lng regulatory issues - cre.gob.mx · lng regulatory issues alberto de la fuente comisión...

TRANSCRIPT

LNG Regulatory Issues

Alberto de la FuenteComisión Reguladora de Energía

La Jolla, CaliforniaJanuary 30, 2004

13th Annual Latin American Energy Conference

Institute of the Americas

2

Index

I.I. Why LNG?Why LNG?

II.II. LNG Projects in MexicoLNG Projects in Mexico

1.1. Where We StandWhere We Stand

2.2. Next StepsNext Steps

III.III. Lessons LearnedLessons Learned

3

Index

I.I. Why LNG?Why LNG?

4

Natural Gas Demand Drivers

Others4%

Petroleum29%

Industrial

22%

Electric

45%

2012

Natural Gas Demand by

SectorOthers3%

Petroleum

41%

Industrial26%

Electric

30%

2002

4,855 MMCFD

9,389 MMCFD

Source: Energy Prospective, Ministry of Energy, 2002

5

Demand for natural gas will exceed national production

6.8 bcfd

9.4 bcfd

Su

pp

lyS

up

plyD

eman

dD

eman

d

2.6 bcfd

2012

Alternatives:

…Natural Gas Demand Drivers

Source: Energy Prospective, Ministry of Energy, 2003-2012

6

1) Efforts to increase natural gas production in Mexico

Mexico is currently producing 4.5 BCFD

? With Multiple Service Contracts & Strategic Gas Program, Pemex estimates that production will increase to 5,800 MMCFD by 2006 and 7,500 MMCFD by 2010

*Source: PEMEX Gas, Bussiness Plan, 2002

4477

4800

1,000

6500

1,000

2002 2006 2010

Pemex Production Multiple Service Contract

7

? Interconnections between Mexico and the U.S. amount to 3.3 bcfd of cross-border firm capacity.

2) Pipeline Interconnection Infrastructure

I

III

VIII

IV

V

VI

II

VII

LNG

San Diego-Mexicali-Rosarito (0.3 Bcfd)

Blythe-Yuma-Tijuana(0.4 Bcfd)

Wilcox-NacoAgua Prieta(0.36 Bcfd) Norteño-

El Paso-Samalayuca0.4 Bcfd)

Eagle Pass-Laredo (Tidelands Oil)0.05 Bcfd

EPFS-Arguelles0.1 Bcfd constrained

•TETCO(Duke)-Reynosa0.15 Bcfd constrained•Tennessee-Reynosa0.35 Bcfd•Tennesee-Rio Bravo0.4 Bcfd

Coral-Arguelles0.35 Bcfd

LNG

LNG

Del Rio-Acuña0.01 Bcfd

KM-Monterrey-Saltillo0.3 Bcfd

Sistema Nacional de Gasoductos (SNG)

Ductos del sector privado

Ductos de Nogales(0.1 Bcfd)

Futuros ductos del sector privado

Ductos en EUA

USA

Mexico

Nueva interconexiòn0.35 Bcfd

Posible almacenamiento

LoopChihuahua0.3 Bcfd

Tama-Centro0.4 Bcfd

LC_Manza-Nillo 0.3 Bcfd

Valladolid-Cancun0.1 BcfdGuadalajara-

Manzanillo0.3 Bcfd

Sn. Fdo. 1 Bcfd

Bajamar- Rosarito(0.5 Bcfd)

Monterrey-SLP0.3 Bcfd

Frontera-Guaymas-Mazatlan0.5 Bcfd

Ductos del sector privado (prefactibilidad)

Palmillas -Toluca 0.3 Bcfd

Gas Zapata0.2 Bcfd

I

III

VIII

IV

V

VI

II

VII

LNG

San Diego-Mexicali-Rosarito (0.3 Bcfd)

Blythe-Yuma-Tijuana(0.4 Bcfd)

Wilcox-NacoAgua Prieta(0.36 Bcfd) Norteño-

El Paso-Samalayuca0.4 Bcfd)

Eagle Pass-Laredo (Tidelands Oil)0.05 Bcfd

EPFS-Arguelles0.1 Bcfd constrained

•TETCO(Duke)-Reynosa0.15 Bcfd constrained•Tennessee-Reynosa0.35 Bcfd•Tennesee-Rio Bravo0.4 Bcfd

Coral-Arguelles0.35 Bcfd

LNG

LNG

Del Rio-Acuña0.01 Bcfd

KM-Monterrey-Saltillo0.3 Bcfd

Sistema Nacional de Gasoductos (SNG)

Ductos del sector privado

Ductos de Nogales(0.1 Bcfd)

Futuros ductos del sector privado

Ductos en EUA

USA

Mexico

Nueva interconexiòn0.35 Bcfd

Posible almacenamiento

LoopChihuahua0.3 Bcfd

Tama-Centro0.4 Bcfd

LC_Manza-Nillo 0.3 Bcfd

Valladolid-Cancun0.1 BcfdGuadalajara-

Manzanillo0.3 Bcfd

Sn. Fdo. 1 Bcfd

Bajamar- Rosarito(0.5 Bcfd)

Monterrey-SLP0.3 Bcfd

Frontera-Guaymas-Mazatlan0.5 Bcfd

Ductos del sector privado (prefactibilidad)

Palmillas -Toluca 0.3 Bcfd

Gas Zapata0.2 Bcfd

8

Net Importer

Net Importer

Net Exporter

526

10,492

732

5

176

223635

Source: U.S. DOE-EIA, Annual Energy Review 2002

Natural gas imports and exports (2002, mcfd)

2) …Pipeline Interconnection Infrastructure

3) Development of LNG Receiving Terminals

9

10

Index

II.II. LNG Projects in MexicoLNG Projects in Mexico

11

Index

Where we StandWhere we Stand

1.02.03.04.05.06.07.08.09.0

10.0

J F M A M J J A S O N D J F M A M J J A S O N D E F M A M J J A S O N D J

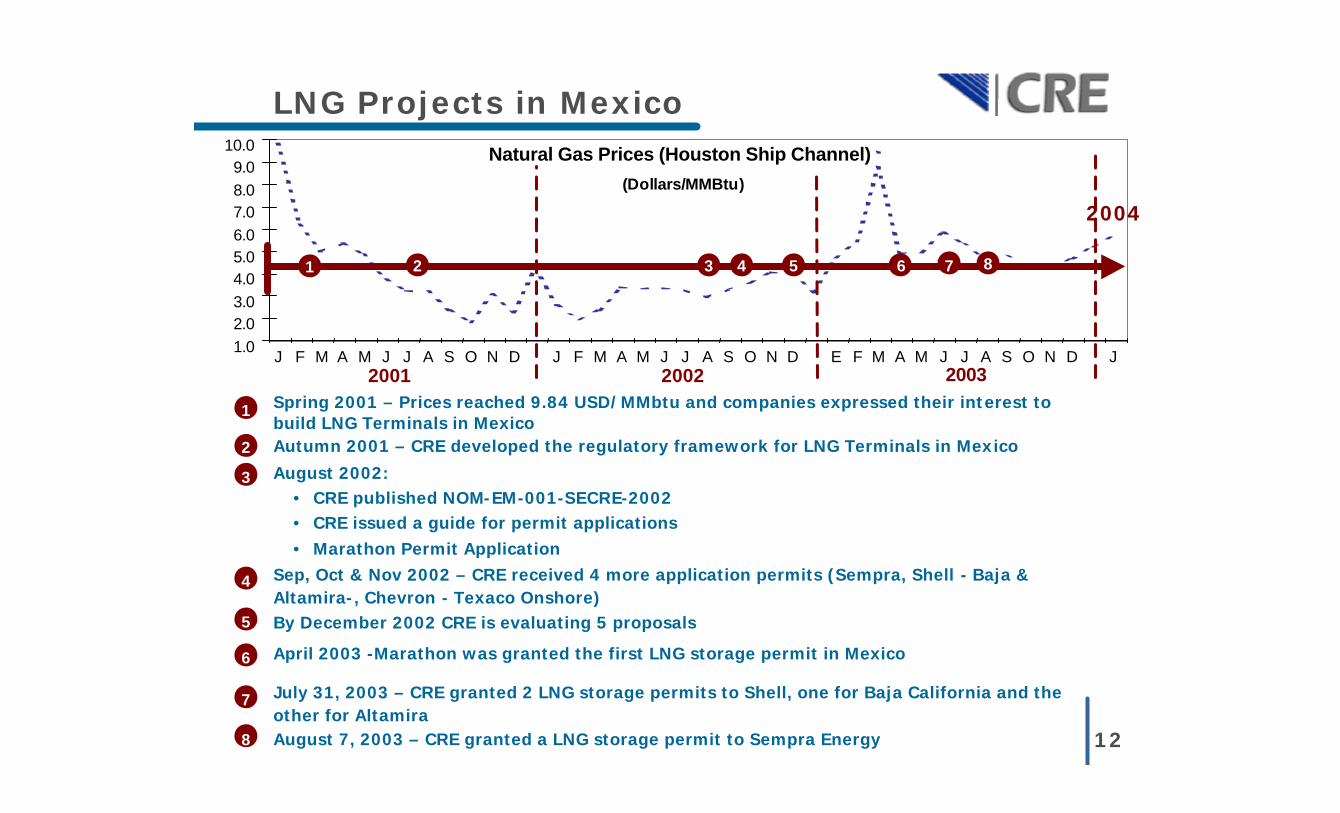

LNG Projects in MexicoNatural Gas Prices (Houston Ship Channel)

(Dollars/MMBtu)

2004

2001 2002 2003

1 2 3 4 5 6 7 8

12

1 Spring 2001 – Prices reached 9.84 USD/MMbtu and companies expressed their interest to build LNG Terminals in Mexico

2 Autumn 2001 – CRE developed the regulatory framework for LNG Terminals in Mexico

3 August 2002:• CRE published NOM-EM-001-SECRE-2002• CRE issued a guide for permit applications

• Marathon Permit Application

6 April 2003 -Marathon was granted the first LNG storage permit in Mexico

4 Sep, Oct & Nov 2002 – CRE received 4 more application permits (Sempra, Shell - Baja & Altamira-, Chevron - Texaco Onshore)

5 By December 2002 CRE is evaluating 5 proposals

7 July 31, 2003 – CRE granted 2 LNG storage permits to Shell, one for Baja California and the other for AltamiraAugust 7, 2003 – CRE granted a LNG storage permit to Sempra Energy8

• Two types of projects

— Bid driven (i.e. Altamira)

— Market driven (i.e. Baja California)

• Regulatory Objectives:

— Safety

— Open Access

— Cost-Based Tariffs

• Several authorizations required

LNG in Mexico

13

Altamira•Shell

Cd. Pemex

Cd Juarez

Chihuahua

Monterrey

Reynosa

Matamoros

TolucaD.F.

Poza Rica

Cd Madero

MexicaliTijuana

RosaritoNaco

LNG Storage Permits Granted

14

Baja California•Marathon (Tijuana)•Sempra (Ensenada)•Shell (Ensenada)

15

LNG Storage Permits in Mexico

Over the last 6 months, the CRE granted 4 permits to build and operate LNG receiving facilities in Mexico

? Three are located in Baja California and one in the Gulf of Mexico

? Potential total firm regasification capacity could be 3.6 bcfd and peak regasification capacity of 4.3 bcfd

? Projects could begin operations in 2006 and 2007

? Open Access requirement on non-contracted capacity

? Storage and regasification tariffs based on cost of providing service

? Projects will diversify sources of gas and help stabilize prices

? Full containment tanks

? Investment commitments, up to 2.4 Billion USD

16

Index

Next StepsNext Steps

17

Offshore LNG Application

Permit Permit ApplicationApplicationChevronChevron--TexacoTexaco

Adittional Adittional Information Information

DeliveryDelivery

AdmissionAdmissionto Formal to Formal Review Review

andandPublicationPublication

Proposal Proposal EvaluationEvaluation

DecisionDecision

10/07/02 12/10/02 01/21/03 2004

Chevron-Texaco de México

Offshore Offshore ApplicationApplication

On July 29, 2003 ChevronTexaco submited a modification regarding the site for the LNG storage facility to place it in the Pacific Ocean, nearby the Coronado Islands

Cd. Pemex

Cd Juarez

Chihuahua

Monterrey

Reynosa

Matamoros

Burgos

TolucaD.F.

Poza Rica

Cd Madero

MexicaliTijuana

RosaritoNaco

Lázaro Cárdenas?

Baja California(Offshore)

Other Possible LNG Storage Terminals

18

Manzanillo?

Topolobampo?

Península de Yucatán

Salina Cruz

19

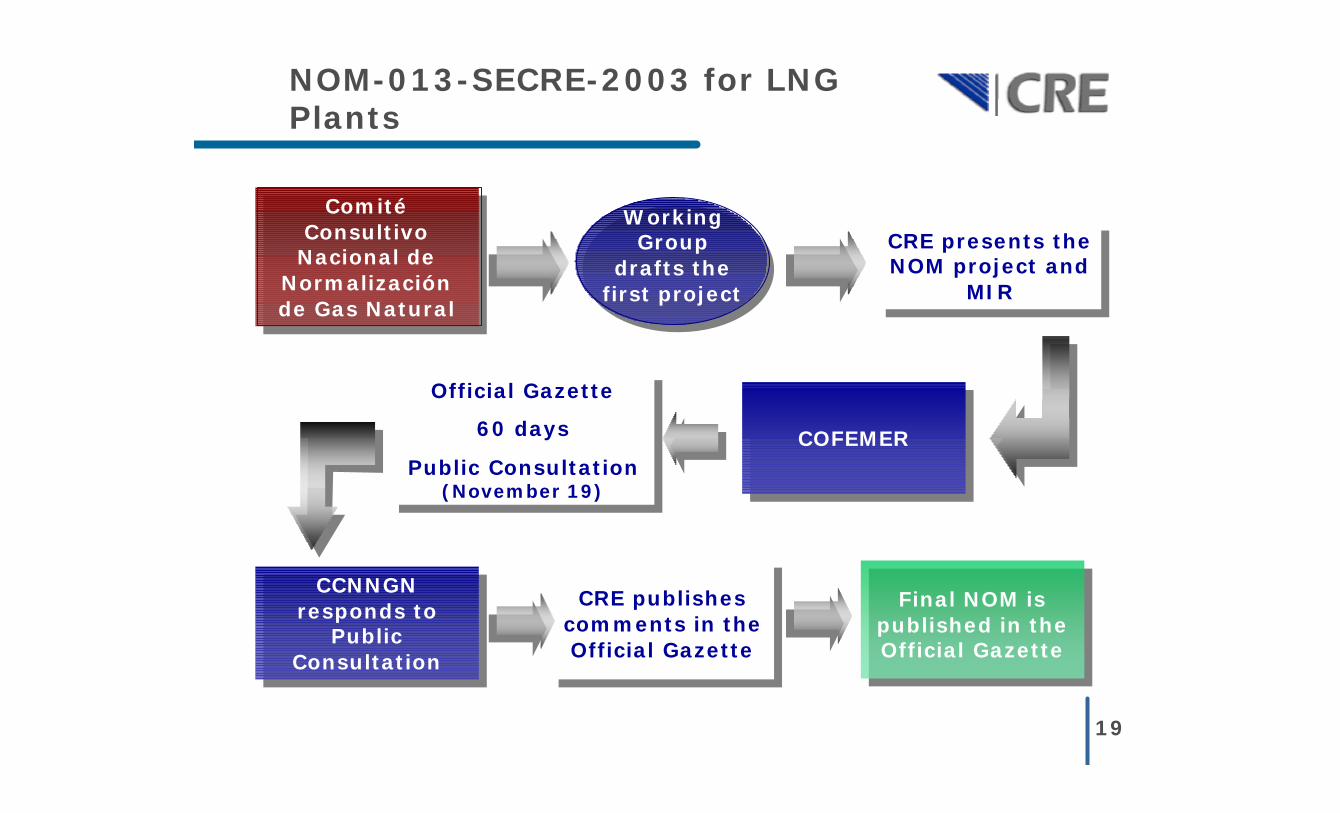

Comité Consultivo Nacional de

Normalización de Gas Natural

Comité Consultivo Nacional de

Normalización de Gas Natural

Working Group

drafts the first project

CRE presents the NOM project and

MIR

CRE presents the NOM project and

MIR

COFEMERCOFEMER

Official Gazette

60 days

Public Consultation(November 19)

Official Gazette

60 days

Public Consultation(November 19)

CCNNGN responds to

Public Consultation

CCNNGN responds to

Public Consultation

CRE publishes comments in the Official Gazette

CRE publishes comments in the Official Gazette

Final NOM is published in the Official Gazette

Final NOM is published in the Official Gazette

NOM-013-SECRE-2003 for LNG Plants

Regulation for Storage Permits

20

• Technical description of the project

• Technical, administrative and financial capability of

project

• Description of safety methods and procedures for the

operation and maintenance of the system

• Non-discriminatory General Terms of Service

• Information on Potential Supply sources

• Justification of potential demand

• Compliance with NOM

Applicants must include among others:

Regulated Activities

21

CRE Permit

SEMARNAT Permit

Other

Permits

Use of Land Permit

Financing

Commercial

Agreements

22

Index

III.III. Lessons LearnedLessons Learned

23

Lessons Learned

Educate, Educate, Educate

The regulatory framework has to adapt permanently to provide stability and certainity to investors

No project is alike

Mexico has to increase its natural gas supply

LNG storage projects will diversify the sources of natural gas and help stabilize prices

www.cre.gob.mxwww.cre.gob.mx