july 2005 state tax return – special volume 12 number 7 …€¦ · · 2005-08-30volume 12...

TRANSCRIPT

Volume 12 Number 7

1

July 2005

State Tax Return – SpecialReport

Escheat -- The Basic Rules, What The U.S. Supreme CourtDictated About Compliance Priorities, B-To-B Exemptions,Gift Card Planning Opportunities, And Recent CasesMaryann B. GallColumbus(614) 281-3924

This special edition of the State Tax Return is a comprehensive review of the historyand evolution of unclaimed property law, an increasingly important area of accountmaintenance, state and federal reporting, and the difficulties which arise upon auditwhen the "holder" does not properly report and remit unclaimed property.

Modern unclaimed property legislation resulted from uniform acts that were promulgatedin 1954, 1966, 1981, and 1995. While various versions of the uniform acts serve as thebasis for state law, some states have not adopted a uniform act at all or have onlyadopted various provisions. Each "holder" must be aware of what specific statestatutory escheat code applies to it at any given point in time.

This report explains the basic concepts in unclaimed property law:

OWNER -- persons with legal or equitable interests in statutorily definedunclaimed property.

HOLDER -- persons who must report and remit unclaimed property to theproper state.

CUSTODIAN -- the concept that states act for the "owner" in a custodialcapacity until the owner appears to claim his or her property. This impactsupon the frequency of reporting and state audits.

UNCLAIMED PROPERTY -- what specific items of intangible property aresubject to escheat and what specific statutory exemptions exist for certainkinds of property. The exemptions vary from state to state.

An important area is the priority rules on escheat of intangible property. These wereestablished by the United States Supreme Court. Various states had different theoriesof reporting and remitting property which resulted in original jurisdiction litigation in the

©Jones Day 2005

2

United States Supreme Court. The "big three" cases were decided in 1965, 1972, and1993. They established the basic framework that each "holder" must understand.

As in state taxation, there are planning opportunities for "holders." One section of thisreport reviews the "business-to-business" exemptions, summarized on Chart B. If youare a retailer or give advice to retailers, you will be interested in the treatment of giftcertificates and gift cards by different states, summarized in Chart A.

Two interesting recent cases are highlighted, both from California. The first deals withthe potential liability of an auditor for failure to disclose escheat obligations of its client.The second case was decided in March, 2005, by the federal Court of Appeals for the9th Circuit. It established a cause of action against the California Controller for violationsof the notice requirements in the California Unclaimed Property Law.

I. HISTORY & EVOLUTION OF UNCLAIMED PROPERTY LAW

A. ENGLISH COMMON LAW

1. Modern unclaimed property laws are rooted in the English common law doctrinesof escheat and bona vacantia. These doctrines were taken into American law by thestates following the Revolutionary War.

2. Escheat: At English common law, escheat was an outgrowth of the feudal tenuresystem of landholding whereby the Crown was recognized as the ultimate owner of allreal property. When some event obstructed the normal course of descent of realproperty, escheat was the means by which land returned to the tenant’s lord, or in theabsence of such a lord, to the Crown. Escheat was therefore originally developed by thecourts to assure continued performance of services to the tenant’s immediate lord toreconvey the land to another tenant able to perform. In England, escheat was applicableonly to real property held in fee. This original rationale for escheat, however, becamealmost non-existent after 1290 when subinfeudation1 was abolished and creation of newmesne-lords was prevented. As the passage of time eliminated existing lords, escheatcame to be considered a royal prerogative.

3. Bona Vacantia: The doctrine of bona vacantia,2 at English common law, wasapplied to personal property. Unlike escheat, the Crown’s claim to personal propertywas based on the absence of any other owner, rather than on its status as an ultimate

1 Subinfeudation was defined as the process whereby, under the feudal system of landholding, a

person receiving a grant of land from a lord, could himself become a mesne-lord by subdividing andsubletting that land to others. One parcel of land could thus be the subject of many different subtenures.Due to dissatisfaction on the increase of such subtenures, a statute was passed in 1290 to abolishsubinfeudation, allowing the tenant to alienate whenever he pleased and freely transfer ownership toothers.

2 Bona vacantia (Latin, meaning vacant goods) is a doctrine of the common law in England underwhich ownerless property passes by law to the Crown. If legal ownership to a property cannot beestablished by anyone else, it falls to the Crown to deal with the assets concerned. Although bonavacantia arose, in origin, by virtue of the royal prerogative at common law, this is still the position to someextent although the right to bona vacantia is now based on statute in England.

©Jones Day 2005

3

owner. Essentially, bona vacantia provided that the personal property without an ownercould be claimed by the Crown. The Crown could claim the property against all but therightful owner. At common law, abandoned personal property was thus not the subjectof escheat, but was subject only to the right of appropriation by the sovereign as bonavacantia.

B. AMERICANIZATION OF ESCHEAT

1. Early in the history of the United States, states adopted laws recognizing theEnglish common law doctrine of escheat and later, the doctrine of bona vacantia. Thestate’s interest in the escheat of real property was derivative of the Crown’s interestunder the English common law. However, as for bona vacantia, instead of the Englishcommon law basis of the Crown’s retention of title, any interest which the stateassumed in personal property under bona vacantia was derived from an expression ofthe state’s police powers because there was no owner to claim the property. Escheatand bona vacantia ultimately merged into a single doctrine which was denominatedescheat. The statutes in the early nineteenth century were in general applicable to realproperty only, but late in the century, a few states began to apply the principles ofescheat to personal property. Statutes applicable to intangible property also evolvedover time.

2. Several early Supreme Court decisions supported the states’ constitutional rightsto escheat. In Hamilton v. Brown, 161 U.S. 256 (1896), the United States SupremeCourt upheld the constitutionality of a statute providing for escheat of real property whenan owner dies intestate. The Court concluded that if the statute enumerated theconditions for escheat and the basis for determining that there were no legal heirs, itmet the due process requirements of the Constitution and therefore did not represent anunconstitutional impairment of contract. In addition, in Cunnius v. Reading Sch. Dist.,198 U.S. 458 (1905), the Court held that a state statute that provided for the state’sadministration of intangible personal property of persons unheard of and absent for aperiod of seven years or more, did not violate the Fourteenth Amendment of theConstitution. The Court concluded that where the provisions of a state statute foradministration on the assets of an absentee were reasonable as to the period ofabsence necessary to create the presumption of death, and created proper safeguardsfor the protection of his interests, the State did not deprive the absentee of his propertywithout notice in violation of the Due Process Clause.

3. Accordingly, the states could by legislation expand the regulation of successionto property to include not only those situations in which an owner died intestate andwithout heirs, but also those in which an owner could not be located or apparentlyabandoned any claim to the property or was otherwise unaware of the existence of theproperty.

©Jones Day 2005

4

II. MODERN UNCLAIMED PROPERTY LEGISLATION

A. OVERVIEW

1. Today, all 50 states and the District of Columbia have unclaimed property laws,most of it modeled after the Uniform Disposition of Unclaimed Property Act of 1954 and1966, or the Uniform Unclaimed Property Act of 1981 and 1995 (“Act”).

2. Prior to the 1954 Act, statutes on unclaimed property were exceedingly diverse incharacter and were often not well formulated. Although most states had statutes dealingwith the disposition of unclaimed tangible personal property and a considerable numberof states have statues dealing with the disposition of unclaimed bank deposits, only 10states then had adopted comprehensive legislation covering the entire field ofunclaimed property. The first Uniform Act was approved by the National Conference ofCommissioners on Uniform State Laws (“NCCUSL”) in 1954 to introduce greatersymmetry in the law for the benefit of persons doing business in more than one state,and to correct the problem of multiple liability encountered by holders of unclaimedproperty. The Uniform Act also serves to protect unknown owners by locating them andreturning property to them, and to give the state rather than the holders of unclaimedproperty the benefit of its retention.

3. All of the Uniform Acts are custodial in nature, and do not result in the loss of theowner’s rights. While a traditional escheat statute transfers the ownership of abandonedproperty to the state, the Uniform Acts provide for transfer of custody of unclaimedproperty from the holder to the state. The state is required to hold until and unless suchproperty is claimed by the rightful owner. The owner therefore retains his right ofpresenting his claim at any time no matter how remote. As such, state records will haveto be kept on a permanent basis. Even though the states do not receive title to theunclaimed funds, they enjoy benefits from the right to hold and use unclaimed funds forthe general benefit of state citizens.

B. THE UNIFORM ACTS

1. General: The 1995 Act and its predecessors provide rules to determine wheneligible property is unclaimed. Once property may be identified as unclaimed, the holderis required to report that property to the state unclaimed property administrator. Afternotice to the owner is formally attempted by the holder, the property is transferred to theunclaimed property administrator. The state administrator once again attempts notice toowners. Cash goes into the state general fund. Non-cash is held for a period of time andthen sold. The administrator maintains a fund from which owners can make claims forpayment. A claims procedure is provided for owners to make their claims.

2. 1954 Act: The 1954 Act revolved around the issue of multiple liabilities. Thisoccurred when two or more states had statutes claiming jurisdiction over the sameproperty held by a particular business. The 1954 Act had a reciprocity provision whichserved to eliminate multiple liabilities for businesses that operated in more than one

©Jones Day 2005

5

state, so the holder was not subject to more than one liability for a single property. Theproposed uniform law was, however, not widely adopted.

3. 1966 Act: The 1966 Act was drafted primarily to deal with specific problemsarising from money orders and traveler’s checks under the 1954 Act. The 1966 Act alsoeliminated the holder’s requirement of reporting the name and address of owners oftraveler’s checks and money orders and the state’s requirement of publication on a list.These changes were necessary due to the inability of an issuer to know who theultimate holder of the instrument was.

4. 1981 Act: The 1981 Act was a complete revision of the 1954 and 1966 Acts inresponse to priority issues that remained. The 1981 Act codified the Court’s prioritystandards set out in Texas v. New Jersey, 379 U.S. 674 (1965), which set forth theprimary and secondary priority rules for resolving competing state claims. In addition,the 1981 Act was revised to impose limitations on service charges imposed onabandoned property. The general dormancy period was also shortened.

5. 1995 Act: The 1995 Act clarified the issue of the identity of the debtor whenpayments by intermediaries such as banks, brokers, or depositories serving as therecord owner of securities are at stake. The Act also reaffirmed the priority rules in the1981 Act, making clear that the holder is required to report unclaimed property to thestate that the holder’s records identify as the owner’s last known address, regardless ofwhether the holder is otherwise subject to jurisdiction of that state. The 1995 Acttherefore applies to persons in other states who are holding unclaimed property,eliminating any requirement that those persons engaged in business in the stateclaiming escheat duties.

C. UNIFORM ACTS SERVING AS THE BASIS FOR STATE LAW

1. 1954 Act: California, Connecticut, Georgia, Vermont.

2. 1966 Act: Alabama, District of Columbia, Illinois, Iowa, Maryland, Minnesota,Mississippi, Missouri, Nebraska, Nevada, Oregon, Pennsylvania, Tennessee, Virginia.

3. 1981 Act: Alaska, Colorado, Florida, Hawaii, Idaho, Michigan, New Hampshire,New Jersey, North Dakota, Oklahoma, Rhode Island, South Carolina, South Dakota,Texas, Utah, Virgin Islands, Washington, Wisconsin, Wyoming.3

4. 1995 Act: Alabama, Arizona, Arkansas, Indiana, Kansas, Louisiana, Maine,Montana, New Mexico, North Carolina, West Virginia.

5. No Uniform Act: Delaware, Kentucky, Massachusetts, New York, Ohio.

3 Many states which adopted the earlier versions of the Uniform Acts had also subsequently

amended their statutes with provisions from the 1981 Act.

©Jones Day 2005

6

III. CONCEPTS IN UNCLAIMED PROPERTY LAWS

A. OWNER:

A person who has a legal or equitable interest in the unclaimed property, as defined bythe 1995 Act. The term includes a depositor in the case of a deposit, a beneficiary in thecase of a trust, and a creditor, a claimant, or payee in the case of other property. Theterm “owner” can also be understood as the rightful owner, actual owner, or the creditor.In addition, both the 1981 and 1995 Acts utilize the concept of an “apparent owner.” Thegeneral rule of Texas v. New Jersey is that the state of last known address of the ownermay claim abandoned property and that such claim is accorded priority over allcompeting claims. For ease of administration, a holder may rely on the name of theowner appearing on its records and is not required to ascertain whether, without noticeto the holder, an owner’s interest passed to another. Accordingly, a definition of the term“apparent owner” was added to the Uniform Act. § 1(2) of both 1981 and 1995 Actsdefine “apparent owner” as the person whose name appears on the records of a holderas the person entitled to property held, issued, or owing by the holder. § 25(a)(3) of the1981 Act and § 14(a)(3) of the 1995 Act make provision for the state of the actual ownerto reclaim the property from the state of the apparent owner upon a showing that therecords of the holder were erroneous.

B. HOLDER:

Any entity who is in possession of property belonging to another or is indebted toanother on an obligation. Specifically, the 1981 Act defines a “holder” as a person whois a trustee, has possession of property belonging to another person, or is indebted onan obligation. The 1995 Act, however, focuses upon the person who is “obligated” tohold for, and pay or deliver property to its owner. This definition of holder in the 1995Act reflects the debtor-creditor concept in Delaware v. New York, 507 U.S. 490 (1993),where the Court indicated that for purposes of unclaimed property laws, the relevantholder was the party who was “legally obligated to deliver unclaimed [property] to [its]owner.” “Holder” includes persons and business associations. The definition of“business association” has been expanded to specifically include unincorporatedassociations, limited liability companies, and mutual funds as well as banking andfinancial organizations of all types. All conceivable forms of public and private entitiesare therefore subject to the 1995 Act’s duties to report and deliver unclaimed property tothe state.

C. CUSTODIAN:

An individual or entity that holds property until it is delivered to the rightful owner. Underthe Uniform Acts, the state acts as custodian of the unclaimed property remitted by theholder and holds the property in custody until it is claimed by the owner.

D. UNCLAIMED PROPERTY:

Generally a financial asset for which there has been no owner activity for a specifiedperiod of time (usually 3 or 5 years). Land, including real property interests, and other

©Jones Day 2005

7

tangible personal property generally do not fall within the reach of the unclaimedproperty laws. In general, unclaimed property laws govern only the abandonment ofintangible personal property. Intangible property is most easily understood as a right tohold or receive something of value. That right is often evidenced by a written document.Uncashed checks, unclaimed stock certificate, unredeemed gift certificates, outstandingmoney orders, and uncashed payroll checks are classic examples of unclaimedintangible personal property. The 1995 Act covers all intangible property and one kindof tangible property, that is, tangible property in a safekeeping depository

E. Briefly, the Uniform Act covers all intangible property and safe deposit boxcontents. It requires the holder to look for the owner. The holder is required to reportand remit the property to the states. Once the property is turned over to the states, theholder is relieved of any liability.

IV. FOUR ESSENTIAL ELEMENTS OF UNCLAIMED PROPERTY

A. THE PROPERTY MUST BE INTANGIBLE

1. With the exception of tangible property held in a safe deposit box or othersafekeeping depository, the 1995 Act provides exclusively for the disposition ofunclaimed intangible property. § 1(13) of the 1995 Act provides the following asproperty covered:

2. Money, check, draft, deposit, interest, or dividend;

3. Credit balance, customer’s overpayment, gift certificate, security deposit, refund,credit memorandum, unpaid wages, unused tickets, mineral proceeds, or unidentifiedremittance;

4. Stock or other evidence of ownership of an interest in a business association orfinancial organization;

5. Bond, debenture, note, or other evidence of indebtedness;

6. Money deposited to redeem stock, bonds, coupons, or other securities or tomake distributions;

7. Amount due and payable under the terms of an annuity or insurance policy;

8. Amount distributable from a trust or custodial fund to provide health welfare,pension, vacation, severance, retirement, stock purchase, or other similar benefits.

B. THERE MUST BE A FIXED AND CERTAIN LEGAL OBLIGATION OF THEHOLDER TO THE OWNER

1. The 1995 Act focuses on the concept that the property that is subject to custodialtaking by the state is the underlying obligation owed by the holder to the apparentowner. As a result, a “holder” is simply defined under § 1(6) as the person “obligated.”

©Jones Day 2005

8

Identifying unclaimed property by reference to such underlying obligation hence makesclear that the unclaimed property is not the money or check or instrument by which theobligation is evidenced or discharged but, rather, the right of the apparent owner againstthe holder.

2. Further, the 1995 Act indicated that the property must be a fixed and certaininterest and that it includes any income or increment accrued to the original interest.The obligation of the holder to the owner must be unconditional and for a specificamount. A holder is therefore not subject to unclaimed property laws with respect to adebt that is not clearly owed and fixed in amounts. Accordingly, this requirement wouldexclude sums that are conditional offers of settlement or payment, or where the sumdue has not been established or agreed upon.

C. THE PROPERTY MUST REMAIN UNCLAIMED BY THE OWNER FOR THEDORMANCY PERIOD

1. Under the 1995 Act, property is unclaimed if, for the dormancy period, theapparent owner has not communicated in writing or by other means reflected in acontemporaneous record prepared by or on behalf of the holder, with the holderconcerning the property or the account in which the property is held, and has nototherwise indicated an interest in the property. An owner may demonstrate interest bypresenting a check, making deposits and withdrawals from an account, payingpremium, or negotiating an instrument.

2. The holder’s obligation to report and remit unclaimed property is triggered whenthere has been no activity by the owner for a specified period of time. This period ofinactivity is referred to as a "dormancy period. The dormancy period generally begins atthe time the property first becomes payable or distributable to the owner and typicallycontinues so long as the owner does not otherwise demonstrate any interest in theproperty. Different states vary in their dormancy periods for unclaimed property. Underthe Uniform Acts, the dormancy period for the presumption of abandonment vary by thetypes of property, and generally have been shortened with each of the succeedingUniform Acts. The 1995 Act combines all dormancy periods in § 2. The dormancyperiod for the more common types of unclaimed property is as follows: (1) money orcredits owed to a customer as a result of a retail business transaction - 3 years after theobligation accrued; (2) gift certificate - 3 years after December 31 of the year in whichthe certificate was sold; (3) wages or other compensation for personal services, -1 yearafter the compensation becomes payable. In addition, § 2(15) is the general dormancyperiod for other property not specifically mentioned in the provision, being 5 years afterthe owner’s right to demand the property or after the obligation to pay or distribute theproperty arises, whichever first occurs.

3. Dormancy Period for Equity Securities/Unclaimed Dividends

a. The 1995 Act provides a single five-year dormancy period for both dividends andunderlying shares, whereas the 1981 Act has a five-year dormancy period for dividendspayable on an equity interest and a seven year period for the underlying interest. Using

©Jones Day 2005

9

the same dormancy period reduces the holder’s burden of continuing to issue and trackunpaid dividends for the 2 additional years until the underlying shares are presumedabandoned.

b. § 2(b) of the 1995 Act presumes the abandonment of all outstanding dividendsand other accretions on the underlying equity interest when the underlying interest itselfis presumed abandoned under § 2(a)(3). The five year dormancy period for equitysecurities begins to run from the time of any one of these factual occurrences: (1) themost recent dividend stock split, or other distribution that is unclaimed; (2) the secondmailing of a statement or communication that is returned as undeliverable; or (3) whenthe holder discontinues mailings to the apparent owner.

4. Dormancy Period for Gift Certificates and Customer Credit Balances

a. While § 14 of the 1981 Act provides a single five year dormancy period forobligations arising from gift certificates and credit memos, the 1995 Act treats themseparately.

§ 2(a)(6) of the 1995 Act provides that money or credits owed to a customer in a retailtransaction have a three-year dormancy that commences from the time that the moneywas payable or the credit issued. § 2(a)(7) of the 1995 Act provides that gift certificatesare deemed abandoned three years after December 31 of the year in which they wereissued. Where the credit or certificate is payable in money, the amount abandoned isthat sum. However, if the contract underlying the gift certificate transaction limitsredemption to merchandise only, the 1995 Act creates a presumption that the amountabandoned is a stated percentage of the face amount of the certificate; sixty percent isthe suggested percentage.

D. THE APPARENT OWNER OF THE PROPERTY CANNOT BE LOCATED

The Uniform Act requires the holder to attempt to locate the owner before reporting andremitting the property to the state. This process is frequently referred to as “duediligence.”

V. COMPLIANCE ISSUES

A. REPORT OF UNCLAIMED PROPERTY

1. Under the Uniform Act, the holder is required to report and remit the property tothe states when the property remains unclaimed after the expiration of the dormancyperiod. The reporting and notice requirements of § 7 of the 1995 Act are substantiallysimilar to those of § 17 of the 1981 Act. Under § 7 of the 1995 Act, the holder has twodistinct duties: (1) the duty to compile a report; and (2) the duty to serve a notice uponthe apparent owner. A holder who fails to perform these duties would be subject to thepenalties under § 24 of the 1995 Act.

2. Report By Holder: Under § 7(b), the report must be verified and must contain thefollowing, generally as: (1) a description of the property; (2) name (if known), last known

©Jones Day 2005

10

address (if any), social security number of the apparent owner of property of the valueof $50 or more; (3) an aggregated amount of items valued under $50 each.

3. Notice Served By Holder: While § 17(e) and 18(d) of the 1981 Act provide for theservice of two notices upon the record owner, one by the holder before delivery to thestate and the other by the state after the delivery, the 1995 Act eliminates the secondnotice by the state. The state’s primary means of contacting the owner is thepublication it makes after receipt of the report and its proceeds.

B. PAYMENT OR DELIVERY OF UNCLAIMED PROPERTY

The 1995 Act provides for simultaneous reporting and remitting of unclaimed property.The holder has a duty under § 8(a) to remit or deliver the unclaimed property along withthe report. There is no longer an interval between the filing of the report and thepayment or delivery of the reported property, as was the case under § 19(a) of the 1981Act.

VI. PRIORITY RULES ON ESCHEAT OF INTANGIBLE PROPERTY

A. BACKGROUND

Prior to the series of Supreme Court cases on the priority rules, many states hadpremised their claims to abandoned property on different jurisdictional standards. As aresult, conflicting claims to property arose. The 1954 and 1966 Uniform Acts attemptedto improve the situation by establishing a uniform priority rule for state claims under § 10(Reciprocity for Property Presumed Abandoned or Escheated under the Laws ofanother State). However, the incidence of conflicting state claims to abandonedproperty did not lessen because (1) few states had adopted either the 1954 or 1966 Act,and effectiveness of § 10’s reciprocity provision depended upon its adoption by allstates laying claim to property; and (2) the section did not define the core concept ofwhat establishes jurisdiction over the holder by a state. Although the due processpersonal jurisdiction standard would permit multiple states to assert claims toabandoned property in a typical transaction, the Supreme Court in 1961 held that DueProcess prevented more than one state from actually escheating a given item ofproperty. Western Union Tel. Co. v. Pennsylvania, 368 U.S. 71 (1961). It was not untilthe U.S. Supreme Court decided Texas v. New Jersey in 1965 that a binding,nationwide priority scheme was created for claims based on state unclaimed propertylaws.

B. TEXAS V. NEW JERSEY, 379 U.S. 674 (1965).

1. Facts: Sun Oil Company (“Sun”), a New Jersey corporation, owned debts thatresulted from the failure of identified creditors to claim payments from Sun. Most of thefunds were physically located in Pennsylvania. Some of these unclaimed debts werecash dividends on Sun’s common stock, which had been deposited in a dividendaccount in a Philadelphia bank. After two years, the funds to pay the unclaimeddividends were transferred to the general bank account of the company in Philadelphia.There were also unclaimed fractional shares of stock issued by the transfer agent of

©Jones Day 2005

11

Sun, Chase Manhattan Bank of New York, which had resulted from stock dividends.These certificates were held in Philadelphia. Two Texas offices had records of the lastknown addresses for most of the creditors. A few of the creditors had no knownaddress. The creditors of funds who were located in various states had not acted.Several states (Texas, New Jersey, Pennsylvania and Florida) presented their claimsunder their respective state unclaimed property laws to the holder, Sun. During thecourse of litigation, four different priority rules were suggested: (1) Texas - contactstest; (2) New Jersey – debtor’s incorporation; (3) Pennsylvania – holder’s principal placeof business; and (4) Florida – creditor’s last known address on debtor’s records

2. Issue: How should the various states’ competing claims to the abandonedintangible property in Sun’s possession be resolved?

3. Holding: The Court chose as a primary priority rule, that unclaimed property go to“the State of the last known address of the creditor, as shown by the debtor’s books andrecords.” The Court prioritized this claim because such rule would “distribute escheatsamong the states in proportion to the commercial activities of their residents.” Sincedebtors frequently will not have records to show last known addresses, or the recordsdo not contain this information, the Court established a secondary priority rule that if thelast known address cannot be determined by the debtor’s books and records, theproperty is subject to escheat by the state of the debtor’s corporate domicile (i.e.,incorporation).

4. Application: The priority rules established in Texas v. New Jersey wereincorporated into the 1981 Act (§ 3) and carried through to the 1995 Act (§ 4). Inaddition, both Uniform Acts included a transaction-based “throwback” provision that wasnot adopted by the Supreme Court in Texas v. New Jersey but which the NCCUSLdrafters deemed a “rational extension of that ruling.” § 3(6) of the 1981 Act and § 4(6) ofthe 1995 Act provide that if both the state of owner’s last known address and the stateof holder’s incorporation decline or fail to exercise jurisdiction over the unclaimedproperty, then the state where the transactions giving rise to such property occurred hasthe right to claim property.

As a result of Texas v. New Jersey, the presence or absence of a “last known address”of the apparent owner is important. Although the 1981 Act defines “last known address”as a description of the location of the apparent owner sufficient for the purposes of thedelivery of mail, the 1995 Act provides no guidance on this. The Supreme Court has yetto elaborate on the concept of “address,” for example, whether a street and locale areneeded, or whether a municipality or state would suffice.

C. PENNSYLVANIA V. NEW YORK, 407 U.S. 206 (1972).

1. Facts: Western Union Company (“Western”), incorporated in New York, heldunclaimed proceeds of money orders purchased from Western’s offices inPennsylvania. Western’s primary records did not reflect either senders or payees. InPennsylvania’s claim to the right to escheat the unclaimed proceeds, Pennsylvaniaurged the Court to amend its secondary priority rule in Texas v. New Jersey to provide

©Jones Day 2005

12

for a transactionally based priority rule in the event where the holder does not makeentries on its books and records indicating the address of the owner. Pennsylvaniarecommended that where the creditor’s address in unknown, the unclaimed proceedsshould escheat to the state where the money orders are purchased, rather than to thestate of incorporation of the debtor.

2. Issue: Whether the unclaimed property should be escheated to Pennsylvania, thestate in which the money order was purchased, or to New York, the state of the debtor’sincorporation.

3. Holding: The Court reaffirmed the secondary priority rule of Texas v. Jersey,which resulted in almost all funds escheating to New York, the state of Western’sincorporation. Even though the case involved a higher percentage of unknownaddresses, the Court held that this fact did not warrant a variation from the rulesarticulated in Texas v. New Jersey.

4. Subsequent History: Shortly after the Court’s decision in Pennsylvania v. NewYork, Congress codified rules pertaining to the escheat of money orders,4 effectivelyadopting Pennsylvania’s recommendation on the transactionally-based priority rule.Under the rules, where no last known address of a purchaser is known, the statuteprovides that the state of the originator of the funds (i.e., state of purchase), not thestate of incorporation of the entity issuing a money order, is entitled to escheat. Wheresuch the state of purchase is unknown, the unclaimed money orders escheat to theentity’s principal place of business rather than state of incorporation.

D. DELAWARE V. NEW YORK, 507 U.S. 490 (1993).

1. Facts: Most of the funds at issue are unclaimed dividends, interest and othersecurities distributions held by intermediary banks, brokers, and depositories in theirown names for beneficial owners whose identity and location were unknown. New Yorkescheated $360 million in such funds. New York’s argument was that the state of thelast known address of the brokerage firms that are unpaid, which it characterized as thecreditor, was entitled to the undistributed amounts under the primary rule of Texas v.New Jersey. New York maintained that retrieving the addresses of the creditor-brokerswas not cost effective, and since most brokerage firms have New York tradingaddresses, New York argued that it was entitled to claim the receipts. Invoking theoriginal jurisdiction of the United States Supreme Court, Delaware filed suit against NewYork, asserting claim to certain unclaimed securities distributions as the state ofincorporation of the debtor under the secondary rule articulated in Texas v. New Jersey.Delaware argued that the distribution was a debt in the hands of its holder, whichDelaware identified as the broker intermediary (i.e., debtor), not as the issuer.Delaware argued that the primary rule of Texas v. Jersey did not apply and that since it

4 Disposition of Abandoned Money Orders and Traveler’s Checks Act, Pub. L. No. 93-495, tit. VI

§ 601, 88 Stat. 1500, 1525 (1974) (codified at 12 U.S.C. § 2501-2053 (1988)). The legislation is strictlyconfined to escheat of money and travelers checks. Congress expressly excluded third party bank checksand all other intangibles.

©Jones Day 2005

13

is the state of incorporation of the broker intermediary, it was entitled to escheat theundistributed funds under the secondary rule.

2. Issue: Whether the unclaimed securities distributions should escheat to NewYork or Delaware.

3. Holding: The Court held that the State in which the intermediary is incorporated(i.e., Delaware) has the right to escheat funds belonging to beneficial owners whocannot be identified or located.

4. Analysis: There are 3 steps in resolving disputes among the States over the rightto escheat intangible personal property. First, the Court must determine the precisedebtor-creditor relationship as defined by the law that creates the property at issue.Second, because the property interest in any debt belongs to the creditor rather thanthe debtor, the primary rule gives the first opportunity to escheat to the State of “thecreditor’s last known address as shown by the debtor’s books and records.” Third, if theprimary rule fails because the debtor’s records disclose no address for a creditor orbecause the creditor’s last known address is in a State whose laws do not provide forescheat, the secondary rule awards the right to escheat to the State in which the debtoris incorporated.

The Court first stated that because the bulk of the abandoned distribution atissue could not be traced to any identifiable beneficial owner, the funds fell out of theprimary rule and into the secondary rule. Importantly, the Court found that theintermediaries who held unclaimed securities distributions in their own names were therelevant “debtors.” The issuers could not be considered debtors once they madedistributions to intermediaries that were record owners, since payment to a recordowner discharged all of an issuer’s obligations to the beneficial owner. An intermediaryserving as the record owner thus was the “debtor” insofar as it had a contractual duty totransmit distributions due under such a contract. Accordingly, Delaware had the right toescheat the unclaimed securities distributions since it was the state of incorporation ofthe debtor.

In addition, the Court pointed out that its priority rules preempt State law and heldthat “no state may supersede them by purporting to prescribe a different priority underState law.” According to the Court, the right of the state of incorporation of theintermediary can only be superseded by a claiming state that is able to prove that thetransaction or other records of the intermediary do show the last known address of theparty entitled to the distribution is in the claiming state.

5. Subsequent History: The ruling in Delaware v. New York rendered inferior theclaims of states in which a holder conducted business, but was incorporated elsewhere.Many states sought to change the priority rules in Congress. In 1993, H.R. 2443 and S.1715 were introduced to amend the right to escheat under the secondary rule to theholder’s “principal executive office,” but the bills were never enacted.

©Jones Day 2005

14

VII. RECENT TRENDS IN STATE UNCLAIMED PROPERTY LAW

Over the past several years, an increasing number of states have exempted giftcertificates and gift cards from their escheat laws. In addition, a number of states havealso adopted a business-to-business exemption.

A. GIFT CERTIFICATES AND GIFT CARDS

1. Gift certificates and gift cards, which are generally includible as unclaimedproperty if abandoned for the dormancy period, have been expressly exempted fromunclaimed property statutes in certain states. As of July 6, 2004, 23 states have giftcertificate or gift-card exemptions. See Chart A for a summary of these states with suchexemptions.

2. The availability of these exemptions generally depends on whether the issuingstores maintain name and address records for purchasers, or issue the gift certificatesor gift cards on an anonymous basis. If such records are maintained, the state of thepurchaser’s last known address has the first priority right to escheat the unusedbalance. If either (a) the purchaser’s last known address is in a state that exempts giftcertificates or gift cards, or (b) the gift certificates or gift cards are issued anonymously,the second priority rule applies, and the holder may be liable to report and pay theunused balances to the holder’s state of incorporation after the relevant dormancyperiod. However, if the holder’s state of incorporation also exempts gift certificates orgift cards, the holder may decide not to report and pay the unused balance to any state.However, even if the first and second rules do not apply, some states may use thetransactional-based priority rule to assert the right to escheat unused balances of giftcertificates or gift cards that are purchased in that state. Although this third priority ruleis of questionable constitutional validity, it has been successfully applied in severallower state court cases.5

3. When an exemption is not available, some retail issuers have attempted toimpose service charges on unused gift certificate and gift-card balances after a certainperiod of nonuse of the product. Whether an issuer can impose such charges dependson the law of the state that would otherwise be entitled to claim the unused balances.Although state law on the service charge issue varies widely, many states do permitsuch charges if they are imposed under a valid contract, are uniformly enforced, and arenot “unconscionable” in amount (for states that adopted the 1995 Act).

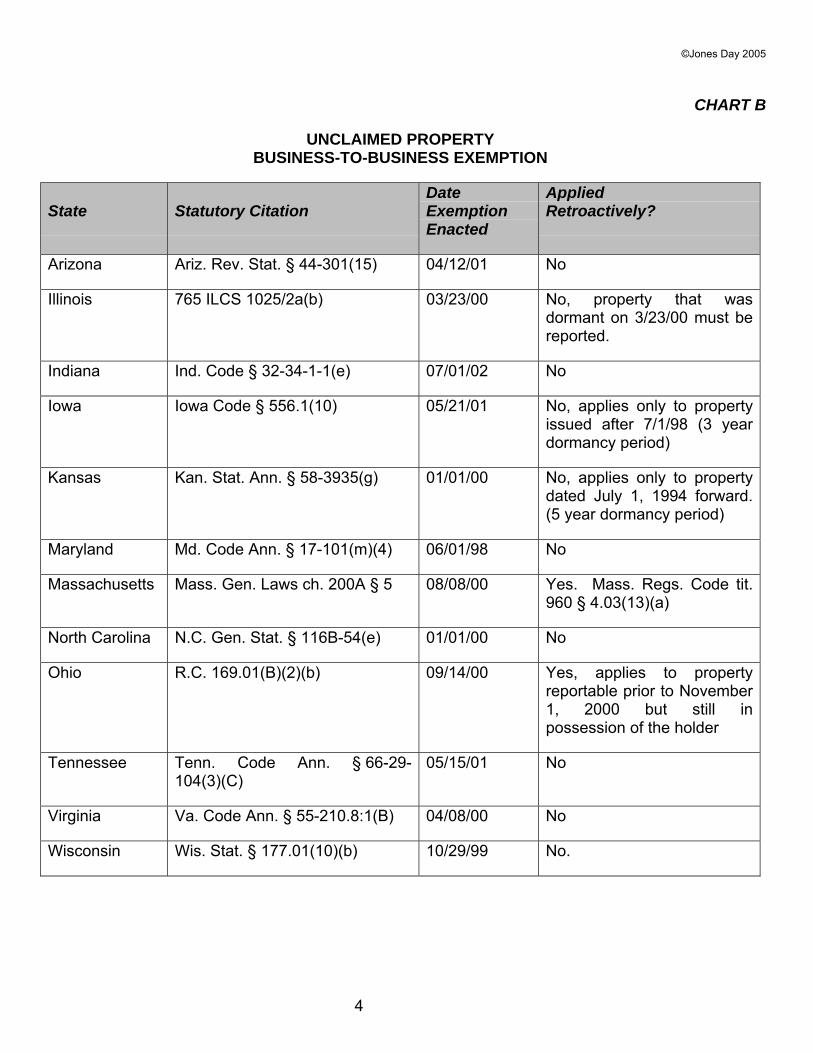

B. BUSINESS-TO-BUSINESS (“B2B”) EXEMPTION

Generally, credit balance issued in the ordinary course of the issuer’s business that hasremained unclaimed by the owner for more than the dormancy period is presumedabandoned. Increasingly however, states have enacted a B2B exemption so as toexempt such credit balances from the unclaimed property laws. As a result, such credit

5 Stephanie Cutler et al., What Corporate America Needs to Know About Unclaimed Property: A

Primer for the Business Holder, 54 THE TAX EXECUTIVE 4, 335 (2002).

©Jones Day 2005

15

balances are not subject to escheat. The B2B exemption is premised on the idea thatthe unclaimed property laws are designed to protect consumers and were neverintended to permit a state to demand payment of amounts appearing on the books ofone business as a credit balance owed to another business. In addition, businesses donot generally neglect to claim funds truly owed to them by another business, and mostsuch credit balances actually represent flawed bookkeeping.6 Presently, 12 states haveenacted a B2B exemption. See Chart B for a summary of the states with such B2Bexemption.

VIII. POTENTIAL AUDITOR’S LIABILITY ON FAILURE TO DISCLOSE ESCHEATVIOLATIONS

A. CALIFORNIA EX REL. HARRIS V. PRICEWATERHOUSECOOPERS LLP,Nos. A095918, 2005 WL 119893 (Cal. App. 1 Dist. Jan. 20, 2005).

1. Facts: Old Republic Title Company (“ORTC”) was an underwritten title companylicensed by the California Department of Insurance (“DOI”) to conduct business as a titleand escrow agent in California. It provided title and escrow services for real estatetransactions in California. As escrow agent, ORTC received funds from purchasers,sellers, borrowers and lenders, prepared documents and closing account statements,as well as disbursed escrow funds at the close of escrow. ORTC aggregated itscustomers’ escrow funds in demand deposit accounts with various banks throughoutCalifornia. The dormant funds then accumulated when customers fail to instruct ORTCto disburse all the funds on deposit, or a party to whom ORTC disbursed funds from theescrow account at the close of escrow would fail to cash the check. By the late 1980s,ORTC began sweeping some of the dormant funds from escrow accounts into itsgeneral fund and recognizing these funds as income. ORTC failed to comply with theunclaimed property law (“UPL”) which required ORTC to submit holder reports to theState Controller (“Controller”) annually and to deliver all escheated property identified inthe reports to the Controller.

2. In 1990, PricewaterhouseCoopers (“PwC”), the independent public accountantfor ORTC, had recommended that ORTC evaluate the dormant escrow amounts whichremained unclaimed and review the policies to ensure compliance with UPL. The PwCauditors were aware of the company’s dormant funds practice, but nonetheless, issuedan unqualified “clean” audit opinion letter, which ORTC submitted to the DOI along withits financial statements. ORTC filed its first holder report in the early 1990s, but it didnot escheat any unclaimed escrow funds to the state until 1992. The government andthe People subsequently sued PwC under the California False Claims Act (“FCA”) andunfair competition law (“UCL”) for allegedly submitting false audit reports that maskedORTC’s liability under the UPL. By the time the government served ORTC with thecomplaint in the lawsuit, ORTC had escheated $9,551,527.89 in unclaimed funds and$7,710,118.19 in statutory interest on those funds to the Controller.

6 Id. at 339.

©Jones Day 2005

16

3. Procedural History: The trial court granted PwC’s motion for summary judgmenton the FCA cause of action and sustained its demurrer on the UCL claim. For a falseclaim to qualify for the FCA, it must material. Materiality depends on “whether the falsestatement has a natural tendency to influence agency action or is capable of influencingagency action.” The trial court held that under the FCA, the government could notrecover from PwC because any omissions from the auditor reports were not material tothe failure of the Controller to collect the unclaimed funds. Although the auditor reportswent to the DOI, the government failed to establish that the DOI would have alerted theController to the improprieties. Thus, full disclosure of ORTC’s escheat violations to theDOI would not have had a tendency to influence the Controller.

The trial court sustained PwC’s demurrer and held that the alleged failure to comply withgenerally accepted auditing standards (“GAAS”) in preparing for the audit reports werenot actionable under the UCL. The UCL in essence prohibits any unlawful business actor practice, and transforms violations of other laws into independently actionableunlawful practices under its statutory umbrella. The trial court also ruled that the Peoplelacked a remedy because ORTC had already escheated the unclaimed funds to theController.

On appeals, the Court of Appeals reversed on both claims. For purposes of the appeal,the Court assumed that PwC submitted false reports to the government when it issuedunqualified audit reports on ORTC’s financial statements for annual submission to theDOI.

4. Issue: Whether the trial court improvidently granted summary judgment in PwC’sfavor on the FCA cause of action. (2) Whether the alleged violations of auditingstandards were actionable under the UCL.

5. Holding: The Court of Appeals held that PwC did not overcome the materialityelement of the FCA cause of action and therefore was not entitled to summary judgmentas a matter of law. The Court first acknowledged that the Controller’s office is theprimary enforcer of the escheat laws, and that such disclosures in the auditorstatements would not, in the natural course of DOI business, be relayed to that office.The Court, however, stated that “although DOI is not the primary UPL enforcer, it doeshave statutory authority and practices and procedures for enforcing laws, including theescheat laws that impact insurance companies.” Furthermore, the Court stated “with thewheels of its internal procedures and practices humming properly, disclosure of ORTC’sescheat violations would have a natural tendency to influence DOI action.” Accordingly,since PwC had not overcome the materiality element of the FCA claim, the Courtconcluded that the trial court had improvidently granted summary judgment in PwC’sfavor.

The Court held that the trial court’s ruling on the UCL claim was erroneous, reasoningthat the allegations of GAAS violations as set forth in the People’s complaint weresufficient to state a cause of action under the UCL. The allegations were directed at thePwC’s numerous GAAS violations in preparing and submitting unqualified audit reportsfor ORTC, based on PwC’s alleged knowledge that (i) the company’s inflated earnings

©Jones Day 2005

17

from unescheated funds was material under GAAS; (ii) the company’s escheat practiceswere possible illegal acts by the client as defined by GAAS; (iii) the company had neverescheated money to the state as it was required to do; (iv) throughout the course of theengagement, the company’s total escheat obligation including penalties was growing;and (v) the violations permeated the engagement in that year after year PwC issuedunqualified opinion letter for ORTC. According to the Court, these allegations weresufficient to state a cause under the UCL.

The Court also rejected PwC’s contention that the UCL action was barred by Bily v.Arthur Young & Co., 834 P.2d 745 (Cal. 1992), where it was held that “an auditor’sliability for general negligence in the conduct of an audit of its client financial statementsis confined to the client” but persons who are “specifically intended beneficiaries of theaudit report who are known to the auditor and for whose benefit it renders the auditreport” could recover on a theory of negligent misrepresentation. The Court first statedthat the UCL action was not a professional negligence claim. Even if Bily applied, theDOI was the “within the universe of potential plaintiffs defined by Bily,” since the auditwas performed to satisfy regulatory requirements. Since DOI received its audit reportsfrom ORTC in the course of its enforcement and regulatory duties performed for thebenefit of the public, the People’s suit is therefore “for practical purposes…indistinguishable from a suit by the [DOI].”

IX. FEDERAL COURT SUSTAINS CAUSE OF ACTION AGAINST CALIFORNIACONTROLLER FOR FAILURE TO PROPERLY NOTICE TRUE OWNERS

A. TAYLOR V. WESTLEY, 402 F.3d 924, 2005 U.S. App. LEXIS 4953, (9th Cir.2005).

1. Facts: Chris Taylor, a former Intel employee, lives in England and owns 52,224shares of Intel stock. Nancy Pepple-Gonsalves, a former TWA flight attendant, lives inRiverside County, California, and owns 7,000 shares of TWA stock. Mr. Taylor and Ms.Pepple-Gonsalves became plaintiffs in a federal lawsuit against the CaliforniaController, the state official responsible for unclaimed property, concerning the allegedunauthorized escheat of their stock as "unclaimed property." The property was treatedas unclaimed because, for three years, the stockholders did not cash dividend checks,respond to proxy notices, or otherwise communicated with Intel and TWA. As a result,Intel and TWA provided the California Controller with lists of shareholders who were"lost" or "unknown" by these three criteria. Intel and TWA then issued "duplicateshareholder certificates" to the California Controller who sold the stock and depositedthe money received in exchange into California's general fund. When Mr. Taylor andMs. Pepple-Gonsalves tried to use their stock, they discovered they were no longershareholders.

2. The issue arose from what the Court of Appeals for the 9th Circuit characterizedas ". . . a new approach used by some state governments, greatly shortening the timebefore which untouched property is treated as though it had been abandoned, greatlyreducing or eliminating notice to the true owner, and ignoring the true owner's pleas."(402 F.3d 926). Specifically in California, the abandonment period for unclaimed

©Jones Day 2005

18

property used to be 16 years. At the time relevant to this litigation, it had beenshortened to 3 years.

3. Moreover, the law dealing with notice to the shareholders, known as "owners"under California's Unclaimed Property Law ("UPL"), required specific notice to the lastaddress of the shareholders. According to the Court of Appeals, ". . . the Controllerdecided that the forms of notice provided for by statute were impractical and unfunded.She decided not to mail notices to shareholders' last known addresses, and not topublish, in newspaper ads, the individual names and property deemed taken asunclaimed." (Id. at 927). As a result, there was no public or official announcement tothe shareholders that they had a problem with their stock.

4. The federal law suit. The Intel shareholder and the TWA shareholder, as classaction representatives, sued the California Controller in the United States District Courtfor the Eastern District of California. The Controller defended on the basis of theEleventh Amendment to the United States Constitution. The Controller's basicargument was that under the Eleventh Amendment, the District Court had no jurisdictionto entertain this action as it sought money damages from the State Controller.Generally, these kinds of actions are barred by the Eleventh Amendment. The Court ofAppeals reversed the District Court, finding that the Eleventh Amendment did not barthe state law claims of the shareholders nor did it bar the creative relief sought by theshareholders.

5. Holding: The Court of Appeals based its determination on the finding that theEleventh Amendment bar to lawsuits for money damages against state government"applies to the state's money." (Id. at 932). Here, it was not the "state's money" thatwas in issue. It was money that the state obtained from the alleged improper escheat ofcommon stock, which was sold and the proceeds thereof deposited in the state'sgeneral revenue fund. According the Court, this was "not the state's money . . . ."Analogizing its holding to the situation when an improperly parked car is towed by thepolice to an impound lot, "[m]oney that the state holds in custody for the benefit ofprivate individuals is not the state's money, anymore than towed cars are the state'scars. Thus, where a permanent escheat determination has not yet been made, thestate's Eleventh Amendment immunity from suit against it for damages payable from itstreasury has not application to escheated property . . . ." (Id. at 932).

In reversing the District Court determination, the Court of Appeals remanded the caseback to the District Court for prospective relief. This included an accounting of thedisposition of the shareholders' shares, whether the Controller had sold them or not,and the net proceeds from the sale of stock. Because there would be insufficient fundsin the Controller's escheat fund, the Court of Appeals indicated that the CaliforniaTreasurer might be ordered to provide the Controller with sufficient money to pay theclaims of the two plaintiffs in this case and, if the case is certified as a class action, anyother potential class action plaintiffs.

The Appellate Court also suggested that an order be issued that the Controller's failureto send statutory notices to the shareholders who were "lost" were likely

©Jones Day 2005

19

unconstitutional. The District Court was asked to review the UPL's notice proceduresand determine which ones should have been used during the period in question. ■

Main Research References:

• Unclaimed Property, Tax Management Multistate Portfolio Series, BNA (2004).

• David J. Epstein, Unclaimed Property Law and Reporting Forms, Matthew Bender &Company (2005).

1

CHART A

UNCLAIMED PROPERTY GIFT CARD EXEMPTIONS

Tab State Statutory Citation Exemption

1. Alabama Ala. Code. § 35-12-7-3 Exempts gift certificates or gift cardsissued or maintained by any personengaged primarily in the business ofselling tangible personal property atretail.

2. Arizona Ariz. Rev. Stat. Ann. § 44-301(15) Exempts gift certificates and giftcards.

3. Arkansas Ark. Code Ann. § 18-28-201(13)(B)

Exempts gift certificates, gift cards,and in-store merchandise creditsissued or maintained by a retailer.

4. California Cal. Civ. Proc. Code § 1520.5 Exempts gift certificates without anexpiration date that are not given inexchange for money or goods.

5. Colorado Co. St. Ann. § 38-13-108.4 Exempts gift certificates if notredeemable for cash.

6. Florida Fla. Stat. Ann. § 717.29renumbered § 717.114 andrepealed 1996.

Provision requiring holders to reportand remit gift certificates was repealedin 1996. This is a "silent" exemption.

7. Illinois 765 ILCS 1025/10.6(b) Exempt unless gift certificate has anexpiration date and issuer has nopolicy to honor expired gift certificates.

8. Indiana Ind. Code Ann. § 32-34-1-1(f) Effective 7/1/03 gift certificates notsubject to Indiana unclaimed propertylaw.

9. Maryland Md. Rev. Stat. § 17-101(m) Exempts gift certificates.

10. Massachusetts

Mass. G.L.c. 200 A § 5D Exempts gift certificates and requiresthat gift certificates be valid for at least7 years.

©Jones Day 2005

2

UNCLAIMED PROPERTY GIFT CARD EXEMPTIONS

Tab State Statutory Citation Exemption

11. Minnesota Mn. St. Ann. § 345.39, Subd. 1 Exempts gift certificates issued by aretailer.

12. NewHampshire

N.H. Rev. Stat. Ann. § 471-C:16 Exempts gift certificates and storecredits of $100 or less.

13. New Jersey In re November 8, 1996Determination of State Dept. ofTreasury, Unclaimed Property,706 A.2d. 1177 (N.J. Super. Ct.App. Div. 1998)

Exempts gift certificates notredeemable for cash.

14. NorthCarolina

N.C. Gen. Stat. § 116B-54(b) Exempts gift certificates and gift cardswhich state do not expire, bear noexpiration date, or that expiration dateis invalid in North Carolina.

15. North Dakota S.B. 2327 (1997) S.B. 2327 deleted gift certificates fromthe definition of intangible property.Gift certificates issued after 3/26/97are not subject to North Dakota'sunclaimed property law.

16. Ohio R.C. 169.01(B)(2)(d) Exempts gift certificates and gift cardsredeemable exclusively formerchandise.

17. Oregon H.B. 2591 (1997) H.B. 2591 deleted gift certificates fromthe definition of intangible property.Gift certificates issued after 6/25/97are not subject to Oregon's unclaimedproperty law.

18. SouthCarolina

H.B. 3657 (2001) H.B. 3657 deleted gift certificates fromthe definition of intangible property.Gift certificates issued after 6/3/96 arenot subject to South Carolina’sunclaimed property law.

©Jones Day 2005

3

UNCLAIMED PROPERTY GIFT CARD EXEMPTIONS

Tab State Statutory Citation Exemption

19. Tennessee Tenn. Code. Ann. § 66-29-135(c) Exempts gift certificates issued after12/31/98 which state do not expire,bear no expiration date, or thatexpiration date is not applicable inTennessee.

20. Utah Utah Code Ann. 67-4a-211 Exempts gift certificates under $25.

21. Virginia Va. Code Ann. § 55-210.8:1 Exempts gift certificates notredeemable for cash

22. Wisconsin Wisc. Act 109; S.S. A.B. 1 (2002) Wisc. Act 109 deleted gift certificatesfrom the definition of intangibleproperty. Gift certificates issued after1997 are not subject to Wisconsinunclaimed property law. This is a"silent" exemption.

23. Wyoming Wy. Stat. Ann. § 34-24-114(a) Gift certificates under $100 areexempt.

©Jones Day 2005

4

CHART B

UNCLAIMED PROPERTYBUSINESS-TO-BUSINESS EXEMPTION

State Statutory CitationDateExemptionEnacted

AppliedRetroactively?

Arizona Ariz. Rev. Stat. § 44-301(15) 04/12/01 No

Illinois 765 ILCS 1025/2a(b) 03/23/00 No, property that wasdormant on 3/23/00 must bereported.

Indiana Ind. Code § 32-34-1-1(e) 07/01/02 No

Iowa Iowa Code § 556.1(10) 05/21/01 No, applies only to propertyissued after 7/1/98 (3 yeardormancy period)

Kansas Kan. Stat. Ann. § 58-3935(g) 01/01/00 No, applies only to propertydated July 1, 1994 forward.(5 year dormancy period)

Maryland Md. Code Ann. § 17-101(m)(4) 06/01/98 No

Massachusetts Mass. Gen. Laws ch. 200A § 5 08/08/00 Yes. Mass. Regs. Code tit.960 § 4.03(13)(a)

North Carolina N.C. Gen. Stat. § 116B-54(e) 01/01/00 No

Ohio R.C. 169.01(B)(2)(b) 09/14/00 Yes, applies to propertyreportable prior to November1, 2000 but still inpossession of the holder

Tennessee Tenn. Code Ann. § 66-29-104(3)(C)

05/15/01 No

Virginia Va. Code Ann. § 55-210.8:1(B) 04/08/00 No

Wisconsin Wis. Stat. § 177.01(10)(b) 10/29/99 No.

©Jones Day 2005

5

This article is reprinted from the State Tax Return, a Jones Day monthly newsletter reporting on recentdevelopments in state and local tax. Requests for a subscription to the State Tax Return or permissionto reproduce this publication, in whole or in part, or comments and suggestions should be sent toChristine Rhodes (614/281-3911 or [email protected]) in Jones Day’s Columbus Office, P.O.Box 165017, Columbus, Ohio 43216-5017.

©Jones Day 2005. All Rights Reserved. No portion of the article may be reproduced or used withoutexpress permission. Because of its generality, the information contained herein should not beconstrued as legal advice on any specific facts and circumstances. The contents are intended forgeneral information purposes only.