lÍnea tÍtulo # 1 - hochschildmining.com · ramp entrance primary crusher being installed ......

TRANSCRIPT

HOCHSCHILD MINING Annual Results 2014

18 March 2015

DISCLAIMER

2

Some statements contained in this presentation or in documents referred to in it are or may be forward-looking statements. Actual results may differ from those expressed in such statements, depending on a variety of factors.

Past performance of the Company or its shares cannot be relied on as a guide to future performance.

Any forward-looking information contained in this presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect, and accordingly, actual results may vary.

This presentation does not constitute, or form part of or contain any invitation or offer to any person to underwrite, subscribe for, otherwise acquire, or dispose of any shares in Hochschild Mining plc or advise persons to do so in any jurisdiction, nor shall it, or any part of it, form the basis of or be relied on in any connection with or act as an inducement to enter into any contract or commitment therefore. No reliance may be placed for any purpose whatsoever on the information or opinions contained in this document or on its completeness and no liability whatsoever is accepted for any loss howsoever arising from any use of this document or its contents otherwise in connection therewith. Nothing in this presentation is to be construed as a profit forecast.

This presentation has been prepared in compliance with English law and English courts will have exclusive jurisdiction over any disputes arising from or connected with this presentation.

INCREASING PRODUCTION, REDUCING COSTS, OPTIMISING OPERATIONS

Key Highlights

3

Delivering profitable growth

Aggressive cash optimisation plan: $300m of savings

New Inmaculada mine poised to double free cash flows: 12m oz @ $11-12/oz (Ag Eq)

Delivering consistent production increases: from 20 to 29m oz (Ag Eq)

AISC reduced from $21.7/oz to $15-16/oz (Ag Eq)

Secure financial position: growth fully financed

HOCHSCHILD MINING Ramon Barua, CFO

Financial Results

Angela vein (Inmaculada)

(42.1)

(56.9)

(56.7)

19.7

17.9

10.3

10.2

7.8

3.2

(20.9)

(5.9)

5

P&L

$m (pre-exceptional) 2014 2013 variance

Revenue 493.0 622.2 (129.2)

Cost of sales (404.6) (466.8) 62.0

Gross profit 88.3 155.4 (67.1)

Gross profit margin 17.9% 25.0% (7.1)

Administrative exp. (43.3) (54.4) 11.1

Selling exp. (28.7) (28.8) 0.1

Exploration exp. (17.2) (42.9) 25.7

Others net (13.4) (11.6) (1.8)

Finance net (30.9) (1.0) (29.9)

FX loss (5.0) (19.8) 14.8

PBT (50.2) 2.9 53.1

Tax (6.5) (45.0) 38.5

Net (loss)/profit (56.7) (42.1) (14.6)

Attrib. net profit (54.9) (50.3) (4.6)

EPS (0.15) (0.15) -

Adjusted EBITDA 135.6 201.0 (65.4)

2014 vs 2013 net profit reconciliation

$m (pre-excep post tax)

2013 Net profit

Production cost

Finance net

Admin

Exploration

Hedge

Prices

Others

2014 Net profit

10

15

20

25

30

35

2013 2014 2015

Average mkt prices for silver

$/oz

Avg: $23.9/oz

Avg: $19.1/oz

FX

Volume

6

ALL-IN SUSTAINING COSTS REDUCED BY ALMOST 30% SINCE 2012

Main operation AISC reconciliation (pre-exceptional)

$/oz Ag Eq

All-in sustaining costs continuing to fall

21.7

18.6 17.4

15-16

(1.0 ) (0.5) (0.2)

0.5

AISC 2012 AISC 2013 Capex Production costs Admin expenses Commercial discounts AISC 2014 AISC 2015

-29%

7

Growth strategy financed

BALANCE SHEET ANALYSIS

286

299

116

3

27 14 3

(33)

19

(26)

(187)

10

Dec 2013 cash balance

Arcata cash generation**

Pallancata cash

generation

San Jose cash generation

Ares cash generation

Corporate & Exploration

Cash balance Debt Interest Project capex & opex

Others Dec 2014 cash balance

Liquidity position

• Cash position: $116m* + $75m in 2015

• Low cost Inmaculada project fully funded

― Remaining construction capex: $72m

• Forward sale of:

― 6moz Ag @$17.75/oz for 2015

― 38,000oz Au @$1,300/oz for 2015

Debt Commitment

size Maturity

Rate (pre tax)

Rate (post tax)

Senior notes 350 2021 7.75% 5.58%

Medium term loan 100 2019 Libor +2.6% 2.06%

Short term funding 75 Feb 2016 1.56% 1.12%

Evolution of cash balance

*As at 31 Dec 2014 **Cash generation is calculated as EBITDA less operational capex & exploration capex

$m

Operations showing positive cash generation

HOCHSCHILD MINING Ignacio Bustamante, CEO

18 March 2015

PRESERVING CAPITAL & OPTIMISING CASHFLOW

9

Cashflow optimisation programme*

Well over $300m of savings identified since plan announcement in mid 2013

• Production costs reduced by $101m (vs initial 2013 guidance)

• Administration costs reduced by $30m (vs 2012)

• Sustaining capex reduced by $135m (2015 guidance of $45m vs initial 2013 guidance)

• Exploration costs reduced by $58m (vs initial 2013 guidance)

• Operational efficiencies in dilution control, supply chain management, commercial negotiations & working capital improvements

• Significant headcount reduction

*Includes dividend suspension in 2013 of $20.2m

INMACULADA

10

• World class gold/silver project close to completion

• Located in Hochschild’s Southern Peru Cluster

• Set to deliver 11-12m oz in 2016

• Operations set to commence in Q2 2015

• Expected to be Hochschild’s lowest cost operation @11.8/oz AISC (Ag Eq)

• Strong geological upside potential

11

Plant commissioning set for Q2 2015

GFMS/UBS Global gold AISC curve (Jan 2015)*

INMACULADA: AISC OF $711/OZ

Initial resource Life-of-Mine 11.3 yrs

Average annual production (Au Eq) 189k oz

Average annual production (Ag Eq) 11.3m oz

Production Data

Pre production capex $420m

AISC (Au Eq) 711/oz

AISC (Ag Eq) 11.8/oz

Updated Operating Summary

*Source: GFMS/UBS Global I/O®: Miner’s Price Review (15 Jan 2015)

Inmaculada (e)

Costs and Capex

GFMS/UBS Global gold AISC curve (Jan 2015)*

90%

34%

90%

100%

100%

100%

100%

100%

100%

90%

10%

66%

10%

Overall progress

Paste backfill

Plant construction

Contracts & Procurement

EIS approval

Permitting

Engineering

Mine development

Electricity transmission line

Infrastructure & Access

Completed Remaining

12

12

Majority of key deliverables completed

Overall project progress

INMACULADA PROGRESS

On track to produce 6-7m oz in 2015

Approx. 200kt of mineral already stockpiled

Processing plant - building housing grinding mills Processing plant - grinding mill installation

Processing plant – pre-thickener Processing plant – lixiviation tanks

Primary crusher being installed Ramp entrance

Main camp Processing plant: CCD tanks

HOCHSCHILD MINING: INMACULADA

13

Hochschild’s new mine set to deliver 11-12m oz in 2016

INMACULADA UPSIDE

14

Quellopata system

Upside outside current Angela resource base

6m average vein width

Selected key intercepts

[email protected] g/t Au & 1,851 g/t Ag [email protected] g/t Au & 531 g/t Ag

[email protected] g/t Au & 188 g/t Ag

[email protected] g/t Au & 81 g/t Ag [email protected] g/t Au & 81 g/t Ag

3.50m@ 7.12g/t Au & 369g/t Ag 1.50m@ 6.34g/t Au & 180g/t Ag

3.12m@ 31.55g/t Au & 199g/t Ag

[email protected] g/t Au & 153 g/t Ag

[email protected] g/t Au & 214 g/t Ag

Inmaculada area

REGIONAL UPSIDE

15

Consolidating a major mining district

• Mining concession & superficial rights secured

• 60km mineralised belt with new veins discovered

• Geochemical results show Au/Ag presence at surface

• Mapping over the whole district to be completed in 2015

• Corina: 100% earn-in with Lara Exploration Ltd.

― 4 km vein with Au values at surface - 20 km from Selene

• Strong potential to:

― Increase resource base at Inmaculada & Pallancata

― Discover a new mine

Substantial land package in Hochschild’s Southern Peru cluster

• Substantial areas of the deposit still to be explored

• Continuing the extension of the Tunnel 4 vein system

• Baja vein re-evaluation including base metal potential

• New Lucero vein discovery:

― Potentially two veins with known 400m strike

― Very high Ag values (>1,000 g/t Ag)

• Pamela Sur veins: Up to 3 km of inferred strike length. Testing for continuity in 2015

PERUVIAN BROWNFIELD EXPLORATION: ARCATA

16

Peruvian assets remain highly prospective

Strong exploration potential remains at Arcata

DDH764 LM-14 (4337) • Vein width: up to 1.43m • Au: up to 4.94 g/t • Ag: up to 2,102 g/t

DDH742 LM-14 (4339) • Vein width: up to 0.97m • Au: up to 11.12 g/t • Ag: up to 1,437 g/t

Lucero veins

DDH742 LM-14 (4335) • Vein width: up to 1.11m • Au: up to 1.55 g/t • Ag: up to 329 g/t

Pamela Sur Veins

Baja SW Baja

Tunel 4

Marion

Marion NW

Pamela NS

PamelaPamela W

Lucero4333

4335

43374339

784000

784000

792000

792000

83

40

00

0

83

40

00

0

83

48

00

0

83

48

00

0

LEGEND

Samples

Mine

Vein

Arcata

Arcata

5Km

DDH742 LM-14 (4335) • Vein width: up to 0.9m • Au: up to 1.75 g/t • Ag: up to 661 g/t

PERUVIAN BROWNFIELD EXPLORATION: PALLANCATA

17

Peruvian assets remain highly prospective

Pallancata exploration programme recommenced

BenefitPlant

Yanacochita

Bolsa

Farallón

Royropata

Pallancata

Mercedes

Rina

Charo

LuisaYurika Virgen del

Carmen

San

CayetanoFalla NS

Alizze

Pacapausa

Pallancata

695000

695000

700000

700000

83

70

00

0

83

70

00

0

83

75

00

0

83

75

00

0

2Km

LEGEND

Resources potential areas

Veins

Observed vein

Pallancata vein

Infered vein

Mine

Project

Claims

• 2014 brownfield exploration programme delayed due to surface rights permission – now secured

• Exploring & drilling new targets in the Yurika – Luisa area

• 19,100m programme in 2015 to focus on inferred resource exploration

• Additional geological mapping of west and south side for new target definition

0

10

20

30

40

2013 2014 2015 2016

PRODUCTION IMPACT

Production uplift

18

3 years of growth

20.5 22.2

M Ag eq oz

24.0

29.0

Inmaculada Ageing operations Core operations

Expected attributable production

MEDIUM TO LONG TERM GROWTH POTENTIAL

19

Pipeline of projects spread across the Americas

Strong portfolio optionality

• Brownfield potential at all current

operations

• Portfolio of growth options spread across

the Americas

• 2015 greenfield activity focused on most

promising options including:

―Riverside JV in Mexico

―Corina & Ibel projects in Peru

Volcan (100% owned)

• Acquired as future strategic resource

• Large Chilean gold deposit

• Water rights purchased by Andina

• 9.6m oz of gold resources

• Open pit project in S.Peru Cluster

• Expected 2.7m Ag Eq p.a.

• Construction permit approved

• Remaining capex of $80m

Crespo (100% owned)

• Several veins delineated

• Over 100m oz of silver Eq resources

• Geological potential in district

• Large overall land package

Azuca (100% owned)

Chile

Peru

Peru

MARKET NOT RECOGNISING INMACULADA VALUE

20

Valuation gap exists versus other primary silver producers

4.8x

5.7x

11.9x

12.0x

12.9x

14.2x

2.9x 3.4x

9.0x

8.0x 8.5x

13.3x

First Majestic Hochschild Tahoe Fresnillo Hecla Pan American

2015e 2016e

*Source: BAML European Metals & Mining Weekly/ North American Precious Metal Weekly

29 40

54

95

132

175

22

41 42

87

120 130

Hochschild Pan American First Majestic Tahoe Hecla Fresnillo

2015e 2016e

BAML EV/EBITDA forecasts vs

primary silver peers*

BAML 2015e adjusted market cap per oz

production vs primary silver peers*

SUMMARY

21

Delivering profitable growth

2015 AISC: $15-16/oz

Key value catalyst

Growth fully financed

Cost Competitiveness • Company savings targets exceeded • All operations cashflow positive

Project Execution • Close to completion of low cost growth driver • Production set to increase by over 30%

Financial Efficiency • Flexible balance sheet strategy • Cashflow set to double

23 Hanover Square, London, W1S 1JB, Tel: +44 (0) 20 3714 9040 www.hochschildmining.com

Charlie Gordon +44 (0)20 3714 9042 [email protected]

CORE ASSETS OPTIMISED

• Located in Southern Peru Cluster - 4,600 MASL

•Underground operation - commenced in 1964

• Conventional & mechanised cut-and-fill mining

• 2014 All-in sustaining costs: $17.7/oz

• Current plant capacity: 1,500 t/day

Arcata

23

100% owned Pallancata 100% owned

• Located in Southern Peru Cluster

•Underground operation – commenced in 2007

•Mined using cut and fill

• 2014 All-in sustaining costs: $16.7/oz

• Current plant capacity:1,800 t/day

San Jose 51% owned

• Located in Argentina, in Santa Cruz province

•Underground operation – commenced in 2007

• Low sulphidation with quartz sulphide veins

• 2014 All-in sustaining costs: $17.8/oz

• Current plant capacity: 1,650 t/day

2014 2013

Ore production (tonnes) 701,947 900,861

Average silver grade (g/t) 286 217

Average gold grade (g/t) 0.85 0.74

Silver produced (koz) 5,827 4,984

Gold produced (koz) 16.89 16.83

Silver equivalent produced (koz) 6,841 5,994

Unit cost ($/t) 89.1 81.3

Total cash cost ($/oz Ag co-product) 12.6 12.7

All-in sustaining cost ($/oz) 17.7 20.9

2014 2013

Ore production (tonnes) 1,051,068 1,088,712

Average silver grade (g/t) 238 264

Average gold grade (g/t) 1.03 1.13

Silver produced (koz) 6,527 7,628

Gold produced (koz) 24.34 27.83

Silver equivalent produced (koz) 7,988 9,298

Unit cost ($/t) 69.3 68.3

Total cash cost ($/oz Ag co-product) 11.0 10.3

All-in sustaining cost ($/oz) 16.7 16.7

2014 2013

Ore production (tonnes) 571,017 536,937

Average silver grade (g/t) 404 425

Average gold grade (g/t) 5.77 6.42

Silver produced (koz) 6,469 6,357

Gold produced (koz) 94.16 98.83

Silver equivalent produced (koz) 12,119 12,286

Unit cost ($/t) 197.8 210.0

Total cash cost ($/oz Ag co-product) 12.1 13.4

All-in sustaining cost ($/oz) 17.8 19.0

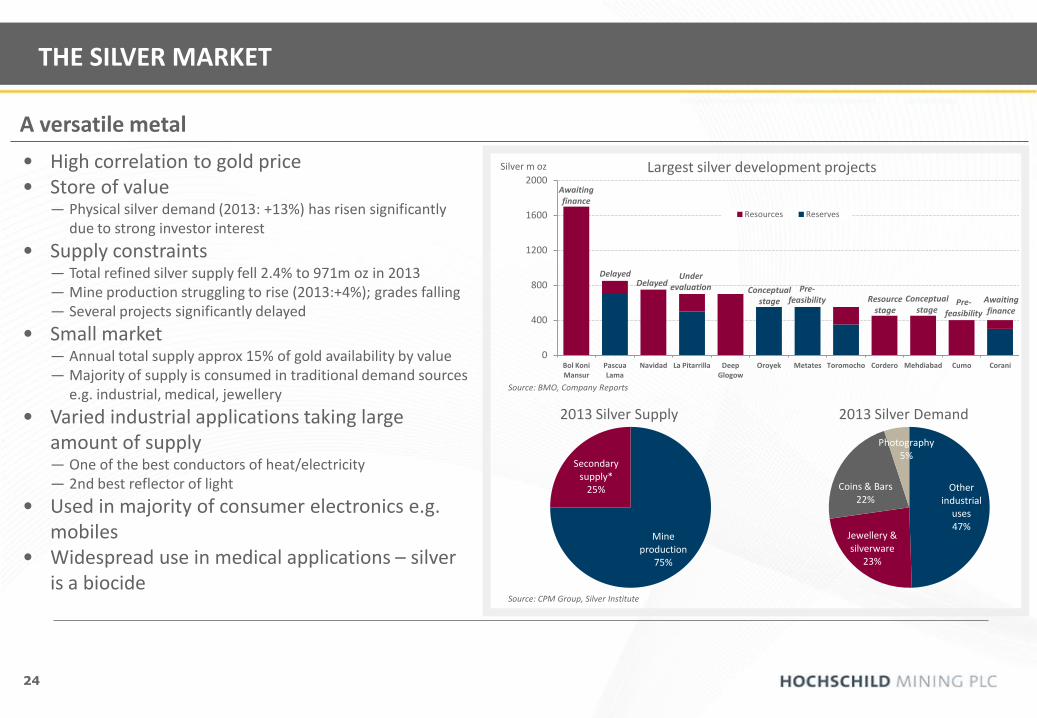

24

0

400

800

1200

1600

2000

Bol Koni Mansur

Pascua Lama

Navidad La Pitarrilla Deep Glogow

Oroyek Metates Toromocho Cordero Mehdiabad Cumo Corani

Resources Reserves

Largest silver development projects

Source: BMO, Company Reports

Silver m oz • High correlation to gold price • Store of value

― Physical silver demand (2013: +13%) has risen significantly due to strong investor interest

• Supply constraints ― Total refined silver supply fell 2.4% to 971m oz in 2013 ― Mine production struggling to rise (2013:+4%); grades falling ― Several projects significantly delayed

• Small market ― Annual total supply approx 15% of gold availability by value ― Majority of supply is consumed in traditional demand sources

e.g. industrial, medical, jewellery

• Varied industrial applications taking large amount of supply ― One of the best conductors of heat/electricity ― 2nd best reflector of light

• Used in majority of consumer electronics e.g. mobiles

• Widespread use in medical applications – silver is a biocide

Mine production

75%

Secondary supply*

25%

2013 Silver Supply

Other industrial

uses 47%

Jewellery & silverware

23%

Coins & Bars 22%

Photography 5%

2013 Silver Demand

A versatile metal

THE SILVER MARKET

Source: CPM Group, Silver Institute

Awaiting finance

Delayed Delayed

Under evaluation Conceptual

stage

Pre-feasibility Resource

stage Conceptual

stage Pre-

feasibility

Awaiting finance