kenya teachers’ saccos association … · 3.2 independent electricity production in kenya ......

TRANSCRIPT

KENYA TEACHERS’ SACCOS ASSOCIATION

COPRORATE STRATEGIC PLAN 2017-2021

TABLE OF CONTENTS

1 INTRODUCTION ...................................................................................................................... 3

2 PURPOSE OF THE STRATEGIC PLAN ...................................................................................... 3

3 CONTEXTUAL FRAMEWORK .................................................................................................. 6

3.1 REAL ESTATE VALUE CHAIN AND STAKEHOLDER MAPPING ..................................... 12

3.2 INDEPENDENT ELECTRICITY PRODUCTION IN KENYA ................................................ 15

4 ORGANIZATIONAL CAPACITY ASSESSMENT ..................................................................... 18

5 KEY BUSINESS DRIVERS & RESULT AREAS ............................................................................ 20

6 STRATEGIC PLAN DELIVERY ................................................................................................. 20

7 IMPLEMENTATION PLAN ...................................................................................................... 22

8 MONITORING, EVALUATION, RESEARCH, & LEARNING FRAMEWORK........................... 30

9 STRATEGY PLANNING TEAM ................................................................................................ 32

1 INTRODUCTION

The Kenya Teachers’ Sacco’s Association was registered in 2012 to provide a

collaborative forum for sharing and learning from one another, as well as addressing

operating challenges of the primary member SACCOs. KETSA also provides common

investment opportunities geared towards improving their general welfare. KETSA

membership currently comprises 12 Teachers’ Saccos in Kenya, with the possibility of

growing outreach to more SACCOS. The current membership includes the following;

1. New Fortis Sacco Society Ltd

2. Mentor Sacco Society Ltd

3. Tower Sacco Society Ltd

4. Solution Sacco Society Ltd

5. WinasSacco Society Ltd

6. TransnationalSacco Society Ltd

7. CosmopolitanSacco Society Ltd

8. OllinSacco Society Ltd

9. IdealSacco Society Ltd

10. Kitui Teachers Sacco Society Ltd

11. XXX

The board of directors is drawn from all the 12 founding Saccos with the respective CEOs

of each Sacco playing the role of the technical team.

2 PURPOSE OF THE STRATEGIC PLAN

To date, KETSA does not have a dedicated secretariat and activities have centered

around advocating for favorable legislative and operating framework, knowledge

sharing and learning, and mobilizing monthly share capital contribution. KETSA has seen

if fit to harness and consolidate the gains made so far by structuring its operations with a

clear Vision and Mission.

At a 2 day, strategic planning workshop, board members, delegates and the technical

team comprising Sacco Chief ExecutiveOfficers, KETSA brainstormed on the future look

of the association, defined its Vision, Mission, Values and Key Business Drivers using a

participatory approach to co learning and creation which entails bringing on board the

diverse views and dreams of the board members and secretariat, while tapping into the

Consultant’s experience.

Vision Statement

‘To be the leading Association in Kenya championing Sacco growth’

Mission statement

‘To innovatively promote unity and social economic growth to Sacco fraternity through

advocacy, resource mobilization and investments, for maximum shareholders’ returns.’

Motto

‘Unity our strength’

Key Business Drivers

Members discussed at length the business activities that they wish to engage in in the

coming years as below. The preferred activities were then ranked in order of priority to

determine what they would focus on, by each member voting for their preferred and

priority business driver

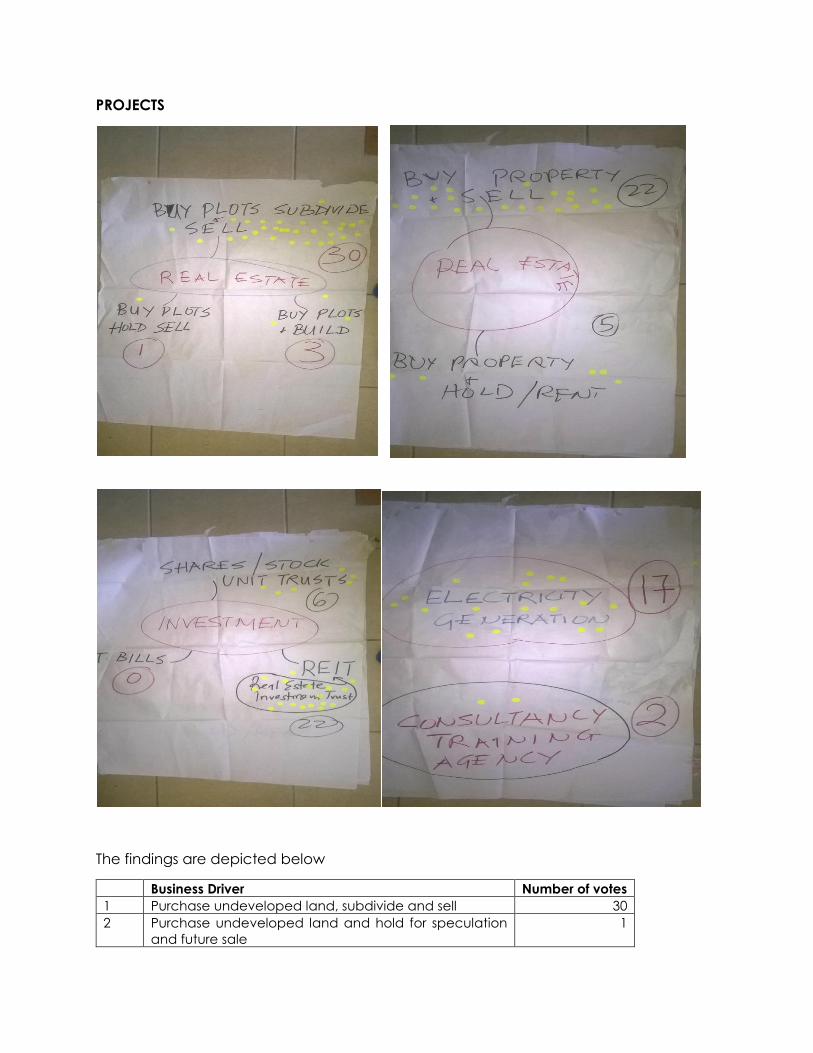

PROJECTS

The findings are depicted below

Business Driver Number of votes

1 Purchase undeveloped land, subdivide and sell 30

2 Purchase undeveloped land and hold for speculation

and future sale

1

3 Purchase undeveloped land and develop for sale 3

4 Purchase developed property and sell 22

5 Purchase developed property and manage for lease 5

5 Establish Consultancy, training, and Agent Banking unit 2

6 Generate electricity and sell to the grid 17

7 Investment inShares, Stocks, Unit Trusts 6

8 Investments in REITS 22

9 Investment in Government instruments 0

The members agreed to invest in the following projects in order of priority, # 1 given the

highest priority.

1. Purchase undeveloped land, subdivide and sell

2. Purchase developed property and sell

3. Generate electricity and sell to the grid

For investment of surpluses, idle, or funds held on behalf of members, KETSA will;

1. Investments in REITS (Real Estate Investment Trusts)

2. Investment in stocks and shares at the NSE

3 CONTEXTUAL FRAMEWORK

The State of Real Estate in Kenya

The current real estate and housing situation in Kenya can be traced back to the colonial

years. Until about 1939, the colonial government did not consider black Africans to be

permanent residents of the urban areas, nor did they encourage families to move to

urban areas. Employers and state agencies provided bed spaces for workers coming to

town. Local laws prohibited Africans from residing in European or white areas. They were

forced to live in “Native Locations”. After 1940, the permanent presence of Africans in

town was accepted, due to the workforce needed for the country’s growth.

Municipalities got the responsibility of providing housing for families and single men.

Several thousand units were built but very few were for families. Women and children had

no choice but to stay in the “bachelor” accommodation, which was basically single

rooms. That set the precedent for poor housing. Informal settlements started to be built.

The first housing response from the government after independence was to encourage

the private sector to build houses and to assist the public sector to expand their programs

through the National Housing Corporation (NHC). The first national housing policy was

formulated in 1966 in the Sessional Paper No. 5, which called on local authorities,

government departments and public corporations to implement their own programs to

supply rental housing. This was a time of centralized government initiatives and, during

the three decades from the 1950s through the 1970s, local authorities built several

subsidized rental housing units. After independence, local authorities were given the

power to implement the Graduated Personal Tax to secure their financial base, which

allowed them to pursue their housing initiatives. However, the tax was abolished in 1973

and never replaced, leaving local authorities with the responsibility of housing without

financial resources.

In the mid-1970s with funding from the International Monetary Fund (IMF) large-scale site

and service projects were implemented. These projects were low-cost housing for the

urban poor and provided full development, including servicing the lots; building the

roads and necessary infrastructure, housing units, sanitary facilities, community facilities;

providing loans for materials and technical assistance.

The actual number of houses constructed by both the private and public sectors was

disappointing compared to the increased need due to urbanization. Moreover, these

housing initiatives were too often not affordable for low-income earners, which meant

that informal settlements continued to grow. In the mid-1980s local authorities stopped

investing in rental housing.

The government’s administration began to be questioned in the late 1980s and early

1990s about human rights, economic performance and corruption. Both the population

and external funders asked for political reform, including the introduction of multi-party

democracy. Throughout the 1990s poverty grew, life expectancy declined, school

enrolment dropped, health services decreased and Kenya showed one of the highest

disparities between rich and poor.

During this period, several approaches were adopted by the government to respond to

the growing housing challenges. These initiatives involved partnerships with local

authorities, Community Based Organizations (CBO) and Non-Governmental

Organizations (NGO). Some initiatives were more successful than others and reached

poorer people. But lack of finances and political interference contributed to the failure

of many. The adoption in 2004 of the new National Housing Policy and KENSUP – the

Kenya Slum Upgrading Program brought hope, as the government made a commitment

to improve living conditions by 2020.

Housing co-operatives were introduced to Kenya in early 1980s. The National

Cooperative Housing Union (NACHU) was established by the Central Organization of

Trade Unions (COTU) which wanted to facilitate better housing for its members. NACHU

was limited in its activities. A restriction from the Commissioner of Cooperatives prevented

NACHU from generating income through general housing development services in

addition to its original mandate of housing co-operative development services. As with

the other cooperative sectors, NACHU’s activities were much under the control of the

government.

From the start, NACHU developed successful partnerships with external housing co-op

movements which aided in capacity building, housing development and community

delivery programs, and organizational support. This partnership is still strong today. The

co-op housing movement has grown in numbers due to the work of NACHU and its

partners.

Description

Key characteristics of the Kenyan Primary Housing Co-operatives (PHC) are:

a) Mostly urban; rural housing co-ops are linked to the agriculture marketing co-

operative sector;

b) The typical size of urban PHCs is 25-50 members;

c) Land is transferred for individual ownership upon full repayment of the loan;

d) Any member cannot hold more than one-fifth of the share capital as required by

the Act;

e) Development done incrementally i.e. land is acquired, services are installed and

houses are built room by room according the money saved and the financial

assistance (loans) available;

f) Development can also be done incrementally for larger buildings;

g) Members often build more rooms and sublet them to generate income;

h) Each member is responsible for taking care of his or her housing unit. NACHU is

considering ways to manage common services such as bore holes / water supply

and shared septic systems. Co-ops also play a role in managing savings collection

and loan repayment;

Some very large rural housing co-ops are saving, with NACHU’s help, for building

investment properties, typically a mix of residential and commercial properties in towns

or cities.

Key players in financing

Co-operatives interested in providing real estate opportunities to members are financed

by members’ savings and housing microfinance (HMF) loans from NACHU. Housing co-

ops have also access to loans from the Savings and Credit Co-operative Society

(SACCOs) they are associated with.

NACHU works with the Co-operative Bank of Kenya (Co-op Bank) on an external

guarantees model and leverages loans for Housing cooperatives on borrower deposits

Co-op Bank (20% of loan amount) is also lending funds for middle-income housing

development done by NACHU, development done as an income generating activity.

NACHU housing microfinance products include loans for new construction, housing

upgrading and expansion, land purchase and resettlement and, group loans for

commercial purpose and infrastructure. Several mechanisms and processes have been

put in place to protect the financial investment administered by NACHU. This includes

financial training provided to the participants in the savings scheme. NACHU savings and

loans scheme is proving to be quite successful to date – the portfolio at risk is within

industry standards. Based on this success, NACHU is attracting the interest of donors and

investors, which will assist NACHU to continue offering housing loans.

NACHU’s lending facility is financed from numerous sources including NACHU’s own

equity and member savings. Rooftops Canada has provided a guarantee and direct

lending facility totaling USD $500,000. Most recently, Homeless International, a UK

organization, has provided substantial funding for several projects through the

Community Led Infrastructure Finance Facility (CLIFF).

Legal framework

The legal instruments for the co-operative housing sector in Kenya are:

a) Cooperative Societies Act (Amended), 2004: guides the formation and operations

of housing co-operatives;

b) Rules and regulations issued: complement the Act;

c) Co-operative By-laws from NACHU: provides standard by-laws to new PHCs which

are readily accepted by the Department responsible for cooperatives;

d) Cooperative Tribunal: arbitrates disputes when the internal co-operative process

fails;

e) Code of Conduct and Ethics for Cooperative Societies: overseen and supervised

for compliance by the Ethics Commission for Cooperative Societies;

f) Land Bill 2012 – Land Registration Bill 2012 – Natural Land Commission Bill 2012;

g) Housing Act: provides for the effective coordination, facilitation, capacity building

and monitoring of the housing and human settlement sector. The Act also

establishes the Kenya Housing Authority and the National Social Housing and

Infrastructure Fund for the provision of housing and related purposes;

h) Local Government Act: deals with housing approvals in the relevant local

authorities;

i) Public Health Act: deals with the issues of sanitation and house occupation;

j) Physical Planning Act enacted in 1996, replaced the Town Planning Act (urban

areas) and the Land Planning Act (rural areas): provides for physical planning and

development control for both urban and rural areas;

k) Draft Eviction and Resettlement Guidelines, 2010

l) The National Construction Authority Act 2014- 0.5% of total cost of building for

properties with construction cost of over Ksh 5 million

m) Finance Act 2014- regarding 5% Capital Gains tax on sale of land, property etc.

n) National Environmental Management Authority NEMA

o) Capital Markets Authority under the Capital Markets Real Estate Investment Trusts,

Collective Investment Schemes Regulations 2013

Challenges

Kenya has faced major challenges in the housing sector but at the same time provided

opportunities for the same. The annual demand for housing is 200,000 urban units and

300,000 rural units. It is expected that the number of units needed over the next 10 years

will be 2.9 million, due to population growth and urbanization. By 2050, 50% of the

population will live in cities. The current annual production is 50,000 units.

Per the Ministry of Housing, 80% of the new houses built are for high-and middle-income

people, whereas 83% of the demand is coming from low-income families. 89% of the

urban population cannot afford a mortgage. In 2010, 50% of the urban households had

monthly incomes below $375. Very few rural people would be able to afford a mortgage.

However, there are challenges that come with real estate investment in Kenya. These

include

a) Expansive growth of slums and informal settlements

b) Distorted access to land, high cost of finance

c) Existence of rigid building laws and regulations

d) Deterioration of housing stock due to lack of a maintenance framework due to

the poor maintenance culture and both the public and residential buildings are

the most affected. To curb this, the ministry has finalized the maintenance policy

whereby all buildings are to be inspected in every 5 years.

e) Lack of affordable finance due to high interest rates and lending conditions that

do not respond to the needs of the population

f) The increasing cost of building materials;

g) The lack of affordable land

Opportunities

Access to both prime and virgin land for housing have provided a perfect opportunity

for investors in the sector. Some laws and regulations have undergone through a review

process to keep up with the best global practices and the ever-growing demand and

challenges.

Such laws include the Housing Policy 2004, Housing Act, and the Building Code. Also, the

current Housing Policy Sessional Paper #3 of 2004 has been reviewed. This helps in

reflecting on the government strategies of wholesomely addressing the challenges

faced by the housing sector.

Interested developers such as the World Bank, UN Habitat, SIDA, AFD and Shelter Afrique

have come on board to help settle the lack of adequate social infrastructure in the

housing sector. Their hard work bore fruits as there has been a rapid growth in the number

of schools, markets, roads, lighting programs, sewer lines and dwelling houses hence

changing the lives of many Kenyans.

Some financial factors have improved in the country, such as a stronger banking and

mortgage sector, and a well-developed microfinance sector.

The government has put in place some modest incentives relating to infrastructure

development, housing finance, and saving mobilization to assist in the production of the

new housing units.

The licensing of Real Estate Investment Trusts in 2015

Kenya has become the 4th African country to provide for trade in REITs after South Africa,

Ghana and Nigeria, with the Stanlib (Fahari-I) IPO (http://www.stanlib.com)in October

2015 and the planned Fusion Real Estate Development Trust planned for 2016

(http://fusioninvestafrica.com)

A REIT is a Real Estate Company which owns, develops, or manages different types of

properties. RElTs are investment instruments that source funds to build or acquire real

estate assets which they sell or rent to generate income. The income generated is

distributed to the shareholders at the end of a financial year. REITs are regulated by the

Capital Markets Authority (CMA) under the Capital Markets Real Investment T- Collective

Investment Schemes Regulations 2013.

RElTs are traded like stocks and investors can buy and sell shares. RElTs may choose to

focus on one main genre of real estate or may diversify to all types. One of the

advantages of Real Estate Investment Trusts is that they are exempted from double

taxation; REIT schemes are exempt from corporation tax and are also exempted from

income tax except for the payment of withholding tax on interest income and dividends.

How will REITS benefit the Real Estate Sector

The capital markets can help mobilize and allocate resources. REITS will enable

mobilizations of savings from individuals and groups. This means savings groups and co-

operatives will be able to invest in the market. Individuals can also get a stake in real

estate with investments of sums of as low as Ksh. 5,000 depending on the structure of the

REIT. REITS will provide a chance for developers to go the capital market to raise funds.

This may make financing developments competitive and thus reduce interest rates for

developments. It may also force banks to review their mortgage rates downwards. RElTs

will also allow Kenya’s capital markets to have a strong role in the further development

of the real estate sector. Specialized RElTs will be encouraged especially those involved

in the low and medium cost residential properties. This will allow for more development

of housing for this group which is under supplied.

3.1 REAL ESTATE VALUE CHAIN AND STAKEHOLDER MAPPING

Figure 1: Real Estate Value Chain Analysis

Questions

a. Who is a valuable stakeholder in the Value Chain?

b. Which resources do we need at each level? List them

c. What challenges are you experiencing in operations and project management at

each of these stages?

d. What are the possible solutions to your challenges?

The members deliberated on the Real Estate Value Chain and mapped critical

stakeholders, challenges in penetrating this market and possible solutions

Findings

OWNERSHIP

Stakeholder Resources Challenges Solutions

o Ministry of lands

o Advocates

o Lands board

o Family

o Community

o Finance

o Savings

o Loans

o Income

o Donations

o Brokers

o Fake

documentation

o High prices

o Bureaucracy

o Due diligence

o Involvement of

family

o Property

valuation by

•Builder/ owner

•Developers Ownership

•Self

•Investors

•Banks

•Mortgage Schemes

Finance

•Contracts

•Procurement/ Supply

•Construction Firms

•Who else?

Construction

•Brokers

•Construction Firms

•Who else?

Transaction

•Use case- residential/ commercial/ commercial resdiential

•Tenant / Long term/ Short terms

•Owners

Use

o Developer

o Merry go

round

o Human

resource

Research

o High taxation

o Access to

finance

o Succession

land issues

independent

bodies

o Use of collateral

for finance

access

o Compliance

FINANCE

Stakeholders Resources Challenges Solutions

o Individual member

Saccos

o Investors

o Sacco

savings

o Sacco loans

o Bank loans /

KUSSCO

o Investor

funding

o High loan

interest

Unsustainable

loans

o Lack of

member

commitment

o Lack of

collateral

o Enforce simple

but strict project

financing

policies

o Co ownership

and charge to

financier as

collateral

o Regular

member

information and

training

o Negotiated

financing –

KUSSCO, Saccos

CONSTRUCTION

Stakeholders Resources Challenges Solutions

o Government agencies

Professionals: planner,

civil engineer,

architect, water,

sewerage etc.

o Community

o Developer

o Contractors

o Manufacturers

o Suppliers

o Feasibility

studies for

every project

Finance

o Skilled labor

o Personnel

o Materials

o End to end

Project plan

o Equipment

o Delay in

approvals

Untrusted

engineers

o Over valuation

of BQs

o High

Management

fees

o Material

sourcing Site

Security

Timeliness

o Lack of

contingency

planning

o Weather

changes

o Fluctuating

prices

o Due diligence

and Open

tendering

procurement

process

o Tender

committee

Professionals

o Consultant

o Clerk of works

o Efficient

accurate

budgets

o Improve

capacity of the

board to

manage

projects

o Project

Insurance

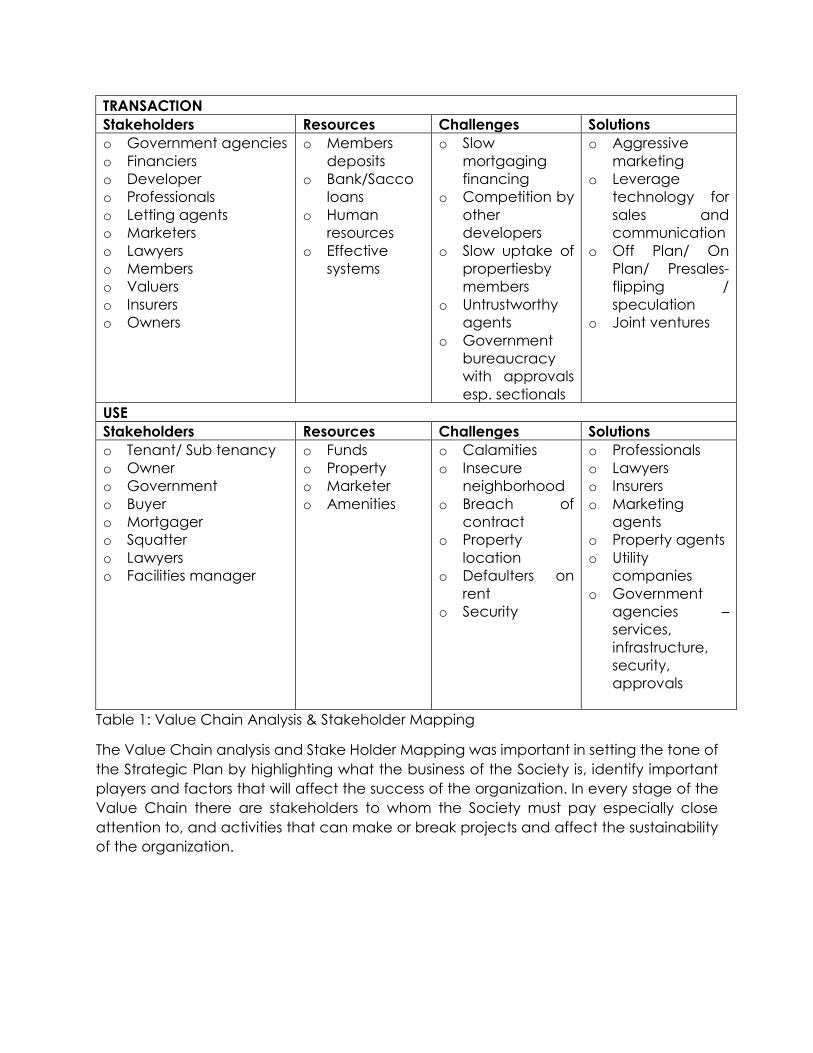

TRANSACTION

Stakeholders Resources Challenges Solutions

o Government agencies

o Financiers

o Developer

o Professionals

o Letting agents

o Marketers

o Lawyers

o Members

o Valuers

o Insurers

o Owners

o Members

deposits

o Bank/Sacco

loans

o Human

resources

o Effective

systems

o Slow

mortgaging

financing

o Competition by

other

developers

o Slow uptake of

propertiesby

members

o Untrustworthy

agents

o Government

bureaucracy

with approvals

esp. sectionals

o Aggressive

marketing

o Leverage

technology for

sales and

communication

o Off Plan/ On

Plan/ Presales-

flipping /

speculation

o Joint ventures

USE

Stakeholders Resources Challenges Solutions

o Tenant/ Sub tenancy

o Owner

o Government

o Buyer

o Mortgager

o Squatter

o Lawyers

o Facilities manager

o Funds

o Property

o Marketer

o Amenities

o Calamities

o Insecure

neighborhood

o Breach of

contract

o Property

location

o Defaulters on

rent

o Security

o Professionals

o Lawyers

o Insurers

o Marketing

agents

o Property agents

o Utility

companies

o Government

agencies –

services,

infrastructure,

security,

approvals

Table 1: Value Chain Analysis & Stakeholder Mapping

The Value Chain analysis and Stake Holder Mapping was important in setting the tone of

the Strategic Plan by highlighting what the business of the Society is, identify important

players and factors that will affect the success of the organization. In every stage of the

Value Chain there are stakeholders to whom the Society must pay especially close

attention to, and activities that can make or break projects and affect the sustainability

of the organization.

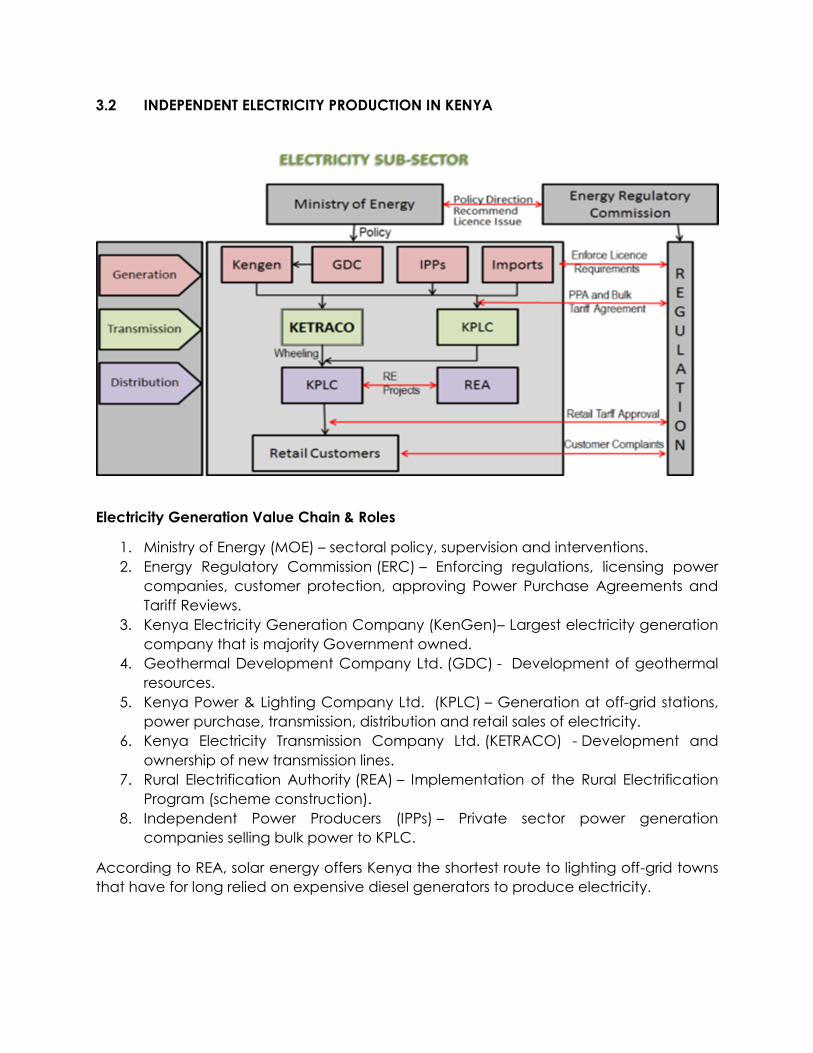

3.2 INDEPENDENT ELECTRICITY PRODUCTION IN KENYA

Electricity Generation Value Chain & Roles

1. Ministry of Energy (MOE) – sectoral policy, supervision and interventions.

2. Energy Regulatory Commission (ERC) – Enforcing regulations, licensing power

companies, customer protection, approving Power Purchase Agreements and

Tariff Reviews.

3. Kenya Electricity Generation Company (KenGen)– Largest electricity generation

company that is majority Government owned.

4. Geothermal Development Company Ltd. (GDC) - Development of geothermal

resources.

5. Kenya Power & Lighting Company Ltd. (KPLC) – Generation at off-grid stations,

power purchase, transmission, distribution and retail sales of electricity.

6. Kenya Electricity Transmission Company Ltd. (KETRACO) - Development and

ownership of new transmission lines.

7. Rural Electrification Authority (REA) – Implementation of the Rural Electrification

Program (scheme construction).

8. Independent Power Producers (IPPs) – Private sector power generation

companies selling bulk power to KPLC.

According to REA, solar energy offers Kenya the shortest route to lighting off-grid towns

that have for long relied on expensive diesel generators to produce electricity.

Kenya has more than 300 days of sunshine per year, double Germany’s — which is the

global leader in solar energy production with an installed capacity of more than 40,000

megawatts.

Kenya’s total power capacity stands at 2,333 megawatts, with solar power accounting

for less than one per cent. The country relies on a mix of hydropower priced at Sh3 per

unit, geothermal (Sh7) while thermal tops Sh20 per unit.

The government in 2013 set an ambitious plan to install additional 5,000 megawatts to

the grid by end of next year from renewable sources such as geothermal, solar, biomass,

and wind farms. Kenya targets to connect all homes to power by 2020. Kenya is banking

on such energy sources to halve the cost of electricity to Sh10 per kWh (¢10.45).

In addition to, Kenya Power also signed contracts to buy power from independent power

producers (IPPs). Independent Power Producers (IPPs) are private investors in the

electricity sector who seek to fill the growing gap between available and required power

under the 3 Feed-in -Tariff Policy. Current players comprise IberAfrica, Tsavo, Or-power,

Rabai, Imenti, and Mumias. Collectively, they account for about 25% of the country‟s

installed capacity from thermal, geothermal and bagasse, as follows: Iberafrica (108 MW

-thermal power plant), OrPower (48 MW -geothermal power plant), Tsavo (74 MW-

thermal power plant), Mumias 3 (26MW -Cogeneration), Imenti (900kW -Mini-Hydro), and

Rabai (90MW- Thermal power plant).

Strathmore University (20.82MW), Ol Ndanyat wind project (10MW), Kwale International

Sugar Company (10 MW) and 0.57MW from Mt Kenya, a community-based organization

are new players in the renewable energy sector, including the VP Group - a Naivasha-

based horticultural firm which became Kenya’s pioneer producer of biogas connected

to the national grid after it started selling 2MW to Kenya Power in March 2016.

Challenges

a) Investors experience financial loss and project delays when pursuing licensing to

be an IPP, PPAs, and the approval from local authorities, the off taker and energy

regulatory agencies

b) Unavailability of long term debt finance from commercial banks to finance the

high cost of renewable energy projects as well as the reluctance of industry to

inject corporate equity into RE projects.

c) Access to finance and ‘high interest rates’

d) Low investment in renewable energy options resulting from low generation tariffs

offered and policy uncertainty.

e) Demands for various forms of guarantees including sovereign guarantees and

letters of credit to cover capacity and energy payments and dedicated revenue

streams occasioning project delays.

f) Overreliance on external/ imported technology.

g) Acquisition of way leaves continues to be a major challenge in the

implementation of the projects and substantial delays have been experienced in

many of the projects.

h) Inadequate skilled financial capacity to develop project finance proposals and

business models

i) Scaling up renewable energy technologies in East Africa has been hampered by

acute shortage of suitable professionals trained in renewable energy.

Other challenges facing the power sector include; vandalism, lack of redundancy for

security of supplies, excessive delays in obtaining permissions to put infrastructure in the

jurisdiction of various local authorities and environmental issues Multiple state agencies

seek to make more revenue from transmission lines pushing up the cost of power. Such

include WARMA, Council charges.

Structure and duration of PPA negotiations

1. Lack of defined timelines when negotiating for PPA’s. KPLC does it in an undefined

time frame which sometimes is more than two years while ERC Does it in 90days.

The lengthy time pushes cost of power.

2. Solution: Restructuring of the PPAs’ negotiations to enhance predictability in the

process.

3. Quality of Training to Engineers: There is a mismatch between training provided to

young engineers and the requirements of the job market.

Opportunities

a) Technology partnerships and human capital development for local research,

development, production and installation of renewable energy generation

capacity.

b) Streamlined renewable energy policy and regulatory framework especially in

terms of tariff setting, PPA negotiation and licensing processes. All the negotiations

for PPA negotiations should be concluded within 120 days (4 months) from the

date of submitting the requisite documents.

c) Development of alternative financing mechanisms including the establishment of

a Clean Energy Fund to finance and /or guarantee development of RE resources

for power generation.

Issues for further discussion could include:

1. What are the constraints on funding an energy fund to serve as basis for providing

guarantees?

2. Should a levy be charged on the existing tariffs? While this may raise cost of

powering the short term, it will ensure sustainability and displacement of high cost

thermal and emergency generation in the long term

3. Implementation of favorable tariffs to attract investments in renewable energy

projects. A recent sector study recommended that a generation tariff of 10-12 us

cents based on technology should be sufficient to attract several projects except

for solar.

4. Development of a standardized guarantee and Letter of Credit (LC) process

through a clear understanding of the expectations of international banks and

DFI’s.

Questions include:

Why do financiers insist on sovereign guarantees?

Are there any alternatives?

When can a letter of Government support substitute for a sovereign guarantee?

What is the role of a MIGA type guarantee?

Does this relate to size of project, specific type of project?

Can the Partial Risk Guarantee suffice?

4 ORGANIZATIONAL CAPACITY ASSESSMENT

Strengths

Weaknesses

o Capital- internally generated capital from

our contributions

o Quality leadership

o Enlightened and knowledgeable

members

o United- KETSA has a common unity of

purpose

o Legally constituted- we are registered

o Dedication/ commitment to the

Association (patriotic members)

o KETSA has come from a region where

there is a rich co-operative movement

o Goodwill from Apex bodies and

government

o Poor communication

o Lack of adequate operating funds

o Inconsistent remittances

o Low membership 12 against all the

available Teacher Saccos in Kenya

o Lack of infrastructure; office

o Lack of road map/ blue print

o Weak capacity in envisioned projects’

management

o Lack of secretariat that will spearhead

establishment of operational structures

o Lack of investment plan

o Lack of policy guidelines

o Lack of committed technical team

o Lack of support by all board members in

the individual member Saccos

o Lack of national outlook

o Legal status of the Association not clear

o Lack of a succession plan

Opportunities

Threats

o Availability of funds for on lending and

ready market

o Potential members - Open membership to

all Teacher Saccos in Kenya

o Investment opportunities

o Partnership and collaborations

o Ability to influence policy on Sacco sector

o Limited funds by individual Sacco

members

o Political interference (internal and

external)

o Competition from external institutions

on investment matters

EXTERNAL ENVIRONMENT ASSESSMENT

POLITICAL ECONOMIC

Opportunities

o Increased interest in renewable energy

o Current government supports

powering all households

Opportunities

o Energy Bill 2014 providing for IPP

investors

o Renewable energy partnerships

o Availability of market leaders to

benchmark with

o Power needs embedded in Vision 2030

Threats

o Ever changing Land reforms

o Bureaucracy and corruption in

granting approvals

o Change of guard in 2017 may derail

existing power generation plans

Threats

o High cost of materials and production

o Inadequate local competence in

renewable energy generation

o Low tariffs offered by partners i.e. KPLC

reducing profitability and sustainability

o High prices of land for investment

purposes

o High taxes in land/ real estate

acquisition

SOCIAL TECHNOLOGY

o High Investment appetite for real

estate and money market

Opportunities

o Customized ERP software available

o Advancements in digital finance and

e- communication

Threats

o Lack of trust in alternative energy

provision by Kenyans

o Land fraud

o Slow resolution of land succession

issues leading to increased project

timelines

Threats

o High cost of technology

o High obsolescence of technology

LEGAL ENVIRONMENTAL

Opportunities

o Structured frameworks for

engagement

Opportunities

o Carbon points for investment in

renewable energy

o High interest and financing for

renewable energy projects

Threats

o Myriad legal frameworks to familiarize

and adhere to

o Unfavorable regulation especially in

Land acquisition

o Lack of binding SLAs with stakeholders

resulting in slow execution of PPAs,

project delays thereby increasing cost

of projects

Threats

o High costs for waste management

o Rigorous bureaucratic assessment by

environmental bodies

5 KEY BUSINESS DRIVERS & RESULT AREAS

1. Governance

a. Membership growth

b. Capacity strengthening and Learning

c. Partnerships

d. Compliance to legal framework

e. Research and Advocacy

2. Operations

a. Optimization of the Organization structure

b. Human Resource Management

c. Risk Management and Internal Control Frameworks

d. Operational Efficiency

3. Enterprise Development -Projects

a. Land purchase and sale

b. Developed property purchase and sale

c. Electricity Generation and sale

4. Finance

a. Share Capital growth

b. Deposits growth

c. Loan portfolio growth

d. Investment Mix and Income

6 STRATEGIC PLAN DELIVERY STRUCTURE

Board of Management Level

AGM

Supervisory Comm

Internal Audit

BOD

CEO

Sub Commitees

Management Structure

* Support staff in electricity plant includePlant Maintenance Technician, Electricity Utility System Operator, Distribution Specialist,

Environmental Engineer, Electric Line Technician, Environmental Compliance Coordinator, Heavy Equipment Operator, Solar Energy

Consultant, Energy Management Analyst, Energy Compliance Associate, Surveyors etc.

Chief Executive

Officer

Finance

& Planning

Accounts Assistant

Recoveries and

Reconciliation Officer

Customer Service

Manager

Support staff

Internal Audit

Audit Assistant

Commercial Director,

Marketing And PR

Credit Manager

Credit officer

Projects Manager/

Clerk of Works

Marketing Officers

Plant Manager-Electricity

Operations Manager

*Support staff

Maintenance Manager

*Support staff

ICT Manager

7 IMPLEMENTATION PLAN

KEY BUSINESS DRIVER: GOVERNANCE KEY RESULT AREA: MEMBERSHIP

OBJECTIVE 1:INCREASE MEMBERSHIP BY 10 SACCOS ANNUALLY TO 50 SACCOS BY 2021

STRATEGY ACTIVITIES KPI TIMELINE RESPONSIBLE

Recruit all teacher based Saccos into

membership

Identify and communicate with all

teacher based Saccos

Report February

2017 and

continuous

Communicate the KETSA widely Open an social media page Social media presence April 2017

Develop a KETSA website Interactive website

Communicate at co-operative days Reports

KEY RESULT AREA: CAPACITY STRENGHTHENING & LEARNING

OBJCETIVE 1: ENHANCE THE CAPACITY OF THE BOARD AND SECRETARIAT TO OVERSEE PROJECTS AND PERFORMANCE

Provide adequate exposure in business

lines to various committees, secretariat

and staff

Conduct an assessment to

understand learning needs and

objectives

Report February

2017

Identify potential learning partners February

2017

Benchmark to understand the various

business lines

April 2017

Conduct training Number of members

trained

May 2017

and

continuous

KEY RESULT AREA: RESEARCH & ADVOCACY

OBJECTIVE 1: PLAY A PIVOTAL ROLE IN CHAMPIONING THE GROWTH OF SACCOS

Consciously stay abreast of matters

affecting the Sacco sector

Establish a Research and Learning

function

Report Continuously

Partner with others in the sector Number of partnerships

Ensure representation at relevant

stakeholder forums

Number of forums

participated in

KEY RESULT AREA: PARTNERSHIPS

OBJECTIVE 1: ENSURE EFFICIENT DELIVERY OF OBJECTIVES

Partner with leaders in the various

business lines e.g. e-channels,

Identify key stakeholders and

manage relationships

Report Continuously

insurance, real estate, electricity

generation, advocacy. etc.

Establish networks with various relevant

sectors

Register with relevant member

association

Number of affiliations Continuously

KEY RESULT AREA: LEGAL COMPLIANCE

OBJECTIVE 1: ENSURE 100% COMPLIANCE WITH RELEVANT FRAMEWORK

Ensure legal compliance with all

relevant government and other

agencies requirements

Identify relevant legal framework Report January 2017

Procure/ avail required guidelines

and communicate to relevant

committees and staff

Number of legal

requirements

communicated

February

2017

Ensure 100% compliance with

requirements

Number of exceptions Continuously

KEY BUSINESS DRIVER: OPERATIONS KEY RESULT AREA: OPTIMIZATION OF THE ORGANIZATION STRUCTURE

OBJECTIVE 1: ENSURE 100% DELIVERY OF THE STRATEGIC PLAN

STRATEGY ACTIVITIES KPI TIMELINE RESPONSIBLE

Optimize organization structure Design optimal organizational

structure with clear delivery and

reporting lines

Org structure approved January 2017

Design role profiles and job

descriptions

February

2017

Recruit competent staff and onboard

Design a mentoring and coaching

program to ensure skills transfer

KEY RESULT AREA: HUMAN RESOURCE MANAGEMENT

OBJECTIVE 1: ENHANCE STAFF PRODUCTIVITY ANNUALLY

Schemes of work Conduct a comparator survey on

schemes of service and competency

frameworks in the industry

Report May 2017

Design and implement adequate

Schemes of Work

Report February

2017

Performance management Design and implement a

performance based personnel

management system complete with

reward/ remedial criteria

Report June 2017

Capacity enhancement Conduct training needs analysis TNA and Training Plan September

2017

Provide best practice adaptation

training

Number of staff trained January 2017

Leave management Develop and implement a

comprehensive leave management

schedule

Report February

2017

Ensure not more than 25% leave days

carried forward

Number of days carried

forward

December

2017

KEY RESULT AREA: RISK MANAGEMENT &INTERNAL CONTROLS

OBJECTIVE 1: ESTABLISH A COMPREHENSIVE RISK MANAGEMENT FRAMEWORK

STRATEGY ACTIVITIES KPI TIMELINE RESPONSIBLE

Standardize operations Assess the required operating

manuals

Report February

2017

Develop relevant manuals and

policies

Number of manuals and

policies developed

Communicate policy guideline and

operating manuals to BOD and staff

Number of BOD and

staff trained

March 2017

Ensure adequate security of KETSA

assets

Establish an internal audit structure Approved structure Mach 2017

Ensure data and information security Conduct daily data back up Number of exceptions

Ensure offsite data back up

Ensure comprehensive data access

rights and audit trail

KEY RESUT AREA: OPERATIONAL EFFICIENCY

OBJECTIVE 1: ENSURE 100% COMPLIANCE TO SERVICE CHARTER

STRATEGY ACTIVITIES KPI TIMELINE RESPONSIBLE

Establish and brand KETSA office Procure and set up KETSA office Office in place February

2017

Enhance processes efficiency Conduct Process Mapping exercise Report June 2017

Identify potential service bottlenecks

and resolve

Ensure adequate competence of

staff

Ensure proper placement of staff

Ensure automation of processes Identify areas that requireautomation February

2017

Conduct MIS Audit February

2017

Define software and hardware

requirements

Procure and install robust ERP system May 2017

Leverage technology Identify areas where mobile/ e

service can be of use and implement

Number of e service

channels

December

2017

Ensure adherence to the internal and

external Service Charter

Develop departmental/ project

based Service Level Agreements

Report June 2017

Monitor compliance to SLAs Exceptions report Continuously

KEY BUSINESS DRIVERS: ECO INCLUSIVE ENTERPRISE DEVELOPMENT KEY RESULT AREA: PROJECTS- LAND PURCHASE & SALE

OBJECTIVE 1: ACQUIRE & SELL 100 ACRES OF PRIME LAND ANNUALLY STRATEGY ACTIVITIES KPI TIMELINE RESPONSIBLE

Source for prime adequate clean land Select a Projects Finance &

Marketing Committee

Committee in place January 2017

Familiarize with Land Law and

requirements

Report on various land

legal requirements and

stakeholders

February

2017

Develop a stakeholder management

plan

Report

Develop a land procurement, pricing

policy, and sale policy

Policy in place

Conduct member survey on land

needs

Report April 2017

Develop land buying criteria and

policy

Policy May 2017

Identify land and conduct due

diligence

Report May 2017

and

continuously

Conduct Feasibility study into

profitability of the Venture

Viability report When land is

identified

Develop an end to end project plan Project Plan

Source for off take financing where

necessary

MOU/ Contracts

Subdivide and sell land Implement the Project plan and

monitor performance

Number of plots

sold/profitability

Per Project

Plan

Close and exit project plan Report

KEY RESULT AREA: PROJECTS- PROPERTY PURCHASE & SALE

OBJECTIVE 1: BUY & SELL ONE DEVELOPED PROPERTY ANNUALLY

Source for prime developed property Select a Projects Finance &

Marketing Committee

Committee in place January 2017

Ensure compliance with legal

framework

Familiarize with Property and Real

estate laws and requirements

Report on various land

legal requirements and

stakeholders

February

2017

Develop a stakeholder management

plan

Report

Conduct member survey on property

needs

Policy in place April 2017

Conduct Feasibility study into various

Venture options’ and profitability

Viability report

Develop a property procurement,

pricing policy, and sale policy

May 2017

Conduct market survey on pricing and

viable locations

Identify property and conduct due

diligence

Report May 2017

and

continuously

Source for off take financing where

necessary

Develop an end to end project plan Project Plan When land is

identified

Off Sell property Implement the Project plan and

monitor performance

Number of plots

sold/profitability

As per

Project Plan

Close and exit project plan Report

KEY RESULT AREA: PROJECTS- ELECTRICITY GENERATION & SALE TO NATIONAL GRID

OBJECTIVE 1: GENERATE ….MW OF ELECTRICITY ANNUALLY FROM 2018

Test viability of the project Select a Projects Finance and

Marketing Committee

Committee in place January 2017

Develop a Feasibility Plan complete

with type of power to be generated,

location, requirements, stakeholder

mapping, capital expenditure

requirements, cost projections, and

profitability measures.

Feasibility study report May 2017

Ensure adherence to legal framework Familiarize with legal and market

requirements for Electricity

Generation for Independent Power

Producers

Report on various legal

requirements and

stakeholders

February

2017 and

continuously

Enhance relationship management

practice

Develop a stakeholder management

plan

Report

February

2017

Enhance capacity of KETSA to

implement a successful project

Identify market leaders to benchmark

with

April 2017

Benchmark and record findings May 2017

Develop end to end Project Plan Project Plan June 2017

Obtain licensing and permits Number of licenses and

permits

June 2017

Enter Power Purchase agreements

(PPA) with buyer

Timely PPAs December

2017

Implement power generation project

plan

Report After PPAs

are in place

Monitor implementation for timelines,

adherence to budgets and

operating efficiency

Weekly performance

reports

Sell power to the national grid MW produced/ Cost

efficiency/ profitability

Enhance sustainability of the power

plat

Establish research, development and

learning function for designing and

constructing sustainable energy

production and delivery systems.

Learning and

improvement reports

Report

KEY BUSINESS DRIVER: FINANCE

KEY RESULT AREA: FINANCIAL INVESTMENTS

OBJECTIVE 1: ENSURE 100% RISK MANAGEMENT FRAMEWORK IN ASSET MIX

STRATEGY ACTIVITIES KPI TIMELINES RESPONSIBLE

Invest excess or idle funds in short term

viable vehicles

Select Investments Committee Committee in place Annual

Identify viable investment vehicles Report

Conduct trend research into viable

investment vehicles

Select investment vehicles by past,

current and projected performance

Enter favorable agreements

Monitor performance and take timely

corrective action

% non-earning assets

annually / % increase in

revenue / loss

Monthly

KEY RESULT AREA: LOAN PORTFOLIO GROWTH

OBJECTIVE 1: DISBURSE KSHS 40 MILLION IN CORPORATE LOANS BY 2017, 80M BY 2018, 120M BY 2019, 160M BY 2020, 180M BY 2021

Offer Bridging Loan products (at 5% per

month?) to Saccos to meet working

capital (WC) requirements

Select Credit Committee & Task

Force

Committee in place January 2017

Conduct member survey on short

term credit needs, tariffs, collaterals,

collection methods

Report February

2017

Develop product prototype

complete with application

requirements, terms, collateral,

appraisal and collection tools

Product prototype

ready for testing

Develop product stationery Stationery

Integrate in MIS system Report

Pilot product and refine Pilot report

Launch loan product Acceptance/

performance report

April 2017

Ensure NIL default rate Establish debt recovery and

reconciliation Team

% NPL/ PAR April 2017

Monitor loan performance on

monthly basis and generate

exception reports for the CEO

Number of payment

exceptions/ irregular

loans/ revenue

collection

Monthly

KEY RESULT AREA: SHARE CAPITAL GROWTH

OBJECTIVE 1: INCREASE SHARE CAPITAL TO KSHS 44M IN 2017, 56.4M BY 2018, 129.6M BY 2019, 172.8M BY 2020, & 216M BY 2021

Increase Share Capital contribution to

Ksh 300,000 per month

Develop Share Capital and Dividend

policy

Approved policy February

2017

Develop value proposition for

members

Report

Integrate Shares Capital into

member database

Number of outstanding

items

March 2017

Establish a Shares Collection system Report February

2017

Identify number of members who are

behind (currently)on their shares

contribution to date, communicate

and regularize

Report January

2017/

Monthly

Create awareness of the need for

Share Capital growth and value

proposition

Communicate to members Number of members

reached

February

2017

Monitor performance complete with

monthly exception reports

Report Monthly

KEY RESULT AREA: DEPOSITS PORTFOLIO GROWTH

OBJECTIVE 1: INCREASE DEPOSITS TO KSHS 14.4 MILLION IN 2017, 28.4M BY 2018, 43.2M BY 2019, 57.6M BY 2020, 72M BY 2021

Increase Deposits of Ksh 100,000 per

member per month

Develop Deposits and Interest policy Approved policy February

2017

Integrate Deposits into member

database

Report March 2017

Establish a Deposits Collection system February

2017

Develop value proposition and

communicate to members

April 2017

Ensure 100% monthly collections Monitor performance, complete with

exception reports and regularize

% monthly collection/

exceptions

February

2017/

Monthly

8 MONITORING, EVALUATION,RESEARCH, & LEARNING FRAMEWORK

Developing a Strategic is the easy fun part. Implementation, monitoring, evaluation,

research to facilitate for effective decision making, taking, sharing and learning from the

process is the hard part.

The MERL framework should guide the guiding the overall strategy and implementation

of related activities and provide timely and relevant information to the BOD. This entails

close communication with all involved, BOD, members, staff, Partners and service

providers.

The CEO will provide leadership and capacity building to the staff in the design and

implementation of monitoring, evaluation and reporting systems. He will develop

presentations and written reports based on evaluation findings and promote capacity

strengthening through mentoring, coaching, and training to staff and BOD to ensure they

have the technical skills and knowledge to provide increasingly professional and

technical support.

Responsibilities and tasks

Setting up the MERL system

a. Develop MERL matrix particularly in the areas of the objective hierarchy, indicators

and monitoring mechanisms.

b. Develop an overall framework for performance reviews based on the Strategic

Plan and Budget, participatory review of achievements, process monitoring,

operations monitoring and lessons-learned workshops.

c. Guide the process for designing the format of progress reports, identifying and

designing the key indicators for each component, to record and report physical

progress made against

d. Guide the process for identifying the key performance questions and parameters

for monitoring performance and comparing it to targets as well as design formats

for such performance reports.

e. Ensure that all service provider contracts include specifications for the internal

monitoring required of them, the reporting systems and the penalties for failure to

report as specified.

f. In consultation with the BOD develop a plan for activity-related capacity-building

for any computer-based support that may be required.

g. Organize and undertake training with stakeholders, including primary

stakeholders, in MERL skills, including participatory aspects.

h. Design the framework for the physical and process monitoring of project activities.

i. Guide staff and BOD in preparing progress reports. Together, analyze these reports

in terms of problems and actions needed. Prepare consolidated progress reports

for Society activities in accordance with approved reporting formats and timing.

j. Review monitoring reports; analyze them for impact on overall strategic plan to

identify the causes of potential bottlenecks and make recommendations

k. Collaborate with staff and implementing partners on qualitative monitoring to

provide relevant information for ongoing evaluation of project activities, effects

and impacts.

l. Plan for regular opportunities to identify lessons learned and the Plan’s most

significant change (MSC).

Figure 1: MERL Framework

We recommend monthly monitoring exercises at every BOD and staff meeting, and a

quarterly review. An annual review consolidates all gains made and takes a bird’s eye

view of the implementation process, and makes recommendation for overall change in

strategy, or enhancements based on the environmental scan, progress made in

achieving KPIs, regulations, and market factors.

Planning

Implementation-provide

resources/ MERL Training/ Develop

MERL tools

Monitor Progress using tools as

above

Communicate with staff and BOD, Identify bottlenecks ,

learning lessons

Evaluate: identify and resolve bottlencks,

Variances, Scan environment

Feedback into Planning

9 STRATEGY PLANNING TEAM