lock-up agreement and updated materials

TRANSCRIPT

25th March 2021

Lock-Up Agreement and

Updated Materials

2

Disclaimer

By reading or attending the presentation that follows, you agree to be bound by the following limitations.

This presentation has been prepared by BAHÍA DE LAS ISLETAS, S.A. and its subsidiaries (the “Company” or “we”) solely for informational purposes and does not constitute, and

should not be construed as, an offer to sell or issue securities or otherwise constitute an invitation or inducement to any person to purchase, underwrite, subscribe to or otherwise

acquire securities in the Company. This presentation is intended to provide a general overview of the Company and its business and does not purport to deal with all aspects and details

regarding the Company.

For the purposes of this disclaimer, the presentation that follows shall mean and include the slides that follow, the oral presentation of the slides by the Company or any person on its

behalf, any question-and-answer session that follows the oral presentation, hard copies of this document and any materials distributed in connection with the presentation. By dialling

into the teleconference during which the presentation is made or reading the presentation, you will be deemed to have agreed to all of the restrictions that apply with regard to the

presentation and acknowledged that you understand the legal regulatory sanctions attached to the misuse, disclosure or improper circulation of the presentation.

The Company has included non-IFRS financial measures in this presentation. These measurements may not be comparable to those of other companies. Reference to these non-IFRS

financial measures should be considered in addition to IFRS financial measures, but should not be considered a substitute for results that are presented in accordance with IFRS.

The information contained in this presentation has not been subject to any independent audit or review. A significant portion of the information contained in this presentation, including

all market data and trend information, is based on estimates or expectations of the Company, and there can be no assurance that these estimates or expectations are or will prove to be

accurate. Our internal estimates have not been verified by an external expert, and we cannot guarantee that a third party using different methods to assemble, analyse or compute

market information and data would obtain or generate the same results. We have not verified the accuracy of such information, data or predictions contained in this presentation that

were taken or derived from industry publications, public documents of our competitors or other external sources. Further, our competitors may define our and their markets differently

than we do. In addition, past performance of the Company is not indicative of future performance. The future performance of the Company will depend on numerous factors, which are

subject to uncertainty, including factors which may be unknown on the date hereof. In addition, the business and viability plans are subject to ongoing update.

Each attendee or recipient acknowledges that neither it nor the Company intends that the Company act or be responsible as a fiduciary to such attendee or recipient, its management,

stockholders, creditors or any other person. By accepting and providing this document, each attendee or recipient and the Company, respectively, expressly disclaims any fiduciary

relationship and agrees that each attendee or recipient is responsible for making its own independent judgment with respect to the Company and any other matters regarding this

document.

Certain statements contained in this presentation that are not statements of historical fact, including, without limitation, any statements preceded by, followed by or including the words

“targets,” “believes,” “expects,” “aims,” “intends,” “may,” “anticipates,” “would,” “could” or similar expressions or the negative thereof, constitute forward-looking statements,

notwithstanding that such statements are not specifically identified. Examples of forward-looking statements include, but are not limited to: (i) statements about future financial and

operating results; (ii) statements of strategic objectives, business prospects, future financial condition, budgets, projected levels of production, projected costs and projected levels of

revenues and profits of the Company or its management or boards of directors; (iii) statements of future economic performance; and (iv) statements of assumptions underlying such

statements.

Forward-looking statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions which are difficult to predict and outside of the control of

the Company. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements. We have based these

assumptions on information currently available to us, if any one or more of these assumptions turn out to be incorrect, actual market results may differ from those predicted. While we do

not know what impact any such differences may have on our business, if there are such differences, our future results of operations and financial condition, could be materially adversely

affected. You should not place undue reliance on these forward-looking statements. Forward-looking statements speak only as of the date on which such statements are made. The

Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statement to reflect events or circumstances after the date on

which such statement is made, or to reflect the occurrence of unanticipated events.

3

Covid19 Response

• 2 routes discontinued in H1 2020, with 17 vessels on

port and a reduction of almost 30% in miles sailed

(70% in certain months)

• 725 employees were subject to an ERTE program

• Renegotiation of port taxes to minimize the cash burn

• Deferment of bareboat/time charter payments for

€15m

• Reduction of maintenance capex through the

reschedule of dry dockings

• Elimination of non-essential expenses

Operational Measures New Financing

• €75.3m new ICO loans

• Agreement to issue a new ring-fenced facility (the

“Vessels Facility”), split into a receivables facility of

€40m and a delayed draw facility of €35m for the

improvement of the vessels fleet (total €46m drawn as

of today)

• Agreement with a group of Noteholders representing

c.72.2% of the 2023 and 2024 notes (the “AHC”) for a

new delayed-draw Bridge Facility of €185m split into

€43m already drawn and c.€142m pending to be

drawn. Of the undrawn amount, €57m will be used for

liquidity of the Company, €25m to backstop new

Working Capital Facilities(1), c.€60m to be used to

refinance the Vessels Facility

• Agreement with Santander to provide c.€44m in new

WC Facilities(2)

The Company has taken a number of measures to improve its liquidity and overcome the negative impact of Covid19

Notes:

1. If remaining Spanish Banks do not provide their pro rata share

2. Corresponds to Santander’s pro rata of the €70m new WC Facilities

4

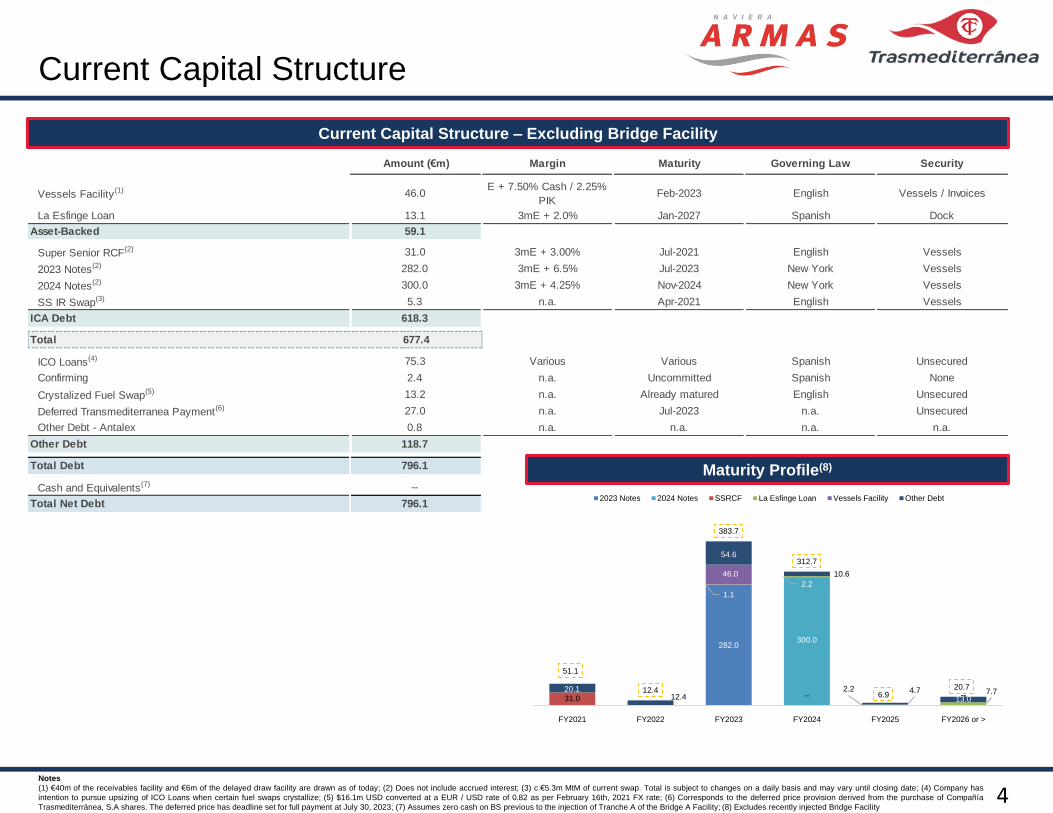

Current Capital Structure

Maturity Profile(8)

Current Capital Structure – Excluding Bridge Facility

282.0

-- --

300.0

--31.0 --

1.1

2.2

2.2 7.7

46.0

20.1 12.4

54.6

10.6

4.7 13.0

51.1

12.4

383.7

312.7

6.9 20.7

FY2021 FY2022 FY2023 FY2024 FY2025 FY2026 or >

2023 Notes 2024 Notes SSRCF La Esfinge Loan Vessels Facility Other Debt

Notes

(1) €40m of the receivables facility and €6m of the delayed draw facility are drawn as of today; (2) Does not include accrued interest; (3) c.€5.3m MtM of current swap. Total is subject to changes on a daily basis and may vary until closing date; (4) Company has

intention to pursue upsizing of ICO Loans when certain fuel swaps crystallize; (5) $16.1m USD converted at a EUR / USD rate of 0.82 as per February 16th, 2021 FX rate; (6) Corresponds to the deferred price provision derived from the purchase of Compañía

Trasmediterránea, S.A shares. The deferred price has deadline set for full payment at July 30, 2023; (7) Assumes zero cash on BS previous to the injection of Tranche A of the Bridge A Facility; (8) Excludes recently injected Bridge Facility

Amount (€m) Margin Maturity Governing Law Security

Vessels Facility(1) 46.0E + 7.50% Cash / 2.25%

PIKFeb-2023 English Vessels / Invoices

La Esfinge Loan 13.1 3mE + 2.0% Jan-2027 Spanish Dock

Asset-Backed 59.1

Super Senior RCF(2) 31.0 3mE + 3.00% Jul-2021 English Vessels

2023 Notes(2) 282.0 3mE + 6.5% Jul-2023 New York Vessels

2024 Notes(2) 300.0 3mE + 4.25% Nov-2024 New York Vessels

SS IR Swap(3) 5.3 n.a. Apr-2021 English Vessels

ICA Debt 618.3

Total 677.4

ICO Loans(4) 75.3 Various Various Spanish Unsecured

Confirming 2.4 n.a. Uncommitted Spanish None

Crystalized Fuel Swap(5) 13.2 n.a. Already matured English Unsecured

Deferred Transmediterranea Payment(6) 27.0 n.a. Jul-2023 n.a. Unsecured

Other Debt - Antalex 0.8 n.a. n.a. n.a. n.a.

Other Debt 118.7

Total Debt 796.1

Cash and Equivalents(7) --

Total Net Debt 796.1

5

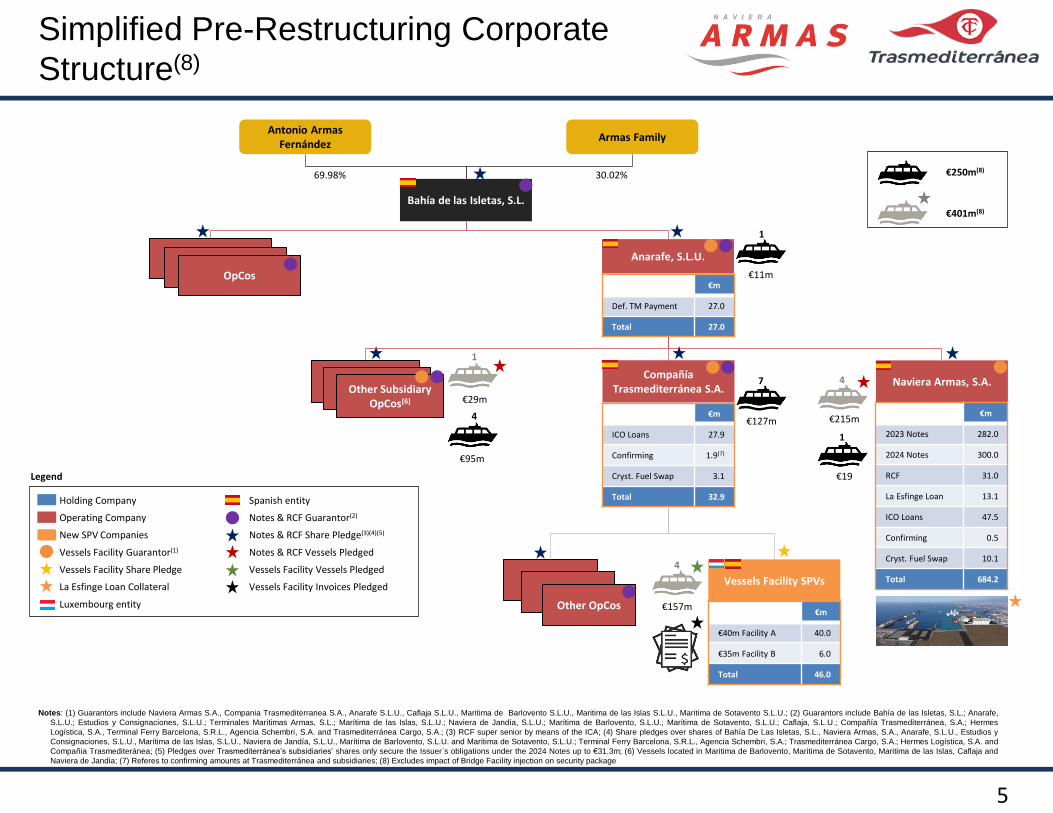

Simplified Pre-Restructuring Corporate

Structure(8)

Notes: (1) Guarantors include Naviera Armas S.A., Compania Trasmediterranea S.A., Anarafe S.L.U., Caflaja S.L.U., Maritima de Barlovento S.L.U., Maritima de las Islas S.L.U., Maritima de Sotavento S.L.U.; (2) Guarantors include Bahía de las Isletas, S.L.; Anarafe,

S.L.U.; Estudios y Consignaciones, S.L.U.; Terminales Marítimas Armas, S.L.; Marítima de las Islas, S.L.U.; Naviera de Jandía, S.L.U.; Marítima de Barlovento, S.L.U.; Marítima de Sotavento, S.L.U.; Caflaja, S.L.U.; Compañía Trasmediterránea, S.A.; Hermes

Logística, S.A., Terminal Ferry Barcelona, S.R.L., Agencia Schembri, S.A. and Trasmediterránea Cargo, S.A.; (3) RCF super senior by means of the ICA; (4) Share pledges over shares of Bahía De Las Isletas, S.L., Naviera Armas, S.A., Anarafe, S.L.U., Estudios y

Consignaciones, S.L.U., Marítima de las Islas, S.L.U., Naviera de Jandía, S.L.U., Marítima de Barlovento, S.L.U. and Marítima de Sotavento, S.L.U.; Terminal Ferry Barcelona, S.R.L., Agencia Schembri, S.A.; Trasmediterránea Cargo, S.A.; Hermes Logística, S.A. and

Compañia Trasmediteránea; (5) Pledges over Trasmediterránea’s subsidiaries’ shares only secure the Issuer´s obligations under the 2024 Notes up to €31.3m; (6) Vessels located in Maritima de Barlovento, Maritima de Sotavento, Maritima de las Islas, Caflaja and

Naviera de Jandia; (7) Referes to confirming amounts at Trasmediterránea and subsidiaries; (8) Excludes impact of Bridge Facility injection on security package

Holding Company

Operating Company

New SPV Companies

Vessels Facility Guarantor(1)

Vessels Facility Share Pledge

La Esfinge Loan Collateral

Luxembourg entity

Naviera Armas, S.A.Compañía

Trasmediterránea S.A.Other Subsidiary OpCos(6)

Other OpCos

Other HoldcosOther Holdcos

OpCos

Vessels Facility SPVs

Bahía de las Isletas, S.L.

€m

€40m Facility A 40.0

€35m Facility B 6.0

Total 46.0

Legend

Anarafe, S.L.U.

Spanish entity

Notes & RCF Guarantor(2)

Notes & RCF Share Pledge(3)(4)(5)

Notes & RCF Vessels Pledged

Vessels Facility Vessels Pledged

Vessels Facility Invoices Pledged

€m

2023 Notes 282.0

2024 Notes 300.0

RCF 31.0

La Esfinge Loan 13.1

ICO Loans 47.5

Confirming 0.5

Cryst. Fuel Swap 10.1

Total 684.2

Antonio ArmasFernández

Armas Family

69.98%

€127m€m

ICO Loans 27.9

Confirming 1.9(7)

Cryst. Fuel Swap 3.1

Total 32.9

€215m

€157m

€29m

€11m

1

47

4

1

€95m

4

€19

1

€401m(8)

€250m(8)30.02%

€m

Def. TM Payment 27.0

Total 27.0

6

Fleet Summary and Unrestricted SPVs(6)

GroupUnrestricted

SPVs

€6.0m

Payable(4)

€105.8m

Receivable(5)

€m(1)

SF Levante 12.5

SF Baleares 27.5

Alcantara Dos 3.8

Almudiana Dos 6.8

Al Andalus --(2)

Tirajana 24.5

Ciudad de Ibiza 24.5

Volcán de

Tagoro75.0

New Fast Ferry 78.0(3)

€24.7m Annual

Charters

€m(1)

Las Palmas de

Gran Canaria9.5

Ciudad de Palma 52.5

Ciudad de

Granada42.5

Ciudad

Autonoma de

Melilla

42.5

Villa de Agaete 19.5

Volcan de

Tamadaba35.0

Volcan de

Taburiente29.5

Volcan de

Tindaya16.5

Volcan de

Teneguia13.5

Volcan de Tauce 10.5

Volcan de

Tamasite28.5

€m(1)

Volcan de Teno 18.5

Volcan de

Tijarafe32.5

Volcan de

Timanfaya29.5

Volcan de

Tinamar76.5

Volcan de Teide 76.5

Almariya 5.5

Ciudad de Ceuta 23.5

Ciudad de

Mahon29.5

Ciudad de

Malaga10.5

JM Entrecanales 29.5

Juan J. Sister 18.5

Total 252.5

Total 650.5

External

Bank Debt

€185.7m(7)

Notes

(1) Alta Shipping latest valuation as of 5th of November, 2020. Additional valuation performed by FEM Shipbrokers shows a €600m valuation of the Group’s vessels as of 24th of November, 2020; (2) No valuation available; (3) Estimated valuation at delivery; (4)

Unpaid InterCo Leases; (5) InterCo Loans provided by the Group to the construction of vessels, accruing interest at a 7.5% rate; (6) Analysis excludes Villa de Teror; (7) Includes 3rd party debt at time of delivery for the New Fast Ferry

7

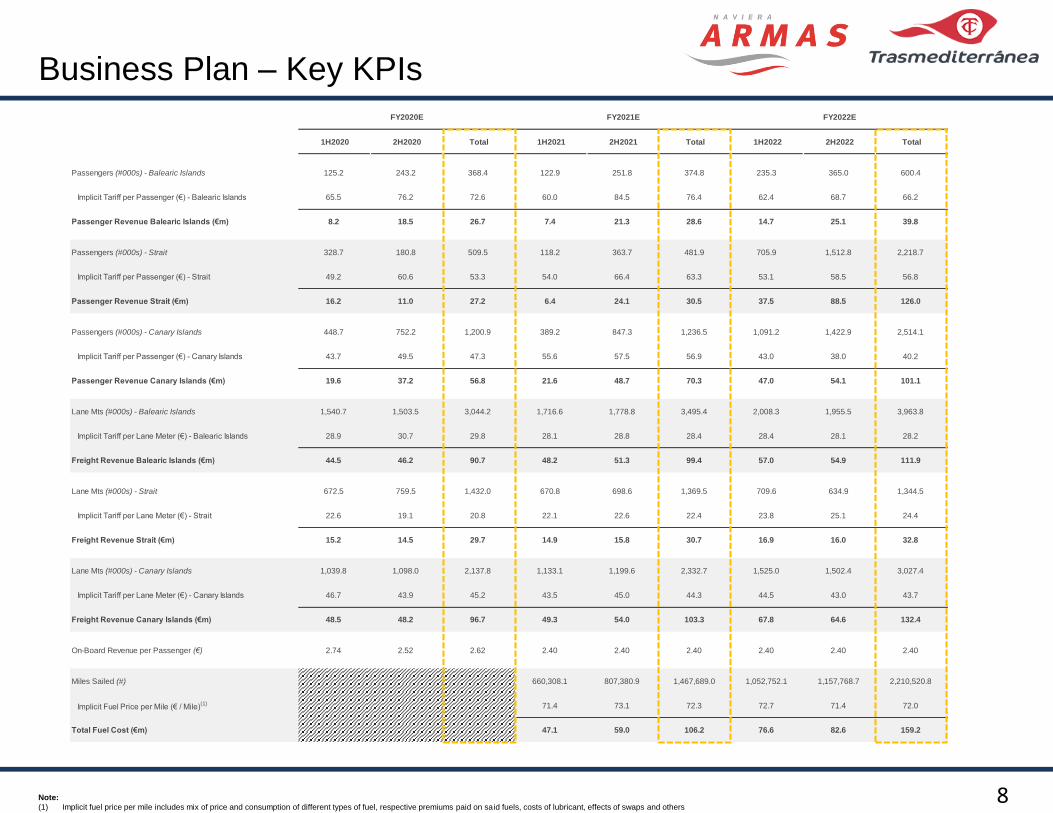

Summary Business Plan

FY21 – FY22 Projections:

• FY21 projected assuming Strait does not open during the year but

there is a general improvement of activity for summer of FY21 vs

FY20

• Price increases in FY21 vs FY20 applied as of January FY21,

and a further price increase of 3% both in cargo and

passengers in FY22

• Both 2021 and 2022 are built bottom-up based on FY20 and FY19

activity and adjusted for planned changes in fleet and routes

• Activity assumes resumed opening of Huelva – Canarias route

in July 2021 previously transferred to FRS in 2017 due to a

competition ruling from the acquisition of Trasmediterránea

• Given uncertainties about timing of Covid solution, FY22

represents a discontinuity case vs FY21. FY 22 projected

based on FY19 actuals including the re-opening of the Strait

• FY21 WC impacted by a high level of overdue normalization (c.€86m),

and FY22 will still be impacted by a normalization of DPO and DSO

FY23 – FY24 Guidance:

• Company expects to generate revenues between €650m - €700m in

FY23 and FY24 as activity returns to historical levels and it is able to

properly implement its business plan

• Company’s gross margin expected to remain similar to FY22, as

historical variable costs as percentage of revenue will continue in line

with historical levels

• EBITDA margins for the two projected years beyond the budget to

remain at c.15% with EBITDA ranging between €95m - €110m, as

fuel, structure and fixed costs of vessels are expected to remain

relatively constant for both years when compared with FY22

• Change in WC for FY23 and FY24 expected to be close to zero as

historical collection and payment days remain relatively constant at

historical levels

• Capex is expected to remain at historical maintenance levels of €30m

for both FY2023 and FY2024

The Company has elaborated a BP assuming that Covid19 restrictions will continue to impact demand until the end of 2021

Notes: (1) Includes other Income, consolidated adjustments and on-board services; (2) Includes only maintenance capex (i.e. no investments in scrubbers included in capex projections); (3) Includes €40m shareholder capital injection, €9.6m Intracompany Loan repayment

and other CFs; (4) Assumes Company has excess vessels capacity and is able to divest c.€150m of vessels between FY22 – FY23

€MM FY2020E FY2021E FY2022E

Passenger Revenue Balearic Islands 26.7 28.6 39.8

Passenger Revenue Strait 27.2 30.5 126.0

Passenger Revenue Canary Islands 56.8 70.3 101.1

Total Passenger Revenue 110.7 129.5 266.8

Freight Revenue Balearic Islands 90.7 99.4 111.9

Freight Revenue Strait 29.7 30.7 32.8

Freight Revenue Canary Islands 96.7 103.3 132.4

Total Freight Revenue 217.1 233.4 277.2

Land Transportation 104.0 105.8 114.9

Other(1) 30.1 23.4 (3.7)

Revenue 462.0 492.1 655.2

Direct Costs (121.1) (122.3) (143.6)

Gross Margin 340.9 369.8 511.5

Gross Margin (%) 73.8% 75.1% 78.1%

Fuel (113.0) (106.2) (159.2)

Structure Costs (64.0) (51.2) (45.9)

Fixed Costs of Vessels and Port Expenses (130.4) (116.7) (117.7)

Personnel Expenses (77.1) (81.0) (89.3)

EBITDA (43.7) 14.8 99.5

EBITDA Margin (%) n.m. 3.0% 15.2%

Change in WC (123.8) (27.3)

CAPEX(2) (15.4) (25.4)

Other CF(3) 22.1 --

Potential Divestments(4) -- 75.0

CF Before Debt Service (102.3) 121.8

8

FY2020E FY2021E FY2022E

1H2020 2H2020 Total 1H2021 2H2021 Total 1H2022 2H2022 Total

Passengers (#000s) - Balearic Islands 125.2 243.2 368.4 122.9 251.8 374.8 235.3 365.0 600.4

Implicit Tariff per Passenger (€) - Balearic Islands 65.5 76.2 72.6 60.0 84.5 76.4 62.4 68.7 66.2

Passenger Revenue Balearic Islands (€m) 8.2 18.5 26.7 7.4 21.3 28.6 14.7 25.1 39.8

Passengers (#000s) - Strait 328.7 180.8 509.5 118.2 363.7 481.9 705.9 1,512.8 2,218.7

Implicit Tariff per Passenger (€) - Strait 49.2 60.6 53.3 54.0 66.4 63.3 53.1 58.5 56.8

Passenger Revenue Strait (€m) 16.2 11.0 27.2 6.4 24.1 30.5 37.5 88.5 126.0

Passengers (#000s) - Canary Islands 448.7 752.2 1,200.9 389.2 847.3 1,236.5 1,091.2 1,422.9 2,514.1

Implicit Tariff per Passenger (€) - Canary Islands 43.7 49.5 47.3 55.6 57.5 56.9 43.0 38.0 40.2

Passenger Revenue Canary Islands (€m) 19.6 37.2 56.8 21.6 48.7 70.3 47.0 54.1 101.1

Lane Mts (#000s) - Balearic Islands 1,540.7 1,503.5 3,044.2 1,716.6 1,778.8 3,495.4 2,008.3 1,955.5 3,963.8

Implicit Tariff per Lane Meter (€) - Balearic Islands 28.9 30.7 29.8 28.1 28.8 28.4 28.4 28.1 28.2

Freight Revenue Balearic Islands (€m) 44.5 46.2 90.7 48.2 51.3 99.4 57.0 54.9 111.9

Lane Mts (#000s) - Strait 672.5 759.5 1,432.0 670.8 698.6 1,369.5 709.6 634.9 1,344.5

Implicit Tariff per Lane Meter (€) - Strait 22.6 19.1 20.8 22.1 22.6 22.4 23.8 25.1 24.4

Freight Revenue Strait (€m) 15.2 14.5 29.7 14.9 15.8 30.7 16.9 16.0 32.8

Lane Mts (#000s) - Canary Islands 1,039.8 1,098.0 2,137.8 1,133.1 1,199.6 2,332.7 1,525.0 1,502.4 3,027.4

Implicit Tariff per Lane Meter (€) - Canary Islands 46.7 43.9 45.2 43.5 45.0 44.3 44.5 43.0 43.7

Freight Revenue Canary Islands (€m) 48.5 48.2 96.7 49.3 54.0 103.3 67.8 64.6 132.4

On-Board Revenue per Passenger (€) 2.74 2.52 2.62 2.40 2.40 2.40 2.40 2.40 2.40

Miles Sailed (#) 660,308.1 807,380.9 1,467,689.0 1,052,752.1 1,157,768.7 2,210,520.8

Implicit Fuel Price per Mile (€ / Mile)(1) 71.4 73.1 72.3 72.7 71.4 72.0

Total Fuel Cost (€m) 47.1 59.0 106.2 76.6 82.6 159.2

Business Plan – Key KPIs

Note:

(1) Implicit fuel price per mile includes mix of price and consumption of different types of fuel, respective premiums paid on said fuels, costs of lubricant, effects of swaps and others

9

Introduction to the Restructuring – Lockup

Agreement

Notes

(1) €25m to be backstopped by the AHC and €43.5m to be provided by Banco Santander; (2) Includes €100m from interim bridge facility, €70m of WC facilities, €40m of capital increase by the shareholder and €9.6m from repayment of Intercompany loans.

Contributions

from all

stakeholders

Current Creditors

Will modify the terms of their debt to extend their

maturities

Will capitalize a substantial portion of their debt

Will contribute €100m of new emergency liquidity

(Tranches A and B on the Bridge Facility) and €70m of

new working capital lines(1)

Will take out the Vessel Facility to simplify the capital

structure

Shareholder

Will contribute €40m of new money through a capital

increase

Will be subject to certain ownership dilution as a result

of the debt capitalization

Advantages

of the

Transaction

Liquidity

Transaction will provide €220m(2) of

new liquidity which will prove sufficient

to endure the Covid-19 pandemic,

even with the assumption that 2021

demand levels remain highly affected

1 Term

Transaction will provide sufficient

runway in order to properly develop

the Business Plan and reach the

expected normalized EBITDA c.

€100m through the extension of the

Group´s maturity profile, particularly

with new Notes maturing in 2026

2 Deleveraging and Recapitalization

Transaction will significantly diminish

the annual financial burden

Reduction of net debt and

recapitalization as a result of debt

capitalization (€245m of Notes

converted into equity), and the capital

increase

3

Stability

Contribute stability to the Group through the

replacement of non-committed bilateral

working capital lines for committed long-term

lines

4 Corporate Governance

Transaction will improve the Company’s corporate governance

by introducing a new board, a chief restructuring officer and a

new executive committee

5

The Company, certain Holders of the Notes represented by members of an ad hoc committee (the “AHC”), Banco Santander and the Shareholder

have entered into a Lock-Up Agreement to implement a Recapitalization transaction. The next pages summarize the key terms of the

restructuring, new capital structure and the new equity / governance arrangements

10

Bridge Facility Key Terms

Key Considerations

Instrument

Delayed-draw Term Loan of €185m

Initial draw of €35m (“Facility A”) made on December 30th, 2020

€65m (“Facility B”), €8m of which were drawn on January 27th, 2021 and the remainder to be drawn following the execution of the

lock-up agreement

€60m (“Facility C”) to refinance the Vessels Facility

€25m (“Facility D”) to backstop the Working Capital Facilities from Caixabank and Sabadell

Issuer Naviera Armas S.A.

Interest E + 250bps cash and E + 750 bps PIK

Guarantors

Bahia de las Isletas, SL, Naviera Armas S.A., Agencia Schembri, S.A., Anarafe SLU, Caflaja SLU, Compañía Trasmediterránea S.A.,

Estudios y Consignaciones SLU, Hermes Logistica SA, Maritima de Barlovento SLU, Maritima de las Islas SLU, Maritima de Sotavento SLU,

Naviera de Jandia SLU, Terminal Ferry de Barcelona SRL, Terminales Maritimas Armas SLU, Armas Trasmediterránea Factoring, S.L

Fees

2.0% backstop fee(1)

5.0% exit fee(1)

2% OID(1)(2)

Prepayment Make-whole premium (carve-out for asset sales and proceeds from any issuance of subordinated capital at 103)

Maturity 31st July, 2021 with option to extend by up to 2 months

Guarantees and

Security Package

Facility A secured by:

Mortgages over the following 4 vessels: Volcán de Tamadaba, Tazacorte, Volcán de Tauce, and Volcán de Tindaya

All intercompany loans with the Unrestricted Group Family SPVs

Super Senior on the ICA common security package (including pledges over shares of the main entities in the Group)(3)

Upon Facility B utilization:

All unencumbered vessels will be incorporated to the common ICA security and Bridge will be super senior

Other The Company continues to work with SEPI to raise additional financing

The AHC has committed a Bridge Facility which will provide sufficient liquidity to implement the Restructuring

Notes

(1) To be paid in kind; (2) 2% OID on total committed amount paid in kind by increasing the principal debt outstanding; (3) Entities include Naviera Armas S.A., Maritima de Sotavento SLU, Naviera de Jandia SLU, Estudios y Consignaciones SLU, Anarafe SLU,

Maritima de Barlovento SLU, Maritima de las Islas SLU, Bahia de las Isletas SL, 99.6% of Hermes Logistica S.A., Compañía Trasmediterranea S.A., Agencia Schembri S.A., Trnsmediterranea Cargo S.A., Terminal Ferry Barcelona SRL,

11

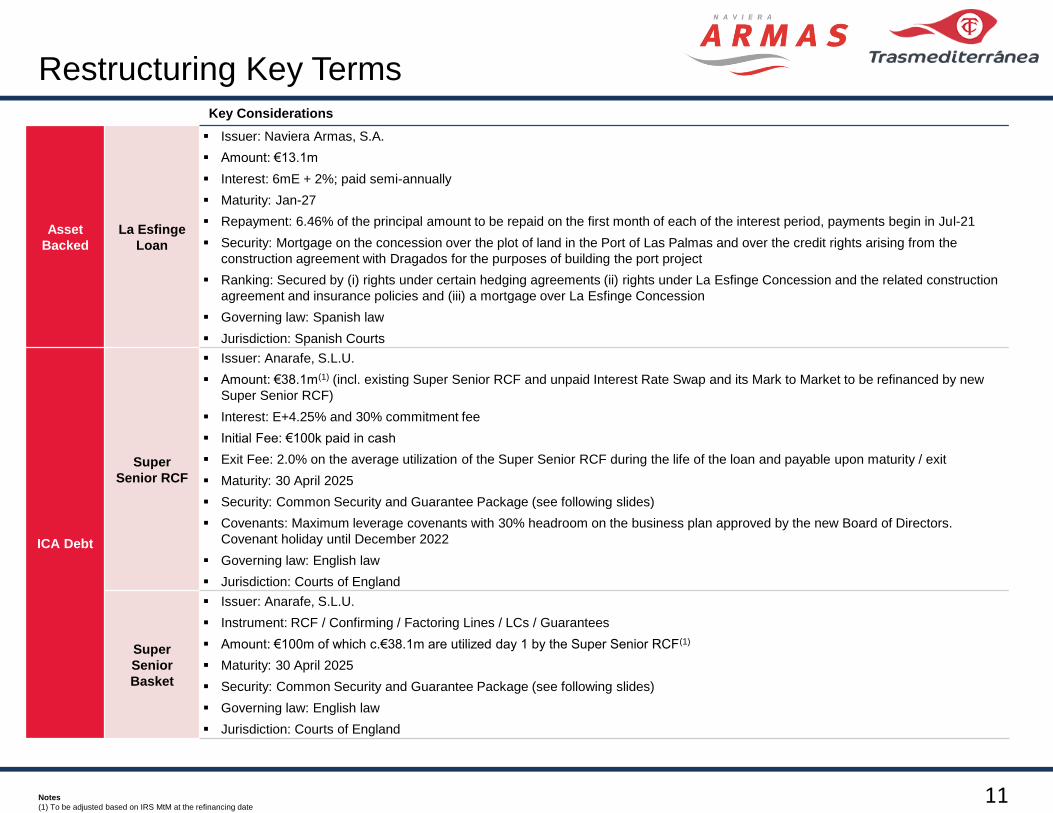

Restructuring Key TermsKey Considerations

Asset

Backed

La Esfinge

Loan

Issuer: Naviera Armas, S.A.

Amount: €13.1m

Interest: 6mE + 2%; paid semi-annually

Maturity: Jan-27

Repayment: 6.46% of the principal amount to be repaid on the first month of each of the interest period, payments begin in Jul-21

Security: Mortgage on the concession over the plot of land in the Port of Las Palmas and over the credit rights arising from the

construction agreement with Dragados for the purposes of building the port project

Ranking: Secured by (i) rights under certain hedging agreements (ii) rights under La Esfinge Concession and the related construction

agreement and insurance policies and (iii) a mortgage over La Esfinge Concession

Governing law: Spanish law

Jurisdiction: Spanish Courts

ICA Debt

Super

Senior RCF

Issuer: Anarafe, S.L.U.

Amount: €38.1m(1) (incl. existing Super Senior RCF and unpaid Interest Rate Swap and its Mark to Market to be refinanced by new

Super Senior RCF)

Interest: E+4.25% and 30% commitment fee

Initial Fee: €100k paid in cash

Exit Fee: 2.0% on the average utilization of the Super Senior RCF during the life of the loan and payable upon maturity / exit

Maturity: 30 April 2025

Security: Common Security and Guarantee Package (see following slides)

Covenants: Maximum leverage covenants with 30% headroom on the business plan approved by the new Board of Directors.

Covenant holiday until December 2022

Governing law: English law

Jurisdiction: Courts of England

Super

Senior

Basket

Issuer: Anarafe, S.L.U.

Instrument: RCF / Confirming / Factoring Lines / LCs / Guarantees

Amount: €100m of which c.€38.1m are utilized day 1 by the Super Senior RCF(1)

Maturity: 30 April 2025

Security: Common Security and Guarantee Package (see following slides)

Governing law: English law

Jurisdiction: Courts of England

Notes

(1) To be adjusted based on IRS MtM at the refinancing date

12

Restructuring Key Terms (Cont.)

Key Considerations

ICA Debt

1L Term

Loan

Issuer: Anarafe, S.L.U.

Amount: Up to €206.5m(1) of the Bridge Facility

Interest: 3mE + 7.5% cash + 2.5% PIK

Maturity: 30 September 2025

Security: Common Security and Guarantee Package (see following slides)

Non-call period: Non-call 21 months from the completion of the Financial Restructuring. Carve out for asset sales and proceeds from

any issuance of subordinated capital at 103

Equity: Equivalent to 5.65% of proforma Class A shares stapled to 1L TL. 7.5% of Class B shares

Covenants: Minimum liquidity of €10m tested monthly for the first 30 post closing months and quarterly thereafter

Governing law: English law

Jurisdiction: Courts of England

New

Confirming

Line

Instrument: New fully committed confirming lines

Amount: €20m

Interest: Euribor (0% floor) + 3.50%

Maturity: 30 April 2025

Lenders: €12.4m Santander / Caixabank and Sabadell to be offered to participate in the confirming in the amount of €5.2m and €2.3m

respectively, and if they do not participate, the AHC will backstop their allocation

Security: Common Security and Guarantee Package (see following slides)

Note

1. Includes €185m principal (includes illustrative assumption that the €25m Facility D is fully drawn at the completion of the Financial Restructuring) plus fees and accrued interest assuming completion of the Financial Restructuring at 30 June 2021

13

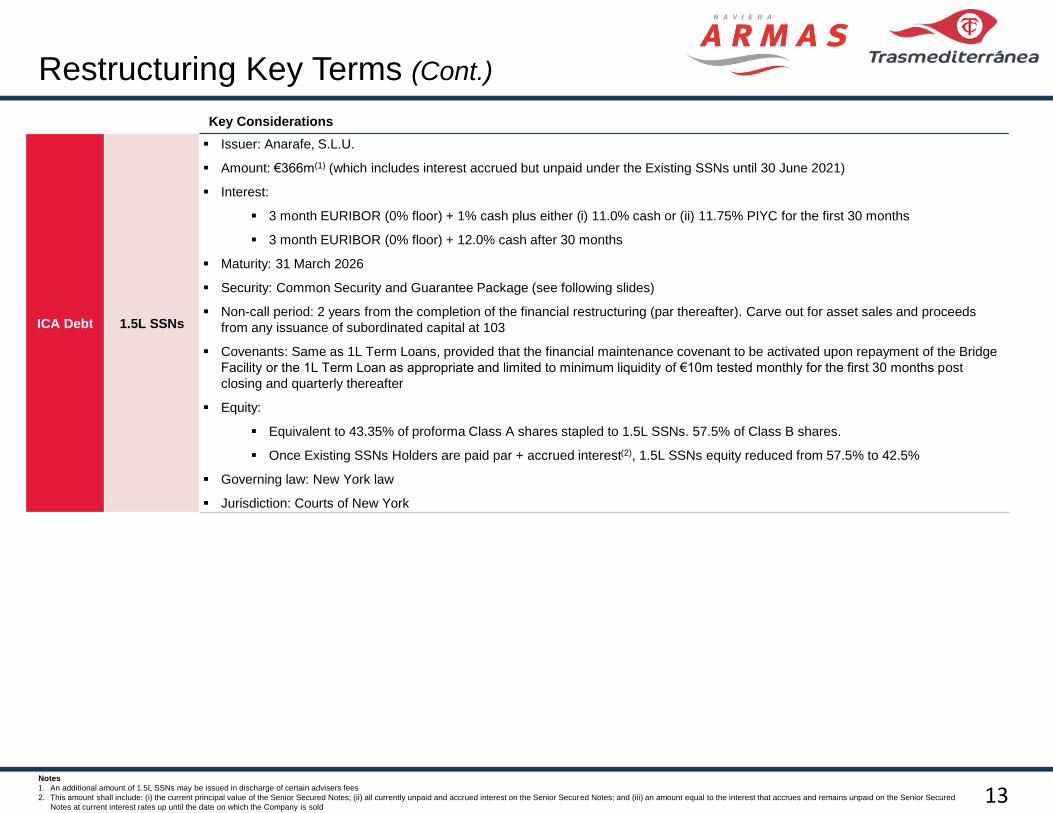

Restructuring Key Terms (Cont.)

Key Considerations

ICA Debt 1.5L SSNs

Issuer: Anarafe, S.L.U.

Amount: €366m(1) (which includes interest accrued but unpaid under the Existing SSNs until 30 June 2021)

Interest:

3 month EURIBOR (0% floor) + 1% cash plus either (i) 11.0% cash or (ii) 11.75% PIYC for the first 30 months

3 month EURIBOR (0% floor) + 12.0% cash after 30 months

Maturity: 31 March 2026

Security: Common Security and Guarantee Package (see following slides)

Non-call period: 2 years from the completion of the financial restructuring (par thereafter). Carve out for asset sales and proceeds

from any issuance of subordinated capital at 103

Covenants: Same as 1L Term Loans, provided that the financial maintenance covenant to be activated upon repayment of the Bridge

Facility or the 1L Term Loan as appropriate and limited to minimum liquidity of €10m tested monthly for the first 30 months post

closing and quarterly thereafter

Equity:

Equivalent to 43.35% of proforma Class A shares stapled to 1.5L SSNs. 57.5% of Class B shares.

Once Existing SSNs Holders are paid par + accrued interest(2), 1.5L SSNs equity reduced from 57.5% to 42.5%

Governing law: New York law

Jurisdiction: Courts of New York

Notes

1. An additional amount of 1.5L SSNs may be issued in discharge of certain advisers fees

2. This amount shall include: (i) the current principal value of the Senior Secured Notes; (ii) all currently unpaid and accrued interest on the Senior Secured Notes; and (iii) an amount equal to the interest that accrues and remains unpaid on the Senior Secured

Notes at current interest rates up until the date on which the Company is sold

14

Restructuring Key Terms (Cont.)

Key Considerations

Common

Security and

Guarantee

Package

Two newly incorporated newcos(1) to be inserted between Bahia de las Isletas and its immediate subsidiaries and a share pledge granted

over such newcos to create a single point of enforcement; and

Security over all Restricted Group vessels and concessions (other than the La Esfinge Concession)

Security over all intercompany loans with SPVs of the Unrestricted Group

Security and guarantee package to replicate that provided to the ICA Security Parties, Bridge Facility and Vessels Facilities immediately prior

to the restructuring effective date in a single shared security and guarantee package

ICA Ranking

1st ranking: RCF and Super Senior Basket

2nd ranking: 1L TL, new Confirming Lines, Fuel Swap New Financing(2) and TM New Financing(2)

3rd ranking: 1.5L SSNs

Note

1. NewCos’ jurisdiction subject to completion of fiscal analysis and tax structuring

2. In case such financing is provided

15

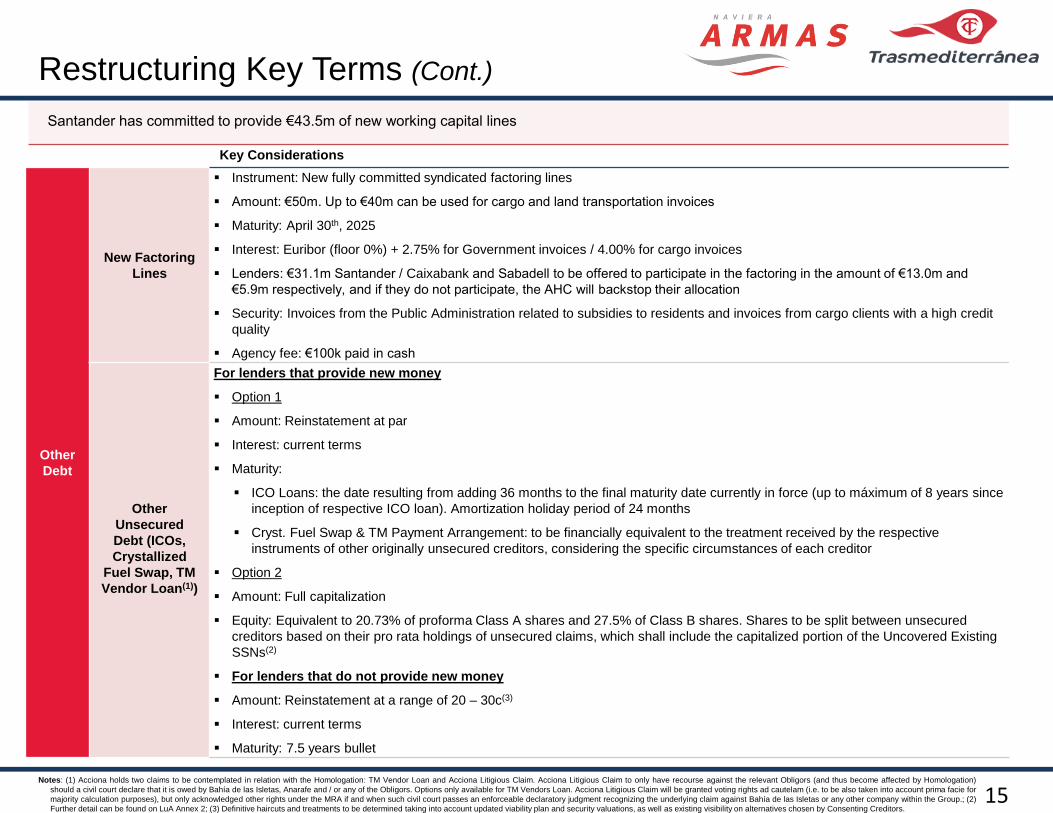

Restructuring Key Terms (Cont.)

Key Considerations

Other

Debt

New Factoring

Lines

Instrument: New fully committed syndicated factoring lines

Amount: €50m. Up to €40m can be used for cargo and land transportation invoices

Maturity: April 30th, 2025

Interest: Euribor (floor 0%) + 2.75% for Government invoices / 4.00% for cargo invoices

Lenders: €31.1m Santander / Caixabank and Sabadell to be offered to participate in the factoring in the amount of €13.0m and

€5.9m respectively, and if they do not participate, the AHC will backstop their allocation

Security: Invoices from the Public Administration related to subsidies to residents and invoices from cargo clients with a high credit

quality

Agency fee: €100k paid in cash

Other

Unsecured

Debt (ICOs,

Crystallized

Fuel Swap, TM

Vendor Loan(1))

For lenders that provide new money

Option 1

Amount: Reinstatement at par

Interest: current terms

Maturity:

ICO Loans: the date resulting from adding 36 months to the final maturity date currently in force (up to máximum of 8 years since

inception of respective ICO loan). Amortization holiday period of 24 months

Cryst. Fuel Swap & TM Payment Arrangement: to be financially equivalent to the treatment received by the respective

instruments of other originally unsecured creditors, considering the specific circumstances of each creditor

Option 2

Amount: Full capitalization

Equity: Equivalent to 20.73% of proforma Class A shares and 27.5% of Class B shares. Shares to be split between unsecured

creditors based on their pro rata holdings of unsecured claims, which shall include the capitalized portion of the Uncovered Existing

SSNs(2)

For lenders that do not provide new money

Amount: Reinstatement at a range of 20 – 30c(3)

Interest: current terms

Maturity: 7.5 years bullet

Santander has committed to provide €43.5m of new working capital lines

Notes: (1) Acciona holds two claims to be contemplated in relation with the Homologation: TM Vendor Loan and Acciona Litigious Claim. Acciona Litigious Claim to only have recourse against the relevant Obligors (and thus become affected by Homologation)

should a civil court declare that it is owed by Bahía de las Isletas, Anarafe and / or any of the Obligors. Options only available for TM Vendors Loan. Acciona Litigious Claim will be granted voting rights ad cautelam (i.e. to be also taken into account prima facie for

majority calculation purposes), but only acknowledged other rights under the MRA if and when such civil court passes an enforceable declaratory judgment recognizing the underlying claim against Bahía de las Isletas or any other company within the Group.; (2)

Further detail can be found on LuA Annex 2; (3) Definitive haircuts and treatments to be determined taking into account updated viability plan and security valuations, as well as existing visibility on alternatives chosen by Consenting Creditors.

16

Equity and Governance

Key Considerations

Board of

Directors

The board of New HoldCo shall at all times be comprised of up to a maximum of 5 directors, namely:

1 executive chairman (who shall be Mr. Antonio Armas as at the Restructuring Effective Date);

1 executive director, being the CEO(1);

1 non-executive director appointed by the Existing Shareholders ; and

2 independent non-executive directors appointed by the two largest Creditor Shareholders

Executive

Management and

Responsibility

Matrix

Search process to be run for management positions

Upon appointment of a General Manager/CEO and until the end of 2022, certain key areas of the Group will be managed by Mr. Antonio

Armas, as Executive Chairman, with the remaining being under the responsibility of the General Manager in accordance with a responsibility

matrix

Mr. Antonio Armas to work on a transition to the General Manager during 2022. Mr. Armas will remain as Chairman of the Board after the

transition

Equity

Distribution

Voting ordinary shares (“Class A shares”) to be split 51% for Existing Shareholders, 43.35% for existing SSN holders and 5.65% for 1L Term

Loan lenders

Economic (“Class B shares”) to be split 35% for Existing Shareholders. 57.5% will be distributed between existing SSN holders (30%),

unsecured lenders (including the existing SSN holders) that provide new money (27.5%) and 7.5% for 1L Term Loan lenders.

The existing SSN holders have agreed between themselves to turnover or re-allocate their entitlements of the Class A Shares and Class B

Shares on a pro rata basis as between all existing SSN holders.

Once existing SSN holders have been paid par + accrued interest on the face value of their existing SSNs at an exit date / liquidity event,

excess value flowing to equity holders to be split 50% for Existing Shareholders, 42.5% for existing SSN holders and 7.5% for 1L Term Loan

lenders

Capital Increase Existing Shareholders to inject €40m

Exit Board to launch a sale process of the Group until March 2024, which shall happen earlier in case the Group achieves a consolidated

EBITDA of €100m

Current Shareholder has committed to inject €40m as part of the Restructuring

Notes

1. If the CEO is not appointed by the Restructuring Effective Date, that Board position shall be filled by an independent non-executive director (the “Interim INED”) until such time as the CEO is appointed

17

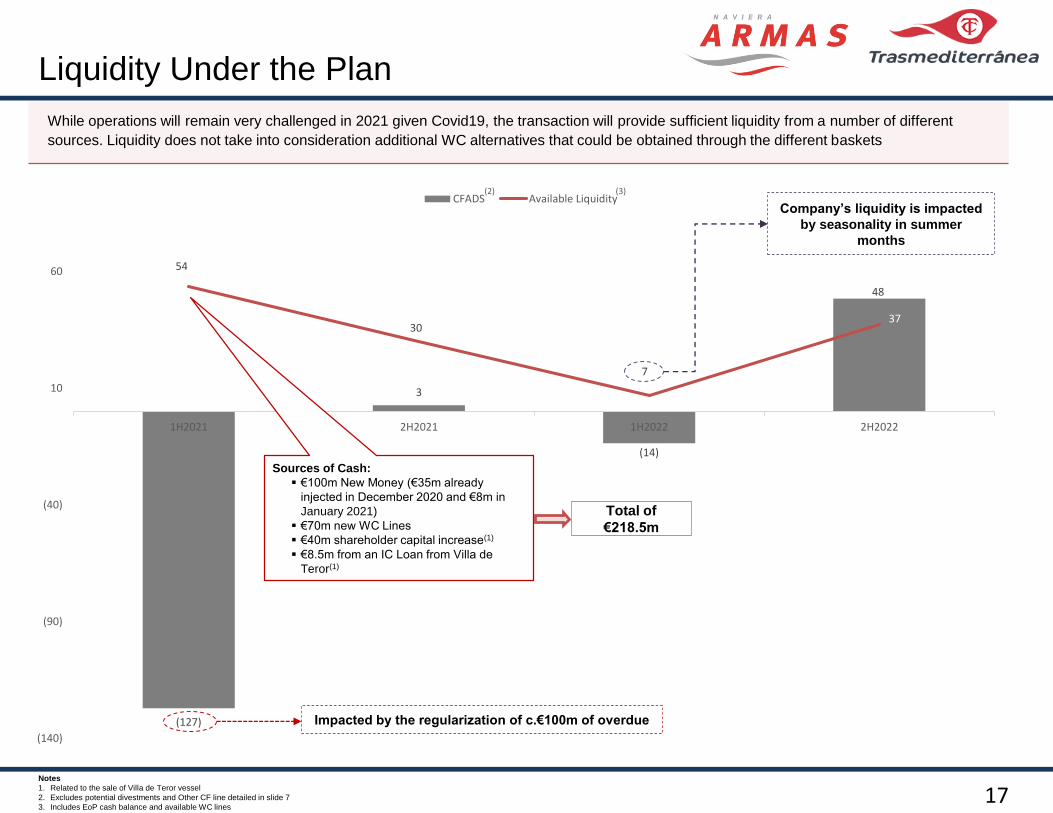

Liquidity Under the Plan

Total of

€218.5m

While operations will remain very challenged in 2021 given Covid19, the transaction will provide sufficient liquidity from a number of different

sources. Liquidity does not take into consideration additional WC alternatives that could be obtained through the different baskets

(2)

Notes

1. Related to the sale of Villa de Teror vessel

2. Excludes potential divestments and Other CF line detailed in slide 7

3. Includes EoP cash balance and available WC lines

Impacted by the regularization of c.€100m of overdue(127)

3

(14)

48

54

30

7

37

(140)

(90)

(40)

10

60

1H2021 2H2021 1H2022 2H2022

CFADS Available LiquidityCompany’s liquidity is impacted

by seasonality in summer

months

Sources of Cash:

€100m New Money (€35m already

injected in December 2020 and €8m in

January 2021)

€70m new WC Lines

€40m shareholder capital increase(1)

€8.5m from an IC Loan from Villa de

Teror(1)

(3)

18

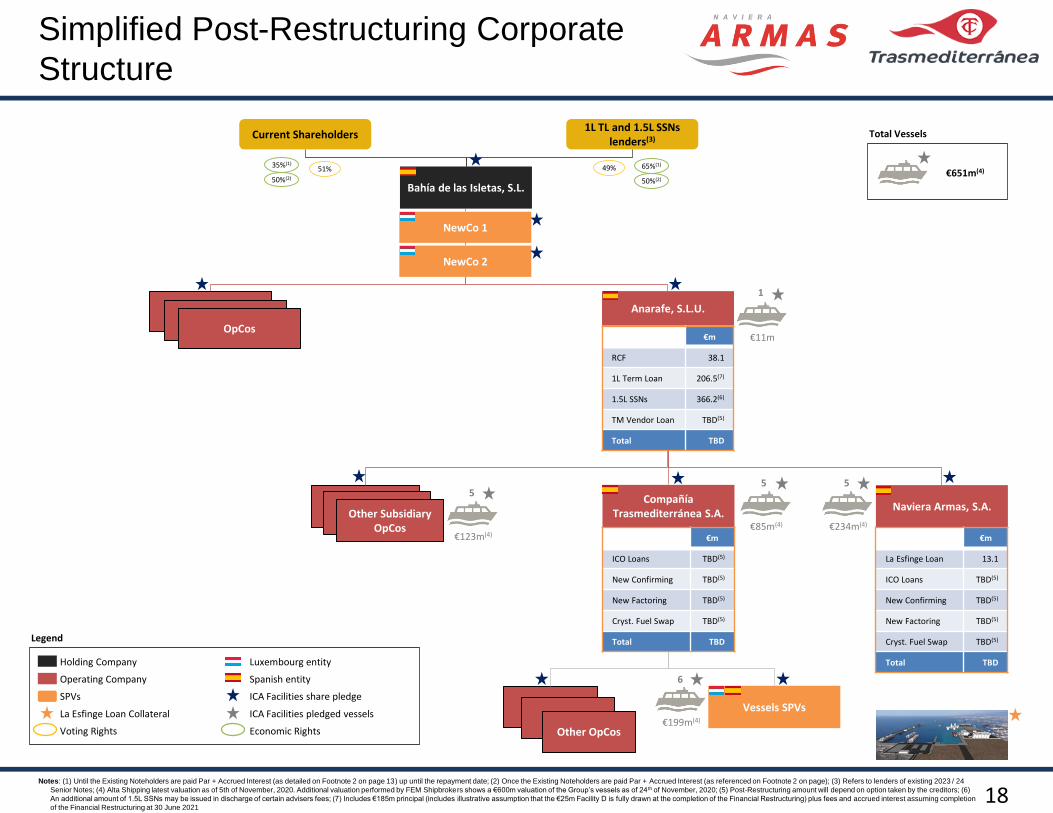

Simplified Post-Restructuring Corporate

Structure

Naviera Armas, S.A.Compañía

Trasmediterránea S.A.Other Subsidiary OpCos

Other OpCos

Other HoldcosOther Holdcos

OpCos

Vessels SPVs

Bahía de las Isletas, S.L.

Anarafe, S.L.U.

€m

La Esfinge Loan 13.1

ICO Loans TBD(5)

New Confirming TBD(5)

New Factoring TBD(5)

Cryst. Fuel Swap TBD(5)

Total TBD

Current Shareholders1L TL and 1.5L SSNs

lenders(3)Total Vessels

€651m(4)

€m

RCF 38.1

1L Term Loan 206.5(7)

1.5L SSNs 366.2(6)

TM Vendor Loan TBD(5)

Total TBD

NewCo 1

NewCo 2

51%35%(1)49% 65%(1)

50%(2) 50%(2)

Holding Company

Operating Company

SPVs

La Esfinge Loan Collateral

Voting Rights

Legend

Luxembourg entity

Spanish entity

ICA Facilities share pledge

ICA Facilities pledged vessels

Economic Rights

Notes: (1) Until the Existing Noteholders are paid Par + Accrued Interest (as detailed on Footnote 2 on page 13) up until the repayment date; (2) Once the Existing Noteholders are paid Par + Accrued Interest (as referenced on Footnote 2 on page); (3) Refers to lenders of existing 2023 / 24

Senior Notes; (4) Alta Shipping latest valuation as of 5th of November, 2020. Additional valuation performed by FEM Shipbrokers shows a €600m valuation of the Group’s vessels as of 24th of November, 2020; (5) Post-Restructuring amount will depend on option taken by the creditors; (6)

An additional amount of 1.5L SSNs may be issued in discharge of certain advisers fees; (7) Includes €185m principal (includes illustrative assumption that the €25m Facility D is fully drawn at the completion of the Financial Restructuring) plus fees and accrued interest assuming completion

of the Financial Restructuring at 30 June 2021

€123m(4)€85m(4) €234m(4)

€199m(4)

€11m

€m

ICO Loans TBD(5)

New Confirming TBD(5)

New Factoring TBD(5)

Cryst. Fuel Swap TBD(5)

Total TBD

1

5 5

6

5

19

Lock-up Accession Instructions

• Noteholders not already party to the Lock-Up Agreement are invited to accede.

• Lucid Issuer Services Limited has been engaged to act as Lock-Up Agent under the Lock-Up Agreement. Any Noteholder that would like to

accede to the Lock-Up Agreement will need to provide to the Lock-Up Agent:

• a duly executed accession letter or, if participating in Facility B2 and Facility D (see below for further details) of the up-sized Bridge

Facility, a duly executed accession and commitment letter; and

• a locked-up debt confirmation letter and its evidence of beneficial holding,

via www.lucid-is.com/navieraarmas as soon as possible and, in any event, by the deadlines set.

• Any Noteholder that would like to accede to the Lock-Up Agreement during the Subscription Period will need to instruct the Clearing

Systems to block their Notes.

• Lenders are invited to contact the Lock-Up Agent at www.lucid-is.com/navieraarmas or by email to [email protected] for further

information regarding the Lock-Up Agreement accession process.

Participation by Noteholders in Facility B2 and Facility D of the Bridge Facility

• The Ad Hoc Committee have agreed to backstop €25m of post-Restructuring working capital facilities which will be included in the Bridge

Facility as Facility D if certain working capital facilities lenders do not accede to the Lock-Up Agreement. With regards to availability and

utilisation:

• Facility B2 (€57m), which shall be provided in any event, will be utilised by the Group prior to completion of the Restructuring as

necessary to address the Group’s immediate liquidity needs; and

• Facility D (€25m), if provided, shall be committed to the Group as part of the Bridge Facility, but is not expected to be available to

the Group for utilisation until the completion of the Restructuring.

• If certain working capital facilities lenders accede to the Lock-Up Agreement, Facility D will not be required, shall not be documented or

made available for participation and the syndication process shall proceed in respect of Facility B2 only.

• Noteholders are invited to participate in Facility B2 and Facility D (if applicable) of the Bridge Facility. Participating Noteholders will be

allocated a proportion of Facility B2 commitments and Facility D commitments (if applicable) such that their total participation in the Bridge

Facility is equal to the proportion which their holdings of Notes bears to the aggregate of all Notes issued. If Facility D is provided,

Participating Noteholders will not be able to elect to participate in only one of Facility B2 or Facility D.

• Each Participating Noteholder will need to provide a duly executed and apostilled power of attorney to accede to the Bridge Facility. Further

information and instructions are available at www.lucid-is.com/navieraarmas.

20

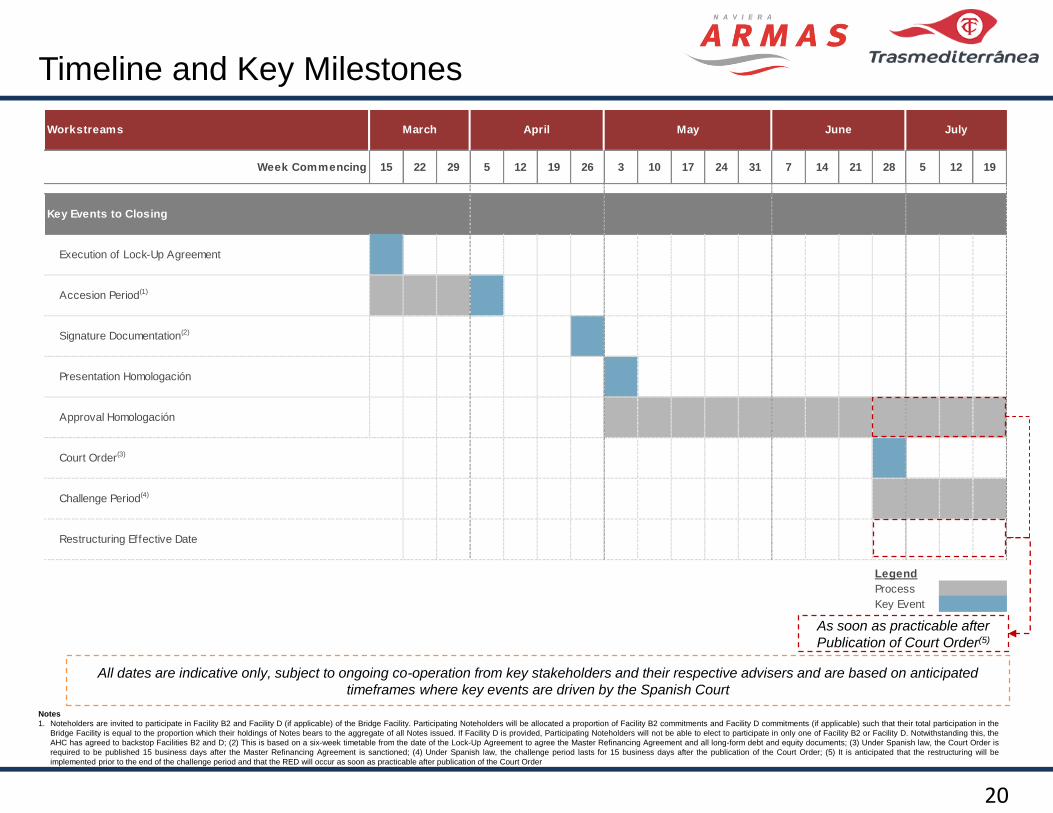

Timeline and Key Milestones

Notes

1. Noteholders are invited to participate in Facility B2 and Facility D (if applicable) of the Bridge Facility. Participating Noteholders will be allocated a proportion of Facility B2 commitments and Facility D commitments (if applicable) such that their total participation in the

Bridge Facility is equal to the proportion which their holdings of Notes bears to the aggregate of all Notes issued. If Facility D is provided, Participating Noteholders will not be able to elect to participate in only one of Facility B2 or Facility D. Notwithstanding this, the

AHC has agreed to backstop Facilities B2 and D; (2) This is based on a six-week timetable from the date of the Lock-Up Agreement to agree the Master Refinancing Agreement and all long-form debt and equity documents; (3) Under Spanish law, the Court Order is

required to be published 15 business days after the Master Refinancing Agreement is sanctioned; (4) Under Spanish law, the challenge period lasts for 15 business days after the publication of the Court Order; (5) It is anticipated that the restructuring will be

implemented prior to the end of the challenge period and that the RED will occur as soon as practicable after publication of the Court Order

All dates are indicative only, subject to ongoing co-operation from key stakeholders and their respective advisers and are based on anticipated

timeframes where key events are driven by the Spanish Court

As soon as practicable after

Publication of Court Order(5)

Workstreams March April May June July

Week Commencing 15 22 29 5 12 19 26 3 10 17 24 31 7 14 21 28 5 12 19

Key Events to Closing

Execution of Lock-Up Agreement 2

Accesion Period(1) 1 1 1 2

Signature Documentation(2) 2

Presentation Homologación 2

Approval Homologación 1 1 1 1 1 1 1 1 1 1 1 1

Court Order(3) 2

Challenge Period(4) 1 1 1 1

Restructuring Effective Date

Legend

Process 1 1

Key Event 2 2

21