lecture 1 - course overview ppt (1)

TRANSCRIPT

1

Lecture 1 - Course Overview

FINM2002 Derivatives

FINM7041 Applied Derivatives

1

1. Course Overview

• This course builds upon the knowledge

you have developed in Foundations of

Finance.

• The unit provides in-depth coverage of

options, futures, forwards and swaps on a

range of underlying commodities including

stocks, interest rates, foreign exchange as

well as more exotic instruments such as

weather and electricity derivatives. 2

1. Course Overview

• At the completion of this unit students are

expected to have a good understanding of

how derivative instruments are priced,

traded and used.

3

2. Lecture Overview • In this lecture we will:

– Recap the basics of forward, futures and options

contracts;

– Revisit the concepts of hedging, speculation and

arbitrage; and

– Discuss the mechanics of futures and forward

markets.

– It would be a good idea to review your Foundations of

Finance notes to ensure you are familiar with all of

the terminology pertaining to futures, forwards and

options contracts. We will only discuss this

prerequisite material briefly.

4

2

3. The Nature of Derivatives

• A derivative is an instrument whose value

depends on the values of other more basic

underlying variables.

• Examples of derivative contracts include

forward, futures and options contracts.

5

4. In What Ways are Derivatives Used

• Derivatives can be used to:

– hedge risks;

– speculate (take a view on the future direction

of the market);

– lock in an arbitrage profit;

– change the nature of a liability; and,

– change the nature of an investment without

incurring the costs of selling one portfolio and

buying another.

6

5. Forwards and Futures Contracts

• A futures/forward contract is an

agreement to buy or sell an asset at a

certain time in the future for a certain

price.

• By contrast in a spot contract there is an

agreement to buy or sell the asset

immediately (or within a very short

period of time).

7

5. Forwards and Futures Contracts

• The future/forward prices for a particular

contract is the price at which you agree to

buy or sell the underlying asset.

• It is determined by supply and demand in

the same way as a spot price.

8

3

5. Forwards and Futures Contracts

• In a forward or futures contracts:

– The party that has agreed to buy has a long

position.

They have a final payoff of St-F.

– The party that has agreed to sell has a

short position.

They have a final payoff of F- St .

9

5. Forwards and Futures Contracts

• Example of a forward/futures contract:

– It is January and an investor enters into

a long futures contract on COMEX to

buy 100 oz of gold @ $1,200 in April

– If in April the spot price of gold ends up

being $1,215 per oz, what is the

investor’s profit?

• As the investor is the long position, the

payoff from the contract is ST-F, which

equals ($1215 - $1200) x 100 = $1,500. 10

5. Forwards and Futures Contracts • No money changes hands when forward and futures contracts

are first negotiated & the contract is settled at maturity.

• The initial value of the contract is zero.

• Forward contract are similar to futures except that they trade in

the over-the-counter market. Futures contracts on the other

hand are exchange traded instruments. In Australia, futures

contracts are traded on the Australian Securities Exchange

(ASX).

• In addition, if you recall from Foundations of Finance,

intermediate gains or losses are posted each day during the

life of the futures contract. This feature is known as marking

to market. The intermediate gains or losses are given by the

difference between today’s futures price and yesterday’s futures

price. These monies are transferred between the margin

accounts of contract parties.

11

5. Forwards and Futures Contracts

• The forward/futures price for a contract is the

delivery price that would be applicable to the contract

if were negotiated today (i.e., it is the delivery price

that would make the contract worth exactly zero).

• In other words, it would make no difference whether

you entered into the forward contract to receive the

asset in 6 months from now, or bought the asset

today and stored it for 6 months. The cost of either

strategy would be identical.

• The forward price may be different for contracts of

different maturities.

12

4

5. Forwards and Futures Contracts

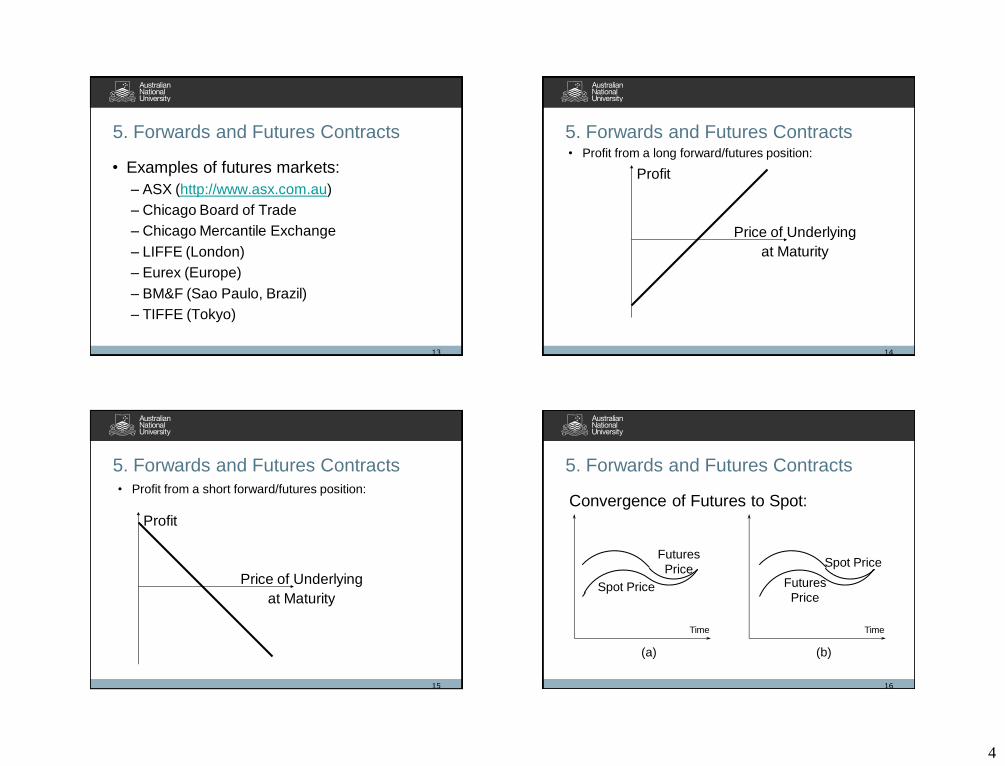

• Examples of futures markets:

– ASX (http://www.asx.com.au)

– Chicago Board of Trade

– Chicago Mercantile Exchange

– LIFFE (London)

– Eurex (Europe)

– BM&F (Sao Paulo, Brazil)

– TIFFE (Tokyo)

13

5. Forwards and Futures Contracts • Profit from a long forward/futures position:

14

Profit

Price of Underlying

at Maturity

5. Forwards and Futures Contracts • Profit from a short forward/futures position:

15

Profit

Price of Underlying

at Maturity

5. Forwards and Futures Contracts

Convergence of Futures to Spot:

16

Time Time

(a) (b)

Futures

Price Futures

Price Spot Price

Spot Price

5

5. Forwards and Futures Contracts

• As the delivery month of a futures contract is

approached, the futures price converges to the spot

price of the underlying asset. When the delivery price is

reached, the futures price equals, or is very close to the

spot price.

• If the futures price is above the spot price during the

delivery period, traders will have an arbitrage

opportunity, and will short the futures contract, buy

the asset and make delivery. This will force the futures

price to fall and converge to the spot price.

17

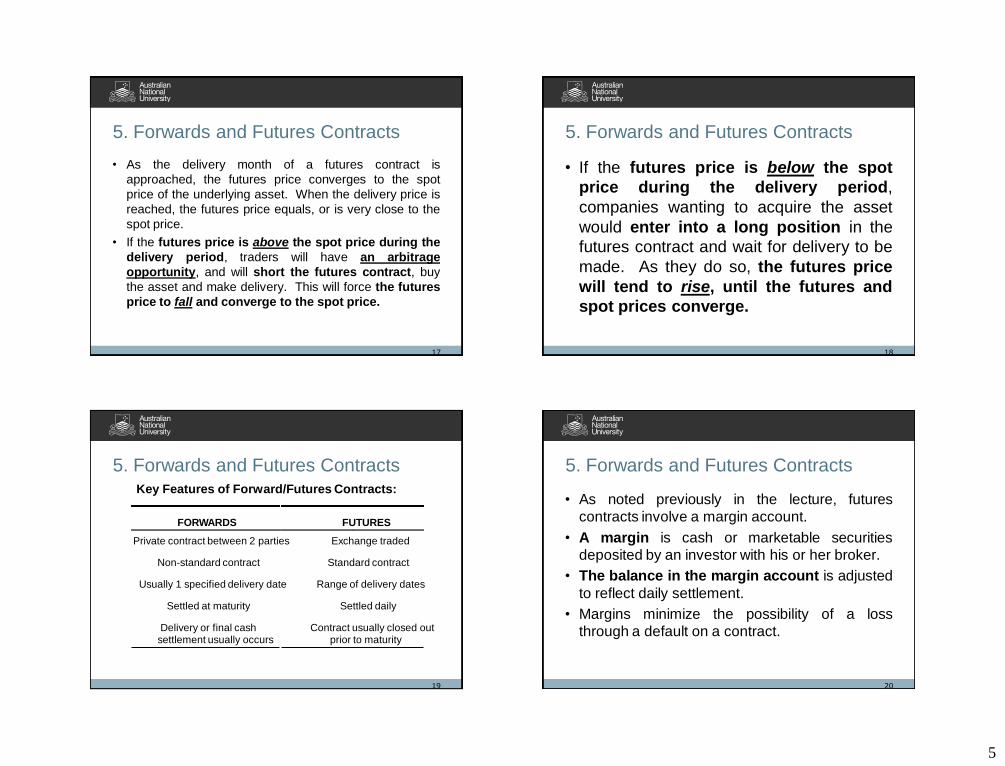

5. Forwards and Futures Contracts

• If the futures price is below the spot

price during the delivery period,

companies wanting to acquire the asset

would enter into a long position in the

futures contract and wait for delivery to be

made. As they do so, the futures price

will tend to rise, until the futures and

spot prices converge.

18

5. Forwards and Futures Contracts

19

Private contract between 2 parties Exchange traded

Non-standard contract Standard contract

Usually 1 specified delivery date Range of delivery dates

Settled at maturity Settled daily

Delivery or final cash settlement usually occurs

Contract usually closed out prior to maturity

FORWARDS FUTURES

Key Features of Forward/Futures Contracts:

5. Forwards and Futures Contracts

• As noted previously in the lecture, futures

contracts involve a margin account.

• A margin is cash or marketable securities

deposited by an investor with his or her broker.

• The balance in the margin account is adjusted

to reflect daily settlement.

• Margins minimize the possibility of a loss

through a default on a contract.

20

6

5. Forwards and Futures Contracts

• Closing out a futures position involves

entering into an offsetting trade. For example, if

you hold a long position in wool, to close it out

you would take a short position on wool on the

same quantity with the same maturity date.

• Most futures contracts are closed out before

maturity.

21

5. Forwards and Futures Contracts

• If a contract is not closed out before maturity,

it is usually settled by delivering the assets

underlying the contract. When there are

alternatives about what is delivered, where it is

delivered, and when it is delivered, the party

with the short position chooses.

• Some contracts (for example, those on stock

indices and Eurodollars) are settled in cash.

• The terms of the contract will stipulate whether

there is physical or cash settlement.

22

5. Forwards and Futures Contracts

• Some futures terminology:

– Open interest: the total number of contracts

outstanding.

• equal to number of long positions or

number of short positions.

– Settlement price: the price just before the final bell

each day.

• used for the daily settlement process.

– Volume of trading: the number of trades in 1 day.

23

5. Forwards and Futures Contracts

• Regulation of futures markets is

designed to protect the public interest.

• Regulators try to prevent questionable

trading practices by either individuals on

the floor of the exchange or outside

groups.

24

7

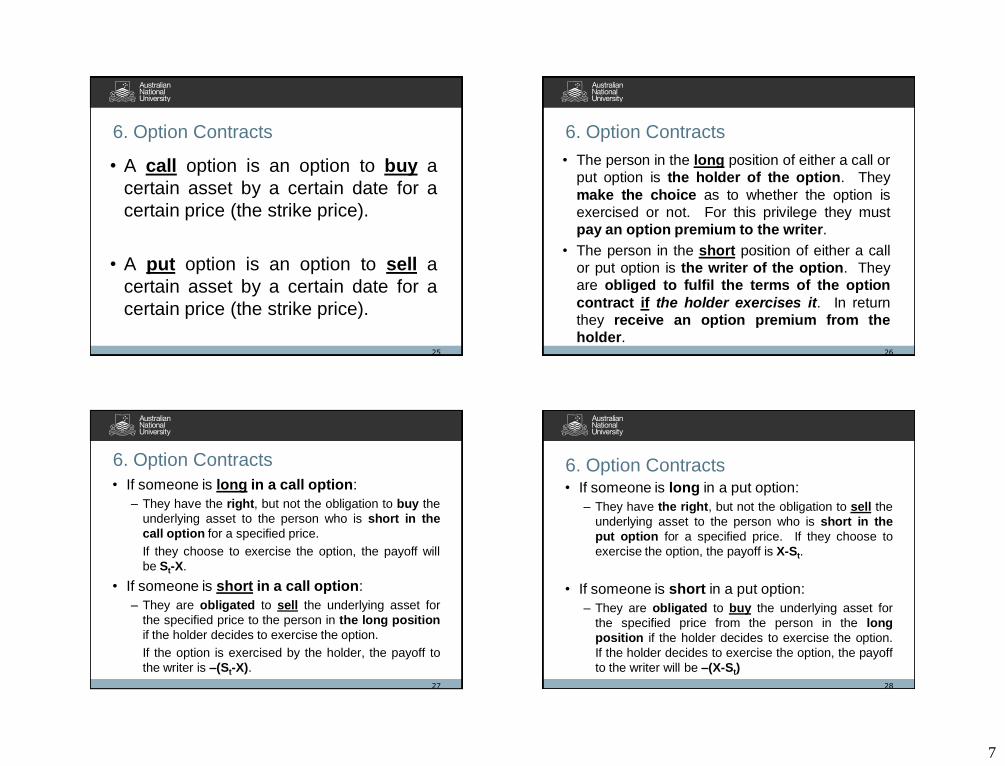

6. Option Contracts

• A call option is an option to buy a

certain asset by a certain date for a

certain price (the strike price).

• A put option is an option to sell a

certain asset by a certain date for a

certain price (the strike price).

25

6. Option Contracts

• The person in the long position of either a call or

put option is the holder of the option. They

make the choice as to whether the option is

exercised or not. For this privilege they must

pay an option premium to the writer.

• The person in the short position of either a call

or put option is the writer of the option. They

are obliged to fulfil the terms of the option

contract if the holder exercises it. In return

they receive an option premium from the

holder. 26

6. Option Contracts

• If someone is long in a call option:

– They have the right, but not the obligation to buy the

underlying asset to the person who is short in the

call option for a specified price.

If they choose to exercise the option, the payoff will

be St-X.

• If someone is short in a call option:

– They are obligated to sell the underlying asset for

the specified price to the person in the long position

if the holder decides to exercise the option.

If the option is exercised by the holder, the payoff to

the writer is –(St-X).

27

6. Option Contracts • If someone is long in a put option:

– They have the right, but not the obligation to sell the

underlying asset to the person who is short in the

put option for a specified price. If they choose to

exercise the option, the payoff is X-St.

• If someone is short in a put option:

– They are obligated to buy the underlying asset for

the specified price from the person in the long

position if the holder decides to exercise the option.

If the holder decides to exercise the option, the payoff

to the writer will be –(X-St)

28

8

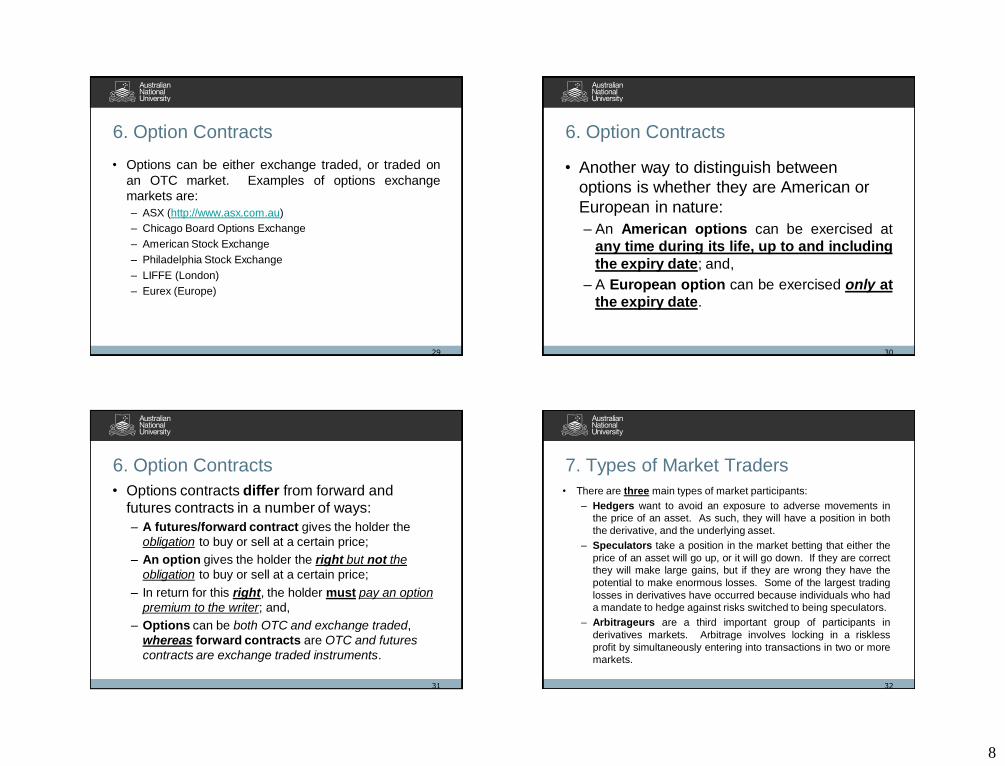

6. Option Contracts

• Options can be either exchange traded, or traded on

an OTC market. Examples of options exchange

markets are:

– ASX (http://www.asx.com.au)

– Chicago Board Options Exchange

– American Stock Exchange

– Philadelphia Stock Exchange

– LIFFE (London)

– Eurex (Europe)

29

6. Option Contracts

• Another way to distinguish between

options is whether they are American or

European in nature:

– An American options can be exercised at

any time during its life, up to and including

the expiry date; and,

– A European option can be exercised only at

the expiry date.

30

6. Option Contracts

• Options contracts differ from forward and

futures contracts in a number of ways:

– A futures/forward contract gives the holder the

obligation to buy or sell at a certain price;

– An option gives the holder the right but not the

obligation to buy or sell at a certain price;

– In return for this right, the holder must pay an option

premium to the writer; and,

– Options can be both OTC and exchange traded,

whereas forward contracts are OTC and futures

contracts are exchange traded instruments.

31

7. Types of Market Traders

• There are three main types of market participants:

– Hedgers want to avoid an exposure to adverse movements in

the price of an asset. As such, they will have a position in both

the derivative, and the underlying asset.

– Speculators take a position in the market betting that either the

price of an asset will go up, or it will go down. If they are correct

they will make large gains, but if they are wrong they have the

potential to make enormous losses. Some of the largest trading

losses in derivatives have occurred because individuals who had

a mandate to hedge against risks switched to being speculators.

– Arbitrageurs are a third important group of participants in

derivatives markets. Arbitrage involves locking in a riskless

profit by simultaneously entering into transactions in two or more

markets.

32

9

7. Types of Market Traders

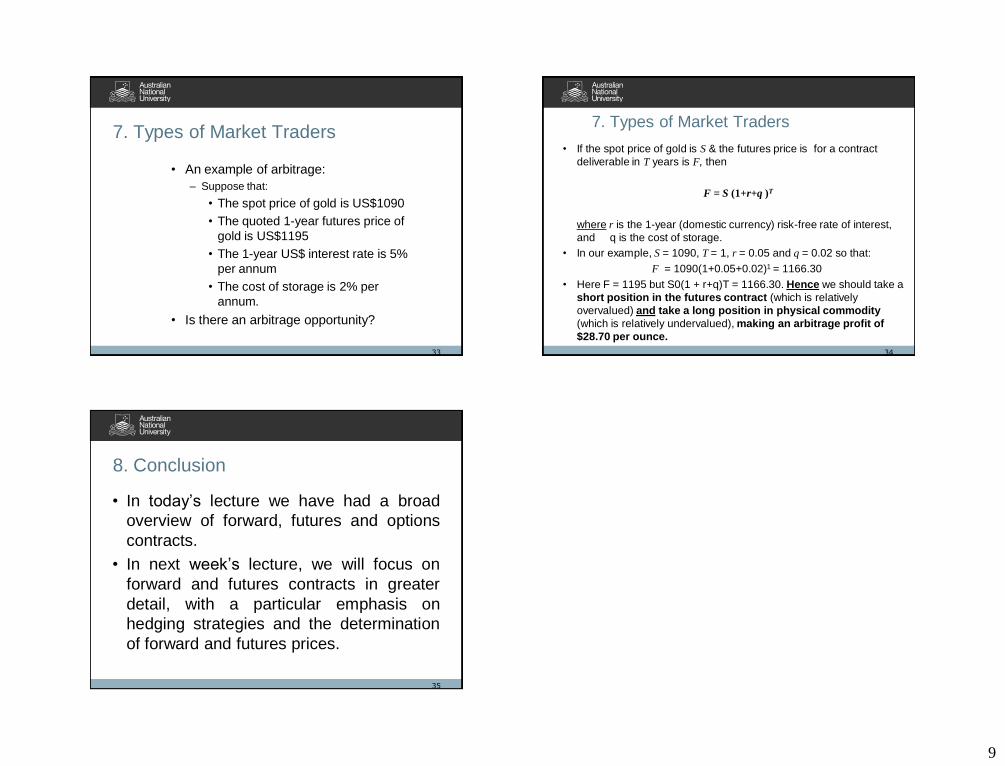

• An example of arbitrage:

– Suppose that:

• The spot price of gold is US$1090

• The quoted 1-year futures price of

gold is US$1195

• The 1-year US$ interest rate is 5%

per annum

• The cost of storage is 2% per

annum.

• Is there an arbitrage opportunity?

33

7. Types of Market Traders

• If the spot price of gold is S & the futures price is for a contract

deliverable in T years is F, then

F = S (1+r+q )T

where r is the 1-year (domestic currency) risk-free rate of interest,

and q is the cost of storage.

• In our example, S = 1090, T = 1, r = 0.05 and q = 0.02 so that:

F = 1090(1+0.05+0.02)1 = 1166.30

• Here F = 1195 but S0(1 + r+q)T = 1166.30. Hence we should take a

short position in the futures contract (which is relatively

overvalued) and take a long position in physical commodity

(which is relatively undervalued), making an arbitrage profit of

$28.70 per ounce.

34

8. Conclusion

• In today’s lecture we have had a broad

overview of forward, futures and options

contracts.

• In next week’s lecture, we will focus on

forward and futures contracts in greater

detail, with a particular emphasis on

hedging strategies and the determination

of forward and futures prices.

35