journal of management & development...

TRANSCRIPT

Published by

Mid- Baneshwor, Kathmandu, NepalTel: 977-1-4488312 | 4475254 | Fax: 977-1-4472083

Email: [email protected] | URL: www.globalcollege.edu.np

(Tribhuvan University Affiliate)

Journal of Management & Development EconomicsApril 2015 Vol. 4 Issue No. 1 ISSN 2392-4551

A Peer Reviewed Journal

Chief EditorProf. Radhe S. Pradhan

Managing EditorDr. Khagendra P. Ojha

Executive EditorMr. Dev Raj Paneru

EditorsMr. Achyut GyawaliMr. Damaru PoudelMr. Santosh Poudel

Advisory BoardProf. Dr. Prem Raj PantProf. Dr. Puskar BajracharyaDr. Tilak RawalProf. Dr. Ajaya Bikram SthapitDr. Manish ThapaDr. Nar Bahadur Bista

Peer Reviewed byProf. Dr. Prem. R. PantProf. Dr. Radheshyam PradhanMr. Dev Raj PaneruMr. Santosh Poudel

Publishing TeamMr. Nabraj BhandariMr. Tulashi Ram ShresthaMr. Baburam Subedi

Design & LayoutDev Nandan Chaudhary

Journal of Management & Development EconomicsApril 2015 Vol. 4 Issue No. 1 ISSN 2392-4551

EditorialJournal of management and development economics is purely an official publication of GlobalCollege of Management, Tribhuvan University Affiliate, located at Mid Baenshwor Kathmandu.The journal is published annually as a regular research publication in April or May. It is not-for profit- publication of the college aimed to promote research and learning activities amongthe college faculties, researchers, university professors and graduate and undergraduate studentsand personnel in administrative positions involved jointly or individually in research ventures;academic or professional, though academic researchers are prioritized. As obvious from thetitle of the journal, mainly the research based; primary and secondary data based articles;qualitative or quantitative but exclusively from the field of management and economics areaccepted for publication.

The journal is the institutional property of Global College of Management and hence, publishingof the journal is solely in the responsibility of the research committee working as the steeringcommittee for the College's Quality Assurance and Accreditation (QAA) department formedin response to the college's commitment as an applicant institution to the QAA indictorsassigned by the University Grants Commission Nepal (The college has entered into the formalprocess for QAA from UGC, Nepal starting from 2013).

The articles published in this journal in all its issues are from economics, finance, and generalmanagement areas and some of the articles are secondary data based whereas others primary.The articles were assigned for peer review to the professors and practitioners in their respectivefield, amendments were recommended followed by editing corrections ensured before theywere processed in this journal as far as possible.

However, the editorial team does not bear responsibility for any incongruences in contentsand patterns presented in the articles as they are purely the products of their authors and hence,the authors are subject to ethical interrogations in the circumstances that are marked to violateethical parameters applicable in the field of academics and research. The articles have been arranged in alphabetical order of the authors' name. Concisely thepurpose of each article has been attached briefed here:

The first article by Achyut Gyanwali titled Influence of Corporate Income Tax on Debt-Financing: Evidence from Nepalese Manufacturing Companies aims at assessing the relationshipbetween corporate income tax and debt-equity mix, and estimate the influence of corporateincome tax on debt financing of the manufacturing companies of Nepal. The purpose of thearticle titled An Analysis of Electricity Consumption in Industrial Sector of Nepal by BholaNath Ghimire is to derive and estimate a consumption function for Nepalese indus trialelectricity use, and to investigate changes in consumption pattern over the time period

Journal of Management & Development EconomicsApril 2015 Vol. 4 Issue No. 1 ISSN 2392-4551

1980-1912. Does development of commercial banks spur economic growth? By Dr. DipakBahadur Bhandari and Keshab Acharya examines the degree of relationship and direction ofcausality between the development of commercial banks and economic growth of Nepal.

The article titled Teacher Management and Development in Higher Secondary Education: ACase of Higher Secondary Education Board of Nepal by Dev Raj Paneru qualitatively examineshuman resource management and development practices undertaken to manage and developteachers serving in the schools under HSEB, Nepal. Globalization: A Trozan Horse: Globalizationis a buzzword that has no precise definition by Prof. Dr. Kanhaiya Ram Bhakta Mathemaexamines how Globalization brings in interconnectedness in economic, cultural, and technologicaldomains via expansion in unrestricted trade.

An Analysis of Foreign Employment and Inflow of Remittance in Nepal by Mr. Mani RatnaLamsal examines the migration and inflow of remittance in Nepal. It deals with literaturereview on remittance, the inflow of remittance from various countries, the contribution ofremittance to GDP, consumption and expenditure pattern. Non-financial PerformanceMeasurement Practices in Nepalese Commercial Banks, by Naba Raj Adhikari, examines thenon-financial performance measurement practices in Nepalese commercial banks.

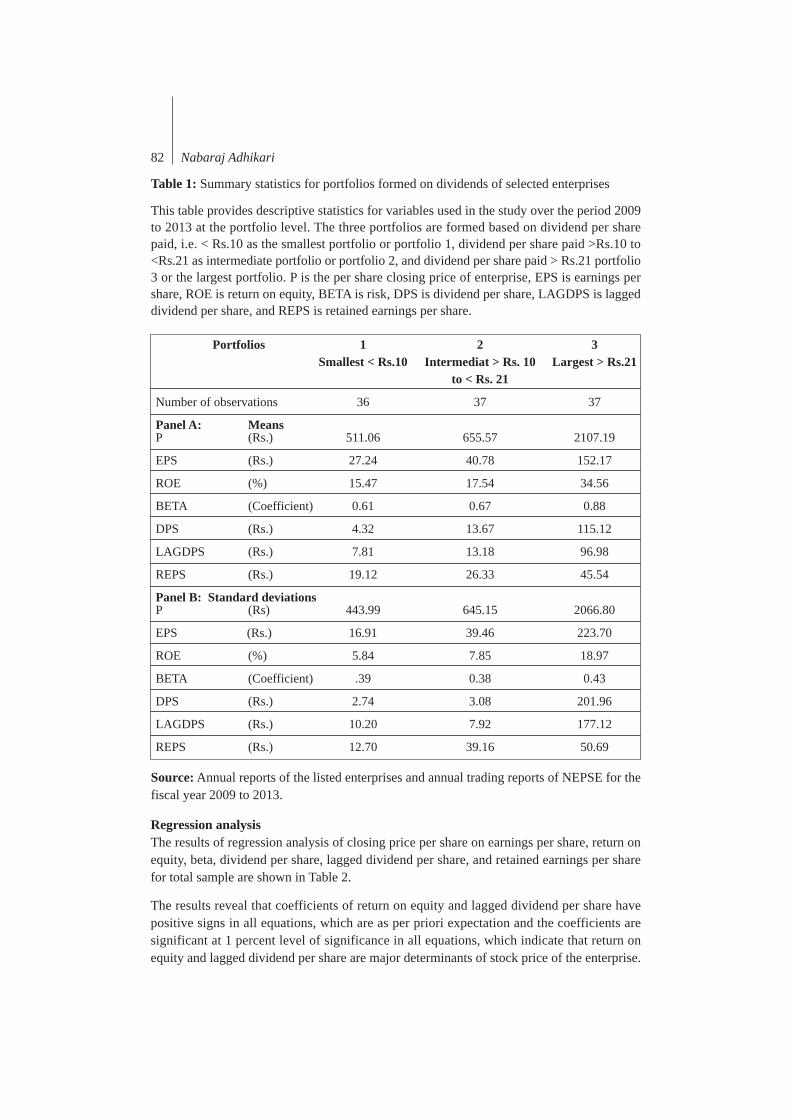

Dividend Policy, Performance, and the Sock Price in Nepal by Dr. Nabaraj Adhikari, aimsat investigating the dividend policy, performance, and the stock price in the pre-emergingcapital market of Nepal employing descriptive cum analytical research. The Cross-Sectionof Expected Stock Returns in Nepal by Prof. Dr. Radhe S. Pradhan aims at examining theability of beta and other company specific factors such as firm size, book to market ratio,sales to price ratio, dividend yield and earning price ratio to explain cross section of stockreturns in Nepal and finally, An Empirical Study on Stock Market, Bank and Economic Growthby Santosh Poudel, examines the relation between economic growth with financial growth.

The editorial team and research committee of the college welcomes all the academic andresearch endeavors to the standard applicable in research and studies in higher education.

Dev Raj PaneruExecutive Editor

Journal of Management and Development EconomicsA peer reviewed journal of Global College of Management

Mid- Baneshwor Kathmandu, Nepal.

Journal of Management & Development EconomicsApril 2015 Vol. 4 Issue No. 1 ISSN 2392-4551

NotesArticles are subject to editorial review by referees from the community of management andeconomics experts. Comments or notes regarding articles are welcome and will be consideredfor publication to the extent possible. The opinions and the interpretations expressed in thearticles are the personal opinions of the authors and reviewers and do not necessarily reflectthe views of the publisher and editors, or of any institution with the information with whichthe author may be associated. The editorial board does not guarantee the accuracy of the dataand the information included in the articles and accepts no responsibility, whatsoever, for anyconsequences of their use.

Subscription informationJournal of Management and Development Economics (JMDE) is a journal published annuallyby Global College of Management. The publication is for the benefit of the managementexperts, economists, planners, professionals as well as those interested in the field of managementand development. Copies of the journal may be subscribed/purchased from Global Collegeof Management. The subscription rates are as follows:

Mailing charge to be paid extraClaims for the missing numbers should be made within the month following the regular monthof publication. The publisher will supply the missing numbers free of cost only when it isconfirmed and when the reserve stock permits.

If you change your address, please notify us immediately, giving both your old and newaddresses. Allow five weeks for the change. Back issues prior to last years' volume, if available,can be obtained from the college. Request for the subscriptions should be addressed to:

Journal of Management and Development EconomicsGlobal College of Management, Mid-BaneshworKathmandu, Nepal014488312, 014472083

Individuals Library and InstitutionPer copy Per Copy

Nepal Rs.500 Rs.900

SAARC Countries US$10.0 US$15.0

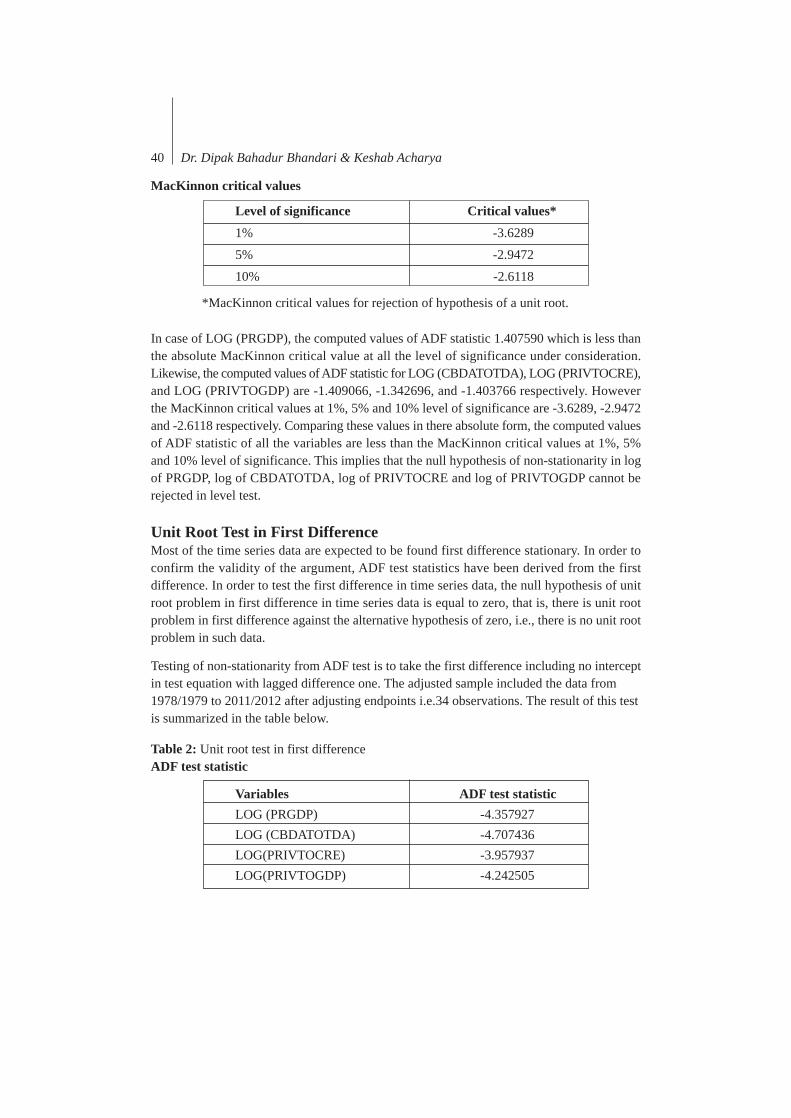

Other Countries US$15.0 US$22.0

Journal of Management & Development EconomicsApril 2015 Vol. 4 Issue No. 1 ISSN 2392-4551

Format for subscription request....................................................................................................................................................................................................................................................................................................I would like to subscribe to Journal of Management and Development Economics an annualpublication of Global College of Management Mid Baneshwor, Kathmandu, Nepal.

Mode of payment: Cash/Cheque/Draft Total amount NRs./US$:..................................................................................................................................................

Name & Designation:....................................................................................................................................................................................................................................................................................................

Institution:....................................................................................................................................................................................................................................................................................................

Mailing Address:....................................................................................................................................................................................................................................................................................................

Telephone: ............................................... E-mail: .................................................................

Fax:....................................................................................................................................................................................................................................................................................................

Please transfer the amount to Global College of Management, Mid- Baneshwor, Kathmandu

- citizens Bank International Ltd., New Road, Kathmandu- Account No: 0070000179 CC, SWIFT: CTZNNPKT- please do not send cash by mail.- only cheques drawable in Kathmandu will be accepted.

For: 1 Year 2 Years …………………..Years.

Subscription type: Personal Institutional Vol. …………… Issue ……

Journal of Management & Development EconomicsApril 2015 Vol. 4 Issue No. 1 ISSN 2392-4551

Contents

AN ANALYSIS OF ELECTRICITY CONSUMPTION IN INDUSTRIALSECTOR OF NEPAL .............................................................................................. 11-18Bhola Nath Ghimire

TEACHER MANAGEMENT AND DEVELOPMENT IN HIGHERSECONDARY EDUCATION .................................................................................. 19-30

Dev Raj Paneru

DOES DEVELOPMENT OF COMMERCIAL BANKS SPUR ECONOMICGROWTH ................................................................................................................. 31-52Dr. Dipak Bahadur Bhandari & Keshab Acharya

GLOBALIZATION: A TROZAN HORSE "GLOBALIZATION IS A BUZZWORDTHAT HAS NO PRECISE DEFINITION." ............................................................. 53-60Dr. Kanhaiya Ram Bhakta Mathema

A Case of Higher Secondary Education Board of Nepal

INFLUENCE OF CORPORATE INCOME TAX ON DEBT FINANCING:EVIDENCE FROM NEPALESE MANUFACTURING COMPANIES ................. 1-10Achyut Gyawali (PhD Scholar)

AN ANALYSIS OF EMPLOYMENT AND INFLOW OF REMITTANCEIN NEPAL ................................................................................................................. 61-70Mani Ratna Lamsal

NON-FINANCIAL PERFORMANCE MEASUREMENT PRACTICESIN NEPALESE COMMERCIAL BANKS ................................................................ 71-76Naba Raj Adhikari, M. Phil

DIVIDEND POLICY PERFORMANCE, AND THE STOCK PRICE IN NEPAL .... 77-90Nabaraj Adhikari, PhD

THE CROSS-SECTION OF EXPECTED STOCK RETURNS IN NEPAL ............. 91-99Prof. Dr. Radhe S. Pradhan

AN EMPIRICAL STUDY ON STOCK MARKET, BANK AND ECONOMICGROWTH ................................................................................................................. 100-112Mr. Santosh Poudel

Journal of Management & Development EconomicsApril 2015 Vol. 4 Issue No. 1 ISSN 2392-4551

of] k]h vfnL /fVg]

Influence of corporate income tax on debt-financing: Evidence from Nepalese manufacturing companies 1

INFLUENCE OF CORPORATE INCOMETAX ON DEBT-FINANCING: EVIDENCEFROM NEPALESE MANUFACTURINGCOMPANIES

Achyut Gyawali (PhD Scholar)...?

AbstractThe main purpose of this paper is to assess the relationship between corporate income taxand debt-equity mix and estimate the influence of corporate income tax on debt financing ofthe manufacturing companies of Nepal. Debt-equity mix has been taken as the dependentvariable to represent the debt financing and effective tax rate has been used as independentvariable to represent the corporate income tax. The secondary data have been utilized toestimate the relationship between the variables and simple regression equation as used inAlessi (1965) study has been employed to infer the relationship. The results of the analysissuggest that debt financing is influenced by corporate income tax positively, but such influenceis not much significant in shaping specific mix of debt and equity capital of the manufacturingcompanies. However, the nature of influence is different across the profitability status of thecompanies.

Keyword: Corporate tax, Manufacturing companies, Debt-equity mix, profitability, Incometax

BackgroundA firm seeking to maximize welfare of its shareholders should take tax factors into elucidationwhile involving in the process of making financing decisions. It is because; the impositionof income tax on corporate business profit reduces the residual amount of income availablefor distribution of returns as dividends to the shareholders (Altman and Subrahmanyam, 1985:181). For corporate income tax purpose, the expenses made on the payment of interest to thebondholders of the company are allowed as a deduction, but the expenses made on disbursementof dividends to the shareholders are not allowed as a deduction. Income tax provision regardingwith eligibility of interest deduction from taxable income is favorable for the firms as it equallyadds benefit to generate valuable tax shield. The debt financing significantly helps increasefirm's cash-flow ancillary in the course of generating operation funds available for returndistribution to the shareholders through its tax shields (Pringle and Harris, 1987: 495). Hence,a resonance proportion of debt in financing mix also increases the market value of themanufacturing firms (Ross, et al., 2013:368). As a result, interest-bearing debts are attractiveto the manufacturing firms for financing their investments (King, 2012: 158). Therefore, the

Mr. Gyawali is the Lecturer of Management at Tribhuvan University. He is the PhD Scholar at T.U.

2 Achyut Gyawali

difference in tax treatment of interest and dividend affect financing choice between debt andequity (Chua, 1995).

Corporate income tax is potentially an important consideration in a firm's financing decision(Fama and French, 1998: 819). It has an effect on the ways of project financing. If it is financedwith the debt capital, tax relief is available on the interest payment (Hutchinson, et al.,1994:296). Therefore, financial managers remain constantly aware of tax consideration intheir day-to-day decisions and spend a considerable part of their managerial effort to reducethe incidence of income tax through an appropriate financing mix. Thus, corporate incometax is an influential factor in the choice of sources to raise required funds.

Funds to finance an investment proposal can be obtained either by borrowing from banks, byselling marketable securities, by selling non-business assets or parts of its business assets, byissuing additional securities or by utilizing the savings generated from business operations.Hence, an investment proposal is either financed by a composite capital mix or by any oneof the sources of funds. Composite capital mix depends on various factors and no uniformstandard can be laid down for all investments of a corporation (Saynyal, 1971: 817). Whenthe corporation uses debt, it must pay interest, on the other hand when it uses equity; it isexpected to distribute dividends to the equity investors. In case the debt is used, the interestexpenses paid by a corporation on it are allowed to deduct from operating income to obtainits taxable income. But the dividends paid to equity holders are not deductible. For this reason,corporate tax system favors debt financing over equity financing. However, it is not alwayspossible to finance an investment exclusively with debt capital, and the risk of doing sosetbacks the benefits of the higher expected income (Brigham, et al., 1999: 56-57). Thus, theproblem of financial manager is to choose proper level of debt to arrive at appropriate financingmix that results into tax benefits.

The major issue in corporate financing is to determine the appropriate mix between debt andequity. Extensive controversial views have come up on this issue. Regardless of the controversialviews, the tax law has given debt financing a definite cost advantage over preferred stock andcommon stock (Martin, et. al. 1991: 48). Taxes tend to place a premium on one form offinancing as compared to the other. For instance, income tax law allows deduction of allinterests paid before arriving at taxable income. This deductible interest makes debt capitalcheaper for corporations to use it for financing the investments (Keown, et. al., and 2001:425). Thus, the financial managers need to know how taxes influence financing decision ofthe firms.

Due to the attractiveness of debt, there would be a tendency for additional investment to bedebt financed (Arditti and Pinkerton, 1978: 65). To the contrary, Fama and Miller (1972),Jensen and Meckling (1976) suggested that debt is not much attractive to maximize thecombined wealth of security holders because it has a tendency to make risky investments.Similarly, Myers (1977) suggested that use of debt in financing mix causes firms to make lessinvestment of funds because the returns are to be shared with debt holders.

In Nepalese corporate income tax system also the interest paid on debt capital is a deductibleexpense whereas dividend paid for equity capital is not deductible for income tax purpose.It means, interest paid on debt reduces the amount of tax to be paid to the government. In

Influence of corporate income tax on debt-financing: Evidence from Nepalese manufacturing companies 3

contrast, the dividend is not the deductible expense and it does not save corporate tax. Thecorporate taxpayers using equity as the source of capital should pay more tax than those usingdebt as the source of capital. Because of this provision, it can be stated that Nepalese corporatetax system provides favoritism to debt capital over the equity capital of the companies, whichis reflected in the process of financing decision. Because of such discrimination between thedebt and equity capitals, there is a scope of favoring the debt financing by the manufacturingcompanies in the context of Nepal (Kandel, 2009:165).

A company may reduce its tax liability substantially if it finances its capital requirementthrough loans due to the deductibility of interest that results into lower tax burden. This isthe reason why debt financing is more attractive than equity financing and Nepalese companiesmay be thinly capitalized in order to reduce income tax liability (Khadka, 2001: 46). In thiscontext, the influence of corporate income tax on debt financing is emerging as an importantaspect to investigate empirically.

In Nepalese context, however, the influence of corporate income taxes on debt financing ofmanufacturing firms is a matter of study. There is absence of adequate studies especially onthe relationship between corporate income taxes and debt financing of Nepalese manufacturingcompanies. Most of the Nepalese studies, in this regard, concentrate macro level analysis, andadministrative aspect of the income taxes. It is therefore difficult to generalize specific Nepalesecase by applying the findings of international studies. In other words, the applicability of thefindings of previous international studies in the area of corporate income taxes and theirinfluence to debt financing of Nepalese companies remains questionable. Thus, this study hasdealt with the following issues:

1. Does corporate income tax influence debt-equity mix of manufacturing listed companies?2. What kind of relationship does exist between corporate income tax and debt-equity

mix of manufacturing companies?3. Is there any difference in the nature of relationship between corporate income tax and

debt-equity mix across profit-making and loss-making companies?

Objectives of the studyThe purpose of this paper is to assess the relationship between corporate income tax and debt-equity mix and estimate the influence of corporate income tax on debt financing of themanufacturing companies of Nepal. It also analyses on relationship does exist betweencorporate income tax and debt-equity mix of manufacturing companies and the nature ofrelationship between corporate income tax and debt-equity mix across profit-making and loss-making companies.

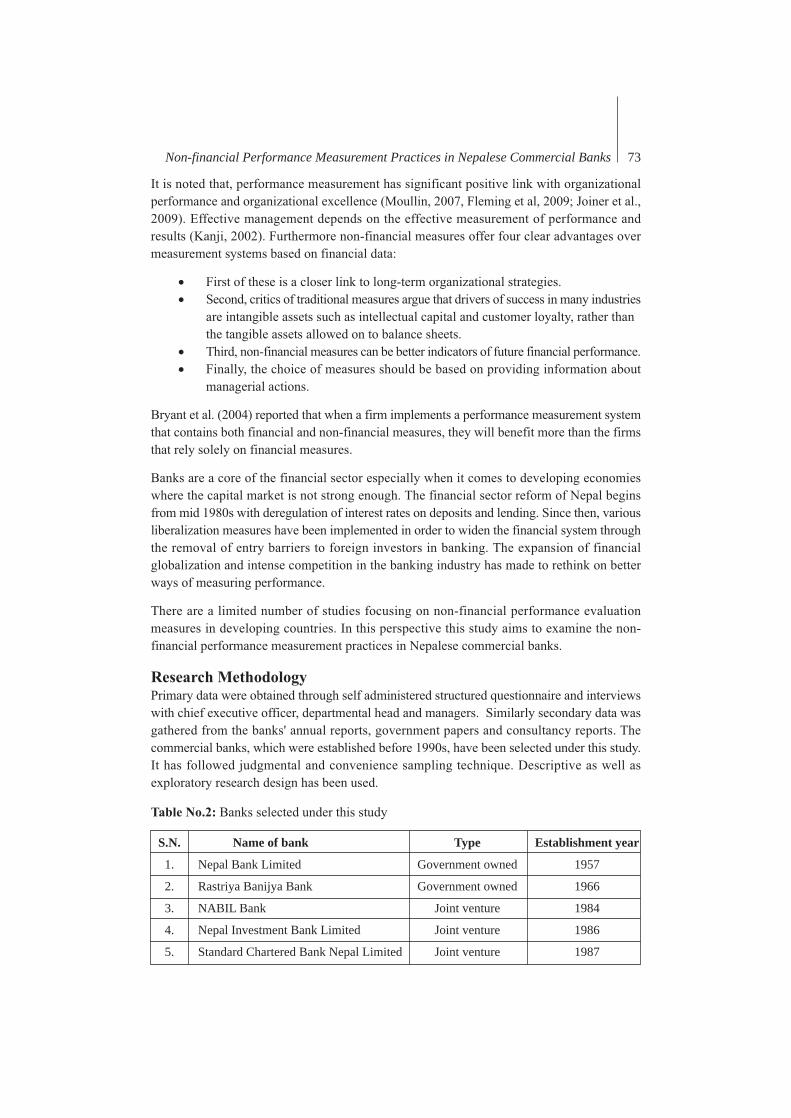

MethodologyIn this study an attempt has been made to assess the relationship between corporate incometax and debt-financing of manufacturing companies which are enlisted in Nepal SecurityExchange Limited. Altogether eight companies were selected by considering reported profitand loss. The manufacturing companies which have reported operating loss in any year outof the last five years (2006/07 to 2011/12) have been taken as loss-making companies. And

4 Achyut Gyawali

obviously, those companies which have reported profit for all last five years of study periodhave been taken as profit-making companies. In this study only secondary data have beenutilized for analysis. The financial accounting data for the period of ten years (2001/02 to2011/12) were collected from the annual and periodic publications of Nepal Stock ExchangeLimited (NEPSE), and Securities Board, Nepal (SEBO/N). The publications of NEPSE like:Financial Statements of Listed Companies, Trading Report, and Monthly Bulletin were utilizedas data sources. Similarly, the publications of SEBO/N like: Securities Board Nepal: AnnualReport, Securities Market Review, and Securities Board Nepal: Journal, were essentially takenas the sources for secondary data. The data that were collected in these ways have beenanalyzed with regression equations for each group of profit-making and loss-making companiesand for total sample.

Alessi (1965) incorporated corporate income tax rate as a single independent variable toinvestigate the effect of corporate income tax on debt-equity mix. In that study, he concludedthat the corporate income tax rate should be considered as a major independent variable inany model intended to explain variations in debt-equity mix. He considered the effect of othernon-tax variables on debt-equity mix to be somewhat less critical and confined to a simplelinear equation having the tax rate as the only independent variable.

Rao and Rao (1975) employed three measures of dependent variable debt-equity mix. Spencer(1969) argued that in an unconstrained reduced form equation the variables included areimportant only in their ability to represent a spectrum of variables which will remove thenontax influences while isolating the tax influence. In another study, Wang (1991) employedthree alternative measures of explanatory variable effective tax rate, computed as: the ratioof tax expenses to gross profit, the ratio of tax expenses to pre-tax profit and the ratio of taxexpenses to earning before interest and tax, in investigating the relationship between firm sizeand effective tax rate. Myers and Brealey (2000) pointed out that the debt equity ratio forcorporations as a whole depends on the corporate tax rate. If corporate tax rate is increased,migration starts again, leading to a higher debt to equity ratio for companies as a whole.

For better result, dependent as well as explanatory variables can be used alternatively toestimate the relationship between debt-equity mix and corporate income tax. Thus, in thisstudy different measures of debt-equity mix such as debt to networth ratio, debt to total assetsratio, and total debt to total assets ratio have been employed as dependent variables. In thesame way, two measures of corporate income tax rates like: statutory corporate tax rate andeffective tax rate have been employed as explanatory variables alternatively.

In the present study, the following equation has been taken as base to specify the equationsshowing linear relationship between debt-equity mix (measure of debt financing) and corporateincome tax rates.

Yt = a0 + a1 Zt-1 + u. …. … … … … (1)

Y = measures of debt-equity mix, Z = effective tax rate, u = error term, a = parameter to beestimated, t = current fiscal year under consideration (Rao and Rao, 1975: 11).Previous empirical studies have suggested that dependent as well as explanatory variablescould be used alternatively to estimate the relationship between debt-equity mix and corporate

Influence of corporate income tax on debt-financing: Evidence from Nepalese manufacturing companies 5

income tax rates (Rao and Rao, 1975:15). Thus, in this study, different measures of debt-equity mix such as debt to networth ratio; debt to total assets ratio, and total debt to total assetsratio were employed as dependent variables. Therefore, equation (1) has been adjusted withalternative measures of dependent variable (debt-equity mix) and the following specifiedlinear regression equations were employed to estimate the relationship between debt-equitymix and effective tax rate in the present study:

(D/NW)i, t = a0 + a1 Zi, t-1 + ui. …. …. (2)

(D/TA)i, t = a0 + a1 Zi, t-1 + ui. …. …. . (3)

(TD/TA)i, t = a0 + a1 Zi, t-1 + ui. …. …. (4)

D = long term and short term borrowings, NW = net worth, TA = total assets,TD = total debt, Z = effective corporate tax rate, t = current fiscal year under consideration;a0, a1 = parameters to be estimated, i = states of nature of the sample companies like: big,medium, small, profit-making, loss-making, and total sample; u = error term.

Debt-Equity MixDebt-equity mix is the financing mix. It is the proportion of debt and equity capitals used tofinance investments. The optimal debt-equity mix of a company normally depends on thenature of the business. There are different motives for borrowing by the firms. Among them,capturing the tax benefits of deductibility of interest is the one (Pringle and Harris, 1987: 493,506). In this context it is to be noted that the empirical results are sensitive to the ways ofmeasurement of variables. The usefulness of a model, hence, has to be tested with possiblealternative measures of the variables. Thus, the ratio of debt to net worth, the ratio of debtto total assets, the ratio of total debt to total assets etc. could be the alternative measures totest the debt-equity mix (Rao and Rao, 1975:15).

In the present study, debt-equity mix has been taken as the measure of debt financing. Threealternative measures of debt-equity mix were employed to examine the relationship betweendebt financing and corporate taxes. These measures were: debt to networth ratio, debt to totalassets ratio, and total debt to total assets ratio. Further, these measures of debt-equity mixwere computed by applying following formulas:

Long term borrowings + Short term borrowingsD/NW = --------------------------------------------------------------- … … (5) Total assets - Total liabilities

Long term borrowings + Short term borrowingsD/TA = -------------------------------------------------------------- … … (6) Total assets

6 Achyut Gyawali

Long term liabilities + Current liabilitiesTD/TA = -------------------------------------------------------------- … … (7)

Total assets

Total assets = current assets, and fixed assets. Current assets = cash and bank balance, sundrydebtors, inventory and misc.current assets. Fixed assets = plant and machinery, land andbuildings, vehicles, furniture and fixture, office equipment and other fixed assets. Totalliabilities = long term liabilities, and current liabilities. Long term liabilities = long termloans, and miscellaneous deferred liabilities. Current liabilities = short term loans and advances,sundry creditors, and misc. current liabilities.

Effective Tax RateThe relation between the income tax accrual and the pre tax income is referred to the effectivetax rate (Bernstein, et al., 2000: 587). The measurement of effective tax rate depends uponthe method of accounting used to report financial activities. It also depends upon the purposeof enquiry to which effective tax rate is essential. Effective tax rate can be measured as theratio of tax provisions to profits before tax (Gandhi, 1968: 39). Alternatively, effective taxrate can be measured as the ratio of income tax expense to pre tax income (Sondhi, et al.,1994: 539). Further, effective tax rate can be measured as the ratio of income tax expensesto profit before tax or gross profit (Wang, 1991:162). Where, a positive relationship betweeneffective tax rate and debt-equity mix is expected.

In the present study effective tax rate has been computed by applying the following formula:

Income tax provisionEffective Tax Rate = ------------------------------- … … … (8) Profits before tax

Relation of Effective Tax Rate to Debt-Equity MixEffective tax rate is a true tax rate applicable to a firm. This rate is usually less than statutorycorporate tax rate. The financing mix of a business firm is affected by an effective tax rate.In order to examine the relationship between debt financing and effective tax rate, the debt-equity mix measures have been regressed on effective tax rate. In addition to this, the sameregression equations have been used to estimate the relationship of debt financing and effectivetax rate separately for profitability-wise states of nature of the selected companies.

The regression results of the measures of debt-equity mix on effective tax rate for profitability-based states of nature of selected companies have been presented in Table 5.6.

Influence of corporate income tax on debt-financing: Evidence from Nepalese manufacturing companies 7

Table:1Results of the Regression of Debt-equity Mix on Effective Tax Rate

S.N Dependent Constant ExplanatoryVariables Variable r2 F N

(Z)t-1

1 (D/NW)tProfit-making 0.458* 0.0736 0.011 0.457 43

(4.041) (0.676)

Loss-making 2.250* -0.269 0.009 0.300 34(6.865) (-0.548)

Total 1.257* -0.023 0.001 0.037 77(6.504) (-0.193)

2 (D/TA)tProfit-making 0.151* 0.0361*** 0.045 1.979 44

(5.433) (1.407)

Loss-making 0.554* -0.0541 0.032 1.068 34(15.889) (-1.033)

Total 0.322* 0.031 0.011 0.67 78(9.612) (0.259)

3 (TD/TA)tProfit-making 0.430* 0.0216 0.009 0.467 51

(14.158) (0.684)

Loss-making 0.717* 0.0137 0.002 0.071 34(21.051) (0.267)

Total 0.542* 0.046 0.012 0.168 85(18.304) (0.410)

Notes: Figures in parenthesis are t-values.* Significant at 1 percent, ** Significant at 5 percent, ***Significant at 10 percent,

The Table: 1 depicts regression results of debt-equity mix measures on effective tax rate forprofit-making and loss-making companies. The coefficient of explanatory variable effectivetax rate for profit-making companies is statistically significant at 10 percent level, with thedependent variable (D/TA)t. The sign associated with the coefficient indicates a positiverelationship between (D/TA) and effective tax rate. However, this coefficient (0.0381) isfollowed by weak r2 showing only about 5 percent variation in debt to total assets ratio isexplained by effective tax rate. Moreover, the 'F' value is observed statistically insignificant,which indicates that there is absence of statistical evidence about the good fitness of regressionequation. On the other hand, the coefficients of this explanatory variable with dependentvariables (D/NW)t and (TD/TA)t have showed positive signs, but these coefficients arestatistically insignificant.

8 Achyut Gyawali

For loss-making companies, it is observed that the coefficients of explanatory variable, effectivetax rate, showed negative signs pertaining to dependent variables (D/NW)t, and (D/TA)t.But, the observed coefficients are not statistically significant at 10 percent level. Thus, thenegative association of effective tax rate and debt-equity mix lacks considerable statisticaljustifications in the context of loss-making companies. The coefficient of explanatory variable,in relation to the dependent variable (TD/TA)t, is appeared with positive sign, suggestingpositive association of effective tax rate with total debt to total assets ratio. However, thiscoefficient is not statistically significant, reflecting negligible association between thesevariables.

For total sample, Table: 1 shows regression coefficients of effective tax rate having positivesign for two measures of dependent variable and negative sign for one measure of dependentvariable. The explanatory coefficients are statistically insignificant. Due to this, it can beconcluded that debt-equity mix and effective tax rate are related positively, but their relationshipis not statistically significant.

ConclusionThe regression coefficient of explanatory variable (effective tax rate) for profit-makingcompanies is observed significant with the dependent variable (D/TA)t. The sign associatedwith this coefficient has indicated a positive relationship between (D/TA) and effective taxrate. Likewise, the coefficients of effective tax rate with dependent variables (D/NW)t and(TD/TA)t have positive signs, however these coefficients are observed insignificant. Thus,an insignificant positive relationship has been found between effective tax rate and debt-equitymix of profit-making companies.

For loss-making companies, the regression coefficients of explanatory variable (effective taxrate) with dependent variables (D/NW)t, and (D/TA)t are observed with negative signs. But,the observed coefficients are not significant. Again, the coefficient of this explanatory variablein relation to the dependent variable (TD/TA)t has been observed with positive sign, suggestingpositive relationship of effective tax rate with debt-equity mix. However, this coefficient ofthe effective tax rate is also not significant. Thus, there is an insignificant negative relationshipbetween effective tax rate and debt-equity mix of loss-making companies.

The results, depending upon the measures of dependent variable used, are consistent with thefindings of Rao and Rao (1971) and Rao and Rao (1975) studies that the relationships ofeffective tax rate with debt-equity mix vary across the measures of dependent variable testedin the model. Moreover, the relationship of effective tax rate and debt-equity mix variesaccording to profitability status of the companies. For total sample, the regression coefficientsof effective tax rate with debt-equity mix are positive. Thus, an insignificant positive relationshiphas been found between effective tax rate and debt-equity mix. This observed relationshiphas indicated that the corporate income tax rate does not influence debt financing ofmanufacturing companies significantly. This finding has implication on financing behaviorof the companies that the Nepalese manufacturing companies do not consider the effects ofcorporate income tax on debt financing while making decision about the appropriate mix ofdebt and equity capital.

Influence of corporate income tax on debt-financing: Evidence from Nepalese manufacturing companies 9

Agrawal, R.P. (1969-July). Financing company expansion The chartered accountant, The Institute ofChartered Accountants of India, P.19.

Alam, Kazi Firoz, (1994). Taxation and investment policy: A survey report on the New Zealandmanufacturing industry. Accounting forum, School of Accounting, University of South Australia,Vol.17, No.4, PP.121-143.

Alessi, Louis De (1965 -Spring). The corporate income tax and debt to equity ratio. Wester economicjournal, PP. 195-199.

Altman, Edward I. and Subrahamanyam, Marit G. (1985). Recent advances in corporate finance"NewYork: Irwin Homewood Illinois

Arditti, F. D. and Pinkerton, J.M. (1978-March). The valuation and cost of capital of the levered firmwith growth opportunities. The journal of finance, Vol. 33, PP. 65-73.

Bernstein, Leopold A. and Wild John J., (2000). Financial statement analysis, theory, application andinterpretation. Seventh Edition, California:Mc Gray Hill.

Brigham, Eugene F., Gapenski Louis C. and Ehrhardt Michael C. (1999). Financial management, theoryand practice. Florida: The Dryden Press, Har Court Brace College Publishers.

Chua, Dale (1995). The concept of cost of capital: Marginal effective tax rate on investment. InParthasarathi Some (Ed.) "Tax policy" Washington: IMF.

Fama, Eugene F. and French Kenneth R. (1998). Taxes, financing decisions, and firm value. The journalof finance, Vol. 53, No. 3, PP. 819-843.

Fama, Eugene F. And Miller Merton H.(1972). The theory of finance. Hinsdale: Dryden Press.

Gandhi, Ved, P. (1968-April). Company tax incidence- industry studies. The indian economic review,Vol. 3, No. 1, PP. 33-47.

Hutchinson, Patrick, Alison Stewart, Gregory Warwick and Lumby Stephen (1994). Financial managementdecisions, principles and practices. Sydney: Thomas Nelson.

Jensen, Michael C. (1986). Agency costs of free cashflow, corporate finance and takeovers. Americaneconomic review, Vol. 76, PP. 323-329.

Jensen, Michael C. And Meckling, William H. (1976). Theory of the firm: Managerial behavior, agencycosts and ownership structure. Journal of financial economics, Vol. 3, PP. 305-360.

Keown, Arthur J., Martin John D., Petty J. William and Scott JR. David F. (2001). Foundations offinance, the logic and practice of financial management.

Third Edition. New Jersey: Prentice Hall International.

Khadka, Rup (1994). Nepalese taxation, a path for reform. Merburg: Merburg Consult for Self HelpPromotion. P.119.

References

10 Achyut Gyawali

Khadka, Rup (2001). Income taxation in Nepal: Retrospect and prospect. Kathmandu: Ratna PustakBhandar.

Kandel, Puspa (2009). Tax laws and tax planning in Nepal. Katmandu: Buddha Academic EnterprisesPvt.Ltd.

King, John R. (2013). Debt and equity financing. In Parthasarathi Some (Ed.) "Tax policy", Washington: IMF. P.158.

Martin, John D., Petty J. William, Keown Arthur J. and Scott David F. (1991). Basic financial management.New Jersey: Prentice Hall International.

Myers, Stewart C. (1977). Determinants of corporate borrowing. Journal of financial economics, Vol.13, No. 2, PP. 147-175.

Myers, Stewart C. And Brealey, Richard A. (2000). Principles of corporate finance. Sixth Edition, NewYork: McGraw Hill.

Pringle, John J. and Harris, Robert S. (1987). Essentials of managerial finance. Sydney: Scott Foresmanand Company.

Rao, S. C. Humananta and Rao, V. Ganapathi, (1971-Dec.). The effects of taxation on corporate capitalstructure. "Indian journal of commerce. Vol. 26, No. 90, PP. 239-248.

Rao, V. G. and Rao K. S. H., (1975-April). The corporate income tax and corporate debt policy. Indianeconomic review, Vol, 10.New Series, No. 1. PP. 7-25.

Ross, Jordan, Bradford D. and Westerfield, Randolph W. (2013). Essential of corporate finance. ThirdEdition, New York: McGraw Hill.

Saynyal, S. K. (1971-May). Trading on the equity: A tool in the hands of the financial manager. Thechartered accountant, The Institute of Chartered Accountants of India, P. 817.

Sondhi, C. Ashwinpaul, White I. Gerald, and Fried Dov, (1994). The analysis and use of financialstatements. New York: John Wiley & Sons, Inc.

Spencer, Byron G. (1969-Feb). The shifting of the corporate income tax in Canada. The Canadian journalof economics, PP. 21-34.

Wang, Shiing Wu (1991). The relation between firm size and effective tax rates: A test of firms' politicalsuccess." The accounting review, American accounting association, Vol. 66, No.1, PP. 158-169.

An Analysis of Electricity Consumption in Industrial Sector of Nepal 11

AN ANALYSIS OF ELECTRICITYCONSUMPTION IN INDUSTRIALSECTOR OF NEPAL

Bhola Nath Ghimire...?Abstract

Nepal has a huge hydropower potential. In fact, the perennial nature of Nepali rivers and thesteep gradient of the country's topography provide ideal conditions for the development ofsome of the world's largest hydroelectric projects in Nepal.The purpose of this article is to derive and estimate a consumption function for Nepaleseindustrial electricity use, and to investigate changes in consumption pattern over the timeperiod 1980-1912. The article employs data on the industrial electricity use, electricity andoil prices and data on the value of production, and specifies a log liner function, which isused running OLS regression. The data are divided in to two time periods 1980-1995 (beforeconflict) and 1996-2012 (conflict and then) in order to test for structural change and theChow test used in the research for testing structural change in consumption. The consumptionfor electricity in second period is higher than that of first period. The own price electricityconsumption and cross price elasticity of consumption have gone by statistically significantin both periods., and the Chow test also shown that there is structural break in consumptionfor hydroelectricity by Nepalese industries.Keyword: Electricity, consumption, elasticity, Chow test, structural break

IntroductionThe use of electricity and fossil fuels over the last decade seems to be accelerating as evidencedby an empirical research carried out recently in Nepal (Dahal, 2004). Nepal has a hugehydropower potential. In fact, the perennial nature of Nepali rivers and the steep gradient ofthe country's topography provide ideal conditions for the development of some of the world'slargest hydroelectric projects in Nepal. The average annual precipitation is approximately1700 mm (80% of which occurs during the monsoon season - June to September). The totalannual average run-off from the nation's 600 perennial rivers is over 200 billion m3 Currentestimates are that Nepal has approximately 42,000 MW of economically feasible hydropowerpotential. However, the present situation is that Nepal has developed only approximately705MW of hydropower. Therefore, bulk of the economically feasible generation has not beenrealized yet. By the end of FY 20012/13 from all projects across the country, 705 MW ofelectricity has been generated. Of the total electricity generated, 697 MW has been connectedto the national grid, while for the rest; the stand-alone micro hydro-electricity centers havebeen supplying them at the local level. Likewise, including the thermal electricity centres'production of 53.4 MW and solar centres' production of 100 KW, the total electricity productionhas reached 758 MW (Source: 13th periodic plan).

Mr. Ghimire is the Lecturer of Economics at Global College of Management

12 Bhola Nath Ghimire

An Analysis of Electricity Consumption in Industrial Sector of Nepal 13

Cross Price Elasticity of ConsumptionThe cross price elasticity of electricity consumption shows the change in consumption forelectricity when the price of the substitute, oil, changes. This cross price elasticity is definedas:

To test for a structural break, Chow test used in the model, which is defined as:

If the cross price elasticity of electricity consumption is positive the goods are said to be grosssubstitutes, implying that the consumption for electricity will increase as the price of thesubstitute increases.

Where RSSR is restricted residual sum of square and RSSUR is called unrestricted residualsum of square and RSSUR is the sum of RSS1 and RSS2. Result is obtained through use ofsoftware stata and all the diagnostic checks such including Autocorrelation, Hetroskedasticityand Multicollenearity done and the model modified as needed and result interpreted accordingly.

Analysis for Elasticity and Structural Break of Electricity Consumptionby Industrial Sector of NepalNepalese industries have been using coal, Hydroelectricity, Petroleum product and otherrecycling solid and liquid materials simultaneously. However according to research topic forsimplicity of the analysis I have used only Petroleum product as substitute source of energy

14 Bhola Nath Ghimire

along with electricity in my research. Its main reason is the price of coal and recycling materialare not found as collective form, from the authentic sources therefore I have avoided thefeasible happing of destruction in my model. The model is, free from autocorrelation andheteroskedasticity problem.

Price and Cross Price Elasticity of Electricity ConsumptionElasticity of consumption refers to change in quantity of goods and services by certainpercentage due to change in determinants of consumption by a one percentage. The Estimatedelasticity consumption of price and cross price based on model, 1 are shown in table 4.1.

Table 1: Estimation of the price elasticity and cross price elasticity of consumption

Variables Coeffi. std.error t-value prob. Coeffi. std.error t-value Prob. Coeffi. std.error t-value prob.

lnPEL -0.10 0.004 -21.25 0.00 -0.19 0.008 -23 0.00 -0.07 0.004 -19.68 0.00

lnPOIL 0.70 0.03 23.03 0.00 0.52 0.57 9.10 0.00 0.35 0.015 24.5 0.00

DW Test 1.54 1.34 1.89

LM Test 0.185 0.67 0.007 0.93 0.887 0.35

Heterosked.Test 12.24 0.20 7.08 0.215 11.20 0.26

R2 0.99 0.95 0.98

F 1030.39 0.00 53.98 0.00 408.19 0.00

Level of significance = 5%

Dependent variable = lnELTime period 1980 – 2012(n = 28) 1980 – 1995(n = 11) 1996 – 2012(n = 17)

Note: where EL = Electricity consumption, PEL = Price of electricity,POIL = Price of Petroleum product, ln = Natural logarithm and Coeffi. = Coefficient.

Own Price Elasticity of Electricity ConsumptionThe elasticity table 4.1 shows that the own price elasticity of electricity consumption issignificant at a five percentage level for the time- period 1980-2012 , 1980-1995 and1996-2012 as well. Where the coefficient for all periods are negative which implies that onepercentage change in price of electricity would lead to a decrease in industry's total consumptionof electricity by 0.10 percentage, 0.19 percentage and 0.07 percentage at1980-2012,1980-1995 and1996 -2012 periods respectively, ( when other things remain constant). It showsthat negative relationship between electricity consumption and price of electricity. Theconsumption is less elastic in the period 1996-2012 than 1980-1995. It could be happened atsecond period due to high consumption of electricity for industry, consumers were standingby to purchase electricity even though price is in increasing order. After signing the consensusof carbon- business agreement, just to reduce carbon mono-dioxide and for environmentfriendly sustainable development, people choose electricity as a first source of energy.Various explanations can be raised for this lower elasticity; first, the price of electricityremained very low and almost constant during the period 1980-2012. Second, industries werenot run properly before privatization programme and in this prospect, government's interestjust could be the cost of producing and transmitting electricity to the industry. Third, governmentmade several policy statements (such as hydropower development policy, rural energy policy,climate change policy etc.). It would keep the price of electricity as low as possible to attractinvestment in industrial sector.

An Analysis of Electricity Consumption in Industrial Sector of Nepal 15

Cross Price Elasticity of Electricity ConsumptionThe elasticity table 4.1 shows that the cross price elasticity of electricity consumption issignificant at a five-percentage level for the period 1980-2012, 1980-1995 and1996-2012 aswell. The coefficient for all periods are positive which implies that one percentage changein price of petroleum product would lead to a increase in industry's total consumption ofelectricity by 0.70 percentage , 0.52 percentage and 0.35 at 1980-2012 , 1980-1995 and1996-2012 periods respectively (when other things remain constant).

It shows that cross elasticity of consumption for electricity the overall period is more elasticthan samples. Therefore, we can say that when increased the price of petroleum product,consumers bought more units of electricity at overall period, it gives that petroleum productbecomes perfect substitute goods for electricity. However, industries were not ready to consumemore units of electricity after 1995 as comparison that of before, when the price of petroleumproduct increased by certain percentage. Industry bought more units of electricity before 1995comparatively after that of period. It could be happened due to high load shedding problems,consumer used their private plant, but previously consumer used energy run by diesel pumpedand when price of petroleum product increased definitely increased in the consumption(consumption) of electricity. At the beginning there were not enough policies regarding toelectricity can be one caused for more elastic. Although diesel has shown its potential as asubstitute for electricity, yet its escalating prices and strict environmental regulation in Nepalmay reduce the substitutability.

Chow Test AnalysisModel 1 assumes that there is no difference, consumption for electricity between the two timeperiods and therefore estimates the relationship between consumption for electricity in industryand price of electricity with its substitute goods price for the entire time period consisting 28observations. If the value of the test statistics is greater than the critical value from the F-distribution, which is an F (k, n1+n2-2k), then reject the null hypothesis that the parametersare stable over time.

Here we have restricted residual sum of square (RSSR) = 0.0870 with df 23 and Unrestrictedresidual sum of square (RSSUR) is given by sum of RSS1 and RSS2 i.e.RSSUR = RSS1 + RSS2 = 0.073.

Period Residual sum square Coefficient Calculated value Tabulated value

1980–2012 RSSR 0.870

1980–1995 RSS1 0.057 10.54(0.00) 3.05

1996–2012 RSS2 0.016

Level of significance 5%

Table 2: Chow test estimation

From the F tables, we find that for 4 and 22 df the 5 percent critical F value is 3.05, whichis smaller than calculated value (10.54). Therefore, we reject the null hypothesis that thecoefficients are the same in the two periods.The chow test shows that the consumption of electricity- price of electricity and price of oilrelation has undergone a structural change in Nepalese industries over the period1980-2012 has been tested. As above chow test could be easily generalized to handle casesof more than one structural break in the model.

16 Bhola Nath Ghimire

– Electricity consumption – Income of energy sector

1980 1990 2000 2010Year

Ele

ctric

ity c

onsu

mpt

ion

/ Inc

ome

108

64

Figure 1: Electricity consumption and Income of energy sectorNote: Electricity consumption is in GWh and Income is in ten millions Rs.

The figure 4.1 shows that the structure of change in consumption and income (Gross DomesticProduct from energy sectors) of electricity as changing period of time in Nepalese industriesbefore conflict period since 1980AD and after and then conflict 1996 AD separately.The income and electricity consumption by Nepalese industries both are increasing initiallyhowever, they are fluctuated in time-to-time (sometimes increasing with increasing rate,increasing with decreasing rate and decreasing). At the target period of time 1996AD, slightlydecreased in electricity consumption and its impact of income seemed in 1997 AD as a resultthe income curve slightly bended (it can be shown in figure 4.1) in 1996/97 AD. Civil war,internal and external disturbance in Nepalese industries, increasingly appeared politicalinstability disturbed in industrial sector as a result the measureable fluctuations came in tonotice of electricity consumption for industry of Nepal.

In the period of 1956-2012 the income elasticity, price elasticity and cross elasticity weregreater than previous period. It shows that due to political recovery phase after a decade civilwar, industrialization become a milestone for future economic activities so consumption forelectricity become more elastic in this period. The consumption for electricity slightly increasedas increased in size of population or consumers in various fiscal years. Nevertheless, thedrastically have not changed in consumption pattern as per possible potentiality of energy,its main cause can be lack of investment environment, political instability (mainly civil war)along with defective laws and policies.

Almost seven years after the end of a 10-year internal conflict, Nepal remains one of thepoorest countries worldwide, ranking 145th out of the187 countries on the Human DevelopmentIndex and enhancing almost 3.5% (in average) of Economic growth per annum. These valuesare less than south Asian average values. Harnessing hydroelectric potential along the Himalayaswill not only provide Nepal with a more reliable source of electricity, it would also addressthe costs currently borne by the population. Rural electrification could mitigate nationalinequalities by ringing health and economic well-being to millions of Nepalese.

An Analysis of Electricity Consumption in Industrial Sector of Nepal 17

Nepal's energy forecast to 2028 indicates the national electricity shortage will only becomemore severe in the future. In 2028, Nepal will face an energy output of 17404 GWh and thesystem peak load is furcated to reach about 3679 MW under a medium growth (NEA).

ConclusionThe purpose of this thesis has been to derive and estimate a consumption function for theNepalese industrial electricity use, this in order to investigate changes in consumption patternsover the time period 1980-2012. By using yearly data on total industrial electricity use,electricity and oil prices and the value of production, conducting OLS regressions on a loglinear consumption function on the entire time period, and , in order to test the model for astructural break, on the two time periods 1980-1995 and 1996-2012 elasticities of consumptionwere obtained.

The coefficients for the own price elasticity of consumption and the cross price elasticity ofconsumption in the first time period as well as second time period were statistically significantrespectively. Whereas own price elasticity and cross price elasticity of consumption both aremore elastic in first and second period than in second and first period respectively. Thisimplies that the industries consumption for electricity has gone from being entirely priceinsensitive to a situation where electricity use responds to changes in the own price also inthe short run. One possible explanation for this is that the electricity price incorporates ahigher uncertainly ever since the electricity market has been deregulated. This induces firmsto expand their flexibility in energy use, and thus make substitution between these inputseasier. It is always spell out using electricity is less economic than using alternative sources.Even the price of electricity is high; industries are ready to consume more units of electricity.It could be main attraction to the investors in electricity production field.The examination on the industrial electricity consumption presented in this report by usingregression analysis and Chow test shown the structural break in hydroelectricity consumption.It means there is changed in consumption for electricity by Nepalese industries in varioustime periods.

These result point out some important conclusions, electricity is today being used moreefficiently in production process than earlier, implying that the value of production is higherper used unit of electricity today. The industrial electricity consumption seems today to bemore influenced by environmental factors such as policy regulations on a more efficientenergy use and environmental policy regulations. Since the environmental awareness and thework on a more efficient energy, use is in an early phase it can be expected that these resultswill be strengthened over time.

ReferencesAltrnative energy promotion center/ energy sector assistant programme (AEPC/ESAP). (2001). Micro-

hydro data of Nepal: Kathmandu, Nepal.

Bhusal, T.P. (2009). Basic econometrics. Ayam Publication Pvt. Ltd., Kathmandu, Nepal.

CBS.(2010). Statistical year book of Nepal 2010. Central Bureau of Statistics, Nepal.

Chama, Y.(2012). An econometric analysis of zambian industrial electricity consumption. An unpublishedM.Phil. dissertation submitted to University of Oslo, Norway.

18 Bhola Nath Ghimire

Chaudhry, A. (2010,September). A panel data analysis of electricity consumption in Pakistan. The labourjournal of economics, Vol.3,pp. 75-106.

Dahal, M.K. (2004). Nepalese economy. Central department of economics and New Hira BooksEnterprises, Kathmandu, Nepal.

Dhungel, K. R. (2007). Trends and patterns of energy consumption in Nepal. An unpublished Ph.D.dissertation submitted to Tribhuvan University, Kathmandu, Nepal.

Dougherty, C. (2007). Introduction to econometrics. Oxford University Press, Newyork.

Enders, W. (2010). Applied econometric time series. Wiley India Pvt. Ltd., New Delhi, India.

Gujarati, D.N. (2006). Basic econometrics. Tata Mc Graw Hill companies.

Http://www.ippan.org.np/Hp in Nepal.html (3/13/2012)

Https://energypedia.info/index.php/Nepal-Country- Situation. (3/13/2012)

Https://trn.gorkhapatraonline.com/index.php/op-ed/11095. (10/10/ 2014).

Hunt, L.,& Judge, G.(2005). Estimating underlying energy demand trends using UK annual data. Appliedeconomics letters, 12(4), 239-244.

IEA.(2013). IEA electricity information. OECD electricity and heat supply and consumption.

Koutsoyiannis, A.(1977). Theory of econometrics. Palgrave, New York, U.S.A.

Lundberg, L. (2009). An econometric analysis of the Swedish industrial electricity consumption. Anunpublished master thesis submitted to Lulea University of Technology, Sweden.

Maddala, G.S.,& Lahiri, K.(2009). Introduction to econometrics. Wiley India Pvt. Ltd., New Delhi,India.

Madnani,G.M.(2005). Introduction to econometrics, principles and applications. Oxford & IBH publishingCo.Pvt.Ltd., New Delhi, India.

MOF. (2001). Economic survey fiscal year 2000/2001. Ministry of Finance, Kathmandu, Nepal.

MOF. (2014). Economic survey fiscal year 2013/2014. Ministry of Finance, Kathmandu, Nepal.

National Planning Commission. (2013). The thirteenth plan (2013-2016). National Planning CommissionSecretariat, Kathmandu, Nepal.

NEA. (2013). Nepal electricity authority FY 2012/2013 a year in review. Nepal Electricity Authority,Kathmandu, Nepal.

Nicholson, W.(2005). Microeconomic theory basic principles and extension. South Western, Thomson,Mason, Ohio.

NOC.(2014). Price survey of petroleum product in Nepal. FY2013/14, Nepal Oil Corporation, Kathmandu,Nepal.

NRB.(2010). Quarterly economic bulletin FY 2010/11. Nepal Rastra Bank, Nepal.

Parajuli,R.(2013). Energy consumption projection of Nepal: An econometric approach,www.elsevier.com/locate/renene.

Sharma, P.N.(2000). Further Nepal and use water resource. The true market, Year 3, No.5.

Water and Energy Commission. (2012). Review of consumption of energy in Nepal FY 2011/12. Waterand Energy Commission Secretariat/Government of Nepal, Kathmandu, Nepal.

A Case of Higher Secondary Education Board of Nepal

TEACHER MANAGEMENT ANDDEVELOPMENT IN HIGHERSECONDARY EDUCATION

Dev Raj Paneru...?

AbstractThis case study on higher secondary education board of Nepal examines qualitatively humanresource management and development practices undertaken to manage and develop teachersserving in the schools under HSEB in reference and against the stated vision, mission andobjectives of higher secondary education board of Nepal. An assessment of HSEB goals, HRMpractices undertaken by the board and universally accepted significance of HRM perspectiveswere used as main research strategies to address the research question stated here: Howdoes HSEB Nepal address teaching faculty management and development issues in an endeavorto address quality educational outcomes as envisioned in its policy documents? The analysisof statistical data from the HSEB office publications, electronic media, and qualitativeinformation, and research participants' opinions showed that integrating sustainable HRMpractices in line with other functions of HSEB was crucial for attaining academic objectivesmeasurably.Key words: management, development, enculturation, globalization, post -secondary,commissions, entrepreneurship, human resource management, efficient, effective.

Education in NepalNepalese education system seems to have endured uneven changes from the time of itsinception. Both internal and external factors are taken accountable for changes in the fieldof education till the date which have been unpredictable. The main stream political systemssuch as authoritarian governments under Rana oligarchy followed by dictatorial monarchies,then in the 21st century multiparty democracy and currently federal republic system yet tobe institutionalized are major internal factors and UNO guidelines, donor support for educationalong with internationalized mindset leading to English enculturation through globalization,are the external factors (Sharma &Sharma, 2066BS), taken accountable to have set Nepal'seducation into today's formal structures generallydivisible in three hierarchical layers. Thelevels are; 1. School level education ;1-5 primary, 6-8 lower secondary, and 9-10 secondary.2. Higher secondary; 11-12 grades and 3. Higher education; bachelors and masters level asuniversity programs, all administered, planed, budgeted, supervised and monitored by ministryof education as the apex body (Wikipedia, 2014).

Teacher Management and Development in Higher Secondary Education 19

Mr. Paneru is the Lecturer of managerial communication at Global College of Management. He is the PhDScholar at Kathmandu University and also an exchange student of Masaryla University Gech Republic underErasmus Mundus Action II

20 Dev Raj Paneru

Turns and bounds that education has so far travelled through are required to be reviewed inorder to gain some insight into the entire system. In this connection, prior to modern education,there was the system of imparting Sanskrit education based on Hinduism that is alleged tohave permitted Brahmins to study Vedas, Upanishada, Jyotish (Astronomy) and science ofrituals (KarmaKanda) and the Chhetris to learn administration and art of warfare. Hence,education was confined to these groups to support the kings in their administration and courts. Buddhist monks imparted education based on their religion during the Malla regime(Http://www.geocities, 2014).

Latterly, Prime Minister Jung Bahadur Rana, on returning home from Europe established anEnglish school in Thapathali Palace on 7th Ashoj 1910 BS to teach his children only and thus,is regarded to have been the founder of modern education. Subsequently, in 1915 BS, EducationDepartment was established that founded Darbar high school which later shifted to RaniPokhari and was named Bhanu Madhmik Vidhyalaya. Ranas as well gave place to Sanskritand Language schools called Bhasa Pathsalas. On closing some of the language schools,Chandra Samser established Tri-Chandra College in 1916 that obviously paved foundationof higher education first time in Nepal (Edusanjal.com, 2014). On demolition of Ranaoligarchy, democracy in 2007 BS merely competed to establish political system but faced asack in 2017 overtaken by King Mahendra who established Panchayat system.However, he is regarded for introducing modern education system by giving place to neweducational system plan in 2028 (Bhattarai, 2014). Ever since, education in Nepal is traceableclearly in the structures as school, and higher education which was further demarcated asschool education, proficiency level and university level. Following this development, educationplanning was embedded with development planning and ever since several commissions havecome into frame in endeavors to reform and modify education to make it time relevant andcontextually beneficial. Bhattarai (2014) observed,

The National Education Planning Commission, which was the first of its kind, was formedin 1954 after the dawn of democracy in 1950 in the country. After this, six other commissionsand committees have been made and they are: The National Education Committee in 1961,The National Education SystemPlan 1971, The Royal Commission on Higher Education 1983,The National Education Commission 1993, The High Level Education commission 1992; andThe Higher Education Task Force, 1999.

Nevertheless, it is often observed that though education has been named modern, it has notleft its past legacy of traditional approach and segregating values even till the date. ProficiencyLevel was operated in TU whereas CTEVT administered technical courses for the same levelsimultaneously. But as proficiency level comprising 11 and 12 grades was becomingburdensome and difficult to operate along with increasing volume of undergraduate andgraduate level education in TU, higher secondary education act was drafted in 1989 to segregatehigher secondary level from university education.

In the same context, Higher Secondary Education Assembly was constituted under thechairmanship of the Minister of Education that introduced Higher Secondary Education Board(HSEB) in 1989 under the same act. Ever since, the board is involved in running the 10+2system in the country which was also recommended as being important toward specializationby Nepal National Commission of Education 1992. This is alleged to have been an initiationfor incorporating extra two years in school education as a change in the existing educationalstructure. The development aimed at meeting the middle level human resource and imparting

Teacher Management and Development in Higher Secondary Education 21

necessary knowledge and skills to the students pursuing further education, need invited byglobalization (www.hseb.edu.np/introduction).

There are approximately 3600 higher secondary schools run in private and community effortshaving Nepali and English medium at present. Nearly, entire higher secondary level populationis accommodated in the schools under HSEBas there is no other entity in Nepal that takenresponsible to educate this age group populace except Cambridge A level run privately inmeager number of institutions with meager number of students and a few technical schoolsrunning CTEVT programs (Ghimire, 2014).

Higher Secondary Education BoardFormation of Higher Secondary Board is often linked with a common realization in theeducation stakeholders that higher secondary level is far more important in extending thenurturing period of school age children from 10 years to 12 years by integrating grade 11 and12 grades deemed essential in shaping and preparing them for university education with qualityand skills (http://www.hseb.edu.np/introduction, 2014). At this turn of the time, highersecondary education board is one of the largest educational administrative bodies like SLCboard and is entitled to planning, organizing, leading and controlling the entire higher secondaryeducation system for general education that includes administrating educational and evaluationactivities, as well as activities relating issuance of credentials.

Producing middle level human resources as well as preparing students for university educationis the key objective that HSEB has adopted since its inception in 1992 as an option to currentlyrunning proficiency level in Tribhuvan University which eventually was phased out in theyear 2010. Understandably, increasing volume of students that a single university was notable to accommodate on one hand and liberalized education policy that opened the horizonfor public as well as private sectors to contribute in the field of educational entrepreneurshipmore freely on the other hand are supposed to have resulted into formation of HSEB.Apart from its key objective that of developing middle level manpower, HSEB aims atpromoting marginal populace for higher secondary education; produce capable and competentscholars and contribute as a feeder level for university education. The higher secondaryeducation council is responsible to forward policy and recommend strategy to the cabinet ofministers so as to address mission, vision and objectives of the board apart from taking theresponsibilities such as granting affiliation to schools , managing teachers, developinginfrastructure, developing curriculum, & controlling quality(ibid).

Presently, there are approximately 36oo higher secondary schools and some of them are newaffiliates in2071 with approximately more than 300000 students taking admissions andappearing in grade 11 exams every year and thus, the entire institution is believed to beaccommodating about 1000000 students in total (Gurung, 2013 in Sampreshana, 2013;Sampreshana, 2014).

Owing to ever increasing size of higher secondary level population and growing number ofschools and institutions, the council of higher secondary education is alleged to be holdinga huge national responsibility of educating almost entire learning population of post secondarylevel. The fact is that along with the increased volume of consumer groups such as schoolsand their students, HSEB is expected to have been preoccupied with policy, management andadministration related functions at centre, region, and local level far more extensively nowthan it used to be prior to 2010, before PCL was phased out from TU (Sharma, 2013 inSampreshana, 2013). As stated in its office website (2014), the specific objectives of Higher

22 Dev Raj Paneru

Teacher Management and Development in Higher Secondary Education 23

24 Dev Raj Paneru

at providing introductory remarks only, it does not seem to be adequate in addressing a largenumber of crucial areas without which management is alleged to remain incomplete.

Olum (2004) has examined modern management theories and practices stressing on thegrowing importance of managerial skills for managing complex organizations indicatingcomplexity in managing human resources in the emerging cross cultural contexts. The paperconcludes utmost importance of human resource over other kinds of resources or conditionsand thus, it shows that organizations either prosper or fail excessively depends on capablehuman resource and this in turn is possible only if HRM is effective and efficient. Despitepowerful advocacy on importance of human resource management, the paper does not seemto specify internal components of human resource management nor does it speak about howto address human resource development issues.

A profile of higher secondary education: Statistics books (2071 BS) is a book of statistics andit presents information on entire national result of the board in seven different methods. Thedivisions of result presentation are 1. Group wise result status of grade XI and XII 2. HigherSecondary School type wise result status 3. Development region wise result status 4. Sectoraloffice wise result status 5. Eco-development wise result status 6. District wise result statusand 7. School wise result status (Statistics Book, 2071 BS).

The presented data in the book showed that HSEB result in the national level in the year 2065BS remained below 46%, it was nearly 47% in the year 2066 BS, the result in the year 2067deteriorated and went down to 44%, it again rose up to 48% in the year 2068 BS but in theyear 2069 the HSEB result went far further down to 42 %, it again progressed a little andreached 44% in gross in the year 2071. From the tabulated data in the book it becomes clearthat HSEB result has remained highest in all categories in the year 2068 and it sustained leastpercentage in the year 2069. Although result status presented in the book may be verysignificant in getting some insights on how HSEB has been functioning, in getting to knowabout students' academic performance which can as well be treated as an indicator of lettingsome insight upon performance of teaching faculties and schools as exam results are prettygood indicators for educating process and personnel competence (Gurung, 2014). However,as there is no other area of information appended in the book, it can't be taken useful ifrecordable data are required in other areas as curriculum, school, teacher, staff managementetc.. Besides, the book contains foreword by member secretary and vice-chairman who claimedthat the purpose of the book is to identify changes that have occurred since 2064BS till thedate and stated that it contains information on different activities of higher secondary educationboard. But in fact, it merely limits to presenting information on result status in seven differentheads including students and schools, regions etc. and hence, it does not speak anythingregarding management, development and status of teaching faculty under HSEB. Sampreshan (2014) a latest publication of HSEB in the form of bulletin stated vision, mission,and objectives that its vision is to develop the youth of 21st century Nepal as able citizenswho would be able to deal with forth coming challenges. The objectives are to develop middlelevel work force and to prepare capable scholars eligible to join university education. Thepublication presents some glimpses on teachers and head teachers training and otheradministration related information but does not seem to provide information about policy andpractices regarding management and development of higher secondary level teaching faculties.It presents the list of schools with their result of XI (2069) and XII (2070) and has only 3266schools listed appeared XI and XII examination in 2069 and 2070 respectively. The result ofXII seems to have been progressive in the year 2070 as it is 52% in gross. Despite ample

Teacher Management and Development in Higher Secondary Education 25

information on various areas, the bulletin does not seem to have given any space for informationabout HRM and HRD to link teaching faculty status.

SSRP MOE (2009), in full form school sector reform project is a national project that is aimedto redesign the school level education including higher secondary education which initiallyhad been a university proficiency level latterly handled by higher secondary board after itsestablishment in 1992. The document speaks in detail on the modalities e.g. structure,curriculum, administration and supervision and monitoring and over all frame of action. Thedocument proposes teaching faculty management as well as development as the keyresponsibilities of department of education which till the date seems to be providing twoteachers to a school on relief quota and the rest to be managed by the school managementcommittee itself for higher secondary level. Nevertheless, the SSRP does not seem to haveworked in details about modality of faculty management so far.

Reform in higher secondary education : Connecting education with the world bank bySharma, T.( 211). is an argumentative feature journal paper aiming to discuss various aspectsof integration of curricula to bring transformation on higher secondary education in Nepal.The paper is useful as it supports the idea of teacher collaboration while exercising thecollaboration of curricula but as it is limited to addressing its key concern i.e. to discuss andadvocate on various modalities of curricula integration, the paper speaks very little aboutteacher management issue. It rather speaks about collaborating teachers as a means to collaboratecurricula. There is no further detail on how teaching resources under HSEB are being managedand developed.

Review in ConclusionThe above reviewed journals, documents and books can be categorized as office documentsof HSEB, theory journal papers and information documents. The theoretical works show thathuman resource management and development is a very crucial area of concern for managementof any organization in any size and it has been more crucial in the today's changed contextsi.e. cross cultures as the external factors in organizations. In this regard, for HSEB as it aimsto develop youth in 21st century Nepal who would be able to tackle with the any kind ofchallenges in their professional life, effective and efficient management and development ofteaching personnel and resources in all its faculties would be essential. But the documentsshow that there are still no clear landmarks nor any frames to deal with this issue as the schoolsare left to manage and develop their teachers on their own except provision of only 2 teachingpersonnel provided to a school in all.

Study ContextThe present study is an exploratory study. Its field is Higher Secondary Education Board. Thehead office of the board is located at Sanothimi- Bhaktapur Nepal. Since the teaching facultymanagement and development issue is supposed to be one of the concerns of HSEB in thelight of the fact that education is centrally controlled phenomenon in the country, head officewas selected over other sectoral, regional and district offices for data generation purpose.Along with Kathmandu district office was contacted for a telephone conversation and thechief of the office was interviewed to learn whether the district offices coordinated the schoolsfor human resource management and development purposes or not.