lloyd hain - ame group

TRANSCRIPT

Page 1

The Competitive Position of Australia in the Seaborne

Market

Lloyd Hain –Technical Research Manager Coal

Page 2

Agenda

• Major Markets for Australian Coal

• How Competitive are Australian Longwalls

• Competitiveness of Longwalls Globally

Hong Kong London Sydney Toronto

Page 3

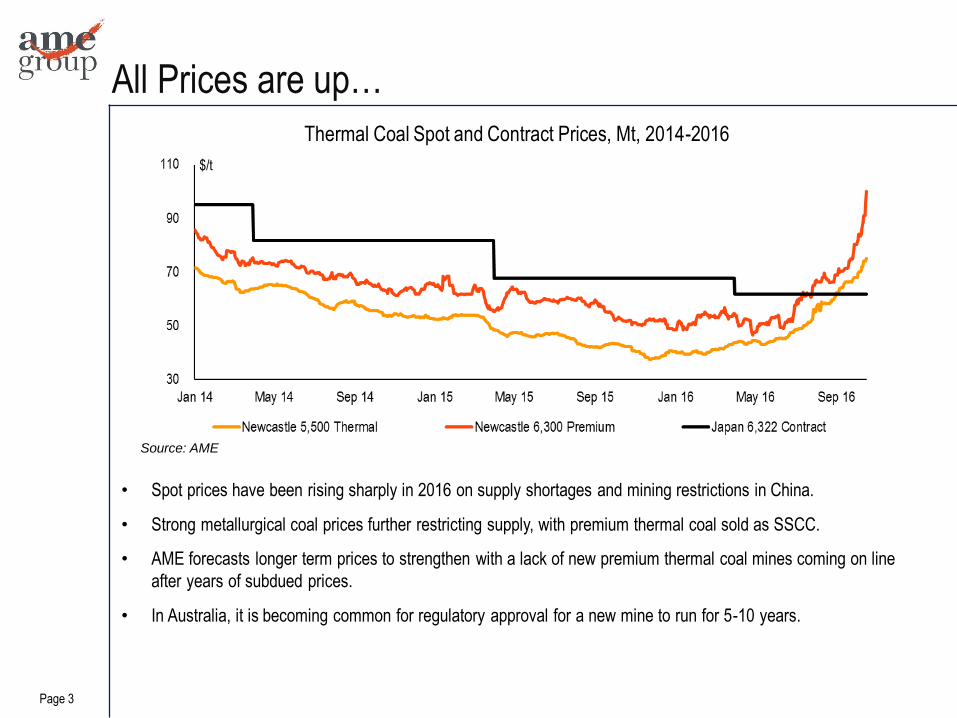

All Prices are up…

• Spot prices have been rising sharply in 2016 on supply shortages and mining restrictions in China.

• Strong metallurgical coal prices further restricting supply, with premium thermal coal sold as SSCC.

• AME forecasts longer term prices to strengthen with a lack of new premium thermal coal mines coming on line

after years of subdued prices.

• In Australia, it is becoming common for regulatory approval for a new mine to run for 5-10 years.

Thermal Coal Spot and Contract Prices, Mt, 2014-2016

Source: AME

$/t

Page 4

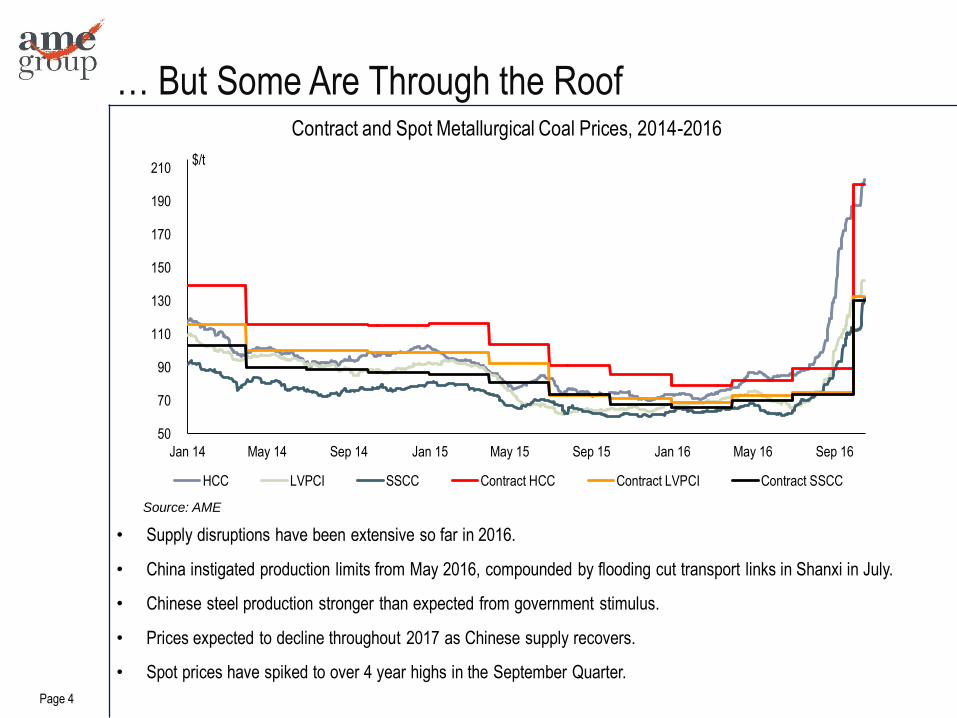

… But Some Are Through the Roof

• Supply disruptions have been extensive so far in 2016.

• China instigated production limits from May 2016, compounded by flooding cut transport links in Shanxi in July.

• Chinese steel production stronger than expected from government stimulus.

• Prices expected to decline throughout 2017 as Chinese supply recovers.

• Spot prices have spiked to over 4 year highs in the September Quarter.

Contract and Spot Metallurgical Coal Prices, 2014-2016

50

70

90

110

130

150

170

190

210

Jan 14 May 14 Sep 14 Jan 15 May 15 Sep 15 Jan 16 May 16 Sep 16

HCC LVPCI SSCC Contract HCC Contract LVPCI Contract SSCC

Source: AME

$/t

Page 5

Where Does the Coal Go…

• North Asia is by far the biggest market for Australian coal, and is still growing

• Chinese demand for Australian coal peaked in 2014 at ~ 24% of exports

• Indian demand has failed to materialize as expected

Australian Coal Exports, 2012-2016

Source: AME, ABS

0

450

2012 2013 2014 2015 2016

China North Asia India Europe Americas SE Asia Other

Mt

Page 6

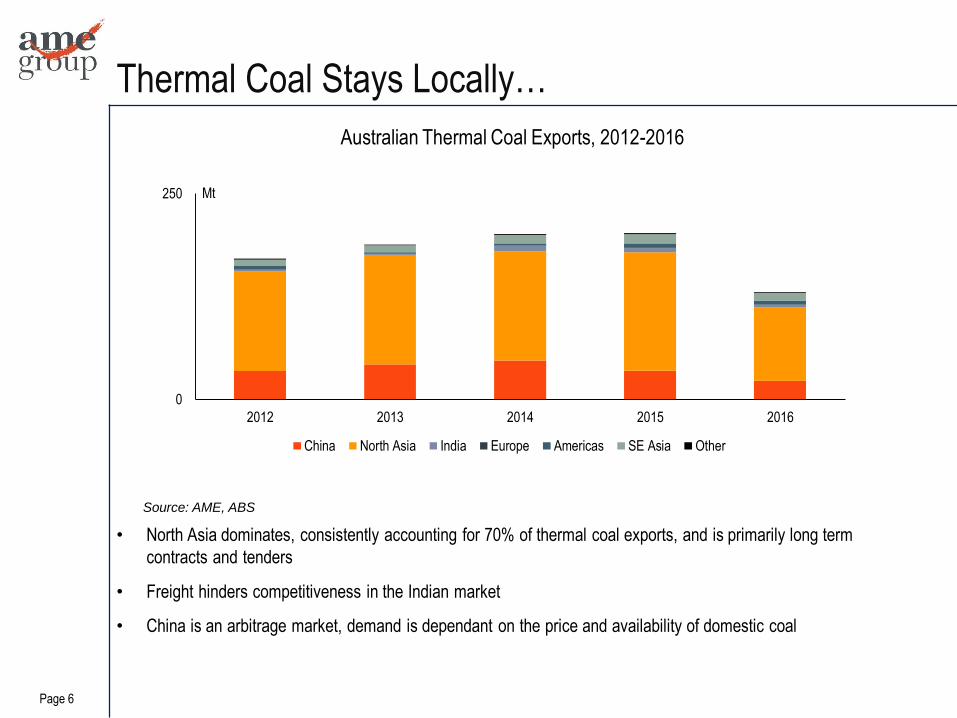

Thermal Coal Stays Locally…

• North Asia dominates, consistently accounting for 70% of thermal coal exports, and is primarily long term

contracts and tenders

• Freight hinders competitiveness in the Indian market

• China is an arbitrage market, demand is dependant on the price and availability of domestic coal

Australian Thermal Coal Exports, 2012-2016

Source: AME, ABS

0

250

2012 2013 2014 2015 2016

China North Asia India Europe Americas SE Asia Other

Mt

Page 7

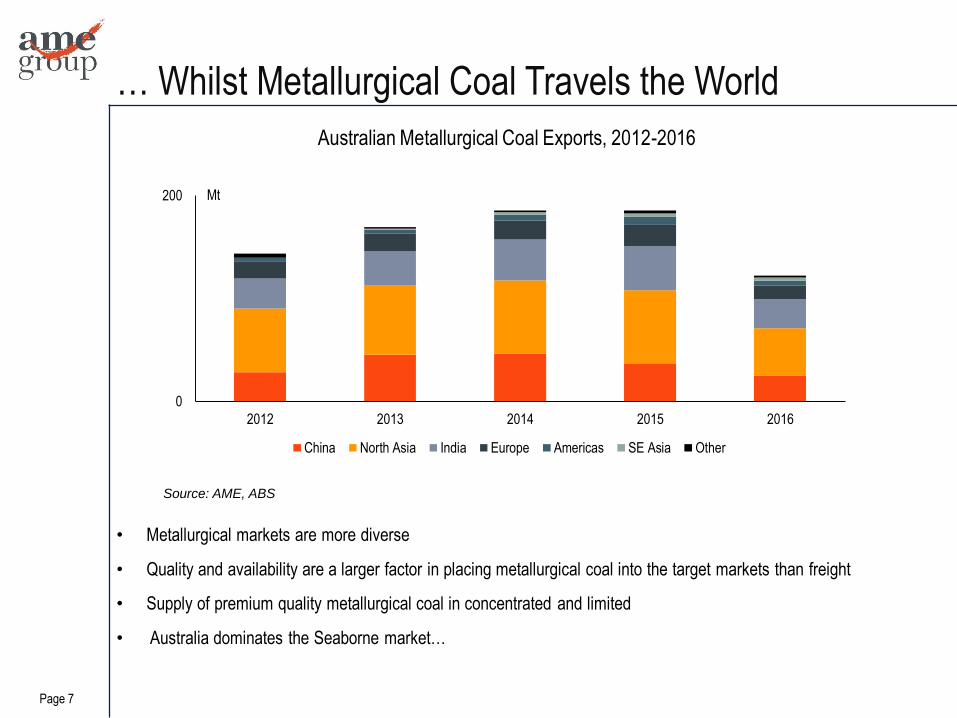

… Whilst Metallurgical Coal Travels the World

• Metallurgical markets are more diverse

• Quality and availability are a larger factor in placing metallurgical coal into the target markets than freight

• Supply of premium quality metallurgical coal in concentrated and limited

• Australia dominates the Seaborne market…

Australian Metallurgical Coal Exports, 2012-2016

Source: AME, ABS

0

200

2012 2013 2014 2015 2016

China North Asia India Europe Americas SE Asia Other

Mt

Page 8

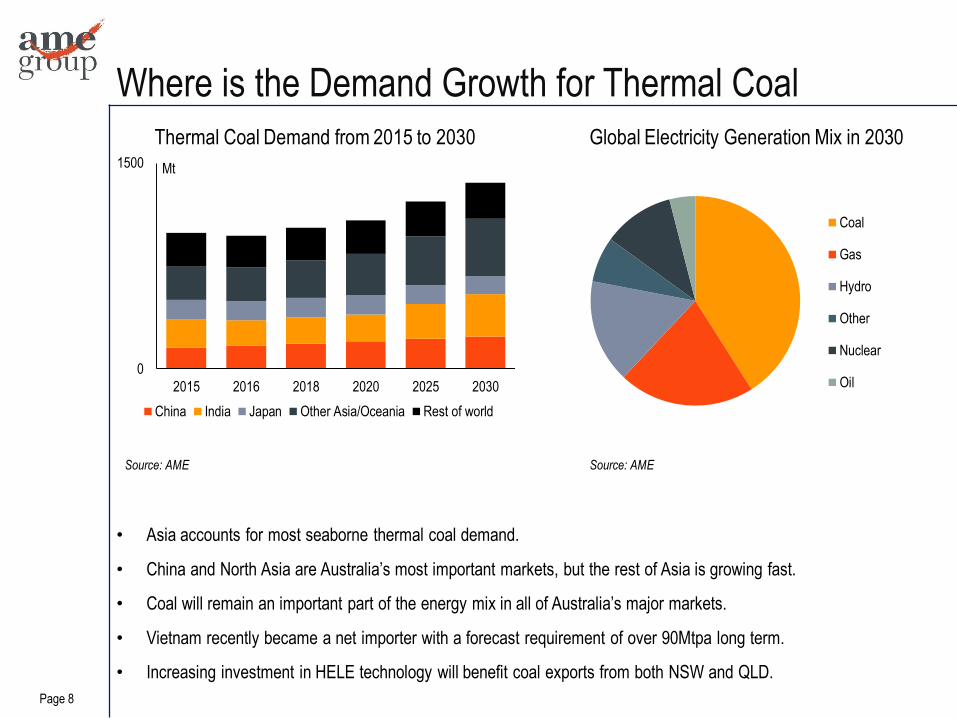

Where is the Demand Growth for Thermal Coal

• Asia accounts for most seaborne thermal coal demand.

• China and North Asia are Australia’s most important markets, but the rest of Asia is growing fast.

• Coal will remain an important part of the energy mix in all of Australia’s major markets.

• Vietnam recently became a net importer with a forecast requirement of over 90Mtpa long term.

• Increasing investment in HELE technology will benefit coal exports from both NSW and QLD.

Global Electricity Generation Mix in 2030Thermal Coal Demand from 2015 to 2030

Source: AME

0

1500

2015 2016 2018 2020 2025 2030

China India Japan Other Asia/Oceania Rest of world

Source: AME

Mt

Coal

Gas

Hydro

Other

Nuclear

Oil

Page 9

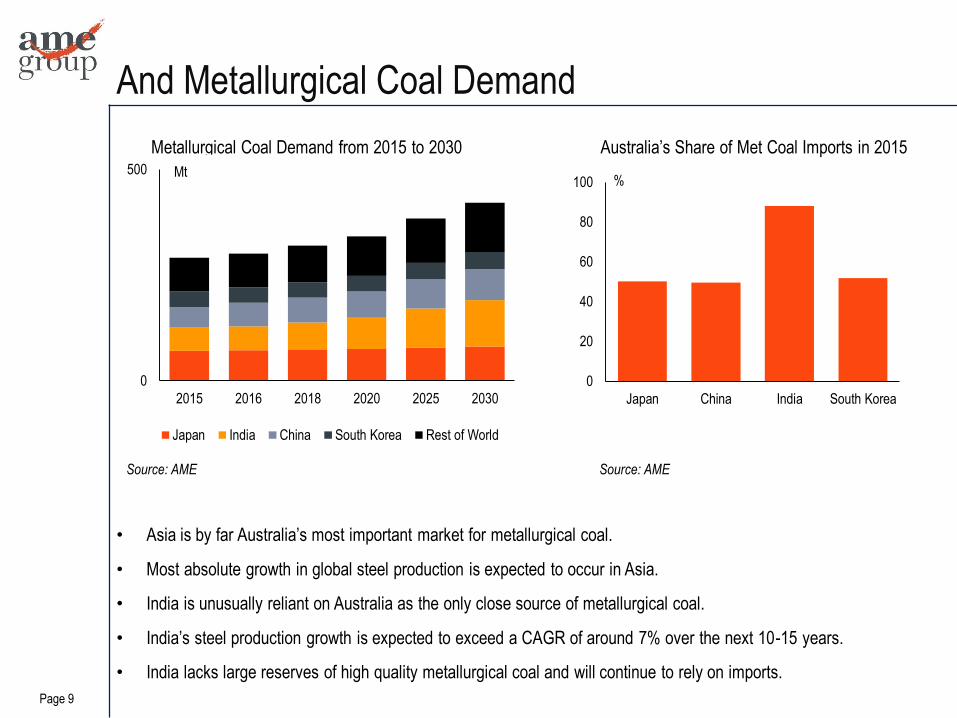

And Metallurgical Coal Demand

• Asia is by far Australia’s most important market for metallurgical coal.

• Most absolute growth in global steel production is expected to occur in Asia.

• India is unusually reliant on Australia as the only close source of metallurgical coal.

• India’s steel production growth is expected to exceed a CAGR of around 7% over the next 10-15 years.

• India lacks large reserves of high quality metallurgical coal and will continue to rely on imports.

Australia’s Share of Met Coal Imports in 2015Metallurgical Coal Demand from 2015 to 2030

0

20

40

60

80

100

Japan China India South Korea

%

Source: AMESource: AME

0

500

2015 2016 2018 2020 2025 2030

Japan India China South Korea Rest of World

Mt

Page 10

Agenda

• The Major Markets for Australian Coal

• How Competitive are Australian Longwalls

• Competitiveness of Longwalls Globally

Hong Kong London Sydney Toronto

Page 11

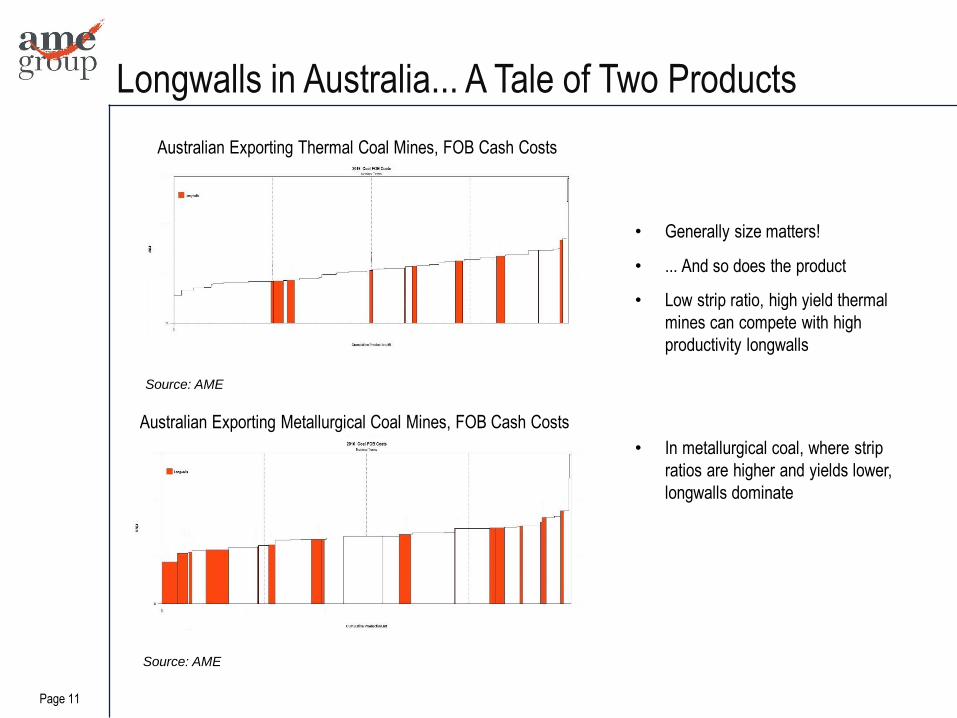

• Generally size matters!

• ... And so does the product

• Low strip ratio, high yield thermal

mines can compete with high

productivity longwalls

• In metallurgical coal, where strip

ratios are higher and yields lower,

longwalls dominate

Australian Exporting Metallurgical Coal Mines, FOB Cash Costs

Australian Exporting Thermal Coal Mines, FOB Cash Costs

Source: AME

Longwalls in Australia... A Tale of Two Products

Source: AME

Page 12

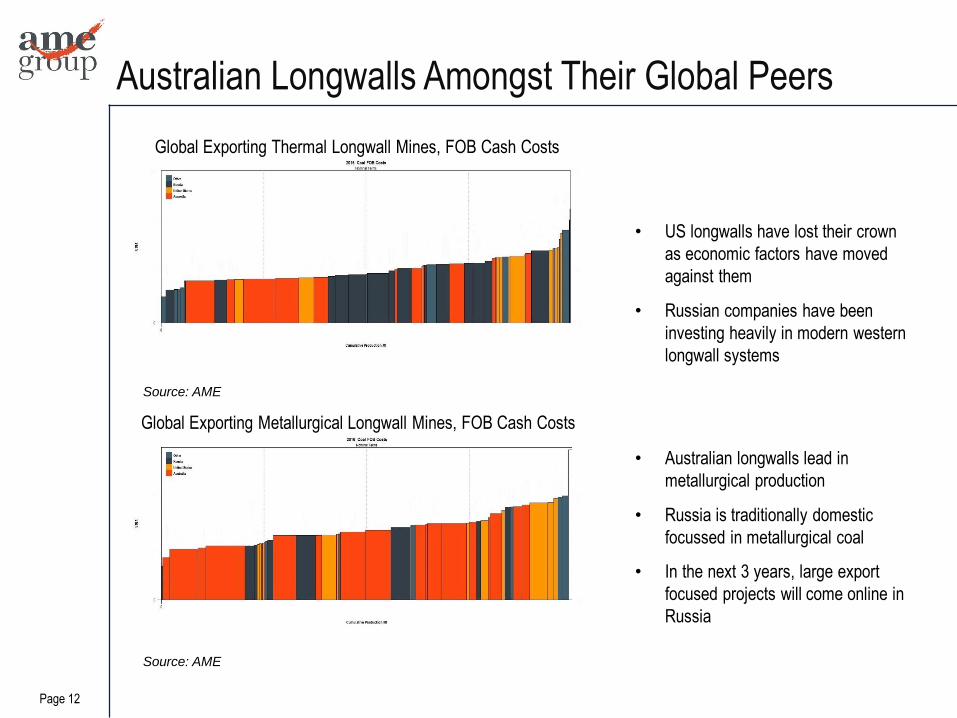

Australian Longwalls Amongst Their Global Peers

• US longwalls have lost their crown

as economic factors have moved

against them

• Russian companies have been

investing heavily in modern western

longwall systems

• Australian longwalls lead in

metallurgical production

• Russia is traditionally domestic

focussed in metallurgical coal

• In the next 3 years, large export

focused projects will come online in

Russia

Global Exporting Thermal Longwall Mines, FOB Cash Costs

Source: AME

Source: AME

Global Exporting Metallurgical Longwall Mines, FOB Cash Costs

Page 13

Agenda

• The Major Markets for Australian Coal

• How Competitive are Australian Longwalls

• Competitiveness of Longwalls Globally

Hong Kong London Sydney Toronto

Page 14

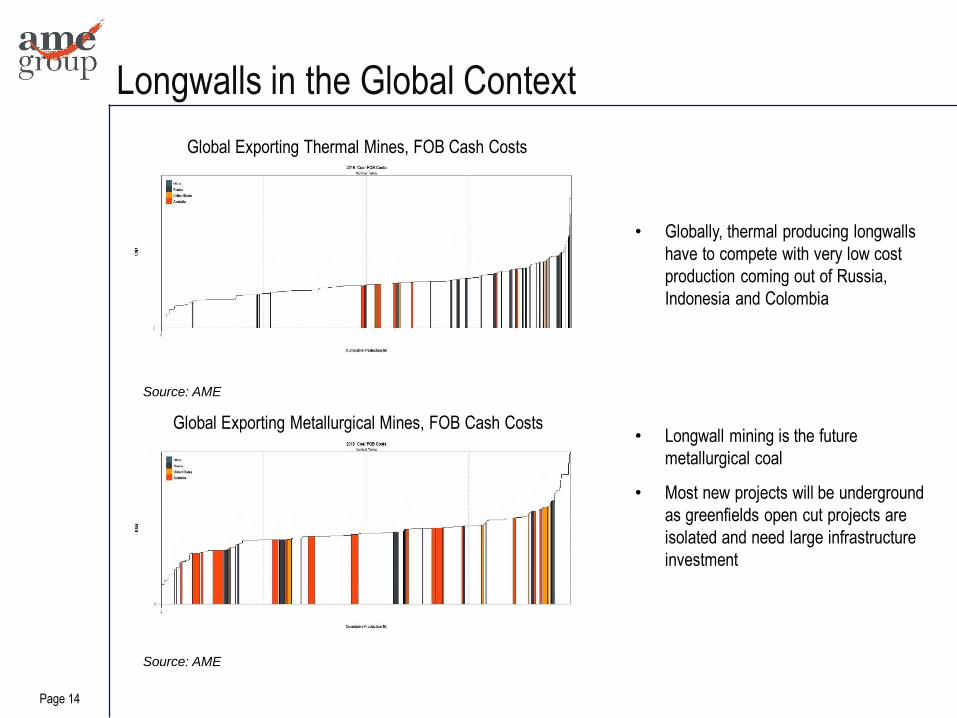

• Globally, thermal producing longwalls

have to compete with very low cost

production coming out of Russia,

Indonesia and Colombia

• Longwall mining is the future

metallurgical coal

• Most new projects will be underground

as greenfields open cut projects are

isolated and need large infrastructure

investment

Global Exporting Thermal Mines, FOB Cash Costs

Source: AME

Source: AME

Global Exporting Metallurgical Mines, FOB Cash Costs

Longwalls in the Global Context

Page 15

Forward looking information

Certain statements and graphics contained in this presentation may contain forward-looking information within the meaning of various securities laws. Such forward-looking

information are identified by words such as "estimates", "intends", "expects", "believes", "may", "will" and included, without limitation, statements regarding the company's

plan of business operations, production levels and costs, potential contractual arrangements and the delivery of equipment, receipt of working capital, anticipated revenues,

mineral reserve and mineral resource estimates, and projected expenditures. There can be no assurance that such statements will prove to be accurate; actual results and

future events could differ materially from such statements. Factors that could cause actual results to differ materially include, among others, metal prices, risks inherent in

the mining industry, financing risks, labour risks, uncertainty of mineral reserve and resource estimates, equipment and supply risks, regulatory risks and environmental

concerns. Most of these factors are outside the control of the company. Investors are cautioned not to put undue reliance on forward-looking information. Except as

otherwise required by applicable securities statutes or regulation, the company expressly disclaims any intent or obligation to update publicly forward-looking information,

whether as a result of new information, future events or otherwise.

Copyright @ AME Group 2016

For further details, please visit our website at www.amegroup.com

Contact Details and Important Notices

Hong Kong

t: +852 2846 8220

London

t: +44 20 3752 7277

Sydney

t: +61 2 9262 2264

Toronto

t: +1 646 736 7887