lafayette parish regional airport commission · lafayette regional airport ... cva/abv.apa* . .,. ,...

TRANSCRIPT

RECEIVE)l.r-W ,V'VF /H.IPJTPP

2007JUNI I AH 10:1*0

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED

GOVERNMENT OF LAFAYETTE, LOUISIANA

ANNUAL FINANCIAL REPORTAND SUPPLEMENTARY INFORMATION

YEAR ENDED DECEMBER 31,2006

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

Release Date

LAFAYETTE REGIONAL AIRPORT

CONTENTSPAGE

INDEPENDENT AUDITORS'REPORT 2-3

REQUIRED SUPPLEMENTARY INFORMATION-PART IManagement's Discussion and Analysis 4-12

BASIC FINANCIAL STATEMENTSGovernment-Wide Financial Statements:

Statement of Net Assets 13Statement of Activities 14

Fund Financial Statements:Balance Sheet-Governmental Fund 16Statement of Revenues, Expenditures and Changes in Fund Balance-Governmental Fund 17

Statement of Net Assets - Proprietary Fund 18Statement of Revenues, Expenses and Changes in Net Assets-

Proprietary Fund 19Statement of Cash Flows - Proprietary Fund 20-21

Notes to the Basic Financial Statements 22-33

REQUIRED SUPPLEMENTARY INFORMATION -PART IISchedule of Revenues, Expenditures and Changes in Fund Balance-

Budget (GAAP Basis) and Actual - General Fund 34

SUPPLEMENTARY INFORMATIONSchedules of Expenses - Proprietary Fund 35Schedule of Expenditures of Federal Awards 36

INDEPENDENT AUDITORS' REPORT ON INTERNAL CONTROL OVERFINANCIAL REPORTING AND ON COMPLIANCE AND OTHERMATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTSPERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 37-38

INDEPENDENT AUDITORS' REPORT ON COMPLIANCE WITH REQUIREMENTSAPPLICABLE TO EACH MAJOR PROGRAM AND INTERNAL CONTROL OVERCOMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133 39-40

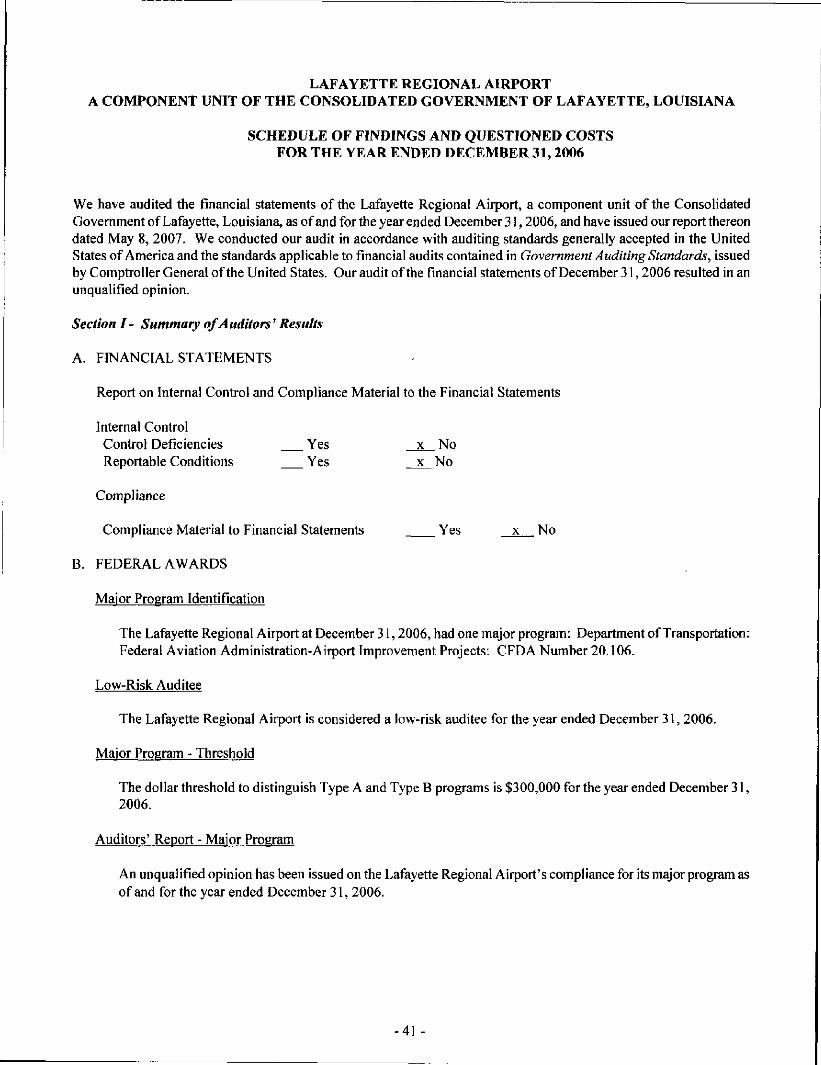

Schedule of Findings and Questioned Costs 41-42

INDEPENDENT AUDITORS' REPORT ON COMPLIANCE WITH REQUIREMENTSAPPLICABLE TO THE PASSENGER FACILITY CHARGE PROGRAM ANDON INTERNAL CONTROL OVER COMPLIANCE 43-44

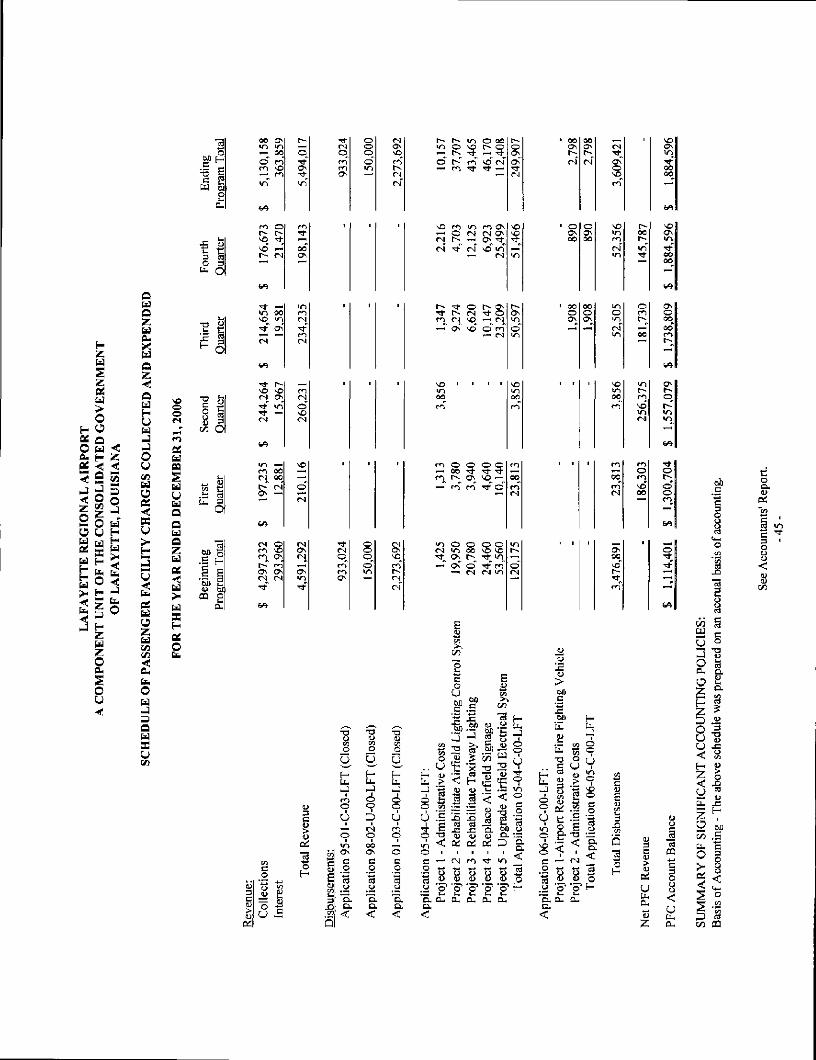

Schedule of Passenger Facility Charges Collected and Expended and Notes Thereto 45

Passenger Facility Charge Program Schedule of Findings and Questioned Costs 46

Passenger Facility Charge Program Audit Summary 47

WRIGHT, MOORE, DEHART, DUPUIS & HUTCHINSON, L.L.C.Certified Public Accountants

100 Petroleum Drive, 70508P O. Box 80569 • Lafayette, Louisiana 70598-0569

(337) 232-3637 • FAX (337) 235-8557wwm.wmJdh.com

JOHN W. WRIGHT, CPA *

JAMES H. DUPUIS, CPA, CFP '

JAN H- COWEN, CPA *

LANCE E. CRAPPELL, CPA *

PAT BAHAM DOUGHT, CPA *

MICAH R. VIDRINE, CPA *

INDEPENDENT AUDITORS' REPORT

To the Board of CommissionersLafayette Airport CommissionLafayette, Louisiana

' A PROFESSIONAL CORPORATION

TRAVIS M. BRINSKO, CPA *We have audited the accompanying financial statements of the governmental activities, the business-

RICK L.STUTES CPA, CVA/ABV.APA* . .,. , , . J f

&, _ _ „ ^ _ . . ° . ^ . _ * i T •* <• *Utype activities and each major fund of Lafayette Regional Airport, A Component Unit of theConsolidated Government of Lafayette, Louisiana, as of and for the year ended December 31,2006,which collectively comprise the Airport's basic financial statements as listed in the table of contents.

.. __ ,innm These financial statements are the responsibility of the Lafayette Regional Airport management. OurM- TROY MOORE, CPA * 4-MICHAEL G. DEHART, CPA. cvA, MBA * Besponsibility is to express opinions on these financial statements based on our audit.+RETIRED

We conducted our audit in accordance with auditing standards generally accepted in the United Statesof America and the standards applicable to financial audits contained in Government AuditingStandards, issued by the Comptroller General of the United States, and the provisions of LouisianaRevised Statutes 24:513 and the Louisiana Governmental Audit Guide. Those standards require thatwe plan and perform the audit to obtain reasonable assurance about whether the financial statementsare free of material misstatement. An audit includes examining, on a test basis, evidence supportingthe amounts and disclosures in the financial statements. An audit also includes assessing theaccounting principles used and significant estimates made by management, as well as evaluating theoverall financial statement presentation. We believe that our audit provides a reasonable basis for ouropinions.

In our opinion, the financial statements referred above present fairly, in all material respects, therespective financial position of the governmental activities, the business-type activities and eachmajor fund of the Lafayette Regional Airport, A Component Unit of the Consolidated Government ofLafayette, Louisiana, as of December 31,2006, and the respective changes in financial position andcash flows, where applicable, thereof for the year then ended in conformity with accountingprinciples generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated May 8,2007, on our consideration of the Lafayette Regional Airport's internal control over financialreporting and on our tests of its compliance with certain provisions of laws, regulations, contracts andgrant agreements and other matters. The purpose of that report is to describe the scope of our testingof internal control over financial reporting and compliance and the results of that testing, and not toprovide an opinion on the internal control over financial reporting or on compliance. That report isan integral part of an audit performed in accordance with Government Auditing Standards and shouldbe considered in assessing the results of our audit.

KRISTffi C. BOUDREAUX, CPA

SHEP E COMEAUX, CPA, MBA

ROBERT T. DUCHARME, II, CPA

CHRISTINE R. DUNN, CPA

DANE P. FALGOUT, CPA

MARY PATRICIA KEELEY, CPA

KYLE L. ROBICHEAUX, CPA

DAMIAN H. SPIESS, CPA, CFP

ROBIN G. STOCKTON, CPA

BRIDGET B. TILLEY, CPA, MT

PATRICK E. WAGUESPACK, CPA

CIRCULAR 230 DISCLOSURE - To ensure compliance with the recently issued U.S. Treasury Circular 230 Notice, unless otherwise expressly indicated, any tax advice contained in this communication,or attachments thereto, was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-re la ted penalties under the Internal Revenue Code, or (ii) promoting) marketing,or recommending any tax-related matter addressed herein.

The management's discussion and analysis and budgetary comparison information on pages 4 through 12 and 34, are not arequired part of the basic financial statements but are supplementary information required by accounting principles generallyaccepted in the United States of America. We have applied certain limited procedures, which consisted principally ofinquiries of management regarding the methods of measurement and presentation of the required supplementary information.However, we did not audit the information and express no opinion on it.

Our audit was performed for the purpose of forming opinions on the financial statements that collectively comprise theLafayette Regional Airport's basic financial statements. The accompanying schedule of expenditures of federal awards ispresented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-l H, Audits ofStates, Local Governments, and 'Non-Profit Organizations^ and is not a required party of the basic financial statements of theLafayette Regional Airport. The remaining supplementary information as listed in the table of contents is presented forpurposes of additional analysis and is also not a required part of the financial statements. The accompanying schedule ofpassenger facility charges collected and expended is presented for purposes of additional analysis as specified in thePassenger Facility Charge Audit Guide for Public Agencies, issued by the Federal Aviation Administration, and is also not arequired part of the basic financial statements. Such information has been subjected to the auditing procedures applied in theaudits of the financial statements and, in our opinion, is fairly stated in all material respects in relation to the financialstatements taken as a whole.

, Moore,(Dupuis f&Jtutchinson, LLQ

WRIGHT, MOORE, DEHART,DUPUIS & HUTCHINSON, L.L.C.Certified Public Accountants

May 8, 2007

MANAGEMENT'S DISCUSSION AND ANALYSIS

The following Management Discussion and Analysis (MD&A) provides an overview of the LafayetteRegional Airport's activities and financial performance for the fiscal year ended December 31,2006.

AIRPORT ACTIVITIES & HIGHLIGHTS

*f In 2006, the Lafayette Regional Airport's enplanements were 211,120, an increase of 32,824,versus enplanements of 178,296 in 2005. The increase resulted from the new serviceprovided by American Eagle to Dallas/Fort Worth. Cargo operations increased from5,587,111 Ibs. in 2005 to 15,558,861 Ibs. in 2006 due to the addition of several cargocompanies operating at the Airport.

In accordance with Federal Aviation Regulations (FAR 139.325), Lafayette Regional Airportconducted a full-scale emergency plan exercise in March. There were approximately fortyagencies involved in this exercise, including, local fire and police departments, Office ofEmergency Preparedness, Red Cross, FAA, TSA, local hospitals, and victim volunteers. Thisdisaster drill is scheduled every three years.

During the year the Airport offered several marketing initiatives to carriers in the hopes offilling a void in the local travel market. One of those carriers, American Eagle, accepted theoffer and began operations at the Lafayette Regional Airport in April 2006. The airline offersthree daily round-trip flights between Lafayette and Dallas/Fort Worth.

In September, the Airport welcomed a new fixed-based operator, Million Air. The companywill provide aircraft sales, aircraft maintenance, flight training, aircraft rental and fuel sales. Inaddition, three new leases were negotiated for construction of new private investmentcorporate hangars at the Airport.

Several projects in progress during 2006 include the following; Taxiway Bravo straighteningand widening, construction of a new Aircraft Rescue and Firefighting facility, and AirfieldElectrical Upgrade. These projects which improve the overall safety of the airport are ongoing at year-end.

- 4 -

FINANCIAL HIGHLIGHTS

Operating Revenues grew by 13.8% from $5.9 million to $6.8 million due to several factors.Specifically, landing fees increased 59.9% over the prior year due to increased cargooperations and parking revenues increased 21.9% also due to increased activity.

Operating Expenses increased by 6.5% from $7.8 million to $8.3 million primarily due torepairs to leased facilities, insurance, contractual services, utilities, and professional fees.

Non-Operating Income/(Expenses) changed from a net income of $5,354 in 2005 to a netincome of $242,388 in 2006 due mostly to additional interest income earned as a result ofhigher interest rates.

Net assets of our business-type activity increased by approximately $4,832,715, or 6.8percent, net assets of our governmental activities remains unchanged due to the annualtransfer of all revenues to our business-type activity.

Additional funding for Airport operations is received through ad valorem tax revenue, whichis transferred into the business-type activities from the governmental activities. In 2006 theAirport received approximately $1.8 million in revenues, compared to $1.7 in 2005. Thisincrease is due to higher assessed property values as compared with the prior year.

Capital grants and contributions received in 2006 were $4,296,158 compared to $3,070,382in 2005. These grants are directly related to the various Airport Improvement Program grantswhich are funded at the federal and state level and fluctuate from year to year dependent uponthe funding and schedules of the Airport's capital projects.

USING THIS REPORT

This audit report consists of a series of financial statements. The Statement of Net Assets and theStatement of Activities provide information about the activities of the Airport as a whole and present alonger-term view of the Airport's finances. For governmental activities, these statements tell howthese services were financed in the short term as well as what remains for future spending. Fundfinancial statements also report the Airport's operations in more detail than the government widestatements by providing information about the Airport's most significant funds.

- 5 -

Reporting the Airport as a Whole

The Statement of Net Assets and the Statement of Activities report information about the Airport as awhole and about its activities in a way that helps answer the question "Is the Airport as a whole betteror worse off as a result of the year's activities?" The statement of Net Assets and the Statement ofActivities report information about the Airport as a whole and about its activities in a way that helpsanswer this question. These statements include all assets and liabilities using the accrual basis ofaccounting, which is similar to the accounting used by most private-sector companies. All of thecurrent year's revenues and expenses are taken into account regardless of when cash is received orpaid.

These two statements report the Airport's net assets and changes in them. Net assets (the differencebetween assets and liabilities) are one way to measure the Airport's financial health, or financialposition. Over time, increases or decreases in the Airport's net assets are one indicator of whether itsfinancial health is improving or deteriorating. You will need to consider other non-financial factors,however, such as changes in the Airport's property tax base and millage rates, as well as capital grantawards, to assess the overall health of the Airport.

In the Statement of Net Assets and the Statement of Activities, we divide the Airport into two kinds ofactivities:

*> Governmental activities - The Airport's property tax revenue is reported here as well as thetransfer of this revenue to the Airport services.

^ Business-type activities - The Airport charges fees to customers to help cover most of the costof the services it provides. The Airport's entire cost of operations is reported here.

Reporting the Airport's Significant Funds

The Airport has two funds, both of which are treated as major funds. This report includes fundfinancial statements, which provides detailed information about these two significant funds. Somefunds are required to be established by State law, such as the General Fund. The Airport's two kindsof funds - governmental and proprietary - use different accounting approaches.

4- Governmental Funds - These fund types are reported using an accounting method calledmodified accrual accounting, which measures cash and all other financial assets that can bereadily converted to cash.

>> Proprietary Funds - When the Airport charges customers for the services it provides, theseservices are generally reported in proprietary funds. Proprietary funds are reported in thesame way that all activities are reported in the Statement of Net Assets and the Statement ofActivities. The Airport's proprietary fund is the same as the business type activities we reportin the government-wide statements but provide more detail and additional information, suchas cash flows.

-6 -

THE AIRPORT AS A WHOLE

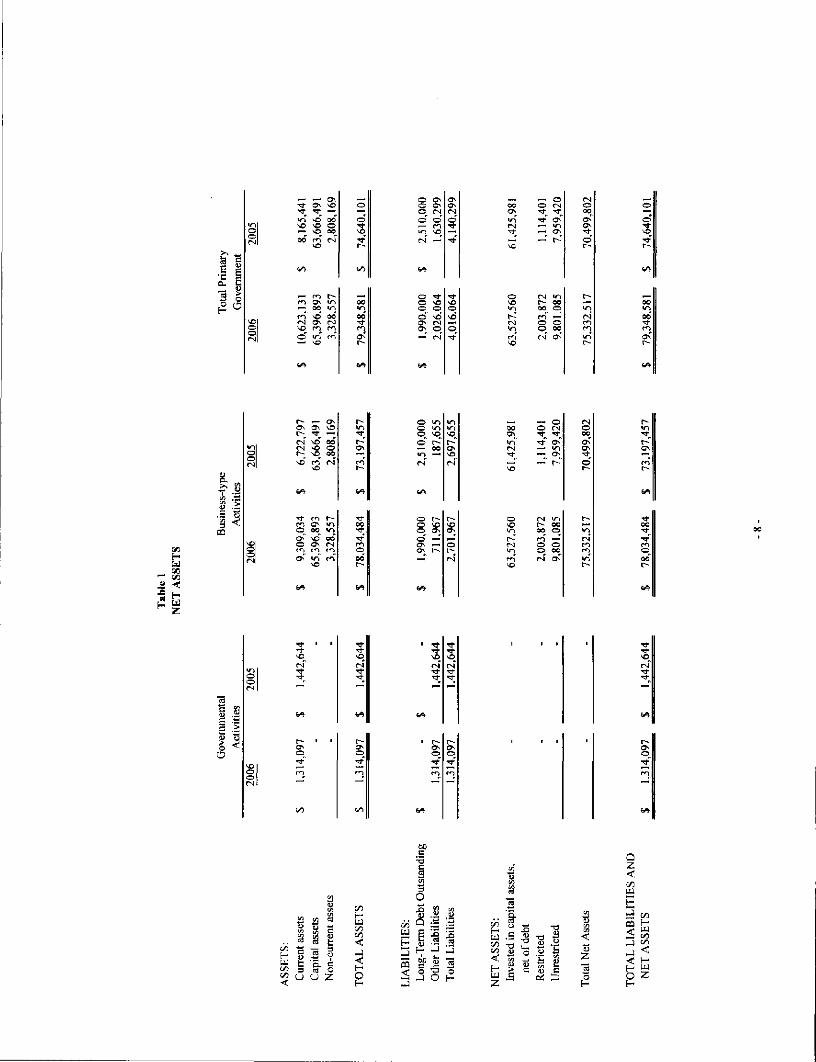

The Airport's combined net assets increased in the current year, from $70.49 million to $75.33million. This increase is due to the business-type activities, which accounts for the operations of theAirport. The increase is due to the growth in the invested in capital assets net of related debt categoryof $2,101,579 as well as the increase in unrestricted net assets of $1,841,665. Our analysis belowfocuses on the net assets (Table 1) and changes in net assets (Table 2) of the Airport's governmentaland business-type activities.

GENERAL FUND BUDGETARY HIGHLIGHTS

The Airport Commission adopted the General Fund Budget in 2005 and no subsequent budgetamendments were required during 2006. General Fund Revenues consist of ad valorem taxcollections, which are based on assessed values as determined by the Tax Assessor of Lafayette Parish,collected by the Lafayette Parish Sheriff and remitted to the Lafayette Regional Airport. The GeneralFund reported a positive variance of $192,292, which is a direct result of property tax collectionsbeing higher than expected. The ad valorem tax revenue reported in the governmental fund istransferred annually to the proprietary fund to support the operations of the Airport.

CAPITAL ASSET AND LONG-TERM DEBT

Capital Assets

At the end of December 31, 2006, the Airport had $63.5 million invested in capital assets, net ofrelated debt, including all equipment, land and buildings. This represents a net increase of $2.1million, or 3.4 percent, over last year.

During 2006, the airport expended $5.3 million on capital activities. This included $4.6 million towardcapital projects: taxiway bravo straightening and widening, aircraft rescue and firefighting facility,and airfield electrical restoration. Other acquisitions and improvements for 2006 included thefollowing: terminal and restaurant upgrades, office equipment, utility tractor and operations vehicle.

Acquisitions and improvements are funded using a variety of financing methods, including Federalgrants with matching State grants, passenger facility charges, debt issuance, and Airport revenues.

DebtAt the end of 2006, the Airport had $2.5 million in taxable and nontaxable bonds outstanding.Scheduled bond payments for the year comprised principal payments of $500,000 and interestpayments of $206,230.

_ 7.

I e£ I

\O NO O— ^o ooOO" fT (N

oTf^o

.2 o3 <

UJ

fNj —

— ON— * r-"

I -3oO

•*rTPNO

O•'

Q2

H

J3 «4) o>

W "*

s st • a3 KJ

t ass

ets

OJ

o

O

C/3h-U

3

TO

TA

L

t«UJ

H

LIA

BIL

I

6s «•S .siQ 56 ^5 -aE — ioo b§ aJ 0

w_u

152j"C3

OH

w

<

LU

tced

1

.sr/)u

_c

1oOJc

-g 1

Res

trict

Unr

estr

in0>to(»<

4)

So

rn -

•c0-

oOO — —

— ( N O r * i o o —

— m o r-

— m

<CO

O^ m O •—• (N O m OO

OO V Ov" O O cT —' <N

tN m rN r*~ wS —' <N

so —Osom m

— m

u

oONrs*

IIO

(N

(Nr\f

Rev

enue

sPr

ogra

m r

even

ues:

w

Cha

rges

for

ser

vice

Ope

ratin

g gr

ants

Cap

ital

gran

ts a

ndC

ontr

ibut

ions

Gen

eral

rev

enue

s:

OD

Prop

erty

tax

esSt

ate

reve

nue

shar

irIn

vest

men

t ea

rnin

gs

n

Oth

er g

ener

al r

even

Tot

al r

even

ues

Pro

gram

exp

ense

sA

dmin

istr

atio

n

1s

Com

mun

icat

ion

& 1

j«

Supp

lies

& M

ater

ia

<uCJ-

Rep

airs

& M

aint

eni

Secu

rity

AR

FFA

irfi

eld

V)

Con

trac

tual

Ser

vice

Mis

cella

neou

sD

epre

ciat

ion

Inte

rest

exp

ense

Ass

esso

r's p

ensi

onT

otal

exp

ense

s

c<DCXX0)

ai

Exc

ess

reve

nues

ovi

befo

re t

rans

fers

Tra

nsfe

rs

Table 3REVENUES

The following chart shows the major sources and percentage of operating revenues of the proprietary fund for the yearended December 31,2006 and December 31, 2005:

Operating Revenues

Other1%

PassengerFacilityCharges

13%

Parking18%

GrantRevenues

2%

Rental cars

Operating Revenues:

Landing feesTerminal rent/chargesHangar rentalsFuel Flowage feesLand & non-terminal facilitiesRental carsParkingPassenger Facility ChargesGrant RevenuesOther

Total Operating Revenues

Non-Operating Revenues:

Interest IncomeInsurance ProceedsOperation & Maintenance Tax

Transferred from General FundCapital Grants and Contributions

Total Non-Operating Revenues

TOTAL REVENUES

Landing fees8%

-- n^^sBBto^

Land & non-terminalfacilities

23%

2006$ 513,271

708,250517,774173,723

1,555,371897,101

1,251,414902,724211,16488,219

6,819,011

376,948137,985

1,872,2924,296,158

6,683,383

$ 13,502,394 <

Terminalrent/charges

10%

Hangar rentals8%

Fuel Flowagefees3%

20055 320,982

675,742501,839253,851

1,503,505844,200

1,026,900503,133296,165

66,342

5,992,659

221.97713,856

1,751,4573,070,382

5,057,672

& 11,050,331

Increase(Decrease)from 2005

$ 192,28932,50815,935

(80,128)51,86652,901

224,514399,591(85,001)21,877

826,352

154,971124,129

120,8351,225,776

1,625,711

$ 2,452,063

PercentIncrease

(Decrease)59.9%4.8%3.2%

-31.6%3.4%6.3%

21.9%79.4%

-28.7%33.0%

69.8%895.9%

6.9%39.9%

-10-

Table 4EXPENSES

The following chart shows the major sources and percentage of operating expenses of the proprietary fund for the yearended December 31, 2006 and December 31, 2005:

Depreciation42%

Miscellaneous0%

Administration16%

Operating ExpensesCommunications

& Utilities4% Supplies &

Materials1%

Repairs &Maintenance

Security9%

ContractualServices

15% Airfield1%

ARFF

Operating Expenses:

AdministrationCommunications & UtilitiesSupplies & MaterialsRepairs & MaintenanceSecurityArffAirfieldContractual ServicesMiscellaneousDepreciation

Total Operating Expenses

Non-Operating Expenses:

Interest expenseAssessor's pension

Total Non-Operating Expenses

TOTAL EXPENSES

2006$ 1,306,601

361,65973,561

390,470747,998575,00087,452

1,293,64533,317

3,527,431

2005$ 1,238,192

304,13069,700

220,409730,320540,709111,734

1,232,68739,917

3,391,178

Increase(Decrease)from 2005

$ 68,41057,5293,861

170,06117,67834,291

(24,282)60,958(6,600)

136,253

PercentIncrease

(Decrease)5.5%

18.9%5.5%

77.2%2.4%6.3%

-21.7%4.9%

-16.5%. 4.0%

8,397,134

206,23066,315

272,545

$ 8,669,679

7,878,975

169,056

61,423

230,479

$ 8,109,454

518,159

37,1744,892

42,066

$ 560,225

22.0%8.0%

-11 -

ECONOMIC FACTORS

The business-type activities will .see changes due to economic factors as well as continued capitalimprovements funded by various grants. Several of the economic factors considered in the budgetaryprocess were:

The economic environment of the airline industry as a whole.

Consumer price index adjustments, which allows for increases in rental charges to tenants ofthe Airport.

Escalating costs of operations including insurance, security, and other contractual services.

REQUEST FOR INFORMATION

This financial report is written to provide a general overview of the Lafayette Regional Airport'sfinancial position for all interested parties and to show the Airport's accountability for the money itreceives. Questions concerning any of the information in the report should be addressed in writing tothe Financial Officer, Lafayette Regional Airport, 200 Terminal Drive, Lafayette, LA 70508.

- 12-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

STATEMENT OF NET ASSETSDECEMBER 31, 2006

GOVERNMENTALACTIVITIES

ASSETS

Current Assets

Cash and Cash EquivalentsInvestment in Certificates of DepositAccounts ReceivableOther ReceivablesAd Valorem Tax ReceivableDue From Lafayette Parish

Sheriffs OfficeGrant Funds ReceivablePrepaids

Total Current Assets

513,062

801,035

BUSINESS-TYPE

ACTIVITIES

1,314,097

$ 6,411,766712,970272,945

3,784

1,656,370251,199

9,309,034

TOTAL

$ 6,411,766712,970272,945

3,784513,062

801,0351,656,370

251,199

10,623,131

Noncurrent Assets:Restricted AssetsUnamortized Debt ExpenseProperty and Equipment (Net)Land

Construction Work in Progress

Total Noncurrent Assets

3,274,28354,274

53,133,8755,521,1166,741,902

68,725,450

3,274,28354,274

53,133,8755,521,1166,741,902

68,725,450

TOTAL ASSETS $ 1,314,097 $ 78,034,484 $79,348,581

The Accompanying Notes are an Integral Part of These Statements.-13 -

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

STATEMENT OF NET ASSETSDECEMBER 31, 2006

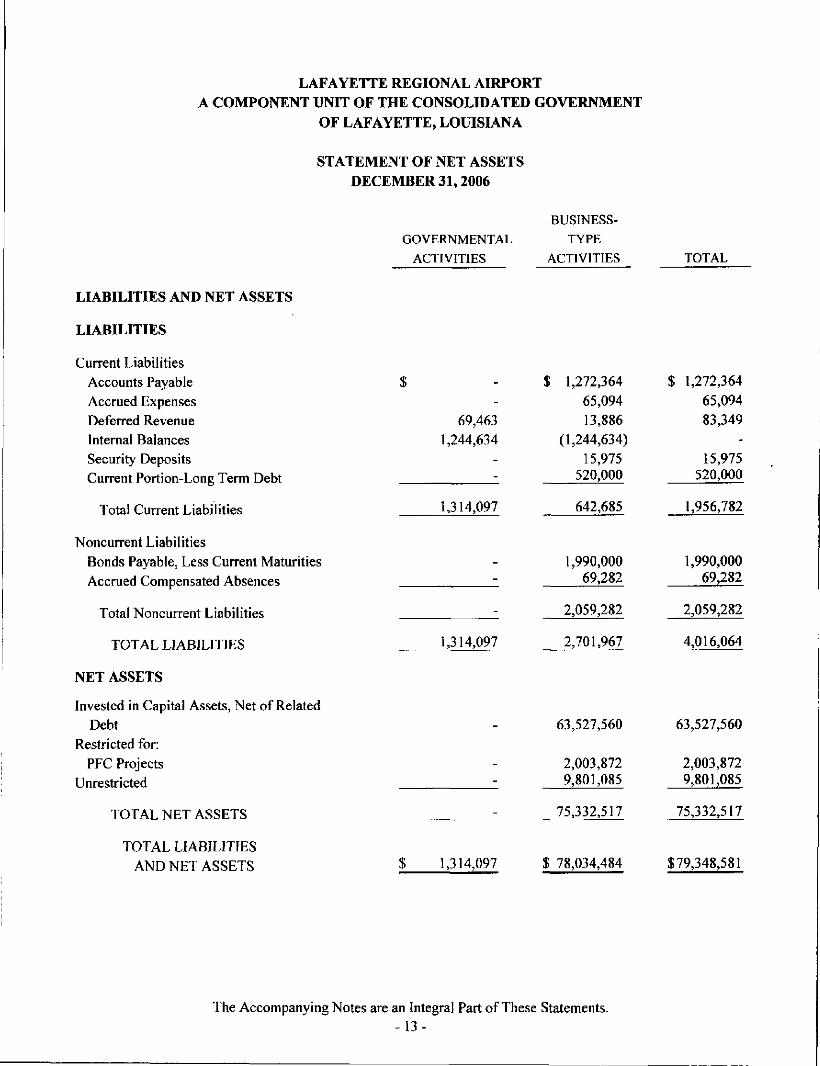

LIABILITIES AND NET ASSETS

LIABILITIES

Current LiabilitiesAccounts PayableAccrued ExpensesDeferred RevenueInternal BalancesSecurity DepositsCurrent Portion-Long Term Debt

Total Current Liabilities

Noncurrent LiabilitiesBonds Payable, Less Current MaturitiesAccrued Compensated Absences

Total Noncurrent Liabilities

TOTAL LIABILITIES

NET ASSETS

Invested in Capital Assets, Net of RelatedDebt

Restricted for:PFC Projects

Unrestricted

TOTAL NET ASSETS

TOTAL LIABILITIESAND NET ASSETS

GOVERNMENTAL

ACTIVITIES

69,4631,244,634

1,314,097

1,314,097

$ 1,314,097

BUSINESS-

TYPE

ACTIVITIES

$ 1,272,36465,09413,886

(1,244,634)15,975

520,000

642,685

1,990,00069,282

2,059,282

2,701,967

63,527,560

2,003,8729,801,085

75,332,517

$ 78,034,484

TOTAL

$ 1,272,36465,09483,349

15,975520,000

1,956,782

1,990,00069,282

2,059,282

4,016,064

63,527,560

2,003,8729,801,085

75,332,517

$79,348,581

The Accompanying Notes are an Integral Part of These Statements.-13-

DO

HH

<u u

2 S.E O

£ £»OD W

11u o

.JtoO

£ HOS >•g wis

AF

AY

ET

TE

RE

GIO

NA

L A

IC

ON

SO

LID

AT

ED

GO

VE

RP

. T . ,l-l W

ffiHtoOH

SOoo<si-5<*)

^ (VM WP W -HW s

ST

AT

EM

EN

T O

F A

CT

IVI

HE

YE

AR

EN

DE

D D

EC

EM

Prog

ram

Rev

er

-£ 1•a ra -3-= ^ £

S s 'Hu - a

•

Ope

ratin

g

Cha

rges

for

G

rant

s an

d

ses

Serv

ices

C

ontr

ibut

ions

H ctr^ u—j CL

tf ,^0to

&*)

w

&e

- br £ -,

(U-C

0,

"3ob

o>fe<«<u*Jo

DOC'

exSo

£ O

fcoOH

SOu

u-<

men

tal

cV

oO

u£

uoO"sucOJO

uGEu>oO

Sot-

uJf^J-4>O.fr««JS'«3

03

Serv

ices

eoO..<

H

1/14>C

^CQ

1o

Q

I

FUND FINANCIAL STATEMENTS

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

BALANCE SHEET - GOVERNMENTAL FUNDDECEMBER 31,2006

LIABILITIES AND FUND BALANCE

LIABILITIES

GeneralFund

ASSETS

Ad Valorem Tax Receivable $ 513,062Due From Lafayette Parish Sheriffs Office 801,035

TOTAL ASSETS $ 1,314,097

Deferred Tax Revenue $ 69,463Due to Proprietary Fund 1,244,634

TOTAL LIABILITIES 1,314,097

FUND BALANCE 1

TOTAL LIABILITIES AND FUND BALANCE $ 1,314,097

The Accompanying Notes are an Integral Part of These Statements.- 1 6 -

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

STATEMENT OF REVENUES, EXPENDITURESAND CHANGES IN FUND BALANCE - GOVERNMENTAL FUND

FOR THE YEAR ENDED DECEMBER 31, 2006

GeneralFund

REVENUE

Ad Valorem Tax $ 1,830,244State Revenue Sharing 42,048

Total Revenues 1,872,292

OTHER FINANCING USES

Transfers to Proprietary Fund (1,872,292)

Total Other Financing Uses (1,872,292)

EXCESS OF REVENUES OVER OTHER FINANCING USES

FUND BALANCE, BEGINNING 1

FUND BALANCE, ENDING I :

The Accompanying Notes are an Integral Part of These Statements.- 17-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

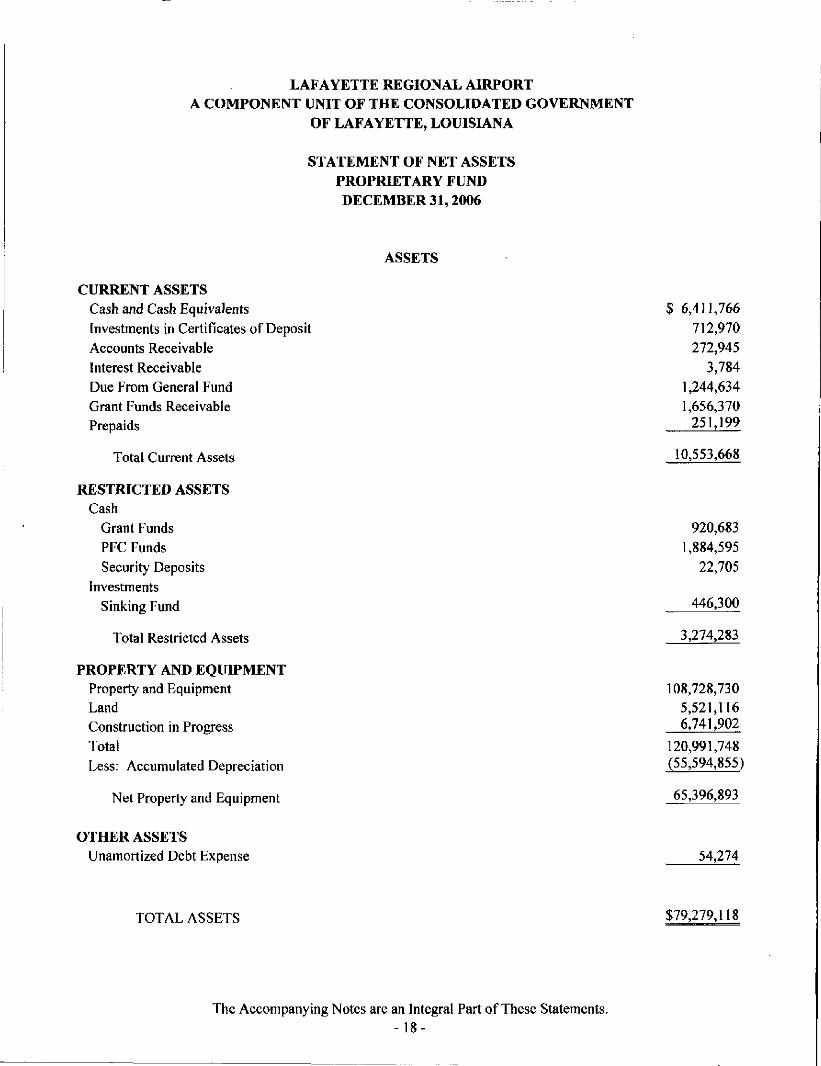

STATEMENT OF NET ASSETSPROPRIETARY FUNDDECEMBER 31,2006

ASSETS

CURRENT ASSETSCash and Cash EquivalentsInvestments in Certificates of DepositAccounts ReceivableInterest ReceivableDue From General FundGrant Funds ReceivablePrepaids

Total Current Assets

RESTRICTED ASSETSCash

Grant FundsPFC FundsSecurity Deposits

InvestmentsSinking Fund

Total Restricted Assets

PROPERTY AND EQUIPMENTProperty and EquipmentLandConstruction in ProgressTotalLess: Accumulated Depreciation

Net Property and Equipment

OTHER ASSETSUnamortized Debt Expense

$ 6,411,766712,970272,945

3,7841,244,6341,656,370

251,199

10,553,668

920,6831,884,595

22,705

446,300

3,274,283

108,728,7305,521,1166,741,902

120,991,748(55,594,855)

65,396,893

54,274

TOTAL ASSETS $79,279,118

The Accompanying Notes are an Integral Part of These Statements.- 1 8 -

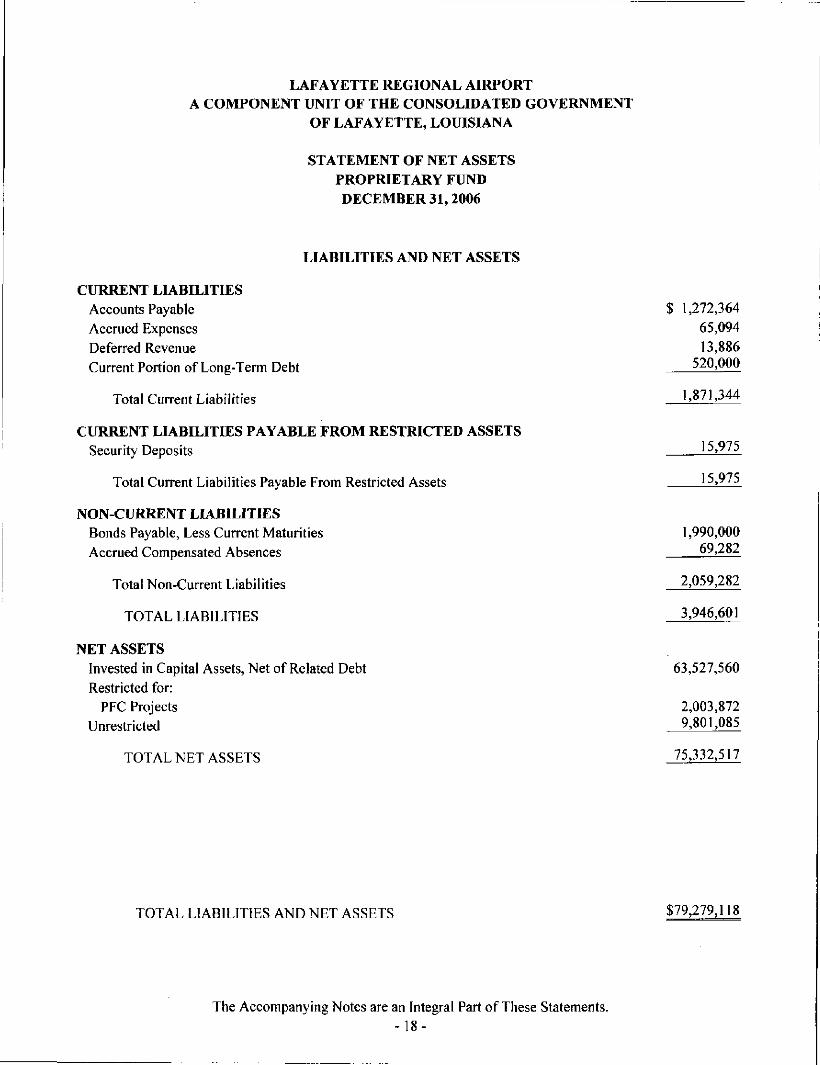

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

STATEMENT OF NET ASSETSPROPRIETARY FUNDDECEMBER 31,2006

LIABILITIES AND NET ASSETS

CURRENT LIABILITIESAccounts PayableAccrued ExpensesDeferred RevenueCurrent Portion of Long-Term Debt

Total Current Liabilities

CURRENT LIABILITIES PAYABLE FROM RESTRICTED ASSETSSecurity Deposits

Total Current Liabilities Payable From Restricted Assets

NON-CURRENT LIABILITIESBonds Payable, Less Current MaturitiesAccrued Compensated Absences

Total Non-Current Liabilities

TOTAL LIABILITIES

NET ASSETSInvested in Capital Assets, Net of Related DebtRestricted for:

PFC ProjectsUnrestricted

TOTAL NET ASSETS

$ 1,272,36465,09413,886

520,000

1,871,344

15,975

15,975

1,990,00069,282

2,059,282

3,946,601

63,527,560

2,003,8729,801,085

75,332,517

TOTAL LIABILITIES AND NET ASSETS $79,279,118

The Accompanying Notes are an Integral Part of These Statements.- 1 8 -

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

STATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET ASSETSPROPRIETARY FUND

FOR THE YEAR ENDED DECEMBER 31,2006

OPERATING REVENUESRentalsCommissionsLanding FeesParking TollsPassenger Facility ChargesGrant RevenuesMiscellaneous

Total Operating Revenues

OPERATING EXPENSESSalaries and Costs of EmploymentSuppliesOther Services and ChargesDepreciation

Total Operating Expenses

OPERATING LOSS

NON-OPERATING REVENUES (EXPENSES)Interest IncomeInsurance ProceedsInterest ExpenseAssessor's Pension

Total Non-Operating Revenues (Expenses)

Loss before Contributions and Transfers

Capital ContributionsTransfers In

INCREASE IN NET ASSETS

NET ASSETS, BEGINNING

NET ASSETS, ENDING

3,678,496173,723513,271

1,251,414902,724211,16488,219

6,819,011

945,16135,689

3,888,8533,527,4318,397,134

(1,578,123)

376,948137,985

(206,230)(66,315)242,388

(1,335,735)

4,296,1581,872,292

4,832,715

70,499,802

$ 75,332,517

The Accompanying Notes are an Integral Part of These Statements.- 19-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

STATEMENT OF CASH FLOWSPROPRIETARY FUND

FOR THE YEAR ENDED DECEMBER 31,2006

CASH FLOWS FROM OPERATING ACTIVITIESCash Received From Providing Services $ 6,892,091Cash Paid to Suppliers (3,610,163)Cash Paid to Employees (939,325)

Net Cash Provided by Operating Activities * 2,342,603

CASH FLOWS FROM INVESTING ACTIVITIESProceeds from Sale of Investments 172,592Purchase of Investments (32,316)Investment Interest Received 375,748

516,024

1,944,278

Net Cash Provided By Investing Activities

CASH FLOWS FROM NON-CAPITAL FINANCING ACTIVITIESTransfers From General Fund 2,010,593Payments for Assessor's Pension (66,315)

Net Cash Provided By Non-Capital Financing Activities

CASH FLOWS FROM CAPITAL AND FINANCING ACTIVITIESCapital Grants Received 3,229,051Acquisition and Construction of Fixed Assets (5,257,833)Principal Payments on Long-Term Debt (500,000)Proceeds From Insurance Claim 137,985Interest Paid (198,360)

Net Cash Used In Capital and Financing Activities (2,589,157)

NET INCREASE IN CASH AND CASH EQUIVALENTS 2,213,748

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR(including $2,127,133 in restricted cash) 7,026,001

CASH AND CASH EQUIVALENTS AT END OF YEAR(including $2,827,983 in restricted cash) $ 9,239,749

The Accompanying Notes are an Integral Part of These Statements.-20-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

STATEMENT OF CASH FLOWS - continuedPROPRIETARY FUND

FOR THE YEAR ENDED DECEMBER 31, 2006

RECONCILIATION OF OPERATING LOSS TO NET CASHPROVIDED BY OPERATING ACTIVITIES:

Operating LossAdjustments to Reconcile Loss From Operations to Net Cash

Provided By Operating Activities:DepreciationChanges in Assets and Liabilities:

Accounts ReceivablePrepaid ExpensesAccounts PayableAccrued ExpensesDeferred RevenueAccrued Compensated Absences

Net Cash Provided By Operating Activities

$(1,578,123)

3,527,431

77,785(50,501)364,880

2,304(4,705)3,532

$ 2,342,603

The Accompanying Notes are an Integral Part of These Statements.-21 -

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(A) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Reporting Entity - Lafayette Regional Airport is a municipally owned, non-hub airport located on U. S.Highway 90 East in the City of Lafayette. The Airport provides passenger service through three regionalcarriers. The major source of revenue for the Airport is rentals on buildings, hangars, land, and terminal space.

The Airport is governed by a seven member, non-elected commission. Five members are appointed by theLafayette Consolidated Government, one member is appointed by the Parish President, and one member isappointed by the mayors of the various municipalities surrounding Lafayette.

The Lafayette Regional Airport's financial statements are prepared in accordance with generally acceptedaccounting principles (GAAP). The Governmental Accounting Standards Board (GASB) is responsible forestablishing GAAP for state and local governments through its pronouncements (Statements and Interpretations).Governments are also required to follow the pronouncements of the Financial Accounting Standards Board(FASB) issued through November 30, 1989 (when applicable) that do not conflict with or contradict GASBpronouncements. The Airport has elected to apply FASB pronouncements issued after that date to its business-type activities and enterprise funds. The more significant accounting policies established in GAAP and used bythe Airport are discussed below.

Basic Financial Statements - Government-Wide Statements - The Airport's basic financial statementsinclude both government-wide (reporting the Airport as a whole) and fund financial statements (reporting theAirport's major funds). Both the government-wide and fund financial statements categorize primary activities aseither governmental or business type. Collection of ad valorem tax revenue is classified as a governmentalactivity. The Airport's operations are classified as a business-type activity.

In the government-wide Statement of Net Assets, both the governmental and business-type activities columns (a)are presented on a consolidated basis by column, (b) and are reported on a full accrual, economic resource basis,which recognizes all long-term assets and receivables as well as long-term debt and obligations. The Airport'snet assets are reported in three parts-invested in capital assets, net of related debt; restricted net assets; andunrestricted net assets. The Airport first utilizes restricted resources to finance qualifying activities.

The government-wide Statement of Activities reports both the gross and net cost of each of the Airport'sfunctions and business-type activities. The functions are also supported by general government revenues(property, sales and use taxes, certain intergovernmental revenues, fines, permits and charges, etc.). TheStatement of Activities reduces gross expenses (including depreciation) by related program revenues, operatingand capital grants. Program revenues must be directly associated with the function or a business-type activity.Operating grants include operating-specific and discretionary (either operating or capital) grants while the capitalgrants column reflects capital-specific grants.

The net costs (by function or business-type activity) are normally covered by general revenue (property, sales orgas taxes, intergovernmental revenues, interest income, etc).

-22-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(A) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - continued

Basic Financial Statements - Government-Wide Statements - continued

The Airport does not allocate indirect costs.

This government-wide focus is more on the sustainability of the Airport as an entity and the change in theAirport's net assets resulting from the current year's activities.

Basic Financial Statements - Fund Financial Statements - The financial transactions of the Airport arereported in individual funds in the fund financial statements. Each fund is accounted for by providing a separateset of self-balancing accounts that comprises its assets, liabilities, reserves, fund equity, revenues andexpenditures/expenses. The various funds are reported by generic classification within the financial statements.

The following fund types are used by the Airport:

Governmental Fund:

The focus of the governmental fund's measurement (in the fund statements) is upon determination offinancial position and changes in financial position (sources, uses, and balances of financial resources) ratherthan upon net income. The following is a description of the governmental fund of the Airport:

General Fund - This fund is used to account for resources traditionally associated with governmentswhich are not required legally or by sound financial management to be accounted for in another fund.The Airport reports its property tax activity in the General Fund.

Proprietary Fund:

The focus of proprietary fund measurement is upon determination of operating income, changes in netassets, financial position, and cash flows. The generally accepted accounting principles applicable are thosesimilar to businesses in the private sector. The following is a description of the proprietary fund of theAirport:

Enterprise Fund - This type of fund is used to account for operations that are financed and operated in amanner similar to private business enterprises where the costs (expenses, including depreciation) ofoperating and maintaining the airport facilities on a continuing basis are financed through user charges.

Measurement Focus/Basis of Accounting - Fund Financial Statements - Measurement focus refers to what isbeing measured; basis of accounting refers to when revenues and expenditures are recognized in the accountsand reported in the financial statements. Basis of accounting relates to the timing of the measurement made,regardless of the measurement focus applied.

-23-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(A) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - continued

Measurement Focus/Basis of Accounting - Fund Financial Statements - continued

The governmental fund uses a financial resources measurement focus and is accounted for using the modifiedaccrual basis of accounting. Its revenues are recognized when susceptible to accrual (i.e., when they becomemeasurable and available as net current assets). Expenditures are generally recognized under the modifiedaccrual basis of accounting when the related fund liability is incurred, if measurable.

The proprietary fund is accounted for on a cost of service measurement focus using the accrual basis ofaccounting. Revenues are recognized when earned and expenses are recognized when the related liabilities areincurred.

Basis of Accounting - Government-Wide Financial Statements - The government-wide financial statements(i.e., the Statement of Net Assets and the Statement of Activities) report information on all of the non-fiduciaryactivities of the government. Governmental activities, which normally are supported by taxes andintergovernmental revenues, are reported separately from business-type activities, which primarily rely on feesand charges for support.

The government-wide financial statements are prepared using the economic resources measurement focus andthe accrual basis of accounting. This is the same approach used in the preparation of the proprietary fundfinancial statements but differs from the manner in which governmental fund financial statements are prepared.Therefore, governmental fund financial statements include reconciliation with brief explanations to betteridentify the relationship between the government-wide statements and the statements for governmental funds.The primary effect of internal activity has been eliminated from the government-wide financial statements.

The government-wide Statement of Activities presents a comparison between expenses, both direct and indirect,and program revenues for each segment of the business-type activities of the Airport and for each governmentalprogram. Direct expenses are those that are specifically associated with a service, program or department andare therefore clearly identifiable to a particular function. Indirect expenses for centralized services andadministrative overhead are allocated to the programs, functions and segments using a full cost allocationapproach and are presented separately to enhance comparability of direct expenses between governments thatallocate direct expenses and those that do not. Program revenues include charges paid by the recipients of thegoods or services offered by the programs and grants and contributions that are restricted to meeting theoperational or capital requirements of a particular program. Revenues not classified as program revenues arepresented as general revenues. The comparison of program revenues and expense identifies the extent to whicheach program or business segment is self-financing or draws from the general revenues of the Airport.

Net assets should be reported as restricted when constraints placed on net asset use are either externally imposedby creditors, grantors, contributors, or laws or regulations of other governments or imposed by law throughconstitutional provisions or enabling legislation.

Separate financial statements are provided for governmental funds and proprietary funds. The general fund andthe proprietary fund are considered major funds of the Airport.

-24-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(A) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - continued

Revenues - Substantially all governmental fund revenues are accrued. Property taxes are billed and collectedwithin the same period in which the taxes are levied. Subsidies and grants to proprietary funds, which financeeither capital or current operations, are reported as non-operating revenue based on GASBS No. 33. In applyingGASBS No. 33 to grant revenues, the provider recognizes liabilities and expenses and the recipient recognizesreceivables and revenue when the applicable eligibility requirements, including time requirements, are met.Resources transmitted before the eligibility requirements are met are reported as advances by the provider anddeferred revenue by the recipient.

Interfund Activity - Interfund activity is reported as either loans or transfers. Loans are reported as interfundreceivables and payables as appropriate and are subject to elimination upon consolidation. All other interfundtransactions are treated as transfers. Transfers between governmental or proprietary funds are netted as part ofthe reconciliation to the government-wide financial statements.

Budgets and Budgetary Accounting - The Lafayette Regional Airport is required to adopt annual budgets foreach fund. Each budget is presented on the modified accrual basis of accounting, which is consistent withaccounting principles generally accepted in the United States of America.

The following procedures are followed in establishing the budgetary data reflected in the financial statements:

The budget is formally adopted by the commission prior to the beginning of the fiscal year, and notices of itscompletion and availability are published. After its adoption, adjustments to the budget must be approved byresolution. All appropriations lapse at the end of the fiscal year.

Property and Equipment - Depreciation of all exhaustible fixed assets used by the Enterprise Fund is chargedas an expense against operations. Accumulated depreciation is reported on the Enterprise Fund Balance Sheet.Depreciation has been provided over the estimated useful lives using the straight-line method. The estimateduseful lives of fixed assets are as follows:

YearsHangars and Buildings 10-30Runways and Navigation Aids 10-20Service Roads and Parking 10 - 20Other Permanent Improvements 10 - 20Equipment 3 - 1 0Lease Purchase Equipment 5

Land and other capital improvements acquired by the Airport prior to October 31, 1971, are stated atreplacement cost as of that date, as historical cost information was not maintained prior to this time. Landacquisitions, which occurred prior to October 31, 1971, are stated at an estimated replacement cost of$4,864,600, which approximates $2,600 per acre. All capital improvements acquired prior to this date are fullydepreciated, and, as such, have no remaining book value at the balance sheet dates. All subsequent assetpurchases are stated at cost. The Airport has a policy in place which requires the capitalization of all assetpurchases of $1,000 or greater.

-25-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(A) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - continued

Property and Equipment - continued

No asset values have been recorded for various improvements constructed by tenants at their own expense,which improvements will revert to the Airport at the expiration of the applicable leases.

Prepaid Items - Payments made to vendors for services that will benefit periods beyond year end are recorded asprepaid items.

Restricted Assets - Proceeds from grant awards are classified as restricted assets on the Balance Sheet becausetheir use is limited to capital acquisition and construction. The Airport records the liability for acting as trusteefor security and bid deposits and follows the practice of segregating deposit monies as restricted assets. Alldeposit refunds are made from deposit funds.

Compensated Absences - Employees of the Airport earn annual leave in amounts from 8 to 12 hours per monthbased on years of service. Annual leave may be carried forward provided the amount carried forward does notexceed two years of an employee's earned annual leave. Unused annual leave (in excess of what can be carriedforward) shall be used or surrendered. Upon termination, employees are paid for all accumulated annual leave.This policy resulted in an accrual for compensated absences of $69,282 at December 31, 2006.

Sick leave is credited to all classified employees at the rate of eight hours per month. All unused sick leave iscarried forward from year to year. No payments are due for such accumulated sick leave upon termination orretirement. Therefore, no liability has been accrued in these financial statements.

Cash and Cash Equivalents - For purposes of the Statement of Cash Flows, the Airport considers all highlyliquid debt instruments purchased with an original maturity of three months or less to be cash equivalents.

Investments -Under State law, the Airport may invest in United States bonds, treasury notes or certificates, timecertificates of deposit of State banks having their principal office in the State of Louisiana, or any other federallyinsured investment. In accordance with GASB Statement No. 31, "Accounting and Financial Reporting forCertain Investments and for External Investment Pools", investments meeting the criteria specified in theStatement are stated at fair value. Investments that do not meet the requirements are stated at cost.

Custodial Credit Risk

Deposits and Investments - The Airport is exposed to custodial credit risk as it relates to their deposits andinvestments with financial institutions. The Airport's policy to ensure there is no exposure to this risk is torequire each financial institution to pledge their own securities to cover any amount in excess of FederalDepository Insurance Coverage. These securities must be held in the Airport's name. Accordingly, the Airporthad no custodial credit risk related to its deposits at December 31, 2006.

-26-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(A) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - continued

Use of Estimates - The preparation of financial statements in conformity with accounting principles generallyaccepted in the United States of America requires management to make estimates and assumptions that affect thereported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of thefinancial statements and the reported amounts of revenues and expenses during the reporting period. Actualresults could differ from those estimates.

Post-Employment Benefits - As a component unit of the Consolidated Government of Lafayette, Louisiana, theAirport was required to implement GASB Statement No. 43 - Financial Reporting for Postemployment BenefitPlans Other Than Pensions for the year beginning January 1,2006. The Airport does not offer any of these typesof benefits to employees and therefore has no liability in relation to the implementation of the new statement.

(B) CASH AND INVESTMENTS

State laws authorize the government to invest in obligations of the U.S. Treasury, obligations guaranteed by theUnited States or any agency thereof, and bonds of this state or any subdivision of this state.

All bank balances of deposits and investments as of the Balance Sheet date are entirely insured or col lateral izedby securities held by the government's agent in the government's name.

Investments consist of Certificates of Deposit with maturity dates of greater than one year.

Interest Rate Risk-As a means of limiting its exposure to fair-value losses arising from rising interest rates, theAirport's investment policy limits the investment portfolio to maturities of less than one year.

Credit Risk/Concentration of Credit Risk- Because all investments of the Airport are time certificates of deposit,there is no credit risk or concentration of credit risk.

Cash included in the Statement of Cash Flows at December 31 is as follows:

2006 2005Petty CashOperating AccountPFC AccountSecurity Deposit AccountReserve for Future ProjectsGrant Account

Cash per Statement of Cash Flows

$ 1,2236,270,4501,884,595

22,705140,093920,683

$ 9,239,749

$ 3914,810,0231,114,401

21,71288,454991,020

$ 7,026,001

-27-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(C) AD VALOREM TAXES

Ad valorem taxes attach as an enforceable lien on property as of January 1 of each year. Taxes are levied by theParish Government in early fall and are actually billed to the taxpayers by the Assessor in October orNovember.Billed taxes are due by December 31, becoming delinquent on January 1 of the following year.

The taxes are based on assessed values determined by the Tax Assessor of Lafayette Parish and are collected bythe Lafayette Parish Sheriff The taxes are remitted to the Airport net of a deduction for Assessor's Pension Fundcontributions.

That portion of the ad valorem taxes dedicated to operations and maintenance of the Airport was assessed toproperty owners in Lafayette Parish at 1.71 mills for 2006. On November 17,2001, voters of Lafayette Parishapproved renewal of the ad valorem tax through expiration of the tax in 2012.

(D) PASSENGER FACILITY CHARGE

During the 2000 fiscal year, the Airport submitted an application to the Federal Aviation Administration (FAA)to impose a Passenger Facility Charge (PFC) at the Lafayette Regional Airport. The FAA approved thecollection and use of PFC revenues for specific projects commencing January 30,2001. Under the terms of theagreement with the FAA, the Airport is allowed to charge a $3 PFC per passenger, less an 8 cent collectioncharge from the airline, to generate maximum net cumulative revenues of $2,323,000. Per an agreement withthe FAA, previous PFC amounts collected due to errors by the airlines will be allocated against this PFCapplication with the remaining cost of the project funded by current PFC revenue. During 2002, an amendmentto this application was approved increasing the charge to $4.50 per passenger. The application has subsequentlyhad several amendments, which increased the maximum net cumulative revenues to $2,973,702 and extendedthe charge expiration date to January 1, 2005. The use of this revenue is restricted by the FAA for specificapproved projects in the amount of $2,973,702. The projects funded with this application were completed in thecurrent fiscal year.

During the 2004 fiscal year, the Airport submitted an application to the Federal Aviation Administration (FAA)to impose a Passenger Facility Charge (PFC) at the Lafayette Regional Airport. Approval of this applicationoccurred in February 2005. The FAA approved the collection and use of PFC revenues for specific projectscommencing May 1, 2005. Under the terms of the agreement with the FAA, the Airport is allowed to charge a$4.50 PFC per passenger, to generate maximum net cumulative revenues of $1,967,250. The FAA estimatesthat the charge expiration date will be April 1, 2008. The use of this revenue is restricted by the FAA forspecific approved projects in the amount of $1,967,250.

During the 2006 fiscal year, the Airport submitted an application to the Federal Aviation Administration (FAA)to impose a Passenger Facility Charge (PFC) at the Lafayette Regional Airport. Approval of this applicationoccurred in May 2006. The FAA approved the collection and use of PFC revenues for specific projectscommencing February 1, 2007. Under the terms of the agreement with the FAA, the Airport is allowed tocharge a $4.50 PFC per passenger, to generate maximum net cumulative revenues of $795,000. The FAAestimates that the charge expiration date will be May 1, 2008. The use of this revenue is restricted by the FAAfor specific approved projects in the amount of $795,000.

-28-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(D) PASSENGER FACILITY CHARGE - continued

Additional projects to be funded by uncommitted RFC revenues will require FAA approval. The Airport hasreserved a portion of its retained earnings for undisbursed PFC revenues. PFC revenues available to fund thespecific projects were $2,003,872 at December 31,2006. This amount is shown on the face of the Statement ofNet Assets as Reserved.

(E) GRANT FUNDS RECEIVABLE

The Airport is in the process of performing various airfield improvement projects with the assistance of federaland state funds. Grant funds receivable at December 31, 2006 consisted of the following:

Transportation SafetyAdministration-Security $ 95,928

Small Community Air Service Grant 143,386AIP Project 24 1,538AIP Project 25 18,107AIP Project 30 504,623AIP Project 31 892,788

Total Grant Funds Receivable $ 1,656,370

(F) RESTRICTED ASSETS

Proprietary Fund assets required to be held and/or used as specified in bond resolutions, grant agreements, orother contractual agreements have been reported as Restricted Assets. Restricted Assets at December 31,2006,consisted of the following:

Cash Investments TotalsGrant Funds $ 920,683 $ - $ 920,683Security Deposits 22,705 - 22,705PFC Accounts 1,884,595 - 1,884,595Sinking Fund 1 446,300 446,300

Totals $ 2,827,983 $ 446,300 $ 3,274,283

-29-

(G)

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

PROPERTY AND EQUIPMENT

The following is a summary of changes in property and equipment:

BeginningBalance12/31/05

$41,636,02342,056,714

5,515,20712,087,5992,661,0051,444,540

105,401,088

(52,067,424)$53,333,664

$ 5,521,116$ 4,811,711

Additions

1,571,345

187,0361,564,801

4,460

3,327,642

(3,527,431)$ (199,789)

$$ 5,171,953

EndingBalance

Deletions 12/31/06$ - $41,636,023

43,628,0595,515,207

12,274,6354,225,8061,449,000

108,728,730

(55,594,855)$ - $53,133,875

$ - $ 5,521,116$ 3,241,762 $ 6,741,902

Hangars and BuildingsRunways and Navigation AidsService Roads and ParkingOther Permanent ImprovementsEquipmentFurniture and Fixtures

Less: Accumulated Depreciationand Amortization

Net Property and Equipment

LandConstruction Work in Progress

Depreciation expense for the year ended December 31,2006 was $3,527,431. The total expense was charged toAirport Services.

(H) DEFINED BENEFIT PENSION PLAN

All full-time employees of Lafayette Regional Airport participate in the Parochial Employees' Retirement System(PERS) of Louisiana, a multiple-employer, cost-sharing public employee retirement plan that was established bythe Louisiana Legislature as of January 1,1953 by Act 205 of 1952. The PERS was revised by Act 765 of 1979.The payroll for Airport employees covered by the PERS for the year ended December 31,2006, was $719,315.

All full-time Airport employees who work at least 28 hours a week and are under 60 years of age are members ofthe plan. Airport commissioners may enroll at their option. Members of the plan may retire with thirty years ofcreditable service regardless of age, with twenty-five years of service at age 55, and with ten years of service atage 60.

Benefit rates are one percent of final compensation (average monthly earnings during the highest 36 consecutivemonths or joined months if service was interrupted) plus $2.00 per month for each year of service credited priorto January 1, 1980, and three percent of final compensation for each year of service after January 1, 1980.

-30-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(H) DEFINED BENEFIT PENSION PLAN - continued

The System also provides disability and survivor benefits. Benefits are established by State statute.

Covered employees are required to contribute 9.5 percent of their earnings to the plan. The Airport contributed12.75 percent to the plan. The total contribution for the year ended December 31, 2006 was $160,048, whichconsisted of $91,713 from the Airport and $68,335 from its employees. For the year ended December 31,2005the total contribution was $151,777, which consisted of $86,974 from the Airport and $64,803 from itsemployees. For the year ended December 31, 2004 the total contribution was $137,515, which consisted of$76,038 from the Airport and $61,477 from its employees. Contributions are also established by State statute.

The "pension benefit obligation" is a standardized disclosure measure of the present value of pension benefits,adjusted for the effects of projected salary increases and step-rate benefits, estimated to be payable in the futureas a result of employee service to date. The measure, which is the actuarial present value of credited projectedbenefits, is intended to help users assess the System's funding status on a going-concern basis, assess progressmade in accumulating sufficient assets to pay benefits when due, and make comparisons among PERS andemployers.

The total PERS pension benefit obligation was $1,713,339,532 and the total PERS net assets available forbenefits were $1,535,416,950 as of December 31, 2005.

The PERS also publishes an annual financial report. The latest report for the year ended December 31,2005 isavailable from Parochial Employees' Retirement System of Louisiana, P.O. Box 14619, Baton Rouge, LA70898-4619.

(I) OPERATING LEASES

The Airport leases buildings, hangars, land and terminal space to a number of tenants. Due to the nature of thoseleases, they are all classified as operating leases. The following is a schedule by years of minimum future rentalson non-cancelable operating leases as of December 31, 2006:

Year Ending December 312007 $ 1,784,3902008 1,719,0272009 1,689,4632010 1,643,2812011 1,576,434

Thereafter 17,573,276Total Minimum Future Rentals $ 25,985,871

Certain rentals included above relate to tenants with scheduled annual CPI adjustments. Those annualadjustments could not be determined. Therefore, the 2006 rents were used for all years.

-31 -

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

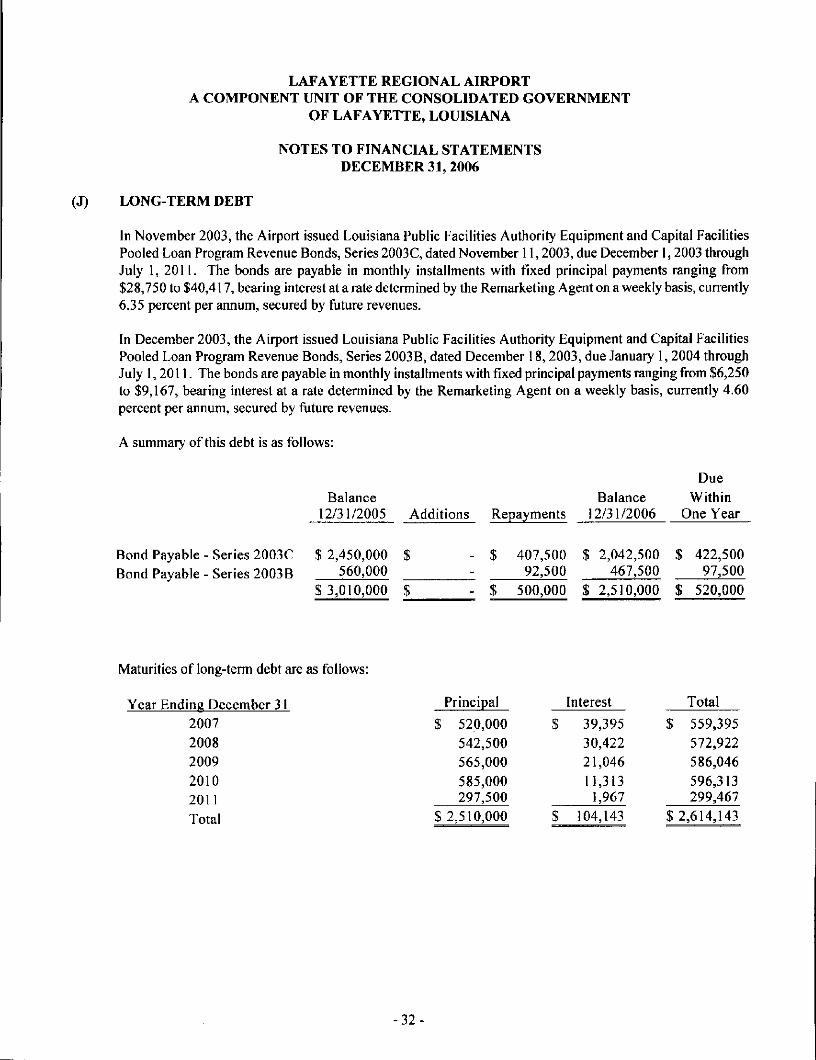

(J) LONG-TERM DEBT

In November 2003, the Airport issued Louisiana Public Facilities Authority Equipment and Capital FacilitiesPooled Loan Program Revenue Bonds, Series 2003C, dated November 11,2003, due December 1,2003 throughJuly 1, 2011. The bonds are payable in monthly installments with fixed principal payments ranging from$28,750 to $40,417, bearing interest at a rate determined by the Remarketing Agent on a weekly basis, currently6.35 percent per annum, secured by future revenues.

In December 2003, the Airport issued Louisiana Public Facilities Authority Equipment and Capital FacilitiesPooled Loan Program Revenue Bonds, Series 2003B, dated December 18,2003, due January 1, 2004 throughJuly 1,2011. The bonds are payable in monthly installments with fixed principal payments ranging from $6,250to $9,167, bearing interest at a rate determined by the Remarketing Agent on a weekly basis, currently 4.60percent per annum, secured by future revenues.

A summary of this debt is as follows:

Balance12/31/2005 Additions Repayments

Balance12/31/2006

DueWithin

One Year

Bond Payable - Series 2003CBond Payable - Series 2003B

$ 2,450,000 $560,000 _

$ 3,010,000 $

407,50092,500

$ 2,042,500467,500

422,50097,500

$ 500,000 $ 2,510,000 $ 520,000

Maturities of long-term debt are as follows:

Year Ending December 3120072008200920102011Total

Principal

$ 520,000542,500565,000585,000297,500

$ 2,510,000

Interest

$ 39,39530,42221,04611,313

1,967$ 104,143

Total

$ 559,395572,922586,046596,313299,467

$2,614,143

-32 -

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

NOTES TO FINANCIAL STATEMENTSDECEMBER 31, 2006

(K) LITIGATION

There is no litigation pending against the Airport as of December 31, 2006.

(L) RISK MANAGEMENT

The Airport is exposed to various risks of loss related to torts; theft of, damage to, and destruction of assets;errors and omissions; and natural disasters. The Airport is insured to reduce the exposure to these risks.

(M) COMMITTMENTS

On a continuing basis, the Airport enters into construction contracts for improvements to the Airport. AtDecember 31, 2006, there are several ongoing projects for which contracts have been entered and work is inprogress. The majority of the costs of these projects are being funded by Airport Improvement Program Grantsthrough the Federal Aviation Administration and the State of Louisiana, Department of Transportation.

In December 2006, the Commission authorized the purchase of an AARF (Airport Rescue and Fire Fighting)vehicle at a total cost of $726,165. The vehicle wil l be funded through a Passenger Facility Charge as discussedin Footnote D.

(N) OTHER MATTERS

During the year under audit, the Louisiana Legislative Auditors' office performed a best practices review of theoperations and administration of the Lafayette Regional Airport. This review resulted in the LegislativeAuditors' Office issuing a report with recommendations intended to improve controls over financial operations,provide advice in implementing good business practices, and to ensure compliance with state laws. This reportis a matter of public record and is available on the Louisiana Legislative Auditors' website.

Additionally, subsequent to the date of these financial statements but prior to the issuance of this report, theDistrict Attorney of the Fifteenth Judicial District completed an investigation into complaints filed against theLafayette Regional Airport Commission. His findings disclosed instances of expenditures that were deemed tobe improper. The District Attorney has issued a statement requiring reimbursement of said funds byCommissioners and staff to the Lafayette Regional Airport. The Airport has subsequently provided the DistrictAttorney with the support for reimbursements of expenditures by Commissioners and staff over the last threeyears, and is currently awaiting a response from the District Attorney regarding this matter. The Airport as anentity has no exposure under the District Attorney's findings, and the District Attorney has indicated that thefindings do not form the basis for criminal actions.

- 3 3 -

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

OF LAFAYETTE, LOUISIANA

SCHEDULE OF REVENUES, EXPENDITURES AND CHANGESIN FUND BALANCE - BUDGET (GAAP BASIS) AND ACTUAL

GENERAL FUNDFOR THE YEAR ENDED DECEMBER 31,2006

REVENUE

Ad Valorem TaxState Revenue Sharing

Total Revenue

OTHER FINANCING USES

Transfer of O & M Funds toProprietary Fund

Total Other Financing Uses

EXCESS OF REVENUES OVEROTHER FINANCING USES

FUND BALANCE, BEGINNING

FUND BALANCE, ENDING

ORIGINALBUDGET

1,680,000

FINALBUDGET

$1,680,000 $1,680,000

1,680,000

VARIANCE2006 FAVORABLE

ACTUAL (UNFAVORABLE)

$1,830,24442,048

1,872,292

(1,680,000) (1,680,000) (1,872,292)

(1,680,000) (1,680,000) (1,872,292)

$ 150,24442,048

192,292

(192,292)

(192,292)

See Accountants' Report.-34-

LAFAYETTE REGIONAL AIRPORTA COMPONENT UNIT OF THE CONSOLIDATED GOVERNMENT

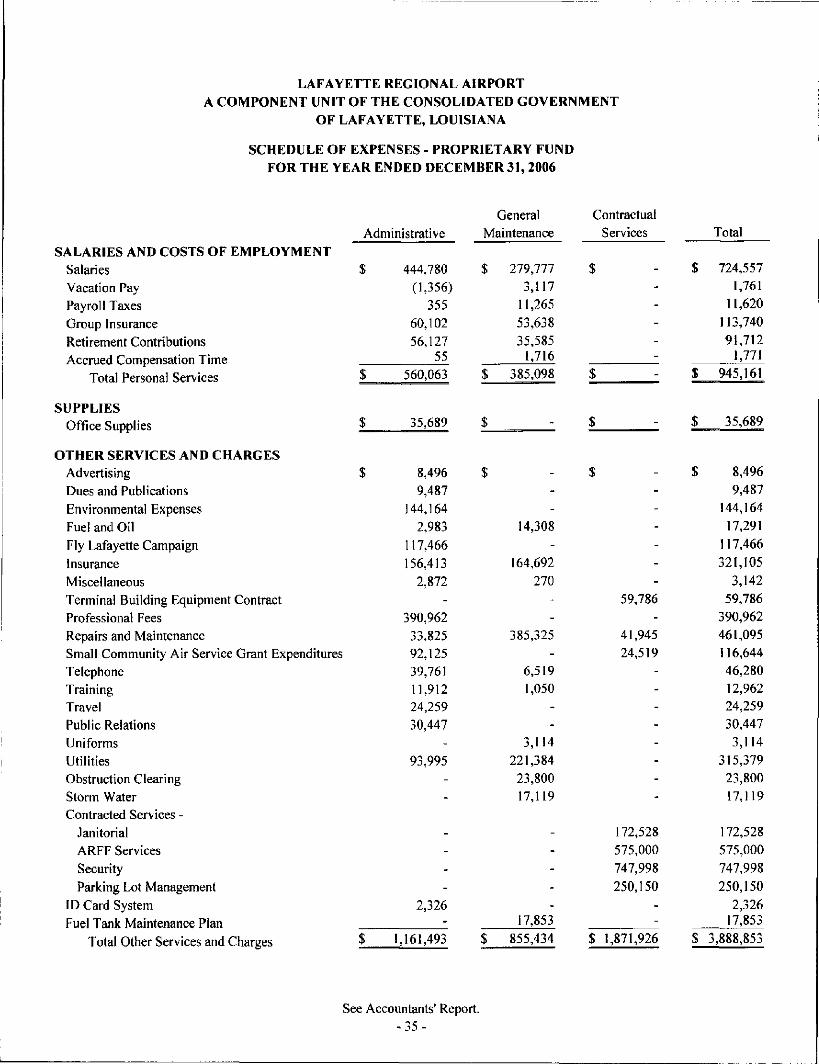

OF LAFAYETTE, LOUISIANA

SCHEDULE OF EXPENSES - PROPRIETARY FUNDFOR THE YEAR ENDED DECEMBER 31, 2006

SALARIES AND COSTS OF EMPLOYMENTSalariesVacation PayPayroll TaxesGroup InsuranceRetirement ContributionsAccrued Compensation Time

Total Personal Services

SUPPLIESOffice Supplies

OTHER SERVICES AND CHARGESAdvertisingDues and PublicationsEnvironmental ExpensesFuel and OilFly Lafayette CampaignInsuranceMiscellaneousTerminal Building Equipment ContractProfessional FeesRepairs and MaintenanceSmall Community Air Service Grant ExpendituresTelephoneTrainingTravelPublic RelationsUniformsUtilitiesObstruction ClearingStorm WaterContracted Services -

JanitorialARFF ServicesSecurityParking Lot Management

ID Card SystemFuel Tank Maintenance Plan

Total Other Services and Charges

Administrative

$ 444,780(1,356)

35560,10256,127

55$ 560,063

35,689

GeneralMaintenance

$ 279,777

3,11711,26553,63835,585

1,716$ 385,098

ContractualServices Total

$ 724,5571,761

11,620

113,740

91,7121,771

$ 945,161

$ 35,689

$ 8,496

9,487

144,164

2,983

117,466

156,413

2,872-

390,962

33,82592,125

39,76111,912

24,259

30,447-

93,995

--

_

---

2,326-

$ 1,161,493

$--

14,308

-164,692

270--

385,325

-6,5191,050

--

3,114221,384

23,80017,119

-

----

17,853

$ 855,434

$ - $ 8,496

9,487

144,164

17,291

117,466

321,105

3,14259,786 59,786

390,962

41,945 461,095

24,519 116,644

46,28012,96224,259

30,4473,114

315,379

23,800

17,119

172,528 172,528

575,000 575,000

747,998 747,998

250,150 250,150

2,32617,853

$ 1,871,926 $ 3,888,853

See Accountants' Report.-35-

0000

om

moo

CMCM SO

O

r-

c-f

COHH

DO-JwHHto"^H

to

-I

AIR

PO

RT

RN

ME

NT

OF

T W

< >

o o

LA

FA

YE

TT

E R

EG

HI C

ON

SO

LID

AT

ED

^^ ^^fflHtoOH2

H

to"

O0-§Ou

COQ

> so!? ^

FE

DE

RA

L A

MB

ER

31,2

0i

t* So ww Q

C O

F E

XP

EN

DIT

UR

TH

E Y

EA

R E

ND

ED

1*1 -D OQ tosUcw

O

CJCQ

00CM o

oCM

SOo

oCM

OCM

eo

C &o

® '-5 -2D, g o

H £ ^s*« ~O C

1 = 1C c l>v o ^

111t;

0)O

0)CO

fa 2

§ tsIIs °-o o

- I13 vS Q

00

c3Ooo

co

T3

O.P

(U•o(D

IX

ut—3*-*

C

cxX

UJ

J3O

00c

o.

0»-CE-

UJHO

WRIGHT, MOORE, DEHART, DUPUIS Sc HUTCHINSON, L.L.C.

JOHN W. WRIGHT, CPA *

JAMES H. DUPUIS, CPA, CFP *

JAN H. COWEN, CPA *

LANCE E. CRAPPELL, CPA *

PAT BAHAM DOUGHT, CPA *

MICAH R. VIDR1NE, CPA *

TRAVIS M. BRINSKO, CPA *

RICK L. STUTES CPA, CVA / ABV, APA '

' A PROFESSIONAL CORPORATION

Certified Public Accountants100 Petroleum Drive, 70508

E O. Box 80569 • Lafayette, Louisiana 70598-0569(337)232-3637 • FAX (337) 235-8557

uww. unruJ4Jfi.com

INDEPENDENT AUDITORS1 REPORT ON INTERNALCONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE ANDOTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS

PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITINGSTANDARDS

To the Board of CommissionersLafayette Airport CommissionLafayette, Louisiana

We have audited the financial statements of the governmental activities, the business-typeactivities and each major fund of Lafayette Regional Airport, A Component Unit of the

T R o M o o R E c p A + Consolidated Government of Lafayette, Louisiana, as of and for the year ended December 31,MICHAELG. DEHART.CPA. CVA. MBA* +2006, which collectively comprise the Airport's basic financial statements and have issued our+RETIRED report thereon dated May 8, 2007. We conducted our audit in accordance with auditing

standards generally accepted in the United States of America, the standards applicable tofinancial audits contained in Government Auditing Standards, issued by the ComptrollerGeneral of the United States, and the provisions of Louisiana Revised Statutes 24:513 and theLouisiana Governmental Audit Guide.

Internal Control Over Financial Reporting

KHISTIE C. BOUDREAUX, CPA

SHEP E COMEAUX, CPA, MBA

ROBERT T. DUCHARME, II, CPA

CHRISTINE R. DUNN, CPA

DANE P. FALGOUT, CPA

MARY PATRICIA KEELEY, CPA

KYLE I. ROBICHEAUX, CPA

DAMIAN H. SPIESS, CPA, CFP

ROBIN G. STOCKTON, CPA

BRIDGET B. TULEY, CPA, MT

PATRICK E. WAGUESPACK, CPA

In planning and performing our audit, we considered Lafayette Regional Airport's internalcontrol over financial reporting as a basis for designing our auditing procedures for the purposeof expressing our opinions on the financial statements, but not for the purpose of expressing anopinion on the effectiveness of the Airport's internal control over financial reporting.

A control deficiency exists when the design or operation of a control does not allowmanagement or employees, in the normal course of performing their assigned functions, toprevent or detect misstatements on a timely basis. A significant deficiency is a controldeficiency, or combination of control deficiencies, that adversely affects the Airport's ability toinitiate, authorize, record, process, or report financial data reliably in accordance with generallyaccepted accounting principles such that there is more than a remote likelihood that amisstatement of the Airport's financial statements that is more than inconsequential will not beprevented or detected by the Airport's internal control.

A material weakness is a significant deficiency, or combination of significant deficiencies, thatresults in more than a remote likelihood that a material misstatement of the financial statementswill not be prevented or detected by the Airport's internal control.

Our consideration of internal control over financial reporting was for the limited purposedescribed in the first paragraph of this section and would not necessarily identify alldeficiencies in internal control that might be significant deficiencies or material weaknesses.We did not identify any deficiencies in internal control over financial reporting that we considerto be material weaknesses, as defined above.

CIRCULAR 230 DISCLOSURE - To ensure compliance with the recently issued U.S. Treasury Circular 230 Notice, unless otherwise expressly indicated, any tax advice contained in this communication,or attachments thereto, was not intended or written to be used, and cannot be used, for the purpose of (1) avoiding tax-related penalties under the Internal Revenue Code, or (ii) promoting, marketing,or recommending any tax-related matter addressed herein.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether Lafayette Regional Airport's financial statements are free ofmaterial misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts andgrant agreements, noncompliance with which could have a direct and material effect on the determination of financialstatement amounts. However, providing an opinion on compliance with those provisions was not an objective of ouraudit and, accordingly, we do not express such an opinion. The results of our tests disclosed no instances ofnoncompliance that are required to be reported under Government Auditing Standards.

This report is intended for the information and use of management and the Board of Commissioners of LafayetteRegional Airport, the Legislative Auditor of the State of Louisiana and the Federal Aviation Administration and is notintended to be and should not be used by anyone other than these specified parties. However, this report is a matter ofpublic record and its distribution is not limited.

t, Moore, <DeJfart,(Dupuis &Jfutcfiinson, LLC

WRIGHT, MOORE, DEHART,DUPUIS & HUTCHINSON, L.L.C.Certified Public Accountants

May 8, 2007

WRIGHT, MOORE, DEHART, DUPUIS 8c HUTCHINSON, L.L.C.Certified Public Accountants

100 Petroleum Drive, 70508P. O. Box 80569 • Lafayette, Louisiana 70598-0569

(337) 232-3637 • FAX (337) 235-8557

JOHN W. WRIGHT, CPA *

JAMES H. DUPUIS, CPA, CFP *

JAN H. COWEN, CPA *

LANCE E. CRAPPELL, CPA *

PAT BAHAM DOUGHT, CPA •

MICAH R. VIDR1NE, CPA *

TRAVIS M. BRINSKO, CPA *

RICK L. STUTES CPA, CVA / ABV, APA *

* A PROFESSIONAL CORPORATION

JOE D. HUTCHINSON, CPA *

+RETIRED

KRISTIE C. BOUDREAUX, CPA

SHEP E COMEAUX, CPA, MBA

ROBERT T. DUCHARME, II, CPA

CHRISTINE R. DUNN, CPA

DANE P. FALGOUT, CPA

MARY PATRICIA KEELEY, CPA

KYLE L. ROBICHEAUX, CPA

DAMIAN H. SPIESS, CPA, CFP

ROBIN G. STOCKTON, CPA

BRIDGET B. TILLEY, CPA, MT

PATRICK E. WAGUESPACK, CPA

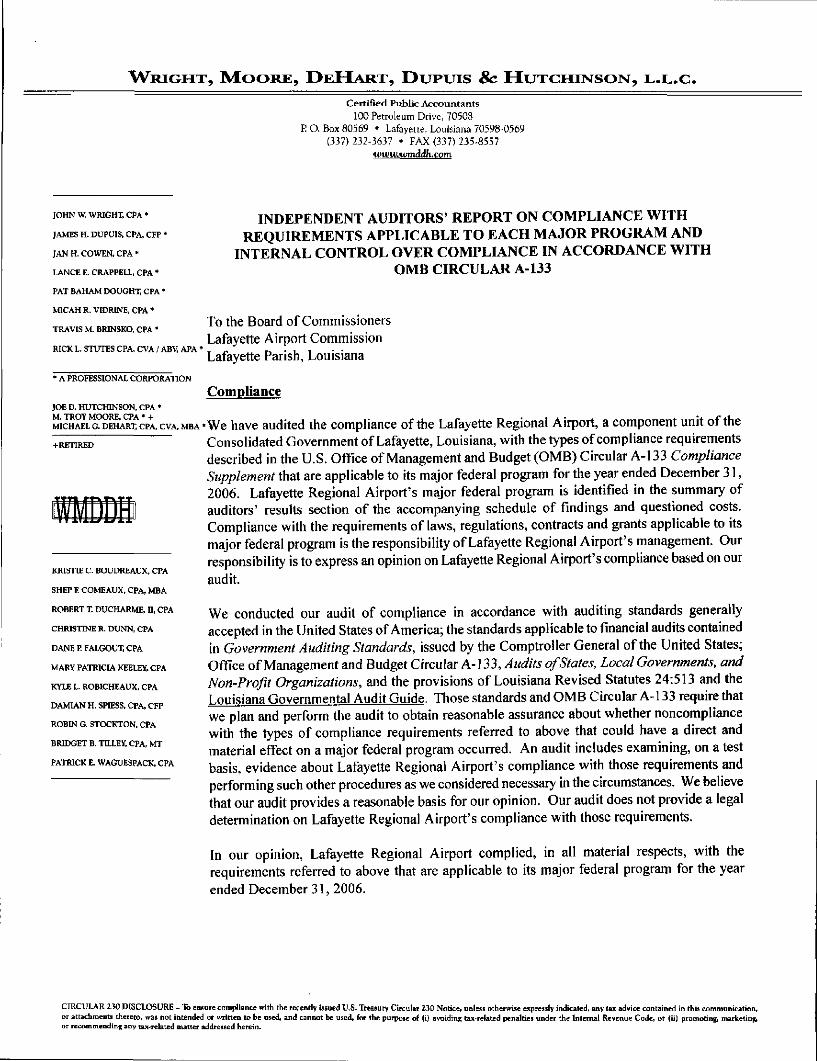

INDEPENDENT AUDITORS' REPORT ON COMPLIANCE WITHREQUIREMENTS APPLICABLE TO EACH MAJOR PROGRAM AND

INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITHOMB CIRCULAR A-133