level 4, 1-3 smail street melbourne it ltd (asx: … sachs...goldman sachs eighth annual small &...

TRANSCRIPT

Melbourne IT Ltd ABN 21 073 716 793 ACN 073 716 793 Level 4, 1-3 Smail Street Ultimo NSW 2007 Australia www.melbourneit.info

27 April 2017

MELBOURNE IT LTD (ASX: MLB)

Goldman Sachs Eighth Annual Small & Mid-Cap Conference Presentation

Attached is a copy of the presentation to be delivered by Melbourne IT’s CEO & Managing Director, Martin Mercer, at the Goldman Sachs Eighth Annual Small and Mid-Cap Conference today in Sydney.

For any enquiries, contact:

Martin Mercer Chief Executive Officer Tel. No. (02) 9934 0555

ENDS.

About Melbourne IT

Melbourne IT Group is a publicly listed company with offices in Melbourne, Sydney, Brisbane, Auckland and Canberra. Melbourne IT’s purpose is to “fuel our customers’ success through the smart use of technology”. By 2020 we aim to have fuelled the success of over one million businesses. Our customers will love us, our people will be our most passionate advocates, and our investors will be rewarded.

Melbourne IT operates two businesses marketed under 7 brands.

The Small and Medium Business Division (SMB) is Australia’s largest domains and hosting business with revenues of approximately $100m. The SMB business operates under the Melbourne IT, WebCentral, Netregistry and TPP brands.

The Enterprise Services Business (ES) is Australia’s leading cloud enabled software and services business with revenues of approximately $70m. ES is based in Sydney, Melbourne and Brisbane and has a blue chip customer base. It operates under three brands, Melbourne IT, Infoready and Outware.

Visit: www.melbourneit.com.au

Transforming Melbourne ITGoldman Sachs Small & Mid Cap ConferenceApril 2017

Purpose and Vision

• We fuel our customers’ success through the smart use of technology.

• We aspire to be Australia’s most impactful digital technology partner.

2

3

Priority Status Comment

Return SMB to Growth

We have repaired the legacy domains and hosting business and succeeded in developing a new “managed marketing solutions” business. Solutions revenue now accounts for 20% of total SMB revenue and is growing at 56%pa. SMB enters 2017 growing at the top and bottom lines.

Accelerate the Transformation of ES

ES is well on its way to becoming Australia’s most impactful digital technology partner for the enterprise market. Over the past three years ES has tripled in size. In 2016 revenue grew 73% while EBITDA grew 87%. ES expects to enjoy strong growth in 2017.

Realise Synergy Savings

The acquisitions of Netregistry (Feb 2014) and Uber Global (April 2015) were expected to deliver combined synergy savings of $10M ($5M by the end of 2015, another $2.5M in 2016, and the final $2.5M in 2017). At the end of 2016 we had realised $8.5M of savings ($1.0M more than originally targeted) and have clear line of sight to the remaining $1.5M.

We have achieved the three priorities that underpinned our turnaround. The future is all about growth.

Priorities: mission accomplished

Growth: consistently strong growth

4Underlying financial information presented adjusts for one-off and non-recurring costs and the pro forma impacts of acquisitions and divestments made in the financial period as outlined in the previous slides.

3.7 3.6 5.2 11.2 2.1

9.2 11.3

17.0

0

10

20

30

2013 2014 2015 2016

Reported EBITDA ($m)

5.8

12.816.5

28.2

3.7 6.1 10.0 10.6 2.1

10.2

12.0 17.8

0

10

20

30

2013 2014 2015 2016

Underlying EBITDA ($m)

5.8

16.3

22.0

28.4

3.9 3.1 4.6 4.6 2.3 5.8

6.0 9.7

0

10

20

2013 2014 2015 2016

Underlying NPAT ($m)

6.28.9

10.7

14.3

4.7 3.3 5.0 4.6

2.8 6.2 6.5 9.6

0

10

20

2013 2014 2015 2016

Underlying EPS (cents)

7.59.5

11.5

14.2

H1H2

3YR CAGR 69%

3YR CAGR 70%

3YR CAGR 24%

3YR CAGR 32%

FY 2017 Outlook: strong growth to continue

5

Measure Range ⇳ %1 Comment

Underlying EBITDA $31M - $34M 15%/20%2

Includes investment of $1.7M in 2017 to support the growth of the business, including $400K in new roles in Shared Services to keep up with the growth in the business, $300K in data analytics to support growth in SMB, $1M to ensure sustainable growth in the rapidly growing ES business.

Underlying EPS $0.15 - $0.17 13%

Dividend 55% - 75% N/A Dividends in FY 2017 will be determined by reference to a payout ratio in the range of 55% to 75% of reported NPAT.

Organic growth will drive another strong year in 2017

1. Change on last year calculated from the mid-point of the guidance range and last year’s actual result2. 20% growth after adjusting for $1.7M incremental investmentNB. Figures throughout this document may not be exact due to rounding and include non-IFRS financial information that is relevant for users understanding the underlying performance.

6

98%

2%

SMB

Revenue: high quality revenue with faster growing solutions business

42%

48% 10%

ES

75%

20%5%

Group

RecurringRepeatableOne Off

Definitions: 1. recurring revenue is contracted annuity income, 2. repeatable projects are instances where we have been consistently billing the same customer for 2 or more years, 3. one-off project revenue is where we do a piece of work for a customer and there is no follow on business

ES: strategy and execution

7

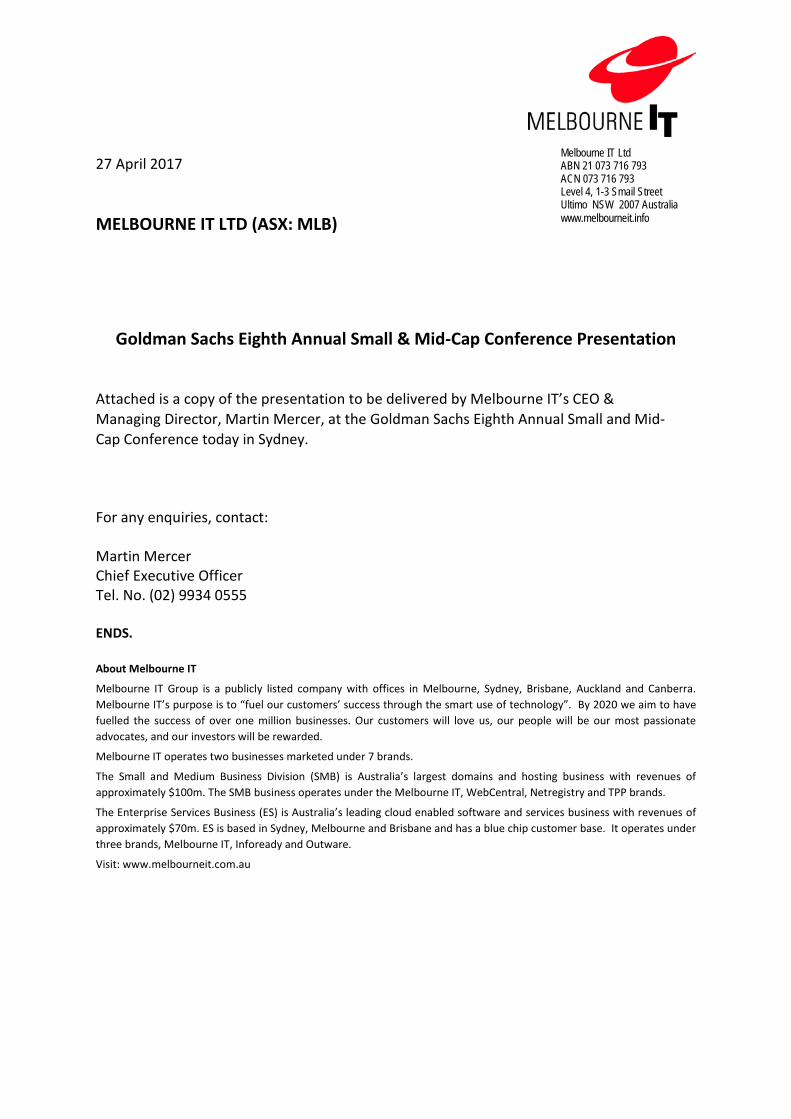

ES: facts and figures

8

Successful reinvention. A provider of complete digital solutions with for large companies and government customers with more than 400 employees across Melbourne, Sydney, and Brisbane

Strong Growth, underlying EBITDA growing at +20%pa

Expertise: Outware founders retained; InfoReady founders retained; AWS Foundation partner in Australia, with multiple AWS accreditations.

Culture of Innovation and Customer Excellence

Enterprise Grade. Blue Chip customer base – 40% of the ASX top 30 are customers. Significant recurring revenues and repeatable project revenue. Governance and balance sheet suitable for Enterprise & Government customer partnering

1

2

3

4

5

9

Digital Solutions: an attractive and strongly growing market

Annual Growth Rate 2015Key: Source: IBM 2015

$1.4b Market$6.5b Market

+

Complete Digital Solutions

Execution: capturing revenue synergies

10

Data & Analytics(Infoready)

Mobile(Outware Mobile)

Cloud & Managed Services

June2016 Dec

2016

SMB: strategy and execution

11

SMB: facts and figures

12

More than 300 employees with offices in Melbourne, Sydney, Brisbane and Canberra

Largest Australian domain name and web hosting provider, with more than 40% market share

We have helped fuel the success of more than 600,000 Australian SMB customers

A portfolio of SMB brands:

Growing web solutions business – the key to revenue growth and value creation

1

2

3

4

5Solutions Revenue (20%) – managed marketing services comprising web design and digital marketing

Components Revenue (80%) – domain names, web hosting and email

Customer Journeys: the key to value creation

131. IPSOS: Melbourne IT Customer Web Journey Study2. IPSOS report 3. IPSOS report

4. IPSOS report

14

Execution: revenue growth

85%

15%

80%

20%

2015

REVENUE SPLIT BY SEGMENT

SOLUTIONSCOMPONENTS

20160

2

4

6

8

10

12

14

16

18

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2016Q4

$M

Direct Revenue - Components vs Solutions

Solutions Components

Acquisition of Uber Global

Acquisition of Netregistry

Execution: stable domain name revenue and volumes

15

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

0

10

20

30

40

50

60

70

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

Pric

e In

dex

Units

('00

0)

Direct .AU Domain Names

Commoditised

Premium Priced

Price Index - Direct

Total Units PCP

CrazyDomainsenters market GoDaddy

enters market

Netregistry acquired. Average price drops due to mix change.

Stable price despite

progressive mix change

Seasonal pattern and consistent growth on PcP

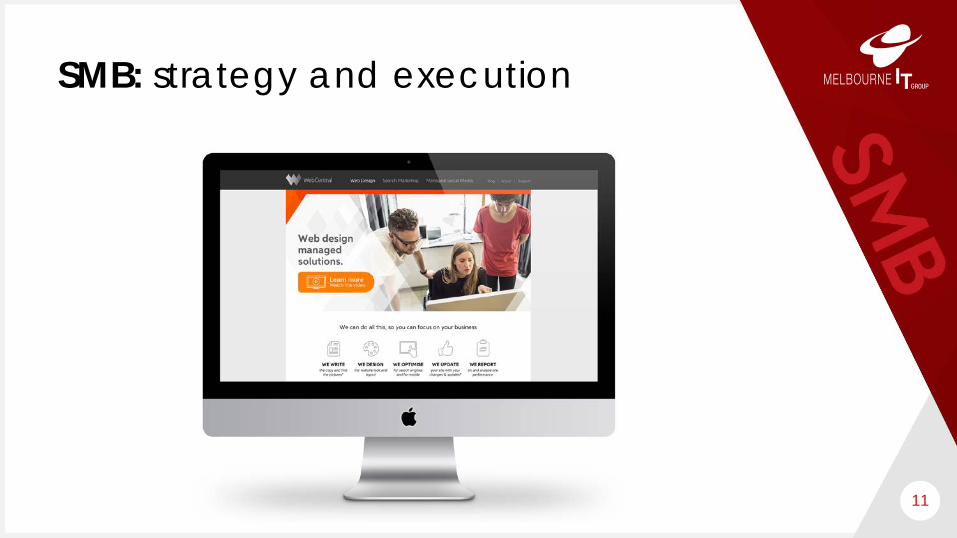

Summary

16

1. Turnaround complete;• $8.5M of synergy savings and clear line of sight to the remaining $1.5M,• SMB exits 2016 with good organic growth driven by strong performance in new

solutions products• ES tripled in size in past three years, in 2016 revenue grew 73% and EBITDA 87%

2. Strong FY 2016 results validate “digital solutions” strategy;• Revenue up 12%, reported EBITDA up 71%, NPAT up 91%, and underlying EBITDA up

29%

3. Continuation of strong growth expected in 2017;• Underlying EBITDA of $31m - $34M, up 15% YoY• underlying EPS of 15c – 17c, up 13% YoY

4. Strong free cash flow driving debt reduction and increased returns;• Debt peaks in June and strong cash generation sees it reduce progressively over 2017• Final dividend of 6c up 50% on 2015, total dividend of 8c up 60% on 2015