lecture 15 - the university of manchestersf/20912lecture15.pdflecture 15 sergei fedotov ......

TRANSCRIPT

Lecture 15

Sergei Fedotov

20912 - Introduction to Financial Mathematics

Sergei Fedotov (University of Manchester) 20912 2010 1 / 6

Lecture 15

1 Black-Scholes Equation and Replicating Portfolio

2 Static and Dynamic Risk-Free Portfolio

Sergei Fedotov (University of Manchester) 20912 2010 2 / 6

Replicating Portfolio

The aim is to show that the option price V (S , t) satisfies theBlack-Scholes equation

∂V

∂t+

1

2σ2

S2 ∂2V

∂S2+ rS

∂V

∂S− rV = 0.

Sergei Fedotov (University of Manchester) 20912 2010 3 / 6

Replicating Portfolio

The aim is to show that the option price V (S , t) satisfies theBlack-Scholes equation

∂V

∂t+

1

2σ2

S2 ∂2V

∂S2+ rS

∂V

∂S− rV = 0.

Consider replicating portfolio of ∆ shares held long and N bonds heldshort.

Sergei Fedotov (University of Manchester) 20912 2010 3 / 6

Replicating Portfolio

The aim is to show that the option price V (S , t) satisfies theBlack-Scholes equation

∂V

∂t+

1

2σ2

S2 ∂2V

∂S2+ rS

∂V

∂S− rV = 0.

Consider replicating portfolio of ∆ shares held long and N bonds heldshort. The value of portfolio: Π = ∆S − NB . Recall that a pair (∆,N) iscalled a trading strategy.

How to find (∆,N) such that Πt = Vt?

Sergei Fedotov (University of Manchester) 20912 2010 3 / 6

Replicating Portfolio

The aim is to show that the option price V (S , t) satisfies theBlack-Scholes equation

∂V

∂t+

1

2σ2

S2 ∂2V

∂S2+ rS

∂V

∂S− rV = 0.

Consider replicating portfolio of ∆ shares held long and N bonds heldshort. The value of portfolio: Π = ∆S − NB . Recall that a pair (∆,N) iscalled a trading strategy.

How to find (∆,N) such that Πt = Vt?

• SDE for a stock price S(t) : dS = µSdt + σSdW .

• Equation for a bond price B (t) : dB = rBdt.

Sergei Fedotov (University of Manchester) 20912 2010 3 / 6

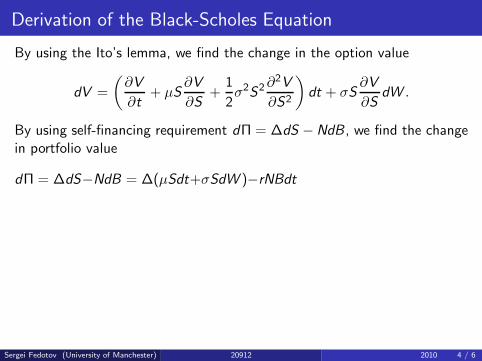

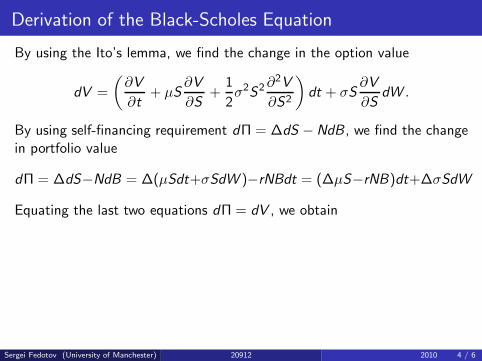

Derivation of the Black-Scholes Equation

By using the Ito’s lemma, we find the change in the option value

dV =

(

∂V

∂t+ µS

∂V

∂S+

1

2σ2

S2 ∂2V

∂S2

)

dt + σS∂V

∂SdW .

Sergei Fedotov (University of Manchester) 20912 2010 4 / 6

Derivation of the Black-Scholes Equation

By using the Ito’s lemma, we find the change in the option value

dV =

(

∂V

∂t+ µS

∂V

∂S+

1

2σ2

S2 ∂2V

∂S2

)

dt + σS∂V

∂SdW .

By using self-financing requirement dΠ = ∆dS −NdB , we find the changein portfolio value

dΠ = ∆dS−NdB = ∆(µSdt+σSdW )−rNBdt

Sergei Fedotov (University of Manchester) 20912 2010 4 / 6

Derivation of the Black-Scholes Equation

By using the Ito’s lemma, we find the change in the option value

dV =

(

∂V

∂t+ µS

∂V

∂S+

1

2σ2

S2 ∂2V

∂S2

)

dt + σS∂V

∂SdW .

By using self-financing requirement dΠ = ∆dS −NdB , we find the changein portfolio value

dΠ = ∆dS−NdB = ∆(µSdt+σSdW )−rNBdt = (∆µS−rNB)dt+∆σSdW

Sergei Fedotov (University of Manchester) 20912 2010 4 / 6

Derivation of the Black-Scholes Equation

By using the Ito’s lemma, we find the change in the option value

dV =

(

∂V

∂t+ µS

∂V

∂S+

1

2σ2

S2 ∂2V

∂S2

)

dt + σS∂V

∂SdW .

By using self-financing requirement dΠ = ∆dS −NdB , we find the changein portfolio value

dΠ = ∆dS−NdB = ∆(µSdt+σSdW )−rNBdt = (∆µS−rNB)dt+∆σSdW

Equating the last two equations dΠ = dV , we obtain

Sergei Fedotov (University of Manchester) 20912 2010 4 / 6

Derivation of the Black-Scholes Equation

By using the Ito’s lemma, we find the change in the option value

dV =

(

∂V

∂t+ µS

∂V

∂S+

1

2σ2

S2 ∂2V

∂S2

)

dt + σS∂V

∂SdW .

By using self-financing requirement dΠ = ∆dS −NdB , we find the changein portfolio value

dΠ = ∆dS−NdB = ∆(µSdt+σSdW )−rNBdt = (∆µS−rNB)dt+∆σSdW

Equating the last two equations dΠ = dV , we obtain

∆ = ∂V

∂S,

Sergei Fedotov (University of Manchester) 20912 2010 4 / 6

Derivation of the Black-Scholes Equation

By using the Ito’s lemma, we find the change in the option value

dV =

(

∂V

∂t+ µS

∂V

∂S+

1

2σ2

S2 ∂2V

∂S2

)

dt + σS∂V

∂SdW .

By using self-financing requirement dΠ = ∆dS −NdB , we find the changein portfolio value

dΠ = ∆dS−NdB = ∆(µSdt+σSdW )−rNBdt = (∆µS−rNB)dt+∆σSdW

Equating the last two equations dΠ = dV , we obtain

∆ = ∂V

∂S, −rNB = ∂V

∂t+ 1

2σ2S2 ∂2V

∂S2 .

Sergei Fedotov (University of Manchester) 20912 2010 4 / 6

Derivation of the Black-Scholes Equation

By using the Ito’s lemma, we find the change in the option value

dV =

(

∂V

∂t+ µS

∂V

∂S+

1

2σ2

S2 ∂2V

∂S2

)

dt + σS∂V

∂SdW .

By using self-financing requirement dΠ = ∆dS −NdB , we find the changein portfolio value

dΠ = ∆dS−NdB = ∆(µSdt+σSdW )−rNBdt = (∆µS−rNB)dt+∆σSdW

Equating the last two equations dΠ = dV , we obtain

∆ = ∂V

∂S, −rNB = ∂V

∂t+ 1

2σ2S2 ∂2V

∂S2 .

Since NB = ∆S − Π =(

S∂V

∂S− V

)

, we get the classical Black-Scholesequation

∂V

∂t+

1

2σ2

S2 ∂2V

∂S2+ rS

∂V

∂S− rV = 0.

Sergei Fedotov (University of Manchester) 20912 2010 4 / 6

Static Risk-free Portfolio

Let me remind you a Put-Call Parity. We set up the portfolio consisting oflong position in one stock, long position in one put and short position inone call with the same T and E .

Sergei Fedotov (University of Manchester) 20912 2010 5 / 6

Static Risk-free Portfolio

Let me remind you a Put-Call Parity. We set up the portfolio consisting oflong position in one stock, long position in one put and short position inone call with the same T and E . The value of this portfolio isΠ = S + P − C .

Sergei Fedotov (University of Manchester) 20912 2010 5 / 6

Static Risk-free Portfolio

Let me remind you a Put-Call Parity. We set up the portfolio consisting oflong position in one stock, long position in one put and short position inone call with the same T and E . The value of this portfolio isΠ = S + P − C .The payoff for this portfolio is

ΠT = S + max (E − S , 0) − max (S − E , 0)

Sergei Fedotov (University of Manchester) 20912 2010 5 / 6

Static Risk-free Portfolio

Let me remind you a Put-Call Parity. We set up the portfolio consisting oflong position in one stock, long position in one put and short position inone call with the same T and E . The value of this portfolio isΠ = S + P − C .The payoff for this portfolio is

ΠT = S + max (E − S , 0) − max (S − E , 0) = E

The payoff is always the same whatever the stock price is at t = T .

Sergei Fedotov (University of Manchester) 20912 2010 5 / 6

Static Risk-free Portfolio

Let me remind you a Put-Call Parity. We set up the portfolio consisting oflong position in one stock, long position in one put and short position inone call with the same T and E . The value of this portfolio isΠ = S + P − C .The payoff for this portfolio is

ΠT = S + max (E − S , 0) − max (S − E , 0) = E

The payoff is always the same whatever the stock price is at t = T .

Using No Arbitrage Principle, we obtain

St + Pt − Ct = Ee−r(T−t),

where Ct = C (St , t) and Pt = P (St , t).

Sergei Fedotov (University of Manchester) 20912 2010 5 / 6

Static Risk-free Portfolio

Let me remind you a Put-Call Parity. We set up the portfolio consisting oflong position in one stock, long position in one put and short position inone call with the same T and E . The value of this portfolio isΠ = S + P − C .The payoff for this portfolio is

ΠT = S + max (E − S , 0) − max (S − E , 0) = E

The payoff is always the same whatever the stock price is at t = T .

Using No Arbitrage Principle, we obtain

St + Pt − Ct = Ee−r(T−t),

where Ct = C (St , t) and Pt = P (St , t).

This is an example of complete risk elimination.

Definition: The risk of a portfolio is the variance of the return.Sergei Fedotov (University of Manchester) 20912 2010 5 / 6

Dynamic Risk-Free Portfolio

Put-Call Parity is an example of complete risk elimination when we carryout only one transaction in call/put options and underlying security.

Sergei Fedotov (University of Manchester) 20912 2010 6 / 6

Dynamic Risk-Free Portfolio

Put-Call Parity is an example of complete risk elimination when we carryout only one transaction in call/put options and underlying security.

Let us consider the dynamic risk elimination procedure.

We could set up a portfolio consisting of a long position in one call optionand a short position in ∆ shares.

The value is Π = C − ∆S .

Sergei Fedotov (University of Manchester) 20912 2010 6 / 6

Dynamic Risk-Free Portfolio

Put-Call Parity is an example of complete risk elimination when we carryout only one transaction in call/put options and underlying security.

Let us consider the dynamic risk elimination procedure.

We could set up a portfolio consisting of a long position in one call optionand a short position in ∆ shares.

The value is Π = C − ∆S .

We can eliminate the random component in Π by choosing

∆ =∂C

∂S.

This is a ∆-hedging! It requires a continuous rebalancing of a number ofshares in the portfolio Π.

Sergei Fedotov (University of Manchester) 20912 2010 6 / 6