lebanon weekly monitor (08) 22-02-2014images.mofcom.gov.cn/lb/201402/20140225190300575.pdfindex...

TRANSCRIPT

1Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

Bank Audi sal - Group Research Department - Bank Audi Plaza - Bab Idriss - PO Box 11-2560 - Lebanon - Tel: 961 1 994 000 - email: [email protected]

CONTACTS

RESEARCH

Treasury & Capital Markets

Micky Chebli

(961-1) 977419

Nadine Akkawi

(961-1) 977401

Bechara Serhal

(961-1) 977421

Private Banking

Toufic Aouad

(961-1) 329328

Corporate Banking

Khalil Debs

(961-1) 977229

Marwan Barakat

(961-1) 977409

Jamil Naayem

(961-1) 977406

Salma Saad Baba

(961-1) 977346

Fadi Kanso

(961-1) 977470

Sarah Borgi

(961-1) 964763

Gerard Arabian

(961-1) 964047

Nivine Turyaki

(961-1) 959615

LEBANON MARKETS: WEEK OF FEBRUARY 17 - FEBRUARY 23, 2014

The LEBANON WEEKLY MONITOR

Economy___________________________________________________________________________

p.2 CABINET FORMATION SPURS IMPROVEMENT IN ECONOMIC OUTLOOK Following a stalemate of 10 months since the new Lebanese Prime Minister was designated, a new

cabinet saw the light last week, leaving a positive impression in business circles and a net improvement

in market conditions.

Also in this issuep.2 Lebanon economy to grow by 2.2% in 2014, according to the EIU

p.4 Lebanon’s Consumer Prices Index rises by 2.9% in the first month of 2013

Surveys___________________________________________________________________________

p.5 BEIRUT’S CENTRAL BUSINESS DISTRICT 24TH MOST EXPENSIVE CITY FOR OFFICE

SPACE GLOBALLY, AS PER CUSHMAN AND WAKEFIELD Cushman and Wakefield published its latest report on most expensive office spaces for 67 cities

around the globe.

Also in this issuep.6 Lebanon in the 91st place globally in the environmental performance index

Corporate News___________________________________________________________________________

p.7 NEW CAR SALES REACH 2,372 IN JANUARY 2014According to data compiled by the Association of Car Importers in Lebanon, the number of newly

registered car sales stood at 2,372 cars in January 2014, against 2,358 cars sold in the corresponding

month of 2013.

Also in this issuep.8 Moulin d’Or opens franchise in Sudan

p.8 FFA Real Estate announces Amchit Bay beach project

p.8 Sama Sannine to launch sales of Sannine Heights in spring

Markets In Brief___________________________________________________________________________

p.9 RISING APPETITE FOR LEBANESE PAPERS FOLLOWING CABINET FORMATION Lebanese capital markets were characterized by a rising momentum during this week on improved

investor sentiment following the cabinet formation, with the equity market registering an increase in

activity that was coupled with price rises, and the Eurobond market recording some local and foreign

appetite for Lebanese debt papers, while the FX market maintained its balanced activity. In details, the

BSE total trading value more than doubled week-on-week to reach circa US$ 12 million, and the price

index moved up by 1.7% to close at 111.64, which is its highest level since April 2013. In parallel, the

Eurobond market saw a local and foreign activity on medium-term to long-term papers. The average

yield pursued its downward slope that has started at the beginning of the year on previous bets about

cabinet formation, and the average spread contracted further by 14 bps to 283 bps, which is its highest

contraction in two months. On the FX market, activity remained balanced, with the LP/US$ interbank

rate ranging between LP 1,502 and LP 1,505, while the BDL remained on the sidelines.

2Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

ECONOMY______________________________________________________________________________

CABINET FORMATION SPURS IMPROVEMENT IN ECONOMIC OUTLOOK

Following a stalemate of 10 months since the new Lebanese Prime Minister was designated, a new cabinet

saw the light last week. The recent government formation has left a positive impression in business circles

and an improvement in market conditions, with the development contributing to an atmosphere of

political calm and a considerable reduction of political bickering.

The primary concerns of the government’s work and content of its ministerial statement are actually

threefold. First, the Cabinet must fight security threats while ensuring the cooperation of all political

parties in confronting this issue. Second, the government urgently needs to fulfill its constitutional

requirements, the most important of which is holding the presidential election on time next May.

Third, the Cabinet must address the crucial issue of reviving the economy following a series of setbacks,

including the diversion of both international and domestic investments, the warnings being applied by

the Arab Gulf and a faltering tourism sector. It is believed that the new cabinet might outline a plan aimed

at improving the macro situation and focusing on re-strengthening economic ties with foreign countries.

Since the government formation, Lebanese officials have received Western signals about launching

international conferences to help Lebanon deal with the large influx of Syrian refugees and support

its institutions, particularly the Army, to enable them to face the threat of terrorism. Western countries

have repeatedly called for the necessity of forming a Cabinet in order to keep open the channels of

communication with the international community. These conferences will begin with the International

Support Group for Lebanon on March 5 in Paris followed by a conference in Rome to support the Army

with military aid at the end of March. The date for a third conference, set to take place in Germany, has

not yet been announced.

The new cabinet formation should also allow the ratification of the decrees that represented obstacles

behind the launch of the gas and oil exploration stage in Lebanon as Lebanon’s first offshore licensing

round has been extended a number of times to 10 April 2014 prior to the recent Cabinet formation. The

latter will now ensure the issuance of two decrees related to the delineation of the Offshore blocks and

the model Exploration and Production agreement by the Lebanese Cabinet. It is worth mentioning in this

respect that out of the ten blocks of the Lebanese offshore, five blocks are open for bidding within the

first licensing round, with the possibility of opening additional blocks for bidding after the cabinet session

that will be convened to ratify the two decrees mentioned above. This actually highlights the importance

of containing and minimizing the cost of delay in an economy that enjoys a huge structural potential.

On that background, the Lebanese economy could now see a relative slight growth improvement in 2014

for a number of domestic and regional considerations. According to the simple average of growth rates

forecasted by 9 foreign institutions that estimate and forecast Lebanon’s GDP, the average real GDP growth

rate is likely to improve in 2014 by at least an additional 1% from the growth reported in 2013. Among the

nine forecasting institutions, eight institutions foresee improving growth rates in 2014, while one foresee

stable growth rate over the year. The possible improvement in growth follows a widening cyclical output

gap over the past few years which could provide a favorable base effect for capacity utilization.

_____________________________________________________________________________

LEBANON ECONOMY TO GROW BY 2.2% IN 2014, ACCORDING TO THE EIU

According to a report published by the Economist Intelligence Unit (EIU), few days before the cabinet

formation, real growth in Lebanon is expected to stand at 2.2% in 2014, up from just over 1% in 2013.

Risks are at the downside given the possibility of the security situation deteriorating further. At the same

time, the economy is expected to grow at an average of 3.6% between 2014 and 2018, with private

consumption and investment being dampened by concerns over security and political risks. The reason

3Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

why Lebanon is still able to register even these modest levels of growth is that it serves as a hub for

moving goods in and out of Syria through both official and unofficial channels, as per the EIU.

Fiscal reform will remain a low priority as policymakers will be preoccupied with the potential for political

unrest. According to the EIU, fiscal reform, mainly the expansion of revenue collection, is vital to the

reduction of the structural deficit. The latter is expected to narrow in the years between 2014 and 2018

but will remain wide at around 7% of GDP in 2018. Some debt restructuring is needed in order to make

manage servicing costs. However, the EIU considers that this is unlikely to happen in the near future.

Inflation is expected to remain low in the above mentioned period. However, the EIU expresses concerns

about the accuracy of government numbers and whether they reflect standing pattern, in particular with

the Central Administration of Statistics (CAS) not publishing data for the first few months of the year.

The current account balance will remain in deficit between 2014 and 2018 but is expected to fall from

around 9% of GDP in 2014 to around 2% of GDP in 2018. Lebanon, which is reliant on energy imports, is

vulnerable to changes in international prices.

The report mentions the role of the central bank in maintaining an accommodative policy stance in order

to support the economy. In fact, the BDL has launched in early-2013 a US$ 1.3 billion stimulus program

through provision of cheap loans to banks that they can extend to customers (at an interest rate capped

at 6%). It has been announced that additional funds will be forthcoming in 2014, albeit at a lower level.

The central bank maintains a policy of holding high levels of foreign reserves at US$ 37 billion as of the

third quarter of 2013, equivalent to 14 to 15 months of import cover, in order to offset any potential flight

to quality.

The awaited oil and gas licensing round has been postponed, again, to April. This has raised doubts over

foreign firms’ interest in participating. In fact, in EIU’s view, political squabbling over the control of the

sector presents risk of regulatory instability to investors.

LEBANON ANNUAL ECONOMIC DATA AND FORECASTS

Sources: Economist Intelligence Unit, Bank Audi's Group Research Department

4Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

_____________________________________________________________________________

LEBANON’S CONSUMER PRICES INDEX RISES BY 2.9% IN THE FIRST MONTH OF 2013

According to the latest data released by the Consultation and Research Institute, Lebanon’s consumer

price index rose by 2.9% between end-2013 and end-January 2014. On an annual basis, the inflation rate

reached 2.5% in January 2014. The 12-month moving average stood at 2.5% in January 2014.

The rise seen between end-2013 and end-January 2014 was tied to a price increase posted by the following

components: food and beverages (+6.2%), miscellaneous goods and services (+5.4%), housing (+3.5%),

transportation and telecommunications (+0.5%), recreational services (+0.3%), and apparel (+0.3%).

With regards to the food and beverages component, the price increase was mainly driven by a rise in

the following sub-components: food (+6.7%), vegetables (+34.7%), fruits (+13.2%), and fish and seafood

(+10.5%).

The cost of the miscellaneous category of good and services was driven by a 10.8% increase in the price

of jewelry along with a 4.7% increase in the price of personal care.

The cost of housing services was higher on account of an increase in the fees for household energy

which moved up by 5.2% between end-2013 and end-January 2014. With regards to transportation

and telecommunications, they became more costly as a result of a 0.5% rise in the fees for the former

mentioned component.

The fifth item to have driven the overall CPI increase was recreational services which were higher by 0.3%

between end-2013 and end-January 2014 due to a 1.9% increase in the cost of reading material and

photography. Finally, apparel goods were the sixth item to have supported the overall increase in the

CPI with their prices moving up by 0.3% on account of a 1.9% increase in the cost of clothing and sewing

materials.

CONSUMER PRICE INDEX (12-MONTH MOVING AVERAGE OF EACH YEAR)

Sources: Consultation and Research Institute, Bank Audi's Research Department

5Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

SURVEYS_____________________________________________________________________________

BEIRUT’S CENTRAL BUSINESS DISTRICT 24TH MOST EXPENSIVE CITY FOR OFFICE

SPACE GLOBALLY, AS PER CUSHMAN AND WAKEFIELD

Cushman and Wakefield published its latest report on most expensive office spaces for 67 cities around

the globe. Beirut came out as the 24th most expensive city in 2014, maintaining the rank registered in

2013. It came directly after the cities of Taipei (Taiwan) and Amsterdam (the Netherlands). On the other

hand, it has outpaced Dublin (Ireland) and Jakarta (Indonesia).

The occupancy cost in Beirut’s Central Business District (CBD), including rents and additional costs, came

at € 505 per square meter per year. Cushman and Wakefield considers the CBD office figures as related to

new prime centre, high specification units of a standard size corresponding to demand in each location.

OCCUPANCY RATE(€)/ SQM/ YEAR IN MOST EXPENSIVE LOCATION IN EACH COUNTRY

Sources: Cushman and Wakefield, Bank Audi's Group Research Department

6Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

In the MENA region, the yearly cost of office space in Beirut’s Central Business District, at € 505 per

square meter, came in directly after Dubai International Financial Center (DIFC) with € 734 /SQM/year

and Doha’s CBD with € 659 /SQM/year, and ahead of Manama and Amman with € 231 and € 179 /SQM/

year, respectively. The Middle East saw a buoyant rental market, with prime rents up by as much as 10%

in certain locations.

On the global level, the offices’ market witnessed prime rents increase by 3% in 2013, which is the third

consecutive year of a similar rental performance. London’s West End emerged as the most expensive

office market across the world for the second consecutive year with € 2,122 /SQM /year, outpacing each

of Hong Kong Central and Moscow’s CBD with € 1,432/SQM /year and € 1,092 /SQM /year, respectively.

____________________________________________________________________________

LEBANON IN THE 91ST PLACE GLOBALLY IN THE ENVIRONMENTAL PERFORMANCE

INDEX

The 2014 Environmental Performance Index (EPI) for the year 2014 has been recently published by both

Yale and Columbia Universities, in collaboration with the World Economic Forum. According to the 2014

EPI, Lebanon ranked 91st out of 176 surveyed countries.

The Environmental Performance Index (EPI) ranks how well countries perform on high-priority

environmental issues in two broad policy areas: protection of human health from environmental harm

and protection of ecosystems. Within these two policy objectives, the EPI scores country performance

in nine issue areas comprised of 20 indicators. Indicators in the EPI measure how close countries are to

meeting internationally established targets or, in the absence of agreed-upon targets, how they compare

to the range of observed countries.

On a regional level, Lebanon came directly after each of Morocco and Bahrain while it outpaced each of

Algeria and Oman. On a global level, Lebanon was outpaced by Belize and Nicaragua while it surpassed

each of Algeria and Argentina.

MENA COUNTRIES GLOBAL RANKS IN THE ECONOMIC PERFORMANCE INDEX

Sources: Economic Performance Index, Bank Audi's Group Research Department

7Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

CORPORATE NEWS_____________________________________________________________________________

NEW CAR SALES REACH 2,372 IN JANUARY 2014

According to data compiled by the Association of Car Importers in Lebanon, the number of newly

registered car sales stood at 2,372 cars in January 2014, against 2,358 cars sold in the corresponding

month of 2013.

According to the same source, new car sales in January 2014 compare with 3,414 new car sales in

December 2013. Moreover, the total number of registered new and imported used cars dropped by 21%

in January 2014 in comparison with December 2013.

It is worth noting that 90% of newly registered cars consist of those of smaller sizes. The luxury cars

represent only 2% of the total new cars registered. The orientation of the market toward the small cars

is due to high fuel prices, to the absence of an adapted and structured public transport, and to the very

strong competition between the makes.

Korea’s Kia ranked first in terms of new car registration in January 2014 with a total of 541 cars, against a

total of 538 cars in the same month of 2013. It was followed by Korea’s Hyundai with a total of 361 newly

registered cars in January 2014, lower than the total of 468 cars registered in the corresponding month

of 2013.

Japan’s Toyota came third with 337 newly registered cars in January 2014, up from 125 cars recorded

in the same month of 2013. Fourth was Japan’s Nissan with 257 newly registered cars in January 2014,

compared with a total of 326 cars recorded in the corresponding month of 2013. France’s Renault ranked

fifth with 92 newly registered cars in January 2014, versus a total of 101 cars posted in January 2013.

A breakdown by continent shows that 902 newly registered cars came from Korea in January 2014, down

by 10% from 1,006 cars recorded in January 2013. Those from Japan amounted to 818 cars in January

2014, against 566 cars in January 2013. They were followed by European cars with a total of 496 vehicles

in January 2014, down by 17% from 596 cars recorded in January 2013. Then came those from the US

with 121 cars in January 2014, down by 19% from the total of 149 cars recorded in January 2013.

TOP TEN BRANDS OF NEWLY REGISTERED CARS IN JANUARY 2014

Sources: Association of Car Importers in Lebanon, Bank Audi's Group Research Department

8Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

_____________________________________________________________________________

MOULIN D’OR OPENS FRANCHISE IN SUDAN

Local bakery Moulin d’Or signed a master franchising agreement with the Sudanese N&B food company,

part of the Sudan Elnefeidi Group Holding, with diversified activities representing major international

brands in Sudan.

N&B invested US$ 15 million in the franchising agreement with Moulin d’Or, which would launch a

production facility and a retail store in Khartoum during the second quarter of 2015.

The total area of the production facility would measure 12,000 square meters, and the retail store at 500

square meters.

According to the CEO of Moulin d’Or, the company would be charging royalty fees on the daily turnover,

and the franchisee would be paying for the staff’s compensation in Sudan.

The company is also planning further expansions in Sudan, South Sudan and various countries in the

African continent, as per the same source.

______________________________________________________________________________

FFA REAL ESTATE ANNOUNCES AMCHIT BAY BEACH PROJECT

FFA Real Estate, a member of FFA Private Bank Group, announced that it would be managing the

development of a new beach project called Amchit Bay for a group of local investors. A senior executive

at FFA Real Estate said that construction works would commence during 2014, and the project would be

finalized within two years.

Amchit Bay would stretch over 10,000 square meters of coastal land, and would have a built-up area of

9,000 square meters. The project would reach an investment of US$ 25 million, including the cost of land.

Amchit Bay consists of seaside chalets, totaling six villas and 19 residences, and frontage onto 80 meters

of coastline. The project would include 2,000 square meters of common landscaped green space, with a

fitness area, pool, clubhouse and children’s playground.

______________________________________________________________________________

SAMA SANNINE TO LAUNCH SALES OF SANNINE HEIGHTS IN SPRING

Sama Sannine, a mixed-use project under construction, plans to launch sales of its first phase in April

2014. The 66,000 square meter project is owned by three partners including Saudi-based Amnest Group.

The project comprises Sannine Village and Mountview Hotel.

The first phase of Sannine Village, called Sannine Heights, is composed of four blocks, with four 159

square meter duplexes.

The second and third phases of Sannine Village are The Hillside and The Nest projects, each made up of

eight blocks with 149 square meter chalets.

The fourth phase includes The Courtyard project, which is made up of three large connected blocks, with

four 159 square meter chalets each. As for Mountview Hotel, it includes 44 VIP rooms, two restaurants,

spa and nightclub.

9Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

CAPITAL MARKETS_____________________________________________________________________________

MONEY MARKET: SIGNIFICANT EXPANSION IN LP CDS PORTFOLIO IN 2013

The money market maintained its regular norms, with the local currency liquidity remaining quite

abundant and the overnight rate standing at its low official level of 2.75% set by the Central Bank of

Lebanon. As to Certificates of Deposits, the Central Bank of Lebanon sold this week LP 15 billion in the

45-day category and LP 1 billion in the 60-day category. Interest rates on these two categories stood

unchanged at 3.57% and 3.85% respectively. In addition, the latest figures released by the Association of

Banks in Lebanon showed that the weighted average rate on LP CDs stood at 8.54% at end-December

2013, as compared to 8.62% at end-November 2013 and 9.28% at end-December 2012. The outstanding

CDs portfolio reached LP 33,815 billion at end-December 2013, down from LP 34,196 billion at end-

November 2013, yet significantly up from LP 23,073 billion at end-December 2012.

At the monetary aggregates level, figures for the week ending 6th of February 2014 released this week

showed a decline in local currency deposits of LP 195 billion, as a result of an increase of LP 84 billion in

LP time deposits and a fall of LP 279 billion in LP demand deposits week-on-week. Deposits in foreign

currencies dropped by US$ 98 million. These weekly variations compare to an average weekly rise of

LP 106 billion for LP deposits, and an average weekly decrease of US$ 62 million for foreign currency

deposits since the beginning of the year 2014. Total money supply in its large sense (M4) expanded by

LP 338 billion. This compared to an average weekly contraction of LP 45 billion since the beginning of

the year 2014.

On a cumulative basis, money supply in its large sense (M4) widened by LP 302 billion since the beginning

of the year 2014. This is the result of a rise in local currency denominated time deposits of LP 665 billion, a

decrease in foreign currency deposits of LP 339 billion (the equivalent of US$ 225 million), a contraction

in money supply (M1) of LP 486 billion, and a growth in Treasury bills held by the public of LP 462 billion.

_____________________________________________________________________________

TREASURY BILLS MARKET: A 30 BPS RISE IN WEIGHTED AVERAGE YIELD ON TBS IN 2013

The secondary Treasury bills market continued to be marked by some local activity on the 12-year category,

which was traded at 8.59%. At the level of the primary market, the latest auction’s results (February 20,

2014) showed stability in the average yields on the one-year, two-year and three-year categories at 5.35%,

5.84% and 6.50% respectively. Also, the auction results for value date 13th of February 2014 released

by the Central Bank of Lebanon showed that total subscriptions amounted to LP 251 billion and were

distributed as follows: LP 17 billion in the three-month category, LP 152 billion in the six-month category,

and LP 82 billion in the five-year category. These compare to maturities of LP 16 billion, resulting in a

nominal surplus of LP 235 billion.

The latest monthly report released by the Association of Banks in Lebanon showed that the weighted

average yield on outstanding LP Treasury bills stood at 6.88% at end-December 2013, versus 6.89% at

end-November 2013 and 6.58% at end-December 2012.

INTEREST RATES

Source: Bloomberg

10Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

TREASURY BILLS

Sources: Central Bank of Lebanon, Bloomberg_____________________________________________________________________________

FOREIGN EXCHANGE MARKET: SIGNIFICANT GROWTH IN BDL’S FOREIGN ASSETS

The foreign exchange market maintained its balanced activity during this week, while commercial banks

traded the US Dollar at a rate hovering between LP 1,502 and LP 1,505. Meanwhile, the Central Bank of

Lebanon remained on the sidelines throughout the week.

The Central Bank of Lebanon’s latest bi-monthly balance sheet ending 15th of February 2014 showed

that foreign assets grew by US$ 674 million during the first half of February to reach US$ 36.3 billion mid-

February. Accordingly, the Central Bank’s foreign assets covered 79.6% of LP money supply mid-February

2014, with this coverage ratio rising to 105.7% when accounting for gold reserves estimated at US$ 11.9

billion. In addition, the BDL’s foreign assets covered 20.5 months of imports. These ratios shed light on the

Central Bank’s strong ability to defend the currency peg and meet demand for foreign currencies should

any pressures rise.

EXCHANGE RATES

Source: Bank Audi’s Group Research Department_____________________________________________________________________________

STOCK MARKET: BSE PRICE INDEX UP BY 1.7% ON IMPROVED INVESTOR SENTIMENT

The equity market was marked this week by a rise in activity that was coupled with price increases, mainly

supported by improved investor sentiment following the cabinet formation. The total trading value more

than doubled week-on-week, moving up from US$ 5.2 million last week to US$ 11.7 million this week.

The average daily trading value surged from US$ 1,302 million last week to US$ 2,330 million this week,

triggering a 78.9% jump in the trading volume index to 100.41. The total number of traded shares went

up from 699,783 shares last week to 1,227,407 shares this week. As far as prices are concerned, the BSE

price index went up by 1.7% to 111.64, which is its highest level since April 2013.

11Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

EUROBONDS INDICATORS

Source: Bank Audi’s Group Research Department

AUDI INDICES FOR BSE

Sources: Beirut Stock Exchange, Bank Audi’s Group Research Department

Solidere shares captured 53.08% of activity. Solidere “A” share price rose by 3.8% to close at US$ 13.50, and

Solidere “B” share price surged by 4.4% to US$ 13.38. Banking shares accounted for 46.85% of the total

trading value. Bank Audi’s “listed” share price increased by 1.1% to US$ 6.44. Bank Audi’s GDR price stood

unchanged at US$ 6.60. BLOM’s “listed” share price went up by 2.9% to close at US$ 8.75. BLOM GDR’s

price increased by 3.1% to US$ 9.18. Byblos Bank’s “listed” share price closed 1.8% higher at US$ 1.68. As

to industrial stocks, Holcim’s share price stood unchanged at US$ 14.50.

The Beirut Stock Exchange’s weekly performance compared to an increase of 0.9% in broader Arabian

markets’ share prices (as per S&P Pan-Arab Composite Index) and a 0.3% rise in broader emerging markets’

share prices (as per S&P Emerging Frontier Super Composite Index).

_____________________________________________________________________________

BOND MARKET: FURTHER RISE IN BOND PRICES FOLLOWING CABINET FORMATION

The Eurobond market was characterized by improved investor sentiment this week following the cabinet

formation. This triggered a rise in local and foreign activity on Lebanese debt papers maturing between

2017 and 2027, driving prices up and resulting into contractions in spreads. In details, the weighted

average bond yield continued to follow a downward trajectory, declining by 14 bps week-on-week to

reach 4.73%, and the average spread contracted further by 14 bps to close at 283 bps amidst a significant

drop in Lebanese yields and a small rise in international benchmark yields. For instance, the five-year

US Treasury yields increased from 1.52% last week to 1.55% this week amidst bets that weaker-than-

expected US economic data resulted from harsh winter weather and won’t keep the US Federal Reserve

from reducing bond purchases further. As to the cost of insuring debt, Lebanon’s five-year CDS spread

hovered between 370-390 bps this week versus 370-400 bps in the previous week.

12Week 08 February 17 - February 23, 2014

FEBRUARY 17 - FEBRUARY 23, 2014

WEEK 08

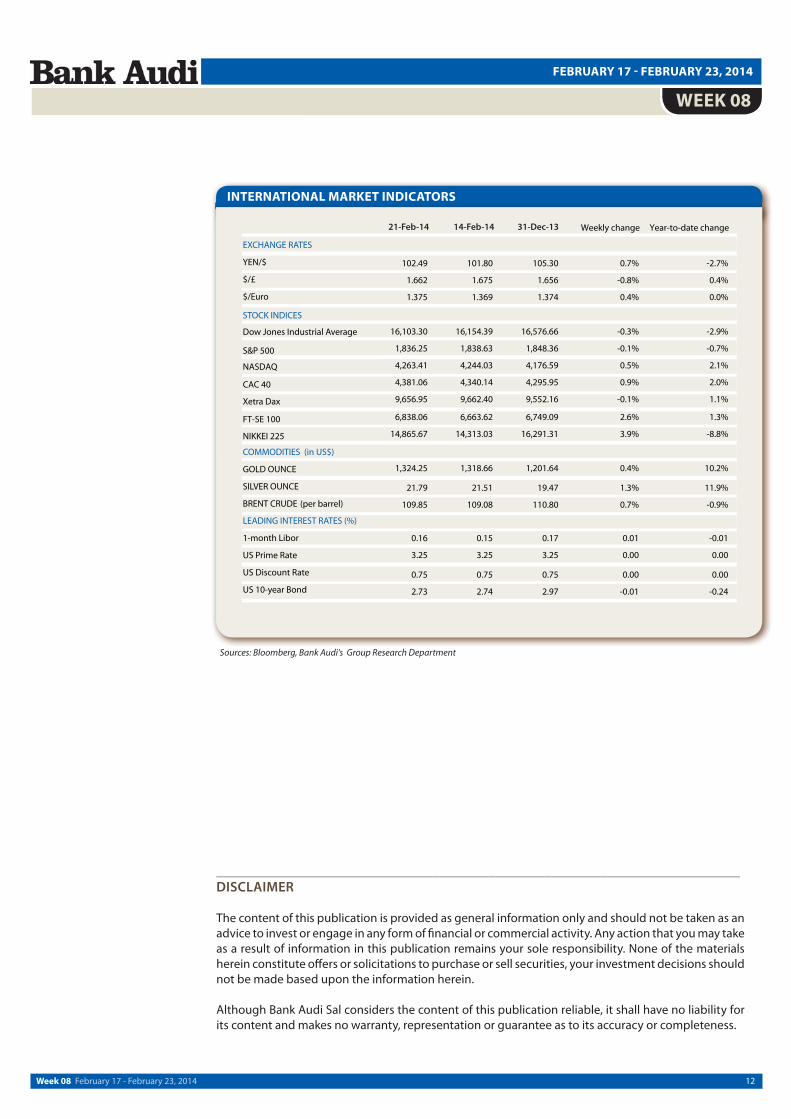

INTERNATIONAL MARKET INDICATORS

Sources: Bloomberg, Bank Audi's Group Research Department

___________________________________________________________________________DISCLAIMER

The content of this publication is provided as general information only and should not be taken as an

advice to invest or engage in any form of financial or commercial activity. Any action that you may take

as a result of information in this publication remains your sole responsibility. None of the materials

herein constitute offers or solicitations to purchase or sell securities, your investment decisions should

not be made based upon the information herein.

Although Bank Audi Sal considers the content of this publication reliable, it shall have no liability for

its content and makes no warranty, representation or guarantee as to its accuracy or completeness.