kansas gfoa 16 - wichita state...

TRANSCRIPT

Kansas GFOA 16th Annual Fall Professional Conference 2015

October 15, 2015

Presented by: Barry W. Fick Senior Vice President Springsted Incorporated [email protected]

PRESENTATION TO

Which Way is Up? The Confusing, Confounding Economy

Springsted Background • Full Service Independent Municipal Advisor Firm

– 60 year history – Municipal Advisor Services (fully registered with SEC, etc.) – Management Advisory Services – Executive Recruiting – Independent Investment Group (SIA Subsidiary)

• HealthCare / Higher Education / Not For Profit Group – Community Hospitals, Not for Profit Hospitals, Univ. Med. Ctrs. – State Authorities – Private & Public individual Colleges and Universities

• www.Springsted.com – click on video link

2

Executive Summary – The Good

• United States Economy shows steady improvement – Economic production statistics showing mostly upward trend – Reported Unemployment improving, but may be misleading

• Housing is improving, but market is volatile – Home prices increasing in most markets – Mortgage rates low

• Qualification is challenging – Foreclosures declining as projected – 1 in 7 Homeowners remain “Underwater” on their mortgage

• Interest rates not likely to rise much through 2015 – FOMC has very mixed signals confronting it

3

Executive Summary – The Not So Good • Pace of US Recovery remains frustratingly slow

– Labor force participation remains low – Mismatch between jobs and labor skills

• Rest of the World is in difficult circumstances – China slowdown – Europe and Greece remains complex problems – South America a growing challenge

• US Housing improving, but not incomes – Existing housing stock doesn’t match future housing demand

• Demographics presents continuing challenges

4

What’s Ahead In the Really Big Picture?

• 2016 Elections eliminate chance of reform – Tax Reform delayed – Entitlement Reform delayed – Health Care Challenges

• State and Local Gov’t – Fill leadership void – Implement fed mandates – Tax Base increasing, but

slowly

5

6 6 6

Economic Background – 2008 Meltdown • 2008 Great Recession – Causes

– Balance Sheet Recession • Asset values declined • Liability values remained stable

– Not demand induced – Finance induced

• Consequences – Long term recovery period – 10yr + – Increasing wealth/net worth disparity

• Demographic challenges further delay recovery

Public Finance Market General – 2015 • Continuation of low interest rates

– US Treasuries rates showing strong volatility since early August – FOMC has kept rates low to date – increase in Oct or Dec or 2016? – Volatility in bond prices from week to week changes rates by > ¼%

• Uncertainty about 2015 4Q Debt Ceiling, FOMC Action – Uncertainty is bane of bondholders – Government Shutdown possible late in 2015

• Municipal Bond Fund Inflows reversed, reducing downward pressure on rates – 19 weeks of 37 weeks in 2015 saw fund outflows of $246M/wk avg. – Retail fear of rate increases

7

Political Challenges

• Debt Ceiling – Decision needs to be made

again in 2015 (NOW) • Sequestration

– 2015 continued budget cuts – 2016 Sequestration %

• Interest Rate Increase • 2016 Election Race in Full

Swing • FOMC – Just Do It

8

Tax Exempt Yield History 1994 - 2015

9

Interest Rate Forecast • FOMC – Likely to Increase

soon – but timing is open – Chair Yellen is data dependent,

focus on “dual mandate” – Inflation and employment

• Decreasing likelihood of maintaining low rates – Fall 2015 rate rise expectation

• 10% expect October • 37% expect December • 45% expect January 2016

• Rate hike reflected in rates

10

Federal Reserve Options • Increase Fed Funds rate

– Pace of Increase will be of great concern to investors – What is “normal” level of interest rates?

• Sell some US Treasury Inventory – $4.5 Trillion inventory purchased since 2010

• No reinvestment as US Treasury matures – Effect is to reduce demand, raise rates

• Reverse course or renew Quantitative Easing – If economy regresses (due to domestic or foreign events) – 0% or negative rates – 4-wk T-bill auction Oct 11, 2015

11

Long Term Challenges Not All Financial • Demographics

– Social and Economic Challenges and Opportunities • Baby Boomers

– 8,000 to 10,000 a day turn 65 – Moving out of work force

• Millennials – Only 26% believe they will be better off than their parents – Less than 20% believe other people can be trusted (40% boomers) – Meaningful employment delayed – Outlook will improve as Boomers retire in force

• Is recent past the “New Normal”?

12

New Option – “Green Bonds” • Green Bonds are issues for environmental projects

– Wind or Solar power projects – Utility projects (water, electricity, sewer, wastewater) – Hazardous waste processing – LEED Qualified building construction

• Increasing in importance globally • Green Bonds have specific requirements to be

considered “Green Qualified” • No observed Interest Rate Benefit to date

– Expected to change – Demand by Pension Funds, European investors leading buyers

13

US Treasury Rate 2015 – 2016 Projection • Bloomberg Panel Projections – Oct. 13, 2015

14

2015 UST Mkt Proj. 4Q15 2Q16 4Q16

US 30-Year 3.08% 3.32% 3.53%

US 10-Year 2.32% 2.62% 2.87%

US 2-Year 0.88% 1.31% 1.68%

US 3-MO LIBOR 0.44% 0.89% 1.34%

Source: Bloomberg Oct. 13 Close

Historic US Treasury Rates

15

Economic Activity & Statistics - 2015

• 2015 US Growth Rate is approximately 2.75% annualized – Approaching long-term trend of 3% +/- Annual growth

• Labor Productivity Growth has slowed to 1% per year – Lower than in past and too low to accelerate US economic growth

• Consumer spending – Automobiles bellwether – Auto sales at record pace, but…

• Average loan exceeds $31,000 & 72 months • Average auto in service for 11+ years

• Deleveraging of consumer long-term debt continues – May take to late 2015 to 2016 before deleverage is complete – Offset by increasing consumer revolving credit borrowing

16

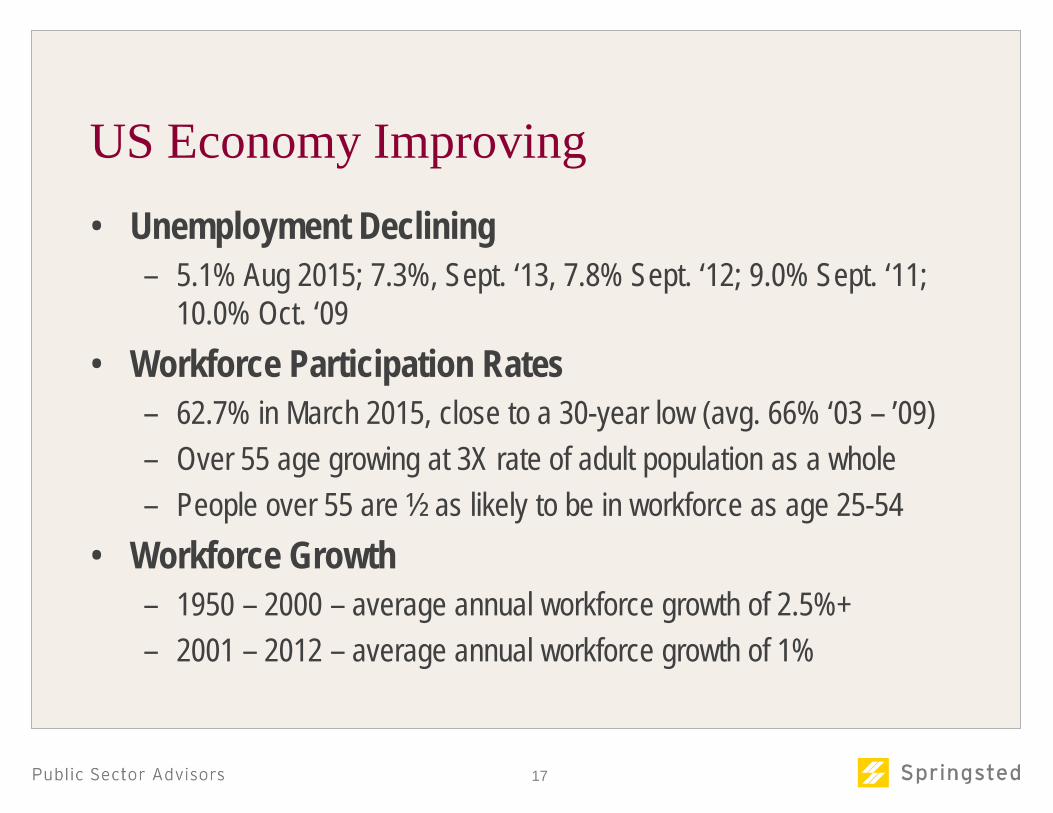

US Economy Improving • Unemployment Declining

– 5.1% Aug 2015; 7.3%, Sept. ‘13, 7.8% Sept. ‘12; 9.0% Sept. ‘11; 10.0% Oct. ‘09

• Workforce Participation Rates – 62.7% in March 2015, close to a 30-year low (avg. 66% ‘03 – ’09) – Over 55 age growing at 3X rate of adult population as a whole – People over 55 are ½ as likely to be in workforce as age 25-54

• Workforce Growth – 1950 – 2000 – average annual workforce growth of 2.5%+ – 2001 – 2012 – average annual workforce growth of 1%

17

US Economy Improving - Housing

• Property values rising 6% year over year thru August – Highest year to year gain since July 2010 – Limited supply of existing homes for sale – Rising rent cost

• Virtually all Metro Areas show price increases in 2015 • Foreclosures slowing dramatically • Avg. 30-year mortgage loan rates are low, but qualifying

is challenging – 3.98% in September 2015 – 3.35% in May 2013 – lowest rate since 1972

18

Financial Issues for Local Government • Productivity

– Increased service delivery per employee – Public Private Partnership opportunities & options – Transfer of work to lower skilled / paid staff

• Full time – Part time staffing

• Cost containment – Increased focus on shared services – Drive for large size, volume discount pricing for goods & services

• Government Regulation – Mandate w/little or no funding provided – Disclosure – Dodd/Frank & “Best Practices”

19

Financial Issues for Local Government • Revenue Growth

– Market competition – Government limitations – New Development / Rehabilitation

• Development Incentives – How to manage & use Incentives

• Capital Funding Options – Alternatives to traditional tax-exempt financing

• Tax Exemption – Can it be maintained? – Should it be maintained?

20

General Municipal Bond Rates History

21

Tax Exemption Observations • Benefits of Tax Exemptions

– Lower rates – Strong buyer base

• Challenges of Tax Exemption – Government regulation

• IRS compliance rules • State restrictions

– Small market ($3.5 trillion vs. $4.5 trillion US Treas held by FOMC) • Self Inflicted Damage

– Embrace of taxable debt (Build America Bonds) – Optics of long maturity taxable debt w/no specific use

22

23

Inflation Environment – Rate Projections • Inflation remains very low

– TIPS Funds lost 5.9% in 2013, Like amount in 2014, but stable in 2015 as Flight to Quality reduced US Treasury rates through Aug.

• Little inflation pressure – Underemployment remains higher than expected – Many new jobs are in service industry, lower wage rates – Fewer households formed, less purchasing of durable goods – Shift from purchase of “goods” to purchase of “services”

• Deflation potential increasing in US & Europe • Substitution of Capital for Labor

24 24 24

The Current & Future Economic World • European challenges

– Europe overall is on brink of recession – Greek economy continues to shrink – Spain, Italy, Portugal, Ireland continue liquidity & finance issues – EU Central Bank has adopted “Quantitative Easing” program

• Brazil, Russia India, China (BRIC) challenges – Economies of BRIC countries are slowing – Strong $ means demand for US Products lower – Economic corruption in some countries delays economic growth – BRIC population growth requires continued economic growth to

maintain/improve living conditions for citizens

The Death of Finance • What if the past 40 years was the aberration?

– For 60+ years prior to 1970’s – US Treasuries near current rates – Disconnect of local funding and lending by financial institutions

• General Electric Sale of GE Financial – “End point to era of deregulation and innovation” – Barron’s 4-14-15 – Reduction in financing options for HealthCare and Higher Ed

• Dodd Frank & SEC Regulatory Oversight – Increasing liquidity requirements – Capital adequacy testing – Restrictions on bank trading with their own funds

25

Market Changes • Bond Insurance use increasing

– Over 5% of governmental debt insured to date in 2015 • Well below 50% use prior to 2008

– Insurance firms very selective in what type of Credit to insure • Bank Placements Continue

– More restrictions, but remains a viable option • Taxable Financing Increases

– Flexibility, new market participants • Public Private Partnerships (P3)

– Increasing use and popularity – Strong demand from Pension funds, Overseas firms

26

27 27 27

Forecast 2015 & 2016 • Market Volatility continues to be significant

– Equity moves – Interest rate moves

• Tax Reform Gains Traction – but stalled until 2017 – Tax Exemption may be reduced by tax reform legislation

• Limitation on Tax Exemption possible • Which itemized deductions to limit?

• Demographics increase their influence on economy – Aging population – Work Force Participation – Cost of seniors

Forecast 2015 & 2016 • Capital improvements delayed since 2008 likely to begin

– Road improvements/repairs – Building deferred maintenance addressed

• New projects continue to meet political resistance – Voters continue to resist new projects

• Refunding of outstanding debt continues at slower pace • Inflation remains subdued • Interest rates – Treasury and Muni – remain low, but

likely to rise modestly and flatten yield curve • Investors continue to search for yield

28

Your Questions, Comments & Thoughts?

29

30 30

16th Annual Kansas GFOA Fall Conference

Thanks for your attendance, participation and attention Our view of the economic outlook is strengthening as there is more positive

than negative moving forward. We expect the next few months to be challenging as the economy confronts economic issues overseas and Congress confronts a possible government shutdown and continues to consider deficit reduction measures in the midst of a Presidential election race.

Contact Springsted staff for additional information or follow-up on questions from today’s Symposium.

For economic questions, contact me at: Barry W. Fick 651.223.3042

31 31 31

Information Sources

• Springsted – www.springsted.com • Federal Open Market – www.federalreserve.gov • Bloomberg – www.bloomberg.com • SIFMA – www.sifma.org • Bureau of Labor Statistics – www.bls.gov • National Association of Realtors – www.realtor.org