jericho presentation june 2015

TRANSCRIPT

For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

Corporate Presentation June 2015

2 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

Forward Looking Statement

Presentation and Reader Advisory This presentation includes certain statements that may be deemed forward-looking statements. All statements in this presentation, other than statements of historical facts, that address future events or developments that Jericho Oil Corporation (“JCO”) expects are forward -looking statements. Forward-looking statements are frequently characterized by words such as "plan", "expect", "project", "intend", "believe", "anticipate", "estimate" and other similar words, or statements that certain events or conditions "may" or "will" occur. In particular, forward-looking statements in this presentation include, but are not limited to, statements with respect to timing and completion of JCO’s exploration and development program on its Kansas oil leases. Forward-looking statements are based on the opinions and estimates of management at the date the statements are made, and are su bject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those anticipated in the forward-looking statements. Some of the risks and other factors could cause results to differ materially from those expressed in the forward-looking statements include, but are not limited to: general economic conditions in Canada, the United States and globally; industry conditions, including fluctuations in commodity prices; governmental regulation of the oil and gas industr y, including environmental regulation; geological, technical and drilling problems; unanticipated operating events; competition for and/or inability to retain drilling rigs and other services; the availability of capital on acceptable terms; the need to obtain required approvals from regulatory authorities; stock market volatility; volatility in market price s for commodities; liabilities inherent in oil and gas exploration, development and production operations; changes in tax laws and incentive programs relating to the oil and gas ex ploration industry; and the other factors described in our public filings available at www.sedar.com. Readers are cautioned that this list of risk factors should not be construed as exhaustive. Although JCO believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Investors should not place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Other than as required under applicable securities laws, JCO does not assume a duty to update these forward-looking statements. For more information on JCO, Investors should review JCO’s filings that are available at www.sedar.com. Information and facts included in this presentation have been obtained from publicly available and published sources and wher e appropriate those sources have been cited in this presentation. JCO does not assume a duty to independently verify publicly available and published sources of information pro vided by arms length third parties.

For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

Business Overview

4 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

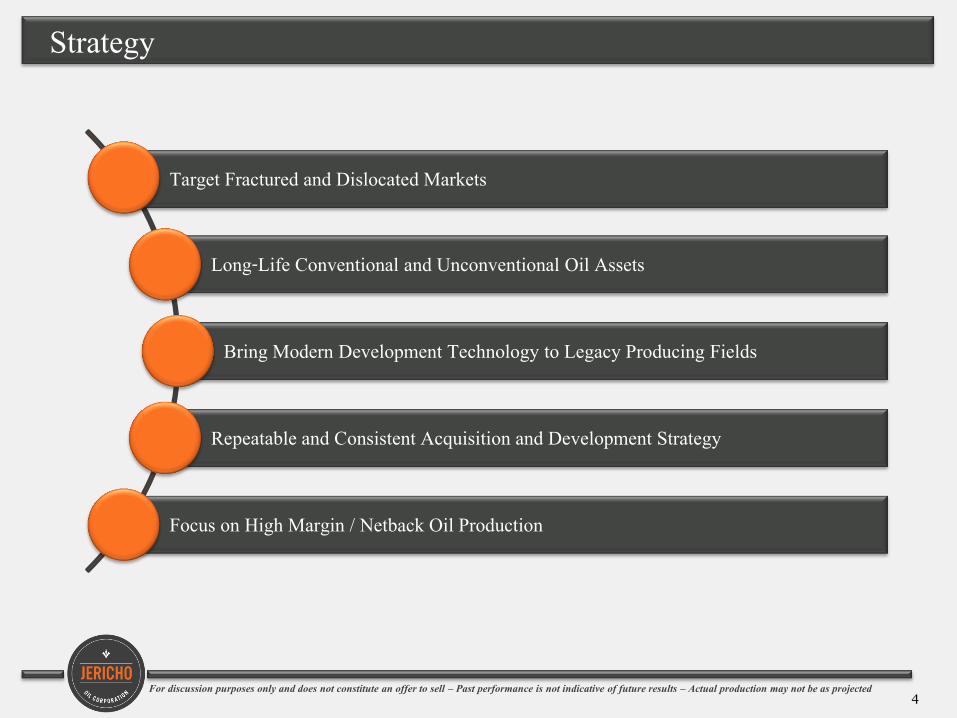

Strategy

Target Fractured and Dislocated Markets

Long-Life Conventional and Unconventional Oil Assets

Bring Modern Development Technology to Legacy Producing Fields

Repeatable and Consistent Acquisition and Development Strategy

Focus on High Margin / Netback Oil Production

5 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

Creating Value Through the Cycle: Acquisition Focused

o Aggressively creating shareholder value through acquisitions

o Bringing high-quality assets into Jericho’s fold for below their intrinsic value – acquisition pricing has fallen correspondingly with the price of oil however bid-ask spreads still remain wide

o As larger, leveraged companies increasingly went after ever more expensive and costly reserves, their business models ‘broke’ with the historical price drop and are looking to shore up balance sheets with cheap asset sales…Jericho is looking, but remains patiently aggressive

o While other companies simply “manage” through the historical oil price downturn, Jericho has shifted it’s focus from drilling and development to:

6 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

Note: Market Data as of May 2015. Dollar amounts in CAD$

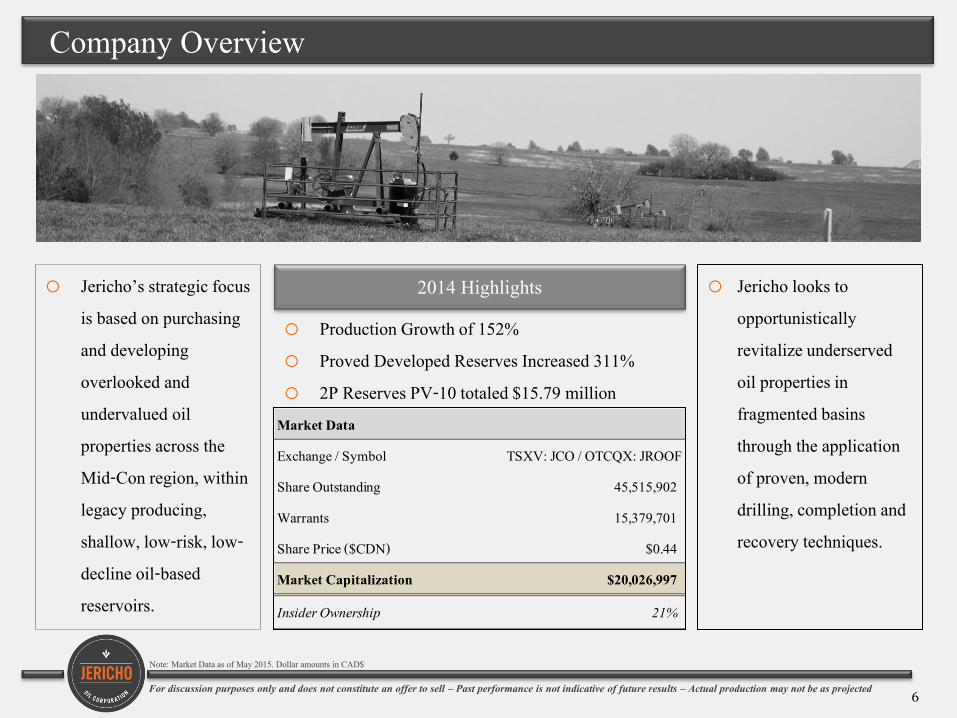

Company Overview

o Jericho’s strategic focus is based on purchasing and developing overlooked and undervalued oil properties across the Mid-Con region, within legacy producing, shallow, low-risk, low-decline oil-based reservoirs.

Oil-focused

2014 Highlights o Production Growth of 152% o Proved Developed Reserves Increased 311% o 2P Reserves PV-10 totaled $15.79 million

Market Data

Exchange / Symbol

Share Outstanding

Warrants

Share Price ($CDN)

Market Capitalization

Insider Ownership 21%

TSXV: JCO / OTCQX: JROOF

45,515,902

15,379,701

$0.44

$20,026,997

o Jericho looks to opportunistically revitalize underserved oil properties in fragmented basins through the application of proven, modern drilling, completion and recovery techniques.

2014 Highlights

7 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

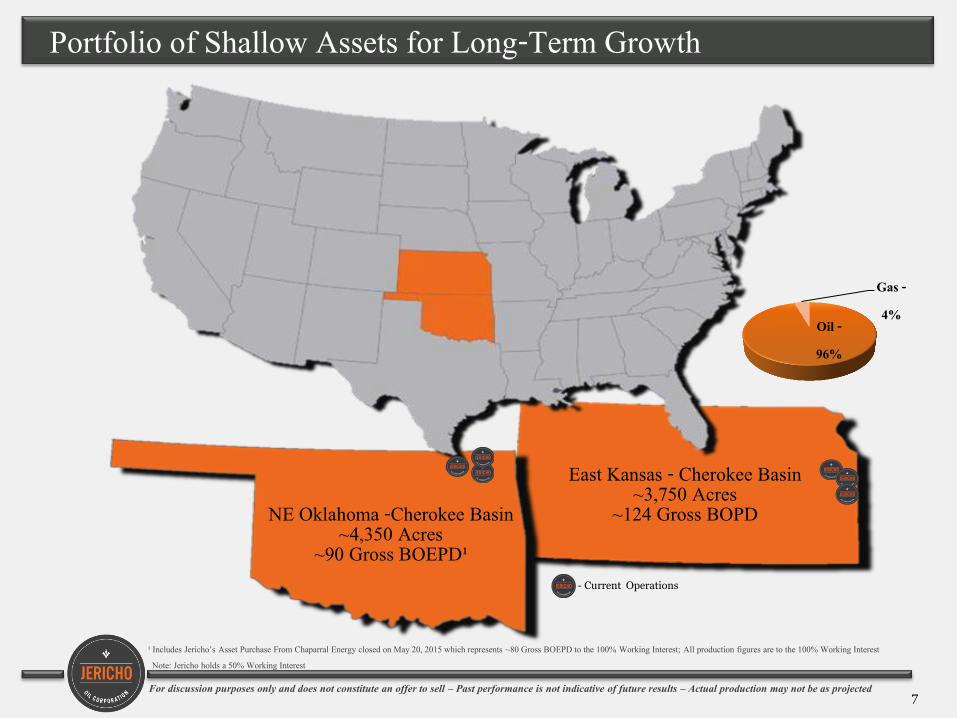

Portfolio of Shallow Assets for Long-Term Growth

NE Oklahoma -Cherokee Basin ~4,350 Acres

~90 Gross BOEPD¹

East Kansas - Cherokee Basin ~3,750 Acres

~124 Gross BOPD

- Current Operations

Oil - 96%

Gas - 4%

¹ Includes Jericho’s Asset Purchase From Chaparral Energy closed on May 20, 2015 which represents ~80 Gross BOEPD to the 100% Working Interest; All production figures are to the 100% Working Interest Note: Jericho holds a 50% Working Interest

8 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

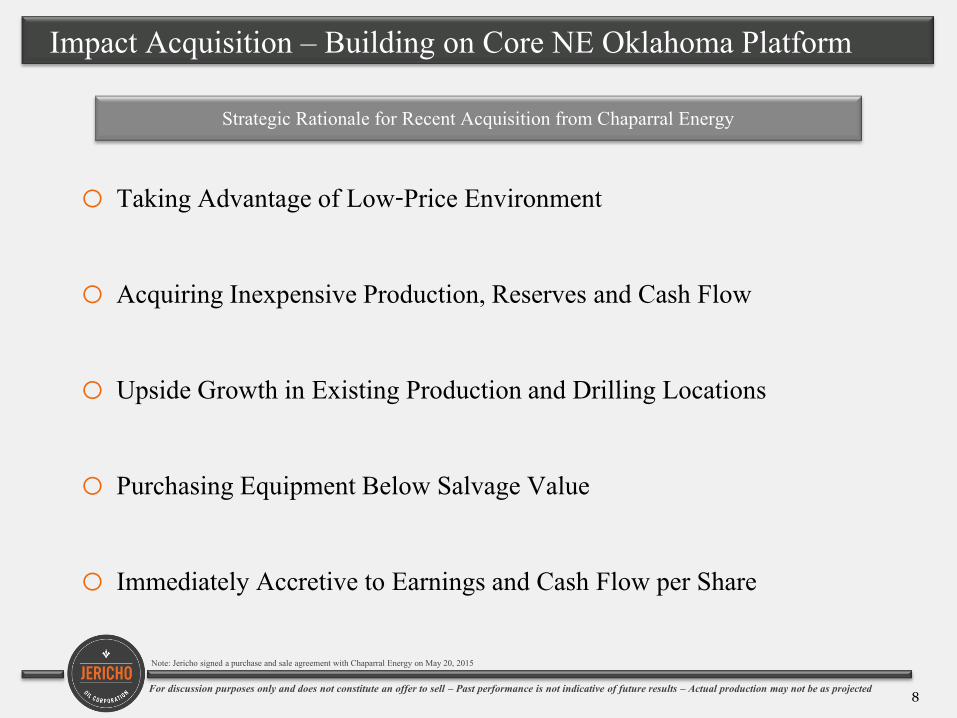

Impact Acquisition – Building on Core NE Oklahoma Platform

o Taking Advantage of Low-Price Environment o Acquiring Inexpensive Production, Reserves and Cash Flow

o Upside Growth in Existing Production and Drilling Locations o Purchasing Equipment Below Salvage Value o Immediately Accretive to Earnings and Cash Flow per Share

Strategic Rationale for Recent Acquisition from Chaparral Energy

Note: Jericho signed a purchase and sale agreement with Chaparral Energy on May 20, 2015

9 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

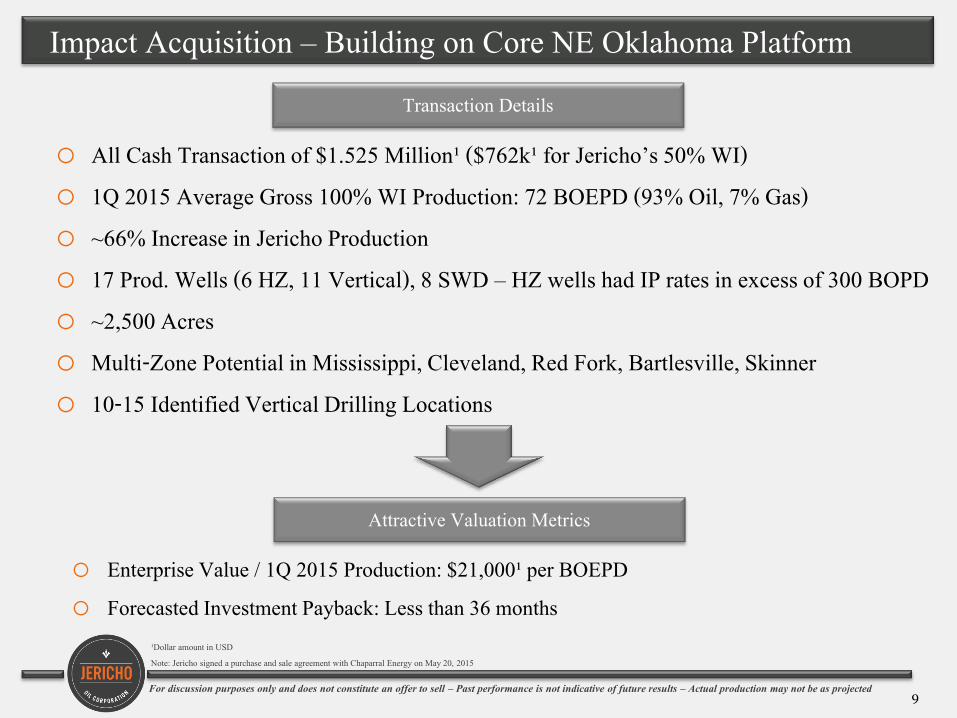

Impact Acquisition – Building on Core NE Oklahoma Platform o All Cash Transaction of $1.525 Million¹ ($762k¹ for Jericho’s 50% WI) o 1Q 2015 Average Gross 100% WI Production: 72 BOEPD (93% Oil, 7% Gas) o ~66% Increase in Jericho Production o 17 Prod. Wells (6 HZ, 11 Vertical), 8 SWD – HZ wells had IP rates in excess of 300 BOPD o ~2,500 Acres o Multi-Zone Potential in Mississippi, Cleveland, Red Fork, Bartlesville, Skinner o 10-15 Identified Vertical Drilling Locations

o Enterprise Value / 1Q 2015 Production: $21,000¹ per BOEPD o Forecasted Investment Payback: Less than 36 months

Transaction Details

Attractive Valuation Metrics

¹Dollar amount in USD Note: Jericho signed a purchase and sale agreement with Chaparral Energy on May 20, 2015

10 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

2,000

2,500

3,000

3,500

Jan-15 Feb-15 Mar-15

2,702 3,125

3,539

Barre

ls of

Oil P

er M

onth

Current Operational Highlights

100% Gross Net

Reserve Category (Mbbl) (Mbbl) (Mbbl)

419.3 209.7 179.7

69.5 34.7 29.6

504.4 252.2 214.9

993.2 496.6 424.2

601.0 300.5 257.2

1,594.1 797.1 681.4

Total Probable

Total Proved + Probable

Proved Developed Producing

Proved Developed Non-Prod.

Proved Undeveloped

Total Proved

0

50,000

100,000

150,000

200,000

250,000

78,573

244,962

Proved Develop Reserves Growth

March 2014 December 2014

26%

4%

32%

38% PDP

PDNP

PUD

Probable

Jericho’s 2014 YE Reserves Breakdown

Jericho’s 2014 YE Proved Developed Reserves

Q1 2015 Gross Production¹ First Oklahoma Acquisition (March ‘15)

¹ Does not include Jericho’s Asset Purchase From Chaparral Energy closed on May 20, 2015 which represents ~80 Gross BOEPD to the 100% Working Interest; Note: Jericho holds a 50% Working Interest Note: “Gross Reserves” represent Jericho’s 50% Working Interest in the NI 51-101 Compliant Independent Reserves Evaluation Prepared by Petrotech Engineering Effective December 31, 2014

11 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

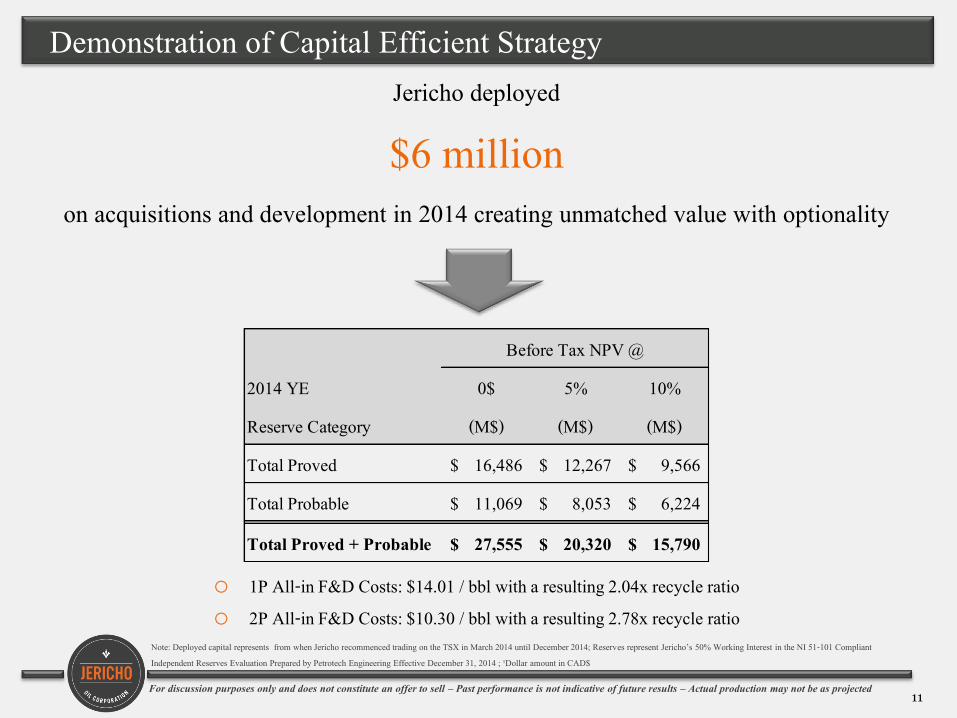

Demonstration of Capital Efficient Strategy Jericho deployed

$6 million on acquisitions and development in 2014 creating unmatched value with optionality

o 1P All-in F&D Costs: $14.01 / bbl with a resulting 2.04x recycle ratio o 2P All-in F&D Costs: $10.30 / bbl with a resulting 2.78x recycle ratio

2014 YE 0$ 5% 10%

Reserve Category (M$) (M$) (M$)

Total Proved 16,486$ 12,267$ 9,566$

Total Probable 11,069$ 8,053$ 6,224$

Total Proved + Probable 27,555$ 20,320$ 15,790$

Before Tax NPV @

Note: Deployed capital represents from when Jericho recommenced trading on the TSX in March 2014 until December 2014; Reserves represent Jericho’s 50% Working Interest in the NI 51-101 Compliant Independent Reserves Evaluation Prepared by Petrotech Engineering Effective December 31, 2014 ; ¹Dollar amount in CAD$

12 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

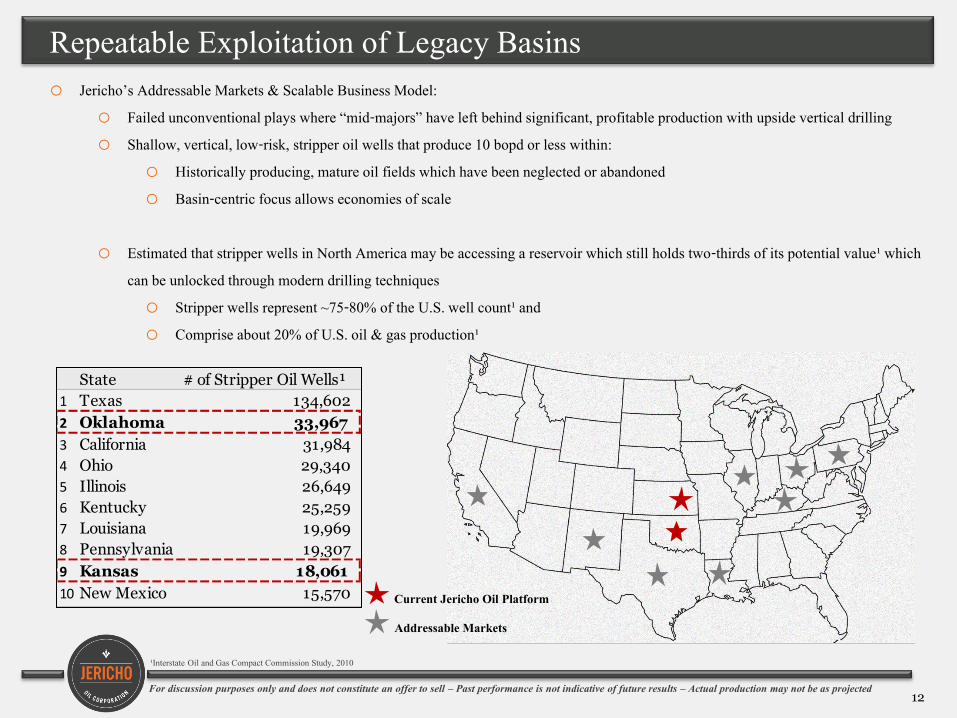

o Jericho’s Addressable Markets & Scalable Business Model: o Failed unconventional plays where “mid-majors” have left behind significant, profitable production with upside vertical drilling o Shallow, vertical, low-risk, stripper oil wells that produce 10 bopd or less within:

o Historically producing, mature oil fields which have been neglected or abandoned o Basin-centric focus allows economies of scale

o Estimated that stripper wells in North America may be accessing a reservoir which still holds two-thirds of its potential value¹ which

can be unlocked through modern drilling techniques o Stripper wells represent ~75-80% of the U.S. well count¹ and o Comprise about 20% of U.S. oil & gas production¹

¹Interstate Oil and Gas Compact Commission Study, 2010

Current Jericho Oil Platform

Addressable Markets

Repeatable Exploitation of Legacy Basins

State # of Stripper Oil Wells¹

1 Texas 134,602

2 Oklahoma 33,967

3 California 31,984

4 Ohio 29,340

5 Illinois 26,649

6 Kentucky 25,259

7 Louisiana 19,969

8 Pennsylvania 19,307

9 Kansas 18,061

10 New Mexico 15,570

13 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

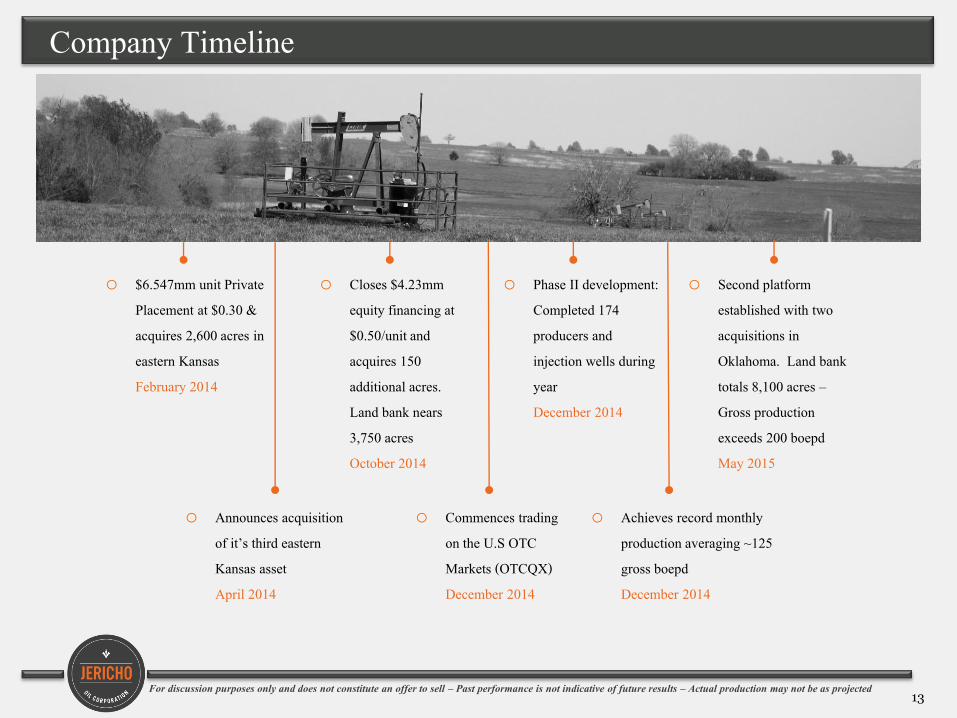

Company Timeline Oil-focused

o $6.547mm unit Private Placement at $0.30 & acquires 2,600 acres in eastern Kansas February 2014

o Closes $4.23mm equity financing at $0.50/unit and acquires 150 additional acres. Land bank nears 3,750 acres October 2014

o Commences trading on the U.S OTC Markets (OTCQX) December 2014

o Achieves record monthly production averaging ~125 gross boepd December 2014

o Phase II development: Completed 174 producers and injection wells during year December 2014

o Second platform established with two acquisitions in Oklahoma. Land bank totals 8,100 acres – Gross production exceeds 200 boepd May 2015

o Announces acquisition of it’s third eastern Kansas asset April 2014

For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

Operations Portfolio: Eastern Kansas & NE Oklahoma

15 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

0

1,000

2,000

3,000

4,000

Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15

824 1,012

1,694

935

1,741

2,818

3,553 3,298

2,851

3,854

2,702 3,125

3,539

Barr

els of

Oil P

er M

onth

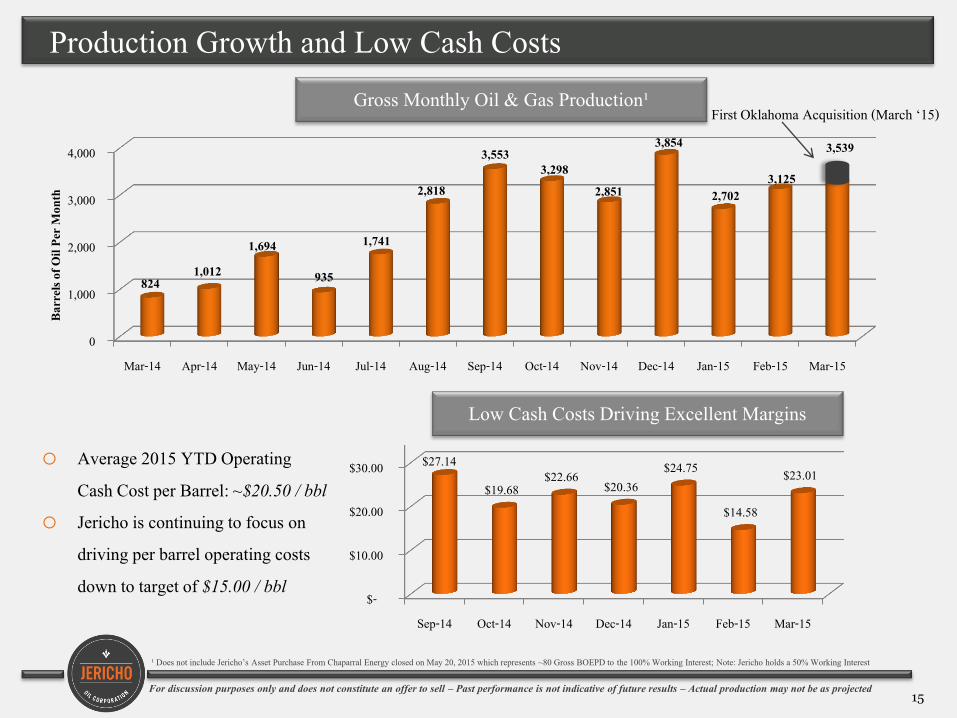

Production Growth and Low Cash Costs

$-

$10.00

$20.00

$30.00

Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15

$27.14

$19.68 $22.66 $20.36

$24.75

$14.58

$23.01 o Average 2015 YTD Operating

Cash Cost per Barrel: ~$20.50 / bbl o Jericho is continuing to focus on

driving per barrel operating costs down to target of $15.00 / bbl

First Oklahoma Acquisition (March ‘15) Gross Monthly Oil & Gas Production¹

Low Cash Costs Driving Excellent Margins

¹ Does not include Jericho’s Asset Purchase From Chaparral Energy closed on May 20, 2015 which represents ~80 Gross BOEPD to the 100% Working Interest; Note: Jericho holds a 50% Working Interest

16 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

0 20 40 60 80 100 120

BO

PM

Production Months

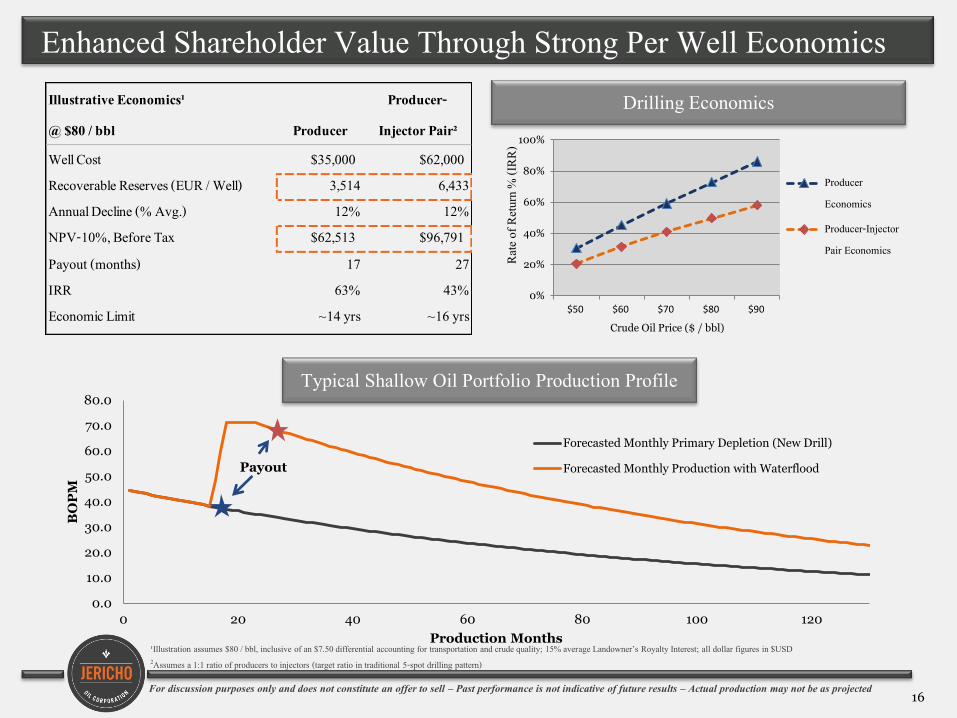

Typical East Kansas Production Profile

Forecasted Monthly Primary Depletion (New Drill)

Forecasted Monthly Production with WaterfloodPayout

¹Illustration assumes $80 / bbl, inclusive of an $7.50 differential accounting for transportation and crude quality; 15% average Landowner’s Royalty Interest; all dollar figures in $USD 2Assumes a 1:1 ratio of producers to injectors (target ratio in traditional 5-spot drilling pattern)

Enhanced Shareholder Value Through Strong Per Well Economics

0%

20%

40%

60%

80%

100%

$50 $60 $70 $80 $90

Rate

of Re

turn %

(IRR

)

Crude Oil Price ($ / bbl)

ProducerEconomics

Producer-InjectorPair Economics

Drilling Economics

Typical Shallow Oil Portfolio Production Profile

Illustrative Economics¹ Producer-

@ $80 / bbl Producer Injector Pair²Well Cost $35,000 $62,000Recoverable Reserves (EUR / Well) 3,514 6,433Annual Decline (% Avg.) 12% 12%NPV-10%, Before Tax $62,513 $96,791Payout (months) 17 27IRR 63% 43%Economic Limit ~14 yrs ~16 yrs

17 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

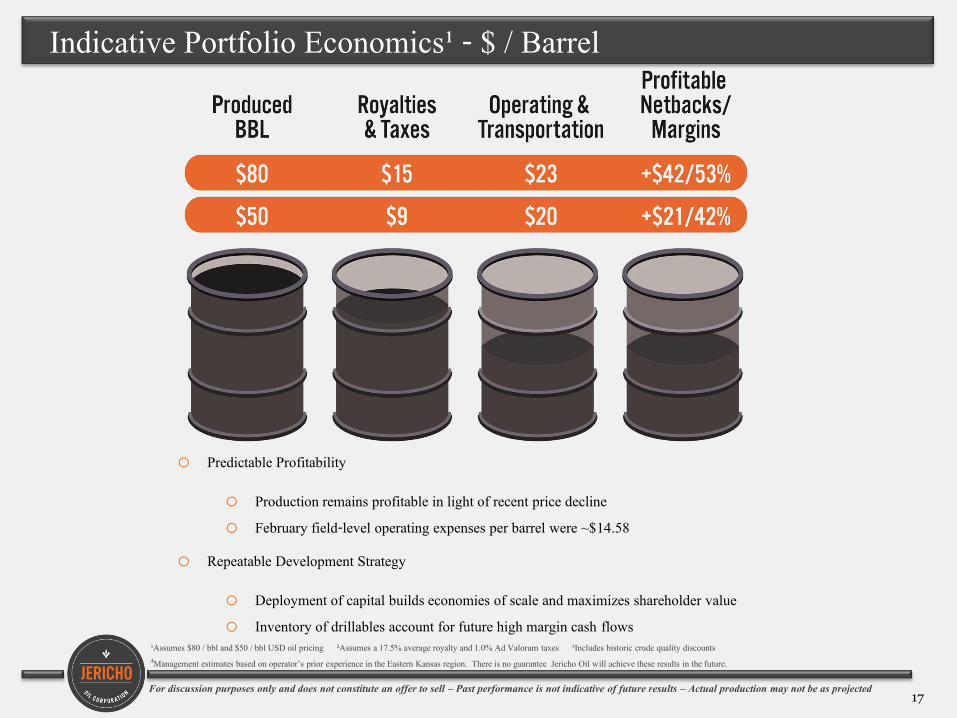

¹Assumes $80 / bbl and $50 / bbl USD oil pricing ²Assumes a 17.5% average royalty and 1.0% Ad Valorum taxes ³Includes historic crude quality discounts 4Management estimates based on operator’s prior experience in the Eastern Kansas region. There is no guarantee Jericho Oil will achieve these results in the future.

Indicative Portfolio Economics¹ - $ / Barrel

o Predictable Profitability

o Production remains profitable in light of recent price decline o February field-level operating expenses per barrel were ~$14.58

o Repeatable Development Strategy

o Deployment of capital builds economies of scale and maximizes shareholder value o Inventory of drillables account for future high margin cash flows

18 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

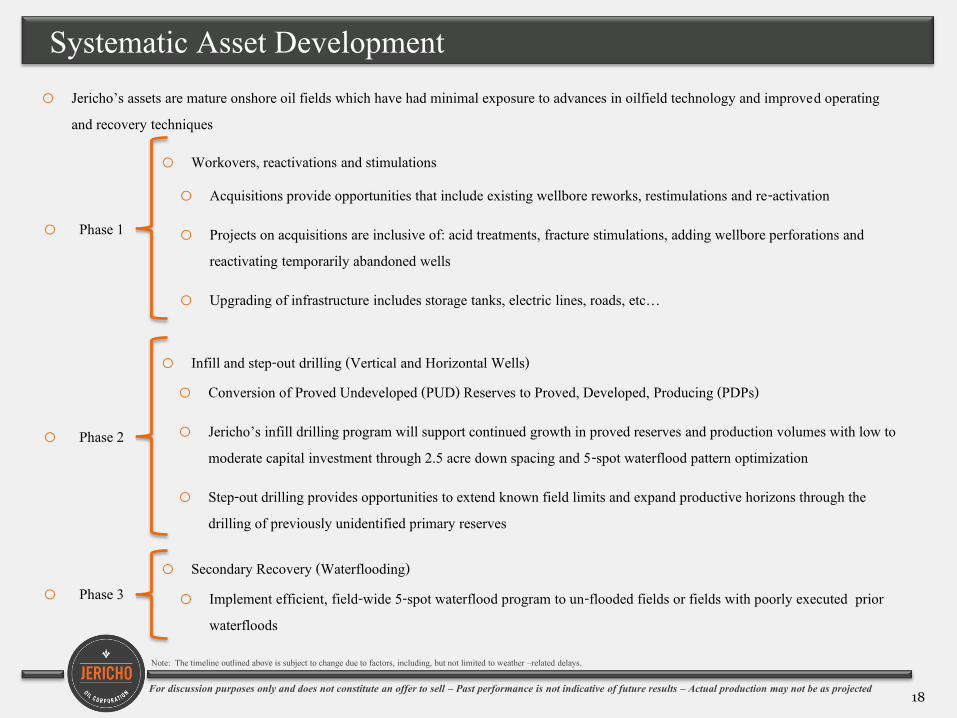

o Jericho’s assets are mature onshore oil fields which have had minimal exposure to advances in oilfield technology and improved operating and recovery techniques

o Workovers, reactivations and stimulations

o Acquisitions provide opportunities that include existing wellbore reworks, restimulations and re-activation

o Projects on acquisitions are inclusive of: acid treatments, fracture stimulations, adding wellbore perforations and reactivating temporarily abandoned wells

o Upgrading of infrastructure includes storage tanks, electric lines, roads, etc…

o Infill and step-out drilling (Vertical and Horizontal Wells) o Conversion of Proved Undeveloped (PUD) Reserves to Proved, Developed, Producing (PDPs)

o Jericho’s infill drilling program will support continued growth in proved reserves and production volumes with low to moderate capital investment through 2.5 acre down spacing and 5-spot waterflood pattern optimization

o Step-out drilling provides opportunities to extend known field limits and expand productive horizons through the drilling of previously unidentified primary reserves

o Secondary Recovery (Waterflooding) o Implement efficient, field-wide 5-spot waterflood program to un-flooded fields or fields with poorly executed prior

waterfloods

o Phase 1

o Phase 2

o Phase 3

Systematic Asset Development

Note: The timeline outlined above is subject to change due to factors, including, but not limited to weather –related delays.

For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

The Appendix

20 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

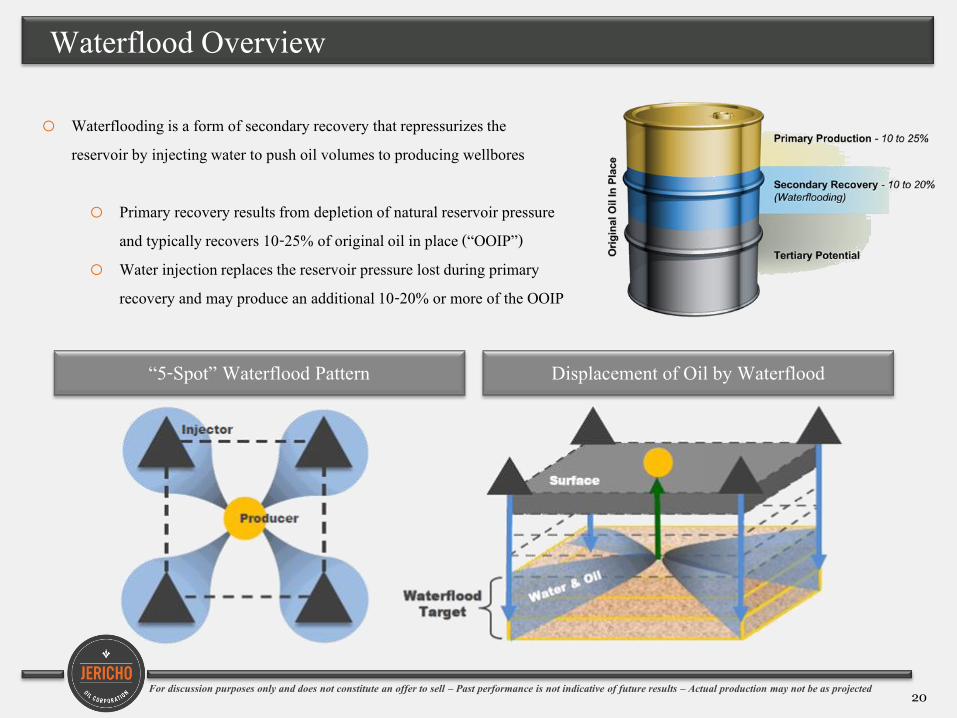

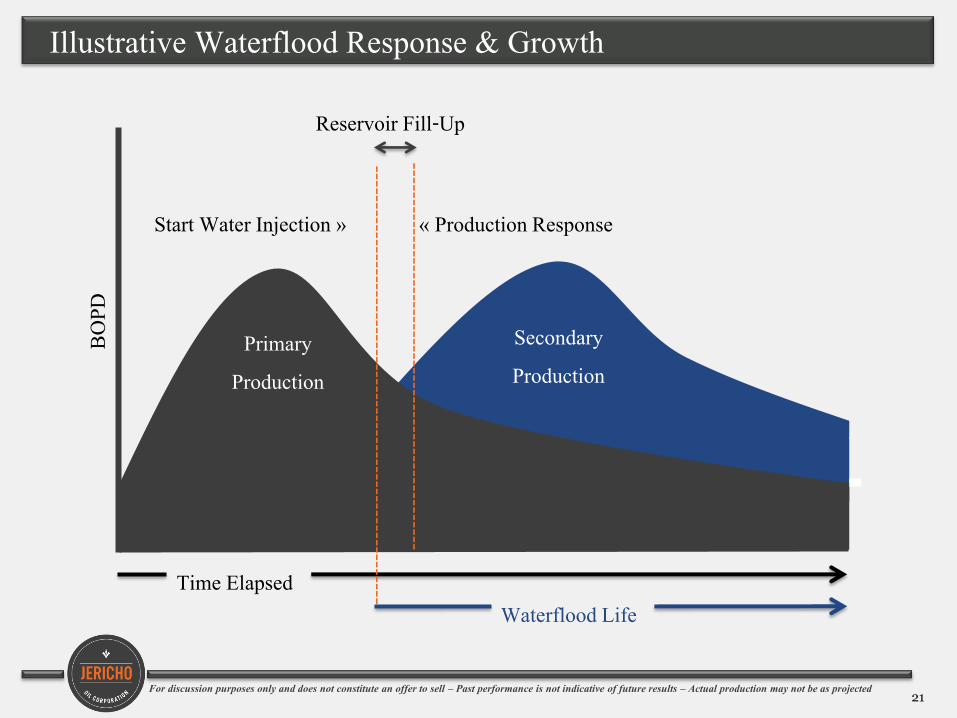

o Waterflooding is a form of secondary recovery that repressurizes the reservoir by injecting water to push oil volumes to producing wellbores

o Primary recovery results from depletion of natural reservoir pressure

and typically recovers 10-25% of original oil in place (“OOIP”) o Water injection replaces the reservoir pressure lost during primary

recovery and may produce an additional 10-20% or more of the OOIP

Waterflood Overview

Displacement of Oil by Waterflood “5-Spot” Waterflood Pattern

21 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

BOPD

Time Elapsed Waterflood Life

Primary Production

Secondary Production

------------------------------------------------------------

----

----

----

----

----

----

----

----

----

----

----

----

----

-

Start Water Injection » « Production Response

Reservoir Fill-Up

Illustrative Waterflood Response & Growth

22 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

o Allen Wilson President, Chief Executive Officer and Director Allen was appointed President, CEO and a director of the Company in September 2011. He brings extensive capital markets and corporate development experience to Jericho. Allen has been a successful investor, fundraiser and business development strategist for the past 20 years, working primarily with micro-cap companies at all stages of growth. He possesses a far-reaching network of relationships across North America and Europe. Allen has been a director of Shasta Gold Corp., a private gold mining company, since October 2010 and a director of Newcastle Energy Corp. since February 2013.

Management Team

o Robin Peterson, CGA, CPA (Canada) Chief Financial Officer Robin was appointed Chief Financial Officer of Jericho Oil in

December 2013. He has current Canadian public company reporting experience with U.S. oil operations and brings extensive financial, compliance and cost management expertise to Jericho. Robin has been a director of Newcastle Energy Corp. since June 2013.

23 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

o Allen Wilson (see management bios)

o Stephen Kenwood, P.Geo. Stephen joined the board of directors of the Company in September 2011. He serves as a geological and management consultant to various public and private companies. He is a registered member of the Association of Professional Engineers and Geoscientists of British Columbia. Stephen received a B. Sc. (Geology) degree from the University of British Columbia in 1987. He has experience in the area of advanced project development, as a geologist with Cominco, Ltd. on the Snip gold project, as a project geologist at the Eskay Creek deposit for Prime Exploration Ltd., and as a project geologist on the Petaquilla copper-gold porphyry deposit in Panama. Stephen currently a director of a number of TSX listed companies.

Board of Directors

o Nicholas W. Baxter Nicholas joined the board of directors of the Company in September 2011. He has a 24 year career in international resource exploration and development. He has served President & CEO of Eurasia Energy Limited (EUENF:OTCQB) since November 2005. Originally trained as a geophysicist, Nicholas received a Bachelor of Science (Honors) from the University of Liverpool in 1975 and has worked on geophysical survey and exploration projects in the U.K., Europe, Africa and the Middle East. He was COO and a director of A&B Geoscience Corporation from 1985 to 2003, where under his guidance the company secured the first onshore production sharing agreement in Azerbaijan in 1998. A&B became controlled by a private Swiss oil trading firm in 2002. Nicholas worked as an independent upstream oil and gas consultant from 2002 to 2004 before joining Eurasia. He has served as a director of Eurasia Energy since March 2005.

o Gerald R. Tuskey Gerald joined the board of directors of the Company in January 2013. For the past 21 years, he has worked as a self-employed corporate/securities lawyer based in Vancouver, British Columbia. Before establishing his own independent practice, Gerald was employed as an associate lawyer by firms in Calgary and Vancouver. He has 28 years’ experience in providing securities and corporate law counsel to a wide variety of domestic and international publicly traded clients. Gerald has acted as an officer and director of various public venture companies and takes primary responsibility for Jericho’s corporate and regulatory filings and compliance.

24 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

o Reserves: Estimated remaining quantities of petroleum anticipated to be commercially recoverable from known subsurface accumulations based on the analysis of historical drilling,

geological, geophysical, and engineering data

o Proved Reserves: Estimated quantities of petroleum which, by analysis of geological and engineering data, can be estimated with reasonable certainty to be commercially recoverable, from a given date forward, from known reservoirs and under current economic conditions, operating methods and government regulations – “Reasonable certainty” is intended to express a high degree of confidence that quantities will be recovered –usually equal to a 90% or greater probability that the estimated quantities of petroleum will be recovered

o Probable Reserves: Estimated quantities of petroleum which analysis of geological and engineering data suggests are more likely than not to be recoverable – meaning there should be at least a 50% probability that the estimated quantities of petroleum will be recovered

o Possible Reserves: Estimated quantities of petroleum which analysis of geological and engineering data suggests are less likely to be recoverable than probable reserves – meaning there should be at least a 10% probability that the estimated quantities of petroleum will be recovered

o Working Interest (“WI”): A percentage of ownership in an oil and gas lease granting the owner the right to explore, drill and produce oil and gas from a tract of property. Working interest owners are obligated to pay a corresponding percentage of the cost of leasing, drilling producing and operating a well or unit. The Working interest owner receives their share of the production revenue after the royalty owners have taken their share and after expenses have been deducted

o Net Revenue Interest (“NRI”): A share of gross production after all burdens, such as royalty and overriding royalty, have been deducted from the working interest. It is the percentage of gross production that each party actually receives

o Total Vertical Depth (‘TVD’): The end of the well, measured by the length of pipe required to reach the bottom

o Barrels of Oil Per Day (“BOPD”): A common unit / abbreviation of the measurement of a volume of crude oil. The volume of a stock tank barrel is equivalent to 42 U.S. gallons

o Barrel (“Bbl”): An abbreviation of oilfield barrel. A volume of 42 U.S. gallons

Source: Society of Petroleum Engineers (“SPE”) and Nontechnical guide to Petroleum Geology, Exploration, Drilling and Produ ction (Norman J. Hyne, Ph.D.)

Glossary of Key Terms

25 For discussion purposes only and does not constitute an offer to sell – Past performance is not indicative of future results – Actual production may not be as projected

o Jericho Oil Corporation Corporate Office 604.343.4534 888 Dunsmuir Street, 11th Floor Vancouver, BC, V6C 3K4 o Regional Office 321 South Boston, Suite 300 Tulsa, OK 74103

o [email protected] www.jerichooil.com TSXV: JCO │ OTCQX: JROOF

Contact Us

o Director, Acquisitions & Divestitures Ryan Breen US 215.383.2434 CN 604.343.2726 o Director, Investor Relations Tony Blancato US 215.383.2433 CN 604.343.2725 o Director, Corporate Communications Adam Rabiner CN 604.343.4534

o