ke 2001 2003 tables for assured lives - home...

TRANSCRIPT

Presentation to the

Regional Congress of Actuaries in Africa

The Kenyan Mortality Tables: KE 2001 - 2003

Crowne Plaza Hotel – Nairobi

3 – 4 November 2011

KE 2001 – 2003

Tables for Assured Lives

Page 2 Slide 2

Agenda

Introduction and Overview of Study

Review of Data Collection Exercise

Summary of Data

Methodology

Period of Investigation

Graduation of Crude Rates

Individual Life, Group Life and Annuitants

Recommendations

Page 3 Slide 3

Introduction and Background

Project entailed an investigation of mortality and

morbidity experience of insured lives in Kenya

Project undertaken in four phases: July 2005 to July 2007

Phase I - mortality experience of individual assured lives

Phase II –mortality experience of group assured lives

Phase III - study of mortality experience of annuitants

Phase IV - study of morbidity (sickness) rates

Completed investigations for all 4 phases and released

final reports

Comments and recommendations from peer review

actuaries (Quindiem Consulting Actuaries) incorporated

in all our final reports

Period of investigation 2001 to 2003 inclusive

Page 4 Slide 4

Review of Data Collection Exercise

Most onerous task of the mortality study and

morbidity study

Data collection exercise commenced in July 2005

18 life companies requested to provide individual life

assured data and group life data

7 companies requested for annuitants data and 10 for

morbidity data

Each company provided with a copy of the data

required and format for the mortality study

Important that all companies participate

Page 5 Slide 5

Review of Data Collection Exercise

Exposure data requested

Data requested for all in-force policies as at 31

December 2000, 2001, 2002, 2003 and 2004

Claims data requested

Data requested for all death claims notified in the

years 2001, 2002, 2003 and 2004

„Principle of Correspondence‟ critical

Page 6 Slide 6

Review of Data Collection Exercise

Significant delays in the data collection exercise

Main reasons for delays in data collection exercise :

Necessary personnel not assigned by insurance companies for the specific purpose of the mortality investigation

Data not readily available or accessible from the different insurance companies

Some companies still hold data in manual registers

Inadequate/ incomplete capture of data records

Inconsistencies in the data provided

Data submitted in tranches

Detailed data checks and validation carried out

Page 7 Slide 7

Review of Data Collection Exercise

A number of significant inconsistencies in data provided by some companies e.g.

Inconsistent dates of birth from one year to the next

Claims not traceable to exposure data

Duplicate lives

Missing gender

Missing dates of birth and policy issue dates

Inconsistent policy numbers from year to year

Missing policyholder names

Inconsistent data formats from year to year

Errors in data, particularly dates

Matured policies and death claims included in part of the in-force data

Inconsistencies in year on year reconciliation

Page 8 Slide 8

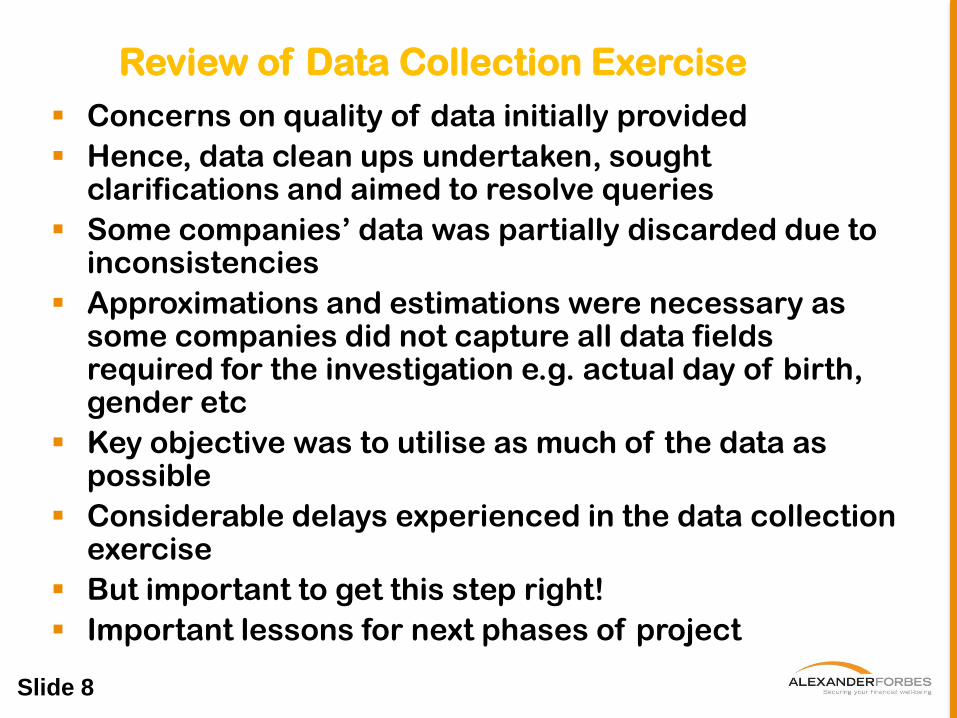

Review of Data Collection Exercise

Concerns on quality of data initially provided

Hence, data clean ups undertaken, sought clarifications and aimed to resolve queries

Some companies‟ data was partially discarded due to inconsistencies

Approximations and estimations were necessary as some companies did not capture all data fields required for the investigation e.g. actual day of birth, gender etc

Key objective was to utilise as much of the data as possible

Considerable delays experienced in the data collection exercise

But important to get this step right!

Important lessons for next phases of project

Page 9 Slide 9

Methodology

Crude mortality rate = Number of Deaths aged x

at age x Total initial exposed to risk at age x

Key principle to bear in mind – Principle of

Correspondence

A life will only be included as part of the exposed to risk

at age x if and only if were the life to die immediately,

then it would be counted as having died aged x

Necessary approximations

Age nearest birthday used as age label

Census approach used to determine crude rates

Page 10 Slide 10

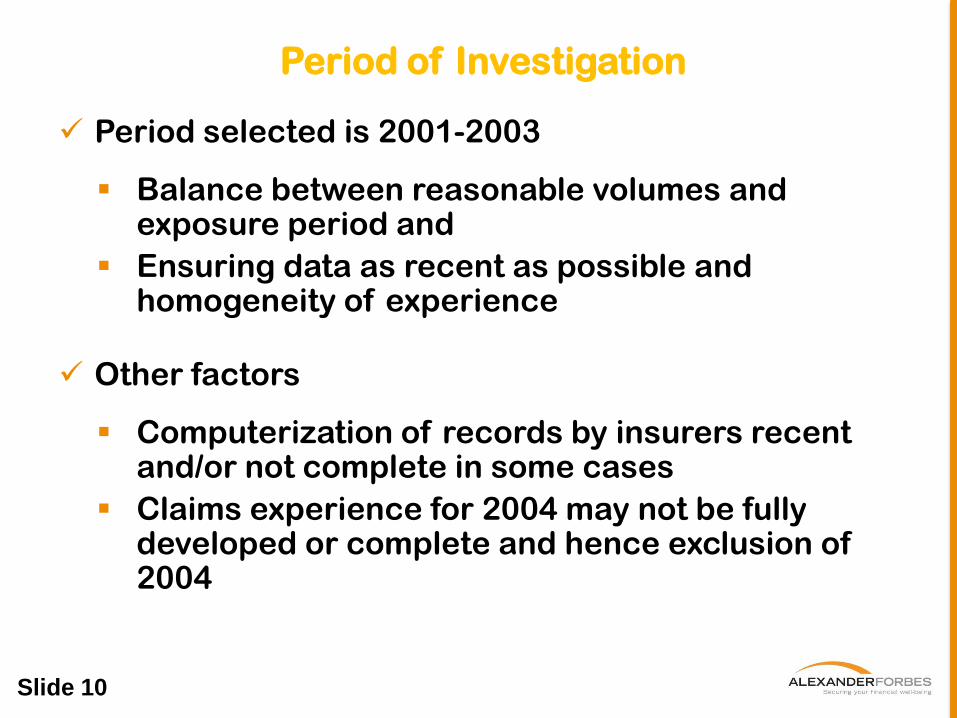

Period of Investigation

Period selected is 2001-2003

Balance between reasonable volumes and exposure period and

Ensuring data as recent as possible and homogeneity of experience

Other factors

Computerization of records by insurers recent and/or not complete in some cases

Claims experience for 2004 may not be fully developed or complete and hence exclusion of 2004

Page 11 Slide 11

Graduation of Crude Rates

Graduation of crude rates necessary in order to:

Produce set of smoothly progressing rates

(“smoothness”)

Reduce the effect of randomly observed deaths

(“goodness of fit”)

However need balance to avoid over or under

graduation

Compare graduated rates with standard published

mortality and morbidity tables commonly in use

Individual Lives

Page 13 Slide 13

Crude Rates - Males

Generally increasing trend of mortality rates

0.00

0.01

0.02

0.03

0.04

0.05

0.06

16 36 56 76 96

Rate

s

Age

Crude Rates

Page 14 Slide 14

Set of Graduated Rates

0.000

0.002

0.004

0.006

0.008

0.010

0.012

Rate

s

Age

Graduated Rates Vs Crude Rates

Graduated Rates Crude Rates

Page 15 Slide 15

Set of Graduated Rates

0.00

0.10

0.20

0.30

0.40

0.50

0.60

61

66

71

76

81

86

91

96

Rate

s

Age

Graduated Rates Vs Crude Rates

Graduated Rates Crude Rates

Page 16 Slide 16

Comparison of Graduated Rates

0.000

0.002

0.004

0.006

0.008

0.010

0.012

0.014

0.016

0.018

0.020

16

21

26

31

36

41

46

51

56

Ra

tes

Age

Comparison

Graduated Rates A1949-52 SA8590

Page 17 Slide 17

Comparison of Graduated Rates

0.00

0.10

0.20

0.30

0.40

0.50

0.60

61

66

71

76

81

86

91

96

Ra

tes

Age

Comparison

Graduated Rates A1949-52 SA8590

Page 18 Slide 18

Impact of HIV/AIDS

Apparent bulge on the graduated rates at around

ages 25-50

Bulge could be as a result of HIV/AIDS related

deaths

Analysed rates in order to calculate an estimate of

AIDS mortality

Used the SA 85-90 (light) table as a base curve to

represent non-AIDS mortality

Estimation was done using statistical techniques

including curve estimation

Page 19 Slide 19

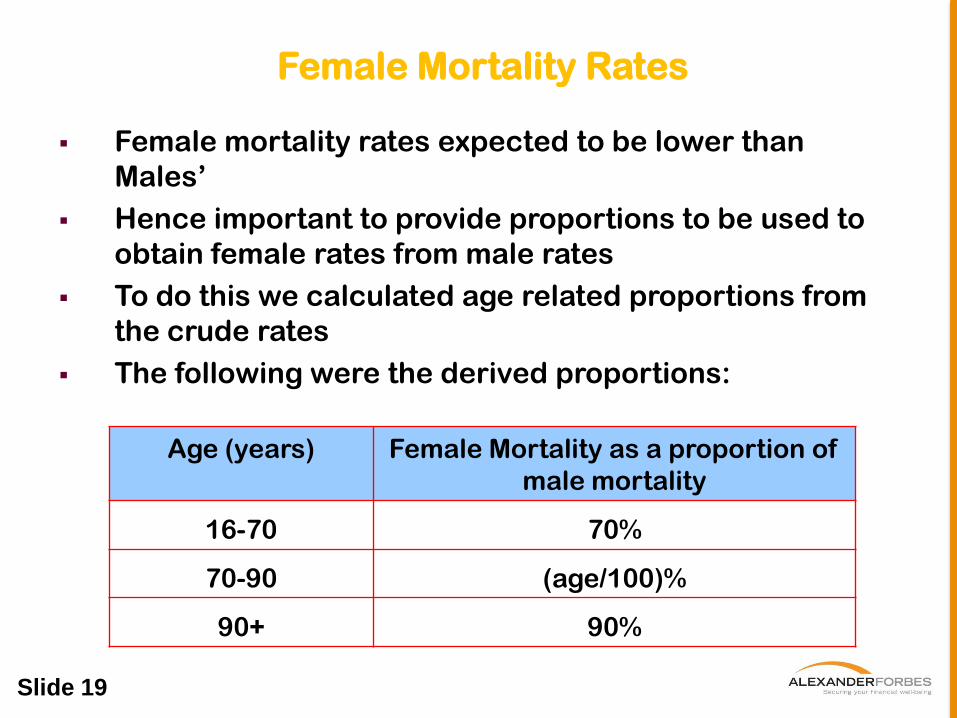

Female Mortality Rates

Female mortality rates expected to be lower than

Males‟

Hence important to provide proportions to be used to

obtain female rates from male rates

To do this we calculated age related proportions from

the crude rates

The following were the derived proportions:

Age (years) Female Mortality as a proportion of

male mortality

16-70 70%

70-90 (age/100)%

90+ 90%

Group Life

Page 21 Slide 21

Male Crude Rates

0.000

0.002

0.004

0.006

0.008

0.010

20 25 30 35 40 45 50 55

Cru

de

Rat

e

Age

Crude Rates

M

General increasing trend up to age 45 with dip thereafter

Page 22 Slide 22

Set of Graduated Rates

0.000

0.002

0.004

0.006

0.008

0.010

Rate

s

Age

Graduated Rates Vs Crude Rates

Graduated Rates Crude Rates

Page 23 Slide 23 Slide 23

Impact of AIDS

Apparent bulge on the graduated rates at around

ages 25-50

Bulge could be as a result of AIDS related deaths

Analysed rates in order to calculate an estimate of

AIDS mortality

Used the SA 85-90 (light) table as a base curve to

represent non-AIDS mortality

Estimation was done using statistical techniques

including curve estimation

Page 24 Slide 24

Female Mortality Rates

Female mortality rates expected to be lower than

Males‟

Hence important to provide proportions to be

used to obtain female rates from male rates

To do this we calculated age related proportions

from the crude rates

The following were the derived proportions:

Age (years) Female Mortality as a proportion of

Male mortality

20-55 80%

55+ (age/100)%

Annuitants

Page 26 Slide 26

Male Crude Rates

-

0.02

0.04

0.06

0.08

0.10

0.12

55

60

65

70

75

80

85

90

95

100

105

Rate

s

Age

Crude Male Rates

Crude Male …

Page 27 Slide 27

Set of Graduated Rates

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90 55

60

65

70

75

80

85

90

95

100

105

Rate

s

Age

Crude Rates Vs Graduated Rates

Grad Rates Crude Male Rates(Qx)

Page 28 Slide 28

Comparison of Graduated Rates

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.9055

60

65

70

75

80

85

90

95

100

105

Rate

s

Age

Comparison

Grad Rates A(90)-M Qx a55(m)-Qx

Page 29 Slide 29 Slide 29

Female Mortality Rates

Females data provided was scanty

Female mortality rates expected to be lower than Males

Hence important to provide proportions to be used to

obtain female rates from male rates

To do this we calculated age related proportions from

the crude rates

The following were the derived proportions:

Age (years) Female Mortality as a

proportion of male mortality

55-100 80%

100+ 100%

Recommendations

Page 31 Slide 31 Slide 31

Recommendations

Mortality studies should be carried out every 5 years

Individual lives, group life and annuity rates to be adopted

for pricing of insurance products and actuarial valuations

of long-term business

Adjustments for the effects of HIV AIDS may be necessary

Individual life rates are “ultimate rates”. However, “select

rates” dependent on policy duration may be derived

Insurance companies need to focus greatly on monitoring

the standard and quality of the data kept

Future morbidity studies need to differentiate between

group and individual rates

This possible only if companies keep proper records for

each class of business

Slide 32

Thank you for your time......