linz – kickoff workshop september 8-12, 2008. 1 · linz – kickoff workshop september 8-12,...

TRANSCRIPT

September 8-12, 2008. 1Linz – Kickoff workshop

Linz – Kickoff workshop September 8-12, 2008. 2

Power and Gas Markets

Challenges for Pricing and Managing Derivatives

Peter Leoni, Electrabel

Linz – Kickoff workshop September 8-12, 2008. 3

OutlinePower Markets:

•Spot Market

•Forward Market

Gas Markets

Derivatives

•Plain Vanilla Products

•Exotic Products

Conclusions

POWER MARKETS

Linz – Kickoff workshop September 8-12, 2008. 4

Linz – Kickoff workshop September 8-12, 2008. 5

Power MarketElectricity is unique:

• cannot be stored (flow commodity)

•No flavours

•Transport is limited

•Production = Consumption (auction)

Trading Power is relatively new

2 Different Markets

•Spot Market

•Forward Market

Power Markets – Spot Market

Day-ahead auction per market (~country)

•Power supply:– Nuclear Power plants

– Gas-fired power plants

– Coal-fired power plants

– Hydro-power plants

– Transport Capacity (import)

– …

Linz – Kickoff workshop September 8-12, 2008. 6

Power Markets – Spot Market

Day-ahead auction per market (~country)

•Power demand:– Transport Capacity (export)

– Industrials

– Home users

– …

Linz – Kickoff workshop September 8-12, 2008. 7

Power Markets – Spot Market

Day-ahead auction per market (~country)

•Auction for each hour of the next day

•Price = (Supply meets demand)

•Price is set by marginal cost

•Price reflects the consumption pattern

Linz – Kickoff workshop September 8-12, 2008. 8

Power Markets – Spot Market

CASE STUDY: NORDIC MARKET

•Considered as Very liquid

•Hydro-driven (closest to storability)

Linz – Kickoff workshop September 8-12, 2008. 9

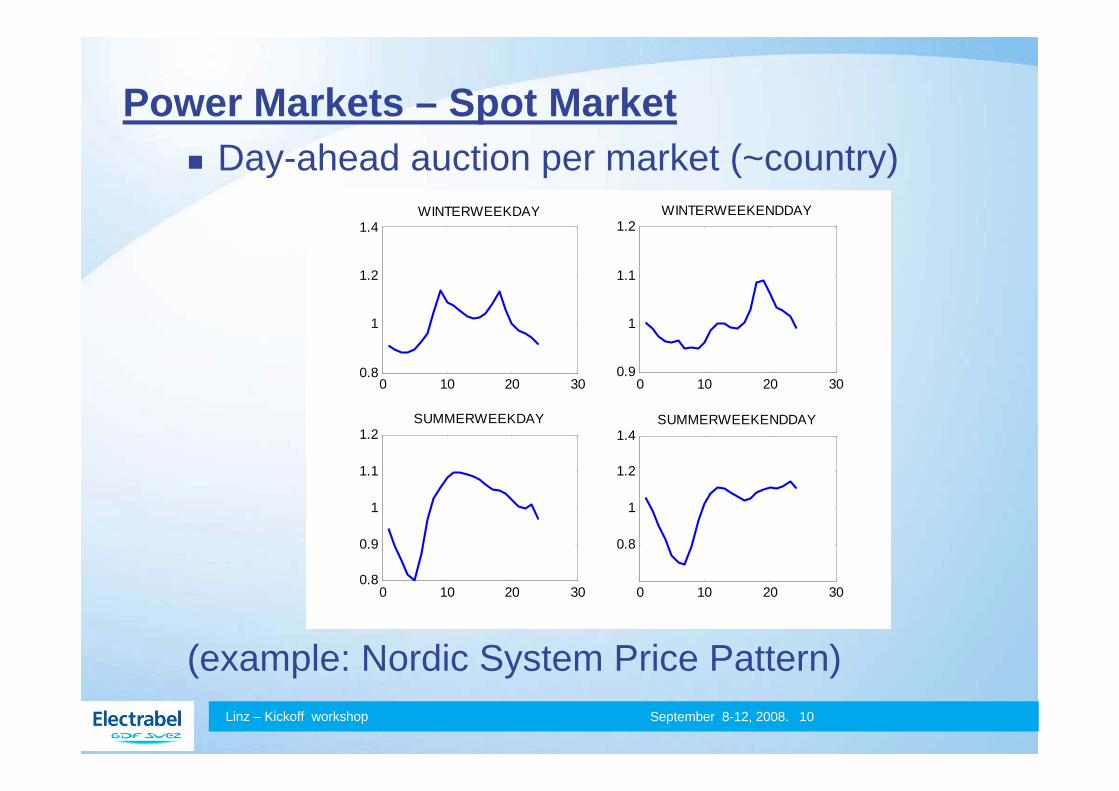

Power Markets – Spot MarketDay-ahead auction per market (~country)

(example: Nordic System Price Pattern)Linz – Kickoff workshop September 8-12, 2008. 10

0 10 20 300.8

1

1.2

1.4WINTERWEEKDAY

0 10 20 300.9

1

1.1

1.2WINTERWEEKENDDAY

0 10 20 300.8

0.9

1

1.1

1.2SUMMERWEEKDAY

0 10 20 30

0.8

1

1.2

1.4SUMMERWEEKENDDAY

Power Markets – Spot MarketIntraday Price Pattern

•Very weather-dependent

•Depends on type of day (weekday/Saturday/Sunday/Holiday)

•Depends on Month

•Very volatile with respect to the ‘average’ profile

•Unpredictable

Linz – Kickoff workshop September 8-12, 2008. 11

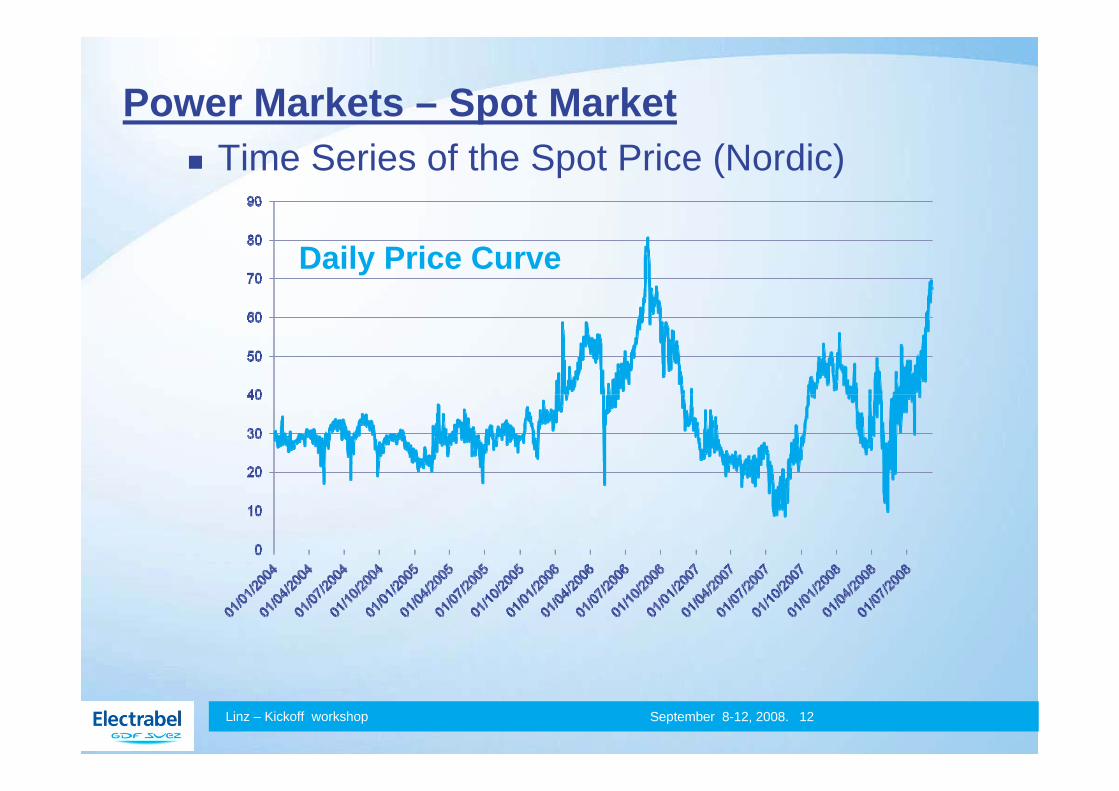

Power Markets – Spot MarketTime Series of the Spot Price (Nordic)

Linz – Kickoff workshop September 8-12, 2008. 12

Daily Price Curve

Power Markets – Spot Market

Features:

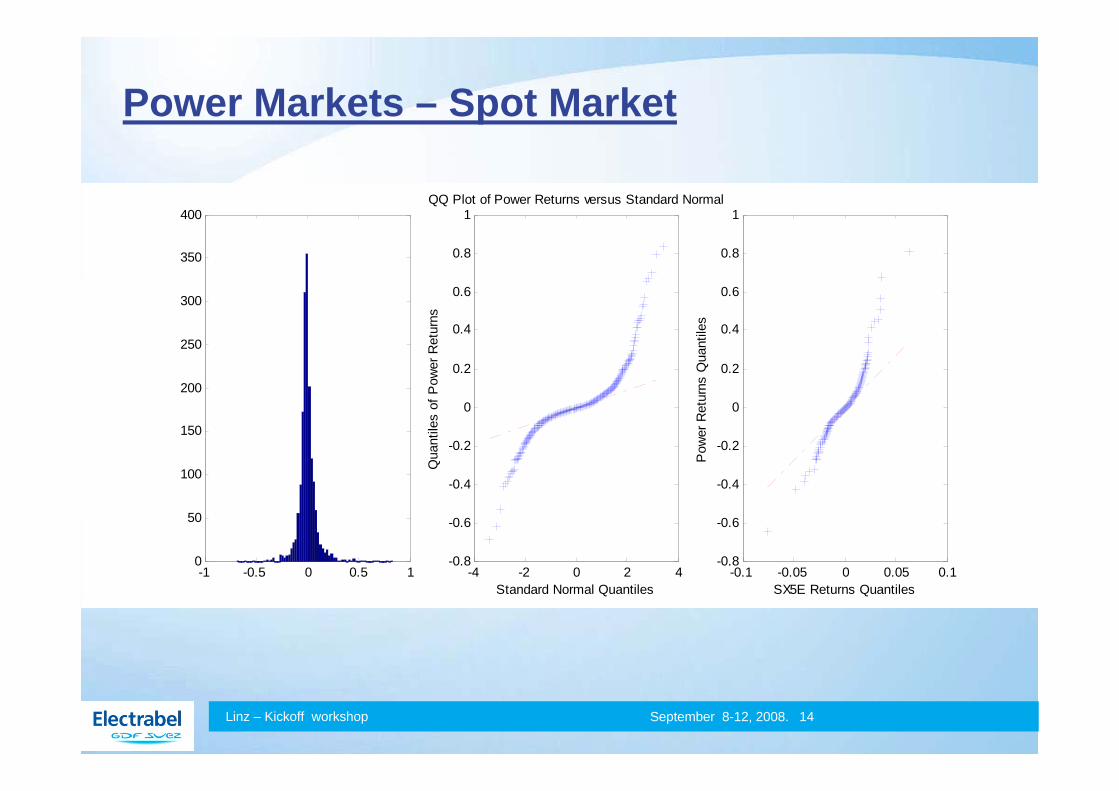

•Very FAT tails

•Prices expected to be – Higher in the winter / Lower in the summer

– Higher during the Week / Lower during the weekend

– Higher During PeakHours / Lower during offpeak (night)

•Mean-reversion(?)

Linz – Kickoff workshop September 8-12, 2008. 13

Power Markets – Spot Market

Linz – Kickoff workshop September 8-12, 2008. 14

-1 -0.5 0 0.5 10

50

100

150

200

250

300

350

400

-4 -2 0 2 4-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Standard Normal Quantiles

Qua

ntile

s of

Pow

er R

etur

ns

QQ Plot of Power Returns versus Standard Normal

-0.1 -0.05 0 0.05 0.1-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

SX5E Returns Quantiles

Pow

er R

etur

ns Q

uant

iles

Power Markets – Spot Market

0 1 2 3 4

x 104

0

20

40

60

80

100

120HYDRO SYSTEM

0 1 2 3 4 5 6 7

x 104

0

500

1000

1500

2000

2500NO HYDRO SYSTEM

Linz – Kickoff workshop September 8-12, 2008. 15

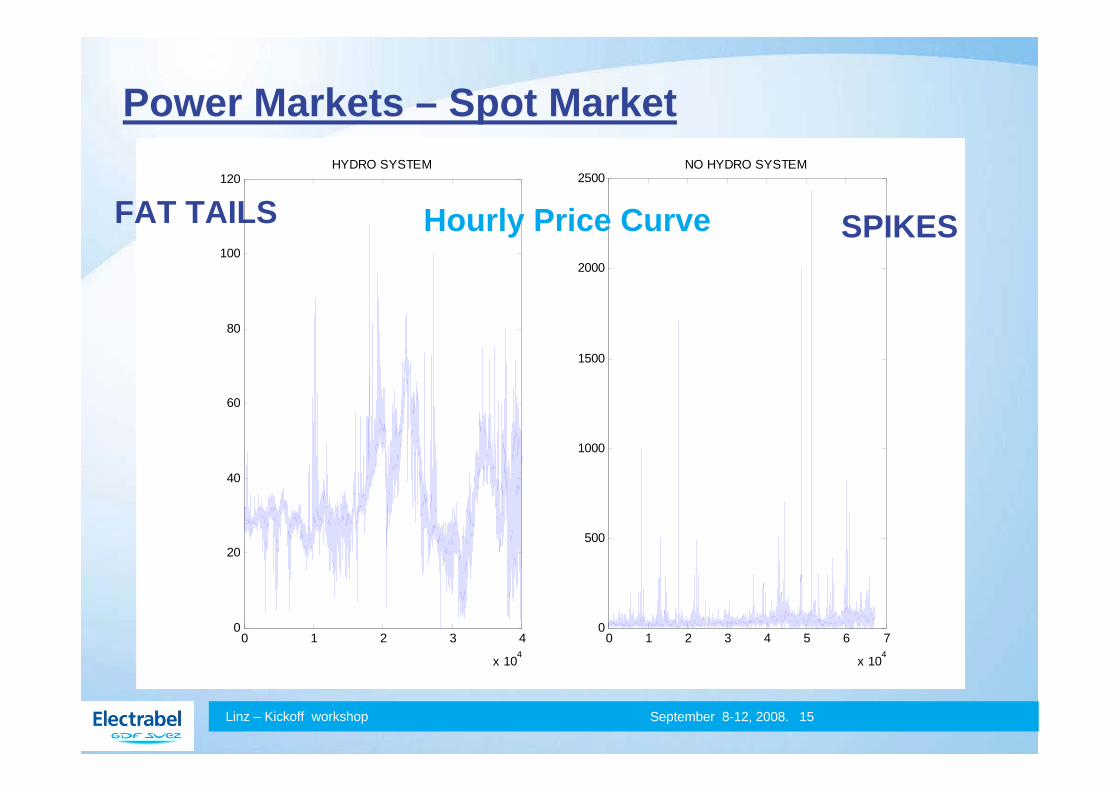

SPIKESFAT TAILS Hourly Price Curve

The need to manage Risk on the Spot Market

led to

the development of the Forward Market

Power Markets

Linz – Kickoff workshop September 8-12, 2008. 16

Power Markets – Forward Market

Forward Contracts F(t, T1, T2):

•Price at time t for the commodity to be delivered (in a constant ‘volume’ during the entire period [T1;T2]

• [T1;T2] = delivery period

•Payment done during the delivery period, usually settled on a monthly basis (swap)

•Price is fixed and constant during delivery

•Forward price is an estimate of the AVERAGE realised Spot price during delivery period.

Linz – Kickoff workshop September 8-12, 2008. 17

Power Markets – Forward MarketDelivery period is bucketed into

•Days – Weeks on the short-end of the curve

•Months / Quarters

•Years

Cascading Mechanism:

•1 Year 4 Quarters

•1 Q 3 Months

•1M 4 Weeks

•1W WEEKEND + DAYS

Linz – Kickoff workshop September 8-12, 2008. 18

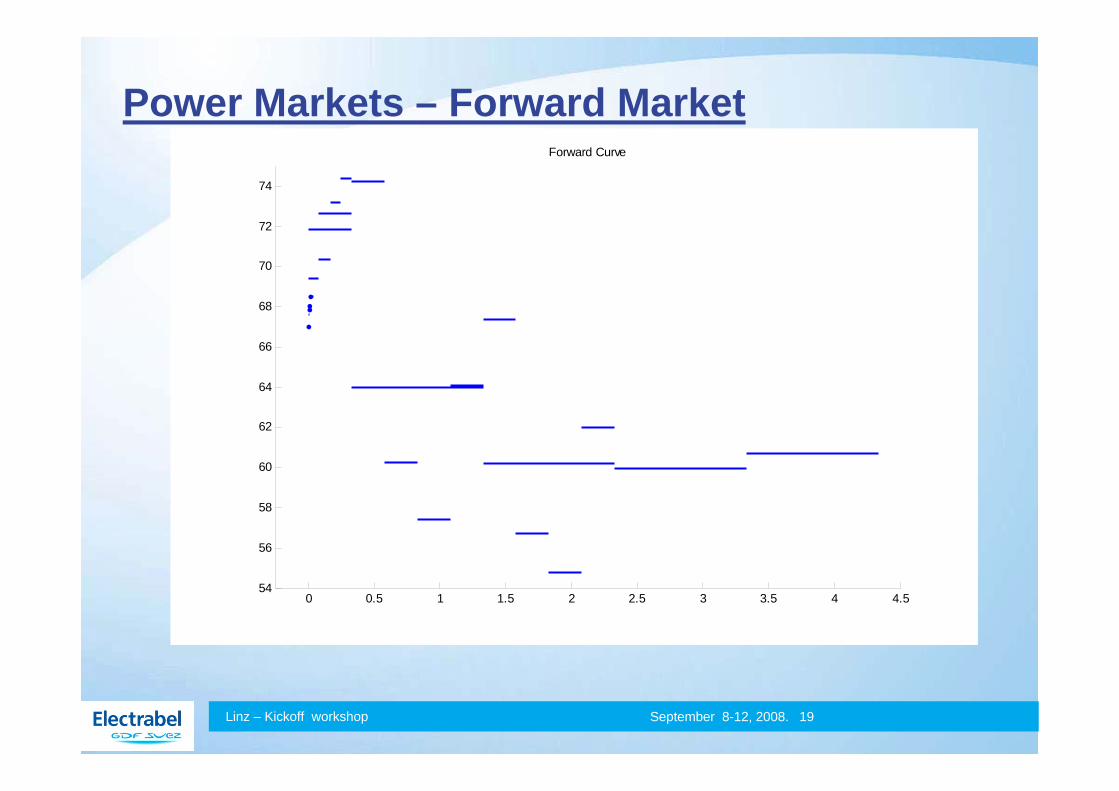

Power Markets – Forward Market

Linz – Kickoff workshop September 8-12, 2008. 19

0 0.5 1 1.5 2 2.5 3 3.5 4 4.554

56

58

60

62

64

66

68

70

72

74

Forward Curve

Power Markets – Forward MarketSeasonality is very obvious in the Forwards

Forward Market Organised in

•Exchange (Futures)

•Brokered OTC Market (very liquid and transparant)

Linz – Kickoff workshop September 8-12, 2008. 20

Power Markets – Forward MarketSome numbers on the Nordic Market:

•First liberalised Market in Europe

•About 150 players in the Forward Market

•About 15 (active) players in the Vol market

•About 3-5 option trades per day

Linz – Kickoff workshop September 8-12, 2008. 21

GAS MARKETS

Linz – Kickoff workshop September 8-12, 2008. 22

Gas Markets

Gas is storable to some extent

•Pipelines

•Day-storages

No Hourly market

No spike-behaviour

Still seasonal, still very fat tails, very physical as wellLinz – Kickoff workshop September 8-12, 2008. 23

PLAIN VANILLA DERIVATIVES

Linz – Kickoff workshop September 8-12, 2008. 24

Derivatives: Plain Vanilla Products

Option Expires before delivery period starts

Power:

•Options on Futures (Exchange)

•Swaptions: Options on the ‘Forward’ (OTC)

• ‘Liquid’ Markets: Nordpool, Germany

Gas:

•Options on Summer/Winter Forwards

•Strip of Options on Summer/Winter (most liquid)

Linz – Kickoff workshop September 8-12, 2008. 25

Derivatives: Plain Vanilla Products

Study (Koekebakker and Ollmar, 2005):

•Multifactor (geometric Brownian) forward dynamics

•2 factors explain 75% of volatility of the forward curve

•10 factors capture 95%

•Low correlation between short-end and long-end

Linz – Kickoff workshop September 8-12, 2008. 26

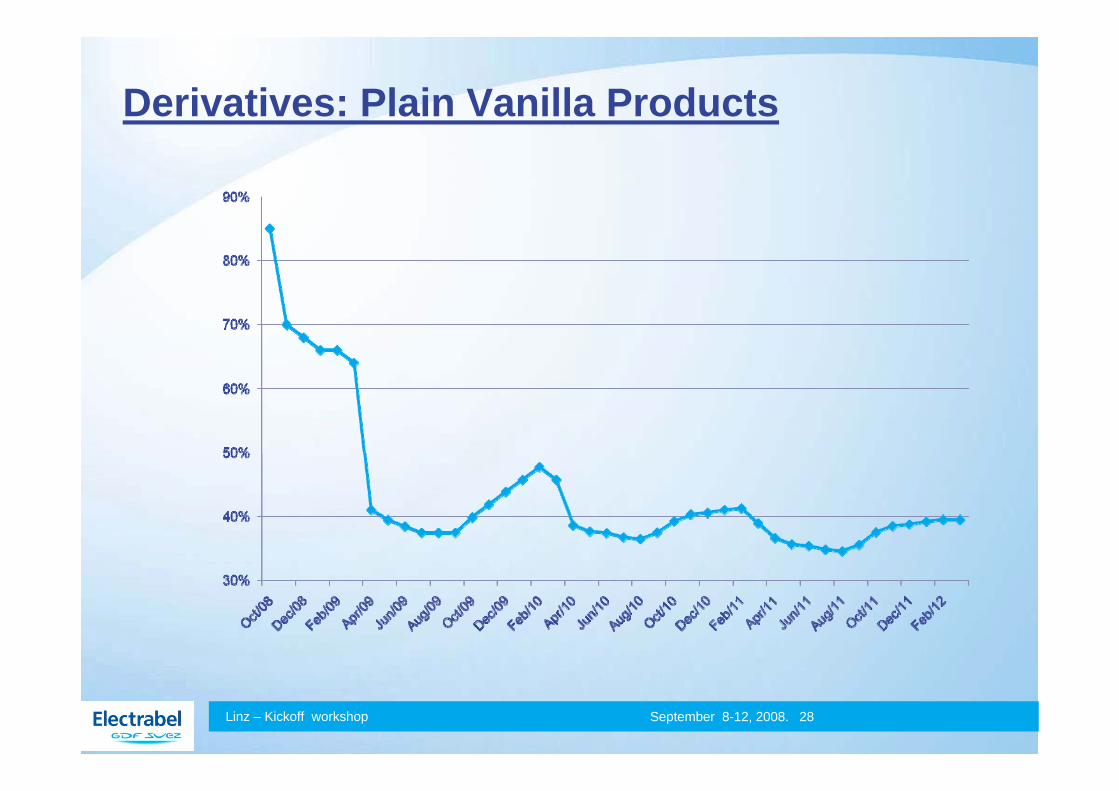

Derivatives: Plain Vanilla Products

Typically only a few expiries per product

Volatility ‘Term Structure’ refers to underlying forward curve

•Short-end of the forward curve: HIGH VOL

•Long-end of the forward curve: LOW VOL

Seasonality in Volatility

•Winter Vol (relative) high

•Summer Vol (relative) lowLinz – Kickoff workshop September 8-12, 2008. 27

Derivatives: Plain Vanilla Products

Linz – Kickoff workshop September 8-12, 2008. 28

Derivatives: Plain Vanilla Products

Challenges for the ‘Plain Vanilla Options’

•Option market is thin (implied vol quotes not always reliable)

• Implied Vol quoted according to bad model (model for forwards rather than swaptions)

•Bid/Offer spreads in the underlying (hedging cost)

•Fat tails (as any market)

•Liquidity

Linz – Kickoff workshop September 8-12, 2008. 29

Derivatives: Plain Vanilla Products

Bid/Offer spreads for Forwards:

•Days: 0.75% - 5% (sometimes even 15%, for SUN)

•Weeks: 1.25% - 6%

•Months: 0.5% - 2% - 5%

•Quarters: 0.10% - 3%

•Cals: 0.25% - 2%

Linz – Kickoff workshop September 8-12, 2008. 30

Derivatives: Plain Vanilla Products

Liquidity in Forwards:

•Can dry up easily and fast

•Risk premium: implied vol is much higher than realised vol (difference about 10%)

Linz – Kickoff workshop September 8-12, 2008. 31

Derivatives: Plain Vanilla Products

Underlying does not (yet) exist

•Strip of Options on Winter/Summer products

•6 Options each expiring right before Monthly-Forward goes into delivery

•Monthly forwards may not be traded at the time of writing the option

•Basis Risk: “Hedging of Untradable Assets,”N. Vandaele, P. Leoni and M. Vanmaele (in preparation)

Linz – Kickoff workshop September 8-12, 2008. 32

Derivatives: Plain Vanilla Products

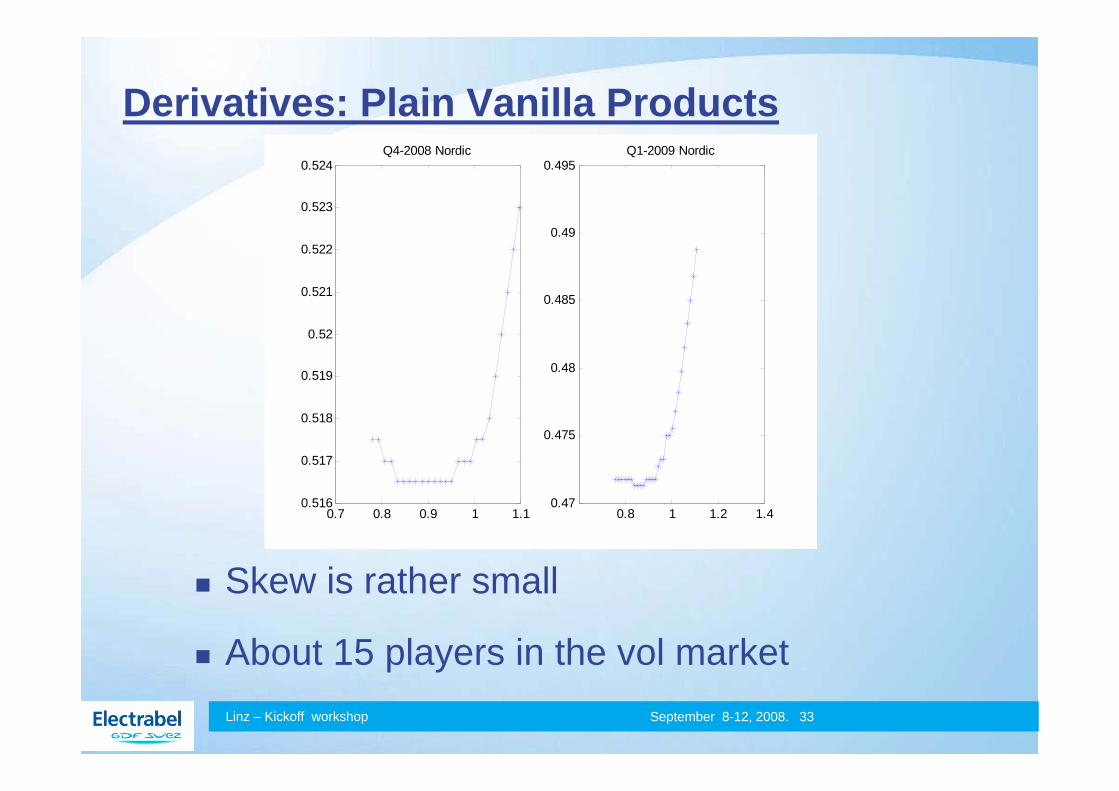

Skew is rather small

About 15 players in the vol marketLinz – Kickoff workshop September 8-12, 2008. 33

0.7 0.8 0.9 1 1.10.516

0.517

0.518

0.519

0.52

0.521

0.522

0.523

0.524Q4-2008 Nordic

0.8 1 1.2 1.40.47

0.475

0.48

0.485

0.49

0.495Q1-2009 Nordic

EXOTIC DERIVATIVES

Linz – Kickoff workshop September 8-12, 2008. 34

Derivatives: Exotic Products

2 Examples and their risks:

•Hourly Option (power)

•Swing Option (gas)

Linz – Kickoff workshop September 8-12, 2008. 35

Derivatives: Exotic Products: Hourly Option

Specifications

•Strip of options expiring on the SPOT market

•For each hour of the day, for each day over the period (typically 3 years), the owner has a right:

•Call/Put

•Fixed strike (can be floating as well)

•For each hour: ‘nomination’ or exercise has to be decided on a day-ahead basis

•Settlement can be financial or physicalLinz – Kickoff workshop September 8-12, 2008. 36

Derivatives: Exotic Products: Hourly Option

Model - Risks:

•Year-to-Quarter-to-Month-to-Week-to-Day profile

• Intraday profile (hourly profile)

•Volatility on each scale

Challenges

•Pricing the product

•Hedging the product (profiles cannot be hedged perfectly)

Linz – Kickoff workshop September 8-12, 2008. 37

Derivatives: Exotic Products: Swing Option

Swing Option:

•Very complex product in an imperfect market

•Traded very often because of physical nature of the (Gas) Market

Linz – Kickoff workshop September 8-12, 2008. 38

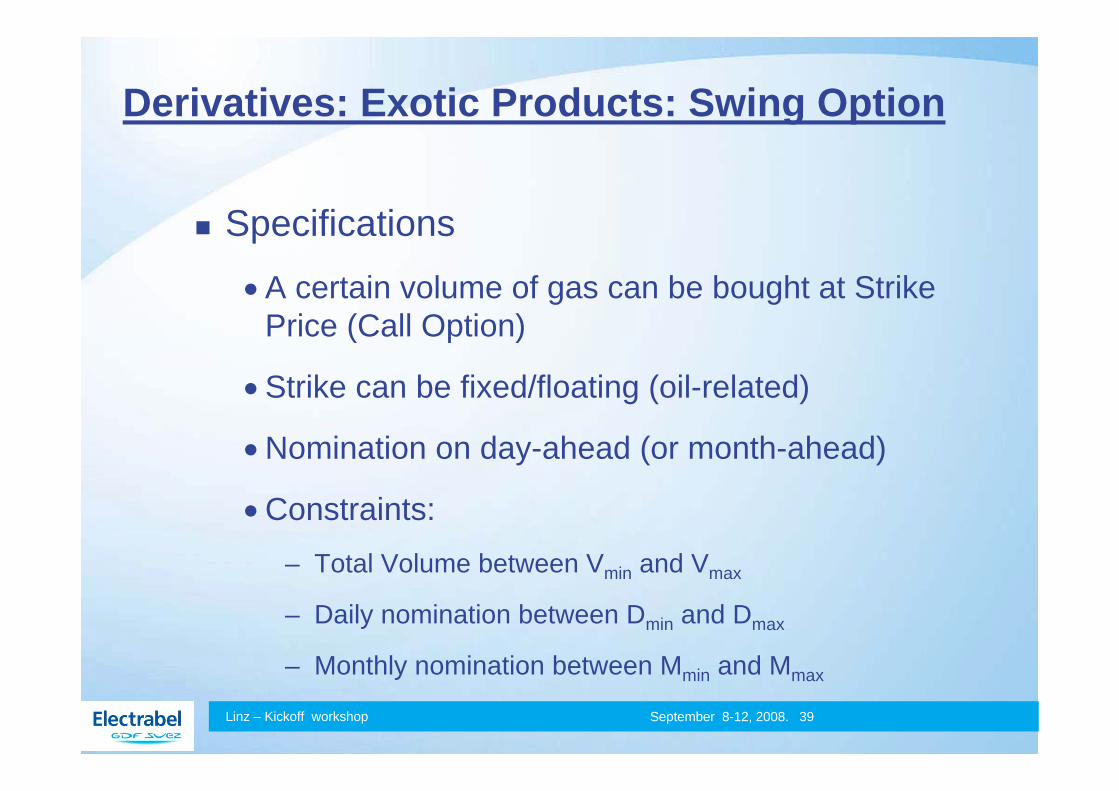

Derivatives: Exotic Products: Swing Option

Specifications

•A certain volume of gas can be bought at Strike Price (Call Option)

•Strike can be fixed/floating (oil-related)

•Nomination on day-ahead (or month-ahead)

•Constraints:– Total Volume between Vmin and Vmax

– Daily nomination between Dmin and Dmax

– Monthly nomination between Mmin and Mmax

Linz – Kickoff workshop September 8-12, 2008. 39

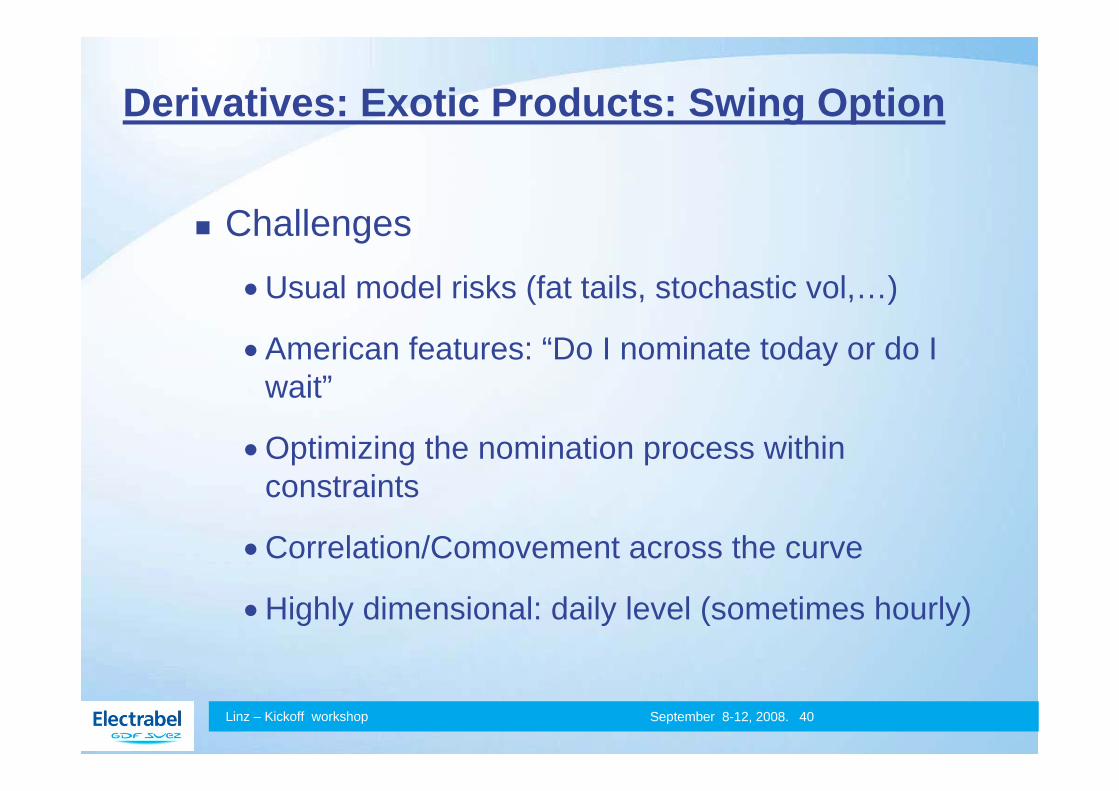

Derivatives: Exotic Products: Swing Option

Challenges

•Usual model risks (fat tails, stochastic vol,…)

•American features: “Do I nominate today or do I wait”

•Optimizing the nomination process within constraints

•Correlation/Comovement across the curve

•Highly dimensional: daily level (sometimes hourly)

Linz – Kickoff workshop September 8-12, 2008. 40

CONCLUSIONS

Linz – Kickoff workshop September 8-12, 2008. 41

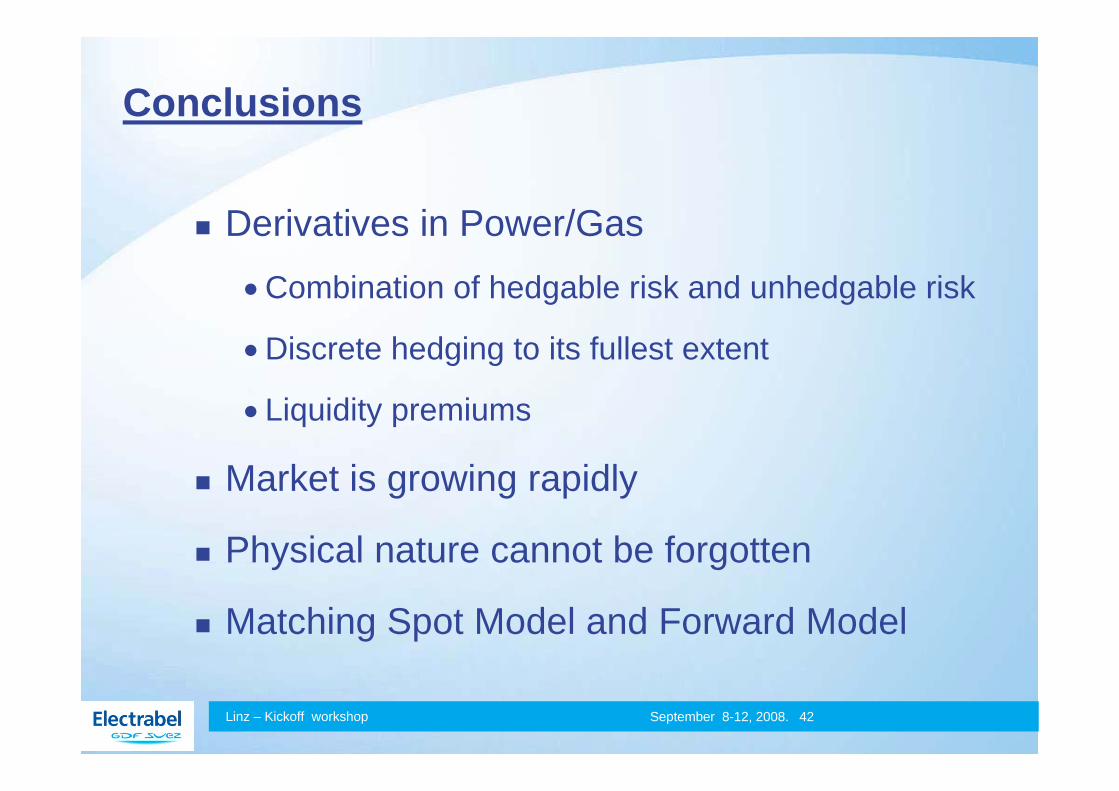

Conclusions

Derivatives in Power/Gas

•Combination of hedgable risk and unhedgable risk

•Discrete hedging to its fullest extent

•Liquidity premiums

Market is growing rapidly

Physical nature cannot be forgotten

Matching Spot Model and Forward Model

Linz – Kickoff workshop September 8-12, 2008. 42

September 8-12, 2008. 43Linz – Kickoff workshop