july 27, 2015 tsxv-ev - squarespacestatic1.squarespace.com/static/535e7e2de4b088f0b623c597/... ·...

TRANSCRIPT

Summary

July 27, 2015 TSXV-EV

Target C$0.23

New

Old

Recommendation Positive N/A

Target C$0.23 N/A

Recent Px Shares O/S

$0.07 ~257M

Shares O/S FD ~270M Market Cap ~C$17.7 Net Cash ~C$1.4M

ERIN VENTURES INC.

//Borates

INITIATING COVERAGE

Boron for the Modern Market

Our recent borates industry report highlighted three major factors

that delineate a modern, world-class boron project: high grade

(likely greater than 25% B2O3 content, of one or more of the four

commercial boron-bearing minerals), low sodium content (so the

majority of the mineral content should be a calcium borate such as

colemanite) and low arsenic content (to meet increasingly stringent

environmental regulations)

The Piskanja deposit belonging to Erin Ventures meets all the above

requirements and is located in a good, albeit generally unrecognized,

mining jurisdiction in Serbia

Our financial analysis, using our borates and boric acid price decks,

suggests that a “risk-free” value for Erin would be more than $1.40.

Based on the state of the financial markets and a 28% discount rate

to properly account for financing risk, we would suggest that Erin is

worth more than $0.20 today, significantly more than the current

trading range. We are initiating coverage on Erin with a positive

recommendation.

Jon Hykawy, PhD President

Tom Chudnovsky Managing Partner

S T O R M C R O W

See the end of report for important disclosures

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 2

In our recent industry report on boron (released April 21, found at: www.stormcrow.ca/research), we noted that the market is growing such that a supply gap of some 300,000 tpa B2O3 equivalent will likely arise by 2023. Even today, however, buyers would likely be receptive to a new producer entering the market, as the space is now dominated by an oligopoly of two major producers: Rio Tinto and its US Borax Boron Mine in California, and ETi Mine Works and their monopoly on boron production in Turkey. We also noted that with increasingly stringent environmental regulation and a continuing emphasis on glass production, what would be particularly useful would be a supplier that can produce arsenic-free colemanite concentrates, since arsenic is an increasing issue for current producers, and colemanite, which is a calcium borate, is much preferred to the more commonly available sodium borates for the production of E-glass types of fiberglass. It is perhaps worth noting that ETi has a virtual monopoly on the current global production of colemanite, as the US Borax Mine overwhelmingly produces sodium borates.

In this report, we will introduce readers to Erin Ventures, a company that, surprisingly, hits all the marks.

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 3

The Boron Industry – A Recap

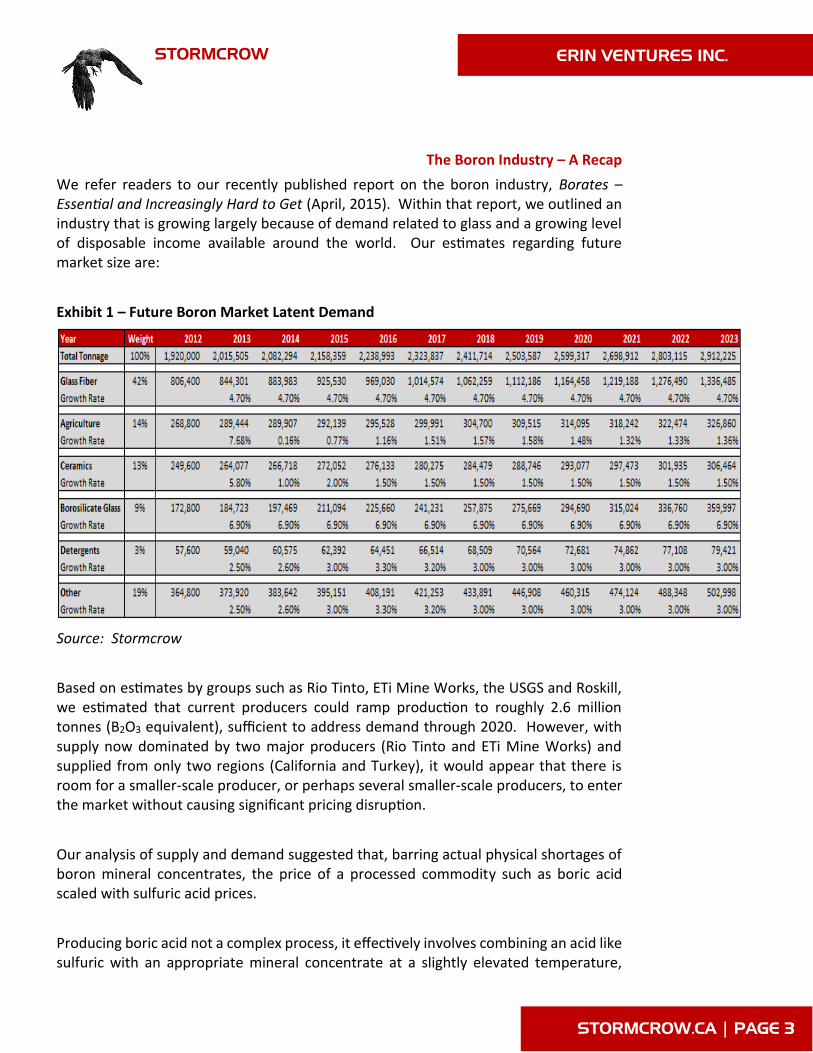

We refer readers to our recently published report on the boron industry, Borates – Essential and Increasingly Hard to Get (April, 2015). Within that report, we outlined an industry that is growing largely because of demand related to glass and a growing level of disposable income available around the world. Our estimates regarding future market size are:

Exhibit 1 – Future Boron Market Latent Demand

Source: Stormcrow

Based on estimates by groups such as Rio Tinto, ETi Mine Works, the USGS and Roskill, we estimated that current producers could ramp production to roughly 2.6 million tonnes (B2O3 equivalent), sufficient to address demand through 2020. However, with supply now dominated by two major producers (Rio Tinto and ETi Mine Works) and supplied from only two regions (California and Turkey), it would appear that there is room for a smaller-scale producer, or perhaps several smaller-scale producers, to enter the market without causing significant pricing disruption.

Our analysis of supply and demand suggested that, barring actual physical shortages of boron mineral concentrates, the price of a processed commodity such as boric acid scaled with sulfuric acid prices.

Producing boric acid not a complex process, it effectively involves combining an acid like sulfuric with an appropriate mineral concentrate at a slightly elevated temperature,

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 4

then precipitating and drying the resulting crystals of boric acid. So the price of a boron mineral such as colemanite must scale to a level allowing for profit both to the miner and to the boric acid producer, with sufficient margin to procure the required sulfuric (or other) acids to convert the colemanite to boric acid. In many cases, the company producing the boric acid already has surplus sulfuric acid available to it at an effective very low cost.

This analysis led us to conclude, again assuming that sufficient production of boron mineral concentrates is available through 2023, that the price of boric acid and a mineral such as colemanite would trend as follows:

Exhibit 2 – Medium-Term Forecasts for Boric Acid (99.9+%) and Colemanite (40% B2O3)

Source: Stormcrow

We chose colemanite as our boron mineral for the analysis for a simple enough reason. There are four primary minerals used in the production of boron chemicals today:

Colemanite (CaB3O4(OH)3·H2O), which is an alteration product of ulexite

Ulexite ((NaCaB5O6(OH)6•5(H2O)), also known as “TV stone” for its optical properties

Tincal/borax (Na2[B4O5(OH)4]·8H2O)

Kernite (Na2B4O6(OH)2·3(H2O))

Note that all but colemanite are sodium borates. Only colemanite is a calcium borate, and a colemanite concentrate would thus contain dramatically less sodium. But boron demand is as shown below:

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 5

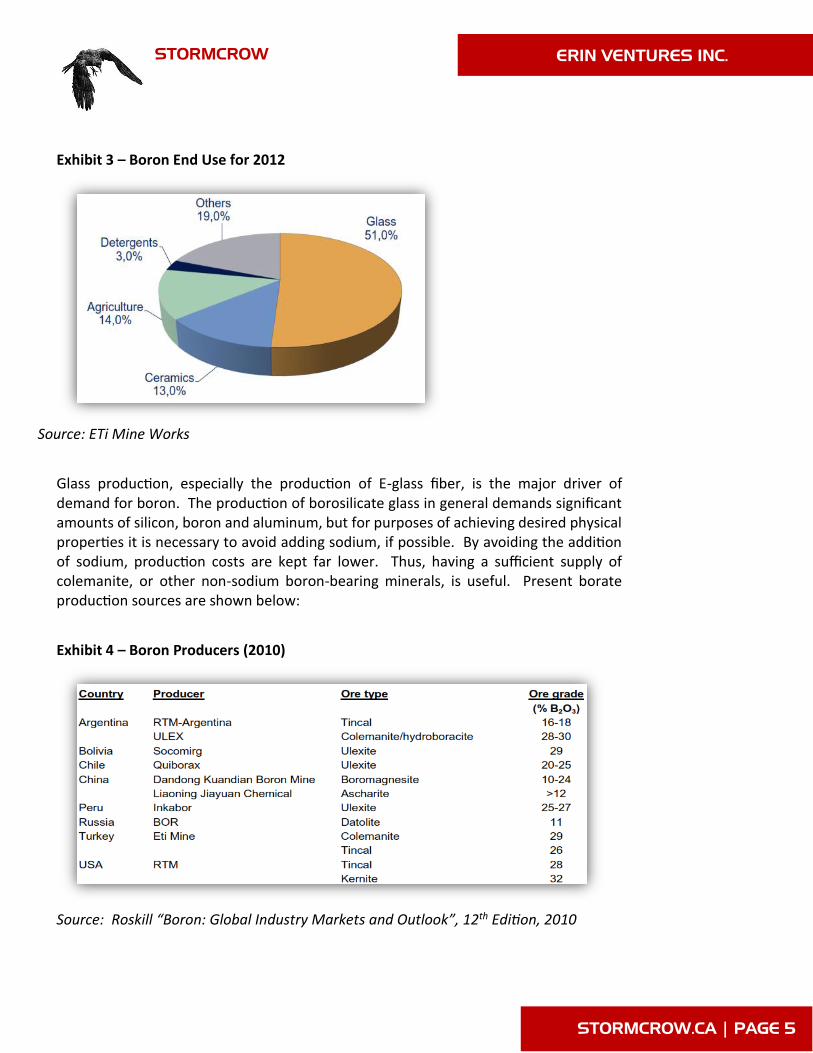

Exhibit 3 – Boron End Use for 2012

Source: ETi Mine Works

Glass production, especially the production of E-glass fiber, is the major driver of demand for boron. The production of borosilicate glass in general demands significant amounts of silicon, boron and aluminum, but for purposes of achieving desired physical properties it is necessary to avoid adding sodium, if possible. By avoiding the addition of sodium, production costs are kept far lower. Thus, having a sufficient supply of colemanite, or other non-sodium boron-bearing minerals, is useful. Present borate production sources are shown below:

Exhibit 4 – Boron Producers (2010)

Source: Roskill “Boron: Global Industry Markets and Outlook”, 12th Edition, 2010

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 6

With the US production from Rio Tinto and the Turkish production from ETi dominating, and the Rio Tinto Boron Mine in California being the single largest global production source at around 23% of annual global output, it would be useful to find additional, initially relatively small, suppliers of colemanite. If those suppliers also had clean colemanite, relatively free of arsenic or other toxins, that would be a significant plus and contribute to lower supply costs, as well.

With all this in mind, we can move on to examining Erin Ventures.

Erin Ventures – Serbian Boron for Tomorrow’s Market

Erin’s claims in Serbia, located approximately 250 km south of Belgrade with access by good paved roads, are known as the Piskanja Deposit. The lithology of the region is composed of soft sedimentary host rock (including shales and limestone) with two primary, shallow borate beds and a total of 10 beds overall. The mineralization of these beds is colemanite, with a small amount of accompanying ulexite and other boron-bearing minerals. That the deposit is primarily colemanite is a significant advantage in selling to manufacturers of fiberglass and other glasses. It should also be understood that a deposit containing some sodium borates is in no way unusual, as almost all the world’s producing boron mines contain more than one mineral type.

Exhibit 4 – Piskanja Location

Source: Erin Ventures

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 7

The area around Piskanja has excellent existing infrastructure, including all-weather roads, rail, electrical power lines, etc. The area has been home to mining for a very long period of time, so there is also an experienced work force in the area. This is not “moose pasture” in the traditional Canadian mining definition of such. The amount of capital required to compensate for a lack of local development at Piskanja would be small.

Exhibit 5 – Cross-Section through Piskanja

Source: Erin Ventures

Our earlier work on the borate industry highlighted the increasing emphasis being placed on a lack of toxic contaminants being present in a boron mine. Specifically, arsenic is causing increasing concern to miners, as higher and higher degrees of scrutiny on tailings disposal is coupled to the need to ship cleaner and cleaner product so that the downstream buyer does not have to deal with their own arsenic problem. It is comforting to learn that the base level of arsenic present in the Piskanja deposit appears to be low, below 10 ppm where typical Turkish concentrates grade over 30 ppm. In addition, questions we asked of company management resulted in our determining that unnamed third party users of borates have already attempted to convert Piskanja concentrate to boric acid, and have done so successfully without any concern regarding the quantity of arsenic in the resulting boric acid.

In Q3 of 2010, the company applied for an exploration license, and was granted both the right to explore the property as well as sole right to apply for a mining license. Roughly one year later, a drill program began.

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 8

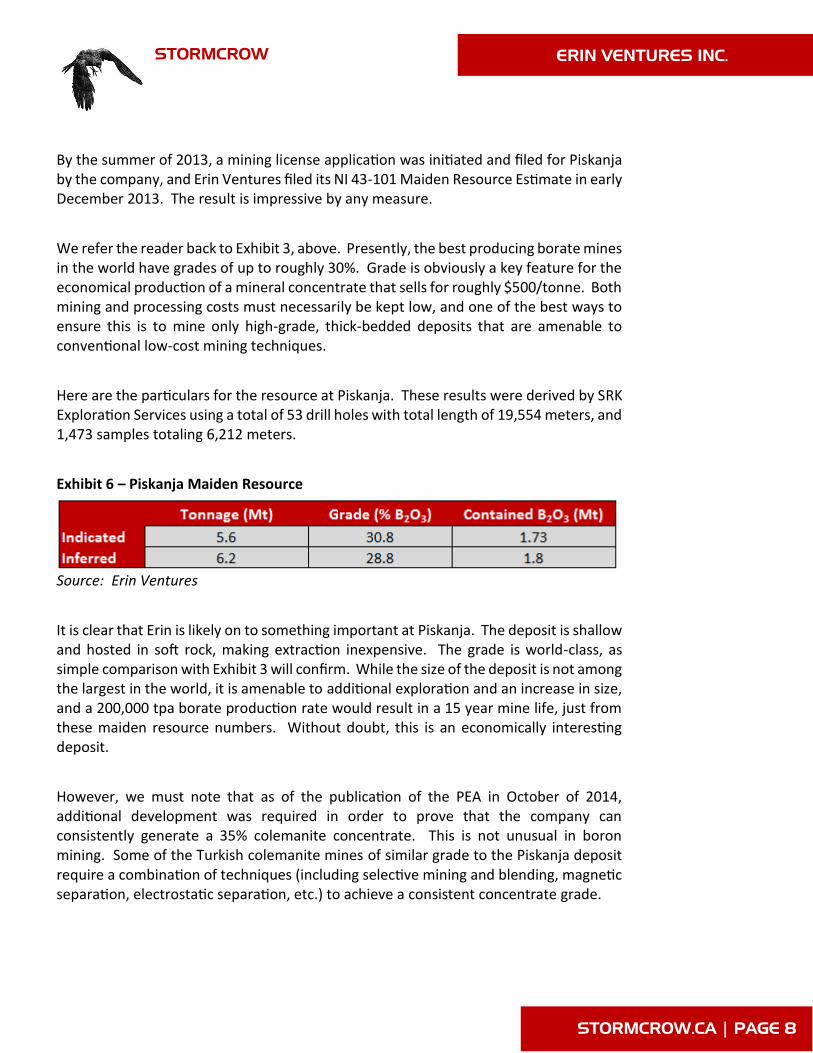

By the summer of 2013, a mining license application was initiated and filed for Piskanja by the company, and Erin Ventures filed its NI 43-101 Maiden Resource Estimate in early December 2013. The result is impressive by any measure.

We refer the reader back to Exhibit 3, above. Presently, the best producing borate mines in the world have grades of up to roughly 30%. Grade is obviously a key feature for the economical production of a mineral concentrate that sells for roughly $500/tonne. Both mining and processing costs must necessarily be kept low, and one of the best ways to ensure this is to mine only high-grade, thick-bedded deposits that are amenable to conventional low-cost mining techniques.

Here are the particulars for the resource at Piskanja. These results were derived by SRK Exploration Services using a total of 53 drill holes with total length of 19,554 meters, and 1,473 samples totaling 6,212 meters.

Exhibit 6 – Piskanja Maiden Resource

Source: Erin Ventures

It is clear that Erin is likely on to something important at Piskanja. The deposit is shallow and hosted in soft rock, making extraction inexpensive. The grade is world-class, as simple comparison with Exhibit 3 will confirm. While the size of the deposit is not among the largest in the world, it is amenable to additional exploration and an increase in size, and a 200,000 tpa borate production rate would result in a 15 year mine life, just from these maiden resource numbers. Without doubt, this is an economically interesting deposit.

However, we must note that as of the publication of the PEA in October of 2014, additional development was required in order to prove that the company can consistently generate a 35% colemanite concentrate. This is not unusual in boron mining. Some of the Turkish colemanite mines of similar grade to the Piskanja deposit require a combination of techniques (including selective mining and blending, magnetic separation, electrostatic separation, etc.) to achieve a consistent concentrate grade.

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 9

Management has discussed several additional paths for achieving this quality of concentrate with us, and we are comfortable that an approach can be developed to reach 35-40% final B2O3 content.

It is important to note that the industry is small enough that the “standards” in the space are effectively set by only one or two entities (Rio Tinto or ETi). The 35-40% concentrate “standard” is a specification largely set by ETi. We understand that It is not unusual for colemanite concentrate shipments from Turkey to contain anywhere from 30-40% B2O3. The final determination as to whether concentrate is useful to a customer will be whether that concentrate works for them, and can be qualified for them for future use.

And as for making boric acid internally, concentrate grade is, for all practical purposes, irrelevant.

Economic Prospects – Some Guesswork Involved, but Profit to Spare

There is little involved in mining borates, beyond the basics common to all mineral projects. Mining the material from a conventional room and pillar operation is simple enough to contemplate, and to conjecture regarding costs. The ore must be ground to an amenable size. The resulting milled ore is then floated and the colemanite is separated from host rock.

Based on the cost of mining at this scale, and our cost estimates for production, we actually believe that the company has been conservative in its estimates that 200,000 tpa colemanite concentrate production and 25,000 tpa boric acid production can be accomplished for a total operating cost average of some $12.6 million. However, given that the current Erin 43-101 is a PEA, we will increase this operating cost estimate by 20%, on the assumption that all PEAs are optimistic, and we will also increase operating cost 2% per annum due to inflation.

As to revenues, we will assume a one year ramp to full production of colemanite concentrate, and an 18 month ramp to full production of boric acid. Our price forecasts for the two materials from Exhibit 2, above, will be used. Obviously, we will assume that Erin will produce both colemanite concentrate as well as the more profitable boric acid. The company is targeting 200,000 tpa production of concentrate and 25,000 tpa production of boric acid.

Capital costs total some $84.6 million, including a 20% contingency. We will assume that this capital cost is financed with half equity, and half debt. The debt will be assumed to carry a 7% interest rate, and be payable over 8 years. The tax rate that Erin will be

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 10

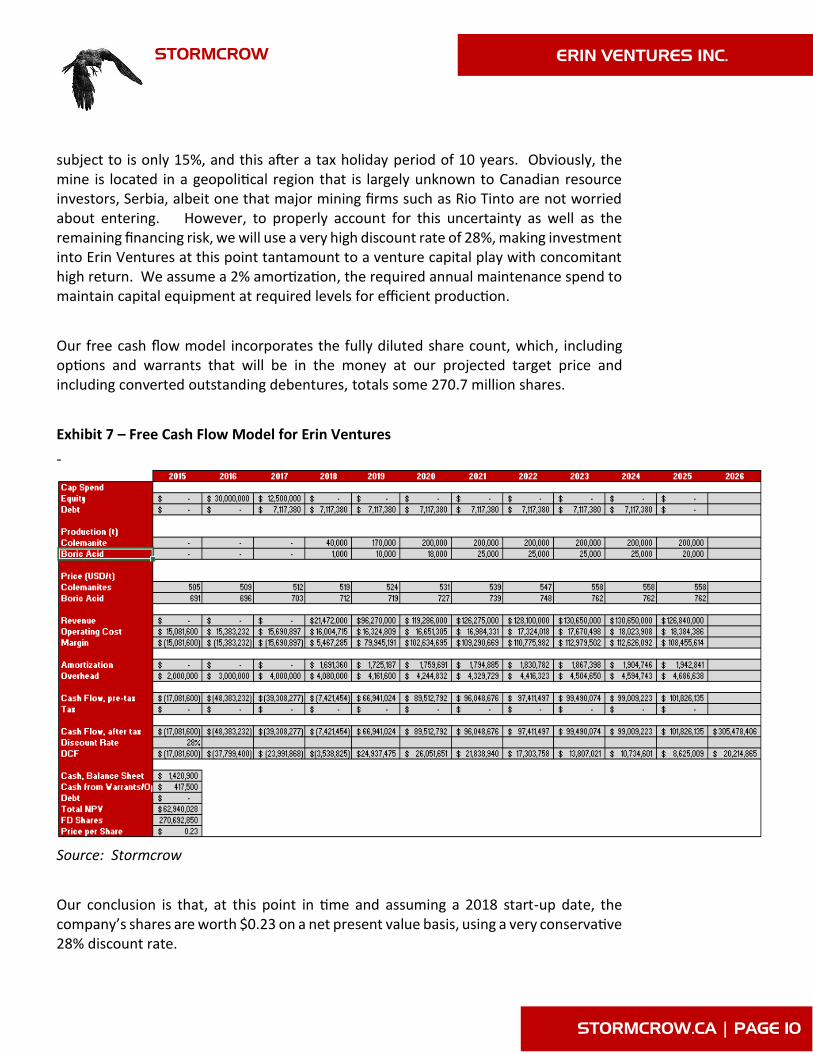

subject to is only 15%, and this after a tax holiday period of 10 years. Obviously, the mine is located in a geopolitical region that is largely unknown to Canadian resource investors, Serbia, albeit one that major mining firms such as Rio Tinto are not worried about entering. However, to properly account for this uncertainty as well as the remaining financing risk, we will use a very high discount rate of 28%, making investment into Erin Ventures at this point tantamount to a venture capital play with concomitant high return. We assume a 2% amortization, the required annual maintenance spend to maintain capital equipment at required levels for efficient production.

Our free cash flow model incorporates the fully diluted share count, which, including options and warrants that will be in the money at our projected target price and including converted outstanding debentures, totals some 270.7 million shares.

Exhibit 7 – Free Cash Flow Model for Erin Ventures

-

Source: Stormcrow

Our conclusion is that, at this point in time and assuming a 2018 start-up date, the company’s shares are worth $0.23 on a net present value basis, using a very conservative 28% discount rate.

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 11

Note that if we use the standardized “risk-free” discount rate of 8% typical of NI 43-101 studies, the target price on Erin with our boron price decks would be more than $1.40. However, no one could logically, at this point in time, argue that the risk facing Erin is properly reflected by an 8% discount rate.

Conclusions – Borate for Tomorrow’s Market

Erin Ventures is in a position to produce an amount of colemanite and boric acid from a world-class deposit in Serbia, in amounts that should be non-disruptive to the existing

borate market. We like the grade and chemistry of the deposit, in that the high-grade colemanite making up the bulk of the mineralization within the Piskanja deposit is naturally sodium free, and the deposit itself is remarkably free of arsenic, which is rapidly becoming a major concern for boron miners.

With our projected future prices for both boric acid and colemanite, Erin Ventures appears to be a highly undervalued mining story, in an industrial commodity space that is largely unknown to Canadian mining investors but one that is increasingly important, globally. Indeed, on a “risk-free” basis, a discounted cash flow analysis suggests that Erin is one of the best free cash generators of any junior mining story we have examined. Our financial analysis, using a very high discount rate to represent the remaining financing risk, suggests that the stock is highly undervalued at present.

We are initiating coverage on Erin Ventures with a positive recommendation and C$0.23 target. In a space where grade and chemical compatibility are beginning to rule the day, Erin Ventures is arriving at precisely the correct time.

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 12

Keywords

Important Disclosures

1. Stormcrow Capital Ltd. (“Stormcrow”) is an Exempt Market Dealer registered with the Ontario Securities Commission.

Stormcrow has both issuer and investor clients. Stormcrow is also a financial and technical/scientific consultant that provides

certain of its clients with some or all of the following services: (i) an assessment of the client’s industry, business plans and

operations, market positioning, economic situation and prospects; (ii) certain technical and scientific commentary, analysis

and advice that is within the expertise of Stormcrow’s staff; (iii) advice regarding optimization strategies for the client’s

business and capital structure; (iv) due diligence investigation services; and (v) opinions regarding the future expected value

of the client’s or a offeror/offeree’s equity securities so as to allow the client to then make capital market, capital budgeting

and capital structure plans. With the consent of Stormcrow’s issuer client, the client and/or its industry sector may be the

subject of an investment or financial research report, newsletter, bulletin or other publication by Stormcrow where such

publication is made publicly available at www.stormcrow.ca or elsewhere or is otherwise distributed by Stormcrow. Any such

publication is limited to generic, non-tailored advice or opinions and should not be construed as investment advice that is

suitable for the reader or recipient. Stormcrow does not offer personalized or tailored investment advice to anyone (other

than its current investor clients) and Stormcrow’s research reports should not be relied upon by anyone in making any

investment decisions. Rather, investors should speak in person with their personal financial advisor(s) to obtain suitable

investment advice.

2. The company that is the subject of this report is currently a client of Stormcrow.

3. Stormcrow and/or some of Stormcrow’s officers, directors, or significant shareholders own, directly or indirectly, shares in

the company that is the subject of this report. As at the date of this report, Stormcrow and its officers, directors, and

significant shareholders beneficially hold an aggregate of less than 1% of the outstanding equity shares of the company that

is the subject of this report. The research analyst(s) and/or associates who prepared this report (or their household members)

do not currently beneficially hold an equity position in the company that is the subject of this report.

4. Although it is a policy of Stormcrow that Stormcrow and its employees are to refrain from trading in a manner that is contrary

to, or inconsistent with, Stormcrow’s most recent published investment recommendations or ratings, Stormcrow does permit

itself and its employees to sell shares in circumstances where working capital and cash flow requirements require the sale of

securities that would otherwise continue to be held. Any shares currently held by Stormcrow and/or some of Stormcrow’s

officers, directors, or significant shareholders in the company that is the subject of this report are held for investment

purposes and may be sold (or additional shares acquired) in the future depending upon market conditions or other relevant

factors.

Industry Boron, Borates, Critical Materials, Mining, Industrial Minerals, Borosilicate

Relevant

Companies

Rio Tinto plc – RIO:LON

Eti Mine Works – Private

Erin Ventures – EV:TSXV

Bacanora Minerals Ltd – BCN:TSXV

Orocobe Minerals – ORL:TSX

Why do we use keywords?

We feel people who could stand to benefit from the contents of this report, are not solely ones who already follow the specific company or sector discussed herein. As such, we hope to provide this free service to as wide an audience as possible—and keywords help to this end.

Sovereign Metals Inc. (SVM | ASX) STORMCROW

ERIN VENTURES INC.

STORMCROW.CA | PAGE 13

5. Stormcrow has, within the previous 12 months, provided paid investment banking or consultant services or has acted as an

underwriter to the company that is the subject of this report.

6. Stormcrow expects that it may provide, within the next 12 months, paid investment banking or consulting services, or that

Stormcrow may act as an underwriter to the company that is the subject of this report.

7. Stormcrow intends to provide regular market updates on the affairs of the company that is the subject of this report (at

Stormcrow’s discretion) and make these updates publicly available at www.stormcrow.ca. Readers who wish to receive

notice when such updates become available, should email to [email protected] with the subject heading “Get Update

Notifications”.

8. All information used in the publication of this report has been compiled from publicly available sources that Stormcrow

believes to be reliable. Stormcrow does not guarantee the accuracy or completeness of the information found in this report

and Stormcrow may not have undertaken any independent investigation to confirm or verify such information. Opinions

contained in this report represent the true opinion of Stormcrow and the author(s) at the time of publication.

9. The securities described in this research report may not be eligible for sale in all jurisdictions or to certain categories of

investors. This report and the content herein should not be construed by anyone as a solicitation to effect, or attempt to

effect, any transaction in a security. This document was prepared and was made available for information purposes only and

should not be construed as an offer or solicitation for investment in any securities mentioned herein. The securities referred

to herein should be considered speculative in nature and should be considered to involve a high amount of financial risk

where investors may lose all of their investment.

10. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of

future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties

and other factors which may cause the actual results, performance or achievements of their subject matter to be materially

different from current expectations. No representation is being made that any investment or security will or is likely to

achieve the return or performance estimated herein. There can be sharp differences between expected performance results

and the actual results.

Dissemination of Research

This research report is widely available to the public via Stormcrow’s website: www.stormcrow.ca. This report is intended solely for the use of persons in jurisdictions where Stormcrow is registered or where the dissemination of this report does not require registration. Stormcrow is not registered as a securities broker-dealer (or an equivalent thereof) in the United States, United Kingdom or any other jurisdiction other than noted above. Stormcrow is not subject to U.S. or U.K. rules with regard to the preparation of research reports and the independence of analysts. This report does not constitute an offer to sell or a solicitation to buy any of the securities discussed herein.

Investment Rating Criteria

We do not provide an investment rating, beyond indicating whether the target price exceeds current trading ranges by a reasonable range, indicated as “Positive”, or whether the target price is either below or roughly equivalent to the current trading range, indicated as “Negative”. Each investor generally has an individual target return in mind, we leave it to the individual investor and his/her/its financial advisor to determine how our target and the current price and investment risks would fit within their portfolio.