key attributes of effective resolution regimes for...

TRANSCRIPT

Key Attributes of Effective Resolution Regimes for Financial Institutions

Overview

FinSAC Workshop: Resolution Regimes in Europe: implementation of effective resolution regimes in the region

19 April 2017Vienna Austria

Overview

• Reducing the probability of failure of systemic financial firms• Reducing the impact of failure by increasing the ability to put such firms

into resolution

Ending “Too Big to Fail” - a two-pronged strategy

• Publication of the “Key Attributes of Effective Resolution Regimes”• Development of single/multiple point of entry resolution strategies• Agreement on a common TLAC minimum requirement• Improvements of the cross-border recognition of resolution actions, in

particular temporary stays on early termination rights in financial contracts• Much progress on resolution planning: bail-in execution, funding of

resolution, operational continuity, continuity in resolution of access to FMIs.

Breakthroughs have been made in achieving the resolution of systemic financial institutions

…but work remains: progress on resolution is a journey

Ending TBTF - timeline2009 Pittsburgh Summit

G20 call for action to address TBTF 2010 Seoul Summit:

G20 endorse the FSB SIFI framework to reduce probability and and impact of SIFI failure

2011 Cannes Summit: G20 endorse the Key

Attributes as new international standard

2012 Los Cabos SummitG20 commit to implementation of the Key Attributes, resolution planning and cooperation agreements for all G-SIFIs

2013 St Petersburg Summit: G20 call for action to ensure loss-absorbing capacity of G-SIBs in

resolution and cross-border recognition

2014 Brisbane SummitG20 welcome proposals on TLAC and action on cross-

border resolution stays

2015 Antalya SummitFinal TLAC standard

2016 Hangzhou SummitShifting the focus on resolvability

of CCP – critical nodes of the financial system

2017 Hamburg Summit…finalising Guidance on CCP resolution

THE KEY ATTRIBUTES

Resolution – a new paradigmPr

e-cr

isis

ban

krup

tcy Legal-entity focused wind-

downs administered by judicial authoritiesApplied to multiple financially and operationally interconnected legal entities in many jurisdictionsDestructive of going-concern asset value Discontinuity of critical economic functionsNo advance planningEx post ring fencingReliance on public funds to maintain critical functions(“bail-out”)

Post

-cris

is re

solu

tion Process controlled by

administrative authoritiesApplied to one or only few resolution entities (SPE/MPE) identified through advance planningAimed at continuing vital economic functionsCoordinated cross-border solutions through ex ante planning and prepositioning TLACCreditor-financed recapitalization (“bail-in”) to avoid the need for public funds to maintain critical functions

The Key Attributes

Resolution regimes

Recovery and

Resolution Planning

Resolvable structures

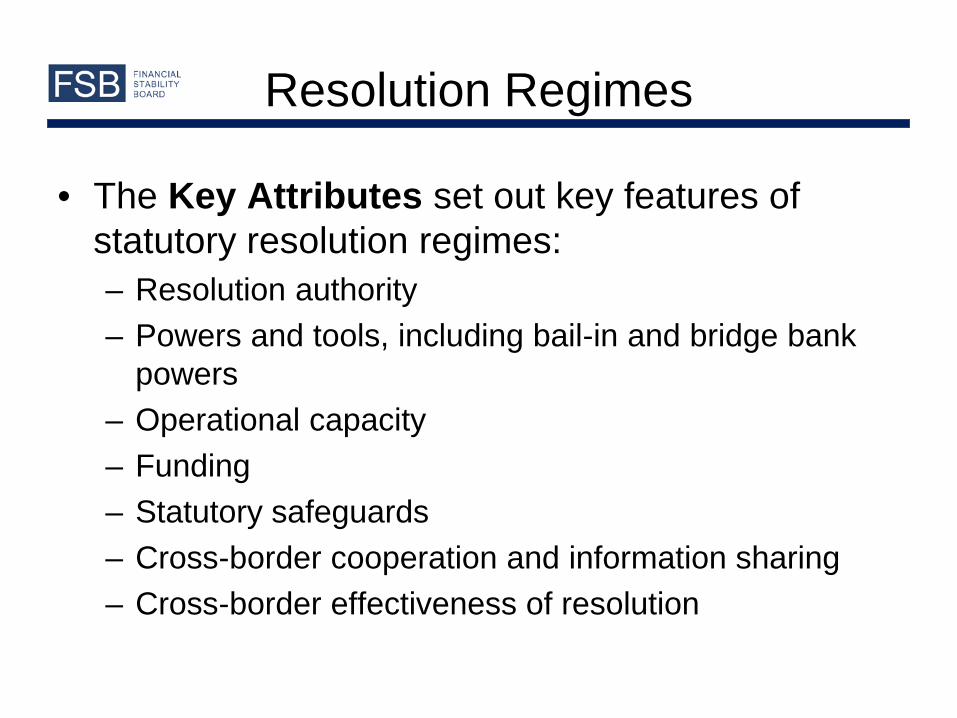

• The Key Attributes set out key features of statutory resolution regimes:– Resolution authority– Powers and tools, including bail-in and bridge bank

powers– Operational capacity– Funding– Statutory safeguards– Cross-border cooperation and information sharing– Cross-border effectiveness of resolution

Resolution Regimes

Key Attributes 1 - 3

1. Scope• Any financial institution that could be systemic if it fails

should be subject to a regime in line with the Key Attributes.

2. Resolution authority• Operationally independent, but accountable administrative

authority with a statutory mandate to pursue financial stability and support the continuity of critical economic functions.

3. Resolution powers• Broad range of powers to intervene and resolve a financial

institution that is no longer viable.8

9

RESOLUTION OPTIONS UNDER THE KEY ATTRIBUTES

Stabilisation options to achieve continuity

Transfer of some or all business to

a bridge institution

another financial institution

“Bail-in” creditor-financed

(re)capitalisation through

Write-down of shareholders’ & creditors’ claims

Debt-for-equity swap to

(re)capitalize

Liquidation options to achieve a value-preserving orderly wind-down

Liquidation with:- timely pay-out or transfer of insured

deposits-prompt access to

transaction accounts & to client funds.

Asset management

vehicle for NPL &difficult-to-value

assets

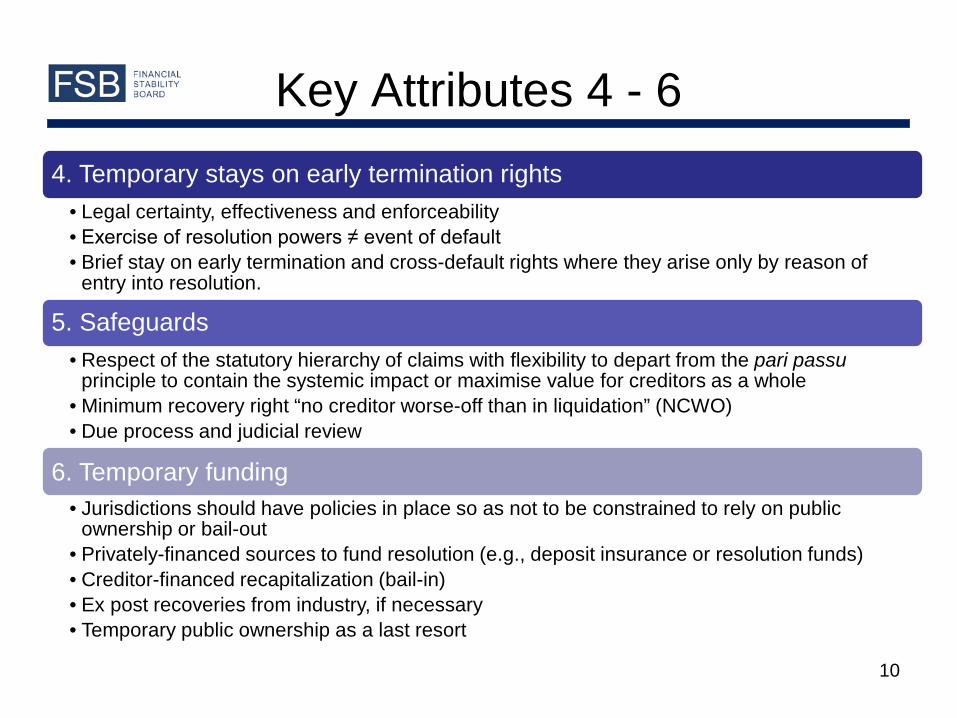

Key Attributes 4 - 64. Temporary stays on early termination rights

• Legal certainty, effectiveness and enforceability • Exercise of resolution powers ≠ event of default• Brief stay on early termination and cross-default rights where they arise only by reason of

entry into resolution.

5. Safeguards• Respect of the statutory hierarchy of claims with flexibility to depart from the pari passu

principle to contain the systemic impact or maximise value for creditors as a whole• Minimum recovery right “no creditor worse-off than in liquidation” (NCWO)• Due process and judicial review

6. Temporary funding• Jurisdictions should have policies in place so as not to be constrained to rely on public

ownership or bail-out• Privately-financed sources to fund resolution (e.g., deposit insurance or resolution funds)• Creditor-financed recapitalization (bail-in)• Ex post recoveries from industry, if necessary• Temporary public ownership as a last resort

10

Key Attributes 7 - 9

7. Cross-border Cooperation• Statutory mandate to cooperate and legal capacity to share information• Frameworks to give effect to foreign resolution measures• No discrimination against creditors on the basis of nationality, location

of the claim or jurisdiction where it is payable

8. Crisis Management Groups (CMGs)• Home and key host central banks, supervisors, resolution authorities of

G-SIFIs to maintain CMGs

9. Institution-specific cross-border cooperation agreements• To set out modalities for cooperation and information sharing among

home and key host authorities in the recovery and resolution planning phase as well as for crisis situations.

11

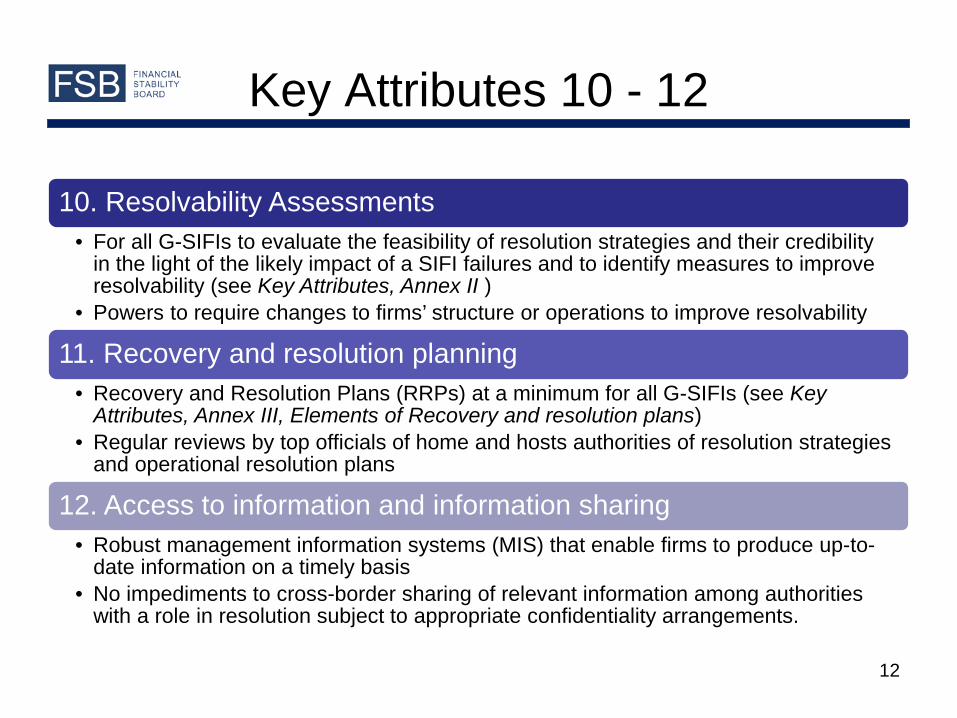

Key Attributes 10 - 12

10. Resolvability Assessments• For all G-SIFIs to evaluate the feasibility of resolution strategies and their credibility

in the light of the likely impact of a SIFI failures and to identify measures to improve resolvability (see Key Attributes, Annex II )

• Powers to require changes to firms’ structure or operations to improve resolvability

11. Recovery and resolution planning• Recovery and Resolution Plans (RRPs) at a minimum for all G-SIFIs (see Key

Attributes, Annex III, Elements of Recovery and resolution plans)• Regular reviews by top officials of home and hosts authorities of resolution strategies

and operational resolution plans

12. Access to information and information sharing• Robust management information systems (MIS) that enable firms to produce up-to-

date information on a timely basis• No impediments to cross-border sharing of relevant information among authorities

with a role in resolution subject to appropriate confidentiality arrangements.

12

Guidance for non-bank resolution

• Cross-sectoral scope of the Key Attributes• October 2014—Implementation Guidance in

new Annexes to the Key Attributes on – The resolution of FMI and FMI participants– The resolution of insurers– Protection of client assets in resolution

• Supplements the Key Attributes by indicating how particular KAs, or elements of particular KAs, should be interpreted when applied to resolution regimes for insurers, FMI or securities firms

13

Key Attributes Methodology

• Banking Sector Module completed; work in progress on Insurance – Drafted & tested– Revised to reflect lessons learned and modularisation of

methodology– Banking module finalised end-2016– Work underway on Insurance Sector module

• Road-tested– Switzerland, late 2013– United States, early 2015– Colombia, late 2015– Used as basis for thematic peer reviews

14

Lessons

• Context & adaptability– Structure of financial system– Complexity of financial system– Characteristics of local market

• Selective applicability & justification– Proportionality an important consideration– Role of Authorities in justifying non-

applicability of certain aspects of the KA– Assessors documentation

15

STATUS OF IMPLEMENTATION OF THE KEY ATTRIBUTES ACROSS FSB JURISDICTIONS

17

• Resolution designated as a priority area• Annual reporting to the G20

FSB Implementation Monitoring

• Second thematic peer review published March 2016• Country reviews with focus on resolution (Russia, Saudi

Arabia, Netherlands, Turkey, Japan)

FSB Thematic and country peer reviews with focus on

resolution issues

• Undertaken by FSB CBCM for G-SIBs • Undertaken by FSB iCBCM for G-SIIs

Monitoring of resolution planning work within CMGs

• First RAP completed for G-SIBs in 2015• Second G-SIB RAP and first G-SII RAP results reported

to 2016 G20 Summit

Resolvability Assessment Process (RAP)

• Assessment Methodology to guide reforms and serve as a tool for IMF and World Bank assessments – respective Boards expected to consider endorsement in 2017

IMF and World Bank FSAP and ROSC Assessments

Key Attributes Implementation

Resolution Thematic Review

18

Overview• Second thematic review on resolution regimes published March 2016• Scope: resolution powers for banks (KA 3) and requirements for

recovery and resolution planning and resolvability assessments for banks (KAs 10 and 11)

Main findings• Progress in reform has slowed• Only a subset of FSB members have a resolution regime with a

comprehensive set of powers in line with the KAs – mostly G-SIB home jurisdictions

• Some jurisdictions still rely on supervisory powers or sector-specific insolvency law

• Variation in (i) scope of application (non-regulated entities, holding companies, branches) and (ii) conditions for use of resolution powers

• Greater progress in recovery planning than resolution planning

19

Resolution Powers• Progress since 2012 made mostly by G-SIB home jurisdictions• Powers that are most commonly missing: bail-in, temporary stay

Resolution Thematic Review

20

Resolution Powers• Planned reforms will close some – but not all – of the gaps

Resolution Thematic Review

21

RRP and resolvability assessments• More progress in recovery planning than resolution planning• Alignment between resolution planning and resolvability assessments• Few jurisdictions have explicit powers to require banks to make

changes to improve resolvability

Recovery and resolution planning and resolvability assessments in FSB jurisdictions

Resolution Thematic Review

22

Recommendations• Recommendation 1: full implementation of the KAs

– Introduction of missing powers– Extension of resolution regimes to holding companies– Introduction of recovery and resolution planning requirements– Adoption of powers to require changes to improve resolvability

• Recommendation 2: additional clarification and guidance on the application of the KAs– Criteria to facilitate timely and early entry into resolution– Resolution powers for branches of foreign banks– Powers to require non-regulated entities to support continuity of

services and functions in resolution• Recommendation 3: supporting implementation of the KAs

– Sharing of experiences and practices

Resolution Thematic Review

Recent Developments

23Reforms issued for public consultation

Draft legislation submitted to legislative body

Final legislation or rule approved

Hong Kong Full resolution regime (June 2016)

Australia Temporary stay power (May 2016)

Canada Bail-in and temporary stay powers (May 2016)

Brazil Resolution bill

Resolution planningAustralia

India Full resolution regime

Indonesia Bridge bank and bail-in powers (April 2016)

Korea RRP, resolution powers

Saudi Arabia

Singapore

Resolution bill

South Africa Resolution bill

Resolution bill

Bridge bank powersTurkey Bridge bank power

• Several reforms introduced / progressed during the last year

24

Beyond the banking sector• Implementation of the KAs outside the banking sector still

at an early stage– Few comprehensive resolution regimes

– Resolution planning at an early stage

• Annexes to the Key Attributes set out resolution powers for insurers and FMIs

• FSB developing supporting guidance on resolution strategies and planning– Guidance on Developing Effective Resolution Strategies and Plans

for Systemically Important Insurers (June 2016)

– Draft Guidance on Central Counterparty Resolution and Resolution Planning (February 2017, final guidance expected July 2017)

Recent Developments