kenya - wesgro 03 food and bev kenya.pdf · 4 kenya is the east african community (eac)'s...

TRANSCRIPT

Kenya Food and Beverages

Executive Summary

SECTOR OVERVIEW IN KENYA

African countries spend more than USD60bn annually importing food for their growing populations, but

the continent has the potential to become a major food exporter.

Fresh cow’s milk was the leading agricultural product in Kenya valued at USD1.6bn in 2013.

Food sales over the forecast period will grow by 13%, from KEM1.2trn in 2016 to KEM2trn in 2020

The largest food sales in Kenya over the five year forecast period to 2020 are expected to be cooking oil

and fats (KEM137bn in 2016 to KEM321bn in 2020) and edible oils (KEM129bn in 2016 to KEM307bn in

2020).

Kenya’s beer sales represented the largest sales of beverages, increasing from 509 million litres in 2012

to a forecasted 791 million litres in 2020.

TRADE

Kenya is a net exporter of food and beverages. Kenya’s exports of food and beverages were valued at

ZAR24.2bn in 2014 compared to ZAR19.6bn in 2013, increasing by 20%.

South Africa and the Western Cape are net exporters of food and beverages to Kenya.

In 2014, South Africa exported food and beverages valued at ZAR673m compared to ZAR513m in 2013,

representing an increase of 31%.

The leading export product from the Western Cape to Kenya in the food and beverages sector was

undenatured ethyl alcohol, valued at ZAR122m.

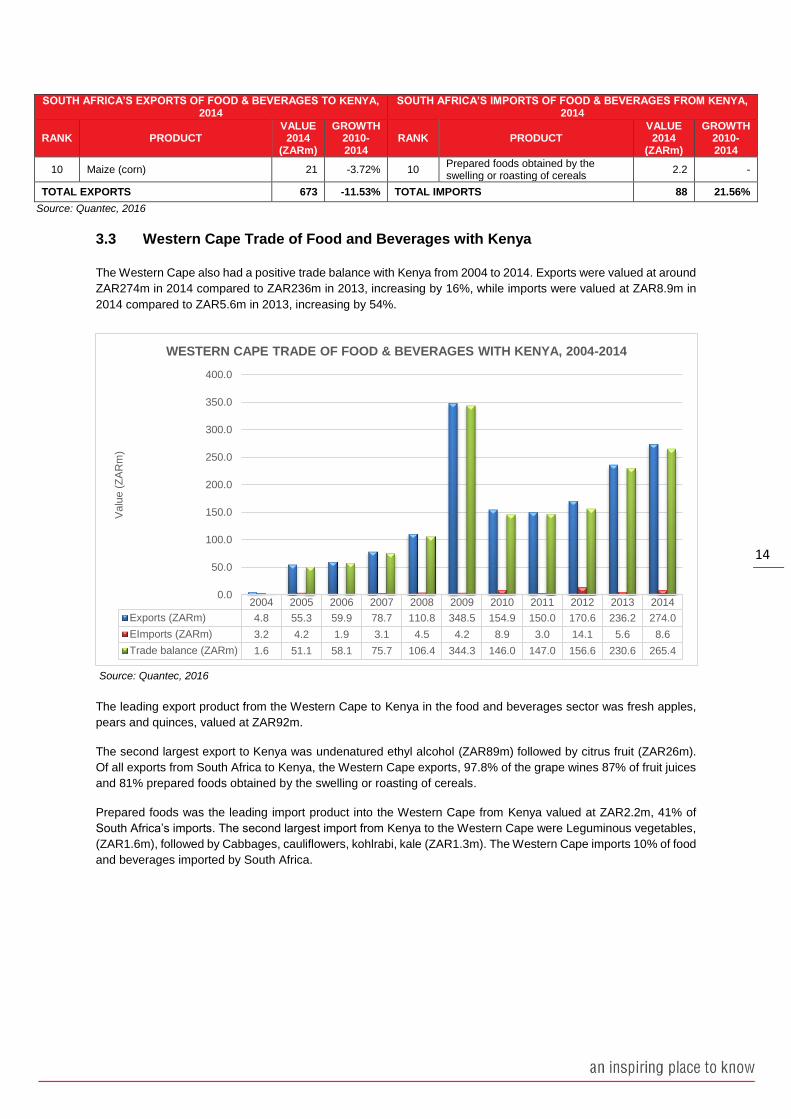

The Western Cape also had a positive trade balance with Kenya from 2004 to 2014. Exports were valued

at around ZAR274m in 2014 compared to ZAR236m in 2013, increasing by 16%.

In 2014, the leading export product from the Western Cape to Kenya in the food and beverages sector

was fresh apples, pears and quinces, valued at ZAR92m.

FDI

Kenya is a net recipient of FDI in the food and beverage sector.

Between January 2003 and August 2015 a total of 36 FDI projects were recorded into the Kenyan food

and beverage sector.

Between January 2003 and August 2015 a total of 33 FDI projects were recorded into the food and

beverage sector by Kenya. These projects represent a total capital investment of ZAR6.88bn.

Between January 2003 and August 2015 a total of 2 FDI projects were recorded from South Africa into

Kenya’s food and beverage sector. These projects represent a total capital investment of ZAR365.57m.

There were no investments with Kenya in this sector from or into the Western Cape.

2

Table of Contents

1. Definitions/descriptions ................................................................................................................... 3

2. Overview of food and beverage market in Kenya ........................................................................... 3

2.1 SWOT analysis of Kenya’s food and beverage sector ........................................................... 7

2.2 Logistics .................................................................................................................................. 8

2.3 Companies .............................................................................................................................. 9

3. Trade ............................................................................................................................................. 10

3.1 Kenya’s Global Trade of Food and Beverages ..................................................................... 10

3.2 South African Trade of Food and Beverages with Kenya ..................................................... 13

3.3 Western Cape Trade of Food and Beverages with Kenya ................................................... 14

3.4 Trade Regulations Markings and Standards ......................................................................... 16

3.4.1. Standards ...................................................................................................................... 16

3.4.2. Labelling ........................................................................................................................ 16

3.5 Tariffs for South African food and beverages ....................................................................... 16

4. FDI ................................................................................................................................................. 18

4.1 Inward FDI into the Kenyan Food & Beverage Sector .......................................................... 18

4.2 Outward FDI .......................................................................................................................... 19

4.3 Bilateral FDI between South Africa and Kenya ..................................................................... 21

3

1. Definitions/descriptions

According to FDI.net (2012), the food and beverage processing sector refers to the manufacturing, processing and

preservation of meat, fish, fruit, vegetables, oils and fats; manufacture of dairy products; manufacture of grain mill

products, starches and starch products and prepared animals feeds; manufacture of other food products (e.g.

bread, sugar, chocolate, pasta, coffee, nuts and spices); and the manufacture of bottled and canned soft drinks,

fruit juices, beer, wines, etc. This analysis includes unprocessed food and beverages such as raw fruit and

vegetables, seeds and nuts.

African countries spend more than USD60bn annually importing food for their growing populations, but the

continent has the potential to become a major food exporter. Large areas of unused arable land, low fertiliser use

and poor irrigation mean there is scope for improving yields in Africa, which are among the lowest in the world. A

rising middle class continues to boost African demand for food products, especially for processed and packaged

food, creating a continental food market that the World Bank estimates could be worth USD1trn in 2030. While

exporters in Asia and Brazil stand to gain in the short term, BMI Research (2015) forecasts that food producers,

processors and shippers in Kenya and South Africa, and retailers in Nigeria are all well placed to serve the growing

African consumer market.

2. Overview of food and beverage market in Kenya

Kenya's food and drink industry will experience robust growth in 2016, as the country's positive economic outlook

drives consumer spending. Kenya's consumer confidence is expected to rise with the increase in household

spending due to growing disposable incomes. It is expected that Kenya's emerging middle class will boost sales

for non-essential goods (BMI, 2016).

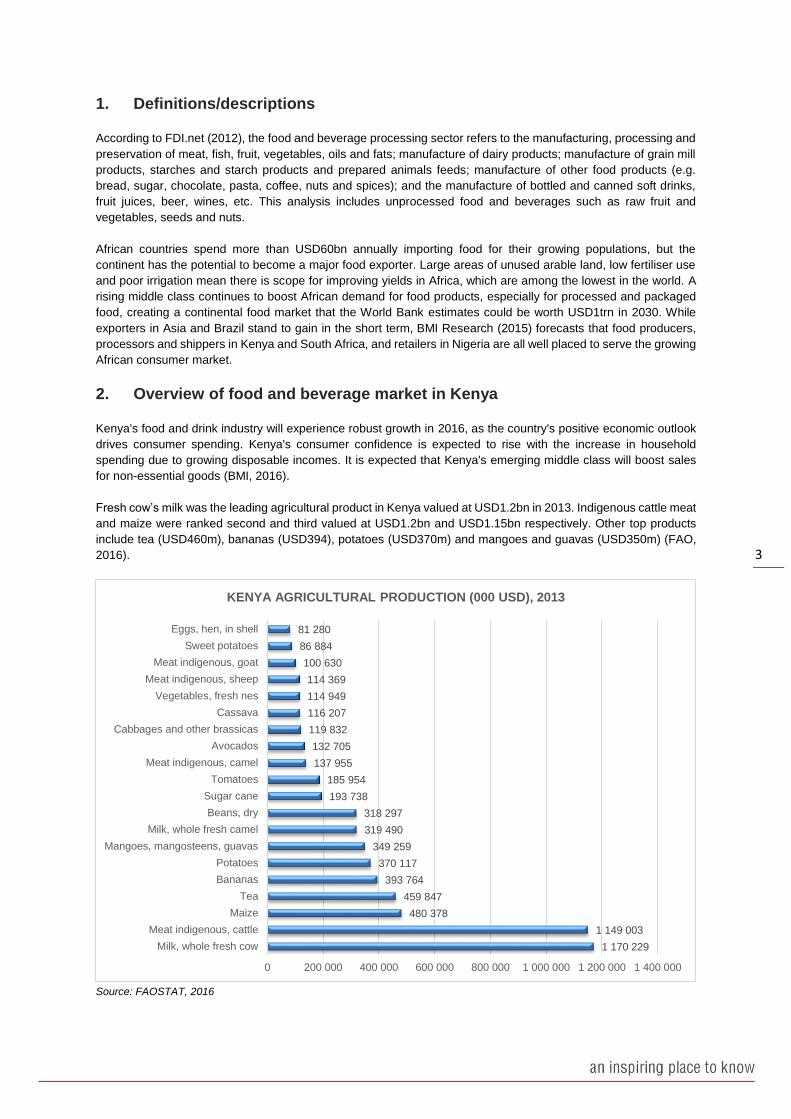

Fresh cow’s milk was the leading agricultural product in Kenya valued at USD1.2bn in 2013. Indigenous cattle meat

and maize were ranked second and third valued at USD1.2bn and USD1.15bn respectively. Other top products

include tea (USD460m), bananas (USD394), potatoes (USD370m) and mangoes and guavas (USD350m) (FAO,

2016).

Source: FAOSTAT, 2016

1 170 229

1 149 003

480 378

459 847

393 764

370 117

349 259

319 490

318 297

193 738

185 954

137 955

132 705

119 832

116 207

114 949

114 369

100 630

86 884

81 280

0 200 000 400 000 600 000 800 000 1 000 000 1 200 000 1 400 000

Milk, whole fresh cow

Meat indigenous, cattle

Maize

Tea

Bananas

Potatoes

Mangoes, mangosteens, guavas

Milk, whole fresh camel

Beans, dry

Sugar cane

Tomatoes

Meat indigenous, camel

Avocados

Cabbages and other brassicas

Cassava

Vegetables, fresh nes

Meat indigenous, sheep

Meat indigenous, goat

Sweet potatoes

Eggs, hen, in shell

KENYA AGRICULTURAL PRODUCTION (000 USD), 2013

4

Kenya is the East African Community (EAC)'s economic hub and comfortably its most dynamic consumer market.

It is expected that robust growth in Kenya's economy will drive positive growth in the food industry. Kenya's

diversified economy makes it one of the region's best performing, as it is less exposed to the downturn in

commodities prices and China's slowdown. Away from Kenya, there are very few countries, if any, in the region

that boast such a competitive food retailing industry that is dominated almost entirely by domestic companies (BMI,

2016).

Food sales over the forecast period to 2020 will grow by 13%, from KEM1.2trn in 2016 to KEM2trn in 2020, driven

primarily by 4.5% private consumption growth. The key drives will be the country's rising incomes, growing middle

class and favourable demographics, as well as growing financial inclusion.

Source: BMI Research, 2016

Kenya's market is exposed to a booming fast food sector, which will boost growth for convenience foods. Market

demand for oils and packaged foods will rise with Kenya's booming fast food industry and growing need for

convenience foods. The long-term opportunities on offer in Kenya, along with the fact that one can source a lot of

retail space locally given the relatively well developed nature of the wider food processing industry, suggest Kenya

is too good an opportunity to miss (BMI, 2016).

The increasing arrival of high-end travellers to Kenya are expected to drive premiumisation in the market and the

country's growing number of middle-income consumers will look to spend more on luxury goods offered by

international retailers.

The largest food sales in Kenya over the five year forecast period are expected to be cooking oil and fats

(KEM137bn in 2016 to KEM321bn in 2020), edible oils (KEM129bn in 2016 to KEM307bn in 2020), sugar

(KEM153bn in 2016 to KEM248bn in 2020) and beef (KEM145bn in 2016 to KEM233n in 2020).

2013 2014 2015 2016f 2017f 2018f 2019f 2020f

KEMbn 840.1 952.2 1 068.5 1 210.4 1 364.4 1 549.5 1 759.6 1 997.9

Growth 13.65% 13.35% 12.21% 13.28% 12.72% 13.57% 13.56% 13.54%

11.00%

11.50%

12.00%

12.50%

13.00%

13.50%

14.00%

0

500

1 000

1 500

2 000

2 500

Gro

wth

Valu

e (

KE

Mbn)

KENYA FOOD SALES, 2013-2020f

5

Source: BMI Research, 2016

2013 2014 2015 2016f 2017f 2018f 2019f 2020f

Cooking oils and fats 67.4 86.9 108.8 137.4 170.4 212.0 262.0 321.2

Edible oils and animal fats 61.4 80.1 101.2 128.8 160.7 201.1 249.5 307.1

Sugar 106.7 120.7 135.2 152.8 171.7 193.9 219.1 247.5

Beef 102.4 115.5 129.0 145.4 162.8 183.2 206.3 232.2

Dairy 146.3 155.9 163.9 171.7 179.8 189.9 198.1 205.8

Milk 126.4 134.6 141.5 148.3 155.6 164.7 171.9 178.5

Rice 65.6 74.6 84.0 95.4 107.7 122.4 139.0 157.9

Bread 47.4 53.3 59.4 66.7 74.5 83.5 93.7 105.1

Bananas (fresh), 40.0 45.6 51.5 58.7 66.6 75.9 86.5 98.6

Poultry 37.9 43.2 48.7 55.5 62.8 71.5 81.4 92.7

Other cereal products 30.5 34.8 39.3 44.8 50.8 57.9 66.1 75.3

Lamb 24.9 28.2 31.7 35.9 40.4 45.8 51.8 58.7

Citrus fruits (fresh) 23.1 26.4 29.8 34.0 38.6 44.1 50.3 57.4

Fresh vegetables 35.4 38.0 40.5 43.4 46.1 49.2 52.2 55.3

Stone fruits (fresh) 18.9 21.5 24.2 27.5 31.1 35.4 40.3 45.8

Fish 20.7 23.1 25.4 28.3 31.2 34.6 38.3 42.4

Salt, spices, herbs 7.5 9.6 11.9 15.0 18.5 22.9 28.2 34.5

Shellfish and preserved fish 14.0 15.8 17.8 20.2 22.8 25.8 29.3 33.2

Sauces and condiments 5.2 6.7 8.4 10.7 13.3 16.6 20.6 25.3

Other fruit 9.1 10.5 11.8 13.5 15.4 17.6 20.1 22.9

Margarine and spreads 9.9 11.1 12.4 13.9 15.6 17.5 19.7 22.1

Baked goods 10.3 11.5 12.7 14.1 15.5 17.1 19.0 20.9

Leaf and stem vegetables 8.9 10.0 11.3 12.8 14.4 16.3 18.4 20.8

Eggs 14.7 15.4 15.8 16.2 16.1 16.3 16.5 16.6

Root vegetables and mushrooms 11.9 12.6 13.1 13.7 14.3 14.9 15.4 15.8

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Valu

e (

KE

Sbn)

TOP 25 KENYA FOOD SALES, 2013-2020f

6

Kenya's emerging middle-class will be the driver of beer sales, with premium beer experiencing positive growth

sales as reported by East African Breweries in H116. Kenyan consumers will switch up from home brewed beer

owing to rising disposable incomes to boost the low-end beer market (BMI, 2016).

Kenya’s beer sales represented the largest sales of beverages, increasing from 509 million litres in 2012 to a

forecasted 791 million litres in 2020. This relatively modest growth in volume may cause market leaders to focus

on premiumisation, even though the low-cost beer revolution is more established in East Africa than it is in West

Africa.

Source: BMI, 2016

Whiskey is expected to be the largest alcoholic beverage sales in Kenya over the five-year forecast period to 2020

with 12.1 million litres being sold in 2020, followed by liqueur and red wine with sales of 5.3 million litres and 3.9

million litres respectively. Overall wine consumption in Kenya grew by 5% during 2013, higher than 2012. The

growth in wine consumption was largely driven by the growing middle-class population in Kenya (Euromonitor,

2014). There is an opportunity for Western Cape wine companies to promote their wines in this growing market.

Kenya Wine Agencies Limited, however, has engaged in extensive marketing and branding to grow and protect its

market share amid increased competition (Euromonitor, 2014).

Source: BMI, 2016

2012 2013 2014 2015 2016f 2017f 2018f 2019f 2020f

Beer 508.6 531.9 557.6 589.4 622.4 657.9 697.6 741.6 790.5

0

100

200

300

400

500

600

700

800

900

litre

s m

illio

n

KENYA BEER SALES, 2012-2020f

2012 2013 2014 2015 2016f 2017f 2018f 2019f 2020f

Whiskey 12.4 12.5 12.3 12.4 12.3 12.3 12.2 12.2 12.1

Liqueur 5.4 5.4 5.4 5.4 5.3 5.3 5.3 5.3 5.3

Red Wine 2.5 2.6 2.8 3.0 3.1 3.3 3.5 3.7 3.9

Gin 3.3 3.5 3.5 3.5 3.5 3.5 3.5 3.5 3.5

White Wine 2.1 2.1 2.2 2.3 2.5 2.6 2.7 2.9 3.1

Vodka 2.3 2.3 2.3 2.3 2.3 2.3 2.2 2.2 2.2

Other Wine 1.0 1.0 0.9 1.0 1.0 1.1 1.1 1.2 1.3

Rum 1.2 1.2 1.1 1.1 1.1 1.1 1.1 1.1 1.1

Vermouth 0.7 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.6

Sparkling Wine 0.2 0.1 0.2 0.2 0.2 0.2 0.2 0.2 0.2

Fermented drinks 0.2 0.0 0.0 0.0 0.1 0.1 0.1 0.1 0.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Litre

s m

illio

n

KENYA ALCOHOLIC BEVERAGE SALES, 2012-2020f

7

Kenya's tea and coffee industry will drive non-alcoholic drinks sales, as hot drinks sales grow by 11% over the five-

year forecast period to 2020. Soft drinks sales will experience positive growth, led by bottled water sales. It is

forecasted that mineral or spring water sales will remain high owing to the country's unsafe tap water. Kenya's

growing fast food industry will boost carbonated drinks sales, which are forecast to grow by 7.5% over our five-

year forecast period to 2020 (BMI, 2016).

Source: BMI, 2016

2.1 SWOT analysis of Kenya’s food and beverage sector

The table below shows the SWOT analysis of Kenya’s food and beverage sector:

STRENGTHS WEAKNESSES

Kenya is the East African Community (EAC)'s economic hub and comfortably its most dynamic consumer market. Its food and drink industry is well developed by regional standards and has many Kenyan companies.

Nakumatt, Uchumi, Tuskys and Naivas, are well established domestic companies in the food retail sector.

Close trade links with Uganda and Tanzania and with large markets in Europe have seen the country develop a major food export industry.

Kenyan firms' ability to manage complex supply chains and experience dealing with European import and health requirements.

Per capita food consumption in Kenya still has a long way to go to match some of Sub-Saharan Africa's wealthiest countries, such as Botswana, Namibia and South Africa.

Kenya ranks 12th out of 14 sub-Saharan African countries in the food and drinks risk-reward rating.

The distribution of products across sub-Saharan Africa to retailers remains challenging hampered further by poor infrastructure and refrigeration systems.

OPPORTUNITIES THREATS

Premiumisation will play a major part in the growth of many segments of the Kenyan food and drink industry.

Kenya's dominant beer company East African Breweries Limited is facing some major issues in Kenya following the introduction of an excise tax

2013 2014 2015 2016f 2017f 2018f 2019f 2020f

Tea 17.8 19.9 22.2 24.9 27.9 31.7 36.0 41.0

Soft Drinks 4.3 4.8 5.3 6.0 6.7 7.6 8.7 9.9

Carbonated Drinks 11.5 12.3 13.2 14.3 15.4 16.4 17.7 18.9

Hot chocolate and other hot drinks 1.4 1.6 1.7 1.8 1.9 2.1 2.3 2.4

Fruit and vegetable juices 1.2 1.3 1.4 1.5 1.6 1.8 1.9 2.1

Mineral or spring waters 8.8 9.5 10.2 11.0 11.8 12.6 13.5 14.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Valu

e (

KE

Mbn)

KENYA NON-ALCOHOLIC BEVERAGE SALES, 2013-2020f

8

Opportunities for M&A with domestic food retailers

Rising middle class boosts African demand for food products (especially for processed and packaged food).

The well-developed dairy industry has the capacity to expand its operation.

Kenya is developing a domestic packaging and processing industry based around firms such as meat producer Farmers' Choice.

levied against its key Senator Keg brand in October 2013.

Source: BMI Research, 2015

2.2 Logistics

There are two Trans-African highways running through Kenya, which form the main international transport routes

and allow for smoother cross-border road transit. The first is the Cairo-Cape Town Highway (number 4), which runs

north to south and connects the country to Ethiopia and Tanzania. This route is largely paved south of Tanzania,

and is mostly used from Nairobi southwards. Northern sections in Kenya and Sudan are of poorer quality. The

second is the Lagos-Mombasa Highway (number 8), which runs east to west and connects Kenya to Uganda and

West Africa. The usage of this route remains limited beyond Uganda, however, as it is largely unpaved through the

Democratic Republic of Congo (EAC, 2015). The road network in Kenya is still below the standard of more

developed countries, and supply chains face serious risks of congestion, checkpoint bribes and armed robbery.

The port delays are especially worrisome for perishable food and beverage products (PwC, 2013). Kenya also has

many established private companies who specialise in the transport of perishable items, these include Sonic Fresh

Co.

Source: Northern Corridor Transit and Transport Coordination Authority, 2014

The Northern corridor, pictured above, is the transport corridor linking the land locked countries of Uganda, Rwanda

and Burundi with Kenya’s maritime port of Mombasa. Similarly, the Northern Corridor serves the eastern part of

the Democratic Republic of Congo, southern Sudan and northern Tanzania. The Northern Corridor infrastructure

connects all the five countries of the East African Community and links around 200 million people to global markets

through the Mombasa port (Northern Corridor Transit and Transport Coordination Authority, 2014).

In terms of port upgrades, Kenya is spending USD366m to construct a new container terminal in Mombassa that

will more than double the capacity of the current port, from handling 900,000 20-foot equivalent unit (TEU)

9

containers to 2,1 million containers (Financial Mail, 2013). A new terminal is also being built on land reclaimed from

the sea by Japan Ports Consultants, with the third phase expected to be completed in 2020. The new terminal will

enable the country to handle larger vessels.

2.3 Companies

The table below gives the key companies in Kenya’s food and beverage sector:

East African Breweries Limited (EABL) is East Africa's leading branded alcohol beverage business with an

outstanding collection of brands that range from beer, spirits and adult non-alcoholic drinks (ANADs) reaffirming

our standing as a total adult beverage (TAB) company.

Unga Group Limited is a Kenya-based holding company that has a majority shareholding in companies involved

with the manufacture and marketing of a broad range of human nutrition, animal nutrition and animal health

products.

Mumias Sugar Company is primarily engaged in the manufacture and sale of sugar. The company grows some

sugar cane; its own estates provide up to 7% of its annual output. Its primary source of sugarcane is over 50,000

registered "out growers" with over 400 square kilometres (99,000 acres) under cultivation.

Sasini has controlling stacks in Tea and Coffee production in Kenya comprising an area of over 2,000 hectares.

Kenya is one of the largest exporters of tea. With an active participation in the weekly Mombasa Tea Auctions,

Sasini supplies increasingly large volumes of tea to the expanding markets of Europe, the Middle East, Egypt and

Pakistan (Moneyhub, 2015).

KENYA FOOD AND BEVERAGE COMPANIES, 2016

COMPANY OWNERSHIP SUBSECTOR SALES (USDm)

East African Breweries Parent company: Diageo Alcohol - beer 707.0

Unga Group Partnership: US-based Seaboard Corporation (35%)

Food - diversified 185.1

Mumias Sugar

Shareholders: Kenyan Government (71%); Commonwealth Development Corp (17%)

Food - sugar 60.6

Sasini - Tea and coffee 31.8

Williamson Tea - Tea 29.0

Kakuzi Parent company: UKbased Camellia PLC (50.7%)

Tea and diversified agribusiness

19.2

Kapchorua Tea - Tea 12.0

Eaagads - Coffee 1.1

Limuru Tea - Tea 1.0

Kenya Orchards - Food - diversified 0.7

Source: BMI, 2016

10

3. Trade

3.1 Kenya’s Global Trade of Food and Beverages

Kenya experienced a positive trade balance from 2004 to 2014, making Kenya a net exporter of food and

beverages. Kenya’s exports of food and beverages were valued at ZAR24.2bn in 2014 compared to ZAR19.6bn in

2013, increasing by 20%, while imports were valued at ZAR21bn in 2014 increasing by 24%.

Source: Trade Map, 2016

Egypt was the leading export market for food and beverages from Kenya in 2014, valued at ZAR3.4bn and growing

by 12% per annum over the last five years. The United Kingdom and Pakistan were ranked second and third,

valued at ZAR3bn and ZAR2.7bn respectively. Other top export markets were Uganda (ZAR953m), Germany

(ZAR1.1bn) and Netherlands (ZAR1bn). The top food and beverage exports to the top three destination markets

are as follows:

Egypt

Tea, ZAR3.3bn

Pipe, chewing , tobacco, ZAR113m

Coconut, abaca, ramie & other vegetable fibers, ZAR17m

United Kingdom:

Tea, ZAR2bn

Cut flowers and flower buds, ZAR987m

Leguminous vegetables, ZAR889m

Pakistan

Tea, ZAR2.5bn

Dried vegetables, ZAR208m

Carbonate; peroxocarbonate, ZAR91m

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports (ZARm) 7 035 7 795 8 494 9 917 15 029 14 221 14 111 16 296 18 468 19 633 24 205

Imports (ZARm) 3 187 2 979 4 032 5 523 8 885 10 993 8 250 13 239 14 428 16 713 21 356

Trade balance (ZARm) 3 848 4 816 4 462 4 395 6 144 3 228 5 861 3 056 4 041 2 920 2 849

0

5 000

10 000

15 000

20 000

25 000

30 000

Valu

e (

ZA

Rm

)

KENYA FOOD & BEVERAGE TRADE, 2004-2014

11

KENYA’S EXPORT MARKETS OF FOOD & BEVERAGES, 2014

RANK DESTINATION MARKETS VALUE

2014 (ZARm)

% GROWTH 2010-2014

1 Egypt 3 354 17.83%

2 United Kingdom 2 962 0.42%

3 Pakistan 2 731 18.69%

4 Uganda 1 232 13.62%

5 United States 1 181 19.98%

6 Germany 1 103 10.02%

7 Netherlands 1 017 10.14%

8 Russian 958 23.27%

9 Tanzania 928 32.44%

10 France 912 8.46%

34 South Africa 88 22.80%

TOTAL EXPORTS 24 205 11.53%

Source: Trade Map, 2016

Pakistan was the leading source market for food and beverages to Kenya valued at ZAR2.9bn, followed by

Tanzania and Uganda valued at ZAR2.8bn and ZAR1.5bn respectively. Other top import markets were Russia

(ZAR1.4bn), Malaysia (ZAR1.4bn) and Indonesia (ZAR1.2bn). The top food and beverage imports from the top

three source markets are as follows:

Pakistan:

Rice, ZAR2.8bn

Knotted nettg of twine, ZAR111m

Woven cotton fabrics, ZAR73m

Tanzania

Maize (corn), ZAR1bn

Twine, cordge and cable, ZAR675m

Frozen vegetables, ZAR573m

Uganda

Tea, ZAR896m

Tobacco unmanufactured; tobacco refuse, ZAR513m

Electrical energy, ZAR312m

12

Source: Trade Map, 2015

Tea was the leading export product from Kenya in 2014, valued at ZAR11bn. Kenya currently exports 14% of the

world’s share of tea, the 3rd largest exporter after Sri Lanka and China. Unilever is the world’s leading tea

manufacturer and buys on average around 12 percent of global supply, which it markets worldwide under the

Lipton, PG Tips and Brooke Bond brand names. In this capacity they are partnering with a New York based

company Nature Source Genetics to create more resilient, “future-proof,” tea crops using a natural breeding

method known as genomic selection in their tea plantations in Kenya. This will likely further the growth of tea

exports from Kenya into the future. Coffee (ZAR3bn) and leguminous vegetables (ZAR1.9bn) were the second

and third largest export products from Kenya. The fastest growing food and beverage exports in 2014 were nuts

and vegetables.

The leading import product into Kenya was wheat and meslin, valued at ZAR4bn. Rice (ZAR3.3bn) and palm oil

(ZAR2.4bn) were the second and third largest imported products in the sector. There was strong growth in the

import of frozen vegetables and tea.

KENYA’S GLOBAL EXPORTS OF FOOD & BEVERAGES, 2014 KENYA’S GLOBAL IMPORTS OF FOOD & BEVERAGES, 2014

RANK PRODUCT VALUE

2014 (ZARm)

% GROWTH 2013-2014

RANK PRODUCT VALUE

2014 (ZARm)

% GROWTH 2013-2014

1 Tea 11 335 -3.10% 1 Wheat and meslin 4 070 65.41%

2 Coffee 2 517 37.36% 2 Rice 3 250 106.52%

3 Leguminous vegetables 1 918 57.60% 3 Palm oil & its fraction 2 433 -51.17%

4 Preserved fruits 843 24.04% 4 Tea 1 997 983.85%

5 Nuts nes 754 3907.64% 5 Maize (corn) 1 312 413.70%

6 Dried vegetables, shelled 494 -5.54% 6 Cane or beet sugar 1 072 -36.56%

7 Dates, figs,pineapples, mangoes, avocadoes, guavas

441 5.73% 7 Frozen vegetables 579 109629.55%

8 Sugar confectionery 410 -31.98% 8 Food preparations, nes 413 -9.43%

9 Vegetables nes, fresh or chilled 398 565.19% 9 Dried vegetables, shelled 356 7.90%

10 Margarine 390 53.63% 10 Fish, frozen, whole 329 257.12%

TOTAL EXPORTS 24 205 11.53% TOTAL IMPORTS 21 356 35.40%

Source: TradeMap, 2016

KENYA’S SOURCE MARKETS OF FOOD & BEVERAGES, 2014

RANK SOURCE MARKETS VALUE

2014 (ZARm)

% GROWTH 2010-2014

1 Pakistan 2 900 37.29%

2 Tanzania 2 815 94.79%

3 Uganda 1 447 14.41%

4 Russian 1 434 80.95%

5 Malaysia 1 390 54.37%

6 Indonesia 1 200 184.27%

7 India 890 51.43%

8 Ukraine 873 111.12%

9 United States of America 687 -6.37%

10 Thailand 674 59.41%

13 South Africa 674 -10.53%

TOTAL IMPORTS 21 356 17.62%

13

3.2 South African Trade of Food and Beverages with Kenya

South Africa has a positive trade balance with Kenya and is a net exporter of food and beverage products from the

country. In 2014, South Africa exported food and beverages valued at ZAR673m compared to ZAR513m in 2013,

representing an increase of 31%.

South Africa imported food and beverages from Kenya valued at ZAR88m in 2014 compared to ZAR118m in 2013,

representing a decrease of 25%. The exports from South Africa in 2009 are so high due to a spike in the export of

maize worth ZAR2.3bn.

Source: Quantec, 2016

The leading export product to Kenya was undenatured ethyl alcohol, valued at ZAR122m, followed by apples, pears

and quinces (ZAR117m) and wine (ZAR95m). The largest growing export to Kenya per annum from 2010 to 2014

was cane or beet sugar (197%), followed by chocolate and other food containing cocoa (162%). The leading import

product into South Africa from Kenya was dried and shelled leguminous vegetables valued at ZAR19m, followed

by tea (ZAR17m). Fresh or chilled leguminous vegetables (ZAR15m) were the third largest import in value terms.

Cabbages, cauliflowers, kohlrabi and kale were the largest growing import into South Africa growing at 348% per

annum over the last five years.

SOUTH AFRICA’S EXPORTS OF FOOD & BEVERAGES TO KENYA, 2014

SOUTH AFRICA’S IMPORTS OF FOOD & BEVERAGES FROM KENYA, 2014

RANK PRODUCT VALUE

2014 (ZARm)

GROWTH 2010-2014

RANK PRODUCT VALUE

2014 (ZARm)

GROWTH 2010-2014

1 Undenatured ethyl alcohol; ethyl alcohol

122 55.24% 1 Dried leguminous vegetables, shelled 19.0 -

2 Apples, pears and quinces, fresh 117 24.70% 2 Tea, whether or not flavoured 16.8 1.88%

3 Wine 95 25.13% 3 Leguminous vegetables, shelled or unshelled, fresh or chilled

15.0 57.05%

4 Cane or beet sugar 79 38.62% 4 Cabbages, cauliflowers, kohlrabi, kale 9.6 348.06%

5 Chocolate 29 225.27% 5 Vegetables frozen 7.7 -

6 Undenatured ethyl alcohol; spirits, liqueurs

27 5.86% 6 Coffee 4.5 29.48%

7 Food preparations nes 26 13.51% 7 Other vegetables, fresh or chilled 3.7 44.03%

8 Preparations of a kind used in animal feeding

23 24.35% 8 Jams, fruit jellies, marmalades, fruit or nut pureé

2.5 -

9 Citrus fruit, fresh or dried 23 26.63% 9 Onions, shallots, garlic, leeks and other alliaceous vegetables

2.4 173.39%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports (ZARm) 392 286 245 287 1 008 2 714 780 382 392 513 673

Imports (ZARm) 25 34 38 35 54 41 58 58 100 118 88

Trade balance (ZARm) 367 252 207 252 955 2 673 722 324 292 394 585

0

500

1 000

1 500

2 000

2 500

3 000

Valu

e (

ZA

Rm

)

SOUTH AFRICAN EXPORTS OF FOOD &BEVERAGES WITH KENYA, 2004-2014

14

SOUTH AFRICA’S EXPORTS OF FOOD & BEVERAGES TO KENYA, 2014

SOUTH AFRICA’S IMPORTS OF FOOD & BEVERAGES FROM KENYA, 2014

RANK PRODUCT VALUE

2014 (ZARm)

GROWTH 2010-2014

RANK PRODUCT VALUE

2014 (ZARm)

GROWTH 2010-2014

10 Maize (corn) 21 -3.72% 10 Prepared foods obtained by the swelling or roasting of cereals

2.2 -

TOTAL EXPORTS 673 -11.53% TOTAL IMPORTS 88 21.56%

Source: Quantec, 2016

3.3 Western Cape Trade of Food and Beverages with Kenya

The Western Cape also had a positive trade balance with Kenya from 2004 to 2014. Exports were valued at around

ZAR274m in 2014 compared to ZAR236m in 2013, increasing by 16%, while imports were valued at ZAR8.9m in

2014 compared to ZAR5.6m in 2013, increasing by 54%.

Source: Quantec, 2016

The leading export product from the Western Cape to Kenya in the food and beverages sector was fresh apples,

pears and quinces, valued at ZAR92m.

The second largest export to Kenya was undenatured ethyl alcohol (ZAR89m) followed by citrus fruit (ZAR26m).

Of all exports from South Africa to Kenya, the Western Cape exports, 97.8% of the grape wines 87% of fruit juices

and 81% prepared foods obtained by the swelling or roasting of cereals.

Prepared foods was the leading import product into the Western Cape from Kenya valued at ZAR2.2m, 41% of

South Africa’s imports. The second largest import from Kenya to the Western Cape were Leguminous vegetables,

(ZAR1.6m), followed by Cabbages, cauliflowers, kohlrabi, kale (ZAR1.3m). The Western Cape imports 10% of food

and beverages imported by South Africa.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports (ZARm) 4.8 55.3 59.9 78.7 110.8 348.5 154.9 150.0 170.6 236.2 274.0

EImports (ZARm) 3.2 4.2 1.9 3.1 4.5 4.2 8.9 3.0 14.1 5.6 8.6

Trade balance (ZARm) 1.6 51.1 58.1 75.7 106.4 344.3 146.0 147.0 156.6 230.6 265.4

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

Valu

e (

ZA

Rm

)

WESTERN CAPE TRADE OF FOOD & BEVERAGES WITH KENYA, 2004-2014

15

WESTERN CAPE’S EXPORTS OF FOOD & BEVERAGES TO KENYA, 2014

WESTERN CAPE’S IMPORTS OF FOOD & BEVERAGES FROM KENYA, 2014

RANK PRODUCT VALUE

2014 (ZARm)

GROWTH 2010-2014

RANK PRODUCT VALUE

2014 (ZARm)

GROWTH 2010-2014

1 Apples, pears and quinces, fresh 91.6 25.60% 1 Prepared foods obtained by the swelling or roasting of cereals

2.2 #DIV/0!

2 Undenatured ethyl alcohol; spirits, liqueurs

88.8 28.66% 2 Other vegetables, fresh or chilled

1.8 55.51%

3 Citrus fruit, fresh or dried 25.9 5.35% 3 Leguminous vegetables 1.6 62.94%

4 Fruit juices 13.1 25.12% 4 Cabbages, cauliflowers, kohlrabi, kale

1.3 491.35%

5 Grapes, fresh or dried 9.6 7.33% 5 Coffee 0.9 620.00%

6 Food preparations nes 8.5 39.79% 6 Jams, fruit jellies, marmalades, fruit or nut pureé

0.7 #DIV/0!

7 Preparations of a kind used in animal feeding

7.0 39.95% 7 Vegetables frozen 0.14 #DIV/0!

8 Sugar confectionery 6.0 52.11% 8 Tea, whether or not flavoured 0.03 17.59%

9 Prepared foods obtained by the swelling or roasting of cereals o

4.9 149.93% 9 - -

-

10 Sauces and preparations 3.5 14.68% 10 - - -

TOTAL EXPORTS 274 1.89% TOTAL IMPORTS 8.6 81.45%

Source: Quantec, 2016

Other fresh fruit was the fastest growing export products in the short term (2013 to 2014), growing at 332% followed

by food preparations and malt preparations, food preparations of flour growing at 130% and 75% respectively. In

the medium term (2010-2014), the fastest growing export product category was also other fresh fruit at 489%

growth.

Source: Quantec, 2016

-19.01%

-9.75%

11.89%

28.06%

29.31%

30.25%

36.83%

38.29%

48.47%

51.27%

51.63%

74.91%

129.65%

332.03%

14.68%

5.35%

39.79%

7.33%

25.12%

52.11%

50.38%

28.66%

26.16%

149.93%

39.86%

295.41%

39.95%

488.80%

-100% 0% 100% 200% 300% 400% 500% 600%

Prepared foods obtained by the swelling or roasting ofcereals

Undenatured ethyl alcohol; spirits, liqueurs

Grapes, fresh or dried

Fruit juices

Citrus fruit, fresh or dried

Preparations of a kind used in animal feeding

Ginger, saffron, turmeric (curcuma), thyme, bay leaves, curry

Apples, pears and quinces, fresh

Sauces and preparations

Sugar confectionery

Other fermented beverages

Malt extract; food preparations of flour, groats, meal, starch

Food preparations nes

Other fruit, fresh

GROWTH OF WESTERN CAPE EXPORTS OF FOOD & BEVERAGES TO KENYA, 2010-2014

2010-2014 2013-2014

16

3.4 Trade Regulations Markings and Standards

Currently there is no FTA between South Africa and Kenya.

In October 2008, SADC joined with the Common Market for Eastern and Southern Africa and the East African

Community to form the African Free Trade Zone, including all members of each of the organizations including

South Africa and Kenya. The African Free Trade Zone, consists of 26 countries with a GDP of an estimated

USD624bn. It is expected to become operational in 2018.

3.4.1. Standards

The Kenya Bureau of Standards (KEBS) is the government regulatory body under Kenya's Ministry of Trade

mandated to develop and ensure compliance with the International Standards Organization (ISO) product

standards. The National Environment Management Authority, under the Ministry of Environment and Natural

Resources, the Department of Public Health, and the Ministry of Health are all government organisations that

develop environmental and public health standards in partnership with KEBS.

The Kenya Plant Health Inspectorate Service (KEPHIS) deals with the certification of all imported plant materials

as well as implementing sanitary & phytosanitary requirements.

3.4.2. Labelling

Special labelling is required for certain goods including condensed milk, vegetables, and butter. Weights and

measure indicators must be in metric form or display both metric and imperial units. Manufacturers are required to

indicate the date of manufacture and expiry on the labels of consumable products.

3.5 Tariffs for South African food and beverages

Kenya imposes the highest tariffs on the import of sugars and sugar confectionary from South Africa at 71.9%. This

is followed by dairy products, eggs, honey and other edible animal product with an imposed tariff of 53.1%.

TARIFFS IMPOSED BY KENYA TO SOUTH AFRICAN FOOD AND BEVERAGE IMPORTS

HS CODE

PRODUCT EQUIVALENT AD

VALOREM TARIFF

02 Meat and edible meat offal 25

03 Fish, crustaceans, molluscs, aquatic invertebrates nes 25

04 Dairy products, eggs, honey, edible animal product nes 53.1

07 Edible vegetables and certain roots and tubers 25

08 Edible fruit, nuts, peel of citrus fruit, melons 24.9

09 Coffee, tea, mate and spices 25

10 Cereals 24

11 Milling products, malt, starches, inulin, wheat gluten 34.1

15 Animal,vegetable fats and oils, cleavage products, etc 13.3

16 Meat, fish and seafood food preparations nes 25

17 Sugars and sugar confectionery 71.9

18 Cocoa and cocoa preparations 11.6

19 Cereal, flour, starch, milk preparations and products 21.4

20 Vegetable, fruit, nut, etc food preparations 25

21 Miscellaneous edible preparations 15.3

22 Beverages, spirits and vinegar 25

Source: TradeMap, 2016

17

The excise duty for alcoholic beverages in Kenya according to the Kenyan treasury (2015) are as follows:

Whiskies, rum, gin and geneva, vodka cordials and distilled spirits like Konyagi and Uganda Waragi will

attract the highest tax rates, that is, Ksh120 per litre or 35 percent whichever is higher.

Beer will attract a tax of Ksh70 per litre or 50 percent per litre, whichever is higher.

Stout and porter beer made from malt and cider will be charged Ksh70 per litre or 50 percent whichever

is higher.

Wine and vermouth will be charges Ksh80 per litre or 50%.

18

4. FDI

4.1 Inward FDI into the Kenyan Food & Beverage Sector

Between January 2003 and August 2015 a total of 36 FDI projects were recorded into the Kenyan food and

beverage sector. These projects represent a total capital investment of ZAR8bn which is an average investment

of ZAR223m per project. During the period, a total of 6,839 jobs were created. Kenya is a net recipient of investment

in this sector.

Source: FDI Intelligence, 2016

The United States was the leading source market for Kenya’s food and beverage sector investments with 9

investment projects representing a capital investment of ZAR2.2bn from 2003 to August 2015, followed by Egypt

and Switzerland with 4 investment projects each. South Africa was the 6th largest global source market for inward

FDI into the Kenya’s food and beverage sector.

GLOBAL FDI INTO KENYA’S FOOD, BEVERAGE & TOBACCO SECTORS, 2003- AUGUST 2015

RANK SOURCE COUNTRY PROJECTS % PROJECTS CAPEX (ZARm) % CAPEX COMPANIES

1 United States 10 27.78% 3 109 38.75% 6

2 Egypt 4 11.11% 412 5.14% 1

3 Switzerland 4 11.11% 677 8.44% 2

4 France 2 5.56% 211 2.63% 2

5 Netherlands 2 5.56% 326 4.06% 2

6 South Africa 2 5.56% 366 4.56% 2

7 UAE 2 5.56% 389 4.85% 1

8 UK 2 5.56% 176 2.19% 2

9 Bermuda 1 2.78% 223 2.78% 1

10 China 1 2.78% 27 0.34% 1

TOTAL 36 100.0 8 022 100.0 26

Source: FDI Intelligence, 2016

Coca-Cola was the largest investor into Kenya’s beverage, food and tobacco sector, with 5 projects worth

ZAR1.7bn. In November 2014 it was announced that Switzerland-based food company Nestlé's (3rd) Kenyan unit

had partnered with Coffee Management Services (CMS) to boost coffee yields and crop production in the country.

Nestlé and CMS will implement the programme in the rural counties of Kiambu, Murang'a, Kirinyaga, Nyeri, Embu

and Meru (BMI Research, 2015).

2003 2004 2005 2006 2008 2009 2010 2011 2012 2013 2014 2015

Capex (ZARm) 306 469 1 640 274 702 141 443 1 059 223 1 105 764 898

Projects 4 3 1 2 2 2 2 2 1 10 5 2

2

4

6

8

10

12

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Pro

jects

Valu

e (

ZA

Rm

)

INWARD FDI INTO KENYA'S FOOD & BEVERAGE SECTOR, 2003-AUGUST 2015

19

COMPANIES INVESTING INTO KENYA’S FOOD & BEVERAGE SECTOR, 2003-AUGUST 2015

INVESTING COMPANY ACTIVITY PROJECTS CAPEX (ZARbn)

Coca-Cola United States 5 1 717

Wadi Egypt 4 412

Nestle Switzerland 3 562

Majid Al Futtaim Group (MAF Group) UAE 2 389

Asia Plantation Capital Singapore 1 197

Bacardi Bermuda 1 223

British American Tobacco (BAT) United Kingdom 1 73

Carrefour France 1 195

Clarion Merchandise Italy 1 37

Coca-Cola Sabco South Africa 1 293

TOTAL FROM TOP 10 INVESTORS 36 8 022

Source: FDI Intelligence, 2016

4.2 Outward FDI

Between January 2003 and August 2015 a total of 33 FDI projects were recorded into the food and beverage sector

by Kenya. These projects represent a total capital investment of ZAR6.88bn which is an average investment of

ZAR209m per project. During the period, a total of 6,329 jobs were created.

Source: FDI Intelligence, 2016

2003 2005 2006 2008 2010 2011 2012 2013 2014 2015

Capex (ZARm) 422 117 223 1 073 184 867 1 503 1 619 389 480

Projects 1 1 1 5 1 4 8 7 2 3

1

2

3

4

5

6

7

8

9

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Pro

jects

Valu

e (

ZA

Rm

)

KENYA'S OUTWARD FDI INTO FOOD & BEVERAGE SECTOR, 2003-AUGUST 2015

20

Uganda was the largest destination FDI market for food and beverages from Kenya from 2003 to August 2015,

followed by Tanzania and Rwanda with 8 investment projects and 3 investment projects each. Approximately 91%

of all investments outward of Kenya were to fellow East African markets.

OUTWARD FDI FROM KENYA INTO THE FOOD, BEVERAGE & TOBACCO SECTOR, 2003- AUGUST 2015

RANK DESTINATION COUNTRY PROJECTS % PROJECTS CAPEX (ZARm) % CAPEX COMPANIES

1 Uganda 15 45.45% 2 822.6 41.04% 8

2 Tanzania 8 24.24% 1 452.9 21.12% 3

3 Rwanda 3 9.09% 448.8 6.52% 2

4 South Sudan 3 9.09% 583.5 8.48% 2

5 Ethiopia 1 3.03% 194.5 2.83% 1

6 Germany 1 3.03% 421.8 6.13% 1

7 India 1 3.03% 301.1 4.38% 1

8 Nigeria 1 3.03% 652.6 9.49% 1

TOTAL 33 100.0 6 877.9 100.0 11

Source: FDI Intelligence, 2016

The food and beverages stores subsector received the largest investments from Kenya both in terms of projects

(76% share) and capex (63% share) from 2003 to August 2015. This was followed by fruit and vegetables and

dairy products.

Source: FDI Intelligence, 2016

75.76%

9.09%

6.06%

6.06%

3.03%

62.69%

14.63%

13.61%

5.83%

3.24%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Food & Beverage Stores

Fruits & vegetables & specialist foods

Dairy products

Grains & oilseed

Breweries & distilleries

KENYA OUTWARD FDI INTO THE FOOD & BEVERAGE SECTOR BY SUBSECTORS, 2003-AUGUST 2015

% Capex % Projects

21

Uchumi Supermarkets was the largest investor from Kenya accounting for 36% of all projects from 2003 to August

2015, followed by Nakumatt Holdings with 27% share.

COMPANIES INVESTING FROM KENYA INTO THE FOOD & BEVERAGE SECTOR, 2003-AUGUST 2015

INVESTING COMPANY PROJECTS CAPEX (ZARbn)

Uchumi Supermarkets 12 2 277

Nakumatt Holdings 9 1 257

Naivas Supermarket 4 778

Bidco Oil Refineries (BIDCO) 1 284

BIDCO Uganda 1 117

Brookside Dairy 1 653

Kenn Foods 1 422

Kenya Maltings 1 223

SAMEER Agriculture and Livestock Limited (SALL)

1 284

Sameer Group 1 284

TOTAL FROM TOP 10 INVESTORS 33 6 878

Source: FDI Intelligence, 2016

4.3 Bilateral FDI between South Africa and Kenya

Between January 2003 and August 2015 a total of 2 FDI projects were recorded from South Africa into Kenya’s

food and beverage sector. These projects represent a total capital investment of ZAR365.57m which is an average

investment of ZAR182.79m per project. During the period, a total of 360 jobs were created.

FDI FROM SOUTH AFRICA INTO THE KENYAN FOOD & BEVERAGES SECTOR, 2003- AUG 2015

DATE INVESTING COMPANY SOURCE

PROVINCE INDUSTRY SECTOR

SUB-SECTOR INDUSTRY ACTIVITY

VALUE (ZARm)

Aug 2004 Nutro Manufacturing EPZ Gauteng Food & Tobacco Grains & oilseed Manufacturing 72.65

May 2004 Coca-Cola Sabco Eastern Cape Beverages Soft drinks & ice Manufacturing 292.93

Source: FDI Intelligence, 2016

There was no FDI from Kenya into the South African food and beverages sector.

There was no inward investment into the food and beverage sector from Kenya into the Western Cape, nor was

there outward investment from the Western Cape to Kenya.

For more information on this publication and other Wesgro publications please contact [email protected] or for more

publications visit the Wesgro publications portal on our website at http://wesgro.co.za/publications