life risk-based capital (e) working group - naic.org · attachment capital adequacy (e) task force...

TRANSCRIPT

© 2017 National Association of Insurance Commissioners 1

Date: 3/30/17 2017 Spring National Meeting

Denver, Colorado

LIFE RISK-BASED CAPITAL (E) WORKING GROUP Saturday, April 8, 2017

10:00 – 11:00 a.m. Colorado Convention Center—Room 107/109/111/113—Street Level

ROLL CALL

Philip Barlow, Chair District of Columbia Fred Andersen Minnesota Kerry Krantz, Vice Chair Florida William Leung Missouri Steve Ostlund Alabama Felix Schirripa New Jersey Perry Kupferman California William Carmello New York Deborah Batista Colorado Frank Stone Oklahoma Wanchin Chou Connecticut Mike Boerner Texas Chris Buchanan Kansas

AGENDA 1. Consider Adoption of its March 17 Minutes—Philip Barlow (DC) Attachment A 2. Receive an Update from the American Academy of Actuaries’ (Academy) Longevity Risk

Task Force—Patricia Matson (Academy) Attachment B

3. Discuss Proposed Risk-Based Capital (RBC) Shortfall Instructional Changes Attachment C —Philip Barlow (DC)

4. Discuss the Federal Home Loan Bank (FHLB) Proposal—Philip Barlow (DC) Attachment D

5. Discuss its 2017 Working Agenda—Philip Barlow (DC) Attachment E

6. Discuss Any Other Matters Brought Before the Working Group—Philip Barlow (DC) 7. Adjournment W:\National Meetings\2017\Spring\Agenda\Agenda LRBC Spring 2017.docx

1

This page intentionally left blank.

2

Attachment Capital Adequacy (E) Task Force

4/--/17

© 2017 National Association of Insurance Commissioners 1

Draft: 3/29/17

Life Risk-Based Capital (E) Working Group Conference Call March 17, 2017

The Life Risk-Based Capital (E) Working Group of the Capital Adequacy (E) Task Force met via conference call March 17, 2017. The following Working Group members participated: Philip Barlow, Chair (DC); Kerry Krantz, Vice Chair (FL); Steve Ostlund (AL); Perry Kupferman (CA); Wanchin Chou and James Jakielo (CT); Chris Buchanan (KS); John Robinson (MN); Felix Schirripa (NJ); William Carmello (NY); Frank Stone (OK); and Mike Boerner (TX).

1. Adopted its Jan. 10 2017 and Fall National Meeting Minutes

Mr. Ostlund made a motion, seconded by Mr. Boerner, to adopt the Working Group’s Jan. 10 2017 (Attachment 1) and Dec. 10 2016 minutes (see NAIC Proceedings – Fall 2016, Capital Adequacy (E) Task Force, Attachment Four). The motion passed unanimously.

2. Adopted Proposal 2017-01-L RBC Ratio

Dave Fleming (NAIC) said the only change to what was exposed is the addition of authorized control level to the line description to specify what the RBC ratio calculation represents. Mr. Ostlund made a motion, seconded by Mr. Krantz to adopt the proposal (Attachment 2) with the added specificity. The motion passed unanimously.

3. Exposed Proposal 2017-02-L Primary Security Shortfall Instructional Change

Mr. Jakielo presented Connecticut’s comments (Attachment 3). Paul Graham (American Council of Life Insurers—ACLI) said he and Mr. Jakielo were in agreement with the changes suggested in items one, two and five in Connecticut’s comments. He said he has also discussed with Rector & Associates their work with NAIC staff on the supplemental XXX-AXXX Reinsurance Exhibit to coordinate the wording between the supplement and RBC. He said he believes the supplement will contain exactly what is needed for RBC and is what the wording in the ACLI’s comment letter (Attachment 4) is trying to get at. He suggested reviewing the completed and exposed supplement changes to ensure consistency. The Working Group agreed to re-expose the proposal with the changes suggested by Connecticut and the ACLI for a comment period of 30 days with any preliminary feedback requested at the Spring National Meeting.

4. Discussed Proposal 2017-03-L FHLB Collateral

Mr. Barlow said the comment letters received (Attachments 5 through 11) were generally supportive of the proposal. Benefits of FHLB membership commonly highlighted in the comments include: 1) low-cost liquidity with favorable risk characteristics; 2) ability to increase and diversify earnings and; 3) improve asset liability matching. It was also commonly noted that FHLB advances are currently subject to three layers of RBC charges. Mr. Schirripa said he believes that FHLB is good for industry and supports it. He suggested, however, the proposal may encourage spread banking and said some companies got in trouble with guaranteed investment contracts (GIC) when this was done in the past. He said it may be prudent to have some sort of limit as a precaution. John Bruins (ACLI) agreed that some companies got in trouble with GICs but asked regulators to consider the broad framework of regulatory oversight that exists. He said there is no limit on GICs today and that it is controlled through that broader framework. Mr. Schirripa said regulators did not need to control this as the markets took care of it through a lack of demand. In this case, FHLB is encouraging this activity so he believes a regulatory response is needed. Mr. Bruins cited other regulatory tools and said the NAIC is moving forward with risk-focused examinations which would include this. He said this would be covered in a company’s ORSA filing where they outline the risks they are taking and how they are managing those risks. He said he understands that there is a concern but regulators have tools beyond RBC and some of those tools already place a limit even though it may not be an explicit percentage or dollar amount. Mr. Schirripa said he did not see how having a guardrail would be objectionable. While there may be other avenues for controlling the use of FHLB loans, Mr. Barlow said it is something that potentially creates risk to the insurance company and it seems an appropriate place to address that is in RBC. Mr. Bruins said there should be consideration for the controls that already exist to determine what, if any, additional controls are needed.

Attachment A

3

Attachment Capital Adequacy (E) Task Force

4/--/17

© 2017 National Association of Insurance Commissioners 2

Don Messier (National Life Group) said it would be helpful to elaborate on the specific risk related to FHLB advances not currently addressed in RBC that is causing the concern. Mr. Schirripa said one risk is that the collateral requirements on a company can change. Mr. Krantz said a risk is that the company becomes overleveraged. Mr. Barlow suggested Mr. Schirripa and the ACLI work together to see if there is a way to modify the proposal to address the concerns raised. Having no further business, the Life Risk-Based Capital (E) Working Group adjourned. w:\national meetings\2017\Spring\tf\CapAdequacy\LifeRBC\Att Life RBC 7016-3-17.doc

Attachment A

4

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

LONGEVITY RISK TASK FORCE UPDATE

TRICIA MATSON, MAAA, FSA CHAIRPERSON, LONGEVITY RISK TASK FORCE (LRTF)

APRIL 8, 2017

Presentation to the NAIC’s Life Risk Based Capital Working Group

Attachment B

5

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

2

Agenda

Review charge of Longevity Risk Task Force (LRTF) LRTF working positions Review mortality improvement experience Limitations Next steps

Attachment B

6

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

3

Charge to LRTF Guided by work of NAIC Joint LATF/LRBC Subgroup (LRSG)

Assess approach for longevity risk charge in RBC, initially focusing on annuity products

Per discussions with LRSG, consensus has been reached that statutory reserves sufficiently cover longevity risk via asset adequacy analysis. LRSG is evaluating whether guidance to the actuary is sufficient.

Specific request for LRTF to evaluate: An appropriate definition of a tail stress event

A potential RBC charge based on the difference between reported statutory reserves and statutory reserves using stressed mortality

An RBC charge expressed as a factor(s) applied to statutory reserves

LRTF focused on methodology; the ultimate statistical safety level for the risk charge (i.e., time horizon and confidence level) will be defined by the regulators

Attachment B

7

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

4

LRTF Current Views RBC charge should reflect the impact of a longevity stress on all

future cash flows Tentative position is to exclude the potential effects of medical

breakthroughs in the initial phase of establishing a risk charge andconsider as a second phase Significant public research performed by research professionals on

potential medical breakthroughs Differing opinions exist on the effect of medical breakthroughs on

mortality improvement Further discussion is needed to determine if potential effects should be

included in RBC

Attachment B

8

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

5

LRTF Current Views Statutory reserves are generally held at the 85th percentile level

Tabular plus any additional reserves from asset adequacy analysis

Capital requirements are established under the assumption that statutory reserves areadequate; RBC is not a balance sheet item and is not intended to make up for shortfallsin reserves

RBC factors generally cover risks in excess of reserves up to a 95th percentileevent The longevity risk stress event is defined at the 1/200 mortality improvement level,

using a 5-10 year time period

Mortality improvements up to the 85th percentile are assumed to be covered inreserves

RBC charge will be based on difference between “current” Statutory reserve andStatutory reserve calculated under a longevity stress

Attachment B

9

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

6

Treatment of Mortality Improvement Longevity risk comprised of:

Base table mis-estimation risk Trend risk (i.e., mortality improvement) Short-term mortality volatility risk

LRTF is focusing on trend risk only Base table mis-estimation; very difficult to separate mis-

estimation risk from trend risk in historical data Short-term volatility risk will have a small financial impact

on longevity products

Attachment B

10

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

7

Working Quantification of Stress Mortality LRTF analyzed historical population data over the period 1900-2013

using Social Security population data Calculated 1, 5, 10, 20, and 40 year rates of improvement by age

bucket and gender Fit historical improvement data to a normal distribution to evaluate

use of a normal model Developed a 95th %ile improvement event, focused on the 20-year

historical period (which is conservative vs current RBC’s typical 5-10 year horizon)

Evaluated difference between 95th %ile and 85th %ile for use in RBC

Attachment B

11

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

8

Calibration of Stress Event by Age – Normal Model

Average improvement (blue bars) has declined with age 85th and 95th percentile improvements relative to the average have increased with age. (red and

green lines sloped up) Net difference between the 85th and 95th%ile outcome (orange line) is our focus for RBC Overall calibration using normal model results in a 25% shock (165% - 140%). The corresponding

shock at an age group level would range from 20% to 52%

Bars show mean, 85th %ile, and 95th %ile annual improvement percentages Lines show the difference between points on the distribution

Attachment B

12

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

9

Historical Data vs Normal Model

LRTF evaluated the average, 85th %ile, and 95th %ile observed directly from the data as well as after fitting the data to a normal model

Historical implied stress from 85th to 95th percentile is

lower than normal model for all age groups

The normal model may not be a good fit

But historical data contains only limited number of non-overlapping 20-yr periods making estimates of tail outcomes less reliable

LRTF now leaning toward direct use of historical data

Attachment B

13

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

10

Impact of Gender on Mortality Improvement

Male and Female results are largely consistent based on either historical data or a normal model Working position is to use the same shock across genders and below age 85, and a higher shock at ages 85+

Attachment B

14

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

11

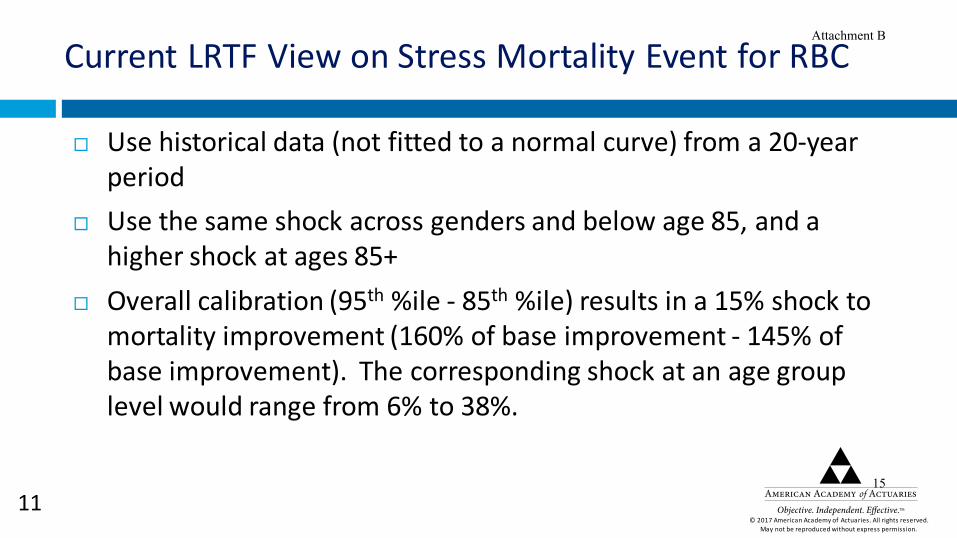

Current LRTF View on Stress Mortality Event for RBC

Use historical data (not fitted to a normal curve) from a 20-year period

Use the same shock across genders and below age 85, and a higher shock at ages 85+

Overall calibration (95th %ile - 85th %ile) results in a 15% shock to mortality improvement (160% of base improvement - 145% of base improvement). The corresponding shock at an age group level would range from 6% to 38%.

Attachment B

15

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

12

Limitations and Considerations

Underlying data for derivation of stress event has limitations, so that resulting stress varies significantly depending on: Data period used and # years evaluated Direct use versus fitting to a distribution

There is significant uncertainty in the estimate of an 85th to 95th percentile stress (currently defined as 15% of baseline)

RBC charge under the proposed approach is dependent on the valuation rate, but that may not be appropriate to reflect in the current RBC construct

Analysis focused on historical mortality data to define risk, without incorporation of different mortality risk events in the future

Attachment B

16

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

13

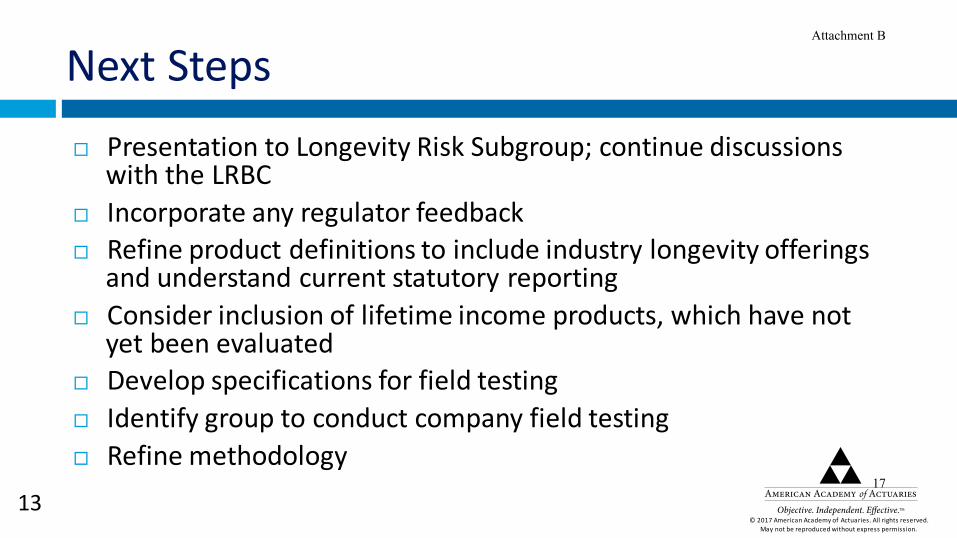

Next Steps Presentation to Longevity Risk Subgroup; continue discussions

with the LRBC Incorporate any regulator feedback Refine product definitions to include industry longevity offerings

and understand current statutory reporting Consider inclusion of lifetime income products, which have not

yet been evaluated Develop specifications for field testing Identify group to conduct company field testing Refine methodology

Attachment B

17

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

Historical Mortality Improvement Data

Appendix

Attachment B

18

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

15

HistoricalMale Average Median 85th % 85th/Avg 85th/50th 95th % 95th/Avg 95th/50th (95th - 85th)/Avg

Overall 0.79% 0.79% 1.31% 1.65 1.66 1.44% 1.82 1.82 0.17Age 35-64 1.09% 1.03% 1.64% 1.51 1.59 1.85% 1.70 1.80 0.20Age 65-84 0.74% 0.68% 1.28% 1.74 1.87 1.74% 2.36 2.54 0.63Age 85+ 0.40% 0.39% 0.76% 1.91 1.98 1.00% 2.51 2.59 0.59

Female Average Median 85th % 85th/Avg 85th/50th 95th % 95th/Avg 95th/50th (95th - 85th)/AvgOverall 0.98% 1.07% 1.53% 1.55 1.42 1.67% 1.70 1.55 0.15Age 35-64 1.43% 1.28% 2.23% 1.56 1.75 2.54% 1.78 1.99 0.22Age 65-84 1.04% 1.18% 1.61% 1.55 1.37 1.74% 1.67 1.47 0.12Age 85+ 0.60% 0.65% 1.17% 1.96 1.79 1.50% 2.50 2.29 0.54

Overall Average Median 85th % 85th/Avg 85th/50th 95th % 95th/Avg 95th/50th (95th - 85th)/AvgOverall 0.89% 0.91% 1.30% 1.46 1.43 1.41% 1.58 1.55 0.12Age 35-64 1.23% 1.28% 1.63% 1.33 1.28 1.83% 1.48 1.43 0.16Age 65-84 0.89% 0.96% 1.32% 1.48 1.37 1.37% 1.55 1.43 0.06Age 85+ 0.53% 0.46% 1.03% 1.96 2.26 1.23% 2.33 2.69 0.38

Normal ModelMale Average Median 85th % 85th/Avg 95th % 95th/Avg (95th - 85th)/Avg

Overall 0.79% 0.79% 1.24% 1.56 1.50% 1.89 0.33Age 35-64 1.09% 1.09% 1.61% 1.48 1.92% 1.77 0.28Age 65-84 0.74% 0.74% 1.29% 1.75 1.61% 2.19 0.44Age 85+ 0.40% 0.40% 0.77% 1.95 1.00% 2.50 0.56

Female Average Median 85th % 85th/Avg 95th % 95th/Avg (95th - 85th)/AvgOverall 0.98% 0.98% 1.49% 1.52 1.79% 1.82 0.30Age 35-64 1.43% 1.43% 2.04% 1.43 2.40% 1.68 0.25Age 65-84 1.04% 1.04% 1.59% 1.52 1.91% 1.83 0.31Age 85+ 0.60% 0.60% 1.16% 1.94 1.49% 2.49 0.55

Overall Average Median 85th % 85th/Avg 95th % 95th/Avg (95th - 85th)/AvgOverall 0.89% 0.89% 1.27% 1.420 1.49% 1.67 0.25Age 35-64 1.23% 1.23% 1.65% 1.34 1.89% 1.54 0.20Age 65-84 0.89% 0.89% 1.31% 1.47 1.56% 1.75 0.28Age 85+ 0.53% 0.53% 1.00% 1.89 1.28% 2.41 0.52

Data Table for 20 Yr Mortality Improvement Calibration

Improvement stress of 140% and 165% for 85th and 95th percentiles based on Overall Normal Model Results (net stress is 25%)

Improvement stress of 145% and 160% for 85th and 95th percentiles based on Historical Data (net stress is 15%)

Attachment B

19

© 2017 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

16

For more information Tricia Matson, MAAA, FSA Chairperson, Longevity Risk Task Force (LRTF) [email protected] Heather Jerbi Assistant Director of Public Policy American Academy of Actuaries [email protected]

Attachment B

20

2017 National Association of Insurance Commissioners

Capital Adequacy (E) Task Force RBC Proposal Form

[ ] Capital Adequacy (E) Task Force [ ] Health RBC (E) Working Group [ x ] Life RBC (E) Working Group

[ ] Catastrophe Risk (E) Subgroup [ ] Investment RBC (E) Working Group [ ] Operational Risk (E) Subgroup [ ] C3 Phase II/ AG43 (E/A) Subgroup [ ] P/C RBC (E) Working Group [ ] Stress Testing (E) Subgroup

DATE: 1/27/17

CONTACT PERSON: Paul Graham

TELEPHONE: (202) 624-2164

EMAIL ADDRESS: [email protected]

ON BEHALF OF:

NAME:

TITLE:

AFFILIATION: ACLI

ADDRESS: 101 Constitution Ave, NW

Washington, DC 20001

FOR NAIC USE ONLY

Agenda Item # 2017-02-L

Year 2017

DISPOSITION

[ ] ADOPTED

[ ] REJECTED

[ ] DEFERRED TO

[ ] REFERRED TO OTHER NAIC GROUP

[ X ] EXPOSED 1/27/17, 3/24/17

[ ] OTHER (SPECIFY)

IDENTIFICATION OF SOURCE AND FORM(S)/INSTRUCTIONS TO BE CHANGED

[ ] Health RBC Blanks [ ] Property/Casualty RBC Blanks [ x ] Life RBC Instructions

[ ] Fraternal RBC Blanks [ ] Health RBC Instructions [ ] Property/Casualty RBC Instructions [ ] Life RBC Blanks [ x ] Fraternal RBC Instructions [ ] OTHER ______________

DESCRIPTION OF CHANGE(S) The proposal includes changes to the instructions for LR031 Calculation of Authorized Control Level RBC and LR036 XXX/AXXX Reinsurance Primary Security Shortfall By Cession. This includes a column heading change to the LR036 schedule.

REASON OR JUSTIFICATION FOR CHANGE ** The proposal makes changes needed due to the adoption of the NAIC Term and Universal Life Insurance Reserve Financing Model Regulation.

Additional Staff Comments:

______________________________________________________________________________________________ ** This section must be completed on all forms. Revised 11-2013

1

Attachment C

21

This page intentionally left blank.

22

1

CALCULATION OF AUTHORIZED CONTROL LEVEL RISK-BASED CAPITAL LR031

The following instructions for the Calculation of Authorized Control Level Risk-Based Capital will remain effective independent of the status of the sunset provision, Section 8, of AG 48 in a particular state or jurisdiction. This instruction will be considered for change once the amendment referenced in AG 48, Section 8, regarding credit for reinsurance, is adopted by the NAIC. Basis of Factors The purpose of the formula is to estimate the risk-based capital levels required to manage losses that can be caused by a series of catastrophic financial events. However, it is remote that all such losses will occur simultaneously. The covariance adjustment states that the combined effect of the C–1o, C-1cs, C–2 and C–3 and a portion of the C-4 risks are not equal to their sum but are equal to the square root calculation described below. It is statistically assumed that the C–1o risk and a portion of the C–3 risk are correlated, while the C-1cs risk, the C–2 risk, the balance of the C-3 risk and a portion of the C-4 risk are independent of both. The split of the C-3 and C-4 risks allows for general consistency with the health RBC formula. This assumption provides a reasonable approximation of the capital requirements needed at any particular level of losses. Authorized Control Level Risk-Based Capital is 50 percent of the sum of items A plus B where: ”A” equals C-0 plus the C–4a risk-based capital and the square root of the sum of the C–1o and C–3a risk-based capital squared, the C-1cs and C-3c risk-based capital squared, the C–2 risk-based capital squared, the C-3b risk-based capital squared and the C-4b risk-based capital squared and, “B” equals the greater of zero and the amount of Primary Security shortfalls for all cessions covered by Actuarial Guideline XLVIII (AG 48) multiplied by two. The intent of this addend is to produce a dollar for dollar increase in the Authorized Control Level for the total of the AG 48 Primary Security shortfall. This Authorized Control Level increase for the amount of Primary Security shortfall applies to all insurers and all XXX/AXXX cessions of Covered Policies as defined in AG 48, that do not fall within an exemption set forth in AG 48, regardless of whether a state may have chosen to waive all or part of AG 48. For example, if a cession is of Covered Policies and no exemption is available under the terms of AG 48 for a particular insurer or transaction, but a state nevertheless determines that the insurer or Appointed Actuary will not be required to comply in full with the Guideline, then for RBC a computation of shortfall, if any, will still be required and an increase to Authorized Control Level for any such shortfall will still apply. This calculation is not required for cessions covered by the state equivalent of the NAIC Term and Universal Life Insurance Reserve Financing Model Regulation (Model #787) so long as the state equivalent regulation has the following similarities to Model #787: the same definition of Primary Security, the same definition of Required Level of Primary Security, the same definition of Covered Policies, the same Exemptions (Section 4), the same Actuarial Method (Section 6), and the same requirement that cessions without sufficient Primary Security and Other Security (Sections 7A3 and 7A4) must directly establish a liability for the difference between the credit for reinsurance taken and the actual Primary Security held. The information reported should be consistent with the information that will be included in Part 2B, Columns 13, 14, 15, and 19, of the annual statement Supplemental Term and Universal Life Insurance Reinsurance Exhibit. Mandatory Control Level Risk-Based Capital is 70 percent of Authorized Control Level Risk-Based Capital. Specific Instructions for Application of the Formula All amounts reflected for the calculation of Authorized Control Level Risk-Based Capital will be calculated automatically by the software. In recognition of the exclusion of the carrying value of Alien Insurance Subsidiaries – Other from Total Adjusted Capital, the carrying value of these entities is also to be excluded from the calculation of C-O risk-based capital.

2

Attachment C

23

1

XXX/AXXX REINSURANCE PRIMARY SECURITY SHORTFALL BY CESSION

LR036 The following instructions for the XXX/AXXX Reinsurance Primary Security Shortfall by Cession will remain effective independent of the status of the sunset provision, Section 8, of AG 48 in a particular state or jurisdiction. This instruction will be considered for change once the amendment referenced in AG 48, Section 8, regarding credit for reinsurance, is adopted by the NAIC. The information reported for this RBC schedule should be consistent with the information that will be included in Part 2B, Columns 13, 14, 15, and 19 of the annual statement Supplemental XXX/AXXX Term and Universal Life Reinsurance Exhibit. Cessions shall be reported on a treaty by treaty basis. The terms below shall have the following definitions for the purposes of Part 1-4 of this Supplemental XXX/AXXX Reinsurance Exhibit this RBC Schedule:

A. Actuarial Method: The methodology used to determine the Required Level of Primary Security, as described in Section 5 of AG 48.

B. Covered Policies: Subject to the exemptions described in Section 3 of AG 48, Covered Policies are those policies that are required to be valued under Sections 6 or 7 of the NAIC Valuation of Life Insurance Policies Model Regulation Model 830 (Model 830) and that have risk ceded to an assuming insurer; of the following policy types: (1) life insurance policies with guaranteed nonlevel gross premiums and/or guaranteed nonlevel benefits, except for flexible premium universal life insurance policies or (2) flexible premium universal life insurance policies with provisions resulting in the ability of a policyholder to keep a policy in force over a secondary guarantee period; provided, however, that Covered Policies shall not include policies that were both (1) issued prior to 1/1/2015 and (2) ceded so that they were part of a reinsurance arrangement, as of 12/31/2014, that would not qualify for exemption as described in Section 3 of AG 48.

C. Required Level of Primary Security: The dollar amount determined by applying the Actuarial Method to the risks ceded with respect to Covered Policies, but not more

than the total reserve ceded.

D. Primary Security: The following forms of security:

1. Cash meeting the requirements of Section 3.A. of the NAIC Credit for Reinsurance Model Law (Model 785);

2. SVO-listed securities meeting the requirements of Section 3.B. of Model 785, but excluding any synthetic letter of credit, contingent note, credit-linked note or other similar security that operates in a manner similar to a letter of credit, and excluding any securities issued by the ceding insurer or any of its affiliates; and

3. For security held in connection with funds-withheld and modified coinsurance reinsurance arrangements:

a. Commercial loans in good standing of CM3 quality and higher;

b. Policy Loans; and

c. Derivatives acquired in the normal course and used to support and hedge liabilities pertaining to the actual risks in the policies ceded pursuant to the

reinsurance arrangementtreaty.

4

Attachment C

24

2

Column 1 – Cession ID

Enter a unique Cession ID for each line (01 – 99). Column 2 – NAIC Company Code

Provide the NAIC code of the assuming insurer. Column 3 – ID Number

Enter one of the following as appropriate for the assuming insurer being reported on the schedule. See the Schedule S General Instructions for more information on these identification numbers.

Federal Employer Identification Number (FEIN) Alien Insurer Identification Number (AIIN) Certified Reinsurer Identification Number (CRIN)

Column 4 – Name of Company

Provide the name of the assuming insurer. Column 5 – Required Level of Primary Security

State the Required Level of Primary Security applicable to the statutory policy reserves as of the current annual statement date. Column 6 – Primary Security and Primary Security Remediation Adjustment

Reflect the values as of the current annual statement date of the Primary Security as defined in D. above held by or on behalf of the reporting entity. Also reflect any amounts qualifying as Primary Security Adjustments as defined in AG 48, Section 6.A.3.(i) Remediation Adjustment established after the annual statement date as provided for in AG 48, Section 6.B.1: 1. Additional Primary Security added on or before March 1 of the year in which the actuarial opinion is being filed held by or on behalf of the ceding insurer, as

security under the reinsurance contractcession, on a funds withheld, Trust, or modified coinsurance basis; or 2. Any liability established equal to some or all of the difference between the Primary Security held pursuant to AG 48, Section 6.A.1.(i) and the Required

Level of Primary Security.

Column 7 – Primary Security Shortfall

For a given cession the Column 7 Primary Security Shortfall equals the greater of (a) zero and (b) Column 5 Required Level of Primary Security less Column 6 Primary Security and Primary Security Remediation Adjustment. The total for line (9999999) will be doubled and added to line (68) of LR031 Calculation of Authorized Control Level Risk-Based Capital. The adjustment will result in a dollar for dollar increase in Authorized Control Level for the total of all primary security shortfalls.

5

Attachment C

25

XXX/AXXX REINSURANCE PRIMARY SECURITY SHORTFALL BY CESSION

(1) (2) (3) (4) (5) (6) (7)

Cession ID

NAIC Company

Code ID Number Name of Company

Required Level of Primary Security

Primary Security and Primary

Security Remediation Adjustment

Primary Security Shortfall

(0000001)(0000002)(0000003)(0000004)(0000005)(0000006)(0000007)(0000008)(0000009)(0000010)(0000011)(0000012)(0000013)(0000014)(0000015)(0000016)(0000017)(0000018)(0000019)(0000020)

(9999999)

Denotes items that must be manually entered on the filing software.

6

Attachment C

26

2016 National Association of Insurance Commissioners

Capital Adequacy (E) Task Force RBC Proposal Form

[ X ] Capital Adequacy (E) Task Force [ ] Health RBC (E) Working Group [ X ] Life RBC (E) Working Group

[ ] Catastrophe Risk (E) Subgroup [ ] Investment RBC (E) Working Group [ ] Operational Risk (E) Subgroup [ ] C3 Phase II/ AG43 (E/A) Subgroup [ ] P/C RBC (E) Working Group [ ] Stress Testing (E) Subgroup

DATE: June 7, 2016

CONTACT PERSON: John Bruins

TELEPHONE: (202) 624-2169

EMAIL ADDRESS: [email protected]

ON BEHALF OF: ACLI

NAME: John Bruins

TITLE: VP & Senior Actuary

AFFILIATION: ACLI

ADDRESS: 101 Constitution Ave, NW

Washington, DC 20001

FOR NAIC USE ONLY

Agenda Item #

Year

DISPOSITION

[ ] ADOPTED

[ ] REJECTED

[ ] DEFERRED TO

[ ] REFERRED TO OTHER NAIC GROUP

[ ] EXPOSED

[ ] OTHER (SPECIFY)

IDENTIFICATION OF SOURCE AND FORM(S)/INSTRUCTIONS TO BE CHANGED

[ ] Health RBC Blanks [ ] Property/Casualty RBC Blanks [ ] Life RBC Instructions

[ X ] Fraternal RBC Blanks [ ] Health RBC Instructions [ ] Property/Casualty RBC Instructions [ X ] Life RBC Blanks [ ] Fraternal RBC Instructions [ ] OTHER ______________

DESCRIPTION OF CHANGE(S) Life RBC currently has a C-0 charge for collateral held for FHLB advances of 1.30% computed on LR017. ACLI proposes that this be changed to be 0 for the collateral equal to the amount advanced, and a factor based on the risk of the FHLB for any excess collateral. Attached as Appendix B is a mark-up of LR017 and Appendix C outlines the instructions to show the specific changes needed.

REASON OR JUSTIFICATION FOR CHANGE ** A detailed description of this proposal and the background is included as Appendix A This proposal is specific to Life RBC. Health and P&C insurers may be FHLB members, and the RBC formulas may have parallel issues for which a parallel change may be appropriate. This proposal also references where FHLB advances are included in the C-3 component, which is unique to Life RBC.

Additional Staff Comments:

______________________________________________________________________________________________ ** This section must be completed on all forms. Revised 11-2013

Attachment D

27

This page intentionally left blank.

28

Appendix A

2

Federal Home Loan Bank Pledged Asset RBC Proposal Executive Summary: When an insurer obtains an advance from a Federal Home Loan Bank (FHLB), collateral is posted using assets from the insurer’s balance sheet. The pledged assets remain on the insurer’s balance sheet and generate an RBC amount based on the credit risk of that asset. The advance may be recorded as either borrowing (Liability, Page 3 Line 20) or as a Funding Agreement (Exhibit 7 – Deposit type contracts). It is generally included in the insurer’s C-3 modeling to generate an RBC amount for asset – liability mismatch. Additionally, since these assets are classified as ‘Non-controlled assets’, there is an RBC factor of 1.3% applied to the collateral in addition to any other RBC amounts for those assets and liabilities. This memo outlines a proposal that this ‘Non-controlled assets’ charge be revised in light of the risks and the other components of RBC. Specifically, we propose that there be a factor of zero for the collateral up to the amount of the advance, and a factor for the excess collateral that is equal to the C-1 Bond factor based on the credit rating of the FHLB. FHLBs and Insurance Companies As participants in the mortgage investment industry, many insurance companies have formed a synergistic relationship with the FHLB. The companies can become members of their local FHLB after satisfying underwriting review, demonstrating housing and mortgage market involvement and support, and purchasing membership stock. As members, they have access to FHLB funding and other banking products and receive dividend returns on the stock. The FHLB system’s mandate is to provide liquidity and promote stability in the mortgage industry by providing cost effective products to its members. As federally chartered, government-sponsored banking cooperatives, the FHLBs are able to access the capital markets at extremely favorable interest rates and are thus able to offer attractive rates to their members. FHLB products provide insurers with a diversified low-cost form of funding, with flexible structuring terms to match their investment funding and capital structuring needs. The programs can be an important and stable source of liquidity for many life insurers even during uncertain economic times. In order to keep funding costs for its members low, the FHLBs mitigate their overall credit risk by lending only on a secured basis. Members are required to pledge assets as collateral to secure their outstanding obligations. Given their specialized expertise in mortgage assets, the FHLBs can even accept as collateral life insurer commercial mortgage loans, which tend to be less liquid and not suitable for other collateral purposes. The collateral is managed, not as specific assets backing any single obligation, but rather as a substitutable collateral pool managed in aggregate. All beneficial interests (investment income, gains/losses on sales, etc) remain with insurers and the assets remain available for the insurers’ use as long as the minimum collateral levels are sustained. These characteristics increase the insurer’s liquidity by freeing up other assets for general liquidity purposes and diversifying its sources and uses of liquidity. Finally, advances from the FHLB are generally pre-payable. It is beneficial to insurers’ long-term economic strength as well as their short- and long- term liquidity, to be able to prudently utilize FHLB products, without punitive risk capital charges. The risk charges

Attachment D

29

Appendix A

3

should recognize the relative risks inherent in the funding and the low counterparty risk of the FHLBs, as well as the pooled and unrestricted nature of the collateral pledged. FHLBs are strong counterparties The FHLB system was established in 1932 and has been making advances to savings and loans, banks, and insurance companies for over 80 years. Unlike commercial lenders that tend to restrict advances when faced with tight liquidity markets, the FHLBs, as government-sponsored enterprises (GSEs), maintain access to the global capital markets and are able to continue making advances to their members across business cycles. During the global liquidity crisis that peaked in 2008, insurance company members increased advances from $28.7 billion in 2007 to $54.9 billion in 2008. FHLBs have implicit US government support, are regulated by the Federal Housing Finance Agency, and are highly rated by the rating agencies. The FHLBs also have a unique structure whereby its borrowers are also its stockholders, leading to a strong alignment of interests. The counterparty risk associated with pledging assets to the FHLBs is minimal. Insurers’ Usage of Federal Home Loan Bank (FHLB) Programs In general, insurers use FHLB funding to provide funding for spread lending purposes or to support general business operations. When used for spread lending purposes, the liabilities are matched by a suitable portfolio of invested assets in order to earn a spread return as an integral part of its insurance business activities. The nature of these two activities is different, as was recognized by the NAIC Emerging Accounting Issues (E) Working Group when it issued INT 08-081. SSAP 52 requires that funding used for spread lending purposes is in substance similar to other insurance activities and should be treated as a funding agreement and reported in the statutory financial statements as an insurance liability whose activity is subject to risk management practices, such as asset-liability management and cash-flow testing adequacy. This is consistent with how rating agencies view FHLB funding agreements; rating agencies treat this form of funding as operating leverage rather than financial leverage. Since the primary risk for this use is the asset liability mismatch, which is being measured by the C-3 component of RBC, the ‘non-controlled asset’ RBC charge is an excess and redundant charge. The FHLBs provide flexible structures that allow insurers to tailor the funding products to better match the characteristics of asset portfolios. Common structures range from overnight and short-term advances to term advances with maturities out to 15 years. Interest crediting options include adjustable rates, with periodic call options without prepayment penalty, or fixed rates with option to amortize. Certain FHLBs also allow for partial terminations of contracts. Such optionality is important to investors in mortgage related assets which often exhibit variability in cash flows.

1 This INT was subsequently nullified, and the guidance incorporates directly into SSAPs 15, 50, and 52.

Attachment D

30

Appendix A

4

SSAP 15 requires that when FHLB advances are used to support general business operations, it is in substance a form of debt financing and is required to be reported as borrowed money. Because these liabilities are not necessarily matched by a specific pool of assets, the risk of default may not be mitigated by the insurers’ typical asset-liability management processes. Rather, repayment of the obligations depends on the residual cash flows of the insurer, like other forms of debt financing. FHLB Programs can Enhance Financial Strength of Insurers The prudent usage of FHLB products can enhance the immediate and on-going financial strength of the company, by providing low cost and flexible funding to match insurers’ investment management and capital structuring needs. The rating agencies acknowledge this benefit in their reviews of insurer financial strength. See recent rating agency comments in the Appendix below. The new annual statement disclosures help regulators and other financial statement users understand how an insurer is using and managing its FHLB business. Even if the insurer enters rehabilitation, the FHLBs have demonstrated in the past a willingness to work with the insurers and rehabilitators, to reach a successful outcome that involved no loss to either the guaranty association or the FHLB in connection with the insurers’ obligations. Multiple-tier Risk Based Capital (RBC) structure FHLB obligations, and the associated collateral, generate RBC amounts in three different parts of the RBC formula. Assets that are pledged as collateral remain as part of the insurer’s balance sheet and are assessed an RBC charge for C-1 asset risk. The fact that the assets are pledged as collateral does not remove them from this requirement, and the insurer continues to have the risk of a reduction in value of these assets. Risks associated with specific liability characteristics and asset-liability mismatches flow through the C-3 risk charges and the associated C3P1 scenario analyses usually in the following categories:

• Deposit-Type Contract liabilities based the risk classification of each liability: 77-115 bps (low risk); 154-231 bps (medium risk); 308-462 bps (high risk)

• Debt with GIC-like characteristics: 308-462 bps (high risk)

The assets pledged as collateral are also reported as a non-controlled asset within General Interrogatory 25, and they receive an additional 1.30% RBC charge similar to many other non-controlled asset items. However most other items reported through Interrogatory 25, such as assets loaned to others under securities lending programs, repurchase and reverse repurchase agreements, are not necessarily subject to the asset-liability risk management practices discussed above, do not allow the insurer to freely substitute the collateral, do not provide options to prepay the liabilities to release the collateral or do not have a GSE quality counterparty.

Attachment D

31

Appendix A

5

Certain categories of non-controlled assets do receive a lower RBC charge. Securities lending programs that conform to appropriate operational and investment risk guidelines are assessed a 0.2% ‘non-controlled asset’ risk charge. The guidelines for conforming programs recognize that such programs are designed to match the liabilities with a suitable portfolio of invested assets. The lower charge reflects the reduction in risk to the pledged assets from risk of default on the securities lending transactions. In another example, assets pledged under the federal TALF program receive a zero ‘non-controlled asset’ risk charge. Certain rating agencies have recognized the relatively lower risks for assets pledged in support of FHLB advances. S&P’s capital model has a non-controlled asset risk charge but assets pledged as collateral to the FHLB are specifically excluded from that charge. Assessing a high risk charge of 1.3% on FHLB pledged assets makes it more costly for insurers to access this low cost and flexible funding source and constrains their sources of liquidity by forcing them to move away from pledging more illiquid assets with higher haircuts and creating competition for uses of liquid assets, particularly in light of the new Dodd-Frank regulations. Excess collateral is defined to be the amount of pledged collateral greater than the FHLB advance. Since collateral equal to the liability poses no net financial risk to the insurer, we propose that the collateral equal to the FHLB advance have an RBC factor of zero. An argument can be made that any collateral in excess of the FHLB advance does have an additional risk based on the credit standing of the FHLB that is holding the collateral. We propose that this excess amount be assessed an RBC factor based on the credit standing of the FHLB. The excess amount could be calculated as the aggregate book value of FHLB pledged assets less the aggregate book value of FHLB advances. Other “Non-controlled Assets” To understand the context of this proposal, discussion of RBC for non-controlled assets was raised at the NAIC Capital Adequacy Task Force in October of 2012. Based on a regulatory review of insurer balance sheets, concern was expressed about companies having excessive amounts of restricted or non-controlled assets. Industry has worked with regulators and several actions have occurred.

• The NAIC established a working group under SAPWG to design additional disclosures about non-controlled assets. These resulted in the Interrogatory 25 disclosures discussed above.

• Information was provided regarding the non-controlled assets relating to reinsurance, and why such arrangements did not create any additional risk

• Educational material has been developed and presented to regulators about the repurchase and reverse repurchase agreements.

• RBC for collateral on conforming Securities Lending programs was revised to 20 bps • ACLI identified FHLB collateral as an issue of concern and has worked with its members to

develop this proposal

Attachment D

32

Appendix A

6

Appendix: Rating Agency comments on Insurers’ FHLB membership Moody’s Investor Service, Sector Comment, June 25, 2015 “Insurers’ Access to Federal Home Loan Banks Lending Capacity is Credit Positive”

“» Access to an alternative, low-cost funding source is credit positive. The FHLBs offer eligible insurers access to low-cost, collateralized borrowing capacity for both their ordinary operating needs and emergency liquidity. This availability is credit positive for insurers when traditional bank credit facilities and the capital markets are no longer available, are unfavorable, or are tapped out. The ability to use less-liquid mortgage related assets on the balance sheet as collateral reduces potential pressure on operating liquidity. » Injudicious or excessive use of FHLB borrowing is credit negative - Poorly duration and/or cash-matched assets against FHLB advances (i.e., for acquisitions or spread lending) and/or borrowing that materially increases a company’s financial leverage or credit risk will increase the insurer's risk profile. In addition, because secured obligations to the FHLB structurally subordinate unsecured policyholders, these borrowings could put downward pressure on a company's ratings if they become too sizable relative to total policyholder liabilities. However, we do not expect this to happen.”

Fitch Ratings Special Report, June 12, 2013 “FHLB's Growing Role in the U.S. Life Insurance Industry”

“Membership in the Federal Home Loan Bank (FHLB) system can enhance liquidity and financial flexibility for insurance companies, particularly those insurers with limited access to capital markets, according to a new report by Fitch Ratings. Further, many life insurers can make use of FHLB advances (loans) as a reasonable low cost source of funds to produce spread income, if done in a controlled manner.”

A.M. Best’s Ratings Methodology, January 12, 2012 “A.M. Best’s Perspective on Operating Leverage”

“FHLB programs provide financial flexibility for insurance company members and are an attractive source of capital due to the low rate offered for advances.”

S&P Ratings Direct, May 15, 2013 “How Federal Home Loan Bank Funding Figures in Ratings on Insurers”

“All else being equal, a company that prudently manages its capital structure, investments underwriting, and risk management can enhance its financial flexibility from FHLB capital funding” “We believe the FHLB will be able to meet members’ borrowing needs during the next market dislocation, providing relatively inexpensive funding for illiquid assets when members have few funding alternatives… in our view, pledged liquid assets would damage the stressed liquidity ratio, whereas pledged illiquid assets do not harm the stressed ratio.”

Attachment D

33

This page intentionally left blank.

34

Appendix B

7

OFF-BALANCE SHEET AND OTHER ITEMS

(1)

(2)

(3)

(4)

(5) (6)

Less Noncontrolled

Assets Funding

Guaranteed

Separate Accounts

RBC Yes/No

Annual Statement Source

Statement Value

or Synthetic GIC's

Subtotal

Factor

Requirement Response

Noncontrolled Assets

(1) Loaned to Others - Conforming Securities General Interrogatories Part 1 Line 24.05

X 0.002 =

Lending Program

(2) Loaned to Others - Securities Lending General Interrogatories Part 1 Line 24.06

X 0.013 =

Programs - Other

(3) Subject to Repurchase Agreements General Interrogatories Part 1 Line 25.21

X 0.013 = (4) Subject to Reverse Repurchase Agreements General Interrogatories Part 1 Line 25.22

X 0.013 =

(5) Subject to Dollar Repurchase Agreements General Interrogatories Part 1 Line 25.23

X 0.013 = (6) Subject to Reverse Dollar Repurchase General Interrogatories Part 1 Line 25.24

X 0.013 =

Agreements

(7) Placed Under Option Agreements General Interrogatories Part 1 Line 25.25

X 0.013 =

(8) Letter Stock or Other Securities Restricted as to sale - excluding FHLB Capital Stock General Interrogatories Part 1 Line 25.26

X 0.013 =

(9) FHLB Capital Stock General Interrogatories Part 1 Line 25.27

X 0.013 = (10) On Deposit with States General Interrogatories Part 1 Line 25.28

X 0.013 =

(11) On Deposit with Other Regulatory Bodies General Interrogatories Part 1 Line 25.29

X 0.013 =

(12.1) Pledged as Collateral - excluding Collateral Pledged to an FHLB General Interrogatories Part 1 Line 25.30

(12.2) Less Derivative Collateral Pledged

Schedule DB Part D Section 2 Column 7, Line 0199999

X 0.004 =

(12.3)

Pledged as Collateral - excluding Collateral Pledged to an FHLB Less Derivatives Collateral Pledged Line (12.1) - (12.2)

X 0.013 =

(13)

Pledged as Collateral to FHLB including Assets Backing Funding Agreements General Interrogatories Part 1 Line 25.31

† X 0.00413# =

(14) Other General Interrogatories Part 1 Line 25.32

X 0.013 =

(15) Total Noncontrolled Assets

Sum of Lines (1) through (11) Plus Lines (12.3) through (14)

Derivative Instruments

Attachment D

35

Appendix B

8

(16) Exchange Traded and Centrally Cleared Schedule DB Part D Section 1 Column 12, Line 0999999, in part

X 0.004 =

(17) Off-Balance Sheet Exposure NAIC 1

Schedule DB Part D Section 1 Column 12, Line 0999999, in part

X 0.004 =

(18) Off-Balance Sheet Exposure NAIC 2

Schedule DB Part D Section 1 Column 12, Line 0999999, in part

X 0.013 =

(19) Off-Balance Sheet Exposure NAIC 3

Schedule DB Part D Section 1 Column 12, Line 0999999, in part

X 0.046 =

(20) Off-Balance Sheet Exposure NAIC 4

Schedule DB Part D Section 1 Column 12, Line 0999999, in part

X 0.100 =

(21) Off-Balance Sheet Exposure NAIC 5

Schedule DB Part D Section 1 Column 12, Line 0999999, in part

X 0.230 =

(22) Off-Balance Sheet Exposure NAIC 6

Schedule DB Part D Section 1 Column 12, Line 0999999, in part

X 0.300 =

(23) Total Derivative Instruments Off-Balance

Sheet Exposure Sum of Lines (16) through (22)

(24) Guarantees for Affiliates

Notes to Financial Statements Number 14A3c1

X 0.013 =

(25) Contingent Liabilities Notes to Financial Statements Number 14A1

X 0.013 =

(26) Long Term Leases Notes to Financial Statements Number 15A2a1

X 0.000 =

(27) Total Off-Balance Sheet Items Lines (15) + (23) + (24) + (25) + (26)

(pre-MODCO/Funds Withheld)

(28) Reduction in RBC for MODCO/Funds Withheld

Reinsurance Ceded Agreements Company Records (enter a pre-tax amount)

(29) Increase in RBC for MODCO/Funds Withheld

Reinsurance Assumed Agreements Company Records (enter a pre-tax amount)

(30) Total Off-Balance Sheet Items

(including MODCO/Funds Withheld.) Lines (27) - (28) + (29)

Other Items (31) Is the entity responsible for filing the U.S. "Yes", "No" or "N/A" in Column (6)

Federal income tax return for the reporting

insurer a regulated insurance company? (32) SSAP No. 101 Paragraph 11a Deferred Tax Assets Notes to Financial Statements Item 9A2(a)

X ‡ =

(33) SSAP No. 101 Paragraph 11b Deferred Tax Assets Notes to Financial Statements Item 9A2(b)

X 0.010 =

(34) Total Off-Balance Sheet and Other Items Line (30) + Line (32) + Line (33)

Attachment D

36

Appendix B

9

†

For Column (2) Line (13), include assets pledged as collateral other than assets related to the Federal Reserve’s Term Asset Loan Facility (TALF). For Column (2) include assets on deposit with an FHLB but not associated with a Funded Advance. For Column (2) also include assets pledged as collateral on FHLB Funded Advance Liabilities subject to C3 Asset/Liability Cash Flow Synchronization Testing, limited to the Statement Value of FHLB Liabilities Subject to C3 Testing.

‡

If Line (31) Column (6) is "Yes", then the factor is 0.005. If Line (31) Column (6) is "No", then the factor is 0.010. If Line (31) Column (6) is "N/A", then the factor is 0.000.

#

Apply a factor based on the NAIC ratings category equivalent to an unsecured debt obligation of the FHLB.

Denotes items that must be manually entered on the filing software.

Attachment D

37

Appendix C

© 1993-2015 National Association of Insurance Commissioners 10 8/28/2015

OFF-BALANCE SHEET AND OTHER ITEMS LR017

Basis of Factors The potential for risk exists in off-balance sheet items. For items other than derivative instruments and assets pledged as collateral to the Federal Home Loan Bank, a 1.3 percent factor was chosen on a judgment basis. The 1.3 percent pre-tax factor will differentiate between the companies that have small and large exposures to this risk. Since there is no firm actuarial basis for assigning the 1.3 percent pre-tax factor to these risks, off-balance sheet items are included in the sensitivity analysis using a factor of 3 percent, and leases are added as an additional off-balance sheet item. For securities lending programs, a reduced charge may apply to certain programs that meet the criteria as outlined below. For assets pledged as collateral on funded Federal Home Loan Bank (FHLB) liabilities included in the C3 Asset/Liability Cash Flow Synchronization Testing at LR027, the C3 calculation already provides adequate provision for potential risks up to the Statement Value of the associated FHLB liabilities tested therein. For any excess of assets pledged as collateral above this Statement Value (FHLB liabilities included in the C3 assessment) the potential exposure is proportionate to the credit risk assessed for the FHLB counterparty, making the bond factor associated with the NAIC designation assigned to the FHLB an appropriate risk provision. Assets on deposit with an FHLB but not associated with a Funded Advance, which can be recalled at will by the reporting entity, do not present non-controlled asset risk and should be excluded. For derivative instruments, the book/adjusted carrying value exposure net of collateral (the balance sheet exposure) is included under miscellaneous C-1o risks. Because collars, swaps, forwards and futures can have book/adjusted carrying values that are positive, zero or negative, the potential exposure to default by the counterparty or exchange for these instruments cannot be measured by the book/adjusted carrying values. Schedule DB, therefore, includes a calculation of the potential exposure that is based on the March 1987 research paper “Potential Credit Exposure on Interest Rate and Foreign Exchange Rate Related Instruments,” supporting the 1988 Bank of International Settlements framework for banks. The off-balance sheet exposure (Schedule DB, Part D, Section 1, Column 12) will measure this potential exposure for risk-based capital purposes. The factors applied to the derivatives off-balance sheet exposure are the same as those applied to bonds. Specific Instructions for Application of the Formula Column (2) Assets directly funding guaranteed separate accounts or synthetic GIC contracts should be excluded from the noncontrolled assets computation. Line (1) Securities lending programs that have all of the following elements are eligible for a lower off-balance sheet charge:

1. A written plan adopted by the Board of Directors that outlines the extent to which the insurer can engage in securities lending activities and how cash collateral received will be invested.

2. Written operational procedures to monitor and control the risks associated with securities lending. Safeguards to be addressed should, at a minimum, provide assurance of the following:

Attachment D

38

Appendix C

© 1993-2015 National Association of Insurance Commissioners 11 8/28/2015

a. Documented investment guidelines, including, where applicable, those between lender and investment manager with established procedure for review of compliance.

b. Investment guidelines for cash collateral that clearly delineate liquidity, diversification, credit quality, and average life/duration requirements. c. Approved borrower lists and loan limits to allow for adequate diversification. d. Holding excess collateral with margin percentages in line with industry standards, which are currently 102% (or 105% for cross currency loans). e. Daily mark-to-market of lent securities and obtaining additional collateral needed to ensure that collateral at all times exceeds the value of the loans to

maintain margin of 102% of market. f. Not subject to any automatic stay in bankruptcy and may be closed out and terminated immediately upon the bankruptcy of any party.

3. A binding securities lending agreement (standard “Master Lending Agreement” from Securities Industry and Financial Markets Association) is in writing between the insurer, or its agent on behalf of the insurer, and the borrowers.

4. Acceptable collateral is defined as cash, cash equivalents, direct obligations of, or securities that are fully guaranteed as to principal and interest by, the government of the United States or any agency of the United States, or by the Federal National Mortgage Association or the Federal Home Loan Mortgage Corporation and NAIC 1-designated securities. Affiliate-issued collateral would not be deemed acceptable. In all cases the collateral held must be permitted investments in the state of domicile for the respective insurer.

Collateral included in General Interrogatories, Part 1, Line 24.05 of the annual statement should be included on Line (1).

Line (2) Collateral from all other securities lending programs should be reported General Interrogatories, Part 1, Line 24.06 and included in Line (2). Lines (3) through (14) Noncontrolled assets are the amount of all assets not exclusively under the control of the company, or assets that have been sold or transferred subject to a put option contract currently in force. For Line (12.1) and (13) include assets pledged as collateral reported in the General Interrogatories Part 1 Line 25.30 and 25.31 other than assets related to the Federal Reserve’s Term Asset Loan Facility (TALF). For Line (12.2), include all collateral pledged, both cash and securities, to derivative counterparties and/or central clearinghouses for initial margin and variation margin. In addition, include securities collateral pledged as initial margin for futures. Line (12.2) should agree to Schedule DB Part D Section 2 Column 7, Line 0199999. Line (12.3) should equal Line (12.1) minus Line (12.2). For Line (13) column 2 include the amount of collateral equal to the FHLB Liabilities subject to C-3 testing and included in LR027. In addition, any collateral in excess of required collateral should be included. Lines (16) through (23) The off-balance sheet exposure for derivative instruments reported on Schedule DB, Part D, Section 1, Column 12, Lines 0199999 through 0899999. Off-balance sheet exposure is reported for aggregate exchange traded derivatives, OTC – bilateral derivatives aggregated by counterparty brought into each individual NAIC designation 1-6, and aggregated centrally cleared derivatives. For 2015, derivative balances subject to central clearing are to be included in Line (16) regardless of the category they are included in for Schedule DB, Part D, Section 1. Line (24) Guarantees for affiliates include guarantees for the benefit of an affiliate that result in a material† contingent exposure of the company’s assets to liability.

Attachment D

39

Appendix C

© 1993-2015 National Association of Insurance Commissioners 12 8/28/2015

Line (26) The exposure amount for long-term leases is the annual rental amount of all leases that could have a material† financial effect. If the rent expense is shared with affiliates, it should be allocated by company. Line (31) “Yes” means the entity which files the US Federal income tax return which includes the reporting entity is a regulated insurance company (including where the reporting entity is the direct filer of the tax return). “No” means the entity which files the US Federal income tax return which includes the reporting entity is not a regulated insurance company (e.g. a non-insurance entity or holding company makes the filing). “N/A” means the entity is exempt from filing a US federal income tax return; lines (32) and (33) should be zero in this case. Lines (32) and (33) Apply a one-percent (1%) charge in the RBC formula, placed outside of the covariance adjustment, to admitted adjusted gross deferred tax assets (DTAs) as described in SSAP No. 101, paragraphs 11a and 11b (lesser of paragraph 11b(i) and 11b(ii)). For the period for which the paragraph 11a component is determined, the charge is reduced to one-half percent (0.5%) when the insurance company either filed its own separate Federal income tax return or it was included in a consolidated Federal income tax of which the common parent is an insurance company. The source for the DTA amounts to use in the calculation is found in the Annual Statement, Notes to Financial Statements, Note 9, Part A, Section 2, Admission Calculation Components for SSAP No. 101. Paragraph 11a is found in Section 2, subpart (a), Paragraph 11b is found in Section 2, subpart (b). † The definition of “material” exposure or financial effect is the same as for annual statement disclosure requirements.

Attachment D

40

Priority 1 – High priority LIFE RISK-BASED CAPITAL (E) WORKING GROUPPriority 2 – Medium priority WORKING AGENDA ITEMS FOR CALENDAR YEAR 2017Priority 3 – Low priority

Expected2017 2017 Completion

# Owner Priority Date Working Agenda Item Source Comments

Ongoing Items – Life RBC1 Life RBC

WGOngoing Ongoing Make technical corrections to Life RBC instructions, blank and /or methods to

provide for consistent treatment among asset types and among the various components of the RBC calculations for a single asset type.

2 Life RBC WG

1 2017 or later Evaluate RBC in light of PBR. Consider changes to RBC needed because of the changes in reserve values, including “right sizing” of reserves, margins in the reserves, any expected increase in reserve volatility, and the overall desired level of solvency measurement and other issues. Consider a total balance sheet approach (e.g. total asset requirement (TAR) type calculation and then subtracting out the PBR reserves) and application of stress scenarios. These charges should include appropriate consideration of international core principles.

Referral from PBR Implementation (E)

Task Force

Being addressed by the Stress Testing (E) Subgroup

3 Life RBC WG

1 2017 or later Evaluate the overall effectiveness of the C3 Phase 2 and AG 43 methodologies by conducting an in-depth analysis of the models, modeling assumptions, processes, supporting documentation and results of a sample of companies writing variable annuities with guarantees and to make recommendations to the Capital Adequacy Task Force or Life Actuarial Task Force on any changes to the methodologies to improve their overall effectiveness.

CATF Being addressed by the C-3 Phase II/AG43 (E/A)

Subgroup

4 Life RBC WG

1 2017 or later Providerecommendationsforrecognizinglongevityriskinstatutoryreservesand/orRBC,asappropriate.

NewJersey Being addressed by the Longevity (E/A) Subgroup

Carry-Over Items Currently being Addressed – Life RBC5 Life RBC

WG1 2017 or later Update the current C-3 Phase I or C-3 Phase II methodology to include indexed

annuitiesAAA

6 LifeRBCWG

1 2017 or later Considerpropertreatmentforbusinesscededtounauthorizedreinsurers.Currently,inmostcasessometypeofsecurityisrequiredforreservesthatarecededtounauthorizedreinsurersbutthereisnosimilarhandlingofRBC.AnotheroptioncouldbeafactorappliedtotheRBCreleaseorsomeotherbase.

NewYork NewYork,FloridaandConnecticutareworkingonthisandplantosubmitsomethingfortheWorkingGrouptoconsider.

7 LifeRBCWG

2 2017 Developguidance,forinclusionintheproposedNAICcontingentdeferredannuity(CDA)guidelines,forstatesastohowcurrentregulationsgoverningrisk‐basedcapitalrequirements,includingC‐3PhaseII,shouldbeappliedtocontingentdeferredannuities(CDAs).RecommendaprocessforreviewingcapitaladequacyforinsurersissuingCDAsandprepareclarifyingguidance,ifnecessary,duetodifferentnomenclaturethenusedwithregardtoCDAs.ThedevelopmentofthisguidancedoesnotprecludetheWorkingGroupfromreviewingCDAsaspartofanyongoingorfuturechargeswhereapplicableandismadewiththeunderstandingthatthisguidancecouldchangeasaresultofsuch a review.

10/21/13ReferralfromACommittee

ItisimportanttoconsidertheimplicationsofworkbeingdonebytheCDAandVAIssuesWorkingGroupstoensureconsistencyinaddressingthesecharges.TheWorkingGroupismonitoringtheprogressofthatwork.

8 LifeRBCWG

1 2017 ReviewandevaluatecompanysubmissionsfortheRBCShortfallscheduleandcorrespondingadjustmenttoTotalAdjustedCapital.

10/16/2015

9 LifeRBCWG

1 2017 ReviewandevaluatecompanysubmissionsforthePrimarySecurityShortfallscheduleandcorrespondingadjustmenttoAuthorizedControlLevel.

10/16/2015

Date Added to Agenda

Attachment E

41