kbc morning sunrise market commentary 09-07-2011

TRANSCRIPT

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 1/10

Sunrise Market CommentaryFrom KBC Market Research Desk - More research on www.kbc.be/dealingroom

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

1

Wednesday, 07 September

Global core bonds end close to unchanged

A surprise move by the Swiss National Bank triggered temporary some risk appetite but eventually investors focussedback on what matters today: the EMU debt woes and the global recession fears. Better than expected US eco datacaused a slight extra sell-off in treasuries.

SNB puts ‘unlimited’ resources in place to cap the rise of the franc

Yesterday, the spotlights were on the SNB as it committed to prevent the CHF from strengthening beyond EUR/CHF1.20. The action of the SNB also had some temporary spill-over effects on other major currency cross rates. However,the global picture hasn’t changed. The euro continues to fight an uphill battle.

News & Calendar: Confidence picks up in the US services sector

Sunrise Headlines

US Equities opened sharply lower after the long weekend, but reversed some of the losses supported by stronger economic data. This morning, Asian shares tradein positive territory, gaining 1.5-2%.

The Swiss National Bank surprised markets yesterday by setting a ceiling for the Swiss franc against the euro as previous measures to weaken its currencyproved ineffective as the worsening euro zone crisis prompted a flight to safety byinvestors.

According to US media, US President Obama plans to propose some $300 bil-lion in tax cuts and government spending to be announced tomorrow in a na-tionally televised speech to Congress.

Italy’s centre right government caved in to pressure from bond markets andEuropean partners late yesterday by announcing a last-minute U-turn tostrengthen Italy’s austerity package.

The Bank of Japan kept is policy unchanged this morning , saving its ammuni-tion for later as the yen stabilized in the wake of Switzerland’s radical action. Thecentral bank maintained its assessment that the economy was steadily picking up

after the devastating earthquake and tsunami.

Minneapolis Fed President Kocherlakota, who opposed the Fed’s last move toease monetary policy signaled yesterday he may balk again if fellow policymak-ers opt for still more stimulus this month.

Australia’s economy grew by 1.2% Q/Q last quarter, the fastest pace in four years, beating forecasts and more than recouping the first quarter’s flood-drivendecline. The Australian dollar strengthened this morning.

Today, the eco calendar contains the German and UK industrial production data.The Fed will publish its Beige Book and the Swedish Riskbank and Bank of Canadawill decide on rates.

S&P

Eurostoxx50

Nikkei

Oil

CRB

Gold

2 yr US 10 yr US

2 yr EMU

10 yr EMU

EUR/USD

USD/JPY

EUR/GBP

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 2/10

Sunrise Market Commentary

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

2

Wednesday, 07 September

Markets: Fixed Income

On Tuesday, the Swiss National Bank surprised markets by setting a minimumexchange rate at CHF 1.20 per euro because the current massive overvalua-

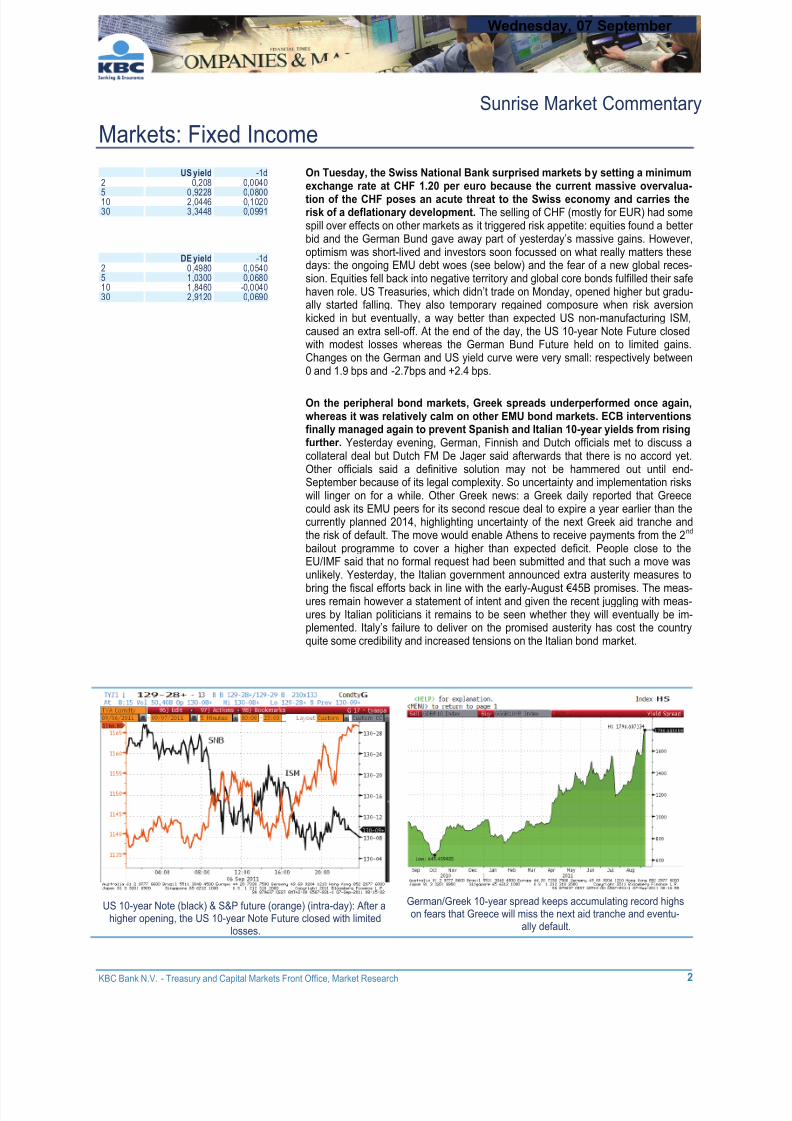

tion of the CHF poses an acute threat to the Swiss economy and carries therisk of a deflationary development. The selling of CHF (mostly for EUR) had somespill over effects on other markets as it triggered risk appetite: equities found a better bid and the German Bund gave away part of yesterday’s massive gains. However,optimism was short-lived and investors soon focussed on what really matters thesedays: the ongoing EMU debt woes (see below) and the fear of a new global reces-sion. Equities fell back into negative territory and global core bonds fulfilled their safehaven role. US Treasuries, which didn’t trade on Monday, opened higher but gradu-ally started falling. They also temporary regained composure when risk aversionkicked in but eventually, a way better than expected US non-manufacturing ISM,caused an extra sell-off. At the end of the day, the US 10-year Note Future closedwith modest losses whereas the German Bund Future held on to limited gains.Changes on the German and US yield curve were very small: respectively between0 and 1.9 bps and -2.7bps and +2.4 bps.

On the peripheral bond markets, Greek spreads underperformed once again,whereas it was relatively calm on other EMU bond markets. ECB interventionsfinally managed again to prevent Spanish and Italian 10-year yields from risingfurther. Yesterday evening, German, Finnish and Dutch officials met to discuss acollateral deal but Dutch FM De Jager said afterwards that there is no accord yet.Other officials said a definitive solution may not be hammered out until end-September because of its legal complexity. So uncertainty and implementation riskswill linger on for a while. Other Greek news: a Greek daily reported that Greececould ask its EMU peers for its second rescue deal to expire a year earlier than thecurrently planned 2014, highlighting uncertainty of the next Greek aid tranche andthe risk of default. The move would enable Athens to receive payments from the 2

nd

bailout programme to cover a higher than expected deficit. People close to theEU/IMF said that no formal request had been submitted and that such a move wasunlikely. Yesterday, the Italian government announced extra austerity measures to

bring the fiscal efforts back in line with the early-August €45B promises. The meas-ures remain however a statement of intent and given the recent juggling with meas-ures by Italian politicians it remains to be seen whether they will eventually be im-plemented. Italy’s failure to deliver on the promised austerity has cost the countryquite some credibility and increased tensions on the Italian bond market.

US 10-year Note (black) & S&P future (orange) (intra-day): After ahigher opening, the US 10-year Note Future closed with limited

losses.

German/Greek 10-year spread keeps accumulating record highson fears that Greece will miss the next aid tranche and eventu-

ally default.

DE yield -1d2 0,4980 0,05405 1,0300 0,068010 1,8460 -0,004030 2,9120 0,0690

US yield -1d2 0,208 0,0040

5 0,9228 0,080010 2,0446 0,102030 3,3448 0,0991

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 3/10

Sunrise Market Commentary

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

3

Wednesday, 07 September

This week, a lot of talk is scheduled. Today, the EFSF bill will be introduced in theBundestag, but final ratification is only expected around September 29. The GermanConstitutional Court will decide on Wednesday on some complaints about the Greekbailout packages. The top court is expected to grant parliament more say over futureaid payments, but stop short of blocking Berlin’s contributions to previous bailout

packages. The ECB meeting on Thursday will be closely monitored, especiallystatements about the SMP-programme. Finally, Friday is the deadline for non-binding offers for the private sector involvement in Greece. Remember FMVenizelos’ call that Greece might pull the plug if the targeted 90% involvement isn’treached. The G-7 Ministers of Finances will meet and discuss the global outlook andthe euro debt crisis. Uncertainty will once again prevail this week and implementa-tion risks are still elevated. Unless the ECB steps in more pronounced than pre-vious weeks, the spreads versus Germany will remain under pressure andwiden further .

Today, the eco calendar is light with only the German and UK industrial productionfigures scheduled for release. After the Bank of Japan this morning, also the Swed-ish Riksbank and Bank of Canada will decide on rates, but more attention will go outto the publication of the Fed’s Beige Book. Besides the Beige Book, the euro zonedebt crisis will remain in the focus of markets as the German Bundestag meets on

the 2nd Greek aid, EU’s Rehn speaks on the Greek economy at the EU parliamentand Portugal will tap the market (T-Bills).

In Germany, industrial production is forecast to have picked up in July after a1.1% M/M decline in June. In the second quarter, German production slowed con-siderably after an excellent start of the year. All available evidence suggests thatweakness will persist in the third quarter with a further slowdown not excluded. Theconsensus is looking for a 0.5% M/M increase but we believe that a downward sur-prise is not excluded after the disappointing sentiment indicators of recent and theweak factory orders yesterday. Also in the UK, the consensus is looking for an in-crease in industrial production by 0.2% M/M, but manufacturing production is fore-cast to have stabilized in July. Also for the British figure, we see the risks on thedownside.

Yesterday, the Austrian treasury tapped the on the run 7-year RAGB (3.2%Feb2017) and the on the run 40-year RAGB (4.15% Mar2037) for a combinedamount of €1.2B (competitive) plus €0.12B (quota of the bund). The AAA-ratedbonds met with good demand. Bid covers were respectively 2.05 and 2.37.

Minneapolis Fed Kocherlakota, who opposed last months further easing of policy,said he may dissent again if his colleagues call for further accommodative action:“The data in August did not justify the additional accommodation provided at that moment . It is unlikely that the data in September will warrant adding still more ac-commodation.” Mid-September, the FOMC has a two-day meeting and the recentflattening of the US yield curve suggests markets are anticipating on the Fed an-nouncement of an “Operation Twist”, in which short term Treasuries will be sold for longer Treasuries. Richmond Fed Lacker, non-voting inflation hawk in the FOMC,warned that further monetary stimulus would fuel inflation without doing much tolower unemployment. Lacker also said he understood but disagreed with Chicago

Fed Evans’ for extra stimulus and his suggestion that a temporarily higher inflation of 3% wouldn’t be a catastrophe: “That case depends critically on the credibility of thecentral bank, on the credibility of their commitment to raise inflation and then lower it later. I don’t view our credibility as complete and solidly enough grounded to be ableto pull that off.”

R2 136,84 -1dR1 136,61BUND 136,12 -9,3200S1 136,07S2 135,79

Technicals Dec! Bund

The LT technical picture of the Bundis bullish, but the market is overex-tended and exhaustion may set thestage for profit taking, if tensions for whatever raison would ease. So,protection of longs may be war-ranted.

On the downside, support stands at136.07(S1,reaction low hourly), at135.79 (S2, STMA), at 135.35 (S3,

current week low) and at 134.29(S4, MTMA).

On the topside, resistance standsat 136.61 (R1, gap hourly) at 136.84(R2, Bollinger top) and at 137.27(R3, new contract high).

The contract is in overextendedconditions.

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 4/10

Sunrise Market Commentary

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

4

Wednesday, 07 September

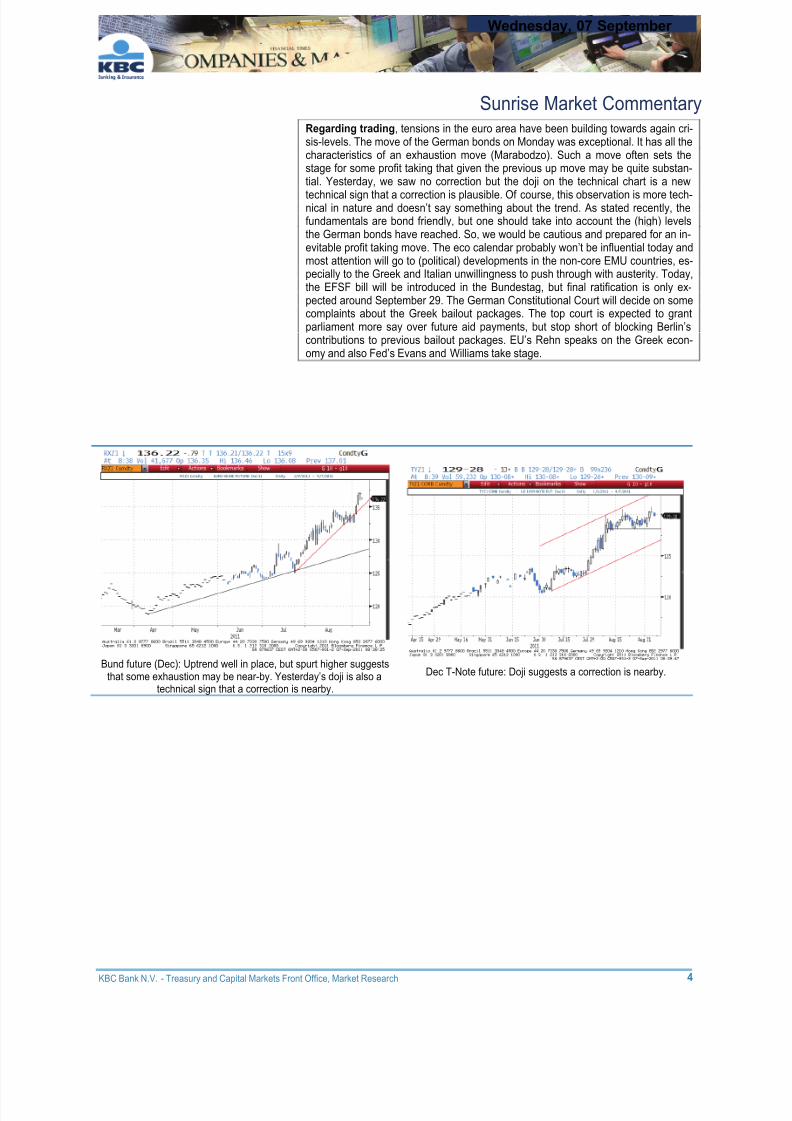

Regarding trading, tensions in the euro area have been building towards again cri-sis-levels. The move of the German bonds on Monday was exceptional. It has all thecharacteristics of an exhaustion move (Marabodzo). Such a move often sets thestage for some profit taking that given the previous up move may be quite substan-tial. Yesterday, we saw no correction but the doji on the technical chart is a new

technical sign that a correction is plausible. Of course, this observation is more tech-nical in nature and doesn’t say something about the trend. As stated recently, thefundamentals are bond friendly, but one should take into account the (high) levelsthe German bonds have reached. So, we would be cautious and prepared for an in-evitable profit taking move. The eco calendar probably won’t be influential today andmost attention will go to (political) developments in the non-core EMU countries, es-pecially to the Greek and Italian unwillingness to push through with austerity. Today,the EFSF bill will be introduced in the Bundestag, but final ratification is only ex-pected around September 29. The German Constitutional Court will decide on somecomplaints about the Greek bailout packages. The top court is expected to grantparliament more say over future aid payments, but stop short of blocking Berlin’scontributions to previous bailout packages. EU’s Rehn speaks on the Greek econ-omy and also Fed’s Evans and Williams take stage.

Bund future (Dec): Uptrend well in place, but spurt higher suggeststhat some exhaustion may be near-by. Yesterday’s doji is also a

technical sign that a correction is nearby.

Dec T-Note future: Doji suggests a correction is nearby.

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 5/10

Sunrise Market Commentary

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

5

Wednesday, 07 September

Currencies: SNB puts ‘unlimited’ resources in place to cap the rise of the franc

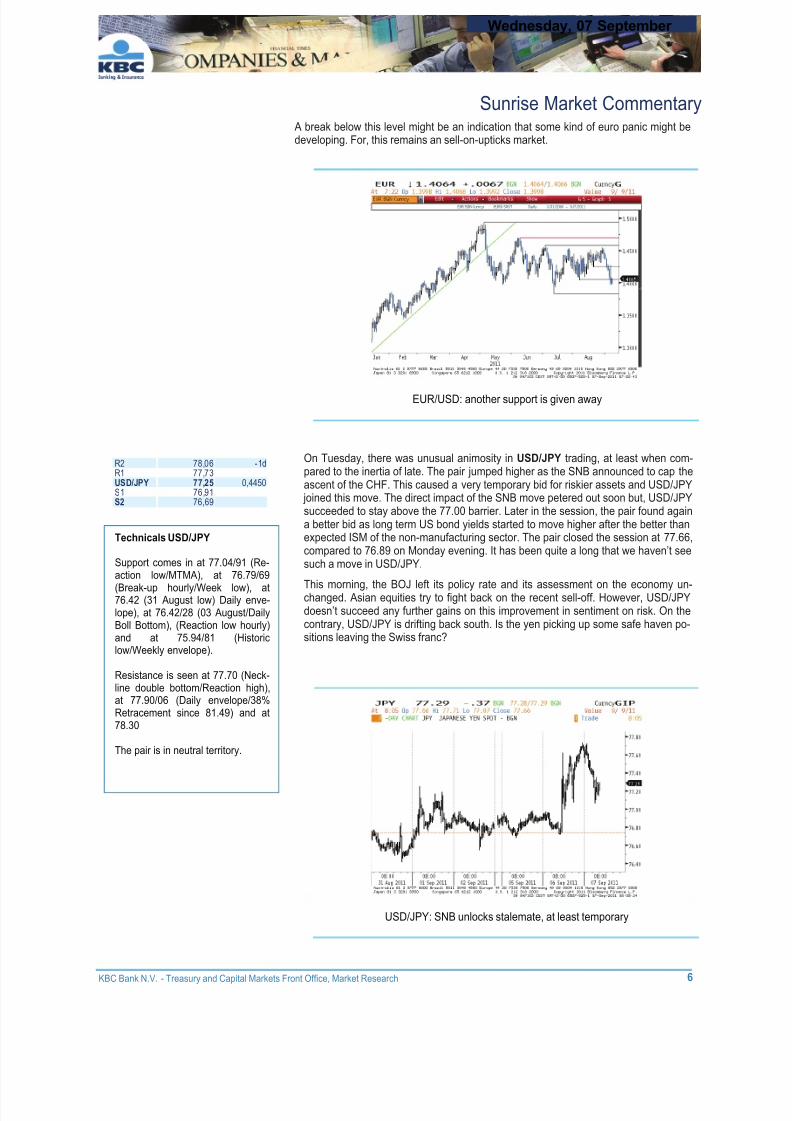

On Tuesday, EUR/USD traders faced an unexpected intermezzo on the one-way de-cline. At the start of the session, it looked that another risk-off day would be on the

cards as there was no indication that Europe was making any progress in solving itsdebt crisis. On the contrary, German policymakers continued to signal that they werenot prepared to ease the conditions for aid to other EMU countries. There was a verylimited rebound on the European equity markets after Monday’s sell-off, but this im-provement was very limited compared to Monday’s losses. So, EUR/USD held close tothe reaction low in the 1.4050/1.041 area. However, this crisis already several timesdemonstrated that is it dangerous to take any development for granted. The Swiss Na-tional Bank announced that the CHF had become much to strong and that it aimed asubstantial and sustained weakening of the CHF. The SNB will no longer tolerated theCHF to be stronger than EUR/CHF 1.20 and is prepared to buy foreign currency inunlimited quantities. EUR/CHF spiked to the target level of 1.20 after the announce-ment. At the same time, EUR/USD gained also two big figures as the major part of theinterventions will probably be executed via the euro. In addition, the SNB interventionsalso caused a very temporary improvement in sentiment on riskier assets. However,this Pavlov reaction was very short-lived as there was no perspective that the debt cri-

sis in Europe would improve anytime soon. The EMU data (GDP revision and Germanfactory orders) were also weaker than expected. So, EUR/USD gradually slipped southagain and the correction accelerated when US traders rejoined the action. EUR/USDalready reached a minor intraday low in the 1.4030 area early in US dealings. The ISMof the non-manufacturing sector in the US was better than expected. However, the re-port hardly slowed the selling in EUR/USD. The cross rate closed the session at1.3998, compared to 1.4098 on Monday evening.

On the borders of the EMU we also have to mention the strong performance of theSwedish and the Norwegian crown. The action of the Swiss national Bank apparentlymade some investors looking for alternative safe haven currencies near the euro area.

Today, the calendar in the US is thin, but investors will keep an eye on the Fed’s BeigeBook preparing the 20/21 September FOMC meeting. However, as was the case of late the focus will be on Europe. The data (German July Industrial production). willprobably only be of second tier importance. The Spanish senate will hold a constitu-tional vote on a balanced budget. In Germany, the Constitutional Court will rule on law-suits that questioned Germany’s involvement in the bailout of other EMU member states. It is expected that the Court will give the Parliament a bigger rule in future aidpayments. This might limit the room of manoeuvre for the German government. A morestrict ruling might be another complication on the road to a ‘smooth’ solution for theEMU debt crisis. This morning, sentiment on the Asian equity markets is less negativecompared to the sell-off earlier this week. This is also easing the pressure on the eurothis morning. However, we don’t expect a profound change/Improvement in sentimenton the single currency.

Global context. Since the EU summit on July 21, EUR/USD held within a remarkablytight sideways trading range. The outcome of the meeting was unable to prevent fur-ther contagion on the EMU government bond markets. On the contrary, Italy came also

in the fire line. In theory, this should have been a negative factor for the euro. However,markets still saw a balance of weakness between the euro and the dollar as the newsflow from the US was also far from inspiring. The eco data indicated that the US mightbe at the brink of a double dip recession and the outcome of the US budget debate il-lustrated that US policymakers have no comprehensive plan to address the debt situa-tion. S&P downgrading the US AAA-credit rating reinforced this feeling and weighed onthe dollar. The Fed committing to extend an extremely accommodative policy at leastuntil 2013 was also no help for the US currency. So, EUR/USD hovered sideways in arange roughly between 1.4050 and 1.4550 in August. Since last week the EMU debtcrisis came again in the spotlights. EUR/USD started a correction off from the rangetop. The first important support (1.4259) was broken last week. The 1.4055 neckline iscurrently under test. The pressure is mounting and the 1.3837 level (12 (July low) iscoming within striking distance.

R2 1 4146 -1dR1 1 4119EUR/USD 1 4 075 3 0 0002S1 1,3959S2 1,3878

Technicals EUR/USD

Support comes in at 1.4019 (200D MA), at 1.3992 (Reactionlow/LT Daily downtrend line), at1.3972/69 (Reaction low/Monthlyenvelope), at 1.3878 (Daily enve-lope) and at 1.3837 (12 Julylow).

Resistance stands at 1.4119(STMA), at 1.4146 (Breakdownhourly), at 1.4286/88 (Reactionhighs), at 1.4308 (MTMA) and at1.43059(Breakdown daily).

The pair is in oversold territory.

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 6/10

Sunrise Market Commentary

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

6

Wednesday, 07 September

A break below this level might be an indication that some kind of euro panic might bedeveloping. For, this remains an sell-on-upticks market.

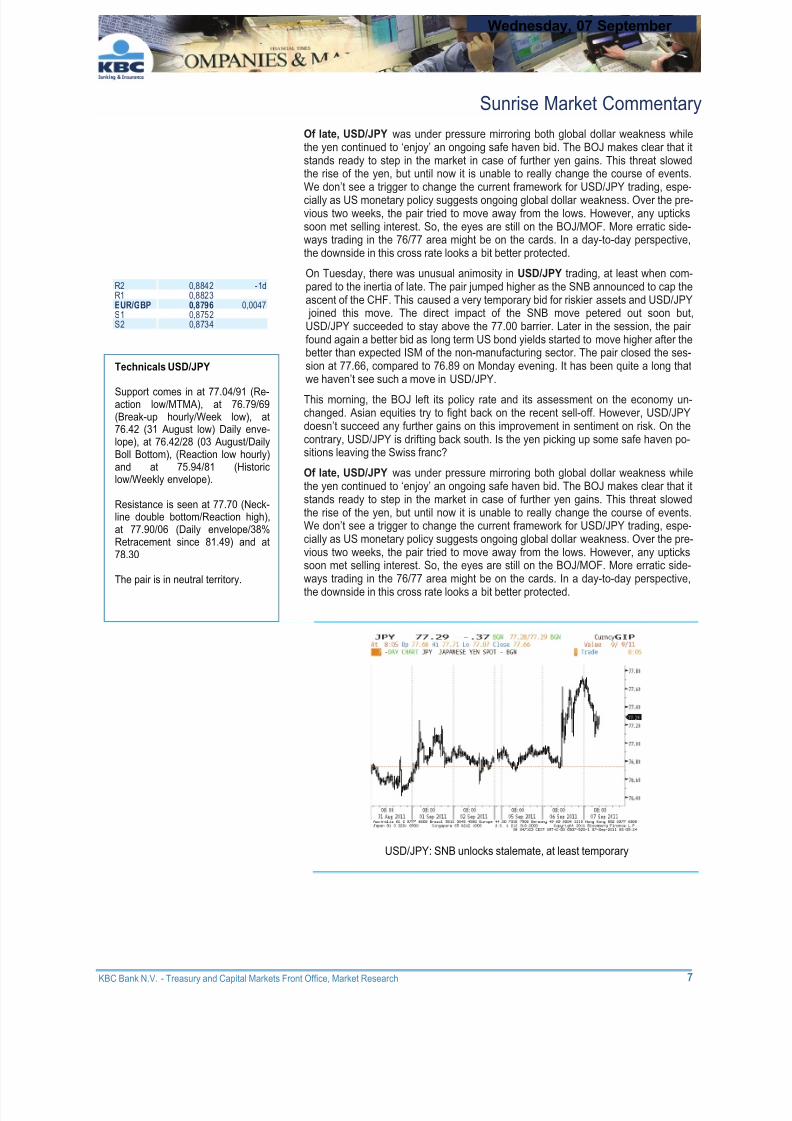

On Tuesday, there was unusual animosity in USD/JPY trading, at least when com-pared to the inertia of late. The pair jumped higher as the SNB announced to cap theascent of the CHF. This caused a very temporary bid for riskier assets and USD/JPY

joined this move. The direct impact of the SNB move petered out soon but, USD/JPYsucceeded to stay above the 77.00 barrier. Later in the session, the pair found againa better bid as long term US bond yields started to move higher after the better thanexpected ISM of the non-manufacturing sector. The pair closed the session at 77.66,compared to 76.89 on Monday evening. It has been quite a long that we haven’t seesuch a move in USD/JPY.

This morning, the BOJ left its policy rate and its assessment on the economy un-changed. Asian equities try to fight back on the recent sell-off. However, USD/JPYdoesn’t succeed any further gains on this improvement in sentiment on risk. On thecontrary, USD/JPY is drifting back south. Is the yen picking up some safe haven po-sitions leaving the Swiss franc?

EUR/USD: another support is given away

USD/JPY: SNB unlocks stalemate, at least temporary

R2 78,06 -1dR1 77,73USD/JPY 77,25 0,4450S1 76,91S2 76,69

Technicals USD/JPY

Support comes in at 77.04/91 (Re-action low/MTMA), at 76.79/69

(Break-up hourly/Week low), at76.42 (31 August low) Daily enve-lope), at 76.42/28 (03 August/DailyBoll Bottom), (Reaction low hourly)and at 75.94/81 (Historiclow/Weekly envelope).

Resistance is seen at 77.70 (Neck-line double bottom/Reaction high),at 77.90/06 (Daily envelope/38%Retracement since 81.49) and at78.30

The pair is in neutral territory.

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 7/10

Sunrise Market Commentary

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

7

Wednesday, 07 September

Of late, USD/JPY was under pressure mirroring both global dollar weakness whilethe yen continued to ‘enjoy’ an ongoing safe haven bid. The BOJ makes clear that itstands ready to step in the market in case of further yen gains. This threat slowedthe rise of the yen, but until now it is unable to really change the course of events.We don’t see a trigger to change the current framework for USD/JPY trading, espe-

cially as US monetary policy suggests ongoing global dollar weakness. Over the pre-vious two weeks, the pair tried to move away from the lows. However, any uptickssoon met selling interest. So, the eyes are still on the BOJ/MOF. More erratic side-ways trading in the 76/77 area might be on the cards. In a day-to-day perspective,the downside in this cross rate looks a bit better protected.

On Tuesday, there was unusual animosity in USD/JPY trading, at least when com-pared to the inertia of late. The pair jumped higher as the SNB announced to cap theascent of the CHF. This caused a very temporary bid for riskier assets and USD/JPY

joined this move. The direct impact of the SNB move petered out soon but,USD/JPY succeeded to stay above the 77.00 barrier. Later in the session, the pair found again a better bid as long term US bond yields started to move higher after thebetter than expected ISM of the non-manufacturing sector. The pair closed the ses-sion at 77.66, compared to 76.89 on Monday evening. It has been quite a long thatwe haven’t see such a move in USD/JPY.

This morning, the BOJ left its policy rate and its assessment on the economy un-changed. Asian equities try to fight back on the recent sell-off. However, USD/JPYdoesn’t succeed any further gains on this improvement in sentiment on risk. On thecontrary, USD/JPY is drifting back south. Is the yen picking up some safe haven po-sitions leaving the Swiss franc?

Of late, USD/JPY was under pressure mirroring both global dollar weakness whilethe yen continued to ‘enjoy’ an ongoing safe haven bid. The BOJ makes clear that itstands ready to step in the market in case of further yen gains. This threat slowedthe rise of the yen, but until now it is unable to really change the course of events.We don’t see a trigger to change the current framework for USD/JPY trading, espe-cially as US monetary policy suggests ongoing global dollar weakness. Over the pre-vious two weeks, the pair tried to move away from the lows. However, any uptickssoon met selling interest. So, the eyes are still on the BOJ/MOF. More erratic side-ways trading in the 76/77 area might be on the cards. In a day-to-day perspective,

the downside in this cross rate looks a bit better protected.

USD/JPY: SNB unlocks stalemate, at least temporary

R2 0,8842 -1dR1 0,8823EUR/GBP 0,8796 0,0047S1 0,8752S2 0,8734

Technicals USD/JPY

Support comes in at 77.04/91 (Re-action low/MTMA), at 76.79/69(Break-up hourly/Week low), at76.42 (31 August low) Daily enve-lope), at 76.42/28 (03 August/DailyBoll Bottom), (Reaction low hourly)and at 75.94/81 (Historiclow/Weekly envelope).

Resistance is seen at 77.70 (Neck-line double bottom/Reaction high),at 77.90/06 (Daily envelope/38%Retracement since 81.49) and at78.30

The pair is in neutral territory.

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 8/10

Sunrise Market Commentary

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

8

Wednesday, 07 September

NewsUS: confidence picks up in the services sector

In August, the US non-manufacturing ISM unexpectedly improved. The headline

index rose from 52.7 to 53.3, reversing previous month’s decline, while the consen-sus was looking for a drop to 51.0. The details show a mixed picture as business ac-tivity (55.6 from 56.1), inventory change (53.5 from 56.5), inventory sentiment (56.0from 59.5) and employment (51.6 from 52.5) deteriorated, while new orders (52.8from 51.7) picked up slightly. Backlog of orders (47.5 from 44.0), supplier deliveries(53.0 from 50.5), new export orders (56.5 from 49.0) and imports (53.5 from 47.5)showed a more significant increase. Cost pressures accelerated again in August asprices paid jumped significantly from 56.1 to 64.2. While both employment andbusiness activity weakened in August, the outlook is more encouraging asboth new orders and new export orders picked up, boding well for the comingmonths. After already an upward surprise in the manufacturing ISM, this out-come suggests that analysts had become too pessimistic. Nevertheless, therisks for a double dip recession remain in place as the manufacturing ISM is atstagnation levels and especially as the labour market remains extremely weak.

EMU: net-exports supported growth in Q2The preliminary estimate of euro zone Q2 GDP confirmed the first estimate, show-ing only meagre growth. In the euro area, GDP expanded by 0.2% Q/Q in the April toJune period, as suggested by the first estimate. More interesting was the first releaseof the details, which were disappointing too. Household consumption fell by 0.2%Q/Q (from 0.2% Q/Q in Q1), while a decline by 0.1% Q/Q was expected and gov-ernment spending contracted unexpectedly (-0.2% Q/Q from 0.4% Q/Q). Gross fixedcapital formation slowed more than expected, posting only a 0.2% Q/Q increase(from 1.8% Q/Q in Q1), while a 0.8% Q/Q rise was expected. Both exports (1.0%Q/Q) and imports (0.5% Q/Q) held up relatively well, adding 0.2% Q/Q to growth andalso change in inventories made a positive contribution to growth (0.1% Q/Q). Thedrag from household consumption was somewhat bigger than expected andalso investments slowed more than forecasted, which makes the report some-what weaker than expected. The positive contribution from net-exports is posi-

tive news, but the outlook is less so as recent data suggested that export or-ders are slowing sharply due to the global economic slowdown.

In July, German factory orders surprised on the downside of expectations, fallingby 2.8% M/M while a decline by 1.5% M/M was expected. The correction is nosurprise as orders rose significantly in each of the previous three months, buta more moderate decline was expected. The details show that weakness wasbased in foreign orders (-7.4% M/M), especially from non-EMU countries (-10.2%M/M), but also orders from euro area member states dropped (by 3.3% M/M) in July.Domestic orders, on the contrary, rebounded by 3.6% M/M after a 10.1% M/M de-cline. The sector breakdown indicates that orders for capital goods fell by 7.0% M/M,while orders for intermediate (2.9% M/M) and consumer (4.5% M/M) goods rose inJuly.

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 9/10

Sunrise Market Commentary

KBC Bank N.V. - Treasury and Capital Markets Front Office, Market Research

9

Wednesday, 07 September

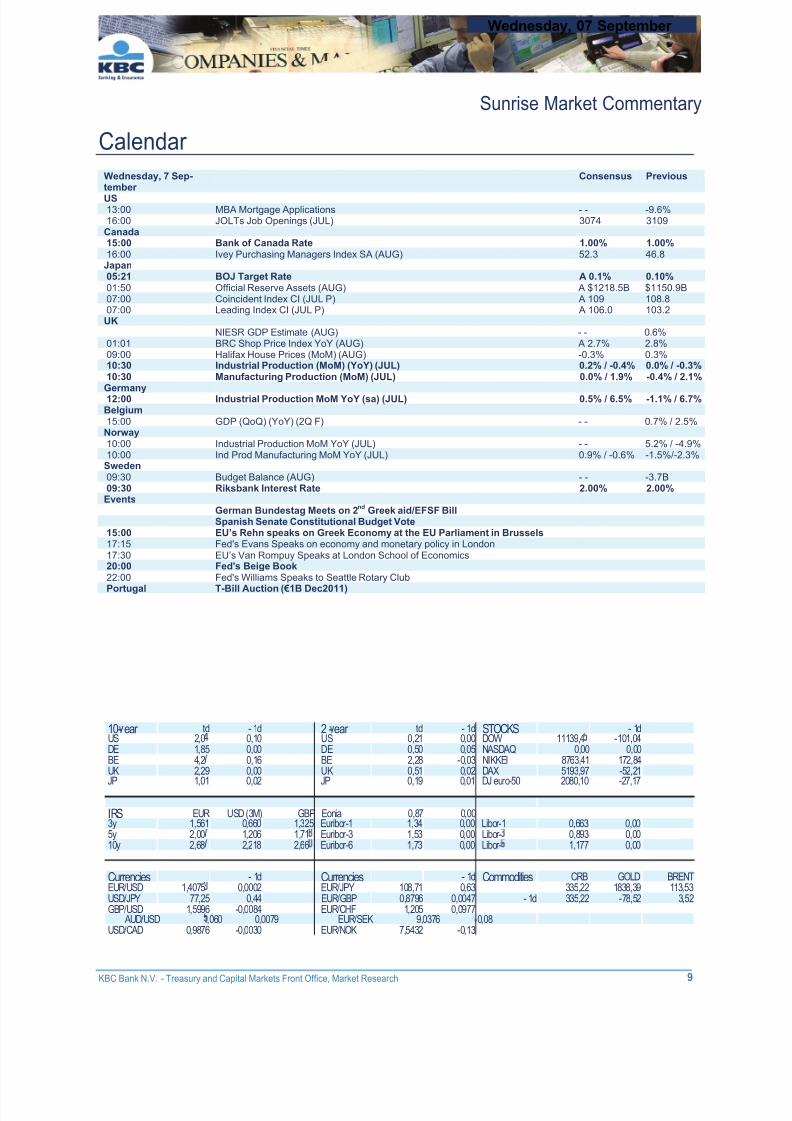

Calendar

Wednesday, 7 Sep-tember

Consensus Previous

US13:00 MBA Mortgage Applications - - -9.6%16:00 JOLTs Job Openings (JUL) 3074 3109Canada15:00 Bank of Canada Rate 1.00% 1.00%16:00 Ivey Purchasing Managers Index SA (AUG) 52.3 46.8Japan05:21 BOJ Target Rate A 0.1% 0.10%01:50 Official Reserve Assets (AUG) A $1218.5B $1150.9B07:00 Coincident Index CI (JUL P) A 109 108.807:00 Leading Index CI (JUL P) A 106.0 103.2UK

NIESR GDP Estimate (AUG) - - 0.6%01:01 BRC Shop Price Index YoY (AUG) A 2.7% 2.8%09:00 Halifax House Prices (MoM) (AUG) -0.3% 0.3%10:30 Industrial Production (MoM) (YoY) (JUL) 0.2% / -0.4% 0.0% / -0.3%10:30 Manufacturing Production (MoM) (JUL) 0.0% / 1.9% -0.4% / 2.1%

Germany12:00 Industrial Production MoM YoY (sa) (JUL) 0.5% / 6.5% -1.1% / 6.7%Belgium15:00 GDP (QoQ) (YoY) (2Q F) - - 0.7% / 2.5%Norway10:00 Industrial Production MoM YoY (JUL) - - 5.2% / -4.9%10:00 Ind Prod Manufacturing MoM YoY (JUL) 0.9% / -0.6% -1.5%/-2.3%Sweden09:30 Budget Balance (AUG) - - -3.7B09:30 Riksbank Interest Rate 2.00% 2.00%Events

German Bundestag Meets on 2nd

Greek aid/EFSF BillSpanish Senate Constitutional Budget Vote

15:00 EU’s Rehn speaks on Greek Economy at the EU Parliament in Brussels17:15 Fed's Evans Speaks on economy and monetary policy in London17:30 EU’s Van Rompuy Speaks at London School of Economics20:00 Fed's Beige Book22:00 Fed's Williams Speaks to Seattle Rotary Club

Portugal T-Bill Auction (€1B Dec2011)

10- ear td - 1d 2 - ear td - 1d STOCKS - 1dUS 2,0 0,10 US 0,21 0,00 DOW 11139,4 -101,04DE 1,85 0,00 DE 0,50 0,05 NASDAQ 0,00 0,00BE 4,2 0,16 BE 2,28 -0,03 NIKKEI 8763,41 172,84UK 2,29 0,00 UK 0,51 0,02 DAX 5193,97 -52,21

JP 1,01 0,02 JP 0,19 0,01 DJ euro-50 2080,10 -27,17

IRS EUR USD (3M) GBP Eonia 0,87 0,003y 1,561 0,660 1,325 Euribor-1 1,34 0,00 Libor-1 0,663 0,005y 2,00 1,206 1,71 Euribor-3 1,53 0,00 Libor- 0,893 0,0010y 2,68 2,218 2,66 Euribor-6 1,73 0,00 Libor- 1,177 0,00

Currencies - 1d Currencies - 1d Commodities CRB GOLD BRENTEUR/USD 1,4075 0,0002 EUR/JPY 108,71 0,63 335,22 1838,39 113,53USD/JPY 77,25 0,44 EUR/GBP 0,8796 0,0047 - 1d 335,22 -78,52 3,52GBP/USD 1,5996 -0,0084 EUR/CHF 1,205 0,0977 AUD/USD 1,060 0,0079 EUR/SEK 9,0376 -0,08USD/CAD 0,9876 -0,0030 EUR/NOK 7,5432 -0,13

8/4/2019 KBC Morning Sunrise Market Commentary 09-07-2011

http://slidepdf.com/reader/full/kbc-morning-sunrise-market-commentary-09-07-2011 10/10