krause fund research: energy

TRANSCRIPT

Nov 16, 2021 [1] Pioneer Natural Resources Company

60.0080.00

100.00120.00140.00160.00180.00200.00

Price

Investment Thesis Drivers

• PXD will benefit from significantly elevated commodity prices compared 2020 levels. Pioneer’s oil & gas revenues declined 26% in 2020, compared to our forecasted increase of 165%.

• Permian Basin focus provides low breakeven costs. PXD extracts oil in the Midland Basin (located in the Permian) which has one of the lowest breakeven costs anywhere in the United States.

• PXD operates more efficiently than its competitors. PXD possesses one of the lowest oil & gas production expenses compared to its competitors.

• Successful M&A activity has established Pioneer as the dominant player in the Permian (Midland) Basin.

Detractors

• Increasing presence of renewables may lead to lower fossil fuel consumption. Slightly offset by stable natural gas demand, over our forecast, we believe renewables will not pose a challenge for PXD.

• Regulatory scrutiny from the current Presidential Administration. President Biden is continuously looking at ways to enhance environmental friendliness of energy companies which will increase the regulatory burden for PXD.

• Increasing electric vehicle use will negatively impact the demand for crude oil. Ford and other automakers have already outlined their plans achieve a large portion of its revenue through electric vehicle sales. We account for this by slowing PXD’s production after 2025.

Stock Performance 52 wk high: $196.64 52 wk low: $77.10 52 wk return: 107.58% YTD return: 61.07%

Stock Details EPS (2020): ($1.21) Market Cap: $45,486 Beta: 1.18 S/O: 244 million Yield:1.4%

Financial Ratios (5y Avg) Total Debt-to-Equity: 25.1 ROA: 1.9% Current Ratio: 1.4 EBITDA Margin: 36.7%

Krause Fund Research: Energy

Date: 11/16/2021

Recommendation: BUY

Price Target: $220

Company Description Pioneer Natural Resources Company is an oil & gas exploration and production company headquartered in Irving, TX. It is one of the largest landholders in the Permian Basin, with the entirety of its oil producing properties in the Midland Basin. Pioneer produces crude oil, natural gas, and natural gas liquids.

Harrison Ersbo [email protected]

James Huerta [email protected]

Nov 16, 2021 [2] Pioneer Natural Resources Company

Important Disclaimer This report was created by students enrolled in the Applied Equity Valuation (FIN: 4250) class at the University of Iowa. The report was originally created to offer an internal investment recommendation for the University of Iowa Krause Fund and its advisory board. The report also provides potential employers and other interested parties an example of the students’ skills, knowledge and abilities. Members of the Krause Fund are not registered investment advisors, brokers or officially licensed financial professionals. The investment advice contained in this report does not represent an offer or solicitation to buy or sell any of the securities mentioned. Unless otherwise noted, facts and figures included in this report are from publicly available sources. This report is not a complete compilation of data, and its accuracy is not guaranteed. From time to time, the University of Iowa, its faculty, staff, students, or the Krause Fund may hold a financial interest in the companies mentioned in this report.

Nov 16, 2021 [3] Pioneer Natural Resources Company

Executive Summary We recommend a buy rating for Pioneer Natural Resources. The stock offers a 21% upside for investors.

Pioneer Natural Resources will continue to benefit from elevated oil prices in the face of a recovering global economy.

Its centralized Permian Basin location, and subsequent breakeven costs, combined with its low production costs will allow it to weather potential future price declines better than its competitors.

Economic Analysis Real GDP Growth

Real GDP growth (both globally and in the United States) plays a pivotal role in the demand for oil & gas and its related products. The largest component of GDP in the United States is personal consumption, approximately 68.8%.1 This aspect is significant for oil & gas production companies as it relates to demand growth. A productive economy will consume more oil due to personal/commercial transportation, and as an input for manufacturing activities.2 In the United States as of 2020, the largest single use for crude oil was gasoline at 44%.3 A productive and growing economy needs gasoline to move people and goods. Thus, when real GDP increases, so does crude oil demand. On the other hand, natural gas has less of a connection with macroeconomic activity. In the United States, its largest uses include electric power (38%), industrial (33%), and residential (15%).4 Natural gas is a much

more “diversified” fuel relating to its end users. Steady population growth will lead to consistent demand for residential applications (heating buildings, cooking, drying clothes), and in turn, electric power generation due to higher utility users.4 Fluctuations in real GDP affect the demand for commodities produced by Pioneer. However, the link between the two is not as strong as one would expect. During the COVID-19 pandemic, when world GDP fell sharply, Pioneer’s total production (barrels of oil equivalent) grew by 7%.35 US Real GDP is projected to grow by 5.5% and 3.9% in 2021 and 2022 respectively.14 World Real GDP growth will be dependent on many different “re-opening” scnarios. Each country has taken a different approach to the COVID-19 pandemic. In the short term, we believe World Real GDP will grow at rates of 5.8% and 4.4% for 2021 and 2022, respectively.14 After this, we believe Real GDP for both the US and the world will grow in-line with historical levels.

Interest Rates

Interest rate fluctuations can have a large effect on companies with large amounts of debt. Movements in the treasury yield curve will affect a company’s cost of debt, which relates to easier access to debt to finance capital investments. Currently, the 10y treasury (used in our WACC calculation), is 1.56%.5 For the next two years, we expect interest rates increase modestly (+23 to +39 bps) compared to the current US 10y Treasury yield. Over the long-term, 5-10 years, we expect rates to increase by a larger (+61 to +87 bps). These amounts were derived using the forward rates for the 10y Treasury note (10y1y, 10y2y, 10y5y,10y10y). We felt this approach to measuring future interest rates was more sound due to the market based aspect of forward rates. We do not believe Pioneer will face significantly higher borrowing costs. If they do, however, they will be offset by elevated commodity prices.

R² = 0.638

-15-10-505

1015

-10 -5 0 5 10 15

World Oil Consumption vs World GDP Growth

Source: EIA, Statista

Nov 16, 2021 [4] Pioneer Natural Resources Company

Source: Bloomberg

Commodity Prices

Commodity prices are perhaps the single largest determinant of an oil and gas production company’s success. Prices are driven by demand factors (increases in real GDP as mentioned before) and supply factors. On the supply side, production among OPEC participants is a large determinant of crude oil prices, as they represent approximately 40% of the world’s oil production.6 Currently, OPEC plans to increase production by 400,000 bbl/day, but this increase will still result in a deficit between supply and demand.7 We believe that OPEC will continue to keep the market free of excess production as the economy continues to recover. This aspect is reflected in our model using the oil futures curve to determine prices. Natural gas prices are also driven by similar factors to crude oil, but also by seasonal factors such as weather.8 While supply is driven by existing natural gas in storage, and the amount of production.9 Natural gas liquids are a result of extracting natural gas from the ground. I.e., NGLs will follow similar supply and demand drivers as crude oil and natural gas due as their end users are in similar sectors.10 Pioneer Natural Resources will benefit from the elevated commodity prices in the near term. However, over the long term as the economic growth slows to pre-pandemic levels, prices should begin to level-off. This aspect is reflected in our model with the use of both the WTI Crude, and Henry Hub Natural Gas futures curves.

Government Regulations

Since becoming elected, President Joe Biden has promised “climate friendly” regulations on various aspects of the oil and gas industry. For example, he issued a pause on new oil and gas leases on federal land/water shortly after being elected, but it was struck down by a federal judge shortly thereafter.11 However, this regulation would not have impacted Pioneer Natural Resources as they have no exposure to federal land.26 More recently, the EPA announced new rules mandating methane leaks be plugged at hundreds of thousands of oil and gas wells in the U.S.12 These new regulations will apply to both existing and new oil/gas wells, and is an attempt to curb the release of methane into the earth’s atmosphere.12 Currently, the oil and gas industry accounts for 30% of the United States methane emissions. 12 Both examples are part of President Biden’s ambitious goal to cut domestic emissions in half by 2030 and achieve net zero by 2050.12 Looking ahead, Pioneer will have to adjust with regulations and other political implications such as these. We did not factor regulations directly into our model, but rather they are implied through slower crude oil production growth rates post 2025. Therefore, we believe there will be no drastic regulations put in place, but incentives to move toward renewables over fossil fuels.

Industry Analysis

Energy Sector and E&P Industry Description

The energy sector consists of two main components. The first being Oil, Gas, and Consumable Fuels, and the second is Energy Equipment and Services.13 Pioneer Natural Resources and others are in the Oil & Gas Exploration and Production sub-industry, within the Oil, Gas, and Consumable Fuels industry of the energy sector. These companies are known as “upstream” companies because they extract oil from the source and sell it to “midstream” and/or” “downstream” companies. PXD and other upstream oil & gas companies make money by finding, extracting, and transporting oil and natural gas. Upstream companies do not refine or market

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

Spot 1Yr 2Yr 5Yr 10Yr

10Y Forward Rates

Nov 16, 2021 [5] Pioneer Natural Resources Company

anything they produce.13 However, not all firms in this industry are created alike. Some firms, such as BP, ConocoPhillips, or Occidental Petroleum engage in both exploration/production and they refine or market their products. Consequently, while they are large players in the E&P industry, they have different financial characteristics (risks, margins, etc.) that one should be aware of.

Customers/Markets

Oil and gas exploration & production companies sell their products to two main parties: crude oil refiners, and natural gas distribution companies.3 In turn, these companies sell refined products such as gasoline, diesel, etc., to gasoline wholesalers, to fuel stations, petrochemical manufacturers, and other industries where crude oil is a key input.16 Pioneer, for example, has three companies which make up 48.37% of its revenue. The companies include, Occidental Petroleum (OXY), Sunoco LP, and Plains All American Pipeline LP.14

Differentiating Factors

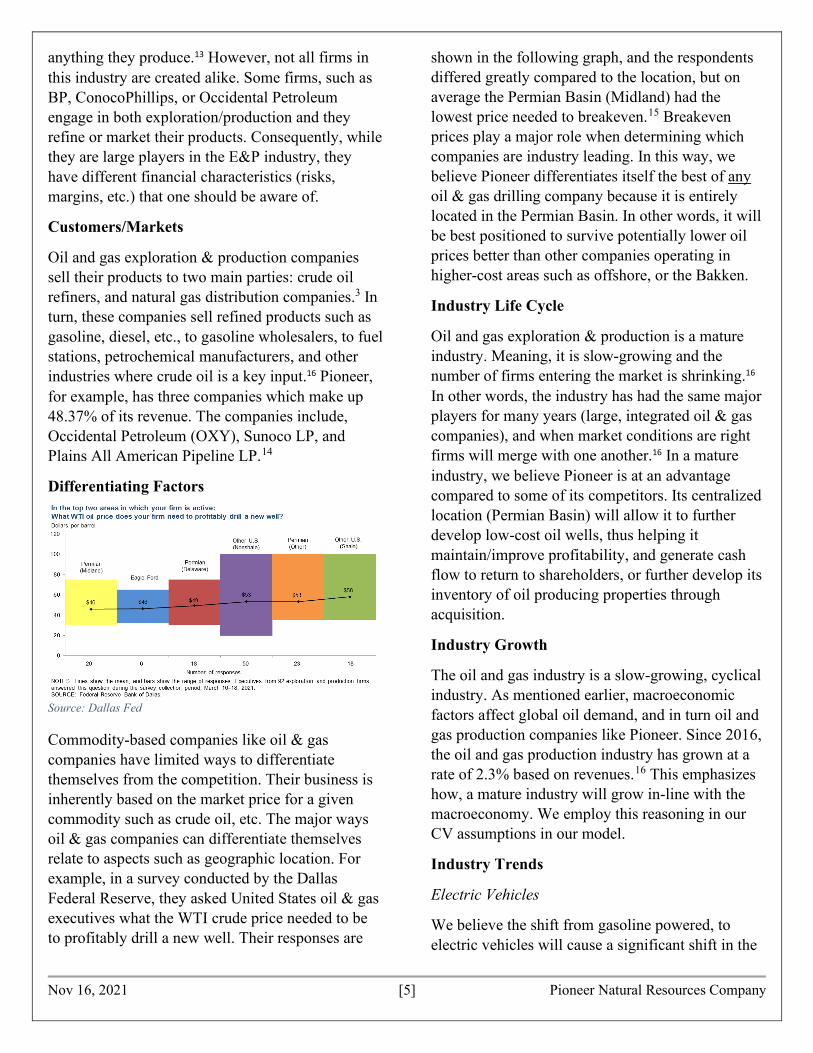

Commodity-based companies like oil & gas companies have limited ways to differentiate themselves from the competition. Their business is inherently based on the market price for a given commodity such as crude oil, etc. The major ways oil & gas companies can differentiate themselves relate to aspects such as geographic location. For example, in a survey conducted by the Dallas Federal Reserve, they asked United States oil & gas executives what the WTI crude price needed to be to profitably drill a new well. Their responses are

shown in the following graph, and the respondents differed greatly compared to the location, but on average the Permian Basin (Midland) had the lowest price needed to breakeven.15 Breakeven prices play a major role when determining which companies are industry leading. In this way, we believe Pioneer differentiates itself the best of any oil & gas drilling company because it is entirely located in the Permian Basin. In other words, it will be best positioned to survive potentially lower oil prices better than other companies operating in higher-cost areas such as offshore, or the Bakken.

Industry Life Cycle

Oil and gas exploration & production is a mature industry. Meaning, it is slow-growing and the number of firms entering the market is shrinking.16 In other words, the industry has had the same major players for many years (large, integrated oil & gas companies), and when market conditions are right firms will merge with one another.16 In a mature industry, we believe Pioneer is at an advantage compared to some of its competitors. Its centralized location (Permian Basin) will allow it to further develop low-cost oil wells, thus helping it maintain/improve profitability, and generate cash flow to return to shareholders, or further develop its inventory of oil producing properties through acquisition.

Industry Growth

The oil and gas industry is a slow-growing, cyclical industry. As mentioned earlier, macroeconomic factors affect global oil demand, and in turn oil and gas production companies like Pioneer. Since 2016, the oil and gas production industry has grown at a rate of 2.3% based on revenues.16 This emphasizes how, a mature industry will grow in-line with the macroeconomy. We employ this reasoning in our CV assumptions in our model.

Industry Trends

Electric Vehicles

We believe the shift from gasoline powered, to electric vehicles will cause a significant shift in the

Source: Dallas Fed

Nov 16, 2021 [6] Pioneer Natural Resources Company

demand for gasoline, ultimately impacting the oil and gas exploration and production industry. Morgan Stanley forecasts EVs will represent 44% of total miles driven by 2040 alone.17 Whether this figure is attained is dependent on factors such as the price of an EV, or the number of EV options for consumers. For example, major auto manufacturers have set ambitious goals and laid out massive investment plans for electric vehicle manufacturing. Ford Motor Company will invest over $30 billion in EVs by 2030, and it aims to have 40% of its global sales volume be completely electric by 2030.18 In this case, 40% of Ford’s global sales using 2019 annual sales represents 2,156 electric vehicles globally. While the average gasoline powered vehicle on the road gets 22 mpg and drives 11,500 miles per year.19 A barrel of oil contains approximately 19 gallons of gasoline.20 Meaning, the average driver consumes (11,500/22) = 523 gallons of gasoline or (523/19) = 28 barrels of oil per year. This shift in Ford’s product mix will result in a decrease in oil consumption of approximately (2,156*523) = 1,127,588 gallons of gas or (1,127,588/19) = 59,347 bbl./year. This figure is not exact, but it can help illustrate the significant impact of a large automaker’s rapid EV adoption. The following chart displays Morgan Stanley’s forecast.

Energy Shift

Natural Gas

While natural gas is not a source of renewable energy, we believe carbon targets will cause an

increase in the demand for natural gas. In almost all cases, coal’s main use is electric power. Currently, 19% of the United States’ electricity is generated by burning coal.21 Over time, we believe this number will be reduced in part by renewables, but mainly due to increasing use of natural gas, a fuel that is much cleaner than coal and other hydrocarbons. For example, Natural gas emits 117 pounds of CO2 per million British thermal units (MMBTU) of natural gas compared to more than 200 pounds of CO2 per MMBtu of coal or over 160 pounds of CO2 per MMBtu of fuel oil.22 While natural gas is not free of carbon emissions, it emits significantly less CO2 than traditional hydrocarbons such as fuel oil.

Renewable Shift

Over time the United States’ energy mix will shift toward renewables. The EIA forecasts by 2050, 41% of the United States’ energy mix will be composed of renewables like hydroelectric power, wind, and solar.23 They also predict that natural gas will hold steady at one-third of the total energy mix.23 While we agree with this forecast, we believe traditional oil E&P companies will have a place in the energy sector. Currently, very little crude oil is used for electricity generation (less than 1%).3 Therefore, we feel a shift toward electric vehicles will be responsible for a decline in oil consumption in the future.

Porter’s Five Forces Porter’s Five Forces is a framework used when viewing how a company is positioned within its competitive landscape.

1. Threat of new entrants is low. Oil and gas exploration and production is an incredibly capital-intensive. Entering the oil & gas industry would require a large amount of capital up-front. New entrants would also have a very difficult time competing with a large established company like Pioneer as it relates to production capabilities and subsequent economies of scale.

2. Degree of rivalry is high. Oil and gas production companies compete on a national

Source: Morgan Stanley

Nov 16, 2021 [7] Pioneer Natural Resources Company

and global scale for oil producing properties and the ability to produce at the lowest cost. Furthermore, integrated oil and gas companies have an advantage over exploration and production companies. Their refining business is integrated with its production, therefore providing a hedge during potential price declines.24

3. Bargaining power of suppliers is low. In the oil and gas production industry, the suppliers are those who extract oil & gas products from the ground.

4. Bargaining power of buyers is low. Prices and demand for oil and gas are on a global scale. Meaning, producers have little to no control over the price and demand for their products.24

5. Threat of substitutes is moderate. Renewable energy sources such as solar, wind, biomass, etc., pose a risk to traditional fossil fuels.24

Competition

Peer Comparison

Pioneer is solely located in the Permian Basin; its closest competitors are those with a similar presence in the region. The following tables display data on Permian Basin operators, and a comparison of financial/leverage metrics.

Peers

• ConocoPhillips (COP): A global, integrated oil & gas company with significant operations in the US, Gulf of Mexico, Canada, China, Indonesia, Malaysia, Australia, Columbia, and Argentina.26

• Hess (HES): An integrated oil & gas production company operating primarily in the Bakken region in North Dakota, Offshore, and Guyana.26

• APA Corp (APA): An oil exploration and production company with operations in the United States, Egypt, and North Sea.26

• EOG Resources (EOG): An integrated oil & gas production company with operations in the

United States (Eagleford and Delaware Basin), Trinidad, China, and Oman. 26

• Diamondback Energy (FANG): A Permian Basin integrated oil & gas production company.26

• Devon Energy (DVN): An oil & gas production company located with operations in Texas (Midland and Eagleford) and Oklahoma.26

• Coterra Energy (CTRA): Formerly Cabot Oil & Gas, Coterra Energy operates in Pennsylvania and produces natural gas.26

The closest direct comparison to Pioneer Natural Resources is Diamondback Energy. It is the only one of Pioneer’s competitors with the entirety of its operations located in the Permian Basin. However, the location differs as Pioneer is entirely located in the Midland Basin, and FANG is in both the Midland and Delaware Basins.26

Operator Lease Count Oil Volume (BBL) Pioneer Natural Resources 2484 107,649,132 Diamondback Energy 1550 81,624,452 XTO Energy 1366 64,419,198 Coterra Energy 1092 63,184,150 Parsley Energy 991 49,864,918 Endeavor Energy Resources 2009 46,047,907 Occidental Petroleum 468 34,378,938 Chevron 1248 30,172,191 SM Energy 448 28,621,556 Anadarko E&P Onshore 835 27,378,257

Source: Texas Railroad Commission

Company Market Value Sales EBITDA Margin

COP 99,910 37,072 25% EOG 56,818 16,742 39% PXD 45,736 14,310 31% DVN 29,781 10,896 25% HES 26,729 6,624 34% FANG 20,457 5,544 66% CTRA 17,378 1,940 45% APA 10,902 6,905 50%

Nov 16, 2021 [8] Pioneer Natural Resources Company

Industry Specific Comparison

Sources: FactSet

Financial and Industry Metrics Summary

The tables/charts display the advantages Pioneer holds over its industry peers. It holds the largest number of leases in the Permian Basin and produces the largest volume of oil.25 Taking note of the industry specific measures, Pioneer has one of the lowest production costs per BOE and has some of the highest quality reserves. Over 90% of its total reserves are developed. Meaning, lower up-front development costs than some of its peers. It is also competitive regarding the life of its reserves at 9.5 years.

M&A

Mergers and acquisition related activity dramatically increased since the prior few years. For example, Pioneer Natural Resources made two large acquisitions in 2020. Specifically, its acquisition of DoublePoint Energy which closed May 4th, 2021, and Parsley Energy which closed on January 12th, 2021. These deals were valued at $6,207.9 billion and $7,583 billion respectively.26 Acquiring DoublePoint Energy allowed Pioneer to expand its already large footprint within the Permian. Pioneer estimates synergies from its Parsley acquisition amounting to $325 million per-year.27 Similarly, Pioneer will realize $175 million in synergies from its DoublePoint acquisition.28 Its competitors have also been taking note of acquisition opportunities given the fortuitous rebound in oil prices. ConocoPhillips recently made a move to overtake Pioneer Natural Resources as the largest Permian player with its acquisition of Shell Enterprises LLC’s (a subsidiary of Royal Dutch Shell) Permian Assets. Specifically, ConocoPhillips paid $9.5 billion in cash for 225,000 net acres of oil producing properties and associated infrastructure.29

Company Analysis Company Overview

Over the last 10 years, Pioneer Natural Resources has evolved from a traditional oil-driller with producing properties in multiple locations, including outside the United States. Now, however,

$- $5.00

$10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00

PXD COP HES DVN EOG FANG APA

2020 Production Costs (BOE)

95.30%

70.90% 69.90%76.40%

51.20%62.00%

91.30%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

PXD COP HES DVN EOG FANG APA

2020 Developed Reserves % of Total

9.50 10.30 10.00

6.10

11.30 12.00

5.40

- 2.00 4.00 6.00 8.00

10.00 12.00 14.00

PXD COP HES DVN EOG FANG APA

2020 Proved Reserve Life Index (Years)

Symbol Total Debt D/E Rating COP 16,154.0 54.1 A- HES 9,075.0 169.1 BBB- APA 9,033.0 #N/A A- EOG 6,752.5 33.3 A- FANG 5,930.0 67.4 BBB- DVN 4,553.0 157.8 BBB- PXD 3,510.0 30.3 BBB CTRA 1,167.5 52.7 N/A

Table Sources: FactSet

Nov 16, 2021 [9] Pioneer Natural Resources Company

it is entirely focused on one region: the Permian Basin in West Texas. It has streamlined its operations, divesting from what are now considered “non-core” assets, and making strategic acquisitions that will further bolster their Permian portfolio.

Production

In 2020, Pioneer produced approximately:

• 77,095 million barrels of crude oil • 31,376 million barrels of natural gas liquids • 155,662 million cubic feet of natural gas

The COVID-19 Pandemic had a modest impact on Pioneer’s crude oil production, falling -1% year-over-year. Growth (or decline) in oil and gas production for pioneer is a factor of more than macroeconomic demand. Capital expenditures play a major role in production growth. A company with high capital expenditures each year will increase its productive capacity in the future.13 Subsequently, lower capital expenditures each year, could mean a producer is expecting a “down year” for oil & gas.13 The relationship between oil prices, capital expenditures, and future production is also important. For example, during fiscal year 2020, Pioneer reduced its capital expenditure budget by 46%, from the subsequent crash in commodity prices and already difficult COVID-19 headwinds.30 With the elevated commodity prices, we believe Pioneer will have a relatively productive year. By taking advantage of M&A opportunities, Pioneer will be able to rebound from a low production/CAPEX year and produce at normal levels.

Source: Statista, Krause Fund Valuation Model

A similar effect can be seen with the number of wells drilled, and the oil price.

Source: FactSet, Statista

Revenue Breakdown

Pioneer Natural Resources generates revenue in two ways. First, they extract oil from the ground and sell it to midstream companies (refineries, pipelines, etc.) which represents their “Oil & Gas” segment. Second, they purchase oil at spot prices, and sell it to fulfill pipeline capacity commitments, which represents their “Sales of Purchased Commodities” segment. An important aspect to note is while sales of purchased commodities represents a large portion of their revenues, it contributes very little (if anything) to their earnings. In 2020, Pioneer’s revenue was composed of:

• 41% crude oil • 7% NGL • 4% natural gas • 48% sales of purchased commodities35

Major Expenses

Oil & Gas Production Expense

Oil and gas production expense represent the costs associated with extracting oil from the ground. Such as, the costs to operate and perform maintenance on wells, and other necessary equipment and facilities.31 For an oil driller, these costs are expressed as a dollar amount per barrel of oil equivalent (BOE). This cost is one of the most significant for Pioneer Natural Resources and can often be a distinguishing factor between oil

0

50

100

150

01000200030004000

CAPEX and Oil Price

CAPEX Oil Price (WTI AVG)

$- $20.00 $40.00 $60.00 $80.00 $100.00 $120.00

0200400600800

1000

Oil Price vs Wells Drilled

Wells Drilled Oil Price

Nov 16, 2021 [10] Pioneer Natural Resources Company

companies. We believe these costs will stay in line with our expectations of $6.41 per BOE.

Production and Ad Valorem Tax

Production taxes are also a significant operating cost for Pioneer Natural Resources. These taxes vary depending on the state, but in Texas, where Pioneer is located, the rate is 4.6% of the market value of the oil produced.32 Ad Valorem taxes represent property taxes paid based on the appraised value of the well containing the oil and gas, as well as the related equipment on the property.33 Production and ad valorem tax will remain at levels comparable to prior years, unless tax rates are increased.

Exploration and Abandonments Cost

Exploration and abandonments cost represent the costs incurred when searching for new oil-producing properties.31

Q3 2021 Earnings Release

Pioneer Natural Resources reported earnings on November 4th, 2021. The company reported basic earnings per share of $4.27, compared to ($0.52) in Q3 2020.34 The increase in earnings was attributable to a rebound in commodity prices compared to the prior quarter.34 These earnings beat Bloomberg consensus estimates of $3.89.14

Capital Expenditures

Pioneer’s capital expenditures fluctuate over time with oil prices. Prior to the pandemic, Pioneer was consistently spending a large portion of its cash flow on capital. A large decline was observed during the COVID-19 pandemic, primarily due to the sharp decline in commodity prices. We observed Pioneer’s CAPEX/Sales ratio in our model. From 2011-2020, it averaged a ratio of 0.6.35 Our assumptions in the forecast period yielded an average CAPEX/Sales ratio of 0.29. This figure makes sense due to our elevated production and

commodity price assumptions in early years, followed by slowing production and stable/falling commodity prices. Moreover, we forecasted CAPEX in the projection period by growing it at the rate of inflation. We believe this was the most accurate way to forecast capital expenditures to account for future unknown risks that could cause an unexpected sharp decline in commodity prices and thus, capital expenditures.

Capital Structure

Long Term Debt

As of Pioneer Natural Resource’s most recent quarterly report, it had $6,685 billion in long-term debt.34 While the company does not provide a target capital structure, it averaged a long-term D/E ratio of 32.54% from 2011-2020.35 Our forecast for Pioneer’s capital structure is slightly lower at an average of 26.99% for 2021-2030.35 We feel this metric is in line with Pioneer’s expectations of paying down existing debt acquired during significant acquisitions in 2020.36 Pioneer has large portions of its debt due in 2025 and 2030 as shown in the following table.

Source: PXD 10-K

Interest Coverage

Interest coverage is critical among oil & gas production companies, due to large amounts of capital financed with debt. From 2011-2020, Pioneer averaged an interest coverage ratio of 2.43x, which represents an amount large enough to cover its interest payments based on its EBIT.35 Our forecasted amount for 2021-2030 is much larger at 29.94x.35 This number reflects our assumptions of higher future oil prices, production, and production

2020 2021E 2022EEPS ($1.21) $11.02 $18.81Est (FactSet) $13.12 $20.69

Debt Maturities 2020 7.50% senior notes due 2020 $— 3.45% senior notes due 2021 140 3.95% senior notes due 2022 244 0.25% convertible senior notes due 2025 1,323 4.45% senior notes due 2026 500 7.20% senior notes due 2028 241 1.90% senior notes due 2030 1,100

Nov 16, 2021 [11] Pioneer Natural Resources Company

costs which result in higher EBIT margins than in the historical period.

Ratings

Pioneer holds investment grade ratings on its long-term debt issues from the three major ratings agencies.14 The subsequent table summarizes the ratings.

Source: Bloomberg

Valuation Model Production and Revenue Growth

We forecasted production growth by looking at historical patterns in production growth for Pioneer Natural Resources. Over our historical period from 2011-2020, Pioneer grew oil production by an average of 20%. We felt this figure better represented production capabilities of the company, than any other forecast methodology. Subsequently, we were able to lower this estimate throughout the projection period to better reflect our assumptions of stable commodity prices and shifts to renewables.

Sales of Purchased Commodities

Pioneer’s sales of purchased commodities business segment is merely a way for them to fulfill capacity commitments. Therefore, we held both sales of purchased commodities, and cost of commodities sold constant throughout the projection period.

Expenses

When forecasting oil & gas production costs, we calculated the historical average of total BOE production costs for lease operating costs, gathering, processing, and transportation, net natural gas plant/gathering, and workover. We obtained an average production cost of $6.41 which we incorporated into our model by multiplying it by BOE production estimates. We applied the same

methodology when calculating production and ad valorem tax and exploration and abandonments expense to achieve values of $2.08 per BOE and $1.30 per BOE.

Dividends and Share Repurchases

Currently, Pioneer has a forward dividend of $2.24 compared to $2.20 in 2020. Recently, Pioneer undertook an ambitious payout policy. Specifically, the company will pay a base dividend (set by the board of directors) and a variable dividend.37 The variable dividend represents 75% of the prior quarters FCF after the base dividend.37 In order to model this, we viewed the base dividend separately from the variable dividend. We grew the base dividend at approximately 10% per year, starting after 2022. When modeling the variable dividend, we used the company’s definition of FCF (Cash from operations less CAPEX). Subsequently, accounted for how the variable dividend represents 75% of only one quarter’s FCF. We feel modeling the dividends in this way allowed us to account for Pioneers aggressive payout policy, while still being realistic as FCF declines in the out years. The prior chart shows the model in practice.

Agency Rating Outlook Moody's Baa2 STABLE S&P BBB STABLE Fitch BBB+ STABLE

0.00

2.00

4.00

6.00

8.00

PXD Dividend Modeling

Variable Dividend (0.25*0.75)/SO Fixed Divdend (PXD Mgmt)

Total dividends per share

Source: Krause Fund Valuation Model

Nov 16, 2021 [12] Pioneer Natural Resources Company

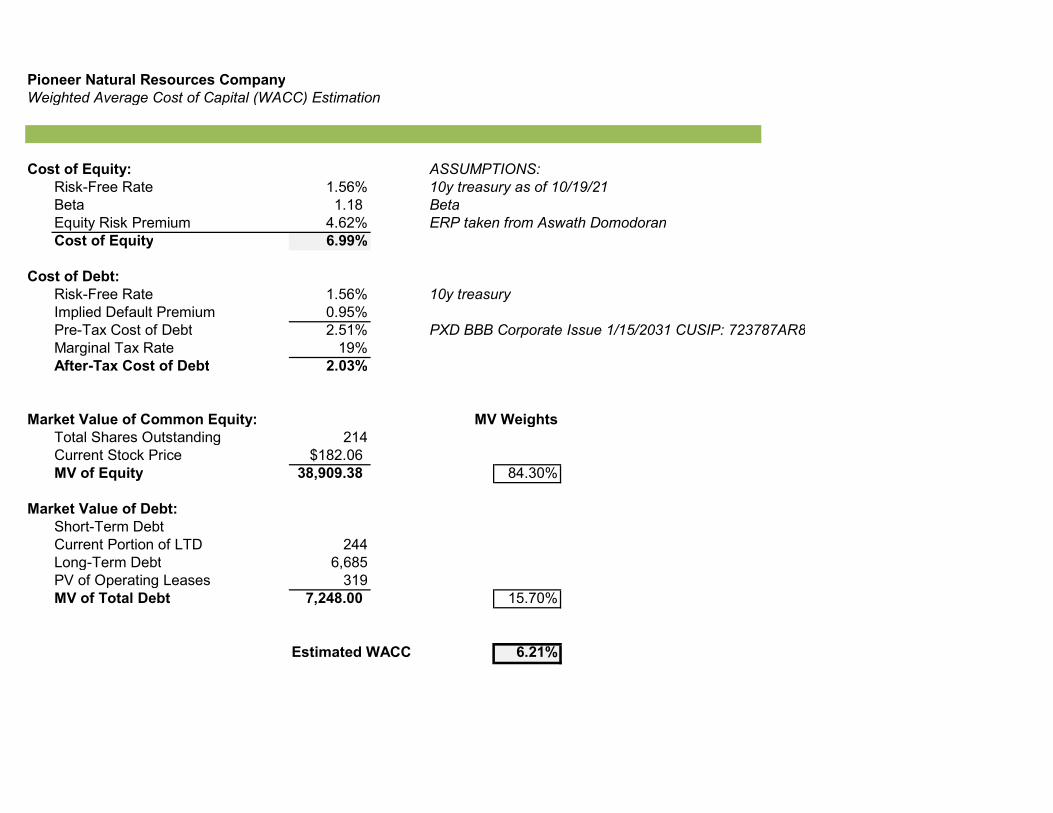

WACC

In our analysis, Pioneer’s capital structure consisted of 84.30% equity, and 15.7% debt.

Cost of Equity

We calculated Pioneer’s cost of equity using the capital asset pricing model. For our risk-free rate, we used the yield of the 10y US Treasury note of 1.56%. For beta, we took the average of the 2-5-, and 10-year weekly beta which resulted in a beta of 1.18. Finally, we used an implied equity risk Premium of 4.62%.38

Cost of Debt

We calculated Pioneer’s after-tax cost of debt using its 10y BBB rated corporate bond (CUSIP:723787AR8) which was yielding 2.51%. We then used our forecasted marginal tax rate of 19% to achieve an after-tax cost of debt of 2.03%.

Overall, Pioneer has a weighted average cost of capital of 6.21%.

Summary

We arrived at a target price of $220 and an associated BUY rating using the discounted cash flow/economic profit valuation model. This target price provides an upside of 21%. We forecasted Pioneer Natural Resource’s future cash flows over a projection period from 2021-2030. We felt this projection period allowed us to incorporate industry trends, and potential regulatory issues into the model. Meaning, our model is relatively conservative in some of its assumptions. For example, our 2030 CV NOPLAT growth assumption is 2%: a number close to but lower than historical economic growth. Furthermore, we forecasted CAPEX at our derived inflation rate of 2.73%, a number lower than historical PPE growth of approximately 8.5%.

Models

DCF/EP

We believe our target price using the DCF/EP model is consistent with our expectations of

production and revenue growth rates. In 2021 we expect NOPLAT of $5,625 billion, compared to $140 in the prior year. We expect this dramatic increase due to a rebound in production and elevated commodity prices. Over our projection period, this number declines to $2,171 by 2030. A similar trend is shown in our economic profit. After negative economic profit in 2020, Pioneer posts economic profit of $4,690. This number also gradually declines by 2030 as Pioneer’s ROIC returns to normal levels.

Relative Valuation

We used price-to-earnings, enterprise value-to-EBITDA, and price-to-sales multiples to value Pioneer on a relative basis. We used comparable companies of ConocoPhillips, EOG Resources, Devon Energy, Diamondback Energy, Coterra Energy, Apache Corporation, and Laredo Petroleum. Averaging each multiple for the 2021 and 2022 estimates yielded a price of $165, lower than the current price of $183. Pioneer trades at lower multiples compared to the average of its competitors (excluding outliers) in terms of P/E. The opposite is true for P/S and EV/EBITDA. Differences in these multiples compared to its competitors potentially reflect the market’s expectation for growth in EPS, EBITDA, and sales. Due to the large differences, we did not incorporate this model into our final valuation.

Dividend Discount Model

Our dividend discount model yielded an unexpectedly low price of $95. Therefore, we decided not to use the DDM in our price target. We found when modeling the dividends using our methods, shareholders equity increased throughout the projection period. Consequently, our CV ROE was very low. Had we modeled dividends based on payout ratio, for example, we would have seen unrealistic assumptions about the size of dividends, and in turn, price, and CV ROE.

Nov 16, 2021 [13] Pioneer Natural Resources Company

Sensitivity Analysis Beta and Equity Risk Premium

Changes in both beta and equity risk premium effect the discount rate, and in turn our valuation. A higher beta indicates higher systematic risk and increases the cost of equity. Whereas a higher equity risk premium indicates a larger excess return over the risk-free rate needed to compensate investors for added risk.

Risk-free Rate and CV Growth of NPLAT

As the risk-free rate increases, Pioneer’s cost of equity will also increase, and subsequently its discount rate. As the CV growth of NOPLAT increases, its valuation will increase due to a larger terminal value. These factors are somewhat offsetting due the CV discounting of the WACC less the growth rate.

WACC and Inflation Rate

In our model, we grew capital expenditures by an implied inflation rate. A higher inflation rate will increase the required return needed by investors. Subsequently, the WACC will increase, thereby increasing the discount rate and lowering valuation.

2030 CV Prod. Growth and Prod. Costs/BOE

As production increases, valuation will also increase. In our sensitivity analysis, as the 2030 production growth increases or decreases by .5%, and production costs are held constant, valuation decreases by approximately $2.20. Therefore, changes in long-term growth does not impact valuation by a significant amount. A scenario of increasing growth and decreasing production costs is most advantageous for Pioneer.

2021 Prod. Growth and 2021 Crude Price

Small changes in production growth affect valuation by a reasonable amount. This is because crude oil is Pioneer’s largest business segment. Small changes in price, a downside/upside of $5, do not affect intrinsic value by a significant amount.

2030 CV Prod. Growth and 2030 Nat. Gas Price

Small changes in production do not affect our estimate for Pioneer’s intrinsic value. However, price increases/decreases have a larger impact on intrinsic value. This is in line with our expectation of natural gas production growing faster than crude oil or NGL.

219.57 1.04 1.09 1.14 1.18 1.24 1.29 1.34 4.32% 259.05 248.63 239.19 232.26 222.76 215.56 208.93 4.42% 253.92 243.77 234.58 227.83 218.57 211.55 205.08 4.52% 249.04 239.15 230.19 223.61 214.57 207.72 201.41 4.62% 244.39 234.74 226.00 219.57 210.76 204.07 197.90 4.72% 239.94 230.53 222.00 215.72 207.11 200.58 194.55 4.82% 235.70 226.50 218.17 212.04 203.63 197.24 191.35 4.92% 231.63 222.65 214.51 208.52 200.29 194.04 188.27

Beta

ERP

219.57 1.25% 1.35% 1.45% 1.56% 1.65% 1.75% 1.85%1.00% 217.99 214.99 212.08 208.99 206.54 203.89 201.33 1.50% 223.79 220.42 217.17 213.72 211.00 208.07 205.24 1.75% 227.21 223.61 220.15 216.48 213.60 210.49 207.50 2.00% 231.06 227.19 223.49 219.57 216.50 213.20 210.02 2.25% 235.43 231.25 227.26 223.06 219.76 216.23 212.84 2.50% 240.43 235.89 231.55 227.01 223.45 219.65 216.01 2.75% 246.22 241.23 236.49 231.53 227.66 223.55 219.61

Risk-free rate

CV

Gro

wth

of N

OPL

AT

219.57 2.13% 2.33% 2.53% 2.73% 2.93% 3.13% 3.33%5.71% 245.88 245.00 244.12 243.23 242.35 241.46 240.57 5.81% 240.60 239.74 238.88 238.02 237.16 236.29 235.43 5.91% 235.58 234.75 233.91 233.07 232.23 231.38 230.54 6.21% 221.91 221.13 220.36 219.57 218.79 218.01 217.22 6.31% 217.76 217.00 216.24 215.48 214.72 213.95 213.18 6.41% 213.80 213.05 212.31 211.57 210.82 210.07 209.32 6.51% 210.00 209.27 208.55 207.82 207.09 206.35 205.62

WAC

C

Inflation Rate

219.57 -0.50% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50%4.91$ 249.64 251.96 254.28 256.60 258.92 261.24 263.56 5.41$ 237.38 239.67 241.97 244.26 246.55 248.85 251.14 5.91$ 225.12 227.38 229.65 231.92 234.18 236.45 238.72 6.41$ 212.86 215.10 217.33 219.57 221.81 224.05 226.29 6.91$ 200.59 202.81 205.02 207.23 209.45 211.66 213.87 7.41$ 188.33 190.52 192.70 194.89 197.08 199.26 201.45 7.91$ 176.07 178.23 180.39 182.55 184.71 186.87 189.03

2030 CV Production Growth

Pro

duct

ion

Cos

ts/B

OE

219.57 22% 23% 24% 25% 26% 27% 28%75.85 198.41 204.14 209.87 215.60 221.33 227.06 232.80 77.85 199.96 205.70 211.45 217.19 222.94 228.68 234.42 79.85 201.51 207.27 213.02 218.78 224.54 230.29 236.05 80.85 202.28 208.05 213.81 219.57 225.34 231.10 236.87 81.85 203.06 208.83 214.60 220.37 226.14 231.91 237.68 83.85 204.61 210.39 216.18 221.96 227.74 233.52 239.31 85.85 206.16 211.96 217.75 223.55 229.34 235.14 240.93

2021 Production Growth

2021

Cru

de P

rice

219.57 1.50% 2% 2.50% 3% 3.50% 4% 4.50%2.81 201.57 201.64 201.71 201.78 201.85 201.91 201.98 3.01 207.46 207.54 207.63 207.71 207.79 207.88 207.96 3.21 213.35 213.45 213.54 213.64 213.74 213.84 213.93 3.41 219.24 219.35 219.46 219.57 219.69 219.80 219.91 3.61 225.13 225.25 225.38 225.51 225.63 225.76 225.89 4.81 260.46 260.67 260.89 261.10 261.31 261.53 261.74 5.01 266.35 266.58 266.81 267.03 267.26 267.49 267.72 20

30 N

at. G

as P

rices

2030 CV Production Growth

Nov 16, 2021 [14] Pioneer Natural Resources Company

References

1 Shares of gross domestic product: Personal consumption expenditures (DPCERE1Q156NBEA) | FRED | St. Louis Fed (stlouisfed.org) 2 Energy & Financial Markets - Crudeoil - U.S. Energy Information Administration (EIA) 3 Use of oil - U.S. Energy Information Administration (EIA))

4 Use of natural gas - U.S. Energy Information Administration (EIA) 5 Daily Treasury Yield Curve Rates 6 Energy & Financial Markets - Crudeoil - U.S. Energy Information Administration (EIA) 7 OPEC cuts 2021 oil demand outlook; still sees big market deficit through year-end | S&P Global Platts (spglobal.com) 8 Factors affecting natural gas prices - U.S. Energy Information Administration (EIA) 9 Factors affecting natural gas prices - U.S. Energy Information Administration (EIA) 10 What are natural gas liquids and how are they used? - Today in Energy - U.S. Energy Information Administration (EIA) 11 Federal judge blocks Biden's pause on new oil, gas leases (apnews.com) 12 Biden EPA gets tough on methane leaks from oil and gas sector (cnbc.com) 13 Fisher, I., Teufel, A., Azelton, A., Lastfisher, I., & Fisher, I. (2009). Fisher investments on energy. ProQuest Ebook Central https://ebookcentral.proquest.com

14Bloomberg

15Dallas Fed survey

16Ross, G. (2021). Oil Drilling & Gas Extraction in the US. IBISWorld Industry Report 21111. Retrieved from IBISWorld

17 Ride-Sharing and Electric Vehicle Growth | Morgan Stanley 18 Ford boosts EV spending, outlines 2030 sales targets, shares near 5-year high | Reuters)

19 (Greenhouse Gas Emissions from a Typical Passenger Vehicle | US EPA) 20 (Frequently Asked Questions (FAQs) - U.S. Energy Information Administration (EIA) 21 (Electricity generation, capacity, and sales in the United States - U.S. Energy Information Administration (EIA)) 22 Natural gas and the environment - U.S. Energy Information Administration (EIA) 23 EIA Renewables Forecast 24 Glickman, Ko. (2021). Oil, Gas, and Consumable Fuels. Net Advantage Industry Survey. Retrieved from S&P Net Advantage 25 Texas Railroad Commission Permian Top 10 26 FactSet 27 Pioneer Parsley Acquisition 28 Pioneer DoublePoint Acquisition 29 Shell sale of Permian business 30 Pioneer Natural Resources Announces 2020 Capital Spending Reduction, Prioritizing Balance Sheet Strength and Free Cash Flow Generation | Pioneer Natural Resources Company (pxd.com) 31 U.S. Energy Information Administration (EIA) - Analysis 32 Crude Oil Production Tax (texas.gov) 33 Tax Information - PDC Energy 34 PXD Q3 10-Q 35 Krause Fund Valuation Model 36 PXD 2020 10-K 37 Pioneer Natural Resources Declares Variable Dividend on Common Shares | Pioneer Natural Resources Company (pxd.com) 38 Damodoran

Graph Sources - Data • West Texas Intermediate oil price annually 1976-2021 | Statista

Pioneer Natural Resources CompanyIncome Statement

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E CV (2030E)

REVENUESOil and gas 4,991 4,916 3,630 9,626 10,207 9,630 9,248 9,056 8,921 8,920 9,011 9,119 9,262

Sales of purchased commodities 4,388 4,755 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394

Interest and other income (loss), net 38 76 (67) 22 87 76 94 128 124 120 124 118 129

Derivative gain (loss), net (292) 55 (281) (2,024) - - - - - - - - -

Gain (loss) on disposition of assets, net 290 (477) 9 14 - - - - - - - - -

Total Revenues 9,415 9,325 6,685 11,033 13,688 13,100 12,737 12,578 12,440 12,435 12,529 12,631 12,785

EXPENSESOil and gas production 855 874 682 992 1,123 1,168 1,191 1,214 1,230 1,247 1,263 1,280 1,297

Production and ad valorem taxes 284 299 242 321 364 378 386 393 398 404 409 414 420

Depletion, depreciation and amortization 1,534 1,711 1,639 1,894 2,075 2,271 2,482 2,711 2,959 3,227 3,517 3,831 4,170

Purchased commodities 3,930 4,472 3,633 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394

Impairment of oil and gas properties 77 - - - - - - - - - - - -

Exploration and abandonments 114 58 47 202 228 237 242 247 250 253 257 260 264

General and administrative 381 324 244 672 713 672 646 632 623 623 629 637 647

Accretion of discount on asset retirement obligations 14 10 9 5 5 5 5 5 5 5 5 5 5

Interest 126 121 129 83 174 99 101 138 121 112 122 120 153

Other 849 448 321 556 690 661 642 634 627 627 632 637 645

Total Expenses 8,164 8,317 6,946 8,119 8,766 8,884 9,089 9,369 9,608 9,891 10,228 10,578 10,994

Income (loss) before income taxes 1,251 1,008 (261) 2,913 4,922 4,215 3,648 3,209 2,832 2,543 2,302 2,053 1,791 Income tax benefit (provision) (276) (235) 61 558 943 808 699 615 543 487 441 393 343

Net Income (loss) 975 773 (200) 2,355 3,979 3,408 2,949 2,594 2,289 2,056 1,861 1,659 1,448

Net loss attributable to noncontrolling interests 3 - - - - - - - - - - - - Net income (loss) attributable to common stockholders 978 773 (200) 2,355 3,979 3,408 2,949 2,594 2,289 2,056 1,861 1,659 1,448

Net income (loss) per share attributable to common stockholders:Basic 5.71$ 4.60$ (1.21)$ 11.02$ 18.81$ 16.26$ 14.20$ 12.61$ 11.22$ 10.16$ 9.26$ 8.32$ 7.31$ Basic weighted average shares outstanding 171 167 216 214 212 210 208 206 204 202 201 199 198Dividends per-share 0.32$ 1.20$ 2.20$ 6.77$ 6.20$ 5.19$ 4.97$ 4.81$ 4.66$ 4.60$ 4.57$ 4.52$ 4.48$

Pioneer Natural Resources CompanyRevenue Decomposition

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E CV (2030E)

ProductionAnnual Sales Volumes

Oil (Mbbls) 69,583 77,509 77,095 96,369 115,643 121,425 123,853 126,330 127,593 128,869 130,158 131,460 132,774 NGLs (MBbls) 23,280 26,398 31,376 31,690 32,007 32,327 32,650 32,976 33,306 33,639 33,976 34,315 34,659 Gas (MMcf) 153,588 133,245 155,662 160,332 165,142 170,096 175,199 180,455 185,869 191,445 197,188 203,104 209,197 Total (MBOE) 116,794 126,114 134,415 154,780 175,173 182,101 185,703 189,382 191,878 194,416 196,998 199,626 202,299

GrowthOil (Mbbls) 20% 11% -1% 25% 20% 5% 2% 2% 1% 1% 1% 1% 1%NGLs (MBbls) 16% 13% 19% 1% 1% 1% 1% 1% 1% 1% 1% 1% 1%Gas (MMcf) 19% -13% 17% 3% 3% 3% 3% 3% 3% 3% 3% 3% 3%Total (MBOE) 17% 8% 7% 3% 3% 3% 3% 3% 3% 3% 3% 3% 3%

Average PricesOil (per Bbl) 57.36 53.77 37.24 80.85 74.91 68.63 65.10 62.47 60.67 59.56 59.17 59.05 59.05 NGL (per Bbl) 29.84 19.33 15.62 31.41 25.94 21.37 19.17 18.46 18.37 18.99 19.59 19.89 20.44 Gas (per Mcf) 2.13 1.79 1.73 5.24 4.32 3.56 3.20 3.08 3.06 3.17 3.27 3.32 3.41 Revenue (per BOE) 42.73 38.98 27.01 62.19 58.27 52.88 49.80 47.82 46.50 45.88 45.74 45.68 45.78

GrowthOil (per Bbl) 19% -6% -31% 117% -7% -8% -5% -4% -3% -2% -1% 0% 0%NGL (per Bbl) 55% -35% -19% 101% -17% -18% -10% -4% 0% 3% 3% 2% 3%Gas (per Mcf) -19% -16% -3% 203% -17% -18% -10% -4% 0% 3% 3% 2% 3%Revenue (per BOE) 21% -9% -31% 130% -6% -9% -6% -4% -3% -1% 0% 0% 0%

Total Production RevenueOil (per Bbl) 3,991 4,168 2,871 7,791.41 8,663.07 8,333.27 8,062.53 7,892.27 7,740.67 7,675.68 7,701.13 7,762.69 7,840.65 NGL (per Bbl) 695 510 490 995.47 830.11 690.87 626.03 608.60 611.74 638.84 665.72 682.65 708.47 Gas (per Mcf) 327 239 269 839.42 713.84 605.87 559.88 555.06 568.97 605.95 643.95 673.41 712.72 Revenue (per BOE) 4,991 4,916 3,631 9,626.30 10,207.02 9,630.01 9,248.44 9,055.93 8,921.38 8,920.48 9,010.80 9,118.76 9,261.84

Total Oil and Gas Revenue 5,013 4,916 3,630 9,626 10,207 9,630 9,248 9,056 8,921 8,920 9,011 9,119 9,262 Growth 42% -2% -26% 165% 6% -6% -4% -2% -1% 0% 1% 1% 2%

Sales of Purchased CommoditiesRevenues 4,388 4,755 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394

Pioneer Natural Resources CompanyBalance Sheet (In Millions)

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E CV (2030E)

ASSETSCurrent assets:Cash and cash equivalents 825 631 1,442 5,598 4,841 6,054 8,230 7,961 7,709 7,977 7,563 8,265 6,544 Short term investments 443 - - - - - - - - - - - - Restricted Cash - 74 59 - - - - - - - - - - Accounts receivable:

Trade, net 694 1,032 695 1,670 1,666 1,571 1,509 1,478 1,456 1,456 1,470 1,488 1,511 Due from affiliates 120 3 - - - - - - - - - - -

Income taxes receivable 7 7 4 1 14 24 20 18 15 14 12 11 10 Notes recievable - - - - - - - - - - - - - Inventories 242 205 224 340 705 665 639 625 616 616 622 630 640 Prepaid Expenses - - - - - - - - - - - - - Derivatives 52 32 5 4 4 4 4 4 4 4 4 4 4 Investment in affiliate 172 187 123 144 - - - - - - - - - Other 25 20 43 45 45 45 46 46 46 46 46 46 47 Total Current Assets 2,580 2,191 2,595 7,802 7,275 8,364 10,448 10,131 9,847 10,112 9,719 10,445 8,755

LONG TERM ASSETSOil and gas properties, using the successful efforts method of accounting:Proved & unproved properties 21,766 23,028 24,510 27,011 29,580 32,367 35,391 38,672 42,232 46,093 50,282 54,828 59,759 Accumulated depletion, depreciation and amortization (8,218) (8,583) (10,071) (11,965) (14,039) (16,310) (18,792) (21,504) (24,463) (27,690) (31,207) (35,037) (39,207)

Total oil and gas properties, net 13,548 14,445 14,439 15,046 15,541 16,057 16,599 17,169 17,769 18,403 19,076 19,790 20,551 Other property and equipment, net 1,291 1,632 1,584 1,763 1,946 2,134 2,328 2,527 2,731 2,941 3,156 3,378 3,605 Operating lease right-of-use assets 280 197 319 332 345 359 374 389 405 422 440 458 Long term Investment 125 - - - - - - - - - - - - Investment in unconsolidated affiliate - - - - - - - - - - - - - Goodwill 264 261 261 261 261 261 261 261 261 261 261 261 261 Derivatives 21 3 3 3 3 3 3 3 3 3 3 3 Other assets, net 95 258 150 136 137 137 138 138 139 139 140 140 141 Total Long Term Assets 15,323 16,897 16,634 17,528 18,219 18,938 19,688 20,471 21,292 22,153 23,058 24,012 25,020

Total Assets 17,903 19,088 19,229 25,330 25,494 27,302 30,136 30,602 31,138 32,265 32,777 34,457 33,775

CURRENT LIABILITIESAccounts payable:

Trade 1,441 1,221 928 2,227 3,091 2,916 2,801 2,742 2,702 2,701 2,729 2,761 2,805 Due to affiliates 183 190 102 168 391 368 354 346 341 341 345 349 354

Interest payable 53 53 35 30 59 33 34 47 41 38 41 41 52 Income taxes payable 2 3 4 18 24 21 18 16 14 12 11 10 9 Deferred income taxes - - - - - - - - - - - - - Liabilities held for sale - - - - - - - - - - - - - Current portion of long-term debt 450 140 244 1,323 500 241 1,100 Derivatives 27 12 234 155 156 156 157 157 158 159 159 160 161 Operating leases - 136 100 158 165 171 178 186 193 201 210 218 228 Other 112 431 363 364 366 367 369 370 372 373 374 376 377 Total Current Liabilities 1,818 2,496 1,906 3,365 4,251 4,034 5,234 4,364 3,820 4,067 3,869 5,015 3,985

LONG TERM LIABILITIESLong-term debt 2,284 1,839 3,160 6,685 3,926 4,039 4,164 4,304 4,453 4,617 4,792 4,978 5,176 Derivatives 8 66 151 152 152 153 153 154 155 155 156 156 Deferred income taxes 1,152 1,393 1,366 1,833 1,834 1,835 1,836 1,837 1,839 1,840 1,841 1,842 1,843 Operating leases 170 110 220 Other liabilities 538 1,046 1,052 1,013 1,017 1,021 1,025 1,029 1,033 1,037 1,041 1,045 1,049

SHAREHOLDERS EQUITYAdditional paid-in capital & Common Stock 9,064 9,163 9,325 9,325 9,325 9,325 9,325 9,325 9,325 9,325 9,325 9,325 9,325 Treasury stock (423) (1,069) (1,234) (1,649) (2,063) (2,478) (2,892) (3,307) (3,721) (4,136) (4,550) (4,965) (5,379) Retained earnings 3,470 4,042 3,478 4,386 7,053 9,374 11,292 12,896 14,235 15,361 16,303 17,060 17,620 Noncontrolling interest in consolidated subsidiariesDeferred hedge losses, net of taxTotal Equity 12,111 12,136 11,569 12,063 14,315 16,221 17,725 18,915 19,839 20,550 21,078 21,421 21,566

Liabilities & Shareholders Equity 17,903 19,088 19,229 25,330 25,494 27,302 30,136 30,602 31,138 32,265 32,777 34,457 33,775

Pioneer Natural Resources CompanyHistorical Cash Flow Statement

Fiscal Years Ending Dec. 31 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

CASH FLOWS FROM OPERATING ACTIVITIESNet income (loss) 882 243 (799) 930 (273) (556) 833 975 773 (200)

Adjustments to reconcile net income (loss)

Depletion, depreciation and amortization 607 810 889 1,047 1,385 1,480 1,400 1,534 1,711 1,639

Impairment of oil and gas properties 354 533 1,495 - 1,056 32 285 77 — —

Impairment of inventory and other property and equipment 62 8 86 8 2 11 38 3

Exploration expenses, including dry holes 47 125 21 90 28 42 22 27 8 11 Deferred income taxes 189 85 (224) 552 (178) (379) (519) 274 240 (52) Gain on disposition of assets, net 4 (58) (209) (9) (782) (2) (208) (290) 477 (9) Loss on early extinguishment of debt - 27 Accretion of discount on asset retirement obligations 8 10 12 12 12 18 19 14 10 9 Discontinued operations (377) (19) 633 251 (4) - - - - Interest expense 31 36 17 17 18 13 5 5 9 51 Derivative related activity (222) 69 164 (609) (3) 851 174 (270) (8) 325 Amortization of stock-based compensation 41 63 71 84 90 89 79 85 100 72 Invesment in affiliate valuation adjustment (15) 64 South texas contingent consideration valuation adjustment 45 42 South texas deficiency fee obligation, net - 80 Amortization of deferred revenue 45 (42) - -Other 22 (40) (6) 34 38 66 74 658 105 125 Change in operating assets and liabilitiesAccounts receivable, net (47) (28) (123) (29) 54 (134) (122) (52) (227) 309 Income taxes receivable 29 (6) 3 (18) (20) 40 (4) -Inventories (137) 33 (39) (37) 8 (32) (35) (70) (20) (20) Derivatives (24) - - -Investments 8 4 -Prepaid expenses (3) 1 (1) (3) - (22) -Other current assets 2 14 4 1 - (7) (3) (1) (33) 24 Accounts payable 136 46 209 104 (258) 58 134 321 (7) (179) Interest payable (2) 11 (6) (22) 25 3 (9) (5) - (19) Income taxes payable (8) (10) - 1 1 (2) - Other current liabilities 61 (38) (27) (38) (35) (44) (45) (55) (91) (219)

Net cash provided by (usied in) operating activities 1,530 1,838 2,146 2,366 1,248 1,498 2,090 3,242 3,115 2,083

CASH FLOWS FROM INVESTING ACTIVITIESProceeds from disposition of assets, net of cash sold 819 96 711 877 553 507 352 469 149 60 Payments for acquisition, net of cash acquired (297) - - (428) - - Proceeds from investments 902 1,465 1,373 624 - Purchase of investments (2,741) (899) (669) - (1) Distribution from unconsolidated subsidiary (90) - 25 - - - - - Additions to oil and gas properties (1,927) (2,758) (2,639) (3,243) (2,110) (1,857) (2,365) (3,520) (2,988) (1,602) Additions to other assets and other property and equipment, net (363) (297) (237) (333) (283) (203) (336) (263) (232) (125)

Net cash provided by (used in) investing activities (1,561) (3,256) (2,140) (2,699) (1,840) 3,820 (1,783) (2,610) (2,447) (1,668)

CASH FLOWS FROM FINANCING ACTIVITIES

Borrowings under long-term debt 197 1,777 467 523 998 - - 2,414 Principal payments on long-term debt (295) (612) (1,547) (523) - (455) (485) (450) - (1,198) Proceeds from issuance of common stock, net of issuance costs - 1,281 980 - 2,534 - - - -

Puchase of derivatives related to issuance of convertibles - (113)

Procceds from issuance of partnership 123 - - - -

Borrowings under credit facility - 800

Repayment of credit facility - (800)

Distributions to noncontrolling interests (27) (36) (36) (1) (1) - - -

Payments of other liabilities (1) (1) (4) - 6 - - (23) (14) (173) Exercise of long-term incentive plan stock options and emp. Stock purchases 4 7 10 13 7 6 8 6 9 Purchase of treasury stock (40) (63) (20) (34) (31) (25) (36) (179) (653) (176) Excess tax benefits from stock-based payment arrangements 31 58 18 19 7 1 - - Payment of financing fees (9) (9) - - (9) - - (4) - (36) Dividends paid (10) (10) (11) (12) (12) (13) (14) (55) (127) (346)

Net cash provided by (used in) financing activities 457 1,111 158 965 958 2,049 (529) (703) (788) 381

Net increase (decrease) in cash and cash equivalents 426 (308) 164 632 366 (273) (222) (71) (120) 796 Cash and cash equivalents, beginning of period 111 537 229 393 1,025 1,391 1,118 896 825 705 Cash and cash equivalents, end of period 537 229 393 1,025 1,391 1,118 896 825 705 1,501

Pioneer Natural Resources CompanyForecasted Cash Flow Statement

Fiscal Years Ending Dec. 31 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E CV (2030E)

Net income $2,355 $3,979 $3,408 $2,949 $2,594 $2,289 $2,056 $1,861 $1,659 $ 1,448

CASH FLOWS FROM OPERATING ACTIVITIESAdjustments to reconcile net income (loss)

Depletion, depreciation, and amortization 1,894 2,075 2,271 2,482 2,711 2,959 3,227 3,517 3,831 4,170 Change in deferred tax liabilities 467 1 1 1 1 1 1 1 1 1 Restricted cash 59 - - - - - - - - - Accounts receivable (975) 4 94 62 31 22 0 (15) (18) (23)Income taxes receivable 3.00 (12.98) (9.64) 3.39 2.72 2.10 1.81 1.38 1.16 1.19 Inventories (116) (365) 40 26 13 9 0 (6) (7) (10)Derivative asset (short-term) 1.00 (0.02) (0.02) (0.02) (0.02) (0.02) (0.02) (0.02) (0.02) (0.02) Other current assets (2.00) (0.18) (0.18) (0.18) (0.18) (0.18) (0.18) (0.18) (0.18) (0.18) Accounts payable

Trade 1,299 864 (175) (116) (58) (41) (0) 27 33 43 Due to affiliates 66 223 (22) (15) (7) (5) (0) 3 4 5

Interest payable (5) 29 (26) 1 12 (6) (3) 3 (1) 11 Derivative liability (short-term) (79.00) 1 1 1 1 1 1 1 1 1 Investment in affiliate (21) 144 - - - - - - - - Other current liabilities 1 1 1 1 1 1 1 1 1 1 Income taxes payable 14 6 (3) (3) (2) (2) (1) (1) (1) (1) Operating lease liability 58 6 7 7 7 8 8 8 9 9

Net cash provided by (used in) operating activities 5,020 6,955 5,587 5,401 5,308 5,239 5,291 5,402 5,513 5,657

CASH FLOWS FROM INVESTING ACTIVITIESAdditions to oil and gas properties (2,501) (2,569) (2,787) (3,024) (3,281) (3,559) (3,862) (4,189) (4,545) (4,931)Additions to other assets and other property and equipment, net (179) (183) (188) (194) (199) (204) (210) (216) (221) (227) Change in operating lease ROU assets (122) (13) (13) (14) (15) (15) (16) (17) (18) (19) Derivative asset (long-term) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) Other assets 14 (1) (1) (1) (1) (1) (1) (1) (1) (1)

Net cash provided by (used in) investing activities (2,788) (2,766) (2,990) (3,232) (3,495) (3,779) (4,088) (4,422) (4,785) (5,178)

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from issuance of debt 3,525 (2,759) 113 125 140 150 163 176 186 198 Changes in current portion of long-term debt 104 (244) - 1,323 (823) (500) 241 (241) 1,100 (1,100) Lease liabilities 110 (220) - - - - - - - - Derivative liability (long-term) 85.00 0.59 0.59 0.59 0.60 0.60 0.60 0.60 0.61 0.61 Other liabilities (39) 4 4 4 4 4 4 4 4 4 Payment of dividends (1,447) (1,313) (1,087) (1,031) (990) (950) (931) (918) (902) (888) Purchase of treasury stock (415) (415) (415) (415) (415) (415) (415) (415) (415) (415)

Net cash provided (used in) by financing activities 1,924 (4,946) (1,384) 7 (2,083) (1,711) (936) (1,393) (26) (2,201)

Net increase (decrease) in cash and cash equivalents 4,156 (757) 1,213 2,176 (270) (251) 267 (413) 702 (1,722) Cash and cash equivalents, beginning of period 1,442 5,598 4,841 6,054 8,230 7,961 7,709 7,977 7,563 8,265

Cash and cash equivalents, end of period 5,598 4,841 6,054 8,230 7,961 7,709 7,977 7,563 8,265 6,544

Pioneer Natural Resources CompanyCommon Size Income Statement

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E (CV) 2030EREVENUES

Oil and gas 53.01% 52.72% 54.30% 87.25% 74.57% 73.51% 72.61% 72.00% 71.72% 71.74% 71.92% 72.19% 72.44%Sales of purchased commodities 46.61% 50.99% 50.77% 30.76% 24.79% 25.91% 26.65% 26.98% 27.28% 27.29% 27.09% 26.87% 26.55%Interest and other income (loss), net 0.40% 0.82% -1.00% 0.20% 0.64% 0.58% 0.74% 1.02% 1.00% 0.97% 0.99% 0.93% 1.01%Derivative gain (loss), net -3.10% 0.59% -4.20% -18.35% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Gain (loss) on disposition of assets, net 3.08% -5.12% 0.13% 0.13% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Total Revenues 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

EXPENSESOil and gas production 9.08% 9.37% 10.20% 9.00% 8.21% 8.91% 9.35% 9.65% 9.89% 10.03% 10.08% 10.13% 10.15%Production and ad valorem taxes 3.02% 3.21% 3.62% 2.91% 2.66% 2.89% 3.03% 3.13% 3.20% 3.25% 3.26% 3.28% 3.28%Depletion, depreciation and amortization 16.29% 18.35% 24.52% 17.16% 15.16% 17.33% 19.49% 21.56% 23.79% 25.95% 28.07% 30.33% 32.62%Purchased commodities 41.74% 47.96% 54.35% 30.76% 24.79% 25.91% 26.65% 26.98% 27.28% 27.29% 27.09% 26.87% 26.55%Impairment of oil and gas properties 0.82% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Exploration and abandonments 1.21% 0.62% 0.70% 1.83% 1.67% 1.81% 1.90% 1.96% 2.01% 2.04% 2.05% 2.06% 2.06%General and administrative 4.05% 3.47% 3.65% 6.09% 5.21% 5.13% 5.07% 5.03% 5.01% 5.01% 5.02% 5.04% 5.06%Accretion of discount on asset retirement obligations 0.15% 0.11% 0.13% 0.05% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04%Interest 1.34% 1.30% 1.93% 0.75% 1.27% 0.75% 0.80% 1.09% 0.97% 0.90% 0.97% 0.95% 1.19%Other 9.02% 4.80% 4.80% 5.04% 5.04% 5.04% 5.04% 5.04% 5.04% 5.04% 5.04% 5.04% 5.04%

Total Expenses 86.71% 89.19% 103.90% 73.59% 64.04% 67.82% 71.36% 74.49% 77.23% 79.55% 81.63% 83.75% 85.99%

Income (loss) before income taxes 13.29% 10.81% -3.90% 26.41% 35.96% 32.18% 28.64% 25.51% 22.77% 20.45% 18.37% 16.25% 14.01%Income tax benefit (provision) -2.93% -2.52% 0.91% 5.06% 6.89% 6.16% 5.49% 4.89% 4.36% 3.92% 3.52% 3.11% 2.68%

Net income (loss) 10.36% 8.29% -2.99% 21.35% 29.07% 26.01% 23.15% 20.63% 18.40% 16.54% 14.85% 13.14% 11.32%

Pioneer Natural Resources CompanyCommon Size Balance Sheet

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E (CV) 2030E

ASSETSCurrent assets:Cash and cash equivalents 4.61% 3.31% 7.50% 22.10% 18.99% 22.17% 27.31% 26.01% 24.76% 24.72% 23.08% 23.99% 19.37%Short term investments 2.47% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Restricted Cash 0.00% 0.39% 0.31% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Accounts receivable:Trade, net 3.88% 5.41% 3.61% 6.59% 6.53% 5.76% 5.01% 4.83% 4.68% 4.51% 4.49% 4.32% 4.47%Due from affiliates 0.67% 0.02% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Income taxes receivable 0.04% 0.04% 0.02% 0.00% 0.05% 0.09% 0.07% 0.06% 0.05% 0.04% 0.04% 0.03% 0.03%Notes recievable 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Inventories 1.35% 1.07% 1.16% 1.34% 2.77% 2.44% 2.12% 2.04% 1.98% 1.91% 1.90% 1.83% 1.89%Prepaid Expenses 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Derivatives 0.29% 0.17% 0.03% 0.02% 0.02% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01%Investment in affiliate 0.96% 0.98% 0.64% 0.57% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Other 0.14% 0.10% 0.22% 0.18% 0.18% 0.17% 0.15% 0.15% 0.15% 0.14% 0.14% 0.13% 0.14%Total current assets 14.41% 11.48% 13.50% 30.80% 28.54% 30.63% 34.67% 33.11% 31.62% 31.34% 29.65% 30.31% 25.92%

LONG TERM ASSETSOil and gas properties, using the successful efforts method of accounting:Proved & unproved properties 121.58% 120.64% 127.46% 106.64% 116.03% 118.55% 117.44% 126.37% 135.63% 142.86% 153.41% 159.12% 176.93%Accumulated depletion, depreciation and amortization -45.90% -44.97% -52.37% -47.24% -55.07% -59.74% -62.36% -70.27% -78.56% -85.82% -95.21% -101.68% -116.08%

Total oil and gas properties, net 75.67% 75.68% 75.09% 59.40% 60.96% 58.81% 55.08% 56.10% 57.06% 57.04% 58.20% 57.44% 60.85%Other property and equipment, net 7.21% 8.55% 8.24% 6.96% 7.63% 7.82% 7.72% 8.26% 8.77% 9.11% 9.63% 9.80% 10.67%Operating lease right-of-use assets 0.00% 1.47% 1.02% 1.26% 1.30% 1.26% 1.19% 1.22% 1.25% 1.26% 1.29% 1.28% 1.36%Long term Investment 0.70% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Investment in unconsolidated affiliate 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Goodwill 1.47% 1.37% 1.36% 1.03% 1.02% 0.96% 0.87% 0.85% 0.84% 0.81% 0.80% 0.76% 0.77%Derivatives 0.00% 0.11% 0.02% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01%Other assets, net 0.53% 1.35% 0.78% 0.54% 0.54% 0.50% 0.46% 0.45% 0.45% 0.43% 0.43% 0.41% 0.42%Total long term assets 85.59% 88.52% 86.50% 69.20% 71.46% 69.37% 65.33% 66.89% 68.38% 68.66% 70.35% 69.69% 74.08%

Total assets 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

CURRENT LIABILITIESAccounts payable:

Trade 8.05% 6.40% 4.83% 8.79% 12.12% 10.68% 9.29% 8.96% 8.68% 8.37% 8.33% 8.01% 8.30%Due to affiliates 1.02% 1.00% 0.53% 0.66% 1.53% 1.35% 1.17% 1.13% 1.10% 1.06% 1.05% 1.01% 1.05%

Interest payable 0.30% 0.28% 0.18% 0.12% 0.23% 0.12% 0.11% 0.15% 0.13% 0.12% 0.13% 0.12% 0.15%Income taxes payable 0.01% 0.02% 0.02% 0.07% 0.09% 0.08% 0.06% 0.05% 0.04% 0.04% 0.03% 0.03% 0.03%Deferred income taxes 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Liabilities held for sale 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Current portion of long-term debt 0.00% 2.36% 0.73% 0.96% 0.00% 0.00% 4.39% 1.63% 0.00% 0.75% 0.00% 3.19% 0.00%Derivatives 0.15% 0.06% 1.22% 0.61% 0.61% 0.57% 0.52% 0.51% 0.51% 0.49% 0.49% 0.46% 0.48%Operating leases 0.00% 0.71% 0.52% 0.63% 0.65% 0.63% 0.59% 0.61% 0.62% 0.62% 0.64% 0.63% 0.67%Other 0.63% 2.26% 1.89% 1.44% 1.43% 1.35% 1.22% 1.21% 1.19% 1.16% 1.14% 1.09% 1.12%Total current liabilities 10.15% 13.08% 9.91% 13.28% 16.67% 14.77% 17.37% 14.26% 12.27% 12.60% 11.81% 14.56% 11.80%

LONG TERM LIABILITIESLong-term debt 12.76% 9.63% 16.43% 26.39% 15.40% 14.79% 13.82% 14.06% 14.30% 14.31% 14.62% 14.45% 15.32%Derivatives 0.00% 0.04% 0.34% 0.60% 0.59% 0.56% 0.51% 0.50% 0.49% 0.48% 0.47% 0.45% 0.46%Deferred income taxes 6.43% 7.30% 7.10% 7.24% 7.19% 6.72% 6.09% 6.00% 5.90% 5.70% 5.62% 5.35% 5.46%Operating leases 0.00% 0.89% 0.57% 0.87% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Other liabilities 3.01% 5.48% 5.47% 4.00% 3.99% 3.74% 3.40% 3.36% 3.32% 3.21% 3.18% 3.03% 3.11%

SHAREHOLDERS EQUITYAdditional paid-in capital 50.63% 48.00% 48.49% 36.81% 36.58% 34.16% 30.94% 30.47% 29.95% 28.90% 28.45% 27.06% 27.61%Treasury stock -2.36% -5.60% -6.42% -6.51% -8.09% -9.07% -9.60% -10.80% -11.95% -12.82% -13.88% -14.41% -15.93%Retained earnings 19.38% 21.18% 18.09% 17.32% 27.67% 34.33% 37.47% 42.14% 45.72% 47.61% 49.74% 49.51% 52.17%Noncontrolling interest in consolidated subsidiaries 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Deferred hedge losses, net of tax 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Total equity 67.65% 63.58% 60.16% 47.62% 56.15% 59.41% 58.82% 61.81% 63.71% 63.69% 64.31% 62.17% 63.85%

Liabilities & Shareholders Equity 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Pioneer Natural Resources CompanyValue Driver Estimation

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E (CV) 2030E

NOPLAT:Operating Revenue 9,379 9,671 7,024 13,020 13,601 13,024 12,642 12,450 12,315 12,314 12,405 12,513 12,656 Operating Expenses

Oil & Gas Production 855 874 682 992 1,123 1,168 1,191 1,214 1,230 1,247 1,263 1,280 1,297 Production and ad valorem taxes 284 299 242 321 364 378 386 393 398 404 409 414 420 SG&A Expenses 381 324 244 672 713 672 646 632 623 623 629 637 647 Depletion, depreciation and amortization 1,534 1,711 1,639 1,894 2,075 2,271 2,482 2,711 2,959 3,227 3,517 3,831 4,170 Purchased commodities (cogs) 3,930 4,472 3,633 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 3,394 Exploration and abandonments 114 58 47 202 228 237 242 247 250 253 257 260 264 Implied interest on operating leases 17 7 5 8 8 9 9 9 10 10 11 11 12 Other 849 448 321 556 690 661 642 634 627 627 632 637 645

EBITA 1,449 1,492 221 4,997 5,022 4,252 3,669 3,233 2,843 2,550 2,315 2,071 1,831 Adjusted Taxes

Marginal Tax Rate 22% 22% 19% 19% 19% 19% 19% 19% 19% 19% 19% 19% 19%Income Tax Provision 276 235 (61) (558) (943) (808) (699) (615) (543) (487) (441) (393) (343)

Less: Interest and Other Income (loss), net 8 17 (13) 4 17 14 18 25 24 23 24 23 25 Less: Derivative Gain (loss), net (64) 12 (54) (388) - - - - - - - - - Less: Gain (loss) on disposition of assets, net 64 (106) 2 3 - - - - - - - - - Add: Impairment of Oil and Gas Properties 17 - - - - - - - - - - - - Add: Interest Expense 28 27 25 16 33 19 19 26 23 21 23 23 29

Total Adjusted Taxes 313 339 29 (161) (926) (803) (697) (613) (543) (489) (441) (393) (339) Change in Deferred Taxes 274 240 (52) 467 1 1 1 1 1 1 1 1 1 NOPLAT 1,410 1,393 140 5,625 5,950 5,056 4,367 3,847 3,387 3,040 2,757 2,465 2,171

Invested Capital (IC):Operating assets

Cash 284 280 207 549 582 549 527 516 509 508 514 520 528 Accounts Receivable 694 1,032 695 1,670 1,666 1,571 1,509 1,478 1,456 1,456 1,470 1,488 1,511 Due from Affiliates 120 3 - - - - - - - - - - - Income Taxes Receivable 7 7 4 1 14 24 20 18 15 14 12 11 10 Inventories 242 205 224 340 705 665 639 625 616 616 622 630 640 Prepaid Expenses - - - - - - - - - - - - - Other 25 20 43 45 45 45 46 46 46 46 46 46 47

Total Operating Assets 1,372 1,547 1,173 2,605 3,012 2,854 2,741 2,683 2,642 2,640 2,665 2,695 2,735

Operating LiabilitiesAccounts Payable 1,624 1,411 1,030 2,395 3,481 3,285 3,155 3,089 3,043 3,043 3,073 3,110 3,159 Income Taxes Payable 2 3 4 18 24 21 18 16 14 12 11 10 9 Interest Payable 53 53 35 30 59 33 34 47 41 38 41 41 52 Other 112 431 363 364 366 367 369 370 372 373 374 376 377

Total Operating Liabilities 1,791 1,898 1,432 2,807 3,930 3,706 3,575 3,521 3,469 3,466 3,500 3,537 3,597 Operating Working Capital (419) (351) (259) (203) (919) (851) (834) (839) (827) (826) (836) (842) (862)

Net PPEOil & Gas Properties, net 13,548 14,445 14,439 15,046 15,541 16,057 16,599 17,169 17,769 18,403 19,076 19,790 20,551 Other Propery and Equipment, net 1,291 1,632 1,584 1,763 1,946 2,134 2,328 2,527 2,731 2,941 3,156 3,378 3,605 Total Net PPE 14,839 16,077 16,023 16,809 17,487 18,192 18,927 19,695 20,500 21,344 22,232 23,168 24,157

Other long-term operating assetsPresent Value of Operating Leases 1,039 280 197 319 332 345 359 374 389 405 422 440 458 Other Assets 95 258 150 136 137 137 138 138 139 139 140 140 141 Total other long-term operating assets 1,134 538 347 455 469 482 497 512 528 544 562 580 599

Other long-term operating liabilitiesOther long-term operating liabilities 538 1,046 1,052 1,013 1,017 1,021 1,025 1,029 1,033 1,037 1,041 1,045 1,049

Total other long-term operating liabilities 538 1,046 1,052 1,013 1,017 1,021 1,025 1,029 1,033 1,037 1,041 1,045 1,049 INVESTED CAPITAL 15,017 15,218 15,059 16,048 16,019 16,802 17,564 18,340 19,167 20,025 20,917 21,861 22,845

Free Cash Flow (FCF):NOPLAT 1,410$ 1,393$ 140$ 5,625$ 5,950$ 5,056$ 4,367$ 3,847$ 3,387$ 3,040$ 2,757$ 2,465$ 2,171$ Change in IC 1,451$ 201$ (159)$ 989$ (29)$ 782$ 763$ 775$ 828$ 858$ 892$ 944$ 984$ FCF (41.35)$ 1,191.84$ 299.59$ 4,636$ 5,979$ 4,274$ 3,605$ 3,072$ 2,560$ 2,182$ 1,865$ 1,521$ 1,187$

Return on Invested Capital (ROIC):NOPLAT 1,410$ 1,393$ 140$ 5,625$ 5,950$ 5,056$ 4,367$ 3,847$ 3,387$ 3,040$ 2,757$ 2,465$ 2,171$ Beginning IC 13,565$ 15,017$ 15,218$ 15,059$ 16,048$ 16,019$ 16,802$ 17,564$ 18,340$ 19,167$ 20,025$ 20,917$ 21,861$ ROIC 10.39% 9.28% 0.92% 37.35% 37.08% 31.56% 25.99% 21.90% 18.47% 15.86% 13.77% 11.78% 9.93%

Economic Profit (EP):Beginning IC $ 13,565 $ 15,017 $ 15,218 $ 15,059 $ 16,048 $ 16,019 $ 16,802 $ 17,564 $ 18,340 $ 19,167 $ 20,025 $ 20,917 $ 21,861 x (ROIC - WACC) 4.18% 3.07% -5.29% 31.14% 30.86% 25.35% 19.78% 15.69% 12.26% 9.65% 7.56% 5.57% 3.72%EP $ 567.48 $ 460.63 $ (804.84) $ 4,690 $ 4,953 $ 4,061 $ 3,324 $ 2,756 $ 2,248 $ 1,850 $ 1,513 $ 1,166 $ 813

Pioneer Natural Resources CompanyWeighted Average Cost of Capital (WACC) Estimation

Cost of Equity: ASSUMPTIONS:Risk-Free Rate 1.56% 10y treasury as of 10/19/21Beta 1.18 BetaEquity Risk Premium 4.62% ERP taken from Aswath DomodoranCost of Equity 6.99%

Cost of Debt:Risk-Free Rate 1.56% 10y treasuryImplied Default Premium 0.95%Pre-Tax Cost of Debt 2.51% PXD BBB Corporate Issue 1/15/2031 CUSIP: 723787AR8Marginal Tax Rate 19%After-Tax Cost of Debt 2.03%

Market Value of Common Equity: MV WeightsTotal Shares Outstanding 214Current Stock Price $182.06MV of Equity 38,909.38 84.30%

Market Value of Debt:Short-Term DebtCurrent Portion of LTD 244Long-Term Debt 6,685PV of Operating Leases 319MV of Total Debt 7,248.00 15.70%

Estimated WACC 6.21%

Pioneer Natural Resources CompanyDiscounted Cash Flow (DCF) and Economic Profit (EP) Valuation Models

Key Inputs: CV Growth of NOPLAT 2.00% CV Year ROIC 9.93% WACC 6.21% Cost of Equity 6.99%

Fiscal Years Ending Dec. 31 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E CV (2030E)

DCF Model:Free Cash Flow (FCF) 4,636 5,979 4,274 3,605 3,072 2,560 2,182 1,865 1,521 1,187 Continuing Value (CV) 41,172 PV of FCF 4,365 5,300 3,567 2,833 2,273 1,783 1,431 1,152 884 23,938

Value of Operating Assets: 47,527 Non-Operating Adjustments

Current Portion LT Debt (244) LT Debt (6,685) Operating Lease (319) Derivatives:

ST Asset 4 LT Asset 3 ST Liability (155) LT Liability (151)

Excess Cash 4,720 Value of Equity 44,700 Shares Outstanding 214 Intrinsic Value of Last FYE 209.15$ Implied Price as of Today 219.57$

EP Model:Economic Profit (EP) 4,690 4,953 4,061 3,324 2,756 2,248 1,850 1,513 1,166 813 Continuing Value (CV) 19,311 PV of EP 4,416 4,391 3,390 2,612 2,039 1,566 1,213 935 678 11,228

Total PV of EP 32,468 Invested Capital (last FYE) 15,059 Value of Operating Assets: 47,527 Non-Operating Adjustments

Current Portion of LT Debt (244) LT Debt (6,685) Operating Lease (319) Derivatives:

ST Asset 4 LT Asset 3 ST Liability (155) LT Liability (151)

Excess Cash 4,720 Value of Equity 44,700 Shares Outstanding 214 Intrinsic Value of Last FYE 209.15$ Implied Price as of Today 219.57$

Pioneer Natural Resources CompanyDividend Discount Model (DDM) or Fundamental P/E Valuation Model

Fiscal Years Ending Dec. 31 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E CV (2030E)

EPS 11.02$ 18.81$ 16.26$ 14.20$ 12.61$ 11.22$ 10.16$ 9.26$ 8.32$ 7.31$

Key Assumptions CV growth of EPS 2.00% CV Year ROE 6.76% Cost of Equity 6.99%

Future Cash Flows P/E Multiple (CV Year) 14.1 EPS (CV Year) 7.31$ Future Stock Price 103.14$ Dividends Per Share 6.77$ 6.20$ 5.19$ 4.97$ 4.81$ 4.66$ 4.60$ 4.57$ 4.52$ Discounted Cash Flows 6.33$ 5.42$ 4.24$ 3.79$ 3.43$ 3.10$ 2.86$ 2.66$ 2.46$ 56.15$

Intrinsic Value as of Last FYE 90.45$ Implied Price as of Today 94.96$

Pioneer Natural Resources CompanyRelative Valuation Models

EPS EPS P/E P/E 2021E 2022E 2021E 2022E 2021E 2022E 2021E 2022ETicker Company Price 2021E 2022E 2021E 2022E EV EBITDA EBITDA EV/EBITDA EV/EBITDA MKT Cap Sales Sales P/S P/SCOP ConocoPhillips $71.71 $5.48 $6.59 13.09 10.88 108,572 19,573 22,544 5.55 4.82 103,150 42,999 46,113 2.40 2.24 EOG EOG Resources $94.93 $7.44 $8.92 12.76 10.64 56,718 10,456 11,473 5.42 4.94 54,906 17,938 19,572 3.06 2.81 DVN Devon Energy $42.11 $3.06 $4.71 13.76 8.94 32,548 5,183 6,723 6.28 4.84 27,527 10,629 11,998 2.59 2.29 FANG Diamondback Energy $109.46 $9.33 $15.84 11.73 6.91 27,895 4,070 5,301 6.85 5.26 20,222 5,815 6,699 3.48 3.02 CTRA Coterra Energy $20.60 $1.97 $2.90 10.46 7.10 19,309 2,018 4,519 9.57 4.27 18,432 2,919 5,225 6.31 3.53 APA Apache Corporation $29.38 $4.09 $4.18 7.18 7.03 19,888 4,502 4,543 4.42 4.38 10,641 6,899 6,967 1.54 1.53 LPI Laredo Petroleum $71.96 ($8.91) $23.42 (8.08) 3.07 2,469 483 854 5.11 2.89 2,469 1,211 1,427 2.04 1.73

Average 13.20 10.15 Average 6.73 4.83 Average 3.86 2.91

NEE Pioneer Natural Resources Company$182.06 $ 11.02 $ 18.81 16.5 9.7 45,031 4,890 7,171 9.2 6.3 39,324 11,033 13,688 3.56 2.87

Implied Relative Value: P/E (EPS21) $ 145.49 P/E (EPS22) 191.00$ EV/EBITDA 21 148.99$ EV/EBITDA 22 115.89$ P/S 21 199.30$ P/S 22 188.36$

164.84$

Pioneer Natural Resources CompanyKey Management Ratios

Fiscal Years Ending Dec. 31 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E

Liquidity Ratios:Current Ratio (CA/CL) 1.42 0.88 1.36 2.32 1.71 2.07 2.00 2.32 2.58 2.49 2.51 2.08 2.20 Quick Ratio (CA-INV/Current Liabilities) 1.29 0.80 1.24 2.22 1.55 1.91 1.87 2.18 2.42 2.34 2.35 1.96 2.04 Cash Ratio (Cash/Current Liabilities) 0.45 0.25 0.76 1.66 1.14 1.50 1.57 1.82 2.02 1.96 1.95 1.65 1.64

Asset-Management Ratios:Total Asset Turnover (Sales/Avg Total Assets) 0.20 0.27 0.26 0.16 0.38 0.39 0.34 0.30 0.29 0.28 0.27 0.27 0.27 Fixed Asset Turnover (Sales/Net Fixed Assets) 0.63 0.58 0.42 0.66 0.78 0.72 0.67 0.64 0.61 0.58 0.56 0.55 0.53 Receivables Turnover Ratio (Sales/Avg Accounts Rec.) 12.95 10.09 7.73 9.33 8.21 8.09 8.27 8.42 8.48 8.54 8.56 8.54 8.53 Inventory Turnover Ratio (Sales/Avg Inventory) 41.48 41.72 31.17 39.12 26.20 19.12 19.54 19.90 20.04 20.18 20.23 20.17 20.14 Capex to Sales (Capex/Sales) 0.40 0.35 0.26 0.24 0.20 0.23 0.25 0.28 0.30 0.33 0.35 0.38 0.40