level 1 qualification in personal finance - bcs.org · the work focused on various hard to reach...

TRANSCRIPT

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

1

Level 1 Qualification in Personal

Finance

TEACHERS’ HANDBOOK

MANAGING MONEY DAY-TO-DAY

CONTROLLING YOUR MONEY

CHOOSING FINANCIAL PRODUCTS AND GETTING HELP

Version 1.0

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

2

Contents 1. Introduction 2. Unit 1: Managing Money Day-to-Day

Assessment criteria Teacher guidance Session plans Handouts Useful resources

3. Unit 2: Controlling Your Money

Assessment criteria Teacher guidance Session plans Handouts Useful resources

4. Unit 3 : Choosing products and getting help

Assessment criteria Teacher guidance Session plans Handouts Useful resources

5. Resource Directory 6. Coverage of the Adult Financial Capability Framework 7. Underpinning Key Skills: Communication, Application of Number and

ICT 8. Coverage of the European Driving Licence 9. PHSE and Maths Curriculum

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

3

Introduction

Background to the Personal Finance Qualification at Level 1

An initial meeting took place in 2006 between the British Computer Society (BCS) and Tribal Group (http://www.ctad.co.uk/) to discuss the potential for developing a level 1 Personal Finance qualification. This came about as a result of the Move On with Equal project (an Equal project funded by the EU and delivered by Tribal Group) which had been working with a wide range of organisations across the Voluntary/Community/Local Government/Private Providers to enable the unemployed gain employment (http://www.mowe.org.uk/ ). The work focused on various hard to reach groups as well as specific groups e.g. ex offenders, homeless, those in debt. This work indicated that there was a need to develop a personal finance course at level 1 to support these groups and organisations. As BCS had developed a level 2 online qualification it was decided that it would be beneficial to work with an organisation who already had the expertise in relation to curriculum as well as an understanding of the wider financial capability agenda. BCS and Tribal Group worked together to develop the qualification. The qualification has a wide and varied target group from those organisations delivering basic personal finance training sessions, providers delivering Level 1 qualifications, as well as learners who will benefit from an online e learning resource and qualification such as those living in rural areas who may not be able to access regular on site provision.

The Qualification

The qualification is aimed at those who require a level of financial understanding for their personal lives. There is a clear gap in the market for a Level 1 personal finance qualification that focuses on the developing of financial competency. Two main resources will help to underpin the content of the proposed qualifications: the developing level of the Adult Financial Capability Framework1 and the FSA’s baseline survey, Measuring Financial Capability2. The qualification aims to demonstrate financial capability and key life skills at the following levels:

• Adult Financial Capability Framework: Developing

• Key Skills: Level 1

• Secondary schools curriculum, financial capability: KS3. Prerequisites

No prior financial knowledge required.

1 Adult Financial Capability Framework,

2 Measuring Financial Capability, FSA, 2006

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

4

Structure

Qualification is awarded on successful assessment in three mandatory units:

• Unit 1: Managing Money Day-to-Day

• Unit 2: Controlling Your Money

• Unit 3: Choosing financial products and getting help. Syllabuses are prescribed for each unit. Courseware providers choose how to deliver syllabus content. Non-mandatory teacher guidance is provided. Teaching hours

It is estimated that each unit will require on average 10 hours tuition, but precise requirements will vary according to learner ability, prior knowledge and needs.

Unit Teaching hours 1: Managing Money Day-to-Day 10 2: Controlling Your Money 10 3: Choosing Financial products and getting help 10 TOTAL 30

Assessment

Assessment of each unit will be by 16-question test. The duration of each test is 30 minutes. Assessment will be delivered and marked by computer. One mark is given for each correctly completed question. The pass mark for each unit is 75 per cent. Learners are required to pass the test for all three units in order to achieve the qualification. Progression

Learners who successfully complete this Level 1 course may wish to proceed to the British Computer Society Personal Finance Qualification Level 2. Teacher guidance

Guidance has been written for each unit to supplement the content outlined in the syllabuses. This guidance complements the syllabuses. Therefore the handbook should be used in conjunction with the syllabuses for each unit. Resources

Two key resources are recommended for the delivery of this qualification: the Personal Finance Handbook3 and the FSA’s Money Made Clear website4. Move on With Equal (MOWE) has developed some online learning materials linked to this accreditation which can be accessed for free on the MOWE website5. Additional resources which might be

3 Personal Finance Handbook, CPAG, 2007

4 www.moneymadeclear.fsa.gov.uk

5 www.mowe.org.uk

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

5

useful have been identified for each unit. Full details for the resources can be found in Section 5. Assessments taking place in 2007-8 will be based on legislation that will have come into force up to and including 1 October 2007 (for example, including the change in national minimum wage from that date). Web-based resources such as FSA and government websites will provide the most up-to-date information. Personal Finance6, a textbook to accompany the Open University module in Personal Finance, could provide useful background information to those who deliver this British Computer Society qualification. Links to frameworks and standards

Coverage of the Adult Financial Capability Framework and the European Driving Licence has been identified along with the underpinning Key Skills required for the units.

6 Personal Finance, Wiley, 2006

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

6

Unit 1: Managing Money Day-to-Day Unit goal:- For learners to be able to manage money on a day-to-day basis using appropriate financial products. LEARNING OUTCOMES

ASSESSMENT CRITERIA

The learner will:

The learner can:

1.1 Recognise the different sources of income.

1.1.a Identify the main sources of income and benefits that are available from working as an employee.

1.1.b Determine for a range of situations

whether the following benefits may be claimed: - income support - jobseeker’s allowance - housing benefit - council tax benefit - working tax credit.

1.2 Understand some key rights

and responsibilities connected with employment income.

1.2.a Determine for simple work situations whether correct rights are being given in respect of: - pay - written contract of employment - rest breaks - paid holiday - sick pay - dismissal.

1.2.b Identify the main features of and

purpose of: - payslip - P60 - P45.

1.2.c Make rough calculations to check the accuracy of entries on a pay slip. 1.2.d Identify sources of help with employee

pay and sources of information about becoming self-employed.

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

7

LEARNING OUTCOMES

ASSESSMENT CRITERIA

The learner will:

The learner can:

1.3 Perform everyday money management tasks.

1.3.a Identify and describe the features of basic bank accounts and current accounts.

1.3.b Undertake a range of money

management tasks using the appropriate bank product feature.

1.3.c List the different methods that are

available to pay for goods and services and identify which offers the best deal.

1.4 Demonstrate the use of personal

budgeting.

1.4.a Use records and statements to construct a personal budget.

1.4.b Use information from a budget and

suggest appropriate action where the budget shows a surplus or shortfall.

1.4.c Distinguish between essential and non-

essential spending.

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

8

Teacher Guidance

The Personal Finance Handbook and the FSA’s Money Made Clear7 website should provide you with the background knowledge to deliver the unit. Further resources that may be useful are also indicated. Full details for the resources can be found in Section 5. Session plans have been provided to illustrate possible activities that can be used to deliver this unit. Signposting to resources, tutor generated examples and exemplar handouts to support the sessions has been provided Each unit has 3 session plans of 3-hours each. The MOWE Personal Finance Hot Topic8, part 1 could be used at the start or finish of the unit to make up the guided learning hours to 10 for each unit. Flipchart, paper and pens given as standard but interactive whiteboard would be preferable if available. If possible each learner should keep a Key Facts file summarising information to be remembered along with definitions of key words. The following guidance referenced to the syllabus provides further details to help delivery of the unit.

7 www.moneymadeclear.fsa.gov.uk

8 www.mowe.org.uk

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

9

1.1 Sources of income Learner is required to recognise different sources of income. 1.1.1 Employment a) Be aware that most people work as an employee

Additional guidance: 1.1.2 Earnings as an employee a) Understand the main forms of pay Additional guidance Learners need to know:

• The main forms of pay: wages and salaries, pension scheme membership, life cover, childcare vouchers, other benefits.

1.1.3 State benefits a) Have a knowledge of the main state support available in the following situations:

• low income

• help with housing costs and provision

• unemployment/ redundancy

• in-work benefits. b) For different scenarios, be able to match appropriate state benefits to the

circumstances described. Additional guidance Learners need to know:

• Income support, including help with mortgage interest, council tax benefit

• Housing benefit, local authority obligations towards homeless people

• Council tax benefit

• Jobseeker’s allowance, New Deal programmes

• Working Tax Credit Learners should know in what circumstances each of the benefits may be claimed but do not need to know current rates or the details of how entitlement is calculated.

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

10

1.2 Rights and Responsibilities Learner is required to understand some key rights and responsibilities connected with employment income 1.2.1 Self Employment a) Know where to get information about becoming self-employed.

Additional guidance Learners need to know:

• HM Revenue & Customs for information on tax when starting up a business.

• Business Links for information on all aspects of running a business, including grants

1.2.2 Working for an employer a) Understand the main deductions from pay, broadly how they are worked out and

what the worker gets in return. b) Have knowledge of key rights in connection with pay and what to do if rights not

observed. c) Have knowledge of the key records an employee receives in connection with

employment, why they should be kept and for how long. d) Know where to get help with pay as an employee. e) Be able to identify the key elements of a pay slip f) Be able confidently to ask for an explanation of entries on a pay slip. g) Be able confidently to seek help with employment rights. Additional guidance Learners need to know:

• The main deductions from pay: National Insurance, income tax, pension contributions, union subscription, broadly how they are worked out and what a worker gets in return

• The key rights in connection with pay: written contract, pay slips, national minimum wage, working hours and holidays, sick pay, dismissal.

• Which records should be kept and for how long.

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

11

1.3 Everyday Money Management Learner is required to distinguish between different types of bank account and know the procedures for opening an account. 1.3.1 Uses and features of bank accounts a) Understand that a bank account is increasingly necessary b) Have knowledge of basic bank accounts and current accounts, the different

features each provides and the circumstances in which each would be appropriate.

c) Be able to identify the appropriate bank account for different situations.

Additional guidance Learners need to know:

• Bank accounts needed to accept wages and benefits NB. Until 2010 benefits can be paid into Post Office® Card Accounts.

1.3.2 Opening a bank account a) Have knowledge of the procedures for opening a bank account, including the

documents required and the requirement on banks to accept alternative forms of identification where standard documents are not available.

b) Be able to apply for a bank account. c) Be able confidently to apply to open an account.

Additional guidance: British Bankers Association publishes a guidance leaflet on documents required to satisfy Money Laundering Regs - ‘Proving Your Identity - How money laundering prevention affects opening an account’ The leaflet is available from the BBA website www.bba.org.uk

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

12

1.4 Personal Budgeting Learner is required to understand the purpose of budgeting and be able to construct and use a budget. 1.4.1 Budgeting a) Understand the reasons for budgeting b) Have knowledge of different ways of handling a budget. c) Distinguish between essential and non-essential spending. d) Understand importance of checking bills and statements. e) Be aware of opportunities to save money. f) Be able to convert figures between weekly, monthly and yearly basis. g) Be able to extract relevant figures from utility bills. h) Be able to read a bank statement. i) Be able to draw up a budget either for day-to-day living or for a special event, such

as a holiday. j) Be confident in ability to monitor and control spending. Additional guidance Learners need to know:

• What a budget is and how it may be used for control of resources, checking current financial position, being able to plan ahead, monitoring progress.

• Cash budgeting, using a bank account, managing over a weekly, fortnightly or monthly cycle.

• Opportunities to save money i.e by using direct debit, paying bills online, switching utility suppliers.

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

13

Session Plans for Unit 1

Sources of Income Unit goal For learners to be able to manage money on a day-to-day basis using appropriate financial products. Learning Outcomes The learner will be able to: 1.1 Recognise the different sources of income. 1.2 Understand some key rights and responsibilities connected with employment

income. Minutes Topic Activity Resources 15 Sources of

income Introduction to session – Brainstorm where people get money from. Sort into income from employment, benefits, self-employment and other using grid on Handout 1. In this unit going to look at income from employment and benefits. (For information on self-employment visit the Citizens Advice website www.adviceguide.org.uk/index/life/employment/self-employment_checklist or Business Link www.businesslink.gov.uk)

Flipchart, paper, pens Handout 1A.1

30 Employment - payslip

If employed, your payslip will show you how much you have been paid in a month (or week) and what money has been deducted. Discuss what the money deducted is used for or sort photos of hospital, expensive car, party, roads, dentist, school, nursing home etc into two piles: one for where money deducted goes and one for what it won’t be spent on. Using an enlarged version of a payslip point out the key elements of a payslip – see the Where Money Comes from section of www.moneymatterstome.org.uk. (Right click image of payslip to print out) Individuals annotate printout of a payslip. Work through activity on MMtM website/CD ROM looking at working out how much tax will be deducted.

Slide/MMtoM website or A3 version of payslip Selection of photos from magazines/newspapers

30 Employment – key rights and responsibilities

Discuss knowledge/experience of being employed. Use newspaper cuttings as a resource to stimulate discussion if knowledge/experience of group likely to be low. Q&A on key rights following on from discussion. Individuals add notes to Handout 2.

Handout 1A.2 Summary of key rights Folders

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

14

Handouts can form basis of a Key Facts File. Explore the difference between a P45 and a P60. Discuss the need to keep them, and provide with a folder to keep key documents in.

15 Break 30 Employment –

getting help Look at where to get help as an employee, with regards to pay and employment rights. In pairs role play querying a pay slip and asking for help with employment rights.

Scenario cards with key facts

30 Benefits – Key points

Return to list of benefits collected at start of session. Use Handout 3 to record who can claim which benefits. Read out information about benefits and ask for name of benefit.

Handout 1A.3 Create factsheets from information on DirectGov website.

25 Benefits – Which benefits?

Create scenario cards and give out to pairs so that they can match the scenarios to benefits.

Scenario cards

5 What next? Recap Next session will be looking at opening bank accounts.

Note: See the Useful Resources section for information on:

• MMtoM: Money Matters to Me website

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

15

Bank Accounts Unit goal For learners to be able to manage money on a day-to-day basis using appropriate financial products. Learning Outcomes The learner will be able to: 1.3 Perform everyday money management tasks. Minutes Topic Activity Resources 15 Why use a bank

account? Introduction to session – Who already has a bank account/knows someone who has? Why have they got an account?

Flipchart, paper, pens

30 Choosing an account - types of bank accounts

In pairs/small groups work through the topic ‘Choose an Account ‘on MGR CD ROM. Make notes in Key Facts file to record the difference between basic and current bank accounts.

MGR CD ROM

30 Features of accounts

Using Colossal Cards talk through the different features of bank accounts, including standing orders, direct debits, overdrafts, online bill payments and how they work. In pairs, learners to design posters to illustrate how one or more of the different features work or to promote an account on the basis of one or more features.

Colossal Cards Paper, pens

15 Choosing an account – factors to consider

Discuss what factors might be involved in choosing a particular bank e.g. online, branch close by, free gifts….

15 Break

20 Opening an account - ID

Discuss why proof is needed to open accounts. Use the sorting diagram on Handout 2.1 to sort types of ID into proof of address/name or both. Check answers. Individuals to identify which proof of name and address they have.

Short Programmes: 2. Need An Account – List of ID Handout 1B.1

25 Opening an account – filling in forms

Individuals to practise filling in forms. Use a highlight pen to mark anything unsure of. Compare with a partner and make a note of any questions to ask whole group. Make notes in margin when got answers. Make a list of information required to apply for a bank account.

Forms from banks or sample form in Financial Products Resource Pack/ Short Programmes: 2. Need An Account

25 Opening an account – visiting the

Split the whole group into two: one set make a list of the questions that you would want to ask when opening an account and the other set make a list

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

16

branch of the questions that you might get asked by the bank. Use the questions to role play in pairs a visit to a bank to open an account.

5 What next? Recap Next session will be looking at budgeting.

Note: See the Useful Resources section for information on:

• Financial Products Resource Pack

• MGR: Money-go-round CD ROM

• Short Programmes: 2. Need an account

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

17

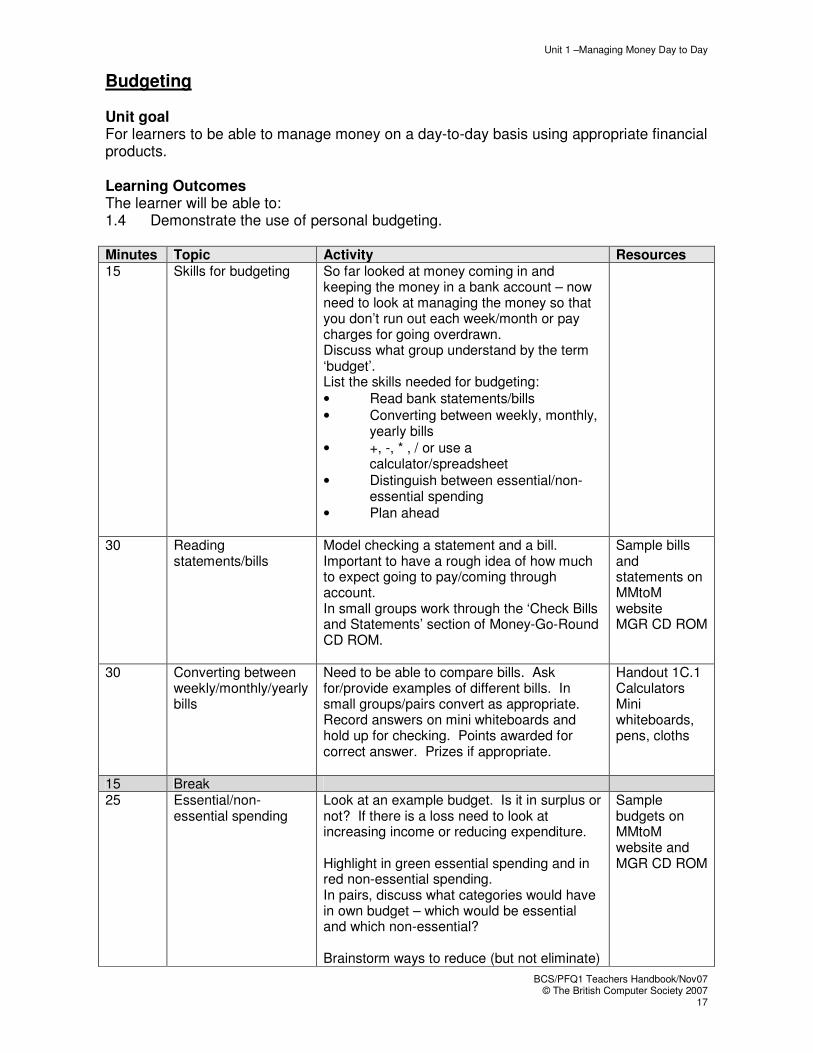

Budgeting Unit goal For learners to be able to manage money on a day-to-day basis using appropriate financial products. Learning Outcomes The learner will be able to: 1.4 Demonstrate the use of personal budgeting. Minutes Topic Activity Resources 15 Skills for budgeting So far looked at money coming in and

keeping the money in a bank account – now need to look at managing the money so that you don’t run out each week/month or pay charges for going overdrawn. Discuss what group understand by the term ‘budget’. List the skills needed for budgeting:

• Read bank statements/bills

• Converting between weekly, monthly, yearly bills

• +, -, * , / or use a calculator/spreadsheet

• Distinguish between essential/non-essential spending

• Plan ahead

30 Reading statements/bills

Model checking a statement and a bill. Important to have a rough idea of how much to expect going to pay/coming through account. In small groups work through the ‘Check Bills and Statements’ section of Money-Go-Round CD ROM.

Sample bills and statements on MMtoM website MGR CD ROM

30 Converting between weekly/monthly/yearly bills

Need to be able to compare bills. Ask for/provide examples of different bills. In small groups/pairs convert as appropriate. Record answers on mini whiteboards and hold up for checking. Points awarded for correct answer. Prizes if appropriate.

Handout 1C.1 Calculators Mini whiteboards, pens, cloths

15 Break 25 Essential/non-

essential spending Look at an example budget. Is it in surplus or not? If there is a loss need to look at increasing income or reducing expenditure. Highlight in green essential spending and in red non-essential spending. In pairs, discuss what categories would have in own budget – which would be essential and which non-essential? Brainstorm ways to reduce (but not eliminate)

Sample budgets on MMtoM website and MGR CD ROM

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

18

essential spending – e.g. switch supplier, reduce amount used.

30 Drawing up a budget Tutor to use a case study or similar from which a budget can be draw up. Give the information to the group. How can the budget be adjusted to build up an emergency fund/stop being overdrawn/save for an event or item?

Case Study

20 Ten top tips for saving money

In small groups draw up list of ten top tips for saving money. Collate list and vote on top 10. Put top 10 in Key Facts file.

5 What next? Recap Next session will be looking at Borrowing.

Note: See the Useful Resources section for information on:

• MGR: Money-go-round CD ROM

• MMtoM: Money Matters to Me website

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

19

Handouts for Unit 1

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

20

Handout 1a.1 - Sources of Income Income Sort

Employment Self-employed

Benefits Other

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

21

Handout 1a.2 - Sources of Income Key Rights

Written Contract

Payslip

National Minimum Wage

Working Hours

Holidays

Sick Pay

Dismissal

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

22

Handout 1a.4 - Sources of Income Main Benefits Which benefits go in which circles?

If you Work If your income is low

Other Situations

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

23

Handout 1b.1 - Bank Accounts

Proof of Address

Proof of Name

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

24

Handout 1c.1 - Budgeting Weekly/Monthly Decide whether you are going to work out a weekly or monthly budget. This will affect your calculations as some of your bills may be weekly, some monthly or some for the whole year (annual) and these will need dividing up or multiplying.

If you are paid weekly, it probably makes sense to work out a weekly budget. To do this you will need to work out approximately how much any monthly, quarterly or annual bills are each week. To change annual bills to weekly, divide by 52. To change quarterly bills to weekly, multiply by 4 and then divide by 52. To change monthly bills to weekly, multiply by 12 and then divide by 52 If you are paid monthly, it probably makes sense to work out a monthly budget. To do this you will need to work out approximately how much any weekly or annual bills are each month. To change annual bills to monthly, divide by 12 To change quarterly bills to monthly, divide by 3. To change weekly bills to monthly, multiply by 52 and then divide by 12

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

25

Useful Resources for Unit 1

Details of where to order resources can be found in the Resource Directory Colossal Cards Information and resources linked to the different types of cards Direct Payment Pack Range of resources linked to opening bank accounts Financial Products Resource Pack Basic Bank Account section provides realia related to a basic bank account Making Ends Meet Topics on opening a bank account and budgeting Money-go-Round – CD ROM Topics on budgeting, bank accounts and payslips NatWest Face 2 Face with Finance – interactive materials and video clips Bank On It Money for Life Personal Finance Handbook Chapter 2 Everyday Money Chapter 9 Benefits and tax credits Short Programmes

• Need an Account? - session plan looking at the literacy and financial skills needed to use a bank account

• Using an Account - session plan looking at the numeracy and financial skills needed to use a bank account

• Keeping Track of Your Money - plan looking at the numeracy and financial skills needed in budgeting

www.direct.gov.uk/en/Employment/Employees Information on rights of employees www.direct.gov.uk/en/MoneyTaxAndBenefits Information on benefits and tax www.moneymadeclear.fsa.gov.uk Sections on budgeting and using a bank account www.moneymatterstome.co.uk (Money Matters to Me) Useful Tools Interactive Budgeter helps you work out your monthly budget on an ongoing basis. Money Matters 2. Where money comes from: employment, self-employment and benefits 4. Introduction to record keeping with interactive activities

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

26

5. Spending and budgeting Workshops Interactive ATM, Chip and PIN machines

Unit 1 –Managing Money Day to Day

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

27

Key Skills

Opportunities for providing evidence for Key Skills Communication, Application of Number and ICT at Level 1: Opening a bank account. Communication

C1.1 Take part in a group discussion on different types of bank accounts C1.2 Read texts about the different features of a bank account C1.3 Make a list of the advantages/disadvantages of the different types of

accounts C1.3 Fill in an application to open a bank account

This theme could also provide evidence for use of ICT. Setting up a budget Set up a budget based on own data or from that of a case study. Gather information from bank statements and utility bills (online and paper based). Compare the budget with that of another learner or case study. Application of Number

N1.1 Gather numerical information to help set up a budget. Find another budget to compare with.

N1.2a,b,c Compare the data from the two budgets. N1.3 Interpret the results and present your findings, in two different ways

ICT ICT1.1 Gather information from online bank statements and bills to help set

up a budget. ICT1.2 Use ICT to combine information from the internet and a non ICT

based information source to set up budget using a spreadsheet. Send an email querying an item on a statement/bill.

ICT1.3 Present the budget information accurately and fit for purpose. This could be by using and image, text or both.

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

28

Unit 2: Controlling Your Money

Unit goal For learners to be able to make decisions about saving and borrowing using appropriate financial products and sources of help.

LEARNING OUTCOMES

ASSESSMENT CRITERIA

The learner will:

The learner can:

2.1 Be able to plan ahead to repay borrowing.

2.1.a Identify how a household budget may be constructed to repay borrowing and how this may be affected by a change in circumstances such as unemployment or interest rate changes. 2.1.b Identify financial products and strategies that can help households protect their budgets against changing circumstances.

2.2 Recognise and seek help with a debt crisis.

2.2.a List debts in order of priority. 2.2.b Construct a personal budget for repaying problem debts. 2.2.c Identify sources of advice and help with debt problems.

2.3 Demonstrate an understanding of short- term goals and how they differ from medium and long-term goals.

2.3.a Differentiate between what is meant by short, medium and long-term goals 2.3.b Identify the main types of products suitable for each of the following: emergency fund, saving for a holiday, saving for retirement. 2.3.c For different scenarios, compare and choose between two or more financial products on the basis of risk and return. 2.3.d Using tables, extract the amount that needs to be saved to meet a short-term savings goal.

2.4 Recognise how to make informed purchasing decisions funded by credit or saving.

2.4.a Distinguish between similar products on the basis of AER or APR and other factors, such as term and risk. 2.4.b Using tables, extract the total cost of an item purchased with borrowing.

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

29

Teachers Guidance

The Personal Finance Handbook and the FSA’s Money Made Clear9 website should provide you with the background knowledge to deliver the unit. Further resources that may be useful are also indicated. Full details for the resources can be found in Section 5. Session plans have been provided to illustrate possible activities that can be used to deliver this unit. Signposting to resources, tutor generated examples and exemplar handouts to support the sessions has been provided Each unit has 3 session plans of 3-hours each. The MOWE Personal Finance Hot Topic10, part 2 could be used at the start or finish of the unit to make up the guided learning hours to 10 for each unit. Flipchart, paper and pens given as standard but interactive whiteboard would be preferable if available. If possible each learner should keep a Key Facts file summarising information to be remembered along with definitions of key words. The following guidance referenced to the syllabus provides further details to help delivery of the unit.

9 www.moneymadeclear.fsa.gov.uk

10 www.mowe.org.uk

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

30

2.1 Borrowing Learner is required to plan how to repay debt, including strategies to manage the risk to debt repayments of changes in circumstances, and be able to compare different ways of borrowing. 2.1.1 Planning ahead a) Have knowledge of different reasons for borrowing. b) Understand the importance of planning how debt will be repaid. c) Understand the circumstances and types of risk that most often upset debt

repayment plans. d) Be able to construct a budget to repay borrowing

Additional guidance Learners need to know about: Effect of uncontrolled spending, uncontrolled gambling, change in interest rates, loss of job, family breakdown

2.1.2 Comparing different ways of borrowing a) Begin to understand the cost of borrowing and how to use Annual Percentage Rates

(APR)s. b) Have knowledge of some key types of borrowing and sources of borrowing and

understand the key differences between them. c) Have a knowledge of financial strategies and products that may help to manage the

risks. d) Be able to use look-up tables and online tools to work out the total cost of an item

bought on credit. e) Be able to compare the relative cost of credit deals using the APR. f) Be able to identify risks associated with borrowing for different scenarios. g) Be able to weigh up whether an insurance product is worth having. h) Be in control of borrowing decisions. i) Be confident turning down unwanted products Additional guidance Learners need to know about:

• traditional credit cards, store cards, pre-pay credit cards, secured and unsecured personal loans

• High Street lenders, credit unions and partnership schemes, cheque cashing services, doorstep lending, loan sharks

• choosing fixed-interest-rate or variable-interest-rate products, building up an emergency fund, insurance products

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

31

2.2 Debt problems Learner is required to be able recognise when borrowing has become problem debt, understand the consequences of failing to pay debts, and know where to get help and advice. 2.2.1 Identifying and tackling debt problems a) Understand the consequences of failing to pay different types of debt. b) Have knowledge of the agencies that offer free advice and help sorting out debt

problems. c) Recognise when debts have become a problem. d) Be able to list debts in order of priority. e) Be able to adjust a budget to release money to tackle debts. f) Be able to find the contact details for agencies offering free debt advice and help

(online and from paper-based directories). g) Be confident seeking help with debt problems.

Additional guidance Learners need to know about: Order of priority for debts Useful websites: http://www.moneymadeclear.fsa.gov.uk/print.aspx?Page=/tools/sorting_out_borrowing_problems

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

32

2.3 Saving Learner is required to understand the advantages and disadvantages of saving and be able to construct a plan to achieve a short-terms savings goal 2.3.1 Interest on savings a) Understand that savings usually earn interest but take time to build up. b) Know that interest rates for savings are expressed as Annual Equivalent Rates (AER)

and how to use the AER. c) Be able to compare different savings deals on the basis of AER.

Additional guidance: 2.3.2 Time span a) Understand that goals may be short, medium or long term and that the approach to

achieving them is likely to differ according to the timespan. b) Have knowledge of the broad types of product that are suitable for goals according to

timespan and how they vary in terms of risk. c) Be able to identify whether goals are short, medium or long term. Additional guidance: Learners need to know about:

• Different types of risk (capital, inflation, shortfall). 2.3.3 Short-term goal a) Have knowledge of the main savings products and sources suitable for a short-term

goal and understand the key differences between them. b) Using look-up tables, be able to work out how much needs to be saved to meet a

defined goal over a defined short-term timespan. c) Be able to suggest suitable savings products for different short-term goals. d) Be able to monitor savings using statements e) Be confident in ability to save up for something. Additional guidance: Learners need to know about:

• bank and building society accounts

• National Savings & Investments

• credit unions

• Savings clubs and payment-in-advance schemes such as Farepak.

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

33

2.4 Saving and borrowing compared Learner is required to judge for given scenarios when borrowing or saving might be the most suitable strategy. 2.4.1 Making saving and borrowing decisions a) Be able to suggest whether saving or borrowing would be most appropriate in

different scenarios, giving reasons for the choice. b) Be confident making purchasing and saving decisions.

Additional guidance:

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

34

Session Plans

Borrowing Unit goal: For learners to be able to make decisions about saving and borrowing using appropriate financial products and sources of help. Learning Outcomes The learner will be able to: 2.1 Plan ahead to repay borrowing. Minutes Topic Activity Resources 15 Why

borrow? In small groups cut out pictures from magazines of items that might need to borrow money in order to buy. Stick pictures on flipchart paper to create posters. Display posters around room. Discuss other reasons why we might need to borrow e.g. to study, pay debts.

Magazines Scissors Glue Flipchart paper

30 Planning repaying debt

Input on need to plan to re-pay debt – see ch4 Personal Finance Handbook. Discuss what might upset a repayment plan. Make notes in Key Facts file.

PFH

15 Comparing ways of borrowing – where from?

In small groups brainstorm types and sources of borrowing. Collate list from ideas gathered in groups. Discuss the differences between them.

Handout 2A.1

15 Comparing ways of borrowing – cost of borrowing

Input on cost of borrowing, APR and how to use.

15 Break 30 Comparing

ways of borrowing – comparing APRs

Using adverts, pairs to find the cheapest loan and the most expensive loan using the APRs. Discuss why APRs vary and what else to look out for when choosing a loan.

Adverts for loans

30 Comparing ways of borrowing – working out cost of borrowing

Introduce online tools and look-up tables to work out cost of borrowing e.g. www.moneymadeclear.fsa.gov.uk/tools/loan_calculator or www.moneymatterstome.co.uk/Interactive-Tools/LoanCalculator . In pairs choose three items from catalogues/magazines. Using look up tables/online tools work out the total cost of borrowing to buy items chosen.

Access to Internet / MMtoM CD ROM

25 Comparing ways of borrowing – managing

Brainstorm ways of managing risks associated with borrowing. Discuss when might take out insurance products and how to turn down unwanted products. If appropriate role play

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

35

risks turning down unwanted products.

5 What next? Recap Next session will be looking at Debt.

Note: See the Further Resources section for information on: PFH: Personal Finance Handbook MMtoM: Money Matters to Me website

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

36

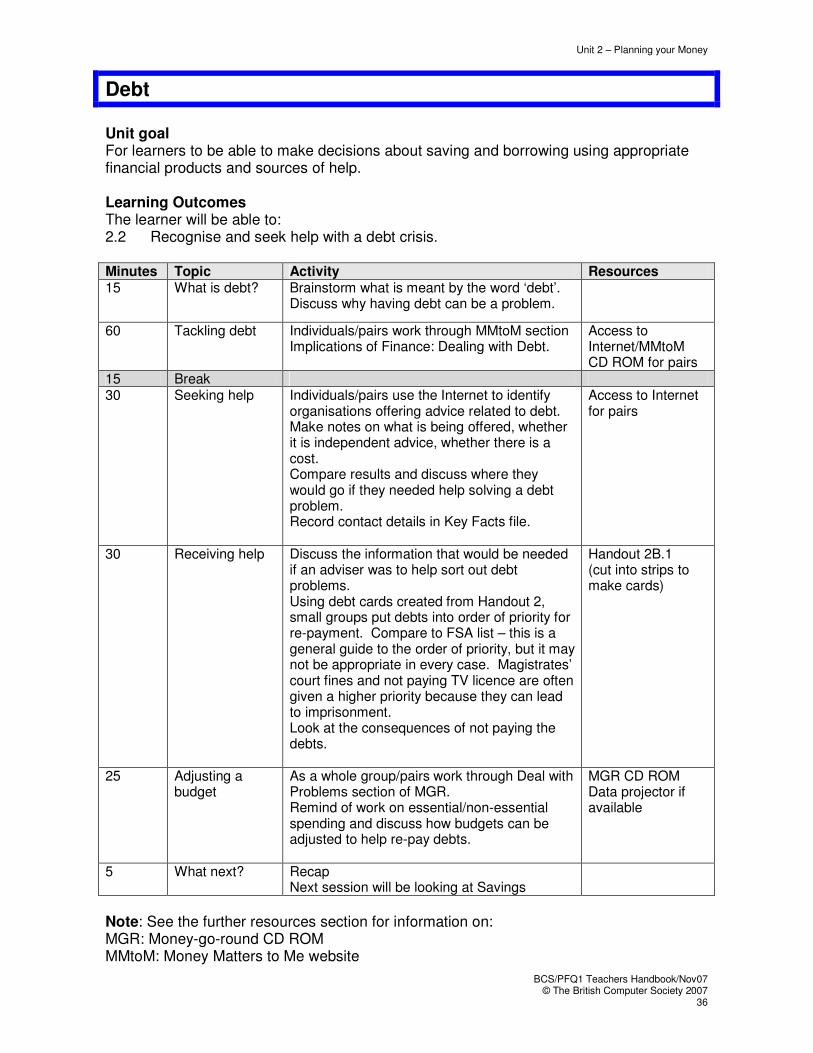

Debt

Unit goal For learners to be able to make decisions about saving and borrowing using appropriate financial products and sources of help. Learning Outcomes The learner will be able to: 2.2 Recognise and seek help with a debt crisis. Minutes Topic Activity Resources 15 What is debt? Brainstorm what is meant by the word ‘debt’.

Discuss why having debt can be a problem.

60 Tackling debt Individuals/pairs work through MMtoM section Implications of Finance: Dealing with Debt.

Access to Internet/MMtoM CD ROM for pairs

15 Break 30 Seeking help Individuals/pairs use the Internet to identify

organisations offering advice related to debt. Make notes on what is being offered, whether it is independent advice, whether there is a cost. Compare results and discuss where they would go if they needed help solving a debt problem. Record contact details in Key Facts file.

Access to Internet for pairs

30 Receiving help Discuss the information that would be needed if an adviser was to help sort out debt problems. Using debt cards created from Handout 2, small groups put debts into order of priority for re-payment. Compare to FSA list – this is a general guide to the order of priority, but it may not be appropriate in every case. Magistrates’ court fines and not paying TV licence are often given a higher priority because they can lead to imprisonment. Look at the consequences of not paying the debts.

Handout 2B.1 (cut into strips to make cards)

25 Adjusting a budget

As a whole group/pairs work through Deal with Problems section of MGR. Remind of work on essential/non-essential spending and discuss how budgets can be adjusted to help re-pay debts.

MGR CD ROM Data projector if available

5 What next? Recap Next session will be looking at Savings

Note: See the further resources section for information on: MGR: Money-go-round CD ROM MMtoM: Money Matters to Me website

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

37

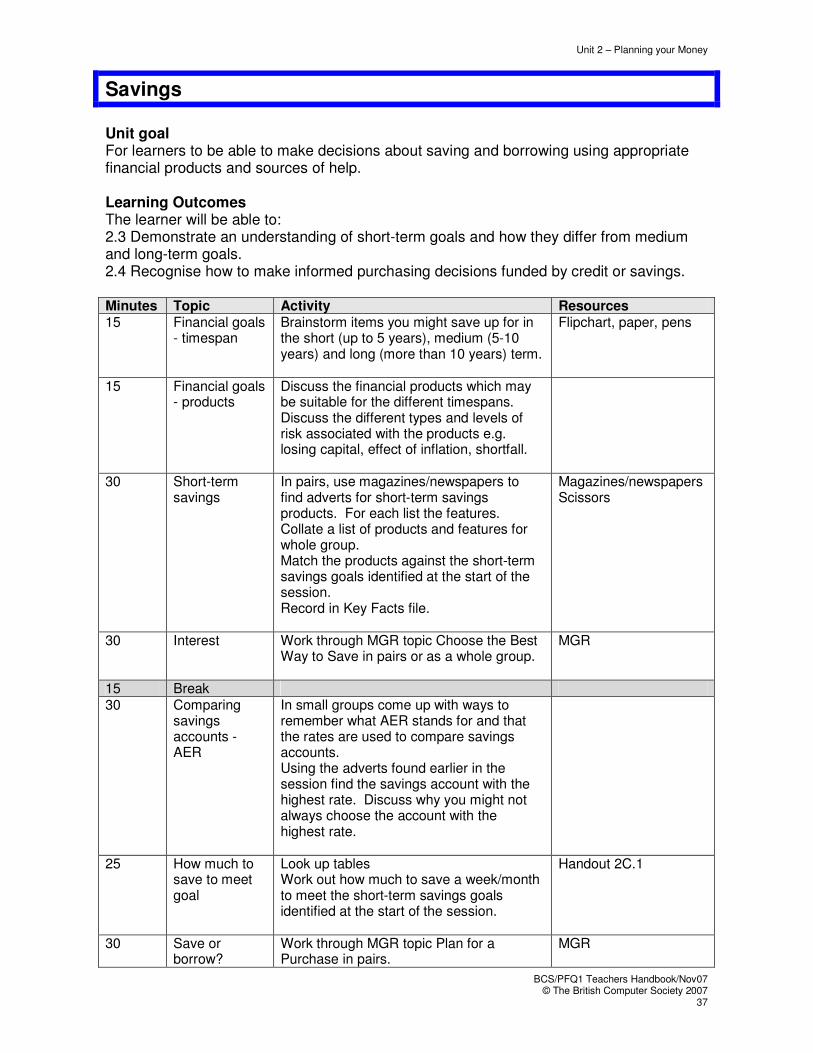

Savings

Unit goal For learners to be able to make decisions about saving and borrowing using appropriate financial products and sources of help. Learning Outcomes The learner will be able to: 2.3 Demonstrate an understanding of short-term goals and how they differ from medium and long-term goals. 2.4 Recognise how to make informed purchasing decisions funded by credit or savings. Minutes Topic Activity Resources 15 Financial goals

- timespan Brainstorm items you might save up for in the short (up to 5 years), medium (5-10 years) and long (more than 10 years) term.

Flipchart, paper, pens

15 Financial goals - products

Discuss the financial products which may be suitable for the different timespans. Discuss the different types and levels of risk associated with the products e.g. losing capital, effect of inflation, shortfall.

30 Short-term savings

In pairs, use magazines/newspapers to find adverts for short-term savings products. For each list the features. Collate a list of products and features for whole group. Match the products against the short-term savings goals identified at the start of the session. Record in Key Facts file.

Magazines/newspapers Scissors

30 Interest Work through MGR topic Choose the Best Way to Save in pairs or as a whole group.

MGR

15 Break 30 Comparing

savings accounts - AER

In small groups come up with ways to remember what AER stands for and that the rates are used to compare savings accounts. Using the adverts found earlier in the session find the savings account with the highest rate. Discuss why you might not always choose the account with the highest rate.

25 How much to save to meet goal

Look up tables Work out how much to save a week/month to meet the short-term savings goals identified at the start of the session.

Handout 2C.1

30 Save or borrow?

Work through MGR topic Plan for a Purchase in pairs.

MGR

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

38

5 What next? Recap Next session will be looking at Choosing Financial Products

www.fsa.gov.uk/financial_capability/tools/fmf/index Choose: budgeting for the cost of children Note: See the Further Resources section for information on: MGR: Money-go-round CD ROM

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

39

Handouts for Unit 2

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

40

Handout 2a.1 - Borrowing Types and Sources of Borrowing

Types of Borrowing Sources of Borrowing

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

41

Handout 2b.1 - Debt Priority Debts

Mortgage (and other loans secured against your home) or rent

Council Tax

Gas and Electricity

Water

Income Tax or VAT arrears

Hire Purchase

Magistrates’ Court Fines

TV Licence

Maintenance to Support a Former Partner or Children

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

42

Loans from Family and Friends

Social Fund Loans, Benefit Overpayments

Unlicensed Lenders

Store Cards, Credit Cards and unsecured Personal Loans and Overdrafts

Business Debts

from http://www.moneymadeclear.fsa.gov.uk/print.aspx?Page=/tools/sorting_out_borrowing_problems The key to sorting out your borrowing problems is the five-step approach:

1) Work out the scale of the problem including which debts are a priority; 2) Draw up your budget; 3) Look for ways to increase your income and/or cut your spending 4) Contact creditors and offer to pay what you can afford (giving priority to your priority

debts), and 5) Don't let matters slide - get help if you need it.

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

43

Handout 2c.1 - Savings Look-up Tables How your weekly savings can build up

And you save this much each week: Amount you build up* if you save for

this long: £1 £5 £10 £25 £50

6 months £26 £132 £264 £660 £1,320 1 year £54 £268 £536 £1,339 £2,679 18 months £82 £408 £816 £2,039 £4,078 2 years £110 £552 £1,104 £2,759 £5,518 3 years £171 £853 £1,706 £4,264 £8,528 4 years £234 £1,172 £2,344 £5,859 £11,718 5 years £302 £1,510 £3,020 £7,550 £15,100

How your monthly savings can build up

And you save this much each month: Amount you build up* if you save for

this long: £1 £5 £10 £25 £50 6 months £6 £31 £61 £153 £305 1 year £12 £62 £124 £310 £619

18 months £19 £94 £189 £471 £943 2 years £26 £128 £255 £638 £1,276 3 years £39 £197 £394 £986 £1,972 4 years £54 £271 £542 £1,355 £2,709 5 years £70 £349 £698 £1,746 £3,491

* Tables show before-tax return assuming interest rate of 6% pa gross.

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

44

Useful Resources for Unit 2

Details of where to order resources can be found in Section 5: Resource Directory Dealing With Your Debts Background information on dealing with debt and setting up budgets Financial Products Resource Pack Savings and Credit Card sections providing realia related to products Making Ends Meet Topics on savings, loans and debt Money-go-Round – CD ROM Topics on saving and borrowing NatWest Face 2 Face with Finance – interactive materials and video clips Credit File Personal Finance Handbook Chapter 1 Financial Planning Chapter 3 Saving Chapter 4 Borrowing Short Programmes Saving for the Future - session plan looking at the numeracy and financial skills needed to look at options for saving. Paying for It All - session plan looking at the numeracy and financial skills needed to look at options for borrowing. www.direct.gov.uk/en/MoneyTaxAndBenefits Information on dealing with debt www.moneymadeclear.fsa.gov.uk Sections on savings, loans, comparing products, loan calculator and dealing with debt www.moneymatterstome.co.uk Money Matters 6. Risk and Return Section on savings and loans, including savings and loan calculators 7. Making Personal Life Choices Section on financial planning and debt www.nationaldebtline.co.uk Useful pack on dealing with debt problems

Unit 2 – Planning your Money

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

45

Key Skills

Opportunities for providing evidence for Key Skills Communication, Application of Number and ICT at Level 1: Borrowing Communication

C1.1 Take part in a group discussion on the different types and sources of borrowing available to consumers.

C1.2 Read text that outlines the cost of borrowing. C2.3 Complete an application form to obtain credit C2.3 Devise a mindmap which illustrates the different types of borrowing

Application of Number

N1.1 Gather numerical information from two sources (showing APR) to identify the best deal for obtaining a loan.

N1.2a,b,c Compare the data from the two sources N1.3 Interpret the results and present your findings, in two different ways

ICT

ICT1.1 Search the Internet to find details on costs of loans. ICT1.2 Use ICT to combine information from the internet and a non ICT

based information source to prepare article on the best deal. Send an email to teacher with draft article attached, for comment.

ICT1.3 Present findings in the form of an article for a student magazine, including an image and numbers.

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

46

Unit 3: Choosing products and Getting Help.

Unit goal For learners to be able to select between competing products and identify appropriate sources of advice and help. LEARNING OUTCOMES

ASSESSMENT CRITERIA

The learner will:

The learner can:

3.1 Be able to select between competing financial products.

3.1.a Distinguish between different products on the basis of cost, accessibility, risk and other terms.

3.1.b Access details of financial products from a range of

sources. 3.1.c Choose appropriate type/s of product which match

specified financial goals.

3.2 Know the sources of information and help that are available when making financial decisions.

3.2.a Choose between sources of information on financial products according to their purpose, independence and reliability.

3.2.b Identify the role of different types of intermediary

that are available to the consumer.

3.3 Know the sources of information and help that are available in the event of complaints about financial products.

3.3.a Identify whether or not a consumer has grounds for complaint for a given range of scenarios.

3.3.b Identify the key characteristics of the main

independent complaints bodies. 3.3.c Demonstrate awareness of the key characteristics

of the main compensation schemes.

3.4 Recognise how financial crime can affect the individual and understand how to protect against it

3.4.a Identify precautions the individual can take to reduce the risk of being a victim of fraud when: - paying by debit card - using online banking - using a cash machine.

3.4.b Recognise inaccurate transactions on statements.

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

47

Teachers Guidance

The Personal Finance Handbook and the FSA’s Money Made Clear11 website should provide you with the background knowledge to deliver the unit. Further resources that may be useful are also indicated. Full details for the resources can be found in Section 5. Session plans have been provided to illustrate possible activities that can be used to deliver this unit. Signposting to resources, tutor generated examples and exemplar handouts to support the sessions has been provided Each unit has 3 session plans of 3-hours each. The MOWE Personal Finance Hot Topic12, part 3 could be used at the start or finish of the unit to make up the guided learning hours to 10 for each unit. Flipchart, paper and pens given as standard but interactive whiteboard would be preferable if available. If possible each learner should keep a Key Facts file summarising information to be remembered along with definitions of key words. The following guidance referenced to the syllabus provides further details to help delivery of the unit.

11

www.moneymadeclear.fsa.gov.uk 12

www.mowe.org.uk

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

48

3.1 Comparing Financial Products The learner will be able to identify the main features that distinguish products and be able to select appropriate products using a variety of sources. 3.1.1 Main features a) Understand that a type of product is characterised by a set of features, some desirable,

some not. b) Understand that the precise features for a specific product generally vary from one

provider to another. c) Understand that the consumer may be able to alter some product features. d) Be able to describe a savings account in terms of its main features. e) Be able to describe a credit card in terms of its main features. f) Be able to describe an insurance policy (e.g car insurance) in terms of its main features.

Additional guidance Learners need to know :

• How to assess features by cost, accessibility, risks, other terms.

• Can change product by the way they choose to pay (eg credit card) or by changing cover or excess (insurance)

3.1.2 Sources of information a) Have knowledge of the main sources of information about product features. b) Be able to distinguish between information sources on the grounds of purpose,

independence and reliability. c) Be aware of how TV and print advertisements may influence choice d) Be able to use online comparative tables to select savings accounts for different

scenarios. e) Be able to use online comparative tables to select personal loans and credit cards for

given scenarios. f) Be wary of taking marketing claims at face value. g) Be confidently able to shop around for suitable deals. Additional guidance Learners need to know about:

• Main sources of information: in particular, TV and print advertisements, marketing literature, terms and conditions, key facts documents, comparative tables in newspapers and online.

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

49

3.2 Sources of information and help The learner will have a basic knowledge of the range of financial products available, where to get information and advice about them, and where to get help and advice with other financial decisions. 3.2.1 Financial goals a) Have knowledge of the range of financial goals that people are likely to have depending

on their household circumstances and stage of life. b) Identify typical goals in specified scenarios.

Additional guidance: 3.2.2 Financial products a) Have a basic knowledge of the types of financial product that may be useful in achieving

different goals. b) Match generic products to specified goals. Additional guidance Learners need to know :

• that FSA comparative tables cover only a limited range of products - e.g. they don’t include credit cards

• the definition of intermediary.

• a list of bodies that can be complained to where a product or service is outside the scope of the Financial Services Ombudsman.

• that FSO are approachable and will provide support to complete the forms. Financial Services Compensation Scheme, Compensation schemes for occupational pensions: Pension Protection Fund, Fraud Compensation Fund, Financial Assistance Scheme 3.2.3 Sources of advice and help a) Have knowledge of the main sources of advice and help and be able to distinguish

between them on the grounds of independence and cost. b) Understand the distinction between information and advice. c) Use the internet and paper-based directories to find contact details for sources of

advice. d) Evaluate sources of advice by independence and cost. e) Be confidently able to seek appropriate advice. f) Be confident rejecting inappropriate or unnecessary advice. Additional guidance Learners need to know: Have knowledge of the main sources of advice and help and be able to distinguish between them on the grounds of independence and cost, in relation to:

• debt-related goals(e.g. Citizens Advice Bureaux, Consumer Credit Counselling Service, National Debtline, other money advice centres)

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

50

• state benefits and claiming them(e.g. Citizens Advice Bureaux, Jobcentre Plus, The Pension Service)

• insurance (eg insurance brokers)

• savings and investments (eg independent financial advisers)

• Learners need to be aware of sources that lack independence, eg debt management companies, product providers, tied advisers (such as most banks and building societies).

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

51

3.3 Complaints The learner will know where to get advice and help when they have a complaint about a financial product.. 3.3.1 Making a complaint a) Be aware of the responsibilities of consumers and when a complaint is likely not to be

valid. b) Have knowledge of the complaints systems financial firms must offer. c) Have knowledge of the Financial Ombudsman Service (FOS) and its scope. d) Have knowledge of other bodies dealing with complaints outside the FOS scope. e) Be able to use the internet and paper-based directories to find the contact details of

FOS and other independent complaints bodies. f) Be able to write a letter of complaint for a given scenario. g) Be confident making a complaint.

Additional guidance: Learner needs to know:

• Circumstances in which a consumer might have a valid claim or might not have a valid claim under FOS or other complaints schemes.

3.3.2 Redress a) Have knowledge of compensation schemes and when they might apply. Additional guidance: Learner needs to know:

• For Financial Services Compensation Scheme: the maximum amounts of compensation payable and in what circumstances.

• For compensation schemes covering occupational pension schemes, the circumstances in which a claim might be made, including relevant dates.

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

52

3.4 Financial crime The learner will understand how to operate financial products safely in order to protect himself/herself from fraud. 3.4.1 Financial crime a) Understand how to operate a bank or savings account safely. b) Be able to check a bank statement for accuracy. Additional guidance Learners need to know about:

• keeping PINs safe, operating a cash machine safely, operating an online account safely, checking statements, disposing of documents carefully

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

53

Session Plans for Unit 3

Choosing Financial Products Unit goal For learners to be able to select between competing products and identify appropriate sources of advice and help. Learning Outcomes The learner will be able to 3.1 Be able to select between competing financial products. Minutes Topic Activity Resources 15 What are

financial products?

In small groups, identify from sets of adverts which are for financial products and draw up list of the types of financial products. Record in Key Facts file.

Adverts

30 Features of financial products

In pairs, each take one of the adverts for a savings account, a credit card and an insurance policy and identify the features, using highlight pens. Compare the features found within the whole group to come up with a list of main features for savings accounts, credit cards and insurance policies. Record in Key Facts file.

Adverts Highlight pens

30 Sources of information - TV

Watch a number of adverts for financial products. eg: www.visit4info.com http://tvs-worst-adverts.co.uk http://www.nationalarchives.gov.uk/films/1979to2006/filmpage_dummy.htm Whilst watching ask group to make a note of any of the main features of the products mentioned. Compare results. Discuss how the adverts will influence choice.

TV/video / Internet

15 Sources of information - print

In pairs re-visit adverts used earlier in the session. How will these adverts influence choice and what other information would you need to make an informed choice?

Adverts

15 Break 30 Sources of

information - online

In pairs search for information on a financial product online. What types of sites come up as a result of the search? Make a note of the sites and comment on purpose, independence and reliability.

Access in pairs to Internet

35 Comparative tables

Model using a comparative table to select a savings account, a personal loan and a credit card. In pairs select a savings account, a personal loan

Access in pairs to Internet www.fsa.g

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

54

and a credit card for a given scenario. Justify to others in small group why chose particular products for own scenario. For savings, personal loans and credit cards, could use www.moneyfacts.co.uk. For savings could use FSA tables - note that PPI being added at some time.

ov.uk/tables : Savings

20 Sources of information - comparison

Look back at the different sources of information – do any others need adding to list of sources. Which would individuals use in future? Make a note in Key Facts file of preferred source of information.

5 What next? Recap Next session will be looking at Sources of Advice.

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

55

Sources of Advice Unit goal For learners to be able to select between competing products and identify appropriate sources of advice and help. Learning Outcomes The learner will be able to 3.2 Know the sources of information and help that are available when making financial decisions.

Minutes Topic Activity Resources 5 Life stages Either draw on paper/board or create a

timeline on floor. Mark off different life stages.

15 Financial goals Work in small groups to identify typical financial goals for each stage.

Handout 3B.1

15 Financial products

Small groups identify for each financial goal appropriate generic financial products.

40 Seeking advice As whole group or in pairs work through MGR – Talk to Experts

MGR

15 Information v advice

Discuss the difference between information and advice.

15 Break

30 Sources of advice

Small groups identify where it would be best to get advice for the products they have identified earlier. Identify whether advice has a cost and is independent. Compare and update information gathered. Put handout in Key Facts file.

Access to Internet Telephone directories

30 Meeting an adviser

In pairs, role play meeting an adviser to talk about one of the products identified earlier. Use appropriate questions from the Talk to Experts section of MGR. Take it in turns to be the adviser and client.

Question cards (available in Short Programmes)

25 Practice test Individuals to have a go at practice test so that areas that need re-enforcing can be identified.

Practice test

5 What next? Recap Next session will be looking at Complaints.

Note: See the Useful resources section for information on: MGR: Money-go-round CD ROM

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

56

Complaints Unit goal For learners to be able to select between competing products and identify appropriate sources of advice and help. Learning Outcomes The learner will be able to: 3.3 Know the sources of information and help that are available in the event of complaints about financial products. 3.4 Recognise how financial crime can affect the individual and understand how to protect against it.

Minutes Topic Activity Resources 15 When to

complain? Brainstorm when you might complain about a financial product.

10 Making a complaint

Input on making a complaint based on FSA’s section on Making a Complaint www.moneymadeclear.fsa.gov.uk/guides/making_a_complaint

20 Financial Ombudsman Service

In pairs visit the site for the Financial Ombudsman Service (FOS) - www.financial-ombudsman.org.uk . Identify which types of complaints the FOS covers. Record in Key Facts file.

Internet access for pairs

15 Other bodies dealing with complaints

Input on bodies dealing with complaints outside the FOS scope. Record in Key Facts file.

15 Financial Services Compensation Scheme

In pairs visit the site for the Financial Services Compensation Scheme (FSCS) - www.fscs.org.uk . Use the flowchart to find out when compensation may be available. Make a note of anything not understood. Share findings.

15 Break

40 Writing letters of complaint

Split the group into two. One half work through www.moneymatterstome.co.uk Consumer Rights and Responsibilities section on Buying Goods and the other half work through section on Buying Services and then compare notes. Complete a letter of complaint based on one of the sample letters. Put copies of sample letters in Key Facts file.

Copies of sample letters from MMtoM

45 Financial crime

Brainstorm scams and swindles to get access to your personal and banking information. Come up with a list of 10 tips to avoid being a victim of financial crime. Make posters to alert others. In teams try the Office of Fair Trading quiz on scams. Prizes for the winners. www.oft.gov.uk/oft_at_work/consumer_initiatives/scams/

Paper, pens, magazines, scissors, glue

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

57

scam-quiz

5 What next? Recap Where next?

Note: See the Useful resources section for information on:

• MMtoM: MoneyMattersToMe website

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

58

Handouts for Unit 3

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

59

Handout 3b.1 - Borrowing Advice on Financial Products Life Stage Goal(s) Product(s) Advice Source:

Cost: (Free, Commission or fee) Independent:

Source: Cost: (Free, Commission or fee) Independent:

Source: Cost: (Free, Commission or fee) Independent:

Source: Cost: (Free, Commission or fee) Independent:

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

60

Useful resources for Unit 3

Details of where to order resources can be found in the Resource Directory Financial Products Resource Packs Insurance, Savings, Credit Card Money-go-Round – CD ROM Topics on getting advice Personal Finance Handbook Chapter 1 Financial Planning Chapter 2 Everyday Money Chapter 3 Saving Chapter 4 Borrowing Chapter 6 Insurance Chapter 7 Getting Advice Chapter 11 Protecting consumers Short Programmes Need Advice? - session plan looking at the literacy and financial skills needed when seeking advice www.consumerdirect.gov.uk Government funded site and phone line to help with consumer advice www.direct.gov.uk/en/MoneyTaxAndBenefits Information on managing money: including comparing products, making complaints and keeping money secure www.moneymadeclear.fsa.gov.uk Sections on comparing products, making a complaint, getting financial advice and staying safe www.moneymatterstome.co.uk 8. Consumer rights and responsibilities

Unit 3 – Choosing Products and Getting Help

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

61

Key Skills

Opportunities for providing evidence for Key Skills Communication, Application of Number and ICT at Level 1: Communication

C1.1 Take part in a group discussion on how to choose a financial product.

C1.2 Read texts about a product and summarise the relevant information. C1.3 Write a letter/email asking for further information. (The email could be

used for ICT to show purposeful use of email). C1.3 Write a short report about the product .

Application of Number N1.1 Interpret numerical information from two different sources to help

choose a savings product (one source must be a table, graph, chart or diagram.

N1.2a,b,c Compare the data from the different sources. Calculate simple interest and compare products

N1.3 Interpret the results and present your findings

ICT ICT1.1 Search on the internet for information on two financial products. ICT1.2 Enter the information about the products into a table. ICT1.3 Present the information, including text, image and number. (This could

be the report for C1.3, email could be used to send information to the teacher)

.

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

62

5. Resource Directory

Title

Publisher Price Ordering details

Mapped to AFCaF/ Key Skills/ Lit/Num CC

Adult Financial Capability Framework A1957

Basic Skills Agency

Free

www.basic-skills.co.uk/ouractivities/financialliteracy or phone 0870 600 2400

Adult Lit/Num CC E3/L2

Colossal Cards A1407

Basic Skills Agency

£10.00 www.basic-skills.co.uk/ouractivities/financialliteracy or phone 0870 600 2400

AFCaF Levels B/D Adult Lit/Num CC E3-L2

Dealing With Your Debts

National Debtline

Free (single copies)

Download or order from www.nationaldebtline.co.uk

N/a

Direct Payment Pack A1705 (English), A1706 (Welsh)

Basic Skills Agency

Free www.basic-skills.co.uk/ouractivities/financialliteracy or phone 0870 600 2400

AFCaF Levels B/D Adult Lit/Num CC E3-L2

Financial Products Resource Packs A1961

Basic Skills Agency

Free www.basic-skills.co.uk/ouractivities/financialliteracy or phone 0870 600 2400

AFCaF Levels B/D Adult Lit/Num CC E3-L2

Making Ends Meet

Axis Education

£39.95 Avanti Books Tel: 01438 747000 Fax: 0143 8741131 Email: [email protected] http://www.avantibooks.com Address: Unit 9, The iO Centre, Whittle Way, Arlington Business Park, Stevenage SG1 2BD

Adult Lit/Num CC E1-L1

NatWest Face 2 Face with Finance materials

National Westminster Bank Plc

Free Order from www.natwestf2f.com

Key Skills L1/L2

Personal Finance Handbook

Child Poverty Action Group

£14.00 ISBN 1-901698-74-2 (2nd edition due out October 2007)

AFCaF Levels D/E

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

63

Title

Publisher Price Ordering details

Mapped to AFCaF/ Key Skills/ Lit/Num CC

Short Programmes A1958

Basic Skills Agency

Free www.basic-skills.co.uk/ouractivities/financialliteracy or phone 0870 600 2400

AFCaF Levels B/D Adult Lit/Num CC E2-L2

CD ROMs Money-go-Round

Basic Skills Agency

£10 www.basic-skills.co.uk/ouractivities/financialliteracy or phone 0870 600 2400

AFCaF Levels B/D Adult Lit/Num CC E3-L1

Websites Adult Financial Literacy Resource Centre website

www.fin-lit-resources.org.uk

Citizens Advice website www.adviceguide.org.uk Consumer advice site www.consumerdirect.gov.uk

Consumer Credit Counselling Service www.cccs.co.uk Compare prices on a wide range of financial products

www.moneyfacts.co.uk

Financial advisers and general personal finance

www.mylocaladviser.com

Financial advisers – list of independent financial advisers

www.unbiased.co.uk

Financial Literacy website www.basic-skills.co.uk/ouractivities/financialliteracy

Financial Ombudsman Service www.financial-ombudsman.org.uk Financial Services Authority – consumer site

www.moneymadeclear.fsa.gov.uk

Forum for all those engaged in financial learning for adults

www.niace.org.uk/spondoolies

Financial Services Authority –for those delivering financial capability

www.fsa.gov.uk/financial_capability

HM Revenue & Customs www.hmrc.gov.uk Money Matters To Me (NIACE) www.moneymatterstome.co.uk Move On With Equal Personal Finance section

www.mowe.org.uk

National Debtline www.nationaldebtline.co.uk

Support and information about dealing with money

www.moneyadvicetrust.org

UK government site with information on wide range of topics and links to all public services

www.direct.gov.uk

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

64

6. Coverage of the Adult Financial Capability Framework

Component Developing level Unit 1 Unit 2 Unit 3

Different types of money/payments (a)

1. Understand that money means different things to different people.

2. Understand that cash isn’t the only way to pay for goods and services and recognize the alternatives.

3. Understand different forms of payment including cheques, cheque guarantee cards and debit cards.

4. Understand and compare different forms of payment including standing orders and direct debit arrangements.

5. Understand the key words credit and debt and relate these terms to savings, borrowing currently undertaken.

1.4.1 1.3.1/1.4.1 1.3.1 1.3.1/1.4.1

2.3.3 2.2.1/2.3.1

Income generation (b)

1. Understand how earnings and salaries are calculated. 2. Understand there are different forms of benefit, how they

are paid for and how to access them. 3. Begin to understand the need for retirement provision

1.1.2/1.2.2 1.1.3 1.1.2/1.2.2

2.3.2

Income disposal (c)

1. Understand personal expenditure and how to manage it. 2. Understand why money, such as tax or pension

contributions is deducted from earnings. 3. Begin to understand local and national taxation and

spending.

1.4.1 1.1.2/1.2.2

2.2.1/2.4.1

Gathering financial information and record keeping (d)

1. Understand keeping money in an account, eg, bank, post office, building society, credit union.

2. Know about some official financial records, eg, bank statements, ATM services, credit card vouchers, etc.

3. Know about personal financial statements and other ways of recording income and expenditure.

4. Able to check for accuracy bank statements, utility and other bills.

1.3.1 1.1.2/1.2.2/1.3.2/1.3.1 1.4.1 1.4.1

2.3.3 2.3.3 2.3.3

3.4.1 3.4.1

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

65

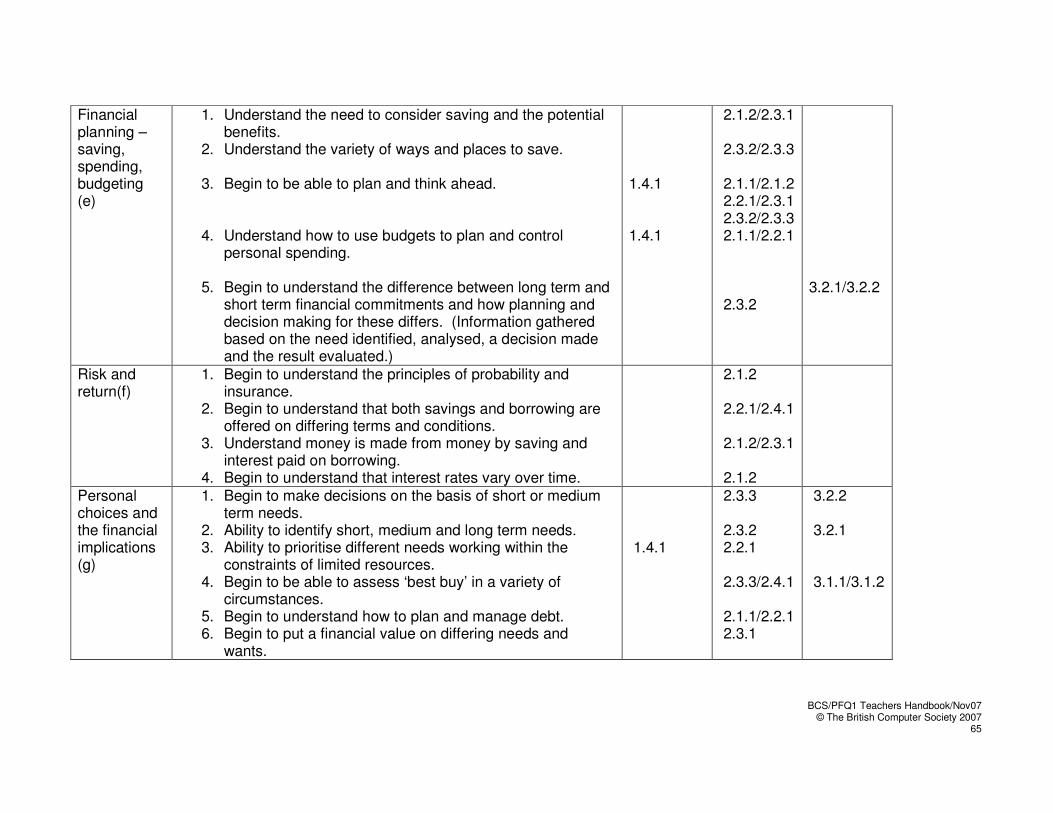

Financial planning – saving, spending, budgeting (e)

1. Understand the need to consider saving and the potential benefits.

2. Understand the variety of ways and places to save. 3. Begin to be able to plan and think ahead. 4. Understand how to use budgets to plan and control

personal spending. 5. Begin to understand the difference between long term and

short term financial commitments and how planning and decision making for these differs. (Information gathered based on the need identified, analysed, a decision made and the result evaluated.)

1.4.1 1.4.1

2.1.2/2.3.1 2.3.2/2.3.3 2.1.1/2.1.22.2.1/2.3.12.3.2/2.3.3 2.1.1/2.2.1 2.3.2

3.2.1/3.2.2

Risk and return(f)

1. Begin to understand the principles of probability and insurance.

2. Begin to understand that both savings and borrowing are offered on differing terms and conditions.

3. Understand money is made from money by saving and interest paid on borrowing.

4. Begin to understand that interest rates vary over time.

2.1.2 2.2.1/2.4.1 2.1.2/2.3.1 2.1.2

Personal choices and the financial implications (g)

1. Begin to make decisions on the basis of short or medium term needs.

2. Ability to identify short, medium and long term needs. 3. Ability to prioritise different needs working within the

constraints of limited resources. 4. Begin to be able to assess ‘best buy’ in a variety of

circumstances. 5. Begin to understand how to plan and manage debt. 6. Begin to put a financial value on differing needs and

wants.

1.4.1

2.3.3 2.3.2 2.2.1 2.3.3/2.4.1 2.1.1/2.2.1 2.3.1

3.2.2 3.2.1 3.1.1/3.1.2

BCS/PFQ1 Teachers Handbook/Nov07 © The British Computer Society 2007

66

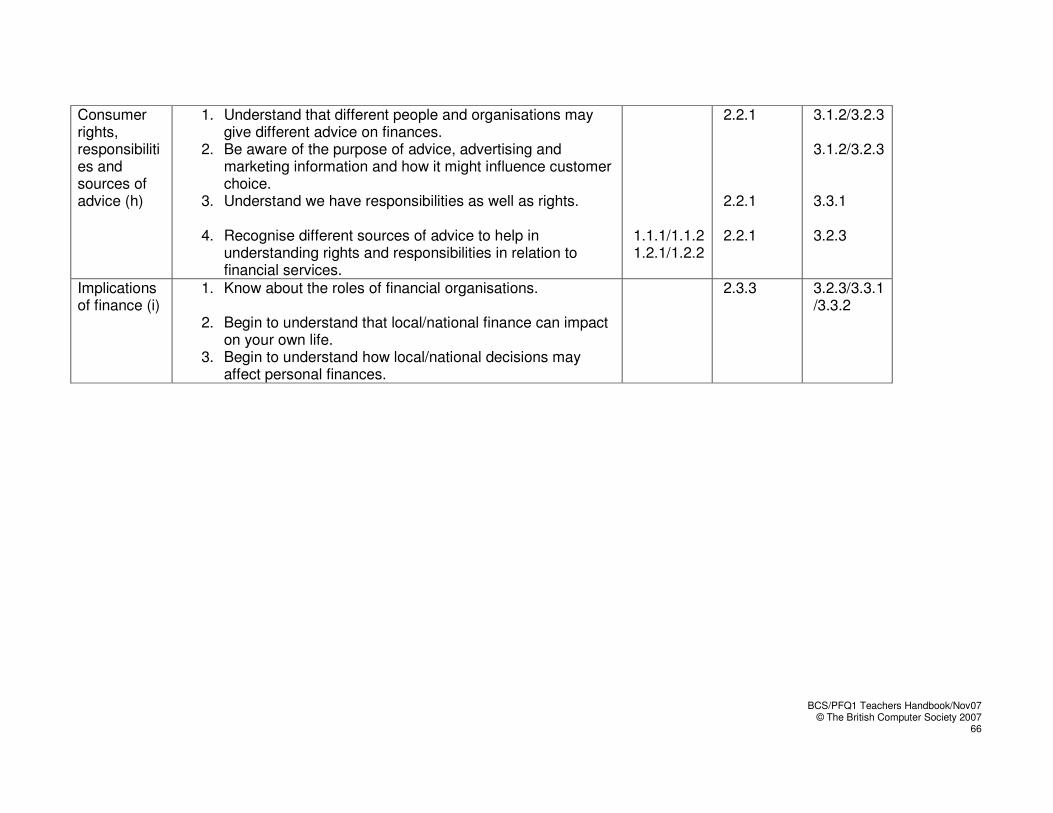

Consumer rights, responsibilities and sources of advice (h)

1. Understand that different people and organisations may give different advice on finances.

2. Be aware of the purpose of advice, advertising and marketing information and how it might influence customer choice.

3. Understand we have responsibilities as well as rights.