lecture 3

DESCRIPTION

Managerial ACCTTRANSCRIPT

Lecture 3

Cost flows and cost terminology

1

Product and Period CostsCharacteristic Product costs Period costs

What constitutes this cost?

Costs related to getting a product or service ready to be sold (i.e. costs incurred in the production process)

Costs that are other than product costs. Related to marketing and administration

Can they be “inventoried”?

Yes. They are inventoried until the products or services are sold to the customer. Called “inventoriable costs”

No. They can’t be inventoried and therefore they can’t flow through inventory accounts

When are they expensed?

Expensed when sold Expensed in the same period that they are incurred. Called “period costs”

Where do they appear in the income statement?

Above the “gross margin” line Below the “gross margin” line

Flow of Costs: Service organizations

Consultant salaries, Travel cost to client sites

Administrator salaries, Travel cost for marketing

staff, advertising cost

Revenues – cost of providing services = Gross margin

- Selling & administration costs = Profit before taxes

Product costs

Period costs

Income Statement

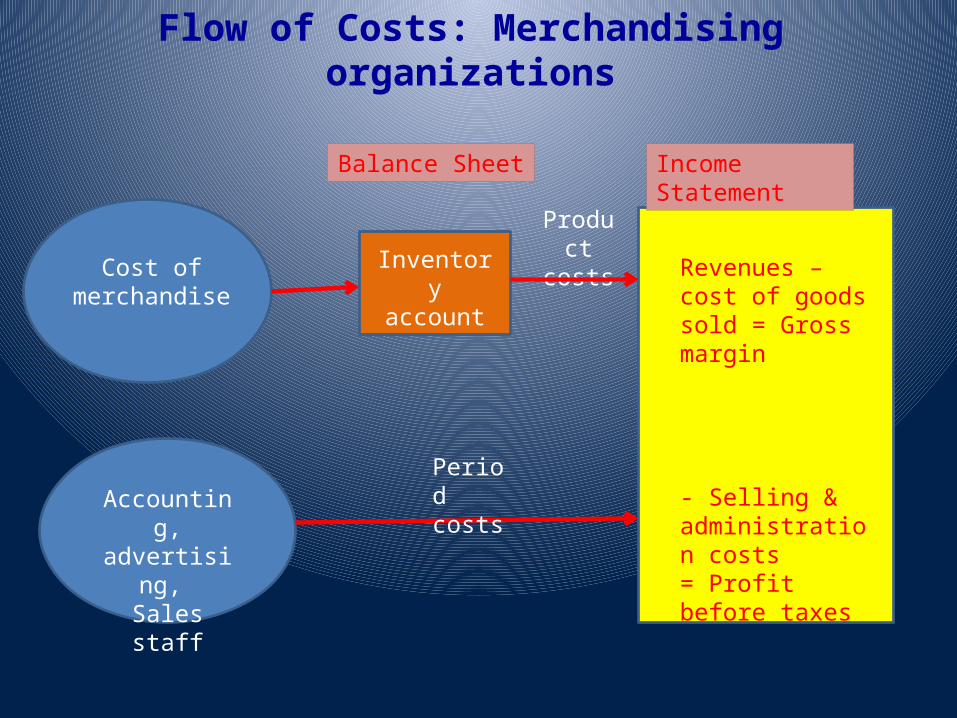

Flow of Costs: Merchandising organizations

Cost of merchandise

Accounting, advertising,

Sales staff

Revenues – cost of goods sold = Gross margin

- Selling & administration costs = Profit before taxes

Product costs

Period costs

Inventory account

Income StatementBalance Sheet

Manufacturing Costs

TheProduct

DirectLabor

DirectMaterial

Manufacturing Overhead

Manufacturing OverheadAll other manufacturing costs

Materials used to support the production process. Examples: lubricants and

cleaning supplies used in an automobile assembly plant.

IndirectLabor

IndirectMaterial

OtherCosts

Cost of personnel who do not work directly on the

product. Examples: maintenance workers,

janitors and security guards.

Examples: depreciation on plant and

equipment, property taxes, insurance,

utilities.

Manufacturing Cost Flows

ManufacturingOverhead

Raw Material

Work in Process

FinishedGoods

Cost of GoodsSold

Selling andAdministrative

Material Purchases

Direct Labor

Balance Sheet Costs Inventories

Income StatementExpenses

Selling andAdministrative

Period Expenses

Product costs

Classifications of Costs in Manufacturing Companies

Manufacturing costs are oftencombined as follows:

PrimeCost

ConversionCost

DirectMaterial

DirectLabor

ManufacturingOverhead

Mechanics of Cost Allocations

• Each allocation has four elements– Cost Pool– Cost objects– Cost Driver– Allocation Volume

• Each allocation has two steps– Calculate rate

• Rate = Cost in pool Denominator volume– Allocate cost to cost object

• Allocated amount = # of driver units in object rate

Cost allocation: example• Stan and James are married to Amy and Gail. The two families

plan a trip for Spring break from Dallas to San Antonio (320 miles each way). They agree to share the costs between the two families. The rental and gas cost comes to $400. At the last minute, Mark, Gail’s brother also decides to join the trip.

• While on their way back from San Antonio, James, Gail and Mark get down in Austin (100 miles from San Antonio) to spend a couple of days in Austin with family. Mark drops James and Gail back in Dallas.

• How should the rental and gas cost to be shared by the two families?

10

Cost allocation: Example• Method 1: Number of families as the cost allocation driver.

– Cost per family = $ 400 / 2 = $200 per family• Method 2: Number of persons as the cost allocation driver.

– Cost per person = $ 400 / 5 = $80 per person– Allocated Cost to Stan’s family = 2 X $80 = $160– Allocated Cost to James’ family = 3 X $80 = $240

• Method 3: Number of passenger miles as the cost allocation driver. Total # of passenger miles travelled = (320 X 5) + {(320 X 2)+(100 X 3) = 2,540

• Cost per passenger mile = $400/2,540 = $0.1575• Cost allocated to Stan’s family =(640X2) X 0.1575 = $201.58 • Cost allocated to James’s family = (420X3) X 0.1575 = $198.42

11

Beware of cost allocations• Uses of allocations

– Inventory valuation, decisions, behavioral• Allocation basis versus cost driver

– GAAP needs allocations– Decisions need assignment– These two are not necessarily the same

• Allocations make it appear as if the allocated cost is variable in the number of driver units

• Cost may be fixed in the short run

• Using allocated cost for decision making can lead to errors

12