key findings from the multi-asset solutions strategy summit

TRANSCRIPT

FOR INSTITUTIONAL/WHOLESALE/PROFESSIONAL CLIENTS AND QUALIFIED INVESTORS ONLY NOT FOR RETAIL USE OR DISTRIBUTION

Global Asset Allocation Views

Key findings from the Multi-Asset Solutions Strategy Summit

3Q 2021

AUTHOR

John Bilton Managing Director Head of Global Multi-Asset Strategy

Multi-Asset Solutions

Cyclical indicators in the U.S. point to a rapidly healing economy now in mid-cycle

EXHIBIT 2: U.S. U-3 UNEMPLOYMENT RATE, % OF LABOR FORCE AND NAIRU ESTIMATE

Source: U.S. Bureau of Labor Statistics, U.S. Congressional Budget Office , J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

0%

2%

4%

6%

8%

10%

12%

14%

2006 2008 2011 2014 2017 2020

U-3 U.S. Unemployment Rate Natural Rate of Unemployment (Long-Term)

Asset class Opportunity Set UW N OW Chg Conviction

MAIN ASSET

CLASSES

Equities High

Duration Low

Credit Low

Cash Moderate

PREF

EREN

CE B

Y AS

SET

CLA

SS

EQU

ITIE

S

U.S. Moderate

Europe Moderate

UK

Japan Moderate

Emerging markets

FIXE

D IN

COM

E

U.S. Treasuries Low

G4 ex-U.S. sovereigns

EMD hard currency ▼

EMD local FX ▼

Corporate inv. grade

Corporate high yield Low

FX

USD

EUR Low

JPY Moderate

EM FX Low

IN B R I E F

• The U.S. economy is moving toward mid cycle, while other developed markets remainlargely in early cycle; signals that the Federal Reserve will eventually removeaccommodation still leave policy today extremely supportive but mitigate inflationfears.

• We are overweight (OW) stocks and favor cyclical regions; we also expect renewedfocus on earnings quality and secular growth themes. We are OW Europe and Japan,and more balanced between U.S. large and small cap, but feel it is too soon to return to emerging markets.

• We have a mild underweight (UW) to duration and have pared our OW to credit,reflecting our belief that rates along the yield curve will increase slowly and that creditspreads are already very tight. Moderately higher U.S. rates also point to more supportfor USD in 2H21.

• Our portfolios are set up for further upside in economic growth and risk asset returns;inflation risks are fading, but the risks relating to vaccine/virus data, earnings growthand policy continue to be areas we watch closely.

EXHIBIT 1: MAS ASSET CLASS VIEWS

GLOBAL ASSET ALLOCATION VIEWS

2 Multi-Asset Solutions

SUMMARY

Since the start of 2021, global equities have advanced 11% and

aggregate 10-year government bond yields have moved 40 basis

points (bps) higher. High frequency data suggest that economic

activity is surging, aggregate household balance sheets are in

good health, and economic output in developed markets is

expected to surpass pre-pandemic levels by 3Q21.

The question, perhaps, might be why the Federal Reserve (Fed)

has not been even more anxious to withdraw monetary stimulus

than the somewhat hawkish tone at the June policy meeting

implied. The answer lies in the high level of unemployment that

has persisted since the pandemic lockdowns. True, economic

reopening will mop up labor slack quickly. But getting people

back to work and reinforcing the recovery remain policymakers’

principal goals today. At the same time, investors worry about

the inflationary implications of massive monetary and fiscal

stimulus. Yet asset markets were less than enthusiastic when the

Fed made clear that it would not allow inflation to run away.

The Fed’s tone was a hawkish surprise even as its current policy

remains dovish. In the context of the prevailing economic data,

the tone suggests that the U.S. economy is now in a mid-cycle

phase. Mid-cycle dynamics tend to support stocks moving higher

and rates rising along the yield curve — something we expect to

see in this cycle, too. However, elevated inflation in the near

term, pent-up demand and an excess of global liquidity imply

that there may be upside risks to the normally steady grind of

mid-cycle returns.

As the reopening trend spreads out from the U.S., we expect to

see a prolonged period of above-trend global growth. Although

economic indicators in the U.S. point to mid cycle, in Europe and

Japan economies still appear to be in the early phase of the cycle.

With capex strong and consumers poised to unleash meaningful

pent-up demand — likely to be directed more toward the services

side of the economy — we expect above-trend global growth to

persist well into 2022. This will in turn lend solid support to

corporate earnings.

Base effects, supply-chain disruption and the impact of fiscal

stimulus have combined to push inflation higher, notably in the

U.S. As we move toward autumn, we expect inflation to ease but

upside risks to persist. Importantly, the Fed’s marginally hawkish

tone suggests that higher rates — when they materialize — will

from here be led by rising real rates rather than further advances

in inflation breakevens.

With the extremes of policy accommodation likely behind us, the

global economic backdrop has slightly changed, taking on a more

mid-cycle feel. Nevertheless, the surge of reopening activity and

already-ample liquidity support a risk-on tilt in portfolios. We

continue to overweight equities with fairly high conviction and

underweight cash with moderate conviction. We also overweight

credit, but at the margin we are reducing exposure, given tight

spreads. And while we retain an underweight in duration, our

conviction level is low, given central bank bond purchases.

Within equities, we keep our preference for cyclical markets in

Europe and Japan, and at the margin have trimmed our tilt

toward value-style stocks. While the value factor remains

attractive relative to the growth factor, we are inclined to also

focus a little more on the quality factor as we move into mid

cycle. This leads us to reevaluate U.S. equities, where we believe

quality of earnings and a renewed focus on secular growth

themes may provide support in 2H21. By contrast, we think it is

too early to rotate back toward emerging market (EM) stocks —

particularly as the Fed’s recent policy shift lends some near-term

support to the dollar. In fixed income, our duration underweights

are concentrated in U.S. Treasuries, and our credit overweight

continues to be expressed in U.S. high yield (HY) and crossover

credit — albeit with lighter exposures. We continue to expect

higher sovereign yields over the remainder of 2021 but see a

much reduced risk of a disorderly bond market sell-off.

Above all, we look increasingly to diversify equity exposure

across a range of markets, in keeping with the broadening of

global growth. Corporate earnings failing to come through,

unjustified policy tightening and new vaccine-resistant strains of

COVID-19 all present downside risks. At the same time, consumer

and corporate spending booms present topside risks — which

could possibly be followed by an inflationary episode. But our

core case remains above-trend growth well into 2022, driving

further upside to global stocks and, eventually, to global yields.

GLOBAL ASSET ALLOCATION VIEWS

3 Multi-Asset Solutions

MACRO OVERVIEW

With virus fears receding in much of the world, a powerful

rebound in economic activity has taken hold, one that we think

will deliver annualized global real GDP growth exceeding 8% in

the middle two quarters of this year. Subsequent deceleration

appears inevitable, but we believe growth will hold above its

medium-term trend rate through 2022. The rapidity of this

bounce has moved the U.S. economy through the early part of

this expansion and into a mid-cycle phase. The associated near-

term rise in inflation has proven more intense than previously

expected, at least in the U.S., and we think some of this pressure

will persist. In our judgment, though, recession risk during our

tactical investment period remains very low, and we think

monetary policy will continue to be accommodative for an

extended period.

INTO MID CYCLE, BUT FEW WARNING SIGNS

Our U.S. business-cycle scorecard now shows most of the

economic categories in mid-cycle territory, and the same is true

for a majority of the market metrics (Exhibit 3). What does this

mean for the outlook? It suggests that the nearly automatic

recovery phase of the expansion is largely complete, with few

remaining easy gains as various forms of activity normalize.

Markets have experienced a similar phenomenon, with valuations

having risen strongly off their lows. We do not, however, believe

that the clock is ticking on the expansion. We see few significant

vulnerabilities in the economy – barring, perhaps, a variant-

driven resurgence of the virus later this year – that could

plausibly lead to a recessionary change in behavior. Nor do we

find a typical mid-cycle slowdown particularly likely. Admittedly,

we forecast deceleration in growth in the second half of this year.

But we do not expect a dip below the trend rate of the type that

dents corporate earnings and causes market participants to

worry about cumulating downside risks.

Much of our comfort with the sustainability of the expansion

stems from the strength of corporate and household balance

sheets and income flows. To be sure, elevated corporate leverage

already caught our eye during the previous expansion, and last

year’s recession not only failed to clear the decks in this area but

resulted in a ratcheting upward of indebtedness. Three factors,

however, temper our concerns on this front. First, the rise in

leverage that resulted from the downturn appears to have run its

course. Most credit metrics leveled off in the first quarter, and

they should improve through the remainder of the year. Second,

with interest rates declining further, debt service obligations

appear moderate by historical standards. Third, corporate flows

look healthy. For example, the corporate financing gap – the

difference between business capex and free cash flow – has

moved into negative territory, meaning firms are easily funding

their investment from internal funds. Corporates thus have not

been behaving in exuberantly expansionary fashion, suggesting

little near-term need or inclination for a pullback.

Thanks to a combination of federal government income support

and very cautious behavior, household balance sheets have

improved sharply in an aggregate sense over the past year.

Household net worth, expressed as a share of income, stands

near a record high. Debt has held steady, but with a favorable

composition shift away from high rate revolving credit to lower

cost mortgages. And the “excess saving” flows since the

pandemic shock now total USD 2.4 trillion, by our estimate. Most

of this savings has gone into cash balances, which look high

relative to other assets (Exhibit 4). While the differing nature of

fiscal stimulus elsewhere in the world means that households in

other economies have accumulated smaller stockpiles, saving

rates are running at elevated levels in many places. We therefore

see room for more expansionary behavior globally, not just in the

U.S.

Excess saving has swelled cash balances

EXHIBIT 4: U.S. HOUSEHOLD CASH HOLDINGS, YEAR-ON-YEAR CHANGE (%)

Source: Haver Analytics, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

-2

-1

0

1

2

3

4

5

-10

-5

0

5

10

15

20

1953 1963 1973 1983 1993 2003 2013

YoY change in % of GDP YoY change in USD(Trillions)

GLOBAL ASSET ALLOCATION VIEWS

4 Multi-Asset Solutions

Productivity growth and its relationship with wage gains, as

always, will play a major role in shaping the length and vigor of

the current expansion. Currently available data show a surge in

unit labor costs over the past few quarters. Taken at face value,

that development implies a combination of downward pressure

on corporate profit margins and an inflationary impulse. But the

national accounts measure of wages, which enters this

calculation, appears to have been distorted by large composition

shifts in the workforce. Metrics that adjust for these changes

show a much more moderate path for wage growth. The

published data for productivity likely suffer from similar effects,

but productivity growth did appear to be turning upward before

the pandemic hit, and the strong early rebound in business

investment spending bodes well for ongoing expansion of the

capital stock. Sustained improvement in productivity growth,

relative to the disappointing experience during the previous

cycle, would allow for a healthy combination of wage increases,

stable inflation and profit margins.

GROWTH: ABOVE-TREND INTO NEXT YEAR

Fluctuations in local virus conditions, with their knock-on effects

on personal mobility and private sector confidence, have

dominated growth outcomes since early 2020. Significant

progress on vaccination should push the virus into the

background as a growth driver, barring the widespread

circulation of a new inoculation-resistant variant. As virus risk

fades, we expect that healthy balance sheets, elevated saving

rates, firm private sector confidence and supportive financial

conditions will facilitate above-trend growth for the global

economy through 2022. In the aggregate, global growth is likely

now in the process of topping out, but we expect a series of

rolling peaks at the country level through the end of this year, in

line with differential easing of restrictions.

In addition to those fundamental drivers, we are monitoring

several cross-country phenomena that will influence growth

outcomes this year and next. First is the gradual waning of fiscal

stimulus. After unprecedented support for private sector incomes

last year and in early 2021, most governments are now stepping

back. To be sure, public sector deficits remain large, and

negotiations are underway in the U.S. toward another package,

this time focused on infrastructure. But even in the U.S., the 12-

month sum of the fiscal deficit has already begun narrowing.

Further, the spending being discussed would be spaced out over

a decade and would not alter that trajectory in the near term. We

believe that the character of fiscal stimulus over the last year,

which essentially replaced (with cash) lost wages and sales,

means that it can be withdrawn smoothly alongside private

sector healing. In our view, this on-paper fiscal tightening will not

generate significant drags on growth, but we will need to

examine this hypothesis repeatedly in coming quarters.

Second, labor markets are healing in very different ways, based

on their immediate reaction to the shock. In Europe, Japan and

Australia, policymakers cushioned labor markets by creating (or

expanding) furlough and short-hour schemes, essentially freezing

firm-employee relations in place. Open unemployment rates thus

rose very little despite the steep contraction in activity. As

economies reopen, labor market data might look oddly weak for

a time, especially if jobs need to be reallocated across the

economy. By contrast, in the U.S. and Canada, labor markets

adjusted sharply last year, and their recovery will now need to be

characterized by rising participation (as sidelined workers return

to the labor force) and better matching (as available openings

are filled with currently unemployed or inactive people). Success

on these fronts should show up in broad measures like the

employment-to-population ratio, which will likely serve as a

better gauge of healing than will payroll figures alone.

Third, as economies reopen, we expect a shift in spending back

toward services, unwinding at least part of the rise in the goods

share of consumption that occurred last year. The recovery in

services should help labor markets, given their more worker-

intensive nature. But goods activities are over-represented in

public equity and credit markets (compared with the composition

of GDP), and an outright fall in goods spending might therefore

represent a headwind for investors. If our forecast for the path of

U.S. consumer spending through the end of 2021 came true and

were accompanied by a full reversal in the goods share, back to

its end-2020 level, U.S. household spending on goods would

indeed decline somewhat. But we think goods activity would

remain well supported globally. Consumption of goods did not

surge as much outside the U.S., having lagged notably in China

and Japan. And capex, which accounts for about one-third of

goods demand, should stay strong almost everywhere. Even in

the U.S., the unwind in the goods share of consumption will likely

take longer than a few quarters to play out, given elevated

housing activity. Meanwhile, near-term supply disruptions are

GLOBAL ASSET ALLOCATION VIEWS

5 Multi-Asset Solutions

leading firms to once again draw down inventories. Companies

attempted to rebuild stocks around the turn of the year, but

factors like the shortage of semiconductors have been thwarting

those plans. As a result, production is running short of sales in

many sectors. As bottlenecks ease later this year, we expect an

inventory rebuilding cycle to give further impetus to industrial

output globally.

Among developed market (DM) economies, Japan has turned in a

relatively lackluster growth performance so far this year. But we

expect momentum to rebound strongly in 2H21, helped by a

faster than expected vaccine rollout, which should prove critical

for Japan’s consumption recovery, and solid external demand.

Limited vaccine supply, which was the main cause of Japan’s

initially slow vaccine rollout, is no longer a problem, as Japan’s

government has secured delivery of 140 million doses by the end

of June, enough to cover 70% of Japan’s adult population.

Logistics problems also turned out to be less severe than

expected. As a result, daily vaccinations have accelerated rapidly

since mid-May to a current rate of around 1.1 million doses per

day.

In our view, the key milestone for Japan’s total vaccination rate is

one-third of the population, which covers all the medical workers

and over-65-year-olds. At the current pace, this target should be

reached before the end of July (Exhibit 5). Vaccinating the elderly

is important for both reopening the economy and spurring a

consumption rebound: over-65-year-olds account for 40% of

total consumption.

Japan’s vaccination rollout gathering speed

EXHIBIT 5: JAPAN’S VACCINATION SCENARIOS

Source: CEIC, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021. *Full coverage of medical workers and over-65-year-olds.

Weakness in Japan’s consumption has been concentrated in the

services sector, and the hit to services consumption has been

particularly large for the elderly households due to health

concerns. Their low e-commerce usage also suggests limited

offset of weaker in-person consumption from online shopping.

The combination of a larger decline in spending with higher

savings and a higher propensity to consume means elderly

households also have higher potential as pent-up spenders.

Solid external demand further supports our bullish outlook for

Japan. The country’s exports are highly leveraged to the global

manufacturing cycle and should continue to benefit from the

strong recovery in global capex currently underway. The

sustained strength in external demand also points to tailwinds for

industrial production. Supply-side bottlenecks, especially in

semiconductor chips, pose downside risks to manufacturing

activities. However, recent data suggest that the negative impact

of the chip shortage is mostly limited to the automobile sector.

The effects are likely to be short-lived, as auto production is

expected to rebound from Q3.

China, the first major economy to emerge out of the COVID-19

crisis, has moved beyond the initial snapback phase; its

sequential growth momentum is moderating. While peak growth

in China is probably behind us, we expect a moderate growth

slowdown in the second half of this year with a shift in growth

drivers to private consumption and manufacturing investment.

A slower than expected consumption recovery likely reflects still-

cautious consumer sentiment, weighed down by recent local

outbreaks across several different provinces. However, China,

which has seen a sharp pickup in the pace of vaccinations, is on

track to fully vaccinate 40% of its population by the end of June.

Significant progress toward herd immunity later this year should

support further normalization of household consumption,

especially services consumption. Recovery of China’s

manufacturing capex also seems to have further room to run.

Continued improvement in corporate profitability and robust

export growth bode well for the manufacturing investment

outlook. This should cushion the expected slowdown in

infrastructure and property investment growth amid fading

policy support. At the same time, we expect China’s export

performance to remain robust, despite near-term logistics and

supply-side constraints.

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21

*

1.2m/day

1m/day

0.8m/day

Total vaccination, % of population, 2 doses

GLOBAL ASSET ALLOCATION VIEWS

6 Multi-Asset Solutions

More broadly, we remain constructive on the outlook for overall

emerging market exports, which underpins our expectation of

further recovery in EM growth. As discussed, we have seen little

evidence of a sharp rotation away from goods spending that

might damage EM sales. Trade data from North Asia (including

China, Korea and Taiwan), which accounts for around half of

overall EM exports, suggest shipments to the U.S. and European

Union (EU) have held up relatively well in recent months (Exhibit

6).

EM export recovery is slowly broadening with volume moving

back above pre-virus levels

EXHIBIT 6: NORTH ASIA EXPORTS BY DESTINATION (2019 = 100, NSA)

Source: CEIC, J.P. Morgan Asset Management Multi-Asset Solutions; data as of May 2021.

While demand for consumer goods could moderate along with

reopening, especially in the U.S., we believe EM exports should

find support from the robust global capex cycle, as investment

demand tends to be more import intensive. In fact, we have

already seen a shift of North Asia’s export growth drivers from

pandemic-related goods such as medical supplies and electronics

to capital goods such as machinery. Robust exports should also

boost EM domestic demand, as they provide support to the labor

market and manufacturing investment.

Looking across both DM and EM economies, we project that

global real GDP growth reaccelerated to a 7.6% annualized pace

in the second quarter, after a dip to a below-trend rate in 1Q21.

That slowdown owed to renewed virus restrictions in the euro

area, the UK and Japan, along with a stumble in China, where the

recovery was already well advanced. With mobility on the rise

and lockdowns easing, activity has picked up strongly in the past

few months. With U.S. growth likely peaking in the second

quarter – the last period to be heavily influenced by direct fiscal

stimulus payments, and the one in which activity will have more

or less closed the gap created by last year’s downturn – the baton

will pass to other economies in the second half of the year. We

expect euro area growth to hit its high point in the third quarter

and global GDP growth to exceed its 2Q21 pace marginally. Japan

would then follow in 4Q21, albeit against the backdrop of

somewhat slower growth worldwide. Still, even that more

moderate pace, in our forecast, would exceed the rate recorded

in any quarter of the prior expansion. While any 2022 projections

are necessarily speculative at this point, we think the

fundamental drivers described earlier will keep global growth

running between 3% and 4% annualized next year. That would

be nearly a percentage point above our estimate of the long-

term trend.

As mentioned, this burst of growth differs from prior episodes in

that EM economies are benefiting less. Instead, we see non-U.S.

DM countries as the “high beta” economies of the moment, given

that levels of activity, relative to the pre-pandemic trend, are

more depressed and that as a group these economies should

benefit from strong global capex. We do, however, see the global

economy as a whole benefiting from strong nominal growth as an

upturn in prices occurs alongside the strength in real activity.

Nominal growth should exceed fairly easily its pace from the

“global reflation” era of 2017–18, creating a supportive

environment for corporate profit growth and debt servicing

capacity (Exhibit 7).

Nominal growth will boost corporate earnings

EXHIBIT 7: GLOBAL GDP GROWTH (% QUARTER-ON-QUARTER, SAAR)

Source: Haver Analytics, J.P. Morgan Asset Management Multi-Asset Solutions; data and forecasts as of June 2021.

60

80

100

120

140

160

Jan-19 May-19 Sep-19 Jan-20 May-20 Sep-20 Jan-21 May-21

North Asia total exports (CN+KR+TW) To US To EU

-10

-5

0

5

10

15

20

2010 2013 2016 2019 2022

Real Nominal

GLOBAL ASSET ALLOCATION VIEWS

7 Multi-Asset Solutions

INFLATION: HOT FOR NOW, MORE MODERATE LATER

With growth running hot as economies reopen, the possibility of

a rise in inflation has occupied considerable attention among

market participants in recent months. Although we had expected

a burst of inflation pressure in the U.S. during the first half of this

year, we have nonetheless been surprised at its intensity. We

have taken on board some of this increase in thinking about our

medium-term forecasts, but we also expect some low side

payback in coming quarters as prices currently being squeezed

sharply higher begin to normalize. On the whole, we continue to

think that inflation will likely run at a somewhat stronger pace in

this expansion than during the previous decade. But we do not

see a dramatic inflation overshoot as particularly likely.

To be sure, U.S. numbers have shown more near-term inflation

than has been observed for decades. In year-on-year terms,

some of the increase reflects simple base effects, given

comparisons with the depths of the pandemic shock in 2020. But

the sequential trend has turned sharply upward as well, for three

reasons. First, a set of prices that collapsed amid plunging

demand during the pandemic have begun to correct. Examples

include airfares and hotels. Second, manufacturing bottlenecks

have led to shortages in some goods, most notably new and (by

extension) used cars but also some types of furniture and home

goods. Third, inflation in other areas has thus far slowed by less

than during the early part of the prior expansion, presumably

reflecting lesser, and less persistent, labor market slack.

Measures of underlying inflation, using trimmed-mean and

similar methods, illustrate these points. They have not moved

significantly higher in recent months, reflecting the importance

of outliers, but neither have they dropped noticeably.

Outside of the U.S., we hear faint echoes of these trends. Relative

to the U.S., greater prevalence of policy interventions, including

tax changes in the euro area and travel-and-leisure subsidies in

the UK and Japan, have affected price levels and made it more

difficult to parse the data. However, reopening effects have

proven smaller thus far, in part because of more drawn-out

processes elsewhere. Moreover, base effects also trail the U.S., as

prices in other economies fell less in 2020. Canada represents

the main exception among DM economies. With its economy

having followed a similar path to that of the U.S., core inflation in

year-on-year terms has moved above 2%. At the other end of the

spectrum, the shock appears to have entrenched further Japan’s

near-zero inflation environment, while inflation in the euro area

and the UK has moved up in the past quarter but remains firmly

below central bank targets.

Our top-down approach to inflation forecasting rests on three

main factors: inertia (as inflation tends to continue doing what it

has recently done), expectations (which we believe act as a

gravitational pull on inflation over time) and slack (which puts a

thumb on the scale in either direction if economies are operating

significantly below or above their potential output levels).

Inflation’s recent jump can thus pass through into the medium-

term outlook through the first two of these. Inertial effects mean

today’s high readings are likely to reverberate for some time.

Private sector inflation expectations appear to have moved

upward, a recent correction notwithstanding. Survey- and

market-based measures of expectations generally stand well

below levels observed during the higher inflation era of the

1970s and 1980s but above the extremely low readings of the

past decade.

With our near-term growth forecasts broadly unchanged, our

estimates of the output gap in coming quarters have not moved

significantly. We continue to believe that the U.S. economy will be

operating with a positive, and increasing, output gap from the

second half of 2021 onward. By our reckoning, this state of affairs

will produce gradual upward pressure on inflation next year, but

not a sharp acceleration.

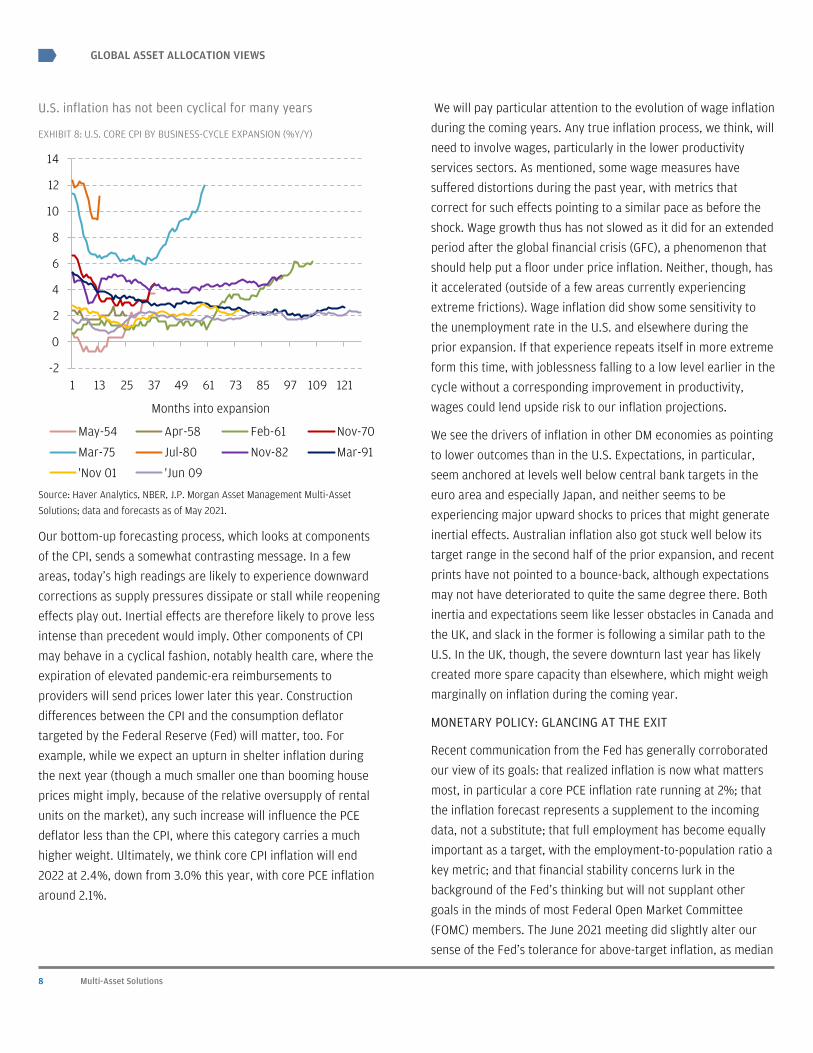

Why do we not expect a surge? For a few decades now, inflation

has showed almost no cyclicality, and therefore the estimated

sensitivity of inflation to the output gap is fairly small (Exhibit 8).

We regard comparisons to the 1960s and 1970s with skepticism.

What was then a largely closed, goods-oriented economy with

strong worker bargaining power and pervasive indexation

mechanisms is now an open, services-oriented economy with

limited unionization or indexation, and indeed with much higher

levels of consumer information. These changes likely make it

more difficult today to “overheat” the economy into truly high

inflation. All told, our top-down model points to the underlying

trend in core CPI inflation moving into the 2 1/2% range by the

end of next year.

GLOBAL ASSET ALLOCATION VIEWS

8 Multi-Asset Solutions

U.S. inflation has not been cyclical for many years

EXHIBIT 8: U.S. CORE CPI BY BUSINESS-CYCLE EXPANSION (%Y/Y)

Source: Haver Analytics, NBER, J.P. Morgan Asset Management Multi-Asset Solutions; data and forecasts as of May 2021.

Our bottom-up forecasting process, which looks at components

of the CPI, sends a somewhat contrasting message. In a few

areas, today’s high readings are likely to experience downward

corrections as supply pressures dissipate or stall while reopening

effects play out. Inertial effects are therefore likely to prove less

intense than precedent would imply. Other components of CPI

may behave in a cyclical fashion, notably health care, where the

expiration of elevated pandemic-era reimbursements to

providers will send prices lower later this year. Construction

differences between the CPI and the consumption deflator

targeted by the Federal Reserve (Fed) will matter, too. For

example, while we expect an upturn in shelter inflation during

the next year (though a much smaller one than booming house

prices might imply, because of the relative oversupply of rental

units on the market), any such increase will influence the PCE

deflator less than the CPI, where this category carries a much

higher weight. Ultimately, we think core CPI inflation will end

2022 at 2.4%, down from 3.0% this year, with core PCE inflation

around 2.1%.

We will pay particular attention to the evolution of wage inflation

during the coming years. Any true inflation process, we think, will

need to involve wages, particularly in the lower productivity

services sectors. As mentioned, some wage measures have

suffered distortions during the past year, with metrics that

correct for such effects pointing to a similar pace as before the

shock. Wage growth thus has not slowed as it did for an extended

period after the global financial crisis (GFC), a phenomenon that

should help put a floor under price inflation. Neither, though, has

it accelerated (outside of a few areas currently experiencing

extreme frictions). Wage inflation did show some sensitivity to

the unemployment rate in the U.S. and elsewhere during the

prior expansion. If that experience repeats itself in more extreme

form this time, with joblessness falling to a low level earlier in the

cycle without a corresponding improvement in productivity,

wages could lend upside risk to our inflation projections.

We see the drivers of inflation in other DM economies as pointing

to lower outcomes than in the U.S. Expectations, in particular,

seem anchored at levels well below central bank targets in the

euro area and especially Japan, and neither seems to be

experiencing major upward shocks to prices that might generate

inertial effects. Australian inflation also got stuck well below its

target range in the second half of the prior expansion, and recent

prints have not pointed to a bounce-back, although expectations

may not have deteriorated to quite the same degree there. Both

inertia and expectations seem like lesser obstacles in Canada and

the UK, and slack in the former is following a similar path to the

U.S. In the UK, though, the severe downturn last year has likely

created more spare capacity than elsewhere, which might weigh

marginally on inflation during the coming year.

MONETARY POLICY: GLANCING AT THE EXIT

Recent communication from the Fed has generally corroborated

our view of its goals: that realized inflation is now what matters

most, in particular a core PCE inflation rate running at 2%; that

the inflation forecast represents a supplement to the incoming

data, not a substitute; that full employment has become equally

important as a target, with the employment-to-population ratio a

key metric; and that financial stability concerns lurk in the

background of the Fed’s thinking but will not supplant other

goals in the minds of most Federal Open Market Committee

(FOMC) members. The June 2021 meeting did slightly alter our

sense of the Fed’s tolerance for above-target inflation, as median

-2

0

2

4

6

8

10

12

14

1 13 25 37 49 61 73 85 97 109 121

May-54 Apr-58 Feb-61 Nov-70

Mar-75 Jul-80 Nov-82 Mar-91

'Nov 01 'Jun 09

Months into expansion

GLOBAL ASSET ALLOCATION VIEWS

9 Multi-Asset Solutions

projections of 2.1% in 2022 and 2023 now, in many FOMC

participants’ minds, imply rate hikes in the second half of the

latter year. We previously thought the Fed might aim for a

slightly larger overshoot.

With that June meeting also bringing the start of a discussion

about “tapering,” or a gradual reduction in the Fed’s asset

purchases, we continue to expect that process to get underway

around the turn of the year, and expect it to run for about 12

months. We believe the FOMC will want to complete its exit from

bond-buying before raising short-term interest rates. A rate hike

would thus become possible in 2023, and we think the first one

will occur in the second half of that year, in line with the FOMC’s

June suggestion. We see little room for tapering to be brought

forward, as the Fed has consistently said it will provide ample

advance warning before it begins. The calendar also implies only

limited space for an earlier rate hike, and the slightly more

hawkish than expected reaction function now on display also

reduces the probability of a significant delay, unless inflation fails

to hold at the 2% mark. Were inflation to behave similarly in this

expansion as in the prior one, running persistently below the

target, we think the FOMC would hold off on raising rates

indefinitely.

Relative to the Fed, the Bank of Canada (BoC) has staked out the

most hawkish territory among DM central banks. With a relatively

comfortable inflation track record, slightly above-target inflation

currently, no framework change in favor of average inflation

targeting and a cyclical, commodity-sensitive economy, the BoC

has already begun reducing asset purchases. It will likely raise its

policy interest rate ahead of the Fed, too. By contrast, the

Reserve Bank of Australia (RBA) – previously a highly cyclical

central bank – has moved toward dovishness in the face of recent

inflation disappointments. Like Canada, Australia features a

mature housing cycle with growing hints of speculative activity,

but the Australian authorities have in the past successfully

addressed such issues with regulatory policy rather than higher

rates. The Bank of Japan will likely stay on hold indefinitely, and

we think the European Central Bank (ECB) may struggle to move

away from maximum accommodation for some time to come.

While the Bank of England is feeling its way in a post-Brexit

environment, its inflation history and outlook both seem

comfortable. We think it will behave more like the Fed than the

ECB.

During the last cycle, many central banks justified extreme

dovishness in part by referring to the likelihood that r*, the

equilibrium real short-term interest rate, had fallen to very low

levels. Estimates of r* produced by various central bank models

remain quite low and appear still to be serving as an anchor for

views about policy over the medium term. These calculations,

though, display high sensitivity to econometric specifications, and

various factors – such as demographics, saving behavior or

technological progress – might conspire to boost equilibrium real

rates as this expansion unfolds. A different view about “natural”

rates could alter the policy landscape, and we will be watching

for evidence that any such shift is taking hold. For now, we

believe that central banks worry more about getting stuck in a

permanently low inflation environment than about overshoots,

and we think monetary policy will retain a dovish tone even after

central banks begin moving to the exit.

Turning to the EM landscape, although China’s overall policy

stance has turned less accommodative since mid-2020, its policy

tightening so far has proceeded more gradually than in previous

cycles. From a financial conditions perspective, the magnitude of

tightening this cycle is only around 25% of what we witnessed

during 2016–18. Weaker growth data in April and May have likely

further reduced the risk of more aggressive tightening later this

year.

We expect monetary policy tightening to remain gradual, mainly

in the form of slower credit growth amid tighter control of

implicit local government debt and shadow banking credit. The

pace of credit slowdown will likely moderate in the coming

months and bottom out in the fourth quarter. Meanwhile, we

believe the People’s Bank of China will keep interbank liquidity

relatively ample to avoid adding further pressure on small and

medium-sized enterprises (SMEs), which were hit hard by the

pandemic. Despite rising producer price index inflation, we do

not expect any policy rate hikes as the government focuses more

on administrative measures to curb commodity price inflation.

Following a large easing cycle during 2019–20, rate cuts in other

EM economies have come to a stop. We expect to see tightening

by several EM central banks in 2H21, mainly in Latin America and

EMEA, but we do not think the tightening will be as prevalent

across emerging markets as it was during 2010 and 2018. We

continue to see limited risks of broad-based EM inflationary

pressure. While EM headline and core CPI inflation rates have

GLOBAL ASSET ALLOCATION VIEWS

10 Multi-Asset Solutions

moved up since the start of the year, driven by base effects and

higher commodity prices, they remain in the lower end of the

post-GFC range. Surveyed inflation expectations have also been

relatively stable in most EM economies despite rising commodity

prices. That said, inflation is more of a concern for some high

yielders, such as Brazil and Russia. Current inflation as well as

surveyed inflation expectations are above both of these central

banks’ inflation targets. As a result, we have already seen three

rate hikes each from Brazil and Russia, and expect further

tightening later this year.

EXHIBIT 3: THE BUSINESS-CYCLE SCORECARD FOR THE U.S.

Overall, we do not expect the rate hiking cycle to pose significant

challenges to the overall EM economic recovery. The EM rates

market has already priced in hikes for the coming quarters.

Moreover, the expected policy normalization in Central Europe

primarily reflects strong growth because of fast vaccine rollouts

and high leverage to the euro area recovery, and therefore

should prove less disruptive.

Early cycle Mid cycle Late cycle Recession

Econ

omic

met

rics

Overall economic output Below potential, rising Near potential, rising Above potential, rising Contracting

Consumption Low, lagging income Recovering High, ahead of income Falling

Capital investment Low as % of GDP Rising, moderate as % of GDP High as % of GDP Falling

Residential investment Low as % of GDP Rising, moderate as % of GDP High as % of GDP Contracting

Price inflation Below central bank target, stable Below CB target, rising Above CB target Falling

Wage inflation Low, stable Moderate, rising High Falling

Private credit formation Low, starting to rise Rising in line with output Rising faster than output Falling

Personal savings rate High relative to income Starting to decline Low relative to income Rising vs. income

Unemployment Well above NAIRU Above NAIRU Around or below NAIRU Rising sharply

Consumer confidence Low Moderate Exuberant Falling

Asse

t mar

ket m

etri

cs

EPS revision ratios Downgrade cycle, improving trend Upgrade cycle, improving trend Upgrade cycle, falling trend Downgrade cycle, falling trend

Corporate margins Rising Peaking Declining Low

Credit spreads Wide, contracting Tight, stable Past cyclical trough Wide, unstable

Aggressive issuance Low as share of total Moderate as share of total High as share of total Nonexistent

M&A activity Low Moderate High Nonexistent

Yield curve Rates low, curve steep Rates rising, curve flattening Rates high, curve flat Rates falling, curve steepening

Volatility Vol high, skew falling Vol low, skew low Vol starting to rise, skew rising Vol high, skew high

Most economic indicators are now in mid-cycle territory

Source: J.P. Morgan Asset Management Multi-Asset Solutions; assessments as of June 2021.

GLOBAL ASSET ALLOCATION VIEWS

11 Multi-Asset Solutions

LEVEL ONE ASSET ALLOCATION

At our June Strategy Summit, two conflicting themes emerged:

robust expectations for economic growth, and concern that

markets have already overshot. In the microcosm of the past

year, projecting some divergence of the economy and markets

over the next couple of quarters might seem reasonable. Not

only have equity valuations surged upward as central bank

liquidity fueled a buying frenzy in the stock market, but in the last

few days the Fed has indicated that time will eventually be called

on the monetary bonanza. However, if we take a sober, longer-

term perspective, we would note that it is unusual for economies

and markets to diverge for very long. Moreover, while economies

transitioning from early to mid cycle – as the U.S. is doing today

– can see shifts in momentum in their stock markets, they seldom

see changes in direction, especially when earnings growth is both

robust and underpriced.

We believe that the U.S. economy has shifted from the initial

early cycle to mid cycle with unprecedented speed, helped along

by massive fiscal stimulus and policy that – in contrast to some

prior cycles – was both proactive and suitably scaled. The result is

aggregate household balance sheets that are unusually healthy

for this point in the cycle, leading to the potential for a sustained

unleashing of pent-up demand as the economy reopens. At the

same time, favorable financing costs have driven a surge of

corporate capex, and banks – the epicenter of the last crisis – are

in very good shape despite the whipsaw of the last 18 months

(Exhibit 9). Concerns rightly linger on the large bloc of

unemployed and furloughed workers, and the slack in labor

markets. But even as the Fed has indicated a marginally more

hawkish turn, getting people back to work remains its primary

policy goal.

Global PMIs remain strong; Capex growth surged following

lockdowns and levels of investment are robust

EXHIBIT 9: GLOBAL CAPEX PMI AND CAPEX (% Q/Q, SAAR)

Source: Haver Analytics, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

The fiscal and monetary bonanza of the last year and a half has

left many fearing a surge in inflation, and base effects have

further conspired to drive a leap in inflation measures in the U.S.

and countries such as the UK. While we acknowledge that the

output gap is closing rapidly, we believe that labor market slack

together with persistent secular disinflation trends such as

automation will serve to prevent higher inflation from becoming

persistent. Indeed, the base effects from 2Q20, the recent jump

in commodity prices and the disruptions in the supply chain that

have caused an outsize price effect in specific areas all appear to

be on the wane. While it is true that upside inflation risks remain

and we expect the volatility of inflation to be rather higher, we

expect the inflation scare to subside in 2H21.

The same might also be said of the Fed, based on its projections:

inflation hitting 3% this year before subsiding to 2.1% in the

subsequent two years. This acknowledgment, together with the

upward shift to forward policy guidance through the Fed’s

Summary of Economic Projections (SEP) “dot plot,” takes some of

the steam out of the upward inflation trend, in our view. To be

sure, Fed policy remains remarkably easy, and based on the

“dots,” fed funds rates would rise only to 50–75bps by the end of

2023. That is hardly tight monetary policy by any reasonable

standard. And yet the FOMC meeting was for investors a hawkish

surprise, consistent with an economy moving rapidly from policy-

reliant early cycle to a self-sustaining mid cycle.

-36

-24

-12

0

12

24

42

44

46

48

50

52

54

56

58

2010 2013 2016 2019

PMI Capex

GLOBAL ASSET ALLOCATION VIEWS

12 Multi-Asset Solutions

The U.S. economy, along with Fed policy, remains clearly ahead

of other developed nations. As we suggested at the start of 2021,

the U.S. would lead in the first half of the year – given a rapid

vaccine rollout and uncompromising policy support – with Europe

and Japan accelerating in the second half. In our view, this

playbook remains broadly intact. With other developed regions

earlier in the cycle, their respective central banks remain some

way from the policy pivot recently taken by the Fed. This has

implications for both the currency and rates outlooks, as we will

explore. But it also implies that the reopening trade has further

to run within equity markets. This should lend support to cyclical

regions outside the U.S., even as market participants begin, once

again, to warm up to some of the secular growth themes deeply

embedded in U.S. equities. Emerging markets are rather more

nuanced. China and the North Asian economies are further ahead

in this cycle than the U.S., buoyed in part by the surge in goods

demand as locked-down householders quickly diverted dollars

destined for services and leisure to consumer goods and home

makeovers. By contrast, countries such as India and Brazil,

recently ravaged by second waves of COVID-19, are only now

beginning to see activity pick up (Exhibit 10).

PMIs show that the U.S. continues to lead the recovery

EXHIBIT 10: MARKIT FINAL COMPOSITE PURCHASING MANAGERS INDEX, SA

Source: Bloomberg, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

Turning to asset markets, we take a reasonably constructive view

on the outlook. At our Strategy Summit, some commentators

argued that the kind of positive economic outlook described in

the preceding paragraphs is already fully – or even excessively –

reflected in prices. We disagree. In our view, bond yields reflect

global policy frameworks at least as much as fundamentals,

suggesting that while there might be information in the direction

or trend in rates, there might be little in the level of yields. In

equity markets, we acknowledge the high optical level of P/E

valuations – especially in the U.S. – but equally note that over a

short time horizon valuation is a poor predictor of returns. Our

expectation that earnings growth will ease the extremes of

valuation is hardly unique. But we do believe that the likely

upside to earnings, both this year and next, is widely

understated. On balance, this leaves us with a high conviction

overweight to equity, a low conviction overweight to credit, a low

conviction underweight to duration and a moderate conviction

underweight to cash – in short, a portfolio tilted for a

continuation of the trends in both economic growth and asset

market returns.

Our equity overweight continues to display a cyclical and value-

style tone, although we note that, at the margin, some of the

impetus for the value tilt coming from steeper curves and higher

rates has diminished. As we see the U.S. economy move to mid

cycle, we anticipate a renewed focus on quality of earnings. In

our view, the early surge of buying and confidence will likely give

way to a sharper focus on sectors, regions and stocks with

reliable earnings. Indeed, we have already seen evidence of this

pattern within small caps, where the distinction between

profitable and nonprofitable stocks in 2Q21 became quite

palpable. Our quant team finds both the value and the quality

factors to be attractive, so building in something of a quality tilt

is further supported. Our cyclical bias continues to lead us to

favor Europe and Japan on a regional basis. In the U.S., we

believe that some of the secular growth themes expressed across

the wider U.S. equity market will receive renewed attention as

the topside risks to inflation and rates subside. By contrast, the

outlook for EM equities remains mixed, especially with further

weakening of the dollar now possibly on hold in 2H21 after the

Fed’s recent shift in stance.

A hiatus in the dollar’s downtrend was not the only outcome of

the Fed’s policy adjustment. The steepening of the U.S. yield

curve also came to an abrupt halt. To be clear, the maximum

steepness of the U.S. 2s10s and 5s30s curves had already been

reached in the first quarter – at around 160bps in both cases –

and the sharp flattening that followed the Fed’s June meeting

was likely exacerbated by positioning (Exhibit 11). Nevertheless,

20

30

40

50

60

70

Jun-18 Dec-18 Jun-19 Dec-19 Jun-20 Dec-20

U.S. Eurozone JapanU.K. Emerging Market

GLOBAL ASSET ALLOCATION VIEWS

13 Multi-Asset Solutions

we are probably now past the point of maximum steepness for

this cycle, in the U.S. Treasury market at least. The short end of

the curve is no longer as anchored as it was, and some of the

inflation fears affecting the back end have lessened. Equally, it is

probably too soon to argue for a flattening trend to take hold.

While short-end rates can move up over time, the Fed has

signaled that tapering will come first, potentially allowing the

longer end of the curve to drift higher. Thus, we expect that rates

do rise gradually – their momentum somewhat governed by the

ongoing duration demand from international central banks and

portfolio de-risking flows – but that it will probably be felt along

the curve rather than in one specific segment.

Yield curves steepened earlier this year; in real terms we

remain close to historically steep levels

EXHIBIT 11: U.S. REAL YIELD 5S30S CURVE SLOPE, BASIS POINTS

Source: Bloomberg, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

Elsewhere in fixed income, we have pared back our enthusiasm

for credit across many portfolios. True, the economic

environment and ample liquidity are supportive for the credit

complex, but at current levels of spread we view credit principally

as a carry asset. To see spreads tighter from here, we would need

to make some fairly heroic calls on a surge in demand for credit

hybrid structures. While low yields elsewhere could spark some

renewed interest, we think the lessons from the global financial

crisis are still quite fresh in investors’ minds. Overall, we see

credit as solid but unexciting and have reduced conviction in our

mild overweight in high yield. Given our expectation that the

downtrend in the U.S. dollar could also be on hold, we also move

EM debt – both hard and local currency – to a neutral stance.

Above all, we prefer to keep a risk-on tone in our portfolios but

believe that returns in 2H21 will be driven by upside surprise to

earnings. We acknowledge lofty P/E valuations in some indices

but equally note that some other metrics of valuation – including

cash flow yields – are far less stretched. Ultimately, we think this

is a time for spreading risk across equity markets but maintaining

something of a cyclical and value/quality tone. At a portfolio

level, the Fed’s action has perhaps reduced the extreme right tail

risk of inflation and, by extension, of rates. As a result, those

seeking to lock in gains from this year’s already strong equity

market performance may feel more compelled to own duration,

even as rates are likely to grind higher. Taking a step back and

for a moment looking through the levels of asset markets and

yields, we would acknowledge that their likely direction does

indeed map quite well to the economic backdrop.

-50

0

50

100

150

200

250

2002 2005 2008 2011 2014 2017 2020

GLOBAL ASSET ALLOCATION VIEWS

14 Multi-Asset Solutions

Our Level One scorecard favors equities and credit

EXHIBIT 12: LEVEL ONE SCORECARD

Considerations Comment Stock Bond Credit Cash

Mac

ro fa

ctor

s

Economic growth A period of above-trend growth lies ahead in 2021, with leadership broadnening out beyond the U.S. + - + 0

Financial conditions Financial conditions should remain easy, with spreads contained + 0 + 0 Monetary policy DM CBs are past the point of maximum accommodation, but will rolling back stimulus only gradually + + + -

Tail risks Quicker withdrawal of policy stimulus; delta variant; inflation upside; China over-tightening - 0 - 0

Mar

ket f

acto

rs

Valuation – absolute Global equities expensive; bond yields look somewhat rich; little scope for spreads to tighten further - 0 0 0 Valuation – relative Equity risk premium, though lower, remains elevated; duration cheaper but not cheap; credit looks rich + 0 - - Fundamentals EPS upside to come; policy turning less positive for bonds; leverage still extended in credit + 0 0 0 Positioning Equity positioning elevated, but not extreme; bonds and credit more evenly balanced 0 0 0 - Flows/sentiment Equity flows still positive; moderate flows in bonds; credit flows turned negative + 0 - -

Overall Score + - + - Source: J.P. Morgan Asset Management Multi-Asset Solutions; assessments as of June 2021.

GLOBAL ASSET ALLOCATION VIEWS

15 Multi-Asset Solutions

LEVEL TWO ASSET ALLOCATION

At this juncture, we shift our perspective. In the preceding pages,

we examined our Level One asset choices, the basic portfolio

decisions involving broad asset classes (for example, stocks vs.

bonds). We now present our Level Two asset decisions. Here we

look within asset classes and determine, for example, what type

of credit (investment grade [IG], high yield or emerging market

debt) appears most attractive.

RATES

We maintain an underweight stance on duration, but with low

conviction. Yields over the last quarter have largely tracked

sideways, with the JP Morgan GBI bond yield unchanged and U.S.

10-year yields 20bps lower. Beneath the surface, however,

markets have been volatile. Positioning-driven moves and a pivot

from the Fed led to sharper moves in the yield curve, with 5s30s

flattening by over 30bps in the quarter. Despite the decline in

U.S. yields, we maintain our short-duration bias. This reflects our

positive macroeconomic outlook along with our sense that the

global economy is likely in a reflationary regime and that easy

monetary policy has passed its peak. While central banks are still

accommodative in an absolute sense, in a relative sense the

direction of travel is toward less emergency accommodation as

economies heal.

We expect the Fed to start tapering asset purchases early next

year. At its latest meeting, the FOMC talked about when tapering

might start and how rate hikes might proceed – a hawkish

surprise for markets. In coming months, we expect further

discussion of both tapering and rate hikes as the central bank

calibrates policy to the post-COVID-19 environment. That

environment will still see significant fiscal stimulus and,

potentially, the unleashing of trillions in “excess” savings

accumulated by households during the pandemic lockdowns.

Going forward, we expect more volatility in shorter-maturity

bonds (the two- to five-year sector) as the market reassesses the

Fed’s reaction function in the average-inflation targeting regime.

The Fed’s marginally hawkish tone complicates an investor’s view

of the yield curve, as the front end is no longer firmly pinned. We

had previously seen the global yield curve steepening, but now

we question this view, especially in the U.S. market (Exhibit 12).

Yield curve steepening view called into question

EXHIBIT 12: U.S. YIELD CURVE SLOPE, BASIS POINTS

Source: Bloomberg, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

High inflation outcomes are likely to persist for the next few

quarters due to economic reopening, supply-chain disruptions

and labor shortage issues. But we expect this to be a temporary

phenomenon, with inflation returning closer to central bank

targets later in 2022. On the policy front, we also learned a little

more about the Fed’s willingness to look through inflation rates

above its target. Effectively, the FOMC is signaling that it is likely

to raise policy rates as inflation rises above 2.1% in core PCE

terms (as inferred from the Fed’s latest Summary of Economic

Projections). This is a lower inflation threshold than we had

previously considered, and it signals a Fed eager to reduce the

right tail of inflation distribution. Given this backdrop, we are

cooling our optimism about inflation breakeven markets and

reduce our positive view on U.S. TIPS (Exhibit 13A and 13B).

Inflation breakeven markets have priced in a lot already

EXHIBIT 13A: 5Y5Y INFLATION SWAP, %

Source: Bloomberg, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 20212s10s 5s30s

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2018 2019 2020 2021

U.S. Euro Area

GLOBAL ASSET ALLOCATION VIEWS

16 Multi-Asset Solutions

EXHIBIT 13B: ESTIMATED COMPOSITION OF CHANGES IN 10-YEAR U.S INFLATION PRICING SINCE JANUARY 2020, %

Source: D’Amico, Kim and Wei (2018) updated by Kim, Walsh and Wei (2019), J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

Market positioning remains short duration in the U.S., a modest

headwind to our stance on duration. But in the wake of the June

FOMC meeting, we have seen a sharp unwind of consensus

positions, pointing to a cleaner investor positioning base.

Moreover, since the meeting our underweight stance on duration

has shifted to intermediate maturities on the yield curve. In the

two- to 10-year part of the yield curve, positioning is less

concentrated (Exhibit 14).

Bond investors were short duration but started to cover this

recently

EXHIBIT 14: NET LONG SHARE OF NONCOMMERCIAL CONTRACTS, %

Source: Bloomberg, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

Our relative preferences across government bond markets

remain relatively unchanged with the U.S., the UK and Canada

our least preferred markets. By contrast, we prefer lower yielding

markets in Europe and Japan on a relative basis. This ranking is

largely a function of our views on relative inflation and central

bank policy as well as these markets’ exhibited cyclical beta.

In the U.S., we expect 10-year bond yields to reach 2% by the end

of the year, driven mainly by a rise in real rates. Historically, real

rates have risen as growth improved and policymakers adjusted

to that growth environment. We expect a similar reaction

function in this cycle – but we think it will be more muted, given

the extraordinary scale of policy stimulus still coursing through

the global monetary system. Crucially, though, this expected rise

in bond yields should coincide with very strong growth outcomes.

Thus, we do not believe that a move higher in yields will

necessarily translate into tighter financial conditions.

We also underweight the UK Gilt and Canadian government bond

markets. In both countries, we already see central banks moving

away from extreme policy accommodation by tapering asset

purchases and even discussing the pathway to lifting policy rates

of the zero bound. In the UK, we see strong growth and rising

inflation against a backdrop of fairly well-anchored inflation

expectations (both survey- and market-based measures). As a

result, we expect the Bank of England will signal the end of QE in

coming months, with rate hikes penciled in for 2022 and beyond.

Markets have adjusted to this thesis, with Gilt yields up over

50bps year-to-date. We expect a continuation of UK market

underperformance in the coming quarters.

In the context of our overall underweight to duration, we

maintain a relative preference for markets in Japan and the euro

area. That view reflects the lack of persistent inflation pressure in

the regions and central banks that are signaling a continued

accommodation. In Europe, we remain positive on peripheral

bond markets, which are the clearest beneficiaries of the pro-

cyclical economic recovery as well as extreme monetary policy

accommodation.

In the last few months, we learned about the disbursement of

funds from the EU Next Generation Fund, and as expected, the

plan is for sizable funding for southern countries. Exhibit 15,

shows the size of grant and loan disbursements (as % of GDP) for

the major economies that have disclosed their plans for usage of

-1.0

-0.5

0.0

0.5

1.0

Jan-20 May-20 Sep-20 Jan-21 May-21

Expected inflation Inflation risk premium Liquidity premium

-60

-50

-40

-30

-20

-10

0

10

20

2019 2020 20212y 5y 10y 30y

GLOBAL ASSET ALLOCATION VIEWS

17 Multi-Asset Solutions

NextGen Funds. Italy is expected to receive over EUR 200 billion

in support. Over the next two years alone, Italy benefits from

loans and grants of over 3% of GDP. This fiscal support alongside

a central bank that remains accommodative provides strong

tailwinds to peripheral bond markets.

Peripheral states benefit disproportionately from NextGenEU

funds

EXHIBIT 15: EU NEXT GENERATION – GRANTS AND LOANS, % OF GDP

Source: EU Comission, Morgan Stanley, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021. EA = euro area, DE = Germany, FR = France, IT = Italy, ES = Spain, NL = Netherlands, BE = Belgium, AT = Austria, PT = Portugal, GR = Greece, IE = Ireland.

We remain neutral on Australia. Historically, Australian bonds

would sit in the higher beta, more cyclically geared bond bucket,

but over the last quarter we have been surprised by how stable

Australian government bonds (ACGBs) have been. We attribute

this lower beta dynamic largely to the Reserve Bank of Australia’s

QE program and anchoring of short rates as inflation remained

weak. We do see a high degree of uncertainty about how long the

RBA will remain this dovish and whether it will follow the Fed in

signaling rate hikes over the foreseeable horizon. This

uncertainty keeps us neutral as we await clearer guidance on the

policy outlook.

FX

Amid improved COVID-19 outcomes and substantial policy

support, we think above-trend global growth will likely persist

over the latter half of 2021. All else equal, this pro-cyclical

environment implies appreciation in high beta FX while

tempering enthusiasm for reserve currencies, particularly USD.

That said, the constructive global outlook is already well

appreciated by FX participants and thus, in isolation, less likely to

be the catalyst for further broad-based USD weakness (Exhibit

16). Instead, over the coming months, we expect compositional

changes in the ongoing global recovery to spark a more

differentiated phase of currency price action.

Year-to-date, the U.S.’s growth lead over RoW has stabilized,

however broad-based dollar depreciation has stalled

EXHIBIT 16: DXY PERFORMANCE AND U.S.-GLOBAL JFRI COMPARISON

Source: Bloomberg, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

Specifically, in aggregate, we anticipate an acceleration in ex-U.S.

rest-of-world (RoW) growth driven by economic reopening,

greater global services sector activity and increasing divergence

in DM monetary policy stances. How individual currencies

perform in this context depends significantly on their countries’

own course of the virus, which in turn dictates domestic

reopening and policy normalization. Generally, we continue to

favor currencies that were vaccine and growth laggards in the

first half of the year, but crucially, we acknowledge that near-

term scope for broader USD weakness is more limited.

USD

We remain circumspect on the U.S. dollar in the medium term,

given the macro backdrop and collapsed nominal yield

differentials. Historically, moderation of U.S. growth leadership

and a persistently dovish Fed have implied sustained dollar

weakness. And we did see spells of DXY depreciation through

April and May as vaccine laggards, particularly in Western

Europe, began to catch up.

0

0.5

1

1.5

2

EA DE FR IT ES NL BE AT PT GR IE

Grant 2021 Grant 2022 Loan 2021 Loan 2022 -3

-2

-1

0

1

2

88

91

94

96

99

102

Apr-20 Jul-20 Oct-20 Jan-21 Apr-21DXY U.S. - Global JFRI (Z-Score, RHS)

GLOBAL ASSET ALLOCATION VIEWS

18 Multi-Asset Solutions

But in June, the Fed’s communication took a hawkish turn,

lending some near-term support to the dollar. Specifically, the

Fed made an upward shift to forward policy guidance through its

“dot plot,” effectively signaling greater data dependency in the

context of mounting inflation and frictional job market weakness.

Further, talk of tapering has escalated broadly among G10

policymakers, with Canada already beginning to decelerate its QE

purchases.

As we have noted in the past, a repricing of UST yields does not

preclude medium-term dollar bearishness. Indeed, collapsed

yield differentials, particularly in real terms, have been one of

our core themes. Yet we find that rates repricing that reflects

improved domestic growth prospects rather than tightening

financial conditions can coexist with selective USD softness. That

said, recent Fed messaging has introduced greater scope for

front-end real rates to rise in a way that is dollar supportive.

Ultimately, we are confident that explicit Fed communication will

comfortably precede any material changes to monetary policy.

We emphasize the distinction between beginning “talks of

tapering” and actually beginning to taper. Currently, the Fed

remains committed to above-target inflation and “substantial

further progress … toward the Committee’s maximum

employment and price stability goals.” We see the Fed’s June

turn as hawkish at the margin while absolute levels of policy

remain highly accommodative, a distinction we believe justifies

maintaining our neutral stance on USD. However, the trajectory

of financial conditions is decidedly less dovish than it was at our

last Summit, skewing the balance of risks toward some near-term

support for USD.

JPY

In Japan, inflation expectations have structurally de-anchored

from the policy target, suggesting that the Bank of Japan will

persistently lag in reflation and monetary policy normalization.

This dynamic has played a key role in yen weakness over the first

half of 2021. Other, more transient headwinds, primarily a third

COVID-19-related “state of emergency,” have also generated

near-term growth underperformance. Still, there is reason to be

constructive on Japanese macro conditions going forward. The

vaccine rollout is clearly gathering speed, suggesting an

impending recovery in domestic services consumption. In

addition, Japan’s gearing to the booming global goods cycle

implies further support from the current account. In sum, we

continue to expect the ongoing global reflation trade to burden

yen performance, but anticipate the more transitory headwinds

to abate somewhat in the coming months.

One tail risk to our yen outlook is the potential for political

instability following a shift in leadership. Though our base case is

that Prime Minister Yoshihide Suga will enjoy greater support

with a successful vaccine rollout, should the Tokyo Olympic

Games be further disrupted prior to the upcoming general

election, the medium-term policy outlook and structural reforms

associated with former Prime Minister Abe and now Suga would

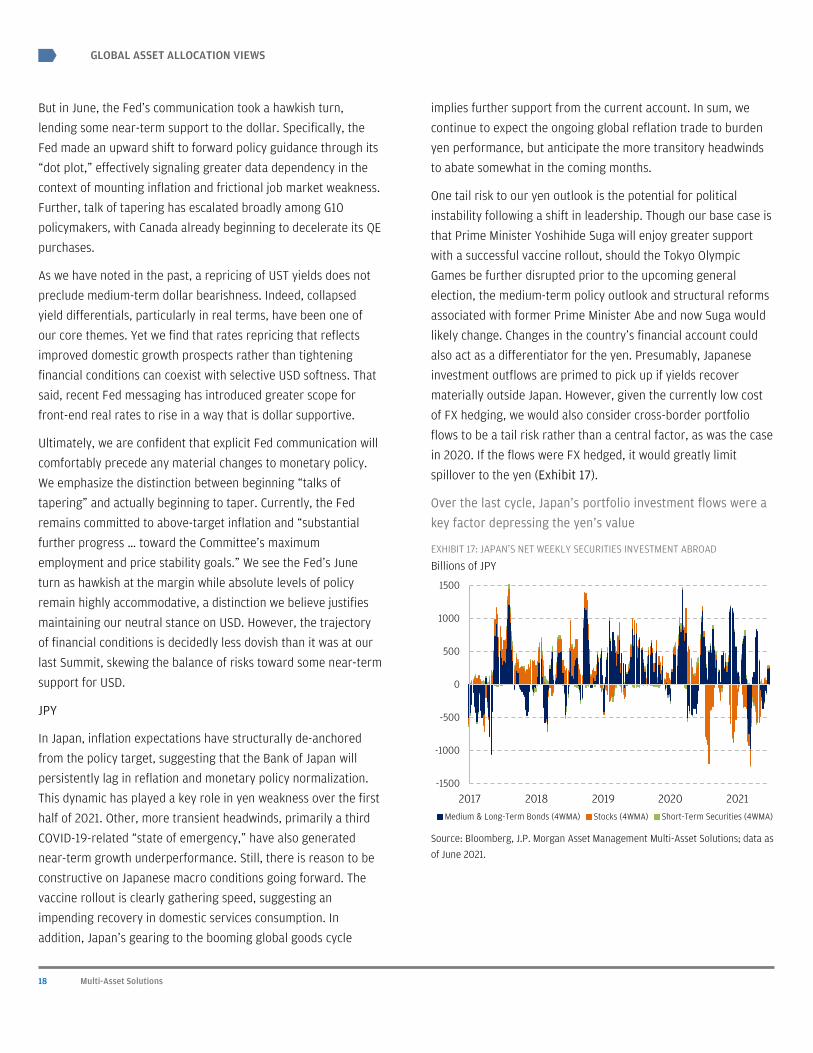

likely change. Changes in the country’s financial account could

also act as a differentiator for the yen. Presumably, Japanese

investment outflows are primed to pick up if yields recover

materially outside Japan. However, given the currently low cost

of FX hedging, we would also consider cross-border portfolio

flows to be a tail risk rather than a central factor, as was the case

in 2020. If the flows were FX hedged, it would greatly limit

spillover to the yen (Exhibit 17).

Over the last cycle, Japan’s portfolio investment flows were a

key factor depressing the yen’s value

EXHIBIT 17: JAPAN’S NET WEEKLY SECURITIES INVESTMENT ABROAD

Source: Bloomberg, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

-1500

-1000

-500

0

500

1000

1500

2017 2018 2019 2020 2021Medium & Long-Term Bonds (4WMA) Stocks (4WMA) Short-Term Securities (4WMA)

Billions of JPY

GLOBAL ASSET ALLOCATION VIEWS

19 Multi-Asset Solutions

EUR

Within G4 FX, the euro continues to be our most preferred

expression of a broadening global economic recovery. Domestic

growth momentum, globally easy financial conditions and, more

recently, equity investment inflows all support the currency.

Market participants largely anticipated strong Q2 growth fueled

by an accelerated vaccine rollout. But we have been further

encouraged by the participation of services activity in recent data

outperformance. A still-significant negative output gap in

services indicates further upside potential for the euro as the

services sector continues to rebound. In addition, net inflows to

European equity funds are tilted in favor of EUR amid the

ongoing equity style rotation (Exhibit 18).

Net equity inflows to European equities have picked-up

EXHIBIT 18: FLOWS INTO EUR-DENOMINATED ETF INSTRUMENTS

Source: Bloomberg, J.P. Morgan Asset Management Multi-Asset Solutions; data as of June 2021.

Opposite this, as talks of monetary policy normalization intensify,

tilting against EUR strength is a decade’s worth of inflation

undershoots. This precedent calls into question the ECB’s

capacity to “keep up” when the global rate hiking cycle

eventually gets underway, and by extension, the euro’s ability to

remain pro-cyclical. Not only are underlying price pressures

structurally weaker in the euro area compared with the U.S., but

in the immediate response to the pandemic, Europe’s fiscal policy

was much less forceful. Together, these factors cast doubt on the

euro area’s ability to meet inflation targets and thus keep pace in

the eventual normalization of monetary policy. For today’s

narrow, EUR-supportive real yield differential to be maintained,

markets likely require continued Fed easing. If the Fed is slow to

implement its recent shift in communication, it should allow EUR

to continue to appreciate as part of the ongoing reflationary

process. Taking all these factors into account, we reduce our EUR

overweight with low conviction.

GBP

As near-term tailwinds continue to largely determine sterling

price action, we’re increasingly less negative on GBP. In

developed markets, the Norges Bank, the Bank of Canada and the