lekcija: maksājumu instrumenti un maksājumu sistēmas pasaulē un latvijā

TRANSCRIPT

Payment Instruments and Payment Systems: A Global and National Perspective

Payment Systems Department2017

Latvijas Banka

Latvijas Banka:• contributes to determining and

implementing of monetary policy;• manages reserve assets, including

gold reserves;• facilitates smooth functioning of

payment systems;• ensures interbank settlements;• ensures smooth circulation of cash

in Latvia;• collects, aggregates and publishes

financial (statistical) data;• represents the interests of Latvia

in international financial institutions.

These functions are performed by:• economists and econometrists;• accountants and bookkeepers;• financial market analysts;• statisticians;• payment systems experts;• financial investment portfolio

managers;• cash-desk transactions

methodology experts;• payment and financial market

analysts.

Content

Payment environment

How does it look in Latvia?

Payment instruments

Development trends

Payment system

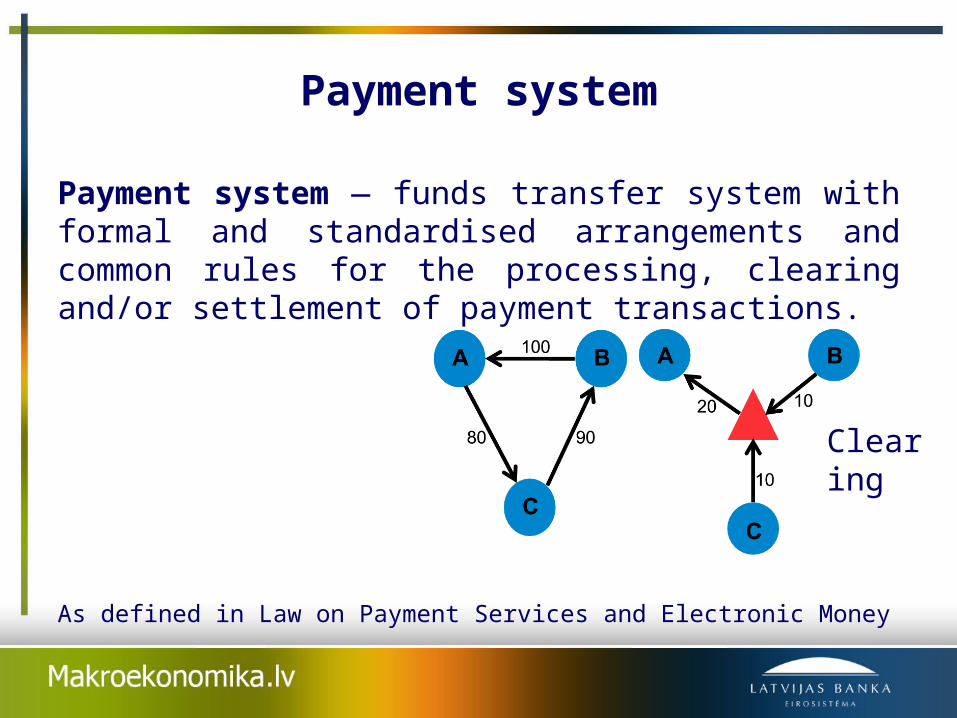

Payment system — funds transfer system with formal and standardised arrangements and common rules for the processing, clearing and/or settlement of payment transactions.

As defined in Law on Payment Services and Electronic Money

Clearing

Payment environment

Large value interbankpayment system

Retail payment systems

Banking services for customers

Person to person payments

Payment environment

Large value interbankpayment system

Retail payment systems

Banking services for customers

Person to person payments

PAYMENTSYSTEMS

Payment system

Source: ECB

What is the importance of payment systems in payment environment?

• Smooth functioning of payment systems – participants’ confidence in those systems and, ultimately, public confidence in the currency;

• Stability of financial institutions and market, promoting systemic stability;

• Implementation of monetary policy;

• The functioning of financial markets and the economy as a whole that favour the welfare of society;

• Mitigation of systemic risk – settlement in central bank money;

• Promoting of domestic and cross-border payments’ efficiency.

Payment systems

Multimedia will be available in the visitors centre of Latvijas Banka "Money World" in the 2nd half of 2017

Types of payment systems

• RTGS - Real Time Gross Settlement systems. Large value, express payments. (also so-called LVPS – Large Value Payment Systems)

• RPS - Retail Payment systems – large volumes. Usually net settlement systems for retail payments.

RTGS

• Settlement transactions between payment systems’ participants (banks);

• Settlement of monetary policy transactions;

• Cash leg settlement of financial and capital market transactions;

• Final settlement of ancillary systems;

• Funds flows from all levels of payment environment – concentrated in significant fund flows and risks;

What types of payment systems there are?

Payments are processed in payment systems of two types:

• gross settlement systems process payments on one by one basis and settle each payment individually without bundling;

• net settlement systems aggregate many payments and settle them in batches in specified time periods during a day.

GROSS SETTLEMENT

1. payment

2. payment

3. payment

4. payment

settlement

settlement

settlement

settlement

NET SETTLEMENT

1. payment

2. payment

3. payment

4. payment

settlement

SWIFT – critical component of payment infrastructure

• SWIFT is an international communication network for safe exchange of standardized financial messages;

• Daily more than 10,000 financial institutions and corporations in 215 countries send over 20 millions of financial messages using SWIFT network;

• Head office of SWIFT located in Belgium and operated under Belgian law.

PAYMENT ENVIRONMENT IN LATVIA

Payment environment in Latvia

Large value interbankpayment system

Retail payment systems

Banking services for customers

Person to person payments

EKS, FDL

TARGET2-Latvija

BanksE-money institutionsPayment institutionsLatvian PostState Treasury

What does Latvijas Banka do in the area of payment systems?

One of the principal tasks of the Latvijas Banka – participate in promoting the smooth operation of payment systems in compliance with the provisions of the Treaty on the Functioning of the European Union and Protocol (No 4) "The Statute of the European System of Central Banks and of the European Central Bank”.

Since the introduction of the euro as a currency, Latvijas Banka performs this task in cooperation with other central banks of the Eurosystem.

Article 9, Law “On the Bank of Latvia”

How does Latvijas Banka perform this function?

3 main roles of Latvijas Banka in payment systems’ area:

• operator of payment systems;

• overseer of payment systems;

• catalyst in payment environment.

EKS and TARGET2-Latvija

Payment systems of Latvijas Banka

Multimedia will be available in the visitors centre of Latvijas Banka "Money World" in the 2nd half of 2017

TARGET2-LatvijaThe euro payment system TARGET2 is a real time payment system used by EU banks for financial market settlements as well as large value and urgent customer payments.

Legally and operationally the decentralisation principle is retained with respect to each Member State joining the TARGET2 system. TARGET2-Latvija is one of 25 TARGET2 component systems.

21 banks, Latvijas Banka and State Treasury, as well as 3 ancillary systems (EKS, LCD system un FDL payment cards processing system) participate in TARGET2-Latvija.

On average TARGET2-Latvija processes 1.7 thousand payments in a value of 0.95 billion euro daily (2016).

Electronic Clearing SystemThe EKS is the only clearing (net settlement) system in Latvia that ensures the settlement of a large volume customer credit transfers in euro.

The EKS positions are settled in TARGET2-Latvija seven times per day.

The EKS is SEPA compliant system, which ensures its participants' capability to send and receive euro payments within SEPA area.

15 direct participants, incl. Latvijas Banka and State Treasury, 12 indirect participants and addressable BIC holders participate in the EKS.

On average the EKS processes 156.9 thousand payments in a value of 0.2 billion euro daily (2016).

What is SEPA and why it is necessary?SEPA (Single Euro Payments Area):

•a project for single market of retail payments in euro;

• three main products – payment cards, credit transfers and direct debits;

•single payment area and unified standards.

What are the benefits of SEPAfor credit transfer?

Equal standards for domestic and cross-border SEPA credit transfers

One price – cheaper cross-border SEPA credit transfers

Main condition – BIC and IBAN

Fee of a transfer initiated through internet-banking in Latvia

Before 01.01.2014. After 01.01.2014

for domestic transfer on average 0.25 lats (0.36 euro)

on average 0.36 euro

for SEPA credit transferin euro

on average 5 lats (7.11 euro) on average 0.36 euro

25

EKS

The route of customer interbank paymentIf both banks are EKS participants

26

EKS

EBA Clearing

The route of customer interbank paymentIf only one of the banks is EKS participant

TOMS AND PAYMENTS

Multimedia will be available in the visitors centre of Latvijas Banka "Money World" in the 2nd half of 2017

Oversight and catalyst functions• assessment of payment systems against international oversight

standards, which also includes providing recommendations aiming to mitigate the risks related to the processing of the payment system;

• payment data analysis;

• cooperation with market participants and infrastructure providers in different projects of payments and securities area;

• expression of the opinion or expertise regarding the different payment systems development issues;

• performing risk analysis on the national payment system in general, aiming to minimise negative affects as far as possible.

Number of bank customers’ accounts in the second half of 2016

3.4 million (decrease compared to previous

year – 0.6 %)

2012 2013 2014 2015 20160

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Number of customer accounts (in millions)

Number of accounts in lats Number of accounts in euro

Payment environment in Latvia

Large value interbankpayment system

Retail payment systems

Banking services for customers

Person to person payments

EKS, FDL

TARGET2-Latvija

BanksE-money institutionsPayment institutionsLatvian PostState Treasury

Payment service providers

•ensure the cashless money in return for cash to customers;

•provide payment services to customers (individuals and legal entities) and infrastructure (means of payment, etc.) to carry out day-to-day settlements;

•provide innovations in payment area (e.g., mobile payment card reader, withdrawal of cash in shops).

Payment service providers

• 26 registered banks and foreign banks’ branches in Latvia;

• 15 electronic money institutions (licenced 3)

• 27 payment institutions (licenced 3)

• Latvian Post (Latvijas Pasts) and State Treasury (Valsts kase

Payment services directive

New payment services:• Payment initiation

service;

• Account information service;

• Payment services directive 2 (PSD2) will stay into force as of 13 January 2018;

Payments and authentication

• Towards strong customer authentication

Financial technology (FinTech)

FinTech – companies, which provide alternative financial services using technological developments and innovative approach

The role of other institutions in Latvia’s payment environment

The Financial and Capital Market Commission (FCMC) – is an autonomous public institution, which carries out the supervision of Latvian banks, payment institutions, electronic money institutions, and other financial and capital market participants.

Consumer rights protection centre (PTAC) – looks through the applications received from consumers, including users of financial services, on violations of rights protection laws and regulations, including those on unfair contract conditions.

The role of other institutions in Latvia’s payment environment

Ombudsman of the Association of Latvian Commercial Banks - handles the complaints of credit institution customers on the actions of credit institutions registered in Latvia and which are linked with non-cash credit transfers or transactions with electronic means of payment.

PAYMENT INSTRUMENTS

Cashless vs cash settlements

How many payments did you do by cash or payment card in the course of last week?

Bāze: visi respondenti: n=1007

5.7

NON-CASH CASH

6.3AVERAGE NUMBER OF PURCHASES:

AVERAGE NUMBER OF PURCHASES:

EUR 54.6AVERAGE TOTAL PURCHASE AMOUNT:

AVERAGE TOTAL PURCHASE AMOUNT: EUR 40.8

Survey by TNS, 2015

Payment instrument and means of paymentPayment instrument — any personalised device(s) and/or set of procedures agreed between the payment service user and the payment service provider and used by the payment service user in order to initiate a payment (payment card, i-bank application).

Payment — an act, initiated by the payer or by the payee, of placing, transferring or withdrawing funds, irrespective of any underlying obligations between the payer and the payee.

As defined in Law on Payment Services and Electronic Money and Credit Institutions Law

What is the most rapidly growing payment instrument?

2012 2013 2014 2015 2016 -

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

Customer credit transfersCard paymentsDirect debitE-money paymentsCheques

Development of most often used means of payment

Card payments rose by 12.8% according to volume (amounting to 242.8 million) and 8.6% according to value (amounting to 4.6 billion euro).

• There were 2.4 million payment cards issued in total (increased by 0.7%).

•Available 38.2 thousand points of sale (POS) (increase by 23.3%)

Customer credit transfers – increased by 6.0% according to volume (amounting to 156.0 million) and decreased by 21.2% according to value (amounting to 284.8 billion euro).

Changes are given for the 2016 compared to the 2015

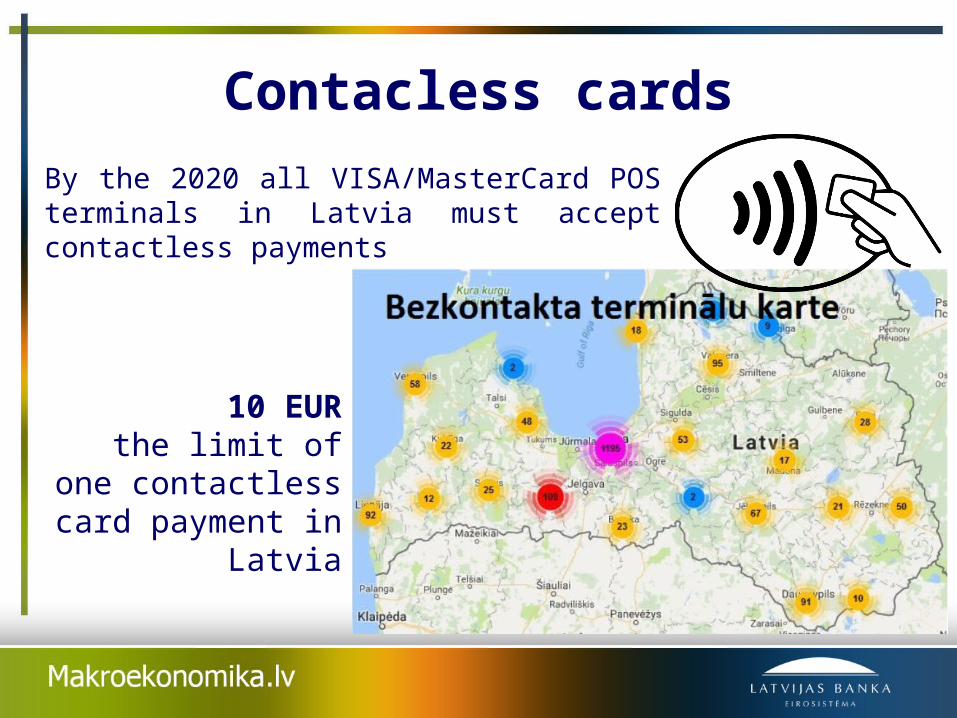

Contacless cardsBy the 2020 all VISA/MasterCard POS terminals in Latvia must accept contactless payments

10 EURthe limit of one

contactless card payment in Latvia

DEVELOPMENT TRENDS

Development trends

Development trends

• payments to become invisible part of the core service

• payments to go mobile; users will use apps more than internet banking;

• contactless solutions (NFC) like contactless cards, NFC in smartphones and other will dominate for small physical purchases;

• payments - instant;

• main issues to become – data protection and security;

52

Principles of Instant Payment

immediately receives funds on the account

Beneficiaryinstant interbank

Clearing

receives confirmation within seconds after initiation

Originator

SEPA Credit Transfer

Instrument

24/7/365

Availability

How do instant payments operate?

Beneficiary Bank

Solis 6

Saņēmēja banka apstiprina saņemšanu

un kreditē kontu

Solis 5

Saņēmēja banka autorizē maksājumu

Instant Payment service

Solis 7

Saņem paziņojumu, ka maksājums ir veiksmīgs

Solis 4

Maksājums apstiprināts

Sender Bank

Solis 8

Maksājuma apstiprinājums

Solis 3

Autorizācija

Customer

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 3

Autorizācija

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 8

Maksājuma apstiprinājums

Solis 3

Autorizācija

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 4

Maksājums apstiprināts

Solis 8

Maksājuma apstiprinājums

Solis 3

Autorizācija

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 5

Saņēmēja banka autorizē maksājumu

Solis 4

Maksājums apstiprināts

Solis 8

Maksājuma apstiprinājums

Solis 3

Autorizācija

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 7

Saņem paziņojumu, ka maksājums ir veiksmīgs

Solis 5

Saņēmēja banka autorizē maksājumu

Solis 4

Maksājums apstiprināts

Solis 8

Maksājuma apstiprinājums

Solis 3

Autorizācija

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 6

Saņēmēja banka apstiprina saņemšanu

un kreditē kontu

Solis 7

Saņem paziņojumu, ka maksājums ir veiksmīgs

Solis 5

Saņēmēja banka autorizē maksājumu

Solis 4

Maksājums apstiprināts

Solis 8

Maksājuma apstiprinājums

Solis 3

Autorizācija

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 5

Saņēmēja banka autorizē maksājumu

Solis 4

Maksājums apstiprināts

Solis 3

Autorizācija

Solis 2

Maksājums tiek iniciēts

Solis 5

Saņēmēja banka autorizē maksājumu

Solis 4

Maksājums apstiprināts

Solis 3

Autorizācija

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 5

Saņēmēja banka autorizē maksājumu

Solis 4

Maksājums apstiprināts

Solis 3

Autorizācija

Solis 8

Maksājuma apstiprinājums

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 5

Saņēmēja banka autorizē maksājumu

Solis 4

Maksājums apstiprināts

Solis 3

Autorizācija

Solis 7

Saņem paziņojumu, ka maksājums ir veiksmīgs

Solis 8

Maksājuma apstiprinājums

Solis 1

Klients sazinās ar banku

Solis 2

Maksājums tiek iniciēts

Solis 5

Saņēmēja banka autorizē maksājumu

Solis 4

Maksājums apstiprināts

Solis 3

Autorizācija

Step 6

Beneficiary bank confirms receipt and

credits account

Step 7

Receives notification that payment was

successful

Step 8

Confirmation on payment

Step 1

Customer contacts bank

Step 2

Payment instruction initiated

Step 5

Beneficiary bank authorises payment

Step 4

Payment validated

Step 3

Authorisation

54

INSTANT PAYMENTS IN THE WORLD

Mexico – SPEI (2004)

Chile – TEF (2008)South Africa – RTC (2006)

Nigeria – NIP (2011)

China – IBPS (2010)Taiwan – CIFS (2010)India – IMPS (2010)

Singapore – FAST (2014)South Korea – KFTC (2014)

UK – FPS (2008)Poland – Elixir Express (2012)

Sweden – BiR (2012)Denmark – Nets (2014)

Italy – SIA (2014)

Australia – (2016)

USA – (2018)

€ area - 2017

Development of the EKS system

Eurosettlement2008

STEP2 directconnectionWorking on holidays2014

Instant Payments2017

Night cycle2015

Launch1998

SEPA2010

• Continue ensuring safe, effective and contemporary interbank payments infrastructure

• Facilitate integration of the Latvian payments market into the Euro area (reachability)

• Facilitate the development of innovative payment instruments in Latvia

Motives of Latvijas Banka to launch Instant Payments service

What is e-money?Money which is circulating concurrently with cash and cashless money in the form of bank deposits:• mean of payment, which arises by paying in (depositing) any cash

amount in the account opened with an e-money institution;• e-money institution makes customer’s funds available to the

equivalent extent in the form of digital money;• the value of e-money is kept in smart card or computer memory;• use of e-money for payment of different goods and services, but only

there, where is particularly indicated, that e-money has been accepted as means of payment.

E-money institutions are commercial entities licensed or registered in e-money institutions’ register of the FCMC, and their activities are supervised. Examples: Mobilly, “Dāvanu karte” Ltd. (Galactico).

What is “virtual currency”?That is not a currency (money). “Virtual currency” is the form of non-regulated digital money, which is not issued and not guaranteed by the central bank and which is possible to use as a means of payment.It is possible to buy “virtual currency” in currency exchange platforms, by paying with an ordinary (normal) currency.While buying, safekeeping and vending “virtual currency”, e.g. Bitcoin, several risks

should be taken into account:- money could be lost in currency exchange platform;- money could be stolen from digital purse;- consumers are not protected if they use “virtual currency” as means of payment;- value of “virtual currency” might rapidly change and even drop down to zero;- it is possible to misuse transactions with “virtual currency” for the purpose of

criminal activities including money laundering.

60

User decides to make a transfer to other user

Their Bitcoin stored in wallets

electronical addresses with balance records

transaction signed by private key and distributed

everybody can verify it using public key

Approx. every 10 min miners combine all new transactions in a block

powerful computers calculate functions

searching for correct value to solve a

block. The function uses a code of

previous block, data of the new block

and random values

the miner solving a block receives 25 Bitcoins

Bitcoin transfer completed(technologically irrevocable)

Reward – main motive to spend a resource in validation of transactions

Blocks combined in blockchain

Bitcoin

1BvBMSEYstWetqTFn5Au4m4GFg7xJaNVN2

Blockchain

transaction or list of transactions create a block

all participants in the network receive information about new block

participants approve the block

block has been attached to the chain thus creating indelible un sound record

distributed database

Conclusions• Payment systems are cornerstone of country’s payment

environment – that is the environment where funds flows are concentrated from all levels of the payment environment.

• Payment systems are interlinked with each other therefore risks in one payment system may impact other.

• Banking system has essential role in the development of means of payment and infrastructure since they offer services to customers.

• Development of means of payment in Latvia shows positive trend – society uses cashless means of payment, which are more safe and convenient compared to cash more frequently.

THANK YOU FOR YOUR ATTENTION!DENISS FILIPOVS

Head of Payment Systems Policy DivisionPayment Systems Department

Latvijas Banka