lcd-75-436 manufacturing technology--a changing challenge

TRANSCRIPT

REPORT TO T7HE CONGRESS qUN-TED STAJES

GENERAM ACCOUNTING OFFICE G

BY THE COMPTROD.JLEItENERALOF THE UNITED SUJPSM

Manufacturing TechnologyA Changing Challenge ToImproved Productivity

With new technology, the United States canincrease the productivity of industries thatproduce goods in small lots. Many foreignindustrial nations have ways of diffusing tech-nological advances throughout their manufac-turing bases. We can learn from these foreignefforts to enhance manufacturing produc-tivity.

The United States needs to make manufactur-ing productivity a national priority to remaininternationally competitive and to maintainstrong industries.

LCD-75-436 JUNE 3,1976

_-s

COMPTROLLER GENERAL OF THE UNITED STATESWASHINGTON. D.C. 20548

B-175132

To the President of the Senate and theSpeaker of the House of Representatives

This is GAO'sfstudy of how the United States comparesto other nations in applying modern manufacturing technologyby discrete parts, batch process manufacturers. These man-ufacturers constitute over 35 percent of the manufacturingfirms in the United States, and they manufacture most of theitems procured by the Federal Government.

This study of manufacturing technology was undertakenbecause to varying degrees, there are sufficient indicationsthat the private sector is having difficulty maintaining itsproductivity in dealing with rapid changes in manufacturingtechnology. Moreover, the Federal Government is the largestsingle purchaser of manufactured goods and if indeed tech-nology and productivity falter then the cost of these goodswill increase accordingly. GAO wanted to provide a documentwhich would encourage discussion and debate on the subject,recognizing that the issue is a very complex one and is in-terrelated with other problems, such as inflation, capitalformation, and international competitiveness.

We were also aware of the interest of several committeesof the Congress in the subjects of increased productivity,competitiveness of the United States in world markets, pricestability, and economic growth, and the role of the NationalCenter for Productivity and Quality of Working Life in re-solving these problems.

The report should be useful to the Congress, the execu-tive branch, and to the private manufacturing sector in iden-tifying policy and actions relating to national manufacturingproductivity, scientific research and development, and tech-nology diffusion.

Our review was made pursuant to the Budget and AccountingAct of 1921 (31 U.S.C. 53), and the Accounting and AuditingAct of 1950 (31 U.S.C. 67).

B-175132

We are sending copies of this report to the Director, 7Office of Management and Budget; the Secretary of Commerce;the Chairman, National Center for Productivity and Quality 967of Working Life; and other interested agencies.

Comptroller Generalof the United States

2

Contents

Page

DIGEST

CHAPTER

1 BACKGROUND 1

2 INTRODUCTION 6National Science Foundation study 7Denison's work 14

3 COMPUTER-INTEGRATED MANUFACTURING--ITSPOTENTIAL 19

A brief summary of types of manufac-turing processes 20

Computers and numerical control 25Computer-aided manufacturing 31Computer-aided design 35What computer-integratedmanufacturing accomplishes 35

Summary 39

4 COMPUTER-INTEGRATED MANUFACTURING--ITS PROBLEMS 40

Invention, innovation, and diffusion 41Problems of diffusion 43Diffusion of CIM 44

5 U.S. POSITION RELATIVE TO FOREIGN NATIONS 52Indicators of relative change in man-

ufacturing base 54Productivity .55GAO observations 69

6 COMPARISON OF NATIONAL INSTITUTIONSFOR IMPROVED PRODUCTIVITY 76

Productivity centers 77U.S. diffusion activities 83

7 MISCELLANEOUS MATTERS 86Marketing 86Antitrust 88Tax policy 90Monetary policy 91State and other productivity and pro-motional centers 91

Education for manufacturing 93

8 SUMMARY AND OBSERVATIONS 95Observations 95

CHAPTER Page

Current activities 98

Recommendations 101

9 REFERENCES 106

APPENDIX

I Survey of manufacturing establishmentsin 13 States 108

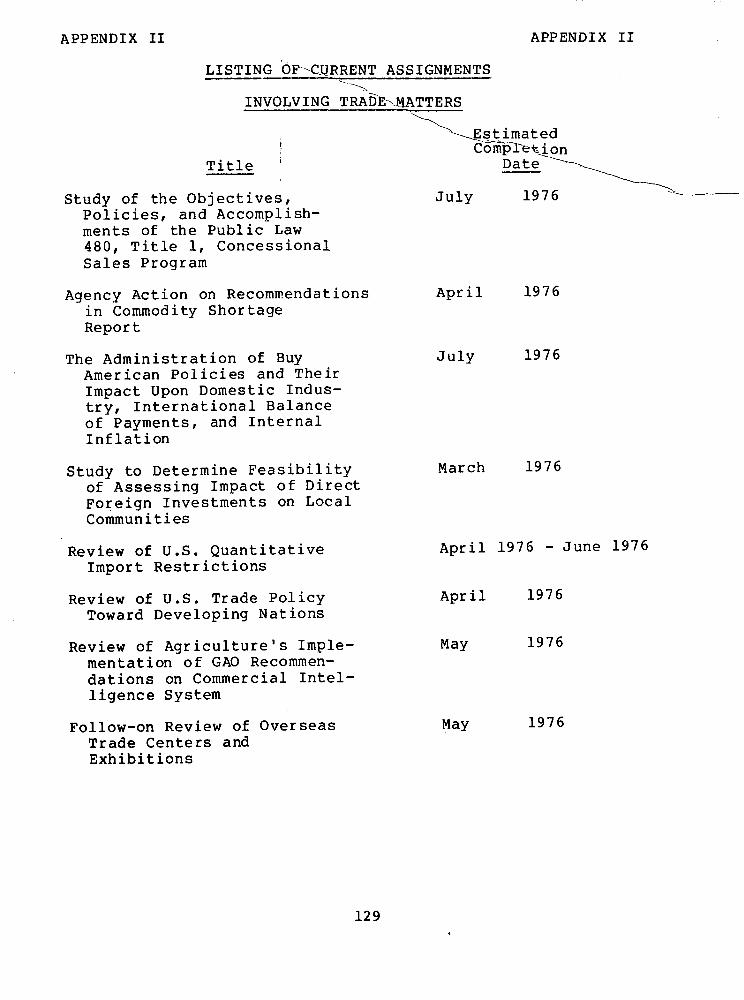

II Listing of General Accounting Office

reports issued since July 1, 1971,

on trade-promotion related matters 125

III Excerpts from "Automation OpportunitiesIn the Service Sector," report of the

Federal Council for Science and Technology,

Committee on Automation Opportunities inthe Service Areas 130

ABBREVIATIONS

APT automatically programed tool

ARC Automation Research CouncilBOM Bill of Materials

CAM-I Computer-Aided Manufacturing-International, Inc.

CIM computer-integrated manufacturingCMPM computer-managed parts manufacturing systems

CNC computer numerical controlDNC direct numerical controlDOD Department of Defense

ERDA Energy Research and Development AdministrationFRG Federal Republic of GermanyGAO General Accounting Office

GNP gross national productJPC Japan Productivity Center

MIT Massachusetts Institute of Technology

MITI Ministry of International Trade and Industry

NASA National Aeronautics and Space Administration

NBS National Bureau of Standards

NC numerical controlNSF National Science FoundationNTIS National Technical Information Service

OECD Organization for Economic C-ooperation andDevelopment

SBA Small Business Administration

REPORT TO THE CONGRESS MANUFACTURING TECHNOLOGY--BY THE COMPTROLLER GENERAL A CHANGING CHALLENGE

TO IMPROVED PRODUCTIVITY

DIGEST

THE EMERGING PROBLEM

The United States is the World's largestproducer of manufactured products and formany years generated most of its raw mate-rials, produced its own manufacturing toolsand consumed most of the products it manu-factured--historically, exporting less than7 percent of its gross national product.

But, the United States is running out of rawmaterials--oil is one--and must increasinglyimport them at higher costs to operate itsfactories. These increased imports must bepaid for by increased exports; and, the in-creased exports must come either from im-proved productivity or from reduced domesticconsumption.

If from the latter, the costs of the avail-able goods will substantially increase to theAmerican consumer and to Federal, State and lo-cal governments.

Meanwhile, the successes of foreign competi-tors in using sophisticated manufacturingtechnology to produce consumer goods are evi-dent.

-- Americans are buying a large quantity andvariety of quality foreign products.

-- Foreign markets that the United States hastraditionally enjoyed are diminishing.

--In 1971 the U.S. balance of trade turned un-favorable for the first time since 1893 andagain showed a deficit in 1972 and 1974.

A significant amount of these goods are madein small lots or batches by industries knownas discrete parts, batch process manufactur-ers. In the United States these manufactur-ers represent over 35 percent of the

Ter Shee. Upon removal, the reporti LCD-75-436cover date should be noted hereon.

manufacturing base and contribute 36 percentof manufacturing's share of the gross nationalproduct.

The technology involved in small batch manu-ufacturing has been undergoing profoundchanges because of the numerically controlledmachine tool (developed in the 1950s) and theincreased use of computers to control manufac-turing processes. Furthermore, foreign com-petitors seem to be surpassing us in usingthis new technology to improve their indus-trial productivity.

In the 30 years since the end of World War II,other industrialized nations have had ratesof improved industrial productivity consist-ently higher than those of the United States.

While a rapid productivity increase rate couldhave been expected for a while in some of theindustrialized nations due to rebuilding indus-trial bases, the effects of the war do not ac-count for the sustained productivity improve-ment rate for the extended 30 year period.Economists who have studied the matter gener-ally agree that productivity improvementsdue to reconstruction activities were com-pleted mostly in the 1950s.

Following World War II, the European countriesand Japan, largely at U.S. insistence estab-lished formal productivity centers that focusedon management and marketing techniques and prob-lems in the service sectors of the economies.

Additionally, and without U.S. encouragement,informal productivity centers were establishedin the areas of manufacturing, science andtechnology. These were joint cooperative ef-forts organized from the Government, labor,industry (including industrial associationsand institutions) and university communities.

The consistently increasing productivity ratesof these industrialized countries can be at-tributed, at least in part, to the productivitycenters.

ii

In the area of advanced manufacturing technol-ogy, the United States generally is using morethan other countries. But it is highly concen-trated in aerospace, electronics, and otherfirms producing defense-related products, andwithout added impetus it does not show promiseof diffusing to small- or medium-sized firms.

However, the general level of technical capa-bility seems about equal in all industrial na-tions.

Looking to the future, it appears that foreigncompetitiors have an advantage of being ableto exploit, develop, and diffuse manufacturingtechnology faster than the United States. Al-though this kind of international technologicalcompetition is healthy and stimulates eachcountry to the common goal of improving worldwide living standards, the U.S. needs to take apositive stance to improve its own diffusion ofmanufacturing technology so as to enhance pro-ductivity and remain competitive.

Normally, the Government would not be inter-ested in an issue of this magnitude unless:

--private industry was neglecting or generallyunaware of the issue,

-- actions being taken by private industry werenot in the best interests of our economy, or

--private industry was not advancing fastenough to sustain our socieconomic way oflife.

Although there are no outright indications ofneglect, a broad cross-section of U.S. manufac-turers generally do not know how advanced man-ufacturing technology affects them. And, thoseapplications of technology contemplated or underway do not seem to be progressing fast enough tosustain us. Consequently, GAO became interestedin the evaluation of manufacturing technologyand its impact on productivity.

GAO now believes that in order to remain in-ternationally competitive and to maintain astrong industrial base, actions must be initi-ated to make manufacturing productivity a na-tional priority.

111ITear Sheet

V (GAO recommends that as a top priority effortthe National Center for Productivity and Qual-

ity of Working Life develop a national policy

and appropriate means for achieving balanced

productivity growth in the industrial/manufac-

turing base. Further, GAO recommends that the

National Center, in carrying out this recom-

mendation, seek the cooperation and assistance

of the Department of Commerce and other appro-

priate agencies. In addition, GAO recommends

that the Department of Commerce strengthen its

efforts to support and develop productivity

enhancing technology related to manufacturing.

The combination of the existing expertise of

the National Center and the Department of Com-

merce in close coordination with other public

and private organizations, would facilitateearly initiatives with a minimum startup time.

Moreover the Department of Commerce could,

thereby, provide the much needed focal point to

coordinate all the disparate Government and

private work in developing, standardizing and

diffusing manufacturing technology. This is

discussed in more detail in chapter 8.

iv

CHAPTER 1

BACKGROUND

The Federal Government spends billions of dollars eachyear for U.S.-manufactured products. Inflation is constantlyraising the unit costs of the products at a time when thereare mounting pressures to limit Government spending. Ittherefore becomes increasingly important that manufacturerssupplying the U.S. Government use the most cost effectivemanufacturing methods in producing products.

We initiated a review of manufacturing technology ap-plied to meeting the Government's civil and national defenseneeds because of the GAO and Federal interest in

-- procuring these goods and services at the lowest prac-tical cost,

-- applying techniques to improve the productivity offederally operated industrial facilities,

-- furthering the objectives of the Congress and the ex-ecutive branch in establishing the National Commissionon Productivity and Work Quality, and more recentlythe National Center for Productivity and Quality ofWorking Life,

-- applying and using the National Science Foundationgrant program as it relates to manufacturing technol-ogy, and

-- providing a document which would encourage discussionand debate on the subject, recognizing that the issueis a very complex one and is related to other prob-lems, such as growth of capital formation and highinflation in plant and equipment costs.

We were also aware of the interest of several committeesof the Congress in the subject of increased productivity,competitiveness of the United States in world markets, pricestability, and economic growth.

Several matters surfaced early in the survey which per-suaded us to expand the project to a survey of manufacturingtechnology generally. First, there were over four milliondifferent items in the Federal supply system. Virtuallyeverything produced in the United States is procured, in oneform or another, by the Federal Government. There were over25,000 contractors producing items or services for the De-partment of Defense alone.

Second, a large number of items procured by the Govern-ment--for instance materials-handling equipment and Armytanks--are products of industries which produce in smalllots or batches. These are known as discrete parts, batchprocess manufacturers.

Third, there was a declining U.S. balance-of-tradeposition which in 1971 turned unfavorable for the first timesince 1893 and again showed a deficit balance in 1972 and1974. An important negative factor was the rate of increasein the imports of high-technology products which have con-sistently been among our major exports. Except for agricul-tural products, many imports and exports were products ofeither U.S. or foreign discrete parts, batch process manufac-turers--the same type which account for the manufacture of alarge proportion of the products procured by the Government.

Fourth, the U.S. rate of increase in productivity inmanufacturing was among the lowest in the world.

And fifth, we were told that the technology of manu-

facturing discrete products in small batches was undergoingprofound changes because of the development in the 1950sof the numerically controlled machine tool (see p. 26)and the burgeoning application of computers to the manu-facturing environment, including computer control andoperation of the machinery of manufacturing. There weresuggestions that our foreign competitors were moving aheadof the United States in applying the new technology to thislarge segment of manufacturing industries.

The Government's interest in issues of this type wouldalso be stimulated by indications that the private sectorwas: (1) neglecting or was generally unaware of the issue,(2) taking actions which were not in the best interests of

our economy, or (3) their initiatives were not moving fastenough to sustain our socioeconomic way of life.

To varying degrees there are sufficient indications

that the private sector is having difficulty in dealing withrapid changes in manufacturing technology which would war-rant the Government's interest. For example, although there

are no outright indications of neglect, there are clear in-dications that a broad cross-section of our manufacturingbase is generally unaware of the impact of advancing manu-facturing technology. Moreover, even though many actionsnow underway or contemplated by selected elements of ourmanufacturer base are in our national interests, their prog-ress may not be fast enough to insure sustaining and advanc-ing our socioeconomic way of life. Based on these observa-tions and coupled with our current state of economic growth

2

we concluded that a survey of U.S. and foreign manufacturinggenerally would satisfy our specific interests in manufac-turing (especially as it relates to Government procurements)and, at the same time provide some useful insights intoproblems of U.S. productivity, relative levels of manufac-turing technology and competition in foreign trade.

In making our study, we surveyed a sample of metal-working companies and held discussions with over 200 U.S.industrial, academic, governmental, and financial organiza-tions. We also visited a smaller number of similar organiza-tions in the United Kingdom, West Germany, France, Italy,Norway, Denmark, and Sweden. Although we did not visit Japan,we discussed the subject with representatives of the Washing-ton, D.C., office of the Japan Productivity Center andconferred with a number of knowledgeable individuals witha firsthand knowledge of manufacturing activities in Japan.

We also surveyed the literature on matters ofproductivity and technology and utilized previous GAO studiesinvolving technology and foreign trade. We did not attemptto study all of the literature in depth, nor do we feel wehave studied all of the literature.

The study of such a broad field involving such a widerange of disciplines, companies, countries, individuals,facts, assumptions, and possibilities for the future requiressubjective evaluations and appraisals by the study partici-pants. No one small group engaged in such a broad studycan lay claim to having considered all pertinent and avail-able information, opinions, and perceptions. Indeed oneof our primary conclusions is that the subject matter studiedis so important, broad, and dynamic as to merit continuingattention in the United States by some responsible, qualified,and properly staffed organization either in the public orthe private sectors or some combination thereof.

We believe our study has been sufficiently comprehensiveto identify some serious productivity problems in the UnitedStates, to provide information and create some controversy,and to suggest potential courses of action to policymakersin the executive and legislative branches--and in the privatesector, that are now engaged in the emerging national inter-est and debate on productivity in the United States.

Several cautions to the reader seem appropriate. Thematters discussed--economic or technical--concerning thisstudy are relevant, in general, only when construed withinthe context of a relatively long timespan, such as 10 to 20years. The computer-integrated manufacturing systems

3

discussed herein probably will not reach full developmentuntil 1985 or beyond in the country or countries providingthe most favorable environment for their development.Therefore, viewing the matters in terms of business or eco-nomic conditions at a particular point or for a brief periodcould yield distorted perspectives.

Although our study focuses primarily on discrete parts,batch-processing industries engaged in various forms ofmetal working--principally metal cutting--the principles,problems, and potential for improved growth throughcomputer-integrated manufacturing apply equally to otherareas of manufacturing, such as plastics, glass and metalforming. The opportunities for improved productivitythrough automation in the service sector of our economy arealso great. The Committee on Automation Opportunities inthe Service Areas of the Federal Council for Science andTechnology issued in June of 1975 the results of a 4-yearstudy of the opportunities for productivity improvement inthe service sector. 1/ The Committee's findings and recom-mendations are very similar to ours, and excerpts from thestudy are contained in appendix III.

Also the reader should be aware that our study does notdiscuss if computer-integrated manufacturing should bebrought about. The development and component applicationsof computer-integrated manufacturing are already takingplace. The question, therefore, is not whether but howquickly and effectively the development process will be com-pleted and which national entities will move most quicklyand effectively. It is primarily these questions to whichour study addresses itself.

Finally, although our study emphasizes the importanceof the emerging computer-integrated manufacturing technology,technology does not stand by itself. Investment capital,employee-management attitudes and relationships, institu-tional characteristics--public and private--monetary policy,raw material endowment,and other factors are all woven to-gether in intricate mosaics, which are different for allcountries. It is the interaction of all of these factorsthat make up a nation's productivity. To encompass all ofthe factors in a single report would be impracticable. Wediscuss or refer to many of these other factors to highlightmanufacturing technology and our problems in realizing thefull potential of the new manufacturing technology.

In developing this report, GAO was fortunate to havehad expert advice and assistance from a wide variety of ex-perts in government, the private sector, and academia in theU.S. and abroad.

4

In January of 1976, we had a one day conference ofexperts on various aspects of manufacturing from Government,industry, labor, and academia to review a draft of our re-port.

Overall we have received a panorama of viewpoints rang-ing from expressions that all is well with U.S. industry andno action is necessary, to the direst of concerns that theU.S. is already falling behind. On balance, however, theaffected government agencies and private organizations arein general agreement with our findings.

We gratefully acknowledge the assistance of these peo-ple and their contributions to our work.

Nevertheless, the observations, judgments, and sugges-tions in the report are those of GAO and do not necessarilyreflect the views of any of those who so generously assistedin the study.

5

CHAPTER 2

INTRODUCTION

To assess the importance of manufacturing technology,the GAO staff surveyed programs in the United States and

selected foreign countries concerned with advancing the

state of the art of manufacturing technology, particularly

the use of computers in the manufacturing environment.

In our analysis, we considered the growing interdepend-

ence of world economies and the fact that such a reviewcould not be limited only to factors internal to the United

States. All industrial nations compete for increasingly

scarce resources of manufacturing as well as for markets

for their end products, and high rates of productivity arenecessary to minimize manufacturing costs and maximize a

countryds competitive position. Importantly, the rates ofproductivity growth in the United States since World War IIhave been the lowest of 11 major industrial nations.

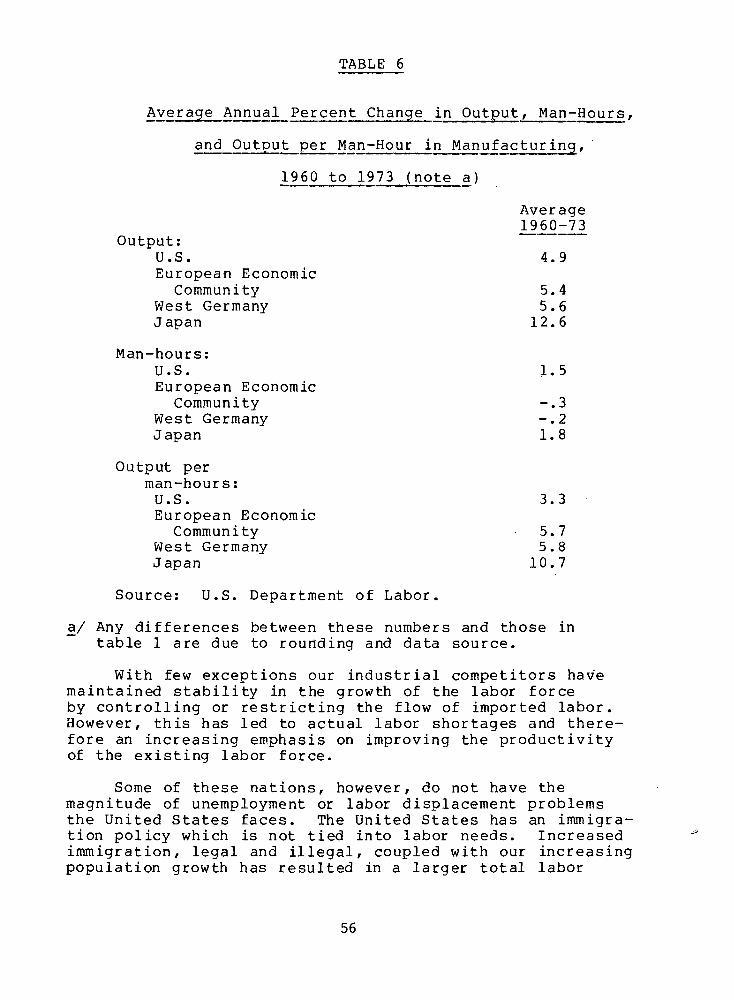

Table 1 shows how the annual rates of manufacturingproductivity growth have increased at a dramatically higher

rate in other industrial nations since 1960.

TABLE 1

Productivity Gains

Average Annual Increase in Output Per Man-Hour

In Manufacturing, 1960-1973

Japan . . . . . . . . . . . . 10.5%Netherlands. . . . . . . . . . . .... 7.5Sweden . . . . . . . . . . . . . . . . . . 7.1Belgium. 6.5

Italy. . . . . . . . . . . . . . ..... 6.4France . . . . . . . . . . . . . .... 6.0

West Germany . . . . . . . . . . . . . 5.8Switzerland. . . . . . . . . . . . ... 5.3Canada . . . . . . . . . . . . . . . ... 4.3

United Kingdom . . . . . . . . . . . ... 4.0United States .... . . . 3.4

Source: U.S. Department of Labor

6

There is extensive literature on economic growth inthe United States centering on broad analyses of applica-tions of land, labor, and capital. And there have been gen-eral discussions of factors contributing to productivitysuch as education and technological advances. There havebeen fewer studies addressing the quantitative importanceof each single factor or analyzing the possible underlyingreasons for the low rate of U.S. productivity growth in re-lation to other countries.

In the following paragraphs, we draw heavily on a studyreport of the National Science Foundation and the work ofEdward F. Denison of the Brookings Institution because (1)they are authorative works, (2) they raise important ques-tions concerning the need or effectiveness of overt effortsto improve national productivity, (3) they bear strongly onsome of the points we make, and (4) they form a prior broadstudy basis for some of the more specific observations wehave made regarding the more specific discrete parts, batchprocess industries and the emerging technology of computer-integrated manufacturing.

NATIONAL SCIENCE FOUNDATION STUDY

The National Science Foundation study examines publicpolicy questions concerning productivity growth. Part ofthe examination was directed to relative rates of growth ofthe United States and other industrialized countries.

In their study Piekarz and Thomas 2/ began their com-parison of the United States productivity performance withthat of foreign countries by making three observations.

First observation

U.S. output for each employed person appears to be, andprobably has been throughout this century, higher than thatof any other nation.

Chart 1 shows that the U.S. ratio of industrial outputfor each person employed in industry has exceeded the ratiosfor the United Kingdom, Germany, and Sweden from 1860 to1970.

Table 2 shows that the U.S. gross domestic product foreach person employed ranked first among the major industrialnations in 1971 as well as in 1961 and 1951. However, asimple comparison of the rate of growth between 1961 and1971 reveals that it substantially lagged behind the othernations.

7

CHART 1

H o t

C4J 4 t

0 00

X2 2 e· o -4 1

.= j IO U ) 0 U ,

0 --

o o .c

- 0, . ..I O JJn r 4-4

o mu

co co ,., _ _-' ' "to o>

0 *

o 0

0~ ~ ~ ~ ~ ~~~c5' -s ~~~as

0 r1

c ,.o .o o1Q

fi jl ~ H dP

4; o ao aN m i Le CD N -V r- z N r. ~4 0 O0 O CS t

'~1

1-

o--

U) ro'~U I m ~CzaC m CIi

-I

3 C~ 0 a L1 0

U' ) *

CC I V a I o 1 C. )D

a)oL(O~~~~) E n,

arJ· ·Z Z Z · -o - c O o

4 0 'U -. .--I 4

CD' I -o0" . 4 14-4 tcl C 00 v> M a

4) 0 1 a LtEit 0I o _ E-4 s C C u .

o , _ h ': 'u c a0I -

ti) CDU ) (U ~ 4 - 4 . J-4

O * @ o04 U) 11' CD o-0 4i-4 0 c4 a, 0 O c 0 u r

U @ .0-- . . .1>w ()Clw C -a )-( Z i\ rz )O _ 4

E- )OQI O 0 O .z O

_ C C rOI C-

oI .t _0 -4o a

Qx L ( H_ Q O OJ , 4 1- aU h

E.) - .- 4) ) C D - a nU)

a a) 0 a-4 . . z v O O

r4 4.))~ ~ * C H oV

0 4J -o 0

O4I . *a C a m aC31 , a Ul Cao a

o C 04-)0 U):1 0_ W ' U) 4

aw400 U . .C . ft4 *0

a .E ~ La- ( a V 1o

U) - z:--.4 a 2

U 0 0 4S C 0

aU) r a, m 4n .l oa _ a E:~ 614) ) 4) 2

UEl 01 tO 9sC OCDP H f

Second observation

The annual rate of U.S. productivity growth, averagedover the past century, seems to have approximated the expe-rience of other industrial nations.

Piekarz and Thomas use table 3 to show that the averageannual rate of growth of GNP per capita of the United Statesover the period 1870 to 1965 compares favorably with most

other industrial nations. The observation is also supportedby chart 1 and an analysis by Kuznets 3/ of the average an-

nual rate of change of national output per unit of labor in-put, and output per unit of labor plus capital input of se-lected countries.

Third observation

Since the post-World War II reconstruction, U.S. pro-ductivity growth has compared less favorably with that ofother countries than it did up to that point.

Piekarz and Thomas state that:

"Among the other industrial nations for the years1955 through 1968, average annual growth of outputper employed person in the economy as a whole, theindustrial sector, and service activities exceededthe U.S. rate by about 50 percent. Only in agri-culture has the U.S. experience been comparable.This performance for most of the other industrialcountries represents an acceleration from theirprevious productivity growth."

Table 4 shows how the United States compares to otherwestern industrialized nations in the rates of growth from1955 to 1968 for the total economy and the agriculture,industry and service sectors.

Piekarz and Thomas found that evidence is lacking todetermine whether the seemingly higher rate of productivitygrowth of other countries as compared to the United Statesis permanent. They found evidence in Denison's work 4/ andothers, as we did, that foreign countries have, for example,a higher rate of investment in production plant and equip-ment. However, they note that the United States comparesfavorably in upgrading labor skills and technology develop-ment.

But they conclude that:

"There is no way to determine whether duringthe next decade or two the gap in overall

10

dP C i O 1- CI O ,UH

..e40C 4J 'E

0 0 U r CY 4 r

3 O- c 4l a M- (a (a O -I -- 4iw o w S C ( L o ro

C' O C Ca ~ co a) N o ) 1- 3 (a U 3 4) c u 4J) .c

4-4 OD O I Q 4-i w O .- i .4 -i :

'0 0J

Oi U1 Q 0 0 0 3 3 C CS- o loa U OOw ro 4

p:A; ~- I-I V '0 C) 0 C)

'0 0 >E -' s-s

E Ur r~l) Co C:

Lit >I >1

:3 Q) co a)aw (L) 4J 0

m : C rT4

Eq O~Q~Q~l ov r~CHr

cr 3 C~~1

TABLE 4

Average Annual Growth of Output Per Employed Person for

13 Industrial Countries

1955 to 1968

Annual Rate of GrowthTotaleconomy Agriculture Industry Services

United States 2.5% 5.4% 2.9% 1.7%

Other major countries(unweighted average) 4.0 6.1 4.6 2.2

Canada 1.9 4.8 3.8 -0.1

France a/ 5.1 6.1 5.3 3.4

Germany a/ 4.4 6.1 5.0 2.5

Italy 6.0 7.8 5.8 3.7

United Kingdom 2.4 5.8 2.9 1.4

Other European countries(unweighted average) 3.9 4.8 4.2 2.6

Austria 4.5 5.1 4.4 3.1

Belgium 3.5 5.8 4.4 2.3

Denmark a/ 3.7 4.3 3.0 3.0

Finland a/ 3.9 4.6 4.1 1.5

Ireland a/ 3.3 3.3 3.4 2.2

Netherlands 4.0 6.2 4.8 2.8

Norway 4.1 2.5 3.9 3.4

Sweden a/ 4.1 6.5 5.6 2.3

All countries (except U.S.)(unweighted average) 3.9 5.3 4.3 2.4

Source: Organization for Economic Cooperation and Development., TheGrowth of Output 1960-1980, Retrospect, Prospect and Prob-lems of Policy, December 1970, p. 35.

a/Covers a shorter time period.

12

technological capabilities between the UnitedStates and the more advanced of the other indus-trialized nations will contract, widen, or remainabout the same."

Our studies do not yield any more conclusive resultsconcerning relative, future national growth rates than thoseof Piekarz and Thomas. However, table 4 shows that only inagriculture does the United States compare favorably ingrowth rates with other nations. When combined with ourother findings, this forms a basis for postulating aboutthe future of the discrete parts, batch-processing segmentof manufacturing industry. In the United States only agri-culture has well-defined national programs and an institu-tional structure for technology enhancement, diffusion, fi-nancing, marketing and productivity improvement.* In theservice sector similar structures and programs may be devel-oping.** In the industrial sector there are a number ofGovernment programs directed to specific areas of manufac-turing, but there is no cohesive national program.

In July 1975 the Joint Economic Committee, Subcommitteeon Economic Growth, held hearings on the lack of a nationaltechnology policy and its impact on the economy. In announc-ing the hearings, Senator Lloyd Bentsen said:

"* * * as of today, the United States has no na-tional policy for encouraging the type of techno-logical innovation that is needed to maintain ahealthy, growing economy. * * * no new system hasbeen developed or adapted to meet the new set ofemerging priorities: economic growth, environmen-tal soundness, export competitiveness and socialwelfare."

*In the broad sense, the activities of the U.S. Departmentof Agriculture, the State Agriculture departments, and theagricultural colleges constitute U.S. "productivity cen-ters" for agriculture.

**For example, the health care research and delivery work ofthe Department of Health, Education, and Welfare which isstrongly funded and the work of the Government's Joint Finan-cial Management Improvement Program which measures productiv-ity in the Federal Government sector. See also the resultsof a study of productivity improvement opportunities in theservice sector by the Federal Council for Science and Tech-nology 1/ and the work of the National Commission on Produc-tivity and the Quality of Work Life.

13

By contrast, the foreign countries we studied havewell-developed national programs for industrial developmentand, through their productivity centers, a structure forservice sector productivity improvement. The establishmentof national structures--formal and informal--for productivityimprovement in foreign countries took place from late in the1940s to early in the 1950s.

This was followed by sustained improvements in produc-tivity growth rates. Thus, there is a presumptive cause-effect relationship between the creation and maintenance ofstructured national productivity efforts and sustained pro-ductivity growth in the foreign countries. (A more detaileddiscussion of foreign productivity centers may be found inchapter 6.) This, compared with sustained high rates ofproductivity improvements in American agriculture--the onlysector in the United States with a fully developed nationalproductivity effort--suggests that formal national productiv-ity programs can influence the rate of growth of nationalproductivity.

DENISON'S WORK

Denison has pioneered in identifying the determinantsof changes in output and measuring of changes in them, and,

as a means of understanding economic growth, he has estimatedthe effect on output of changes in each. In his earlierwork 5/ Denison identified 31 change determinants. He findsthat changes in the following categories were chiefly respon-sible for long-term growth. 6/ The categories are (1) thenumber of employed persons and their demographic composition,(2) working hours, including the proportion of part-timeworkers, (3) the education of employed persons, (4) the sizeof the capital stock, (5) the state of knowledge, (6) theproportion of labor allocated to inefficient uses, (7) thesize of markets, and (8) the strength and pattern of short-term demand pressures. Advances in knowledge were the big-gest single source of growth, and lengthier education of thelabor force also appeared as a major source of growth. (Ourstudy focuses primarily on advances in knowledge, but we didsome survey work on education. (See ch. 7.)

In Denison's work 6/, advances in knowledge includetechnological knowledge; i.e., knowledge concerning thephysical properties of things and how to make, combine, oruse them in a physical sense. It also includes managerialknowledge; i.e., knowledge of business organization and ofmanagement techniques construed in the broadest sense. Ad-vances in knowledge comprise knowledge originating in theUnited States and abroad and knowledge obtained in any way:by organized research, by individual research workers andinventors, and by simple observation and experience.

14

Denison goes so far as to state 4/ that in the verylong run changes in the state of the arts (i.e., advanceof knowledge) and gains from economies of scale are thefundamental sources of growth in output per unit of input.

In this report we recognize the high quality ofAmerican managerial knowledge by observing that foreignproductivity centers have had missions of acquiring anddisseminating American managerial know-how and in compensat-ing for the lack, in their own countries, of well-developedschools of business and of organizations such as the Ameri-can Management Association. (See ch. 6.) Denison makes thesame point and concludes, along with many others, thatAmerican management technology is the best developed of theindustrialized nations.

Our study, therefore, concentrated primarily on techno-logical knowledge because of its importance to nationalgrowth and because of the emerging new technology ofcomputer-integrated manufacturing, which can impact on sucha large sector of American manufacturing.

Denison also makes the point 4/ that any scientificdiscovery, theory, or knowledge of any new materials, ma-chines, techniques, procedures, and practices that ariseanywhere in the world quickly spreads to all industrializedcountries. By accelerating its own contribution to advancesof knowledge, one industrialized country cannot expect togain more than a temporary advantage over the others withrespect to knowledge available for use.

The experts with whom we discussed this matter in theUnited States and abroad agreed that knowledge can spreadquickly among countries.

There is an important difference, however, in the ac-quisition of technological information by the United Statesand other industrialized countries. One of the major prob-lems we encountered in attempting to assess the level ofdevelopment of computer-integrated manufacturing in foreigncountries was the virtual dearth of information in theUnited States on foreign developments. Foreign publica-tions and research works on manufacturing technology werenot routinely scanned, translated, or published in theUnited States. Only a relative handful of private industryprofessionals routinely visited foreign countries for first-hand appraisals of foreign technology. (By this we meanmanufacturing generally. We found many individual Americancompanies which were well aware of the manufacturing proc-esses used by foreign competitors in the same product line.)We could find only a few academicians who had a firsthand

15

knowledge of foreign developments, and, while we found someFederal Government officials who had firsthand knowledge ofspecialty areas of foreign technology and some who had hear-say knowledge of foreign developments, we found few whocould speak authoritatively or out of personal knowledge onforeign technological developments in manufacturing technol-ogy in general.

By contrast, in all of the foreign countries we stud-ied, the industrial, academic, and Government communitieshad well-structured practices for keeping up with develop-ments in all foreign countries including particularly theUnited States and had mechanisms for diffusing this knowl-edge. (We did not attempt to evaluate the effectiveness ofthe diffusion mechanisms.)

Denison did not address the different attitudes andmechanisms in various countries for acquiring and diffusinginformation on foreign technological developments, and hetends to minimize the importance to relative economic growthamong countries of attempts by one country to accelerate itsown contributions to advances of knowledge. However, thedifferences we have perceived in countries' capacities orsystems to acquire and apply the best in-world technology(as well as to expedite the diffusion of the technology tothe industrial base) could well be one of the important fac-tors contributing to the differing rates of productivity im-provement in the industrial sectors of foreign governments.

A perplexing and different problem in any study of rel-ative productivity or economic growth is the length of timeit takes to spread or diffuse the first successful applica-tion of a new technology throughout the industrial base.(We discuss this problem of diffusion in greater detail inch. 4.) Not surprisingly, therefore, Denison also had thisproblem in his analysis of-why growth rates differ in var-ious countries.

Denison characterizes the difference between the bestpractice (in the case we are discussing here, this would bemanufacturing practice) possible with the knowledge avail-able at any given time and the average practice actually inuse as the lag. 3/ Thus he states that one may distinguishin principle between the contribution to growth of advancesof knowledge and the contribution that may be made by achange in the lag of average practice behind the best known.He states:

"This is an essential distinction * * * anda common one, but it is difficult to give it pre-cision." 4/

16

Denison has found no way to isolate the various reasons thataverage practice is below the best or that the margin ofdifference changes.

He states that there is a possibility that changes inthe lag may differ importantly from country to country andthat the average level of technique in Europe is generallyconsidered to be below and behind that in the United States,particularly in the techniques of management and the organi-zation of business as distinct from more narrowly definedtechnology. He observes therefore that there appears to beopportunity for the European countries to add substantialincrements to their growth rates by imitating and adoptingAmerican practices. He summarizes the organizational andstudy efforts of foreign productivity centers to apply thebest of U.S. practice and states:

"Under these conditions, a finding that theEuropean countries have secured a substantial in-crement to growth by narrowing the gap betweenEuropean and American practices would not be asurprise."

Denison's own calculations do not show that effortsat narrowing the gap explain the considerable differencesbetween the rates of productivity growth in the UnitedStates and foreign countries, but he states that this lackof evidence does not prove conclusively that improvedEuropean practices were not an important source of differ-ence between the growth rates of the United States and theEuropean countries studied.

Keeping in mind that Denison's studies were directed tothe total national economies, our studies would not serve toalter Denison's analyses.

However, with regard to specific sectors of variouseconomies, Denison's results drawn from a broad analysiswould not necessarily apply. As pointed out above, althoughoverall productivity is lower abroad than in the UnitedStates (see chart 1 and table 2), in all countries, expertswith whom we discussed the matter, agree that state of theart or best practice in discrete parts, batch process manu-facturing is about equal (although the level of average prac-tice in each of various countries is different).

When one evaluates the level of nationally supportedeffort being applied by the differing nations to enhance anddiffuse computer-integrated manufacturing, particularly con-sidering the successful results of their past effort, in re-lation to a virtual lack of a directed U.S. national effort,

17

one cannot help but be concerned about the relative rate ofprogress of the United States over the next 10 to 20 years.

In other words, as we will point out, two importanttechnological advances, the computer and the numericallycontrolled machine tool, were brought to their present lev-els of development with major financial support from theFederal Government. Other countries have adopted and en-hanced this technology and have large and well-establishednational programs for further developments. Since thesepast developments are the result of successful Federal ef-forts and since there is now no important continuingdirected/coordinated Federal effort or other cohesive na-tional effort, there is ample support for concern of thefuture impact of foreign efforts on U.S. trade balances.There is also concern that American products procured by theGovernment are not being produced using the most efficientmanufacturing methods.

To obtain better information on the use of advancedmanufactory methods within our industrial sector, we ran-domly surveyed some 200 U.S. manufactures to determine -theiruse of numerically controlled machine tools and computers.The result of this survey clearly supports our concern that,for a large body of American industry, the use of these ad-vanced methods is almost nonexistent. (See app. I.)

18

CHAPTER 3

COMPUTER-INTEGRATED MANUFACTURING--

ITS POTENTIAL

Peter Drucker said that three main areas in a typicalmanufacturing business account for three-quarters of thecapital invested. 7/ These are (1) machinery and equipment,(2) inventories of materials, supplies, and finished goods,and (3) receivables. Yet he says that despite its importanceand payoff, not many business managers pay much attention tothe productivity of capital. One reason, he says, and"perhaps the single most important one, is that managers,as a rule, get little information on the productivity ofcapital in their business."

Our work indicates that the emerging technology ofcomputer-integrated manufacturing (CIM) will not only pro-vide managers with better information on the use of capitalbut also improve the use (and therefore the productivity)of capital. Dozens of machine tools can now be simultane-ously operated and controlled by a single, hierarchal com-puter system known as "direct numerical control" (DNC).Machine use is increased and work-in-process inventory canbe reduced. The computer can not only send instructions tothe machine tools but it can automatically receive back in-formation and provide managers with the operational resultsof its instructions and the status of work in process.The computer aids designers in making better designs inless time than manual methods (in some cases modern designers'work cannot practicably be accomplished by manual methods)and frees the designer of laborious manual tasks, thus givinghim more time to use his creative skills. Computers can beused to perform production planning and control tasks; todirect work pieces from one machine to another; to test theperformance and inspect the quality of finished work; andto direct and control materials handling, storage, and dis-tribution systems. Computers are also used to program andcontrol plant maintenance and to plan factory layouts andmachine locations in factories.

Dr. Joseph Harrington, an authority on manufacturingand author of a pioneer work on applying of computersto manufacturing, has characterized this expanding appli-cation of computers to the manufacturing environment asfollows:

19

"It now seems apparent that things are about tochange--not incrementally, but radically. Frac-tionated management skills are being reintegratedand the new managers with their broader perspec-tives are directly controlling versatile machinescapable of manufacturing diversified and customizedproducts. The total manufacturing effort is beingreintegrated into a responsive directable entity.It is a giant step and a step in a new direction.

"This radical change in direction is a resultof the coinciding of many small advances in thestate-of-the-art. Taken individually, each advanceis an incremental improvement in one field. Takencollectively, when the fields are contiguous, theresult is more than just the sum of the parts. Allthe tumblers in the lock are falling into place;the door is swinging open. It is one of these raremoments in time when all of a compatible and con-nected set of conditions has been achieved."8/

We have observed some of the above functions being per-formed by computers in some plants. Some of the more so-phisticated and highly capitalized firms are using computersfor many of these functions. We found no one firm using allof them. And some firms, particularly small and mediumsized firms, who could benefit from these are using none ofthem.

A BRIEF SUMMARY OF TYPES OFMANUFACTURING PROCESSES

For our study it is convenient to divide manufacturinginto three broad categories: (1) continuous process, (2)high volume or mass production of discrete parts, and (3) lowvolume or batch process of discrete parts.

Continuous process manufacturers turn out a flow of un-distinguishable goods in "continuous activity in which thenature of the material is changed." 8/ These include man-ufactures such as oil refining, brewing, paper, and steel.These industries are highly automated through use of comput-erization and/or electromechanical devices.

The discrete parts manufacturing industries "change theshape of materials to produce discrete components that areassembled into functional end products."8/ These includemanufactures such as lawn mowers, hand tools, appliances,automobiles, or their components. Where standardized dis-crete parts or products (e.g., brake drums, engine blocks,axles) are produced in high volume (e.g., 500 to 20,000) in

20

a single production order, mass production techniques canbe economically used. High volume is required because themechanization is expensive and relatively inflexible. Theautomotive "transfer line" (see fig. 1) is a typical example.It is set up to process a particular type of product in highvolume over an extended period of time. To produce a new ordifferent product using transfer lines requires a closedownof the line and its redesign or reconfiguration before produc-tion on the new product line can be commenced. Although theremay be differences in detail from country to country, Americanmass production industries in general are considered to beamong the most advanced in the world.

In contrast to mass production is batch production.(See fig. 2.) This method of production is required whenseveral discrete products are manufactured but the volume ofany one product is relatively low, and there is little prod-uct standardization. About 75 percent of all metalworkingparts are produced in this manner. Consequently a greatdeal of flexibility is required, and it is necessary forbatch production plants to use a wide range of general pur-pose machines adaptable for making a wide variety of prod-ucts. (See fig. 3.) This production method, although re-quiring a smaller initial capital investment than mass pro-duction methods, results in a much higher cost for eachproduct. As shown later, modern technology can change this.

There is also general agreement that this area of man-ufacturing is undergoing profound changes and offers thegreatest opportunity for productivity improvements in thefuture. Each of the industrialized nations is pursuing itsown programs to exploit and enhance this technology.

The manufacturing sequence

Manufacturing may be defined as the process of conceiv-ing a product, designing it, and then through applying man-power, energy, materials, and technology, translating thedesign into a saleable item.

In this process the product is first designed on aseries of drawings by skilled design engineers and draftsmen.The final detailed drawings become the basis for planningthe methods to be used to produce the item, such as the typeof equipment needed, machining sequences, required materials,etc. These elements are brought together on the shop floorwhere the skilled craftsman (e.g., machinists) applies histrade to maximize production quality and quantities whileminimizing the consumption of energy and raw materials. Be-fore the development of the computer these functions wereperformed manually, and the quality and efficiency of

21

0

kk~~~~~~~~~~~~~~~~~~~~~~~-

'1~i ~~~~z

~,,,'',v,,,,, ,,~, . ~"~. ~ ;.

-. '"*;"-

I ,r .

lk ' ~~,, ~.. ~.

1Ž; 2*1~ 1.:I,,Ls~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~L.~ii.. ~I ,. ' '¥~'." ~ I ?r~~. k\" '"' l· k , ; ..; :,: .. = !~ It 0

· ~~~~~~,· a~~~~~~UI" I x

ow~~~~~~~~~~~~

I '~~~~~~~~~~~~~~~~~~~s~~~~~~~~~~~'

i: ,~~~~~~~~~~~~~~~~~· . ,,,,iZ

0C~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~,:

. ~ ~ ~ ~ ~ ~ ~ ',; I,,, .. *"~..;*. ii:" P

Z

f", 'A L· · ,~,m:: , , ~,u, ~;,22,

1, i:"7 r· ;i~~~~, · ~ ~ ~~~' "i~;," ": " "

iu~~~~~~~~. 'i. ;i

r.~~~~~~ *nijb?~~~~~~~~~~~i:.~~" "~"' :, ",

i, .. ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~. i::;:l

· · · i r~ *; · · r .. 1 · * · ii · " 0LL

-II "'~' """"'~~~~~~~~~~""" """'~~~~~"~'* ?': ~ ~ C

~~5)i I i I~ ~:~~~~~~, i·~~~~~~~~~~~~LQ) ··~~~~~~~~~~~~~~~~ . 0

Cliff A'~~~~~1: :e,, o~~~~~~

~~~~I r~ ~~~~~2

A~ ' 'w,. E

I _i

, -- lIP..a. a l .

co . "'- -i D _

fli ;r i

a ..................",'~"~·'~~~~~LL Z

23 z

0w

Ar n o.

CNJ .. 3"' ? h

.ii ' 0

'. I' . 3 I

. L, . - -J.

II

it ~ij it ','B.' ':

Figure 3

GENERAL PURPOSE MACHINE TOOL

I .

'*I,V-' '... :! ....... '

,.. '.*; '';in' '

_^S 1 i is-· L -.. .. '- ..... .

- .._ . . . . . . - - x ¶;"~~~~~~~~. .........3' 8.__,,,,_,~~ . ~_ _. __~,.,~--~._~'~, x . ................

; _3 .|F j·· _ * -

.~ , ,T - .".- yj: _

_~ ~ ~ ~~* I'js-

1: " * /--~ . :.. · ,._.

;~~~~~~ ~ :::

· ~? .?. : .,. " 1

. '. ~ · ; d, -~ ,B ^..:. -:'- . . 0 . ', .."

(COURTESY OF CINCINNATI MILACRON)

24

production were dependent on the personal skills of thedesigner, production planner, tool operator, inventory con-trol manager, etc.

The computer has now been applied to virtually allphases of manufacturing. Our survey indicates that in firmswhere computer techniques have been applied, manual skillshave been been augmented; functions which could not practi-cably be performed manually are now being performed; costshave been improved, productivity has increased, and customerservice and satisfaction improved. All of the improvedfunctions are playing important parts.

For example, for each product it produces, a companymust construct a listing or record of the materials, parts,and components that go into producing the product. The listis known as the bill of materials (BOM). BOM is used to planfor and obtain the materials required for a production run,to record engineering changes, to identify parts common tovarious and different products, and various other functions.It is a key activity in the manufacturing process. 8/

Many manufacturers said that computerized maintenanceand control of the bill of materials file have saved themmillions of dollars. Other manufacturers continue to relyon manual methods.

A detailed discussion of techniques and advantages ofBOM and of each of the elements of computer-integrated man-ufacturing is beyond the scope of this report. The individ-ual subjects are covered in great. detail in the literature.

However, the efforts of manufacturing are directed inthe last analysis to creating parts, components, and finalproducts. The two recent developments that are making majorcontributions to these efforts which are crucial to continuedproductivity improvement in the batch production industriesare the minicomputer and its adaption to operating machinetools, materials handling equipment, and industrial robots.

COMPUTERS AND NUMERICAL CONTROL

The importance of computers and numerical control toimproved productivity in batch production can best be appre-ciated against a background of the manual operations tradi-tionally employed in machining a part out of metal.

Basic machining function

Seven basic functions have been identified to operatethe general purpose machines used in metalworking batch

25

operations. These are performed by the skilled craftsmanor machinists on each discrete product produced. Theyare illustrated in chart 2.

Most parts require several different types of operationsthat call for the use of different types of machines. There-fore, after the part is worked on one machine, it would haveto be routed to another machine for the additional operationswhich would again require an operator to perform these sevenfunctions. This rerouting, set up, load, unload, manual con-trol, and waiting for the next operation result in much losttime. Authoritative estimates are that a machine tool in abatch process is actually cutting metal only about 15 percentof the time. The remainder is spent primarily waiting forparts, although tool changing and maintenance is also in-volved. Consequently, there are important productivity im-proving opportunities through applying technologies whichminimize the lost time. In fact, it has been estimated thatsome applications of computer and advanced machine tool tech-nology could result in machine utilization increases in batchprocessing of 600 percent or more. Resulting reduction of in-direct capital and labor costs and improvement of productiv-ity have been estimated to be potentially as high as ten-fold.

The computer and the numericallycontrolled machine

A forerunner to applying computers to the actual machin-ing of parts was the development of the numerically con-trolled (NC) machine tool in the late 1950s. The NC machinewas developed by the Massachusetts Institute of Technology.under contract with the Air Force. The need arose from theadvent of high performance aircraft, the parts of which re-quired three dimensional machining with a much higher degreeof accuracy than could be achieved on manually operated ma-chines.

Essentially, a basic NC machine is one that is controlledautomatically by coded instructions. Such a system has twoelements--a machine to perform the work and an electroniccontrol unit which directs the machine's motions. (See fig.4.) The coded instructions, representing the cutting pathand other operations of the machine are input to the controlunit in the form of programed numerical values punched intopaper tape or recorded on magnetic tape. This numerical datais automatically read and decoded; operating as an integratedunit, the control device causes corresponding machine movementto perform its functional operations (e.g., drilling, boring,etc.). (See fig. 5.) This system replaces certain functionsof the skilled craftsman/machinist, most notably functions4 and 5 (described above); i.e., establishing machine feedsand speeds, etc. and control of the machine motion. However,

26

CHART 2

ILLUSTRATION OF SEVEN BASICFUNCTIONS OF BATCH PRODUCTION

1. MOVE THE WORKPIECE 5. CONTROL THE MOTION OFTO THE MACHINE. a [ THE CUTTING TOOL.

2. LOAD THE WORKPIECE /*/j ._ 6. SEQUENCE DIFFERENTON THE MACHINE l i -ls TOOLS AND MOTIONSAND AFFIX IT r i l UNTIL ALL POSSIBLEACCURATELY. OPERATI ONS ON THAT oACCURATELY. OMACHINE ARE FINISHED. C

3. SELECT THE PROPER CUTTINGTOOL AND INSERT ITINTO THE MACHINE. /j.' 7. UNLOAD THE PART

FROM THE MACHINE.

4. ESTABLISH AND SET THEMACHINE OPERATING SPEEDSAND OTHER CONDITIONS.

R27~-

27

.

.o · I;I r ' .

Aii *

- cc i ' ;\ _

28

28

o _q~~~~~~~~

-J.I

I ' Z

U

-

Ir 0

oW ~ 4*A' __'

0

M 0M

C-i

rr~ )Hj~~~~~~~~~~~~~~L

CLII UC II( ~~g~ 1 .y

LF O~

411

uj

Z--~k ~.,>i," :;.

a,~~~~~~~~ Ip H ~V~;L(~~~~~~C

CA.)~~~~~~~~~~~~~~~~~~~~~~~~~fCIO) P

pjr-

a~.

cccLII~ ~ ~ ~ ~ ~ ~~~I ~ ~:,~,:,.;

LA.

o-z I b-~. ,~., :i

to .......Z~.~'~'~' ~.'

-J ~~~~~0

29

-~, I 7~,'~.~ J

o~- (~ .,~'I' : ~ ' " ·' i~~-,.~ui'?""':'T~- ~'~':~'

azco) v, ' '' ::I '` " '

C.. ~,,.~ ~..

P:~~ oLL1~~~~~~~~~~~~~~~., ~.,

29

the system created another highly skilled job--a part pro-gramer. This new job requires the expertise of both a skilledmachinist and a mathematician's understanding of computerlanguages. It is his job to extract from the engineeringdrawings all the data necessary to program the numerical cal-culations to control the machine movements.*

Numerical control by computer

Although tape is the most common input device in usetoday, in the latter 1960s software was developed to enablethe computer to directly input the numerical data to themachine control unit and to bypass the tape. There are sev-eral ways to accomplish this. A large central computer canbe used to directly control any number of machines. Thissystem is referred to as direct numerical control or DNC.However, what may be a more important technological advanceto computer-integrated manufacturing is the minicomputerand more recently the microcomputer.

These computers can be used to operate a single machineor several machines and can be linked to larger computers ina hierarchal system. This is referred to as computer numeri-cal control, or CNC. Before the development of the minicom-puter and microcomputer, only companies with large computercomplexes could consider DNC. However, the minicomputerand microcomputer have been reduced in costs so that CNCunits are competitive with the older, tape-driven controlunits.

The use of computers to replace tape controllers addsan element of time saving in reprograming, on a real timebasis, the numerical sequences in part programs to correcterrors or to implement design changes and enables the feed-back of data to management.

As a flexible automation method NC can be programed toperform different functions on a variety of different parts,using the general purpose machine tool in a more efficientmanner than possible with manual operation. A major benefitto be gained from using NC equipment is the quality of thepart. For example, sophisticated jet aircraft parts require

*Since the same mathematical data base is needed to createthe design as well as to program the machine tool to makethe part, the technology has advanced to the point where,in some companies, no engineering drawing need be made.The design is captured in the data base and the computerprograms the cutting path.

30

high precision cuts to meet tolerance requirements. Suchparts can be made only with NC. Also with NC each part willbe identical to the preceeding one since the judgment elementis removed from the cutting procedure. This provides tremen-dous benefits to the follow on assembly operations, becausewith closer tolerances, assembly becomes simpler and conse-quently less costly. Some users feel the major cost advan-tages come from easier assembly.

COMPUTER-AIDED MANUFACTURING

It has been estimated that a part is on a machine lessthan 5 percent of the time it is in the shop and for only aportion of that time is the tool cutting metal. (See chart3.) The remaining time is spent on waiting, moving, setup,downtime, assembly, inspection, etc. The improvements beingdeveloped in these operations, not just additional improve-ment of the metal cutting operation, hold the key to futurequantum increases in productivity of batch manufacturing op-erations.

Early NC machines controlled the operation of only asingle type of cutter, such as a drill. As they evolved,these machines were equipped with automatic tool changersthat hold various types of cutting tools. These are knownas machining centers (see fig. 6) which, as one single ma-chine, perform the functions of several NC machine tools,i.e., drilling, milling, boring, etc. For work in thesecenters the parts can be fixed onto moveable pallets whicheliminates setup time at the machine.

Additionally, there are systems which integrate multi-ple machining centers and automatically control the movementof work pieces from one NC center to the next on computer-controlled material handling systems. Not only can severaldifferent machining functions be performed without removingthe parts being machined from this system, but the machinetool operator is relieved of various manual duties in thata single operator can apply his skills to several machinesrather than to one. (See fig. 7.) Unlike mass productiontransfer lines, these computer-controlled flexible systemscan randomly handle different types of parts and selectand load the part onto the machine that can most economicallyperform the required operations.

Systems are also in use or are under development forautomatically selecting work pieces from storage and movingthem to machining centers; moving semifinished parts tointermediate storage and return for final processing, andmoving finished work pieces to storage pending shippingand distribution--all under computer control.

31

CHART 3

MZCD

z

cn IZ ~ ~ ~ ~ ~ ~ ~

CD

0~~~~~~~~

ui~ ~ ~ ~ ~ ~ ~ ~ ~ ~~~~~~~~u

CD

a o~~~~-D

Z~~~~~~~~~

-- __ f'~

LL=

) -- -- ----- --

o

C^

~~~~~--LLIJI I

Z0

I-o

I ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ I

=~~~~~~~~~~~ I"

32

~~~~~~~aXI~~~~~~~~~~~~~~~~~I.·; ;· 8 [r~~~~~~~~~~~~~~~~~~~~~~~~~~~~~Ui, Ifi L~~~~~~~5;: ~

r: · ,~~~~~~~~~~~~~~U

.. ~ ~ ~ ~ ~ ~ .1

tt

-~. ..

*, *. rL~ I

I.r· J3 w;;'

I.~~~~~~~~~~~~~;, /

I..~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~.i

I' .·

~ · ·~ ;i ·P%733

Figure 7

**;n'; .'.... . .; I.~*;;,-,I.,...W *<.. .# * . ; ..... ; .0 ....... .. sb.; ,',.; ! .r'C

· ~ ~ , .i .. ,.

),, , ~. .#9l, ,_ *i, ! ~ _ _ -- :- x > :_. .*· . - ..- - 7. .; ' M ZI , . ·. . r .i... 7 .

.. , .. . - - ,g - b e"¾ I-t; .

: : K' . -'p ,r,. . .". ., -.

· ~~~r ~~ * .. , . .

... "-.j " '.- .i "

. . ,.''

Jet:1 _.-.. ... :., ~-o, .

.. . * . . .. l O I R-R C

S.-~~~~~.... , I:-

.4 ..u.. ·;.,s…

(COURTESY OF INGERSOLL-RAND COMPANY)

COMPUTER INTEGRATED MANUFACTURING FACILITY

3434

Assembly is a major area in which time consuming manualoperations are performed. However, development work is be-ing done on industrial robots (artificial intelligence)which can recognize the shape of parts and be programed toperform multiple assembly operations in random sequence.

Work is also being performed to develop systems whichmonitor maintenance requirements and are able to pinpointproblems and order replacement parts with great time savingsand a minimization of downtime. In another area, sensordevices called adaptive controls are being developed whichmeasure such performance factors of an NC tool as heat,vibration, torque, and deflection and automatically adjustthe speed and other cutting operations to optimize cuttingefficiency and reduce tool wear. Systems which automaticallyinspect discrete parts, either when finished or while inprocess, are also being used or developed.

COMPUTER-AIDED DESIGN

Another phase of using computers for manufacturing isin the design process through a procedure called computer-aided design. For many years computers have aided the prod-uct designer by performing the mathematical calculationsnecessary to solve a large variety of design problems. Re-cent developments in computer technology, however, haveprovided the designer with "electronic drawing boards" inthe form of television tubes (cathode ray tubes) on whichhe may "sketch" his design ideas. (See fig. 8.) These sys-tems provide the designer with instant feedback as to theengineering feasibility of each sketch. When the designeris satisfied that he has a final design, he can instantlystore that design and all the necessary accompanying data incomputer files. These files are simultaneously accessibleto everyone else in the plant who needs the information.This data is then available to produce the instructions nec-essary to create a numerical control parts program, orderraw materials, sequence the operations and, in some cases,predict the cost to manufacture.

WHAT COMPUTER-INTEGRATEDMANUFACTURING ACCOMPLISHES

We have already alluded to the benefits from such func-tions as material requirements planning and inventory con-trols. Our discussion here will attempt to summarize onlythe benefits of the basic design and manufacturing opera-tions.

The flexibility of these systems provides a methodof increasing productivity while at the same time permitting

35

CL~

0

a

Er,

C')

0

I-

w

c-D

-J

C,

'3) 1'~21I~ w

r;'~~~~~~~~~~;o

6 0

i·:i· ~~·.r '* t~

· ·- ~ ~ I

ii~~~~~~ I· ;;W

~ ~~· rr~~~~~~~~~i~~~~T ~~~~S

ii~~~~j *

1~~~~3

responsiveness to changing market demands. Product changesand improvements can be incorporated easily without costlyretooling and downtime. A greater variety of customizedproducts is possible, and recent market trends indicate con-sumers are demanding a wider variety of products. Eliminat-ing costly setup time gives to the batch industry the bene-fits of lower cost for each item, without the inflexibilityof transfer line techniques used in high volumes.*

A convenient understanding of the results of CIM isobtained by comparing how the seven basic manual functionsshown in chart 2, page 27, are accomplished using thecomputer-controlled methods we have described. Table 5illustrates these seven functions under various degrees ofcomputer control. Using the most sophisticated machiningsystems, the computer-controlled machine tools and materialshandling equipment accomplish steps one through seven whichwere previously performed manually. Instead of steps oneand seven, the machinist loads the workpiece on a pallet orfixture, but the integrated machining systems moves it tothe machine and affixes it, machines it, unloads it, and re-turns it to the machinist for removal from the pallet orfixture.

For the machining centers, manual steps three throughsix are eliminated, as opposed to steps four and five whichare eliminated by basic stand-alone NC.

As indicated earlier, an area of potentially great im-provement is that of percent of machine utilization. Thisin turn would lead to a reduction of parts in process andthe resulting inventory of unfinished parts on the shopfloor which are in line for the next operation or assembly.This inventory could be reduced by up to 90 percent. Theresulting reduction of indirect capital and labor costs andimprovement of productivity could be enormous.

Productivity increases through use of automated systemsare usually considered in terms of freeing labor and capitalfor redeployment in other phases of our economy. However,equally, if not more important today, are other resourcessuch as raw materials and energy. One source recentlystated that the manufacturing sector consumes 40 percent ofall U.S. energy. Through the benefits available with

*This is not to say that CIM yields unit costs as low asthose achieved using transfer lines. Given the proper vol-ume transfer lines continue to yield the lowest unit cost.

37

TABLE 5

COMPARISON OF MANUAL MANUFACTURING STEPS

ELIMINATED BY VARIOUS DEGREES

OF COMPUTER CONTROL

Production methods

Standalone Machining

Step Conventional NC center CIM

1. Move workpiece tomachine M M M C

2. Load and affixworkpiece onmachine M M M C

3. Select and inserttool M M C C

4. Establish and setspeeds M C C C

5. Control cutting M C C C

6. Sequence tools andmotions M M C C

7. Unload part frommachine M M M C

M = Manual operationC = Computer-controlled operation

38

CIM--i.e., optimization of cutting, better use of time andfacilities, better planning of needs and fewer rejects--sub-stantial energy and materiel savings would accrue.

The new technology also holds the possibility of man-aging and operating a factory without technicians in the ma-chining areas. The Japanese have developed a concept forjust such a plant. (See ch. 6.) An oversimplification, butnonetheless pertinent statement, is that you do not needlight or heat in an unmanned factory.

Computer integrated manufacturing can also contributeto the objectives of the Occupational Safety and Health Actof 1970. Computer-controlled machines can reduce or elimi-inate physical contact of the technician with his machine ormachines. In systems which are now evolving (and in somenow operating) the machines can operate for long periods inisolation from their human controllers. Thus human exposureto physical injury, noise pollution, and contaminated or un-clean environments can be reduced.

SUMMARY

Computer-integrated manufacturing systems are changingthe management of manufacturing, are improving productivity,and hold great promise for bringing about continued improve-ments in discrete parts batch process manufacturing. Theyprovide the basis for improving the productivity of bothcapital and labor, economies in using materials and energy,and reducing exposure to the hazardous and less appealingwork in factories.

39

CHAPTER 4

COMPUTER-INTEGRATED MANUFACTURING--ITS PROBLEMS

As indicated in chapter 3, various components ofcomputer-integrated manufacturing (CIM) are already yield-ing improved productivity of capital and labor and CIM hasgreat promise for the future. This is a new technologywhose full potential is only now beginning to be understood.It has had problems in reaching its present level of develop-ment, and there are problems to be solved and technologicalgaps to be filled in before fully integrated systems will beachieved or their maximum efficiency will be realized.

Computers applied to manufacturing require new and un-familiar management and technical skills; the hardware andsoftware products of different manufacturers are not compat-ible; many areas of standardization need to be studied; fur-ther developments and innovations are needed in such areasas process planning and component and finished parts assemblyand testing; life cycle costing and cost benefit analysis ofthe more sophisticated systems are imprecise; and our studiesshow that many manufacturers are not aware of the technologyavailable to them. Despite their advantages, many componentsof the new systems are more costly than the older systems ormachines they replace, which increases both problems of cap-ital formation and risk. Also the applied research neces-sary to develop pilot systems designed to reach the potentiallimits of the new technology require long leadtimes and largeamounts of capital and are beyond the capacities of the indi-vidual firms which could most benefit from them. For muchthe same reasons, basic research on new manufacturing methodsis minimal.

Additionally, there are weaknesses in (1) national pol-icy for technology,* (2) communication between Governmentagencies and Government and industry, and (3) market defects(this is a generalization embracing many of the more specificproblems mentioned in the paragraphs above) for diffusing thetechnology and marketing its products.

The list is not complete, but it is sufficiently compre-hensive for the reader to sense the problems.

The potential of CIM, the magnitude of the problems tobe solved, and differing national approaches to their solu-tion are major factors that dictate a need to examine intothe adequacy of the U.S. national effort.

*See the quote of Senator Bentson, p. 13.

40

We shall not attempt to discuss all the problems. Weshall discuss some of those which are important to the costof Government procurement, which involve the most difficulty,and for which foreign competitors have developed nationalinstitutional mechanisms.

INVENTION, INNOVATION, AND DIFFUSION

In discussing manufacturing technology, it is importantto recognize that technology is not a single entity. Tech-nology is the result of a delicate process which can be use-fully separated into three phases.

--Invention.-- Innovation.--Diffusion.

1. Invention is the creative part of the process thatis difficult to dictate on demand. The environment providedto the inventor is probably the single most important factorto which public and private institutions can contribute.The environment that should be provided is one that wouldallow a creative individual or organization to bring ideasto realization. This is the rationale of basic researchdone at universities and in the public and private sectors.

2. Innovation is the first introduction of an inven-tion into successful practice. It is sometimes describedsynonymously as being the first new application of a tech-nology.

3. Diffusion is the successive and widespreadimitation of successful innovation.

It is the second two phases of technology, namely, in-novation and diffusion, on which institutions and managementcan best exert directed influence. This is not to say thatGovernment is ineffective in encouraging invention. Quite tothe contrary. By providing a constructive climate, fundingand definition of need, inventors can be encouraged to directtheir "inventiveness" in particular directions. The "Re-search Applied to National Needs" (RANN) program of the Na-tional Science Foundation is an example of a program to en-courage new development in manufacturing technology.* Both

*Concerning influencing invention, Hough 9/ states that "thedirection of new technology generation [Tnvention] can bechanged by defining Society's technical needs or goals andproviding a market for items which satisfy those needs."

41

the rate and the direction of innovation and diffusion can,to some extent, be controlled.

The United States has historically excelled intranslating both invention and innovation into useful appli-cations, and from our study we believe that this country gen-erally has in place and in operation more of the most ad-vanced manufacturing technology than other countries. Thisshould not necessarily provide a basis for complacency.

Our discussions and research indicate that the UnitedStates continues to be a leader in invention and innovation.However, our work suggests that the U.S. applications areconcentrated in a relatively few large firms within high-technology industries or within high-capital intensive in-dustries. For the most part these applications are privatelysponsored, proprietary systems and the underlying technologyis not well diffused throughout the U.S. industrial base.(See app. III for a brief discussion of the stage of develop-ment of the automation industry.)

This situation is due to the fact that bringing any newtechnology through the steps from invention to widespreaduse is an expensive, time-consuming and risky process, andonly the larger and stronger firms can support such efforts.This is generally true for both U.S. and foreign firms.

A general rule of thumb puts the development life cycleof any new technology at 10 to 20 years.