kerala - ibefkerala state co-operative rubber marketing federation cochin port trust, new indian...

TRANSCRIPT

1 1 JULY 2015 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

2 2

Executive Summary……………….….…. 3 Advantage State……………………..…... 5

Kerala Vision 2030 ………………….…... 6

Kerala – An Introduction………….….….. 7

Budget 2015-16…………………….…... 18

Infrastructure Status………………..…... 19

Key Industries………….………..…..….. 47

Doing Business in Kerala…………...… 65

State Acts & Policies………………....... 73

For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

JULY 2015

3 3 For updated information, please visit www.ibef.org

EXECUTIVE SUMMARY … (1/2)

Source: Economic Review of Kerala 2014-15 http://www.emergingkerala2012.org/infrastructure.php, News articles, Census 2011

NRI Achievers Bureau

KERALA GOD'S OWN COUNTRY

Cultural diversity and well developed tourism

sector

• Kerala is known as God’s own country. It is one of the few states to have marketed its natural beauty successfully to the leisure tourism sector. The state’s unique heritage and cultural diversity have helped attract tourists from the world over.

Highest literacy and sex ratio

• Kerala has the highest literacy rate (94.6 per cent) and sex ratio (1,084 women for 1,000 men) in India. Literacy rate for male population is the highest at 96.67 per cent.

Largest recipient of foreign remittances in

the country

• In 2014-15, Kerala received NRI remittances of US$ 16.50 billion. In 2013-14, NRI remittances of the state were US$ 2.3 billion, up by 10 per cent compared to 2012-13.

Ranks second in Investment Climate

Index

• Kerala holds second rank in the Investment Climate Index followed by Karnataka, as per a policy research working paper by the World Bank. The state stands second due to its world-class infrastructure and well-trained human resource pool.

JULY 2015

4 4 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

EXECUTIVE SUMMARY … (2/2)

Source: Economic Review of Kerala 2014-15 , Kerala IT Policy, TEU’s = Twenty-foot Equivalent Unit Rubber Board, Ministry of Commerce and Industry, Government of India Kerala State Co-operative Rubber Marketing Federation

Cochin Port Trust, New Indian Express

Strong agricultural sector

• Kerala is a leading agricultural state in the country and the largest producer of rubber, pepper, coconut and coir. In 2014-15, the state accounted for 73% share in the pepper production and 69% share in the natural rubber production of the country.

First international container transhipment

terminal

• Kerala has the first international transshipment terminal in India, having a design capacity of around 4 million TEUs and providing better connectivity between Kerala and other ports in India.

Presence of world class technology park

• Kerala has been promoting knowledge-based industries such as IT/ITeS, computer hardware and biotechnology. It is the first state having a technology park with CMMI level 4 quality certification and a world-class IT campus in Thiruvananthapuram.

Cochin-favourite port for luxury cruses

• Cochin port is one of the favourite ports for luxury cruses. Number of cruise arrivals at Cochin port stood at 34 in 2013-14 that reached to 39 by 2014-15.

JULY 2015

5 5 For updated information, please visit www.ibef.org

Source: Economic Review of Kerala 2014-15, Tourism Vision 2030, GSDP: Gross State Domestic Product

KERALA GOD'S OWN COUNTRY

Growing demand High economic growth

• Kerala’s gross state domestic product (GSDP) surged at a compound annual growth rate (CAGR) of 9.9 per cent between 2004-05 and 2014-15.

• Kerala is the leader in rubber production; high demand of rubber has opened up immense opportunities for the state in the rubber industry.

Leader in tourism

• In 2015, Kerala was rewarded as the winner of PATA awards by Macau Government Tourism Office (MGTO)

• BBC Travel survey has rated Kerala as the top favourite tourist destination among foreign travellers.

• Foreign and domestic tourist arrivals increased respectively by 8 per cent and 10.4 per cent during 2014 over 2013.

Policy and infrastructure support

• Kerala has a wide range of fiscal and policy incentives for businesses under the Industrial and Commercial Policy and has well-drafted sector-specific policies.

• It has a well-developed social, physical and industrial infrastructure and virtual connectivity, and good power, airport, IT, and port infrastructure. E-governance initiatives will further strengthen transparency and bridge digital divide.

Rich labour pool

• Kerala has a large base of skilled labour, making it an ideal destination for knowledge-intensive sectors.

• The state has the highest literacy rate in the country.

• It has a large pool of semi-skilled and unskilled labourers.

• The state has over 160 engineering colleges.

2014

Foreign tourist

arrivals:

0.92 million

2021E

Foreign tourist

arrivals:

3.0 million

Advantage Kerala

ADVANTAGE: KERALA

JULY 2015

6 6 For updated information, please visit www.ibef.org

KERALA VISION 2030

KERALA GOD'S OWN COUNTRY

Forestry

Energy

Agriculture & livestock

Transport

Education Labour

Industry

• Increase the share of forestry in GSDP to 0.5 per cent.

• Increase the productivity of forests through improved management of resources.

• Shift from subsistence farming to highly knowledge intensive, competitive farming.

• Self sufficiency in supply of fish, meat, milk and other dairy products to the local market.

• Affordable and clean power to all. • Exploit the full potential of hydro-

electric generation. • 100 per cent electrified households

with 24*7 availability.

• Green, sustainable and safe transport.

• Provide high quality education at affordable rates.

• Create a global brand name in education and develop into a knowledge hub by 2030.

• Growth oriented labour welfare policy.

• Connecting labour supply with demand.

• Increasing employment opportunities.

• Increase the share of manufacturing to 10 per cent of the GSDP by 2030.

• Sustained increase in employment in manufacturing.

Health

• Increase health expenditure to GSDP ratio from 0.6 per cent in 2012 to 4-5 per cent by 2027−31.

• Set up three medical cities by 2030.

• Provide health insurance cover to all.

Vision 2030

Source: Government of Kerala

JULY 2015

7 7 For updated information, please visit www.ibef.org

KERALA FACT FILE

Kerala is located along the coastline to the extreme south-west of the Indian peninsula, flanked by the Arabian Sea on the west and the mountains of the Western Ghats on the east. The state has a 580 km long coastline. Malayalam is the most commonly spoken language. Hindi, English and Tamil are the other languages used. Kochi, Kozhikode, Kollam, Thrissur, Alappuzha, Palakkad, Thalassery, Ponnani and Manjeri are some of the key cities in the state.

There are 44 rivers flowing through Kerala, the major ones being Periyar (244 km), Bharathapuzha (209 km) and Pamba (176 km). Out of these 44 rivers 41 are west flowing and 3 are east flowing.

Source: Kerala at a glance, Economic Survey of Kerala,2014-15 Government of Kerala website, www.kerala.gov.in, Census 2011

Central Statistics Office

Parameters Kerala

Capital Thiruvananthapuram

Geographical area (sq km) 38,863

Administrative districts (No) 14

Population density (persons per sq km)

860

Total population (million) 33.41

Male population (million) 16.02

Female population (million)

17.38

Sex ratio (females per 1,000 males)

1,084

Literacy rate (%) 94.6

KERALA GOD'S OWN COUNTRY

Source: Maps of India

JULY 2015

8 8

Parameter Kerala All states Source

Economy 2014-15 2014-15

GSDP as a percentage of all states’ GSDP

3.35 100.0 TechSci Estimates based on “Advanced Estimates” provided by Directorate of Economics and Statistics

of Kerala

GSDP growth rate (%) 2.85 7.3 TechSci Estimates based on “Advanced Estimates” provided by Directorate of Economics and Statistics

of Kerala

Per capita GSDP (US$) 1,961 1,389.61 TechSci Estimates based on “Advanced Estimates” provided by Directorate of Economics and Statistics

of Kerala

Physical Infrastructure

Installed power capacity (MW) 4,084.67^ 272,502.95 Central Electricity Authority, as of May 2015

Wireless subscribers (No) 31,775,409* 973,347,094 Telecom Regulatory Authority of India- April 2015

Broadband subscribers (No) 355,0000** 100,760,000 Telecom Regulatory Authority of India- April 2015

National Highway length (km) 1,811.52 92,851.07 National Highway Authority of India April-2015

Major and minor ports (No) 1+17 13+187 Indian Ports Association 2015

Airports (No) 3 132 Airports Authority of India

For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

KERALA IN FIGURES … (1/2)

^As of June 2015, *As of May 2015, ** As of March 2014

JULY 2015

9 9

Parameter Kerala All states Source

Social Indicators

Literacy rate (%) 94.6 73.0 Census, 2011

Birth rate (per 1,000 population each year) 15.2 21.4 SRS Bulletin, September 2014

Investment

FDI equity inflows (US$ billion) 1.21 248.5 Department of Industrial Policy & Promotion,

April 2000 to March 2015

Outstanding investments (US$ billion) 48.0 2,414.2 CMIE (2013-14)

Industrial Infrastructure

PPP projects (No) 31 1,409 DEA, Ministry of Finance, Government of India

SEZ (No) 25 347 Notified as of March 2015, Ministry of

Commerce & Industry

PPP: Public-Private Partnership, SEZ: Special Economic Zone, SRS: Sample Registration System

For updated information, please visit www.ibef.org

KERALA IN FIGURES … (2/2)

KERALA GOD'S OWN COUNTRY

JULY 2015

10 10

26.6 31.0 34.1

43.5 43.9 48.9

57.8 65.7 64.3 66.6 68.5

20

04-0

5

20

05-0

6

20

06-0

7

20

07-0

8

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

20

14-1

5

CAGR 9.9%

At current prices, Kerala’s GSDP was about US$ 68.5 billion in 2014-15.

The state’s GSDP recorded at a CAGR of 9.9 per cent between 2004-05 and 2014-15.

Growth was mainly driven by secondary and tertiary sectors.

Source: TechSci Estimates based on “Advanced Estimates” provided by Directorate of Economics and Statistics of Kerala

GSDP of Kerala at current prices (US$ billion)

For updated information, please visit www.ibef.org

ECONOMIC SNAPSHOT – GSDP

KERALA GOD'S OWN COUNTRY

JULY 2015

11 11

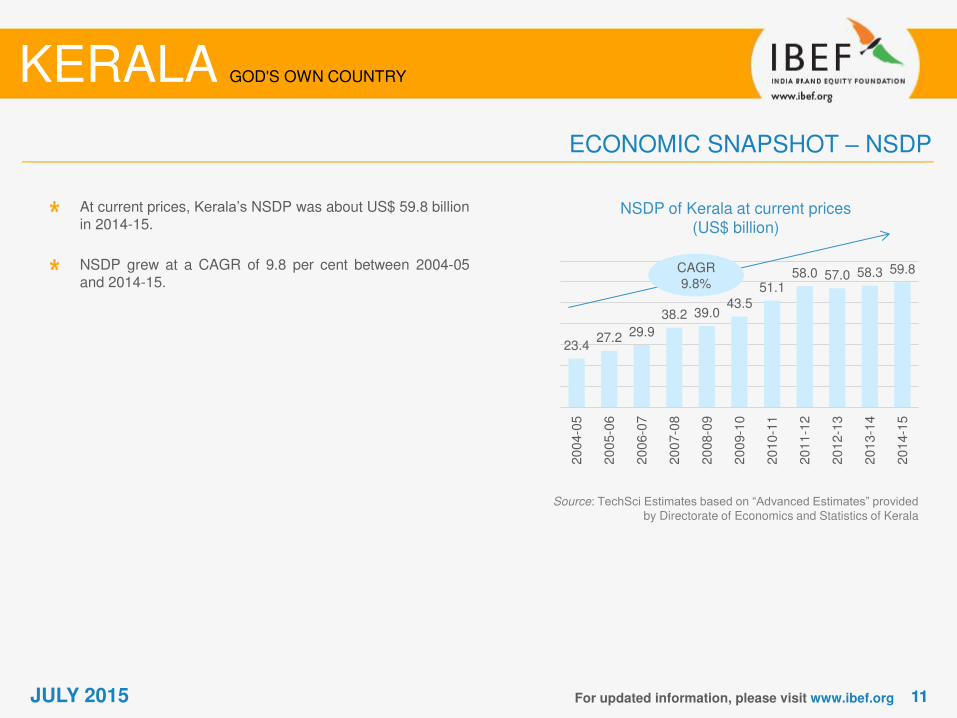

At current prices, Kerala’s NSDP was about US$ 59.8 billion in 2014-15.

NSDP grew at a CAGR of 9.8 per cent between 2004-05 and 2014-15.

NSDP of Kerala at current prices (US$ billion)

For updated information, please visit www.ibef.org

ECONOMIC SNAPSHOT – NSDP

KERALA GOD'S OWN COUNTRY

JULY 2015

23.4 27.2 29.9

38.2 39.0 43.5

51.1 58.0 57.0 58.3 59.8

20

04-0

5

20

05-0

6

20

06-0

7

20

07-0

8

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

20

14-1

5

Source: TechSci Estimates based on “Advanced Estimates” provided by Directorate of Economics and Statistics of Kerala

CAGR 9.8%

12 12

The state’s per capita GSDP was US$ 1,961 during 2014-15 compared to US$ 810 during 2004-05.

Per capita GSDP increased at a CAGR of 9.3 per cent between 2004-05 and 2014-15.

GSDP per capita of Kerala at current prices (US$)

For updated information, please visit www.ibef.org

ECONOMIC SNAPSHOT – PER CAPITA GSDP

KERALA GOD'S OWN COUNTRY

JULY 2015

Source: TechSci Estimates based on “Advanced Estimates” provided by Directorate of Economics and Statistics of Kerala

810 935 1,019

1,291 1,294 1,430

1,678 1,892 1,841 1,907 1,961

20

04-0

5

20

05-0

6

20

06-0

7

20

07-0

8

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

CAGR 9.3%

13 13

Kerala’s per capita NSDP was US$ 1,713 in 2014-15 compared to US$ 711 during 2004-05.

Per capita NSDP grew a CAGR of 9.2 per cent between 2004-05 and 2014-15.

NSDP per capita of Kerala at current prices (US$)

For updated information, please visit www.ibef.org

ECONOMIC SNAPSHOT – PER CAPITA NSDP

KERALA GOD'S OWN COUNTRY

JULY 2015

Source: TechSci Estimates based on “Advanced Estimates” provided by Directorate of Economics and Statistics of Kerala

711 822 895 1,135 1,150

1,270 1,483

1,672 1,630 1,668 1,713

20

04-0

5

20

05-0

6

20

06-0

7

20

07-0

8

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

20

14-1

5

CAGR 9.2%

14 14

17.90% 14.09%

22.50% 20.06%

59.60% 65.85%

2004-05 2014-15

Primary Secondary Tertiary

In 2014-15, the tertiary sector contributed 65.85 per cent to the state’s GSDP at current prices, followed by the secondary sector at 20.06 per cent.

The tertiary sector grew at a CAGR of 11.0 per cent between 2004-05 and 2014-15. Growth was driven by storage, transport, financial and real estate segments.

The secondary sector grew at an average rate of 8.7 per cent between 2004-05 and 2014-15. Growth was led by manufacturing, construction, and electricity, gas & water supply segments.

The primary sector expanded at an average rate of 7.3 per cent between 2004-05 and 2014-15, mainly supported by growth across agriculture and mining & quarrying segments.

Source: TechSci Estimates based on “Advanced Estimates” provided by Directorate of Economics and Statistics of Kerala

Economic Survey 2014-15

GSDP composition by sector

For updated information, please visit www.ibef.org

ECONOMIC SNAPSHOT – PERCENTAGE DISTRIBUTION OF GSDP

KERALA GOD'S OWN COUNTRY

CAGR

7.3%

11.0%

8.7%

JULY 2015

15 15

Source: Directorate of Economics and Statistics, *Production in million nuts, Values, ^In 2013-14 Tea Board India, Directorate of Economics and Statistics, Kerala

Crop Annual production in 2014-15 (metric tonnes)

Tapioca 2,581,382

Rubber 6,55,000

Banana 528,205

Rice 161,476

Areca nut* 119,349

Coffee 67,700

Tea 67,200

Pepper 43,600

Cashew nut 33,375^

Ginger 20,791

Pulses 3,019^

Groundnut 621.4

Turmeric 6,253^

Coconut 5,969

Total Cereals 564,635^

Agriculture and allied sectors contributed 11.8 per cent to Kerala’s GSDP in 2012-13.

Kerala is one of the leading pepper producers in the country. During 2014-15, production increased by 21.9 per cent to 43,600 metric tonnes compared to 2013-14.

The state is also one of the largest producers of natural rubber in India. Production was 655,000 metric tonnes during 2014-15.

During 2014-15, total area under foodgrains and oilseed crops stood at 156.68 thousand hectares, wherein majority of the share is accounted to foodgrains.

Under foodgrain crops jowar and maize are the prominent crops. During 2014-15, the production of jowar and maize was recorded as 128.4 metric tonnes and 62.0 metric tonnes respectively.

For updated information, please visit www.ibef.org

ECONOMIC SNAPSHOT – AGRICULTURAL PRODUCTION

KERALA GOD'S OWN COUNTRY

JULY 2015

16 16

2,503

3,611 3,709

4,393 4,046 4,028

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

For updated information, please visit www.ibef.org

ECONOMIC SNAPSHOT – EXPORTS

KERALA GOD'S OWN COUNTRY

Exports from Cochin port improved at a CAGR of 29.7 per cent to 4.2 million MT from 2009-10 to 2013-14. In value terms, exports from Cochin port increased at a CAGR of 10 per cent to reach US$ 4,028 million by 2013-14.

The increase in exports from CSEZs in the past years can be attributed to a substantial rise in gems and jewellery exports. Gems and jewellery accounted for 18.7 per cent share in the overall exports from the CSEZ.

Source: Economic Review of Kerala 2014-15 CSEZ - Cochin Special Economic Zone

Total exports turnover from CSEZs (US$ million)

CAGR 10%

Exports break-up, Cochin Port (2013-14)

Sectors (US$ million)

Tea 85.2

Cashew kernels 442.8

Sea Foods 666.6

Coir products 64.2

Spices 109.1

Coffee 145.3

Miscellaneous 2,514.8

JULY 2015

17 17

According to DIPP, FDI inflows to the state (including Lakshadweep) totalled US$ 1.21 billion during 2000 to March 2015. As of January 2015, The Kannur airport received additional investments of US$ 316 million for development activities. As of March 2015, US$ 4.1 billion has been sanctioned for infrastructure development for the next three years The state government has sanctioned investments of US$ 100 million, US$ 156 million and US$ 8.3 million for the Vizhinjam International Seaport project, Kochi Metro Rail Project and for land acquisition for Kozhikode and Thiruvananthapuram international airports respectively.

As of 2015, an investment of US$ 6.5 million has been sanctioned for Class I works under Minor Irrigation project and US$ 179.1 million is approved for General Education. As of 2015, growth of 15% in the state manufacturing sector and 8% in the country’s manufacturing sector is expected owing to rising investments in Make in Kerala project.

Source: DIPP - Department of Industrial Policy & Promotion, Including Lakshadweep, Government of Kerala, News articles

FDI equity inflows, 2008-09 to 2014-15* (US$ million)

For updated information, please visit www.ibef.org

ECONOMIC SNAPSHOT – FDI INFLOWS & INVESTMENTS

KERALA GOD'S OWN COUNTRY

Mega projects conceptualised and developed in Kerala include Supplementary Gas Infrastructure Project by Kerala Gail Gas Limited (US$ 400 million), Kochi Metro Rail Project (US$ 900 million), and a monorail project in Thiruvananthapuram (US$ 682 million).

JULY 2015

82 128

37

471

72 70

230

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

20

14-1

5

18 18 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

ANNUAL BUDGET 2015-16

JULY 2015

Source: Finance Department, Government of Kerala, India

Annual Budget 2015-16

Sector Investment (US$ million)

Agriculture 113.97

Soil and water conservation 13.31

Animal husbandry 0.36

Dairy development 13.11

Development of fisheries sector & welfare of fishermen

30.19

Forest & wildlife 25.22

Panchayats 3.32

Urban development 3.32

Rural development 8.29

Industries 96.58

Water resources 4.64

Water supply & sewerage 149.37

Power 243.40

Annual Budget 2015-16

Sector Investment (US$ million)

Housing 1.24

Science, technology & environment

25.43

General education 178.27

Transport 207.70

Social justice 0.83

Tourism 37.00

Art & culture 0.17

Museum & zoo 2.70

19 19 For updated information, please visit www.ibef.org

In Kerala, the Public Works Department (PWD) has a total road length of 33,623.07 km and 1,811.52 km of national highways. The state is well-connected to its neighbouring states and other parts of India through nine National Highways.

Agencies maintaining roads in Kerala include the Public Works Department (PWD); panchayats; municipalities, corporations; the departments of forests, irrigation, railways; and the Kerala State Electricity Board (KSEB).

As of March 2015, around 6.66 km of PWD roads are made of cement concrete, 30,744.4 km are black-topped, and 447.3 km are water-bound macadam. Nearly 97 per cent of the total roads are black-topped surfaces.

During 12th Five Year Plan the state government proposed to develop 290 kilometers of roads under various scheme. As of 2015-16, an allocation of US$ 36.6 million is allocated to KSRTC (Kerala State Road Transport Corporation). State government has sanctioned an amount of US$ 0.49 million for the construction of Palluruthy-Naalpathady road.

For the same year, an amount of US$ 1.3 million is set apart for the infrastructural development and modernisation of the Workshops and Depots of KSRTC.

Source: Economic Review of Kerala, 2014-15 Kerala State Industrial Development Corporation Ltd.

Ministry of Road Transport & Highways, Government of Kerala

Road type Road length (km)

National highways 1,811.52

State highways 4,341.65

Major district roads 27,469.9

KERALA GOD'S OWN COUNTRY

PHYSICAL INFRASTRUCTURE – ROADS

Source: Maps of India

JULY 2015

20 20 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

PHYSICAL INFRASTRUCTURE – RAILWAYS

Kerala is well connected to other parts of the country via railways. As of March 2014, it had a railway network of 1,257 km, with around 200 railway stations and 13 railway routes.

The state government has appointed Kerala State Industrial Development Corporation Ltd (KSIDC) as the nodal agency for developing a project to establish a north-south High-speed Rail Corridor (HSRC) to facilitate smooth and speedy passenger movement between various cities and towns in the state.

Railway divisions in Thiruvananthapuram, Palakkad and Madurai jointly carry out railway operations in Kerala.

Works for Kochi Metro Rail System Phase 1 are underway. It involves investment of US$ 864 million and is expected to be completed in mid-2016.

First train is expected to be operational by the end of January 2016. The second phase i.e. Maharajas College to Pettah (about 7.5 kms and 6 stations) is in progress.

As per Budget 2015-16, Government of India has allocated US$ 106.6 million for Kochi Metro Rail Project.

Source: Maps of India Source: Economic Review of Kerala, 2014-15

Kerala State Industrial Development Corporation Ltd, Government of Kerala

JULY 2015

21 21 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

PHYSICAL INFRASTRUCTURE – AIRPORTS…(1/2)

Kerala has three airports handling domestic and international flights, located at Thiruvananthapuram, Kochi and Kozhikode. The Cochin International Airport Limited (CIAL) has displayed consistent growth in both passenger traffic and aircraft movements since it opened in 1999. The airport handled 6.45 million passengers in 2014-15, an increase of 19.66 per cent from the previous year. In 2014-15, Kerala witnessed arrival of 12.63 million tourists, out of which 11.7 million tourists were domestic and remaining were foreign tourists. The airport recorded 47,072 aircraft movements during 2013-14, 13.32 per cent higher compared to the previous year. During 2014-15, the aircraft movement reached to 52,800. CIAL’s cargo division turnover increased 17 per cent as total cargo handled stood at 54,440 tonnes in 2013-14 against the previous year’s 46,530.3 tonnes. As per Budget 2015-16, Government of India has allocated US$ 8.3 million for acquisition of land for international airports at Calicut and Thiruvananthapuram.

Source: Maps of India Source: Economic Review of Kerala, 2014-15, Airports Authority of India, Kerala State Industrial Development Corporation Ltd, News articles,

Government of Kerala

Airport

JULY 2015

22 22 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

PHYSICAL INFRASTRUCTURE – AIRPORTS…(2/2)

In order to promote the tourism sector of the state, Union Minister of State for Tourism (Independent Charge) launched ‘Visit Kerala’ campaign in April 2015.

Prime feature of this campaign are as follows -

The major focus of the campaign is to increase the number of tourist arrivals in Kerala to 13.7 million by the end of 2015.

The government is planning to use social media to promote tourism in Kerala. To introduce Kerala’s authentic cuisines, government is planning to arrange food festivals in major Indian cities like Mumbai and New Delhi. To ensure greater women empowerment, a major share of women personnel are expected to be hired in the tourism industry.

Source: Government of Kerala

JULY 2015

23 23

Kerala has 18 ports, of which, Cochin is the major one. Furthermore, there are three intermediate and 14 minor ports.

Kerala is constructing the Vizhinjam deep-water international container transhipment terminal at Vizhinjam, 17 km south of Thiruvananthapuram, under the PPP mode.

Government has already approved Cochin Port’s land utilisation policy, which will be placed before cabinet.

In 2013-14, the Government prepared a master plan for “Kollam Port City”. This initiative is a part of Coastal Shipping Project implementation.

Source: Cochin Port Trust, ipa.nic.in, Kerala Ports, Economic Review of Kerala, 2014-15

State Planning Board

For updated information, please visit www.ibef.org

PHYSICAL INFRASTRUCTURE – PORTS … (1/4)

KERALA GOD'S OWN COUNTRY

Existing ports

Major ports • Cochin

Intermediate ports

• Neendakara • Alappuzha • Kozhikkode

Minor ports

• Vizhinjam • Valiyathura • Vadakara • Ponnani • Thankasserry • Kayamkulam • Manakkodam • Munambam • Beypore • Thalasserry • Manjeswaram • Neeleswaram • Kannur • Azhikkal • Kasaragode

JULY 2015

24 24

15.8 15.2 17.4 17.9

20.1 19.8 20.9 21.5

20

07-0

8

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

20

14-1

5

During 2014-15, total trade volume handled at the Cochin port surged to 21.5 million tonnes from 20.9 million tonnes in 2013-14.

Bulk cargo handling during 2014-15 grew by 15.2 per cent compared to 2013-14, whereas oil cargo handling increased by 3.5 per cent and container cargo edged up by 3.2 per cent.

The Union Ministry of Defence and the state government are endeavouring towards more commercialisation of the Cochin port.

Kerala Maritime Board has been constituted for the administrative control and management of non-major ports in Kerala.

A token provision is provided for the functioning of the Board to supplement additional funds later.

Source: Cochin Port Trust, News articles, Economic Survey 2014-15

For updated information, please visit www.ibef.org

PHYSICAL INFRASTRUCTURE – PORTS … (2/4)

KERALA GOD'S OWN COUNTRY

Cochin port traffic (million tonnes)

CAGR 4.5%

JULY 2015

25 25

The Cochin port is a favourite port-of-call for luxury cruise liners from around the world.

During 2014-15, 39 cruise liners arrived at the Cochin port.

Around 28,342 cruise passengers embarked in Kochi in 2014-15.

The arrival of a cruise vessel has an added impact on the regional economy as cruise tourists are high end passengers. On an average, each tourist is estimated to spend US$ 200 during the stopover of less than a day.

Source: Cochin Port Trust, New Indian Express Economic Survey 2014-15, News article

For updated information, please visit www.ibef.org

PHYSICAL INFRASTRUCTURE – PORTS … (3/4)

KERALA GOD'S OWN COUNTRY

Number of cruise arrivals at Cochin port

JULY 2015

26

38

43

36

45 41

44 42

34

39

20

05-0

6

20

06-0

7

20

07-0

8

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

20

14-1

5

Cruise passenger in Kerala

Year Passenger

2011-12 34,768

2012-13 37,389

2013-14 24,535

2014-15 28,342

26 26

Source: Cochin Port Trust, New Indian Express

For updated information, please visit www.ibef.org

PHYSICAL INFRASTRUCTURE – PORTS … (4/4)

KERALA GOD'S OWN COUNTRY

JULY 2015

CATEGORY WISE DISTRIBUTION OF VESSELS ENTERING THE COCHIN PORT

Year Number of Vessel

Containers Coal Fertilizers & raw materials

Others Food Grains

General Cargo

Tankers Passenger

cum No Cargo

2005-06 421 4 38 8 0 109 383 236

2006-07 382 7 27 15 5 92 382 225

2007-08 350 6 15 11 2 73 352 269

2008-09 334 6 22 23 0 63 305 293

2009-10 390 5 17 36 0 45 381 359

2010-11 360 2 18 28 0 39 372 396

2011-12 390 2 15 33 0 37 361 504

2012-13 439 1 12 47 0 24 354 449

2013-14 501 0 11 62 0 41 382 399

2014-15 529 2 15 62 0 33 356 440

27 27

3,514.0 3,553.7

3,718.8

3,827.7 3,856.4 3,892.0

4,106.5 4,084.7

200

8-0

9

200

9-1

0

201

0-1

1

201

1-1

2

201

2-1

3

201

3-1

4

201

4-1

5

201

5-1

6*

As of June 2015, the state had total installed power generation capacity of 4,084.67 MW, which consisted of 2,240.02 MW under state utilities, 1,590.62 MW under central utilities, and 254.03 MW under the private sector. Thermal power contributed 1,770.62 MW to total installed power generation capacity. Hydropower (1,881.50 MW), nuclear power (228.60 MW), and renewable power (203.95 MW) are the other main energy sources. Kerala’s state utilities, which account for 54.83 per cent of overall capacity, generate 83.99 per cent of the energy through hydroelectric power plants, and the remaining 16.01 per cent through thermal and renewable power generation plants. Kerala is among the prominent Indian states to have achieved 100 per cent rural electrification.

Source: Central Electricity Authority, Business Standard, *As of June 2015

Installed power capacity (MW)

For updated information, please visit www.ibef.org

PHYSICAL INFRASTRUCTURE – POWER … (1/2)

KERALA GOD'S OWN COUNTRY

CAGR 2.17%

JULY 2015

28 28 For updated information, please visit www.ibef.org

PHYSICAL INFRASTRUCTURE – POWER … (2/2)

KERALA GOD'S OWN COUNTRY

JULY 2015

Budget Highlights-2015-16:

An investment of US$ 244.5 million has been sanctioned to enhance power generation through different methods such as thermal, hydro, coal etc.

An investment of US$ 0.16 million has been sanctioned to establish a coal based power plant at Cheemeni as a joint venture of KSEB & KSIDC.

An investment of US$ 2.5 million has been sanctioned for the Senkulam Augmentation scheme which is projected to be commissioned by February 2016.

An amount of US$ 3.3 million has been sanctioned for the Chethan kotta small hydro electric project. The project is expected to be commissioned by October 2015.

Source: Finance Department, Government of Kerala, India

29 29

Telecom infrastructure (May 2015)

Wireless subscribers 31,775,409

Wire-line subscribers 2,547,365

Broadband subscribers 355,0000*

Post offices 5,067*

Telephone exchanges 1,266^

Teledensity (in per cent) 95.35^

Source: Telecom Regulatory Authority of India, Economic Review of Kerala, 2014-15 , *As of March 2014, ^As of April 2015

Kerala had an overall tele-density of 95.35 per cent as against an all-India average of 78.16 per cent, as of April 2015.

The state has 1,266 telephonic exchanges. About 98.0 per cent of Kerala's telephone exchanges have internet connectivity through the National Internet Backbone (NIB).

VSNL has an international communication gateway in Kochi, with two high-speed submarine cable landings (SEA-ME-WE-3 and SAFE), offering 15 gigabytes per second (Gbps) bandwidth.

According to the Telecom- Regulatory Authority of India (TRAI), as of May 2015, Kerala had nearly 31.78 million wireless subscribers and 2.5 million wire-line subscribers (including Lakshadweep).

Currently, Kerala is the largest revenue contributing state of BSNL and accounts for nearly 25 per cent of the company’s national revenue. The company expects to post a record profit of around US$ 66.4 million during 2013-14.

As of May 2015, the wireless market share of BSNL in Kerala is 21.07 percent.

For updated information, please visit www.ibef.org

PHYSICAL INFRASTRUCTURE – TELECOM

KERALA GOD'S OWN COUNTRY

Major telecom operators in Kerala

Bharat Sanchar Nigam Limited (BSNL)

Bharti Airtel

Aircel Limited

Vodafone Essar

IDEA Cellular

Tata Teleservices

Reliance Communications

Source: Telecom Regulatory Authority of India

JULY 2015

30 30

Under the Jawaharlal Nehru National Urban Renewal Mission (JnNURM), ten projects worth US$ 238 million have been approved during 2005-2012 for the development of urban infrastructure in Thiruvananthapuram and Kochi. As on 31st March 2014, 10 projects with a total cost of US$ 160.9 million are in progress. The Kerala Sustainable Urban Development Project (KSUDP) is an Asian Development Bank-assisted project covering the five municipalities of Thiruvananthapuram, Kochi, Kozhikode, Kollam and Thrissur. With an investment of US$ 221.2 million, the project focuses on urban infrastructure improvement, community upgrading, local government infrastructure development and capacity building, and implementation assistance. The Kerala Water Authority (KWA) is responsible for the design, construction, execution, operation and maintenance of most of the water supply schemes, and the collection and disposal of waste water in Kerala. Construction of the first phase of SmartCity Kochi, a self-sustained industry township project that is a conglomerate promoted by Dubai Holding member TECOM Investments for knowledge-based companies, would be completed within 18 months from the start of construction in June 2013. “Kudumbashree”, the State Poverty Eradication Mission, is involved in “Clean Kerala Business’’ to collect door-to-door household waste and process it for economic benefits. A Rural Water Supply and Environmental Sanitation Project had been implemented by the World Bank in September 2008; another similar project is under implementation and is expected to be completed by June 2017, with an estimated cost of US$ 222.3 million. The World Bank has approved a US$ 216 million loan for the Kerala State Transport Project II to support the Government of Kerala improve the condition, traffic flow, and safety of its road network.

For updated information, please visit www.ibef.org

DEVELOPMENT PROJECTS: URBAN INFRASTRUCTURE

KERALA GOD'S OWN COUNTRY

Source: JNNURM, Ministry of Urban Development, Economic Review of Kerala, 2012, World Bank

JULY 2015

31 31

Project name Sector PPP type Contact authority Project cost (US$ million)

Cochin International Airport Airports BOO Airport Authority of India 50.3

Vallarpadam Container Transshipment Terminal

Ports BOT-Toll Cochin Port Trust 351.4

LNG Regasification Terminal at Cochin Port Ports NA Ministry of Shipping 530.0

Crude Oil Handling for Kochi Refineries Ltd Ports Lease Cochin Port Trust 116.6

Thrissur-Edapalli Roads BOT-Toll National Highways Authority of India 51.8

Six laning of Vadakkancherry-Thrissur section

Roads BOT-Toll National Highways Authority of India 102.4

Four laning of Walayar-Vadakkancherry section

Roads BOT-Toll National Highways Authority of India 113.1

Source: Overseas Indian Facilitation Centre BOT: Build-Operate-Transfer, BOO: Build-Own-Operate

For updated information, please visit www.ibef.org

DEVELOPMENT PROJECTS: KEY PUBLIC-PRIVATE PARTNERSHIP (PPP) PROJECTS … (1/2)

KERALA GOD'S OWN COUNTRY

As of March 2015, Kerala had around 31 PPP projects, spreading across various sectors such as airports, roads, tourism, urban infrastructure and ports.

JULY 2015

32 32

Project name Sector PPP type Contact authority Project cost (US$ million)

Four-laning of Karnataka & Kerala Border to Kannur section

Roads BOT-Toll National Highways Authority of India 191.9

Kannur -Kuttipuram Package- 2 Roads BOT-Toll National Highways Authority of India 217.7

Kannur-Kuttipuram Package – 1 Roads BOT-Toll National Highways Authority of India 226.6

Vizhinjam Port International Ports BOT - Annuity Directorate of Ports, Government of

Kerala 887.2

Development of a new bridge connecting Mattancherry and Willingdon Island at Cochin

Roads BOT-Toll The Greater Cochin Development

Authority 4.5

Development of resorts at Bekal Kasaraode Dist

Tourism BOO Bekal Resorts Development

Corporation BRDC KTDC 9.1

Kochi Metro Rail Project Urban

development BOT -

Annuity Kerala Industrial Infrastructure

Development Corporation 505.6

Trivandrum City Road Improvement Urban

development BOT-Toll Kerala Road Fund Board 18.6

For updated information, please visit www.ibef.org

DEVELOPMENT PROJECTS: KEY PUBLIC-PRIVATE PARTNERSHIP (PPP) PROJECTS … (2/2)

KERALA GOD'S OWN COUNTRY

Source: Overseas Indian Facilitation Centre BOT: Build-Operate-Transfer, BOO: Build-Own-Operate

JULY 2015

33 33 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

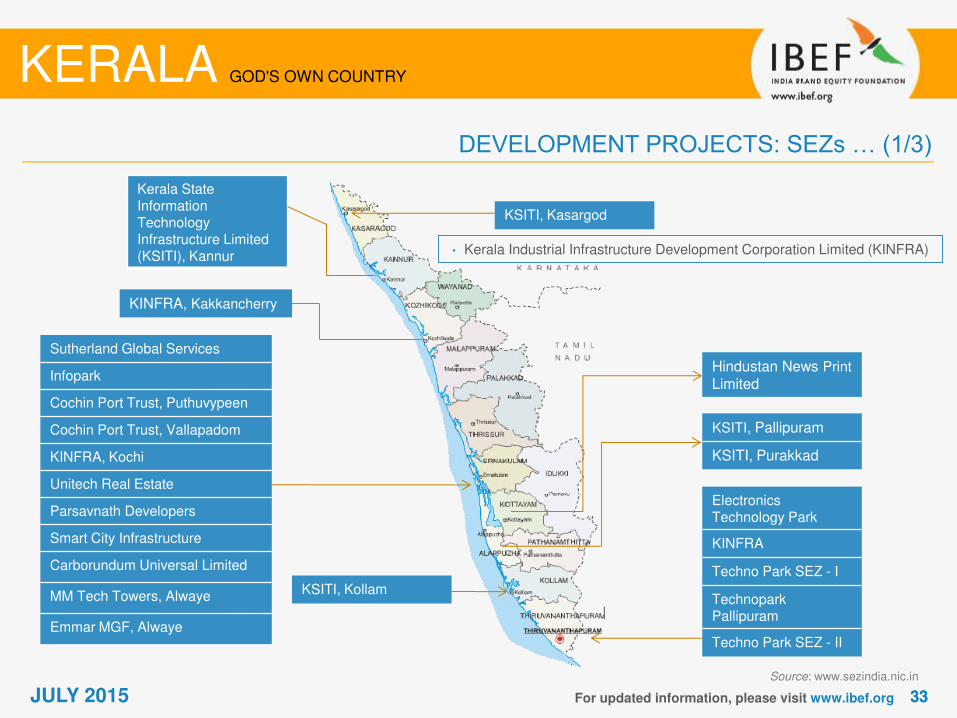

DEVELOPMENT PROJECTS: SEZs … (1/3)

Sutherland Global Services

Infopark

Cochin Port Trust, Puthuvypeen

Cochin Port Trust, Vallapadom

KINFRA, Kochi

Unitech Real Estate

Parsavnath Developers

Smart City Infrastructure

Carborundum Universal Limited

MM Tech Towers, Alwaye

Emmar MGF, Alwaye

Electronics Technology Park

KINFRA

Techno Park SEZ - I

Technopark Pallipuram

Techno Park SEZ - II

KINFRA, Kakkancherry

KSITI, Pallipuram

KSITI, Purakkad

• Kerala Industrial Infrastructure Development Corporation Limited (KINFRA)

KSITI, Kasargod

Kerala State Information Technology Infrastructure Limited (KSITI), Kannur

Hindustan News Print Limited

KSITI, Kollam

Source: www.sezindia.nic.in

JULY 2015

34 34

Source: www.sezindia.nic.in, SEZ: Special Economic Zone

Name/Developer Location Primary industry

Cochin SEZ Cochin Multi-product

Infopark SEZ Kochi IT/ITeS

Electronic Technology Park-SEZ-I Thiruvananthapuram IT/ITeS

Electronic Technology Park-SEZ-II Thiruvananthapuram IT/ITeS

Cochin Port Trust Vallarpadam Port-based

KINFRA Film & Video Park Thiruvananthapuram Animation & gaming

Kerala State Information Technology Infrastructure Ltd Cherthala IT/ITeS

Kerala Industrial Infrastructure Development Corporation (KINFRA)

Pathanamthitta Food processing

Operational SEZs in Kerala

For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

DEVELOPMENT PROJECTS: SEZs … (2/3)

Kerala has eight operational SEZs.

JULY 2015

35 35 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

DEVELOPMENT PROJECTS: SEZs … (3/3)

Source: www.sezindia.nic.in, SEZ: Special Economic Zone

Name/Developer Location Primary industry

Cochin Port Trust Vallarpadam Port based

Cochin Port Trust Puthuvypeen, Ernakulam Port based

KINFRA Kazhakoottam,

Thiruvananthapuram IT (Animation & gaming)

Smart City (Kochi) Infrastructure Pvt Ltd Kakkanad, Ernakulam IT/ITeS

Kerala State Information Technology Infrastructure Ltd (KSITIL)

Cherthalai, Alappuzha IT/ITeS

Infoparks, Kerala Kunnathunad, Ernakulam IT/ITeS

Cochin International Airport Ltd Ernakulam Airport based

Some of formally approved SEZs in Kerala

Kerala had 32 SEZs with formal approval and 25 notified SEZs.

JULY 2015

36 36 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

DEVELOPMENT PROJECTS: NATIONAL INVESTMENT AND MANUFACTURING ZONES (NIMZ)

NIMZ - National Investment and Manufacturing Zone, The Hindu

NIMZ • The Central Government has granted in-principle approval to the Kochi-Palakkad National

Investment and Manufacturing Zone (NIMZ) in 2013. • The NIMZ is proposed to be set up in an area of 6,000 acres across 20 identified nodes.

State-of-the-art infrastructure

• The state was exempted from the provisions related to geographical continuity in the National Investment and Manufacturing Zone.

• Other infrastructure facilities required to be created include internal roads, drainages, water treatment plants, and gas-based power plants for a total capacity of 2,500 MW.

• The cost of infrastructure development will exceed US$ 8.8 billion including the cost of land.

Opportunity • The opportunities available in these projects are industrial plots, export and import-related

opportunities, packaging services, logistic services, etc.

Total employment potential of around 0.5

million

• Kerala expects to generate direct employment for 0.5 million people in five years and indirect employment for 2.5 million people in 10 years.

JULY 2015

37 37

Educational infrastructure (2014-15)

Schools 12,626

Universities 16

Engineering institutions 161*

Arts and science colleges 197

Polytechnics 48

Kerala has the highest literacy rate among all states in the country. As of 2014-15, the state has a literacy rate of 94.6 per cent; male and female literacy rates stood at 96.67 per cent and 92.65 per cent, respectively. As of 2013-14, about 36.58 per cent of total students were enrolled in government schools, 56.61 per cent in government-aided private schools, and 6.81 per cent in unaided private schools. As of 2013-14, girl students accounted for around 49.47 per cent of total student enrolment in schools in the state. Kerala has 2,964 higher secondary schools as of 2015. Of these, 1,216 (41.02 per cent) were government schools, 1,210 (40.83 per cent) aided schools, and the remaining 538 (18.15 per cent) unaided schools.

For updated information, please visit www.ibef.org

SOCIAL INFRASTRUCTURE – EDUCATION … (1/3)

KERALA GOD'S OWN COUNTRY

Source: Economic Survey of Kerala, 2013-14 and 2014-15 *As of 2013-14

JULY 2015

38 38 For updated information, please visit www.ibef.org

SOCIAL INFRASTRUCTURE – EDUCATION … (2/3)

KERALA GOD'S OWN COUNTRY

Kerala primary education statistics (2014-15)

Schools (No)

Lower primary: 6,749

Upper primary: 2,913

High schools: 2,964

School dropout rate (%) (2013-14)

Lower primary: 0.60

Upper primary: 0.27

High school: 0.56

Pupil-teacher ratio 26:1

Nature of schools (2014-15)

Student strength (in million)

Share of total student strength (%)

Government 1.17 30.7

Government-aided 2.27 59.7

Unaided 0.35 9.21

Total 3.80 100.0

Source: Economic Survey of Kerala 2013-14 and 2014-15, News Articles

JULY 2015

39 39

Major medical colleges in Kerala - 2014

• Medical colleges: 25 • Dental colleges: 22 • Nursing colleges: 111 • Ayurveda medical colleges: 18 • Homeopathy medical colleges: 5 • Siddha: 2

Source: Economic Review of Kerala,2014-15 NHP India, Director of Technical Education, Kerala,

University Grants Commission

Kerala is home to premier institutions such as:

Indian Institute of Management, Kozhikode. Indian Institute of Space Science and Technology, Thiruvananthapuram. National Institute of Technology, Calicut. National University of Advanced Legal Studies, Kaloor. Central Institute of Fisheries Nautical and Engineering Training, Kochi. Central Institute of Fisheries Technology, Cochin. Central Marine Fisheries Research Institute, Ernakulam. Institute of Human Resource Development, Thiruvananthapuram. Besides, the medical council has received 13 proposals from Kerala.

For updated information, please visit www.ibef.org

SOCIAL INFRASTRUCTURE – EDUCATION … (3/3)

KERALA GOD'S OWN COUNTRY

Technical institutions under Directorate of Technical Education-2014

Institutions Numbers

Government technical high schools 39

Government commercial institutes 17

Tailoring and garment making training centres

42

Vocational training centres 4

JULY 2015

40 40

Source: Sample Registration System (SRS) Bulletin September 2014 Economic Review of Kerala, 2014-15

*Per thousand persons, **Per thousand live births

Health indicators as of 2014

Birth rate* 15.2

Death rate* 7.0

Infant mortality rate** 12

Life expectancy at birth (years)

Male 71.4

Female 76.3

Kerala has good health infrastructure with 681 primary health centres, 25 dispensaries and 233 community health centres. As of 2014, Kerala’s total healthcare institutions, 1,281 are Allopathic, three Ayurvedic and 661 under Homoeopathic. As of 2014, the 1,281 health institutions under the Allopathic segment contained 37,415 beds under the Health Services Department.

In 2015-16 budget, state government announced plans to invest US$ 110.37 million for the development of health sector.

For updated information, please visit www.ibef.org

SOCIAL INFRASTRUCTURE – HEALTH

KERALA GOD'S OWN COUNTRY

Health infrastructure as of 2014

• Primary health centres: 681 • Community health centres: 230 • Taluka hospitals: 79 • District Hospitals: 16 • General hospital: 18 • TB clinics/centres: 17 • Specialty: 20 • 24x7 PHC: 171 • Others: 49 • Total: 1,281

Source: Economic Review of Kerala, 2014-15

JULY 2015

State government of Kerala announced plans to invest US$ 0.89 million for the establishment of a cath Lab facilities in the district hospital, Kollam and the General hospitals of Ernakulam and Kozhikode. Government

41 41

Kerala has been rated as one of the Thirteen Paradises of the World by National Geographic Traveller; it has been promoted as ‘God’s Own Country’.

Health and wellness tourism in Ayurvedic medicine has grown tremendously in the past years.

Sri Padmanabhaswamy temple makes the state one of the attractive religious tourism spots in India.

Other temples in Kerala, such as Guruvayoor and Sabarimala, are also major religious attractions.

In June 2015, Kerala organised a road show in Shanghai and participated in Beijing International Tourism Expo (BITE) 2015. The BITE 2015 witnessed participation of 70 buyers from the Chinese travel and tourism industry. The main objective of the initiative was to strengthen the Spice Route heritage with other countries and promote sustainable tourism aimed at achieving world peace.

.

For updated information, please visit www.ibef.org

CULTURAL INFRASTRUCTURE … (1/2)

KERALA GOD'S OWN COUNTRY

Popular tourist locations

Beaches Kovalam, Varkala, Marari, Bekal and Kannur

Backwaters Kumarakom, Alappuzha, Kollam, Kochi and Kozhikode

Hill stations Ponmudi, Munnar, Wyanad and Vagamon

Wildlife reserves

Periyar Wildlife Sanctuary,

Eraviikulam National Park,

Thattekad Bird Sanctuary

Parambikulam Wildlife Sanctuary

Source: Department of Tourism, Government of Kerala, News Articles, Economic Review of Kerala 2014-15

JULY 2015

42 42

Art and culture are being fostered and promoted through various bodies such as:

Kerala Sahitya Academy – To promote Malayalam literature. Kerala Sangeetha Nataka Akademi – To promote traditional arts. Kerala Lalithkala Academy – To promote painters and sculptors. Kerala Folklore Academy – To promote Kerala folklore. Kerala State Chalachitra Academy – Academy for motion pictures. Kerala Kalamandalam – To teach traditional dances.

The cities in Kerala have modern amenities for recreation such as golf courses, shopping malls, theatres, café-lounges and resto-bars. Kerala got 25 new sports facilities owing to the National Games held at the start of 2015.

For updated information, please visit www.ibef.org

CULTURAL INFRASTRUCTURE … (2/2)

KERALA GOD'S OWN COUNTRY

New sports infrastructure projects in Kerala

New hockey stadium at Kollam

Rajiv Gandhi Indoor Stadium, Kochi

Shooting range at Vattiyoorkkavu, Thiruvananthapuarm

Corporation Stadium, Kollam

V.K.N. Indoor Hall, Thrissur

VKK Menon Stadium, Kozhikode

CSN Stadium, Thiruvananthapuram

New football stadium at medical college ground, Kozhikkode

New multipurpose hall, Kannur

Kariavattom main stadium, Thiruvananathapuam

Synthetic Athletic track at University of Calicut, Malapuram (Approved under Urban Sports Infrastructure Scheme (USIS))

Source: Department of Tourism, Government of Kerala, Economic Review of Kerala 2012, News articles

JULY 2015

43 43

The state has 32 SEZs with formal approvals and 25 notified SEZs. A cyber-park spread over a 68 acre campus is being developed in Kozhikode.

For updated information, please visit www.ibef.org

INDUSTRIAL INFRASTRUCTURE … (1/3)

KERALA GOD'S OWN COUNTRY

Source: http://www.technopark.org/

Infrastructure Project description

Technopark

• The Technopark at Thiruvananthapuram is spread over 760 acres. • It currently hosts over 300 IT and ITeS companies, employing over 46,000 IT professionals. • Technopark Phase-II has been declared an SEZ by the Government of India. • The technology park is spread across 7.2 million sq ft built-up space (completed) and 3.5 million

sq ft (work-in-progress) • As a part of the Phase-IV, named Technocity, Technopark is developing 431 acres of land in

Pallippuram, 5 km north of the main campus on the National Highway-47 to Kollam.

Infopark

• The Infopark at Kochi is best suited for ITeS due to its proximity to the submarine optical-cable landings.

• The total land available with Infopark is 98.25 acres, of which 75 acres has been notified as an SEZ by the Ministry of Commerce, Government of India.

Special Economic Zones

• Apart from the SEZs in Technopark and Infopark, the other SEZs in Kerala include the KINFRA Electronics Park SEZ in Kalamassery; a multi-product SEZ at Kochi; two port-based SEZs at Vallarpadam and Puthuvypeen at Kochi; a food processing SEZ near Calicut; a pulp and paper SEZ at Kottayam; and a non-conventional energy sources SEZ at Kalamassery.

JULY 2015

44 44 For updated information, please visit www.ibef.org

INDUSTRIAL INFRASTRUCTURE – INDUSTRIAL CLUSTERS … (2/3)

KERALA GOD'S OWN COUNTRY

Symbol Industries

IT

Engineering

Minerals and mining

Handlooms and power looms

Textile

Tiles

Canning

Coir products

Agriculture and forest-based

Sericulture

Rubber

Food products

Beedi

JULY 2015

45 45 For updated information, please visit www.ibef.org

INDUSTRIAL INFRASTRUCTURE – INDUSTRIAL CLUSTERS … (3/3)

KERALA GOD'S OWN COUNTRY

District Industries

Kannur Handlooms, power looms, beedi

Alappuzha Coir products

Idukki Agriculture and forest based

Thiruvananthapuram Handlooms, IT

Thrissur Power looms, handlooms, textile, timber, tile, canning

Palakkad Power looms, sericulture

Kollam Minerals and mining

Kozhikode Rubber

Wayanad Minerals and mining

Kasargod Minerals and mining

Kottayam Rubber, food products, engineering

Ernakulam IT

JULY 2015

46 46 For updated information, please visit www.ibef.org

As of June 2015, seven cities of the state have been earmarked to be developed as a smart cities.

In 2015, along with the smart cities, 18 cities of Kerala have also been selected for infrastructure development. The infrastructure development will be done under the Atal Mission for Rejuvenation and Urban Transformation (AMRUT) scheme. Under this scheme, the central government has approved an investment of US$ 8.3 billion for the first phase.

SMART CITIES

KERALA GOD'S OWN COUNTRY

Proposed Smart Cities in Kerala

Cities Population Area (Sq Km) Literacy Rate

Cochin 2,117,990 600 97.50%

Ernakulam 3,282,388 3063 95.89%

Kollam 2,635,375 2483 94.09%

Kottayam 1,974,551 2206 97.21%

Thiruvananthapuram 3,301,427 2189 93.02%

Thrissur 3,121,200 3027 95.08%

Tiruvalla 223,503 164.62 97.64%

Source: TechSci Research

Thiruvananthapuram

Kollam

Ernakulam

Thrissur

Kochin

Tiruvalla

47 47

Kerala’s strategic location on the trans-national trade corridor, rich natural resources, and simple and transparent procedures are favourably suited for investments in key sectors such as tourism, IT/ITeS, manufacturing and mining.

Kerala’s traditional industries include handloom, cashew, coir and handicrafts.

KINFRA, KITCO Limited (formerly, Kerala Industrial and Technical Consultancy Organisation Limited), the Directorate of Industries and Commerce, and the Small Industries Development Corporation are jointly responsible for the development of industrial infrastructure in the state.

Forming industrial clusters and developing infrastructure (such as rubber parks, electronic hardware park, coconut industrial park, organic industrial park and food processing parks) have been integral to the state’s strategies to attract investments in various industries.

The total number of functional micro, small and medium enterprises (both registered and unregistered) in Kerala stood at 159,450 and 2,192,969, respectively, as of March 2014. These units employed a total of 5,274,606 people (660,123 employed under registered sector and 4,614,483 employed under unregistered sector).

The total number of SSIs/MSMEs registered in Kerala by the end of March 2014 stood at 234,251 against 219,444 in the previous year, indicating a growth of about 6.3 per cent.

For updated information, please visit www.ibef.org

KEY INDUSTRIES

KERALA GOD'S OWN COUNTRY

Key industries in Kerala

• Handlooms and power looms

• Rubber

• Bamboo

• Coir

• Khadi and village industry

• Sericulture

• Seafood and other marine products

• Cashew

• Mining

• Tourism

• Food processing

• Spices and spice extracts

• IT & electronics

In terms of industrial growth, the state’s average growth from 2004-05 to 2012-13 was 14 per cent at current prices

SME’s generated more than US$16 million worth of orders from B2B meet held in February 2015 in Kochi.

Source: Economic Review of Kerala, 2014-15, News articles

JULY 2015

48 48

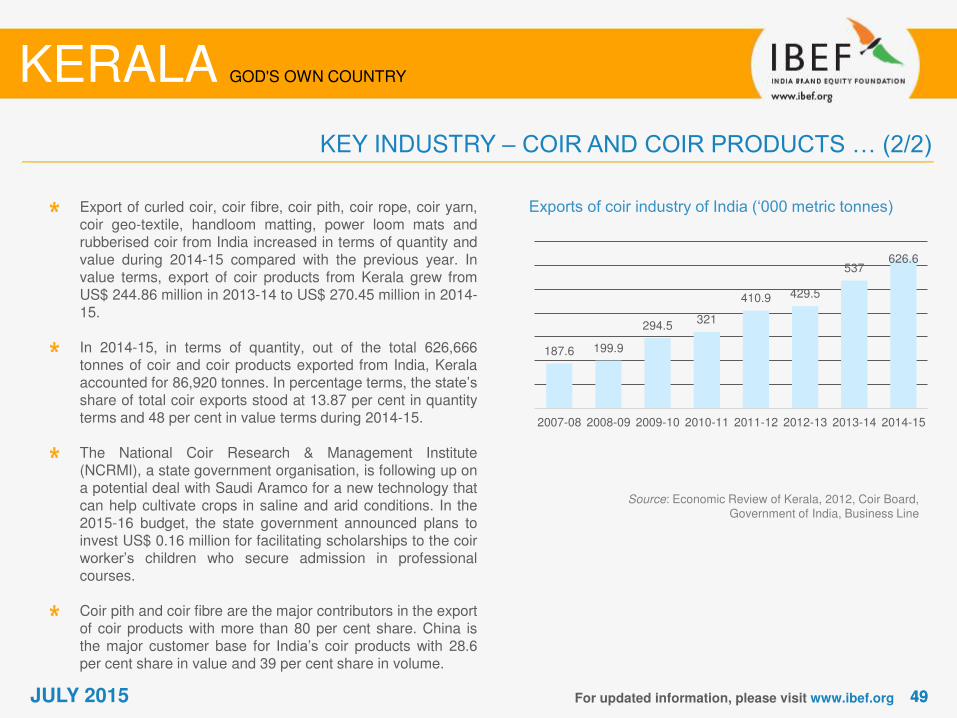

As of 2014-15, Kerala accounts for approximately 51.7 per cent (in terms of value) and about 84.8 per cent (in terms of volume) of total coir and coir products produced in India.

The coir industry provides employment to around 375,000 people.

The state has three coir parks: two in Alappuzha and one in Perumon (Kollam).

The Coir Co-operative Marketing Federation (COIRFED) is the apex federation of 842 primary coir co-operatives societies.

The US is the largest importer of coir products from India, followed by the Netherlands, the UK, Germany, Italy and Spain.

The Coir Kerala trade fair held in February 2015 witnessed the participation of around 170 foreign buyers from over 53 countries.

As per Budget 2015-16, an amount of US$ 19.5 million has been allocated for the development of the coir sector.

In the 2015-16 budget, Government has allocated a budget of US$ 0.16 million to provide scholarships to the children of coir workers.

For updated information, please visit www.ibef.org

KEY INDUSTRY – COIR AND COIR PRODUCTS … (1/2)

KERALA GOD'S OWN COUNTRY

Source: Economic Review of Kerala, 2014-15, Government of Kerala, Coir Board, News articles

JULY 2015

49 49 For updated information, please visit www.ibef.org

KEY INDUSTRY – COIR AND COIR PRODUCTS … (2/2)

KERALA GOD'S OWN COUNTRY

Export of curled coir, coir fibre, coir pith, coir rope, coir yarn, coir geo-textile, handloom matting, power loom mats and rubberised coir from India increased in terms of quantity and value during 2014-15 compared with the previous year. In value terms, export of coir products from Kerala grew from US$ 244.86 million in 2013-14 to US$ 270.45 million in 2014-15. In 2014-15, in terms of quantity, out of the total 626,666 tonnes of coir and coir products exported from India, Kerala accounted for 86,920 tonnes. In percentage terms, the state’s share of total coir exports stood at 13.87 per cent in quantity terms and 48 per cent in value terms during 2014-15. The National Coir Research & Management Institute (NCRMI), a state government organisation, is following up on a potential deal with Saudi Aramco for a new technology that can help cultivate crops in saline and arid conditions. In the 2015-16 budget, the state government announced plans to invest US$ 0.16 million for facilitating scholarships to the coir worker’s children who secure admission in professional courses. Coir pith and coir fibre are the major contributors in the export of coir products with more than 80 per cent share. China is the major customer base for India’s coir products with 28.6 per cent share in value and 39 per cent share in volume.

Source: Economic Review of Kerala, 2012, Coir Board, Government of India, Business Line

Exports of coir industry of India (‘000 metric tonnes)

JULY 2015

187.6 199.9

294.5 321

410.9 429.5

537 626.6

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

50 50 For updated information, please visit www.ibef.org

KEY INDUSTRIES – HANDLOOM AND POWER LOOM

KERALA GOD'S OWN COUNTRY

Source: Economic Review of Kerala, 2014-15 Kerala State Handloom Development Corporation Ltd

Among the traditional industries of Kerala, the handloom sector stands second to the coir sector in providing employment. The industry is concentrated in Thiruvananthapuram and Kannur districts and in some parts of Kozhikode, Palakkad, Thrissur, Ernakulam, Kollam and Kasaragod districts. Around 94.0 per cent of the total number of looms are under the cooperative sector (consists of factory type and cottage type societies), the remaining being under industrial entrepreneurs. During 2013-14, the state government approved an investment of US$ 2.63 million to the handloom sector, whereas the central government and the financial institution group (NCDC, NABARD & HUDCO) approved investments of US$ 0.07 million and US$ 0.2 million, respectively for the same period of time. At the end of March 2014, Kerala accounted for 705 registered Primary Handloom Weavers Co-operative Societies (PHWCS), consisting of 171 factory type societies and 534 cottage type societies. Kerala’s four integrated power loom co-operative societies in Calicut, Wayanad, Neyyattinkara and Kottayam have been expanded by providing budgetary support. The Calicut Integrated Powerloom Co-operative Society Ltd has been converted into a textile park comprising all the segments of a composite mill (weaving, processing and garment making). At the society, semi-automatic power looms, automatic looms and highly sophisticated machines are operational. The total value of handloom production in the state was US$ 35.09 million in 2013-14. The total number of weavers employed in the state was 21,230 in 2013-14. The number of women employed has also decreased from 21,434 in 2012-13 to 13,061 in 2013-14. Total employment generated decreased from 10.58 million man days in 2012-13 to 9.2 million man days in 2013-14.

JULY 2015

51 51

Kochi has emerged as a unique IT destination and is connected by two submarine cables and satellite gateways that directly support major IT cities, including Bengaluru.

The annual plan outlay for information technology during 2013-14 is 34.4 per cent higher than that for 2012-13. According to 2015-16 Annual Plan, an investment of US$ 66,000 was announced for application of information technology.

Kerala possesses a cost-effective and highly skilled human resource base with the lowest attrition rate (less than 5 per cent).

The state has a techno park in Thiruvananthapuram, an info park in Kochi, and a cyber park in Kozhikode. It also has private IT parks such as Smart City (Kochi), L&T Park (Kochi), Leela Info Park (Thiruvananthapuram), Brigade Park (Kochi) and Muthoot Pappachan Techno Polis (Kochi).

In 2007-08, the state’s software exports from registered units through Software Technology Parks of India (STPI) were valued at US$ 298.3 million that reached US$ 626.5 million by 2014-15.

As of 2014-15, Kerala has seven operational IT/ITeS SEZs. Out of the seven IT/ITeS SEZs, three are operational and located at Kochi (one) and Thiruvananthapuram (two).

The IT industry of the state is growing at a higher pace. Leading IT companies such as TCS, Infosys and UST are providing job opportunities and the industry is expected to add 23,500 new jobs by 2017 .

For updated information, please visit www.ibef.org

KEY INDUSTRIES – IT … (1/3)

KERALA GOD'S OWN COUNTRY

Source: Kerala IT Policy 2012, Economic Review of Kerala 2012-13 and 2014-15 State Annual Plan

News articles

JULY 2015

52 52

298.3 392.7 412.6 454.6 413.4

644.4 676.6 626.5

20

07-0

8

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

20

14-1

5

For updated information, please visit www.ibef.org

KEY INDUSTRIES – IT … (2/3)

KERALA GOD'S OWN COUNTRY

IT exports from Kerala increased at a CAGR of 11.2 per cent between 2007-08 and 2014-15.

Operational costs in the state are among the lowest in India (40 per cent lower as compared to other major IT locations in India). Also, rental/real estate costs are lower than major IT cities in the country.

Around 11 per cent of the national IT pool is contributed by skilled human resources from Kerala.

Kerala has a strong e-governance infrastructure and is a leading state in e-governance.

State government is planning to provide job opportunities to 0.5 million people in IT sector by 2020.

Kochi Info Park registered IT exports worth US$ 391 million in 2013-14 that reached US$ 375.8 million in 2014-15.

Source: Kerala IT Policy 2012, Economic survey of Kerala, 2014-15, News articles

Software Technology Parks of India

Exports from IT industry (US$ million)

CAGR 11.2%

JULY 2015

53 53 For updated information, please visit www.ibef.org

KEY INDUSTRIES – IT … (3/3)

KERALA GOD'S OWN COUNTRY

Tata Consultancy Services

Infosys

Collabera

RR Donnelley India Outsource Pvt Ltd

• Tata Consultancy Services (TCS) is among the largest providers of IT and Business Process Outsourcing (BPO) services in India. TCS employed more than 300,000 IT consultants in 46 countries and generated revenue of US$ 12.2 billion in FY’15.

• TCS provides IT consulting and services in financial services, healthcare and life sciences, insurance, manufacturing, media, entertainment, transportation etc. It has a software development and training centre at Technopark in Thiruvananthapuram and plans to set up the world’s largest corporate learning centre in Thiruvananthapuram.

• Established in 1981, Infosys employs more than 160,000 people. The company generated US$ 7.8 billion in revenue in FY’15. It is engaged in IT consulting, modular global sourcing, process re-engineering, and BPO services.

• The company has operations in Australia, China and the US, and marketing and technological alliances with Informatica, IBM, HP, Microsoft, Oracle, etc. Infosys has offices in 30 countries and development centres in India, China, Australia, the UK, Canada, Japan, etc. It has a centre at Technopark, Thiruvananthapuram.

• Collabera is a fast-growing, end-to-end information technology services and solutions provider, working with leading global 2,000 organisations from banking & financial services, communications, media, manufacturing, retail, energy and utilities domains. The company employs over 9,000 professionals across more than 25 offices and four world-class delivery centres in the US, the UK, India, Singapore and Philippines. The company has an office at Technopark, Thiruvananthapuram. In 2014, it generated US$ 500 million in revenue.

• Founded in 1995, RR Donnelley Global BPO has 7,700 employees in 28 delivery and 41 onsite operation centres across nine countries and had a revenue of US$ 11.6 billion in 2014.

• It is a subsidiary of RR Donnelley (RRD), a global provider of integrated communications, business services and supply chain solutions. RR Donnelley is a US$ 11 billion Fortune 300 company, with around 65,000 employees across the world. The company has an office at Technopark, Thiruvananthapuram.

JULY 2015 Source: Company website and annual report

54 54 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

KEY INDUSTRIES – ELECTRONICS … (1/2)

The self contained Electronics Technology Park at Technopark, Thiruvananthapuram, has been instrumental in attracting global electronics manufacturers. The state has ample availability of skilled and semi-skilled workers for the electronics industry. The electronic hub proposed at Kochi is a prestigious project of the Government of Kerala to promote electronic hardware manufacturing and assembling units and R&D centres, and to support infrastructure for the same. This hub is a high-priority area, which would promote a large number of small-, medium- and large-scale industries in the state. It would also form a National Investment & Manufacturing Zone (NIMZ) for manufacturing electronic hardware items. In November 2012, Hindustan Aeronautics Limited has set up phase-I of an electronics factory at the cost of US$ 12.1 million at Kasaragod to manufacture advanced avionics for aircraft and helicopters. This factory enhanced the growth of subsidiary industries, which in turn generating secondary employment opportunities and augment skill-sets in this area.

Key players

• Traco Cable Company Limited

• Transformers and Electricals Kerala Ltd (TELK)

• Kerala State Electronics Development Corporation Ltd (Keltron)

Source: Economic Review of Kerala, 2014-15 Government of Kerala

KSDIC: Kerala State Industrial Development Corporation News Article

JULY 2015

In 2013-14, KSIDC developed Electronic Hardware Park which is a manufacturing and Research & Development (R&D) facility based in Kochi. As per the Budget 2015-16, the tax rate on government notified electronic goods and systems which is meant for defence purposes has been reduced to 5%.

55 55 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

KEY INDUSTRIES – ELECTRONICS … (2/2)

Traco Cable Co Ltd

Transformers and Electricals Kerala Ltd

(TELK)

Kerala State Electronics Development Corp

(Keltron)

• Traco Cable Company Limited commenced operations in 1964. It manufactures high-quality cables and wires in technical collaboration with Kelesey Engineering Co Ltd, Canada. TRACO currently meets the needs of public sector undertakings in India such as railways and the electricity boards of various states. The company is headquartered in Kochi and has factories in Ernakulam, Kannur and Thiruvalla.

• TELK was incorporated in 1963 under an agreement with the Government of Kerala, Kerala State Industrial Development Corporation, and Hitachi Limited, Japan. It manufactures transformers, bushings and tap changing gears. The factory and corporate office are located in Angamally, near Kochi. In 2012. TELK won the Kerala Safety Award for very large factories in the engineering category.

• TELK provided its first 400 KV Class Transformer, 315 MVA Auto Transformer and Generator Transformer to India's first 500 MW Thermal Unit.

• Founded in 1973, Keltron is a state-owned electronics enterprise, employing around 1,800 people and has 10 manufacturing centres. It provides technical manpower to leading organisations such as Oil and Natural Gas Corporation Limited (ONGC). The company’s products span categories including aerospace electronics, security and surveillance systems, intelligent transportation systems, strategic electronics products, IT solutions, IT infrastructure solutions, process automation, ID card projects, power electronics, electronic components and TE units.

• Keltron is headquartered in Thiruvananthapuram and has training centres in 30 locations across Kerala with a strong infrastructure spread over 700,000 sq ft of built up area.

JULY 2015

Source: Company website and annual report

56 56 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

KEY INDUSTRIES – TOURISM … (1/2)

The tourism sector of Kerala is a significant contributor to the state economy. As of 2014-15, revenue from the tourism sector accounted for 9.84 per cent share of the state’s GDP. Total revenue (including direct and indirect) from tourism surged by about 12.11 per cent to US$ 4,106.5 million in 2014. In 2015, Kerala was awarded as the winner of PATA awards by Macau Government Tourism Office (MGTO). Kerala Tourism bagged four of the top honours at the Pacific Asia Travel Association (PATA) Awards 2011, announced in Bangkok, for outstanding achievement in tourism. In 2013, a survey conducted by BBC World News has rated Kerala as the most popular tourist in India spot among foreign travellers. Kerala Tourism has won many national and international awards. The state has been voted the Best Asian Holiday Destination 2010 by SmartTravelAsia.com, ahead of other destinations such as Bali, Phuket and Maldives. Popular tourist destinations in Kerala include beaches of Kovalam, Varkala, Marari, Bekal and Kannur; backwaters of Kumarakom, Alappuzha, Kollam, Kochi and Kozhikode; and hill stations of Ponmudi, Munnar, Wayanad and Wagamon. Kerala has a number of well-known wildlife reserves, including the Periyar Wildlife Sanctuary, the Eravikulam National Park, the Thattekkad Bird Sanctuary and the Parambikulam Wildlife Sanctuary. The State Tourism Department is developing eco-friendly, rural tourism packages in Kumarakom, Wayanad, Kovalam and Muziris heritage circuit. Kerala accounted for 4.8 per cent of total foreign tourist visitors in the country in 2014.

Source: Economic Review of Kerala, 2014-15, www.keralatourism.org, News articles

JULY 2015

57 57

KERALA GOD'S OWN COUNTRY

KEY INDUSTRIES – TOURISM … (2/2)

Source: Economic Survey 2014-15 The Hindu, www.keralatourism.org, Ministry of Tourism, Government of India

Arrivals of domestic and foreign tourists in Kerala increased at a CAGR of 8.0 per cent and 10.4 per cent, respectively, over 2009-2014.

Major initiatives of Kerala Tourism - 12th FYP:

An investment of US$ 0.67 million was announced for Kerala waste free destination scheme. Ab investment of US$ 2.47 million was announced for the promotion and marketing activity of Kerala tourism sector. For the sea plane project, an investment of US$ 1 million was announced. For the strengthening and modernisation of tourism institutions an investment of US$ 0.24 million was announced.

Domestic tourist arrivals in Kerala (in million)

Foreign tourist arrivals in Kerala (in million)

For updated information, please visit www.ibef.org JULY 2015

7.9 8.6

9.4 10.1

10.9 11.6

2009 2010 2011 2012 2013 2014

0.56 0.66

0.73 0.79

0.86 0.92

2009 2010 2011 2012 2013 2014

58 58 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

KEY INDUSTRIES – RUBBER INDUSTRY

Source: Economic Review of Kerala, 2014-15, Rubber Board, Ministry of Commerce and Industry, Government of India Kerala State Co-operative Rubber Marketing Federation, Kerala farmer Online JV = Joint Venture, MT = Metric Tonnes

Kerala is the leader in rubber production in the country. State accounted for about 69% share in the total rubber production and also holds a cultivation area of 5.45 lakh hectares.

Natural rubber production in Kerala was 774.0 thousand MT during 2013-14, a 7.6 per cent increase over 2012-13. The production witnessed a decline during 2014-15 and stood at 655 thousand metric tons.

In the 2015-16 budget, state government of Kerala announced that rubber wood would be totally exempted from tax.

KINFRA, through a JV with the Rubber Board, has developed India’s first rubber park in Kochi. Kerala also has a major rubber cluster in Kottayam.

As per Budget 2015-16, Government announced plans to invest US$ 3.3 million for the expansion of the rubber industry in Kerala. The government is also offering an exemption on taxes, which is applicable on the purchase of rubber in the state.

Exports of natural rubber from India (000’ tonnes)

Consumption of natural rubber in India (000’ tonnes)

JULY 2015

25.1 29.9

27.1 30.6 30.6

51.8

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

947.7 964.4 972.7 981.5

771.5

2010-11 2011-12 2012-13 2013-14 2014-15

59 59

Kerala can be termed as the land of spices, considering the large variety of spices grown in the state. Kerala is the largest producer of pepper in India and accounts for about 76 per cent share in India’s production.

In 2013-14, the state witnessed pepper production of 29,408 tonnes whereas the area under pepper cultivation was recorded as 84,065 hectares. Global pepper production has dropped drastically, which led to increase in pepper prices. In line with the global trend, the price surge has been sharp in India considering the substantial domestic consumption compared with other pepper producing countries.

Apart from pepper, other spices produced in the state include ginger, cardamom, nutmeg, tamarind, etc. Spices exports from Kerala (through Cochin and Thiruvananthapuram ports) surged at a CAGR of 7.78 per cent between 2007-08 and 2014-15.

For updated information, please visit www.ibef.org

KEY INDUSTRIES – SPICES…(1/2)

KERALA GOD'S OWN COUNTRY

Exports of spices from Kerala (through Cochin and Thiruvananthapuram ports) in US$ million

Source: Economic Review of Kerala, 2014-15, News articles, Government of Kerala, Horticulture 2014-15

JULY 2015

314.1 320.4 307.3 413.7

667.6

467.1 542.2 530.08

20

07-0

8

20

08-0

9

20

09-1

0

20

10-1

1

20

11-1

2

20

12-1

3

20

13-1

4

20

14-1

5

As per Budget 2015-16, an investment of US$ 3.3 million is planned by the government to boost the spices cultivation in the state.

CAGR 7.78%

60 60

As of 2013-14, the overall exports of spices from India was recorded as 8,17,250 tons that reached 8,93,920 tons in 2014-15, with Kerala being the major contributor. In terms of value, pepper exports from Cochin port were recorded at US$ 183.6 million during 2014-15. For the same period of time, the export values of cardamom, nutmeg, ginger and turmeric were recorded as US$ 20.56 million, US$ 16.30 million, US$ 7.93 million and US$ 7.57 million respectively.

For updated information, please visit www.ibef.org

KEY INDUSTRIES – SPICES…(2/2)

KERALA GOD'S OWN COUNTRY

Source: Economic Review of Kerala, 2014-15, News Articles

JULY 2015

Volume of exports through Cochin Port (tons)

Spices 2013-14 2014-15

Ginger 2,125.3 1,750.8

Cardamom 858.3 1,607.7

Chilies 4,425.3 5,565.4

Nutmeg 1,822.9 1,997.9

Pepper 15,978.7 16,203.6

Turmeric 3,607.7 4,444.6

61 61 For updated information, please visit www.ibef.org

KERALA GOD'S OWN COUNTRY

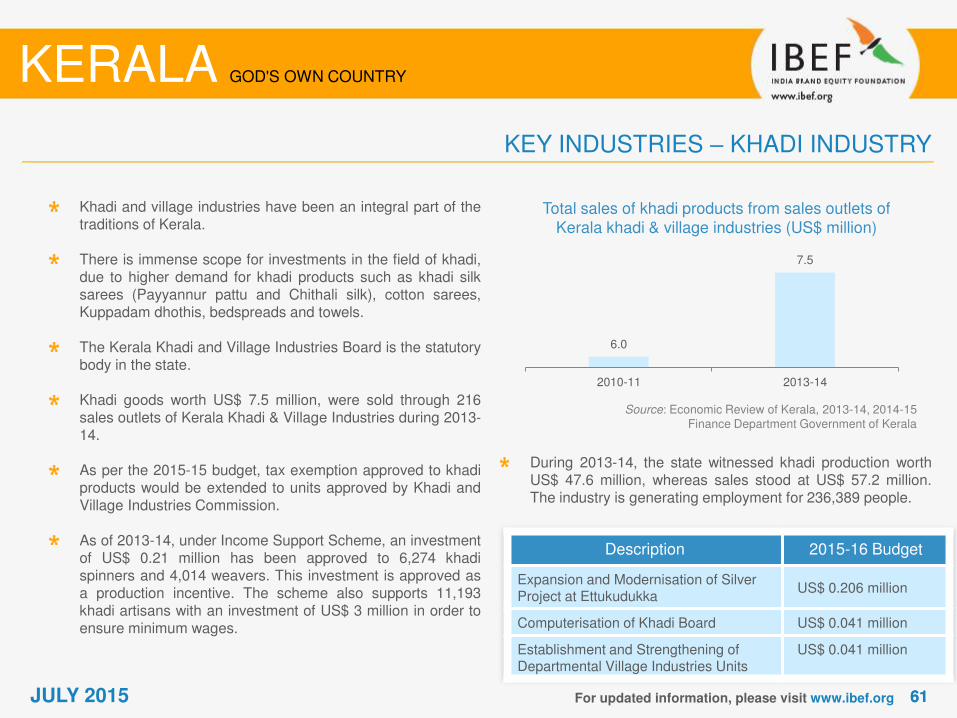

KEY INDUSTRIES – KHADI INDUSTRY

Khadi and village industries have been an integral part of the traditions of Kerala. There is immense scope for investments in the field of khadi, due to higher demand for khadi products such as khadi silk sarees (Payyannur pattu and Chithali silk), cotton sarees, Kuppadam dhothis, bedspreads and towels. The Kerala Khadi and Village Industries Board is the statutory body in the state. Khadi goods worth US$ 7.5 million, were sold through 216 sales outlets of Kerala Khadi & Village Industries during 2013-14. As per the 2015-15 budget, tax exemption approved to khadi products would be extended to units approved by Khadi and Village Industries Commission.