jeddah real estate market overview - q1 2013 office market overview office supply and demand •...

TRANSCRIPT

Dubai Real Estate Market Overview

Q1 2013

Jeddah

Macroeconomic overview

2

Indicator 2012 2013 (f) 2014 (f)

Saudi Arabia

Population (millions) 29.3 30.2 31.1

Real GDP Growth (Y-o-Y) 6.8% 4.2% 3.6%

Inflation (% Change) 4.5% 4.3% 3.8%

Budget Surplus (USD billions) 103 47 35

Jeddah

Population (millions) 37 3.8 3.9

Cost of Living Index (% change) 4.9% 3.5% 3.6%

Sources: Sama, Jadwa, IHS Global Insights April 2013, CDS , 2012

f:forecasted

Economic highlights – Q1 2013

3

Real GDP in KSA grew by 6.8% in 2012. High oil production and expansionary fiscal policy have kept the Kingdom‟s growth at a high level.

Retail sales continued to increase, growing by 25% in Q1 2013 compared to the same quarter last year.

Bank lending to building and construction has increased by 27% in Q1 2013 from the same period last year. This reflects greater participation in infrastructure and housing projects.

To facilitate housing construction program, King Abdullah has approved the creation of a new USD 67 billion housing fund.

At 3.9% Y-o-Y, inflation increased for the third consecutive month in March. This was almost entirely due to higher rental inflation and increasing food prices.

Saudi banks increased their lending to real estate end users (mostly mortgages) by 30% in 2012, the largest increase during the last five years.

Property & project news– Q1 2013

4

• Jeddah Municipality has approved 64,000 residential units in a

range of projects across Jeddah. These include developments by

Jeddah Development & Urban Regeneration Company (JDURC),

the Ministry of Housing and private developers.

• Da‟em Real Estate Company has announced a new residential

project in Jeddah called Da‟em Residence. Located in Al Marwa

district, it consists of 120 residential units to be completed in

2015.

• Saudi Industrial Property Authority (MODON) has approved

SAR 50 million to develop the infrastructure of phase-1 of the

Fourth Industrial City, located 25km north of Jeddah. Land rents

in the project have been set at SAR 3 sq m per year

• Makkah Municipality has allocated another 1 million sq m of land

near Makkah Gate to its industrial city project.

• Makkiyoun has announced a new 1,800 unit residential project in

Makkah called Makkah Oaisi. The company has also announced

that the completion date for its Al Tilal Project will be late 2015.

This project in Al Haram area, consists of a mall, wedding hall

and a conference hall.

• Kingdom Holdings expects work on the world second deepest

(72m) pumping station in Jeddah to be complete in Q2 2013.

5

Jeddah prime rental clock

*Hotel clock reflects the movement of RevPAR.

Note: The property clock illustrates where Jones Lang LaSalle estimate each prime market is within its individual rental cycle as at end of relevant quarter.

Source: Jones Lang LaSalle

5

Jeddah office market overview

Office supply and demand

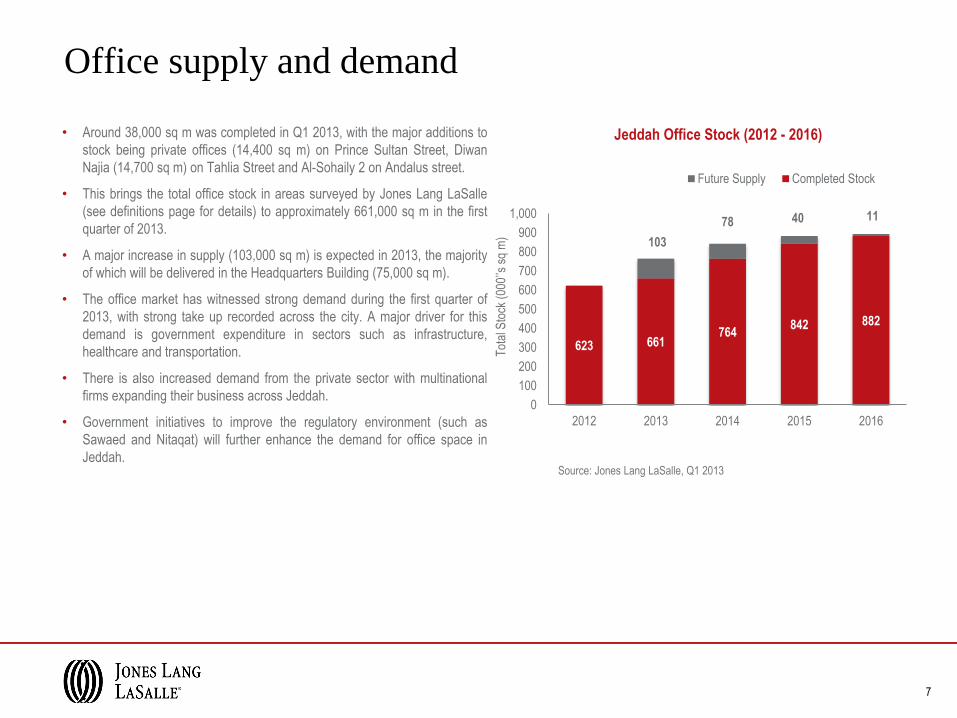

• Around 38,000 sq m was completed in Q1 2013, with the major additions to

stock being private offices (14,400 sq m) on Prince Sultan Street, Diwan

Najia (14,700 sq m) on Tahlia Street and Al-Sohaily 2 on Andalus street.

• This brings the total office stock in areas surveyed by Jones Lang LaSalle

(see definitions page for details) to approximately 661,000 sq m in the first

quarter of 2013.

• A major increase in supply (103,000 sq m) is expected in 2013, the majority

of which will be delivered in the Headquarters Building (75,000 sq m).

• The office market has witnessed strong demand during the first quarter of

2013, with strong take up recorded across the city. A major driver for this

demand is government expenditure in sectors such as infrastructure,

healthcare and transportation.

• There is also increased demand from the private sector with multinational

firms expanding their business across Jeddah.

• Government initiatives to improve the regulatory environment (such as

Sawaed and Nitaqat) will further enhance the demand for office space in

Jeddah.

Source: Jones Lang LaSalle, Q1 2013

7

Tot

al S

tock

(00

0‟‟s

sq

m)

623 661 764

842 882

103

78 40 11

0

100

200

300

400

500

600

700

800

900

1,000

2012 2013 2014 2015 2016

Jeddah Office Stock (2012 - 2016)

Future Supply Completed Stock

8 8

Major Existing & Future Offices Projects

1 KAFD

2 ITCC

Existing

Olaya Towers

MIG Tower

8

Major existing & future offices projects 1 Zahran

2 King Road Tower

3 Bin Sulaiman

4 Jameel Square

1

3

1 3

2

4

Existing

Future

4

2 Murjan Tower

2

5 Jeddah 7575

5

1 Headquarters

3 Al Khair Tower

6 Private Offices

7 Diwan Najyah

6

7

Rental performance

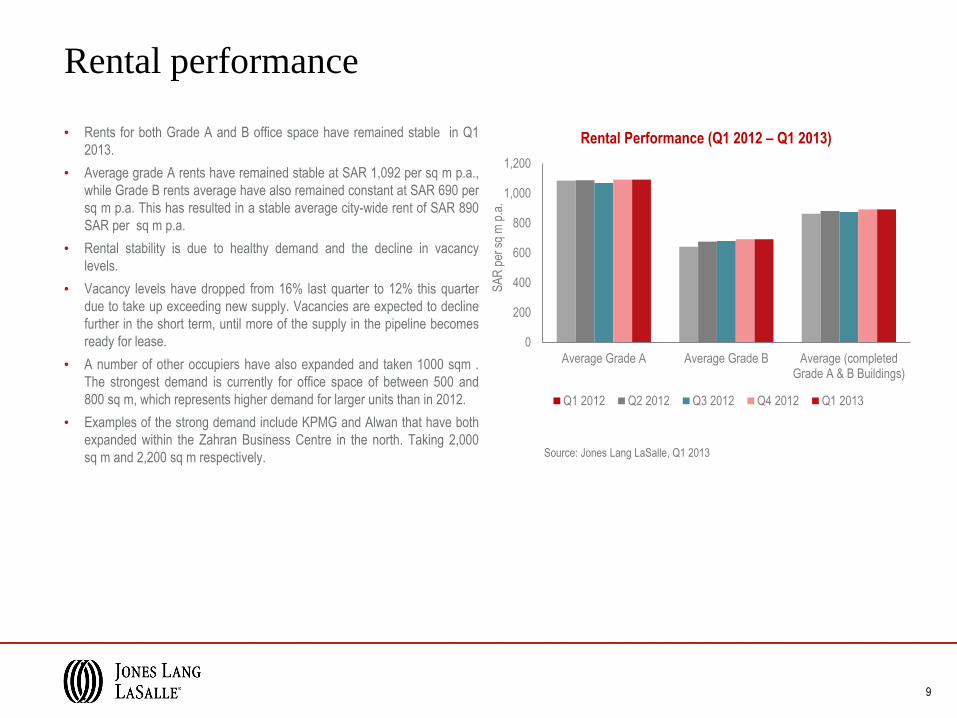

• Rents for both Grade A and B office space have remained stable in Q1

2013.

• Average grade A rents have remained stable at SAR 1,092 per sq m p.a.,

while Grade B rents average have also remained constant at SAR 690 per

sq m p.a. This has resulted in a stable average city-wide rent of SAR 890

SAR per sq m p.a.

• Rental stability is due to healthy demand and the decline in vacancy

levels.

• Vacancy levels have dropped from 16% last quarter to 12% this quarter

due to take up exceeding new supply. Vacancies are expected to decline

further in the short term, until more of the supply in the pipeline becomes

ready for lease.

• A number of other occupiers have also expanded and taken 1000 sqm .

The strongest demand is currently for office space of between 500 and

800 sq m, which represents higher demand for larger units than in 2012.

• Examples of the strong demand include KPMG and Alwan that have both

expanded within the Zahran Business Centre in the north. Taking 2,000

sq m and 2,200 sq m respectively.

9

0

200

400

600

800

1,000

1,200

Average Grade A Average Grade B Average (completedGrade A & B Buildings)

Rental Performance (Q1 2012 – Q1 2013)

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

Source: Jones Lang LaSalle, Q1 2013

SA

R p

er s

q m

p.a

.

Office market summary

10

Indicator Level Comment / Outlook

Current Office Stock (CBD) 661,000 sq m

Includes Grade A & B buildings within the CBD. Increase in stock in

Q1 2013 is due to the completion of Private Offices, Diwan Najia and

Al-Sohaily 2. Total city-wide stock is estimated to be around 1.8 million

sq m GLA.

Future Supply (2013 – 2016) 232,000 sq m Major future supply will be available on major roads such as Madinah

and Prince Sultan.

CBD Vacancy 12%

The vacancy rate has decreased, due to

continued strong demand.

Average CBD Rental

Average – Grade A Rental

Average – Grade B Rental

SAR 890 per sq m p.a.

SAR 1,092 per sq m p.a.

SAR 690 per sq m p.a..

No change in Q1 2013 with prospects for

stable rental levels in 2013

Jeddah residential market overview

Residential supply and demand

• Apart from a small number of mega government projects, the majority of

new residential supply is coming from individuals and small developers

undertaking small scale projects.

• Approximately 4,500 units were completed in projects monitored by

Jones Lang LaSalle during first quarter of 2013. This new supply has all

been in small projects comprising between 40-100 units, with no major

projects completed.

• A further 15,000 additional residential units are expected to be completed

during the remainder of 2013. Once again the majority of this new supply

will be in small projects.

• Aayan Real Estate Development will complete its Diyar Jaddah 2 project

located in South Obhor in the final quarter of 2013.

• Da‟em Residences, offering 120 units (expected to be completed by

2015) is the only major project announced during Q1 2013.

• Ewan has commenced construction of the second phase of its Al Faridah

Residential Project (460 units) as well as commencing the infrastructure

work for the third and fourth phases.

• A number of major high-rise towers located on the Corniche are expected

to complete during 2013 including Al Jawhara Tower, developed by

Damac and the Beach Tower.

• Diyar Jeddah Fund has progressed with the servicing of raw land in its

new subdivision “Diyar Jeddah 2”, located east of Jeddah.

Source: Jones Lang LaSalle, Q1 2013

12

735 739 754

778 803

15

24

25

24

680

700

720

740

760

780

800

820

840

2012 2013 2014 2015 2016

Tot

al S

tock

(N

umbe

r of

uni

ts in

000

's)

Jeddah Residential Stock (2012 - 2016)

Future Supply Completed Stock

13

Major existing & future residential projects

1

2 1

3 2

3

4

5 6

Existing

Future

7

4

1 JDURC

2 Fareeda

3 Masharef

4 PPA

5 Lamar

6 Jawhara

7 Kingdom Tower

1 Diyar Al-Bahar

2 Farsi Towers

3 Corniche Dreams

Jeddah Gate 4

Residential sale prices

• The average sale price of villas in those locations monitored by

Jones Lang LaSalle has increased to SAR 4,600 per sq m in Q1 2013.

Average villa prices are however remain at the same level as Q1 2012.

• This average disguises considerable variation between different districts.

Sale prices for villas continued to increase in the Western districts of

Jeddah during Q1. In the North, the previous decline has been reversed

with a small increase recorded in Q1. North East districts have seen

prices continue to decline due to new supply.

• The Western region (closest to the Red Sea) remains the prime location

for villas, with the price exceeding SAR 6,600 per sq m in selective

locations.

• Demand for apartments is currently higher than that for villas in Jeddah,

which is keeping average prices stable.

• The average asking price for apartments has remained stable during Q1

at SAR 4,150 per sq m.

• The average sale price of apartments has declined slightly in the South

and West districts of Jeddah while prices of apartments in the East

continue to increase. It should be noted that this data does not include

high end waterfront projects and apartments e.g Jeddah Gate.

14

Source: Jones Lang LaSalle, Q1 2013 Source: Jones Lang LaSalle, Q1 2013

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

West North North-East

Villa - Average Sales Price

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

0

1,000

2,000

3,000

4,000

5,000

6,000

West East South

Apartment - Average Sales Price

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

SA

R/p

er s

q m

SA

R/p

er s

q m

Rental performance

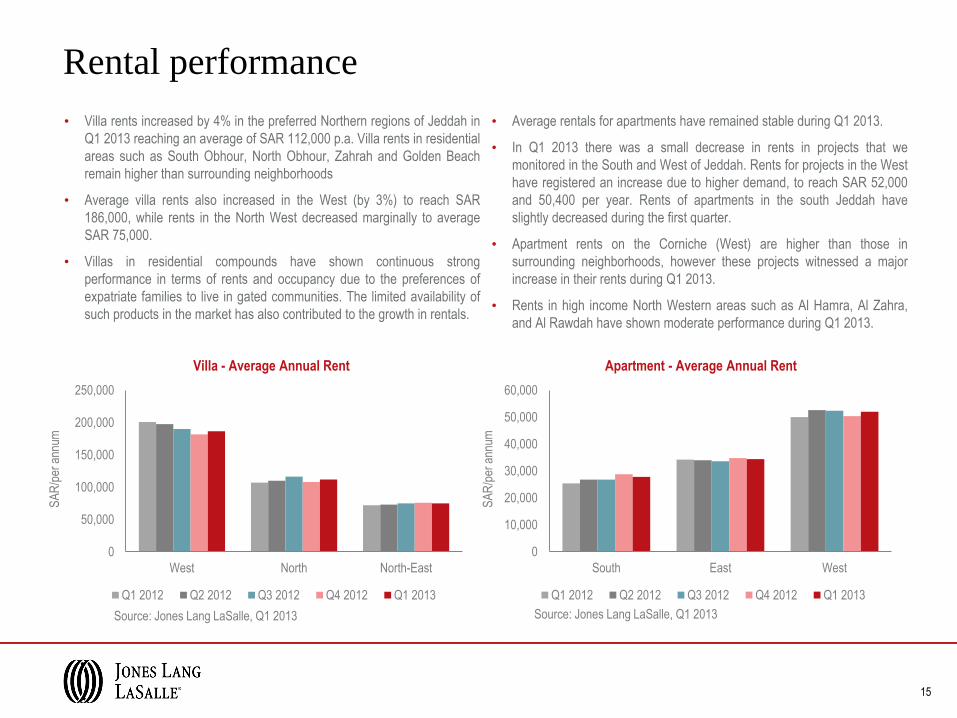

• Villa rents increased by 4% in the preferred Northern regions of Jeddah in

Q1 2013 reaching an average of SAR 112,000 p.a. Villa rents in residential

areas such as South Obhour, North Obhour, Zahrah and Golden Beach

remain higher than surrounding neighborhoods

• Average villa rents also increased in the West (by 3%) to reach SAR

186,000, while rents in the North West decreased marginally to average

SAR 75,000.

• Villas in residential compounds have shown continuous strong

performance in terms of rents and occupancy due to the preferences of

expatriate families to live in gated communities. The limited availability of

such products in the market has also contributed to the growth in rentals.

• Average rentals for apartments have remained stable during Q1 2013.

• In Q1 2013 there was a small decrease in rents in projects that we

monitored in the South and West of Jeddah. Rents for projects in the West

have registered an increase due to higher demand, to reach SAR 52,000

and 50,400 per year. Rents of apartments in the south Jeddah have

slightly decreased during the first quarter.

• Apartment rents on the Corniche (West) are higher than those in

surrounding neighborhoods, however these projects witnessed a major

increase in their rents during Q1 2013.

• Rents in high income North Western areas such as Al Hamra, Al Zahra,

and Al Rawdah have shown moderate performance during Q1 2013.

15

0

50,000

100,000

150,000

200,000

250,000

West North North-East

Villa - Average Annual Rent

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

0

10,000

20,000

30,000

40,000

50,000

60,000

South East West

Apartment - Average Annual Rent

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

Source: Jones Lang LaSalle, Q1 2013 Source: Jones Lang LaSalle, Q1 2013

SA

R/p

er a

nnum

SA

R/p

er a

nnum

Residential market summary

Note: Direction arrows are based on the performance of the REIDIN monthly index.

16

Indicator Level Comment / Outlook

Current Residential Stock 739,000 units Based on National Housing Census (2010) and units completed in

locations monitored by Jones Lang LaSalle since 2010.

Future Supply (2013 – 2016) 89,000 additional units in

all projects

New affordable housing stock built by JDURC, PPA and the Ministry of

Housing may increase this figure.

Average 3 Bed Apartment

Rent SAR 38,000 p.a.

Apartment rents expected to increase further throughout

2013 due to higher demand for apartments for lease

from expatriates.

Average 3 Bed

Apartment Sale Price SAR 4,150 per sq m

Increase in middle priced units will escalate average

prices.

Average 4 Bed Villa Rent SAR 124,000 p.a. Rents are expected to increase despite significant

additions to supply.

Average 4 Bed Villa Sale Price SAR 4,600 per sq m Average villa sale price has remained stable in Q1 but is

expected to increase over the coming year

Jeddah retail market overview

780 780 873

969 1,044

93 96

75

0

200

400

600

800

1,000

1,200

2012 2013 2014 2015 2016

Jeddah Retail Stock (2012 – 2016)

Future Supply Completed Stock

Tot

al S

tock

(„0

00 s

q m

)

Retail supply and demand

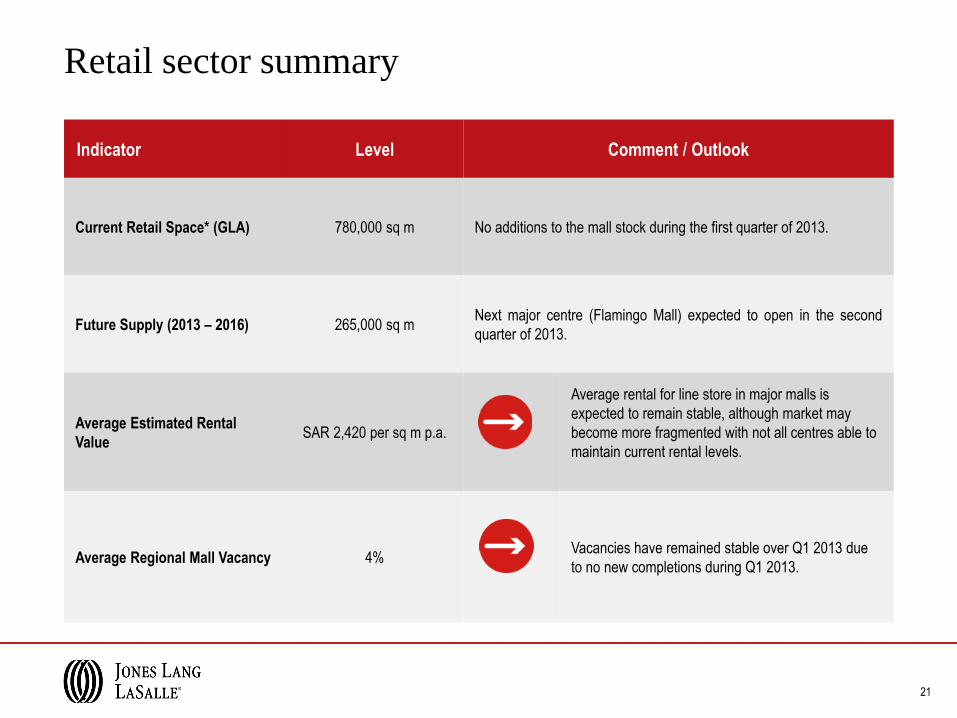

• There were no additions to shopping mall stock in Jeddah during Q1 2013.

• At the first quarter, the total stock of mall based retail space in Jeddah

stayed constant at 780,000 sq m. Flamingo Mall on Prince Majid road is

the next major mall expected to be completed in the second quarter of

2013.

• We are witnessing strong demand from retailers for locations to the North

and North East of Jeddah to service the residential growth planned in this

area.

• There also remains demand from retailers for malls located in the city

center, such as Tahliyah, due to high population and workforce

catchments in central Jeddah.

• The Red Sea Mall (one of the leading retail centers in Jeddah) has

reopened after a recent fire. The repositioning of non performing retail

centers also continues.

• Mall operators continue to refresh their tenant mix and replace existing

tenants with better quality brands to maintain high footfall.

Source: Jones Lang LaSalle, Q1 2013

18

19 19

Major existing & future retail projects 1 Red Sea mall

2 Arab Mall

1 Le Prestige

2 Galleria

3 Andalus Mall

1

3

2

3 Sairafi 2

4 Flamingo

1

2

4

3

Existing

Future

4 Le Beteau

5 Stars Avenue

4 5

Rental Performance – Estimated Rental Value (ERV)

• Overall ERV‟s remain stable across all types of retail centres, with a

slight increase on average in regional shopping malls. The average ERV

is approximately SAR 2,420 per sq m p.a. in Q1 2013.

• Most of the newer shopping malls have high occupancy rates. Demand is

strong and all centres under construction have managed to prelease a

significant proportion of their space. Increased take up in Central Park

has kept the market wide vacancy rate around 4% in Q1 2013.

• Mall rents are expected to remain stable over the second half of 2013.

• Increasing occupancy of regional malls has resulted in a marginal

increase in average rentals of regional malls from SAR 2,367 per sq m to

SAR 2,392 per sq m. Average rentals in community malls have reduced

by a similar marginal amount during Q1.

• Entertainment options and F&B retailers continue to be a major source of

attraction and differentiation between malls in Jeddah.

• With no completions during Q1 2013, projects that are under construction

(eg La Prestige and Flamingo Mall) are experiencing continued demand

and have preleased significant space before opening.

• Strip retail centers continue to perform well across the city due to high

demand from customers. We see future opportunities for this product,

especially towards the north and north east of Jeddah.

20

Source: Jones Lang LaSalle, Q1 2013

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

Community Regional Super Regional

SA

R/p

er s

q m

Average Retail Rentals

Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012

Indicator Level Comment / Outlook

Current Retail Space* (GLA) 780,000 sq m No additions to the mall stock during the first quarter of 2013.

Future Supply (2013 – 2016) 265,000 sq m Next major centre (Flamingo Mall) expected to open in the second

quarter of 2013.

Average Estimated Rental

Value SAR 2,420 per sq m p.a.

Average rental for line store in major malls is

expected to remain stable, although market may

become more fragmented with not all centres able to

maintain current rental levels.

Average Regional Mall Vacancy 4% Vacancies have remained stable over Q1 2013 due

to no new completions during Q1 2013.

Retail sector summary

21

Jeddah hotel market overview

11,300 11,300 12,750 12,750

1,440 311

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2012 2013 2014 2015

No.

of R

oom

s

Completed Stock Future Supply

Hotel supply

• There have been no major supply additions to the Jeddah market over the past three years and no projects were completed in Q1 2013.

• With many of the proposed projects currently on hold or cancelled, no new hotels are expected enter the Jeddah market during 2013.

• There are a number of projects that could deliver an additional 1,440 rooms over the remainder of 2013. These include the Rocco Forte, Novotel Jeddah, Elaf Galleria on Tahliah Road, the Dusit Thani overlooking the Obhur Creek, the Park Inn by Radisson and the Ibis Jeddah on Malik Road. In reality many of these projects are likely to experience further delays and not enter the market in 2014.

• These additions will increase the total hotel room supply in Jeddah to around 13 000 quality hotel rooms by the end of 2015, an increase of around 15% on the current stock of rooms.

• Looking forward, the hospitality supply is spreading from the North Corniche Strip and moving further inland as well as to the north of Jeddah.

Source: Jones Lang LaSalle, Q1 2013

23

Jeddah Hotel Stock (2012 – 2015)

Hotel performance

• Jeddah remained one of the best performing hotels markets in the

Middle East in terms of occupancy during 2012.

• Occupancy levels have increased continuously since 2010 but are

now stabilising, with Q1 2013 recording the same occupancy level as

Q1 2012 (78%).

• Average room rates (ADR) have also registered a continuous

increase since 2010, 2012 showed an increase of 9.3% over last

year. On a YT [explain] March basis, the ADR increased by 10.3% in

comparison to YT March 2012.

• The combination of stabilized occupancy and higher room rates have

resulted in a 10% growth in RevPAR over YT March 2012 at USD

182.

• The strong performance of the hotel sector reflects the continued

attractiveness of Jeddah as a leisure destination for Saudi families.

Source: STR Global

24

Hotel Performance (2008 – YT March 2013)

170 182 190 204 223 212 234

74% 73% 68%

71%

79% 78% 78%

30%

40%

50%

60%

70%

80%

90%

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 YTD2012

YTD2013

Occ

upan

cy (

%)

AD

R (

in U

SD

)

Average Daily Rate Occupancy Rate

Hotel market summary

25

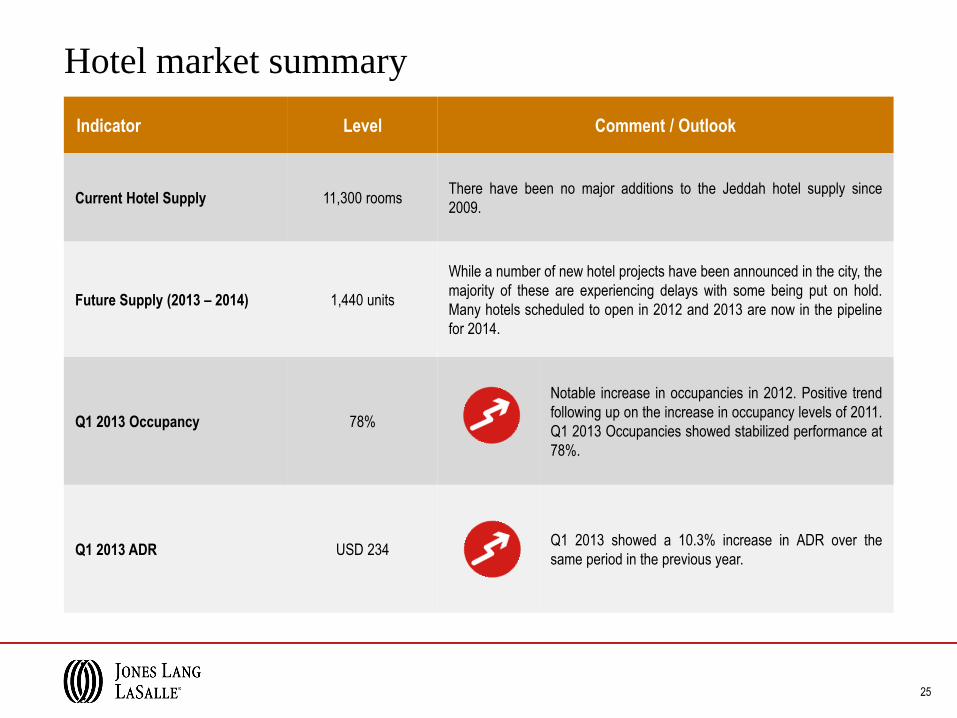

Indicator Level Comment / Outlook

Current Hotel Supply 11,300 rooms There have been no major additions to the Jeddah hotel supply since

2009.

Future Supply (2013 – 2014) 1,440 units

While a number of new hotel projects have been announced in the city, the

majority of these are experiencing delays with some being put on hold.

Many hotels scheduled to open in 2012 and 2013 are now in the pipeline

for 2014.

Q1 2013 Occupancy 78%

Notable increase in occupancies in 2012. Positive trend

following up on the increase in occupancy levels of 2011.

Q1 2013 Occupancies showed stabilized performance at

78%.

Q1 2013 ADR USD 234 Q1 2013 showed a 10.3% increase in ADR over the

same period in the previous year.

Definitions and Methodology Residential: • The supply data is based on the National Housing Census

(2010) and our quarterly survey of major projects and stand

alone developments in selected areas of:

• Completed building refers to a building that is handed over for

immediate occupation.

• Residential performance data is based on two separate

baskets one for rentals in villas and apartments and another

basket for sales performance for both villas and apartments.

The two baskets cover projects in selected locations across

Jeddah.

Retail: • Retail supply data covers floor space of organised malls over

10,000 sq m. Classification of Retail Centres is based upon

the ULI definition as published in Retail Development, 4th

Edition published by ULI.

• Rent represents the quoted average rent for the major

shopping malls in Jeddah Retail supply relates to the Gross

Lettable Area (GLA) within retail malls.

Office: • The supply data is based on our quarterly survey of the Grade

A & B office space located in the Jeddah CBD, defined as

Prince Sultan, Tahlia, Al-Malek, Ibrahim Al Jaffali, Madinah,

King Abdullah and Rowdah Streets.

• Completed building refers to a building that is handed over for

immediate occupation.

• Prime Office Rent represents the top open-market rent that

could be expected for a notional office unit of the highest

quality and specification in the best location in a market, as at

the survey date (normally at the end of each quarter period).

The Prime Rent reflects an occupational lease that is standard

for the local market. It is a face rent that does not reflect the

financial impact of tenant incentives, and excludes service

charges and local taxes.

Hotels: • Hotel room supply is based on existing supply figures

provided by Saudi Commission for Tourism and Antiques as

well as future hotel development data tracked by Jones Lang

LaSalle Hotels. Room supply includes all graded supply and

excludes serviced apartments.

• STR performance data is based on monthly survey conducted

by STR Global.

26

Market Sector Districts Covered

North (Villa) North Obhor and South Obhor

West (Villa) Basateen, Shatie, Mohammadia

North-East (Villa) Asfan, Salhia, Kassarat

West (Apt) Zahra, Rowdah, Salamah, Hamra

East (Apt) Al Marwah, Safa, Al Manar, Naseem

South (Apt) Waziria, Shafa, Madaen Al Fahad, Ajaweed

www.jll–mena.com

COPYRIGHT © JONES LANG LASALLE IP, INC. 2013

This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior

written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation is

made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not accept

any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Contacts:

@JLLNews youtube.com/joneslanglasalle linkedin.com/company/jones-lang-lasalle joneslanglasalleblog.com/EMEAResearch

Peter Bibby

Co-Head

Jeddah

Craig Plumb

Head of Research

MENA

John Harris

Co-Head

Riyadh

Fayyaz Ahmad

Associate Director, Advisory

Saudi Arabia

Andrew Williamson

Head of Retail

MENA

Diyaa Ayoub

Senior Analyst

Saudi Arabia

Gabriel Matar

Director, MEA

Hotels & Hospitality Group