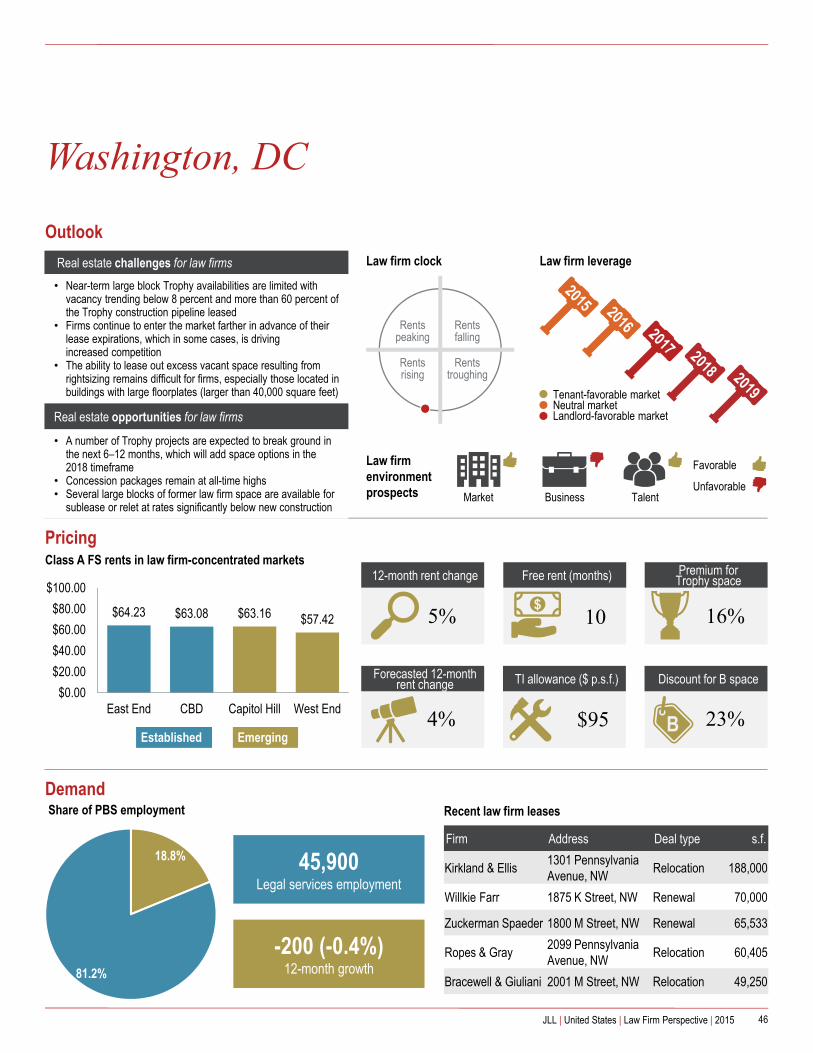

law firm perspective - typepad · 2015-10-26 · table of contents united states law firm market...

TRANSCRIPT

Law Firm Perspective

United States | 2015

Creating opportunities in a growth

economy and market

Table of contents

United States Law Firm market – Office outlook 3

Local Law Firm markets 7

Atlanta 8Austin 9Baltimore 10Boston 11Charlotte 12Chicago 13Cincinnati 14Cleveland 15Columbus 16Dallas 17Denver 18Detroit 19Fairfield County 20Fort Lauderdale 21Houston 22Indianapolis 23Long Island 24Los Angeles 25Miami 26Milwaukee 27Minneapolis 28New Jersey 29New York 30Oakland 31Orange County 32Philadelphia 33Phoenix 34Pittsburgh 35Portland 36Raleigh-Durham 37Richmond 38Sacramento 39San Diego 40San Francisco 41Seattle-Bellevue 42Silicon Valley 43St. Louis 44Tampa 45Washington, DC 46Westchester County 47

2JLL | United States | Law Firm Perspective | 2015

LAW FIRM PERFORMANCE IS:

REVIVINGAmLaw 100 revenue

reached a record

$81 billion in 2014 and is growing consistently at around

4.5% per year.

$$ RISING $$

16% of AmLaw100 firms now have profits per partner greater than $2.5 million.

OFFICE MARKET IS:

TIGHTENING

CBD Class A direct vacancy is down by 100 basis points year-on-year to

11.1% in Q2 2015

CBD Class A direct vacancy below 10%:

Pittsburgh5.9%

Portland6.4%

Charlotte7.1%

Midtown (NY)8.5%

San Francisco9.0%

1/3 more Class A development is underway now than at this time last year, totaling:

38.3 million s.f.Firms have more options for quality space with the construction pipeline preleasing rate at:

38.1% vs. 47.8% average

NEW SUPPLY PIPELINE WILL PROVIDE:

RELIEF

Will law firm demand grow over the next 12 months?

Job growth has reached the highest level since the late ‘90s with 10.4 million jobs created since the trough in 2010. Further, economic growth prospects for 2016 remain bullish with most recent second quarter 2015 growth pegged at 3.9 percent annually, with growth diversified across business and consumers. Different from earlier points in the cycle, companies across sectors and geographies are growing, including the office-using heavyweight of banking and finance, thereby adding talent and office space.

Nowhere are these trends more present than in CBD Trophy and Class A space, the same subset of the market in which law firms locate their offices. A combination of demographic shifts, limited supply, accelerated rent increases and record sales pricing pushing up underwritten rents has placed law firms in a landlord-favorable setting across markets from Boston to Miami and New York to San Francisco.

16.0%4.0%

80.0%

Increase

Decrease

Stable

United States Law Firm marketOffice outlook

In line with improvements in the broader economic picture, law firms have begun to see a more uplifting business environment. AmLaw 100 gross revenue reached a record $81.0 billion, rising 4.6 percent over the year, with revenues now growing at or above 4.5 percent annually for four of the past five years. This rate is increasingly becoming the new normal, demonstrating growth but stability from the 10 percent growth rates many firms experienced in the earlier part of the decade.

Fee compression as well as weaker demand for legal services following the recession, however, have forced law firms to focus on enhanced efficiencies for two of their largest expenditures: talent and real estate. The industry’s deep focus on operational leverage has helped firms buoy two key industry metrics in the slower-growth environment of recent years, revenue per lawyer and profits per partner, the latter of which rose by 5.3 percent in 2014 to $1.6 million.

Meanwhile, a greater focus on diversified practice groups such as cybersecurity, financial regulations, health care data management and privacy has boosted financial gains at the market level as well, strengthened by consistent hiring across industries in geographies as diverse as San Francisco (tech and intellectual property), Dallas (corporate law), Miami (international finance) and Denver (ancillary services). For perhaps the first time since the late 2000s, law firms have reason to be more optimistic, with their business outlook improving.

On the other hand, law firms face a tighter and more competitive office market than in previous years just as they are beginning to expand.

3JLL | United States | Law Firm Perspective | 2015

KEY HIGHLIGHTS:

1Record AmLaw 100 revenue of $81.0 billion and stable rates of growth are helping to revive the legal sector

2Just as firm revenue is expanding, improving economic conditions are boosting office market performance, creating a more competitive environment

3CBD Class A space is seeing vacancy fall into single-digit territory in many markets, while Trophy rents are rising 2.5x faster than the market average

4Development has been catalyzed in response to demand, although new space commands a 20 to 25 percent premium

Firms looking for low-cost space are actively taking interest in secondary and tertiary markets

OVERALL

PRIMARY

SECONDARYTERTIARY

How tight is the CBD Class A market? Very tight.

Law firms comprise approximately 17.0 percent of Trophy andClass A office space across cities with firms accounting for more than one quarter of occupancy in markets such as Washington DC, Palo Alto, Cleveland, Columbus, Fort Lauderdale and Austin. Nationally, as of September 2015, direct vacancy in this segment of the office market averaged 11.1 percent, far below the 14.2 percent rate for the overall office market. Across the highest-end of the market (the Trophy swath of the market) fundamentals are even tighter with vacancy levels dipping below 10.0 percent as of September 2015.

In many key mid-sized markets, direct vacancy has dropped to single-digit levels: Pittsburgh (5.9 percent), Portland (6.4 percent), Charlotte (7.1 percent), Midtown Manhattan (8.5 percent) and San Francisco (9.0 percent). Among large geographies, only Dallas and Atlanta reported significantly above-average direct vacancy yet even in those markets year-over-year vacancy declines have been some of the most dramatic decreases. These two markets witnessed a combined 989,327 square feet of occupancy growth year-to-date and we expect that vacancy will continue to fall until new construction delivers in 2016 and 2017 and companies put space back onto the market upon relocation.

This lack of supply has helped to boost rents sharply. Since 2010, CBD Class A rents have risen by 22.7 percent to $47.19 per square foot. Over the course of the recovery, Trophy rents have spiked by 28.3 percent to $57.97 per square foot and, at annual rates, we expect that they will jump at an annual rate of 18.1 percent through 2015. Respectively, CBD Class A and Trophy rents are growing at 2.0x and 2.5x the rate of overall market asking rents, a trend that we foresee continuing through 2016 and into early 2017 due to sustained employment growth in urban areas.

Leasing remains focused on efficiency

As one of the largest and most high-profile components of the national tenant base, law firms remain an outlier compared to other industries in terms of their share of leasing activity. Among transactions larger than 20,000 square feet, law firms accounted for just 7.2 percent of activity by volume over the past year. This is the fourth-largest contribution of any sector after finance, technology and government, but marginal compared to their 17.0 percent share of occupancy across the country.

Why has this evolved? First, high-growth segments of the economy, such as the high-tech and creative sectors, are dominating activity, accounting for 28.9 percent of leasing volumes. Second, law firms remain focused on efficiency plays and thus are largely stagnant from a real estate perspective. For example, 38.7 percent of law firm activity represented rightsizing with only 22.4 percent being expansionary, largely in industry-specific markets such as Silicon Valley, with high-growth practice groups such as intellectual property. In comparison, 75.2 and 69.8 percent of leasing for advertising/marketing and tech, respectively, has represented growth in recent quarters, signaling firms are not just competing against themselves, but more broadly against the new economy.

From a geographical perspective, the “big four” law markets of New York, Washington DC, Chicago and Los Angeles posted 4.3 million square feet of law firm leasing activity, or 50.5 percent of the national total. Other focal points include Dallas, San Francisco, Denver, Boston and Minneapolis, where diversified growth across industry sectors continues to power office demand and rent levels.

Firms experiment with core-fringe locations

As a result of tightening fundamentals across core urban areas, law firms have begun to consider relocating to core-fringe CBD micromarkets, particularly for firms looking at new construction. These core-fringe locations, such as the Seaport District in Boston, Hudson Yards in New York and Mount Vernon Triangle in Washington, DC, provide better access to younger talent in quality space, more mixed-use and less office-focused parts of the urban core and some of the most efficient workspace designs available. These are three key strategies all firms should be focused on as their businesses evolve, especially since in some of these core-fringe areas, there is an economic discount for first movers.

In New York, Skadden and Boies Schiller have signed on as anchor tenants for Brookfield’s 1 Manhattan West and Related’s 55 Hudson Yards, respectively, transitioning away from the traditional Midtown submarkets of Times Square, Grand Central and the Plaza District to the western edge of Manhattan. Similarly, in Washington DC, Venable and Arnold & Porter will move across the street from each other at 600 and 601 Massachusetts Avenue NW, respectively, in the emerging Mount Vernon Triangle area of the East End.

4JLL | United States | Law Firm Perspective | 2015

Will rents rise, fall or remain stable over the next 12 months?

Law firms represent 7.2 percent of leasing activity

22%

18%

7%7%

46%

Banking and finance

Tech and telecom

Government

Law firm

All other industries

7.2%

76.0%

4.0%

20.0% Increase

Decrease

Stable

Law firms across the board are in a rising-rent environment

OVERALL

PRIMARY

SECONDARY

TERTIARY

Development will help alleviate constraints, but at a price

In response to impending supply shortages as well as generally improving macroeconomic conditions, developers have begun to ratchet up the pace of groundbreakings offering firms limited opportunities over the next 12 months, but greater opportunity over the next 36 months. CBD Class A development activity currently totals 38.3 million square feet, the highest figure in seven years and more than one-third higher than halfway into 2014. This total will jump more in the coming quarters as the rate of groundbreakings increases. Rents for this space currently command far above-average premiums; in Q2 2015, CBD Class A space under construction had asking rents averaging $54.68 per square foot, 15.9 percent above rates for existing space.

Demand for new space has been widespread, resulting in a preleasing rate for CBD Class A space of 38.1 percent. Although still above historic norms, drops in preleasing due to increases in speculative development has resulted in available space under construction totaling slightly under 15.0 million square feet. Importantly, available space underway is growing faster than preleasing, which will bode well for law firms and other occupiers.

Constraints at the top of the market have also provided owners of second-generation properties with the opportunity to look at repositioning assets to provide more modern amenities and improved work environments in central and highly-accessible locations to capture latent demand at a slightly discounted price; for law firms, this space will provide additional options at lesser expense.

Outlook for law firms is one of competition and trade-offs

Nearing the peak of both the economic and real estate cycles over the next 12 to 18 months, law firms over the shorter-term face a very landlord-favorable environment and will need to assess a variety of factors from location to predicted footprint to talent access and retention.

Overall, the environment for tenants across the board is competitive, with law firms’ position in the market even more so. With some ingenuity and prioritization of needs, firms can buffer against escalating costs and dwindling options. Improved corporate and personal consumption are likely to boost revenue and business for firms, as will growing demand for mergers and acquisitions. Further, more accelerated increases in output across diversified industries will provide opportunities for firms with growing new practice groups in specific markets.

5JLL | United States | Law Firm Perspective | 2015

Top markets for law firm leasing activity (s.f.) – past 12 months

New York 2,004,220

Washington, DC 1,844,568

Dallas 770,125

Chicago 602,000

San Francisco 353,274

Minneapolis 317,887

Denver 310,547

United States law firm leasing total 8,791,872

Declining availability means firms in most markets need to look at new construction

OVERALL 52.0%48.0%

Yes No

66.7%

33.3%

40.0%

60.0%55.6%

44.4%

PRIMARY

SECONDARY TERTIARY

Are large law firms limited to new construction?

JLL | United States | Law Firm Perspective | 2015 6

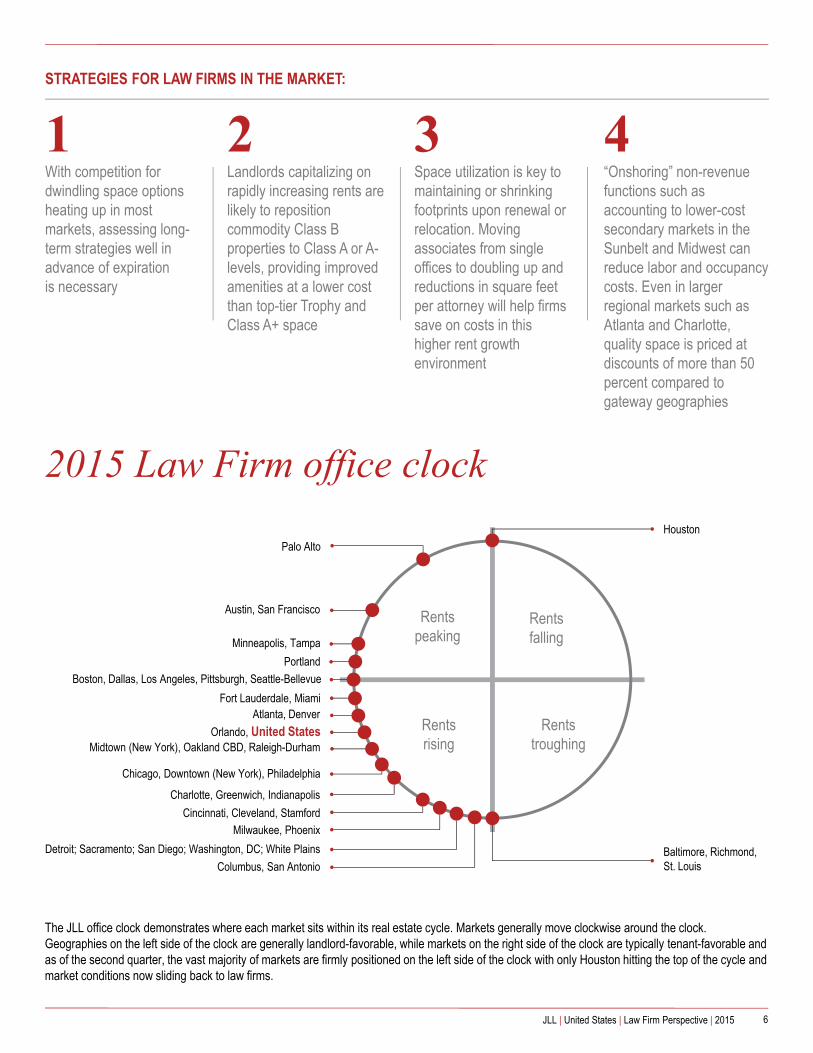

The JLL office clock demonstrates where each market sits within its real estate cycle. Markets generally move clockwise around the clock. Geographies on the left side of the clock are generally landlord-favorable, while markets on the right side of the clock are typically tenant-favorable and as of the second quarter, the vast majority of markets are firmly positioned on the left side of the clock with only Houston hitting the top of the cycle and market conditions now sliding back to law firms.

2015 Law Firm office clock

Rents peaking

Rents falling

Rents rising

Rents troughing

Fort Lauderdale, Miami

Baltimore, Richmond, St. Louis

Milwaukee, Phoenix

Charlotte, Greenwich, Indianapolis

Boston, Dallas, Los Angeles, Pittsburgh, Seattle-Bellevue

Orlando, United States

Cincinnati, Cleveland, Stamford

Columbus, San Antonio

Minneapolis, Tampa

Detroit; Sacramento; San Diego; Washington, DC; White Plains

Atlanta, Denver

Midtown (New York), Oakland CBD, Raleigh-Durham

Austin, San Francisco

Chicago, Downtown (New York), Philadelphia

Palo Alto

Portland

Houston

STRATEGIES FOR LAW FIRMS IN THE MARKET:

1With competition for dwindling space options heating up in most markets, assessing long-term strategies well in advance of expiration is necessary

2Landlords capitalizing on rapidly increasing rents are likely to reposition commodity Class B properties to Class A or A-levels, providing improved amenities at a lower cost than top-tier Trophy and Class A+ space

3Space utilization is key to maintaining or shrinking footprints upon renewal or relocation. Moving associates from single offices to doubling up and reductions in square feet per attorney will help firms save on costs in this higher rent growth environment

4“Onshoring” non-revenue functions such as accounting to lower-cost secondary markets in the Sunbelt and Midwest can reduce labor and occupancy costs. Even in larger regional markets such as Atlanta and Charlotte, quality space is priced at discounts of more than 50 percent compared to gateway geographies

Local Law Firm markets

7JLL | United States | Law Firm Perspective | 2015

Atlanta

8JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Landlords with availabilities in Buckhead have increased asking

rates exponentially, leveraging current supply constrained market conditions

• Even available creative loft options are few and far between, frustrating smaller independent firms with leases coming due

• Technology companies are migrating to Midtown, the epicenter of Atlanta’s law firms, presenting a cultural mismatch within popular buildings

Real estate opportunities for law firms

• Large Midtown occupiers will find several opportunities to partner with developers on build-to-suit arrangements

• The Northwest and Northeast suburban submarkets offer several space options for moving secondary operations outside the CBD, offering larger floorplates and more affordable rents

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$29.79 $27.56$21.53

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Buckhead Midtown Downtown

12-month rent change

6%

Demand

Free rent (months)

7$

5.0%

95.0%

Share PBS* employment

$60

TI allowance ($ p.s.f.)Forecasted 12-month rent change

5%

Discount for B space

B 21%

Premium for Trophy space

46%

Firm Address Deal type s.f.

Hall Booth Smith191 Peachtree Street NE

Renewal 64,359

Holland & Knight1180 W Peachtree Street

Relocation 44,971

Finnegan 271 17th Street Relocation 26,252

Scrudder Bass 900 Circle 75 Parkway Renewal 13,546

Recent law firm leases

Law firm leverageLaw firm clock

Favorable

UnfavorableMarket Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

Established

Pricing

24,100Legal services employment

+0 (+0.0%)12-month growth

Law firm environment prospects

Class A FS rents in law firm-concentrated markets

*PBS refers to professional and business services employment, which includes the legal services sector

Austin

9JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Demand for CBD space, combined with low vacancy, has

caused rates to consistently increase year-over-year• Austin has a booming tech sector that is driving a trend of open

office floorplans, thus limiting the amount of move-in-ready space for firms that prefer an office-intensive configuration

• Rise of boutique law firms: Due to the start-up friendly business climate in Austin, many large law firms have seen partners establish or join smaller boutique law firms

Real estate opportunities for law firms

• UT Austin’s LBJ Law School consistently ranks as one of the top law schools in the nation. Local law firms have a rich talent pool with law school graduates who prefer Austin’s quality of life versus relocating to other markets

• Flourishing government and tech sectors: Demand for law firms will remain robust as government agencies, anchored by the State Capitol, and tech start-ups seek legal counsel

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$46.66

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Downtown

12-month rent change

8%

Demand

Free rent (months)

1$

5.4%

94.6%

Share of PBS employment

$30

TI allowance ($ p.s.f.)Forecasted 12-month rent change

8%

Discount for B space

B 27%

Firm Address Deal type s.f.

Scott Douglass Colorado Tower Relocation 40,000

DuBois Bryant Colorado Tower Relocation 24,000

Munsch Hardt Colorado Tower Relocation 14,700

Kelly Hart Colorado Tower Relocation 14,000

Ogletree301 Congress Avenue

Renewal 9,600

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Premium for Trophy space

9%

Tenant-favorable marketNeutral marketLandlord-favorable market

8,500Legal services employment

+100 (+1.2%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

10JLL | United States | Law Firm Perspective | 2015

Baltimore

Real estate challenges for law firms• Availability for space larger than 10,000 square feet along the

waterfront from the Pratt Street Corridor to Harbor East has become scarce following several key renewals over the past year

• New construction opportunities are limited in the law firm-concentrated submarkets of the CBD and Harbor East

Real estate opportunities for law firms

• Opportunities remain for tenants not requiring Class A space along the waterfront with the Baltimore and Charles Street Corridors in the CBD continuing to face elevated vacancy

• Exelon’s pending relocation from more than 100,000 square feet at 750 E Pratt Street to their new headquarters at Harbor Point will create a new block of Class A availability on Pratt Street in 2017 and 2018

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$23.25$28.80

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

CBD Baltimore SE

12-month rent change

5%

Demand

Free rent (months)

4$

5.3%

94.7%

Share of PBS employment

$41

TI allowance ($ p.s.f.)Forecasted 12-month rent change

2%

Discount for B space

B 20%

Firm Address Deal type s.f.

Kramon & Graham 1 South Street Renewal 25,853

Niles Barton & Wilmer 111 S Calvert Street Renewal 21,835

ARD&H 7 St. Paul Street Renewal 19,682

Offit Kurman 300 E Lombard Street Expansion 16,650

Salsbury Clements 300 W Pratt Street Renewal 10,755

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Premium for Trophy space

75%

Tenant-favorable marketNeutral marketLandlord-favorable market

12,000Legal services employment

-500 (-4.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

Boston

11JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• While law firms make up only 6.0 percent of the active tenants

currently shopping for space in Boston CBD, competition is intensifying from financial services and technology companies

• With vacancy in the Financial District the lowest since 2009, law firms are challenged to find viable options

• Rents in Boston CBD continue to grow and law firms currently negotiating leases downtown will pay a premium

Real estate opportunities for law firms

• Rents have been rising rapidly, but most of the growth has occurred in high-rise and premium spaces. There are still many low-rise opportunities for value-seeking law firms

• New supply expected to deliver at 888 Boylston Street, only 30 percent preleased, will be an opportunity for tenants seeking premium space in the Back Bay

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$61.03 $56.36 $59.30

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

Back Bay Financial District Seaport District

12-month rent change

5%

Demand

Free rent (months)

3$

5.3%

94.7%

Share of PBS employment

$50

TI allowance ($ p.s.f.)Forecasted 12-month rent change

7%

Discount for B space

B 27%

Firm Address Deal type s.f.

Hemenway & Barnes 75 State Street Relocation 44,233

Fragomen 100 High Street Relocation 43,186

Centrulo 2 Seaport Lane Relocation 33,209

Manion Gaynor & Manning

125 High Street Renewal 31,203

Sunstein 125 Summer Street Relocation 28,502

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

10%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

24,600Legal services employment

+300 (+1.2%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

Charlotte

12JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• With vacancy in Uptown at 8.2 percent, demand is high for

Trophy and Class A Trophy space • Average rents stand at the highest rate since 2009, and

landlords confidence and leverage over the near-term only appears to be expanding

• Growing competition for Class A space from financial institutions (for tech use) poses a competitive threat for law firms

Real estate opportunities for law firms

• With 714,459 square feet of Class A office space under construction in the CBD, tenants will have the opportunity to secure high-quality space when it hits the market over the next 24 to 30 months

• Although rents have increased, rates are substantially discounted to other major markets. Combine that with talent levels and Charlotte is an ideal back-office location for firms

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$28.27 $30.70

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Downtown Southpark

12-month rent change

10%

Demand

Free rent (months)

5$

3.9%

96.1%

Share of PBS employment

$25

TI allowance ($ p.s.f.)Forecasted 12-month rent change

2%

Discount for B space

B 26%

Firm Address Deal type s.f.

McGuireWoods 201 N Tryon Street Renewal 144,293

Womble Carlyle 301 S College Street Renewal 55,000

Cozen O’Connor 301 S College StreetNew to market

6,533

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

9%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

7,200Legal services employment

+200 (+2.9%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Chicago

13JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Blocks of available Class A space are diminishing greatly with

only 13 such blocks larger than 100,000 s.f.• Tightening conditions will continue into mid-2017 and as a result,

the market for large blocks will grow increasingly competitive • With growing demand for large blocks, rents will continue to rise

and concessions will compress

Real estate opportunities for law firms

• Firms willing to consider second-generation space will have opportunities prior to 2017

• Holding out on real estate decisions until 2017 will give firms a more tenant-favorable market for negotiating due to new supply in the form of the construction pipeline downtown

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$44.62 $40.99 $40.00 $38.21

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

River North West Loop Central Loop East Loop

12-month rent change

1%

Demand

Free rent (months)

12$

5.7%

94.3%

Share of PBS employment

$44

TI allowance ($ p.s.f.)Forecasted 12-month rent change

3%

Discount for B space

B 14%

Firm Address Deal type s.f.

Mayer Brown 71 S Wacker Drive Renewal 240,000

Freeborn & Peters 311 S Wacker Drive Renewal 112,000

Polsinelli 150 N Riverside Plaza Relocation 110,000

Butler Rubin 540 W Madison Street Relocation 90,000

SmithAmundsen150 N Michigan Avenue

Renewal 50,000

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

6%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

47,500Legal services employment

+300 (+0.6%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Cincinnati

14JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Large blocks of quality space are dwindling, particularly in the

CBD, the preferred location of many Cincinnati law firms • Firms in the market for space must act soon as meaningful rent

growth will begin to surface in the next 12–24 months, especially for Class A space, as steady leasing activity has tightened the market

Real estate opportunities for law firms

• Planned office space at The Banks development will provide additional Trophy space in the CBD

• Rents will remain at stable levels in the short-term, giving potential tenants a window to make any leasing decisions prior to rent growth

• Attractive concession packages remain in the CBD

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$22.57 $23.58

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

CBD Midtown

12-month rent change

Demand

Free rent (months)

6$

4.3%

95.7%

Share of PBS employment

$40

TI allowance ($ p.s.f.)Forecasted 12-month rent change

2%

Discount for B space

B 27%

Firm Address Deal type s.f.

Dinsmore & Shohl 255 E 5th Street Expansion 8,039

Marshall Dennehey 312 Elm StreetNew to market

7,292

The Wolfe Practice 4438 Carver Woods Sublease 6,500

Frost Brown Todd9277 Centre Pointe Drive

Expansion 6,318

Kirby Thomas Brandenburg

24 Remick Boulevard Relocation 5,070

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

20%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

1%

7,500Legal services employment

+200 (+2.7%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

Cleveland

15JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Reserved, climate-controlled parking is extremely limited

downtown and hard to acquire, thus tenants will find they are only able to negotiate a limited number of reserved spaces into their lease agreement

• Signage opportunities on existing assets in the CBD are limited • New construction is limited, but several projects have been

proposed and tenants will pay a premium upward of 50 percent for such space

Real estate opportunities for law firms

• Several of Cleveland’s corporate tenants have announced rightsizings in the last 18–24 months, which has created large blocks of space for landlords to market to prospective tenants

• Demand fluctuations have dampened rent growth over the last year and this trend will continue into 2016, providing tenants an opportunity to renew or extend leases at discounted rates

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$25.12$21.27

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Public Square Financial

12-month rent change

1%

Demand

Free rent (months)

8$

7.2%

92.8%

Share of PBS employment

$35

TI allowance ($ p.s.f.)Forecasted 12-month rent change

1%

Discount for B space

B 10%

Firm Address Deal type s.f.

Ulmer & Berne Skylight Office Tower Renewal 87,000

Benesch 413 E Huron Road Relocation 66,500

Frantz Ward 200 Public Square Relocation 45,806

Javitch Block 1100 Superior Street Renewal 44,700

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

25%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

10,900Legal services employment

+100 (+0.9%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

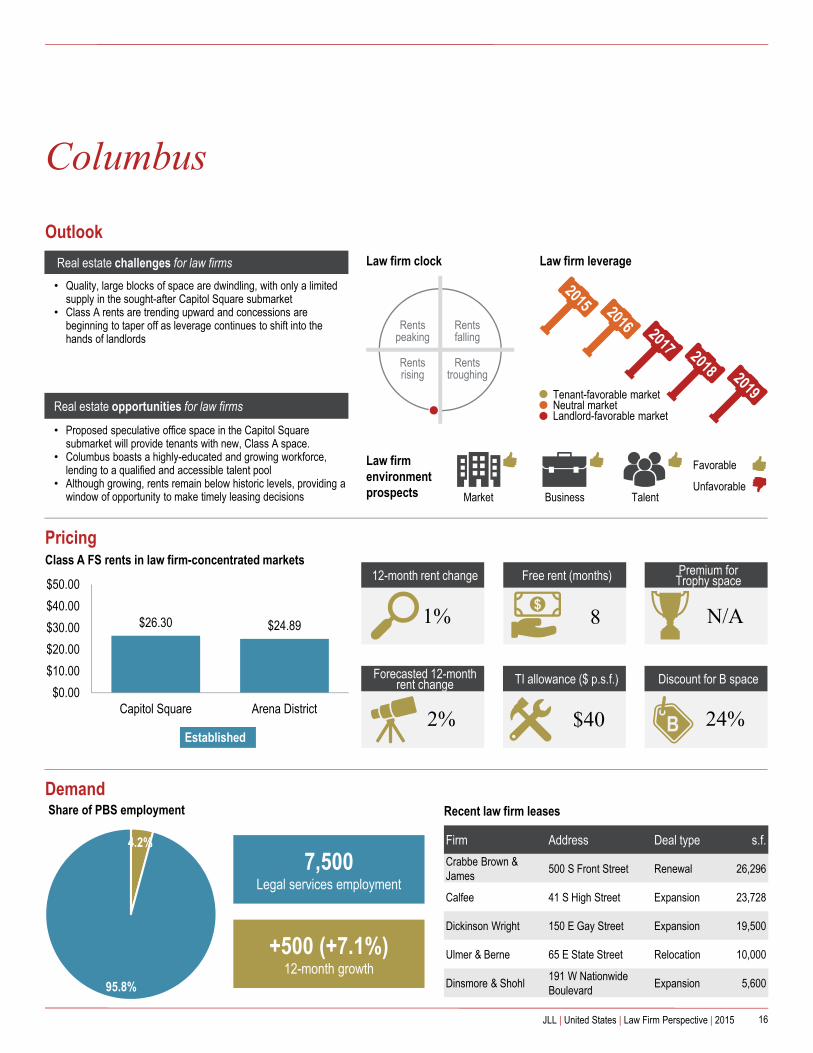

Columbus

16JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Quality, large blocks of space are dwindling, with only a limited

supply in the sought-after Capitol Square submarket • Class A rents are trending upward and concessions are

beginning to taper off as leverage continues to shift into the hands of landlords

Real estate opportunities for law firms

• Proposed speculative office space in the Capitol Square submarket will provide tenants with new, Class A space.

• Columbus boasts a highly-educated and growing workforce, lending to a qualified and accessible talent pool

• Although growing, rents remain below historic levels, providing a window of opportunity to make timely leasing decisions

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$26.30 $24.89

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Capitol Square Arena District

12-month rent change

1%

Demand

Free rent (months)

8$

4.2%

95.8%

Share of PBS employment

$40

TI allowance ($ p.s.f.)Forecasted 12-month rent change

2%

Discount for B space

B 24%

Firm Address Deal type s.f.

Crabbe Brown & James

500 S Front Street Renewal 26,296

Calfee 41 S High Street Expansion 23,728

Dickinson Wright 150 E Gay Street Expansion 19,500

Ulmer & Berne 65 E State Street Relocation 10,000

Dinsmore & Shohl191 W Nationwide Boulevard

Expansion 5,600

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

N/A

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

7,500Legal services employment

+500 (+7.1%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Dallas

17JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Limited space is available in most desirable properties• Low vacancy and much higher priced new construction are

creating significant upward rent pressure• Law firm buildout costs are skyrocketing – what was $40.00 per

square foot is now $75 per square foot and even upward of $100 per square foot in properties under construction

• Firms need to upgrade space to be competitive for talent

Real estate opportunities for law firms

• Significant economic growth and corporate relocations have put Dallas on the radar of firms looking to open new regional offices

• New construction is delivering premium spaces to Uptown and CBD

• Some firms are not relocating, but moving within a property to get updated, more efficient buildout at higher, but competitive rates

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$34.35

$23.55

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Uptown CBD

12-month rent change

6%

Demand

Free rent (months)

7$

4.7%

95.3%

Share of PBS employment

$40

TI allowance ($ p.s.f.)Forecasted 12-month rent change

7%

Discount for B space

B 15%

Firm Address Deal type s.f.

Gardere McKinney & Olive Relocation 109,000

Jackson Walker KPMG Hall Arts Relocation 104,000

Hunton & Williams Fountain Place Renewal 88,000

Sidley Austin McKinney & Olive Relocation 75,000

Strasburger & Price Bank of America PlazaRelocation in building

65,000

Meadows Collier Bank of America Plaza Renewal 41,000

Law firm clock

Market Business Talent

Premium for Trophy space

20%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

26,700Legal services employment

+0 (+0.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Recent law firm leases

Established

Denver

18JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Growing demand from multiple industries continues to curtail

supply of large blocks of Trophy quality available space• Stringent credit requirements make competitive deal terms more

difficult to obtain for all but strong, national-credit firms• Owners, many pursuing capital improvement projects, are

raising asking rents given limited available options for users• Construction and labor expenditures continue to rise, driving up

the cost of space build-outs

Real estate opportunities for law firms

• A measure of relief greets tenants in the form of new construction set to deliver; seven CBD projects will add nearly 1.9 million square feet of space to the market within the next 10 quarters

• Sublease dispositions create additional options for users. At present, energy sector companies are sublessors to some 52 percent of CBD sublease space; law firms use similar space

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$34.60 $37.36$42.96

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

West CBD Midtown CBD LoDo

12-month rent change

14%

Demand

Free rent (months)

8$

5.6%

94.4%

Share of PBS employment

$55

TI allowance ($ p.s.f.)Forecasted 12-month rent change

4%

Discount for B space

B 18%

Firm Address Deal type s.f.

Hogan Lovells 1601 Wewatta Street Relocation 72,000

Moye White 16 Market Square Expansion 41,110

Otten Johnson U.S. Bank Tower Renewal 28,942

Burleson Wells Fargo Center Renewal 23,161

Morrison Foerster Republic Plaza Relocation 18,071

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

15%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

13,800Legal services employment

-400 (-2.8%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

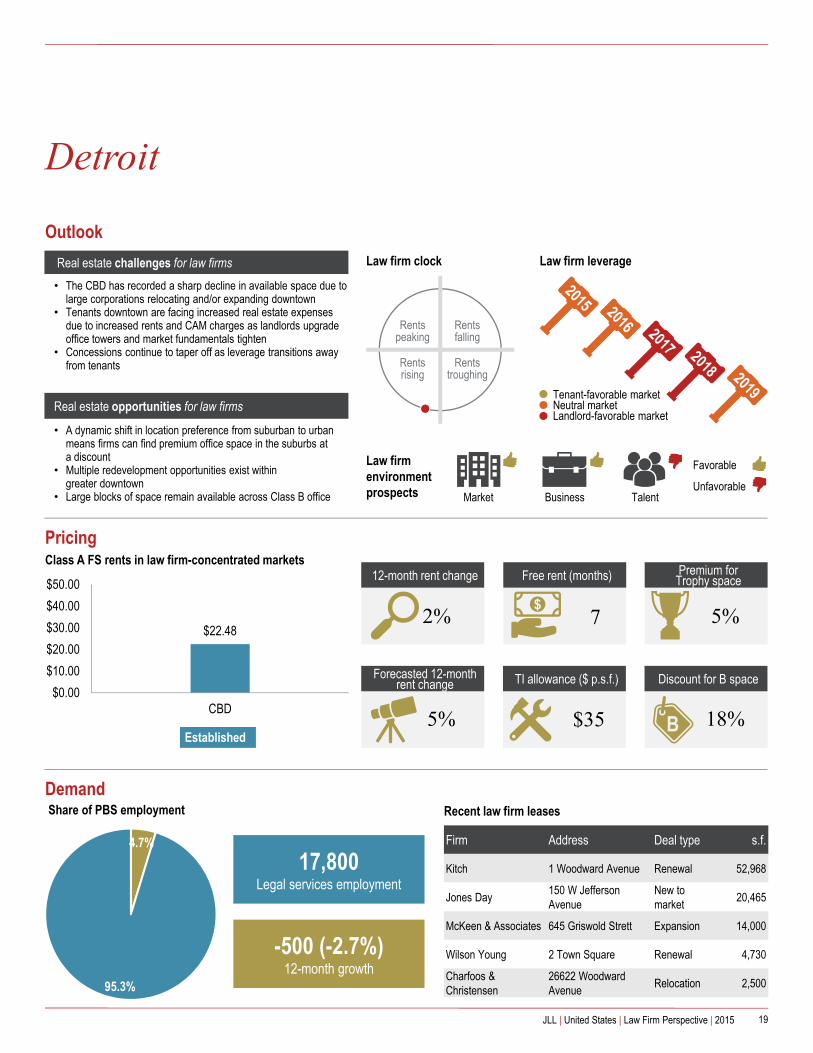

Detroit

19JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• The CBD has recorded a sharp decline in available space due to

large corporations relocating and/or expanding downtown• Tenants downtown are facing increased real estate expenses

due to increased rents and CAM charges as landlords upgrade office towers and market fundamentals tighten

• Concessions continue to taper off as leverage transitions away from tenants

Real estate opportunities for law firms

• A dynamic shift in location preference from suburban to urban means firms can find premium office space in the suburbs at a discount

• Multiple redevelopment opportunities exist within greater downtown

• Large blocks of space remain available across Class B office

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$22.48

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

CBD

12-month rent change

2%

Demand

Free rent (months)

7$

4.7%

95.3%

Share of PBS employment

$35

TI allowance ($ p.s.f.)Forecasted 12-month rent change

5%

Discount for B space

B 18%

Firm Address Deal type s.f.

Kitch 1 Woodward Avenue Renewal 52,968

Jones Day150 W Jefferson Avenue

New to market

20,465

McKeen & Associates 645 Griswold Strett Expansion 14,000

Wilson Young 2 Town Square Renewal 4,730

Charfoos & Christensen

26622 Woodward Avenue

Relocation 2,500

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

5%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

17,800Legal services employment

-500 (-2.7%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Fairfield County

20JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Attracting young talent to travel from New York City to

Greenwich and Stamford has been a challenge for law firms• Rents in Greenwich are comparable to New York City and firms

who choose to relocate there will find greater business challenges than New York City due to shortage of both talent and business prospects

Real estate opportunities for law firms

• Building and Land Technology recently purchased the former Pitney Bowes headquarters with the plan of repositioning the building for smaller tenants, which will add quality space to South Stamford

• Connecticut has made a 30-year, $100 billion commitment to long-term transportation upgrades, which will make commuting from New York City quicker and easier

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$45.80

$89.20

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

Stamford CBD Greenwich CBD

12-month rent change

-3%

Demand

Free rent (months)

6$

5.0%

95.0%

Share of PBS employment

$50

TI allowance ($ p.s.f.)Forecasted 12-month rent change

1%

Discount for B space

B 40%

Firm Address Deal type s.f.

Cummings and Lockwood

6 Landmark Square Relocation 55,643

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

N/A

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

3,600Legal services employment

+0 (+0.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Fort Lauderdale

21JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Landlords downtown have regained control and continue to drop

concessions for new tenants and those looking to renew• Law firms with large requirements are feeling the effects of a

tightening market as large blocks downtown and in the suburbs continue to diminish, especially within Class A properties

• As rates across the board continue to rise, downtown deals are being executed at rates above peak levels

Real estate opportunities for law firms

• Smaller law firms are beginning to take advantage of spec suites, which are increasingly being built by landlords

• While there are no large availabilities within the Trophy assets, if Two Financial can secure an anchor tenant, the development of a new downtown property would be ideal for law firms looking to enter, relocate or expand downtown

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$35.67

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Downtown

12-month rent change

7%

Demand

Free rent (months)

6$

10.5%

89.5%

Share of PBS employment

$35

TI allowance ($ p.s.f.)Forecasted 12-month rent change

6%

Discount for B space

B 21%

Firm Address Deal type s.f.

Greenberg Traurig401 E Las OlasBoulevard

Renewal 48,800

CSK Legal600 N Pine Island Road

Expansion 30,500

Kahane & Associates 8201 Peters Road Renewal 29,900

Shutts & Bowen200 E Broward Boulevard

Renewal 17,000

Lewis Brisbois 110 SE 6th Street Relocation 14,500

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

31%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

14,800Legal services employment

+200 (1.3%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Houston

22JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• The biggest challenge for law firms is to forecast their own

occupancy plans for the coming 5–10 years and timing the market, especially those with energy or mergers & acquisitions practice groups

• Despite slowing leasing activity and an uptick in availability –both on a direct and sublease basis – Trophy and Class A properties in the CBD are still well leased and leverage may not be tenant-favorable in the most sought-after addresses

Real estate opportunities for law firms

• With all forecasts pointing toward continued softening, 2016 will be an excellent time to lock in aggressive, long-term deals

• The vast amount of sublease space hitting the market is allowing firms to potentially occupy space at a steep discount

• Concessions in the form of tenant improvement allowances and free rent are becoming more commonplace

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$42.61$35.28

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

CBD Galleria

12-month rent change

1%

Demand

Free rent (months)

4$

5.3%

94.7%

Share of PBS employment

$45

TI allowance ($ p.s.f.)Forecasted 12-month rent change

-5%

Discount for B space

B 23%

Firm Address Deal type s.f.

Mayer BrownBank of America Center

Renewal 54,902

Johnson Law Group Kirby Grove Relocation 21,975

Shannon Martin 1001 McKinney Street Renewal 20,001

Coats Rose 9 Greenway Plaza Relocation 50,000

AZA LyondellBasell Tower New 34,864

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

18%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

25,100Legal services employment

+200 (+0.8%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

Indianapolis

23JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Availability has declined markedly within the urban core, which

firms increasingly desire for talent retention due to its mixed-use nature

• Strong investor sentiment for core properties will also boost rents higher as buyers seek to capitalize on above-market sales prices

• New construction has largely been limited to the suburbs and has not catered to law firms

Real estate opportunities for law firms

• Availability within lower floors of CBD office buildings remains high, providing tenants with greater flexibility

• Refurbishment and repositioning of office properties in lieu of new construction may give tenants more space options

• Tenants still have some negotiating power for greater concession packages, although these are eroding quickly

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$20.92 $21.23

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

CBD Keystone

12-month rent change

1%

Demand

Free rent (months)

8$

4.8%

95.2%

Share of PBS employment

$25

TI allowance ($ p.s.f.)Forecasted 12-month rent change

1%

Discount for B space

B 17%

Firm Address Deal type s.f.

Hall Render 500 N Meridian Street Relocation 105,000

Bingham Greenebaum Doll

Market Tower Renewal 80,000

Scopelitis Market Tower Renewal 36,000

Wooden & McLaughlin

Regions Tower Renewal 27,000

Woodard Emhart Chase Tower Renewal 20,000

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

22%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

7,700Legal services employment

+100 (+1.3%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Long Island

24JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Flight-to-quality in the office market has reduced the supply of

Trophy and Class A availabilities for expanding firms• High construction costs are driving law firm renewals rather than

relocations due to firms not wanting to allocate capital to move and build-out costs not covered by landlords

Real estate opportunities for law firms

• Access to major highways, mass transit and the courts will keep Garden City on the radar screen for law firms

• However, limited quality availabilities in Garden City may shift larger law firm requirements east to Jericho and Melville

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$31.83$27.40

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Nassau County Suffolk County

12-month rent change

0%

Demand

Free rent (months)

10$

11.0%

89.0%

Share of PBS employment

$30

TI allowance ($ p.s.f.)Forecasted 12-month rent change

1%

Discount for B space

B 17%

Firm Address Deal type s.f.

Ruskin MoscouFaltischek

1225 RXR Plaza Renewal 63,000

Farrell Fritz 1225 RXR PlazaRelocation in building

45,000

Meyer Suozzi English& Klein

990 Stewart Avenue Renewal 35,000

Jackson Lewis 58 S Service Road Renewal 28,000

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

N/A

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

19,100Legal services employment

+0 (+0.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Los Angeles

25JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Concentrated institutional ownership groups in Century City and

Downtown have successfully increased rents• Westside rents are nearing peak prerecession levels, forcing

some firms with pending expirations to consider options in more affordable submarkets

• Law firms seeking a presence in Los Angeles micromarketsdominated by creative and tech tenants will face sticker shock and more competition for quality space

Real estate opportunities for law firms

• Downtown’s burgeoning amenity base and residential options have become a selling point for recruiting new associates

• Large blocks of space in Trophy assets creates an opportunity for law firms seeking to trade up their image

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$52.45$42.09 $40.45

$60.25

$36.81

$0.00$20.00$40.00$60.00$80.00

$100.00

CenturyCity

Bunker Hill FinancialDistrict

SantaMonica

Marina DelRey/Culver

City

12-month rent change

9%

Demand

Free rent (months)

8$

7.9%

92.1%

Share of PBS employment

$48

TI allowance ($ p.s.f.)Forecasted 12-month rent change

6%

Discount for B space

B 10%

Firm Address Deal type s.f.

Lewis Brisbois 633 W 5th Street Renewal 215,230

Irell & Manella 1800 Avenue of the Stars Renewal 125,250

Manning & Kass 801 S Figueroa Street Renewal 80,328

Pillsbury 725 S Figueroa Street Renewal 61,000

Milbank 2029 Century Park E Relocation 56,527

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

22%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

49,800Legal services employment

+800 (+1.6%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

Miami

26JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• As building occupancies increase, premium spaces are

commanding higher rates. As rents continue to rise and rent abatement continues to diminish, law firms may have to weigh the benefits of locating in the CBD to the savings of relocating to more cost-effective submarkets

• Law firms touring the market have limited options as large blocks in the CBD diminish. View space in particular is becoming scarce within the urban core

Real estate opportunities for law firms

• Rates, at least for the foreseeable future, will continue to rise. Given this expectation, early renewals will be beneficial for firms with leases expiring in the next 24 months for long-term rent savings

• Tenants willing to tour spaces lacking views may have more negotiating power with lease terms

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$45.53 $41.54

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Brickell Downtown

12-month rent change

5%

Demand

Free rent (months)

2$

14.5%

85.5%

Share of PBS employment

$40

TI allowance ($ p.s.f.)Forecasted 12-month rent change

4%

Discount for B space

B 33%

Firm Address Deal type s.f.

Akerman Senterfitt 96 SE 7th Street Relocation 110,500

Stearns Weaver 150 W Flagler Street Renewal 103,000

Gray Robinson333 Avenue of Americas

Relocation 35,400

McDonald Hopkins200 S BiscayneBoulevard

Expansion 25,310

Hughes Hubbard201 S Biscayne Boulevard

Renewal 23,600

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

17%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

22,500Legal services employment

+500 (+2.3%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

27JLL | United States | Law Firm Perspective | 2015

Milwaukee

Real estate challenges for law firms• Lack of large block Class A availabilities• Rising construction costs are making it difficult for developers to

build new Class A product• With tightening market for Class A space, landlords are pushing

rents more aggressively

Real estate opportunities for law firms

• A new office development is under construction for the first time in more than 10 years, providing new Class A space that appeals to law firms

• There is also at least one more development in the pipeline so firms can expect conditions to soften as this space comes online

• Smaller firms and firms willing to consider Class B space still have options

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

12-month rent change

3%

Demand

Free rent (months)

5$

$35

TI allowance ($ p.s.f.)Forecasted 12-month rent change

2%

Discount for B space

B 20%

Premium for Trophy space

17%

Firm Address Deal type s.f.

Michael Best & Friedrich

100 E Wisconsin Renewal 89,725

The Previant Law Firm

310 W Wisconsin New 15,081

Whyte HirschboeckDudek

20800 SwensonDrive

New 12,921

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

$28.00$20.00 $16.00

$0.00$10.00$20.00$30.00$40.00$50.00

Downtown E ThirdWard/Walker's

Point

Downtown W

2.4%

97.6%

Share of PBS employment

7,400Legal services employment

+0 (+0.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Minneapolis

28JLL | United States | Law Firm Perspective | 2015

Rents peaking

Rents falling

Rents rising

Rents troughing

$36.00

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Minneapolis CBD

12-month rent change

13%

Demand

Free rent (months)

5$

4.9%

95.1%

Share of PBS employment

$50

TI allowance ($ p.s.f.)Forecasted 12-month rent change

2%

Discount for B space

B 24%

Premium for Trophy space

19%

Firm Address Deal type s.f.

Meagher & Geer 33 S 6th StreetExpansion in building

51,000

Fish & Richardson 60 S 6th StreetRenewal & expansion

100,000

Best & Flanagan 60 S 6th Street Renewal 28,000

Nichols Kaster 80 S 8th Street Relocation 23,560

Lindquist & Vennum 80 S 8th Street Renewal 85,000

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

Real estate challenges for law firms• Rental rates have increased significantly over the past

18 months• Pressure from clients to reduce rates means that firms have less

to spend on real estate and thus firms are looking at alternative locations to traditional Class A buildings

Real estate opportunities for law firms

• Some firms are finding solutions to these constraints by considering Class A space instead of Trophy space

• Firms are also moving back-office operations to less expensive nodes of the market

Outlook

15,300Legal services employment

-100 (-0.6%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

New Jersey

29JLL | United States | Law Firm Perspective | 2015

Real estate challenges for law firms• Aging suburban inventory base with more than one-half of the

office market developed during the 1980s leaves firms with many inefficient options

• Younger associates’ preference for locations in CBD markets and not suburban markets challenge recruiting efforts

• High build-out costs for second generation space

Real estate opportunities for law firms

• New Jersey’s use of economic incentive programs to retain and attract new corporate investments

• Consolidation and restructuring by other sectors are adding availabilities to the market

• Rental rate appreciation is being restrained by transitional office market conditions

Outlook

Rents peaking

Rents falling

Rents rising

Rents troughing

$32.80 $30.71$24.82

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Newark Route 24 Route 280Corridor

12-month rent change

-2%

Demand

Free rent (months)

12$

6.9%

93.1%

Share of PBS employment

$45

TI allowance ($ p.s.f.)Forecasted 12-month rent change

1%

Discount for B space

B 41%

Firm Address Deal type s.f.

Riker Danzig 1 Speedwell Avenue Renewal 110,000

Chiesa Shahinian & Giantomasi

1 Boland DriveRenewal/expansion

95,000

Sills Cummis 1 Riverfront Plaza Renewal 73,000

Greenberg Traurig 500 Campus Drive Relocation 47,000

Eckert Seamans 2000 Lenox Drive Relocation 25,000

Recent law firm leases

Law firm clock

Market Business Talent

Premium for Trophy space

7%

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverage

38,500Legal services employment

-400 (-1.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

New York

30JLL | United States | Law Firm Perspective | 2015

Rents peaking

Rents falling

Rents rising

Rents troughing

$88.54 $79.13$67.47

$85-$100

$0.00$20.00$40.00$60.00$80.00

$100.00

PlazaDistrict

TimesSquare

GrandCentral

HudsonYards

12-month rent change

5%

Demand

Free rent (months)

9$

11.4%

88.6%

Share of PBS employment

$70

TI allowance ($ p.s.f.)Forecasted 12-month rent change

3%

Discount for B space

B 28%

Premium for Trophy space

11%

Firm Address Deal type s.f.

Skadden 1 Manhattan West Relocation 535,000

Norton Rose Fulbright

1301 Avenue of the Americas

Relocation 135,000

Curtis Mallet 101 Park Avenue Renewal 91,482

Boies Schiller 55 Hudson Yards Relocation 81,835

Morgan Lewis 101 Park AvenueExpansion in building

75,000

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

Real estate challenges for law firms• Most existing law offices are inefficient and not built to support

current law firm requirements• Short-term renovations to improve efficiency are out of favor due

to rising construction costs, short amortization periods and the disruption caused by in-place renovations

• Limited large-block availability both in the market and contiguous within properties may create challenges for expanding firms

Real estate opportunities for law firms• If a firm can free up surplus space, there is a ready market for

short-term built law firm premises• Significant amounts of second-generation law firm space will be

coming to market, much of which, while not as efficient as newly built space, can be adapted with much lower out-of-pocket firm capital

• New developments at the Hudson Yards and the World Trade Center offer modern, efficient space at competitive pricing

Outlook

79,300Legal services employment

+700 (+0.9%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

Oakland

31JLL | United States | Law Firm Perspective | 2015

Rents peaking

Rents falling

Rents rising

Rents troughing

$39.84

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

CBD

12-month rent change

13%

Demand

Free rent (months)

2$

3.3%

96.7%

Share of PBS employment

$25

TI allowance ($ p.s.f.)Forecasted 12-month rent change

18%

Discount for B space

B 17%

Premium for Trophy space

n/a

Firm Address Deal type s.f.

Barney & Barney1340 Treat Boulevard

Relocation 14,235

Lewis Feinberg 1333 Broadway Relocation 12,013

Foran Glennon 2000 Powell Street Renewal 10,342

Yaron & Associates 1300 Clay Street Relocation 6,081

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

Law firm leverageReal estate challenges for law firms• Law firms represent a small portion of the tenant base in

the CBD • Downtown revitalization and east-bound migration have further

diversified the tenant market, and heightened demand has resulted in a spike in rental rates for both Class A and B space

• Cost-conscious law firms are consolidating or renewing in place, or considering other options outside of the desirable CBD

Real estate opportunities for law firms

• Law firms are demanding an open space office layout, creating the opportunity to update old, historical space

• Law firms are looking to East Bay suburban markets where rental rates for desirable Class A space are lower and similar amenities are available including transportation

Outlook

6,100Legal services employment

-400 (-6.2%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

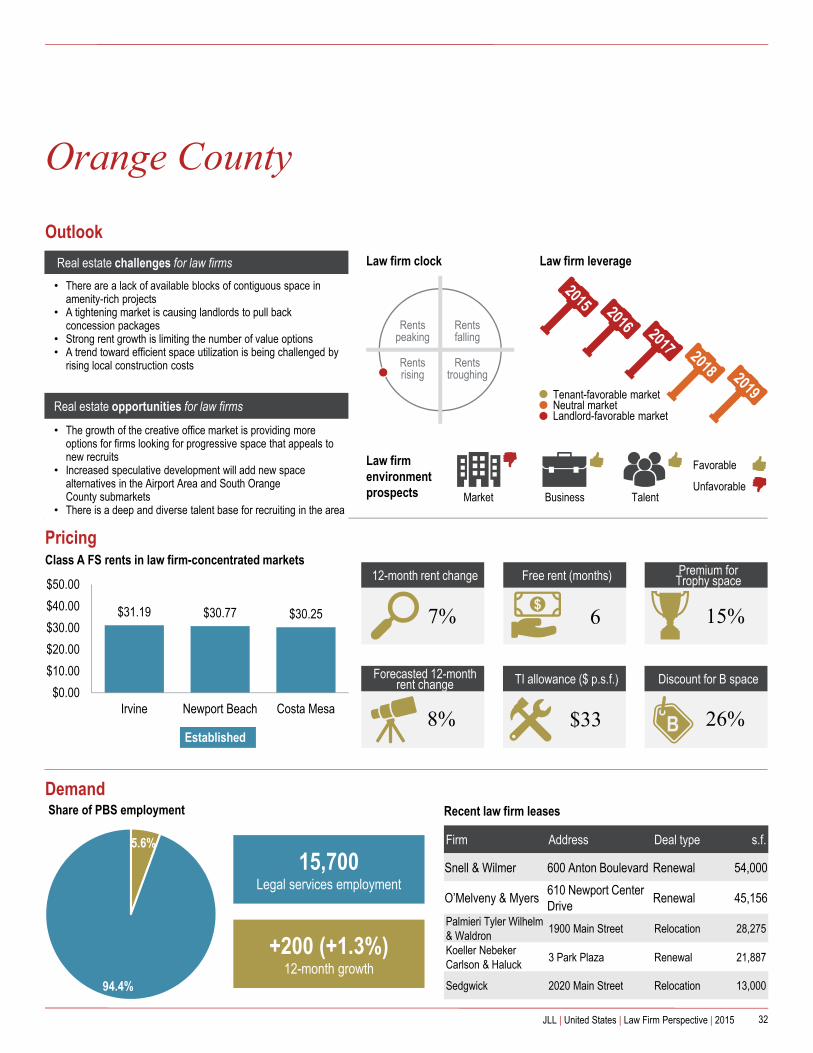

Orange County

32JLL | United States | Law Firm Perspective | 2015

Rents peaking

Rents falling

Rents rising

Rents troughing

12-month rent change

7%

Demand

Free rent (months)

6$

5.6%

94.4%

Share of PBS employment

$33

TI allowance ($ p.s.f.)Forecasted 12-month rent change

8%

Discount for B space

B 26%

Premium for Trophy space

15%

Firm Address Deal type s.f.

Snell & Wilmer 600 Anton Boulevard Renewal 54,000

O’Melveny & Myers 610 Newport Center Drive

Renewal 45,156

Palmieri Tyler Wilhelm & Waldron

1900 Main Street Relocation 28,275

Koeller NebekerCarlson & Haluck

3 Park Plaza Renewal 21,887

Sedgwick 2020 Main Street Relocation 13,000

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

$31.19 $30.77 $30.25

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Irvine Newport Beach Costa Mesa

Real estate challenges for law firms• There are a lack of available blocks of contiguous space in

amenity-rich projects• A tightening market is causing landlords to pull back

concession packages• Strong rent growth is limiting the number of value options• A trend toward efficient space utilization is being challenged by

rising local construction costs

Real estate opportunities for law firms

• The growth of the creative office market is providing more options for firms looking for progressive space that appeals to new recruits

• Increased speculative development will add new space alternatives in the Airport Area and South Orange County submarkets

• There is a deep and diverse talent base for recruiting in the area

Outlook

15,700Legal services employment

+200 (+1.3%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

33JLL | United States | Law Firm Perspective | 2015

Philadelphia

Rents peaking

Rents falling

Rents rising

Rents troughing

$28.73

$40.73

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Market Street West University City

12-month rent change

3%

Demand

Free rent (months)

6$

8.4%

91.6%

Share of PBS employment

$45

TI allowance ($ p.s.f.)Forecasted 12-month rent change

3%

Discount for B space

B 19%

Premium for Trophy space

23%

Firm Address Deal type s.f.

Stradley Ronon 1 Commerce Square Relocation 92,000

Rawle & Henderson 1 S Penn Square Renewal 69,420

Schnader Harrison 1600 Market Street Renewal 67,000

Pond Lehocky 1 Commerce Square Relocation 58,000

Hangley Aronchick One Logan Square Renewal 41,529

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

Real estate challenges for law firms• Limited availability of quality Trophy blocks, vacancy rates at all-

time lows, and continuing conversions of Class B office space have resulted in rising rental rates and stiff competition for law firms seeking space in Center City’s premier office towers

• Ongoing landlord confidence has put continued downward pressure on concessions

Real estate opportunities for law firms

• Delivery of nearly 300,000 square feet of speculative Trophy space and two large blocks coming online at 1735 Market Street will ease strong landlord leverage between 2016 and 2017

• Center City has the strongest millennial growth rate of any major U.S. city, making it easy for firms to attract young talent

• The resurgence of Market East is making the submarket newly attractive to value-conscious law firms

Outlook

38,300Legal services employment

-700 (-1.8%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

Phoenix

34JLL | United States | Law Firm Perspective | 2015

Rents peaking

Rents falling

Rents rising

Rents troughing

$27.51$22.69

$30.08

$0.00$10.00$20.00$30.00$40.00$50.00

Downtown Midtown CamelbackCorridor

12-month rent change

6%

Demand

Free rent (months)

6$

4.1%

95.9%

Share of PBS employment

$20

TI allowance ($ p.s.f.)Forecasted 12-month rent change

5%

Discount for B space

B 20%

Premium for Trophy space

9%

Firm Address Deal type s.f.

Jones Skelton & Hochuli

40 N Central Avenue Relocation 60,000

Wilkes & McHugh2355 E Camelback Road

Renewal 6,557

Morrill & Aronson 1 E Camelback Road Renewal 6,400

Russell A. Brown3838 N Central Avenue

Renewal 5,034

Holden Willits 2 N Central Avenue Relocation 3,680

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

Real estate challenges for law firms• Availability of Class A space is shrinking• Rental rates in law firm-concentrated markets are escalating,

with several markets approaching prerecession levels• There is a limited availability of high-quality space with premium

views preferred by law firms

Real estate opportunities for law firms

• An active development pipeline will provide new Class A availabilities over the next 18 months

• Availabilities for small-sized law firms (less than 10,000 square feet) remain abundant

Outlook

13,600Legal services employment

+400 (+3.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established Emerging

Pittsburgh

35JLL | United States | Law Firm Perspective | 2015

Rents peaking

Rents falling

Rents rising

Rents troughing

$27.98

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

CBD

12-month rent change

2%

Demand

Free rent (months)

3$

7.2%

92.8%

Share of PBS employment

$35

TI allowance ($ p.s.f.)Forecasted 12-month rent change

1%

Discount for B space

B 20%

Premium for Trophy space

10%

Firm Address Deal type s.f.

Eckert Seamans 600 Grant Street Renewal 120,000

Burns White 3 Crossings Relocation 105,000

Fox Rothschild 500 Grant Street Relocation 22,000

Swartz Campbell 436 Seventh Avenue Relocation 20,000

Robb Leonard Mulvihill

500 Grant Street Renewal 16,000

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

Real estate challenges for law firms• Trophy space remains at near-full occupancy levels, limiting

options for tenants looking to upgrade offices• Concessions are at cyclical lows requiring tenants to make

significant outlays related to build-out costs when relocating• While several large-scale projects have been proposed in the

CBD, only one multi-tenant office building, Tower Two-Sixty, is under construction, limiting options for tenants

Real estate opportunities for law firms

• Several corporate tenants have announced rightsizings in the last 18 months, which has created a number of large blocks

• Demand fluctuations have dampened the prospects of rent growth over the next year, providing tenants an opportunity to renew or extend leases at non-peak rates

• Tenants have regained some leverage, particularly in Class B space, and may find landlords more flexible on terms

Outlook

13,500Legal services employment

+1,000 (+8.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

Portland

36JLL | United States | Law Firm Perspective | 2015

Rents peaking

Rents falling

Rents rising

Rents troughing

12-month rent change

3%

Demand

Free rent (months)

4$

4.6%

95.4%

Share of PBS employment

$55

TI allowance ($ p.s.f.)Forecasted 12-month rent change

4%

Discount for B space

B 5%

Premium for Trophy space

21%

Firm Address Deal type s.f.

Troutman Sanders 100 SW Main Street Relocation 16,478

Greene Markley 1515 Market Square Relocation 14,095

Stewart Sokol & Larkin 2300 SW 1st Avenue Renewal 13,949

Sather Byerly & Holloway

111 SW 5th Avenue Renewal 13,704

Reinisch Wilson Weier10260 SW Greenburg Road

Renewal 12,848

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

$30.03

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

CBD

Real estate challenges for law firms

• Rapidly-rising rents mean value-conscious law firms, whose leases were negotiated during the height of the recession, are facing significantly higher base rents

• Law firms are competing against tenants with better credit and quicker decision-making capability

• Local and regional firms will be challenged to find options where partners do not have to fund tenant improvements

Real estate opportunities for law firms

• A supply of commodity and traditional space is still available• New construction will soon be hitting the Portland market,

yielding more options, but at a rent premium• Spaces in the 5,000-15,000-square-foot range are still plentiful

and allow for decent leverage for tenants on TIs and free rent

Outlook

8,100Legal services employment

-300 (-3.6%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Established

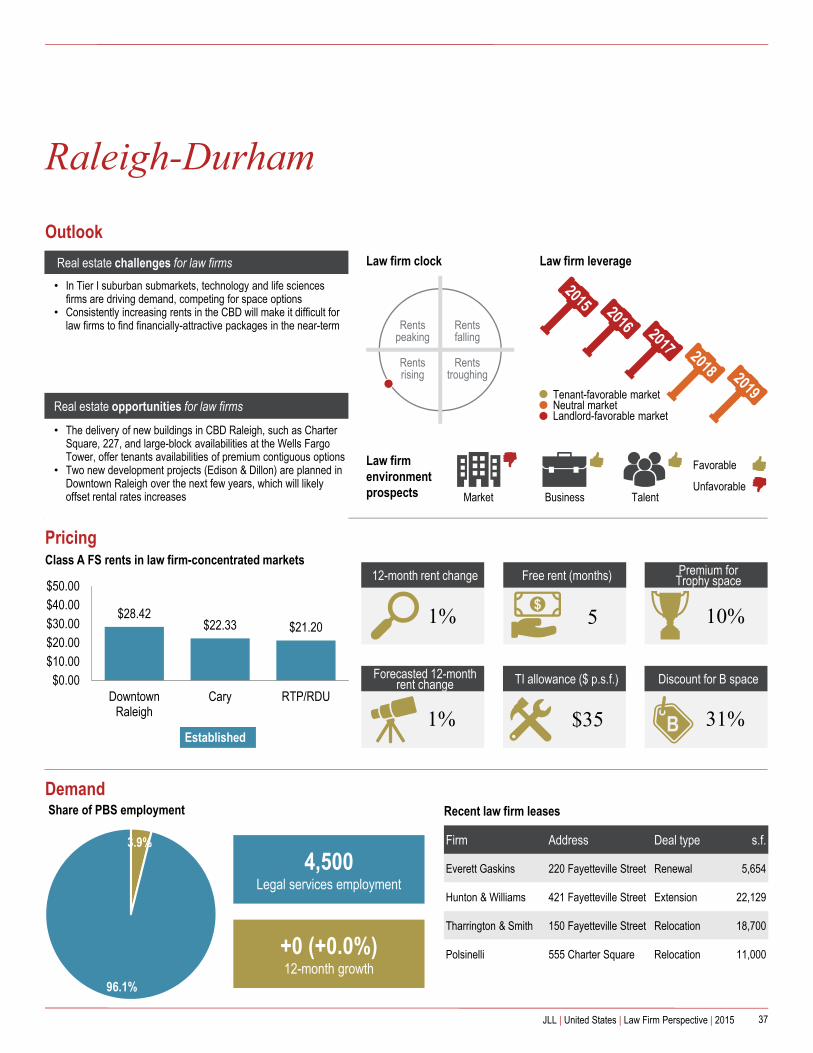

Raleigh-Durham

37JLL | United States | Law Firm Perspective | 2015

Rents peaking

Rents falling

Rents rising

Rents troughing

$28.42$22.33 $21.20

$0.00$10.00$20.00$30.00$40.00$50.00

DowntownRaleigh

Cary RTP/RDU

12-month rent change

1%

Demand

Free rent (months)

5$

3.9%

96.1%

Share of PBS employment

$35

TI allowance ($ p.s.f.)Forecasted 12-month rent change

1%

Discount for B space

B 31%

Premium for Trophy space

10%

Recent law firm leases

Law firm leverageLaw firm clock

Market Business Talent

Tenant-favorable marketNeutral marketLandlord-favorable market

Real estate challenges for law firms• In Tier I suburban submarkets, technology and life sciences

firms are driving demand, competing for space options• Consistently increasing rents in the CBD will make it difficult for

law firms to find financially-attractive packages in the near-term

Real estate opportunities for law firms

• The delivery of new buildings in CBD Raleigh, such as Charter Square, 227, and large-block availabilities at the Wells Fargo Tower, offer tenants availabilities of premium contiguous options

• Two new development projects (Edison & Dillon) are planned in Downtown Raleigh over the next few years, which will likely offset rental rates increases

Outlook

4,500Legal services employment

+0 (+0.0%)12-month growth

Law firm environment prospects

PricingClass A FS rents in law firm-concentrated markets

Favorable

Unfavorable

Firm Address Deal type s.f.

Everett Gaskins 220 Fayetteville Street Renewal 5,654

Hunton & Williams 421 Fayetteville Street Extension 22,129

Tharrington & Smith 150 Fayetteville Street Relocation 18,700