linking tiam and klem: economic impacts of wb2d mitigation pathways

TRANSCRIPT

Linking TIAM-KLEM: Economic impacts of WB2D mitigation pathways(Work in Progress, please don’t cite)

James Glynn, Frédéric Ghersi, Brian Ó Gallachóir

70th ETSAP Workshop

CIEMAT, MADRID | 17th – 18th November 2016

Outline

• What is the key motivation?• Understand feedbacks, structural changes and welfare effects

due to energy system decarbonisation

• Update on soft-link method between TIAM and KLEM• KLEM Computable General Model

• Harmonising updated World Bank/OECD Driver to TIAM

• Some precursory results, aggregated at world level highlighting the difference between BASE economic outlook and current macroeconomic outlook from SSP/OECD/World Banks

Why Hybrid Linking?

• Update TIAM Macroeconomic outlook(s)

• Harmonisation of energy service demands with changing economic outlook.

• Aim for best of both worlds.• Technological Explicitness• Macroeconomic realism• Sectoral Dynamics (Energy, Non Energy, Households)

• Demand response is considerable in decarbonisation scenarios.

• Moving forward from TIAM-MACRO/MSA• Investigate multi-sector dynamics

• Aim for better representation socio-economic dynamics

Overview of linkage

• TIMES-MACRO (Remme & Blesl, 2006)

• TIAM-KLEM

TIAM

Sectoral

Energy p&qs

KLEM

Labour

ES investment

Households’ consumption

Public consumption

International trade

Investment

Non-E/E Capital

Non-E output

?Non-E prices?

KLEM Prerequisites

• National accounting framework to access• Complete cost structures K, L, E, M(1,…,n)

• Inter-industry flows i.e. structural change, dematerialisation

• Market instruments recycling options

• Distributive issues, at least firms/government/households

• Dual accounting in monetary and physical units• To keep track of energy volumes in stand-alone versions

• To model agent-specific pricing

• Explicit investment profiles• To account for transitional strain on shorter time intervals

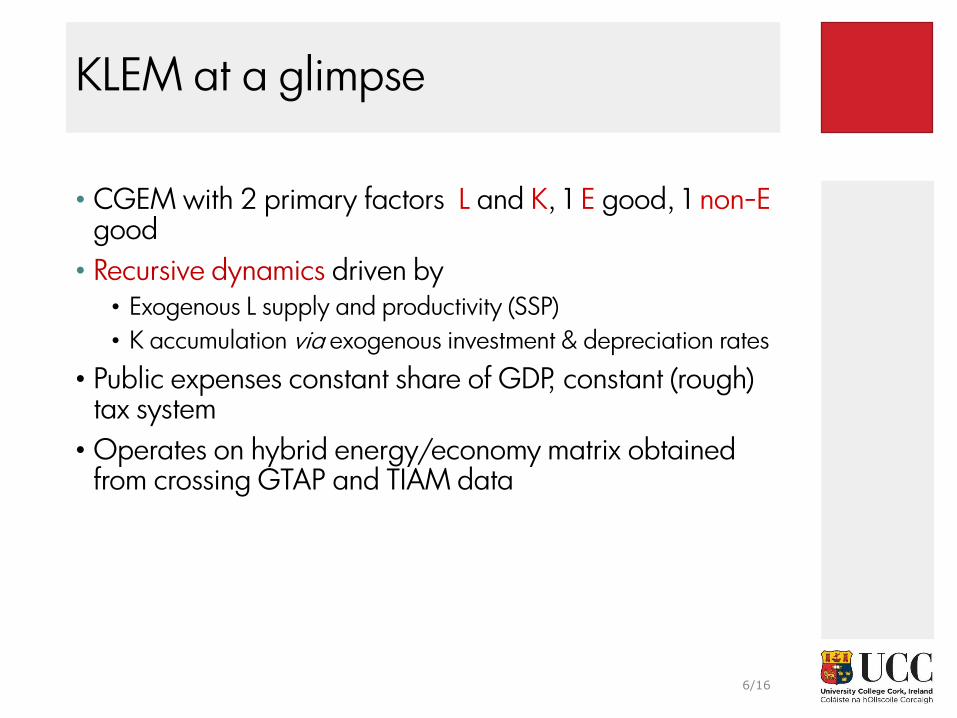

KLEM at a glimpse

• CGEM with 2 primary factors L and K, 1 E good, 1 non-Egood

• Recursive dynamics driven by• Exogenous L supply and productivity (SSP)

• K accumulation via exogenous investment & depreciation rates

• Public expenses constant share of GDP, constant (rough) tax system

• Operates on hybrid energy/economy matrix obtained from crossing GTAP and TIAM data

6/16

B$ Non-E E C G I X Uses

Non-E 14 085 90 9 022 3 235 3 410 2 158 32 000

E 430 627 249 - - 269 1 574

L net 5 859 41

L taxes 2 060 15

Y taxes 649 87

K 5 681 137

M 1 980 461

SM non-E - 103

SM E - -14

SM C - -58

SM X - -30

Sales taxes 1 257 116

Resources 32 000 1 574

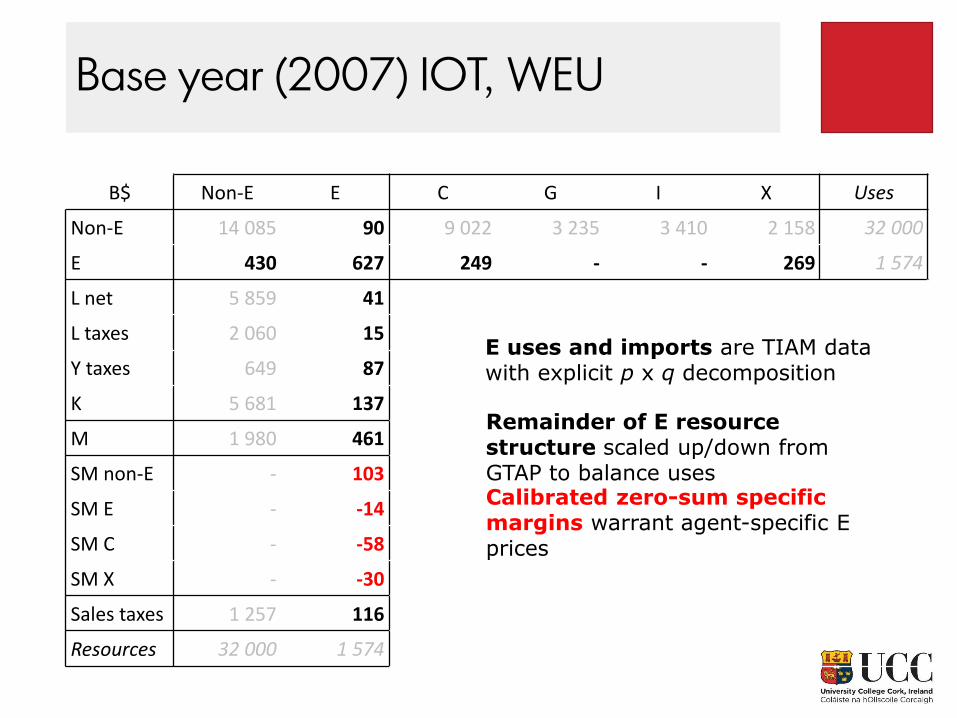

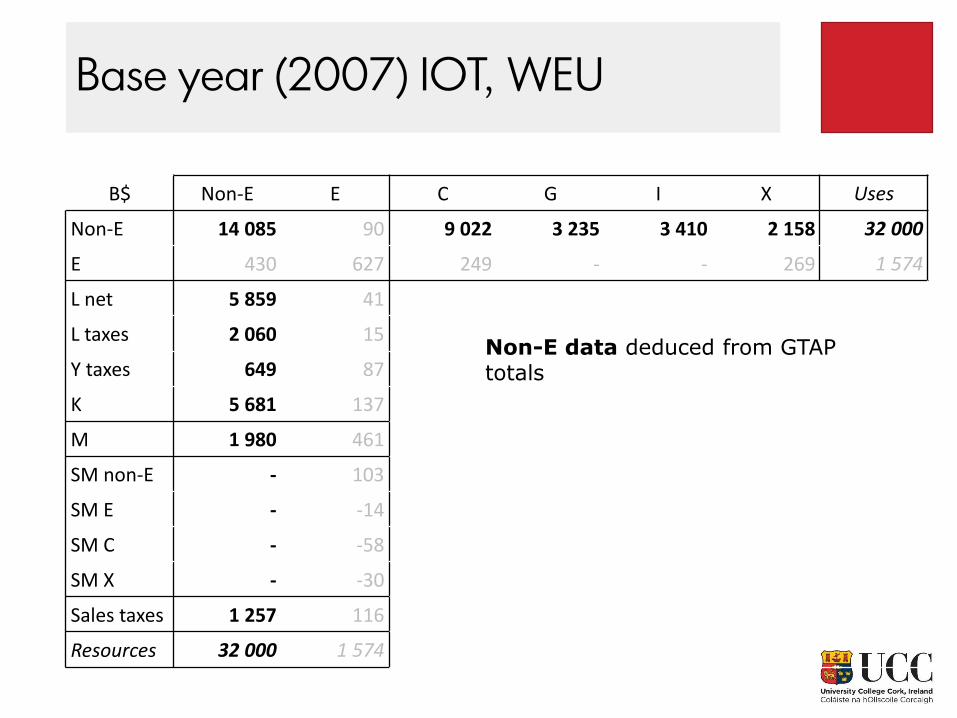

Base year (2007) IOT, WEU

Base year (2007) IOT, WEU

B$ Non-E E C G I X Uses

Non-E 14 085 90 9 022 3 235 3 410 2 158 32 000

E 430 627 249 - - 269 1 574

L net 5 859 41

L taxes 2 060 15

Y taxes 649 87

K 5 681 137

M 1 980 461

SM non-E - 103

SM E - -14

SM C - -58

SM X - -30

Sales taxes 1 257 116

Resources 32 000 1 574

E uses and imports are TIAM data with explicit p x q decomposition

Base year (2007) IOT, WEU

B$ Non-E E C G I X Uses

Non-E 14 085 90 9 022 3 235 3 410 2 158 32 000

E 430 627 249 - - 269 1 574

L net 5 859 41

L taxes 2 060 15

Y taxes 649 87

K 5 681 137

M 1 980 461

SM non-E - 103

SM E - -14

SM C - -58

SM X - -30

Sales taxes 1 257 116

Resources 32 000 1 574

Remainder of E resource structure scaled up/down from GTAP to balance uses

E uses and imports are TIAM data with explicit p x q decomposition

Base year (2007) IOT, WEU

B$ Non-E E C G I X Uses

Non-E 14 085 90 9 022 3 235 3 410 2 158 32 000

E 430 627 249 - - 269 1 574

L net 5 859 41

L taxes 2 060 15

Y taxes 649 87

K 5 681 137

M 1 980 461

SM non-E - 103

SM E - -14

SM C - -58

SM X - -30

Sales taxes 1 257 116

Resources 32 000 1 574

Calibrated zero-sum specific margins warrant agent-specific E prices

E uses and imports are TIAM data with explicit p x q decomposition

Remainder of E resource structure scaled up/down from GTAP to balance uses

Base year (2007) IOT, WEU

B$ Non-E E C G I X Uses

Non-E 14 085 90 9 022 3 235 3 410 2 158 32 000

E 430 627 249 - - 269 1 574

L net 5 859 41

L taxes 2 060 15

Y taxes 649 87

K 5 681 137

M 1 980 461

SM non-E - 103

SM E - -14

SM C - -58

SM X - -30

Sales taxes 1 257 116

Resources 32 000 1 574

Non-E data deduced from GTAP totals

KLEM behavioural assumptions

• Output sequential trade-off of K vs. L then KL vs. E then KLE vs. ‘M’ (aggregate of non-E goods)• K vs. L, KLE vs. M settled by CES functions

• KL (VA) vs. E from TIAMunder a maintained CES assumption for KLE

• Aggregate savings rate exogenous (recursive dynamics)

• Households’ E consumption from TIAM

• International trade• E trade from TIAM

• Non-E trade: ratio of M to Y isoelastic to terms of trade; X settled by international good CES of exported goods (Armington)

12/16

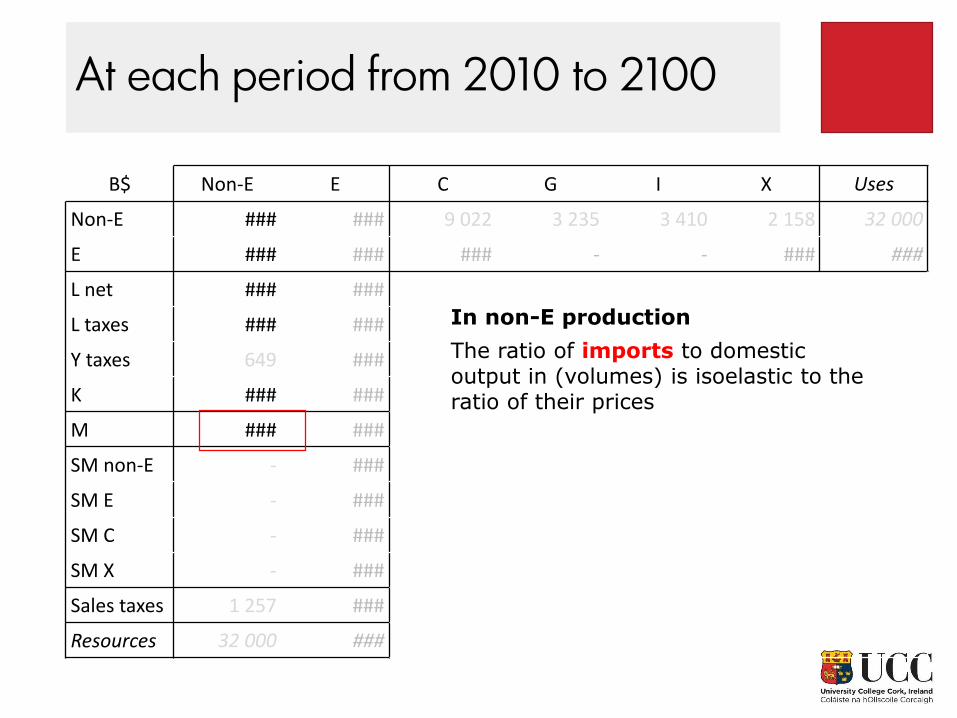

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E 14 085 90 9 022 3 235 3 410 2 158 32 000

E ### ### ### - - ### ###

L net 5 859 41

L taxes 2 060 15

Y taxes 649 87

K 5 681 ###

M 1 980 ###

SM non-E - 103

SM E - -14

SM C - -58

SM X - -30

Sales taxes 1 257 116

Resources 32 000 1 574

TIAM trajectory prescribes E uses and imports as well as E investment requirements, which drive KEaccumulation

K rental price adjusts to balance remainder of K supply and K demand by non-E production

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E 14 085 90 9 022 3 235 3 410 2 158 32 000

E ### ### ### - - ### ###

L net 5 859 ###

L taxes 2 060 ###

Y taxes 649 87

K 5 681 ###

M 1 980 ###

SM non-E - 103

SM E - -14

SM C - -58

SM X - -30

Sales taxes 1 257 116

Resources 32 000 1 574

Labour intensity of E production assumed constant, wage adjusts to balance remainder of L supply and Ldemand by non-E production

Optional imperfect L market magnifies cost of E investment crowding out non-E investment

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E 14 085 ### 9 022 3 235 3 410 2 158 32 000

E ### ### ### - - ### ###

L net 5 859 ###

L taxes 2 060 ###

Y taxes 649 ###

K 5 681 ###

M 1 980 ###

SM non-E - 103

SM E - -14

SM C - -58

SM X - -30

Sales taxes 1 257 ###

Resources 32 000 1 574

‘M’ (non-E) intensity of E production trades off with KLE aggregate under a constant elasticity of substitution assumption

Output and sales taxes constant ad valorem rates

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E 14 085 ### 9 022 3 235 3 410 2 158 32 000

E ### ### ### - - ### ###

L net 5 859 ###

L taxes 2 060 ###

Y taxes 649 ###

K 5 681 ###

M 1 980 ###

SM non-E - ###

SM E - ###

SM C - ###

SM X - ###

Sales taxes 1 257 ###

Resources 32 000 ###

Specific margins adjust to have E end-use prices match TIAM agent-specific prices

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E 14 085 ### 9 022 3 235 3 410 2 158 32 000

E ### ### ### - - ### ###

L net ### ###

L taxes ### ###

Y taxes 649 ###

K ### ###

M 1 980 ###

SM non-E - ###

SM E - ###

SM C - ###

SM X - ###

Sales taxes 1 257 ###

Resources 32 000 ###

In non-E production

K and L trade off with constant elasticity to produce aggregate KL (VA) considering wage and rent adjusted to clear markets

Optional imperfect L market magnifies cost of E investment crowding-out non-E investment

Resulting K, L and E combine into aggregate KLE following CES specification

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E ### ### 9 022 3 235 3 410 2 158 32 000

E ### ### ### - - ### ###

L net ### ###

L taxes ### ###

Y taxes 649 ###

K ### ###

M 1 980 ###

SM non-E - ###

SM E - ###

SM C - ###

SM X - ###

Sales taxes 1 257 ###

Resources 32 000 ###

In non-E production

Non-E intensity of non-E production and KLE aggregate trade off to produce domestic output Y

The price of the non-E good is the weighted average of domestic and import prices

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E ### ### 9 022 3 235 3 410 2 158 32 000

E ### ### ### - - ### ###

L net ### ###

L taxes ### ###

Y taxes 649 ###

K ### ###

M ### ###

SM non-E - ###

SM E - ###

SM C - ###

SM X - ###

Sales taxes 1 257 ###

Resources 32 000 ###

In non-E production

The ratio of imports to domestic output in (volumes) is isoelastic to the ratio of their prices

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E ### ### 9 022 3 235 3 410 2 158 32 000

E ### ### ### - - ### ###

L net ### ###

L taxes ### ###

Y taxes ### ###

K ### ###

M ### ###

SM non-E - ###

SM E - ###

SM C - ###

SM X - ###

Sales taxes 1 ### ###

Resources 32 000 ###

In non-E production

Exogenous tax rates

At each period from 2010 to 2100

B$ Non-E E C G I X Uses

Non-E ### ### ### ### ### ### ###

E ### ### ### - - ### ###

L net ### ###

L taxes ### ###

Y taxes ### ###

K ### ###

M ### ###

SM non-E - ###

SM E - ###

SM C - ###

SM X - ###

Sales taxes 1 ### ###

Resources ### ###

Final non-E consumptions

G and I are exogenous shares of GDP

X trades off with Xs of other regions at constant elasticity of substitution (Armington) to provide sum of Ms

Closure of accounting balance defines C

Overview of linkage

• TIMES-MACRO (Remme & Blesl, 2006)

• TIAM-KLEM

TIAM

Energy p&qs

KLEM

Labour

ES investment

Households’ consumption

Public consumption

International trade

Investment

Non-E/E Capital

Non-E output

Simultaneously

Iteratively

?Non-E prices?

Harmonising Drivers

• Why? – Initial calibration run not converging with significant differences in BASE calibration

• OECD-SSP2 economic outlook is quite different to existing ETSAP-TIAM macroeconomic drivers.

• SSP2• OECD_SSP2 IIASA-DB

• GDP, POP, Urbanisation

• OECD – ENV-LINKS model Sectoral projections• PAGR, PSERV, PCHEM, PISNF, POEI, POI• OECD in Paris were happy to provide baseline SSP2 consistent Gross

production and value added for results for their GTAP CGE model (25 regions/ 35 sectors)

• World Bank • Historical value added by sector• 2005 – 2010• Full data not available to 2015 yet.

New generation of scenarios

In the lead up to the IPCC’s Sixth Assessment Report new scenarios have been developed to more systematically explore key uncertainties in future socioeconomic developments

Five Shared Socioeconomic Pathways (SSPs) have been developed to explore challenges to adaptation and mitigation. Shared Policy Assumptions (SPAs) are used to achieve target forcing levels (W/m2).

Source: Riahi et al. 2016; IIASA SSP Database; Global Carbon Budget 2016

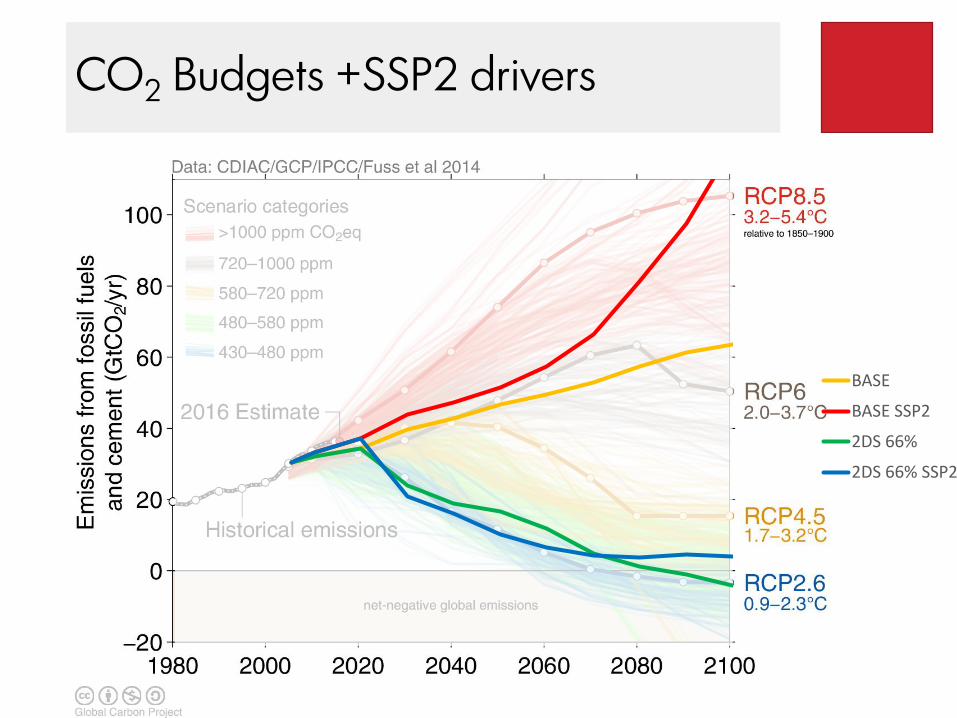

CO2 Budgets +SSP2 drivers

BASE

BASE SSP2

2DS 66%

2DS 66% SSP2

Driver Differences to SSP2

0

10

20

30

40

50

60

70

2000 2025 2050 2075 2100

GDP: AFR

BASE 15R

BASE 15R SSP2

0

5

10

15

20

25

2000 2025 2050 2075 2100

GDP: CHI

0

10

20

30

40

2000 2025 2050 2075 2100

GDP: IND

0

1

2

3

4

2000 2025 2050 2075 2100

GDP: WEU

0

0.5

1

1.5

2

2.5

3

3.5

2000 2025 2050 2075 2100

POP: AFR

BASE 15R

BASE 15R SSP21

1.1

1.2

1.3

1.4

1.5

1.6

2000 2025 2050 2075 2100

POP: IND

0.5

0.7

0.9

1.1

1.3

2000 2025 2050 2075 2100

POP: CHI

0.8

0.9

1

1.1

1.2

2000 2025 2050 2075 2100

POP: WEU

Driver Differences to SSP2

0

20

40

60

80

100

2000 2025 2050 2075 2100

SERV: AFR

BASE 15R

BASE 15R SSP2

0

20

40

60

80

2000 2025 2050 2075 2100

SERV: IND

0

1

2

3

4

5

2000 2025 2050 2075 2100

SERV: WEU

0

50

100

150

200

2000 2025 2050 2075 2100

ISNF: AFR

BASE 15R

BASE 15R SSP2

0

200

400

600

800

2000 2025 2050 2075 2100

ISNF: IND

0

0.5

1

1.5

2

2.5

3

2000 2025 2050 2075 2100

ISNF: WEU

0

10

20

30

40

50

2000 2025 2050 2075 2100

ISNF: CHI

0

5

10

15

20

25

2000 2025 2050 2075 2100

SERV: CHI

??

Primary Energy

0

200

400

600

800

1000

1200

BASE BASE BASESSP2

2DS 66% 2DS 66%SSP2

BASE BASESSP2

2DS 66% 2DS 66%SSP2

2005 2030 2050

ExaJ

ou

les

Coal Oil Gas Nuclear Hydro Biomass Renewable except hydro and biomass

0

500

1000

1500

2000

2500

BASE BASESSP2

2DS66%

2DS66%SSP2

2100

ExaJ

ou

les

Final Energy

-

100

200

300

400

500

600

700

BASE BASE BASESSP2

2DS 66% 2DS 66%SSP2

BASE BASESSP2

2DS 66% 2DS 66%SSP2

2005 2030 2050

ExaJ

ou

les

Coal Oil ProductsGas ElectricityBiomass (excludes liquid biofuels) BiodieselAlcohol Other RenewableHeat Hydrogen

-

200

400

600

800

1,000

1,200

1,400

1,600

BASE BASESSP2

2DS 66% 2DS 66%SSP2

2100Ex

aJo

ule

s

Electricity Capacity

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

BASE BASESSP2

2DS66%

2DS66%SSP2

BASE BASESSP2

2DS66%

2DS66%SSP2

BASE BASESSP2

2DS66%

2DS66%SSP2

2005 2030 2050

GW

Electricity Generation Installed Capacities (GW)

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

BASE BASESSP2

2DS66%

2DS66%SSP2

2100

GW

Solar Thermal

Solar PV

Geo, Tidal andWave

Wind

Biomass CCS

Biomass

Hydro

Nuclear

Gas CCS

Gas and Oil

Coal

Electricity Generation

0

20

40

60

80

100

120

140

160

BASE BASE BASESSP2

2DS66%

2DS66%SSP2

BASE BASESSP2

2DS66%

2DS66%SSP2

2005 2030 2050

Exaj

ou

les

Total Electricity Generation

0

100

200

300

400

500

600

BASE BASESSP2

2DS66%

2DS66%SSP2

2100

Exaj

ou

les

SolarThermalSolar PV

Geo, Tidaland WaveWind

BiomassCCSBiomass

Hydro

Nuclear

CH4OptionsGas CCS

Gas andOil

KLEM eventual Outputs

• GDP change

• Consumption change across sectors

• Employment change

• Re-estimated output/drivers • Residential,

• Energy firms

• Non-Energy – Commercial/Services

Conclusions

• This hybrid type of approach steps towards sectoral specific dynamics of decarbonising from a bottom up technology explicit perspective• Unemployment, structural changes, sectoral outputs, drivers

• A broader approach to assess demand uncertainty using the SSP narratives could be integrated into TIAM/regional/or National Models• A CGE such as KLEM or GTAP is required to generate sectoral SSP drivers.

(disaggregate GDP)• Is it appropriate that we generally don’t have multiple drivers scenarios?• Long term OECD-SSP2 drivers cause extreme growth indices post 2060 in

emerging economies. – review elasticities…

• A Hybrid (GE) TIAM is ideal for NDC analysis given TIAM’s bottom up nature and a hybrid general equilibrium with the economy.• Technology specific NDCs - USA• Economic Intensity NDCs - INDIA/CHINA• Carbon limits - Europe

Environmental Research InstituteInstiúd Taighde Comshaoil

Energy Policy and Modelling Groupwww.ucc.ie/energypolicy

@james_glynn

Lahinch Beach, Co Clare, IRELAND– Monday, January 6th

Thanks youQUESTIONS?

@james_glynn is a Postdoctoral researcher in @MaREIcentre @ERIUCC @UCC

working on global integrated assessment models linking detailed energy-economy-climate

models, to assess equitable, ambitious and secure decarbonisation of the energy system

eMail: [email protected]

Twitter: @james_glynn

Web: www.ucc.ie/energypolicy

Profile: http://www.ucc.ie/en/energypolicy/people/jamesglynn/

Energy Policy & Modelling Collaborators and Funders

GLOBAL ETSAP-TIAM model

• Linear programming bottom-up energy system model of IEA-ETSAP

• Integrated model of the entire energy system

• Prospective analysis on medium to long term horizon (2100)• Demand driven by exogenous energy service demands

• Partial and dynamic equilibrium (perfect market)

• Optimal technology selection

• Minimizes the total system cost

• Environmental constraints• Integrated Climate Model

• 15 Region Global Model

• Price-elastic demands

• Macro Stand Alone• Single consumer-producer, multi-regional, inter-temporal general equilibrium model which

maximises regional utility.• The utility is a logarithmic function of the consumption of a single generic consumer.• Production inputs are labour, capital and energy.• Energy demand and energy costs from ETSAP-TIAM model.• MSA Re-estimates Energy Service Demands based on energy cost

IPCC INDC Synthesis Report

ETSAP-TIAMReference Energy System

Source: Loulou, R., Labriet, M., 2008. ETSAP-TIAM: the TIMES integrated assessment model Part I: Model structure. Comput. Manag. Sci. 5, 7–40. doi:10.1007/s10287-007-0046-z

ETSAP-TIAM 15 Regions

AFR

CAN

USA

MEX

CSA

WEU

EEU

MEA

IND

CHISKO

JPN

AUS

ODA

GDP losses & Costs of Delayed Action

0 2 4 6 8 10 12 14 16 18 20

2DS 50%

2DS 50% DA20

2DS 50%

2DS 50% DA20

2DS 50%

2DS 50% DA20

2DS 50%

2DS 50% DA20

20

30

.2

05

0.

20

70

.2

10

0

GDP Loss %

Former Soviet Union

Australia & NZ

South Korea

Other Developing Asia

Canada

Middle East

China

East Europe

Africa

India

West Europe

Japan

USA

Central South America

Mexico

ETSAP-TIAM MSA (TMSA)Macro Stand Alone

𝑀𝑎𝑥 𝑈 =

𝑡=1

𝑇

𝑟

𝑛𝑤𝑡𝑟 . 𝑝𝑤𝑡𝑡. 𝑑𝑓𝑎𝑐𝑡𝑟,𝑡. 𝑙𝑛 𝐶𝑟,𝑡 (1) (MSA OBJz)

𝑌𝑟,𝑡 = 𝐶𝑟,𝑡 + 𝐼𝑁𝑉𝑟,𝑡 + 𝐸𝐶𝑟,𝑡 + 𝑁𝑇𝑋(𝑛𝑚𝑟)𝑟,𝑡 (2)

𝑌𝑟,𝑡 = 𝑎𝑘𝑙𝑟 ∙ 𝐾𝑟,𝑡𝑘𝑝𝑣𝑠𝑟∙𝜌𝑟 ∙ 𝑙𝑟,𝑡

(1−𝑘𝑝𝑣𝑠𝑟)𝜌𝑟 +

𝑘

𝑏𝑟,𝑘 ∙ 𝐷𝐸𝑀𝑟,𝑡,𝑘𝜌𝑟

1𝜌𝑟

(3)

• nwt – Negishi Weights

• pwt – weight Multiplier

• dfact – utility discount factor

• C - Consumption

• Y – Production

• INV – Investment

• EC – Energy Cost

• NTX – Net exports

• akl – production fn constant

• K – Capital

• kpvs – capital value share

• l - Labour annual growth

• b – Demand coefficient

• p – elasticity of substitution

• DEM - Energy Demands

R

r YEARSy

yREFYR

yr yrANNCOSTdNPVMin1

, ),()1( (TIAM OBJz)

TIMES Energy System Model

Cost and emissions balance

GDP

Process

Heating area

Population

Light

Comms

Power

Person kilometers

Freight kilometers

Service Demands

Coal processing

Refineries

Power plantsand

Transportation

CHP plantsand district

heat networks

Gas network

Industry

Commercial and

Tertiary

Households

Transport

Final energyPrimary energy

Domesticsources

Imports

De

ma

nd

sE

ne

rgy p

rice

s, R

eso

urc

e a

vaila

bili

ty