joint eccb and ifrs foundation regional train the...

TRANSCRIPT

Joint ECCB and IFRS Foundation

Regional Train the Trainer Workshop for the Non-banking Financial Institutions

hosted by the ECCB funded by the World Bank

Monday 25 to Friday 29 February 2013

St Kitts and Nevis

Joint ECCB and IFRS Foundation Regional Train the Trainer Workshop for the Non-banking Financial Institutions

hosted by the ECCB and funded by the World Bank

Monday 25 to Friday 29 February 2013 St Kitts and Nevis

Day 1 Day 2 Day 3 Day 4 (morning) Day 5 Framework-based

Understanding of IFRSs (main principles and estimates and judgements to apply)

Framework-based Understanding of IFRSs (main principles and estimates and judgements to apply)

Accounting for Financial Instruments in accordance with IFRSs

IASB’s project to improve accounting for financial instruments

A former banking and insurance CFO’s experience

08:30

Introduction ECCB

Overview of non-financial liabilities MW

Presenting financial instruments in accordance with IAS 32 DS

IASB’s project to replace IAS 39 DS

Regulatory filings DS

09:00

The Conceptual Framework MW

10:00 Tea Tea Tea Tea Tea 10:30 Quiz and discussion

MW Overview of non-financial liabilities continued MW

Accounting for financial instruments in accordance with IFRS 9 and IAS 39 continued DS

IASB’s project to replace IAS 39 DS

Regulatory filings DS

11:30 Overview of non-financial assets MW

Overview of reporting financial performance MW

Quiz and discussion DS

Questions from the audience and discussion DS

12:30 Lunch Lunch Lunch Lunch Lunch

1

Day 1 Day 2 Day 3 Day 4 Day 5 Framework-based

Understanding of IFRSs (main principles and estimates and judgements to apply)

Framework-based Understanding of IFRSs (main principles and estimates and judgements to apply)

Accounting for Financial Instruments in accordance with IFRSs

Accounting for Insurance Contracts in accordance with IFRSs

External audit standards and practices for NBFIs

13:30 Overview of non-financial assets MW

Overview of business combinations and consolidated financial statements in accordance with IFRSs MW

Quiz and discussion DS

Accounting for insurance contracts in (IFRS 4) DS

RJ

14:30 Overview of display related IFRSs MW

Disclosing financial instruments (IFRS 7) DS

15:30 Tea Case study and discussion Open Safari’s functional currency and its presentation currency MW

Tea Tea Tea

16:00 The Open Safari case study and discussion MW

Tea Quiz and discussion DS

IASB’s Insurance Contracts project DS

RJ

16:30 DG

17:00 Quiz and discussion DS

RJ

18:00 Close Close Close Close Close KEY: DG: Dave Grace DS: Darrel Scott, IASB member RJ: Rubin John, KPMG partner MW: Michael Wells, IASB staff

2

Joint ECCB and IFRS Foundation Regional Train the Trainer Workshop for the

Non-banking Financial Institutions

Monday 25 to Friday 29 February 2013 St Kitts and Nevis

Introduction by the ECCB

3

4

Joint ECCB and IFRS Foundation Regional Train the Trainer Workshop for the

Non-banking Financial Institutions

Monday 25 to Friday 29 February 2013 St Kitts and Nevis

Day 1

5

6

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Conceptual Framework

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Joint ECCB and IFRS Foundation workshopwith the support of a World Bank financed project

Michael Wells, Director, IFRS Education Initiative, IASB

22

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The requirements are set out in International Financial Reporting Standards (IFRSs), as issued by the IASB at 1 January 2013 with an effective date after 1 January 2013 but not the IFRSs they will replace.Disclaimer: The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for any loss caused by acting or refraining from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.

33

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• relates IFRS requirements to the concepts in the Conceptual Framework

• reasons why some IFRS requirements do not maximise those concepts (eg application of the cost constraint or inherited requirements)

Concepts PrinciplesRules

Framework-based understanding… 44

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Yes, the starting point for understanding all IFRS information is the objective and the concepts that flow logically from that objective:– IASB uses Framework to set IFRSs– Teachers/Trainers use Framework-based teaching

to prepare students to make judgements that are necessary to apply IFRSs

– Preparers use Framework to make the judgements that are necessary to apply IFRSs

– Auditors and regulators assess those judgements– Investors, lenders and others consider those

judgements when using IFRS financial information to inform their decisions

Does the Framework help me understand IFRSs?

55

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Framework sets out agreed concepts that underlie IFRS financial reporting– the objective of general purpose financial

reporting– qualitative characteristics– elements of financial statements– recognition– measurement– presentation and disclosure

Other concepts all flow from the objective

The IASB’s Conceptual Framework 66

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

“Provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity.”

Those decisions involve buying, selling or holding equity and debt instruments, and providing or settling loans or other forms of credit

Objective of financial reporting

7

77

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Primary users – provide resources, but cannot demand

information – common information needs

• Assess the prospects for future net cash inflows– buy, sell, hold– efficient and effective use of resources

Objective of financial reporting 88

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Relevance– predictive value– confirmatory value– materiality, entity-specific

• Faithful representation (replaces reliability)

– completeness– neutrality– free from error

Fundamental qualitative characteristics

99

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

A large listed profitable manufacturer• financial statements in millions of CUs • recognises individual items of PPE that cost

less than CU1,000 as an expense on initial recognition

• In 20X1 this policy resulted in CU100,000 being recognised as an expense

Does the Entity’s policy contravene IFRSs?

Example: materiality 10Enhancing Qualitative Characteristics

• Comparability: like things look alike; different things look different

• Verifiability: knowledgeable and independent observers could reach consensus, but not necessarily complete agreement, that a depiction is a faithful representation

• Timeliness: having information available to decision-makers in time to be capable of influencing their decisions

• Understandability: Classify, characterise, and present information clearly and concisely

10

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

1111

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Objective• Concepts including qualitative characteristics

– faithful representation– comparability

• Principles – Prior period error: retrospective restatement– Change in policy: retrospective application– Change in estimate: prospective application

• Rules– impracticable exception– specified disclosures

Examples:errors and changes in policies and estimates 1212

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Cost – IASB assesses whether the benefits of reporting

particular information are likely to justify the costs incurred to provide and use that information.

Note: It is consistent with the Framework for an IFRS requirement not to maximise the objective of financial reporting when the costs of doing so would exceed the benefits.

Pervasive constraint

8

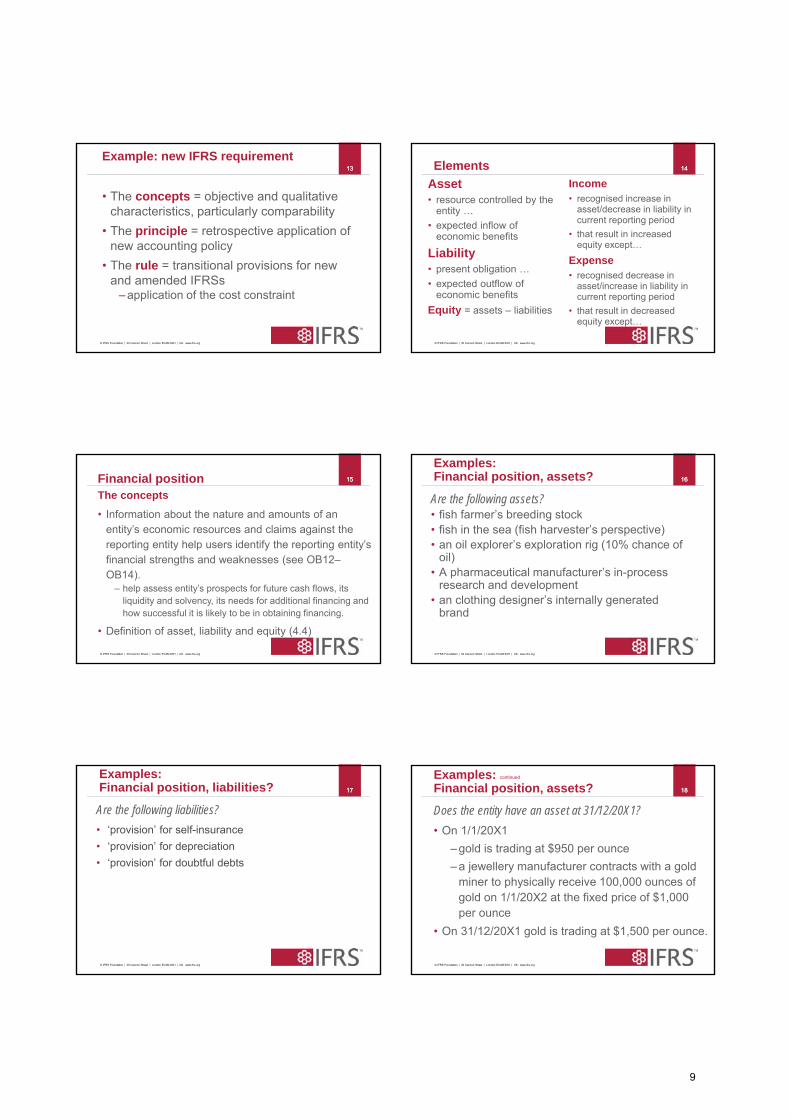

1313

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• The concepts = objective and qualitative characteristics, particularly comparability

• The principle = retrospective application of new accounting policy

• The rule = transitional provisions for new and amended IFRSs

– application of the cost constraint

Example: new IFRS requirement1414

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Asset• resource controlled by the

entity …• expected inflow of

economic benefits

Liability • present obligation … • expected outflow of

economic benefitsEquity = assets – liabilities

Income• recognised increase in

asset/decrease in liability in current reporting period

• that result in increased equity except…

Expense• recognised decrease in

asset/increase in liability in current reporting period

• that result in decreased equity except…

Elements

1515

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The concepts

• Information about the nature and amounts of an entity’s economic resources and claims against the reporting entity help users identify the reporting entity’s financial strengths and weaknesses (see OB12–OB14).

– help assess entity’s prospects for future cash flows, its liquidity and solvency, its needs for additional financing and how successful it is likely to be in obtaining financing.

• Definition of asset, liability and equity (4.4)

Financial position 1616

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Are the following assets?• fish farmer’s breeding stock• fish in the sea (fish harvester’s perspective)• an oil explorer’s exploration rig (10% chance of

oil)• A pharmaceutical manufacturer’s in-process

research and development• an clothing designer’s internally generated

brand

Examples:Financial position, assets?

1717

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Are the following liabilities?• ‘provision’ for self-insurance• ‘provision’ for depreciation• ‘provision’ for doubtful debts

Examples:Financial position, liabilities? 1818

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Does the entity have an asset at 31/12/20X1?• On 1/1/20X1

– gold is trading at $950 per ounce– a jewellery manufacturer contracts with a gold

miner to physically receive 100,000 ounces of gold on 1/1/20X2 at the fixed price of $1,000 per ounce

• On 31/12/20X1 gold is trading at $1,500 per ounce.

Examples: continued

Financial position, assets?

9

1919

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Does the entity have a liability at 31/12/20X1?• on 01/01/20X2 an entity declared a final dividend for

the year ended 31/12/20X1.• At 31/12/20X1 an entity expects to undertake major

maintenance of its manufacturing plant in 20X9. • due to extraordinarily high snowfall in 20X1 a snow ski

operator received higher than average revenue for 20X1. Management wants to recognise a liability (and expense in 20X1) for the anticipated effects of expected future warmer years.

Examples:Financial position, liabilities? 2020

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Does the entity have equity, liability or part equity and part liability?• non-controlling shareholders own 25% of the equity of a

subsidiary.• an entity issues a 3-year term convertible bond for

CU1,000 (= par = face value). Interest is payable at 6% pa. The bond is convertible at any time up to maturity into 250 ordinary shares. When the bonds are issued, the prevailing market interest rate for similar debt without conversion options is 9%.

Examples:Financial position, equity or liability?

2121

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Concepts

• Information about an entity’s financial performance (particular changes in its economic resources and claims) helps users understand the return that the entity has produced on its economic resources and is usually helpful in predicting the entity’s future returns on its economic resources (see OB16)

• Definition of income and expense (see 4.25)

Financial performance the concepts 2222

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Accrual basis of accounting (the concepts)– depicts the effects of transactions and other events

and circumstances on a reporting entity’s economic resources and claims in the periods in which those effects occur (see OB17)

– financial performance during a period, reflected by changes in its economic resources and claims other than by obtaining additional resources directly from investors and creditors, is useful in assessing the entity’s past and future ability to generate net cash inflows (see OB18)

Recognition the concepts

2323

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Recognise item that meets element definition when– probable that benefits will flow to/from the entity– has cost or value that can measured reliably

(see 4.38)

• Accrual basis of accounting (the principle)– recognise elements (eg asset) when they satisfy the

definition and recognition criteria (see IAS1.28)

• Applying the principle (see individual IFRSs)

What does probable mean?

Recognition principle and rules 2424

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Recognise the asset?• a hospital’s backup backup generator (expect

never to use)• advertising expenditure • research and development expenditure • internally generated brand• lessee—short-term car rental agreement• firm order to acquire gold, cannot settle net

Examples: asset recognition

10

2525

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• The unit of account is the level at which an asset is aggregated or disaggregated for recognition purposes.

• Most IFRS do not prescribe the unit of account therefore judgement is required in applying recognition criteria to an entity’s specific circumstances. For example:

– individually insignificant items, such as moulds, tools and dies may be aggregated when applying the recognition criteria in IAS 16.

– cows would usually be recognised individually whereas bees would usually be recognised as a swarm when applying IAS 41.

Unit of account for recognition 2626

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Measurement is the process of determining monetary amounts at which elements are recognised and carried. (4.54)

• To a large extent, financial reports are based on estimates, judgements and models rather than exact depictions. The Framework establishes the concepts that underlie those estimates, judgements and models (OB11)

• IASB guided by objective and qualitative characteristics when specifying measurements.

Measurement concepts

2727

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Derecognition of an asset refers to when an asset previously recognised by an entity is removed from the entity’s statement of financial position

– derecognition requirements are specified at the standards level.

– derecognition does not necessarily occur when the asset no longer satisfies the conditions specified for its initial recognition (ie derecognition does not necessarily coincide with the loss of control of the asset )

• IASB guided by objective, qualitative characteristics and elements

Derecognition of assets 2828

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Objective of financial reporting• Presentation: financial statements portray financial

effects of transactions and events by:– grouping into broad classes (the elements, eg asset) – sub-classify elements (eg assets sub-classified by their

nature or function in the business)

• IAS 1– application of IFRSs with additional disclosures when

necessary results in a fair presentation (faithful representation of transactions, events and conditions)

– don’t offset assets & liabilities or income & expenses

Presentation and disclosure

2929

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• a cohesive understanding of IFRSs – Framework facilitates consistent and logical

formulation of IFRSs

• a basis for judgement in applying IFRSs – Framework established the concepts that underlie

the estimates, judgements and models on which IFRS financial statements are based

• a basis for continuously updating IFRS knowledge and IFRS competencies

Framework-based understanding provides… 3030

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Does the Framework help me apply IFRSs?• Yes, Framework is in IAS 8 hierarchy (see next

slide) – Preparers use the Framework to make the

judgements that are necessary to apply IFRSs– Auditors and regulators assess those

judgements– Investors, lenders and others consider those

judgements when using IFRS financial information to inform their decisions

Framework’s role in applying IFRSs

11

3131

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Use judgement to– develop a policy that results in relevant

information that faithfully represents (ie complete, neutral and error free)

– Hierarchy: 1st IFRS dealing with similar and related issue2nd Framework definitions, recognition crit. etc Can also in parallel refer to GAAPs with similar Framework

If no specific IFRS requirement 3232

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Framework-based approach would ask:• What is the economics of the phenomenon (eg

transaction or event)?• What relevant information using the accrual

basis of accounting faithfully present that economic phenomenon to inform decisions of investors and lenders (potential and existing)?

• Is there anything in IFRSs that prevents me from providing that information?

In other words, if no IFRS requirement…

3333

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Before IFRIC 17, entity distributes non-cash asset (eg land or shares in another) whose fair value = CU1 mill. Carrying amount of asset = cost = CU1K

• Economics = reduce owners’ claims against the entity by distributing to them an asset worth CU1 million.

• Relevant information for investors and lenders that faithfully represents the economics: – investors received CU1 million refund of capital. – value of assets available to meet lenders’ claims

reduced by CU1 million.

Example 5: non-cash distribution 34Example 5: non-cash distribution

Before IFRIC 17, entity distributes non-cash asset (eg land or shares in another) whose fair value = CU1 mill. Carrying amount of asset = cost = CU1K

• Economics = reduce owners’ claims against the entity by distributing to them an asset worth CU1 million.

• Relevant information for investors and lenders that faithfully represents the economics: – investors received CU1 million refund of capital. – value of assets available to meet lenders’ claims

reduced by CU1 million.

34

3535

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Before IFRIC 17… (continued)• Does IFRSs prevent providing that information?

No. Therefore:– recognise CU999K income (previously

unrecognised increase in the value of the asset derecognised).

– recognise CU1 million distribution to owners.

Example 5: non-cash distribution 3636

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Before IFRS 2, entity pays employee in own shares. Par value of shares issued = CU1K. Fair value of services provided = CU1 million = fair value of shares.

• Economics = entity paid employees CU1 million for services. Employees invested CU1 million in entity.

• Relevant information for investors and lenders that faithfully represents the economics:– CU1 million services received = staff cost.– CU1 million invested = increased owner equity.

• Does IFRSs prevent providing that information? No. Therefore, recognise CU1 million expense and recognise CU1 million increase in owners’ equity.

Example 6: share-based payment

12

3737

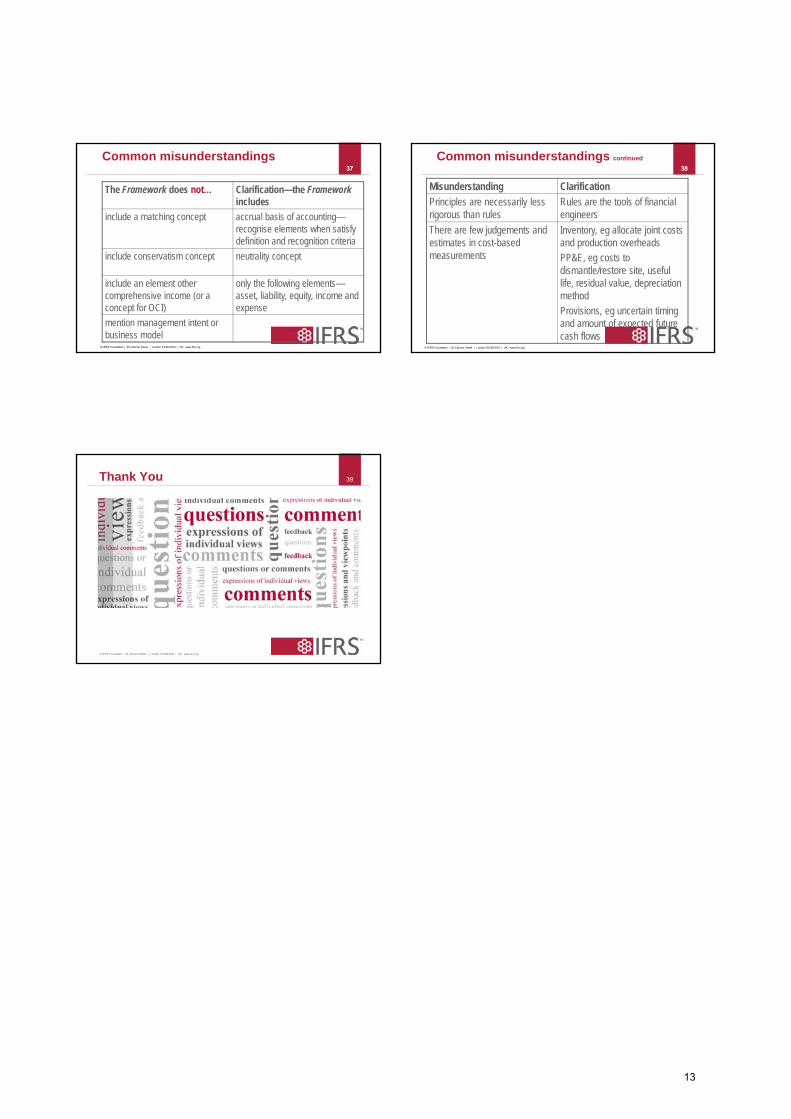

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The Framework does not… Clarification—the Frameworkincludes

include a matching concept accrual basis of accounting—recognise elements when satisfy definition and recognition criteria

include conservatism concept neutrality concept

include an element other comprehensive income (or a concept for OCI)

only the following elements—asset, liability, equity, income and expense

mention management intent or business model

Common misunderstandings3838

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Misunderstanding Clarification

Principles are necessarily less rigorous than rules

Rules are the tools of financial engineers

There are few judgements and estimates in cost-based measurements

Inventory, eg allocate joint costs and production overheadsPP&E, eg costs to dismantle/restore site, useful life, residual value, depreciation methodProvisions, eg uncertain timing and amount of expected future cash flows

Common misunderstandings continued

39

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Thank You

13

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

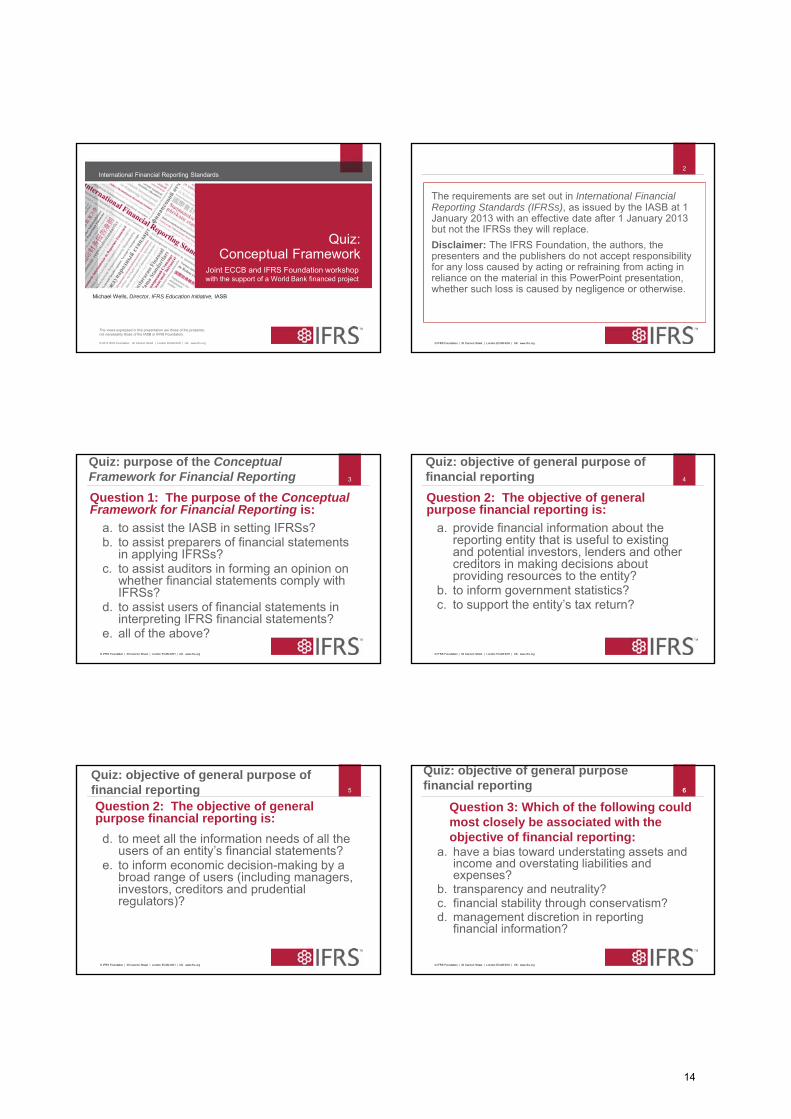

Quiz:Conceptual Framework

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Joint ECCB and IFRS Foundation workshopwith the support of a World Bank financed project

Michael Wells, Director, IFRS Education Initiative, IASB

2

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The requirements are set out in International Financial Reporting Standards (IFRSs), as issued by the IASB at 1 January 2013 with an effective date after 1 January 2013 but not the IFRSs they will replace.Disclaimer: The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for any loss caused by acting or refraining from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.

3

Quiz: purpose of the Conceptual Framework for Financial ReportingQuestion 1: The purpose of the Conceptual Framework for Financial Reporting is:

a. to assist the IASB in setting IFRSs?b. to assist preparers of financial statements

in applying IFRSs?c. to assist auditors in forming an opinion on

whether financial statements comply with IFRSs?

d. to assist users of financial statements in interpreting IFRS financial statements?

e. all of the above?© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

4

Quiz: objective of general purpose of financial reporting

Question 2: The objective of general purpose financial reporting is:

a. provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity?

b. to inform government statistics?c. to support the entity’s tax return?

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

5

Quiz: objective of general purpose of financial reportingQuestion 2: The objective of general purpose financial reporting is:

d. to meet all the information needs of all the users of an entity’s financial statements?

e. to inform economic decision-making by a broad range of users (including managers, investors, creditors and prudential regulators)?

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

66

Quiz: objective of general purpose financial reporting

Question 3: Which of the following could most closely be associated with the objective of financial reporting:

a. have a bias toward understating assets and income and overstating liabilities and expenses?

b. transparency and neutrality?c. financial stability through conservatism?d. management discretion in reporting

financial information?

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

14

77

Quiz: fundamental qualitative characteristics

Question 4: The fundamental qualitative characteristics are:

a. comparability and relevance?b. relevance and reliability?c. relevance, reliability and comparability?d. relevance and faithful representation?e. comparability, relevance and faithful

representation?

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

88Quiz: qualitative characteristics

Question 5: verifiability means knowledgeable and independent observers:

a. would reach complete agreement that a depiction is a faithful representation?

b. cannot reach consensus that a depiction is a faithful representation?

c. could reach consensus, but not necessarily complete agreement, that a depiction is a faithful representation?

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

99Quiz: qualitative characteristics

Question 6: which statement/s are true?a. Relevance is a fundamental qualitative

characteristic.b. Financial information without both

relevance and faithful representation is not useful.

c. Financial information without both relevance and faithful representation cannot be made useful by being more comparable, verifiable, timely or understandable.

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

1010Quiz: qualitative characteristics

Question 6: which of the statements below are true?d. Financial information that is relevant and

faithfully represented may still be useful even if it does not have any of the enhancing qualitative characteristics

e. All of the above statements.f. None of the above statements.

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

1111Quiz: recognition

Question 7: Expenses are recognised in comprehensive income (profit or OCI):a. using the matching basis—on the basis of

a direct association between the costs incurred and the earning of specific items of income?

b. using the accrual basis—items are recognised as assets, liabilities, equity, income or expenses when they satisfy the definitions and recognition criteria for those items?

c. at the discretion of management?© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

12Quiz: uncertain future cash flows

Question 8: Recognition criteria determine when to recognise an item.Measurement is determining the monetary amounts at which to measure an item. Uncertainties about the extent of future cash flows:

12

a. only affect the decision about whether to recognise?

b. only affect the estimation of the amount at which to measure the item?

c. could affect both recognition and measurement?

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

15

13Quiz: measurement

Question 9: How many measurement bases does IFRSs specify for the measurement of assets?

13

a. one—historical costb. one—fair value c. two—historical cost and fair valued. many—including historical cost, fair value,

value in use, estimated selling price less costs to complete and sell, etc

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

14

Quiz: status of Conceptual Framework

Question 10: the Conceptual Framework:

14

a. is an IFRS?b. overrides all other IFRS requirements?c. does not define standards for any particular

measurement or disclosure issue?d. is in the hierarchy that management must in

the absence of a specific IFRS requirement apply in developing an accounting policy that results in information that is relevant and reliable?

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

15

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Thank You

16

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Non-financial asset

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Joint ECCB and IFRS Foundation workshopwith the support of a World Bank financed project

Michael Wells, Director, IFRS Education Initiative, IASB

22

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The requirements are set out in International Financial Reporting Standards (IFRSs), as issued by the IASB at 1 January 2013 with an effective date after 1 January 2013 but not the IFRSs they will replace.Disclaimer: The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for any loss caused by acting or refraining from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation

Classifying non-financial assets

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

44

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Objective of financial reporting• Financial statements portray financial effects of

transactions and events by:– grouping into broad classes (the elements, eg asset) – sub-classify elements (eg assets sub-classified by their

nature or function in the business)

• IAS 1– application of IFRSs with additional disclosures when

necessary results in a fair presentation (faithful representation of transactions, events and conditions)

– don’t offset assets & liabilities or income & expenses

Classification concepts

55

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Information about the nature and amounts of a reporting entity’s economic resources and claims can help users to identify the reporting entity’s financial strengths and weaknesses.

• That information can help users to: – assess the reporting entity’s liquidity and

solvency – its needs for additional financing and how

successful it is likely to be in obtaining that financing.

(CF.OB13)

Classification concepts—assets and claims 66

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Different types of economic resources affect a user’s assessment of the reporting entity's prospects for future cash flows differently.

– Some future cash flows result directly from existing economic resources (eg accounts receivable and investment property).

– Other cash flows result from using several resources in combination to produce and market goods or services to customers (eg PPE and intangible assets). Although those cash flows cannot be identified with individual economic resources (or claims), users of financial reports need to know the nature and amount of the resources available for use in a reporting entity’s operations. (CF.OB14)

Classification concepts—assets

17

77

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Different assets exhibit different characteristics (nature) and can be put to a variety of uses (use) in order to generate future economic benefits

• Nature and use determine the classification of assets• IFRS defines a number of assets• For some assets significant judgement is required to

determine their classification

Classification of assets 88

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

ASSET TYPE USE IN BUSINESS ? FORM OF FUTURE ECONOMIC BENEFITS

Inventory (IAS 2) Sale or used in production of items for sale or in services

Usually cash or other asset received in exchange

PPE (IAS 16) Used in production or supply of goods or services, rental or administration (more than one period)

Usually cash through sale of ‘final’ product or service

Intangibles (IAS 38) Used in production or supply of goods or services

Usually cash through sale of ‘final’ product or service

Investment property IAS 40)

Earn rentals or capital appreciation

Usually cash inflows independent from other assets

Biological assets in agricultural activity(IAS 41)

managing biological transformation and harvest for sale or for conversion into agricultural produce or into additional biological assets

Usually cash inflows through sale of harvested produce or progeny

Non-financial asset classifications

99

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Definition

• Inventories are assets:• held for sale in the ordinary course of business;• in the process of production for sale; or• materials or supplies to be used in the production

for sale.

Definition of inventory (IAS 2) 1010

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Definition

• Property, plant and equipment (PPE) are tangible items that are

• held for use in the production or supply of goods or services, for rental to others, or for administration purposes; and

• are expected to be used during more than one period.

Definition of property, plant and equipment (IAS 16)

1111

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Intangible assets

• Management intention relating to intangible assets is similar to that of property, plant and equipment (ie to be used to generate future economic benefits as part of a production process or the provision of services for a period in excess of one year).

• An intangible asset is an identifiable non-monetary asset without physical substance. Such an asset is identifiable when it is separable, or when it arises from contractual or other legal rights.

Definition of intangible assets (IAS 38) 1212

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• It is sometimes difficult to assess whether an internally generated intangible asset qualifies for recognition because of problems in:

a. identifying whether and when there is an identifiable asset that will generate expected future economic benefits; and

b. determining the cost of the asset reliably. In some cases, the cost of generating an intangible asset internally cannot be distinguished from the cost of maintaining or enhancing the entity's internally generated goodwill or of running day-to-day operations.

• Therefore, special requirements in addition to the general requirements for recognition of an internally generated intangible asset apply.

Recognition of intangible assets (IAS 38)

18

1313

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Expenditure on particular internally generated intangible assets must be recognised as an expense when incurred (eg research activities—the original and planned investigation undertaken with the prospect of gaining new scientific or technical knowledge and understanding.

Recognition of research costs(IAS 38) 1414

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

An intangible asset arising from the development phase of an internal project must be recognised if, and only if, an entity can demonstrate all of the following: a. the technical feasibility of completing the intangible asset so that

it will be available for use or sale.b. its intention to complete the intangible asset and use or sell it.c. its ability to use or sell the intangible asset.d. how the intangible asset will generate probable future economic

benefits. Among other things, the entity can demonstrate the existence of a market for the output of the intangible asset or the intangible asset itself or, if it is to be used internally, the usefulness of the intangible asset.

e. the availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset.

f. its ability to measure reliably the expenditure attributable to the intangible asset during its development.

Recognition of development cost(IAS 38)

1515

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Definition• Investment property is land or a building

(including part of a building) or both, held to earn rentals or for capital appreciation or both.

• It is neither owner-occupied (see IAS 16 Property, Plant and Equipment) nor held for sale in the ordinary course of business (see IAS 2 Inventories).

Definition of investment property (IAS 40) 1616

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Sometimes it is difficult to identify investment property. In such cases an entity develops criteria so that it can exercise that judgement consistently

• eg, owner of a hotel transfers some responsibilities to third parties under a management contract (PPE or investment property?)

Judgements and estimates (IAS 40)

1717

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• IAS 41 specifies the accounting for: • biological assets (living plant or animal) whose

biological transformation (growth, degeneration, production and procreation) and harvest is managed by an entity for sale or for conversion into agricultural produce or into additional biological assets (ie agricultural activity); and

• agricultural produce up to the point of harvest. • It does not address the processing of agricultural

produce after harvest (eg processing grapes into wine, or wool into yarn).

Introduction (IAS 41) 1818

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Biological assets that are attached to land (eg trees in a plantation forest) are classified separately from the land. If owner-occupied the land is property accounted for in accordance with IAS 16.

Classification (IAS 41)

19

1919

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

IAS 41 Agriculture 2020

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• It can be difficult to determine whether particular biological assets are engaged in agricultural activity and therefore in the scope of IAS 41—eg the breeding stock of an exotic bird breeding zoo.

Judgements and estimates (IAS 41)

2121

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• A non-current asset is classified as ‘held for sale’ if its carrying amount will be recovered principally through a sale transaction, rather than through continuing use (paragraph 6).

• To be classified as a non-current asset held for sale:

• The asset must be available for immediate sale in its present condition (subject only to terms that are usual and customary for sales of such assets).

• The sale must be highly probable (appropriate management commitment, actively seeking a buyer, reasonable price, 12 month limit).

Non-current Assets Held for Sale (IFRS 5) 2222

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Which IFRS applies to the following assets? • a bird breeder’s birds• a non-breeding zoo’s birds• a breeding zoo’s birds• a vintner’s grape bearing vines, harvested grapes,

partially fermented wine and mature bottled wine• a mushroom farmer’s mushrooms• a farmer’s cattle (breeding stock) and tractor used

to transport feed to the herd• gold

Assets—classification examples

2323

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Which IFRS applies to the following assets? • a property trader’s (ie it buys property to sell it

at a profit near-term) land• a licence trader’s transferable taxi licences• an entity owns digital films and audio

recordings which it licenses to its customers• a manufacturer’s lubricants—expected to be

consumed by its machines in producing goods • Entity B buys a building to earn rentals under

an operating lease from Entity A (its parent). The parent sells its products from the building

Assets—classification examples 2424

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Which IFRS applies to the hotel building? • An entity operates a hotel from a building it

owns– it rents out hotel rooms for short-stays– guest services included in the room rate =

breakfast and television– services charged for separately = other

meals, room bar, gymnasium facilities & guided tours

Assets—classification examples continued

20

2525

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

– when unclear what purpose of acquiring property is (inventories, IP or PP&E?)

– when property owner provide ancillary services to the occupants of a property (IP or PP&E?)

– mixed use property (IP or PP&E?)– when is undue cost or effort necessary to

measure the fair value of an IP on an ongoing basis (IP or PP&E?)

Examples of classification judgementsInternational Financial Reporting Standards

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation

Measurement

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

2727

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Measurement is the process of determining the monetary amounts at which the recognisedelements are carried.

• Many measurements for assets in IFRS, eg:– cost-based measures (eg historical cost and

depreciated historical cost)– fair value– other (eg net realisable value and value in use).

• IFRS measurements are largely based on estimates, judgements and models.

• Most IFRS measures require significant estimates and judgements.

MeasurementInternational Financial Reporting Standards

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation

Cost

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

Cost-based IFRS measures 29

• Few things measured at historical cost – unimpaired land (IAS 16 + IAS 40 cost model)– unimpaired indefinite life intangibles (IAS 38)– unimpaired inventories (IAS 2)

• Cost-based measures are more common– unimpaired depreciated historic cost (IAS 16)– unimpaired amortised historical cost (IAS 38)– amortised cost (IFRS 9) Impairment changes to a fair value or other measure

29

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

3030

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• The cost of an item is: – the amount of cash or cash equivalents

paid; or– the fair value of the other consideration

given to acquire an asset at the time of its acquisition or construction; or

– where applicable, the amount attributed to that asset when initially recognised in accordance with other IFRSs (eg IAS 16.6)

• Cost is described further (eg IAS 16.7–28)

The historical cost ‘concept’

21

3131

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Question: what is the cost of the asset received? • transferable option exercised to acquire

an lear jet• decommissioning liability for a nuclear

power plant (and changes therein)• deferred payment/advance payment• exchange used lear jet and landing

rights (consequently discontinue that route) for new lear jet

• exchange similar used lear jets

Historical cost of an asset 3232

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

ASSET TYPE MEASUREMENT AT INITIAL RECOGNITION

COST MODEL BASIS OF IMPAIRMEN

T TESTIAS 2 Inventory Cost of purchase and/or conversion

costs and costs to get the item to the location and condition for sale

Cost unless impaired Lower of cost (initial recognition) and net realisable value

IAS 16 Property, Plant and Equipment

Purchase costs + construction costs + costs to bring to the location and condition necessary to be capable of operating in the manner intended by management.

Accounting policy choice: cost less accumulated depreciation and impairment, if any

Compare carrying amount to recoverable amount.

Recoverable amount is greater of value in use and fair value less disposal costs (IAS 36)

IAS 38 IntangiblesAssets

Purchase costs + development costs + costs to bring to the location and condition necessary to be capable of operating as intended by management

Accounting policy choice: cost less accumulated amortisation (unless indefinite life asset) and amortisation, if any

IAS 40 Investment Property

Cost including transaction costs Accounting policy choice: cost less accumulated depreciation (unless land) and impairment (if any)

3333

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Inventories are initially measured at cost. • The cost of inventory includes costs of purchase

and production or conversion.– cost does not include abnormal wastage,

administrative overheads that are not production costs and selling costs.

• Cost is assigned to each item of unique inventory using specific identification. FIFO or weighted average cost are used for ordinarily interchangeable inventory items. LIFO is prohibited.

• Inventory can be a qualifying asset in terms of IAS 23 Borrowing Costs

IAS 2 Inventories: measurement 3434

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• A buys a good priced at CU500 per unit from Z. Z awards A a 20% discount on orders of +100 units and 10% discount when A buys +999 units in 1 year. The discounts apply to all units acquired in a year. A buys as follows: 800 units on 1/1/20X1 and 200 units on 24/12/20X1.

On 31/12/20X1, 150 units were unsold (ieinventories of A).

IAS 2 Inventories:example—cost of purchase

3535

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

A measures the cost of the inventories in 20X1 at CU350,000 [ie 1,000 units × (CU500 list price less 30%(CU500) volume discount)], because all units purchased in the year get the full 30% discount.

• A recognises: – expense (cost of sales) of CU297,500 [ie

850 units sold × (CU500 list price less 30%(CU500) volume discount)] in profit or loss in 20X1

– asset (inventories) of CU52,500 [ie 150 units unsold × (CU500 less 30%(CU500) discount)] at 31/12/20X1.

IAS 2 Inventories:example—cost of purchase 3636

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• A makes concrete blocks in reusable moulds. Blocks dry in a drying room for 2 weeks. Dried blocks & raw mat’s stored in separate rooms.

A front-end loader (man 1) adds materials to the mixing machine operated by man 2. Casual labourers remove blocks from moulds. Man 3 supervises the factory. Man 4 does admin, finance and sales.

A operates from rented premises (fixed payments).

IAS 2 Inventories:example—conversion costs

22

3737

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Costs of conversion include– direct costs: casual labour.– production overheads: factory rent (incl.

raw mat’s area & drying room but excl. finished goods room); staff cost of man 1,2 & 3; depreciation of equipment (front end loader, mixing machine and moulds).

IAS 2 Inventories:example—conversion costs 3838

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Inventories are reduced to NRV when this is lower than cost.

– NRV is estimated selling price less estimated costs to complete and sell (entity specific value).

• The write-down is made on an item by item basis. The write-down of groups of items may occur when the grouped items have similar uses, are produced or marketed in the same area and cannot be practicably evaluated separately from other items in that product line.

• Write-downs can be reversed.

IAS 2 Inventories: impairment to net realisable value (NRV)

3939

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Ex 1: At reporting date– CA (cost) of raw materials = 100– replacement cost = 80 – est. selling price of finished good = 200 – est. costs to convert the raw material into

finished good = 60– est. costs to sell the finished good = 30

• Ex 2: Same as Ex 1 except est. selling price = 180

IAS 2 Inventories:examples—NRV write-down 4040

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• At 31/12/20X1 – because of a decline in economic

circumstances recognised an impairment loss on an item of inventory of 30 (ie cost = 100 & SP-CTC&S = 70)

At 31/12/20X2

– because of an improvement in economic circumstance the SP-CTC&S of that item is 120

IAS 2 Inventories:example—reverse impairment

4141

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Inventory may qualify as a qualifying asset in accordance with IAS 23—borrowing costs incurred on qualifying assets may be considered for capitalisation.

• Unlike IAS 23, Section 25 Borrowing Costs of the IFRS for SMEs prohibits the capitalisation of borrowing costs—all borrowing costs are expensed.

IAS 2 Inventories:comparison to IFRS for SMEs 4242

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Calculating the cost of a manufacturer’s inventory involves a number of judgements, including:

• normal wastage• allocating overheads (including plant

depreciation)• allocating joint costs to joint products.

IAS 2 Inventories:judgements and estimates

23

4343

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Impairment• identifying impaired inventories• estimating net realisable value.

• Net realisable value is an entity-specific measure and therefore judgement is required in order to determine the amounts expected to be realised upon sale of the inventory.

IAS 2 Inventories:judgements and estimates continued 4444

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• PPE is initially recognised at cost• Cost includes:

• purchase costs • construction costs • costs to bring to the location and condition

necessary to be capable of operating in the manner intended by management

• Subsequent costs qualify for capitalisation if they meet the asset recognition criteria

IAS 16 PPE: measurement

4545

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• After initial recognition entity chooses to measure PPE either:

• at cost less accumulated depreciation and accumulated impairment (cost model); or

• at fair value less subsequent accumulated depreciation and accumulated impairment (revaluation model).

IAS 16 PPE: measurement continued 4646

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Depreciation represents the consumption of the assets service potential in the period.

– land’s service potential generally does not reduce with time

• Systematic allocation (application guidance):– depreciation method must closely reflects the pattern in

which the asset’s future economic benefits are expected to be consumed by the entity

– unit of measure for depreciation is different from that for an item of PPE. By depreciating significant parts of an item of PPE separately, depreciation more faithfully represents the consumption of the assets service potential. (IAS16.BC26)

IAS 16 PPE: measurement continued

allocating depreciation: concepts

4747

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• On 1/1/20X1 buy machine for CU100,000. Initial estimates & judgements: – useful life = 10 yrs & residual value = 0 – straight-line depreciation is appropriate

At 31/12/20X5 year-end reassess:– useful life = 24 yrs (from the date of acq)

and residual value = CU20,000– straight-line depreciation is appropriate

IAS 16 PPE: example—depreciation 4848

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Full IFRSs require an annual review of residual value, useful life and depreciation method of property, plant and equipment. Section 17 Property, Plant and Equipment of the IFRS for SMEs requires a review only if there is an indication that there has been a significant change since the last annual reporting date.

IAS 16 PPE: comparison to the IFRS for SMEs

24

4949

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Cost of some items includes significant estimates

• costs of dismantling, removal, restoration• costs of self constructed PPE

• Depreciation requires: • identifying significant components to be

depreciated separately • estimating useful life and residual value• identifying the depreciation method that reflects

most closely the consumption of the service potential of the item of PPE

IAS 16 PPE: judgements and estimates 5050

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Determining the classes of PPE for presentation purposes.

IAS 16 PPE: judgements and estimates continued

5151

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Intangible assets are measured initially at cost. • Thereafter, intangible assets are usually measured

using the cost model—cost less accumulated amortisation (unless indefinite life) and impairment, if any.

• An intangible asset with a finite useful life is amortised and tested for impairment similarly to PPE.

• An intangible asset with an indefinite useful life is not amortised, but is tested annually for impairment or where evidence of impairment exists.

IAS 38 Intangible Assets:measurement 5252

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Ex 1: A acquires a customer list. Expects to benefit from list for 1–3 years.

• Ex 2: B acquires a 5-year airline route authority (ARA) that is renewable every 5 years at no cost– renewal is routine if specified rules and

regulations are complied with– B is compliant and expects to fly the route

indefinitely– an analysis of demand and cash flows

supports those assumptions

IAS 38 Intangible Assets:examples—estimating useful life

5353

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• The primary differences between IAS 38 and Section 18 Intangible Assets other than Goodwill of the IFRS for SMEs include that, in accordance with Section 18:

• all intangible assets are considered to have definite useful lives and, therefore, must all be amortised

• amortisation estimates need only be reviewed where there is an indication of a significant change

IAS 38 Intangible Assets: comparison with the IFRS for SMEs 5454

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Control of an asset arises when the entity has the power to obtain future economic benefits from the underlying resource and to restrict the access of other to those benefits. Intangible items of value to an entity may not be controlled by it, eg the assembled workforce and customer relationships.

• Research phase expenditures cannot be capitalised as assets. Development phase expenditures are capitalised when the specified criteria for asset recognition are satisfied.

IAS 38 Intangible Assets: judgements and estimates

25

5555

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Amorisation requires: • identifying a finite useful life intangible asset• estimating useful life• (residual value is usually assumed to be zero

unless there is an active market)• identifying the amortisation method that reflects

most closely the consumption of the service potential of the item of the intangible asset.

• Impairment testing requires many estimates (see IAS 36).

IAS 38 Intangible Assets: judgements and estimates continued 5656

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• An investment property is measured initially at cost.

• The cost of a property interest held under a lease is measured in accordance with IAS 17 Leases at the lower of the fair value of the property interest and the present value of the minimum lease payments.

IAS 40 Investment Property:initial measurement

5757

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• For subsequent measurement an entity must adopt either the fair value model or the cost model for all investment properties.

• All entities must estimate the fair value of investment property, either for measurement (if the entity uses the fair value model) or for disclosure (if it uses the cost model).

• Measure fair value in accordance with IFRS 13 Fair Value Measurement.

IAS 40 Investment Property: subsequent measurement 5858

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Investment property is measured at cost less accumulated depreciation and any accumulated impairment losses (ie using the cost model in IAS 16 Property, Plant and Equipment).

• Similar impairment consideration and principles must be applied.

IAS 40 Investment Property: cost model

5959

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• The main differences between IAS 40 and Section 16 Investment Property of the IFRS for SMEs include:

– the IFRS for SMEs does not have an accounting policy choice for measurement. The accounting for investment property is driven by circumstances. If an entity knows or can measure the fair value of an item of investment property without undue cost or effort on an ongoing basis, it must use the fair value through profit or loss model for that investment property. It must use the cost-depreciation-impairment model

– unlike IAS 40, the IFRS for SMEs does not require disclosure of the fair values of investment property measured on a cost basis.

IAS 40 Investment Property: comparison to the IFRS for SMEs 6060

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Sometimes it is difficult to identify investment property. In such cases an entity develops criteria so that it can exercise that judgement consistently

• eg, owner of a hotel transfers some responsibilities to third parties under a management contract (PPE or investment property?)

• In some cases measuring fair value (see IFRS 13)• When cost model used measuring depreciation

(see IAS 16 for estimating residual value, depreciation method and useful life)

IAS 40 Investment Property: judgements and estimates

26

6161

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• IAS 23 prescribes the accounting treatment for borrowing costs.

• Borrowing costs are interest and other costs incurred in connection with borrowing.

IAS 23 Borrowing Costs:introduction 6262

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• An entity shall capitalise borrowing costs that are directly attributable to the acquisition, construction or production of an asset that takes a substantial time to get ready for its intended use or sale (a qualifying asset).

• Other borrowing costs are recognised as an expense in the period in which they are incurred.

IAS 23 Borrowing Costs: recognition

6363

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Borrowing costs directly attributable to the acquisition, construction or production of a qualifying asset are those that would have been avoided if the expenditure on the asset had not been made.

• They may be borrowing costs incurred on funds borrowed specifically for obtaining a qualifying asset or a calculated amount based on a weighted average borrowing rate applied to expenditure on the asset.

IAS 23 Borrowing Costs: recognition continued 6464

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Capitalisation of borrowing costs takes place during the development of the asset, and ends when the asset is ready for its intended use or sale.

• When the asset is completed in parts, capitalisation of borrowing costs ceases when each part is ready for intended use or sale.

IAS 23 Borrowing Costs: recognition continued

6565

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Determining the amount of borrowing costs that are directly attributable to the acquisition of a qualifying assets requires judgement. For example:

• it might be difficult to identify a direct relationship between particular borrowings and a qualifying asset and to determine the borrowings that could otherwise have been avoided, particularly when financing is co-ordinated centrally.

IAS 23 Borrowing Costs: judgements and estimates 6666

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• IAS 36 applies to all assets other than those not within the scope of the Standard (IAS 36.2)

• Assets not within the scope include:• Inventories• Deferred tax assets• Financial assets within the scope of IFRS 9• Investment property measured at fair value

IAS 36 Impairment of Assets:which assets?

27

6767

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• An entity must, at the end of every reporting period, assess whether there is any indication that an asset (or cash-generating unit) is impaired

• Irrespective of whether an indication of impairment exists, annual impairment tests must be conducted for:

• Intangible assets with an indefinite useful life; • Intangible assets not yet available for use; and• Goodwill acquired in a business combination.

IAS 36 Impairment of Assets: when to test for impairment? 6868

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Impairment (IAS 36):• Comparison of the asset’s (or cash-generating unit’s) carrying

amount to its recoverable amount• Recoverable amount is the higher of fair value less costs to

sell and value in use. – Fair value less costs to sell is the arm’s length sale price

between knowledgeable, willing parties less the costs of disposal.

– The value in use of an asset is the expected future cash flows the asset in its current condition will produce, discounted to present value using an appropriate pre-tax discount rate.

IAS 36 Impairment of Assets: measurement

6969

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Impairment (per IAS 36):• An impairment loss is recognised immediately in the

statement of comprehensive income. • When an impairment loss is recognised, the

carrying amount of the asset (or cash-generating unit) is reduced.

• In a cash-generating unit, goodwill is reduced first, then other assets are reduced pro rata.

• The depreciation charge is adjusted in future periods to allocate the asset’s revised carrying amount over its remaining useful life.

IAS 36 Impairment of Assets: measurement 7070

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• At 31/12/20X1 CA of a CGU’s assets = 210 (ie150 taxis, 50 taxi licence & 10 goodwill)Impairment indicated & RA = 170. Fair value of taxis = 140.

Impairment loss = 40 (ie 210 CA less 170 RA)1st allocate 10 loss to goodwill2nd allocate remaining 30 loss, ie 22.5 to taxis & 7.5 to licence (pro rata on CA)3rd reallocate 12.5 loss from taxis to licence

IAS 36 Impairment of Assets: example—CGU impairment

7171

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Reversing an impairment loss (per IAS 36)• Consistent with the ‘principle’ of not recognising

an asset for internally generated goodwill, an impairment loss for goodwill is never reversed.

• For other assets, when the circumstances that caused the impairment loss are resolved, the impairment loss is reversed.

• However, the reversal is limited to the amount that the asset would have been had there been no impairment loss in prior years.

IAS 36 Impairment of Assets: measurement continued 7272

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Facts from CGU impairment example. At 31/12/20X2 CA of CGU = 120 (ie 100 taxis & 20 licence)

Impairment reversal indicated & RA estimated = 150

Potential impairment reversal = 30 (ie 150 RA less 120 CA) but limited to 20 (as follows)1st allocate to assets pro rata on CAs, ie 5 to licence & 25 to taxis2nd limit amt allocated to taxis to 7 (if no impairment in 20X1, CA at 20X2 = 107)

IAS 36 Impairment of Assets: example—impairment reversal

28

7373

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

3rd reallocate 18 reversal from taxis to licenceTotal reversal provisionally allocated to licence = 23 (ie 5 + 18)4th limit amt allocated to licences to 13 (if no impairment in 20X1, CA at 20X2 = 33)5th as there are no other assets to reallocate the unallocated 10 (ie 23 less 13) reversal to, limit the total impairment reversal to 20 (ie 7 for taxis and 13 for licence)

IAS 36 Impairment of Assets: example—impairment reversal 7474

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Identifying some indicators of impairment requires judgement (eg decline in an asset’s market value; adverse changes in the technological, market, economic or legal environment; increase in market interest rates, among others).

• Identifying the lowest level of independent cash inflows for some groups of assets (ie cash-generating unit) requires judgement.

• Allocating goodwill to cash-generating units requires judgement.

IAS 36 Impairment of Assets: judgements and estimates

7575

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Identifying some indicators of impairment requires judgement (eg decline in an asset’s market value; adverse changes in the technological, market, economic or legal environment; increase in market interest rates, among others).

• Identifying the lowest level of independent cash inflows for some groups of assets (ie cash-generating unit) requires judgement.

• Allocating goodwill to cash-generating units requires judgement.

IAS 36 Impairment of Assets: judgements and estimates 7676

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Measuring the value in use (an entity-specific measure) of an asset or group of assets involves

• estimating future cash flows that the entity expects to derive from the assets (its use and subsequent disposal) taking account of expectations about possible variations in the amount or timing of those cash flows

• adjusting for risks specific to the asset that market participants would reflect in pricing the asset

• identifying appropriate discount rates.

IAS 36 Impairment of Assets: judgements and estimates continued

7777

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Measuring the fair value less costs to sell of an asset or group of assets involves judgement

• see IFRS 13 for judgements and estimates in measuring fair value.

• estimating costs to sell can involve significant estimates.

IAS 36 Impairment of Assets: judgements and estimates continued

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation

Fair value

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

29

7979

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Fair value is the price that would be received to sell an asset or paid to transfer a liability (exit price) in an orderly transaction (not a forced sale) between market participants (market-based view) at the measurement date (current price).

• Fair value is a market-based measurement (it is not an entity-specific measurement)

• Consequently, the entity’s intention to hold an asset or to settle or otherwise fulfil a liability is not relevant when measuring fair value.

IFRS 13 Fair Value Measurement: definition 8080

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Excluded from the scope

• IFRS 2 and IAS 17

Disclosures in IFRS 13 not required for

• Plan assets (IAS 19)• Retirement benefit plan investments

(IAS 26)• Assets for which recoverable amount is fair

value less cost of disposal (IAS 36)

Not required for measurements similar

to fair value

• IAS 2 (net realisable value) • IAS 36 (value in use)

IFRS 13 Fair Value Measurement: when does IFRS 13 not apply?

8181

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• When measuring fair value use assumptions that market participants would use when pricing the asset or liability under current market conditions, including assumptions about risk.

• Characteristics of a particular asset or liability that a market participant would take into account when pricing the item at the measurment date, include:

– age, condition and location of the asset– restrictions on the sale or use.

IFRS 13 Fair Value Measurement: application guidance 8282

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Measured using the price in the principal market for the asset or liability (ie the market with the greatest volume and level of activity for the asset or liability) or, in the absence of a principal market, the most advantageous market for the asset or liability.

IFRS 13 Fair Value Measurement: transaction and price

8383

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Must reflect the use of a non-financial asset by market participants that maximises the value of the asset

– physically possible – legally permissible– financially feasible

• Highest and best use is usually (but not always) the current use.

IFRS 13 Fair Value Measurement: non-financial assets 8484

IFRS 13 Fair Value Measurement: the fair value hierarchy

Is there a quoted price in an active market for an identical

asset or liability?(Level 1 input)

Are there any observable inputs* other than quoted

prices for an identical asset or liability?

Use the Level 1 input = Level 1 measurement

Must use without adjustment

No use of significant unobservable

(Level 3) inputs‡ = Level 2

measurement

Use of significant unobservable

(Level 3) inputs‡ = Level 3

measurement

* Maximise the use of relevantobservable inputs. Observable inputs include market data (prices and other information) that is publicly available

‡ Unobservable inputs include the entity’s own data (egbudgets, forecasts), which must be adjusted if market participants would use different assumptions

Yes

Yes No

No

30

8585

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Information about an entity’s valuation processes is required for fair value measurements categorised within Level 3 of the fair value hierarchy.

• A narrative discussion is required about the sensitivity of a fair value measurement categorised within Level 3.

• Quantitative sensitivity analysis is required for financial instruments measured at fair value.

IFRS 13 Fair Value Measurement: disclosure 8686

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• An entity must take all information that is reasonably available to search for a principal market.

• determining fair value and the highest and best-use.for a non-financial asset.

• Assumptions that a market participant would use (including assumptions about risk).

• Determining the correct valuation technique to use and the inputs to the techniques, particularly on the income approach, require a wide range of estimates as:

• discount rates• future cash flows• risks and uncertainty

IFRS 13 Fair Value Measurement: judgements and estimates

8787

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• The inputs used in the valuation techniques should primarily be based on observable inputs (where possible) to minimise the use of unobservable inputs.

IFRS 13 Fair Value Measurement: judgements and estimates continued 8888

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

ASSET TYPE MEASUREMENT AT INITIAL

RECOGNITION

MODEL BASEDON FAIR VALUE

BASIS OF IMPAIRMENT

TEST

IAS 16 Property, Plant and Equipment

Purchase costs + construction costs + costs to bring to the location and condition necessary to be capable of operating in the manner intended by management.

Accounting policy choice: revaluation model

Compare carrying amount to recoverable amount.

Recoverable amount is greater of value in use and fair value less disposal costs (IAS 36)

IAS 38 IntangibleAssets

Purchase costs + development costs + costs to bring to the location and condition necessary to be capable of operating as intended by management

Accounting policy choice: revaluation model

IAS 40Investment Property

Cost including transaction costs

Accounting policy choice: fair value

IAS 41 Agriculture Fair value less costs to sell Fair value less costs to sell

8989

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Biological assets (and agricultural produce at the point of harvest) are measured at fair value less costs to sell (initial and subsequent measurement)

• changes in fair value less costs to sell are presented in profit or loss.

• Biological assets that are attached to land (eg trees in a plantation forest) are measured separately from the land. If owner-occupied the land is accounted for in accordance with IAS 16.

IAS 41 Agriculture:measurement 9090

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• The value accretion of agricultural assets is unique• Fair value measurement provides relevant, reliable,

comparable and understandable measurement of future economic benefits

• Historical cost cannot accurately portray the value of an accreting asset

Exception—when on initial recognition estimates of fair value are determined to be clearly unreliable, the cost-depreciation-impairment model should be used

IAS 41 Agriculture: why fair value measurement?

31

9191

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• In some cases, measuring fair value requires judgements and estimates

• A PwC study observed 3 different methods for valuing standing timber:

• discounted cash-flow (of expected or current log prices), • historical cost (of newly planted trees) and • market value (of trees approaching harvest age at

current market prices).

IAS 41 Agriculture: judgements and estimates 9292

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• The PwC study observed that in applying DCF-models management made several important assumptions including:

• expected income at harvest—variables included growth rate and price per unit of volume

• expected costs during growth—including silvicultural costs, eg maintenance and thinning