jorge madias, metallon: a review of the production and consumption of steel in south america

TRANSCRIPT

A REVIEW OF STEEL

PRODUCTION AND

CONSUMPTION IN

SOUTH AMERICAN

COUNTRIES OTHER

THAN BRAZIL Jorge Madias

6th Annual Americas Iron Ore Conference, November 2013, Rio de Janeiro, Brazil

Introduction

Discussion country by country

Conclusions

Agenda 2

metallon 3

Consulting & training company

Based in San Nicolas, Argentina

Serving the steel industry and its chain value in Latin America

Technical courses (open, in company, self learning)

Technical assistance (ironmaking, steelmaking, rolling)

Library services

Met lab services

www.metallon.com.ar

Introduction 4

Argentina, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, Venezuela

Hot metal production, 2012: 3,556,000 t

DRI/HBI production, 2012: 6,176,000 t

Production crude steel, 2012: 11,855,000 t

Production rolled products, 2012: 11,730,000 t

Imports rolled products 2012: 7,908,500 t

Exports rolled products 2012: 1,471,600 t

Apparent consumption 2012: 18,167,400 t

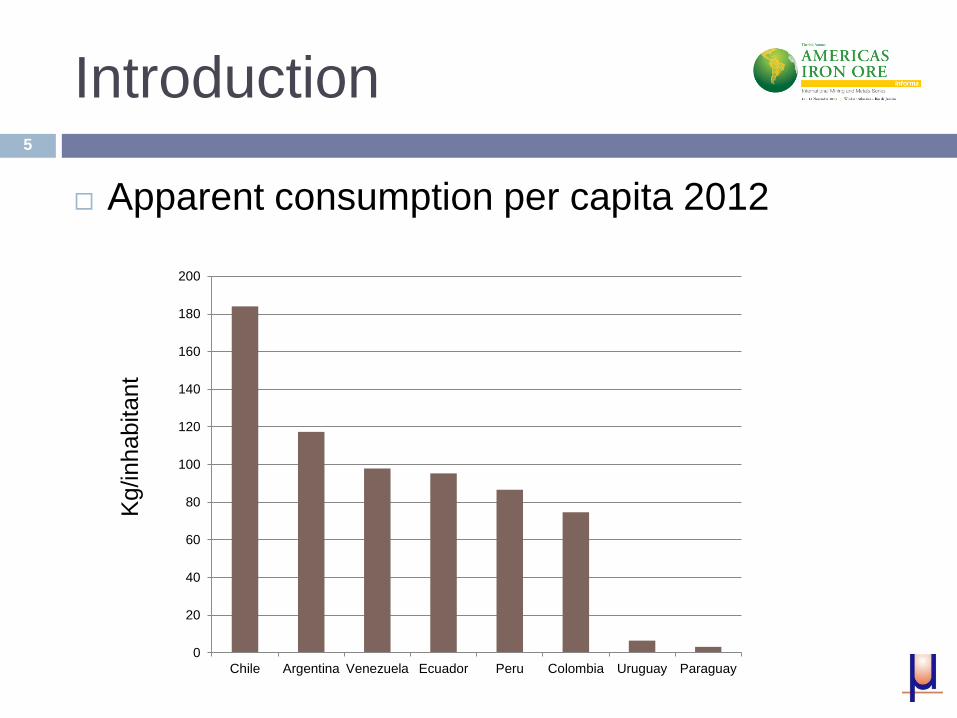

Introduction 5

Apparent consumption per capita 2012

0

20

40

60

80

100

120

140

160

180

200

Chile Argentina Venezuela Ecuador Peru Colombia Uruguay Paraguay

Kg

/inh

ab

ita

nt

Introduction 6

Discussion country by country

Companies - Ownership

Ironmaking units, iron ore suppliers

Production of rolled steel (flat and long

products)

Apparent consumption

Imports and exports

Investments

Consequences on iron ore demand

Argentina: Market protection 7

SIDERAR (Ternium – Techint Group) Flat

products

Acindar (ArcelorMittal) Long products

AcerBrag (Votorantin) Long products

SIPAR (Gerdau Group) Long products

Aceros Zapla (Taselli Group) Long products

SIDERCA (Tenaris – Techint Group) Seamless

pipes

Small producers of rebar and ingots for forging

Argentina: Market protection 8

Ironmaking units

SIDERAR: Blast furnace 1 & 2

ACINDAR: Midrex shaft furnace

SIDERCA: Midrex shaft furnace

Iron ore supply

Brazilian pellets (Minas Gerais & Carajas)

Brazilian lumps (Corumba)

Argentina: Market protection 9

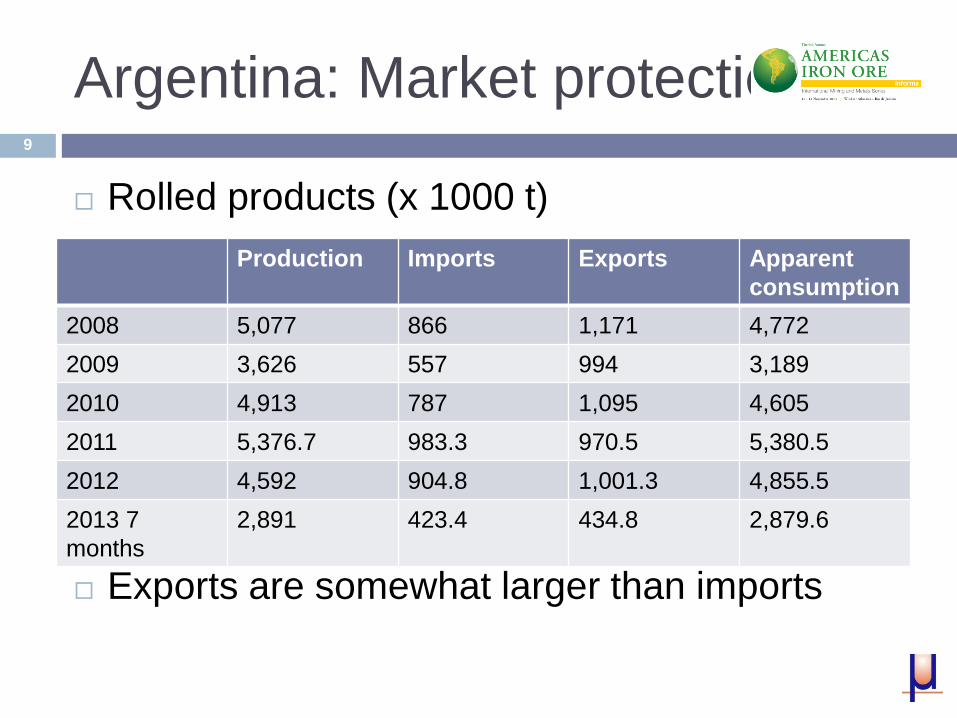

Rolled products (x 1000 t)

Exports are somewhat larger than imports

Production Imports Exports Apparent

consumption

2008 5,077 866 1,171 4,772

2009 3,626 557 994 3,189

2010 4,913 787 1,095 4,605

2011 5,376.7 983.3 970.5 5,380.5

2012 4,592 904.8 1,001.3 4,855.5

2013 7

months

2,891 423.4 434.8 2,879.6

Argentina: Market protection 10

Rolled long products

More imports than exports

Imports: SBQ, heavy shapes

Exports: bar, wire rod

Rolled flat products

More exports than imports just in crisis times

Imports: heavy plate, exposed car body cold rolled, stainless and other special steel strip

Exports: hot and cold rolled carbon steel strip

Seamless pipes

Mostly exported

Argentina: Market protection 11

Steel production oriented to the domestic market, except for seamless pipes

Current investments (driver: substitution of imports)

SIDERAR

RH for ultra low carbon and higher API X grades (in start up)

Second slab caster (in start-up)

Laminados Industriales – Beltrame Group

Heavy plate rolling mill (in start-up)

Announced

Acindar, new rolling mill for rebar, M USD 100

Gerdau, new meltshop (integration of a re-roller)

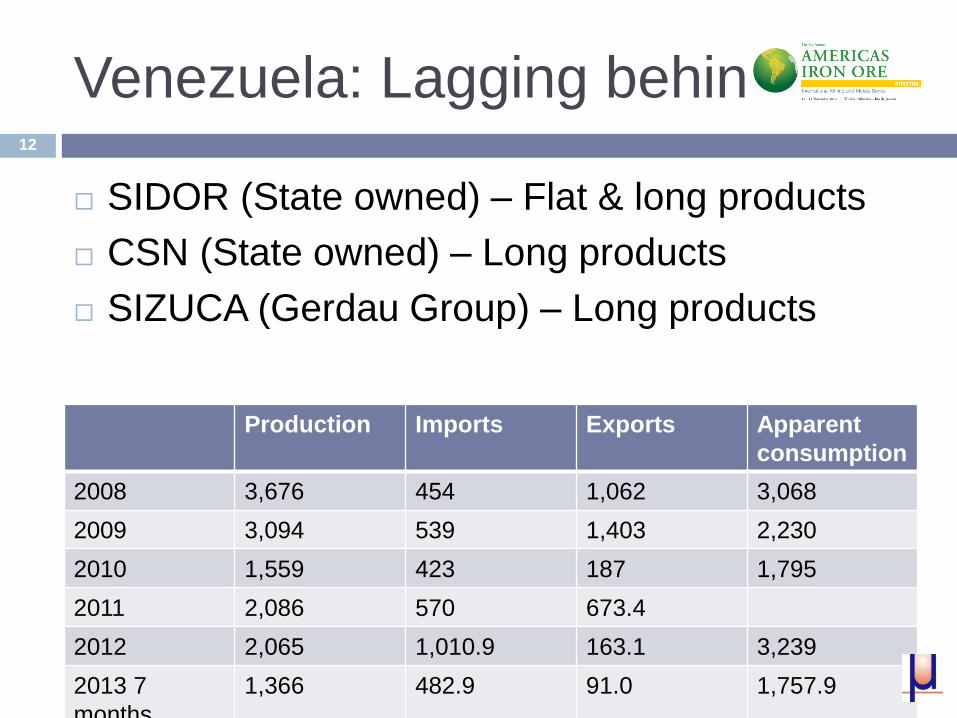

Venezuela: Lagging behind 12

SIDOR (State owned) – Flat & long products

CSN (State owned) – Long products

SIZUCA (Gerdau Group) – Long products

Production Imports Exports Apparent

consumption

2008 3,676 454 1,062 3,068

2009 3,094 539 1,403 2,230

2010 1,559 423 187 1,795

2011 2,086 570 673.4

2012 2,065 1,010.9 163.1 3,239

2013 7

months

1,366 482.9 91.0 1,757.9

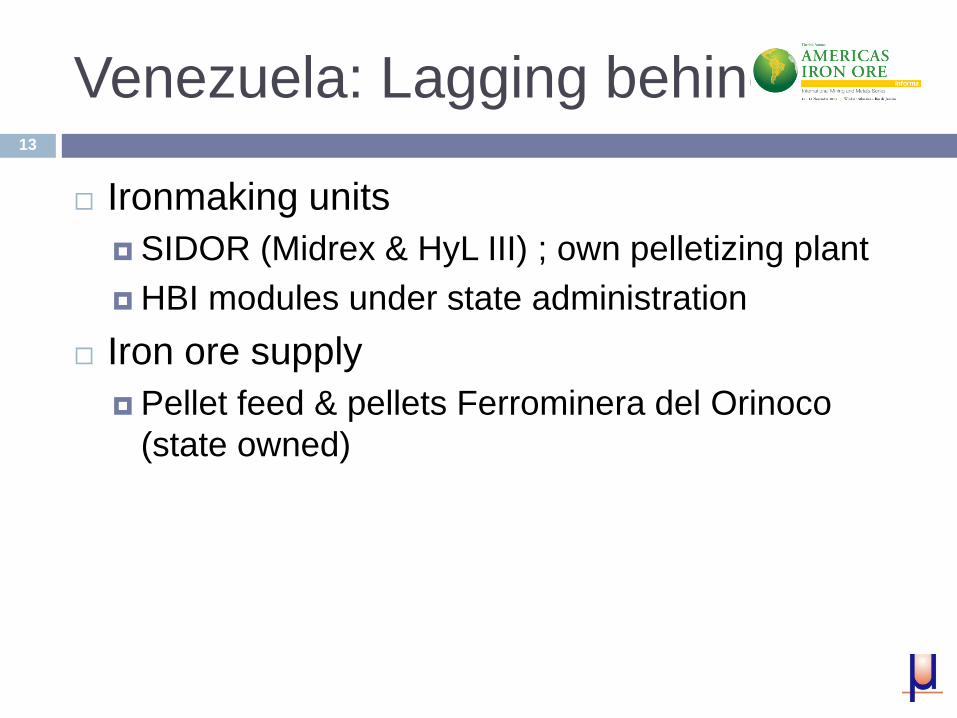

Venezuela: Lagging behind 13

Ironmaking units

SIDOR (Midrex & HyL III) ; own pelletizing plant

HBI modules under state administration

Iron ore supply

Pellet feed & pellets Ferrominera del Orinoco

(state owned)

Venezuela: Lagging behind 14

Rolled products (flat, long, pipes)

Decline after nationalization

Switch to long products

Flat Long Pipes

2008 2,252 1,476 45

2009 1,655 1,436 4

2010 721 838 -

2011 866.1 1,220.3

2012 957 1,108 -

2013 7

months

683 682 -

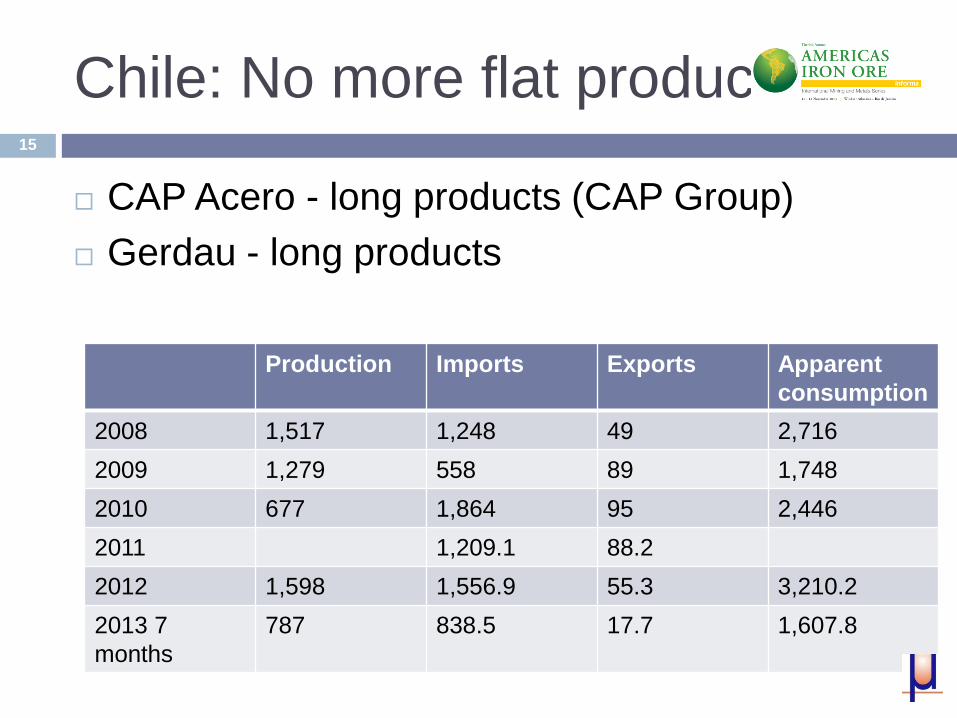

Chile: No more flat products 15

CAP Acero - long products (CAP Group)

Gerdau - long products

Production Imports Exports Apparent

consumption

2008 1,517 1,248 49 2,716

2009 1,279 558 89 1,748

2010 677 1,864 95 2,446

2011 1,209.1 88.2

2012 1,598 1,556.9 55.3 3,210.2

2013 7

months

787 838.5 17.7 1,607.8

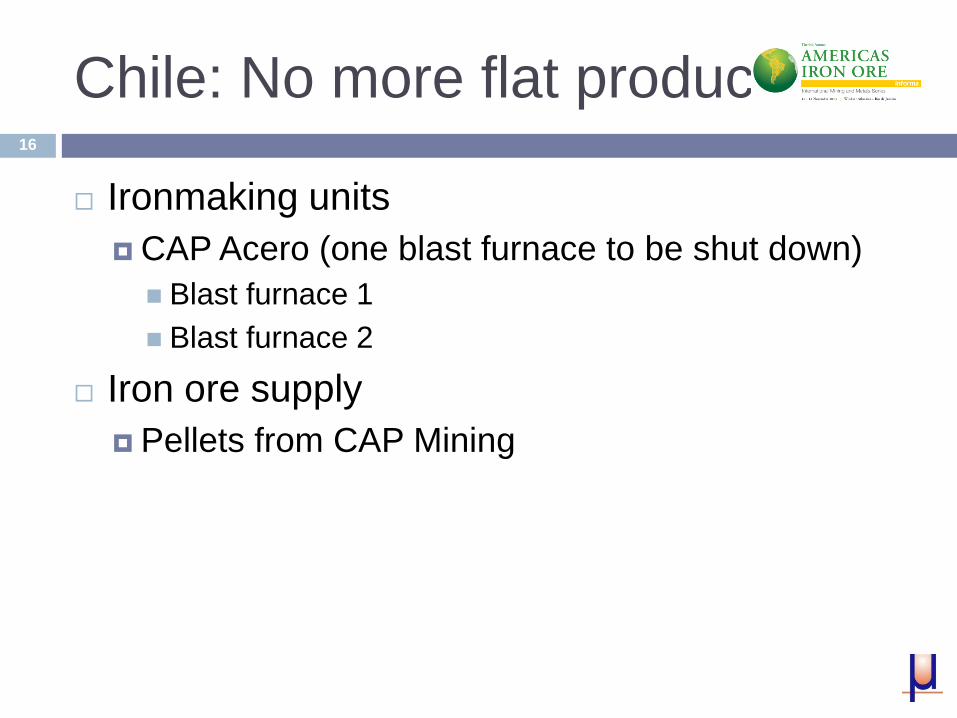

Chile: No more flat products 16

Ironmaking units

CAP Acero (one blast furnace to be shut down)

Blast furnace 1

Blast furnace 2

Iron ore supply

Pellets from CAP Mining

Chile: No more flat products 17

Local steelmakers are far of supplying the

domestic market with their own production

CAP Acero leaving flat products (shut down of

slab caster, hot rolling mill and downstream

facilities

Investment

CAP Acero: billet caster, long products rolling mill

Consequences for iron ore demand

Fall due to imminent shut down of one blast

furnace

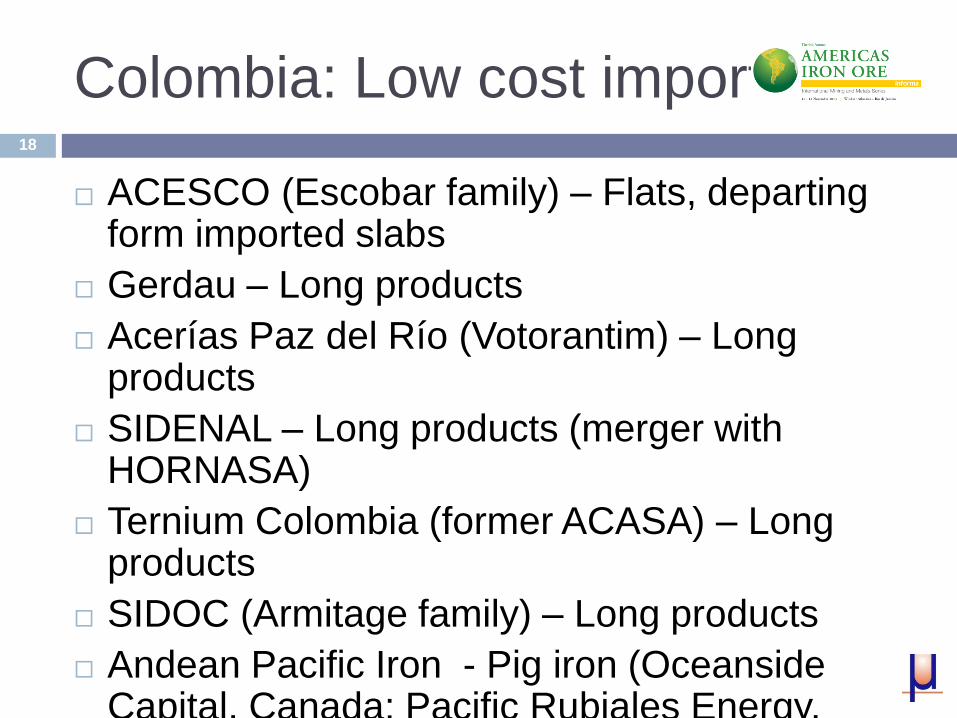

Colombia: Low cost imports 18

ACESCO (Escobar family) – Flats, departing form imported slabs

Gerdau – Long products

Acerías Paz del Río (Votorantim) – Long products

SIDENAL – Long products (merger with HORNASA)

Ternium Colombia (former ACASA) – Long products

SIDOC (Armitage family) – Long products

Andean Pacific Iron - Pig iron (Oceanside Capital, Canada; Pacific Rubiales Energy, Venezuela)

Colombia: Low cost imports 19

Ironmaking units

Acerias Paz del Rio

Mini Blast Furnace

Andean Pacific Iron (Zipaquira)

Mini Blast Furnace 1 in start up

Mini Blast Furnace 2 under construction

Iron ore supply

Acerias Paz del Rio: Minas Paz del Rio (lumps)

Andean Pacific Iron: own mine

Colombia: Low cost imports 20

Production Imports Exports Apparent

consumption

2008 1,435 1,922 158 3,199

2009 1,464 1,280 147 2,597

2010 1,641 1,762 150 3,253

2011 1,779.5 1,981.2 124.5 3,636.2

2012 1,725 1,894.1 101.9 3,721

2013 738 1,095.2 73.5 1,759.7

Colombia: Low cost imports 21

Despite of mergers and acquisitions, still there is a low grade of concentration of the offer, in long products

More imports than production

Industry working at 60% capacity

Heavy losses for Paz del Rio and Gerdau

Investments

CIPROCOLSA – Pig iron project (?)

Ternium Colombia M USD 25

Paz del Rio: decline to invest due to fierce competition of wire rod imports

Peru: Jumping forward? 22

Corporación Aceros Arequipa, Cilloniz family and others, long products

Siderperú, Gerdau Group, long products

Ironmaking units

Two Coal-based DRI rotary kilns, Aceros Arequipa

Mini Blast Furnace in Siderperu: revamped but still idle

Iron ore supply

Shougang Hierroperu, pellets

Aceros Arequipa mines, lumps

Peru: Jumping forward? 23

Growing domestic demand, satisfied with

increased imports, for both flat and long

products Production Imports Exports Apparent

consumption

2008 926 1,289 66 2,149

2009 871 781 111 1,541

2010 1,035 1,476 130 2,381

2011 913.1 1,253.5 124.5 2,022.9

2012 1,211 1,573.1 143.7 2,927.8

2013 7

months

806 981.3 69.6 1,717.7

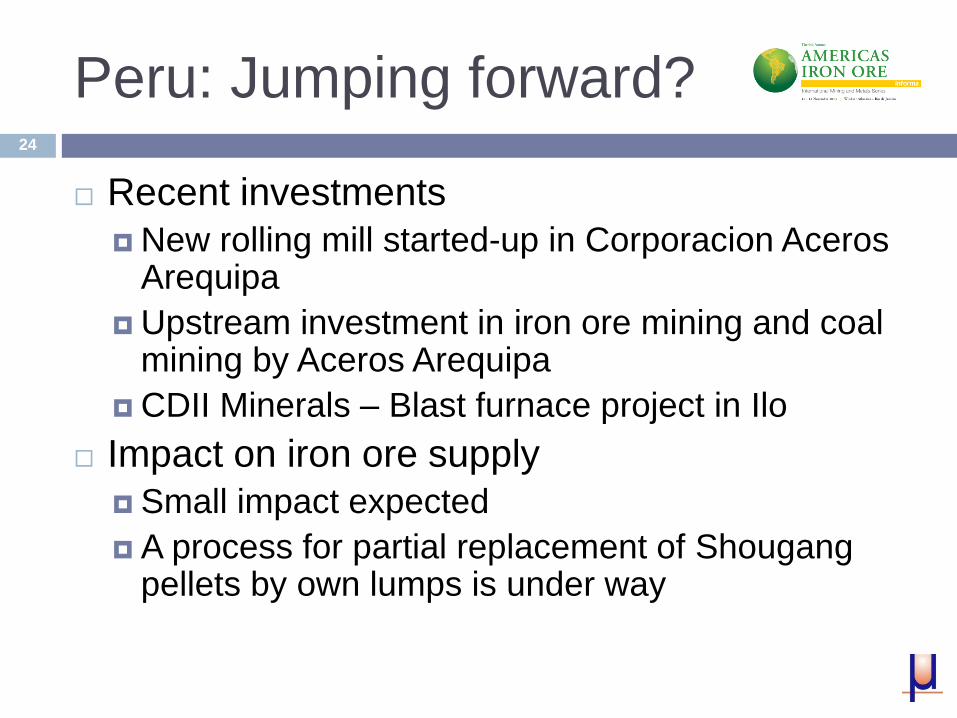

Peru: Jumping forward? 24

Recent investments

New rolling mill started-up in Corporacion Aceros Arequipa

Upstream investment in iron ore mining and coal mining by Aceros Arequipa

CDII Minerals – Blast furnace project in Ilo

Impact on iron ore supply

Small impact expected

A process for partial replacement of Shougang pellets by own lumps is under way

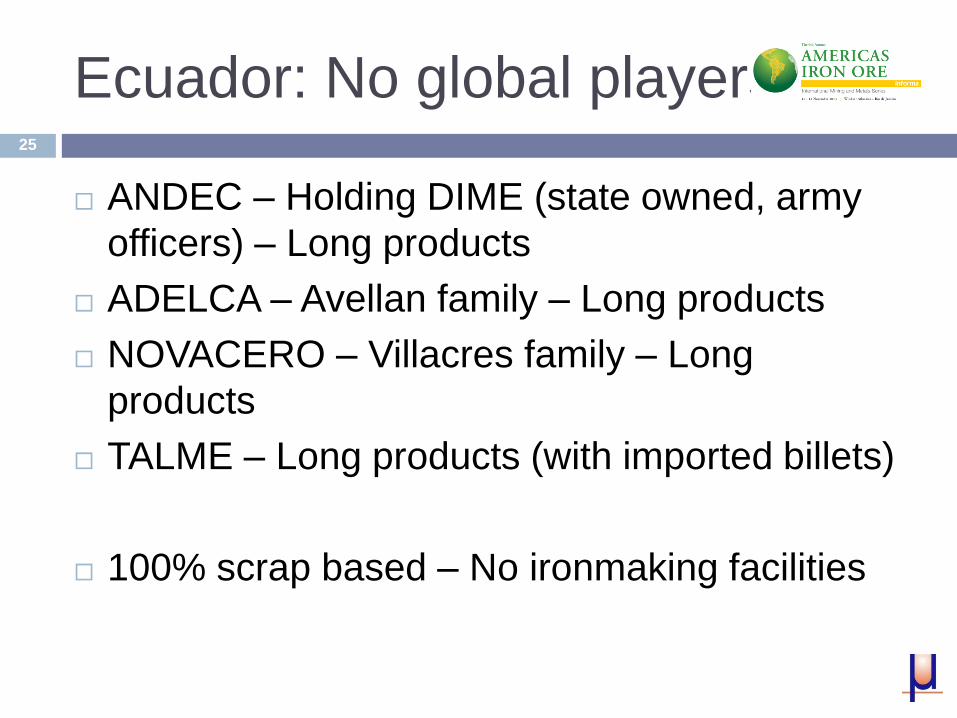

Ecuador: No global players 25

ANDEC – Holding DIME (state owned, army

officers) – Long products

ADELCA – Avellan family – Long products

NOVACERO – Villacres family – Long

products

TALME – Long products (with imported billets)

100% scrap based – No ironmaking facilities

Ecuador: No global players 26

Only long products are produced; no exports

Domestic demand unsatisfied

Recent investments:

Consteel EAF at ANDEC and NOVACERO

3rd continuous casting strand at ANDEC

Consteel EAF at NOVACERO Production Imports Exports App.

Consum.

2008 560 762 - 1,322

2009 442 1,127 - 1,569

2010 500 765 7 1,258

2011 523 974.5 14.7 1,482.8

2012 556 953.9 5.4 1,515.3

2013 7

months

432 702.7 6.9 1,127.8

Smaller markets 27

Paraguay: ACEPAR (Taselli Group) – Long products

2012: 22 Kt

2013: 2 charcoal based blast furnaces idled

Uruguay: LAISA (Gerdau Group) – Long products

2012: Prod. 74 Kt; Imp. 141 Kt; Exp. 1 Kt

Bolivia No local production

No import figures published

LAMINOR starting up in Oruro (Las Lomas Group)

Conclusions 28

Two different worlds Pacific countries

No protection for the industry

Unrestricted imports

Industry below capacity while importing more than is produced locally

Iron ore exported to China, then steel imported from China (Chile, Peru)

Argentina Strong protection of the industry

Pressure for substitution of imports

Venezuela Far from realizing its potential as a steelmaking country

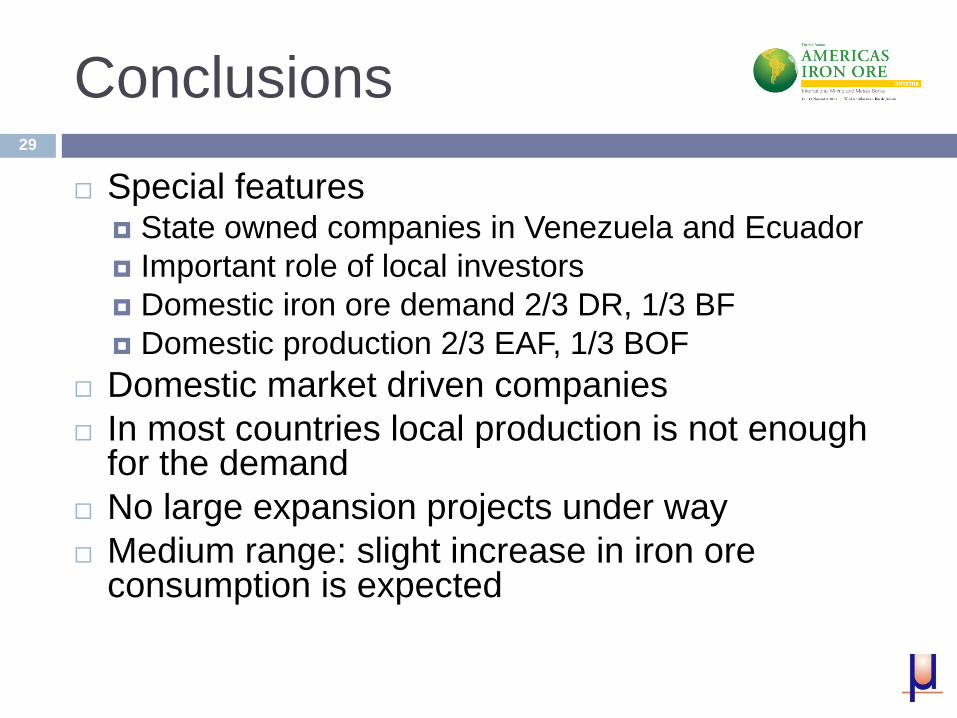

Conclusions 29

Special features State owned companies in Venezuela and Ecuador

Important role of local investors

Domestic iron ore demand 2/3 DR, 1/3 BF

Domestic production 2/3 EAF, 1/3 BOF

Domestic market driven companies

In most countries local production is not enough for the demand

No large expansion projects under way

Medium range: slight increase in iron ore consumption is expected