listing on sgx

TRANSCRIPT

Listing on Singapore Exchange (SGX)

December 2010

PricewaterhouseCoopers Corporate Finance Pte Ltd

Draft for discussion - Strictly Private and Confidential

Important Notice

The information and opinions expressed in this document have been obtained from public and private sources believed to be

reliable, but no representation or warranty, express or implied, is made that such information is accurate or complete and it

should not be relied upon as such.

Information and opinions contained in this document are not to be relied upon as authoritative or taken in substitution for the

exercise of judgment by you, and are subject to change without notice. Please note that any prospective financial information

contained in the document is based on assumptions regarding future events, which may or may not occur as assumed and

consequently the actual results achieved may materially differ from those presented in this document.

This document is not, and should not be construed as, an offer document or an offer or solicitation to buy, sell or otherwise

deal in any securities, assets or liabilities. While PricewaterhouseCoopers Corporate Finance Pte Ltd (“PwCCF”) has

assembled the data presented, it does not accept responsibility for the accuracy of any of the data included in this report.

In no event will PwCCF or its related partnerships or corporations, or the partners, agents or employees thereof be liable for

any decision or any direct or consequential loss arising from any use of material contained in this document.

By accepting this document, you agree to be bound by the foregoing limitations. This document, related material and

analysis, at all times, remains the property of PwCCF, and may not be reproduced, distributed, disseminated, revealed or

published for any purpose, without the explicit, prior written approval of PwCCF.

Agenda

1. Introduction

2. IPO process and key issues

3. RTO process and key issues

4. Why PwCCF

PricewaterhouseCoopers Corporate Finance

Private & Confidential

September 2008

Page 4

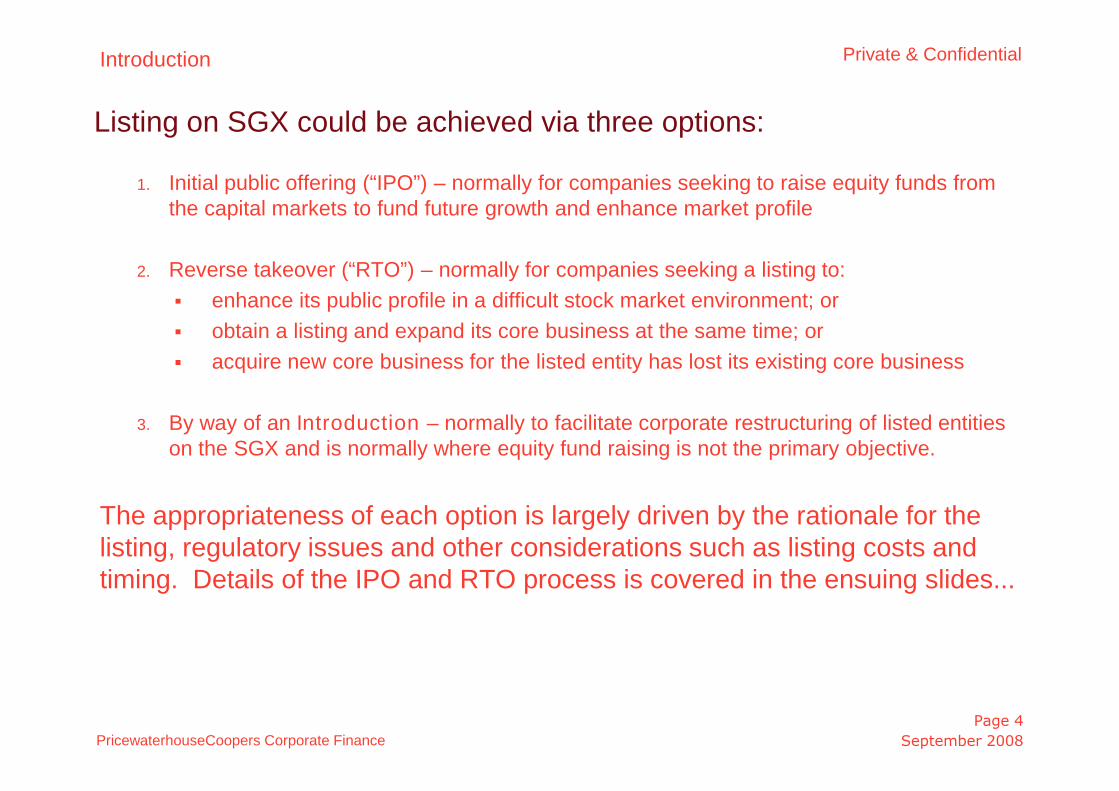

Listing on SGX could be achieved via three options:

1. Initial public offering (“IPO”) – normally for companies seeking to raise equity funds fromthe capital markets to fund future growth and enhance market profile

2. Reverse takeover (“RTO”) – normally for companies seeking a listing to:

enhance its public profile in a difficult stock market environment; or

obtain a listing and expand its core business at the same time; or

acquire new core business for the listed entity has lost its existing core business

3. By way of an Introduction – normally to facilitate corporate restructuring of listed entitieson the SGX and is normally where equity fund raising is not the primary objective.

The appropriateness of each option is largely driven by the rationale for thelisting, regulatory issues and other considerations such as listing costs andtiming. Details of the IPO and RTO process is covered in the ensuing slides...

Introduction

Agenda

1. Introduction

2. IPO process and key issues

3. RTO process and key issues

4. Why PwCCF

Draft for discussion - Private & Confidential

Page 6PricewaterhouseCoopers Corporate Finance Pte Ltd

Basic financial listing requirements for SGX MainBoard –current and proposed

Current criteria Proposed criteria (in consultation)

Pre-tax profits Market cap Pre-tax profits Market cap

Criteria 1 S$7.5m cumulativeover 3 years; and notless than S$1m in eachof those 3 years

Nil Profitable in latestfinancial year (excl.non-recurring itemsetc.)

Operating track recordof 3 years

S$150 million basedon issue price andpost-invitation issuedshare capital

Criteria 2 S$10m in 1 or 2 years Nil Operating revenue(either actual or proforma) in the latestfinancial year of>S$300m

At least S$300 millionbased on issue price*and post-invitationissued share capital

Criteria 3 Nil S$80m based onissue price

NA NA

* Issue price to be raised to S$0.50 from S$0.20

Mainboard listing aspirants to satisfy one of the following criteria

IPO process and key issues

Draft for discussion - Private & Confidential

Page 7PricewaterhouseCoopers Corporate Finance Pte Ltd

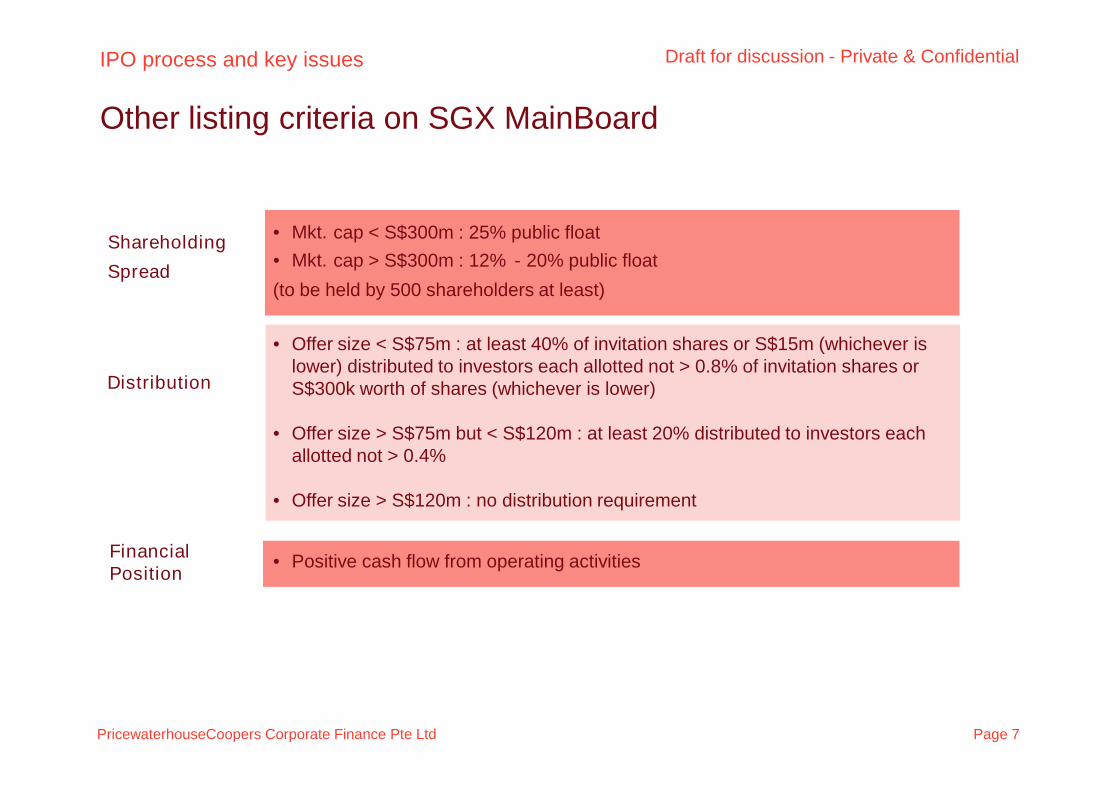

Other listing criteria on SGX MainBoard

Shareholding

Spread

Distribution

FinancialPosition

• Mkt. cap < S$300m : 25% public float

• Mkt. cap > S$300m : 12% - 20% public float

(to be held by 500 shareholders at least)

• Offer size < S$75m : at least 40% of invitation shares or S$15m (whichever islower) distributed to investors each allotted not > 0.8% of invitation shares orS$300k worth of shares (whichever is lower)

• Offer size > S$75m but < S$120m : at least 20% distributed to investors eachallotted not > 0.4%

• Offer size > S$120m : no distribution requirement

• Positive cash flow from operating activities

IPO process and key issues

January 2009

Strictly Private & Confidential – Not for circulation

Page 8

- Maintains statutory records as well as share registers.

- Prepares documentation for new company structure.

Key Roles of Different Professionals in the Listing Process

- Prepare the accountants’ report.

- Review the profit and cash flow forecasts.

- Report on internal control and accounting system.

- Organises press conferences and publicity events.

- Handles corporate communication matters related to the IPO.

The Issuer(providesnecessary

information)

OtherProfessionals Registrar

Public relations

consultant

Company

secretary

KeyProfessionals

Lead manager

Underwritersand placementagents

Reporting

accountants

- Prepares the Company for listing and manages the entire listing

process up to trading day.

- Liaises with SGX on all matters arising from the application for

listing.

- Underwrite the IPO and place the shares, if required.

Solicitors

- Review litigation matters and verify all legal documents pertaining

to the Issuer.

- Prepare underwriting and placement agreements.

- Draw up directors’ service contracts.

- Processes share applications and allotments.

- Refunds excess application monies.

IPO process and key issues

PricewaterhouseCoopers Corporate Finance Pte Ltd

Draft for discussion - Private & Confidential

Page 9PricewaterhouseCoopers Corporate Finance Pte Ltd

Indicative Timeline for Listing

Appointment of professional parties

Completion of due diligence

Finalisation of Accountant’s Report

Verification Meetings

Drafting of Prospectus

Week 0 – 22

Submission to the SingaporeExchange

Approval from Singapore Exchange

Week 22 - 30

Submission of ListingApplication to MAS

Approval from MAS

Week 30 - 34

Completion of IPO (ie. roadshows, printing etc.)

Listing on SGX

Week 34 - 36

The timeframe for the entire listing process varies for different companies. On the average, the wholeprocess should take not more than nine months:

IPO process and key issues

Draft for discussion - Private & Confidential

Page 10PricewaterhouseCoopers Corporate Finance Pte Ltd

Good attributes of an IPO candidate

Strong financial track record

Cashflow positive with healthy balance sheet

Strong market share and not dependent on any singlecustomer or supplier

Recognizable/established brand name

Sustainable and scalable growth with healthy margins

Market leading products with new products launchedfrequently

Proven, established management team and continuity

Good Corporate Governance culture

Strong ROI/ROE

IPO process and key issues

January 2009

Strictly Private & Confidential – Not for circulation

Page 11

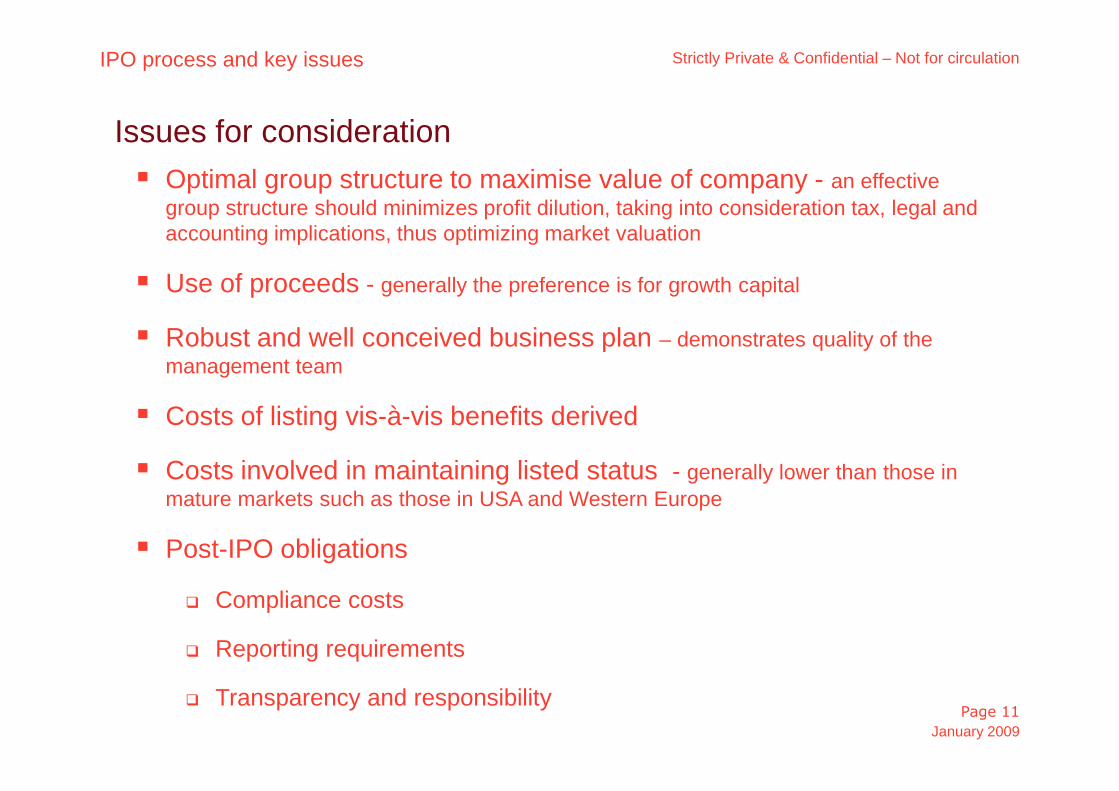

Issues for consideration

Optimal group structure to maximise value of company - an effective

group structure should minimizes profit dilution, taking into consideration tax, legal andaccounting implications, thus optimizing market valuation

Use of proceeds - generally the preference is for growth capital

Robust and well conceived business plan – demonstrates quality of the

management team

Costs of listing vis-à-vis benefits derived

Costs involved in maintaining listed status - generally lower than those in

mature markets such as those in USA and Western Europe

Post-IPO obligations

Compliance costs

Reporting requirements

Transparency and responsibility

IPO process and key issues

Agenda

1. Introduction

2. IPO process and key issues

3. RTO process and key issues

4. Why PwCCF

Draft for discussion - Private & Confidential

Page 13PricewaterhouseCoopers Corporate Finance Pte Ltd

Why RTO?

• Ownership of a listed company

Increased liquidity of their shares

Ability to tap the capital markets for funds andleverage on its new listed status

• Better bargaining power to secure a good valuefor the assets to be transferred to the listed entityas oppose to negotiating with the underwriters inan IPO

• Greater certainty of listing as there is only a needfor a smaller compliance share placement*;compared to an IPO where the entire public floatis subject to fickle market sentiment during theoffer period

• More flexible timing

Benefits to the Target Benefits to listed company’s shareholders

• Revived market interest and thus theenhanced share price in listed company viathe attraction of an acquisition of a qualitybusiness and strong management team

• Existing shareholders will be part owners ofthe enlarged entity (Listed Co + Target)although their shareholding will be diluted

• Strong growth potential via organic growth orthrough acquisitions of other players in theregion or complimentary businesses

* Share placement may be required to ensure sufficient public float ismet and/or also to raise new funds. Placements to the public wouldneed to meet the shareholding distribution rules as applicable to IPO

RTO process and key issues

Draft for discussion - Private & Confidential

Page 14PricewaterhouseCoopers Corporate Finance Pte Ltd

The RTO Process

The timeframe for a listing varies for different companies. In normal market conditions, the wholeprocess may take about 6 – 9 months. The specific timeframe in this case would depend on activelymanaging the SGX query resolution process which may range from 6 weeks to 12 weeks.

Listed Shellholds EGM to

obtainShareholders’

approval

Financial &Legal DD ofTarget andListed Shell

Drafting &execution

of conditionalS&P

Agreement(s)

Appointmentof

FinancialAdviser

Completionof RTO

Agree-in-principle on

deal structure- Term sheet

ReceiveApproval-In-Principle fromSGX and SIC

Pre-clearance fromSGX on Target and

from SIC onwhitewash resolution,

if any

Appointmentof

Legal Adviser

Shareplacement, if

applicable

RTO process and key issues

Preparation ofCircular andverificationmeetings

Submissionto SGX

Presentation ofRTO proposal/structure toListed Shell’s

Board

Appointment ofother

professionalparties

Report fromindependent

financialadviser

Draft for discussion - Private & Confidential

Page 15PricewaterhouseCoopers Corporate Finance Pte Ltd

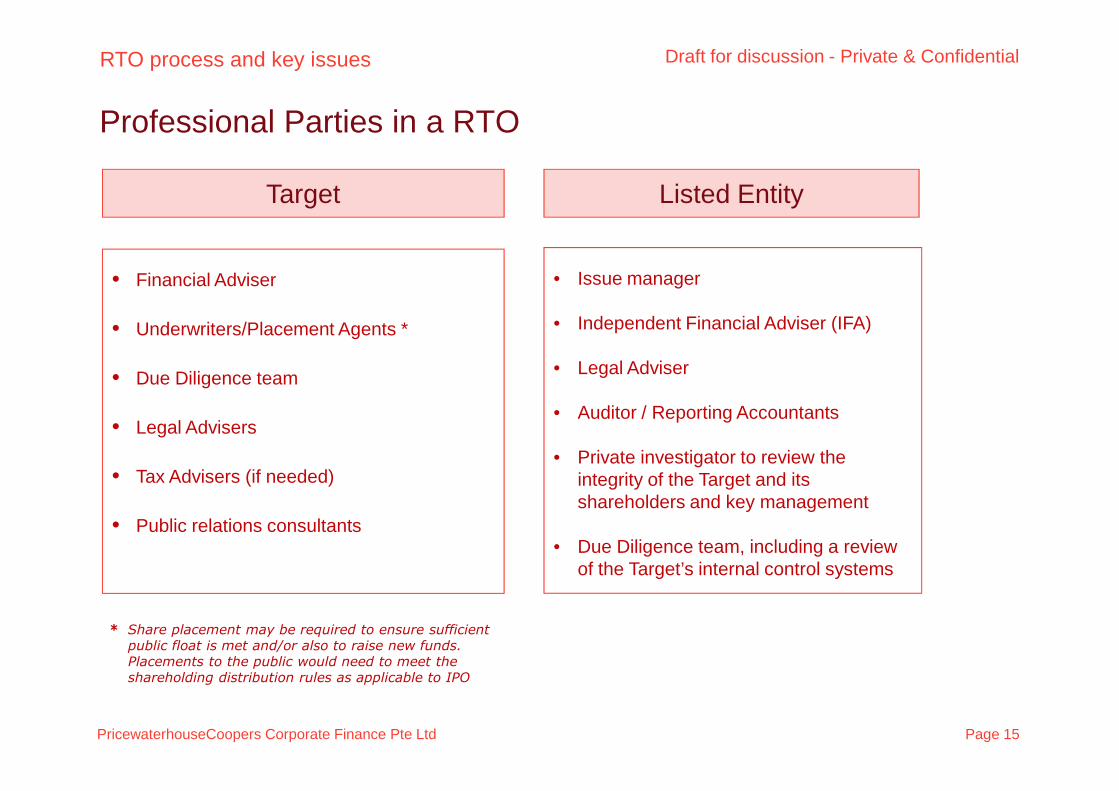

• Financial Adviser

• Underwriters/Placement Agents *

• Due Diligence team

• Legal Advisers

• Tax Advisers (if needed)

• Public relations consultants

Professional Parties in a RTO

• Issue manager

• Independent Financial Adviser (IFA)

• Legal Adviser

• Auditor / Reporting Accountants

• Private investigator to review theintegrity of the Target and itsshareholders and key management

• Due Diligence team, including a reviewof the Target’s internal control systems

Target Listed Entity

* Share placement may be required to ensure sufficientpublic float is met and/or also to raise new funds.Placements to the public would need to meet theshareholding distribution rules as applicable to IPO

RTO process and key issues

Draft for discussion - Private & Confidential

Page 16PricewaterhouseCoopers Corporate Finance Pte Ltd

Roles of key professional parties to be engaged by Target

• Independent investigation of Target track record and management’s history

Public relationsconsultant

Target

Financialadviser

Underwriter/placement agent

Privateinvestigator

• Lead negotiations on structure and valuation with Listed Shell and its advisers

• Review legal documentation and SGX circulars/announcements on Target

• Co-ordinate with Listed Shell and its advisers on all matters arising from application to SGX/SIC

• Placement of shares to meet public float and shareholding spread (if required)

Solicitors

RTO process and key issues

• Review litigation matters and verify legal documents relating to Listed Shell including shareholder’scircular and whitewash waiver application to SIC

• Obtain SIC clearance and other regulatory matters

• Organizes press conferences and publicity events

• Handles corporate communication matters related to the RTO

• Financial due diligence and review of the internal control and accounting systemDue Diligence

• Prepares the accountants’ report

• Reviews the board memorandum (i.e. profit projections) of Target

• Opinion to independent directors on valuation and structure for the benefit of minority shareholdersIndependentfinancial adviser

Issue manager

• Liaise with SGX to address queries relating to RTO application

• Co-ordinate with all professional parties acting for Listed Shell and project manage the RTO process

Tax advisers • Develop an optimal tax efficient structure for Target’s sale of business

ListedShell

Reportingaccountants

• Review SPA, prepare and lodge circular, additional listing application

• Organise verification meetings and represent Listed Shell in all relevant meetings with SGX/SICLegal adviser

Draft for discussion - Private & Confidential

Page 17PricewaterhouseCoopers Corporate Finance Pte Ltd

Key issues envisaged in the RTO process

Develop and design the right RTO structure should optimise valuation and facilitate a smoothapplication process

• Quality of Target’s business and management team from both the regulators’ and the market’sperspectives

potential conflict of interests with related companies (similar shareholders) outside the listing group

• Valuation

Valuation of Target and/or its businesses to be injected

Valuation of listed company

• Corporate restructuring of Target, if required (More to avoid potential conflict of interests and to excludecertain non-core businesses)

Timing and costs

• There is little difference in the SGX’s review process for both RTO and IPO (Mainboard listing criteriaare being revised, further detailed in next slide)

• Contingent on the listed company’s shareholders approval at the EGM

RTO process and key issues

Agenda

1. Introduction

2. IPO process and key issues

3. RTO process and key issues

4. Why PwCCF

PricewaterhouseCoopers Corporate Finance

Draft for discussion - Private & Confidential

Page 19

PricewaterhouseCoopers (www.pwc.com) provides industry-focused assurance, tax and advisory services to build public trustand enhance value for its clients and their stakeholders. More than 155,000 people in 153 countries across our network sharetheir thinking, experience and solutions to develop fresh perspectives and practical advice

Assurance

Tax

Financial Services

Technology, Media &Telecommunications

Global coverageServices Industries

advisoryConsumer & IndustrialProducts and Services

Asia Pacific

North America Europe

Latin America Africa

PwC is a global professional service firm…

Why PwCCF

Page 19

PricewaterhouseCoopers Corporate Finance

Draft for discussion - Private & Confidential

Page 20

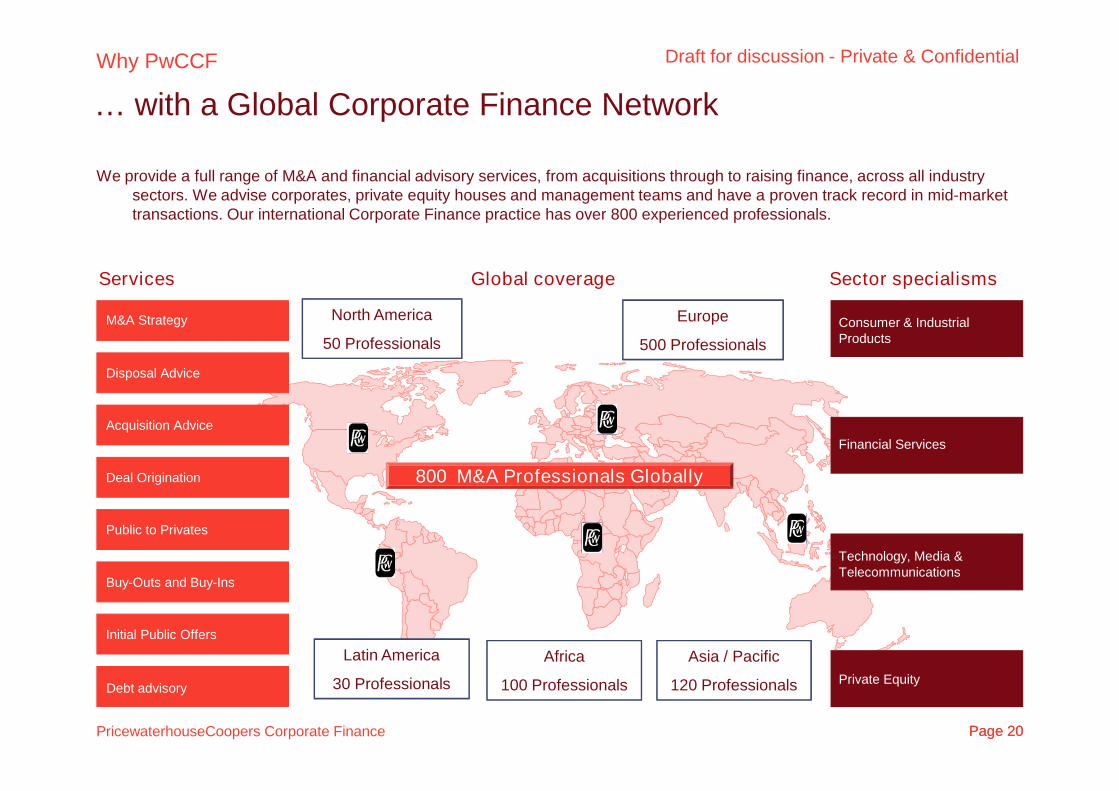

… with a Global Corporate Finance Network

We provide a full range of M&A and financial advisory services, from acquisitions through to raising finance, across all industrysectors. We advise corporates, private equity houses and management teams and have a proven track record in mid-markettransactions. Our international Corporate Finance practice has over 800 experienced professionals.

Global coverageServices Sector specialisms

M&A Strategy

Disposal Advice

Deal Origination

Public to Privates

Buy-Outs and Buy-Ins

Consumer & IndustrialProducts

Financial Services

Technology, Media &Telecommunications

Acquisition Advice

Initial Public Offers

Private EquityDebt advisory

800 M&A Professionals Globally

North America

50 Professionals

Europe

500 Professionals

Latin America

30 Professionals

Africa

100 Professionals

Asia / Pacific

120 Professionals

Page 20

Why PwCCF

Draft for discussion - Private & Confidential

Page 21PricewaterhouseCoopers Corporate Finance Pte Ltd

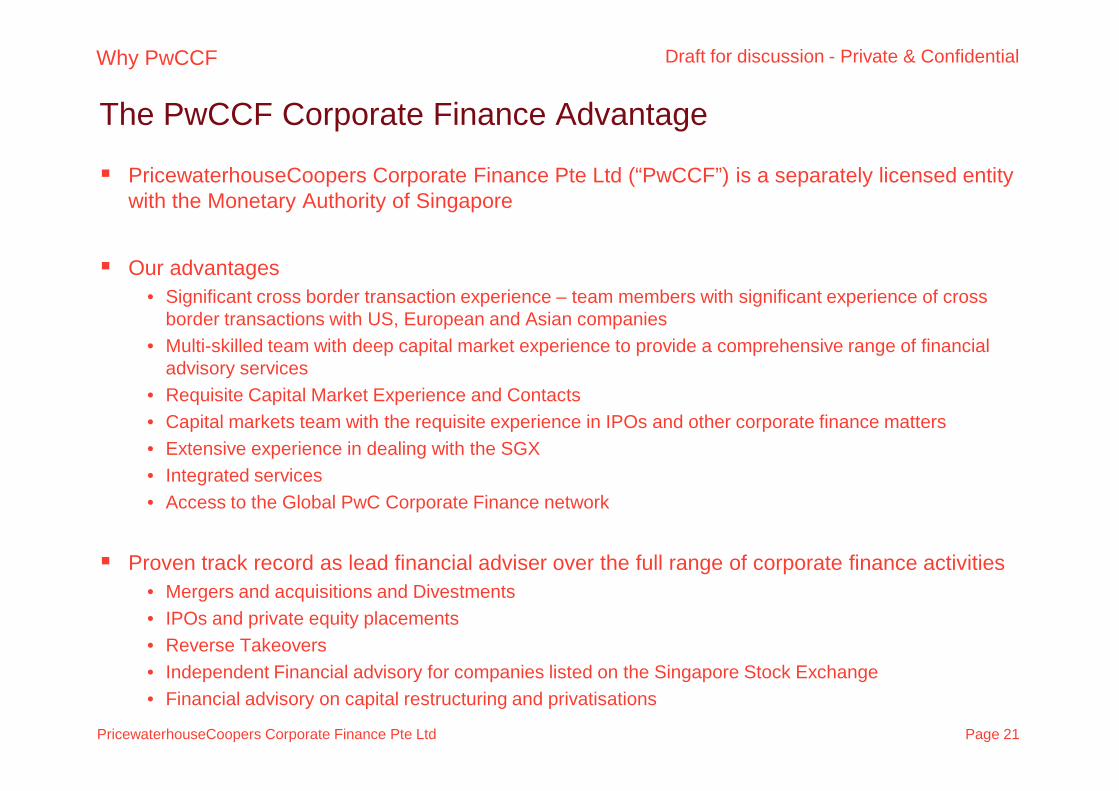

The PwCCF Corporate Finance Advantage

PricewaterhouseCoopers Corporate Finance Pte Ltd (“PwCCF”) is a separately licensed entitywith the Monetary Authority of Singapore

Our advantages

• Significant cross border transaction experience – team members with significant experience of crossborder transactions with US, European and Asian companies

• Multi-skilled team with deep capital market experience to provide a comprehensive range of financialadvisory services

• Requisite Capital Market Experience and Contacts

• Capital markets team with the requisite experience in IPOs and other corporate finance matters

• Extensive experience in dealing with the SGX

• Integrated services

• Access to the Global PwC Corporate Finance network

Proven track record as lead financial adviser over the full range of corporate finance activities

• Mergers and acquisitions and Divestments

• IPOs and private equity placements

• Reverse Takeovers

• Independent Financial advisory for companies listed on the Singapore Stock Exchange

• Financial advisory on capital restructuring and privatisations

Why PwCCF

January 2009

Strictly Private & Confidential – Not for circulation

Page 22

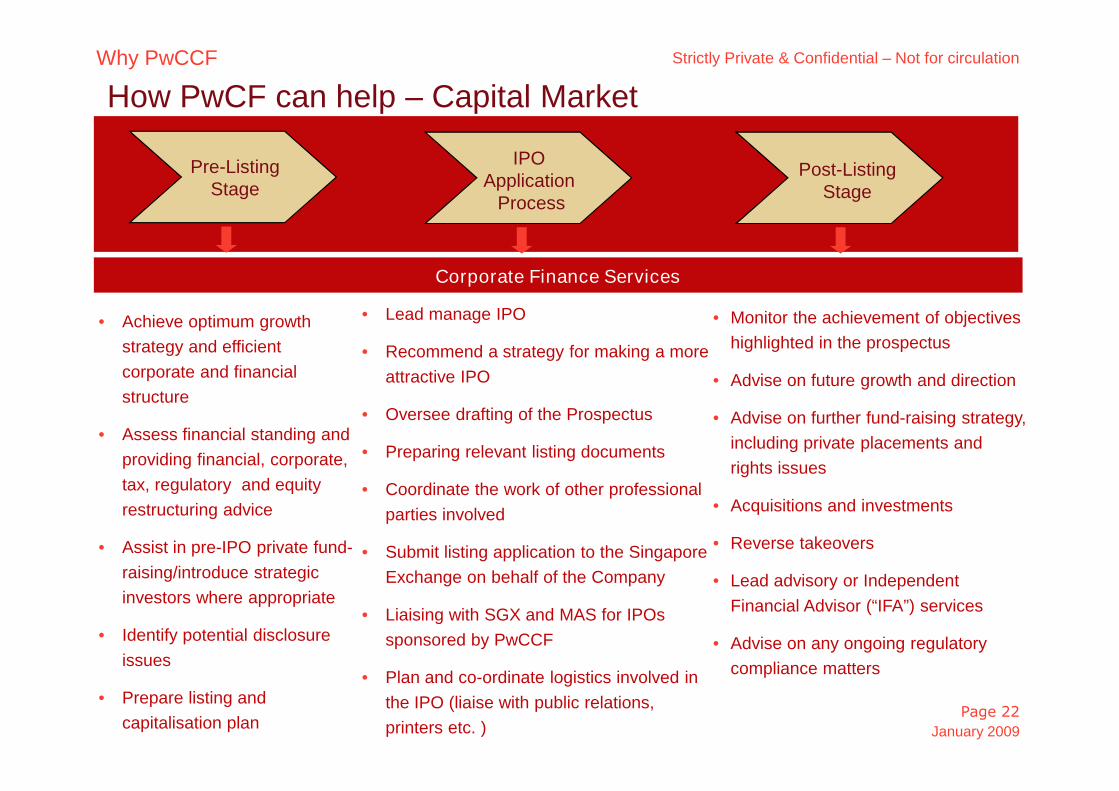

How PwCF can help – Capital Market

IPOApplication

Process

Corporate Finance Services

• Monitor the achievement of objectives

highlighted in the prospectus

• Advise on future growth and direction

• Advise on further fund-raising strategy,

including private placements and

rights issues

• Acquisitions and investments

• Reverse takeovers

• Lead advisory or Independent

Financial Advisor (“IFA”) services

• Advise on any ongoing regulatory

compliance matters

• Achieve optimum growth

strategy and efficient

corporate and financial

structure

• Assess financial standing and

providing financial, corporate,

tax, regulatory and equity

restructuring advice

• Assist in pre-IPO private fund-

raising/introduce strategic

investors where appropriate

• Identify potential disclosure

issues

• Prepare listing and

capitalisation plan

• Lead manage IPO

• Recommend a strategy for making a more

attractive IPO

• Oversee drafting of the Prospectus

• Preparing relevant listing documents

• Coordinate the work of other professional

parties involved

• Submit listing application to the Singapore

Exchange on behalf of the Company

• Liaising with SGX and MAS for IPOs

sponsored by PwCCF

• Plan and co-ordinate logistics involved in

the IPO (liaise with public relations,

printers etc. )

Post-ListingStage

Pre-ListingStage

Why PwCCF

January 2009

Strictly Private & Confidential – Not for circulation

Page 23

PricewaterhouseCoopers Corporate Finance Pte Ltd

IPO News

Why PwCCF

January 2009

Strictly Private & Confidential – Not for circulation

Page 24

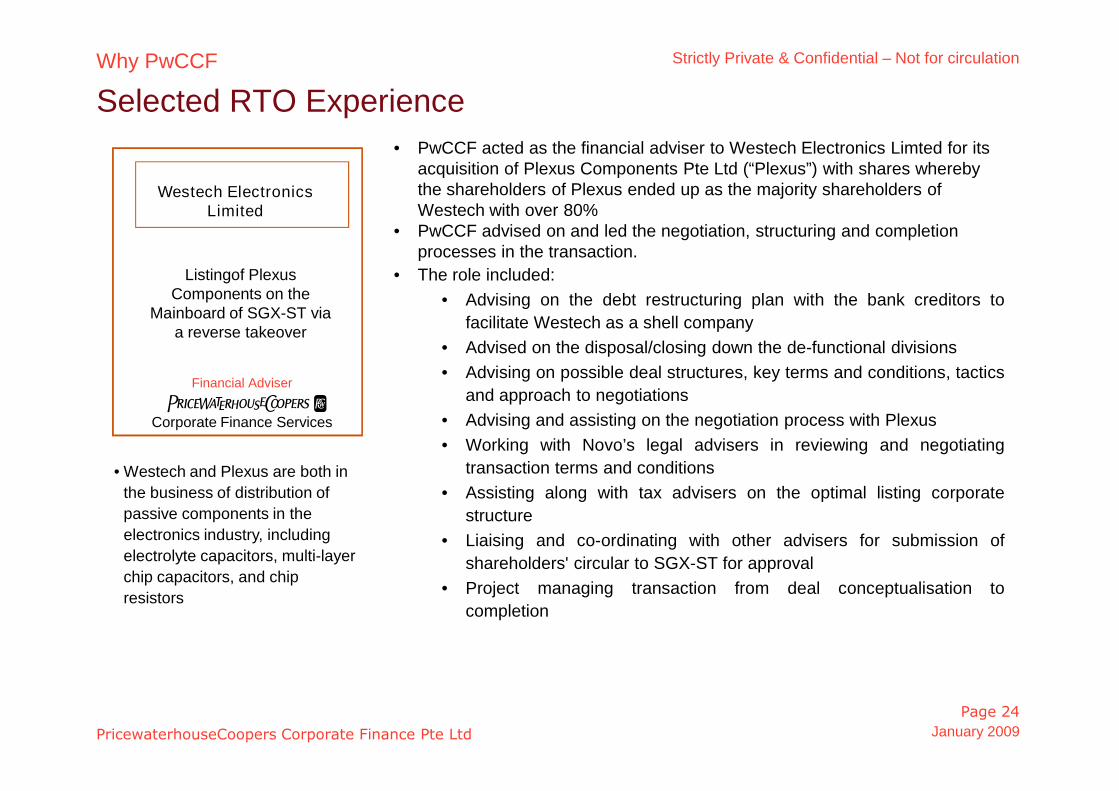

• PwCCF acted as the financial adviser to Westech Electronics Limted for itsacquisition of Plexus Components Pte Ltd (“Plexus”) with shares wherebythe shareholders of Plexus ended up as the majority shareholders ofWestech with over 80%

• PwCCF advised on and led the negotiation, structuring and completionprocesses in the transaction.

• The role included:

• Advising on the debt restructuring plan with the bank creditors to

facilitate Westech as a shell company

• Advised on the disposal/closing down the de-functional divisions

• Advising on possible deal structures, key terms and conditions, tactics

and approach to negotiations

• Advising and assisting on the negotiation process with Plexus

• Working with Novo’s legal advisers in reviewing and negotiating

transaction terms and conditions

• Assisting along with tax advisers on the optimal listing corporate

structure

• Liaising and co-ordinating with other advisers for submission of

shareholders' circular to SGX-ST for approval

• Project managing transaction from deal conceptualisation to

completion

Selected RTO Experience

Financial Adviser

Listingof PlexusComponents on the

Mainboard of SGX-ST viaa reverse takeover

Corporate Finance Services

PwC

• Westech and Plexus are both in

the business of distribution of

passive components in the

electronics industry, including

electrolyte capacitors, multi-layer

chip capacitors, and chip

resistors

Why PwCCF

Westech ElectronicsLimited

PricewaterhouseCoopers Corporate Finance Pte Ltd

Draft for discussion - Private & Confidential

Page 25PricewaterhouseCoopers Corporate Finance Pte Ltd

• PwCCF acted as the financial adviser to Novo Group Ltd. (“Novo”) in itsacquisition of NeoCorp International Ltd (“NeoCorp”) and its subsequentlisting on the Mainboard of SGX-ST on 28 April 2008 on completion of thecompliance share placement.

• PwCCF originated the transaction on a proprietary basis and advised on and

led the negotiation, structuring and completion processes in the transaction.

• The role included:

• Advising on the options available to seeking a listing on SGX-ST

• Identifying and evaluating potential Reverse Take Over (RTO) targets

for Novo

• Shortlisting RTO targets and presenting their merits and demerits to

the Board

• Advising on possible deal structures, key terms and conditions, tactics

and approach to negotiations

• Advising and assisting on the negotiation process with the selected

RTO target

• Working with Novo’s legal advisers in reviewing and negotiating

transaction terms and conditions

• Assisting along with tax advisers on the optimal listing corporate

structure

• Liaising and co-ordinating with other advisers for submission of

shareholders' circular to SGX-ST for approval

• Working with placement agent on the compliance placement exercise

• Project managing transaction from deal conceptualisation to

completion

Selected RTO Experience

Financial Adviser

Listing of Novo GroupLtd. on the Mainboard of

SGX-ST via a reversetakeover

Corporate Finance Services

PwC

• Novo Group Ltd is a global steel

supply chain management

company that provides support

services throughout the value-

chain – from demand aggregation

and disaggregation to logistics

and trade financing (both for

suppliers and customers).

• Transaction value S$140 million

Why PwCCF

Draft for discussion - Private & Confidential

Page 26PricewaterhouseCoopers Corporate Finance Pte Ltd

• Tektronix’s takeover of Poh Lian was a unique transaction in Singapore

• PwCCF acted as financial adviser to Tektronix and project managed thetransaction through the various stages. Our services included

• Value assessment of the companies to be injected into Poh Lian

• Negotiations with Poh Lian and their advisers

• Advise on restructuring to optimise taxation by the use of offshoreentities

• Co-ordinating financial and tax due diligence on the target

• PwCCF was able to provide valuable assistance in interaction with the SICand SGX , including obtaining various approvals and waivers

• PwC was able to convince the SIC to provide a “whitewash” waiver inthis transaction to help Tektronix avoid making a general offer to theshareholders of Poh Lian (triggered by the Singapore Takeover Code),subject to the fulfilment of certain conditions and approval byshareholders

• PwC also obtained SGX approval to avoid onerous guidelines thatrequired a large percentage of shares to be held by non-substantialshareholders

• Tektronix was thus able to retain a large post-dilution stake in the entityand avoid the additional outlay that would have been required inmaking a general offer for the balance shareholding of Poh Lian

Tektronix IndustriesLimited

Takeover of Poh Lian HoldingsLimited via an injection of two

Indonesian forestry companies, PTMenara Hutan Buana and PT

Marga Buana Bumi Mulia

• Tektronix is controlled by amajority of shareholders inSweden's unlisted CellMarkHolding AB, one of the world'slargest marketers of forestproducts.

• The company completed areverse takeover of SGX-listedPoh Lian Holdings by injection ofIndonesian forest assets

• The transaction value wasestimated at S$272 million

Selected RTO Experience

Financial Adviser

Corporate Finance Services

PwC

Why PwCCF

Draft for discussion - Private & Confidential

Page 27PricewaterhouseCoopers Corporate Finance Pte Ltd

PwCCF is the only accounting firm that has acted in the capacityof an issue manager and has previously advised 4 IPOs…

Why PwCCF

Thank you

© 2009 PricewaterhouseCoopers Corporate Finance Pte Ltd. All rights reserved."PricewaterhouseCoopers" refers to PricewaterhouseCoopers Corporate Finance Pte Ltd or, as thecontext requires, the PricewaterhouseCoopers global network or other member firms of the network,each of which is a separate and independent legal entity.

PwC