lessons from hedge fund registration

TRANSCRIPT

Mandatory Disclosure and Operational Risk: Evidence from Hedge Fund

Registration

, Stephen Brown William, Goetzmann

, Bing Liang Chris topherSchwarz

www.stern.nyu.edu/~sbrown

Overview

The importance of operational ris k

Analys is of Form ADV filings

Important ro le of conflic ts of interes t

A quantitative meas ure of operational ris k

.. ?Do inves tors know or care

Growth of US Hedge Fund Industry

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

$M

illio

n A

ss

ets

un

de

r m

an

ag

em

en

t

Multi-Strategy

Managed Futures

Long/Short Equity Hedge

Global Macro

Fixed Income Arbitrage

Event Driven

Equity Market Neutral

Emerging Markets

Dedicated Short Bias

Convertible Arbitrage

Source: Lipper TASS

Institutional concern about risk

Fiduc iary guide lines imply concern for ris k

Financial ris k

Operational ris k

Ins titutional demand Growing popularity of market neutrals tyles

Explos ive growth of funds of funds

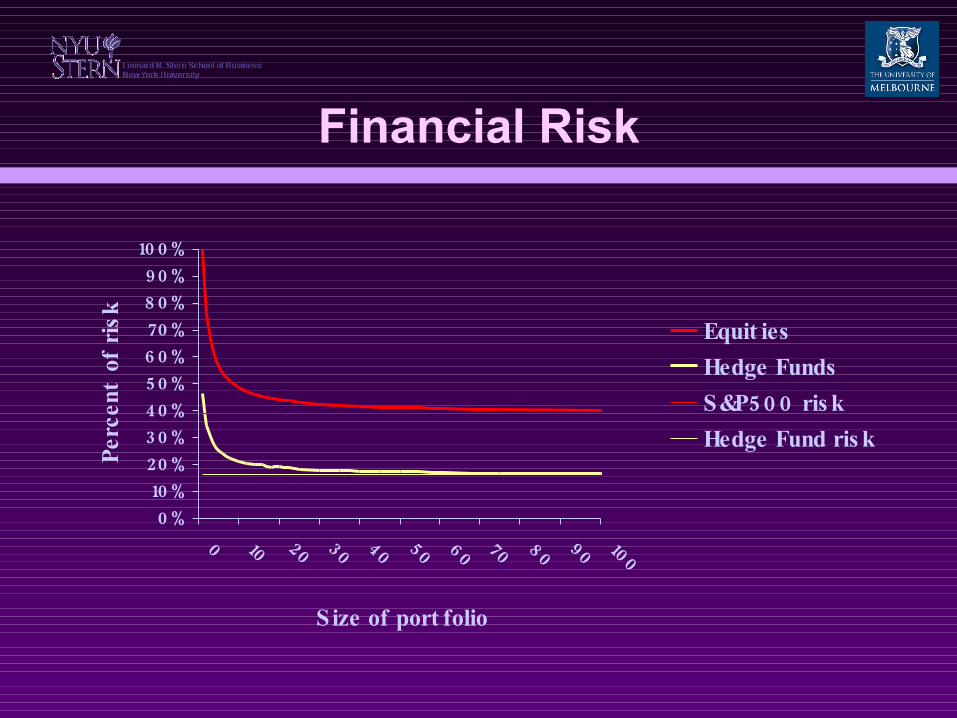

Financial Risk

0 %10 %20 %30 %40 %50 %6 0 %70 %8 0 %90 %

10 0 %

0 10 20 30 40 50 6 0 70 8 0 90 10 0

Size of port folio

Percent

ofrisk

Equit ies

500 S&P ris k

: 1995. Source Elton and Gruber Ris k is meas ured re lative to the s tandard deviation of the average s tock

Financial Risk

0 %10 %20 %30 %40 %50 %6 0 %70 %8 0 %90 %

10 0 %

0 10 20 30 40 50 6 0 70 8 0 90 10 0

Size of port folio

Percent

ofrisk Equit ies

Hedge Funds

500 S&P ris k

Hedge Fund ris k

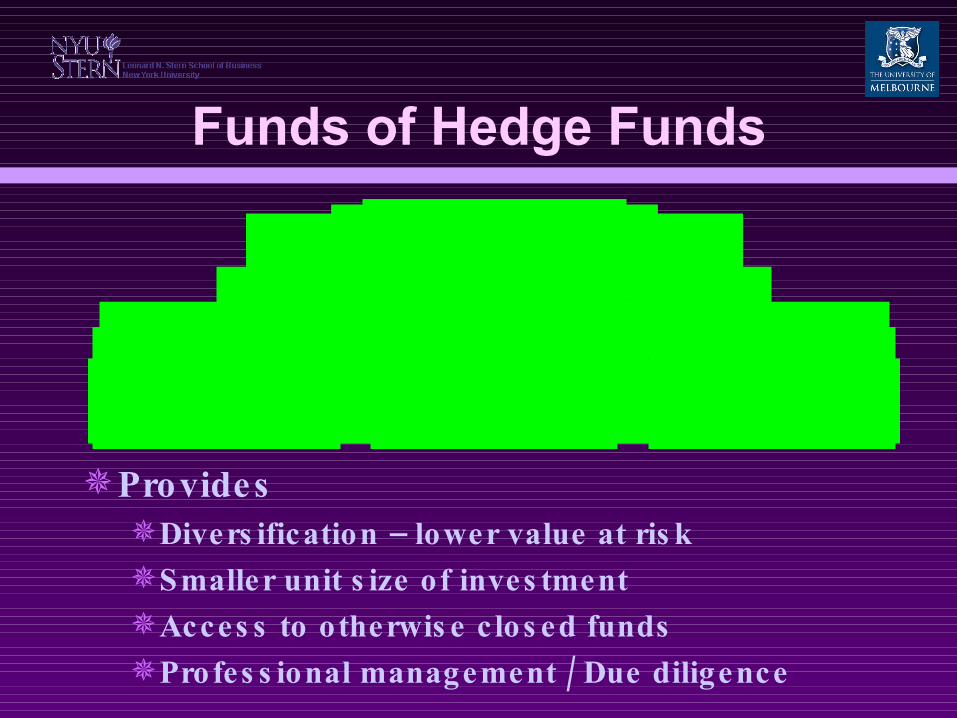

Funds of Hedge Funds

Provides – Divers ification lower value at ris k

Smaller unit s ize of inves tment

Acces s to otherwis e c los ed funds

/ Profes s ional management Due diligence

1H e d g e F u n d 2H e d g e F u n d 3H e d g e F u n d

F u n d o f F u n d s

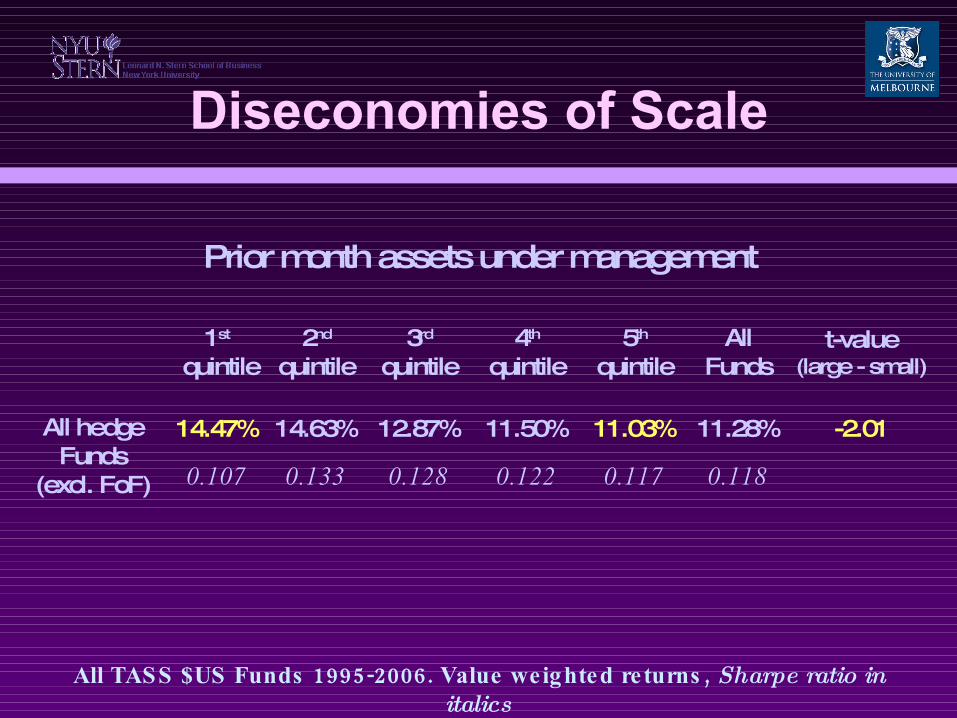

Diseconomies of Scale

Prior month assets under management

1st

quintile2nd

quintile3rd

quintile4th

quintile5th

quintileAll

Fundst-value

(large - small)

All hedgeFunds

(excl. FoF)

14.47% 14.63% 12.87% 11.50% 11.03% 11.28% -2.01

0.107 0.133 0.128 0.122 0.117 0.118

1995-2006. , All TASS $US Funds Value weighted returns Sharpe ratio in italics

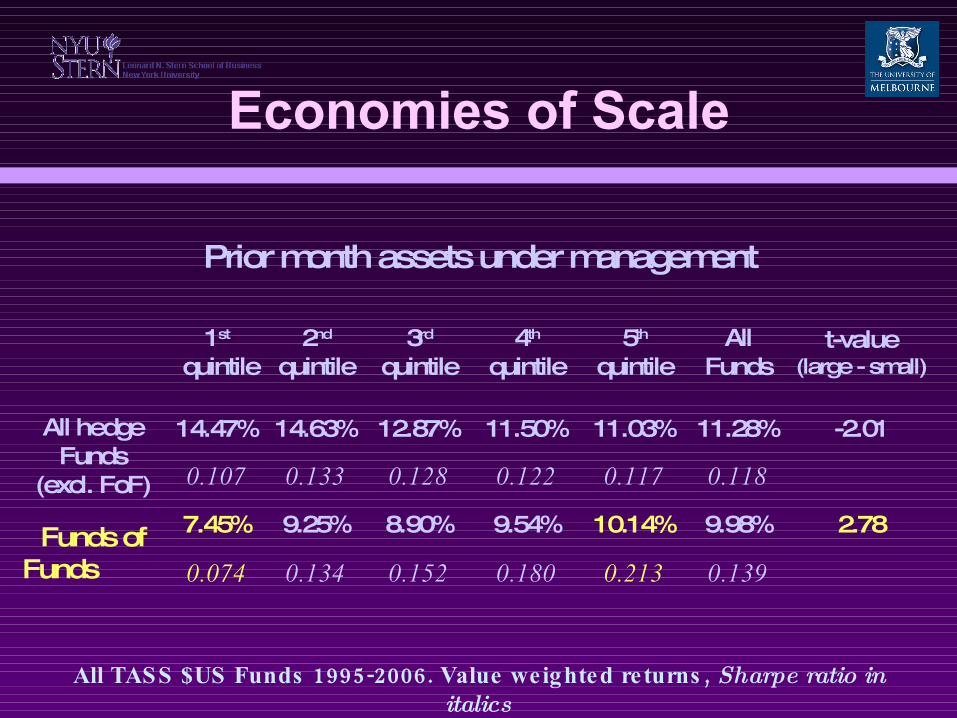

Economies of Scale

Prior month assets under management

1st

quintile2nd

quintile3rd

quintile4th

quintile5th

quintileAll

Fundst-value

(large - small)

All hedgeFunds

(excl. FoF)

14.47% 14.63% 12.87% 11.50% 11.03% 11.28% -2.01

0.107 0.133 0.128 0.122 0.117 0.118

Funds ofFunds

7.45% 9.25% 8.90% 9.54% 10.14% 9.98% 2.78

0.074 0.134 0.152 0.180 0.213 0.139

1995-2006. , All TASS $US Funds Value weighted returns Sharpe ratio in italics

Economies of Scale

Prior month assets under management

1st

quintile2nd

quintile3rd

quintile4th

quintile5th

quintileAll

Fundst-value

(large - small)

All hedgeFunds

(excl. FoF)

14.47% 14.63% 12.87% 11.50% 11.03% 11.28% -2.01

0.107 0.133 0.128 0.122 0.117 0.118

Funds ofFunds

7.45% 9.25% 8.90% 9.54% 10.14% 9.98% 2.78

0.074 0.134 0.152 0.180 0.213 0.139

1995-2006. , All TASS $US Funds Value weighted returns Sharpe ratio in italics

26% of Funds of Funds <$25M !!!

MotivationMotivation

SEC mandated hedge funds file Form 1ADV by February s t, 2006

Controvers ial requirement overturned 23June rd, 2006

:Interes ting res earch ques tions ?What is the purpos e of s uch mandated dis c los ures What is the dis tinc tion between operational and

financ ial ris k Does the dis c los ure provide material information ?To whom

Data

All Form ADV filings in February2006

Hedge fund characteris tic s from TASS

management companies matched with ADV forms by both name and addres s ..from the “Company” TASS file

Brown, Stephen J., Goetzmann, William N., Liang, Bing and Schwarz, Christopher, "Optimal Disclosure and Operational Risk: Evidence from Hedge Fund Registration" (January 7, 2007). Yale ICF Working Paper No. 06-15 Available at SSRN: http://ssrn.com/abstract=918461

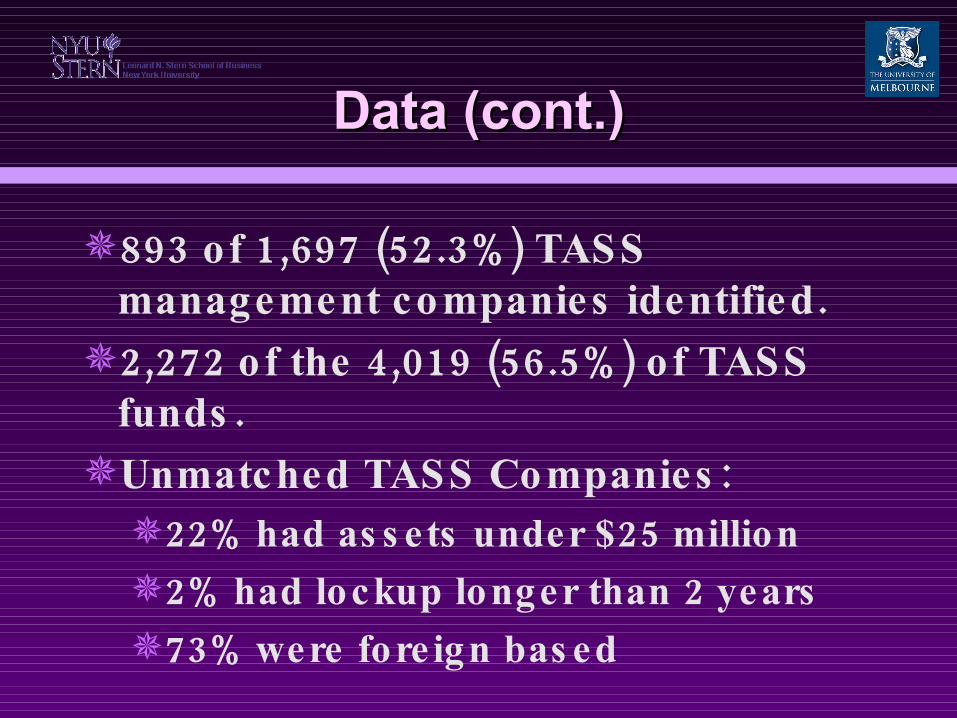

Data (cont.)Data (cont.)

893 1,697 (52.3%) of TASS .management companies identified

2,272 4,019 (56.5%) of the of TASS.funds

:Unmatched TASS Companies22% 25 had as s ets under $ million

2% 2 had lockup longer than years

73% were fore ign bas ed

Form ADVForm ADV

35 .pages long

General information

:Ques tions on potential conflic ts of interes t

[ 11]legal or regulatory is s ues Item

( owners hip s tructure both direct and)indirect

No ques tions about holdings ors trategy

Phil GoldsteinPhil Goldstein

ADV form as ks everything from “your las t small pox vacc ination to every dirty joke you got on Email”

11ItemFelonies

- Inves tment re lated mis demeanors

, - Any SEC CFTC or s e lf regulatoryis s ues

Laws uits

Tests and ResultsTests and Results

= A “Problem” fund a fund whos e management company answered

‘ ’ 11.Yes to ANY ques tion on Item 2,272 358 (15.8%) Of funds are

.defined as “problem ”128 893 (14.3%) of management

.companies

10,295 , Of the total ADV regis trations1,526 (14.8%) .had a “problem ”

17

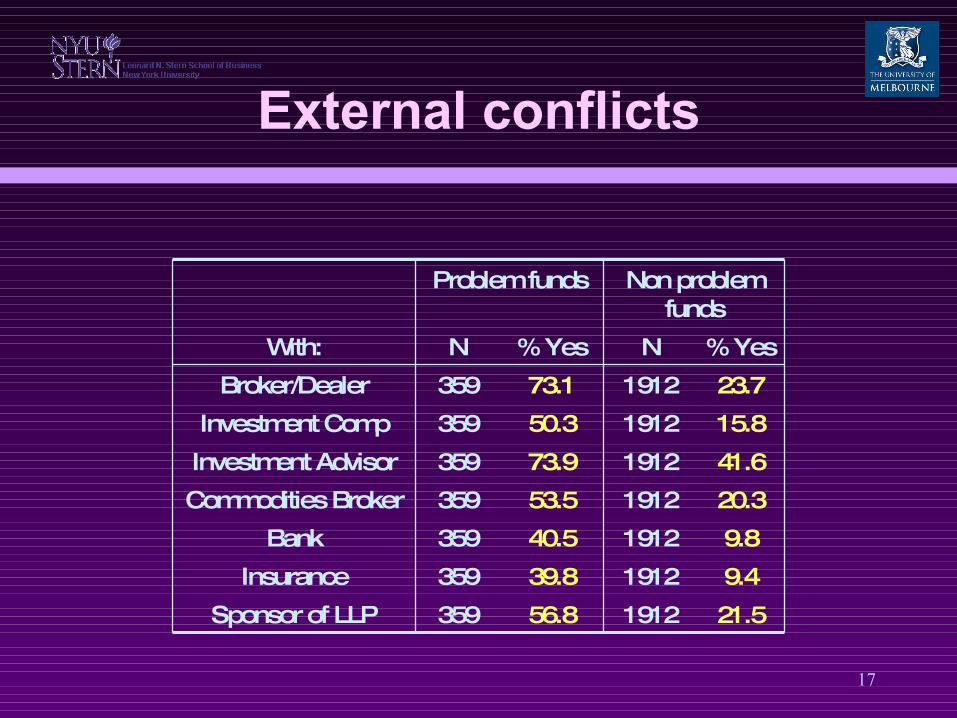

External conflicts

Problem funds Non problemfunds

With: N % Yes N % Yes

Broker/Dealer 359 73.1 1912 23.7

Investment Comp 359 50.3 1912 15.8

Investment Advisor 359 73.9 1912 41.6

Commodities Broker 359 53.5 1912 20.3

Bank 359 40.5 1912 9.8

Insurance 359 39.8 1912 9.4

Sponsor of LLP 359 56.8 1912 21.5

18

Internal conflicts

Problem funds Non problemfunds

With: N % Yes N % Yes

Trade securities with clients 359 30.7 1912 8.3

Allow trading on own account 359 84.8 1912 69.3

Recommend own securities 359 75.5 1912 50.4

In-house broker dealer 359 31.2 1912 2.3

Recommends own underwriting service

359 69.4 1912 46.8

Recommends commission fee items

359 22.6 1912 15.7

Recommends brokers 359 46.7 1912 38.0

Use broker provided external research

359 81.0 1912 70.5

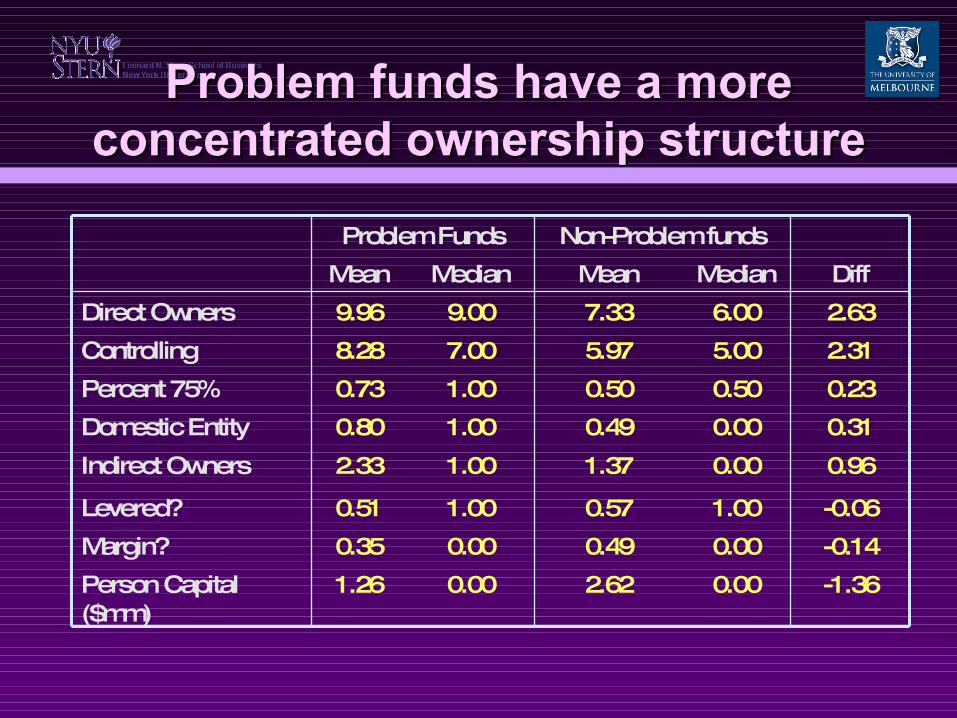

Problem funds have a more Problem funds have a more concentrated ownership structureconcentrated ownership structure

Problem Funds Non-Problem funds

Mean Median Mean Median Diff

Direct Owners 9.96 9.00 7.33 6.00 2.63

Controlling 8.28 7.00 5.97 5.00 2.31

Percent 75% 0.73 1.00 0.50 0.50 0.23

Domestic Entity 0.80 1.00 0.49 0.00 0.31

Indirect Owners 2.33 1.00 1.37 0.00 0.96

Levered? 0.51 1.00 0.57 1.00 -0.06

Margin? 0.35 0.00 0.49 0.00 -0.14

Person Capital ($mm)

1.26 0.00 2.62 0.00 -1.36

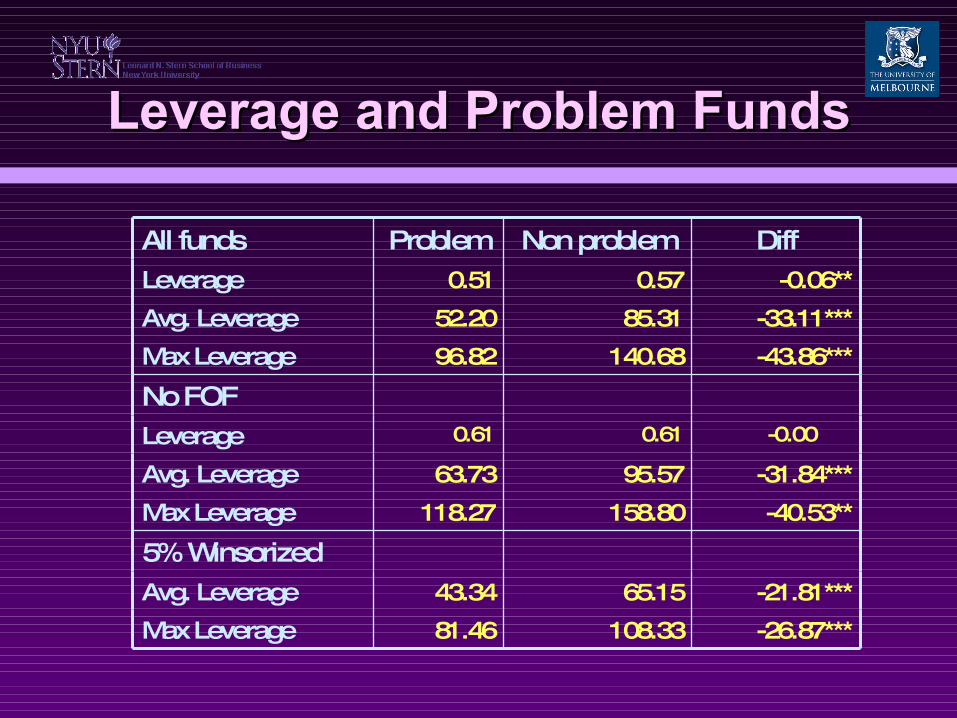

Leverage and Problem Funds

( Can lenders te ll the difference prior to2006)?

TASS leverage variables

Average leverage

Maximum leverage

Style controls Lenders already unders tand content of

ADV dis c los ure

Leverage and Problem FundsLeverage and Problem Funds

All funds Problem Non problem DiffLeverage 0.51 0.57 -0.06**

Avg. Leverage 52.20 85.31 -33.11***

Max Leverage 96.82 140.68 -43.86***

No FOFLeverage 0.61 0.61 -0.00

Avg. Leverage 63.73 95.57 -31.84***

Max Leverage 118.27 158.80 -40.53**

5% WinsorizedAvg. Leverage 43.34 65.15 -21.81***

Max Leverage 81.46 108.33 -26.87***

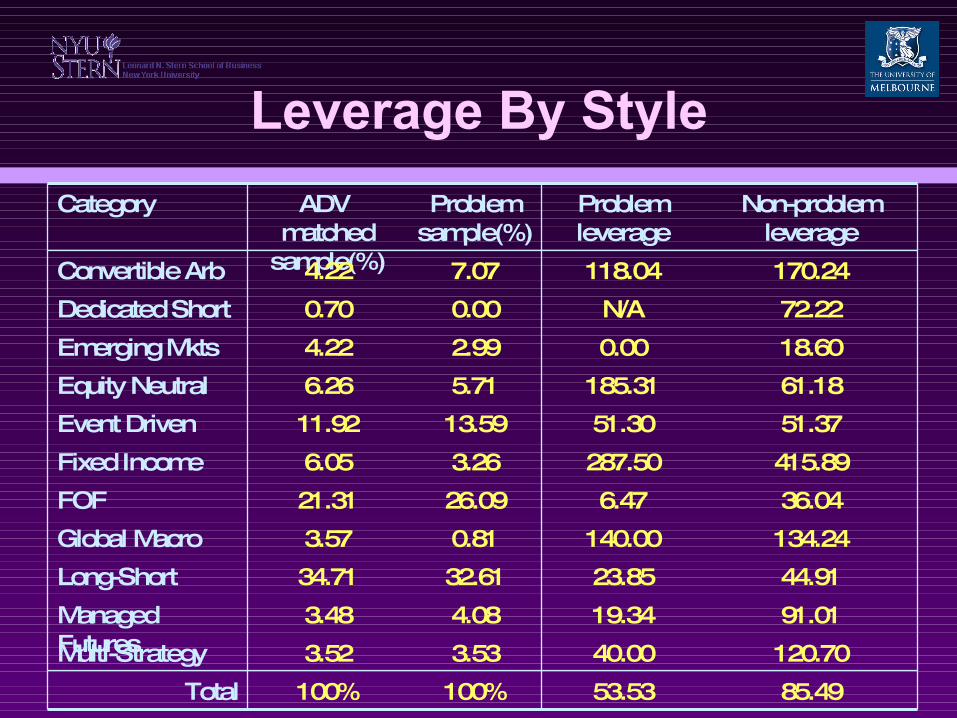

Leverage By Style

Category ADV matched

sample(%)

Problem sample(%)

Problem leverage

Non-problem leverage

Convertible Arb 4.22 7.07 118.04 170.24

Dedicated Short 0.70 0.00 N/A 72.22

Emerging Mkts 4.22 2.99 0.00 18.60

Equity Neutral 6.26 5.71 185.31 61.18

Event Driven 11.92 13.59 51.30 51.37

Fixed Income 6.05 3.26 287.50 415.89

FOF 21.31 26.09 6.47 36.04

Global Macro 3.57 0.81 140.00 134.24

Long-Short 34.71 32.61 23.85 44.91

Managed Futures

3.48 4.08 19.34 91.01

Multi-Strategy 3.52 3.53 40.00 120.70

Total 100% 100% 53.53 85.49

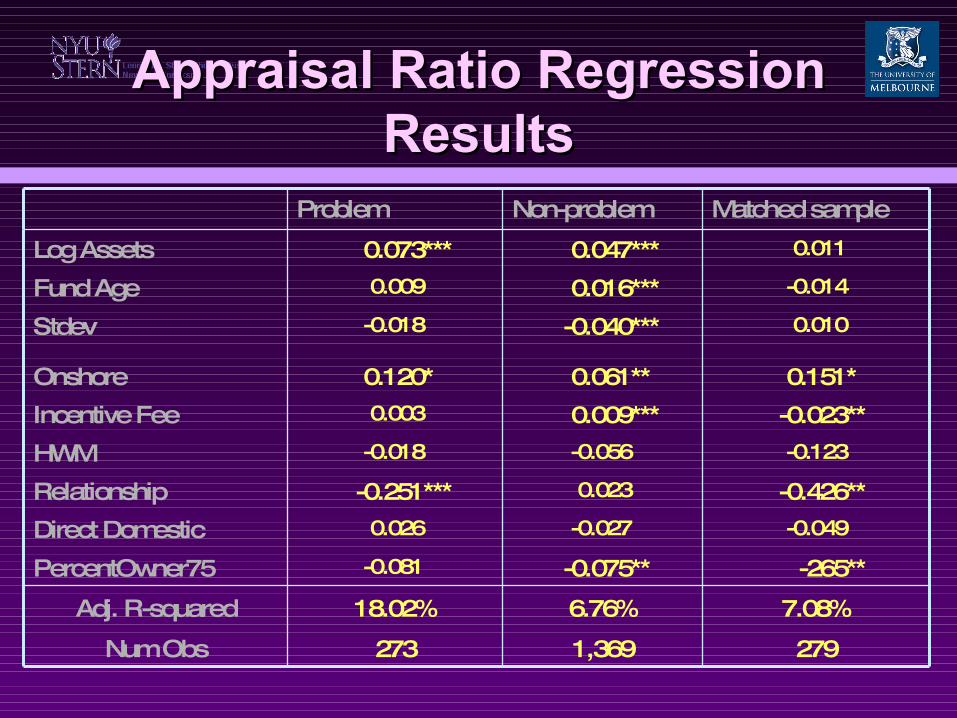

Appraisal Ratio Regression Appraisal Ratio Regression ResultsResults

Problem Non-problem Matched sample

Log Assets 0.073*** 0.047*** 0.011

Fund Age 0.009 0.016*** -0.014

Stdev -0.018 -0.040*** 0.010

Onshore 0.120* 0.061** 0.151*

Incentive Fee 0.003 0.009*** -0.023**

HWM -0.018 -0.056 -0.123

Relationship -0.251*** 0.023 -0.426**

Direct Domestic 0.026 -0.027 -0.049

PercentOwner75 -0.081 -0.075** -265**

Adj. R-squared 18.02% 6.76% 7.08%

Num Obs 273 1,369 279

What have we learned?

Factors as s oc iated with operational ris k External conflic ts of interes t

Internal conflic ts of interes t

Operational ris k is unders tood by s ophis ticatedinves tors Problem funds have concentrated owners hip

Problem funds have difficulty borrowing money

This s ugges ts an important ro le for due diligence

A univariate measure of A univariate measure of operational riskoperational risk

TASS ADV

Previous Returns -0.27*** AgencyCrossTrans

0.06**

Previous Std. Dev. -0.35*** RelBrokerDealer 0.28***

Fund Age -0.07*** RelInvestComp 0.24***

Log of Assets 0.13*** RelInvAdvisor 0.24***

Reports Assets 0.12*** RelPartSponser 0.30***

Incentive Fee -0.88*** BuySellYouOwn 0.08**

Margin -0.29*** BuySellYourClient -0.08***

Audited -0.19*** RecSecYouOwn 0.33***

Personal Capital -0.29*** RecUnderwriter 0.26***

Onshor -0.05*** RecSalesInterest 0.28***

OpenToInv 0.08 RecBrokers -0.33***

Accepts Mgd. Accts. -0.13*** PercentOwner75 0.15***

Corr ADV & TASS 0.42*** DirectDomestic 0.31***

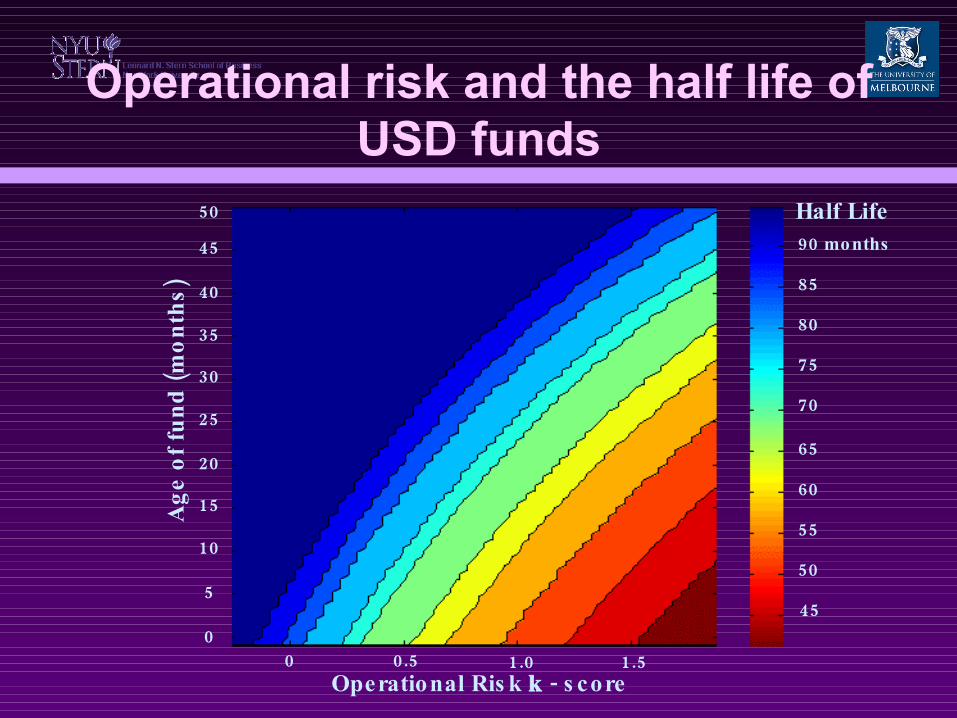

Operational risk and the half life of USD funds

0 0.5 1.0 1.5

5045

40

35

30

25

20

15

10

5

0

90 months

85

80

75

70

65

60

55

50

45

Half Life

()

Ageoffund

months

Operational Ris k k - s core

Does the operational risk measure Does the operational risk measure predict leverage?predict leverage?

TASS Style Dummies B-G Style Dummies

Coeff t-value Coeff t-value

2005 -18.04 -4.04*** -6.39 -6.80***

2004 -28.87 -5.85*** -35.16 -8.25***

2003 -24.76 -4.76*** -33.38 -7.19***

2002 -17.36 -3.28*** -26.96 -5.68***

2001 -21.75 -3.96*** -27.21 -5.30***

Average -22.16 -10.33*** -25.82 -5.04***

Avg. Adj. R-sq. 13.74% 2.61%

Avg. Obs 2279 2279

Does the operational risk measure predict returns?

Year Operational risk coefficient t-value1994 -2.28% -2.2**1995 0.10% 0.121996 -3.27% -4.76***1997 -2.61% -3.71***… … …2002 -1.48% -4.43***2003 -0.41% -1.122004 -0.67% -2.45**2005 -0.11% -1.31Average Value -0.92% -2.66**Avg. Adjusted R² 40.17%

Average Observations

1,027

, Cros s s ectional return regres s ion on prior operational ris k financial ris k and s tyle dummies

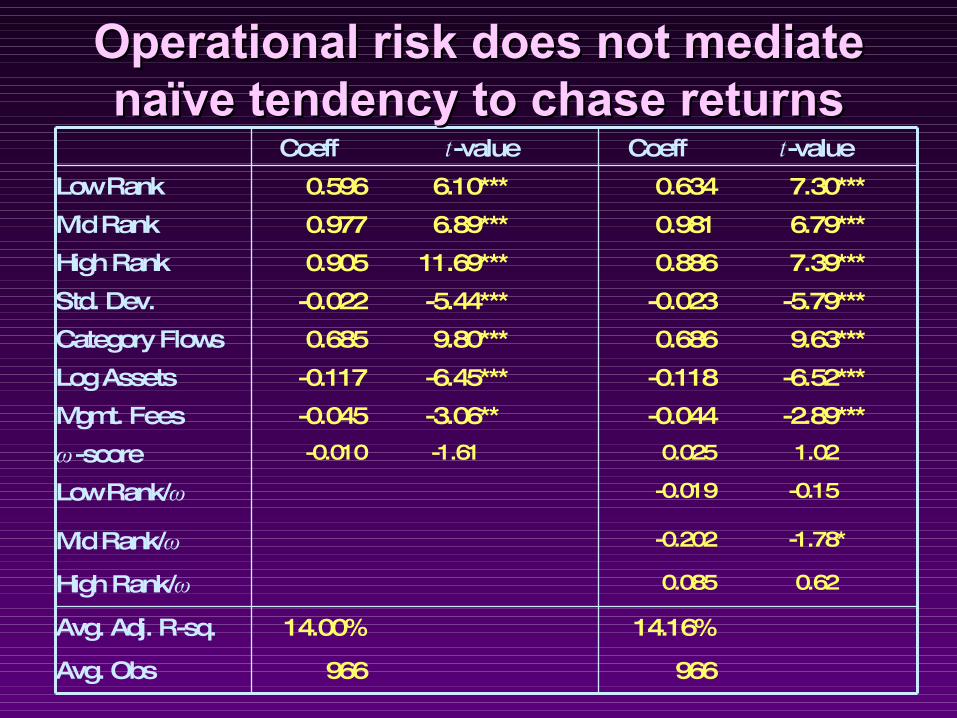

Investor Flows and Problem Investor Flows and Problem FundsFunds

Operational ris k influences owners hip andleverage

Lenders and hedge fund equity inves tors already unders tand ris k content of Form ADV

dis c los ures

-Does operational ris k modify the flow ?performance re lations hip

?Do inves tors care

Coeff t-value Coeff t-value

Low Rank 0.596 6.10*** 0.634 7.30***

Mid Rank 0.977 6.89*** 0.981 6.79***

High Rank 0.905 11.69*** 0.886 7.39***

Std. Dev. -0.022 -5.44*** -0.023 -5.79***

Category Flows 0.685 9.80*** 0.686 9.63***

Log Assets -0.117 -6.45*** -0.118 -6.52***

Mgmt. Fees -0.045 -3.06** -0.044 -2.89***

ω-score -0.010 -1.61 0.025 1.02

Low Rank/ω -0.019 -0.15

Mid Rank/ω -0.202 -1.78*

High Rank/ω 0.085 0.62

Avg. Adj. R-sq. 14.00% 14.16%

Avg. Obs 966 966

Operational risk does not mediate Operational risk does not mediate naïve tendency to chase returnsnaïve tendency to chase returns

ConclusionConclusion

Important to quantify operational ris k

ConclusionConclusion

Important to quantify operational ris k

This ris k is as s oc iated with conflic ts ofinteres t

ConclusionConclusion

Important to quantify operational ris k

This ris k is as s oc iated with conflic ts ofinteres t

+ = Operational ris k conflic t low returns

ConclusionConclusion

Important to quantify operational ris k

This ris k is as s oc iated with conflic ts ofinteres t

+ = Operational ris k conflic t low returns

Operational ris k does not mediate the naïve tendency of inves tors to chas e

returns

ConclusionConclusion

Important to quantify operational ris k

This ris k is as s oc iated with conflic ts ofinteres t

+ = Operational ris k conflic t low returns

Operational ris k does not mediate the naïve tendency of inves tors to chas e

returns

Either inves tors do not unders tand operational ris k

ConclusionConclusion

Important to quantify operational ris k

This ris k is as s oc iated with conflic ts ofinteres t

+ = Operational ris k conflic t low returns

Operational ris k does not mediate the naïve tendency of inves tors to chas e

returns

Either inves tors do not unders tand operational ris k

Or inves tors know and do not care

Important implication

Hedge funds on average have pos itivealpha

Excluding operational ris k increas es alpha

Due diligence adds value to hedge fundinves tors

Sugges ts a new approach to hedge fundinves ting