knm group bhd 0.625 5.0 51.1 takaso res 0.515 (14.2)...

TRANSCRIPT

Daybreak│Malaysia

February 5, 2015

1

MALAYSIA

Malaysia Daybreak | 5 February 2015

▌What’s on the Table…

——————————————————————————————————————————————————————————————————————

Plantations - Preview of Jan palm oil stocks

A survey conducted by our futures team with 17 planters revealed that Malaysian palm oil output probably declined 17% mom to 1.13m tonnes in Jan 15, the lowest since Feb 11, due seasonal factor and flooding in East Malaysia. However, palm oil exports have also remained weak, falling by 14.8% mom due to competition from other edible oils and weaker demand for biodiesel usage. Overall, we project stocks to decline by 13% mom to a 6-month low to 1.75m tonnes as at end-Jan 15. The lower stock is near-term supportive of CPO price but our concerns over biodiesel demand risk remains. We maintain our Neutral rating and preference for First Resources, AALI and SIMP.

Alpha Edge - Asia’s time to shine?

US equity long-term indicators have just turned negative and it looks like for now, it is Asia’s time to outperform. We are already seeing signs of breaking out in some equity indexes in Asia. This uptrend is also evident in ASEAN equity indexes where Indonesia’s Jakarta Composite Index has recently surpassed its 2013 high. In view of recent weakness in the US$, crude oil prices finally rebounded last week but the medium-term trend remains down for oil.

Eco World Development Group Bhd - Pudu Jail joint venture finalised

Eco World announced today that it is subscribing to 40% of BBCC Development, which is a joint venture to develop 19.4 acres of land at the former site of the Pudu Jail. This announcement is not a surprise but will nonetheless be viewed positively, given the prime location of the land in Kuala Lumpur, the reasonable land cost and the high GDV value of RM8bn. The landbanking increases the ex-rights with free warrants RNAV from RM2.73 to RM2.79, and our target price rises accordingly. Eco World remains an Add with an unchanged target price basis of 20% discount to RNAV. No changes to our EPS forecasts, as details of the development have yet to be finalised. Eco World remains one of our top picks and its aggressive landbanking and strong sales are the key catalysts.

Muhibbah Engineering - Smaller wins for infra recovery

New information regarding job prospects suggests a slightly muted period for large-scale contract tenders in the months ahead. Muhibbah forgoing the RM1bn Pengerang jetty project due to pricing issues was a negative surprise but this is mitigated by its maiden contract win in Rapid today, and prospects for other domestic infra/port jobs, potentially resulting in contract flows similar to 2014’s. We cut FY14-16 EPS forecasts to reflect our more conservative assumptions while the lower target price is the result of a wider RNAV discount of 30% (20% previously) as smaller (but still lucrative) contract wins are more likely this year. The stock remains oversold and still offers attractive upside. Maintain Add. Muhibbah is our small/mid-cap pick.

▌News of the Day…

—————————————————————————————————————————————————————————————————————— • The RM8bn Bukit Bintang City Centre (BBCC) will kick off in 2Q15

• President/CEO of Petronas has been offered a 7-month contract extension

• Muhibbah Engineering was awarded its maiden job in Petronas's Rapid

• 1MDB filed for a 6-month extension for Jimah East power plant

• Khairy Jamaluddin has called on Tenaga to consider a tariff reduction

Sources: CIMB. COMPANY REPORTS

Sources: CIMB. COMPANY REPORTS

Key Metrics

FBMKLCI Index

1,650

1,700

1,750

1,800

1,850

1,900

Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Jan-15

———————————————————————————

FBMKLCI

1803.02 21.76pts 1.22%Feb Futures Mar Futures

1804.5 - (1.49% ) 1802 - (1.00% )———————————————————————————

Gainers Losers Unchanged468 398 318

———————————————————————————

Turnover2413.24m shares / RM2692.253m

3m avg volume traded 1809.01m shares

3m avg value traded RM1917.64m———————————————————————————

Regional IndicesFBMKLCI FSSTI JCI SET HSI

1,803 3,418 5,315 1,600 24,680 ————————————————————————————————

Close % chg YTD % chg

FBMKLCI 1,803.02 1.2 2.4

FBM100 12,098.83 1.0 2.4

FBMSC 16,016.95 0.9 6.5

FBMMES 6,513.45 (0.7) 15.2

Dow Jones 17,673.02 0.0 (0.8)

NASDAQ 4,716.70 (0.2) (0.4)

FSSTI 3,417.57 0.3 1.6

FTSE-100 6,860.02 (0.2) 4.5

SENSEX 28,883.11 (0.4) 5.0

Hang Seng 24,679.76 0.5 4.6

JCI 5,315.28 0.4 1.7

KOSPI 1,962.79 0.6 2.5

Nikkei 225 17,678.74 2.0 1.3

PCOMP 7,716.06 1.4 6.7

SET 1,599.81 (0.2) 6.8

Shanghai 3,174.13 (1.0) (1.9)

Taiwan 9,513.92 0.7 2.2————————————————————————————————

Close % chg Vol. (m)

ASIA BIOENERGY T 0.185 (24.5) 172.3

NEXGRAM HOLDINGS 0.080 6.7 66.4

SUMATEC RESOURCE 0.225 7.1 62.4

TAKASO RES 0.515 (14.2) 59.2

KNM GROUP BHD 0.625 5.0 51.1

DAYA MATERIALS 0.155 3.3 47.3

SANICHI TECHNOLO 0.085 (5.6) 44.5

EDUSPEC HOLDINGS 0.310 3.3 41.9————————————————————————————————

Close % chg

US$/Euro 1.1334 (0.11)

RM/US$ (Spot) 3.5625 (0.04)

RM/US$ (12-mth NDF) 3.6955 (0.34)

OPR (% ) 3.17 (2.16)

BR (% , CIMB Bank) 4.00 0.00

GOLD ( US$/oz) 1,269.68 0.04

WTI crude oil US spot (US$/barrel) 48.45 (8.67)

CPO spot price (RM/tonne) 2,180.00 2.35

Market Indices

Top Actives

Economic Statistics

————————————————————————————————————————

Terence WONG, CFA T (60) 3 2261 9088 E [email protected]

Show Style "View Doc Map"

Daybreak│Malaysia

February 5, 2015

2

Global Economic News

The US ISM's non-manufacturing purchasing managers index (PMI) stood at 56.7 in Jan (56.5 in Dec). (WSJ)

The US service-sector composite PMI by Markit rebounded to 54.2 in Jan (53.3 in Dec). Composite PMI was 54.4 in Jan (53.5 in Dec). (WSJ, Bloomberg)

US private employers added 213,000 jobs in Jan (253,000 in Dec). (CNBC)

Expressing confidence that weak inflation will eventually rise again, US Federal Reserve Bank of Cleveland President Loretta Mester said the central bank remains on track for raising rates in the next few months. She said “if incoming economic information supports my forecast, I would be comfortable with lift-off in the first half of this year." (WSJ)

Eurozone’s final Composite PMI stood at 52.6 in Jan (51.4 in Dec). Services PMI stood at 52.7 in Jan (51.6 in Dec). (Reuters, Bloomberg)

Eurozone retail sales grew 0.3% mom in Dec (+0.7% mom in Nov). On a yearly basis, retail sales growth accelerated to 2.8% yoy in Dec (+1.6% yoy in Nov). (RTT)

Japan’s average labour cash earnings advanced 1.6% yoy in Dec (+0.1% yoy in Nov). Real wages, adjusted for inflation, dropped 1.4% yoy in Dec (-2.7% yoy in Nov). (Japan Times, Bloomberg)

Japan's Markit/JMMA services PMI scored 51.3 in Jan (51.7 in Dec). The composite PMI posted a score of 51.7 in Jan (51.9 in Dec). (RTT)

The China HSBC/Markit Services PMI slowed to 51.8 in Jan (53.4 in Dec). The HSBC Composite PMI was 51.0 in Jan (51.4 in Dec). (Reuters, Bloomberg)

The People's Bank of China (PBOC) decided to lower the reserve requirement ratio (RRR) by 50 basis points from 5 Feb.

Currently, big banks must hold 20% of their deposits in reserve, while the ratio for small and medium-sized banks is 16.5%.

The PBOC also increased support to some target areas, cutting the RRR by an extra 50 basis points for certain commercial banks engaged in proportionate lending to small firms, the farming sector and major water projects.

The Agricultural Development Bank of China, the sole policy lender for agriculture, gets an RRR reduction of 4% pts. (Xinhua)

India’s HSBC Services PMI rose to 52.4 in Jan (51.1 in Dec). The composite PMI rose to 53.3 in Jan (52.9 in Dec). (India Times)

Daybreak│Malaysia

February 5, 2015

3

The Reserve Bank of India (RBI) Governor Raghuram Rajan said inflation is still a concern for the central bank and the monetary policy continues being "conventional".

"We still have concerns over inflation. So, given the deflationary environment elsewhere, it is actually easier for us because we are not fighting inflation in an environment where inflation is picking up elsewhere. I think we are still in conventional monetary policy territory," he said. (India Times)

South Korea’s foreign exchange reserves reached US$362.2bn in Jan (US$363.6bn in Dec). (Korea Herald)

Hong Kong’s HSBC manufacturing PMI fell to 49.4 in Jan (50.3 in Dec). (WSJ)

The Indonesian government has decided to lower the price of subsidized diesel fuel, which currently stands at IDR6,400 (US$0.51) per liter, in the near future, Energy and Mineral Resources Ministry said, thanks to cost reductions amounting to IDR300 per liter. (Jakarta Post)

Bank Indonesia’s Consumer Confidence Index increased to 120.2 point in Jan (116.5 in Dec). (Jakarta Post)

Thailand GDP could be boosted by about 1% this year thanks to lower global oil prices, according to a study by the Commerce Ministry's Policies and Trade Strategies Bureau.

The ministry's study also projected that the average global oil price would be about US$65 per barrel this year.

GDP could be fattened by 0.96%, inflation could be lower than the previously forecast of 1.8-2.5%, and export growth could expand by a 1% pts, it said in the study. (The Nation)

Malaysian Economic News

Moody’s Investors Service vice-president and senior analyst Christian de Guzman said the impact of lower oil prices on trade balance on Malaysia may be less immediate.

“The health of Malaysia’s current account surplus will likely depend on the follow-on impact of lower oil prices on LNG prices. The impact will be mitigated because much of the country’s LNG exports are secured by long-term offtaker contracts and are thus insulated to a certain extent from near-term volatility in the spot market,” he added.

He also said The sharp depreciation of the ringgit, which has fallen about 11% against the US dollar in the past six months, has “limited impact” on Malaysia’s sovereign ratings, said rating agency Moody’s Investors Service. This is because 97% of the Government debt is denominated in ringgit. (Financial Daily, Star)

The inclusion of a fiscal risk statement in the annual budget should help Malaysia plan for the medium term better, the World Bank’s senior economist for Malaysia, Dr Frederico Gil Sander, said.

Daybreak│Malaysia

February 5, 2015

4

Gil Sander also said this statement would include a sensitivity analysis and forecast of oil prices as well as how such price movements would impact the budget. “This will help the Government plan in advance,” he said. He suggested the adoption of the statement as part of the tabling of the annual budget to Parliament. Gil Sander said this would be a good time for Malaysia to implement the reforms aimed at lowering the fiscal deficit, as the country “is not facing a crisis”. (Star)

The ringgit gained the most since Sep 2013 and the benchmark stock index closed near the highest level in two months as an oil price recovery eased concern the nation’s finances will deteriorate.

The currency climbed 1.9% from 30 Jan to 3.5625 a dollar on 4 Feb. Brent crude jumped 5.8% on 3 Feb and has increased almost 19% in five days to US$57.38 a barrel. (Bloomberg)

Tun Dr Mahathir Mohamed has warned that falling oil prices and a weakening ringgit can hurt the Malaysian economy, refuting Putrajaya’s attempts to calm such fears in the past few weeks.

“Simply assuming that we are immune to the massive and widespread decline in the prices of almost all the raw materials and goods we produce for consumption and export does not reflect the depth of our understanding of the problems we face. We are a trading nation and changes affecting the world market must affect us one way or another,” he said. (Malaysian Insider)

The Cabinet advised traders to be responsible and considerate in determining the prices of goods and services in line with the drop in the prices of fuel, according to a statement issued by the Prime Minister's Office in Putrajaya.

The Cabinet felt that this would enable the consumers to feel the effects of the price reduction, the statement said. The Cabinet also advised consumers to exercise wisdom and use their power to coax traders to come up with reasonable prices for their goods. (Bernama)

Domestic Trade, Cooperatives and Consumerism Minister Datuk Seri Hasan Malek is to meet with wholesalers next week to seek an explanation on the prices of goods which consumers want reduced following the drop in fuel prices.

He said it was necessary to listen to their explanation because some of them had argued that the prices of goods were influenced not only by the prices of fuel but also other factors such as the rate of minimum wages and electricity tariff. (Malay Mail)

Moody's Investors Service expects the country’s residential property demand to slow further this year, crimped by property cooling measures imposed in 2013 and weak buyer sentiment.

“We expect the anticipation of higher mortgage rates in 2015 and the implementation of a 6% Goods and Services Tax in Apr to dampen sales in 2015, as buyers take a wait-and-see approach,” said Moody’s assistant vice-president and analyst Jacintha Poh. She added the magnitude of the sales impact will depend on Malaysian property developers' target segment of project launches and pricing. (Financial Daily)

Daybreak│Malaysia

February 5, 2015

5

Political News

Business leaders have condemned Datuk Seri Ismail Sabri Yaakob for his "irresponsible" call to boycott Chinese traders as it would only hurt the economy. They said attempts by Unity Minister Tan Sri Joseph Kurup to defuse the situation by saying Ismail Sabri's comments were "well-intended" only aggravated the matter.

Malaysia-China Chamber of Commerce fiscal and economic research deputy chairman Datuk Seri Gavin Tee said Ismail Sabri, who is agriculture and agro-based industry minister, had hampered the chamber's efforts to promote foreign trade and investment.

"Malaysia is facing strong competition, even within Asean," he said. Tee said other countries had negative perceptions about Malaysia being associated with "Islamism" and "terrorism".

"We have been trying our best to promote the country as a beautiful, peaceful and hamonious nation. We spent our own money and time so we could bring wealth to the country. In just a minute, Ismail Sabri has wasted all our hard work. It's akin to telling us to balik kampung, and forget about getting foreign investment."

Associated Chinese Chamber of Commerce and Industry Malaysia president Datuk Lim Kok Cheong said such a statement should not have been uttered by a minister. "It is unbelievable that such an irresponsible and racist remark was made by a federal minister who should be more sensitive," he said. (Malay Mail)

Umno leaders have succumbed to their own concoction of lies in an attempt to "poison" the minds of their Malay vote bank, opposition MP Tony Pua said yesterday. "Datuk Ismail Sabri, Datuk Zahid Hamidi and many other top BN and Umno leaders are all cut from the same cloth. They have no morals nor ethics, and they practice and believe in the Nazi propagandist, Dr Joseph Goebbels 'Big Lie'," Pua said in a statement.

He said Ismail Sabri's assertions that ethnic Chinese traders were deliberately hiking up the price of their goods and services as well as Perak DAP leader Datuk Ngeh Koo Ham being "anti-Islam" and the owner of cafe chain Old Town White Coffee were not only baseless but recycled claims that had been circulating on social media for over a year.

Home Minister Datuk Seri Ahmad Zahid Hamidi has also been found out to have told lies in alleging Pua a criminal suspect in Singapore who was let off after brokering a deal with its government to act as the republic's agent here, the DAP national publicity secretary said. He added that the home minister had to apologise openly in court last August as part of a settlement to the defamation suit he initiated against Ahmad. (Malay Mail)

The Cabinet was informed on Wednesday that a posting made on social media by Agriculture and Agro-Based Industry Minister Datuk Seri Ismail Sabri Yaakob was intended to advise traders who refused to reduce the prices of their goods in line with falling oil prices. The Prime Minister's Office (PMO) clarified that the minister's remarks were not targeted at a single race, but directed at all traders. "Prime Minister Datuk Seri Najib Razak has always stressed that Barisan Nasional will preserve and uphold the interests of all races. "Therefore, any dispute that can lead to racial polarisation in this country should not be prolonged as it will only harm us," PMO said in a statement on Wednesday. (Star)

Former Perak DAP chairman Datuk Ngeh Koo Ham yesterday tweeted a picture of him at the Ipoh police headquarters lodging a police report against Agriculture and Agro-based Industry Ministry Datuk Seri Ismail Sabri Yaakob. The report is believed to be linked to the remark Ismail had made on

Daybreak│Malaysia

February 5, 2015

6

Facebook which had created a stir due to him singling out Chinese traders who refused to lower the prices of their goods. Meanwhile, Ngeh, who is also Beruas Member of Parliament, clarified that there was only one DAP Ngeh family in the whole of Perak. This could be in response to Ismail's statement earlier that he did not specify which Ngeh in his Facebook remark that had gone viral. "He avoided responsibility for his statement by saying that he was not referring to me specifically by name as there are many Ngehs in Perak. (The Rakyat Post)

Datuk Seri Ismail Sabri Yaakob will not apologise for his Facebook post calling on the Malays to boycott Chinese traders who refuse to lower prices despite the fall in fuel prices. The Agriculture and Agro-based Industries Minister said he would also not apologise to Ngeh Koo Ham over an alleged remark that the Perak DAP adviser owned shares in the Old Town White Coffee cafe franchise and a purported reference to its halal status. (Star)

The MCA has made its stand clear on the Datuk Seri Ismail Sabri Yaakob's "boycott Chinese traders" remark at the Cabinet meeting. "I have conveyed the MCA stance on this issue to the Cabinet, and it has been agreed that such comments polarise the community and should cease immediately," party president Datuk Seri Liow Tiong Lai said. "It was clear cut racial profiling. We reject all forms of extremism and MCA has always been in this position and will continue to uphold this good value," Liow said. (Star)

Former Prime Minister Dr Mahathir Mohamad believed that Tong Kooi Ong is being attacked by anonymous bloggers due to the coverage of the 1Malaysia Development Bhd (1MDB) debacle by the latter's media organisations. "This is all because he was criticising 1MDB, so he is accused of betting against the ringgit. If he had not criticised 1MDB, even if the currency falls, he (Tong) won't matter, but just don't criticise 1MDB," said Mahathir. The former premier seemed to make light of allegations that Tong had manipulated the currency market to sabotage the economy. "Investigate first whether it is true or not. Because The Edge has criticised 1MDB a lot. This is what he (Tong) is now facing, accusations that he is betting against the ringgit. "Last time, our currency fell because of international traders. After that we can investigate whether he (Tong) has ties with (George) Soros," he said. (Malaysiakini, Malaysian Insider)

Opposition leader Datuk Seri Anwar Ibrahim said yesterday that any move to jail him next week on controversial sodomy charges could backfire against the Malaysian government. The nation's highest court is to deliver a final decision Tuesday on Anwar's appeal against a sodomy conviction and five-year jail term handed down last year.

A guilty verdict could effectively end the 67-year-old's career, removing the key player in a opposition coalition that has one of the world's longest-ruling governments on the run.

"That to my mind is for sure," Anwar said, when asked whether jailing him would turn him into a martyr and drive yet more support to the opposition. "Throughout history, (persecuting political opponents) has always backfired."

"Will this lead to further disgruntlement and therefore a surge in support (for the opposition)? I believe so," he said. Anwar stopped short of calling on supporters to take to the streets. (Malay Mail)

Daybreak│Malaysia

February 5, 2015

7

Corporate News

Lay Hong Bhd has proposed to issue 15.7m new shares, or 30% of its enlarged paid-up share capital, to independent third-party investors which it did not identify. The move, the company said in a filing with Bursa Malaysia yesterday, was intended to increase its public shareholding spread and comply with the exchange’s rules. The exercise, if approved by Lay Hong’s shareholders, will effectively dilute QL’s stake in the company. QL is currently the single-largest shareholder in Lay Hong with a 38.7% stake. Lay Hong said its proposals were expected to be completed in 2Q15. (StarBiz)

Comment: If this exercise goes through, it will have negligible impact on QL's bottom line (~1% impact) given the small net profit generated by Lay Hong.

The much-touted RM8bn redevelopment of the former Pudu jail site, to be known as Bukit Bintang City Centre (BBCC), will kick off as early as the second quarter of this year, after the site had been abandoned for nearly four years. The 19.4-acre piece of land will get a new lease of life through a special purpose vehicle (SPV) owned by Eco World Development Group (40%), UDA Holdings Bhd (40%) and the Employees Provident Fund Board (EPF) (20%), which will jointly develop the land into a mixed residential and commercial project. Under a joint development agreement signed yesterday, land-owner UDA will grant to the SPV - BBCC Development Sdn Bhd - full rights to carry out the development for RM1.013bn. (Financial Daily)

Pengerang Independent Terminals Sdn Bhd (PITSB), a joint venture vehicle between Dialog Group Bhd, the State Secretary of Johor and Rotterdam-based Royal Vopak NV, has leased its storage tanks to BP plc and Total SA, according to a Reuters report yesterday. "BP has leased more than half of the storage from Vopak, while Total will use the remainder," said Reuters, quoting industry resources, adding that the leases are likely for more than a year. A top company official in Vopak told a news agency that Vopak, the world's largest independent storage company, would start operations at the first commercial crude oil tank farm in Southeast Asia in March this year. However, it has been reported that MT Vinalise Glory was the first ship to dock at the terminal on April 12 last year. Dialog officials could not be reached for comment at the time of writing. (Financial Daily)

Muhibbah Engineering (M) Bhd clinched a USD32m (RM113.92m) construction subcontract for the Petroliam Nasiona Bhd's (Petronas) Refinery and Petrochemicals Integrated Development (Rapid) project in Pengerang Johor. In a filing with Bursa Malaysia yesterday, Muhibbah said it clinched the contract from Petronas contractor Tecnicas Reunidas SA Group. Muhibbah said it was appointed by Tecnicas Reunidas to design and build "temporary construction facilities and accommodation camp". The subcontract comes under package three of the Rapid project. (Financial Daily)

Youth and Sports Minister Khairy Jamaluddin has called on Tenaga Nasional Bhd to consider a reduction in the electricity tariff in line with the drop in the fuel price currently. "TNB should probably consider reducing the electricity tariff. Recently they had asked the Cabinet to raise the tariff because of the rise in fuel cost. Now, it has come down," he said. (Malaysian Reserve)

TH Heavy Engineering has called off its proposed rights issue with bonus issue. It said the approval from Bursa Malaysia Securities for more time to submit the draft circular and additional listing application in relation to the proposals to Bursa Securities had lapsed. TH Heavy said with the latest development, the proposed corporate exercise had been discontinued. (StarBiz)

Daybreak│Malaysia

February 5, 2015

8

IRM Group Bhd is facing the risk of its shares being delisted from Bursa Malaysia after having failed to submit a regularisation plan to the stock market regulator. Trading in the shares of IRM, whose subsidiaries are involved in the manufacturing and trading of plastic material, will be suspended from Feb 11. The company’s shares could be delisted on Feb 13 unless an appeal is submitted to the bourse on or before Feb 10. (StarBiz)

WZ Satu Bhd has just added another win to its order book after securing a RM124.12m contract to construct an elevated bridge over the existing Bayan Lepas Expressway at Batu Maung, Penang. Based on a filing with Bursa Malaysia, the company’s wholly-owned subsidiary WZS KenKeong Sdn Bhd received a letter of award for the job from UEM Construction Sdn Bhd. The project is expected to be completed by Nov 30, 2015. (Financial Daily)

Aluminium maker Press Metal Bhd (PMB) expects its production capacity to increase by 10% to 15% this year, driven by the second phase of its RM2bn expansion project for its aluminium smelter plant in Samalaju Industrial Park, Sarawak. "We foresee there will be about 10% to 15% (increase in production) for this year compared to 2014, boosted by the second phase of Samalaju's plant which is now operating at full capacity," its group CEO Datuk Paul Koon Poh Keong told. Koon said the group is currently constructing the third phase of its smelter plant in Samalaju Industrial Park, which is expected to start operating by the fourth quarter of 2015. He noted that the group will spend about RM1.34bn (two-third of RM2bn) for its capital expenditure for the financial year ended Dec 31, 2015. (The Sun)

Offshore support vessel service provider Silk Holdings Bhd has bagged a contract worth RM24.5m to provide one straight supply vessel with accommodation to ExxonMobil Exploration and Production Inc. Silk said the contract, which was awarded to its subsidiary Jasa Merin (M) Sdn Bhd, was for a primary term of two years and might be extended for a further one year at the discretion of ExxonMobil. (StarBiz)

Electronic component maker Inari Amertron Bhd’s net profit surged by 65% to RM40.32m in the second quarter ended Dec 31, 2014 from RM24.43m a year ago. This was achieved on the back of higher revenue while the company benefitted from a favourable foreign exchange rate and lower gold prices. Revenue jumped 22% to RM227.91m from a year ago, driven by higher trading volumes from existing business units, specifically the radio frequency business due to higher demand for smartphones and mobile devices. (Starbiz)

In a surprising move, Tan Sri Shamsul Azhar Abbas, the president and CEO of Petroliam Nasional Bhd (Petronas) is being offered a seven-month extension to his contract, according to sources. Previous media speculation had reported that Shamsul would be offered at least a one-year extension when his contract ends this Sunday. It is not clear why he is being offered only a seven-month extension but sources said that the Government would make an announcement soon on Shamsul’s successor.

Among the potential candidates as successor, according to sources, are Datuk Wan Zulkiflee Wan Ariffin, Datuk Mohd Anuar Taib and Datuk Ahmad Nizam Salleh. Wan Zulkiflee and Anuar are two names which have been repeatedly said to be strong replacements for the top job at Petronas, while Ahmad Nizam, as a potential contender, has somewhat come as a surprise.

Wan Zulkiflee, 54, is currently the chief operating officer and executive director of Petronas. He is also the executive vice-president of the

Daybreak│Malaysia

February 5, 2015

9

downstream business at the oil company and chairman of Petronas Chemicals Group Bhd and Petronas Dagangan Bhd.

Anuar is senior vice-president of Petronas’ upstream business in Malaysia, but is better known for his stint at Shell Malaysia, where he was chairman and vice-president of its upstream international business. However, industry observers opined that Anuar, at 48, was considered too young a candidate for the top post at Petronas.

The lesser-known Ahmad Nizam, who is 59 years old, is the managing director and CEO of Petronas’ 80%-owned unit Engen Ltd based in Cape Town, South Africa. Ahmad Nizam’s name had also surfaced a few years ago when he was said to be a possible candidate to replace former Petronas president and CEO Tan Sri Hassan Marican. Hassan left Petronas in February 2010.(StarBiz)

1Malaysia Development Bhd is believed to have filed for a six-month extension for the start of the operations for its Jimah East power plant due to financing difficulties, according to a source. However, this does not affect the timetable for the construction of the plant. Sources familiar to the matter said the extension is a breach of the power purchase agreement if approved. (Malaysian Reserve)

Daybreak│Malaysia

February 5, 2015

10

BMSB: Changes in shareholdings

Type of No of Ave Price

4-Feb-15 Date transaction securities Company (RM)

EPF 28/1 Disposed 3,000,000 DIALOG GROUP

EPF 28/1 Disposed 3,000,000 SP SETIA

EPF 28/1 Disposed 2,270,000 MAXIS

EPF 28/1 Disposed 2,137,200 TELEKOM MALAYSIA

EPF 28/1 Disposed 2,000,000 YTL CORPORATION

EPF 26/1-27/1 Disposed 1,135,300 FELDA GLOBAL VENTURES

EPF 28/1 Disposed 775,900 PUBLIC BANK

EPF 28/1 Disposed 710,400 UMW HOLDINGS

EPF 28/1 Disposed 568,300 YTL POWER INTERNATIONAL

EPF 28/1 Disposed 422,000 UEM SUNRISE

EPF 28/1 Disposed 300,000 CAPITAMALLS MALAYSIA TRUST

EPF 28/1 Disposed 300,000 MEDIA PRIMA

EPF 28/1 Disposed 216,300 AEON CO. (M)

EPF 28/1 Disposed 115,300 MAH SING GROUP

EPF 28/1 Disposed 26,600 NESTLE (MALAYSIA)

EPF 28/1 Disposed 20,000 IHH HEALTHCARE

EPF 28/1 Disposed 12,900 MBM RESOURCES

EPF 28/1 Disposed 8,300 SHELL REFINING

Skim Amanah Saham Bumiputera 29/1 Disposed 355,500 SUNWAY REIT

Skim Amanah Saham Bumiputera 28/1 Disposed 17,500 TENAGA NASIONAL

KHAZANAH NASIONAL BERHAD 29/1 Disposed 112,000,000 TENAGA NASIONAL

Permodalan Nasional Berhad 29/1 Disposed 600,000 UMW HOLDINGS

Kumpulan Wang Persaraan 26/1-27/1 Disposed 4,668,700 PRESTARIANG

Kumpulan Wang Persaraan 26/1-27/1 Disposed 1,223,100 PETRONAS GAS

Kumpulan Wang Persaraan 26/1-27/1 Disposed 1,198,800 GENTING PLANTATIONS

Kumpulan Wang Persaraan 26/1-27/1 Disposed 141,100 TOP GLOVE

T. Rowe Price Associates, Inc 26/1-28/1 Disposed 1,223,000 ASTRO MALAYSIA

Aberdeen Asset Management PLC 28/1-29/1 Disposed 19,900 TASEK CORPORATION

Mitsubishi UFJ Financial Group, Inc 28/1 Disposed 434,000 POS MALAYSIA

Mitsubishi UFJ Financial Group, Inc 28/1-29/1 Disposed 19,900 TASEK CORPORATION

EPF 28/1 Acquired 2,894,600 AFG

EPF 28/1 Acquired 850,000 SAPURAKENCANA PETROLEUM

EPF 28/1 Acquired 616,900 AMMB HOLDINGS

EPF 23/1-28/1 Acquired 374,400 KOSSAN RUBBER INDUSTRIES

EPF 28/1 Acquired 300,200 PETRONAS GAS

EPF 28/1 Acquired 179,000 MALAYSIA AIRPORTS

EPF 28/1 Acquired 76,500 HARTALEGA HOLDINGS

EPF 28/1 Acquired 39,200 TOP GLOVE

EPF 28/1 Acquired 38,700 AXIS REIT

EPF 27/1-28/1 Acquired 8,900 TENAGA NASIONAL

Skim Amanah Saham Bumiputera 29/1 Acquired 400,000 UMW HOLDINGS

Kumpulan Wang Persaraan 26/1-27/1 Acquired 1,198,800 GENTING PLANTATIONS

Kumpulan Wang Persaraan 26/1-27/1 Acquired 1,005,600 POS MALAYSIA

Kumpulan Wang Persaraan 26/1 Acquired 900,000 IGB REIT

Kumpulan Wang Persaraan 26/1-27/1 Acquired 838,300 UZMA

Kumpulan Wang Persaraan 26/1 Acquired 485,100 TDM BERHAD

Kumpulan Wang Persaraan 27/1 Acquired 410,400 SP SETIA

Genesis Investment Management, LLP 29/1 Acquired 499,900 7-ELEVEN MALAYSIA

Mitsubishi UFJ Financial Group, Inc 28/1-29/1 Acquired 40,722 BAT SOURCES: BMSB

Daybreak│Malaysia

February 5, 2015

11

MSB: ESOS & others

5-Feb-15 No Of New Shares Date of Listing Nature of transaction

IOI CORPORATION 186,000 05-Feb-15 Exercise of ESOS SOURCES: BMSB

BMSB: Off-market transactions

4-Feb-15 Vol

MATRIX 10,000,000

MEDAINC 10,000,000

NIHSIN 5,300,000

SIME 3,000,000

MAGNUM 3,000,000

TITIJYA 1,500,000

AEM 1,230,100

KRETAM 1,000,000

CHINWEL 700,000 Notes:CN-Crossing deal on board lots, MN-Married deal on board lots, MO-Married deal on odd lots

SOURCES: BMSB

BMSB: Entitlements & trading rights

5-Feb-15 Ann Date Entitlement Ex-date Entitlement

MALAYSIA

AIRPORTS

28-Nov-14 Right issue 1:5 @ RM4.78 24-Feb-15 26-Feb-15 SOURCES: BMSB, TE: Tax Exempt

BMSB: Dividends

Company Particulars Gross DPS (Sen) Ann Date Ex-Date Lodgement Payment

KLCC PROPERTY Final Income Distribution 4.86 26-Jan-15 9-Feb-15 11-Feb-15 27-Feb-15

IGB REIT Final Income Distribution 3.82 27-Jan-15 10-Feb-15 12-Feb-15 27-Feb-15

SUNWAY REIT Second Income Distribution 2.27 28-Jan-15 12-Feb-15 16-Feb-15 3-Mar-15

KUALA LUMPUR KEPONG Final dividend - single tier 40.00 19-Nov-14 19-Feb-15 23-Feb-15 17-Mar-15 SOURCES: BMSB

BMSB: Proposed cash calls & trading of rights…

5-Feb-15 Ann Date Proposed

ECO WORLD 25-Apr-14 1 Rights @ 2, 4 Free Warrants @ 5, Private Placement

ASIA FILE CORP 6-Aug-14 Bonus issue 3:5

BUMI ARMADA 12-Sep-14 1 Rights : 2 shares @ RM1.35

BENALEC HOLDINGS 12-Sep-14 > RM200m of 7-year Redeemable Convertible Secured Bonds

TH HEAVY ENGINEERING 24-Sep-14 Private placement of up to 10% of the issued shares of THHE

TH HEAVY ENGINEERING 3-Oct-14 Rights issue with bonus issue, 1 bonus issue : 5 Rights shares

MAH SING GROUP 20-Nov-14 Bonus issue 1:4

AIRASIA X 30-Nov-14 Rights issue of RM0.15 with free detachable warrants

SOURCES: BMSB

Daybreak│Malaysia

February 5, 2015

12

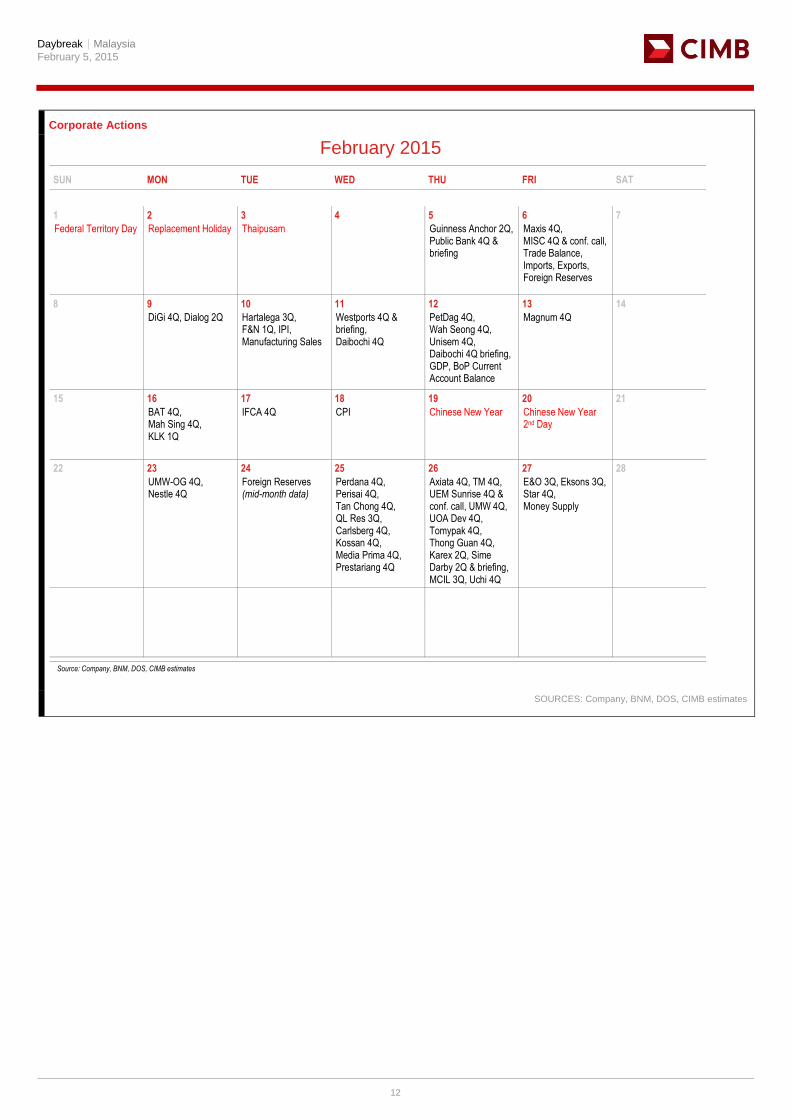

Corporate Actions

February 2015

SUN MON TUE WED THU FRI SAT

1 2 3 4 5 6 7

Federal Territory Day Replacement Holiday Thaipusam Guinness Anchor 2Q, Public Bank 4Q & briefing

Maxis 4Q, MISC 4Q & conf. call, Trade Balance, Imports, Exports, Foreign Reserves

8 9 10 11 12 13 14

DiGi 4Q, Dialog 2Q Hartalega 3Q, F&N 1Q, IPI, Manufacturing Sales

Westports 4Q & briefing, Daibochi 4Q

PetDag 4Q, Wah Seong 4Q, Unisem 4Q, Daibochi 4Q briefing, GDP, BoP Current Account Balance

Magnum 4Q

15 16 17 18 19 20 21

BAT 4Q, Mah Sing 4Q, KLK 1Q

IFCA 4Q CPI Chinese New Year Chinese New Year 2nd Day

22 23 24 25 26 27 28

UMW-OG 4Q, Nestle 4Q

Foreign Reserves (mid-month data)

Perdana 4Q, Perisai 4Q, Tan Chong 4Q, QL Res 3Q, Carlsberg 4Q, Kossan 4Q, Media Prima 4Q, Prestariang 4Q

Axiata 4Q, TM 4Q, UEM Sunrise 4Q & conf. call, UMW 4Q, UOA Dev 4Q, Tomypak 4Q, Thong Guan 4Q, Karex 2Q, Sime Darby 2Q & briefing, MCIL 3Q, Uchi 4Q

E&O 3Q, Eksons 3Q, Star 4Q, Money Supply

Source: Company, BNM, DOS, CIMB estimates

SOURCES: Company, BNM, DOS, CIMB estimates

Daybreak│Malaysia

February 5, 2015

13

Corporate Actions

March 2015

SUN MON TUE WED THU FRI SAT

1 2 3 4 5 6 7

BNM OPR Exports, Imports Trade Balance, Foreign Reserves

8 9 10 11 12 13 14

IPI, BNM OPR, Manufacturing Sales

15 16 17 18 19 20 21

CPI Foreign Reserves (mid-month data)

22 23 24 25 26 27 28

29 30 31

Money Supply

Source: Company, BNM, DOS, CIMB estimates

SOURCES: Company, BNM, DOS, CIMB estimates

Daybreak│Malaysia

February 5, 2015

14

DISCLAIMER #05

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

By accepting this report, the recipient hereof represents and warrants that he is entitled to receive such report in accordance with the restrictions set forth below and agrees to be bound by the limitations contained herein (including the “Restrictions on Distributions” set out below). Any failure to comply with these limitations may constitute a violation of law. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this report may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

Unless otherwise specified, this report is based upon sources which CIMB considers to be reasonable. Such sources will, unless otherwise specified, for market data, be market data and prices available from the main stock exchange or market where the relevant security is listed, or, where appropriate, any other market. Information on the accounts and business of company(ies) will generally be based on published statements of the company(ies), information disseminated by regulatory information services, other publicly available information and information resulting from our research.

Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Past performance is not a reliable indicator of future performance. The value of investments may go down as well as up and those investing may, depending on the investments in question, lose more than the initial investment. No report shall constitute an offer or an invitation by or on behalf of CIMB or its affiliates to any person to buy or sell any investments.

CIMB, its affiliates and related companies, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CIMB, its affiliates and its related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report.

CIMB or its affiliates may enter into an agreement with the company(ies) covered in this report relating to the production of research reports. CIMB may disclose the contents of this report to the company(ies) covered by it and may have amended the contents of this report following such disclosure.

The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. No part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations(s) or view(s) in this report. CIMB prohibits the analyst(s) who prepared this research report from receiving any compensation, incentive or bonus based on specific investment banking transactions or for providing a specific recommendation for, or view of, a particular company. Information barriers and other arrangements may be established where necessary to prevent conflicts of interests arising. However, the analyst(s) may receive compensation that is based on his/their coverage of company(ies) in the performance of his/their duties or the performance of his/their recommendations and the research personnel involved in the preparation of this report may also participate in the solicitation of the businesses as described above. In reviewing this research report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request.

Reports relating to a specific geographical area are produced by the corresponding CIMB entity as listed in the table below. The term “CIMB” shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, CIMB Group Holdings Berhad ("CIMBGH") and its affiliates, subsidiaries and related companies.

Country CIMB Entity Regulated by

Australia CIMB Securities (Australia) Limited Australian Securities & Investments Commission

Hong Kong CIMB Securities Limited Securities and Futures Commission Hong Kong

Indonesia PT CIMB Securities Indonesia Financial Services Authority of Indonesia

India CIMB Securities (India) Private Limited Securities and Exchange Board of India (SEBI)

Malaysia CIMB Investment Bank Berhad Securities Commission Malaysia

Singapore CIMB Research Pte. Ltd. Monetary Authority of Singapore

South Korea CIMB Securities Limited, Korea Branch Financial Services Commission and Financial Supervisory Service

Taiwan CIMB Securities Limited, Taiwan Branch Financial Supervisory Commission

Thailand CIMB Securities (Thailand) Co. Ltd. Securities and Exchange Commission Thailand

Information in this report is a summary derived from CIMB individual research reports. As such, readers are directed to the CIMB individual research report or note to review the individual Research Analyst's full analysis of the subject company. Important disclosures relating to the companies that are the subject of research reports published by CIMB and the proprietary positions by CIMB and shareholdings of its Research Analysts’ who prepared the report in the securities of the company(s) are available in the individual research report.

The information contained in this research report is prepared from data believed to be correct and reliable at the time of issue of this report. CIMB may or may not issue regular reports on the subject matter of this report at any frequency and may cease to do so or change the periodicity of reports at any time. CIMB is under no obligation to update this report in the event of a material change to the information contained in this report. This report does not purport to contain all the information that a prospective investor may require. CIMB or any of its affiliates does not make any

Daybreak│Malaysia

February 5, 2015

15

guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and opinion contained in this report. Neither CIMB nor any of its affiliates nor its related persons shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

This report is general in nature and has been prepared for information purposes only. It is intended for circulation amongst CIMB and its affiliates’ clients generally and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information and opinions in this report are not and should not be construed or considered as an offer, recommendation or solicitation to buy or sell the subject securities, related investments or other financial instruments thereof.

Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this research report. The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Australia: Despite anything in this report to the contrary, this research is provided in Australia by CIMB Securities (Australia) Limited (“CSAL”) (ABN 84 002 768 701, AFS Licence number 240 530). CSAL is a Market Participant of ASX Ltd, a Clearing Participant of ASX Clear Pty Ltd, a Settlement Participant of ASX Settlement Pty Ltd, and, a participant of Chi X Australia Pty Ltd. This research is only available in Australia to persons who are “wholesale clients” (within the meaning of the Corporations Act 2001 (Cth)) and is supplied solely for the use of such wholesale clients and shall not be distributed or passed on to any other person. This research has been prepared without taking into account the objectives, financial situation or needs of the individual recipient.

France: Only qualified investors within the meaning of French law shall have access to this report. This report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial instruments and it is not intended as a solicitation for the purchase of any financial instrument.

Hong Kong: This report is issued and distributed in Hong Kong by CIMB Securities Limited (“CHK”) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact the Head of Sales at CIMB Securities Limited. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CHK has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CHK. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CHK. Unless permitted to do so by the securities laws of Hong Kong, no person may issue or have in its possession for the purposes of issue, whether in Hong Kong or elsewhere, any advertisement, invitation or document relating to the securities covered in this report, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the securities laws of Hong Kong).

India: This report is issued and distributed in India by CIMB Securities (India) Private Limited (“CIMB India”) which is registered with SEBI as a stock-broker under the Securities and Exchange Board of India (Stock Brokers and Sub-Brokers) Regulations, 1992 and in accordance with the provisions of Regulation 4 (g) of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, CIMB India is not required to seek registration with SEBI as an Investment Adviser.

The research analysts, strategists or economists principally responsible for the preparation of this research report are segregated from the other activities of CIMB India and they have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues, client feedback and competitive factors. Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed or proposed to be performed by CIMB India or its affiliates.

Indonesia: This report is issued and distributed by PT CIMB Securities Indonesia (“CIMBI”). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBI has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBI. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBI. Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens wherever they are domiciled or to Indonesia residents except in compliance with applicable Indonesian capital market laws and regulations.

Malaysia: This report is issued and distributed by CIMB Investment Bank Berhad (“CIMB”). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMB has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMB. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

New Zealand: In New Zealand, this report is for distribution only to persons whose principal business is the investment of money or who, in the course of, and for the purposes of their business, habitually invest money pursuant to Section 3(2)(a)(ii) of the Securities Act 1978.

Daybreak│Malaysia

February 5, 2015

16

Singapore: This report is issued and distributed by CIMB Research Pte Ltd (“CIMBR”). Recipients of this report are to contact CIMBR in Singapore in respect of any matters arising from, or in connection with, this report. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBR has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only. If the recipient of this research report is not an accredited investor, expert investor or institutional investor, CIMBR accepts legal responsibility for the contents of the report without any disclaimer limiting or otherwise curtailing such legal responsibility. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBR..

As of February 4, 2015, CIMBR does not have a proprietary position in the recommended securities in this report.

South Korea: This report is issued and distributed in South Korea by CIMB Securities Limited, Korea Branch ("CIMB Korea") which is licensed as a cash equity broker, and regulated by the Financial Services Commission and Financial Supervisory Service of Korea.

The views and opinions in this research report are our own as of the date hereof and are subject to change, and this report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial investment instruments and it is not intended as a solicitation for the purchase of any financial investment instrument.

This publication is strictly confidential and is for private circulation only, and no part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB Korea.

Sweden: This report contains only marketing information and has not been approved by the Swedish Financial Supervisory Authority. The distribution of this report is not an offer to sell to any person in Sweden or a solicitation to any person in Sweden to buy any instruments described herein and may not be forwarded to the public in Sweden.

Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer or a placement within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China.

Thailand: This report is issued and distributed by CIMB Securities (Thailand) Company Limited (CIMBS). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBS has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBS. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBS.

CIMB Securities (Thailand) Co., Ltd. may act or acts as Market Maker and issuer including offering of Derivative Warrants Underlying securities of the following securities. Investors should carefully read and study the details of the derivative warrants in the prospectus before making investment decisions.

AAV, ADVANC, AMATA, ANAN, AOT, AP, ASP, BANPU, BAY, BBL, BCH, BCP, BEC, BECL, BGH, BH, BIGC, BJC, BJCHI, BLA, BLAND, BMCL, BTS, CENTEL, CK, CPALL, CPF, CPN, DCC, DELTA, DEMCO, DTAC, EARTH, EGCO, ERW, ESSO, GFPT, GLOBAL, GLOW, GUNKUL, HEMRAJ, HMPRO, INTUCH, IRPC, ITD, IVL, JAS, KBANK, KCE, KKP, KTB, KTC, LH, LOXLEY, LPN, M, MAJOR, MC, MCOT, MEGA, MINT, NOK, NYT, PS, PSL, PTT, PTTEP, PTTGC, QH, RATCH, ROBINS, RS, SAMART, SCB, SCC, SCCC, SIRI, SPALI, SPCG, SRICHA, STA, STEC, STPI, SVI, TASCO, TCAP, TFD, THAI, THCOM, THRE, THREL, TICON, TISCO, TMB, TOP, TPIPL, TTA, TTCL, TTW, TUF, UMI, UV, VGI, TRUE, WHA.

Corporate Governance Report:

The disclosure of the survey result of the Thai Institute of Directors Association (“IOD”) regarding corporate governance is made pursuant to the policy of the Office of the Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailand and the Market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from the perspective of a third party. It is not an evaluation of operation and is not based on inside information.

The survey result is as of the date appearing in the Corporate Governance Report of Thai Listed Companies. As a result, the survey result may be changed after that date. CIMBS does not confirm nor certify the accuracy of such survey result.

Score Range: 90 - 100 80 - 89 70 - 79 Below 70 or No Survey Result

Description: Excellent Very Good Good N/A

United Arab Emirates: The distributor of this report has not been approved or licensed by the UAE Central Bank or any other relevant licensing authorities or governmental agencies in the United Arab Emirates. This report is strictly private and confidential and has not been reviewed by, deposited or registered with UAE Central Bank or any other licensing authority or governmental agencies in the United Arab Emirates. This report is being issued outside the United Arab Emirates to a limited number of institutional investors and must not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose. Further, the information contained in this report is not intended to lead to the sale of investments under any subscription agreement or the conclusion of any other contract of whatsoever nature within the territory of the United Arab Emirates.

Daybreak│Malaysia

February 5, 2015

17

United Kingdom and Europe: In the United Kingdom and European Economic Area, this report is being disseminated by CIMB Securities (UK) Limited (“CIMB UK”). CIMB UK is authorised and regulated by the Financial Conduct Authority and its registered office is at 27 Knightsbridge, London, SW1X 7YB. This report is for distribution only to, and is solely directed at, selected persons on the basis that those persons: (a) are persons that are eligible counterparties and professional clients of CIMB UK; (b) have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the “Order”); (c) are persons falling within Article 49 (2) (a) to (d) (“high net worth companies, unincorporated associations etc”) of the Order; (d) are outside the United Kingdom; or (e) are persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) in connection with any investments to which this report relates may otherwise lawfully be communicated or caused to be communicated (all such persons together being referred to as “relevant persons”). This report is directed only at relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this report relates is available only to relevant persons and will be engaged in only with relevant persons.

Only where this report is labelled as non-independent, it does not provide an impartial or objective assessment of the subject matter and does not constitute independent "investment research" under the applicable rules of the Financial Conduct Authority in the UK. Consequently, any such non-independent report will not have been prepared in accordance with legal requirements designed to promote the independence of investment research and will not subject to any prohibition on dealing ahead of the dissemination of investment research.

United States: This research report is distributed in the United States of America by CIMB Securities (USA) Inc, a U.S.-registered broker-dealer and a related company of CIMB Research Pte Ltd, CIMB Investment Bank Berhad, PT CIMB Securities Indonesia, CIMB Securities (Thailand) Co. Ltd, CIMB Securities Limited, CIMB Securities (Australia) Limited, CIMB Securities (India) Private Limited, and is distributed solely to persons who qualify as "U.S. Institutional Investors" as defined in Rule 15a-6 under the Securities and Exchange Act of 1934. This communication is only for Institutional Investors whose ordinary business activities involve investing in shares, bonds and associated securities and/or derivative securities and who have professional experience in such investments. Any person who is not a U.S. Institutional Investor or Major Institutional Investor must not rely on this communication. The delivery of this research report to any person in the United States of America is not a recommendation to effect any transactions in the securities discussed herein, or an endorsement of any opinion expressed herein. CIMB Securities (USA) Inc, is a FINRA/SIPC member and takes responsibility for the content of this report. For further information or to place an order in any of the above-mentioned securities please contact a registered representative of CIMB Securities (USA) Inc.

Other jurisdictions: In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is only for distribution to professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (Thai IOD) in 2014.

AAV – Very Good, ADVANC – Very Good, AEONTS – not available, AMATA - Good, ANAN – Very Good, AOT – Very Good, AP - Good, ASK – Very Good, ASP – Very Good, BANPU – Very Good , BAY – Very Good , BBL – Very Good, BCH – not available, BCP - Excellent, BEAUTY – Good, BEC - Good, BECL – Very Good, BGH - not available, BH - Good, BIGC - Very Good, BJC – Good, BLA – Very Good, BMCL - Very Good, BTS - Excellent, CCET – Good, CENTEL – Very Good, CHG – not available, CK – Very Good, CPALL – not available, CPF – Very Good, CPN - Excellent, DELTA - Very Good, DEMCO – Good, DTAC – Very Good, EA - Good, ECL – not available, EGCO - Excellent, GFPT - Very Good, GLOBAL - Good, GLOW - Good, GRAMMY - Excellent, HANA - Excellent, HEMRAJ – Very Good, HMPRO - Very Good, ICHI - not available, INTUCH - Excellent, ITD – Good, IVL - Excellent, JAS – not available, JUBILE – not available, KAMART – not available, KBANK - Excellent, KCE - Very Good, KGI – Good, KKP – Excellent, KTB - Excellent, KTC – Good, LH - Very Good, LPN – Very Good, M - not available, MAJOR - Good, MAKRO – Good, MBKET – Good, MC – Very Good, MCOT – Very Good, MEGA – Good, MINT - Excellent, OFM – Very Good, OISHI – Good, PS – Very Good, PSL - Excellent, PTT - Excellent, PTTEP - Excellent, PTTGC - Excellent, QH – Very Good, RATCH – Very Good, ROBINS – Very Good, RS – Very Good, SAMART - Excellent, SAPPE - not available, SAT – Excellent, SAWAD – not available, SC – Excellent, SCB - Excellent, SCBLIF – Good, SCC – Very Good, SCCC - Good, SIM - Excellent, SIRI - Good, SPALI - Excellent, STA – Very Good, STEC - Good, SVI – Very Good, TASCO – Good, TCAP – Very Good, THAI – Very Good, THANI – Very Good, THCOM – Very Good, THRE – not available, THREL – Good, TICON – Good, TISCO - Excellent, TK – Very Good, TMB - Excellent, TOP - Excellent, TRUE – Very Good, TTW – Very Good, TUF - Good, VGI – Very Good, WORK – not available.

Daybreak│Malaysia

February 5, 2015

18

CIMB Recommendation Framework

Stock Ratings Definition:

Add The stock’s total return is expected to exceed 10% over the next 12 months.

Hold The stock’s total return is expected to be between 0% and positive 10% over the next 12 months.

Reduce The stock’s total return is expected to fall below 0% or more over the next 12 months.

The total expected return of a stock is defined as the sum of the: (i) percentage difference between the target price and the current price and (ii) the forward net dividend yields of the stock. Stock price targets have an investment horizon of 12 months.

Sector Ratings Definition:

Overweight An Overweight rating means stocks in the sector have, on a market cap-weighted basis, a positive absolute recommendation.

Neutral A Neutral rating means stocks in the sector have, on a market cap-weighted basis, a neutral absolute recommendation.

Underweight An Underweight rating means stocks in the sector have, on a market cap-weighted basis, a negative absolute recommendation.

Country Ratings Definition:

Overweight An Overweight rating means investors should be positioned with an above-market weight in this country relative to benchmark.

Neutral A Neutral rating means investors should be positioned with a neutral weight in this country relative to benchmark.

Underweight An Underweight rating means investors should be positioned with a below-market weight in this country relative to benchmark.

*Prior to December 2013 CIMB recommendation framework for stocks listed on the Singapore Stock Exchange, Bursa Malaysia, Stock Exchange of Thailand, Jakarta Stock Exchange, Australian Securities Exchange, Taiwan Stock Exchange and National Stock Exchange of India/Bombay Stock Exchange were based on a stock’s total return relative to the relevant benchmarks total return. Outperform: expected to exceed by 5% or more over the next 12 months. Neutral: expected to be within +/-5% over the next 12 months. Underperform: expected to be below by 5% or more over the next 12 months. Trading Buy: expected to exceed by 3% or more over the next 3 months. Trading Sell: expected to be below by 3% or more over the next 3 months. For stocks listed on Korea Exchange, Hong Kong Stock Exchange and China listings on the Singapore Stock Exchange. Outperform: Expected positive total returns of 10% or more over the next 12 months. Neutral: Expected total returns of between -10% and +10% over the next 12 months. Underperform: Expected negative total returns of 10% or more over the next 12 months. Trading Buy: Expected positive total returns of 10% or more over the next 3 months. Trading Sell: Expected negative total returns of 10% or more over the next 3 months.