kom 2002 elkom tel · tel kom t elkom group annual report 2002 tel kom te lkom group annual report...

TRANSCRIPT

Telkomwww.telkom.co.za

TelkomGroup Annual Report2002

Telkom

Telkom G

roup A

nnual Rep

ort 20

02

Telkom AR Covers 26370 8/20/02 15:53 Page 1

This Annual Report does not constitute an offer of securities for sale in the United States. Securities may not be offered or sold in the UnitedStates absent registration or an exemption from registration under the United States Securities Act of 1933, as amended. Any public offeringof shares to be made in the United States must be made by means of a prospectus that will be available from Telkom SA Limited (Telkom)or the Government of South Africa and will contain detailed information about Telkom and its management as well as its financial statements.

Disclosure regarding forward-looking statements

Many of the statements included in this Annual Report, including the description of our plans, strategies, capital expenditures, anticipatedcost savings and financing plans are forward-looking statements. You can generally identify forward-looking statements by the useof terminology such as “may”, “will”, “expect”, “intend”, “plan”, “estimate”, “anticipate”, “believe” or similar phrases. Our actual futureperformance could differ materially from these forward-looking statements.

These forward-looking statements involve a number of risks and uncertainties. Important factors that could cause actual results to differmaterially from our expectations include, but are not limited to, our ability and the ability of Vodacom Group (Proprietary) Limited (Vodacom)to successfully compete with new entrants in the South African fixed-line and mobile markets; our ability to minimise customer non-payments,theft and vandalism; future growth in the South African economy generally as well as the South African fixed-line and mobilecommunications markets; Vodacom’s ability to expand internationally; Vodacom’s ability to manage growth; the actual or perceived healthrisks relating to mobile handsets; our ability to attract and retain key personnel; our significant indebtness; rapid changes in technologies;future regulatory developments; the political, social, economic and operational risks relating to South Africa; the cost of compliance withlabour laws and our ability to manage labour relations; fluctuations in the value of the currency against foreign currencies and South Africanexchange control restrictions as well as other matters not yet known to us or not currently considered material by us. We caution you not toplace undue reliance on these forward-looking statements. There are risks that may be difficult for us to achieve the outcomes predicted inour forward-looking statements. All written and oral forward-looking statements attributable to us and persons acting on our behalf arequalified in their entirety by these cautionary statements.

G R A P H I C O R 2 6 3 7 0

US securities legend

Profile 1

Operational highlights 2

Financial highlights 3

Chairman’s statement 16

Group structure 20

Chief Executive Officer’s review 22

Executive management team 30

Contents

Board of Directors 34

Chief Financial Officer’s review 36

Segment review – Wireline 38

Segment review – Wireless 43

Corporate governance 46

Corporate social responsibility 50

Group annual financial statements 53

Telkom

Our vision is to be a world-class communicationsgroup

Group Annual Report 2002

Company SecretaryVincent MashaleTel: +27 12 311 [email protected]

Investor RelationsBelinda WilliamsTel: +27 12 311 [email protected]

Corporate CommunicationAmanda SingletonTel: +27 12 311 [email protected]

Government and RegulatoryVictor MocheTel: +27 12 311 [email protected]

Customer call centre10219

Business call centre10217

Websitewww.telkom.co.za

Company registration number1991/005476/06

Head officeTelkom Towers North152 Proes StreetPretoria0002South AfricaPrivate Bag X881, Pretoria 0001, South AfricaTel: +27 12 311 7000

AuditorsErnst & YoungWanderers Office Park52 Corlett DriveIllovo2000PO Box 2322, Johannesburg, 2000Tel: +27 11 772 3000Fax: +27 11 772 4000

KMMT Incorporated1226 Schoeman StreetHatfield0083PO Box 11265, Hatfield, 0028Tel: +27 12 431 1300Fax: +27 12 431 1301

Legal advisorsWerksmans 155 – 5th StreetSandownSandton2196South Africa Tel: +27 11 535 8000

Administration

Telkom AR Covers 26370 8/20/02 15:53 Page 2

Telkom Group Annual Report 2002 1Telkom Group Annual Report 2002 1

We are South Africa’sleading integratedcommunications groupWe provide wireline and wireless services throughout South Africa and

increasingly into other African countries.

Telkom is the incumbent fixed-line operator in South Africa and held the

exclusive licence to provide public switched telecommunication services

until May 2002. Our 50% shareholding in Vodacom makes us Africa’s leading

provider of wireless services.

We are committed to becoming a world-class communications group

and delivering sustainable shareholder value by focusing on our key

strategic objectives:

• Growing and defending core markets• Exploiting convergence opportunities• Driving operational and capital efficiencies• Improving the customer experience• Investing in our people

Telkom Group Annual Report 20022

Operational highlights

2002 707 881

2001 479 935

47% increasefixed-line prepaid

2002 467 518

2001 374 062

25% increaseISDN channels

2002 6 862 976

2001 5 212 242

32% increasemobile subscribers

%for the year ended 31 March 2002 2001 change

Total fixed-line access lines 4 924 458 4 961 743 (1)

Fixed-line postpaid 3 553 660 3 929 633 (10)

Fixed-line prepaid 707 881 479 935 47

ISDN channels 467 518 374 062 25

Payphones 195 399 178 113 10

Mobile subscribers1 6 862 976 5 212 242 32

Mobile contract subscribers 1 137 782 1 087 388 5

Mobile prepaid subscribers 5 725 194 4 124 854 39

Fixed-line employees 39 444 43 758 (10)

Mobile employees1 4 353 4 272 2

Revenue per fixed-line (ZAR) 5 547 5 233 6

Fixed lines per employee 125 113 11Mobile subscribers per employee1 1 577 1 220 29

1100% of Vodacom Group

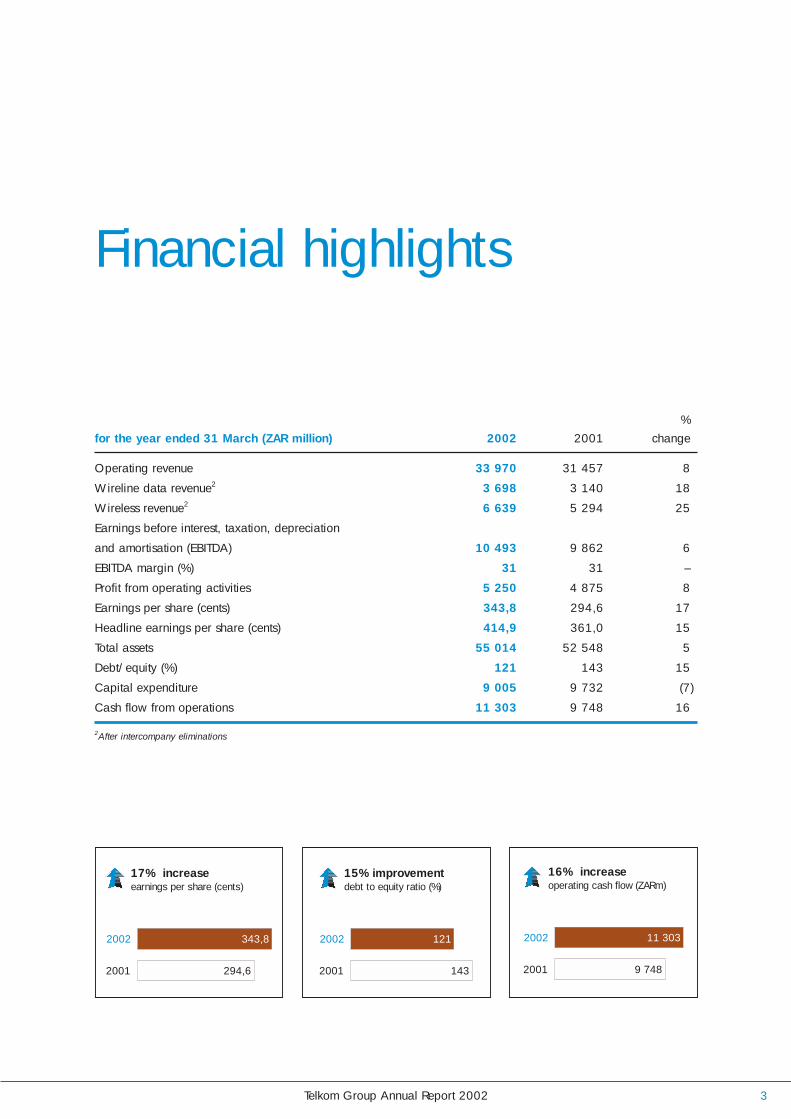

Telkom Group Annual Report 2002 3

Financial highlights

2002 343,8

2001 294,6

17% increaseearnings per share (cents)

2002 121

2001 143

15% improvementdebt to equity ratio (%)

2002 11 303

2001 9 748

16% increaseoperating cash flow (ZARm)

Operating revenue 33 970 31 457 8

Wireline data revenue2 3 698 3 140 18

Wireless revenue2 6 639 5 294 25

Earnings before interest, taxation, depreciation

and amortisation (EBITDA) 10 493 9 862 6

EBITDA margin (%) 31 31 –

Profit from operating activities 5 250 4 875 8

Earnings per share (cents) 343,8 294,6 17

Headline earnings per share (cents) 414,9 361,0 15

Total assets 55 014 52 548 5

Debt/equity (%) 121 143 15

Capital expenditure 9 005 9 732 (7)

Cash flow from operations 11 303 9 748 16

2After intercompany eliminations

%for the year ended 31 March (ZAR million) 2002 2001 change

Telkom Group Annual Report 2002

1> Integrated communications

Telkom is a group that benefits from two key segments in different life cycles.

We have a wireline segment that is stable and has the ability to deliver strong

cash flows. We have a wireless segment delivering good growth prospects in

Africa and further growth in the South African market.

By delivering a total end-to-end solution, in both voice and data, we can deliver a communications

product, whether by mobile phone, payphone, on the Internet or over a video link, to our broad and

diverse customer base.

• Launched Afrolinque (SAT-3/WASC/SAFE) submarine cable

• Vodacom expanded into the Democratic Republic of Congo

• Acquired a further 10% in Telkom Directory Services

• Acquired a further 40% in Swiftnet

We further strengthened our integrated offer

Telkom Group Annual Report 20024

A diversified base

Fixed-line postpaid 3 553 660

Fixed-line prepaid 707 881

Payphones 195 399

ISDN 467 518

Mobile 6 862 976

Telkom Group Annual Report 2002 5Telkom Group Annual Report 2002

2> Stretching ourreach

We have created world-class communications networks with best technologies,

exciting in their potential and reliable in their application. We can deliver value-

added products and services within reach of the majority of South Africans and

increasingly, the rest of Africa.

• 4,9 million fixed-line subscribers and 6,6 million mobile subscribers in South Africa

• Network now 99,8% digital compared to 74% in 1997

• 195 ATM switches

• 5 050 mobile base stations in South Africa

• 94% mobile access provided to the South African population

Our networks provide the platform for growth

Telkom Group Annual Report 20026

Growth in lines

Fixed-line postpaid (10%)

Fixed-line prepaid 47%

Payphones 10%

ISDN 25%

Mobile 32%

Our investment in the networks is delivering strong growth in our customer base and will facilitate the rapid

delivery of convergence products and services.

Telkom Group Annual Report 2002 7

3> Improving the customer experience

We understand that a long-term customer relationship is far more sustainable

than simply delivering a product.

• Average time to answer a fixed-line call in our call centres has improvedfrom 119 seconds in 2000 to 22 seconds in 2002

• Improved availability of coin payphones from 88% in 1998 to 95% in 2002

• Launch of various new products, MyRing, RingBack and 4U (mobile persecond billing)

• First communications group in the world to provide fixed-line prepaid

Mobile contract churn(%)

Telkom Group Annual Report 20028

2002 15

2001 19

Average residential installation(days)

2002 8

2001 18

Average business installation(days)

2002 5

2001 11

Our stated intention of improving the customer experience is realised through continuous product

development, improving the customer interface, increasing access to services and a drive for

uncompromising reliability.

Telkom Group Annual Report 2002 9

4> Strength throughmulti-skilling

Our international partnerships ensure that world-class skills are entrenched. We continue to retain and

attract the best skills while driving a competitive mindset throughout our business.

Our greatest challenge is to achieve more with less, using the talents of smart

and committed people to achieve measurable goals. Our people are our

greatest asset. Value is created through their energy and ability.

Training expenditure ZAR 506m

Technical training days 191 000

Training days per employee 10

Employee tuition sponsorships 6 654

• Optimal blend of international and local skills with Thintana CommunicationsLLC (a consortium of SBC Communications Inc and Telekom Malaysia Berhad)as group investors and Vodafone’s direct investment in Vodacom

• 39 Strategic Equity Partner (SEP) employees in 2002 compared to 75 in 1997

• Fixed lines per employee increased 11% to 125

• Mobile subscribers per employee increased 29% to 1 577

An ever-improving skills base is driving performance

Telkom Group Annual Report 200210

Fixed-line training commitments

Telkom Group Annual Report 2002 11

5> Measuring upto the mark

We are driving our business in a strategic direction that is based on delivering

optimal financial returns.

Applying the most stringent measures, we are focused on driving operational and capital efficiencies

throughout our operations.

• Successfully reduced group capital expenditure through refocusing our investment criteria on high-return areas

• Established Operational Support Systems (OSS) division

• SAP/R3 implementation launched in April 2002 to drive greater operationalefficiencies

• Continued optimisation of staff numbers with a 10% reduction in fixed-lineheadcount

Telkom Group Annual Report 200212

Group capex as a % of revenues

2002 27%

2001 31%

Mobile revenue peremployee (ZAR 000)2

2002 3 719

2001 3 105

Fixed-line revenue peremployee (ZAR 000)1

2002 693

2001 5931Fixed-line employees only 2100% Vodacom revenues and employees

Telkom Group Annual Report 2002 13

6> In touch with our base

As a South African corporate citizen we are committed to the upliftment of the

communities in which we work.

BEE contributions

Fixed-line BEE spend ZAR 4,6bn

Mobile BEE spend ZAR 0,4bn

Black staff fixed-line 56%

Black staff mobile 63%

• Increased fixed-line Black Economic Empowerment (BEE) procurementspend from R58 million in 1997 to R4,6 billion in 2002

• Telkom and Vodacom Foundations spent R33 million in 2002

• Partnerships with rural entrepreneurs with self-containedpayphone units

• Vodacom’s community service network expanded to 27 884 payphone units

Our investments in South Africa include:

Telkom Group Annual Report 200214

Telkom strives to be a catalyst for change, both as a business and as a corporate citizen. We recognise

our responsibility to our country and we strive to create wealth for all our stakeholders.

Telkom Group Annual Report 2002 15

Chairman’s statementEric Molobi

“May 2002 saw the end of Telkom’s exclusivity period

and we now face, with the imminent introduction of a

second national operator and the licensing of Sentech,

an increasingly competitive landscape. I believe the

liberalisation of the South African market, through the

introduction of facilities-based competition will be very

positive for the country, as it will encourage foreign direct

investment, create jobs and result in improvements in

teledensity, thus meeting many of the Government’s primary

objectives for the communications sector.”

The year under review was defined by significant change in the communicationslandscape. In 2001, we saw the introduction of a third mobile operator and the amendment to South African telecommunications legislation. In 2002 we will seethe introduction of competition into the fixed-line voice market.

The economic backdrop remained challenging. In 2001, our currency suffered asignificant devaluation, GDP growth was below expectations and unemployment athigh levels. During the first quarter of this calendar year, we saw a strengthening ofour currency, reflecting a return of investor confidence in the South African economy.

Telkom as a major participant in the South African economy, is not immune to theeconomic difficulties of the country. However, the business in many ways, has neverbeen stronger due to strategic and operational changes that were driven throughoutthe Group over the past 5 years.

Telkom Group Annual Report 200216

Telkom Group Annual Report 2002 17

The results

The Group’s financial results for the year indicate that Telkom is well positioned toboth operate in a liberalised market and be judged against its international peersas it prepares for an Initial Public Offering.

Group operating cash flow grew 16% to R11,3 billion. Earnings per share grew17% to 343,8 cents. While we maintained our EBITDA (earnings before interest,taxation, depreciation and amortisation) margin at 31%, there is strong evidence ofimproved capital and operational efficiencies across the Group.

Unlike some of our international peers, Telkom has maintained its investment gradecredit rating with international credit rating agencies Moody’s and Standard &Poor’s. This reflects a view that within the next few years the Group will reduce itsdebt and strengthen its balance sheet.

Regulatory environment

The past twelve months represented a defining year in the development of boththe South African communications sector and Telkom. The introduction ofcompetition was facilitated by the Telecommunications Amendment Act, which waspromulgated in November 2001. Government is committed to a managedliberalisation process, with an emphasis on facilities-based competition. WhilstGovernment recognises the need to balance a healthy competitive landscape withimproved public telephony services, its prime objective is to increase accessibilityand affordability. To this end, Telkom has rolled out 2,8 million fixed lines andVodacom has connected 6 million mobile subscribers over the past 5 years, resultingin an increase in overall teledensity in South Africa from 12% in 1997 to anestimated 36% in 2002.

The end of Telkom’s fixed-line exclusivity period on 7 May 2002 paves the wayfor the introduction of fixed-line competition. There is no doubt that the newcompetitive landscape will provide a major boost to the South Africancommunications market.

Telkom has been criticised for trying to “hang on” to its monopoly. The truth is, wewelcome competition. We are looking forward to competing on a level playing fieldwhere we are not expected to subsidise our competitors and where all players willhave a proportionate share of socio-economic commitments, including investment ininfrastructure to further broaden public access to communications.

In the same spirit, we also welcome the new regulatory process. Within the processour priority is to ensure that we can operate effectively as a business in a sustainablecommunications sector.

Initial Public Offering (IPO)

The changes that were implemented across the business have prepared the Groupfor increased competition, and to meet additional obligations it may have as a

Telkom Group Annual Report 200218

publicly-listed company. Government remains committed to the process ofprivatisation and the IPO of Telkom.

Empowerment and social responsibility

Telkom strives to be a catalyst for change, both as a business and a corporatecitizen. We are a powerful organisation and with that power comes responsibilityto the broader community. Telkom is committed to increasing its Black EconomicEmpowerment (BEE) procurement spend. Our Group procurement spend on BEEincreased to approximately R5 billion in 2002 from R4 billion in 2001.

The Telkom and Vodacom Foundations continue to contribute to the transformation ofdisadvantaged communities through sustainable social development programmes.The Telkom Foundation committed R100 million over a 5-year period, while ourStrategic Equity Partner (SEP), Thintana Communications LLC (a joint venture betweenSBC Communications Inc and Telekom Malaysia Berhad), committed an additionalR120 million over the same period. During 2002, the Telkom and VodacomFoundations contributed R33 million towards various social initiatives.

Since 1998 Telkom and Thintana have sponsored 70 students at the MalaysianMultimedia University at a total cost of R5,5 million. The future of our country lies inthe education of our people and therefore education remains the key focus of ourexternal social investment programmes.

Relationships with organised labour

We continue to develop long-term relationships with both our unions:Communication Workers Union (CWU) and the Alliance of Telkom Unions (ATU).In February 2002 we concluded a landmark deal with CWU, signing the JobSecurity and Retrenchment Framework Agreement. This provides us with guidelinesfor managing staff optimisation while ensuring a long-term, mutually workablerelationship with the union and our employees.

Board changes

During the year under review Advocate Dikgang Moseneke resigned as Chairmanof the Board in order to pursue his career on the bench. Dikgang’s contribution wasinvaluable and much of what Telkom has achieved during the past 7 years can beattributed to his leadership, enthusiasm and keen business sense. With Dikgang’sdeparture, I was appointed Chairman on a one-year contract. I have decided not torenew my contract when it expires on 31 July 2002.

Telkom has delivered very good results for the current year and the association withthe SEP, especially in transferring skills and transforming the Company, has addedsignificant value.

Two further changes to the Telkom Board took place after year-end. Effective from12 July 2002, Shawn McKenzie takes over as Chief Operating Officer (COO) fromTom Barry, who will retire after an outstanding career spanning more than 35 yearsin communications with 4 of these as Telkom’s COO.

Chairman’s statement

Telkom Group Annual Report 2002 19

Shawn McKenzie, who is currently a President of SBC Communications Inc, hasbeen with SBC for 23 years in various roles, which include Network Operations andRegulatory Affairs.

Shan Manickam also retires after 5 years as the Group’s Chief Strategic Officer. Thiswas preceded by 28 years with Telekom Malaysia. Chian Khai Tan takes over asChief Strategic Officer from 27 June 2002. Chian Khai Tan is currently Senior VicePresident for Consumer and Business at Telekom Malaysia and has worked forTelekom Malaysia for 29 years.

Shawn McKenzie and Chian Khai Tan will serve on Telkom’s Board of Directors inthe Thintana positions vacated by their predecessors.

Acknowledgements

Given the significant market changes that confronted Telkom over the past year,I would like to express my admiration and appreciation for the efforts of the Telkommanagement team. Our CEO, Sizwe Nxasana, in particular, has shown exceptionalleadership qualities and has effectively managed the sensitive task of balancing thedemands of a new regulatory process with the need to deliver value to shareholders.Telkom’s progress towards achieving its strategic objectives was made possible bythe passion and dedication of all our employees.

I would also like to thank Thintana for their continued contribution to Telkom’stransformation these past 5 years. Their technological expertise and experience ofbest-practice business and marketing processes, and the associated knowledgetransfer between Thintana and Telkom, enhanced our initiatives immeasurably.

Prospects

We anticipate challenging market conditions through to 2003, with moderateeconomic growth and a changing regulatory environment. Nevertheless, withTelkom’s world-class technology platform, the improved competitive culture and afocus on delivering efficiencies, we are well positioned to profitably service thecommunications needs of our nation.

Eric MolobiNon-executive Chairman

Telkom Group Annual Report 200220

Group structure

Vodacom Group(Pty) Ltd

Swiftnet(Pty) Ltd

Telkom DirectoryServices(Pty) Ltd

Intekom(Pty) Ltd

Q-Trunk(Pty) Ltd

50% 100%64,9% 100% 100%

Telkom SA Ltd

Group operational structure

Wireline

Wireless

Fixed-line

Directories

Mobile

Wireless data

Segment Business line Legal entity

Telkom

Telkom Group Annual Report 2002 21

Shareholders

Vodacom Group (Proprietary) Limited

Telkom shareholding: 50% (2001: 50%)Vodacom is a leading mobile communications company providing a GSM (GlobalSystem for Mobile Communications) service to almost 7 million customers in SouthAfrica, Tanzania, Lesotho and the Democratic Republic of Congo. Vodacom is SouthAfrica’s leading cellular network with an estimated 60% market share. Vodacomprovides coverage to 94% of the South African population and 60% of thegeographical area of South Africa.

Telkom Directory Services (Proprietary) Limited

Telkom shareholding: 64,9% (2001: 54,9%)Telkom Directory Services (TDS) was formed on 1 September 1997, as a result of a jointventure between Telkom SA Limited and Maister Directories’ directory businesses. TDSprovides complete Yellow and White page directory services, an electronic directoryservice, 10118 “The Talking Yellow Pages”, and an on-line web directory service.

Swiftnet (Proprietary) Limited

Telkom shareholding: 100% (2001: 60%)Swiftnet started in 1994 as a Telkom initiative and trades under the name FastNetWireless Service. FastNet is a wireless network providing asynchronous wireless accesson Telkom’s X.25 network, Saponet-P, to its customer base. Services include retail creditcard and cheque terminal verification, telemetry, security and fleet mobility.

Subsidiaries and joint venture

Government: 67%

The Government of South Africa is the majority shareholder in Telkom SA Limited.

Thintana Communications LLC: 30%

Thintana is a consortium consisting of SBC Communications Inc (SBC Communications)and Telekom Malaysia Berhad (Telekom Malaysia), operating through a USA limitedliability company, Thintana Communications LLC, which is registered in the state ofDelaware in the United States of America. SBC Communications and Telekom Malaysiahold 60% and 40% respectively of the 30% investment in Telkom.

Ucingo Investments (Proprietary) Limited: 3%

Ucingo Investments is a broad-based investment company representing more than20 empowerment groups from all 9 provinces of South Africa.

Chief Executive Officer’s reviewSizwe Nxasana

I strongly believe that the imminent introduction of competition in our fixed-linebusiness will be good for Telkom. In particular, it has focused our minds on creatinga better business, motivated us to adopt the right business approach to strengthenour investment proposition and positioned us for real future growth.

For the year ended March 2002 the Group delivered robust results. Thisperformance was achieved against a difficult background of balancing the lastleg of our fixed-line licence obligations with positioning Telkom for both increasedcompetition and the Initial Public 0ffering (IPO). We have now completed our fixed-line licence obligations, set out in the 1997 agreement with Government,demonstrating our ability to deliver on commitments. We largely met our line rolloutobligations missing our 2,7 million target, excluding payphones, by only16 448 lines. However, we successfully met our underserviced line and payphonetargets. We met all our service targets, except for the residential faults rate.

We have now successfully shifted our focus from fulfilling licence obligations tostrategic and operational initiatives based on margin improvement and earningsgrowth. This will allow us to optimally allocate capital to enhance our offerings tocustomers and facilitate increased returns to our shareholders.

Telkom Group Annual Report 200222

“As we look back on the past 12 months, it is clear that

the changes we continue to implement are resulting in a

well-positioned, integrated communications group that is

ready to be measured against its global peers, both as

a world-class provider of communications products and

services and as an investment that can deliver real value

to its shareholders. This success has been underpinned

by our focus on the Group’s strategic objectives which

include growing and defending our core markets,

expanding our convergence business, achieving greater

customer satisfaction and improving corporate

performance.”

Telkom Group Annual Report 2002 23

As an integrated group we benefit from two key segments in different lifecycles. Wehave a wireline segment that is stable and has the ability to deliver strong cash flowsand a wireless segment delivering good growth prospects in Africa and furthergrowth in the South African market.

We now offer a full range of products and services across voice and data, fixed andmobile, and have completed a substantial capital investment programme in ournetworks, incorporating the world’s best technologies. Our customer service isconsistently improving both in terms of service levels and product delivery. We haveinvested in the right skills and have developed a performance driven culture acrossour leadership team and into our workforce with new measures to drive higherproductivity. We now have all the fundamentals in place to operate successfully ina liberalised market.

More than just a telephone company

For many years it was sufficient to supply customers with just telephones, either intheir homes, their offices or in public places. However, the revolution that has takenplace in the communications sector over the past decade brought with it increaseddemands for more advanced communications solutions. Exciting technologies suchas mobile phones and the Internet have been developed, and we were able todeliver these technologies to our customers.

With the introduction of mobile communications in South Africa eight years ago,Telkom invested in a joint venture with Vodafone Plc and the Rembrandt Group tocreate Vodacom, which is now South Africa’s leading supplier of mobilecommunications services. Vodacom expanded its African operations by investing ina new venture with a 51% interest in a GSM licence in the Democratic Republic ofCongo in December 2001, and successfully launched operations in May 2002.Vodacom now operates in South Africa, Lesotho, Tanzania and the DemocraticRepublic of Congo. Wireless services continue to be an important part of theGroup’s strategy and now represent 20% of revenues.

We continue to focus on expanding our wireline data offerings, as it is a key driverof growth in our wireline segment. Through our strategic partnerships we are nowbetter positioned to offer a total solution in network management and relatedservices, with one of the most comprehensive service level agreements in the SouthAfrican data market.

The establishment of Telkom Business Integration Services (TBIS) in September 2001,and the integration of Intekom, South Africa’s third-largest Internet Service Providerinto TBIS, consolidated the Group’s Internet and e-business operations into a singleportfolio. The TBIS portfolio of services includes hosting, security, LAN services,Internet access and e-commerce. These services are fully supported by our new datacentre in Centurion.

International connectivity remains a key growth area through our strategy to becomethe connectivity hub for Africa. We have invested in upgrading our links withneighbouring countries Namibia, Zimbabwe, Swaziland, Lesotho, Mozambiqueand Botswana. Our international connectivity strategy is strengthened through our

Telkom Group Annual Report 200224

Chief Executive Officer’s review

US$85 million (13%) asset investment in Afrolinque, the SAT-3/WASC/SAFEsubmarine cable, which represents a technological breakthrough of greatsignificance to the continent as it offers faster, more efficient trading channelsbetween Africa and international markets.

We have deployed an extensive Voice over Internet Protocol (VoIP) network, andlaunched a regional clearinghouse to serve as a hub for voice traffic on theAfrican continent.

In October 2001, we purchased an additional 10% in Telkom Directory Services(TDS) for R160,3 million, increasing our shareholding to 64,9%. In May 2001, wepurchased an additional 40% in Swiftnet for R22 million, increasing ourshareholding to 100%. Swiftnet provides wireless transmission links largely for retailpoint-of-sale terminals.

Our network – world-class and delivering value

The Group’s capital investment of R48 billion over the past five years has allowed us toconnect a significantly greater number of customers. In 2002, we invested R9,0 billionprimarily in our fixed and mobile networks and operational support systems, whichresulted in further enhancements to our networks’ capability. Digitisation of the fixed-linenetwork today stands at 99,8% compared to 74% in 1997.

The wide-ranging enhancements in our network’s capacity and functionalitycombined with our ability to deliver new and innovative value-added products andservices to our customers, has resulted in good growth during the year in our totalsubscriber base, including: • a 10% increase in payphones to 195 399;• a 25% increase in ISDN channels to 467 518;• a 28% increase in South African mobile subscribers to 6 556 820; and • a 193% increase in other African mobile subscribers to 306 156.

While we connected 2,8 million fixed lines over the past 5 years to meet our licencerollout obligations, our net line growth over the licence period was 665 819. Thisresulted in a total of 4,9 million fixed lines including payphones andISDN, at 31 March 2002. Our net fixed-line growth over the five-year period wasdisappointing. While we succeeded in connecting millions of customers, wewere adversely impacted by a high rate of disconnections. Disconnectionscan be attributed to the poor domestic economic climate coupled with thephenomenal growth in mobile subscribers over the five-year period. Fixed-lineteledensity currently stands at 11% and fixed-line household penetration at anestimated 31%.

Recognising that prepaid services and payphones are key solutions to addressaccessibility and affordability, we have successfully offered prepaid services to bothour mobile and fixed-line customers. In 1998, we were the first communicationscompany in the world to provide prepaid services on a fixed-line network and currentlywe have 707 881 prepaid subscribers. Vodacom has successfully grown SouthAfrican mobile prepaid subscribers from 76 763 in 1997 to 5,4 million in 2002.

24

Fixed-line teledensity(per 100 inhabitants)

1997

10,1

1999

11,8

2000

12,8

2001

11,5

2002

11,4

1998

10,8

Mobile teledensity(per 100 inhabitants)

1997

2,3

1999

7,1

2000

12,1

2001

19,3

2002

24,9

1998

4,0

Telkom Group Annual Report 2002 25

We remain committed to increasing universal access to telephony services in SouthAfrica and our continued deployment of payphones has allowed us to achievethis. In July 2001 we launched containerised semi-public fixed-line telephones and500 containers have been introduced to date. These containers bring telephony andelectronic services to rural and urban communities.

The strength and quality of our networks are critical to both our wireless and wirelineconvergence strategies and our investment has resulted in unequalled networks inSouthern Africa. A significant portion of our capital expenditure was allocated to thefuture network, one that will deliver converged voice, data and video.

Telkom is adopting an evolutionary approach towards a Next Generation Network,using the Packet Mode Architecture-model to maximise existing infrastructure whileadding new functionality. By utilising Packet Mode Architecture (PMA), InternetProtocol (IP), Asynchronous Transfer Mode (ATM) and the wider bandwidth madepossible by Asymmetric Digital Subscriber Line (ADSL) technology, Telkom is able tooffer customers a fully converged Next Generation Network.

Future developments in the mobile network will focus on enhancing revenuesfrom customers through the deployment of data services, which will be facilitatedthrough the rollout of General Packet Radio Services (GPRS). Vodacom is currentlyawaiting the issuance of the 1 800 MHz spectrum that will allow for the capacity todeploy GPRS.

We are servicing the customer better than ever

Our strategy of relentlessly improving service delivery continues. This year sawadditional improvements in our fixed-line installation and fault repair times. Wecontinue to improve our customer interfaces and have made further improvements inour call centre response times.

Much of our success in improving customer satisfaction statistics began with amarket segmentation process we started 5 years ago. The diverse nature of ourmarket demanded a more focused set of strategies for each segment which haveallowed us to deliver prepaid and value-added services in the consumer market andtailor-made data solutions for the corporate market.

“One cannot take a payphone into a rural community without priorconsultation. Before you present rural communities with a valueproposition, one has to understand exactly how communications willenhance their lifestyle. We have learned that consultation leads tocooperation and ultimately to co-responsibility. This reduces vandalismand thus increases the usage of payphones and returns on investment.”

Mike MlenganaManaging Executive: Public Services

Telkom Group Annual Report 200226

We continued to refine our customer segmentation process. Whereas we initiallyconcentrated on corporate customers, we have now extended this process tobusiness customers.

During the year we also continued to focus on improving our distribution channels.We strengthened our relationships with strategic partners in our payphone businessand facilitated the relocation of payphones into high traffic areas. The launch ofvirtual vouchers improved our distribution of fixed-line prepaid considerably. In ourmobile business, we have moved closer to understanding our customer base andhave focused strongly on improving our customer retentions. This is evidenced in ourcontract churn reducing to 15% in 2002 (2001: 19%).

An ever-improving skills base is driving performance

Recognising that a skilled, knowledgeable workforce is key to gaining acompetitive advantage, we have been consolidating our skills base through anunprecedented training and development drive. In 2002 the number of trainingdays in the fixed-line business amounted to 388 397, an increase of 10%from 2001. This amounts to 9,8 training days per employee, an increase of21% from 2001. Training spend for 2002 amounted to R506 million, or R12 836 perfixed-line employee.

We continued to strengthen and transform the Group’s leadership team. Wesuccessfully transferred South Africans into top management positions previouslyheld by Thintana. Nombulelo Moholi was appointed Chief Sales andMarketing Officer and Reuben September was appointed Chief Technical Officer.In our mobile business, Andrew Mthembu was promoted to Deputy CEO of theVodacom Group.

We attracted some key individuals from outside the Group, Essa Govender as GroupExecutive for Procurement, Oupa Magashula as Group Executive for Human Resourcesand Thami Magazi as Managing Executive of Consumer Markets. In May 2002,Charlotte Mokoena joined as Group Executive of the Centre for Learning and ThaboSeopa as Managing Director of Telkom Directory Services.

SBC Communications and Telekom Malaysia’s shareholding in Telkom throughThintana, as well as Vodafone’s direct investment in Vodacom, continue to benefit

Chief Executive Officer’s review

“Everything we do, whether it’s customer care training fortechnical staff, setting ourselves more stringent service qualitytargets or finding ways to streamline our processes, is done withone goal in mind: Better service to our customers.”

Nombulelo MoholiChief Sales and Marketing Officer

Telkom Group Annual Report 2002 27

the Group. We have seen the successful transfer of skills from Thintana over the 5-year period with the number of foreign employees declining from 75 in 1997to 39 at 31 March 2002. Skills transfer continues in accordance with the StrategicServices Agreement.

Our proactive approach to equity in the workplace has enabled us to make furtherprogress this year in establishing a representative workforce. 56% of the fixed-lineworkforce, 63% of the mobile workforce and 80% of Telkom’s Group and ManagingExecutives (excluding Strategic Equity Partner employees) are black.

Our focus on people development is also key to achieving the level of transformationthat is needed to succeed in a competitive market. It is crucial that each and everyemployee learns to think and act differently. Therefore we have initiated, and arebusy implementing, a company-wide internal culture change initiative known as theCompetitive Mindset. This culture change initiative has its basis in our core values,which are focused on an increasingly performance-driven culture.

And our performance shows it is working

Despite the fact that we had to fulfill certain licence obligations in our fixed-line business,we also focused on developing value-added products and services to drive margingrowth. We continued to maximise efficiencies and drive costs out of the business, at thesame time improving current service levels. A key focus area is increasing revenueintensity through value-added services, particularly in our data business.

We maintained the group operating margin at 15% and will continue to focuson driving operational and capital efficiencies to maximise free cash flows. Ouremployee optimisation programme in our fixed-line business continues. Duringthe year we successfully reduced our fixed-line employee numbers by10% to 39 444 resulting in an 11% increase in fixed lines per employee to 125. Inour mobile business, we have also achieved greater efficiencies as indicated by the29% increase in mobile subscribers per employee to 1 577.

The investment in Operations Support Systems (OSS) in our fixed-line business is apriority as we prepare for competition and drive greater operational efficiencies,flexibility and speed to meet new market demand. While we experienced an initial

“The fact that we managed to significantly reduce staff numberswithout losing productivity, tells me our people have the skills, the attitude and the competitive instinct to make this Groupexceptional.”

Oupa Magashula Group Executive: Human Resources

Telkom Group Annual Report 200228

setback in 2001 with the termination of the Telcordia contract, we are now on trackwith a strong internal project management team.

We are beginning to realise benefits from our improved capital allocation process,which ensures that our capital is allocated to areas that will produce maximumreturn. This has resulted in a 15% reduction in capital expenditure in our wirelinesegment this year. Overall group capital expenditure has reduced from 31% ofrevenues in 2001 to 27% in 2002. Going forward we intend to continue to reduceour capital expenditure and invest in capital that will result in an internal returngreater than our cost of capital.

Regulatory environment

During the past 12 months we have worked through a challenging regulatoryperiod. We hope that our detailed local knowledge and the international experienceof our Strategic Equity Partner, Thintana, has enabled us to contribute meaningfullyto the development of legislation and regulations. We are optimistic that regulationswill be developed to support the principles contained in the legislation promulgatedby the Telecommunications Amendment Act in 2001, and the objectives oftelecommunications policy in South Africa.

Government’s objective of managed liberalisation has resulted in the licensing ofSentech with both an international carrier-of-carrier and multimedia licence on6 May 2002. On 20 December 2001 the Government issued an Invitation to Apply(ITA) for the 19% black economic empowerment stake in the Second NationalOperator (SNO). The issuing of the ITA for the 51% strategic equity stake in theSNO followed on 24 May 2002.

While we acknowledge the progress both Government and ICASA (the IndependentCommunications Authority of South Africa) have made in facilitating theliberalisation process, regulations still need to provide greater clarity on issuessuch as:• the interpretation and implementation of the multimedia licence granted to

Sentech;• the manner of and cost recovery for the implementation of carrier pre-selection;• the requirements and definitions for facilities leasing/sharing; and• interconnection guidelines.

Chief Executive Officer’s review

“The fact that we continuously strive to build a solid, ongoingrelationship with the Regulator enables us to engage inconstructive debate to find ways of establishing a matureregulatory environment that will benefit the industry as a whole.”

Victor MocheGroup Executive: Government and Regulatory Relations

Telkom Group Annual Report 2002 29

Telkom made further progress during the year in its efforts to rebalance tariffs.Telkom’s tariff rebalancing is a process mandated by Government. Initiated in 1997,the process aims to align the tariffs that consumers pay for specific services with thecosts incurred in providing them.

In November 2001, Telkom successfully negotiated new interconnection agreementswith the three mobile operators. Telkom’s fixed-line business was previouslyadversely affected by an unfair interconnection agreement that remainedunchanged since 1994. The renegotiation of the interconnection regime hasallowed Telkom’s fixed-line business to negotiate separate agreements with themobile operators for both interconnection and facilities leasing.

We renegotiated the interconnection agreement with the mobile operators in goodfaith that the Regulatory Authority would accede to our appeal to remove the fixed-to-mobile revenues from the basket of tariff services. Unfortunately, this has not yettranspired with the result that the negotiated benefits have not materialised. We willcontinue to pursue this matter with the Regulatory Authority.

Telkom’s future in the context of increased competition

Telkom is ready to operate in a more competitive environment. Many of theinitiatives already discussed represent Telkom’s strategy for positioning the Group tosucceed in an increased competitive landscape.

As an integrated communications group, we are confident of our ability to compete.We can now deploy advanced technologies through our state-of-the-art network toservice the specific needs of our diverse customer base. We can provide improvedcustomer service through multi-skilling our people and creating a truly competitivemindset throughout our workforce. We can compete through the quality of ourservice and prove to our customers that we have what it takes to be theircommunications provider of choice. We remain focused on our strategy to reducecosts and achieve greater efficiencies to drive higher returns for shareholders.

Sizwe NxasanaChief Executive Officer

Telkom Group Annual Report 200230

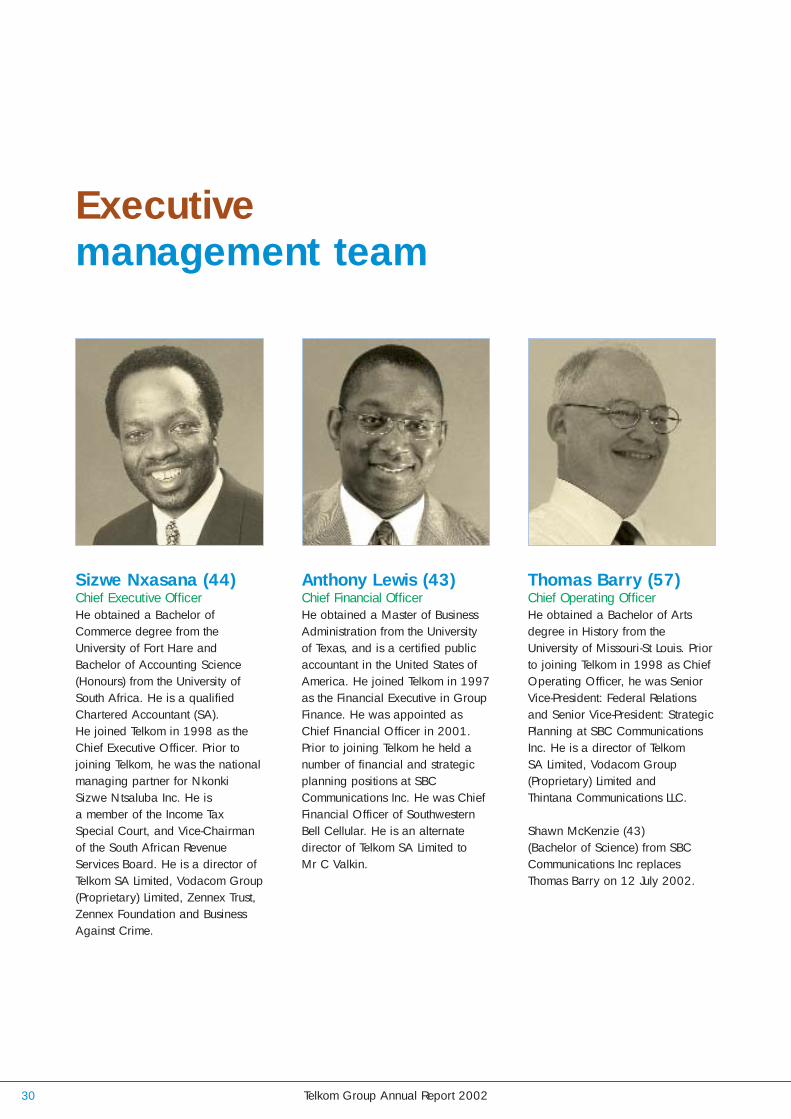

Executive management team

Anthony Lewis (43)Chief Financial OfficerHe obtained a Master of BusinessAdministration from the Universityof Texas, and is a certified publicaccountant in the United States ofAmerica. He joined Telkom in 1997as the Financial Executive in GroupFinance. He was appointed asChief Financial Officer in 2001.Prior to joining Telkom he held anumber of financial and strategicplanning positions at SBCCommunications Inc. He was ChiefFinancial Officer of SouthwesternBell Cellular. He is an alternatedirector of Telkom SA Limited toMr C Valkin.

Sizwe Nxasana (44)Chief Executive OfficerHe obtained a Bachelor ofCommerce degree from theUniversity of Fort Hare andBachelor of Accounting Science(Honours) from the University ofSouth Africa. He is a qualifiedChartered Accountant (SA).He joined Telkom in 1998 as theChief Executive Officer. Prior tojoining Telkom, he was the nationalmanaging partner for NkonkiSizwe Ntsaluba Inc. He isa member of the Income TaxSpecial Court, and Vice-Chairmanof the South African RevenueServices Board. He is a director ofTelkom SA Limited, Vodacom Group(Proprietary) Limited, Zennex Trust,Zennex Foundation and BusinessAgainst Crime.

Thomas Barry (57)Chief Operating OfficerHe obtained a Bachelor of Artsdegree in History from theUniversity of Missouri-St Louis. Priorto joining Telkom in 1998 as ChiefOperating Officer, he was SeniorVice-President: Federal Relationsand Senior Vice-President: StrategicPlanning at SBC CommunicationsInc. He is a director of TelkomSA Limited, Vodacom Group(Proprietary) Limited andThintana Communications LLC.

Shawn McKenzie (43) (Bachelor of Science) from SBCCommunications Inc replacesThomas Barry on 12 July 2002.

Telkom Group Annual Report 2002 31

Reuben September (44)Chief Technical OfficerHe obtained a Bachelor of Science(Electrical and ElectronicEngineering) degree from theUniversity of Cape Town. He joinedTelkom in 1977. He was appointedas Chief Technical Officer in May2002. Prior to his appointment asChief Technical Officer Reuben wasthe Managing Executive:Technology and Network Services.He has also worked in variousengineering and commercialpositions in Telkom. He isregistered as a ProfessionalEngineer with the EngineeringCouncil of South Africa (ECSA).

Nombulelo Moholi (42)Chief Sales and Marketing OfficerShe obtained a Bachelor of Science(Electrical and ElectronicEngineering) degree from theUniversity of Cape Town. Shejoined Telkom in 1994 as theGeneral Manager of the PayphoneBusiness, and moved on to becomeGroup Executive: Regulatory Affairsand later Managing Executive:International and Special Markets.She was appointed as the ChiefSales and Marketing Officer inApril 2002. Prior to joining Telkomshe worked for GEC and Siemens.She is the Chairman of the SouthAfrican Bureau of Standards(SABS), and a director of TelkomDirectory Services (Proprietary)Limited.

Shanmugan Manickam (57)Chief Strategic OfficerHe obtained a Bachelor of Electronics (Honours) from the University of Canterbury, New Zealand, and MS Engineering –Economics System and MS Engineering Management from Stanford University. He joined Telkom in 1997 as the Chief Strategic Officer. Prior to joining Telkom, he was the Vice President, CorporateStrategy at Telekom Malaysia and held various positions with theTelecommunications Department ofMalaysia. He is a director of Telkom SA Limited.

Chian Khai Tan (51) (Bachelor ofEngineering (Honours)) from TelekomMalaysia Berhad replaces Shanmugan Manickam as Chief Strategic Officer on 27 June 2002.

Telkom Group Annual Report 200232

Thami Magazi (45)Managing Executive: Consumer MarketsMaster of Business Administration Bachelor of Science (Business Administration) Joined Telkom in 2001

Godfrey Ntoele (41)Managing Executive: Business MarketsBachelor of Arts (Law) Joined Telkom in 1997

Mike Mlengana (42)Managing Executive: Public ServicesMaster of Arts (International Economics and Development Economics)Bachelor of Arts (Honours)Joined Telkom in 1995

Wally Beelders (42)Managing Executive: International and SpecialMarketsMaster Diploma in Technology Joined Telkom in 1977

Motlatsi Nzeku (41)Managing Executive: Customer ServicesBachelor of Science (Mathematics and Physics),Bachelor of Engineering Joined Telkom in 1994

Victor Moche (55)Group Executive: Regulatory and GovernmentRelationsMaster of Arts (Journalism) Joined Telkom in 1996

Kenneth Raley (48)Managing Executive: Network OperationsBachelor of Science (Business and Biology)Joined Telkom in 1997Strategic Equity Partner employee from SBC Communications Inc

Theo Hess (44)Managing Executive: Access Network Operations Management Advanced ProgrammeNational Certificate for Technicians National Diploma in Business Human Resource ManagementJoined Telkom in 1976

Bashier Sallie (34)Managing Executive: Data and Special ServicesManagement Advancement ProgrammeJoined Telkom in 1986

Johan Mare (47)Managing Executive: Operations Support SystemsNational Diploma in Technology – Telecommunications National Diploma in TechnologyJoined Telkom in 1972

Melvin McArthur Jr (41)Managing Executive: Information TechnologyMaster of Business Administration, Bachelor of Arts (Computer Science) Joined Telkom in 2001 Strategic Equity Partner employee from SBC Communications Inc

Randall Seidl (45)Managing Executive: Corporate and Global MarketsBachelor of Science (Business Administration andAgricultural Business)Joined Telkom in 1997Strategic Equity Partner employee from SBC Communications Inc

Executive management team continued

Telkom Group Annual Report 2002 33

Oupa Magashula (40)Group Executive: Human ResourcesBachelor of Science (Chemistry)Joined Telkom in 2001

Mandla Ngcobo (42)Group Executive: Legal ServicesMaster of LawsBachelor of Jurisprudence Bachelor of LawsJoined Telkom in 1998

Amanda Singleton (40)Group Executive: Corporate CommunicationBachelor of Arts (Communications) Joined Telkom in 1987

Martin Kerckhoff (37)Group Executive: Corporate Development and Initial Public OfferingMaster of Law (International Law)Joined Telkom in 1997Strategic Equity Partner employee from SBC Communications Inc

Essa Govender (45)Group Executive: ProcurementBachelor of CommercePurchasing Management DiplomaJoined Telkom in 2001

Kaushik Patel (39)Deputy Chief Financial OfficerBachelor of Accounting Science (Honours), CA (SA)Joined Telkom in 2000

Joseph Rajaratnam (61)Group Executive: Centre for LearningDiploma in Technical EngineeringJoined Telkom in 1997Strategic Equity Partner employee from Telekom Malaysia BerhadReplaced in May 2002 by Charlotte Mokoena (37)(Bachelor of Arts (Honours) Human ResourcesDevelopment, Bachelor of Social Sciences)

Nkhetheleng Vokwana (40)Chief Executive Officer: Telkom FoundationBachelor of EducationMaster of Science Joined Telkom in 1997

Alan Knott-Craig (50)Chief Executive Officer: Vodacom GroupBachelor of Science (Electrical Engineering)Master of Business LeadershipJoined Vodacom in 1993

Andrew Mthembu (46)Deputy Chief Executive Officer: Vodacom GroupBachelor of Science (Chemistry and Biology)Bachelor of Science (Civil Engineering)Master of Science (Construction Management)Joined Vodacom in 1998

Thabo Seopa (36)Managing Director: Telkom Directory ServicesBachelor of Accounting Higher diploma in Tax LawJoined Telkom Directory Services in 2002

Nicolaas Hall (40)Managing Director: SwiftnetBachelor of Commerce (Accounting)Master of Business Administration Joined Swiftnet in 1994

Telkom Group Annual Report 200234

Board of Directors

Eric Molobi (57) Bachelor of ArtsChairman Telkom SA LimitedAppointed to the Boardon 29 April 1997

Sizwe Nxasana (44) Bachelor of Commerce,Bachelor of AccountingScience (Honours), CA (SA)CEO: Telkom SA LimitedAppointed to the Board on1 April 1998

Wendy Luhabe (45) Bachelor of Commerce Management ConsultantAppointed to the Board on29 April 1997

Thomas Barry (57)#Bachelor of ArtsCOO: Telkom SA LimitedAppointed to the Board on15 November 1998

Wendy Lucas-Bull (48) Bachelor of Science

CEO: FirstRand RetailAppointed to the Board on

1 July 2000

Shanmugan Manickam (57)*Bachelor of Electronics (Honours),Master of Science (Engineering and Economics)CSO: Telkom SA LimitedAppointed to the Board on 15 May 1999

Telkom Group Annual Report 2002 35

Richard Menell (46)Bachelor of Arts (Honours),Master of Science (NaturalSciences), Master of Arts(Geology) (Mineral Explorationand Management)CEO: Anglovaal Mining LimitedAppointed to the Board on1 July 2000

Colin Smith (45)President: South AfricanCommunications UnionAppointed to the Boardon 29 April 1997

Drew Roy (55)#Advanced ManagementProgrammePresident: SBCCommunications Inc,International OperationsAppointed to the Board on15 September 2000

# American* Malaysian+ Zimbabwean

Charles Valkin (68) Bachelor of Commerce,Bachelor of Law,Higher Diploma in TaxationAttorneyAppointed to the Board on 29 April 1997

Diliza Mji (49)Bachelor of Medicine,

Bachelor of SurgeryFellow of the College

of Surgeons (SA)Surgeon

Appointed to the Board on 1 July 2000

Tan Sri Dato’ Ir.Muhammad RadziMansor (60)*Diploma: ElectricalEngineering, Master ofScience (TechnologicalEconomics)Chairman: Telekom MalaysiaAppointed to the Board on 23 October 1999

Peter Moyo (40)+Bachelor of Accounting Science(Honours), CA (SA), HigherDiploma in TaxationDeputy Managing Director: Old Mutual Life Assurance CoAppointed to the Board on 19 September 2001

Tlhalefang Sekano (43)Executive Chairperson:Communication WorkersInvestment CompanyAppointed to the Board on 19 September 2001

“The Group has delivered strong results for the year.

Our continual focus on increasing cash flows and driving

greater capital and operational efficiencies has allowed

us to deliver solid earnings per share growth of 17%.

Telkom’s results confirm that the Group is a sound

business with good prospects as evidenced by our

stable credit rating.”

Telkom Group Annual Report 200236

Chief Financial Officer’s reviewAnthony Lewis

Operating cash flow growth of 16% to R11,3 billion

The Group is committed to maximising cash flow from operations. This has beenachieved through a 6% growth in earnings before interest, taxation, depreciation andamortisation (EBITDA) to R10,5 billion and further improvements to our working capitalmanagement driven by improved debtors management and a reduction in inventories.Net cash from operating activities was R8,7 billion, which largely covered cashrequirements for capital expenditure of R8,8 billion.

Earnings per share growth of 17% to 343,8 cents

Group earnings per share grew by 17% to 343,8 cents (2001: 294,6 cents) andheadline earnings per share grew by 15% to 414,9 cents (2001: 361,0 cents). Whileoperating profits grew 8%, the lower than the prior year increase in finance chargesof 1% and the lower effective taxation rate of 29% (2001: 30%) contributed to the17% growth in earnings per share.

Operating margin maintained at 15%

We maintained our group operating margin at 15%. Group operating expenditureincreased 9% to R23,5 billion (2001: R21,6 billion). The increase in operatingexpenditure during 2002 was impacted by the significant asset impairment losses ofR445 million (2001: R234 million), bad debts of R965 million (2001: R671 million)and retrenchment costs of R373 million (2001: R132 million) in the wireline segment.

Group staff costs increased 8% to R7,2 billion (2001: R6,6 billion). However, ifretrenchment costs are excluded, group staff costs increased by only 5%. Group staffcosts, including retrenchment costs, represent 21% (2001: 21%) of group revenues.

Telkom Group Annual Report 2002 37

The impact of adopting AC133

The adoption of AC133, Financial Instruments: Measurement and Recognition requiresfair value adjustments in respect of financial instruments of R1,7 billion to be recognisedthrough the income statement, as Telkom does not apply hedge accounting in terms ofthe statement. Such fair value adjustments are to be considered together with foreignexchange losses now recognised in the income statement of R1,1 billion in accordancewith AC112. The impact of adopting AC133 is R468 million. The ongoing impact ofadopting AC133 will be material if there are significant fluctuations in the currency giventhe volume of hedging instruments utilised into by the Group in respect of foreign debtand foreign purchases. The impact could cause fluctuations in future earnings.

Revenue growth of 8% to R34,0 billion

Group revenues for 2002 were R34,0 billion (2001: R31,5 billion), representing an8% increase on the previous year. We experienced moderate revenue growth in ourwireline segment of 4% to R27,3 billion (2001: R26,2 billion) after intercompanyeliminations. Our wireless segment remains a key growth driver; delivering revenuegrowth of 25% to R6,6 billion (2001: R5,3 billion) after intercompany eliminations.During the year we changed the accounting treatment for network fraud. Network fraudof R174 million (2001: R274 million) was previously included in operating expenditureand is now offset against revenues for both 2002 and 2001.

Capital expenditure reduced to 27% of group revenues

Group capital expenditure decreased by 7% to R9,0 billion (2001: R9,7 billion) dueto the 15% reduction in our wireline segment’s capital expenditure to R6,9 billion (2001: R8,1 billion). We completed an extensive capital programme in our wirelinesegment over the past five years to modernise and digitalise our fixed-line network whiledelivering on most of our licence obligations. Future capital expenditure in our wirelinesegment will be driven solely by investment criteria that deliver maximum returns. Thegroup capital budget authorised for 2003 is R7,5 billion (2002: R11,0 billion).

Stable investment grade credit rating

We are committed to maintaining our investment grade debt rating. We have embarkedon a debt refinancing process to better align our funding with our financing requirements.We successfully refinanced foreign loans with domestic funds ahead of the currencydevaluation, resulting in a reduction of our foreign debt exposure from 38% to23% of outstanding debt. Short-term debt now represents 8% of total outstanding debtdown from 22% in the prior year. Net interest-bearing debt for the Group wasR21,1 billion (2001: R21,2 billion) and gearing stands at 121% (2001: 143%).Moody’s and Standard & Poor’s maintained our investment grade credit rating, with astable outlook.

Anthony LewisChief Financial Officer

Telkom Group Annual Report 200238

Segment reviewWireline

2002 27 898

2001 26 512

5% increaserevenues (Rm)

2002 42 478

2001 42 112

1% increaseassets (Rm)

2002 3 316

2001 3 662

9% decreaseoperating profit (Rm)

2002 6 892

2001 8 129

15% reductioncapex (Rm)

The wireline segment, which accounted for 80% of group revenues, provides

fixed-line services including access, national and international voice, data and

directory services. The wireline segment includes the consolidated results of

our subsidiary, Telkom Directory Services (Proprietary) Limited.

Note: Segment results presented before intercompany eliminations

Telkom Group Annual Report 2002 39

A mature fixed-line voice market

In 2002 revenues from our wireline segment grew by 5% to R27,9 billion (before inter-company eliminations). The underlying developments within our wireline segmentwere mixed. Despite a slowdown in the fixed-line voice market, we have seen stronggrowth in data leased lines, prepaid and payphone services.

Within our wireline segment, fixed-line access revenues grew by 5% as a result ofincreased connection and rental charges. Despite the overall average tariff increaseof between 5% and 6%, fixed-line traffic revenues grew 3% as a result of thenegative growth in net access lines and declining voice volumes. Directoriesrevenues grew 13% with the delivery of 7,8 million directories in 2002 (2001: 7,6 million).

Fixed access lines decreased by 1% in 2002 resulting in total access lines of4 924 458 at 31 March 2002. We continued to see a strong migration of ourpostpaid subscriber base to our fixed-line prepaid, ISDN and mobile offerings. The10% decrease in postpaid subscribers was offset by a 47% increase in fixed-lineprepaid to 707 881, a 25% increase in ISDN channels to 467 518, and a 10% increase in payphone units to 195 399.

Driving greater revenue intensity

We continue to focus on selling higher-quality and higher-value services to customersand have increased revenue per fixed-line by 6% in 2002. We are constantlydeveloping innovative, value-added products to enhance the customer experience.The TalkPlus portfolio of value-added fixed voice services available to the residentialand small-office-home-office (SOHO) market was further expanded during theyear with the launch of MyRing and RingBack. TalkPlus penetration has increasedfrom 24% in March 2001 to 32% in March 2002. Our prepaid service wasalso enhanced with the addition of the value-added products Call Answerand MultiPin in May 2001. Electronic PrePaidFone vouchers were introduced inMarch 2001. The 1023 directory service was enhanced with the introduction of1023 AutoComplete in December 2001, allowing customers to automaticallyconnect to a requested number.

Data – the growth engine in fixed-line

Revenues from our data business grew 18% to R3,9 billion (2001: R3,3 billion),contributing 14% to wireline revenues. An increase in leased lines, increased demandfor high bandwidth solutions and the growth in our managed network services drovethe solid revenue growth. The number of leased lines has increased by 16% to over87 000. The need for higher bandwidth data circuits continues to increase demandfor Diginet Plus and Megaline services.

We continued to expand our managed data network services, by adding55 customers and 1 877 sites during the year. We now have 169 customers and6 511 sites under management. Our portfolio of data managed services wasexpanded in October 2001 with the launch of VIPLink, an Internet Protocol wide-

Total access lines (m)

1998

4,65

1999

5,08

2000

5,49

2001

4,96

2002

4,92

Fixed-line postpaid lines (m)

19984,

521999

4,77

2000

4,67

2001

3,93

2002

3,55

Fixed-line prepaid lines

1998NA

1999NA

2000

380

955

2001

479

935

2002

707

881

Payphone units

1998

127

272

1999

153

476

2000

173

064

2001

178

113

2002

195

399

NA – not available

Telkom Group Annual Report 200240

Segment review – Wireline

area-network solution and VIPDial, a telecommuting solution. Our strategicrelationships with companies such as Cisco and Sun Microsystems underpin ourintegrated value-added data service offerings.

We saw a promising initial growth in our TBIS (Telkom Business Integration Services)service offerings, largely driven by our hosting and Internet access services. OurInternet subscriber base grew 31% to 48 811.

Rebalancing tariffs

In 2002, we furthered our tariff rebalancing process in advance of full competition.The focus of the rebalancing is twofold, namely to achieve an appropriate ratiobetween local and long distance call charges as well as between lower and higherbandwidth data circuits.

In 2002 the effective price per minute for a local call in standard time increased by23,9% whereas the effective rate per minute for a long distance call in standard timedecreased by 12%. The rebalancing of tariffs for data products culminated in anaverage reduction of 4% in 2002. Apart from rebalancing tariffs, there is also adrive to ensure that tariffs reflect the costs associated with a particular product orservice. Tariffs for installation and monthly residential telephone rental wereconsequently increased by 15% and 8% respectively. In order to ensure that we staycompetitive with regard to international telephony, the average effective price perminute to the basket of international destinations was reduced by 18% in 2002.

Over the 5-year licence period in which we were mandated to rebalance our tariffs,we reduced the ratio of a 3-minute long distance call to a 3-minute local call from1:14 in 1997 to 1:2,7 in 2002. This places us in line with international best practiceand positions us strongly for competition in the fixed-line market.

“Even though we have extended our data business beyondconnectivity to network IT services, we will remain true to ourcore business which is the network. We have the infrastructure,skills, strategic partnerships and the most comprehensive servicelevel agreements to compete in this market.”

Randall SeidlManaging Executive: Corporate and Global Markets

ISDN channels

1998 1999

153

672

2000

271

272

2001

374

062

2002

467

518

Local to long distance call ratio

1997

14,0

1999

7,8

2000

6,9

2001

5,8

2002

2,7

1998

10,0

Telkom Group Annual Report 2002 41

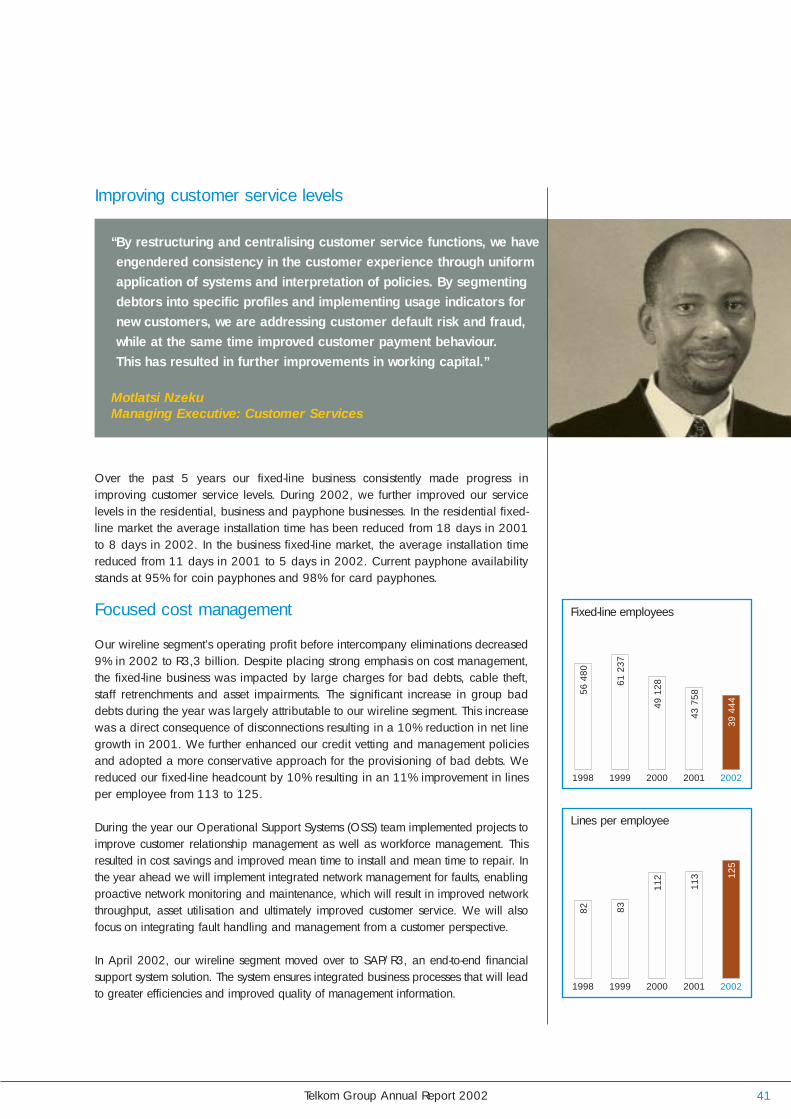

Improving customer service levels

Over the past 5 years our fixed-line business consistently made progress inimproving customer service levels. During 2002, we further improved our servicelevels in the residential, business and payphone businesses. In the residential fixed-line market the average installation time has been reduced from 18 days in 2001to 8 days in 2002. In the business fixed-line market, the average installation timereduced from 11 days in 2001 to 5 days in 2002. Current payphone availabilitystands at 95% for coin payphones and 98% for card payphones.

Focused cost management

Our wireline segment’s operating profit before intercompany eliminations decreased9% in 2002 to R3,3 billion. Despite placing strong emphasis on cost management,the fixed-line business was impacted by large charges for bad debts, cable theft,staff retrenchments and asset impairments. The significant increase in group baddebts during the year was largely attributable to our wireline segment. This increasewas a direct consequence of disconnections resulting in a 10% reduction in net linegrowth in 2001. We further enhanced our credit vetting and management policiesand adopted a more conservative approach for the provisioning of bad debts. Wereduced our fixed-line headcount by 10% resulting in an 11% improvement in linesper employee from 113 to 125.

During the year our Operational Support Systems (OSS) team implemented projects toimprove customer relationship management as well as workforce management. Thisresulted in cost savings and improved mean time to install and mean time to repair. Inthe year ahead we will implement integrated network management for faults, enablingproactive network monitoring and maintenance, which will result in improved networkthroughput, asset utilisation and ultimately improved customer service. We will alsofocus on integrating fault handling and management from a customer perspective.

In April 2002, our wireline segment moved over to SAP/R3, an end-to-end financialsupport system solution. The system ensures integrated business processes that will leadto greater efficiencies and improved quality of management information.

“By restructuring and centralising customer service functions, we haveengendered consistency in the customer experience through uniformapplication of systems and interpretation of policies. By segmentingdebtors into specific profiles and implementing usage indicators fornew customers, we are addressing customer default risk and fraud,while at the same time improved customer payment behaviour. This has resulted in further improvements in working capital.”

Motlatsi NzekuManaging Executive: Customer Services

Fixed-line employees

1998

56 4

80

1999

61 2

37

2000

49 1

28

2001

43 7

58

2002

39 4

44

Lines per employee

1998

82

1999

83

2000

112

2001

113

2002

125

Telkom Group Annual Report 200242

Combating cable theft and network fraud

We continue to face the challenge of eliminating both cable theft and network fraud.The impact of network fraud, including subscription and clip-on fraud, has successfullybeen reduced to R174 million (2001: R274 million) as a result of enhanced systemsand proactive management. In 2002 we changed the manner in which we accountfor cable theft to include all direct costs. The new method of recording cable thefttogether with the increase in the number of theft incidents resulted in an increase toR249 million (2001: R131 million). Although the number of incidents increasedduring the year, the number of customers affected decreased as we effectively focusedon high-traffic routes and improved cable alarm monitoring to minimise revenue loss.

Decline in capital expenditure and change in structure

As we reach the end of our licence obligations, we have changed our capital spendingdecision process to ensure that adequate returns on investment are achieved. We arefocused on reducing capital expenditure in our wireline segment without impacting servicelevels. This year we started the process by reducing our capital spend to R6,9 billion,25% of revenues, from R8,1 billion in 2001, 31% of revenues.

During 2002 we further expanded our network capacity and continued the modernisationof the fixed-line network. We increased the number of digital exchanges to 4 083 (2001:3 894). Telkom has digitised 653 switches since 1998 and digitisation of the fixed-linenetwork today stands at 99,8% compared to 74% in 1997. There are now 195 (2001:129) Asynchronous Transfer Mode (ATM) switches connecting customers. Our fixed-linenetwork is fully managed from a single, centralised point, the National NetworkOperations Centre (NNOC).

Future capital expenditure will focus to a greater extent on improvements in operationssupport systems and maintaining the technological competence of our network.

“The past year was characterised by the balance we achievedbetween capital spend and service levels. Despite capitalcutbacks, service levels still improved. This is encouraging as itwill become more and more important to drive the cost out ofthe business without sacrificing quality.”

Ken Raley Managing Executive: Network Operations

Segment review – Wireline

ATM switches

1998

0

1999

45

2000

116

2001

129

2002

195

Exchange units

1998 1999

3 51

2

2000

3 69

7

2001

3 89

4

2002

4 08

3

3 01

9

Telkom Group Annual Report 2002 43

Segment reviewWireless

2002 8 170

2001 6 693

22% increaserevenues (Rm)

2002 1 984

2001 1 324

50% increaseoperating profit (Rm)

2002 7 778

2001 5 722

36% increaseassets (Rm)

2002 2 113

2001 1 603

32% increasecapex (Rm)

The wireless segment, which accounted for 20% (2001: 17%) of group

revenues, includes the results of Vodacom Group (Proprietary) Limited and

Swiftnet (Proprietary) Limited. We account for the 50% joint venture interest

in Vodacom under this segment using proportional consolidation.

Note: Segment results presented before intercompany eliminations

Telkom Group Annual Report 200244

Segment review – Wireless

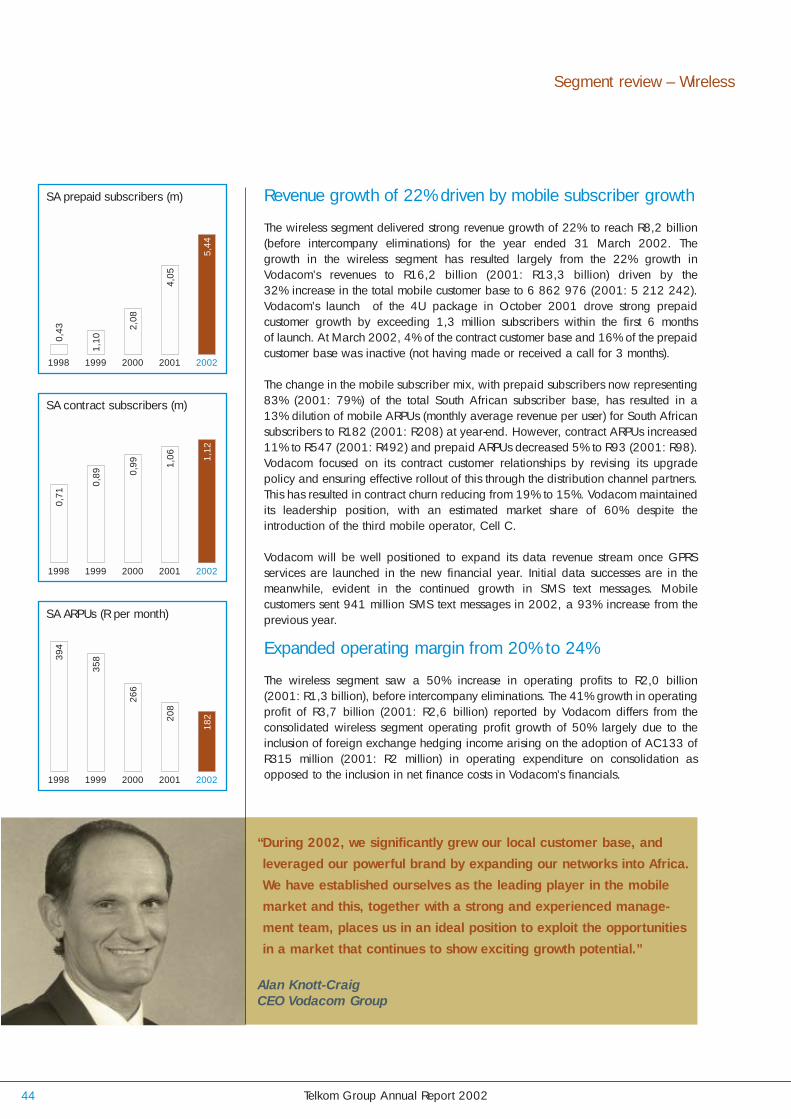

Revenue growth of 22% driven by mobile subscriber growth

The wireless segment delivered strong revenue growth of 22% to reach R8,2 billion(before intercompany eliminations) for the year ended 31 March 2002. Thegrowth in the wireless segment has resulted largely from the 22% growth inVodacom’s revenues to R16,2 billion (2001: R13,3 billion) driven by the32% increase in the total mobile customer base to 6 862 976 (2001: 5 212 242).Vodacom’s launch of the 4U package in October 2001 drove strong prepaidcustomer growth by exceeding 1,3 million subscribers within the first 6 monthsof launch. At March 2002, 4% of the contract customer base and 16% of the prepaidcustomer base was inactive (not having made or received a call for 3 months).

The change in the mobile subscriber mix, with prepaid subscribers now representing83% (2001: 79%) of the total South African subscriber base, has resulted in a13% dilution of mobile ARPUs (monthly average revenue per user) for South Africansubscribers to R182 (2001: R208) at year-end. However, contract ARPUs increased11% to R547 (2001: R492) and prepaid ARPUs decreased 5% to R93 (2001: R98).Vodacom focused on its contract customer relationships by revising its upgradepolicy and ensuring effective rollout of this through the distribution channel partners.This has resulted in contract churn reducing from 19% to 15%. Vodacom maintainedits leadership position, with an estimated market share of 60% despite theintroduction of the third mobile operator, Cell C.

Vodacom will be well positioned to expand its data revenue stream once GPRSservices are launched in the new financial year. Initial data successes are in themeanwhile, evident in the continued growth in SMS text messages. Mobilecustomers sent 941 million SMS text messages in 2002, a 93% increase from theprevious year.

Expanded operating margin from 20% to 24%

The wireless segment saw a 50% increase in operating profits to R2,0 billion(2001: R1,3 billion), before intercompany eliminations. The 41% growth in operatingprofit of R3,7 billion (2001: R2,6 billion) reported by Vodacom differs from theconsolidated wireless segment operating profit growth of 50% largely due to theinclusion of foreign exchange hedging income arising on the adoption of AC133 ofR315 million (2001: R2 million) in operating expenditure on consolidation asopposed to the inclusion in net finance costs in Vodacom’s financials.

SA prepaid subscribers (m)

1998 1999

1,10

2000

2,08

2001

4,05

2002

5,44

0,43

SA contract subscribers (m)

1998 1999

0,89

2000

0,99

2001

1,06

2002

1,12

0,71

SA ARPUs (R per month)

1998 1999

358

2000

266

2001

208

2002

182

394

“During 2002, we significantly grew our local customer base, andleveraged our powerful brand by expanding our networks into Africa.We have established ourselves as the leading player in the mobilemarket and this, together with a strong and experienced manage-ment team, places us in an ideal position to exploit the opportunitiesin a market that continues to show exciting growth potential.”

Alan Knott-CraigCEO Vodacom Group

Telkom Group Annual Report 2002 45

While Vodacom defended its market leadership position in South Africa and continuedto add customers to its network, it also ensured that further market penetration wasachieved at an acceptable margin. Despite expansion into Africa, administrative costshave successfully been contained. Vodacom has improved its efficiencies as evidencedby a 29% increase in subscribers per employee to 1 577 (2001:1 220).

As part of a longer term strategy, Vodacom refocused its activities to concentrateon its core businesses. This was assisted by the disposal of the investments in thesubsidiaries, Vodacom Sport and Entertainment (Proprietary) Limited and Film Fun(Holdings) (Proprietary) Limited, trading as Teljoy, and the 40% equity interest inVodacom World Online (Proprietary) Limited.

African expansion

Expanding our wireless segment further into Africa was facilitated by the VodacomBoard approval for the creation of a new company, Vodacom International.Vodacom’s future growth is supported by a strong balance sheet and it has adopteda conservative approach to its expansion strategy into Africa. Recourse to the SouthAfrican operations is limited where possible through the use of project finance.