laurent freixe nestlé europe ceo - nestlé global · nestlé in europe . 5 our passion for...

TRANSCRIPT

1

Laurent Freixe

Nestlé Europe CEO

Brussels, 9th May 2012

2 2

Disclaimer This presentation contains forward looking statements

which reflect Management’s current views and

estimates. The forward looking statements involve

certain risks and uncertainties that could cause actual

results to differ materially from those contained in the

forward looking statements. Potential risks and

uncertainties include such factors as general economic

conditions, foreign exchange fluctuations, competitive

product and pricing pressures and regulatory

developments.

3

Our mission, Our Objective:

Consumers to trust Nestlé to always offer

the tastiest and healthiest choices

4

€ 21.5 billion in sales in 2011

95 000 employees

88 factories in 19 countries

Brands and Products for every age, every

occasion

215 000 Customers

Nestlé in Europe

5

Our passion for

Consumers

Shoppers is at

the heart of all

what we do,

everyday

6

our passion for

our Customers is at

the heart of our

engagement and

commitment to

collaboration,

everyday, everywhere

7

SHOPPER &

CATEGORY

CUSTOMER

RELATIONSHIPS

EXCELLING IN

EXECUTION

CUSTOMER FACING

SUPPLY CHAIN

A Global Initiative with Local

Implementations

8

Nestlé Shopper Insight Centres

Setting the stage for engagement and collaboration

9

Customer Strategy

Trade & Industry Best Practices &

Standards

Nestlé Strategy

...for a sustainable

collaboration

The power of alignment....

10

Our engagement with Industry & Trade Organisations

to drive collaboration along the value chain

Global

Regional

Local

The Consumer Goods Forum

GS1

Industry & Trade Collaborative Platforms (ECR Europe, ECR Asia Pacific, etc.)

Manufacturer Associations (GMA, AIM, FoodDrink Europe, FCPC, FIA, etc)

Industry & Trade Collaborative Platforms (ECR Nationals)

Manufacturer Associations

11

Foundations

Advanced practices

Innovative practices

12

Challenging

times may

slow down

efforts for

collaboration and

implementation

A New Reality

13

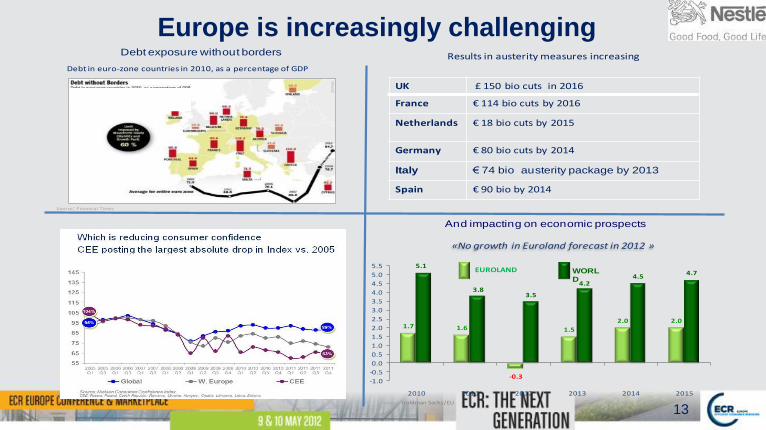

Europe is increasingly challenging

And impacting on economic prospects

«No growth in Euroland forecast in 2012 »

Source: EU

Source: Goldman Sachs/EU

1.7 1.6

-0.3

1.5

2.0 2.0

5.1

3.83.5

4.24.5

4.7

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2010 2011 2012 2013 2014 2015

EUROLAND WORLD

Debt exposure without borders

Debt in euro-zone countries in 2010, as a percentage of GDP

Source: Financial Times

Results in austerity measures increasing

UK £ 150 bio cuts in 2016

France € 114 bio cuts by 2016

Netherlands € 18 bio cuts by 2015

Germany € 80 bio cuts by 2014

Italy € 74 bio austerity package by 2013

Spain € 90 bio by 2014

14

Understanding the needs and consequences

of ageing populations

15

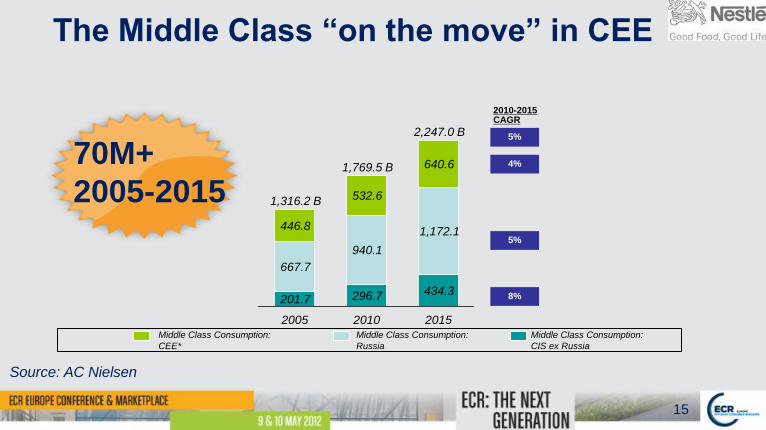

The Middle Class “on the move” in CEE

Middle Class Consumption:

CIS ex Russia

Middle Class Consumption:

Russia

Middle Class Consumption:

CEE*

2015

2,247.0 B

434.3

1,172.1

640.6

2010

1,769.5 B

296.7

940.1

532.6

2005

1,316.2 B

201.7

667.7

446.8

2010-2015 CAGR

5%

5%

4%

8%

70M+

2005-2015

Source: AC Nielsen

16

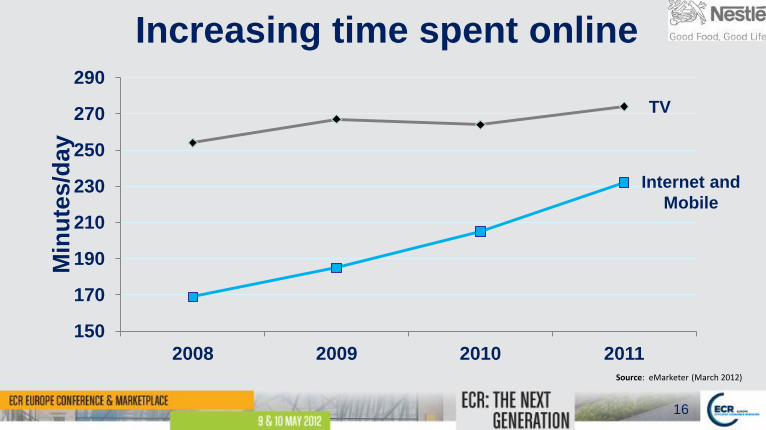

Increasing time spent online

150

170

190

210

230

250

270

290

2008 2009 2010 2011

Min

ute

s/d

ay

Source: eMarketer (March 2012)

TV

Internet and

Mobile

17

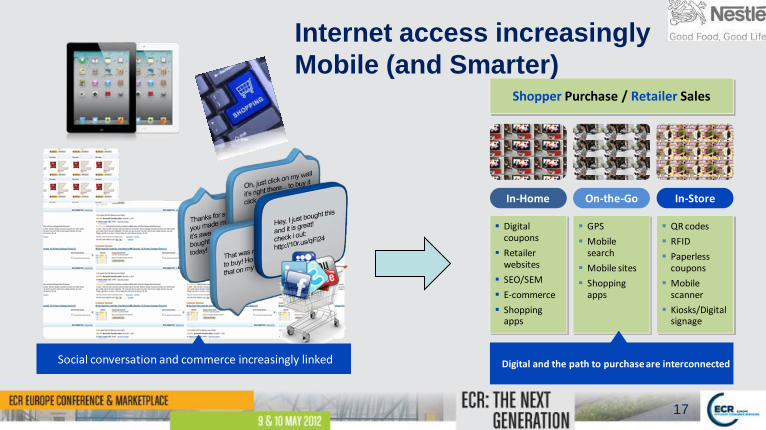

Social conversation and commerce increasingly linked Digital and the path to purchase are interconnected

Digital coupons

Retailer websites

SEO/SEM

E-commerce

Shopping apps

GPS

Mobile search

Mobile sites

Shopping apps

QR codes

RFID

Paperless coupons

Mobile scanner

Kiosks/Digital signage

In-Home On-the-Go In-Store

Shopper Purchase / Retailer Sales

Internet access increasingly

Mobile (and Smarter)

18

Consumer Online Purchase is booming

Note: Numbers in Billions USD, Source: Forrester (2011)

E-commerce

sales growing by

more than 19% a

year and will be

almost $1.4

trillion by 2015

19

New Realities,

New Opportunities

20

Capitalising the

Knowhow to excel

in execution

Adapting

shopper

solutions

Innovating

Focus collaboration on value creation and

waste elimination along the supply chain

21

Products Systems Services

Standardised

Customized Solutions

Innovation is a game changer

Addressing

increasingly

complex

consumer

needs

22

Collaboration is a game changer

Step 5

Monitor &

adapt

Step 1

Review the economic and

shopper environment

Conditions

for success

Step 3

Define and

agree 3-year

JAG plan

Step 4

Execute the

JAG plan

Step 2

Review

performance

and agree

growth

strategy

Step 3

Define and

agree 3-year

JAG plan

Jointly Agreed Growth (JAG)

A Pragmatic Approach

for Developing and

Implementing Jointly

Agreed Growth Plans

A

Framework

– Approach focused on Shopper Value

– 3 year + joint category development plan

– Data sharing

– Demand & Supply

– In-store execution

– On-Shelf Availability: service to the shopper

– Monitoring / Joint KPIs

– Joint investment plans

Successfully

implemented with

23

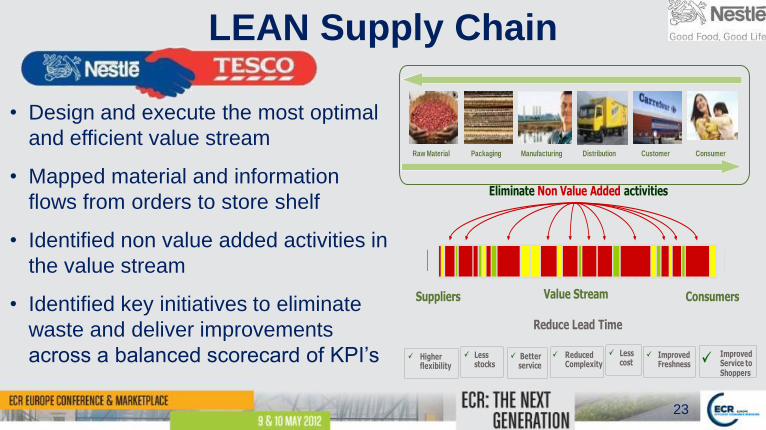

LEAN Supply Chain

Value Stream ConsumersSuppliers

Reduce Lead Time

Eliminate Non Value Added activities

Better service

Less stocks

Less cost

Higher

flexibility

ImprovedFreshness

Reduced Complexity

ImprovedService to Shoppers

Distribution CustomerPackagingRaw Material Manufacturing Consumer

• Design and execute the most optimal

and efficient value stream

• Mapped material and information

flows from orders to store shelf

• Identified non value added activities in

the value stream

• Identified key initiatives to eliminate

waste and deliver improvements

across a balanced scorecard of KPI’s

24

Sustainable Supply Chain • Reducing the overall environmental footprint

– Transport

– Packaging

– Warehousing

– Etc.

• Example of Sustainable Packaging

– Leverage The Consumer Goods Forum work

in Europe

– One language for common understanding

and metrics

– “Reconcile” the requirements for Shelf Ready

Packaging and Sustainable Packaging

25

Open

perspectives

for the future

26

Manufacturers and Retailers collaborating…

EU 2020 agenda

•Single Market

•Digital Market

•Innovation to boost

consumption and recover

growth

•Green and inclusive

growth

Trade & Industry Agenda

• Accelerating implementation

of existing best practices

• Product & service Innovation

• Health & Wellness /Ageing

Populations

•Environmental Sustainability

27

Thank You