leuthold global clean technology fund - … · leuthold global clean technology fund ... where the...

TRANSCRIPT

Leuthold Global Clean Technology Fund

Investors should consider the investment objectives, risks, charges and expenses of the investment company carefully before investing. The Prospectus contains this and other information about the

Funds. For current Prospectus, call toll-free, 1-800-273-6886, or download from our web site:www.LeutholdFunds.com. Please read the Prospectus carefully before you invest.

Not FDIC Insured. No Bank Guarantee. May Lose ValueMutual Fund Distributor: Rafferty Capital Markets, LLC, Garden City, NY 11530

DOFU: 11/20/2009

For Professional Use Only. Do Not Distribute.

Leuthold Weeden Capital Management Overview

Leuthold Weeden Capital Management (LWCM), based in Minneapolis, MN, has been managing assets since 1987. Total firm assets are approximately $3.9 Billion.

• Tactical asset allocation strategies

• Long only equities, short only equities, long/short

• Experienced Investment Professionals and Client Focused

– Steve Leuthold has over 40 years of experience in the investment field and Portfolio Managers have been at the firm on average 13 years.

– We have closed strategies at relatively small sizes to maintain flexibility.

LWCM Affiliations

• Leuthold Weeden Institutional Research– Founded in 1981—An institutional investment research firm, Leuthold’s

research is led by Steve Leuthold and conducted by a staff of eight analysts.

– Our proprietary research includes technical and quantitative analysis, broad sector and industry group analysis, earnings momentum, supply/demand dynamics, valuation studies, etc.

• Weeden & Co., L.P.– Founded in 1932—exclusively an institutional trading firm based in

Greenwich, CT.

2

Our Strategy for CleanTech

• Blend top-down, quantitative & technical investment prowess with bottom-up fundamental expertise and CleanTech-specific knowledge

– Co-Portfolio Managers: Steve Leuthold & Eric Bjorgen– CleanTech veteran investor: David H. Kurzman– Fundamental analyst: Jun Zhu

Steve Eric David Jun

• Identification of trends is the first step to profiting from them.

• Market and socio-political environment have matured sufficiently to justify a sector-specific fund.

• We believe Clean Technology is one of the most important investment opportunities for the world economy for the next several decades.

We have a history of identifying investment themes:

Build the Right Team

3

Our Strategy for CleanTech

• Achieve capital appreciation & long-term growth by investing globally primarily in common stocks

– We are in this to make money for our investors

• Leverage our traditional group rotation strategies

• Build a “best-in-class” portfolio of global CleanTec h companies

– This requires substantial bottom-up stock picking effort that is directed by a macro economic, geo-political, and financial market understanding.

• Anticipate the changing market

– This market is very dynamic, changing in quality and substance.

– There will be no magic-bullet solution that will “fix” our energy, water, transportation, and pollution problems; requires broad thinking across numerous markets.

How we are different from other CleanTech investors :

• We are not a private equity or venture capital vehicle

– Looking for proven business models, savvy managers, & revenue growth

• We are not large-cap, conglomerate focused

– The great majority of our best ideas will likely be “S/Mid-cap” companies– Identifying stocks where the CleanTech revenues “move the needle”

• We are not a U.S.-focused fund

– We will typically have at least 40% of assets invested in foreign securities

4

CleanTech Market Overview

Defining Clean Technology

• Any technology or service that reduces humans’ impact on the environment

• When we say CleanTech, most people think of Alternative Energy, but…

– CleanTech is very diverse

– Encompasses part of many existing industrial sectors, including transportation, energy transmission & storage, water treatment, pollution control, advanced materials, recycling, and many others.

Addressable Markets

• Is the CleanTech universe of public companies investable?

– Yes!

– >400 publicly traded stocks represent $800B of market capitalization

• Excludes ~$500B of market capitalization from Diversified-sector companies (CleanTech conglomerates, ETFs, “green” funds, etc.)

• A growing universe, as VC/private equity companies will “graduate”

– It’s great to have progressive ideals, but we exclude companies:

• …with CleanTech business groups that do not represent a significant contribution to revenues/profits

• …simply because they adopted green technologies or recycle wastes• …because they implemented employee-progressive programs

5

Why We Launched Our CleanTech Fund

There are numerous market drivers

• The basic laws of economics (drive for productivity & efficiency)

• Political motivation (multi-governmental; Obama administration would like to invest $150 Billion over next ten years on clean energy)

• Consumer demand (is green the new “luxury” for the developed world?)

• Corporate agendas (green-colored glasses & “green washing”)

• Technological advancement (demand for energy; cost reductions)

• Social stimuli (rising living standards) New “Americums”

• Global climate change (socio-political consciousness; self-preservation)

• Population growth (U.S. Census Bureau estimates the approximate 6 billion world population in 1999 will be about 9 billion by 2040)

• Higher fossil fuel prices

6

Leuthold Global Clean Technology Fund

Investment Objective - The Leuthold Global Clean Technology investment objective is to achieve capital appreciation and long term growth by investing globally primarily in common stocks; our investment emphasis is price appreciation.

• The Leuthold Global Clean Technology strategy will allocate its assets primarily in companies that we believe will benefit from the expected growth in spending and investment in energy efficient and “clean” technologies, innovations and solutions.

• The Leuthold Group has experience investing in environmentally focused firms since the 1990s as part of our quantitative Select Industries group rotation style of investing.

• The strategy will typically invest at least 40% of its assets in securities from international markets.

7

Leuthold Global Clean Technology Fund

• Universe: Over 400 global firms

– Fund universe will continue to expand as new technologies, new markets, and new entrants emerge.

• Four Primary Sectors

– Alternative Energy– Resource Conservation– Clean Water– Clean Environment

• Invests in micro cap to large cap companies

• To help enhance the strategy, our universe is organ ized in approximately 30 different sub-industries.

8

Sub-Industry Detail (10/09)

Leuthold Global Clean Technology Strategy

Number Of Percent Of Market Percent OfCompanies Universe Cap (Mil. ) Universe

Alternative Energy (Totals) 240 50.1% $610,918 44.6%

Biofuels/Ethanol/Cellulosic/Synthetic 33 6.9% 51,576 3.8%Clean Power Storage, Delivery Technology 9 1.9% 7,612 0.6%Construction & Eng-Alt Energy Plants 15 3.1% 25,829 1.9%Div. Renewable Power Generation/Developers 37 7.7% 267,684 19.6%Fuel Cells 15 3.1% 1,183 0.1%Geothermal 10 2.1% 4,452 0.3%Hydro Electricity/Tidal 6 1.3% 22,653 1.7%Nuclear Energy Equipment & Services 7 1.5% 27,234 2.0%Renewable & Conventional Power Generation-Systems, Controls 20 4.2% 68,494 5.0%Renewable Power Generation-Support & Services 1 0.2% 33 0.0%Solar-Materials & Components 21 4.4% 41,407 3.0%Solar-Photovoltaic Cells, Wafers, Panels 36 7.5% 35,964 2.6%Turbines, Flywheel, Energy Transmission 3 0.6% 378 0.0%Uranium Mining 10 2.1% 20,989 1.5%Wind Turbines & Components/Wind Power 17 3.5% 35,430 2.6%

Resource Conservation (Totals) 82 17.1% $69,259 5.1%

Batteries/Energy Storage Systems 18 3.8% 9,097 0.7%Efficient Lighting/LEDs 11 2.3% 10,835 0.8%Energy Efficiency/Conservation Products 20 4.2% 27,593 2.0%Energy From Waste/Biomass/Synthetic 12 2.5% 5,897 0.4%Recycling and Recycling Products 15 3.1% 12,329 0.9%Water Conservation Systems, Technology 6 1.3% 3,507 0.3%

Clean Water (Totals) 55 11.5% $82,241 6.0%

Clean Water, Water Treatment Technologies 24 5.0% 30,586 2.2%Water Infrastructure Rehabilitation 6 1.3% 8,042 0.6%Water Utilities 25 5.2% 43,614 3.2%

Clean Environment (Totals) 45 9.4% $75,230 5.5%

Clean Agriculture 4 0.8% 4,158 0.3%Clean Transportation, Components, & Systems 12 2.5% 20,612 1.5%Environmental Services 15 3.1% 41,746 3.0%Pollution and Emissions Controls & Monitors 14 2.9% 8,715 0.6%

Diversified (Totals) 57 11.9% $531,173 38.8%

Conglomerates 30 6.3% 523,584 38.3%Investment, ETFs, Funds, Envir. Trading 27 5.6% 7,589 0.6%

9

Portfolio Construction

• Portfolio construction utilizes fundamental analysis along with industry group analysis, other quantitative methodology, and macro outlooks in a dynamic process.

• Quantitative analysis is utilized for screening, where the focus is growth potential.

• Industry group analysis and macro outlook help determine emerging leadership that could lead to buying more on an industry scale rather than individual stock picking.

– Modified weighted group charts used to identify industry-level strength and weakness.

• Stocks exhibiting desired growth characteristics are analyzed for leadership potential, proprietary and technological advantages, financial condition, sales and earnings growth potential as well as their economic, political and regulatory environments.

• Country and market cap exposures driven by stock selection.

10

Selling Strategy

Stock Level Factors

• Firm fails to achieve its assumed objectives of growth.

• Stock price of an individual position lags that of its peers.

• Market share deterioration.

• Balance sheet deterioration.

• Execution Issues.

Industry/Macro Factors

• May look to sell entire industry exposures due to influences that are expected to negatively impact all/most stocks in a group.

• Expected to be used less frequently than stock level sell decisions, but at times, could be significant.

• Examples of macro influence may include:

– Tax policies and/or subsidies

– Changes in the prevailing or expected cost of substitutes

– Changes in regulations

– Technology breakthroughs

11

Strategy by Leuthold Sectors as of 10/31/09

Leuthold Global Clean Technology Strategy

12

Alternative Energy53%

Clean Water8%

Clean Environment

10%

Resource Conservation

10%

Cash1%Diversified

11%

Two Classes of Shares

Retail Class: LGCTX

• New Accounts: $10,000 min. ($1,000 min. for IRA accounts)

• Existing Accounts: $50 Automatic Investment Plan “AIP” ($100 for non-AIP)– Dividend Reinvestment: No minimum

• Available on numerous platforms, including:– Ameriprise — Prudential– Charles Schwab — Raymond James– E*Trade — RBC Dain Rauscher– Fidelity — Scottrade– LPL — TD Ameritrade– Pershing — Vanguard

Institutional Class: LGCIX

• Account minimum $1 million (including IRAs)

Disclosures

• Investing in foreign securities presents risks that may be greater than U.S. securities. These risks include, but are not limited to, currency rate fluctuations, regulatory differences, accounting standards, higher trading costs, and political risks.

• Investing in developing or emerging markets involves risks different from, or greater than, risks of investing in developed foreign countries, such as smaller capitalization, periods of illiquidity, significant price volatility and restrictions on foreign investments.

• Investing in small and midsized companies can involve such risks as having less publicly available information, higher volatility, and less liquidity than in the case of larger companies.

• Funds that concentrate investments in a certain sector may be subject to greater risk than funds that invest more broadly, as companies in that sector may share common characteristics and may react similarly to market developments or other factors affecting their values. Overweighting investments in certain sectors or industries increases the risk of loss due to general declines in the prices of stocks in those sectors or industries.

• Investors should consider the investment objectives, risks, charges and expenses of the investment company carefully before investing. The Prospectus contains this and other information about the Funds. For current Prospectus, call toll-free 1-800-273-6886, or go to www.LeutholdFunds.com. Please read the Prospectus carefully before you invest.

Not FDIC Insured ~ No Bank Guarantee ~ May Lose ValueDistributor: Rafferty Capital Markets, LLC, Garden City, NY 11530

13

Investment Professionals

Steven C. Leuthold

Steve has been an investment strategist, manager, and researcher for over 40 years. From 1969 to 1977, he was an officer and investment strategist at Piper, Jaffray & Hopwood. From 1977 to 1981 he was an officer and portfolio manager of two mutual funds for Criterion Investment Management. In 1981 Steve founded The Leuthold Group, an investment research firm where he leads a research team that uses quantitative historical research to develop sophisticated investment models. Steve is also CIO of LWCM and a Portfolio Manager for The Leuthold Funds, Inc.

Steve is the author of many books and articles, including The Myths of Inflation and Investing and Index Funds, the Risks and Pitfalls. He has been a frequent contributor to leading trade journals, including Barron’s, Corporate Report, The Journal of Portfolio Management and the Financial Analysts Journal. In 1999, Mr. Leuthold and Leuthold team member, Eric Bjorgen, CFA, co-authored a special study, Corporate Insiders’ Big Block Transactions, for which they won the prestigious Charles H. Dow Award. In addition, Steve Leuthold’s Financial Analyst Journal article “Inflation, Deflation and Interest Rates,” was awarded the 1982 Graham and Dodd Scroll by the Financial Analysts Federation.

Eric Bjorgen, CFA

Eric is a Senior Analyst and Co-Portfolio Manager for the Leuthold Core, Asset Allocation, Select Industries Fund, Undervalued & Unloved, and Global Clean Technology Funds. He is a member of the investment strategy committee, a key contributor to the monthly Perception for the Professional publication.

In 1999 Eric was a co-author with Steve Leuthold of the Corporate Insiders’ Big Block Transactions special study, which won the prestigious Charles H. Dow award. A graduate of the University of Minnesota’s Carlson School of Management with a BS in Finance, Eric is also a CFA charterholder and a member of the CFA Society of Minnesota.

David Kurzman

David is a Senior Analyst at the Leuthold Group focusing on our Global Clean Technology Fund. Prior to joining the Leuthold team, David was Managing Partner of Kurzman CleanTech Research, a private research and consulting firm, and managed a pool of private capital for high-net worth investors.

David has held a number of research positions in Clean Technology areas including Senior Vice President of the Clean Technology Research Group for Panel Intelligence, LLC, and sell-side analyst for Needham & Co. and H.C. Wainwright & Co. David was also an Analyst at Value Line Inc. and the Weitz Funds, an Omaha-based mutual fund company.

David’s work has been recognized by leading news channels, including CNBC, PBS’, Bloomberg News, Reuters, The New York Times, The Wall Street Journal, Barron’s Financial Weekly and others. David was named “Best On The Street” by The Wall Street Journal in 2003 for the area of Electronic Components & Equipment, was rated as a Zack’s All-Star Analyst in 2001 and 2002.

Jun Zhu

Jun joined The Leuthold Group, LLC, as a Senior Analyst in 2008. Prior to joining the Leuthold team, she worked as an investment intern at Riverbridge Partners in Minneapolis. At The Leuthold Group, she contributes to Leuthold research publications, group analysis, and is a member of the investment strategy committee.

Jun received her MBA from the Applied Security Analysis Program at the University of Wisconsin-Madison, where she co-managed a $60 million university endowment fund run by students in the program. She also earned an MS degree in Biomedical Sciences from the University of Wisconsin, and a BS degree from Sichuan University in China. Jun has worked on several biotechnology research projects at leading institutes both in China and the United States. She brings strong analytical skills, industry experience and an international background to the Leuthold team. Jun is currently a level three CFA Candidate.

14

Investment ProfessionalsAndy Engel, CFAAndy Engel is a Co-Portfolio Manager of the Leuthold Core Investment Fund and the Leuthold Asset Allocation Fund, as well as a Senior Analyst for The Leuthold Group, LLC. With more than 20 years of investment experience, he has assisted in the development and ongoing monitoring of a number of Leuthold asset allocation tools, and the formulation of strategy disciplines used in each of the Leuthold investment methodologies. Andy also serves as a member of the strategy committee which directs the investment decisions of the managed portfolios.

Andy is frequently used as a resource for input by the financial press, performs speaking engagements to various organizations throughout the U.S., and has appeared on CNBC a number of times. A 1982 graduate of Carleton College with a BA in Political Science, Andy is a CFA charterholder and a member of the CFA Society of Minnesota.

Jim Floyd, CFAJim is a Senior Analyst for The Leuthold Group, LLC, and Co-Portfolio Manager of the Leuthold Undervalued & Unloved Fund and Select Industries Fund. With over 30 years of experience, Jim specializes in quantitative analysis and equity/fixed income research. In addition to authoring various institutional financial publications and articles, Jim designs custom analysis on investment themes, produces inventive techniques for assessing market dynamics, and plays a role on the investment strategy committee.

Jim has built a reputation among the financial media as a knowledgeable resource; he is frequently cited in leading trade journals and publications, and has made many presentations and speaking appearances throughout the country. Jim is a CFA charterholder and a member of the CFA Society of Minnesota. He holds both BS and MS degrees from the University of Minnesota.

Doug Ramsey, CFADoug joined The Leuthold Group, LLC in late 2005. He is Director of Research at The Leuthold Group and Co-Portfolio Manager of the Leuthold Global Fund. Prior to joining the Leuthold team, he was Chief Investment Officer of Treis Capital in Des Moines, Iowa, where he managed equity portfolios and published a quantitative equity research product, The Behavioral Strategist.

Doug is a Phi Beta Kappa graduate of Coe College in Cedar Rapids, IA, where he majored in Economics and Business Administration. He also played four years of varsity basketball at Coe, earning Academic All-America honors in 1986-87. He then earned an MA degree in Economics from The Ohio State University in 1990. Doug earned his CFA designation in 1996 and became a Chartered Market Technician in 2003. Prior to coming to the Leuthold Group Doug was a Portfolio Manager at Principal Global Investors.

Matt Paschke, CFAMatt is a Senior Analyst for The Leuthold Group, LLC, and Co-Portfolio Manager of the Grizzly Short Fund, Leuthold Asset Allocation Fund, Leuthold Select Equities Fund and Leuthold Global Funds. Matt contributes to the compilation of the Group Selection Scores, the Major Trend Index and the Vulnerability/Opportunity Index. He is responsible for back-testing the various components used as input for the quantitative investment methodologies, and a member of the investment strategy committee.

Matt began his career at Honeywell prior to joining The Leuthold Group in 2000. He is a CFA charterholder and a member of the CFA Society of Minnesota. He is an honors graduate of the University of Northern Iowa with a BA in Finance and a minor in Math. Matt received an MBA from the University of Minnesota’s Carlson School of Management.

Greg Swenson, CFAGreg is a Co-Portfolio Manager of the Leuthold Grizzly Short Fund. He joined The Leuthold Group in 2006 and is a Senior Research Analyst. Before joining the Leuthold Group, he worked for FactSet Research Systems in Chicago as a Consultant and Account Executive. While working for FactSet Greg worked extensively with the research team at Leuthold. Greg is a CFA charterholder and graduated with honors from the University of Iowa with a Bachelor of Business Administration in Finance.

Chun Wang, CFA, PRMChun joined The Leuthold Group, LLC in June 2009 as a Senior Analyst. Prior to joining the Leuthold team, Chun was a Quantitative Equities Portfolio Manager and Head of Quantitative Research at LIM Advisors, a Hong-Kong based Asia-Pacific focused multi-strategy hedge fund. Prior to that, Chun was with Ned Davis Research for 11 years as Director of Research & Development, responsible for quantitative product development and a quantitative research publication called Quantitative Review. Chun also worked as an equity analyst with Shanghai International Securities in China.

In addition to his global experience, Chun has a BS degree in Economics from Xiamen University and a MS degree in Economics from the University of Florida. Chun holds a number of professional designations and certifications including the Chartered Financial Analyst (CFA), Professional Risk Manager (PRM), Certified JAVA Programmer, SAS Certified Professional, and the Certificate in Financial Engineering from UC Berkeley.

15

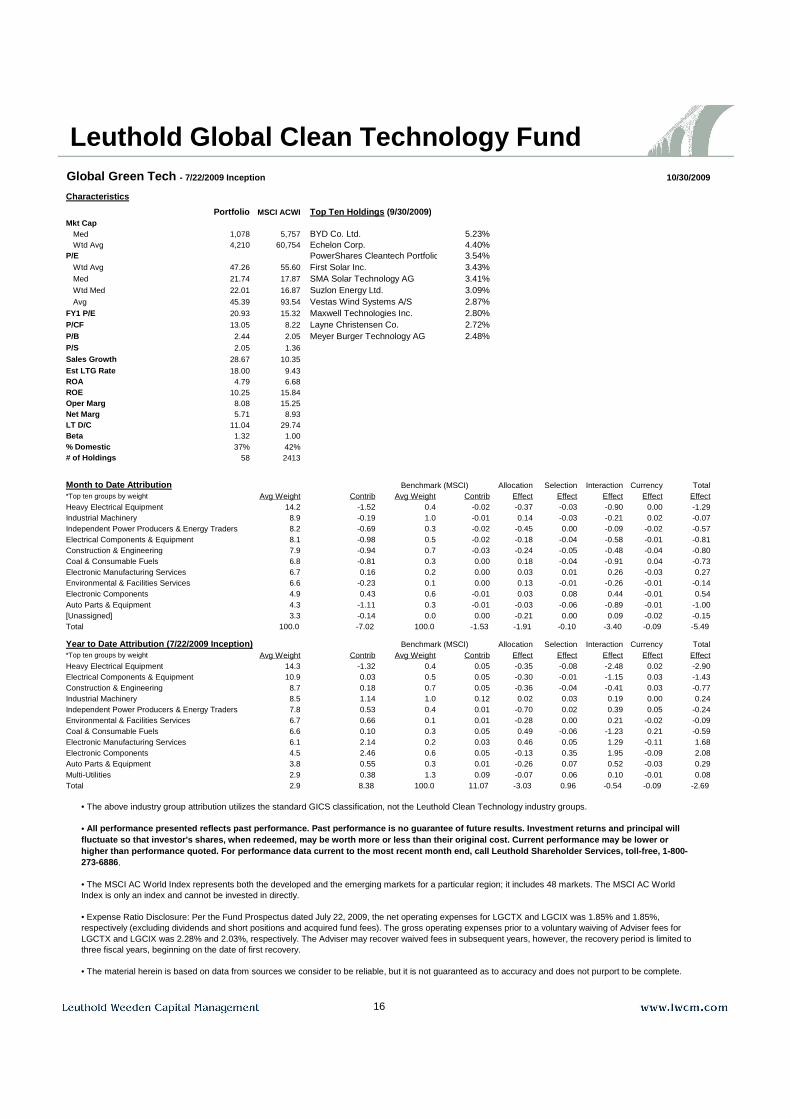

Leuthold Global Clean Technology Fund

16

Global Green Tech - 7/22/2009 Inception 10/30/2009

Characteristics

Portfolio MSCI ACWI Top Ten Holdings (9/30/2009)Mkt Cap

Med 1,078 5,757 BYD Co. Ltd. 5.23%Wtd Avg 4,210 60,754 Echelon Corp. 4.40%

P/E PowerShares Cleantech Portfolio 3.54%Wtd Avg 47.26 55.60 First Solar Inc. 3.43%Med 21.74 17.87 SMA Solar Technology AG 3.41%Wtd Med 22.01 16.87 Suzlon Energy Ltd. 3.09%Avg 45.39 93.54 Vestas Wind Systems A/S 2.87%

FY1 P/E 20.93 15.32 Maxwell Technologies Inc. 2.80%P/CF 13.05 8.22 Layne Christensen Co. 2.72%P/B 2.44 2.05 Meyer Burger Technology AG 2.48%P/S 2.05 1.36Sales Growth 28.67 10.35Est LTG Rate 18.00 9.43ROA 4.79 6.68ROE 10.25 15.84Oper Marg 8.08 15.25Net Marg 5.71 8.93LT D/C 11.04 29.74Beta 1.32 1.00% Domestic 37% 42%# of Holdings 58 2413

Month to Date Attribution Allocation Selection Interaction Currency Total*Top ten groups by weight Avg Weight Contrib Avg Weight Contrib Effect Effect Effect Effect EffectHeavy Electrical Equipment 14.2 -1.52 0.4 -0.02 -0.37 -0.03 -0.90 0.00 -1.29Industrial Machinery 8.9 -0.19 1.0 -0.01 0.14 -0.03 -0.21 0.02 -0.07Independent Power Producers & Energy Traders 8.2 -0.69 0.3 -0.02 -0.45 0.00 -0.09 -0.02 -0.57Electrical Components & Equipment 8.1 -0.98 0.5 -0.02 -0.18 -0.04 -0.58 -0.01 -0.81Construction & Engineering 7.9 -0.94 0.7 -0.03 -0.24 -0.05 -0.48 -0.04 -0.80Coal & Consumable Fuels 6.8 -0.81 0.3 0.00 0.18 -0.04 -0.91 0.04 -0.73Electronic Manufacturing Services 6.7 0.16 0.2 0.00 0.03 0.01 0.26 -0.03 0.27Environmental & Facilities Services 6.6 -0.23 0.1 0.00 0.13 -0.01 -0.26 -0.01 -0.14Electronic Components 4.9 0.43 0.6 -0.01 0.03 0.08 0.44 -0.01 0.54Auto Parts & Equipment 4.3 -1.11 0.3 -0.01 -0.03 -0.06 -0.89 -0.01 -1.00[Unassigned] 3.3 -0.14 0.0 0.00 -0.21 0.00 0.09 -0.02 -0.15Total 100.0 -7.02 100.0 -1.53 -1.91 -0.10 -3.40 -0.09 -5.49

Year to Date Attribution (7/22/2009 Inception) Allocation Selection Interaction Currency Total*Top ten groups by weight Avg Weight Contrib Avg Weight Contrib Effect Effect Effect Effect EffectHeavy Electrical Equipment 14.3 -1.32 0.4 0.05 -0.35 -0.08 -2.48 0.02 -2.90Electrical Components & Equipment 10.9 0.03 0.5 0.05 -0.30 -0.01 -1.15 0.03 -1.43Construction & Engineering 8.7 0.18 0.7 0.05 -0.36 -0.04 -0.41 0.03 -0.77Industrial Machinery 8.5 1.14 1.0 0.12 0.02 0.03 0.19 0.00 0.24Independent Power Producers & Energy Traders 7.8 0.53 0.4 0.01 -0.70 0.02 0.39 0.05 -0.24Environmental & Facilities Services 6.7 0.66 0.1 0.01 -0.28 0.00 0.21 -0.02 -0.09Coal & Consumable Fuels 6.6 0.10 0.3 0.05 0.49 -0.06 -1.23 0.21 -0.59Electronic Manufacturing Services 6.1 2.14 0.2 0.03 0.46 0.05 1.29 -0.11 1.68Electronic Components 4.5 2.46 0.6 0.05 -0.13 0.35 1.95 -0.09 2.08Auto Parts & Equipment 3.8 0.55 0.3 0.01 -0.26 0.07 0.52 -0.03 0.29Multi-Utilities 2.9 0.38 1.3 0.09 -0.07 0.06 0.10 -0.01 0.08Total 2.9 8.38 100.0 11.07 -3.03 0.96 -0.54 -0.09 -2.69

Benchmark (MSCI)

Benchmark (MSCI)

• The above industry group attribution utilizes the standard GICS classification, not the Leuthold Clean Technology industry groups.

• All performance presented reflects past performance . Past performance is no guarantee of future result s. Investment returns and principal will fluctuate so that investor's shares, when redeemed, may be worth more or less than their original cost . Current performance may be lower or higher than performance quoted. For performance dat a current to the most recent month end, call Leutho ld Shareholder Services, toll-free, 1-800-273-6886.

• The MSCI AC World Index represents both the developed and the emerging markets for a particular region; it includes 48 markets. The MSCI AC World Index is only an index and cannot be invested in directly.

• Expense Ratio Disclosure: Per the Fund Prospectus dated July 22, 2009, the net operating expenses for LGCTX and LGCIX was 1.85% and 1.85%, respectively (excluding dividends and short positions and acquired fund fees). The gross operating expenses prior to a voluntary waiving of Adviser fees for LGCTX and LGCIX was 2.28% and 2.03%, respectively. The Adviser may recover waived fees in subsequent years, however, the recovery period is limited to three fiscal years, beginning on the date of first recovery.

• The material herein is based on data from sources we consider to be reliable, but it is not guaranteed as to accuracy and does not purport to be complete.