k-12 school spending and performance review -...

TRANSCRIPT

State of Washington Joint Legislative Audit and Review Committee (JLARC)

K-12 School Spending and Performance Review

Report 05-19

November 30, 2005

Upon request, this document is available in alternative formats for persons with disabilities.

JOINT LEGISLATIVE AUDIT AND REVIEW COMMITTEE 506 16th Avenue SE PO Box 40910 Olympia, WA 98501-2323 (360) 786-5171 (360) 786-5180 Fax http://jlarc.leg.wa.gov

Committee Members SENATORS Brad Benson

Jeanne Kohl-Welles

Bob Oke

Linda Evans Parlette, Vice Chair

Debbie Regala

Phil Rockefeller, Asst. Secretary

Pat Thibaudeau

Joseph Zarelli

REPRESENTATIVES Gary Alexander, Secretary

Glenn Anderson

Kathy Haigh

Janéa Holmquist

Ross Hunter, Chair

Fred Jarrett

Kelli Linville

Deb Wallace

LEGISLATIVE AUDITOR Ruta Fanning

The Joint Legislative Audit and Review Committee (JLARC) carries out oversight, review, and evaluation of state-funded programs and activities on behalf of the Legislature and the citizens of Washington State. This joint, bipartisan committee consists of eight senators and eight representatives, equally divided between the two major political parties. Its statutory authority is established in RCW 44.28. JLARC staff, under the direction of the Committee and the Legislative Auditor, conduct performance audits, program evaluations, sunset reviews, and other policy and fiscal studies. These studies assess the efficiency and effectiveness of agency operations, impacts and outcomes of state programs, and levels of compliance with legislative direction and intent. The Committee makes recommendations to improve state government performance and to correct problems it identifies. The Committee also follows up on these recommendations to determine how they have been implemented. JLARC has, in recent years, received national recognition for a number of its major studies.

K-12 SCHOOL SPENDING AND

PERFORMANCE REVIEW

REPORT 05-19

REPORT DIGEST

NOVEMBER 30, 2005

STATE OF WASHINGTON

JOINT LEGISLATIVE AUDIT AND REVIEW COMMITTEE

STUDY TEAM STEPHANIE HOFFMAN

LISA JEREMIAH

LEGISLATIVE AUDITOR RUTA FANNING

Copies of Final reports and Digests are

available on the JLARC website at:

http://jlarc.leg.wa.gov

or contact

Joint Legislative Audit & Review Committee

506 16th Avenue SE Olympia, WA 98501-2323

(360) 786-5171 (360) 786-5180 FAX

Study Background As part of its 2003-05 Work Plan, JLARC initiated this study of spending and performance assessment of individual schools within the state’s K-12 public education system. In the state’s 2005-07 budget, K-12 public schools receive $10.9 billion, or 42 percent of the State General Fund.

Legislators wanted to know how school districts distribute resources to individual schools and what information on school spending and performance is available. This study describes:

• District budgeting and decision-making practices;

• District and school spending patterns;

• The types of assessments schools use to understand student performance;

• Data that the state collects on districts and schools; and

• Alternative approaches in other states and school districts to reporting and budgeting school spending.

To conduct this review, we surveyed all 296 school districts within the state and interviewed six case study districts. We hired consultants to review budgeting and reporting practices in other states.

District Budgeting and Decision-Making PracticesBased on our review of district budgeting, accounting, and decision-making practices, we have the following findings:

• Districts allocate money to schools in various ways, but most districts consider student enrollment as one factor when allocating resources.

• Districts use different methods of tracking school expenditures within their own accounting systems. This makes it difficult to compare school spending across districts.

• In general, school principals have limited authority to make decisions about their school budgets.

• Districts and schools are using performance data in budgeting and program decision-making.

Data Availability and Reporting Requirements We reviewed data that is collected by the state on district and school budgeting and spending. We found:

• The state does not collect spending data from individual schools, though schools, along with districts, are accountable for the performance of their students. The state does collect district-level spending data.

• The state already requires numerous reports from districts. Policymakers should be cautious about adding reporting requirements without first considering streamlining or discontinuing other requirements.

Alternative Approaches to Reporting and Budgeting School Expenditures JLARC hired consultants to look at how other states and districts outside of Washington report school-level spending data and make budgeting decisions.

• States and districts around the country are considering other ways of reporting and budgeting school-level spending to address various goals, such as increasing accountability and transparency of decision-making, and linking performance and spending.

• Generally, individual districts initiate budgeting changes, but reporting changes have been made by both districts and states. Some states are requiring districts to report more information on school spending.

• Gaining additional information about school-level spending is possible in Washington, but higher levels of detail or uniformity in reporting will come at greater costs. Currently, changes in budgeting are possible at the district level, but staffing ratio requirements, categorical spending restrictions, and collective bargaining agreements limit the amount of discretion schools have over spending their resources.

Conclusion Before beginning any effort at changing district reporting requirements or budgeting practices, the Legislature should consider:

• What the state’s role should be in school-level finance given that state law dictates that the state allocation formula “…shall be for state allocation and equalization purposes only and shall not be construed as mandating specific operational functions of local school districts….”;1

• How policymakers would use additional financial data to answer questions about school performance; and

• Whether the usefulness of school-level spending data would justify the costs of collecting and analyzing it.

1 RCW 28A.150.260.

COMMITTEE ADDENDUM ON K-12 SCHOOL SPENDING AND PERFORMANCE REVIEW REPORT: The Joint Legislative Audit and Review Committee recognizes there are significant costs and implementation challenges to develop a reporting system that would collect uniform and reliable school level spending information from all local school districts. However, the Committee also believes that assessing how instructional resources and policy choices impact student learning outcomes is an important constitutional duty of the state. Therefore, the Committee recommends JLARC add a future study to our work plan, which would, in conjunction with the Governor’s Washington Learns initiative, and with representatives from local school districts and boards, identify critical school performance data that would enhance both the Legislature’s and districts’ ability to make informed resource commitments. The study would also address related changes to information systems and accounting practices.

TABLE OF CONTENTS

CHAPTER ONE: INTRODUCTION................................................................................. 1 STUDY OVERVIEW.......................................................................................................... 1 K-12 BUDGET AND ENROLLMENT..................................................................................... 1 EDUCATION REFORM...................................................................................................... 2 PAST AND CURRENT K-12 STUDIES................................................................................. 2 CURRENT JLARC STUDY ............................................................................................... 2

CHAPTER TWO: BASICS OF K-12 FUNDING.............................................................. 5 CHAPTER OVERVIEW...................................................................................................... 5 SCHOOL DISTRICT FUND SOURCES ................................................................................. 5 SCHOOL DISTRICT SPENDING.......................................................................................... 7

CHAPTER THREE: RESOURCE ALLOCATIONS, EXPENDITURES, AND DECISION-MAKING AUTHORITY.................................................................................................... 9

CHAPTER OVERVIEW...................................................................................................... 9 BACKGROUND................................................................................................................ 9 DISTRICT SPENDING..................................................................................................... 10 SCHOOL SPENDING ...................................................................................................... 11 DECISION-MAKING AUTHORITY...................................................................................... 14 IN SUMMARY................................................................................................................ 18

CHAPTER FOUR: PERFORMANCE ASSESSMENT.................................................. 19 CHAPTER OVERVIEW.................................................................................................... 19 ACCOUNTABILITY IN EDUCATION .................................................................................... 19 PERFORMANCE ASSESSMENTS...................................................................................... 19 USING ASSESSMENT DATA............................................................................................ 21 SHARING PERFORMANCE ASSESSMENT AND IMPROVEMENT STRATEGIES......................... 22 LIMITS TO UNDERSTANDING PERFORMANCE THROUGH BUDGETS .................................... 23 IN SUMMARY................................................................................................................ 23

CHAPTER FIVE: REPORTING REQUIREMENTS AND DATA AVAILABILITY.......... 25 CHAPTER OVERVIEW.................................................................................................... 25 CURRENT REPORTING REQUIREMENTS.......................................................................... 25 IN SUMMARY................................................................................................................ 28

CHAPTER SIX: ALTERNATIVE APPROACHES TO REPORTING AND BUDGETING SCHOOL EXPENDITURES .......................................................................................... 29

CHAPTER OVERVIEW.................................................................................................... 29 WHY CHANGE SCHOOL REPORTING AND BUDGETING PRACTICES? .................................. 29 NINE OPTIONS FOR CHANGE......................................................................................... 30 IN SUMMARY................................................................................................................ 36

CHAPTER SEVEN: CONCLUSION.............................................................................. 37 STUDY FINDINGS.......................................................................................................... 37 CONCLUSION ............................................................................................................... 38

AGENCY RESPONSES ................................................................................................... 38 ACKNOWLEDGEMENTS.................................................................................................. 39

APPENDIX 1: SCOPE AND OBJECTIVES.................................................................. 41

APPENDIX 2: AGENCY RESPONSES ........................................................................ 43

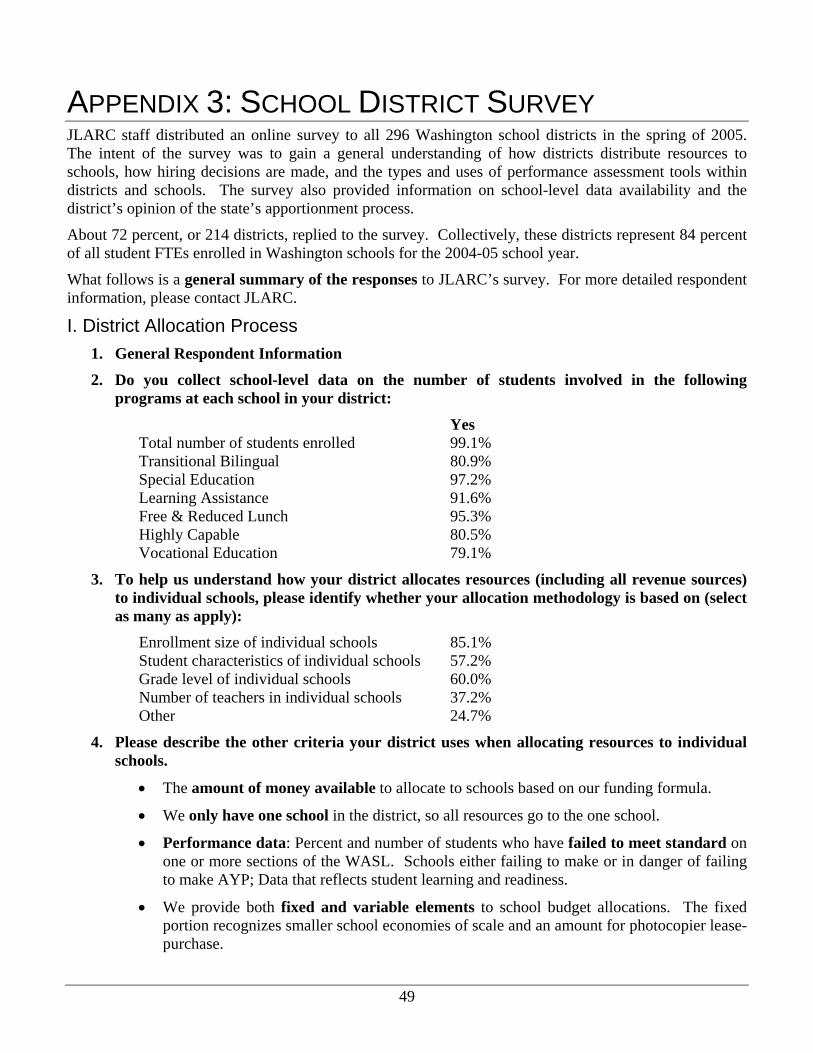

APPENDIX 3: SCHOOL DISTRICT SURVEY .............................................................. 49

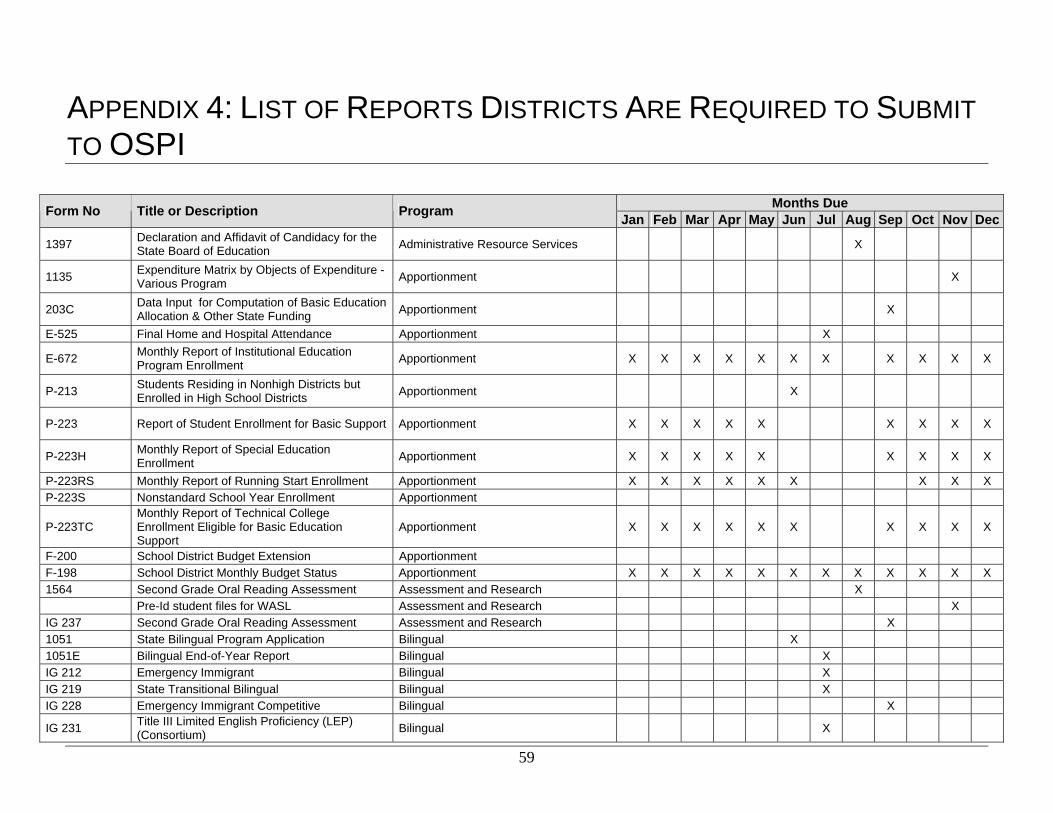

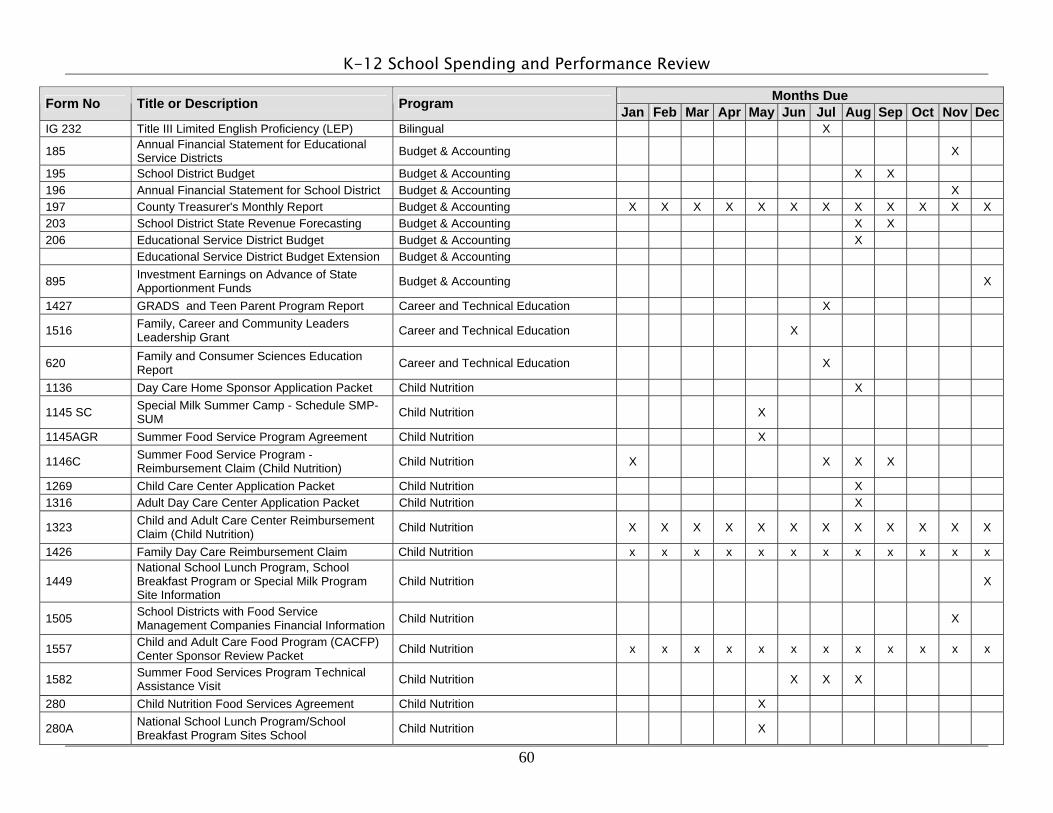

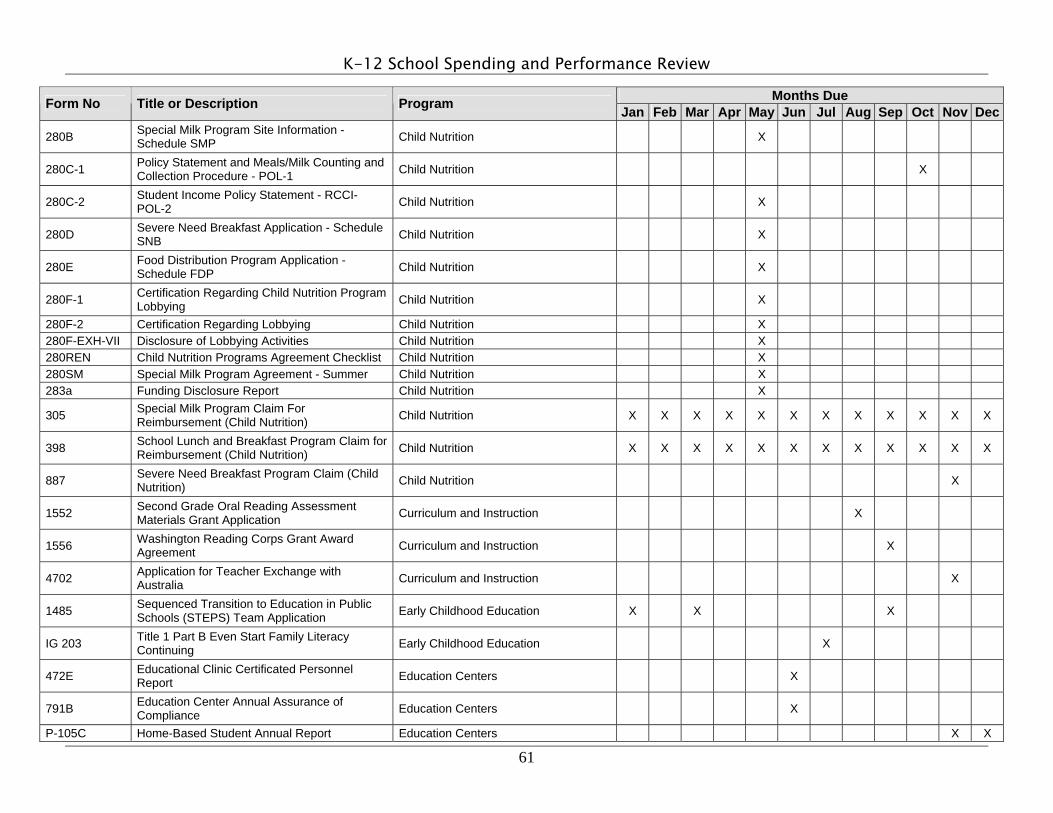

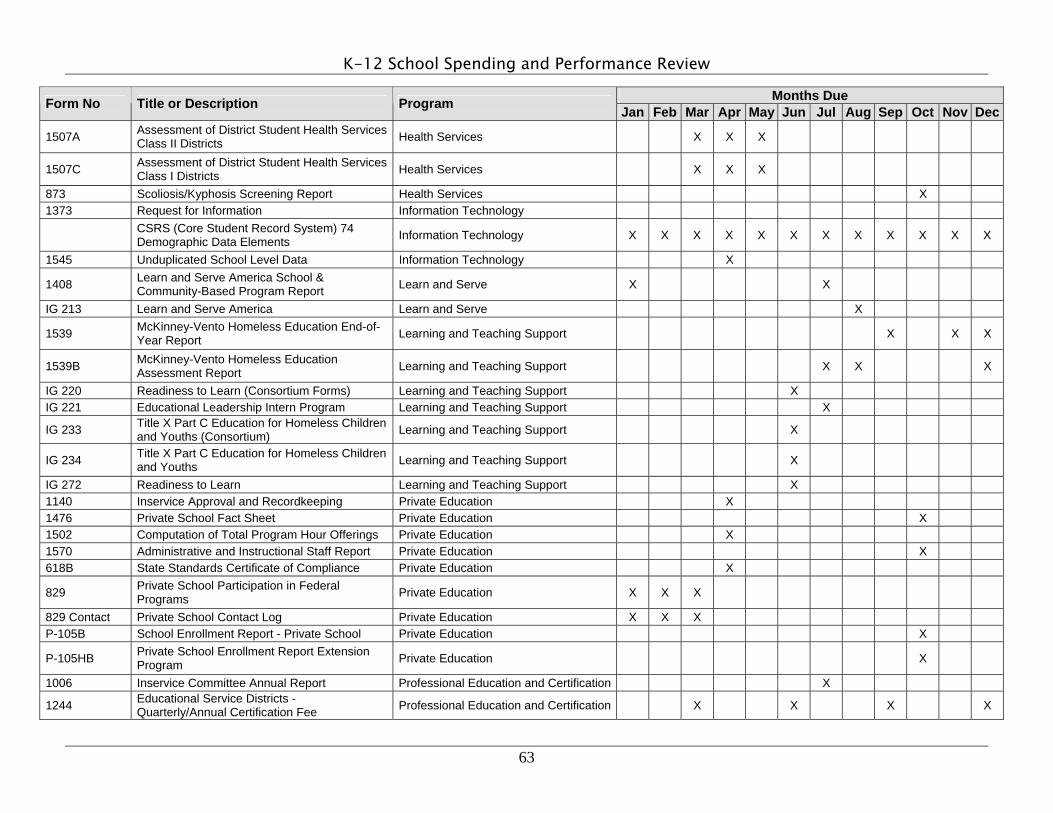

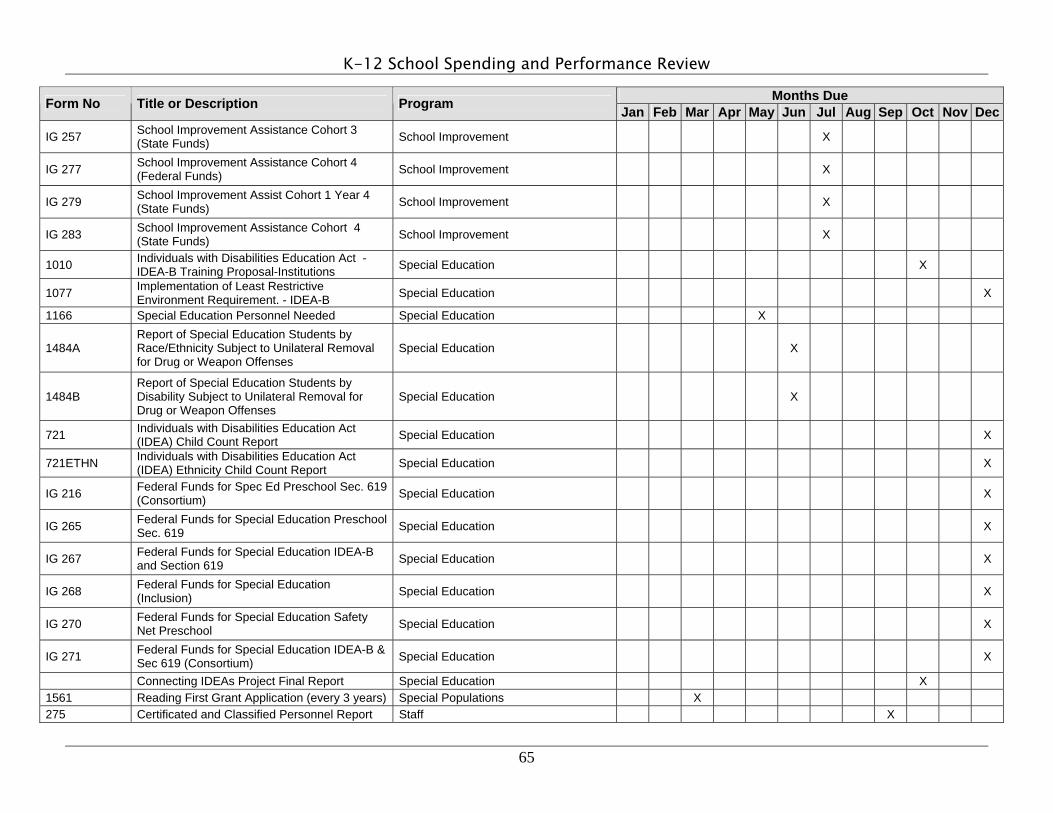

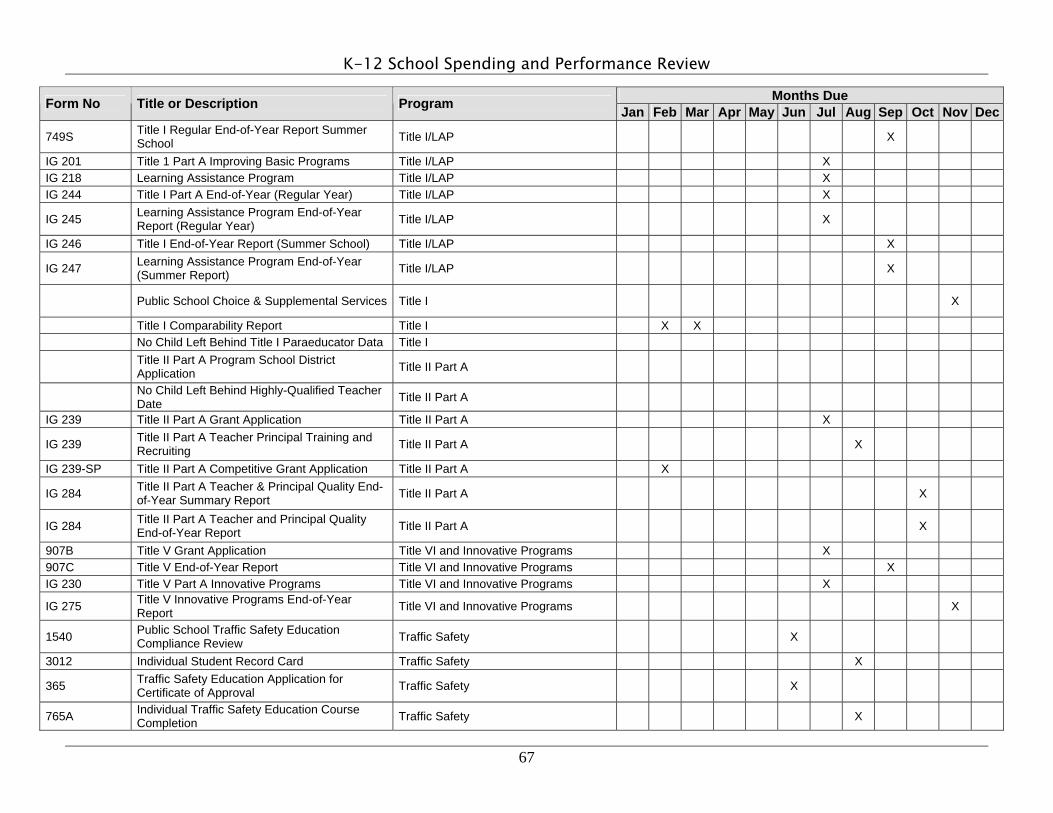

APPENDIX 4: LIST OF REPORTS DISTRICTS ARE REQUIRED TO SUBMIT TO OSPI.............................................................................................................................. 59

APPENDIX 5: ADDITIONAL RESEARCH ON ALTERNATIVE APPROACHES TO REPORTING AND BUDGETING SCHOOL EXPENDITURES..................................... 69

CHAPTER ONE: INTRODUCTION STUDY OVERVIEW As part of its 2003-05 Work Plan, JLARC initiated this study of school spending and performance assessment within the state’s K-12 system. Legislators wanted to know how school districts distribute resources to individual schools and how much discretion school principals have over allocating resources within their schools. This study comes at a time when schools are increasingly held responsible for the achievement of their students. Yet, the state only requires school districts, and not individual schools, to report spending data.

This study examines district and school decision-making practices in order to understand how districts and schools manage resources to improve student achievement. It also reviews the types of assessments schools use to understand student performance. Finally, it identifies other states’ and school districts’ approaches to reporting and budgeting school spending.

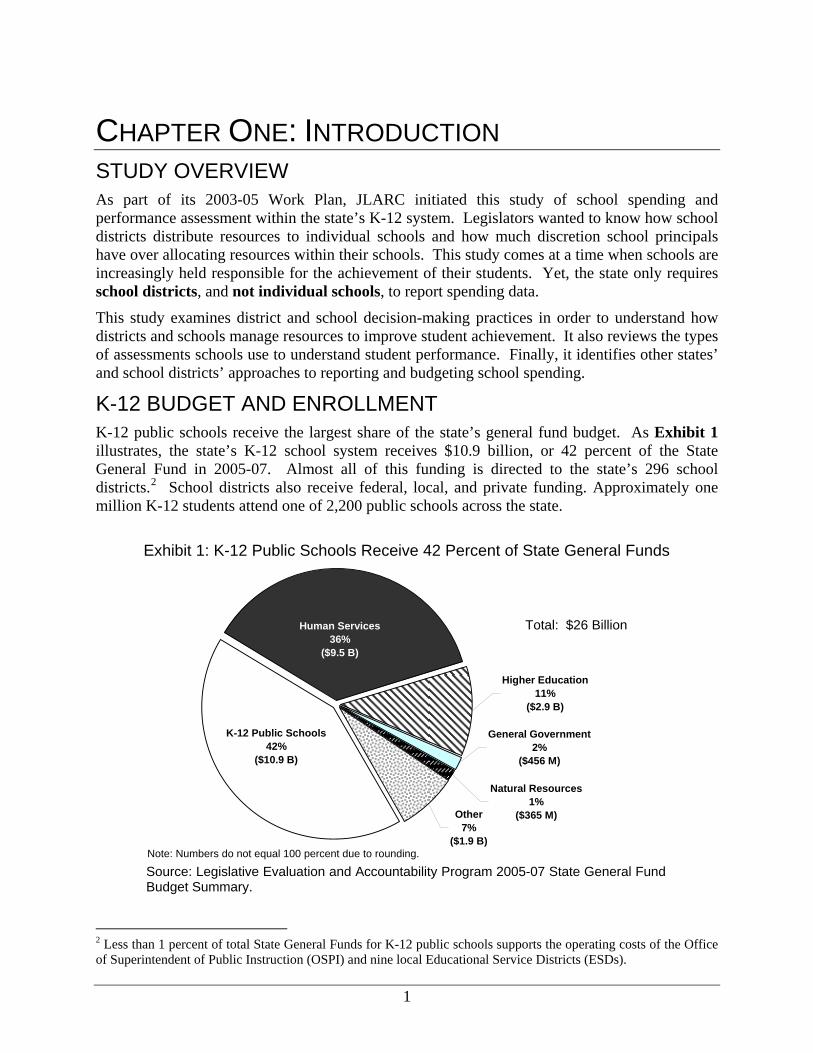

K-12 BUDGET AND ENROLLMENT K-12 public schools receive the largest share of the state’s general fund budget. As Exhibit 1 illustrates, the state’s K-12 school system receives $10.9 billion, or 42 percent of the State General Fund in 2005-07. Almost all of this funding is directed to the state’s 296 school districts.2 School districts also receive federal, local, and private funding. Approximately one million K-12 students attend one of 2,200 public schools across the state.

Human Services36%

($9.5 B)

K-12 Public Schools42%

($10.9 B)

Higher Education11%

($2.9 B)

General Government2%

($456 M)

Natural Resources1%

($365 M)Other7%

($1.9 B)

Source: Legislative Evaluation and Accountability Program 2005-07 State General Fund Budget Summary.

Total: $26 Billion

Exhibit 1: K-12 Public Schools Receive 42 Percent of State General Funds

Note: Numbers do not equal 100 percent due to rounding.

2 Less than 1 percent of total State General Funds for K-12 public schools supports the operating costs of the Office of Superintendent of Public Instruction (OSPI) and nine local Educational Service Districts (ESDs).

1

K-12 School Spending and Performance Review

EDUCATION REFORM State and national education reform efforts have shaped the focus and expectations of Washington’s schools for more than a decade. Washington’s education reform holds schools responsible for meeting essential academic learning requirements for reading, writing, math, and other skills.3 Students in elementary, middle, and high schools take the Washington Assessment of Student Learning (WASL) to demonstrate whether they have mastered the essential academic learning requirements. Beginning in 2008, all high school seniors must meet the proficient standard on the reading, writing, and mathematics assessments to receive a Certificate of Academic Achievement—a requirement for high school graduation.4

Schools in Washington also are subject to new requirements under the federal No Child Left Behind Act of 2001 (NCLB). NCLB mandates minimum achievement standards for every school, expands assessment requirements, and sets a mandatory national deadline of 2014 for schools to have nearly 100 percent of their students meeting a “proficient” achievement level as defined by each state. In Washington, the WASL is used to evaluate student proficiency levels.

PAST AND CURRENT K-12 STUDIES This study of school spending and performance assessment is one of many studies completed or currently being conducted on K-12 issues. Since 1995, JLARC has completed 15 K-12 reports on topics ranging from special education and the Learning Assistance Program to supplemental contracts and school bus bidding and purchasing.

In 1999, JLARC completed a “K-12 Finance and Student Performance Study.”5 This study found that: (1) revenue allocation is equitable around the state, (2) districts spend money in similar ways, and (3) the state does not collect data on spending from individual schools. At the time, JLARC did not recommend that the state collect school-level expenditure data. Instead, JLARC concluded that the Legislature could use data on staffing to approximate school spending because personnel costs represent about 90 percent of total district spending.

Beyond JLARC’s work, many public and private organizations continue to examine different aspects of K-12 funding and student achievement. In 2005, the Legislature passed E2SSB 5441, requiring a comprehensive study on early learning, K-12, and higher education finance and policy. This effort, now known as “Washington Learns,” will look broadly at the state’s education system and how it uses funds to provide all students with the opportunity to achieve state standards. It is scheduled to be completed in November 2006.

CURRENT JLARC STUDY In light of other K-12 study efforts underway, it is important to clarify the scope of this study and how it relates to other work taking place. This is a descriptive analysis of school district and school-level spending, decision-making and performance assessment practices. This study does

3 Chapter 336, Laws of 1993 (ESHB 1209). 4 Students who do not meet proficient standards in one or more content areas can retake the WASL up to four times. Exceptions to the assessment requirements include students who have an Individual Education Plan requiring an alternative assessment and students who qualify to demonstrate that they meet the same reading, writing, and/or mathematics proficiency standards in an alternative format. 5 JLARC Report 99-9.

2

K-12 School Spending and Performance Review

not evaluate the statewide finance structure. Rather, it describes how resources are allocated once they reach the state’s school districts. This study addresses the following questions:

1. What processes do districts use to distribute funds to schools?

2. What information does the state have on school spending?

3. Who has authority over school spending decisions?

4. What performance assessments do districts and schools use to understand student achievement and make programmatic and budgeting decisions?

5. What are the national trends in school-based or student-based budgeting and reporting and how might these be applied in Washington?

General conclusions from this report can inform the broader discussions taking place on Washington’s education finance and performance systems.

Study Methodology To answer these questions, JLARC surveyed all 296 school districts within the state about their resource allocation methodologies and assessment practices. About 72 percent, or 214 districts, responded to the survey. Collectively, these districts represent 84 percent of all student FTEs enrolled in Washington public schools. Survey responses are summarized in Appendix 3.

We also selected six case study districts to learn about their budgeting processes and expenditures in greater detail. The size of these districts ranged from just under 1,000 to over 20,000 students. Case study districts are located in eastern and western Washington and educate students with a variety of socio-economic and racial backgrounds. We visited each of the six districts to talk to their administrators and school principals. We also reviewed budget and expenditure data for each district. These districts are anonymous in this report because our intent is to describe the range of practices, rather than to evaluate individual districts’ practices.

Additionally, JLARC hired consultants to review other states’ and school districts’ reporting and budgeting practices.

Report Organization Chapter 2 provides a summary of K-12 funding in Washington by describing major fund sources and spending categories. Chapter 3 describes the following:

• The processes that districts use to allocate money to schools; • What we do – and do not – know about school spending; and • Three levels of expenditure decision-making authority.

Chapter 4 describes the state’s performance assessment system and how schools use performance data to make program and budgeting decisions. Chapter 5 summarizes the type of district and school data the state collects. Chapter 6 provides information on alternative ways that districts and other states report and budget expenditures. Chapter 7 presents the report’s conclusions.

3

K-12 School Spending and Performance Review

4

CHAPTER TWO: BASICS OF K-12 FUNDING CHAPTER OVERVIEW This chapter provides a brief overview of where funding for school districts comes from and how districts spend it. In Washington, most school district funding comes from the state. The rest comes from local taxes, the federal government, and other local and private sources. Districts around the state spend their money in similar ways.

SCHOOL DISTRICT FUND SOURCES In Washington, K-12 funding comes primarily from the state general fund. Additional funding comes from local taxes, the federal government, and other sources.

State Funding As shown in Exhibit 2, approximately 70 percent of school district funds come from the state.

State70%

($5.2 B)

Federal10%

($732 M)

Other4%

($321 M)

Local Taxes 16%

($1.2 B)

Exhibit 2: School District Fund Sources, School Year 2003-04

Source: JLARC analysis of OSPI’s State Summary School District Financial Reports 2003-04, available at www.k12.wa.us/safs/PUB/FIN/0304/FinSum2.pdf.

Total: $7.47 Billion

State 70%

($5.2 B)

5

K-12 School Spending and Performance Review

Of this state funding, 88 percent goes to what the Legislature has defined as basic education, which includes the following:

• General apportionment is the main source of basic education funding. The apportionment funding formula is based on the average annual enrollment of students in the district.

• Special education allocation is for costs of serving students with disabilities that exceed the general apportionment allotment. Funding is based on the number of special education students in a district.

• Pupil transportation funding is based on the number of students transported and the distance these students must travel to school.

• Learning Assistance Program provides funding for districts to assist underachieving students. As a result of changes passed by the Legislature in 2005, beginning in the 2005-06 school year, district funding is based on the number of students eligible for lunch at a free or reduced price.6

• Bilingual education funding is for students who speak little or no English. Funding is based on the number of students enrolled in the bilingual program.

• Education provided in juvenile detention centers and state institutions is the final segment of basic education funding. Funding is based on the number of students served.

The remaining 12 percent of state funding is for expenses such as school food services, levy equalization funding to help districts with above-average tax rates due to low property values, and the Student Achievement Fund which was created by Initiative 728 in 2000 to reduce class sizes and pay for other learning improvement opportunities.

Local Taxes Local property tax funding makes up 16 percent of school district revenue. Districts use levy revenues to fund local priorities. The Levy Lid Act of 1977 prohibits districts from using local levies to collect more than 24 percent of the total amount of most state and federal revenues to the district. Currently, the 24 percent lid applies to 205 of the 296 districts. The other 91 school districts have levy lids up to 33.9 percent because they had higher local levies when the Levy Lid Act was passed. Not all districts have passed levies and some districts tax below the levy lid.

Federal Funding Federal funding provides ten percent of school district revenue. This funding is provided by Congress to local education agencies for several federal programs. The three largest, which together make up approximately 60 percent of all federal funds, are:

• Special education, through the Individuals with Disabilities Education Act;

• Programs for improving academic achievement in high-poverty schools; and

• School food services.

6 ESHB 2314.

6

K-12 School Spending and Performance Review

Other Fund Sources Additionally, districts receive about four percent of their revenue from other sources, such as fees for extra-curricular programs, school lunch charges, revenue from other school districts, rental income, and private donations.

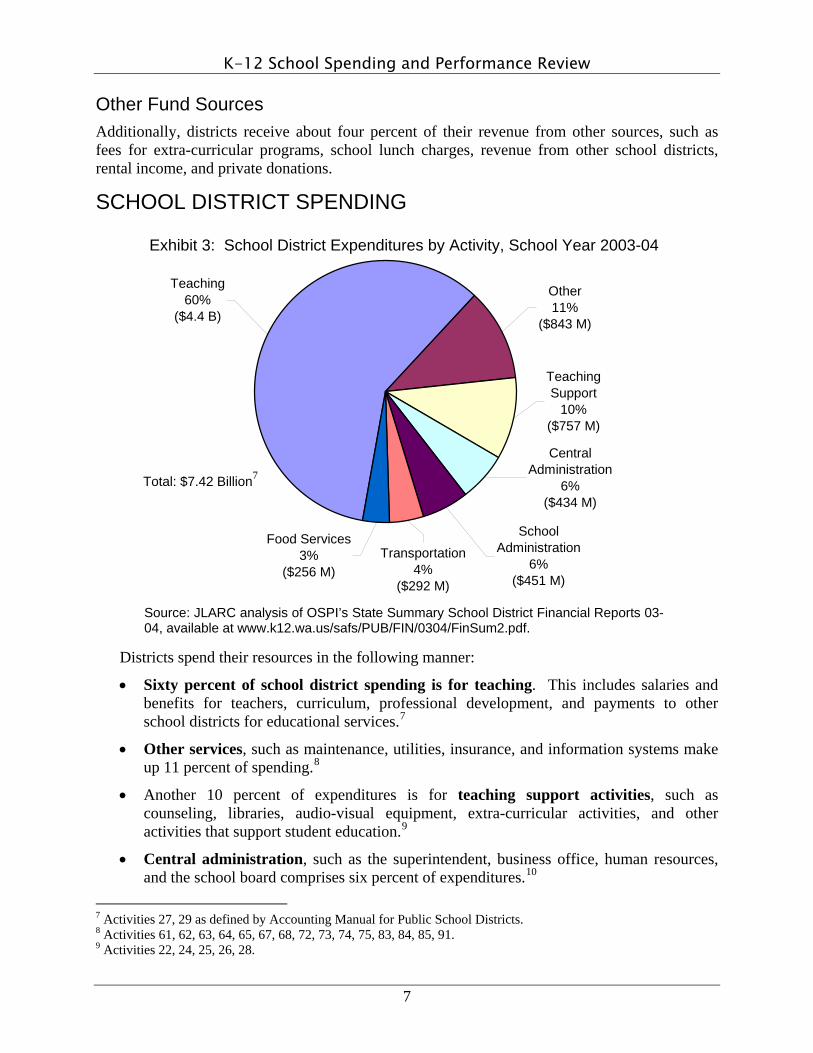

SCHOOL DISTRICT SPENDING

Teaching 60%

($4.4 B)

Other 11%

($843 M)

Teaching Support

10%($757 M)

Food Services 3%

($256 M)Transportation

4%($292 M)

Central Administration

6%($434 M)

SchoolAdministration

6%($451 M)

Exhibit 3: School District Expenditures by Activity, School Year 2003-04

Source: JLARC analysis of OSPI’s State Summary School District Financial Reports 03-04, available at www.k12.wa.us/safs/PUB/FIN/0304/FinSum2.pdf.

Total: $7.42 Billion7

Districts spend their resources in the following manner:

• Sixty percent of school district spending is for teaching. This includes salaries and benefits for teachers, curriculum, professional development, and payments to other school districts for educational services.7

• Other services, such as maintenance, utilities, insurance, and information systems make up 11 percent of spending.8

• Another 10 percent of expenditures is for teaching support activities, such as counseling, libraries, audio-visual equipment, extra-curricular activities, and other activities that support student education.9

• Central administration, such as the superintendent, business office, human resources, and the school board comprises six percent of expenditures.10

7 Activities 27, 29 as defined by Accounting Manual for Public School Districts. 8 Activities 61, 62, 63, 64, 65, 67, 68, 72, 73, 74, 75, 83, 84, 85, 91. 9 Activities 22, 24, 25, 26, 28.

7

K-12 School Spending and Performance Review

• School administration, including principals, makes up another 6 percent of expenditures.11

• Transportation makes up 4 percent of expenditures. This includes operational and maintenance costs of busing students to and from school and related program supervision.12

• Food service is an additional 3 percent of expenditures, including food purchases and the operational and supervisory costs for the provision of school meals.13

10 Activities 11, 12, 13, 14, 21 as defined by Accounting Manual for Public School Districts. 11 Activity 23. 12 Activities 51, 52, 53, 56, 59. 13 Activities 41, 42, 43, 44, 49.

8

CHAPTER THREE: RESOURCE ALLOCATIONS, EXPENDITURES, AND DECISION-MAKING AUTHORITY CHAPTER OVERVIEW This chapter provides general information on how resources are allocated and spent by districts and schools. It examines the various methods districts use for allocating resources to schools and identifies commonalities and differences. It also describes district and school spending patterns and identifies limitations of school-level spending information accounted for by districts. Finally, the chapter discusses three levels of spending authority: 1) district-managed expenses, 2) school-managed expenses, and 3) jointly-managed expenses.

BACKGROUND The Office of the Superintendent of Public Instruction (OSPI) collects information about how federal, state, and local funds are generated and distributed to its 296 school districts. The state has little information, however, about how districts distribute funds to cover district-wide and school-level expenses. Since much of the accountability for performance is now focused on schools, policymakers are interested in the answers to these questions:

• How do districts allocate funds to schools? • How do districts and schools spend the money? • Who is primarily responsible for making decisions about district and school spending?

DISTRICT METHODS FOR ALLOCATING RESOURCES Washington’s school districts have independent control over how they manage and allocate their resources. RCW 28A.150.260 states that the state allocation formula “shall be for state allocation and equalization purposes only and shall not be construed as mandating specific operational functions of local school districts….” While subject to certain guidelines tied to public revenue sources, school districts retain overall responsibility for determining how to allocate resources to schools.

The next section highlights similarities and differences in the way districts allocate funds. This information is based on general findings from JLARC’s survey and interviews with six case study districts. Although our intent is to describe the range in practices among districts, the findings on district allocation methods may not reflect the practices in very small districts that only distribute resources to one or a few schools.

Districts Consider Similar Factors When Allocating Resources to Schools Even though there is a high degree of independent control, districts use some common factors when making allocation decisions.

• About 85 percent of the 214 districts responding to our survey said that they allocate resources to schools based on the size of student enrollment.

9

K-12 School Spending and Performance Review

• Over half of the responding districts also said they consider grade levels (elementary, middle, or high school) and student characteristics (such as number of students receiving free and reduced price meals) when deciding how to allocate resources.

• A third of responding districts consider the number of teachers at each of their schools as a factor when deciding how to distribute funds for non-employee related expenses.

• Districts also reported that the needs and expectations of district stakeholders, a school’s unique facilities or programs, and student performance assessment indicators (such as WASL scores, classroom assessment data, and Adequate Yearly Progress status) influence how they distribute resources to schools. 14

Districts Use Different Processes for Distributing Resources In interviews with our six case study districts, we learned that the actual processes for distributing public funds to schools vary greatly across the state. Some districts allocate staff and additional resources based on a fixed number of staff and dollars per student FTE. For example, a district might allocate one teacher for every 25 students or $100 per elementary student for non-employee related costs.

Some districts make flat staffing and supplemental allocations (e.g., one principal, secretary, and counselor for every school or fixed allocations for field trips, extracurricular activities, furniture, and printing expenses). Still others use a combination of these approaches. A few districts make lump sum allocations to schools, allowing principals and their school management teams to allocate resources for staffing, curriculum, professional development, supplies, and other school expenses.

Private revenues are also distributed in varying ways. Some districts have private foundations that provide supplemental funding for all the schools in the district (for example, $250 for every teacher). Private organizations also may award grants and donations directly to schools, which must manage those funds according to the donor’s conditions or requirements.

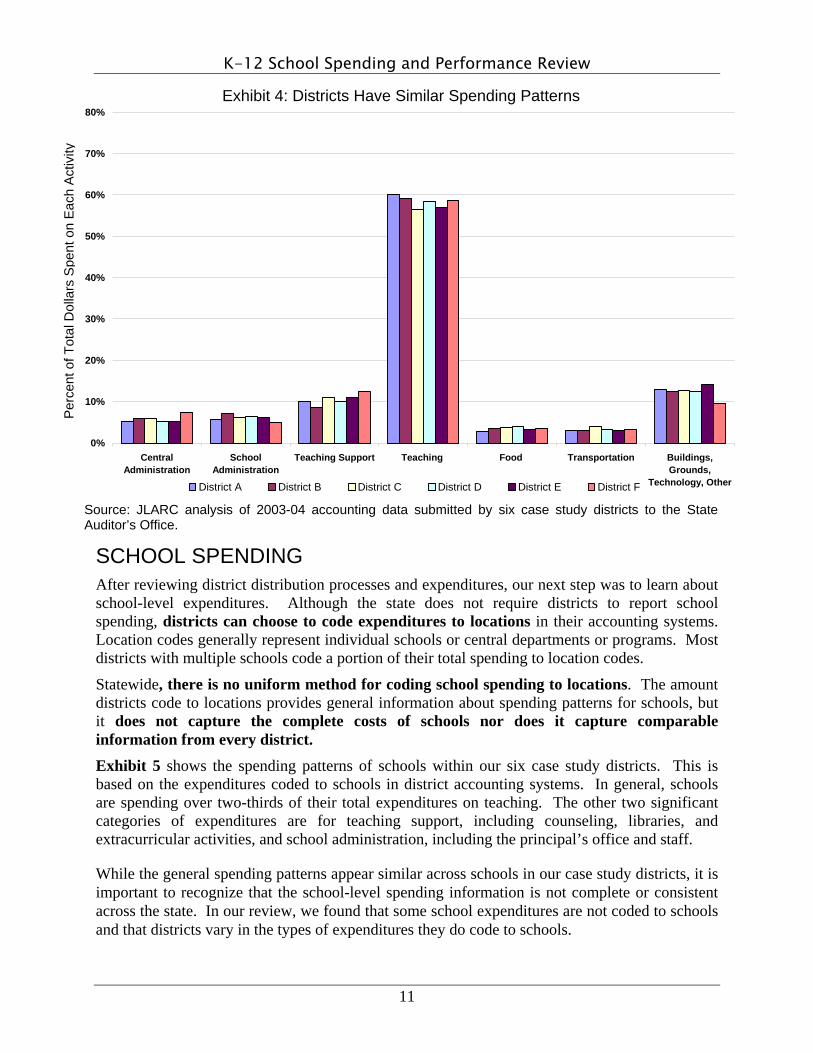

DISTRICT SPENDING Despite the differences across districts in how resources are allocated to schools, JLARC’s 1999 K-12 Finance and Student Performance Study found that districts and schools across the state spend their money in similar ways. Although the amount districts spend on various state-defined activities is different, the proportion of money spent on each of those activities is similar. For example, districts tend to spend about 60 percent of their budgets on teaching (which includes expenditures for teacher salaries and benefits, curriculum, and professional development).

For this study, JLARC looked at spending in six case study districts and again found that districts have the same patterns of expenditures as the 1999 report identified. These patterns are also the same as those exhibited statewide (see Chapter 2). Exhibit 4 illustrates the spending patterns of our case study districts.

14 Adequate Yearly Progress (AYP) is a key element of the federal No Child Left Behind Act. In Washington, AYP measures how much student performance in a school has improved annually on the WASL in reading and math.

10

K-12 School Spending and Performance Review

0%

10%

20%

30%

40%

50%

60%

70%

80%

CentralAdministration

SchoolAdministration

Teaching Support Teaching Food Transportation Buildings,Grounds,

Technology, Other

SCHOOL SPENDING After reviewing district distribution processes and expenditures, our next step was to learn about school-level expenditures. Although the state does not require districts to report school spending, districts can choose to code expenditures to locations in their accounting systems. Location codes generally represent individual schools or central departments or programs. Most districts with multiple schools code a portion of their total spending to location codes.

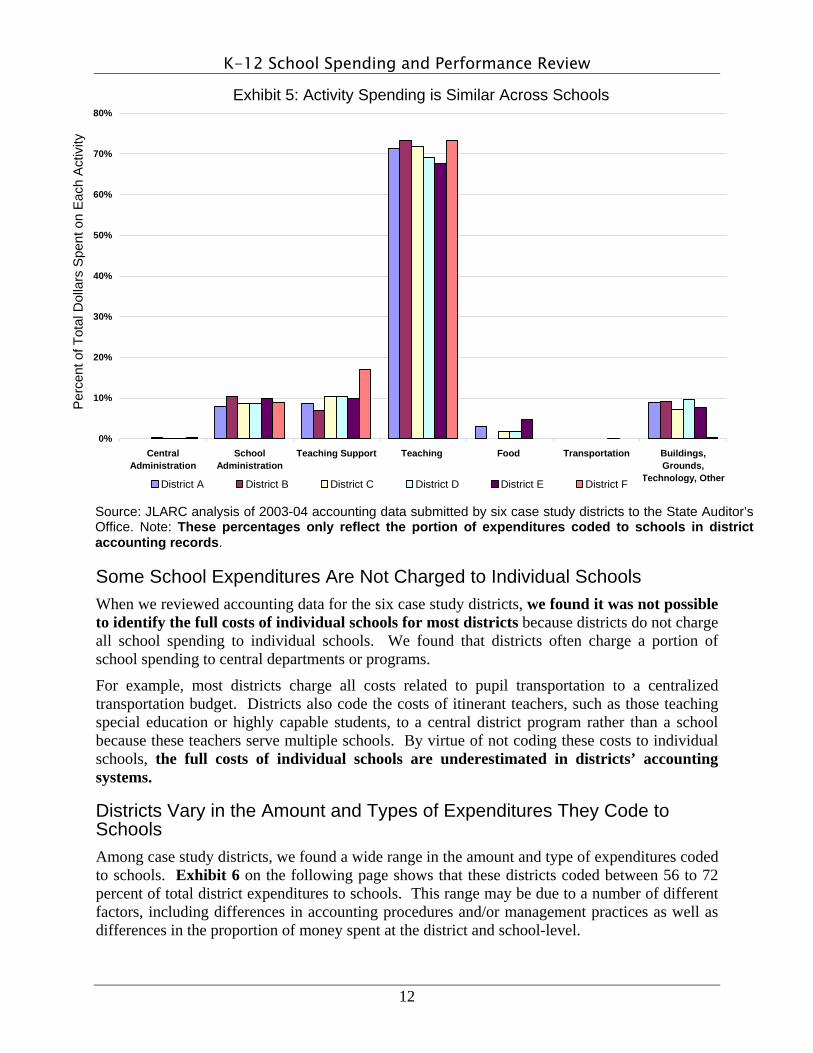

Statewide, there is no uniform method for coding school spending to locations. The amount districts code to locations provides general information about spending patterns for schools, but it does not capture the complete costs of schools nor does it capture comparable information from every district. Exhibit 5 shows the spending patterns of schools within our six case study districts. This is based on the expenditures coded to schools in district accounting systems. In general, schools are spending over two-thirds of their total expenditures on teaching. The other two significant categories of expenditures are for teaching support, including counseling, libraries, and extracurricular activities, and school administration, including the principal’s office and staff.

While the general spending patterns appear similar across schools in our case study districts, it is important to recognize that the school-level spending information is not complete or consistent across the state. In our review, we found that some school expenditures are not coded to schools and that districts vary in the types of expenditures they do code to schools.

District A District B District C District D District E District F

Exhibit 4: Districts Have Similar Spending Patterns

Source: JLARC analysis of 2003-04 accounting data submitted by six case study districts to the State Auditor’s Office.

Per

cent

of T

otal

Dol

lars

S

pent

on

Eac

h A

ctiv

ity

11

K-12 School Spending and Performance Review

0%

10%

20%

30%

40%

50%

60%

70%

80%

CentralAdministration

SchoolAdministration

Teaching Support Teaching Food Transportation Buildings,Grounds,

Technology, Other

Some School Expenditures Are Not Charged to Individual Schools When we reviewed accounting data for the six case study districts, we found it was not possible to identify the full costs of individual schools for most districts because districts do not charge all school spending to individual schools. We found that districts often charge a portion of school spending to central departments or programs.

For example, most districts charge all costs related to pupil transportation to a centralized transportation budget. Districts also code the costs of itinerant teachers, such as those teaching special education or highly capable students, to a central district program rather than a school because these teachers serve multiple schools. By virtue of not coding these costs to individual schools, the full costs of individual schools are underestimated in districts’ accounting systems.

Districts Vary in the Amount and Types of Expenditures They Code to Schools Among case study districts, we found a wide range in the amount and type of expenditures coded to schools. Exhibit 6 on the following page shows that these districts coded between 56 to 72 percent of total district expenditures to schools. This range may be due to a number of different factors, including differences in accounting procedures and/or management practices as well as differences in the proportion of money spent at the district and school-level.

District A District B District C District D District E District F

Exhibit 5: Activity Spending is Similar Across Schools

Source: JLARC analysis of 2003-04 accounting data submitted by six case study districts to the State Auditor’s Office. Note: These percentages only reflect the portion of expenditures coded to schools in district accounting records.

Per

cent

of T

otal

Dol

lars

S

pent

on

Eac

h A

ctiv

ity

12

K-12 School Spending and Performance Review

Coded To Schools

56%

60%

72%

71%

67%

71%

44%

40%

28%

29%

33%

29%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

District F

District E

District D

District C

District B

District A

Not Coded to Schools

Exhibit 6: Districts Code Different Proportions of Their Budgets to Schools

Source: JLARC analysis of 2003-04 accounting data submitted by six case study districts to the State Auditor’s Office.

Districts also vary in the types of expenses coded to schools. As Exhibit 7 on the following page illustrates, some activities are more often coded to schools than others. For example, costs of school administration (e.g., principal’s office) are almost entirely coded to schools while transportation and central administration costs (e.g., superintendent, business and human resources offices) are generally not coded to schools.

Some activities, such as teaching, include costs coded to both schools and to central departments. As mentioned earlier, teachers who are full-time basic education teachers may be coded to the schools where they teach. Itinerant teachers serving multiple schools, however, may be coded to the district office.

The most striking variation in how districts code costs to schools is in food services – districts allocate anywhere from zero to 85 percent of their food costs to schools. Some districts may code all of their food costs centrally, while other districts allocate food costs to individual schools. In both cases, food services are delivered at the school-level but only some districts track those costs to individual schools in their accounting systems.

Due to the variation across districts in the types of expenditures coded to schools, it is not possible to rely on accounting data alone to understand the total spending for individual schools in most districts. For many districts, identifying total school-level costs would require tracking new information, such as itinerant staff recording their time and expenses for each school they serve. Tracking these costs would take substantial time and effort, as is further discussed in Chapters 5 and 6.

13

K-12 School Spending and Performance Review

14

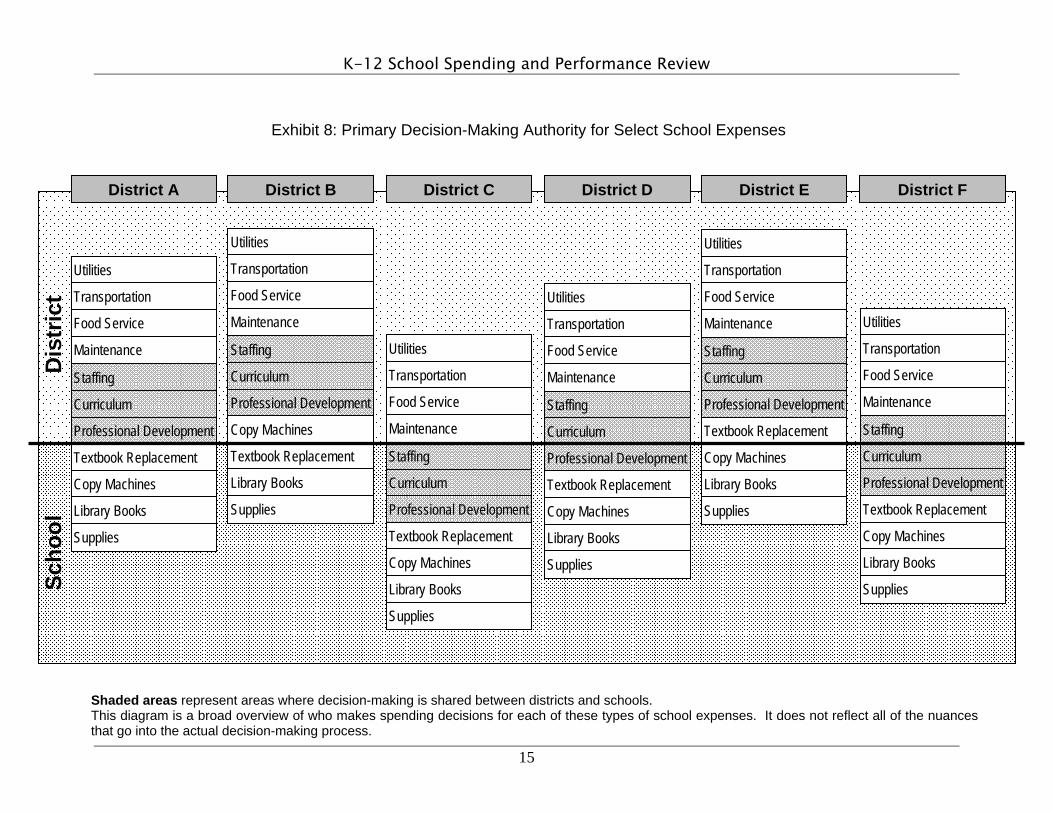

DECISION-MAKING AUTHORITY Another important distinction to make regarding school-level financial information is that the expenditures coded to schools do not necessarily reflect who is primarily responsible for making decisions about how those funds are spent. Coding expenditures to schools is generally an exercise in expenditure tracking. In many cases, the school principals have limited influence over most of the funds coded to their schools by the district. For instance, one of our case study districts coded $1.7 million in expenditures to an elementary school in the district’s accounting system, but the principal of that school only had management discretion over approximately $52,000, or about 3 percent of the school’s expenditures. The following section describes who has the primary authority for making decisions about school spending. Exhibit 8 on the next page lists some of the major expenses for operating a school that were identified by the district and school personnel we interviewed. This diagram highlights who is primarily responsible for making decisions about these common school expenses.15

Decision-Making Authority for District-Managed Expenses Items above the thick black line in Exhibit 8 represent spending primarily determined by the district. All six of our case study districts reported that the district has primary authority for costs related to utilities, transportation, food services, and maintenance. Districts may choose to control these expenses centrally in order to benefit from cost efficiencies, such as centralizing transportation functions, or to share resources among multiple schools, such as centrally-managed maintenance crews. 15 The expenses do not directly align with the statewide activities discussed previously because some of the expenses fall into more than one activity category.

0%

20%

40%

60%

80%

100%

CentralAdministration

SchoolAdministration

Teaching Support Teaching Food Transportation Buildings,Grounds,

Technology, Other

District A District B District C District D District E District F

Per

cent

of E

xpen

ditu

res

Cod

ed to

Sch

ools

Exhibit 7: Districts Vary in the Types of Expenditures They Code to Schools

Source: JLARC analysis of 2003-04 accounting data submitted by six case study districts to the State Auditor’s Office.

K-12 School Spending and Performance Review

15

Exhibit 8: Primary Decision-Making Authority for Select School Expenses

Utilities

Transportation

Food Service

Maintenance

Staffing

Curriculum

Professional Development

Textbook Replacement

Copy Machines

Library Books

Supplies

Utilities

Transportation

Food Service

Maintenance

Staffing

Curriculum

Professional Development

Copy Machines

Textbook Replacement

Library Books

Supplies

Utilities

Transportation

Food Service

Maintenance

Staffing

Curriculum

Professional Development

Textbook Replacement

Copy Machines

Library Books

Supplies

Utilities

Transportation

Food Service

Maintenance

Staffing

Curriculum

Professional Development

Textbook Replacement

Copy Machines

Library Books

Supplies

Utilities

Transportation

Food Service

Maintenance

Staffing

Curriculum

Professional Development

Textbook Replacement

Copy Machines

Library Books

Supplies

Utilities

Transportation

Food Service

Maintenance

Staffing

Curriculum

Professional Development

Textbook Replacement

Copy Machines

Library Books

Supplies Scho

ol

Dis

tric

t

District A District B District C District D District E District F

eas represent areas where decision-making is shared between districts and schools. agram is a broad overview of who makes spending decisions for each of these types of school expenses. It does not reflect all of the nuance

ecision-making process.

Shaded arThis di s that go into the actual d

K-12 School Spending and Performance Review

Decision-Making Authority for School-Managed Expenses Schools control the spending that appears below the thick black line on Exhibit 8. Major spending decisions for schools generally include buying supplies (for classrooms, offices, and health care), library books, textbook replacements, and copier machine contracts.

Many of the principals of our case study schools reported managing very limited budgets. They may have discretion over less than 5 percent of the resources coded to their schools in district accounting systems. Small increases in printing, postage, or textbook replacement costs can consume all of their discretionary resources. Several principals specifically mentioned that copy machine expenses represent a significant portion of their budgets and that they often have to save money for this purchase for several years.

The exception to this characterization among our case study districts is District C, which is a district that gives principals more decision-making responsibility. This district uses site-based management because it believes that schools should be more involved in financial decisions since schools are accountable for student achievement.

In District C, principals make more significant spending decisions related to staffing, curriculum, and professional development than any of the other principals in our case studies. For example, the district coded $3.5 million in expenditures to one middle school, and the principal managed a budget of over $3 million, or over 85 percent of the expenditures coded to that school.

Decision-Making Authority for Jointly-Managed Expenses The shaded areas on Exhibit 8 represent items that are decided on jointly between districts and schools. Their placement above or below the line depends on whether the district or school has final decision-making responsibility and which organizational budget is responsible for paying for those items. These joint areas also represent areas where there was considerable variation among our case study districts. These expenses include some of the large instruction-related costs, such as staffing, curriculum, and professional development. Both district and school leaders talked about the direct impact these major expenditures have on student learning.

Staffing – In most cases, central administrators determine the number of certificated and classified staff assigned to individual schools. Almost 96 percent of districts responding to JLARC’s survey said that central administrators determine whether to hire additional teachers and 89 percent said central administrators determine the number and type of classified staff employed at each school.

One of our case study districts was an exception to this practice. Again, in District C, the site-based model, schools receive a lump sum dollar allocation based on student enrollment and grade level (elementary, middle, or high school), and the schools can decide how to use this money. In this district, the school leaders decide how many staff and the type of staff to hire, as long as they stay within the state’s statutory class size limits.

Although decisions about staffing levels for many schools are made by the district office, the principals and superintendents both make decisions about whom to hire. In the JLARC survey, a little over half of the districts reported that central administrators make the decision about which teacher candidate to hire. The remaining districts reported that school principals make these decisions. Under both scenarios, hiring decisions are influenced by district collective bargaining requirements. For example, collective bargaining may require that the most senior teachers in

16

K-12 School Spending and Performance Review

the district have priority over teachers from outside the district or less experienced teachers when they apply for jobs.

Curriculum – In four of the six districts we studied, central administrators make final curriculum decisions (i.e., selecting and purchasing text books and associated supplies). Funding for the curriculum comes from district budgets. Central administrators reported that they maintained primary authority in curriculum decisions for two reasons: (1) to ensure continuity for students who move between schools within their district; and (2) to consolidate the number of different curriculum materials the school board needs to approve.

In two districts, school principals have more influence over their curriculum selection. District C selects curriculum for different grade levels, but individual schools have the option of choosing to use alternative instructional materials. District F is a small district with only one elementary, middle, and high school. Here principals, teachers, and central administrators work together to select curriculum. The school board then must approve the curriculum.

Professional development – This is one other area in which there is variation across districts about who makes decisions. In many districts, this is a shared process where both principals and central administrators have a role in identifying and organizing professional development programs; the variation revolves around how much control each level has, and the types of professional development offered by each. For example, central staff typically facilitate professional development around district curriculum, general district programs and policies, and state-level requirements. Principals, on the other hand, tend to use their professional development funds to target more specific school challenges identified through student assessments and classroom observations. Of course, in districts where the schools choose and purchase their own curriculum, the schools also have a greater responsibility for providing professional development opportunities that assist staff in implementing the curriculum.

Note on the Role of the School Board, Principal, and School Site Council To fully understand how spending decisions are made at districts and schools, it is important to consider the roles of the school boards, principals, and site councils.

State law is clear that the school board has the “…final responsibility for the setting of policies ensuring quality in the content and extent of its educational program…”16 As such, state law directs school boards to set policies to:

• Develop performance criteria and evaluation processes for certificated personnel;

• Determine staff assignments;

• Determine the number of instructional hours;

• Determine the allocation of certificated and classified staff time;

• Establish curriculum standards; and

• Evaluate teaching materials, including text books, teaching aids, handouts, or other printed material.

16 RCW 28A.150.230.

17

K-12 School Spending and Performance Review

Depending on the philosophy of the district’s school board, the principals play more or less of a role in making spending decisions. In many centralized districts, principals are primarily the instructional leader of the school. These principals are actively involved in the day-to-day delivery of instruction, but do not make substantial spending decisions. In districts where principals have more budgeting authority, they are site managers as well. Some principals that we spoke with enjoy this additional responsibility. Other principals, however, prefer to focus on their role as instructional leaders without the added financial management responsibilities.

Almost all of the principals we spoke with use site councils to help them manage their schools. These councils are generally made up of the principal and representatives of certificated and classified staff, parents, and community members. At many schools, site councils are involved in budget decision-making. However, a few principals did tell us that their site councils were primarily focused on student learning issues and not interested in talking about finances.

IN SUMMARY Districts around the state have different processes for distributing resources to schools, but their spending patterns are similar. While districts are not required to do so, most use existing accounting systems to track some spending to the school level. However, districts vary in the amount and types of expenditures they code to schools and some school-level expenditures are accounted for at the district-level rather than by individual school. Because districts code costs in different ways, the school spending information tracked in district accounting systems is not comparable across districts. We also found differences among the case study districts in who makes budget and spending decisions: the central administrators and/or individual school principals. In most districts, principals only have discretion over a limited amount of the total spending for their schools.

18

CHAPTER FOUR: PERFORMANCE ASSESSMENT CHAPTER OVERVIEW State and federal education reform has focused the attention of policymakers on accountability for district and school performance. Schools have increasingly become the point of focus for improving student achievement as reform measures require students to meet higher standards. This chapter begins with a summary of education reform policies. It then describes different types of assessments and how districts and schools are using assessment data to make budgeting and programmatic decisions.

ACCOUNTABILITY IN EDUCATION In 1993, the Legislature passed the Education Reform Act, with the goals of improving student achievement and strengthening the state’s educational accountability system.17 The Education Reform Act created the Washington Commission on Student Learning. The job of the Commission was to develop “Essential Academic Learning Requirements” based on student learning goals and an academic assessment system to determine if students were meeting these requirements.18

The other major accountability change for education is the federal No Child Left Behind Act (NCLB) of 2001, which increased the federal role in education. Under NCLB, states must use assessment systems to hold schools and districts accountable for student learning. NCLB can have a significant impact on schools that receive federal Title 1 funding for improving the achievement of low-performing students.19 Currently, 45 percent of Washington schools receive Title 1. These schools will face a series of increasing sanctions if they fail to meet Adequate Yearly Progress (AYP) for improving student performance. These sanctions include allowing students to transfer to other schools and providing supplemental instruction services from an OSPI-approved provider.

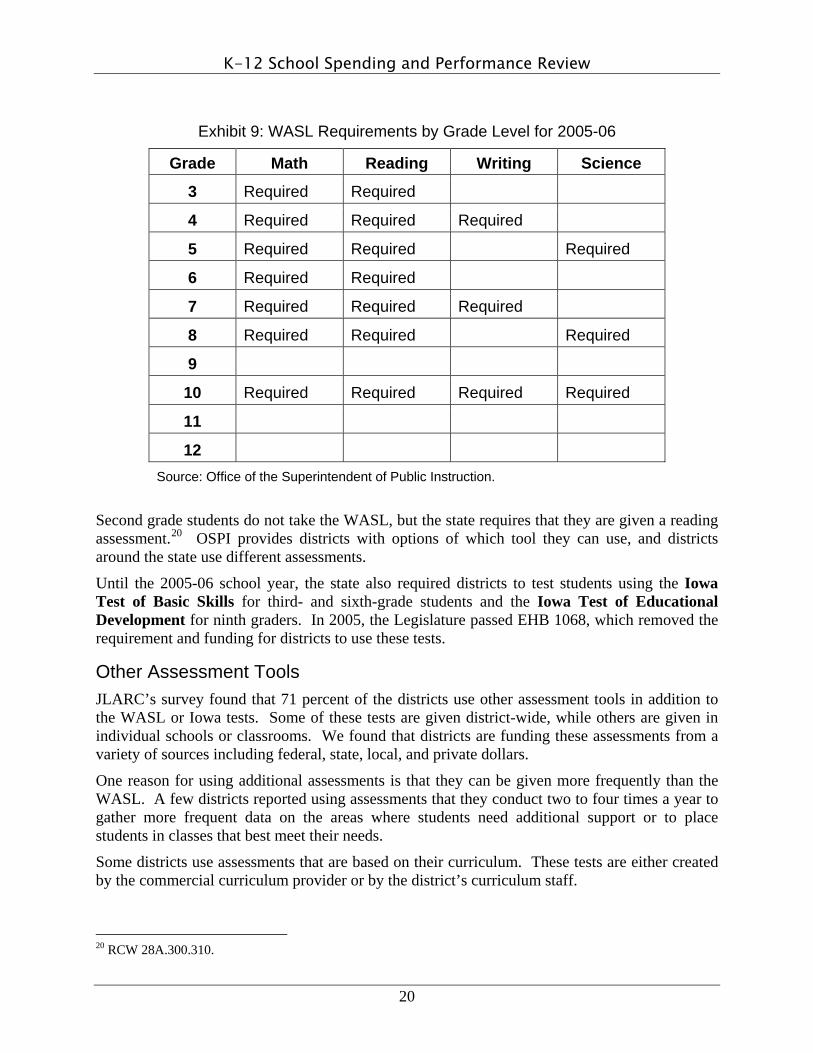

PERFORMANCE ASSESSMENTS State Assessments The primary performance assessment the state requires all schools to use is the Washington Assessment of Student Learning (WASL), which is the test developed after the Education Reform Act of 1993. The WASL is also used to satisfy NCLB requirements of a criterion-based assessment to measure state standards. Exhibit 9 on the following page shows WASL requirements for each grade level. Beginning in the 2005-06 school year, students in third, fifth, sixth, and eighth grade will be tested in reading and math to comply with NCLB requirements.

17 Chapter 336, Laws of 1993 (ESHB 1209). 18 The Washington Commission on Student Learning was replaced by the Academic Achievement and Accountability Committee in 1999. This committee was dissolved in 2005 and its duties were transferred to the State Board of Education. 19 Title 1 of the No Child Left Behind Act provides funding for helping disadvantaged children.

19

K-12 School Spending and Performance Review

Exhibit 9: WASL Requirements by Grade Level for 2005-06

Grade Math Reading Writing Science

3 Required Required

4 Required Required Required

5 Required Required Required

6 Required Required

7 Required Required Required

8 Required Required Required

9

10 Required Required Required Required

11

12 Source: Office of the Superintendent of Public Instruction.

Second grade students do not take the WASL, but the state requires that they are given a reading assessment.20 OSPI provides districts with options of which tool they can use, and districts around the state use different assessments.

Until the 2005-06 school year, the state also required districts to test students using the Iowa Test of Basic Skills for third- and sixth-grade students and the Iowa Test of Educational Development for ninth graders. In 2005, the Legislature passed EHB 1068, which removed the requirement and funding for districts to use these tests.

Other Assessment Tools JLARC’s survey found that 71 percent of the districts use other assessment tools in addition to the WASL or Iowa tests. Some of these tests are given district-wide, while others are given in individual schools or classrooms. We found that districts are funding these assessments from a variety of sources including federal, state, local, and private dollars.

One reason for using additional assessments is that they can be given more frequently than the WASL. A few districts reported using assessments that they conduct two to four times a year to gather more frequent data on the areas where students need additional support or to place students in classes that best meet their needs.

Some districts use assessments that are based on their curriculum. These tests are either created by the commercial curriculum provider or by the district’s curriculum staff.

20 RCW 28A.300.310.

20

K-12 School Spending and Performance Review

OSPI also provides teachers with classroom-based assessments for use throughout the school year. These tests can be tailored to the unique needs and learning styles of students and enable teachers to measure student progress over time.

In addition, several districts are using surveys of teachers, parents, and students to assess the education the districts are providing and to identify areas in need of improvement. One district described an annual survey they provide to all students in the district asking them what they learned in the prior school year that prepared them for their current grade-level course work.

USING ASSESSMENT DATA In both our survey and our interviews with case study district personnel, we heard many examples of how districts and schools use assessment data to make decisions. Several case study districts said that performance data has helped them become “smarter about what they do.” Below we describe some of the most common uses of performance data identified in our survey and case study districts.

Review Teaching Practices We found that two-thirds of survey respondents use the results from assessments to make changes to their programs and services. As one principal in a case study district said, “Assessment drives how we do things.”

In one case study district, teachers review performance data of students and use those results to modify instruction. An elementary school principal mentioned that the teachers decided to re-teach multiplication after seeing that their students had not done well on a math assessment.

Another district also looks at performance data to identify how well it is delivering curriculum district-wide. For example, we heard from a high school principal that performance data showed ninth graders were struggling in math and English. Rather than just looking within the high school to solve this problem, the principal worked with the middle school principals to set targets for performance in every grade level.

Some case study district principals and superintendents mentioned that they use performance data to determine areas for professional development. In one case study district, we heard from elementary, middle, and high school principals about how they use WASL scores and other performance data to make decisions about professional development needs.

Review Curriculum Other districts described using performance data in making decisions about what curriculum to use. For example, one district used WASL results to evaluate their middle school math curriculum. The district found that their curriculum and materials were not preparing students for the WASL. The district looked at which math skills were areas of weakness for their students and, in 2001, the district purchased new curriculum and changed the way that instructors teach math. Between 2001 and 2004, the percentage of seventh-grade students passing the math WASL has nearly doubled in this district.

21

K-12 School Spending and Performance Review

Identify Students Who Need Extra Assistance Several principals in our case study districts talked about the ways that they use performance data to identify individual students, groups, or classes that need additional assistance. One principal has an assessment notebook that shows the reading performance of all of her students. At this school, the principal, assistant principal, curriculum coach, and kindergarten teachers form a “swat team” to give individual attention to kindergarteners who need extra help learning to read.

Another principal has similar spreadsheets that show the performance of all students in a class. In addition to using this data to identify students who need additional assistance, this principal also uses this data to identify strengths and weaknesses of individual teachers. He can then use this data in making decisions about professional development needs.

Another of the districts we studied uses reading assessments to place students in reading classes depending on their abilities. Additionally, the staff of every school has two or more meetings a year to assess the academic, social, health, and well-being of all of their students.

SHARING PERFORMANCE ASSESSMENT AND IMPROVEMENT STRATEGIES While districts and schools have considerable flexibility in the types of assessments and interventions used to evaluate and improve student performance, the state has several methods for collecting and sharing evidence of successful strategies.

• Professional development programs – The primary mode of identifying and sharing promising practices for improving student achievement is through professional development conferences and trainings. OSPI selects schools that have effectively improved student achievement scores as presenters at state-sponsored conferences and summer institutes. OSPI also makes presentations on best practices at other trainings held throughout the state and works with local educational service districts to share these practices as well.

• Nine characteristics of high performing schools – Through a broad research effort, OSPI identified nine common features of effective schools. OSPI shares this information with schools through trainings held across the state. The characteristics include having effective school leadership, high levels of collaboration, frequent monitoring of teaching and learning, and focused professional development.

• Evaluating curriculum to ensure it is aligned with state standards – OSPI brings together stakeholders to evaluate and score curriculum materials based on how well they align with state learning standards. This information is shared with school districts on OSPI’s website.

• Focused assistance program – OSPI provides three years of focused assistance to select schools that have been identified as needing “school improvement” under No Child Left Behind. This assistance includes a comprehensive educational audit, a school improvement facilitator to help with the development and implementation of a school improvement plan, and other necessary tools, resources, and training for improving student achievement. These efforts are funded by both federal and state sources.

22

K-12 School Spending and Performance Review

LIMITS TO UNDERSTANDING PERFORMANCE THROUGH BUDGETS Most school districts around Washington report using performance data to make budget and program decisions. They use this data to evaluate curriculum and teaching, and to identify students that need additional help. However, this is not readily apparent by looking only at district and school budgets.

The budgets may show that a district bought new curriculum, but it does not tell the story of how districts select one curriculum over another, such as selecting a curriculum that addresses specific weaknesses in student learning. Budgets also can identify the total amount spent on professional development training within a district or school, but not necessarily show how those funds were targeted at areas where students were having the most difficulty meeting state standards.

Some examples from our case studies illustrate the difficulty in relying only on budgets to understand how schools are strategically using resources to improve student performance:

• One principal described how he made additional instructional assistance available for struggling students after reorganizing the schedules of his staff assistants. By coordinating their schedules to avoid unnecessary time spent traveling from one end of the building to the other, the principal was able to gain more time to serve students in need of extra support. This efficiency change is not reflected in the school’s budget because the assistants continue to work the same amount of hours per day.

• Similarly, another principal described how he carved out portions of staff time from the school’s total staffing allotment to provide support classes for students to help them succeed in challenging classes. The school chose to increase class size in certain subject areas to fill the need for additional certificated staff time for before and after school support classes for struggling students. Again, this type of change would not be reflected in a traditional school or district budget.

• To help improve student reading scores, one of the case study high schools decided to focus its professional development dollars on reading. Teachers from all departments and subject areas receive reading training in order to help their students improve their reading abilities. While the total budget for professional development may not have changed, the targeted training represents a new effort to address areas of weakness in the school.

Although budgets often provide a window into understanding district and school priorities and philosophies, they do not capture all of the strategic decisions and detailed resource allocations that are made to improve student performance and achieve state learning standards.

IN SUMMARY Districts around the state are using performance data in making budget and program decisions. They are using assessment results to review curriculum and teaching practices, and to identify students who need help. However, policymakers would not necessarily be able to look at district and school budgets to identify the strategic manner in which they are using assessment data.

23

K-12 School Spending and Performance Review

24

CHAPTER FIVE: REPORTING REQUIREMENTS AND DATA AVAILABILITY CHAPTER OVERVIEW School districts have extensive reporting requirements. The state collects data on districts’ budgets, spending, enrollment, and student achievement. Individual schools also report information on student enrollment and student characteristics. Yet the state does not collect budget or spending data for individual schools.

CURRENT REPORTING REQUIREMENTS During the course of this review, we heard from many district staff that fulfilling state reporting requirements requires significant time and resources. Districts report that they often submit the same data elements to multiple programs at OSPI and that they are uncertain how some of these reports are used by the state. OSPI’s current list of reporting requirements is provided in Appendix 4.

Current state reporting requirements include the following types of information:

• Monthly school district enrollment;

• School district budgets and spending;

• School district personnel data, such as salaries, benefits, education and experience levels and professional certifications; and

• Numerous program-specific reports, such as reports on Bilingual Education, Special Education, Vocational/Career and Technical Education, Child Nutrition, Transportation, and Health Services.

In addition to its own reports, OSPI also collects district reports required by the federal Department of Education and Washington State’s Departments of Health, Social and Health Services, and Corrections. OSPI forwards some of these reports directly to the sponsoring agency, while OSPI reviews others for accuracy before passing them on.

DATA AVAILABILITY Several types of data are needed to understand and evaluate how well schools are meeting performance standards and to make comparisons of schools with similar student characteristics. These include student enrollment, performance, and financial data.

25

K-12 School Spending and Performance Review

Enrollment Data The state collects monthly student enrollment data by district and school. The state also gathers student enrollment in specific programs, including vocational and bilingual education. Enrollment in special education and highly-capable programs is reported at the district level. OSPI also tracks some student characteristics at the school-level, such as ethnicity and percent of students receiving free or reduced-price meals.

Performance Data State-mandated performance data is readily available at both the district and school level. OSPI’s “Report Card” webpage displays the WASL and Iowa Test scores for all districts and schools.21 The Report Card also shows the dropout rates and graduation rates for each high school and district, and shows whether schools are meeting Adequate Yearly Progress (AYP) standards according to No Child Left Behind requirements.

Financial Data The state collects district-level financial information. The funding source and expenditure data presented in Chapter 2 of this report is available for all school districts, organized by state-defined programs, objects of expenditures, and activities. The state also collects personnel costs from each district, including the salaries, and education and experience levels of all certificated and classified staff employed by the district. Most districts code a portion of their personnel to individual schools, but some school personnel are assigned to central departments or programs. As mentioned previously, OSPI does not currently collect spending data for individual schools.

A Note on Collecting School-Level Expenditures JLARC’s 1999 K-12 Finance and Student Performance Study recognized that expenditure data for individual schools would be useful, but concluded that the state did not need to collect this data. The 1999 report stated that the staffing data that OSPI does collect on schools could be used to estimate school-level expenditures since a significant portion of school expenditures are for staffing.

Since the 1999 report was issued, schools and districts are under increased pressure to meet accountability standards set by No Child Left Behind. While staffing continues to represent a major portion of school spending today, district leaders and policymakers may benefit from having more detailed school spending data to help understand and assess school performance. Chapter 6 outlines in more detail some options for reporting and budgeting school expenditures. Exhibit 10 on the next page describes some of the benefits and challenges to collecting school-level spending data.

21 OSPI’s Washington State Report Card is at http://reportcard.ospi.k12.wa.us/default.aspx.

26

K-12 School Spending and Performance Review

• School-level financial data does not provide complete picture of changes made to improve performance. Budgets and expenditure reporting alone do not reveal all of the strategic decisions and resource allocations made to improve student achievement. School-level financial data would have to be combined with other types of information in order to fully understand school performance.

• Unclear whether school-level financial data will answer questions about performance. Some research suggests that the biggest influence on student performance is student characteristics, not spending in schools. If the state collects school-level spending data, it will need to be clear on the type of analyses it hopes to conduct with the information to ensure that the burden of collecting this information outweighs the benefits, and that it is collected in a format that lends itself to specific types of analyses.

• Allocating shared staff and services to individual schools may be difficult. Many districts have staff and programs that serve more than one school. Shared staff may include psychologists, speech language pathologists, and health specialists. Shared programs may include a program for highly capable students or other special needs programs managed by the district and serving multiple schools. Allocating these costs to individual schools would require more extensive timekeeping and reporting than currently is maintained by most school districts. Additionally, to obtain comparable information, districts would need to track these costs in a consistent manner.

• Districts have different ways of accounting for school-level spending in their accounting systems. As discussed in Chapter 3, districts have different ways of coding expenditures to schools. The state would need to develop and require the use of uniform accounting standards for school-level expenditures in order to collect comparable information about school-level spending from districts around the state.

• An increased transparency and accountability in K-12 spending. School-level financial data would allow the public to see exactly what is being spent at individual schools and how resources are allocated within school districts and schools.

Challenges:

• An improved understanding of the impact (if any) spending may have on performance. Researchers in education policy do not agree on whether and to what extent school spending patterns influence student achievement. If school expenditure information was readily available, including spending on professional development, curriculum, teacher mentorship, and special supports for struggling students, more detailed analysis could be conducted on the linkage between spending and performance.

Benefits: • A more complete picture of school spending than current state personnel system can

provide. In general, districts assign most of their certificated and classified staff to individual schools. However, some employees are assigned to a central department or program because they serve multiple schools. These employee expenditures are often lost in any analysis that uses existing personnel assignments as a proxy for school expenditures.

Exhibit 10 – Benefits and Challenges of Collecting and Using School-Level Spending Data

27

K-12 School Spending and Performance Review

IN SUMMARY The state collects data on district spending, enrollment, and performance. However, it does not collect spending data for individual schools. This information could be useful because of increased attention on school performance. It would provide a more complete picture of school-level spending, provide data to examine the link between spending and performance, and increase transparency and accountability. However, reporting this data may be difficult for districts and schools. It also is unclear how this data would be used by the state to understand school performance, especially since expenditure data alone does not tell the entire story of how districts and schools are making strategic changes to improve performance.

28

CHAPTER SIX: ALTERNATIVE APPROACHES TO REPORTING AND BUDGETING SCHOOL EXPENDITURES CHAPTER OVERVIEW This chapter discusses alternative approaches to reporting and budgeting school expenditures that are being considered or implemented throughout the country. The nine alternative approaches outlined here respond to a variety of district or state goals. When policymakers consider these varying approaches, it is important to think about the appropriate role of the state in school-level finance and the specific goals intended behind each alternative approach.

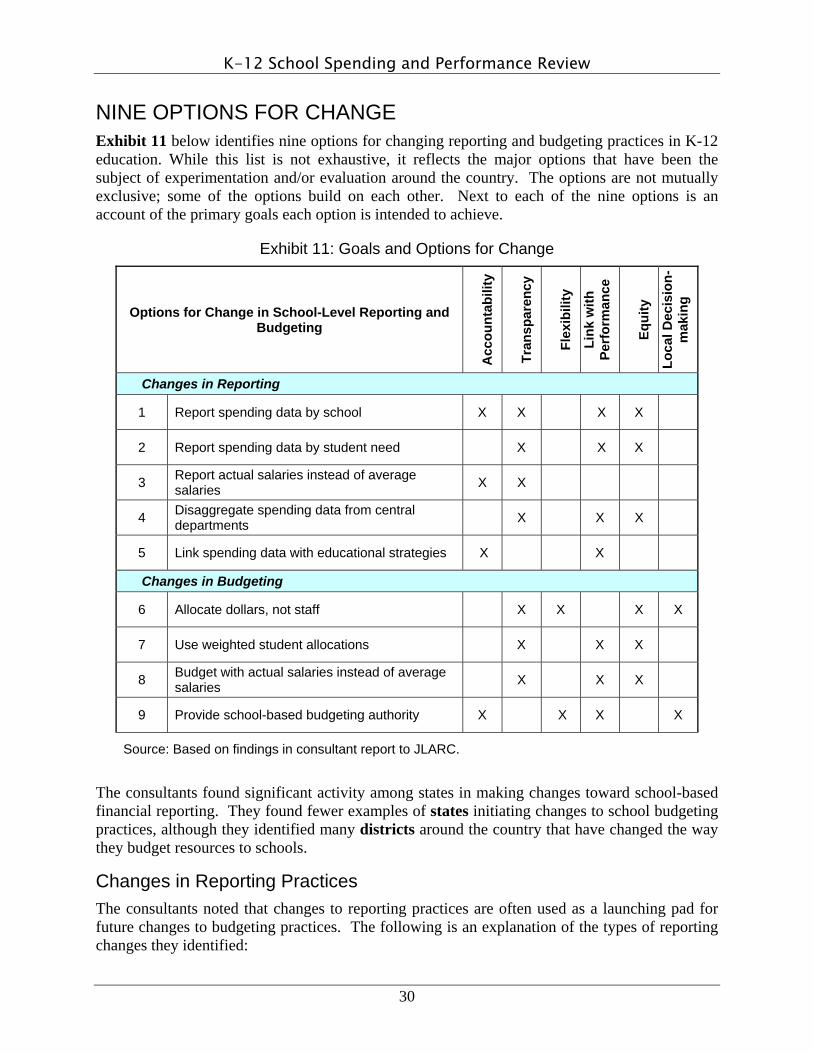

This chapter is based on a report completed by consultants JLARC hired for this review.22 The full report includes specific examples of states and districts that are engaged in alternative reporting and budgeting practices. Here, we focus on the merits and challenges of each option and its applicability to Washington State.

WHY CHANGE SCHOOL REPORTING AND BUDGETING PRACTICES? As education reform has placed increased emphasis on school-level accountability, some policymakers have become interested in changing the way school finances are reported and budgeted to achieve varying goals, as indicated below:

• Align finance with school accountability so policymakers can see how much is spent at individual schools;

• Provide for greater spending transparency and clarity;

• Allow for increased flexibility in resource use;

• Link spending with student performance;

• Increase equity among schools within each district; and

• Allow schools greater discretion in budgeting decisions.

If policymakers consider changes to school reporting and budgeting practices, it is important to have a clear idea of which of these goals they are trying to address.

22 The group of consultants JLARC hired for this piece of analysis is Marguerite Roza, Research Assistant Professor and research consultant at the University of Washington; Claudine Swartz, independent policy consultant for the development of K-12 education reforms; and Jennifer Harris, attorney and research consultant in public finance. Their work is based on a review of literature on this topic and their original research on what is happening around the country and in Washington school districts.

29