latin american update, no. 1 – february, 2009 · pdf filelatin american update, no. 1...

TRANSCRIPT

Latin American Update, No. 1 – February, 2009

“Whilst every care has been taken in preparing this document, no respons ibility or liability is accepted as to the correctness and/or the accuracy of the information contained herein. Any views expressed regarding future conditions must not be regarded as promises or guarantees . All opinions and estimates contained in this report may be changed after publication at any time without notice. No liability is accepted whatsoever for any direct or consequential loss arising from the use of this document.”

Arne-Christian [email protected]+ 47 55 21 19 53

Karen Kosberg [email protected]+ 47 22 94 46 59

Tom Mario [email protected]+ 55 21 22 85 17 95

Lars [email protected]+ 47 55 21 18 11

Marcela Hernández M.Chile [email protected]+ 562 9230100

Latin American DeskIf you need fi nancial advice or services related to your business in Latin America, please contact DnB NOR’s Latin American desk by e-mail or telephone and we will do our best to assist you. If you wish to subscribe to this free bi-monthly newsletter, please contact us at [email protected].

Brazil – Ambitious Petrobras Investment Plan for 2009–2013 2

Chile – Fiscal stimulus package totalling US$ 4 bn designed to protect growth and employment in 2009 4

Mexico – Sharp deterioration in the economy 5

Peru – Well-prepared to face the financial crisis according to S&P 6

Argentina – Luck is up, but bad policies continue 7

Colombia – Unclear if President Uribe is allowed to run for re-election 8

Venezuela – Mr Chávez wins national referendum 9

Content

Brazil

Politics: According to President Lula, the Brazilian economy will not manage in 2009 to post the strong economic performance of 2008. He affirms that Brazil will grow less, but will not enter into a recession. He is boosting public investments via PAC – the public growth acceleration program. It is evident that the global crisis has reached Brazil, and a more negative public sentiment on the development of the economy, lower sales and economic activity, increasing unemployment, etc., are daily news in the Brazilian press. Increased international trade protectionism from the developed countries is also a concern of President Lula.

At the beginning of February Senator Jose Sarney and Representative Michel Temer, both from the PMDB party, a centre left and the largest political party in Brazil, were respectively elected President of the Senate and President of the House of Representatives. Both have held these positions before, and Sarney has formerly been President of Brazil. These two important positions which determine much of the Congress legislative work and priorities during the next 2 years, will certainly help to position PMDB, either to the left or to the right in the upcoming 2010 presidential elections. It seems as if Chief of Staff Dilma Rousseff who has been brought forth by President Lula might become the PT Presidential candidate. As to the PSDB party of former President Fernando Henrique Cardoso, they still have to decide on either Governor of Sao Paulo Jose Serra or Governor of Minas Gerais, Aecio Neves.

Many in Brazil question today where the political opposition is. They have not been seen or heard during the last years. President Lula continues posting record high approval ratings.

In an interview granted to Veja Magazine, the respected Senator Jarbas Vasconcellos, a founder and member of PMDB party criticized his own party and its politicians with corruption allegations and characterizing the election of Sarney as President of the Senate as a complete regression. The PT party was also criticized, as well as the government of President Lula.

Economics: Despite a weaker 4th quarter in 2008, perspectives for GDP growth in 2008 remain at 5%. For 2009 according to Focus report in mid February, compiled by Banco Central, average GDP growth estimate for 2009 is becoming lower, now at 1.5%. There are however some economists from leading banks estimating a negative performance of GDP in Brazil in 2009. The slump in the industry is considered to be the worst since 1991.

The government continues to be pro-active as to several pre-emptive anti-cyclical measures to avoid worsening of the current crisis. They have cut some taxes and reduced the SELIC rate in January and will continue doing so throughout their bi- monthly meetings this year.

So far, the large Brazilian banks have not been affected by the financial crisis. Real estate financing has been negligible in Brazil approx. 3% of total credit due to high domestic interest rates and investment banking activities. The banks who have posted 2008 results are profitable, but with lower profits than 2007.

The Real ended January at BRL 2.32 per USD, virtually unaltered from the end of November and December. Mid February the Real / USD quote is the same. There has however been strong volatility in the currency markets influenced by both domestic and international developments.

The performance of monthly inflation figures in Brazil ectations is the SELIC basis interest rate. In the past inflation has been the main priority of the government of President Lula. With the reduction in economic activity taking place globally and in Brazil, there seems to have been in a shift in priority granting more importance in sustaining economic activity than following inflation target and performance. In January Banco Central cut the SELIC rate by 1% to 12.75% – the first reduction in 16 months and the largest reduction in 5 years. It is expected that in the next Banco Central SELIC meeting on March 10–11, this interest rate will be cut by further 1%, despite slightly higher January IPCA figure.

The IPCA index for January came out at 0.48% in relation to 0.28% in December. Expectations for this index in February are that it may remain at approx. the same monthly figure.

Foreign trade performance is deteriorating due to higher imports and lower exports. The trade balance for January posted a deficit of USD 518 million, resulting from exports of USD 9.8 billion and imports of USD 10.3 billion. The fall in exports in relation to previous month was 29%, which is the largest drop ever. The trade deficit was the first negative monthly figure in 8 years. Current account figure ended 2008 at a deficit of USD 22.7 billion. Foreign direct

2

investments in 2008 compensated the current account deficit, posting a record figure of USD 45.1 billion. Currency reserves were by the end of January at USD 200.8 billion. The total external debt of both public and private sectors was at end of November estimated at USD 200.2 billion. Brazil is maintaining its currency reserves in relation to other BRIC and developing countries.

The public fiscal accounts reached its targets, whereby the ex-interest consolidated public sector budget surplus target for 2008 was 3.8% of GDP. The result for 2008 was a surplus of 4.5%.

Unemployment figures are increasing and according to IBGE ended at 7.8% for 2008. Record high firings took place during December reported at 655,000 employees loosing their jobs.

Finance:The stocks market remains volatile, but with slight positive trend. The IBOVESPA stock market index in USD closed at the end January posting a gain of 5.6% in relation to the previous month and in December a small gain of 2.4% in relation to November. In mid February the Brazilian stock market is taking a big hit.

Bond prices have slightly increased during the last month. The BR 40 bond posted at the end of January a spread of 394 basis points over US Treasury bills and has a falling trend. The JP Morgan risk index EMBI+ Brazil was mid February at 379 basis points.

Business:BNDES the Brazilian National Development Bank, the main source for medium and long term investments in Brazil is almost doubling its lending budget for 2009 to BRL 166 billion with more funding provided by the Treasury. In 2008 it disbursed BRL 93 billion in loans. Part of the funds available for lending in 2009 will be targeted to Petrobras.

The Votorantim Group, the largest private industrial conglomerate in Brazil has been active selling and buying assets. It sold off half of its bank operations in Banco Votorantim to Banco do Brasil for BRL 4.2 billion. Especially attractive for Banco do Brasil is the leading position in car financing in Brazil. It further sold assets in the electrical sector in the CPFL company to Camargo Correa for BRL 2.7 billion. On the acquisition side it increased its stake in Aracruz to control and thereafter merge the company with VCP. This acquisition came out at BRL 5.4 billion and had the participation of BNDES.

Forecasts:The Focus Report posted by Banco Central at the middle of February, based on survey among economists from 100 Brazilian banks, came out with the following forecasts: IPCA inflation index for 2009 at 4.69% and for 2010 4.5%. Exchange rate at end of 2009 estimated at BRL 2.30 per USD and at end of 2010 at BRL 2.28 per USD. GDP growth set for 2009 at 1.5% and for 2010 at 3.6%. The trade surplus for 2009 is estimated at USD 14 billion and in 2010 at 13.85 billion. Foreign direct investment is expected to

reach in 2009 USD 23 billion and in 2010 USD 25 billion. The current account is expected to post a deficit in 2009 at USD 25 billion and in 2010 a deficit of USD 27 billion. The Selic benchmark interest rate is expected to end 2009 at 10.5% p.a. and at end 2010 also at 10.5%. The net public debt to GDP ratio is estimated to reach by end 2009 level of 36.2% and at end 2010 at 36.25%.

As to economic activity, first semester 2009 will be marked by difficulties, reductions and volatility. A possible recovery can only be expected for second semester 2009.

Story of the month: Petobras has announced ambitious investment plan Petobras announced in January its ambitious investment plan for 2009–2013. The figure announced for the coming 5 years investments was USD 174 billion. In this amount the development of pre-salt fields are envisaged and targets of production for 3.7 million of barrels per day of oil equivalent are set for 2013 and a corresponding target of 5.7 million for 2020. The financing of this ambitious plan will certainly be a challenge, but according to announcements by the company, the 2009 financing needs are under control as well as most of the budgeted amount for 2010. BNDES will participate in a large portion of the financing requirements, something not common in the past. There are not only financial but also technical, logistical, etc challenges to be met. However, the sentiment for the oil and gas sector remains very positive and both foreign and domestic companies are positioning themselves to supply Petrobras with equipment and technology to fulfil their ambitious plans. There are and will be many interesting business opportunities both domestically and internationally for equipment suppliers, and companies working within the shipping and oil & gas sectors targeting Brazil and Petrobras.

3

Chile

Politics:After having seen her popularity dip to as low as 35% in the second year of her term, Ms. Bachelet now enjoys a 51% approval rating according to a December poll (Adimark). Her revived popularity should, in theory, lift the chances of the likely Concertación candidate, former President Eduardo Frei (1994–2000). However, Mr. Frei trails Mr. Piñera in opinion polls with a 27% rating against Mr. Piñera’s 52%.

Economics: As a small and open economy, Chile is feeling the effects of the global recession and declining commodity prices. However, Chile is in a stronger position than most other countries in Latin America and also in other regions. Thanks to its strong public sector financial position it is able to implement policies to cope with the downturn.

Although Chile has an excellent record of diversifying its export markets through its network of free trade agreements, the synchronized nature of the downturn will mean that this diversification will not provide the protection that it did during the last global downturn, when growing US demand offset falls in Asia. Demand growth in Chile’s main markets is set to fall sharply or remain low in 2009.

Global growth prospects for 2009 showed a severe downshift, to figures not seen in decades. The annual pace of economic growth slowed to 1.1% in the fourth quarter from 4.8%. Economists in Central Bank polls have cut their forecasts of growth for this year to 1.2% from 4.2% in September (GDP in 2008 was 3.5%). Some analysts have already said that the country is in a “technical recession”, when they measure GDP as in developed economies.

Monthly annual inflation has come down fast, particularly because of the significant drop in energy prices. Inflation is slowing and there are signs of deceleration in the economy. At the end of 2008, year on year inflation remains high, but it slowed in December to 7.1%. Inflation should converge quickly to target (even many analysts are forecasting an inflation rate of 2.8% in 2009).

On the other hand, the Central Bank decided on February 12th to cut the interest rate by 250 basis points, the biggest cut in the history of the instrument, taking it to 4.75%. The cut in the interest rate was much higher than expected by the market, which was located in a range between 100 and 150 basis points. It’s expected that it will continue to fall until it reaches 4% by the third quarter 2009.

Chile’s unemployment during 2008 averaged at 7.8%, which is 0.7 percentage points higher than the previous year. Some consultants have estimated that between September and December 2008, the economy lost about 50,000 jobs. Construction and mining were the sectors hardest hit, which was partly compensated by seasonal agriculture and fishing. Some analysts are forecasting an unemployment rate with double digits in March this year. By the standards of emerging economies, Chile has a relatively high level of personal consumer debt, and a period of retrenchment is starting. The last time unemployment was at 10 percent in Chile was in 2002. Since then, it has been in continual decline, reaching 7 percent in early 2008.

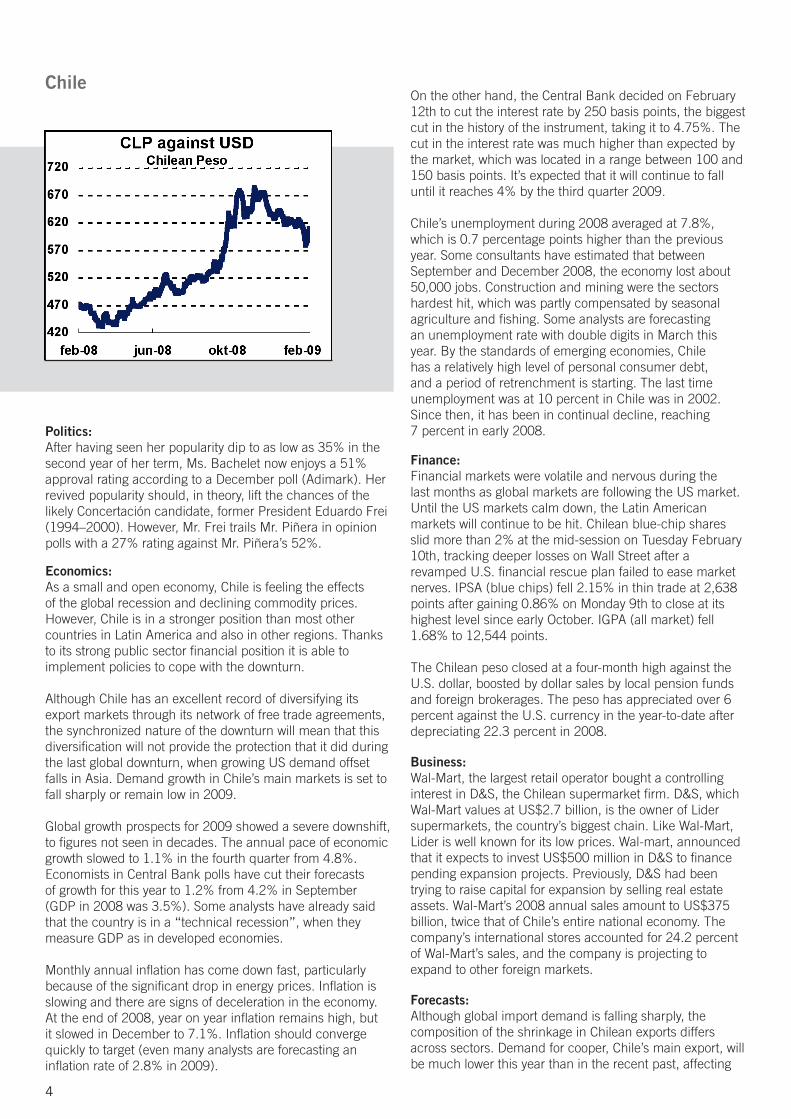

Finance:Financial markets were volatile and nervous during the last months as global markets are following the US market. Until the US markets calm down, the Latin American markets will continue to be hit. Chilean blue-chip shares slid more than 2% at the mid-session on Tuesday February 10th, tracking deeper losses on Wall Street after a revamped U.S. financial rescue plan failed to ease market nerves. IPSA (blue chips) fell 2.15% in thin trade at 2,638 points after gaining 0.86% on Monday 9th to close at its highest level since early October. IGPA (all market) fell 1.68% to 12,544 points.

The Chilean peso closed at a four-month high against the U.S. dollar, boosted by dollar sales by local pension funds and foreign brokerages. The peso has appreciated over 6 percent against the U.S. currency in the year-to-date after depreciating 22.3 percent in 2008.

Business:Wal-Mart, the largest retail operator bought a controlling interest in D&S, the Chilean supermarket firm. D&S, which Wal-Mart values at US$2.7 billion, is the owner of Lider supermarkets, the country’s biggest chain. Like Wal-Mart, Lider is well known for its low prices. Wal-mart, announced that it expects to invest US$500 million in D&S to finance pending expansion projects. Previously, D&S had been trying to raise capital for expansion by selling real estate assets. Wal-Mart’s 2008 annual sales amount to US$375 billion, twice that of Chile’s entire national economy. The company’s international stores accounted for 24.2 percent of Wal-Mart’s sales, and the company is projecting to expand to other foreign markets.

Forecasts:Although global import demand is falling sharply, the composition of the shrinkage in Chilean exports differs across sectors. Demand for cooper, Chile’s main export, will be much lower this year than in the recent past, affecting

4

both volume and value exports. However, Chile is also a major exporter of agricultural and agri-business goods, and demand for many of these products is not falling as fast as those for heavy industries.

Since financing conditions will remain tight throughout 2009, and possibly longer, prospects for investments are also mixed. The global investment environment has undergone a structural change since September 2008, and all countries are facing lower levels of investments for the coming years. Chile is no different. A new report released by the Corporation for Technological Development and Capital Goods, which measures investment in Chile, claims that US$ 17.2 bn of investment projects in Chile scheduled for the next five years have been delayed or shelved, with the mining and construction sector worst affected. However, investment plans for the energy sector have not been affected by the global downturn, and while 2008 will prove to be the peak of the investment cycle, Chile is still attracting both foreign and domestic investment.

Story of the month: Fiscal stimulus package totalling US$ 4 bn designed to protect growth and employment in 2009

On January 5th, the Chilean government announced a fiscal stimulus package amounting to the equivalent of 2.8% of GDP (US$ 4 bn.). This represents the largest such package in the country’s history. The government will allocate spending to expand infrastructure projects, help poor families, encourage investment by small and medium companies, increase youth employment and bolster worker training. There will be some tax breaks, and officials will also assist the mining industry, which is hurting from low international copper prices. This package is designed to provide a counter-cyclical boost to growth. The fiscal rule has guaranteed public sector solvency, and the large copper-aided surpluses of recent years have helped Chile to create substantial offshore liquid assets through its two sovereign wealth funds. These now hold around US$ 27bn (16% of GDP). The US$ 4 bn fiscal stimulus package comes through one percentage point of GDP in extra funds for public expenditure.

International analysts believe that Chile has devised the best-focused and best financed anti crisis plan in Latin America. As a result, the government now expects a deficit of 2.9% of GDP in 2009 (compared with a surplus of 8.8% of GDP in 2007 and an estimated surplus of 5.9% of GDP last year).

Mexico:

Politics:Mid-term elections will be held in July, and a sharp deterioration of the Mexican economy is expected to result in a poor performance for the government. There is a severe problem of escalating violent crime that may be made even worse by more difficult economic conditions. The opposition parties accuse Mexico’s president, Felipe Calderón, and the minister of finance, Agustín Carstens, of failing to provide an adequate response to rising unemployment. With the crisis deepening and legislative elections approaching, both the PRD and the Partido Revolucionario Institucional (PRI) are concentrating their criticism on the government’s management of the economy.

Economics: Mexico’s consumer confidence index fell to a record low of 81.9 points in January from 84.1 points in December according to the national statistics agency. The Mexican economy is expected to shrink around 1 percent this year as falling U.S. demand affect sales of cars, televisions and other goods exported by Mexico. Consumers were more pessimistic about their current economic situation and less confident about their future economic health, according to the index.

About 270,000 factory- workers lost their jobs in 2008, according to data from the social security institute.

According to Bloomberg, Mexico’s gross domestic product expanded 1.6 percent from a year earlier in the third quarter. The central bank predicts GDP may shrink as much as 1.8 percent this year.

Business:According to Bloomberg, Mexico’s auto production declined 3.5 percent in December as exports, which make up 89 % of output, fell 10 percent. In January production plunged 51%.

The decline in oil production is accelerating. Petróleos Mexicanos (PEMEX), the state oil company, produced 2.72

5

6

million barrels a day in December, which is an 8 percent drop compared to last year.

However, companies that sell to the construction industry may get a boost from a pledge by President Felipe Calderón to spend a record 570 billion pesos (USD 40 bn) this year on roads, bridges, rail and other infrastructure.

The head of Citigroup’s Mexican bank – Banco Nacional de Mexico (Banamex) - has denied reports that the U.S. bank plans to sell Banamex. Banamex is Mexico’s second-largest bank and one of Citigroup’s most lucrative properties -- raising speculation it might be sold to shore up capital for its parent. Mexico’s banking sector, a veteran of past crises that required their own massive bailouts, has not been exposed this time to as many toxic assets as U.S. and European banks, insulating it to a degree from the huge financial losses seen in other countries.

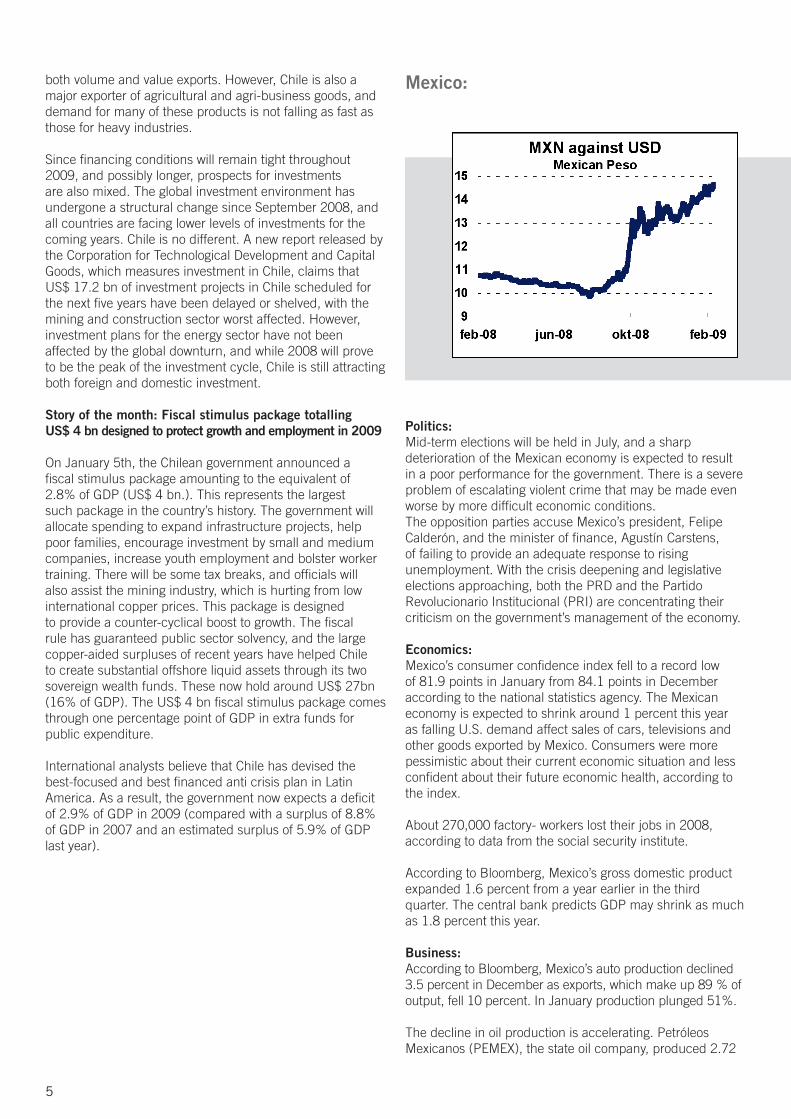

Finance:The Mexican peso has dropped 27% against the US dollar during the last 5 months - the biggest drop among the 16 most-traded currencies. Five-year credit-default swaps on Mexico’s bonds, have increased approx. 60 basis points to 4.09 percentage points in the past three months according to Bloomberg, signalling the increased cost of protecting Mexican debt against default. Mexico’s peso has underperformed other emerging market currencies in the global crisis, partly due to Mexico’s close economic links with the United States, which buys 80 percent of Mexican exports.

Mexico’s government has promised to keep defending the peso and Finance Minister Agustin Carstens has said that the central bank will continue with a new policy of discretionary currency sales to banks in order to contain the volatility of the peso. The bank had been offering dollars through daily auctions since the peso started sliding sharply in October.

Peru

Politics:Mr. Luis Carranza – who served as finance minister during the first two years of president García’s term, has been brought back to the post to administer a stimulus package and to guide the economy through the financial crisis. His predecessor had been in the position only for six months, thus the move was unexpected and signals a concern in the administration about the impact of the global recession on Peru.

President García’s popularity is decreasing. However he has publicly confirmed that he would like to run for a third term. Under the constitution, Mr García is not allowed to stand as a candidate in 2011. However, he could run again in 2016.

Head of the Peruvian Congress’s economy committee – Mr. Guido Lombardi Elias – has asked the government to speed the implementation of a stimulus plan worth 10 bn soles (USD 3 bn) to offset the effects of the global financial crisis. Economics: The global crisis is causing the Peruvian record economic growth of 9.8% in 2008 to slow down as demand and prices for metals exports is depressed. Peru’s annual expansion in December slowed to 4.9 percent from 6.4 percent in November, according to the National Statistics Institute. The global recession is causing the merchandise trade surplus to decrease to USD 47million in December from USD 1bn a year earlier, as export revenue fell by 30.7% year on year to USD 1.9 bn.

According to the Economist Intelligence Unit (EIU) domestic demand growth is keeping up relatively well, although signs of a slowdown are emerging. The import bill continued to rise in December, but the growth was slower – 5.8% year on year.

The central bank has unexpectedly lowered its benchmark reference interest rate by 25 basis points, to 6.25%. This is

7

the first cut in interest rates in more than five years. Falling commodity prices and slowing domestic demand growth have begun to weaken inflationary pressures thus the central bank had room for interest cut. The month-on-month rate of consumer price inflation eased to 0.1% in January, the lowest rate in 14 months, while annual inflation slowed to 6.5%.

Business:Delegates from Peru, Ecuador and Colombia have entered the first round of negotiations for a free trade agreement with the European Union (EU). The policy of the EU is to negotiate free trade agreements only with trade blocks, such as the Andean Community - and not with individual countries. Bolivia, however, has refused to negotiate any free trade treaty and initially, Ecuador also rejected the proposal. Ecuador has however now joined Colombia and Peru to work together for an agreement with the EU.

ForecastsThe merchandise trade surplus fell to USD 3.2bn in 2008 from USD 8.4bn in 2007 and the EIU expects that it will narrow further in 2009, despite falling import demand. They expect that demand for Peru’s exported goods will decrease in response to the sharp recessions in the US, EU and Japan. In addition they expect that export revenue will be further hit by falling prices for Peru’s mineral exports, which will reduce earnings by more than the fall in the import bill. However, the merchandise trade surplus is expected to recover in 2010 amid weak import spending and a recovery in export earnings as global demand stages a modest recovery.

Story of the month: Peru is well-prepared to face the financial crisis according to S&PAccording to Standard & Poor’s associate director for sovereign ratings, Sebastian Briozzo, Peru is well-prepared to face the financial crisis. However, he also considers that precautions should be taken. According to Mr. Briozzo “Peru was protected with correct and good macroeconomic policies of debt management. However, even though the financial channel is moderated, Peru will also have to take some preventive measures”.

Argentina

Politics:According to polls from Poliarquia, President Cristina Fernández de Kirchner has a higher disapproval rate, 39 percent, than approval rate, 28 percent. This is bad news for the president who has just finished her first year in office.

The global financial turmoil, combined with controversial political measures and new allegations of corruption, makes her outlook pretty grim as well. The Economist Intelligence Unit (EIU) believes it is going to cost the allies of Kirchner the majority position in the October 2009 legislative elections.

The president’s confrontational style of politics is cited as one of the important reasons for why she is having a hard time. After a four month conflict with the country’s powerful farming community over new taxation last year, Ms Fernández reduced the export tax on several agricultural products in December, except Soya. This has been interpreted as retaliation for the conflict earlier in 2008.

In the middle of January, Ms Fernández tried to help the farmers again by introducing subsidized credit lines for the purpose of buying machinery. However, the falling commodity prices are hitting the agro-economy of Argentina hard. And together with the export restriction the government still imposes on the marked, the conflict from a year back is starting to reappear.

According to some analysts, Argentina’s problem is that they have had great luck over the past years due to high commodity prices, and that has covered for their bad policies. Now the luck is up, but the bad policies continue.

Economics: Argentina’s trade surplus widened to $13.176 billion last year from $11.07 billion in 2007. The trade surplus was $862 million in December 2008, narrowing from the $1.804 billion surplus registered in December 2007, due in part to

8

lower commodity prices, a statement from the government’s statistics department said.

In the fourth quarter, South America’s second-largest economy grew 4.9 percent from the same period a year earlier, gross domestic product contracted 0.3 percent from the previous quarter, leaving the annual growth at 7 percent, the slowest expansion in the past six years.

Export revenues fell about USD 17 bn, or about 5 percent of GDP, according to Fundación de Investigaciones Económicas Latinoamericanas (FIEL). Total export revenues ended 25 percent below the revenues in the record year 2007. FIEL divides Latin American economies in three: Chile, that saves their extra revenues when experiencing high commodity prices and has a prudent fiscal policy. Brazil and Uruguay that does save, but lack prudency in their fiscal policies. And finally Argentina and Venezuela that increase public spending as revenues increase.

There is widespread belief that Argentina will suffer the global financial crisis as hard as the rest of the region in 2009. Positive analysts foresees a 3.2 percent growth in the Economy, others believe the economy will retract with as much as 3 percent. The official number, as stated in the fiscal budget, is 4 percent growth. In any case, 2009 will most likely see the worst economic development in Argentina since the year of the crisis, 2002.

EIU expects public spending to increase by 5 percent in 2009, after the government take-over of the private pension fund. This money will be spent to help the economy and to boost the government’s popularity before the mid-term elections in October. It is also believed that the private investment will fall, mainly due to the same reasons. And generally because of the deteriorating global economic outlook.

Finance:One of the largest challenges for the Argentine Economy in 2009 will be the flight of capital. In 2008, estimates put the total amount of capital flight at USD 150 bn, approximately the value of half of Argentina’s GDP. The government is trying to make tax incentives to bring back the capital, but analysts doubt their success.

However, the general opinion is that the country still is a long way from another default as they experienced in 2001/02. USD 21 bn of capital and interest is due in 2009. But with government revenues falling and its access to international markets closed since 2001 amid legal suits from the holders of defaulted bonds now owed $29bn plus interest, many remain concerned about 2010.

Argentina’s hopes of buying more time to service its debt could receive another boost as International holders of so-called Guaranteed Loans - issued in 2001 as Argentina lurched towards a $95bn default, the biggest sovereign default in history - will be invited to swap their bonds for new 5-year paper, with a 2 per cent capital reduction and a fixed 15.4 per cent rate for the first year and a variable rate after that.

Colombia

Politics:It is not determined whether Colombia’s president Alvaro Uribe will be able to run for a third period in the May 2010 presidential election. A bill has been passed allowing for a national referendum to be held over whether the president will be allowed to stand for re-election in 2014. It is possible that the bill, could be amended to allow him to run in 2010, but the legality of such an amendment is not certain.

One of the government’s allied parties, the right-wing Cambio Radical (CR), is likely to vote against the referendum in the Senate. Although Mr Uribe is still getting high popularity ratings (70% in December) support for his third term run has fallen from 74% in July to 54%.

Economics: Since President Uribe took office in 2002, consumer demand has surged in Colombia. Consumer prices were increasing 7.7 percent in 2008, the highest end-of-year rate since 2000, and above the bank’s annual target of 3.5 percent to 4.5 percent. However, this trend is now reversed as the financial crisis hits the economy. Consumer confidence, unemployment and vehicle sales indicators for December point to a sharp deterioration in private consumption.

The central bank has now lowered its benchmark rate for the second time – from 9.5 percent to 9 percent to encourage consumer spending and revive the economy.

The national jobless rate increased by 0.7 percentage points in December to 10.6%, however the rise in unemployment has so far been relatively modest compared to other countries in the region.

The government is trying to soften the impact of the financial crisis by prioritising spending on labour-intensive infrastructure projects, such as road transportation, housing, water and sanitation. The government is planning infrastructure investments totalling Peso 23 trn in 2009. However, as 50% of these projects are public-private

9

initiatives, credit restrictions and a lack of interest from international private participants may create obstacles.

Other stimulus programs by the government are tax cuts: such as a 1% cut in the income tax and a cut in the stamp tax – which is required for business documents.

Finance:The Colombian peso has weakened 26 percent in the past six months.

Business:Following successful bids in a concession auction last November, two Korean oil companies, Korea National Oil Corp (KNOC) and SK Energy, have signed up for a total of four exploration blocks. KNOC is cooperating with Pluspetrol from Argentina in two blocks in the eastern Llanos Basin, while SK Energy will explore and develop one of its block alone and partner in a 50:50 joint-venture with Colombia’s Petropuli for the second block.

Forecasts:The central bank has cut its 2009 economic growth estimate from 4 percent to a range of 1 percent to 3 percent as consumer spending is hit by the financial crisis. According to the central bank 2008 growth slowed to about 3.2 percent, down from a November estimate of 3.5 percent.

Inflation is expected to meet the central bank’s target this year of 4.5 percent to 5.5 percent as food and oil prices decline.

Venezuela

Politics:On February 15th, President Hugo Chávez managed to get the answer he wanted in the referendum on removing the cap on the number of times an elected official may serve. In December 2007, a similar referendum was held, but that time Chávez lost. This time around 55 percent of the electorate gave him the yes vote, and Venezuela can keep Mr Chávez as president until he dies, if he dies.

However the president’s popularity is falling. In the local elections last December, the “chavistas” only got 9 percent

more votes than the opposition. In the presidential election in 2006, the margin was 25 percent. It may well be that the much oil-fuelled popularity of the self proclaimed leader of the Bolivarian revolution will take further hits as the oil price keeps sliding downwards.

Mr Chávez has admitted that there is a financial crisis, but has proclaimed that it will not affect the Venezuelan Economy. This is probably not just wrong, but possibly also a source for optimism for the opposition that won important provinces in the last elections. The crisis will affect Venezuela, and unless the oil price make considerable hikes during 2009, it is believed that Chávez will have trouble with maintaining his level of spending.

Economics: At current oil prices, the Venezuelan oil revenues for 2009 will be USD 21.6 bn, according the Economist Intelligence Unit (EIU). This is down from USD 92.9 bn in 2008. The Venezuelan Economy is heavily dependant on oil, which is basically the only thing being exported from the country and represents half of the government revenues. The EIU believes 2009-10 will bring along a sharp downturn in the Venezuelan economy that is likely to take its toll on Mr. Chavez’ popularity.

Due to his insistence on the fact that Venezuelan economy will not be affected by the global financial crisis, analysts believe that the Venezuelan economy could eventually be hit harder than other Latin American economies because there has not been taken the same amount of measures to counter the effects of the crisis.

The inflation rate is expected to ease a bit during the end of 2009, but still remain around 30 percent, considerably higher than the number expected in the government’s budget of 15 percent. In 2008 the inflation rate was 31 percent.

The economy grew 4.9 percent last year, which is actually the lowest in five years – quite impressive in a year when global oil prices reached a whooping 147 USD per barrel (The Venezuelan oil sells at approximately 10 USD below brent). Finance:Mr Chávez maintains that the currency will not be devaluated – today it is held at a fixed relationship towards the USD at 2.15 Bolivares to 1 dollar. Goldman Sachs analysts said earlier this moths that they expect a devaluation during 2009.

The government is trying to postpone the need for devaluating by introducing tighter restrictions on dollar access; in January the government announced that the maximum dollar quota for Venezuelans travelling abroad would be cut from USD 5000 per year for credit card use, to USD 2500, while the maximum cash advance would be reduced from USD 500 to USD 400.

Cadivi, the foreign exchange control office, assigned around USD 5 bn in 2008 for overseas travel, this change will save the government several billion dollars in 2009, according to the EIU. The loss of oil revenues will however work in the opposite direction. There have also been introduced restrictions on imports.