to the overall U.S.

economy. A significant component of California’s freight flows arise from through traffic of international

shipments. California is regarded as the breadbasket of the U.S. economy, supplying more than 50 percent of its

agricultural goods, and combined with manufacturing, and especially the high-value manufacturing industries,

California has a freight-heavy economy. The freight growth drivers impacting California are:

The growth in international trade;

Growth in the local consumer population, and

A move towards inventory-pull systems and an increase in manufacturing output.

The four priority freight regions identified in California (Los Angeles/Inland Empire Region, Bay Area Region,

San Diego/Border Region, Central Valley Region) all experience very high levels of road-freight volumes that

result in rapid infrastructure deterioration and congestion. Capacity constraints hamper all transport modes in

California but are especially acute for road infrastructure. Deterioration and aging road infrastructure also pose a

critical problem for freight movement in California. However, there is great opportunity for road-rail intermodal

solutions, specifically long-haul rail services and short-haul rail shuttle services, to reduce congestion and

overall transport costs in California.

xvi UCPRC-RR-2014-02

Public Sector Perspective

The role of the public sector is in the planning, ownership and maintenance of road-freight infrastructure as well

as in creating the economic environment within which private entities operate through regulations. There are key

role players on every level of government that directly impact road-freight transportation in California. Key

drivers of public sector decision making include investment and financing, economic regulation, providing and

maintaining infrastructure, land use, environmental issues, safety, operations and jobs and employment.

State-level strategic plans that hold particular relevance for this study are the California Transportation Plan

2025, the California State Rail Plan 2007-08 to 2017-18 and the Goods Movement Action Plan. The recent San

Joaquin Valley Interregional Goods Movement Plan and the Central Coast California Commercial Flows Study

are also of particular interest as they followed a directed and successful private and public sector engagement

approach in identifying and prioritizing regional freight challenges and projects. In addition, the 2010 Regional

Transportation Plan Guidelines are explicit about freight modeling requirements and cooperation and

collaboration requirements for Regional Transport Plans. The move towards activity-based freight models will

provide better decision support and it will also require a far better understanding of private sector operations and

decision making, as well as extensive access to private sector data; this will not be achieved without close

cooperation and collaboration with a large number of private companies. The guidelines now also require

explicit private sector involvement in the formulation of regional plans, similar to the extensive public

participation processes currently employed during the development of plans. Insights and findings relevant to

road-freight transportation were extracted from a selected number of Regional Transport Plans relevant to the

operational investigation that will be conducted in Task L3 of this pilot study.

Private Sector Perspective

The role of the private sector is to generate earnings for shareholders through the selling of goods and services.

In fulfilling this role, the private sector is a user of the available road-freight systems to transport goods in the

most competitive manner possible. Private sector decisions can be strategic (long-term), operational (short- to

medium-term) or tactical (short-term) in nature. The key decision drivers that cut across all levels of private

sector decisions are market and shipper demand, financial performance metrics, efficient operational

management, and regulatory issues.

Outsourcing is a growing logistics trend even despite tough market conditions and the growing volatility of

logistics chains. Outsourcing practices obscure the locus of control for many logistics decisions in the private

sector. These days, shippers are demanding disruptive innovation from third-party logistics (3PL) providers,

which requires real-time information technology solutions and the ability to extract business value from big

data—and herein lies an opportunity for the public sector to collaborate with the private sector and obtain the

data required for accurate freight modeling.

UCPRC-RR-2014-02 xvii

The move toward inventory-pull systems is greatly increasing the demand for transportation, generally negating

the benefits of economies of scale. Higher-value inventory is being reduced at the cost of increasing lower-value

transport activities. However, this trend greatly contributes to congestion and emissions, especially in urban

areas where the e-commerce industry has skyrocketed.

The need for road-rail intermodal services is increasingly apparent among rising fuel costs, increased congestion

and escalating environmental pressures. But for intermodal solutions to be viable alternatives to door-to-door

trucking requires efficient and reliable rail service (akin to trucking performance) and efficient and aptly located

intermodal terminals.

Some trends in the trucking industry also have bearing on the efficiency of road-freight transport in California.

In particular, the disaggregated nature of the industry, with 90 percent of motor carriers having six or less power

units, has a distinct impact on private sector decision making and behavior. Fleet capacity constraints caused by

driver shortages and increased regulation of driver working conditions and vehicles is anticipated to become a

major choke point for the logistics industry in the future. Road congestion is also especially rife in California

with dire consequences to trucking competitiveness. Fifteen of the 250 truck bottlenecks identified by the

Federal Highway Administration (FHWA) and American Transportation Research Institute (ATRI) in the U.S.

are in California [1].

Interdependence of Public and Private Decisions

Differences in decision-making paradigms between the public and private sector arise from their fundamentally

different roles and objectives when engaging with road-freight systems. Particular differences relate to the

following decision characteristics: scale of investment, geography, the process whereby decisions are reached,

planning horizons and timing, the objectives of decisions and the decision-making attitude. Recommendations

for successful private-public interactions based on case studies conducted by the National Cooperative Freight

Research Program (NCFRP) highlight the importance of communication, education and appreciation between

the two parties.

SECTION 2: CASE STUDY RESEARCH REGARDING THE INTERSECTION OF SUPPLY CHAINS AND

ROAD INFRASTRUCTURE AND REGULATION

Section 2 of this study is specifically targeted to apprise Caltrans (public sector) of the practical ways in which

California road infrastructure and regulations affect daily supply chain management practices within specific

economic sectors.

xviii UCPRC-RR-2014-02

Task L3: Operational Investigation

Within the scope of this pilot study, the operational investigation served to show how the case study method

could yield useful practical insights for specific industries when founded on a comprehensive literature review.

Narrowing the focus to road-freight systems under the jurisdiction of Caltrans, this operational investigation

explores and describes the practical elements of the interdependence between the public and private sector by

observing operations at companies and conducting structured interviews with private sector managers. A case

study approach is used for this exploratory and descriptive investigation. In order to validate the empirical

evidence from the case studies, the findings will be tested against the literature review and various triangulation

methods have been designed into the case study methodology. Explicit privacy and confidentiality protocols

were also developed to safeguard the anonymity and confidentiality of the companies that participated in this

study. Operational investigations were conducted at two companies, Company A and Company B.

Company A

Company A is in the agricultural and food processing sector. Its primary business is the production of a range of

bulk food products from fresh produce. The company harvests its own fresh produce from farms in northern and

southern California and it leases and operates a truck fleet that transports the produce from the farms to the

processing facilities. The company also owns and operates a number of processing and storage facilities in

California, and its transport division handles the staging of empty tins and packaging materials between these

facilities. Company A’s transport division also handles some deliveries of finished products to customers. The

operational investigation of Company A was conducted over three days, May15, 16, and 17, 2013.

The scope of business operations and resource planning in Company A hinges on the seasonality of the fresh

produce. This is typical of agricultural supply chains where the harvesting cycle sets the tempo for downstream

logistics activities. Due to peak-season surges in supply and the fact that there is no inventory buffer between the

inbound logistics and the processing facilities, the timing and efficiency of inbound logistics are critical. Road

works and traffic congestion pose the greatest threat to the efficiency of inbound logistics.

Outbound logistics efficiency is decoupled from processing plant operations by a significant inventory buffer.

Although outbound logistics efficiency does not affect plant operations, it is still important from a cost-saving

and customer service point-of-view. The biggest threat to outbound logistics efficiency is erratic customer

orders.

Drivers are highly motivated as a result of the following organizational practices:

None of the drivers at Company A are unionized;

Drivers are all paid per load and distance (not per hour), and

The majority of drivers are employed seasonally with stringent recruitment/readmission criteria.

UCPRC-RR-2014-02 xix

Compliance, Safety, Accountability (CSA) regulations are strictly enforced using an On Board Computer (OBC)

system and there is no leniency for safety or regulatory violations. Three factors that dampen driver morale are

situations where drivers believe they are not being fully utilized (and therefore not accruing maximum earnings),

physical comfort while driving, and road safety. Rough road conditions increase driver discomfort and physical

fatigue. The short merging lanes on some highways and the mixing of passenger and truck traffic both pose

significant road safety hazards and frustrate the drivers. Drivers generally know the predetermined routes by

heart, and when traffic is diverted from these routes (due to road works or accidents) it can be tricky to

recalculate the shortest route while taking into consideration prevailing route restrictions. As key motivators,

drivers cited their love of driving, the freedom and independence of driving their own truck, and their self-

determination.

A successful example of public-private interaction is where one of the processing plants joined forces with other

companies in the area to contribute financially to the upkeep and maintenance of the rural road leading to their

facilities. This ensured that local agencies promptly attend to road repairs. Other than this initiative, Company A

had minimal interaction with public agencies. The Senior Manager agreed that there would definitely be mutual

benefit to more structured interaction between public and private agencies, and he indicated willingness to

dedicate a couple of days to such initiatives. A quick-win in this regard would be better communication

regarding the scheduling of road works during peak-season, as these could greatly disrupt inbound logistics.

Road infrastructure considerations contribute marginally to Company A’s decisions regarding whether to take on

certain customers or suppliers; this is a strategic-level decision. On the operational and tactical levels, the daily

scheduling and routing of pickups and deliveries are affected by road works and congestion while CSA

regulations affect driver management and trip planning.

Company B

Company B is an asset-based motor carrier with two primary business streams:

Consolidating less-than-truckload (LTL) shipments from the continental U.S. for shipment to Canadian

terminals, and

Domestic LTL shipments across the continental U.S.

Company B has a number of terminals within its network in the U.S. as well as partner terminals in Canada and

the U.S. The California terminal where the researchers conducted their operational investigation has an

additional business stream that was inherited from the company that previously operated from that terminal and

it is unique within Company B’s network. This business stream is the pickup and delivery of intrastate LTL

freight. The operational investigation of Company B was conducted over two days, May 21 and 22, 2013.

xx UCPRC-RR-2014-02

LTL shippers need to be very flexible and adaptable to serve their customer’s transport needs amid volatile

business cycles. The efficacy and efficiency of the consolidation and synchronization of shipments is critical in

keeping costs and lead times down. Achieving this requires constant coordination and communication among

the terminals in the network and thus the physical structure of the network, i.e., the location of terminal facilities

and their interconnectivity , greatly influences the business’s performance.

Drivers are permanently employed by Company B, are paid by the hour (and compensated for distance) and are

not unionized. Drivers that can adhere to Company B’s stringent safety requirements and have the right

credentials for CSA accreditation are in short supply. CSA accreditation is essential for drivers crossing the

Canadian border. Drivers cite the thrill of driving and the freedom and autonomy of truck driving as primary

motivators. Meanwhile, road safety, congestion and waiting at client terminals cause great frustration. Drivers at

Company B also state that the short merging lanes and mixing of passenger and truck traffic are road safety

hazards and they suggest truck-only lanes. Narrow streets and driveways and a lack of truck parking also cause

great frustration when executing pickups and deliveries in urban areas. Drivers noted a clear difference in road

conditions between California and neighboring states, and reported that rougher road conditions affect their

driving comfort and fatigue.

Road regulation hampers Company B’s operations, especially when compared with other states. Firstly, the

process to register new trucks is reportedly cumbersome. Secondly, the implementation schedule of the new

environmental efficiency regulations for trucks is forcing Company B to retire trucks long before their 750,000

mile cut-off point, causing severe financial repercussions. The excessive inspections performed on trucks also

waste a lot of time. While the content of environmental and road safety regulations are supported in principle,

their implementation causes operational inefficiencies. Route restrictions in Northern California are considered

excessive and are causing severe traffic chokepoints in the Bay Area. Company B makes two pertinent

suggestions regarding road regulations: allowing triple trailers and opening of the road to trucks through truck-

only lanes and the lifting of route restrictions.

Road infrastructure and regulation can play a key role in deciding where to build a network terminal, which is a

strategic level decision. Conversely, although congestion, road works and road conditions frustrate drivers and

managers, these factors do not seem to affect actual operational and tactical level decisions.

The issues uncovered and suggestions made during the case studies were congruent with those challenges

identified and projects prioritized in the San Joaquin Valley Interregional Goods Movement Plan.

UCPRC-RR-2014-02 xxi

Supply Chain Design and Vulnerability

Transport infrastructure and regulation affects the supply chain in two ways:

The design, location, performance and regulation of transport infrastructure are critical inputs to the

design of the supply chain network, and

The propensity of transport disruptions and delays caused by infrastructure failure contributes to overall

supply chain vulnerability.

There are three classes of supply chain risk sources, namely demand-side risk sources, supply-side risk sources,

and supply chain structure risk sources. Road infrastructure and regulation can render supply chains more

vulnerable to these risk sources on three levels—on the product or process level, on the asset and infrastructure

dependency level, or on the operating environment level. The analysis of how road infrastructure and regulation

affects supply chain vulnerability was conducted considering industry/economic sector aggregation. In this pilot

study, two of the ten goods movement-dependent economic sectors of California were considered in case

studies, namely the Agriculture, Forestry and Fishing sector and the Transportation and Warehousing sector.

The major hazards facing the agricultural industry in general are broad-based, contributing to each one of the

three supply chain risk source categories. In the case of Company A, weather-related hazards, natural disasters

and biological or environmental hazards can have a great impact because all of their suppliers are geographically

concentrated. Logistics and infrastructure hazards are also especially detrimental due to the perishable nature of

its products and the seasonal pressures of inbound logistics. Agricultural products are generally low margin

products and thus changes in input costs (such as energy or transport costs) can be debilitating. Transport

efficiency plays a tremendous role in ensuring that product is not lost and that costs are kept low. In addition,

studies have shown that food supply chains are very vulnerable to terrorist attacks and that targeting the

transport function (either through jeopardizing infrastructure or vehicles) would be the most effective way to

undermine these supply chains.

The Transport and Warehousing sector is comprised mostly of third-party logistics (3PL) companies to whom

one or more logistics activity has been outsourced. The U.S. 3PL sector has grown significantly, with revenue

quadrupling between 1996 and 2008. 3PL companies are mostly exposed to two groups of risks: volatility in

business demand as a result of any one of the previously mentioned risk sources in their clients’ supply chains;

and vulnerability to factors that jeopardize 3PLs’ abilities to deliver the expected service. The factors that could

seriously jeopardize 3PLs’ abilities to deliver the expected service are related to transport infrastructure,

communication infrastructure, economic volatility, environmental regulation, and geopolitical unrest. Given

California’s heavy dependence on road infrastructure, even short-term delays or capacity constrictions caused by

congestion or construction could be detrimental to the 3PL industry, not just the large-scale disruptions caused

xxii UCPRC-RR-2014-02

by, for example, terrorist attacks or earthquakes. The implementation of ever-stricter environmental regulation

also places severe financial and operational burdens on Company B and other asset-based motor carriers.

Supply chain network design is also significantly affected by transport infrastructure and regulation. Supply

chain network design has been defined by Klibi et al. [2] as the “strategic decisions on the number, location,

capacity and mission of production-distribution facilities in a company, or of a set of collaborating companies, in

order to provide goods to a predetermined, but possibly evolving, customer base. It also involves decisions

related to the selection of suppliers, subcontractors and 3PLs, and to the offers to make to product-markets.”

During supply chain network design, a number of value drivers have to be balanced among many diverse supply

chain organizations. These value drivers are related to revenue (customer service, product, market coverage),

cost (product cost, logistics cost, overheads), and capital expenditures (network investments, value of current

assets). Transport infrastructure and regulation affect revenue by impacting customer service, product

availability, and potential market coverage. In addition, transport costs are the greatest drivers of logistics costs

and are heavily influenced by the design, location and performance of infrastructure as well as the cost of

adhering to regulations. Lastly, infrastructure and regulation affect decisions regarding facility location (capital

expenditures).

The Spread of Economic Sectors in California and Implications for Road Infrastructure and Regulation

Ten of the economic sectors identified by the United State Census Bureau are considered goods movement-

dependent economic sectors, namely:

Mining;

Utilities;

Agriculture, Forestry and Fishing;

Manufacturing;

Transportation and Warehousing;

Retail Trade;

Wholesale Trade;

Waste Management;

Health Care and Social Assistance, and

Accommodation and Food Services

The supply chain design and vulnerability factors relevant within each of these economic sectors varies greatly

and thus the manner in which road infrastructure and regulation affects each of these sectors also varies. The

Agriculture, Forestry and Fishing and Transport and Warehousing sectors have been discussed in this pilot study

based on the case study findings. Analysis of the other eight sectors is beyond the scope of this pilot study. It is

UCPRC-RR-2014-02 xxiii

critical for Caltrans to be aware of which sectors are present in which counties and the size of those sectors.

Having this awareness could alert Caltrans to the potential impact of certain road infrastructure and regulation

decisions on the various sectors present and spur collaboration with private industry to mitigate potential

negative effects.

Analysis of these economic sectors within the 58 Californian counties was based on the economic values

reported by the United States Census Bureau’s American Fact Finder tool. (Economic contribution was

considered instead of tons transported to ascertain a better picture of the potential economic impact of supply

chains in these sectors.) Los Angeles, Orange, Santa Clara, Alameda and San Diego are the five most prominent

counties, with wholesale trade, retail trade and manufacturing contributing most to these counties’ economic

well-being. Individual county analyses for all 58 counties are presented in the technical appendices.

CONCLUSIONS AND WAY FORWARD

This study has shown through desktop studies, qualitative analysis, and case studies that road infrastructure and

regulation, as managed by Caltrans, has a marked impact on supply chain operations and strategies. This is one

instance where public sector decision making greatly influences private sector decision making. The analysis has

shown that, in this instance, the reciprocal influence of private sector decision making on public sector decision

making is not as significant. Given the critical role that supply chains play in the economic well-being and

quality of life in California and the dependence of these supply chains on road infrastructure and regulation, it is

imperative that the public sector (Caltrans) and private sector are engage throughout the planning and

construction of road infrastructure as well as during the drafting and implementation of policy. There have been

a few successful efforts in this regard, for example in the recent establishment of the California Freight Advisory

Committee and in the deliberate and interactive inclusion of the private sector stakeholders during drafting of

the San Joaquin Valley (SJV) Interregional Good Movement Plan.

The first step in more meaningful engagement between Caltrans and the private sector is an adequate

understanding of how and when road infrastructure and regulation influence supply chains. In this pilot study, it

has been identified that road infrastructure and regulation have a direct effect on supply chain vulnerability and

design, and that private companies make decisions that take these two elements into consideration. However,

supply chain vulnerability and design are different for each economic goods movement-dependent sector and

therefore a blanket approach would not suffice.

xxiv UCPRC-RR-2014-02

This pilot study presented the methodology for a sector-by-sector analysis that can inform Caltrans regarding the

intricacies and considerations of supply chain vulnerability and design in different sectors. The scope of the pilot

study was limited in the following terms:

Only two of the ten identified goods movement-dependent sectors were analyzed, namely the

Agriculture, Forestry and Fishing sector and the Transportation and Warehousing sector, and

Case studies were only conducted at one company in each of the sectors mentioned above.

In order for this study to be comprehensive enough to form part of routine Caltrans decision making regarding

road infrastructure and regulation, its scope needs to be expanded to cover all goods movement-dependent

sectors and it also needs to be deepened by conducting a representative ensemble of case studies in each sector.

UCPRC-RR-2014-02 xxv

LIST OF ABBREVIATIONS

3PL Third-party logistics

AASHTO American Association of State Highway and Transportation Officials

ARTBA American Road & Transportation Builders Association

ATA American Trucking Association

ATRI American Transportation Research Institute

Caltrans California Department of Transportation

CSA Compliance, Safety, Accountability

CSRP California State Rail Plan

CTA California Trucking Association

CTP California Transportation Plan 2025

EXW Ex Works

FAST Freight Action Strategy Taskforce

FHWA Federal Highway Administration

FOB Free on Board

GMAP Goods Movement Action Plan

GPS General Pavement Studies

ICC International Chamber of Commerce

MPO Metropolitan Planning Organizations

NCFRP National Cooperative Freight Research Program

OBC On Board Computer

PPRC SPE Partnered Pavement Research Center Strategic Plan Element

RTP Regional Transportation Plan

RTPA Regional Transportation Planning Agencies

SCAG Southern California Association of Governments

SCN Supply Chain Network

TEU Twenty-foot Equivalent Unit container

UCPRC University of California Pavement Research Center

USDA United States Department of Agriculture

xxvi UCPRC-RR-2014-02

SI* (MODERN METRIC) CONVERSION FACTORS APPROXIMATE CONVERSIONS TO SI UNITS

Symbol When You Know Multiply By To Find Symbol LENGTH

in inches 25.4 Millimeters mm ft feet 0.305 Meters m yd yards 0.914 Meters m mi miles 1.61 Kilometers Km

AREAin2 square inches 645.2 Square millimeters mm2

ft2 square feet 0.093 Square meters m2 yd2 square yard 0.836 Square meters m2

ac acres 0.405 Hectares ha mi2 square miles 2.59 Square kilometers km2

VOLUMEfl oz fluid ounces 29.57 Milliliters mL gal gallons 3.785 Liters L ft3 cubic feet 0.028 cubic meters m3 yd3 cubic yards 0.765 cubic meters m3

NOTE: volumes greater than 1000 L shall be shown in m3

MASSoz ounces 28.35 Grams g lb pounds 0.454 Kilograms kg T short tons (2000 lb) 0.907 megagrams (or "metric ton") Mg (or "t")

TEMPERATURE (exact degrees)°F Fahrenheit 5 (F-32)/9 Celsius °C

or (F-32)/1.8

ILLUMINATION fc foot-candles 10.76 Lux lx fl foot-Lamberts 3.426 candela/m2 cd/m2

FORCE and PRESSURE or STRESS lbf poundforce 4.45 Newtons N lbf/in2 poundforce per square inch 6.89 Kilopascals kPa

APPROXIMATE CONVERSIONS FROM SI UNITS

Symbol When You Know Multiply By To Find Symbol LENGTH

mm millimeters 0.039 Inches in m meters 3.28 Feet ft m meters 1.09 Yards yd km kilometers 0.621 Miles mi

AREAmm2 square millimeters 0.0016 square inches in2

m2 square meters 10.764 square feet ft2

m2 square meters 1.195 square yards yd2 ha Hectares 2.47 Acres ac km2 square kilometers 0.386 square miles mi2

VOLUMEmL Milliliters 0.034 fluid ounces fl oz L liters 0.264 Gallons gal m3 cubic meters 35.314 cubic feet ft3

m3 cubic meters 1.307 cubic yards yd3

MASSg grams 0.035 Ounces oz kg kilograms 2.202 Pounds lb Mg (or "t") megagrams (or "metric ton") 1.103 short tons (2000 lb) T

TEMPERATURE (exact degrees) °C Celsius 1.8C+32 Fahrenheit °F

ILLUMINATION lx lux 0.0929 foot-candles fc cd/m2 candela/m2 0.2919 foot-Lamberts fl

FORCE and PRESSURE or STRESSN newtons 0.225 Poundforce lbf kPa kilopascals 0.145 poundforce per square inch lbf/in2

*SI is the symbol for the International System of Units. Appropriate rounding should be made to comply with Section 4 of ASTM E380 (Revised March 2003).

UCPRC-RR-2014-02 1

SECTION 1: BACKGROUND INVESTIGATION AND

LITERATURE STUDY

2 UCPRC-RR-2014-02

UCPRC-RR-2014-02 3

1 INTRODUCTION

1.1 Background to the Logistics Augmentation Study

The topic of the logistics augmentation study originated from the Pilot Study Investigating the Interaction and

Effects for State Highway Pavements, Trucks, Freight and Logistics (hereafter referred to as the Vehicle-

Pavement Interaction Pilot Study).

One of the tasks of the Vehicle-Pavement Interaction Pilot Study entailed, among its other elements, was the

investigation of how rough road conditions could impact the logistics activities of cargo owners through its

contribution to cargo damage during transportation. This work led to discussions regarding the interface between

the public and private sectors in road-freight transportation, which made it apparent that there is a need for

Caltrans to better understand the road-freight users they serve. This pilot study was conceptualized based on

these discussions, and it was deemed appropriate to conduct the study as a value-adding funding augmentation

to the Vehicle-Pavement Interaction Pilot Study.

1.2 The Interface Between the Public and Private Sector in Road Freight Systems

The efficient movement of goods within an economy is a crucial lever to competitiveness. The impact that the

efficiency of logistics activities, especially the cost of logistics, has on the cost of doing business within a

specific region is a topic of ongoing study worldwide [3, 4, 5]. Road freight transportation is a significant

element of logistics activities in California with 78 percent of communities depending exclusively on trucks to

transport their goods and 88 percent of all manufactured tonnage in the state being moved on trucks [1]. Road

freight transportation is the predominant freight transport mode in California and it is used for long-haul

shipments, interregional transport and last-mile or urban distribution. It serves all industries and is a critical link

in any intermodal logistics chain. The efficiency of road-freight transportation is dependent on the capacity and

performance of the publicly owned and managed road networks, as well as on the capacity and performance of

privately owned truck fleets.

California’s growing population and growing economy place increasing strain on existing (and aging) road

infrastructure in the state. One results of this is that rapidly growing populations of passenger and freight road

users are colliding in a daily battle for space on the road. The impact of congestion on passenger travel and

perceived quality of life has been extensively studied in transport planning. However, there is far less

appreciation for the impact of congestion on the trucking industry. A study conducted by Golob and Regan

(2000) reported that more than 80 percent of managers of trucking operations cited highway congestion as a

serious to critical problem. The five aspects that affect their business in particular are slow average speeds,

4 UCPRC-RR-2014-02

unreliable travel times, increased driver frustration and lower morale, higher fuel and maintenance costs, and

higher accident and insurance costs. Other issues that impact road-freight efficiency are the deteriorating

condition of road infrastructure (exacerbated by increased traffic volumes), increasing route restrictions and

efficiency of shared infrastructure, such as intermodal terminals.

Growing freight volumes and the increasing demands on freight transportation systems to be reliable, cost

efficient, time efficient, flexible and adaptable are highlighting the importance of the interdependence between

the public and private sector in providing the population with the essential freight systems it requires. As the

NCFRP report Public and Private Sector Interdependence in Freight Transportation Markets succinctly states:

“With excess capacity on public portions of the system used up and increasing security and environmental

regulations, the public sector-related constraints on freight have become more important for the private sector’s

operations and planning” [6].

Despite the importance of this interdependence between the public and private sector in road-freight

transportation, the divergent decision-making styles between the two parties hamper collaboration. In essence,

the differences between these two parties arise from the fundamentally different roles they play. The public

sector in California is the owner and custodian of road infrastructure, aiming to provide “a safe, sustainable,

world-class transportation system that provides for mobility and accessibility of people, goods, services, and

information through an integrated, multimodal network that is developed through collaboration and achieves a

Prosperous Economy, a Quality Environment, and Social Equity” [7]. The private sector, on the other hand, uses

the road network to transport the goods and services that are the lifeblood of the economy. Their objective is the

bottom line, generating revenue and competing in a cutthroat environment against local and global businesses

for market share. These divergent objectives lead to divergent decision making as illustrated in Table 1.1.

Table 1.1: Key Differences in Public and Private Sector Freight Decision Making [6]

Differences Public Sector Private Sector

Scale of investment Entire system within its jurisdiction

One company at a time but international

Geography U.S. political boundary Global market Process of reaching decisions Collaborative Hierarchical Planning horizons and timing Longer-run, slower Shorter-run, quicker

Objectives and decisions Social and political as well as economic development

Increase shareholder value through higher profits/revenues

Attitudes Attempts to address all stakeholder concerns

Satisfy owners, customers and employees

UCPRC-RR-2014-02 5

The fact that these two parties have different objectives and divergent decision-making styles is not the root

cause to be addressed, instead it is the lack of understanding between these two parties that creates problems in

road-freight transportation. It is generally recognized that public sector agencies are unfamiliar with private

sector operations and planning [8] and of the ways that public sector decision making affects private sector

operations and planning activities [6]. This leads to situations where public agencies develop road infrastructure

plans and policies without an accurate understanding of how those plans and policies will affect daily business

operations and, consequently, of how the private sector will adapt.

Much research has been done on a conceptual level regarding the relationship between the public and private

sector, their divergent decision-making styles and how this affects freight transportation. This pilot study takes a

far more practical approach to identifying and describing those particular interdependencies affecting road-

freight transportation in the state of California.

1.3 Objectives of the Logistics Augmentation Study

The objectives of this study are to:

Provide a basic understanding to Caltrans of private sector decision making in road-freight

transportation;

Identify and describe the comprehensive set of interactions between the efficiency and efficacy of road-

freight transportation and the capacity, performance and regulation of road infrastructure, in the state

and recommend which of these interactions warrant more in-depth assessment on a state-wide scale to

quantify the overall economic and efficiency impact road infrastructure decisions have on the economy

of California, and

Illustrate the value of direct interactions and consultations with private companies in exploring private

sector decision making and the interdependence of these decisions on public sector actions.

1.4 Scope of the Logistics Augmentation Study

This logistics augmentation study is an exploratory study of the interdependencies between public and private

sector decision making relating to road-freight transportation in the state of California. In particular, it

investigates private sector decisions, on a strategic, operational and tactical level, that are affected by the current

road infrastructure in California as well as by road-freight regulation. This study will identify and explore

specific interdependencies through an operational investigation of a limited number of companies to illustrate