leal and regulatory issues i b - tkbb consider some of the main issues that arise in connection with...

TRANSCRIPT

WORLD BANK – BRSA –PBAT JOİNT WORKSOP11 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

MİCHAEL J.T. MCMİLLEN

WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

ISTANBUL, TURKEY

MARCH 3, 2017

LEAL AND REGULATORY ISSUES İN ISLAMİC BANKİNG

Curtis, Mallet-Prevost, Colt & Mosle LLPAdvisor to The World Bank

WORLD BANK – BRSA –PBAT JOİNT WORKSOP2

Objective and Perspectives

Objective: Consider some of the main issues that arise in connection with legal and regulatory reform efforts within the Islamic banking sector?

Perspectives:

World Bank advisory activities to capital markets boards, national treasuries and central banks in connection with the implementation of Islamic banking and Islamic capital markets legal and regulatory reforms in various countries.

International perspective, with some references to the issues as applicable in Turkey.

NOTE: Some of these matters have been addressed and resolved, at least in part, in Turkey.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP3

Reform Objectives

Compare each conventional interest-based banking structure with its equivalent Islamic banking structure.

Principles:

there should be a level playing field as between conventional interest-based banking structures and the equivalent Islamic banking structures for all regulatory, legal, financial and economic purposes.

Neither conventional banking nor Islamic banking should have an advantage or a disadvantage.

In the case of taxation, the Islamic banking framework should be tax neutral:

No increased burdens on taxpayers. No less revenue to the taxing authority.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP4

Main Issues

Taxation

Special purpose vehicles

Trusts and beneficial interests in property

Asset backed – asset based considerations and beneficial interests in property

Collateral security

Bankruptcy and insolvency

Shari’ah governance

Willingness of government divisions and entities to participate

WORLD BANK – BRSA –PBAT JOİNT WORKSOP55 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Perspective

WORLD BANK – BRSA –PBAT JOİNT WORKSOP6

Regulatory and Supervisory Perspective

Developing and refining the Islamic finance (banking and capital markets) regime is dependent upon understanding:

The structures and arrangements used by an Islamic bank or window to source funds from the customers and the associated risks.

The role of the bank in the Islamic banking process and the associated risks.

The structures and arrangements used by an Islamic bank to put the customer’s funds to use, which means investing those funds and the associated risks.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP7

Regulatory and Supervisory Perspective

Islamic banks (including Islamic windows) use different structures than are used by conventional interest-based banks.

Most (not all) of the Islamic banking structures are designed to achieve the same ends as interest-based loans. That is:

Both provide financing amounts to customers.

Both provide a return or charge a rate to customers and banks.

The return or rate charged on conventional instruments is “interest”, the return or rate charged on Islamic instruments is “profit” – frequently the rates are the same.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP88 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Islamic Banking Activities

WORLD BANK – BRSA –PBAT JOİNT WORKSOP9

Two Structures: Murabaha and Ijara

Two examples:

Murabaha (cost-plus purchase and sale).

Ijara (lease, which is a sale of usufruct under the Shari’ah).

WORLD BANK – BRSA –PBAT JOİNT WORKSOP1010 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Murabaha

WORLD BANK – BRSA –PBAT JOİNT WORKSOP11

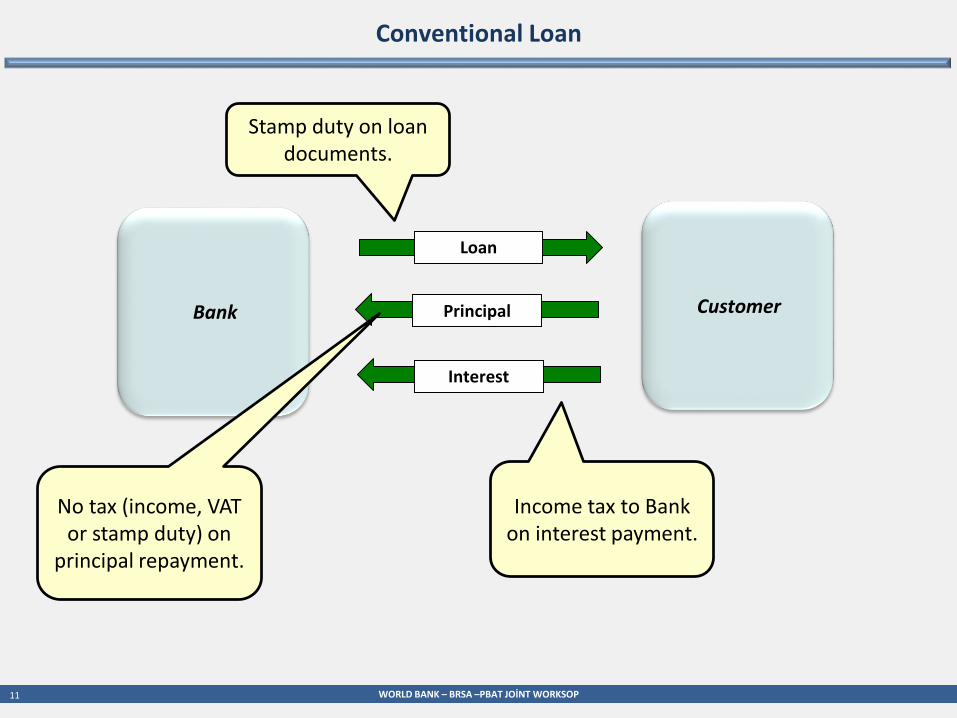

Conventional Loan

Principal CustomerBank

Loan

No tax (income, VAT or stamp duty) on

principal repayment.

Income tax to Bank on interest payment.

Stamp duty on loan documents.

Interest

WORLD BANK – BRSA –PBAT JOİNT WORKSOP12

Murabaha as a Loan Substitute

Purchase and sale of a commodity or other object at a mark-up: itis a sale and must meet all sale requirements

Mediation of a financier in the purchase of an object at the request of a party needing financing.

Financier purchases the object on the spot market and then sells it to the party needing financing on a deferred payment basis

WORLD BANK – BRSA –PBAT JOİNT WORKSOP13

Basic Commodity Murabaha

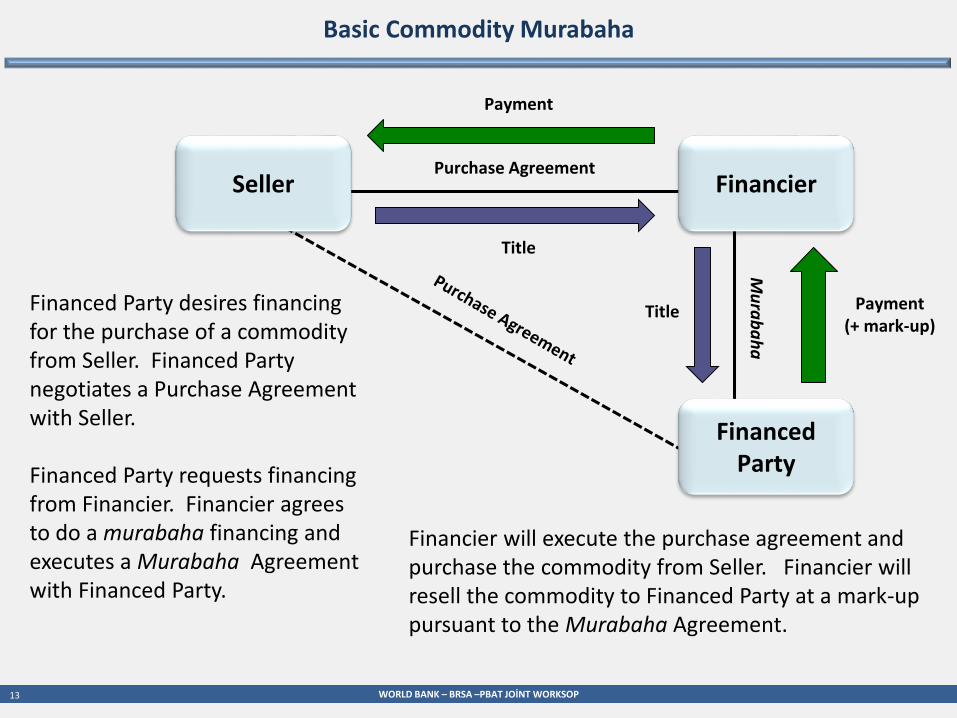

Murabaha

Purchase AgreementSeller

Financier will execute the purchase agreement and purchase the commodity from Seller. Financier will resell the commodity to Financed Party at a mark-up pursuant to the Murabaha Agreement.

Financier

Financed Party

Title

Title Payment (+ mark-up)

Payment

Financed Party desires financing for the purchase of a commodity from Seller. Financed Party negotiates a Purchase Agreement with Seller.

Financed Party requests financing from Financier. Financier agrees to do a murabaha financing and executes a Murabaha Agreement with Financed Party.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP14

Basic Commodity Murabaha

Murabaha

Purchase AgreementSeller Financier

Financed Party

Title

Title Payment (+ mark-up)

Payment

Stamp duty on murabaha documents (equivalent to loan).

VAT on purchase.

Stamp duty purchase documents.

VAT on purchase.

Income tax on profit (interest equivalent)

and on principal equivalent.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP15

MurabahaAgreement

Asset Purchase Agreement

Generic Vector Murabaha Transaction

Seller

Financier purchases the metal from Seller on the spot market for immediate payment. Financier then sells the metal on a deferred payment basis to Financed Party. Financed Party then sells the metal Purchaser on the spot market for immediate payment.

Purchaser

Financier

Financed Party

Title

Title

Spot Market Payment

Title

Spot Market Payment

DeferredPayments

Negotiation of Asset Purchase

Agreement

①②③ There are three VAT, stamp duty and income tax assessments for what is really a loan. In ② VAT is assessed before the payments are made.

①

②

③

WORLD BANK – BRSA –PBAT JOİNT WORKSOP1616 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Lease (Ijara) Transactions

WORLD BANK – BRSA –PBAT JOİNT WORKSOP17

Conventional Loan

Principal CustomerBank

Loan

No tax (income, VAT or stamp duty) on

principal repayment.

Income tax to Bank on interest payment.

Stamp duty on loan documents.

Interest

WORLD BANK – BRSA –PBAT JOİNT WORKSOP18

Lease as Loan

Lease Arrangement CustomerFunding Company

Bank

Loan

Interest and Principalvia

Basic Rent PaymentsPurchase Price Payments

The economic substance of the transaction is a loan from the Bank to the Customer.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP1919 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Simple Lease Transactions

WORLD BANK – BRSA –PBAT JOİNT WORKSOP20

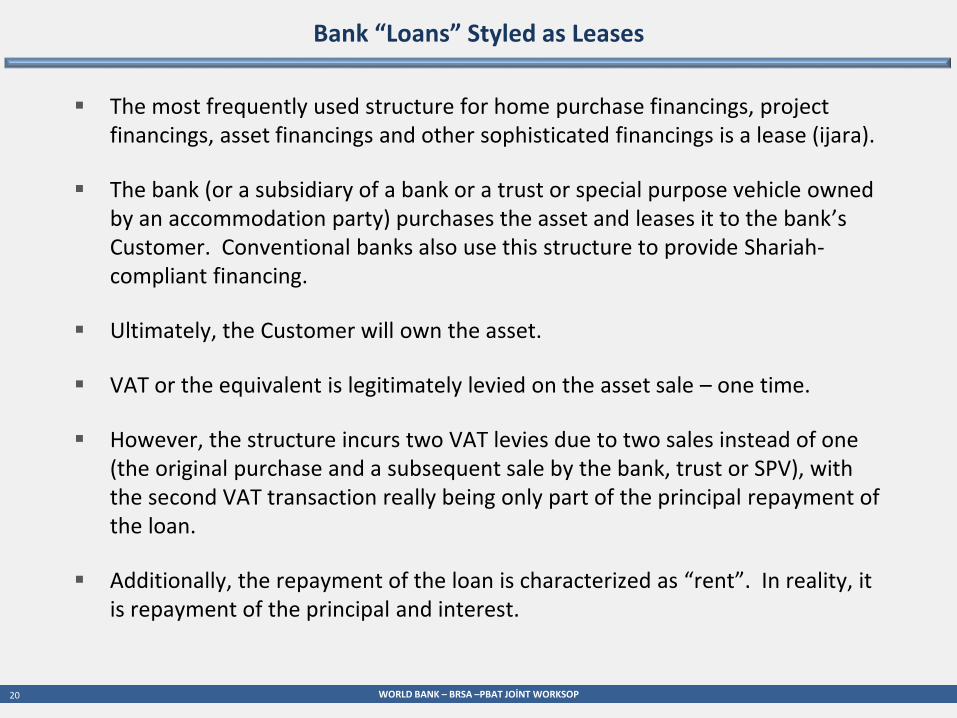

Bank “Loans” Styled as Leases

The most frequently used structure for home purchase financings, project financings, asset financings and other sophisticated financings is a lease (ijara).

The bank (or a subsidiary of a bank or a trust or special purpose vehicle owned by an accommodation party) purchases the asset and leases it to the bank’s Customer. Conventional banks also use this structure to provide Shariah-compliant financing.

Ultimately, the Customer will own the asset.

VAT or the equivalent is legitimately levied on the asset sale – one time.

However, the structure incurs two VAT levies due to two sales instead of one (the original purchase and a subsequent sale by the bank, trust or SPV), with the second VAT transaction really being only part of the principal repayment of the loan.

Additionally, the repayment of the loan is characterized as “rent”. In reality, it is repayment of the principal and interest.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP21

Simple Generic Ijara: Documentation

Understanding to Purchase

Lease (Ijara)

Understanding to Sell

Managing Contractor Agreement

Asset Seller

CustomerBank

Asset Purchase Agreement

The rent on the Lease (Ijara) is really a loan repayment to the bank. Rent is comprised of a basic rent amount (i.e., the principal) and a profit amount (i.e., the interest component.

The Understandings are styled as “purchase” arrangements (a put option) and “sale” arrangements (a call option in the customer). They are not really purchases and sales. They are mechanisms to

effect repayment of outstanding principal amounts of the financing. The Customer will ultimately own the asset.

VAT on the asset sale. This is really a sale of the asset to the Customer

(with a loan financing styled as

a lease.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP22

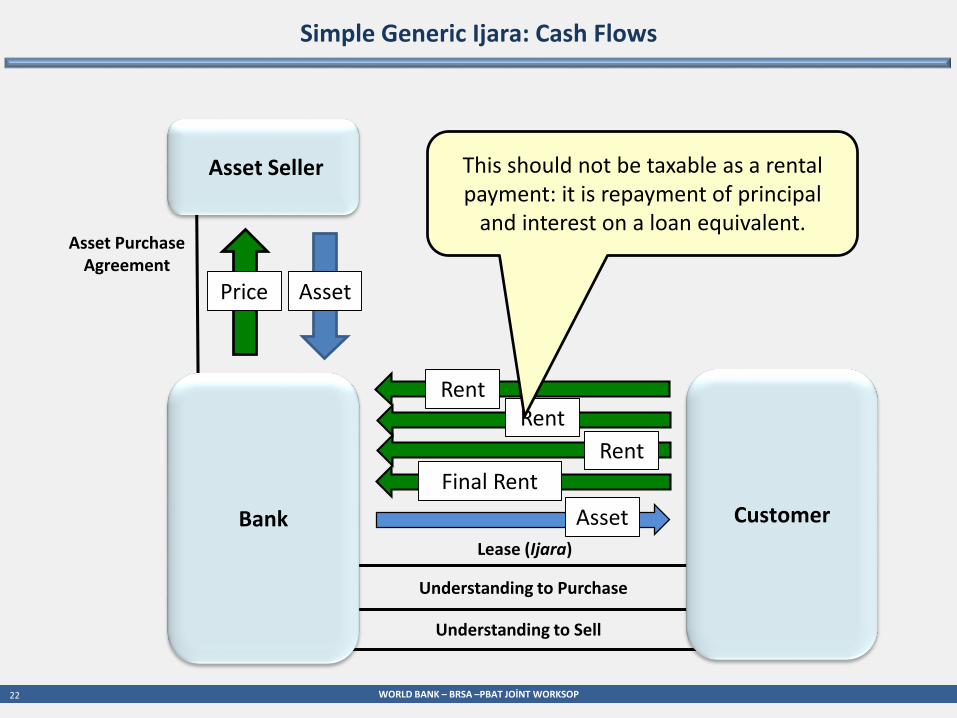

Asset Purchase Agreement

Simple Generic Ijara: Cash Flows

Understanding to Purchase

Lease (Ijara)

Understanding to Sell

Asset Seller

CustomerBank

Price Asset

RentRent

Rent

Final Rent

Asset

This should not be taxable as a rental payment: it is repayment of principal

and interest on a loan equivalent.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP2323 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Bifurcated Structures:Generic Ijara

WORLD BANK – BRSA –PBAT JOİNT WORKSOP24

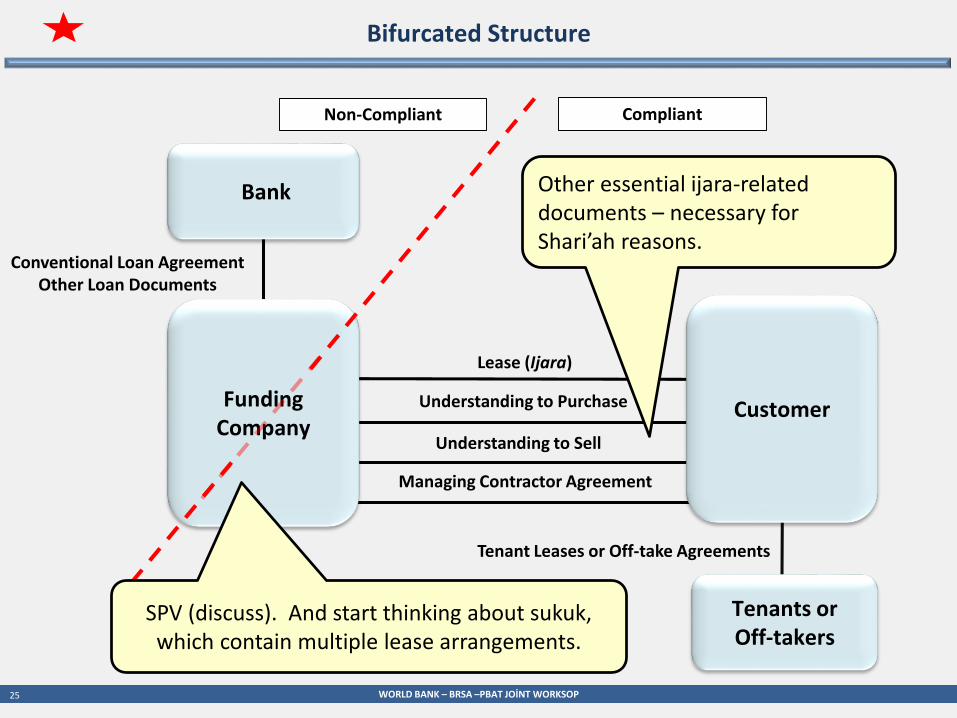

Bifurcated Structure: Most Jurisdictions

Lease (Ijara)

Bank

CustomerFunding Company

Tenants or Off-takers

Tenant Leases or Off-take Agreements

Non-Compliant Compliant

Conventional Loan AgreementOther Loan Documents

The Funding Company is usually owned by a third party as an “accommodation”. The third party has no other participation in

the transaction is paid a small fee to own the entity.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP25

Bifurcated Structure

Understanding to Purchase

Lease (Ijara)

Understanding to Sell

Managing Contractor Agreement

Bank

CustomerFunding Company

Tenants or Off-takers

Tenant Leases or Off-take Agreements

Non-Compliant Compliant

Conventional Loan AgreementOther Loan Documents

Other essential ijara-related documents – necessary for Shari’ah reasons.

SPV (discuss). And start thinking about sukuk, which contain multiple lease arrangements.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP26

Special Purpose Vehicles

SPVs are widely used in Shari’ah-compliant financings.

Often to hold the asset and allow the asset to be leased.

To limit the credit exposures of the transaction.

For bankruptcy remoteness: and here the issues pertaining to collateral security regimes arise (not so many issues in Turkey).

Is enforceability clear and predictable?

Are Shari’ah principles incorporated?

For sukuk issuances.

One of the main issues, around the world, is how easy or difficult it is to form and SPV. Difficulty in formation is an impediment to Islamic finance.

SPV formation in the United States as an example.

A related issue is whether and how the SPV is taxed. Consider the “check the box” regulations.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP27

Conversion of Bifurcated Structure to Shariʿah-Compliant Structure

Understanding to Purchase

Lease (Ijara)

Understanding to Sell

Managing Contractor Agreement

Bank

CustomerFunding Company

Tenants or Off-takers

Tenant Leases or Off-take Agreements

Shariʿah-Compliant Financing Documents

Additional stamp duty and VAT.

Additional tax considerations depend upon the exact type of Shariʿah-compliant financing that is used.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP28

Funds Infusion

Lease (Ijara)

Financing AgreementOther Financing Documents

Debt

InvestmentCustomerFunding

Company

Bank

Seller

Purchase Price

WORLD BANK – BRSA –PBAT JOİNT WORKSOP29

Lease (Ijara)

Lease (Ijara)

Financing AgreementOther Financing Documents

Tenants or Off-takers

The Funding Company, as the lessor, will lease the Project or asset to the Customer, as the lessee, pursuant to the Lease (Ijara). This is a Shariʿah-compliant lease. In the US, Basic Rent equals periodic debt service, precisely.

Debt Service

Rent

Rent or Payments

Loan PaymentsDividends

CustomerFunding Company

BankCustomer Retention

Tenant Leases orOff-take Agreements

WORLD BANK – BRSA –PBAT JOİNT WORKSOP30

Lease (Ijāra)

Tenant Leases orOff-take Agreements

Lease (Ijara)

Financing AgreementOther Financing Documents

Bank

Tenants of Off-takers

The Funding Company, as the lessor, will lease the Project or asset to the Customer, as the lessee, pursuant to the Lease (Ijara). This is a Shariʿah-compliant lease. In the US, Rent equals periodic debt service, precisely.

Rent

Rent or Payments

Loan PaymentsDividends

CustomerFunding Company

Debt Service

Retention

Is this a taxable entity?Double taxation issue.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP31

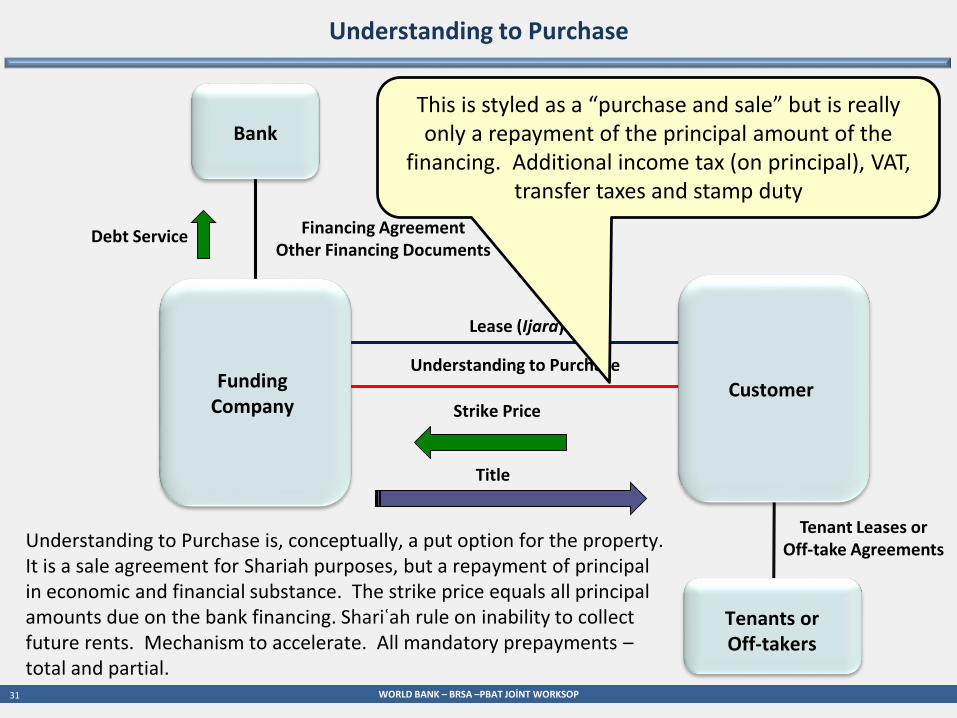

Understanding to Purchase

Understanding to Purchase

Lease (Ijara)

Financing AgreementOther Financing Documents

Tenants or Off-takers

Tenant Leases orOff-take AgreementsUnderstanding to Purchase is, conceptually, a put option for the property.

It is a sale agreement for Shariah purposes, but a repayment of principal in economic and financial substance. The strike price equals all principal amounts due on the bank financing. Shariʿah rule on inability to collect future rents. Mechanism to accelerate. All mandatory prepayments –total and partial.

Strike PriceCustomerFunding

Company

Bank

Title

Debt Service

This is styled as a “purchase and sale” but is really only a repayment of the principal amount of the

financing. Additional income tax (on principal), VAT, transfer taxes and stamp duty

WORLD BANK – BRSA –PBAT JOİNT WORKSOP32

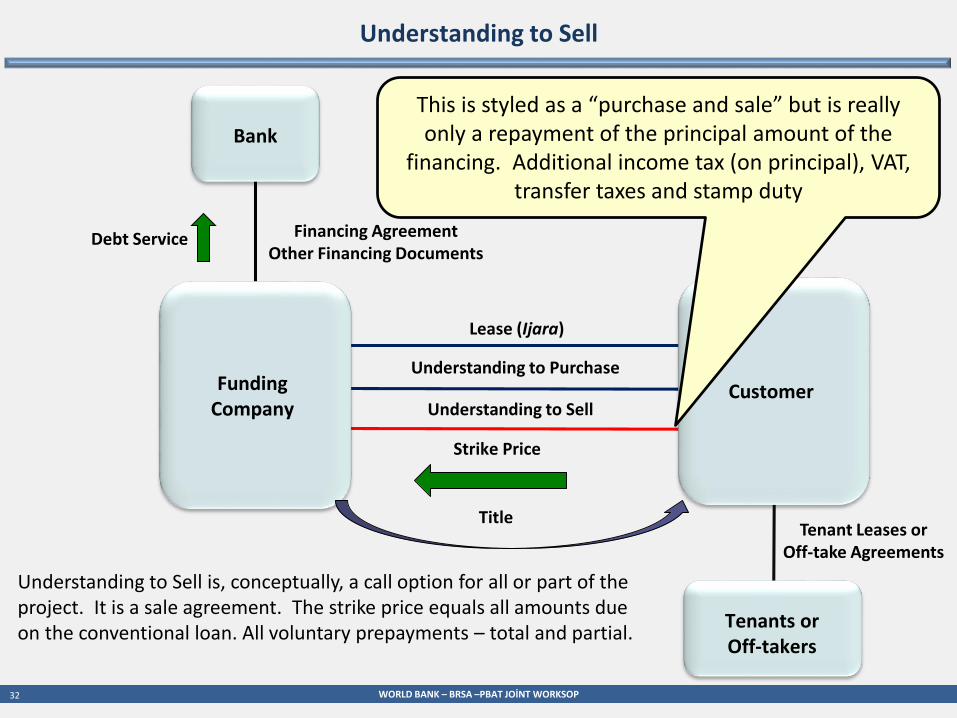

Understanding to Sell

Understanding to Purchase

Lease (Ijara)

Financing AgreementOther Financing Documents

Understanding to Sell

Tenants or Off-takers

Tenant Leases orOff-take Agreements

Understanding to Sell is, conceptually, a call option for all or part of the project. It is a sale agreement. The strike price equals all amounts due on the conventional loan. All voluntary prepayments – total and partial.

Strike Price

CustomerFunding Company

Bank

Title

Debt Service

This is styled as a “purchase and sale” but is really only a repayment of the principal amount of the

financing. Additional income tax (on principal), VAT, transfer taxes and stamp duty

WORLD BANK – BRSA –PBAT JOİNT WORKSOP3333 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Sukuk

WORLD BANK – BRSA –PBAT JOİNT WORKSOP343

4

Sukūk

This is what we are after.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP35

Pay

Pay

Pay

Pay

Pay

Pay

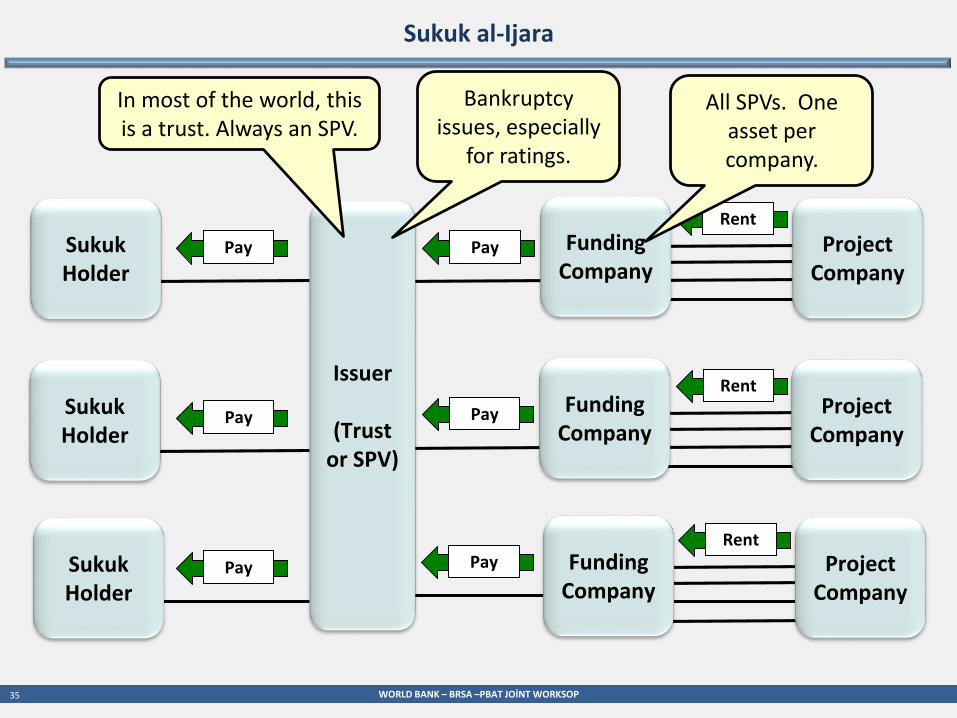

Sukuk al-Ijara

Funding Company

Issuer

(Trust or SPV)

Rent

Project Company

Funding Company

Project Company

Funding Company

Project Company

Sukuk Holder

Sukuk Holder

Sukuk Holder

Rent

Rent

In most of the world, this is a trust. Always an SPV.

Bankruptcy issues, especially

for ratings.

All SPVs. One asset per company.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP36

True Sale

Asset Originator

Sukuk HolderIssuer

Asset Transfer

Creditors of Asset Originator

No True Sale

WORLD BANK – BRSA –PBAT JOİNT WORKSOP37

True Sale

Asset Originator

Sukuk HolderIssuer

Asset Transfer

Creditors of Asset Originator

True Sale

WORLD BANK – BRSA –PBAT JOİNT WORKSOP38

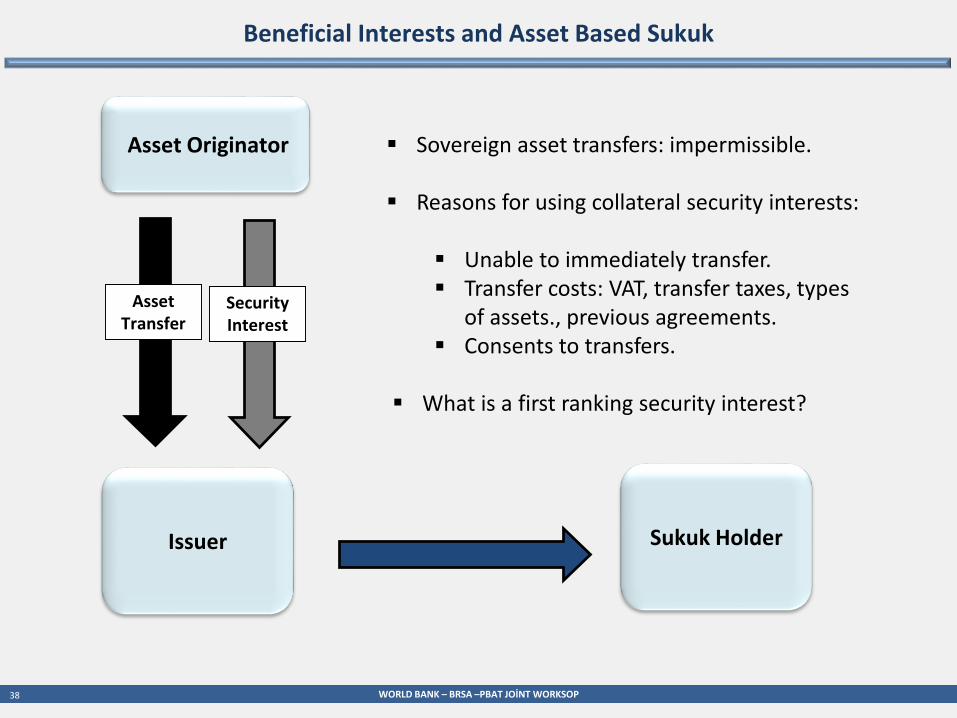

Beneficial Interests and Asset Based Sukuk

Sovereign asset transfers: impermissible.

Reasons for using collateral security interests:

Unable to immediately transfer. Transfer costs: VAT, transfer taxes, types

of assets., previous agreements. Consents to transfers.

What is a first ranking security interest?

Asset Originator

Sukuk HolderIssuer

Asset Transfer

Security Interest

WORLD BANK – BRSA –PBAT JOİNT WORKSOP3939 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Shari’ah Governance

WORLD BANK – BRSA –PBAT JOİNT WORKSOP40

Shari’ah Governance

First thought: Shari’ah Boards.

What Shariah boards? At level of each bank (market diversity)? At government level (Malaysia)? At a market participant association (some standardization, and then how much)? Combinations.

Qualifications of scholars? Fitness issues.

Authority and role within the organization and as a matter of law.

Liability of Shari’ah board members.

Conflicts of interest.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP41

Shari’ah Governance

Many other elements of Shari’ah governance that are often ignored (at least at inception).

Malaysia is a good example of a model of a well-developed Shari’ah governance system.

Shari’ah risk management and control function.

Shari’ah review function.

Shari’ah audit function: internal and external.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP4242 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

The Will to Participate

WORLD BANK – BRSA –PBAT JOİNT WORKSOP43

Political and Market Participant Will

A critical factor in implementing truly competitive Islamic banking and Islamic capital markets initiatives is the will and desire of the government and of the market participants.

An example: municipalities, which often have the assets and the capabilities.

An example: banks, which see the capital markets as competitors.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP4444 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

THANK YOU

WORLD BANK – BRSA –PBAT JOİNT WORKSOP4545 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Islamic Banking Models

WORLD BANK – BRSA –PBAT JOİNT WORKSOP46

Islamic Banking Models

Theoretical models for the structure of Islamic financial intermediation and banking:

wakala (agency) model

two-tier mudaraba (service-capital partnership) model.

The type of model is not necessarily determinative of how the arrangement should be taxed: it is important to understand what use the bank makes of the customer’s funds in each model.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP4747 WORLD BANK – BRSA – PBAT JOİNT WORKSHOP

Service-Capital (Mudaraba) Models

WORLD BANK – BRSA –PBAT JOİNT WORKSOP48

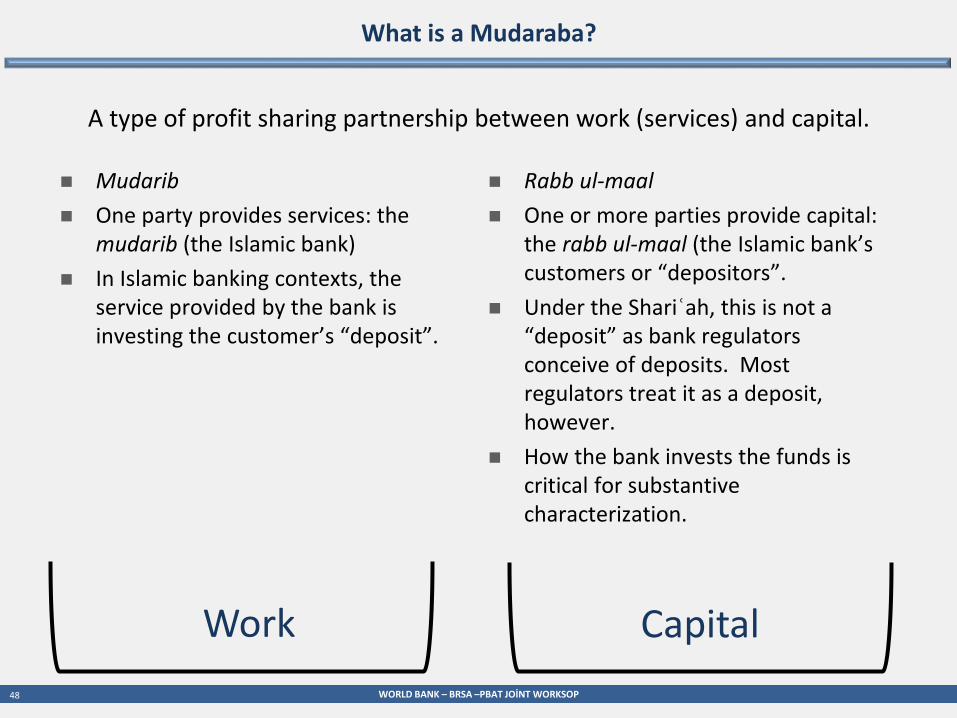

Mudarib

One party provides services: the mudarib (the Islamic bank)

In Islamic banking contexts, the service provided by the bank is investing the customer’s “deposit”.

Rabb ul-maal

One or more parties provide capital: the rabb ul-maal (the Islamic bank’s customers or “depositors”.

Under the Shariʿah, this is not a “deposit” as bank regulators conceive of deposits. Most regulators treat it as a deposit, however.

How the bank invests the funds is critical for substantive characterization.

A type of profit sharing partnership between work (services) and capital.

What is a Mudaraba?

Work Capital

WORLD BANK – BRSA –PBAT JOİNT WORKSOP49

Mudaraba – a type of partnership in which one partner contributes services and one partner (or group) of investors contributes cash

The service provider is the mudarib; in Islamic banking, this is the bank.

The cash investors are the rabb ul-maal; in Islamic banking, this is the bank’s customer.

Most bank regulators treat the customer’s contribution to the partnership as a “deposit” that must be insured.

The Shariʿah treats the customer’s contribution as a partnership contribution (much as a limited partner makes a contribution in a limited partnership arrangement).

What the Islamic bank does with the money – the type of investment – is the determinative factor, as a substantive matter.

Some investments are equivalent to “deposits” with deposit returns (e.g., vector murabaha investments); others are true profit sharing arrangements.

Mudaraba Elements: Definition

WORLD BANK – BRSA –PBAT JOİNT WORKSOP50

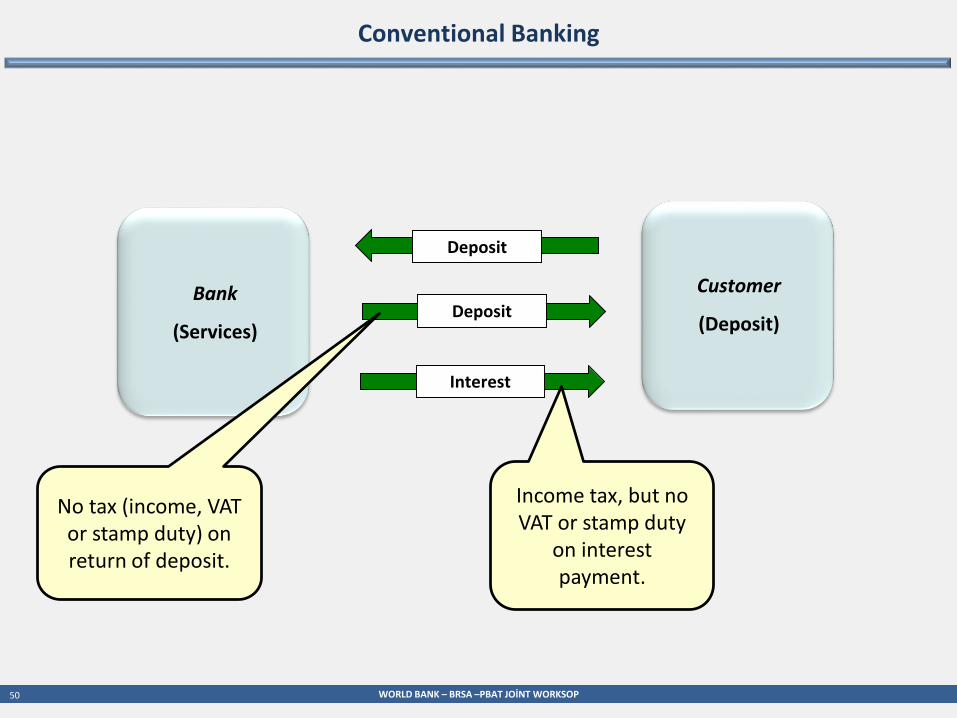

Conventional Banking

Deposit

Customer

(Deposit)

Bank

(Services)

Interest

Deposit

No tax (income, VAT or stamp duty) on return of deposit.

Income tax, but no VAT or stamp duty

on interest payment.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP51

Mudaraba Generally

Mudaraba Agreement

Capital

Rabb ul-Maal

(Capital)

Mudarib

(Services)

Mudaraba

Business Activities

Revenue

Profit

WORLD BANK – BRSA –PBAT JOİNT WORKSOP52

Banking Mudaraba

Mudaraba Agreement

Capital Customer

(“Deposits”)

Bank

(Services)

Banking Mudaraba

Business Activities

Revenue

Profit

Usually stamp duty.

Often stamp duty.’

Capital

Income tax.

Income tax.

Maybe tax.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP53

Banking Mudaraba

Mudaraba Agreement

Capital

Customer

(“Deposits”)

Bank

(Services)

Banking Mudaraba

Business Activities

Revenue

Profit

This “Revenue” stream can be either (a) true profit-and-loss sharing or (b) a vector murabaha to generate the equivalent of an interest rate return.

WORLD BANK – BRSA –PBAT JOİNT WORKSOP54

Mudaraba

Two-Tier Banking Mudaraba

Mudaraba

Profit

Investment Profit

Business Activities

Profits

Investments

Capital

Mudaraba Agreement

Bank(Services)

Rabb ul-Maal(Capital)

Customer

(“Deposits”)

Mudarib(Services)

Five possible taxes (four certain taxes) at Tier 1 – not shown. The second tier adds at least two more taxes.

Often stamp duty.’Income tax.

Capital