japan insurance market 2010

TRANSCRIPT

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 1/43

The Toa Reinsurance Company, Limited

Japan’s Insurance Market 2010

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 2/43

To Our Clients

Hiroshi Fukushima

President and Chief Executive, The Toa Reinsurance Company, Limited 1

1. Trends in Japan’s P&C Insurance Market and Sompo Japan’s Business Strategy Kengo Sakurada

President and Chief Executive Officer, SOMPO JAPAN INSURANCE INC. 2

2. New Developments in the Regulation and Supervision of Japan’s Non-Life Insurance Industry

Naohiko Matsuo

Attorney-at-law, Admitted In Japan & New York Nishimura & Asahi

(Former Director for Financial Instruments and Exchange Act and General Counsel of the Financial Services Agency of Japan) 8

3. Challenges of the Major Japanese General Insurance Groups in Promoting Global OperationsKatsuo Matsushita

Special Advisor and Liaison Officer for Japan and East Asia of the Geneva Association 15

4. A Foreign Insurer’s Perspective on Japan

Neil C. A. Smith

Regional President, ACE Far East

(Vice Chairman, & Past Chairman, of Foreign Non-Life Insurance Association of Japan) 19

5. Trends in Japan’s Non-Life Insurance Industry

Underwriting & Planning Department

The Toa Reinsurance Company, Limited 26

6. Trends in Japan’s Life Insurance Industry

Life Underwriting & Planning Department

The Toa Reinsurance Company, Limited 31

Supplemental Data: Results of Japanese listed non-life insurance groups (company)

for fiscal 2009, ended March 31, 2010 (Non-Consolidated Basis) 40

Japan’s Insurance Market 2010

Contents Page

©2010 The Toa Reinsurance Company, Limited. All rights reserved. The contents may be reproduced only with the written permission

of The Toa Reinsurance Company, Limited.

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 3/43

1

Hiroshi Fukushima President and Chief Executive,The Toa Reinsurance Company, Limited

To Our Clients

It gives me great pleasure to have the opportunity to welcome you to our brochure, ‘Japan’s

Insurance Market 2010.’ It is encouraging to know that over the years our brochures have been well

received even beyond our own industry’s boundaries as a source of useful, up-to-date information about

Japan’s insurance market, as well as contributing to a wider interest in and understanding of our domes-

tic market.

During fiscal 2009, the year ended March 31, 2010, the Japanese economy remained generally

lackluster. Although personal consumption picked up thanks to the government’s economic stimulus

package and exports increased, centering on those for emerging economies, the situation regarding

employment and personal income remained sluggish and deflation continued.In the non-life insurance industry in Japan, all lines of businesses were adversely affected by the sluggish

economy; in particular, a decline in logistics led to lower premium income from marine insurance. In the life

insurance industry in Japan, the tough situation continued, centering on death benefit products, reflecting the

declining population owing to the low birth rate and also the lackluster economy.

The reinsurance market, after hardening mainly because of decreases in reinsurers’ capital amid the

financial crisis, softened somewhat in line with the recovery of capacity in the second half of fiscal 2009.

Far-reaching changes in the operating environment of the Toa Re Group are in prospect owing to

climate change, the increasing size and complexity of risks, and revisions to international regulations and

systems for reinsurance.

In order to respond to these changes in the business environment in a timely and effective manner,

and to achieve sustainable growth of the Toa Re Group, we recognize that the provision of high added

value services to our customers and the reinforcement of risk management and other internal control

systems throughout the Group are important issues. With the aim of promoting the development of the

entire Group and enhancing our corporate value, we formulated a medium-term management plan,

“Crescendo 2011.” Inspired by this vision, the Toa Re Group is making a concerted effort to achieve the

goals set in this plan.

By endeavoring to act as an exemplary reinsurance company, we are resolved to fulfill our mission:

“Providing Peace of Mind.”

In conclusion, I hope that our brochure will provide a greater insight into the Japanese insurancemarket and I would like to express my gratitude to all who kindly contributed so much time and effort

towards its making.

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 4/43

2

As of April 1, 2009, Japan’s property and casualty (P&C) insurance industry

comprised 51 P&C insurance companies, including 5 reinsurance companies. This

industry provided P&C insurance products and services through approximately

220,000 agencies, 33 insurance brokers, and direct sales.

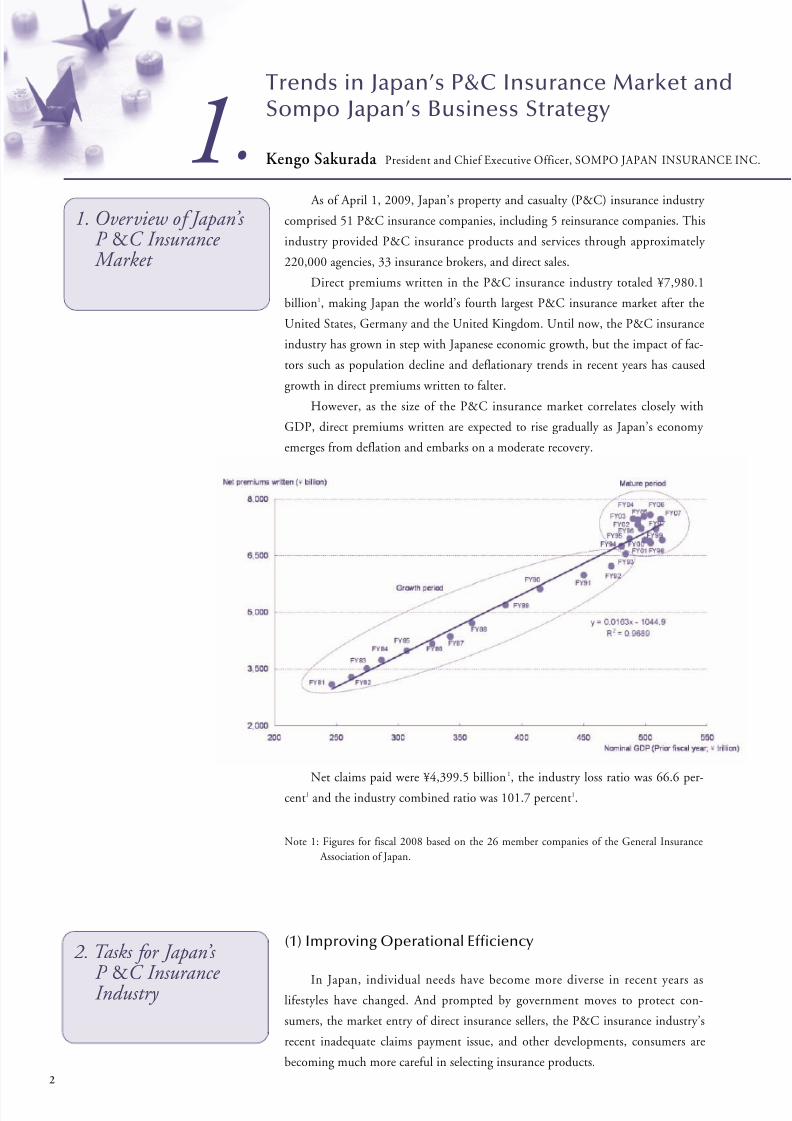

Direct premiums written in the P&C insurance industry totaled ¥7,980.1

billion1, making Japan the world’s fourth largest P&C insurance market after the

United States, Germany and the United Kingdom. Until now, the P&C insurance

industry has grown in step with Japanese economic growth, but the impact of fac-

tors such as population decline and deflationary trends in recent years has caused

growth in direct premiums written to falter.However, as the size of the P&C insurance market correlates closely with

GDP, direct premiums written are expected to rise gradually as Japan’s economy

emerges from deflation and embarks on a moderate recovery.

Net claims paid were ¥4,399.5 billion1, the industry loss ratio was 66.6 per-

cent1 and the industry combined ratio was 101.7 percent1.

Note 1: Figures for fiscal 2008 based on the 26 member companies of the General Insurance

Association of Japan.

(1) Improving Operational Efficiency

In Japan, individual needs have become more diverse in recent years aslifestyles have changed. And prompted by government moves to protect con-

sumers, the market entry of direct insurance sellers, the P&C insurance industry’s

recent inadequate claims payment issue, and other developments, consumers are

becoming much more careful in selecting insurance products.

1. Kengo Sakurada President and Chief Executive Officer, SOMPO JAPAN INSURANCE INC.

Trends in Japan’s P&C Insurance Market andSompo Japan’s Business Strategy

2. Tasks for Japan’s

P &C Insurance Industry

1. Overview of Japan’s P &C Insurance

Market

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 5/43

3

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

Customers are placing increased quality demands on P&C insurance compa-

nies. They expect, for example, products that are easy to understand and rationally

priced, thorough policy explanations, and prompt, fair claims payment.

Companies must raise the quality of their operations to meet the needs and expec-

tations of customers.

(2) Enhancing Profitability in the Japanese Market

Amid a declining birthrate, societal aging and population decline in Japan,

the markets for automobile and fire insurance, which account for approximately 75 percent of direct premiums written, are maturing and rapid growth in premi-

ums seems doubtful.

However, Japan’s ¥8 trillion P&C insurance market is unlikely to contract

sharply. So a key issue for Japanese P&C insurance companies is to enhance the

quality of their operations to garner customer support while also enhancing opera-

tional efficiency, using information and communication technologies (ICT) in

order to raise profitability.

(3) Business Development in Foreign Countries

In the meantime, each Japanese P&C insurance company is expanding its

overseas business, as it is regarded as a growing field. An important part of future

growth strategy for Japan’s major P&C insurance companies will be to enter busi-

ness in countries in which further economic growth is expected and the penetra-

tion rate of insurance is still low, such as China, India and ASEAN nations. This is

significant from the perspective of contributions to develop in these regions and to

people’s higher quality of life through the benefit of insurance.

(4) Dealing with Environmental Issues

Japan has always been prone to natural catastrophes such as earthquakes and

typhoons. Extreme weather caused by recent climate change has made natural

catastrophes more intense and frequent, and awareness of environmental issues is

increasing.

Society will adapt globally and rapidly to environmental issues in various

ways, such as accelerating research and development of environmental technolo-

gies, expanding the use of electric vehicles and wind power generation, and creat-

ing financial mechanisms to mitigate the effects of climate change.

In light of these circumstances, not only will Japan’s P&C insurance industry

need to deal with risks by improving methods for quantifying natural catastrophe

risks, increasing underwriting capacity, and hedging through reinsurance. The

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 6/43

4

industry must also seize society’s environmental needs as business opportunities

and proactively deal with environmental issues by providing products and services

that help decrease environmental loads.

(1) Emergence of Three Mega Groups

As mentioned above, Japan’s P&C insurance industry must enhance opera-

tions’ quality and efficiency. Companies in the industry, primarily major players,continue to restructure to realize both of these objectives and to efficiently deploy

resources in areas of high growth potential. On April 1, 2010, Sompo Japan

Insurance Inc. and Nipponkoa Insurance Co., Ltd. established a joint-holding

company for business integration, as did Mitsui Sumitomo Insurance Co., Ltd.,

Aioi Insurance Co., Ltd. and Nissay Dowa General Insurance Co., Ltd. This her-

alds a new era of fierce competition mainly among three mega groups – the NKSJ

Group, the MS&AD Group and the Tokio Marine Group – whose combined

market share is approximately 90 percent.

(2) NKSJ Group’s Vision and Strategy

Sompo Japan and Nipponkoa established NKSJ Holdings, Inc., a joint hold-

ing company in April 2010. Aiming to contribute to society as a corporate group,

the NKSJ Group makes all value judgements from the customer’s perspective and

provides customers with absolute security and services of the highest quality.

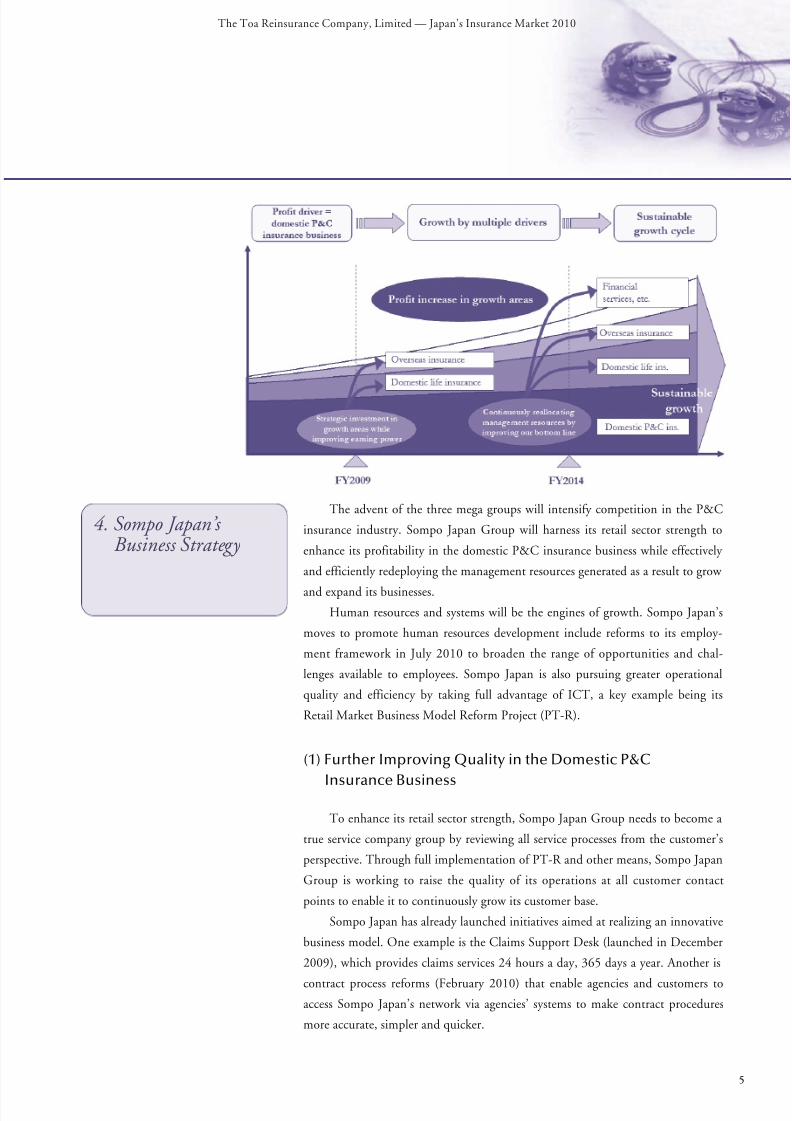

The NKSJ Group will build a well-balanced business portfolio by further

enhancing profitability in its domestic P&C insurance business, a profit driver,

and shifting management resources generated as a result to promising areas such as

its domestic life insurance (especially medical insurance) and overseas insurance

businesses. The NKSJ Group will then expand its businesses through a sustained

growth cycle whereby increased earnings from multiple profit drivers are reinvested

in growing businesses.

The NKSJ Group is targeting adjusted profit of ¥160.0 billion and adjusted

ROE of 7 percent in fiscal 2014.

1. Trends in Japan’s P&C Insurance Market and Sompo Japan’s Business Strategy

3. Industry Reorganization and

the NKSJ Group

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 7/43

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

5

The advent of the three mega groups will intensify competition in the P&C

insurance industry. Sompo Japan Group will harness its retail sector strength to

enhance its profitability in the domestic P&C insurance business while effectively

and efficiently redeploying the management resources generated as a result to grow

and expand its businesses.

Human resources and systems will be the engines of growth. Sompo Japan’s

moves to promote human resources development include reforms to its employ-

ment framework in July 2010 to broaden the range of opportunities and chal-

lenges available to employees. Sompo Japan is also pursuing greater operational

quality and efficiency by taking full advantage of ICT, a key example being its

Retail Market Business Model Reform Project (PT-R).

(1) Further Improving Quality in the Domestic P&C

Insurance Business

To enhance its retail sector strength, Sompo Japan Group needs to become a

true service company group by reviewing all service processes from the customer’s

perspective. Through full implementation of PT-R and other means, Sompo Japan

Group is working to raise the quality of its operations at all customer contact

points to enable it to continuously grow its customer base.

Sompo Japan has already launched initiatives aimed at realizing an innovative

business model. One example is the Claims Support Desk (launched in December

2009), which provides claims services 24 hours a day, 365 days a year. Another is

contract process reforms (February 2010) that enable agencies and customers to

access Sompo Japan’s network via agencies’ systems to make contract procedures

more accurate, simpler and quicker.

4. Sompo Japan’s Business Strategy

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 8/43

6

(2) Enhancing the Profitability of the Domestic P&C

Insurance Business

Sompo Japan will work assiduously to improve profitability while providing

high-quality products and services through high-quality operations. Specific efforts

include expanding market share by strengthening its sales network and customer

relationships, reducing business expenses by raising businesses’ operating efficiency,

improving its loss ratio by enhancing its underwriting operations, and bolstering

investment capabilities.

Sompo Japan aims to rapidly capitalize on the synergistic effects of itsbusiness integration with Nipponkoa and increase profitability. The group will

establish a highly productive, cost-competitive administrative structure whereby

products and administrative systems are integrated, infrastructure is shared, and

procurement is handled jointly.

(3) Strengthening and Diversifying Sources of Earnings

through Growth in Group Businesses

While strengthening the profitability of its domestic P&C insurance business,

Sompo Japan Group will also continue shifting management resources into

growth areas to expand other areas such as its domestic life insurance (especially

medical insurance) and overseas insurance businesses.

Sompo Japan Group continues to grow steadily in the life insurance business,

backed by strong customer support for Sompo Japan Himawari Life Insurance’s

medical insurance product, for instance. Himawari Life will continue to pursue

growth and plans to merge with Nipponkoa Life in October 2011.

In its overseas insurance business, Sompo Japan Group intends to expand

earnings by using mergers, acquisitions, and alliances to develop business in local

markets in countries such as the BRICs, which promise strong growth and prof-itability. Sompo Japan Group will also strengthen its reinsurance business in over-

seas markets.

* Sompo Japan Group is engaged in broad-ranging P&C insurance business activities in China

through four locations in Liaoning Province, Shanghai, Guangdong Province and Jiangsu

Province. Sompo Japan Group has established a Regional Headquarters in Singapore to fur-

ther develop business in the ASEAN countries, where it employs more than 800 high-caliber

staff across 7 countries.

In India, Sompo Japan Group has established Universal Sompo General Insurance, a joint

venture with local banks and other companies. Universal Sompo is now selling insurance

products through 4,800 bank branches and other marketing channels.

Sompo Japan Group entered the Brazilian P&C insurance business through a subsidiary 50years ago, and has subsequently expanded its business by, for example, acquiring Marítima

Seguros S.A. in 2009.

Sompo Japan Group plans to continue expanding its reinsurance business in Asia and the

Middle East by utilizing its excellent credit ratings and offering long-term stable reinsurance

capacity.

1. Trends in Japan’s P&C Insurance Market and Sompo Japan’s Business Strategy

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 9/43

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

7

(4) CSR and Environmental Initiatives

To achieve sustained growth together with society, the Sompo Japan Group

must meet stakeholders’ diverse expectations by bringing its insurance business

strengths to bear in helping to solve societal issues, with each and every employee

thinking and acting with initiative.

The Sompo Japan Group is actively working on four material CSR issues:

adaptation to and mitigation of climate change; risk management for safety and

security; CSR financing; and community involvement. For example, Sompo Japan

Group has developed a weather index insurance scheme for farmers in northeastThailand to help them counter the effects of climate change. The product is

offered as an option to bank loan customers. Sompo Japan Group also has devel-

oped eco-funds, continuously holds public seminars on the environment, and pro-

motes Eco-safe Driving, a program that helps to protect the environment and pre-

vent accidents.

These activities have attracted domestic and international recognition. For

example, Sompo Japan was recently selected for the second consecutive year as one

of the Global 100 Most Sustainable Corporations in the World, announced annu-

ally at the Davos World Economic Forum.

Financial industry performance languished in fiscal 2008 amid global eco-

nomic turmoil triggered by Lehman Brothers’ collapse. The effects have eased in

fiscal 2009 and the outlook for the business environment is less gloomy. However,

concern about sovereign risk sparked by Greece’s financial woes has spread and

circumstances remain unpredictable.

While the operating environment is challenging, Sompo Japan Group will

strive to be the best insurance group in Japan in three respects by developinghuman resources and using ICT while upholding its customer-first principle,

which it has consistently adhered to for more than 120 years since inception.

Specifically, Sompo Japan Group will strive to achieve the greatest customer satis-

faction, employ the best talent in terms of employees and agencies, and provide

the quickest, simplest and easiest to understand services. By being the best in these

areas, Sompo Japan Group hopes to be the most trusted and most familiar services

industry group, its ultimate aim being to achieve sustained growth and continu-

ously enhance corporate value.

5. Conclusion

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 10/43

8

2 . Naohiko Matsuo Attorney-at-law, Admitted In Japan & New York

Nishimura & Asahi (Former Director for Financial Instruments and Exchange Act and

General Counsel of the Financial Services Agency of Japan)

New Developments in the Regulation andSupervision of Japan’s Non-Life InsuranceIndustry

More than 18 months have passed since events, including the collapse of

the U.S. company Lehman Brothers on September 15, 2008 and the bail out of

U.S. company American Insurance Group (AIG) the following day, that

touched off a global economic crisis. This market-driven financial crisis high-

lighted the systemic risk to which non-bank financial institutions such as secu-

rities and insurance companies are exposed. The third summit of G20 leaders

held in the United States on September 24 and 25, 2009 agreed on the orienta-

tion of strengthening global financial regulation and supervision, including key

financial institutions within the non-bank system, and this commitment was

reaffirmed at the fourth G20 summit held in Canada on June 26 and 27, 2010.

Japan is strengthening regulation and supervision of non-life insurance

companies as part of the process of strengthening global financial regulation

and supervision. Moreover, on September 16, 2009 a major political develop-

ment took place as a multi-party coalition centered on the Democratic Party

assumed the reins of government in Japan. A House of Councilors election held

on July 11, 2010 put the Democratic Party in a minority position at the House,

which would further complicate the process of policy development.

This paper examines new developments in the regulation and supervision

of Japan’s non-life insurance companies as a result of these significant changes

occurring in Japan and around the world.

(1) Policy-Making during Liberal Democratic Party

Administrations

Japan has a parliamentary system of government, in which the ruling party

forms a cabinet. The Liberal Democratic Party (LDP) had been in power con-

tinuously, with the exception of the period from August 1993 to June 1994,

from its formation in 1955 until the regime change of September 2009.

The key characteristic of the policy-making process during the LDP era

was that bureaucrats and the ruling party dominated policy. Undeniably, this

characteristic strongly influenced Cabinet and ministerial agendas.

For example, the typical process for planning and drafting amendments to

the Insurance Business Law regulating the insurance industry was 1) in July of a

particular year Financial Services Agency (FSA) officials studied potential

amendments following a personnel reshuffle; 2) from around September the

Financial System Council, an advisory body of experts and interested parties,

studied potential amendments and summarized them in a report in or around

December; 3) during this time, FSA officials negotiated with related ministries,

industries, consumer representatives and other interested parties to formulate a

draft bill and received a preliminary review from the Cabinet Legislation

Bureau; 4) in January and February FSA officials received a formal review from

1. Introduction

2. Changes in the Policy-Making Process in Japan’s Financial Sector

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 11/43

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

9

the Cabinet Legislation Bureau, conducted ongoing negotiations as needed with

interested parties, and obtained the approval of the administration by explain-

ing the subject amendments to the administration (administrative review) and

revising them as necessary; and 5) on or around March 10, the Cabinet

approved the amendments and presented them to the Diet.

The key characteristics of this policy-making process during the LDP era

were that first, FSA officials handled planning, proposals and policy coordina-

tion; secondly, the Financial System Council which was open to public provid-

ed a forum for policy coordination; and thirdly, on a political level, the

approval of the ruling party was more important than that of the Cabinet.

(2) Policy-Making under the New Regime

In contrast, the multi-party coalition led by the Democratic Party advo-

cates a policy-making process in which politicians, not bureaucrats, draft initia-

tives, and parties are unified within the government.

First, the three leaders of each ministry - the minister, vice minister and

secretary, each of whom are politicians in the government, - propose, coordi-

nate and decide their political agenda and provide guidance and oversight of

bureaucrats. In a related move, the Financial System Council has been suspend-

ed. On the other hand, bureaucrats with the required expertise mainly execute

and administer policy in accordance with relevant laws and regulations, and

provide advice on proposals, coordination and decisions by politicians.

Secondly, all of the functions of the ruling Democratic Party’s Policy Research

Council have shifted to the Cabinet, and ministerial policy councils chaired by

vice ministers at which the vice minister and bureaucrats confer with ruling-

party members have become the mechanism for exchanging views.

On March 9, 2010 the Cabinet finalized a partial revision of the Financial

Instruments and Exchange Act and submitted it to the Diet. This act included

proposed revisions to the Insurance Business Law that came before the Diet on

May 12, 2010 and were promulgated on May 19, 2010 (Act No. 32 of 2010).

The policy-making process leading up to the promulgation of this act is

clearly different. 1) On November 13, 2009 the three leaders of the FSA

announced the fundamental process for “Development of Institutional

Frameworks Pertaining to Financial and Capital Markets”; 2) on December 17,

2009 the FSA announced the proposed “Draft Blueprint for the Development

of Institutional Frameworks Pertaining to Financial and Capital Markets” and

began soliciting public comments; 3) on December 24 and 25, 2009, the FSA

exchanged views with interested organizations and experts; 4) on January 21,

2010 the FSA announced the “Development of Institutional Frameworks

Pertaining to Financial and Capital Markets”; and 5) the FSA Policy Council

exchanged views on amendments over the course of three meetings held on

January 22, February 25 and March 2, 2010.

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 12/43

10

This new policy-making process for the financial sector is still in its forma-

tive stage, and judgment would be premature. However, this writer sees three

key features. First, at the political level the government, rather than the ruling

party, has been driving the policy-making process. It should be noted, on the

other hand, that the Policy Research Council of the Democratic Party would

play an important role in policy-making under the new Prime Minister who

took office on June 8, 2010, and the ministerial policy councils would be abol-

ished. Secondly, due to the suspension of the public Financial System Council,

the fundamental philosophy and overall policy direction of financial reform has

not been well clarified, the transparency of the policy-making process has not

been well ensured, and the opinions of interested parties from the private sector

have not been sufficiently reflected in policy-making. Thirdly, reflecting the

new policy-making process, the influence of the three leaders of the FSA and

the FSA bureaucrats is now rather greater than in the past.

(3) Trends in Financial Administration and Management

under the New Government

No particular changes have appeared in the management of enforcement

(financial inspection and supervision and market oversight) as a result of finan-

cial administration under the new government. Decisions by officials of the

FSA, Securities and Exchange Surveillance Commission continue to set a politi-

cally neutral administrative agenda.

Moreover, the three leaders of the FSA from the new administration have

not mentioned the so-called “better regulation,” or qualitative improvements to

financial regulation, proposed by the commissioner of the FSA under the for-

mer administration in July 2007. The Financial Services Authority of Great

Britain, the originator of the term “better regulation,” has focused exclusively

on strengthening financial regulation and supervision following the financial

crisis and has also stopped mentioning better regulation.

In this regard, under the new administration FSA officials have not deviated

from their noteworthy efforts to further define and promote better regulation.

The first pillar of better regulation is optimum integration of rule-based and

principle-based supervision. Clarity and predictability in the application of regula-

tions are important in Japan’s legal environment, and principle-based regulation is

unfamiliar. Given this background, methods for enforcing financial regulation in

Japan are influenced by the inspection- and inspector-based supervisory approach of

the U.S. rather than the supervisory approach of the British model.

(4) Legal Foundation of Financial Regulation

Financial management and administration in Japan rel ies more on

“Supervisory Guidelines” and “Inspection Manuals” than on laws and regula-

2. New Developments in the Regulation and Supervision ofJapan’s Non-Life Insurance Industry

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 13/43

11

tions as the source of regulatory supervision. Supervisory Guidelines and

Inspection Manuals are akin to guidebooks for the staff of government agencies,

and technically are not legally binding on financial firms. In actual practice,

however, the points of supervision and inspections indicated in Supervisory

Guidelines and Inspection Manuals have de facto binding force on financial

firms, which manage their operations accordingly.

Supervisory Guidelines and Inspection Manuals are easier to understand

than laws and regulations, and allow flexible revision as required by changing

circumstances. Moreover, they offer transparency in the process of formulation

because they are established after being open to public comment. On the other

hand, recent financial administration has in substance revived a kind of admin-

istrative ordinances by using “detailed refinement” of Supervisory Guidances

and Inspection Manuals and expanding elements of administrative guidance.

A pattern of reviving administrative ordinances has emerged in the area of

insurance regulation. Insurance companies must now provide potential cus-

tomers with a contract summary, key reminders, and a written acknowledge-

ment of intention. Except for the written contract summary and key reminders

that are legally required prior to the conclusion of a contract for insurance

products with high emphasis on investment such as variable insurance products

and foreign currency denominated insurance products (specified insurance con-

tracts), these documents do not have a clear legal basis and are practically based

on the FSA’s supervisory guidelines for insurance companies. Their nature is

policies for administrative guidance.

This kind of administration seems to be of a different nature from the per-

spective of the thorough application of fair and transparent financial administra-

tion based on clear rules. A duty of providing these documents should be clearly

stipulated in the Insurance Business Act and its regulations. However, the new

government has not seemed to hold this view, and the reliance on the use of

Supervisory Guidelines and Inspection Manuals does not seem likely to change.

(1) Basic Philosophy

The basic philosophy underlying Japan’s response to the global financial

crisis did not come from the administration, but from the suspended Financial

System Council and the report of its Roundtable Committee on Fundamental

Issues of the Financial System Council, “Designing the Japanese Financial

System in Light of the Global Financial Cris is” (December 9, 2009;

“Roundtable Report”).

At the start of the twenty-first century, Japan intended to move to a two-

track financial system that includes the industrial finance model of financial

intermediation through bank deposits and loans but centers on the market

3. Japan’s Administrative Response to the Global Financial Crisis

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 14/43

12

financing model of market-based financial intermediation. Given the concen-

tration of risk in the banking sector, the worsening problem of non-performing

loans, and the increasingly challenging real economy, it was assumed that the

market financing model could broadly diffuse risk with choices of numerous

market participants.

In this regard, the Roundtable Report made three key points.

First, it stated that while maintaining the two-track financial system con-

tinues to be a key challenge for Japan’s financial system, because the global

financial crisis originated in the markets, it is important that a two-track finan-

cial system does not excessively depend on market-based finance but is based on

the right balance between market-based finance and financing made through

deposit-taking and lending in the banking sector.

Second, it pointed out challenges for the financial services industry, saying

financial institutions must properly perform their social responsibility, and

must engage in financing that supports the creation of value by companies,

rather than a business model that depends on “arbitrage transactions” focusing

on the distortion of the price system and price volatility. It also indicated the

importance of seeking to achieve the development of the financial industry by

supporting the creation of value of domestic and foreign companies.

Third, the Roundtable Report said that the “3S” approach is important to

efforts to design the future financial system: i.e., (1) ensuring the suitability to

the ac tua l c i rcumstances o f the marke t s and the f inanc ia l indust ry

(“Suitability”), (2) supporting the sustainable functioning of financial interme-

diation and sustainable economic growth (“Sustainability”) and (3) securing the

stability of the financial system (“Stability”).

(2) Policy Responses and Measures

In the current global financial crisis Japan’s financial system is compara-

tively stable, and Japan’s policy responses and measures will therefore be based

on the “3S” approach. An examination of relevance to the non-life insurance

sector follows.

First, while the consolidated regulatory and supervisory framework has

been established with regard to insurance companies and insurance holding

companies under the Insurance Business Act, in May 2010 the Diet passed

amendments to the Insurance Business Act that include a standard for consoli-

dated financial soundness using the consolidated solvency margin. The

Roundtable Report stated that through the current financial crisis, “It has also

become clear that, in the insurance sector as well, imbalances that could trigger

a financial crisis may be accumulated through group companies.” The subse-

quent G20 summit debate on the Financial Stability Board (FSB) and the

International Association of Insurance Supervisors (IAIS), and the EU’s pro-

2. New Developments in the Regulation and Supervision ofJapan’s Non-Life Insurance Industry

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 15/43

13

posed introduction of the Solvency II standards in 2012 also served as the basis

for the Diet’s amendments. The new amendments must be put into effect on a

date to be specified by a Cabinet Order within two years of the date the amend-

ed law comes into force, meaning no later than May 18, 2012.

Second, the FSA has announced that on April 9, 2010 it revised the solvency

margin used as an indicator in assessing the financial soundness of insurance com-

panies. The revision includes the changes of a risk coefficient and margin items,

and it will go into force on March 31, 2012. The FSA also plans to study the

future introduction of solvency assessment based on economic value.

Third, on March 4, 2010 the FSA revised Supervisory Guidelines to

include the compensation structure of insurance and other companies with

operations such as overseas bases. This revision was based on the FSF Principles

for Sound Compensation Practices (April 2, 2009) of the Financial Stability

Forum (FSF) and the FSB Principles for Sound Compensation Practices -

Implementation Standards (September 25, 2009) of the FSB. Thus regulation

of compensation systems in Japan is the result of supervisory measures rather

than legal amendment. This revision appears to indicate that the compensation

system of Japanese insurance companies is not generally recognized as a cause of

excessive risk-taking among executives and employees.

Fourth, the Supervisory Guidelines for Insurance and Other Companies of

August 18, 2009 for FSA’s fiscal year ending June 30, 2010 stressed that insur-

ance companies must enhance the sophistication of risk management in light of

the financial crisis. On June 8, 2009, the FSA revised Supervisory Guidelines to

add items including comprehensive risk management, the use of stress testing,

management of the risk of investing in securitized financial instruments and

management of the risk of financial guarantee insurance and credit default swap

transactions as central tenets of supervisory guidance.

It is important to recognize that the Cabinet decision on June 18, 2010

regarding “The New Growth Strategy-Blueprint for Revitalizing Japan”

includes “financial strategy” as one of the seven strategic areas. The Japanese

Government will set out to take concrete steps immediately in 2010 with a view

to build a “new financial market-based nation,” which will play a significant

role as an Asian financial center in the growth process of the global economy

driven by Asian and other emerging economies. In view of the eagerness of the

non-life insurance companies in Japan to expand their businesses in Asia, such

policy approach is greatly welcomed from the viewpoint of enhancing interna-

tional competitiveness of Japan’s financial markets and financial industry

including non-life insurance industry.

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 16/43

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 17/43

15

3. Katsuo Matsushita Special Advisor and Liaison Officer for Japan and East Asia of

the Geneva Association

Challenges of the Major Japanese GeneralInsurance Groups in Promoting GlobalOperations

In order to address challenges caused by the financial crisis, a series of regulatory

initiatives have been undertaken by international forums such as the G20, FSB

(Financial Stability Board), Basel Committee, IOSCO and IAIS with the main focus

on the prevention of systemic risk.

In the wake of the Greek sovereign crisis, how to deal with an excessive budget

deficit and government debt in developed countries has been the focal point of dis-

cussion at the G20 Summit held in Toronto in late June, 2010.

Also, the risk landscape has been constantly evolving, including the volcanic

eruption suspending the international supply chain and the huge oil spill in the Gulf

of Mexico causing devastating environmental damage. It continues to be a tough

time for both governments and markets, for regulator and the regulated. Against this economic and regulatory backdrop, major Japanese general insur-

ance groups (MS&AD Holdings, NKSJ Holdings and Tokio Marine Holdings) have

been promoting international operations. I would like to discuss briefly the chal-

lenges and opportunities in their pursuit of strategic achievement.

There are three main reasons for strategic operations beyond the national market.

(1) To respond to the global operations of Japanese companies and their insuranceneeds, general insurance groups are expanding insurance and risk management

service networks globally as well. Given the recent trend where not only major

multinational companies but also SMEs are also investing and participating in

international supply-chain, cross border insurance service networks have become

an ever more important competitive edge.

(2) While we cannot predict exactly to what extent diversification credit will be

allowed under the international solvency framework now discussed in the IAIS, it

is desirable and prudent to make the insurance portfolio more geographically

diversified through international primary and reinsurance undertaking.

(3) Like any other global insurance group, for major Japanese general insurance

groups, the search for opportunities for sustainable growth is one of the drivers

for investment beyond national borders, especially into emerging markets.

Japanese insurers do not intend to develop international networks from scratch.

They will activate the existing international networks and business models as a lever

(when appropriate) to upgrade services and evolve themselves into truly international

service providers. Let me introduce the following:

(1) A current international service network: The three groups, combined, now have

more than 100 subsidiaries, affiliated companies and branches in around 30

countries with national staff around 30,000.

2. Rationale of Global

Operations

1. Introduction

3. Lever and Stepping Stones for Global Operations

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 18/43

16

(2) A relatively strong financial buffer and ratings assigned by international rating

agencies which remain at a comparable level with other insurers with multina-

tional presence.

(3) A competitive Japanese insurance market and demanding customers have been

encouraging Japanese insurers to develop risk solutions tailored to each risk prob-

lem and risk situation of customers through combining risk financing and loss

prevention/risk management services.

(4) On the retail side or personal lines of insurance, Japanese insurers are competing

through various types of sales channel such as agents, banks and direct marketingto meet the needs of segmented customers. Also, cross selling of general and life

insurance products through various channels has been promoted. These experi-

ences will be worth applying in host markets with appropriate, customized modi-

fication.

(5) While agents remain the main communication line between customers and

insurers, Japanese insurers have also been putting emphasis on direct communi-

cation and feedback from customers in order to strengthen their commitment to

the quality of services and product/service development.

After the financial crisis, the G20, the political forum, initiated a stronger push

for reform and the FSB (Financial Stability Board) has increased its influence over

the global regulatory agenda, assigning a mandate to international standard setters,

including the IAIS, to deliver internationally consistent regulation and its timely

implementation.

Regulatory focus has shifted from micro-prudential supervision to macro-

prudential supervision, from solo-entity to group-wide supervision aiming at the

prevention of the recurrence of systemic risk.

As a lesson from the financial crisis, the IAIS recognized that a coherent, com-

prehensive and effective policy/regulatory response is called for to address the grow-

ing presence of insurance groups and insurance-related conglomerates. This is a clear

paradigm shift in insurance regulation and the Executive Committee of the IAIS

decided to build ComFrame (Common Framework for the Supervision of

Internationally Active Insurance Groups, IAIGs) in January 2010. According to a

leading member of the IAIS subcommittee in charge of this initiative, ComFrame is

designed to address holistically the risks arising in groups and to provide a global

supervisory approach with an expected building phase from 2010 to 2013.

Insurance industry associations and insurance companies have been presenting

their respective positions to minimize the possibility of overly burdensome regulation

(especially excessive capital requirement) being introduced. The Geneva Association

with membership of around 80 CEOs from the world’s top (re)insurance companies

4. Overview of Recent Regulatory Landscape

3. Challenges of the Major Japanese General Insurance Groups in Promoting Global Operations

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 19/43

17

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

sent letters to the G20, FSB and the IAIS, advocating that while they welcome the

right regulation, it is highly important that any solutions designed to increase the

resilience of the financial system appropriately acknowledge the difference in character-

istics of insurance from other financial services such as banks. Three Japanese insurance

groups are sharing this position as members of the Geneva Association. International

insurance communities, especially in developed markets, are also reiterating the promo-

tion of regulatory harmonization and convergence (when appropriate) to bring effi-

ciency to insurance markets and, ultimately, lower prices to consumers.

To address the new, economic value-based (risk-based) solvency framework

now discussed in the international forum is a “must” for the successful deployment

of strategic insurance operations. This is because solvency is not just a capital

requirement. It is more about risk management, especially an upgrade of ERM

(Enterprise Risk Management), and ultimately quality of management. Without

this, a competitive credit rating may be hard to maintain. Enhancement of ERM

needs change in corporate culture as well, for example, from silo to holistic, and a

shift to simple and agile communications with operating entities and employees

located in many jurisdictions.

While adapting to the risk-based, group-wide solvency framework is a big chal-lenge, Japanese insurance groups are responding to this challenge by recognizing pos-

itive momentum in the process of its adaptation. Namely, momentum for: (A)

Strategic shift toward more focus on quality of management and services rather than

quantity, (B) Enhanced risk management across the organization, group companies,

(C) Efficient capital allocation, including the integration of reinsurance purchase

policy into capital management.

Policyholders’ increasing concern about the security of insurers and the cost of

insurance in the difficult economic climate, empowered consumers and increasing

responsibility of management along with a shift to principle-based regulation are the

driving forces toward a focus on ERM and quality management.

One of the most critical challenges is how to translate the risk-based, risk-sensi-

tive solvency framework into truly risk-based underwriting (pricing, terms and con-

ditions, etc.) and strategic capital allocation. This is an essential pre-condition to

build and maintain a sustainable insurance market, providing availability and afford-

ability of basic insurance cover throughout benign and tough economic situations.

To this end, the insurance industry has to address regulatory barriers in some juris-

dictions that will hinder risk-based underwriting. An important aspect of risk-based

pricing is that it will eventually provide insurance purchasers with an incentive to

improve their risk, for example, through more careful driving behavior and abiding

by a stricter building code, thus making our society safer and more resilient against

natural disasters and any other type of risk. Sharing this view, one of the US regula-

tors emphasized in the recent Geneva Association’s General Assembly held in Zurich

that providing these incentives is a part of the social responsibility of insurers.

5. Challenges Ahead under Risk-Based Solvency Regime

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 20/43

18

To help host countries achieve these, Japanese insurers are expected to con-

tribute in providing experience and know-how in order to build an industry database

on top of business activities.

Insurance is and will continue to be a human-related and communication-

driven business. Insurance begins with caring for people and empathy with people,

especially those exposed to hazards, potential catastrophes and victims or injured

persons as a result of the occurrence of accidents or disasters. For the sustainable and

sound management of an insurance group, team spirit, fair evaluation and an

open-communication culture are critical. Human resource development and

appropriate assignment throughout the whole group are one of the key success

factors.In line with group-wide ERM, effective internal control and financial reporting

system, and an IT platform that will support agile communication and information

sharing covering the global operation are an indispensable part of core competence.

Despite the geographical location of Japan, so prone to natural hazards such as

earthquake and typhoon, our market has been developing in a sustainable way and

insurers have been keeping a resilient financial position to date. We have a built-in

system which supports this. For example, an earthquake insurance scheme for resi-dential houses, public and private sector partnership to protect households against

earthquake risk, has been providing a kind of template to other countries in disaster-

prone areas.

Another example is catastrophe reserve provision against large-scale risks. While

booking this reserve as liability may not be allowed under the current discussions of

the international accounting standard, given the repeated emphasis by the G20 and

FSB on the importance of building a financial buffer during benign times and diffi-

culty of raising capital in the capital market shortly after a large-scale disaster, the

necessity of this type of reserve is worth refocusing and serious discussion in jurisdic-

tions exposed to catastrophic risks. Japanese insurers are expected to provide hands-

on information and experience of such a scheme to host markets.

Our experience and common sense tell us that there is a strong linkage between

prevention of natural disasters and environmental preservation. Let us remember the

serious risk of flood and landslide caused by devastating deforestation. What is bad

for the environment is also bad for disaster prevention. Japanese insurers have been

putting an emphasis on environmental protection and the realization of a low carbon

society by declaring them as part of core corporate values. It is confidently expected

that they will continue to promote these values through their corporate social activi-

ties in host communities.

(The views expressed in this article are those of the author and do not represent the

official position of the organization he is engaged in.)

3. Challenges of the Major Japanese General Insurance Groups in Promoting Global Operations

6. Contribution toCommunity, Society

and Insurance Market in Host Countries

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 21/43

19

4 . Neil C. A. Smith Regional President, ACE Far East

(Vice Chairman, & Past Chairman, of Foreign Non-Life Insurance Association of Japan)

A Foreign Insurer’s Perspective on Japan

As a foreigner originally setting foot on these shores almost 17 years ago I

promised myself that I would never utter the words “Japan is different” during

my tenure in the land of the rising sun. In time, however, I learnt that the non-

life insurance marketplace and business practices are indeed quite different to

what we generally face in many countries around the world (and I’ve worked in

many different markets). When you add in language and cultural differences

you now have a mix that clearly requires a great deal of patience and unique

skills if you are to effectively operate and be successful in this market. This is

the first lesson foreign companies quickly learn when operating here.

Since the early 1990’s, Japan has gone through a continued process of

deregulation as it endeavors to shake off the shackles of the past so it can be

more competitive and hold its head up high in the international insurance fast

lane. This process has freed up certain market sectors (notably the 3rd sector)

and allowed greater product flexibility and improved access to distribution

channels.

The recent industry focus on providing increased customer protection and

improving corporate governance has, however, uncovered a range of poor

industry business practices needing immediate attention and eradication. These

include claims non-payment of fringe benefit covers and incorrect premium

charges for certain products. Whilst companies immediately responded and

addressed these issues, it nonetheless tarnished the image of the industry and it

will take some time to fully restore consumer confidence in the industry.

The revision this past April of Japan’s archaic insurance contract law is the

latest step toward better governance and restoring consumer confidence. These

revisions include insurance contracts and promotional materials with plain and

simple wording, improved guidelines on claims payments, more stringent con-

sumer protection and measures to help consumers better understand insurance

products. We’re also seeing plans to substantially strengthen the quality and

expertise of insurance agents and solicitors, improve the agency examination

process and introduce strong renewable agent accreditation. These actions will

significantly help strengthen the ability, quality and capabilities of the entire

insurance industry. New regulations have been introduced for the Kyosai busi-

ness which have improved and strengthened controls on this previously unregu-

lated industry, but additional improvements are still needed to ensure there’s a

level playing field for everyone. This applies equally to the recently privatized

Japan Post Insurance subsidiary whose broad based distribution network and

business should be governed by the same rules as other competitors within the

non-life insurance industry.

Introduction

Two Decades of Change

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 22/43

20

Japan is a highly regulated environment with restricted freedom around

price and form flexibility. The Non-Life Rating Insurance Organization sets

“pure” premium rates on major lines which the industry follows, and companies

are required to file and get regulatory approval fo r their products. The market is

large and complex and the three largest Japanese companies have around 90%

market share. This is supported by strong historical relationships and all too

often cross shareholdings between major corporations. This situation makes it

difficult for foreign competitors to gain access to large customers.

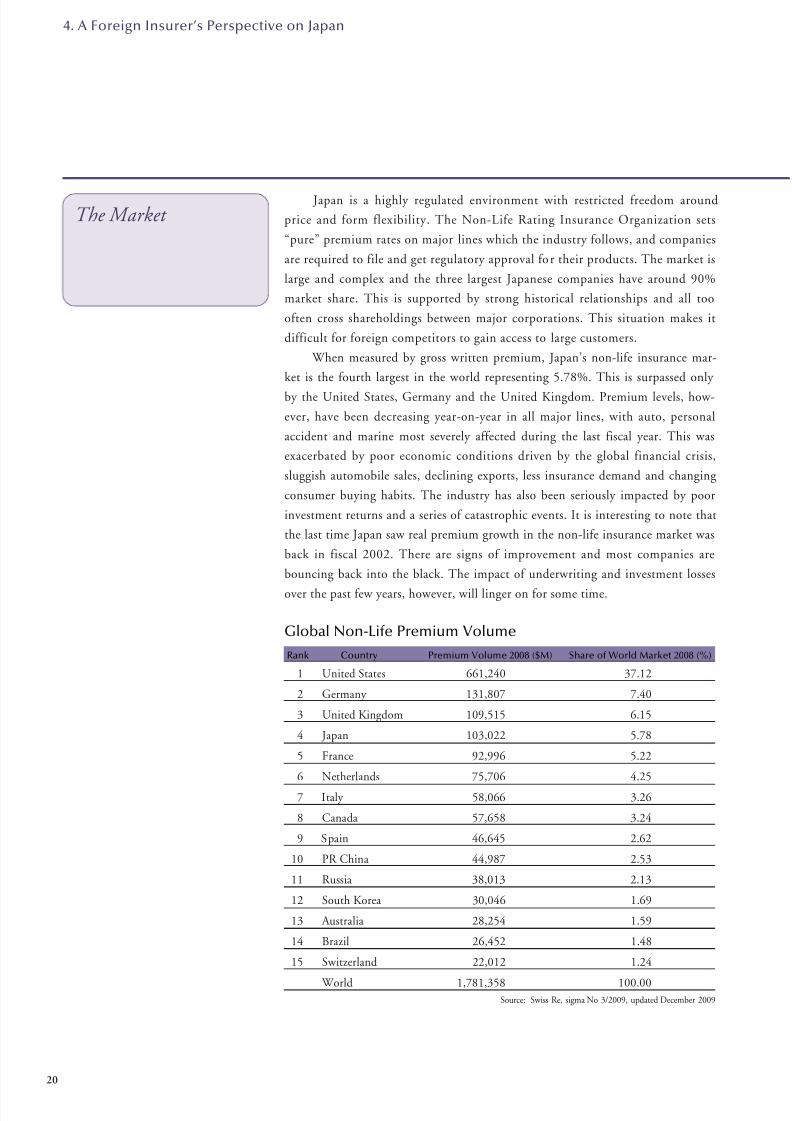

When measured by gross written premium, Japan’s non-life insurance mar-

ket is the fourth largest in the world representing 5.78%. This is surpassed only

by the United States, Germany and the United Kingdom. Premium levels, how-

ever, have been decreasing year-on-year in all major lines, with auto, personal

accident and marine most severely affected during the last fiscal year. This was

exacerbated by poor economic conditions driven by the global financial crisis,

sluggish automobile sales, declining exports, less insurance demand and changing

consumer buying habits. The industry has also been seriously impacted by poor

investment returns and a series of catastrophic events. It is interesting to note that

the last time Japan saw real premium growth in the non-life insurance market was

back in fiscal 2002. There are signs of improvement and most companies are

bouncing back into the black. The impact of underwriting and investment losses

over the past few years, however, will linger on for some time.

The Market

4. A Foreign Insurer’s Perspective on Japan

Global Non-Life Premium Volume

Rank Country Premium Volume 2008 ($M) Share of World Market 2008 (%)

1 United States 661,240 37.12

2 Germany 131,807 7.40

3 United Kingdom 109,515 6.15

4 Japan 103,022 5.78

5 France 92,996 5.22

6 Netherlands 75,706 4.25

7 Italy 58,066 3.26

8 Canada 57,658 3.24

9 Spain 46,645 2.62

10 PR China 44,987 2.53

11 Russia 38,013 2.13

12 South Korea 30,046 1.69

13 Australia 28,254 1.59

14 Brazil 26,452 1.48

15 Switzerland 22,012 1.24

World 1,781,358 100.00Source: Swiss Re, sigma No 3/2009, updated December 2009

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 23/43

21

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

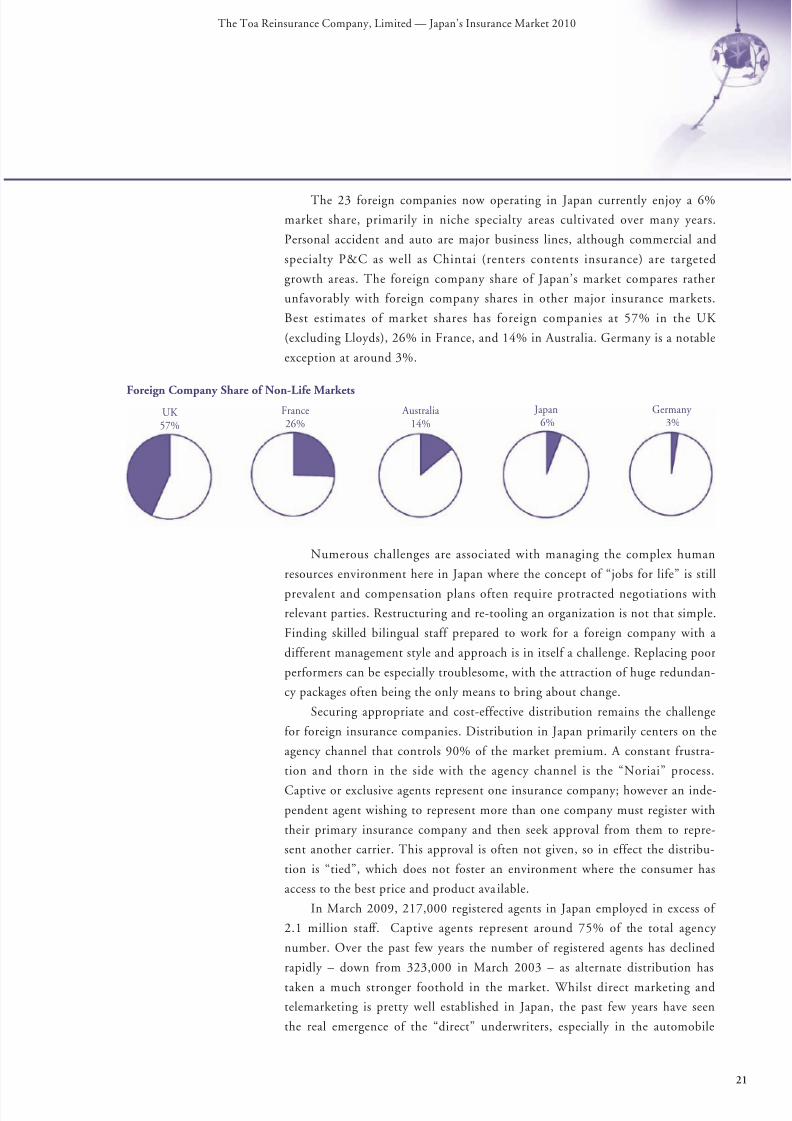

The 23 foreign companies now operating in Japan currently enjoy a 6%

market share, primarily in niche specialty areas cultivated over many years.

Personal accident and auto are major business lines, although commercial and

specialty P&C as well as Chintai (renters contents insurance) are targeted

growth areas. The foreign company share of Japan’s market compares rather

unfavorably with foreign company shares in other major insurance markets.

Best estimates of market shares has foreign companies at 57% in the UK

(excluding Lloyds), 26% in France, and 14% in Australia. Germany is a notable

exception at around 3%.

Numerous challenges are associated with managing the complex human

resources environment here in Japan where the concept of “jobs for life” is still

prevalent and compensation plans often require protracted negotiations with

relevant parties. Restructuring and re-tooling an organization is not that simple.

Finding skilled bilingual staff prepared to work for a foreign company with a

different management style and approach is in itself a challenge. Replacing poor

performers can be especially troublesome, with the attraction of huge redundan-

cy packages often being the only means to bring about change.

Securing appropriate and cost-effective distribution remains the challenge

for foreign insurance companies. Distribution in Japan primarily centers on the

agency channel that controls 90% of the market premium. A constant frustra-

tion and thorn in the side with the agency channel is the “Noriai” process.

Captive or exclusive agents represent one insurance company; however an inde-

pendent agent wishing to represent more than one company must register with

their primary insurance company and then seek approval from them to repre-

sent another carrier. This approval is often not given, so in effect the distribu-

tion is “tied”, which does not foster an environment where the consumer has

access to the best price and product ava ilable.

In March 2009, 217,000 registered agents in Japan employed in excess of

2.1 million staff. Captive agents represent around 75% of the total agency

number. Over the past few years the number of registered agents has declined

rapidly – down from 323,000 in March 2003 – as alternate distribution has

taken a much stronger foothold in the market. Whilst direct marketing and

telemarketing is pretty well established in Japan, the past few years have seen

the real emergence of the “direct” underwriters, especially in the automobile

UK 57%

France26%

Australia14%

Japan6%

Germany 3%

Foreign Company Share of Non-Life Markets

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 24/43

arena. Many of these direct writers are foreign companies. This direct sales

channel now has around 7% market share – still well below the 32% direct sales

share of the UK personal lines market and the 12.6% direct response share in

the USA, so there’s still plenty of room for this channel to grow.

Another channel still in its infancy and with huge potential is the broker

channel. Brokers represent the customer/client, but at this juncture they are

limited to providing consultative services. If and when their role is expanded

along the lines of the rest of the world, this channel will play a much more

important role within the overall distribution channel mix.

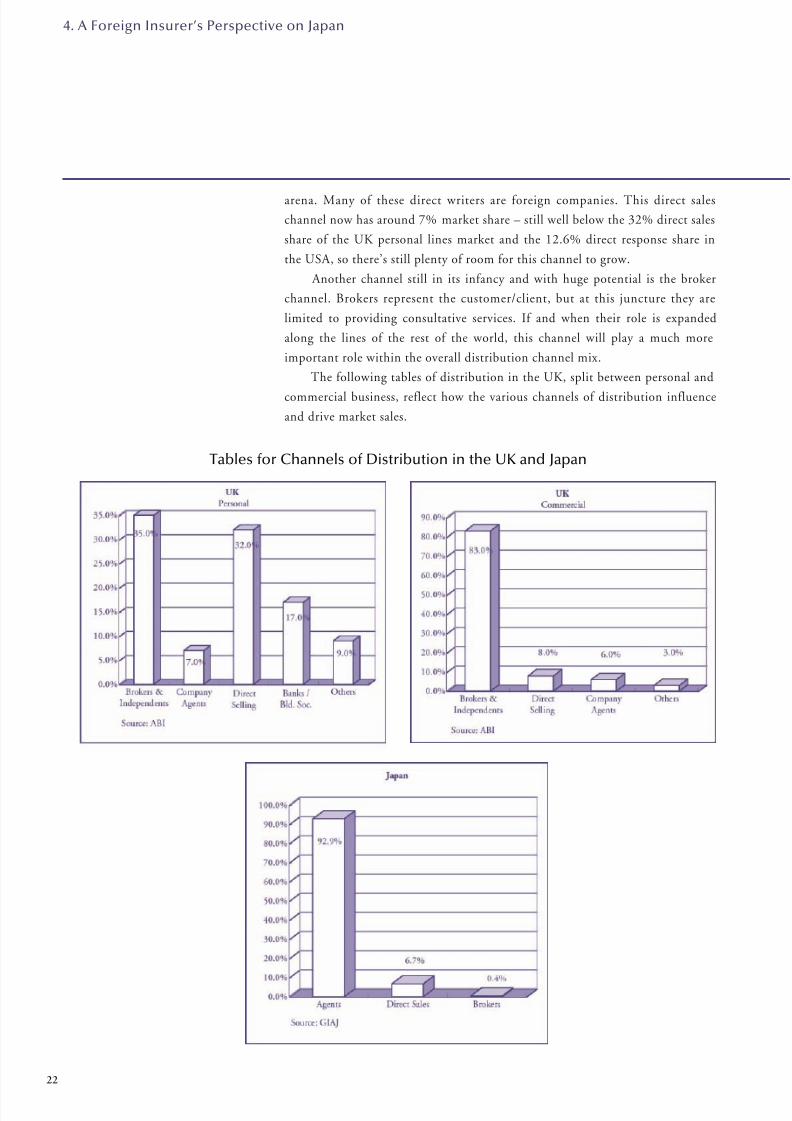

The following tables of distribution in the UK, split between personal and

commercial business, reflect how the various channels of distribution influence

and drive market sales.

22

4. A Foreign Insurer’s Perspective on Japan

Tables for Channels of Distribution in the UK and Japan

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 25/43

23

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

Market Attractiveness

As stated earlier, expanded governance has resulted in significantly more

requirements for companies. These include improving claims service, increased

documentation, cross checking, the introduction of the new insurance contract

law, the establishment of new alternative dispute resolution (ADR) capabilities,

enhancing customer protection and generally improving overall compliance.

This has increased the expense and cost structure for small foreign companies

not having the breadth and scale of large Japanese competitors.

Despite all the difficulties and potential barriers to entry, the Japanese

market-place remains attractive. As a player on the global insurance stage one

simply cannot afford not to be part of this important market and help drive

change over the coming years.

Areas that specifically stand out as attractive include the following:

• The stability of the market which means there’s less volatil ity in terms of pric-

ing.

• The quality of risk is good as evidenced by loss ratios in chosen sectors/

segments.

• Improving and heightened risk management. The way of managing risk

will likely be enhanced with more emphasis on the risk manager role and

responsibilities.

• Financial crises and subsequent market consolidation over time will drive

increased flight to quality via fewer competitors. Customers will seek more

choice as they look to spread their risk.

• Foreign companies delivering new products and added value services will

prosper. Knowledge transfer from overseas markets to Japan is critical as dif-

ferentiation will eventually win the day.

• Japanese companies are increasingly becoming more global and/or seeking

global partners as evidenced by the activities of Nippon Ita Garasu, Nomura

Securities, Sony Corporation, Japan Tobacco and more recently some of the

large Japanese insurers. Global expansion, fuelled by lack of domestic

demand, will undoubtedly bring new ideas, products and management tech-

niques to Japan. Many large traditional Japanese corporations have already

recruited foreign leaders and senior management to supplement their existing

management structure.

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 26/43

This complex, mature market has historically been slow to change; however it

is clearly catching up and embracing new ideas and learning from other market

experiences. The question constantly on our minds is how quickly will full

deregulation (products and pricing) be introduced, if ever. I believe the real

process of change is already long under way and this cannot and will not be

allowed to regress over the coming years. Old, outdated practices will disappear.

Major challenges, however, remain. These include the following:

• Market domination by large Japanese insurance companies

• Keiretsu and cross shareholdings

• Real freedom of product and price

• Noriai practice

• Brand recognition and strong customer loyalty to large traditional Japanese

carriers

• Access to cost effective distribution

• Low awareness of corporate risk management needs

• Expense management and containment

• Management of catastrophic risk

ACE has operated in Japan (under the banners of AFIA, INA, CIGNA and

now ACE) for close to 90 years, although our current market presence and size

may not adequately reflect the effort we have exerted over this period. We have

established a good market niche for our chosen products and services and built

an appropriate infrastructure to support this business. We are now focusing on

developing a medium- to long-term plan that will harness the power of the

global ACE platform and look to grow in this stagnant market. This effectively

means the introduction of new products to the market, expanding our presence

(where we have strong capabilities) in areas where we’re not currently active,

building world class operational and claims centers of excellence, promoting

customer protection and delivering sustainable growth and profit to ACE

Limited shareholders.

ACE Japan has a strong and important role to play in being an active

member in this unique and strategically important insurance market.

24

4. A Foreign Insurer’s Perspective on Japan

Market Challenges

The ACE Direction

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 27/43

25

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

Looking Ahead The road ahead will undoubtedly be challenging. To affect meaningful

change in Japan’s non-life insurance industry, a number of things need to take

place:

• The government must first tackle its responsibilities around economic reform

and financial stimulation.

• The insurance market needs a period of stability to once again earn customer

trust and respect.

• Mega mergers and consolidations should be reined in.

• Regulators should continue their good work along the path of continued

deregulation to further free up the market.

• Archaic practices must be stamped out in order to level the playing field for

all entrants and competitors.

• Japanese companies should accelerate globalization efforts and introduce new

leadership and best practices to the market.

• Foreign companies should be encouraged to expand their presence and inject

new energy – and capital – into their Japan businesses so that they become

even more strategically important to their global platforms.

After so many years and two assignments here, I now have to admit that

Japan is indeed different. Nevertheless, when you understand and appreciate

how this part of the world ticks, I truly believe that foreign companies can be

successful and help to make a difference. Those who develop the right business

model, the right distribution mix, and who employ correct risk and capital

management strategies and have underwriting discipline as their core competen-

cy will certainly prosper in the future. And of course it goes without saying that

without strong leadership, no one will survive.

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 28/43

26

5 . Underwriting & Planning Department The Toa Reinsurance Company, Limited

Trends in Japan’s Non-Life Insurance Industry

(1) Domestic Market

Net premium income of the 9 major domestic non-life insurance companies

decreased in Fiscal 2009 for the third consecutive year. This was because of a decline

in motor insurance, a mainstay product, as well as in marine insurance resulting

from a decline in marine freight due to the global economic recession.

In the previous year, these companies posted a significant fall in ordinary profit

due to large losses on revaluation of securities associated with the financial crisis.

However, their ordinary profit increased in Fiscal 2009 due to the recovery in the

equity market.

(2) Industry Reorganization

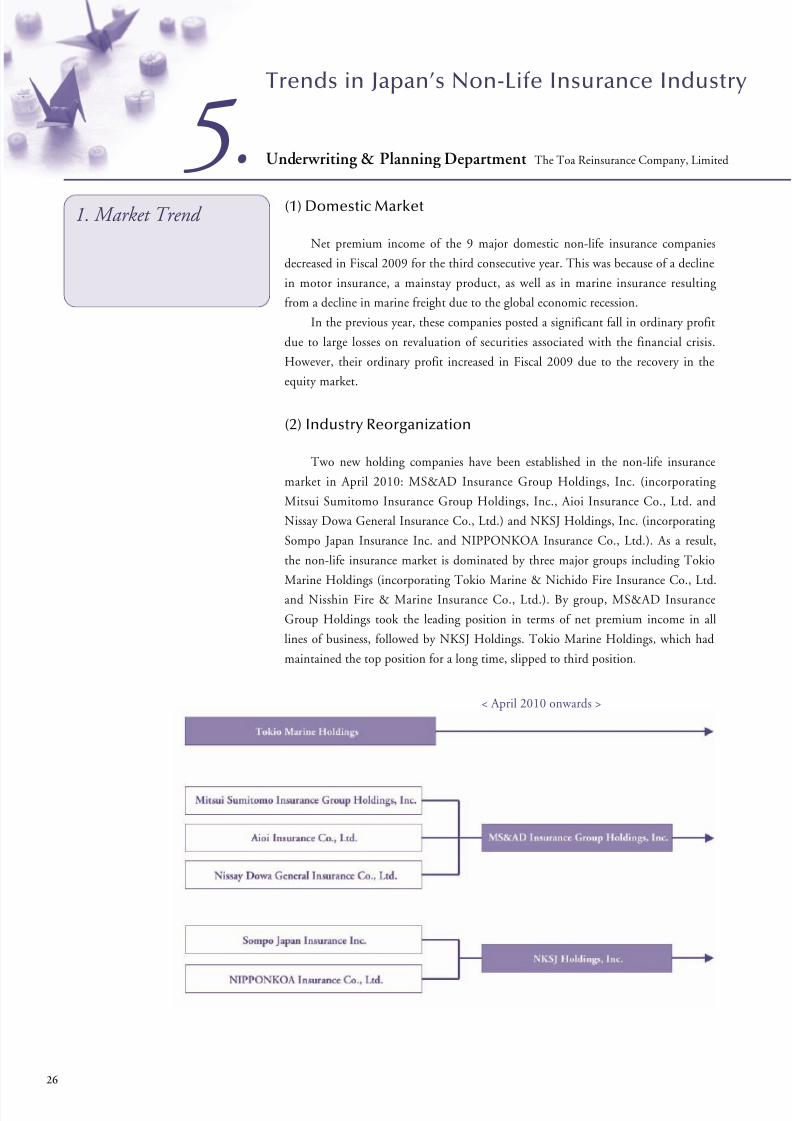

Two new holding companies have been established in the non-life insurance

market in April 2010: MS&AD Insurance Group Holdings, Inc. (incorporating

Mitsui Sumitomo Insurance Group Holdings, Inc., Aioi Insurance Co., Ltd. and

Nissay Dowa General Insurance Co., Ltd.) and NKSJ Holdings, Inc. (incorporating

Sompo Japan Insurance Inc. and NIPPONKOA Insurance Co., Ltd.). As a result,

the non-life insurance market is dominated by three major groups including Tokio

Marine Holdings (incorporating Tokio Marine & Nichido Fire Insurance Co., Ltd.

and Nisshin Fire & Marine Insurance Co., Ltd.). By group, MS&AD Insurance

Group Holdings took the leading position in terms of net premium income in all

lines of business, followed by NKSJ Holdings. Tokio Marine Holdings, which had

maintained the top position for a long time, slipped to third position.

1. Market Trend

< April 2010 onwards >

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 29/43

27

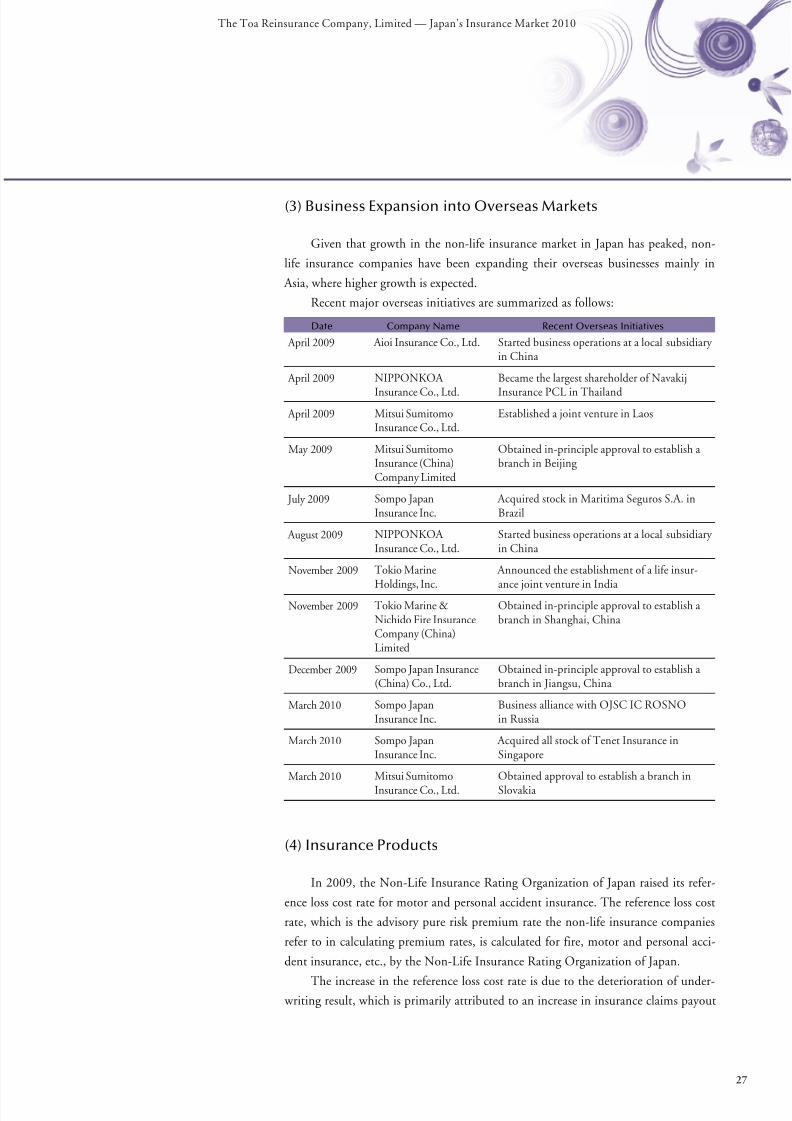

(3) Business Expansion into Overseas Markets

Given that growth in the non-life insurance market in Japan has peaked, non-

life insurance companies have been expanding their overseas businesses mainly in

Asia, where higher growth is expected.

Recent major overseas initiatives are summarized as follows:

(4) Insurance Products

In 2009, the Non-Life Insurance Rating Organization of Japan raised its refer-

ence loss cost rate for motor and personal accident insurance. The reference loss cost

rate, which is the advisory pure risk premium rate the non-life insurance companies

refer to in calculating premium rates, is calculated for fire, motor and personal acci-

dent insurance, etc., by the Non-Life Insurance Rating Organization of Japan.

The increase in the reference loss cost rate is due to the deterioration of under- writing result, which is primarily attributed to an increase in insurance claims payout

Date Company Name Recent Overseas Initiatives

April 2009

April 2009

April 2009

May 2009

July 2009

August 2009

November 2009

November 2009

December 2009

March 2010

March 2010

March 2010

Aioi Insurance Co., Ltd.

NIPPONKOA

Insurance Co., Ltd.

Mitsui SumitomoInsurance Co., Ltd.

Mitsui SumitomoInsurance (China)Company Limited

Sompo JapanInsurance Inc.

NIPPONKOA Insurance Co., Ltd.

Tokio Marine

Holdings, Inc.Tokio Marine &Nichido Fire InsuranceCompany (China)Limited

Sompo Japan Insurance(China) Co., Ltd.

Sompo JapanInsurance Inc.

Sompo JapanInsurance Inc.

Mitsui Sumitomo

Insurance Co., Ltd.

Started business operations at a local subsidiary in China

Became the largest shareholder of Navakij

Insurance PCL in Thailand

Established a joint venture in Laos

Obtained in-principle approval to establish abranch in Beijing

Acquired stock in Maritima Seguros S.A. inBrazil

Started business operations at a local subsidiary in China

Announced the establishment of a life insur-

ance joint venture in IndiaObtained in-principle approval to establish abranch in Shanghai, China

Obtained in-principle approval to establish abranch in Jiangsu, China

Business alliance with OJSC IC ROSNOin Russia

Acquired all stock of Tenet Insurance inSingapore

Obtained approval to establish a branch in

Slovakia

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 30/43

resulting from the improvement of payment practices among the non-life insurance

companies following the problem of unpaid insurance claims. In addition, the

increase was influenced by the following factors: a decline in motor insurance premi-

um income due to a rise in the number of compact cars with low premium rates, an

increase in the number of policy holders with highly discounted accident-free rates, a

decline in the number of young drivers with high premium rates, and an increase in

personal accident insurance claims payout due to the rise in permanent disability

benefit payments, mainly to elderly people, as well as because of the extended num-

ber of days for insurance benefit for outpatients.

Following the increase in the reference loss cost rate, the non-life insurance

companies announced an increase in premiums for motor and personal accident

insurance.

(5) Distribution Channels

The non-life insurance companies are striving to increase sales through tie-ups

with communications companies.

In June 2009, Tokio Marine Holdings, Inc. established “E.design Insurance

Co., Ltd.” with NTT FINANCE CORPORATION. The joint venture has started

business operations. In March 2010, Tokio Marine & Nichido Fire Insurance Co.,

Ltd. announced a business alliance with NTT DOCOMO, Inc. and Aioi Insurance

Co., Ltd. announced the establishment of a joint venture with KDDI Corporation.

Through distribution channels such as mobile phones and the Internet, these new

companies offer products characterized by substantial reductions in the procedural

requirements and time required to buy a product in comparison with doing so

through an insurance agent.

These companies aim to acquire young customers, many of whom are mobile

phone and Internet users.

(6) Regulations on Co-operatives

In accordance with implementation of the revised Insurance Business Law in

2006, the unregulated co-operative sector, which had not been controlled under a

specific law, has also become subject to regulations under the Insurance Business

Law. However, many co-operatives found it difficult to respond to the regulations

and maintain their co-operative business.

In May 2010, the government submitted to the Diet the drafting amendments

of the Insurance Business Law, which would permit the co-operatives conducting

business before 2006 (when the revised Insurance Business Law came into effect) to

conduct business as an “authorized specific insurance business” if they meet certain

requirements. When it comes before the Diet, the Financial Services Agency (FSA)

28

5. Trends in Japan’s Non-life Insurance Industry

8/6/2019 Japan Insurance Market 2010

http://slidepdf.com/reader/full/japan-insurance-market-2010 31/43

29

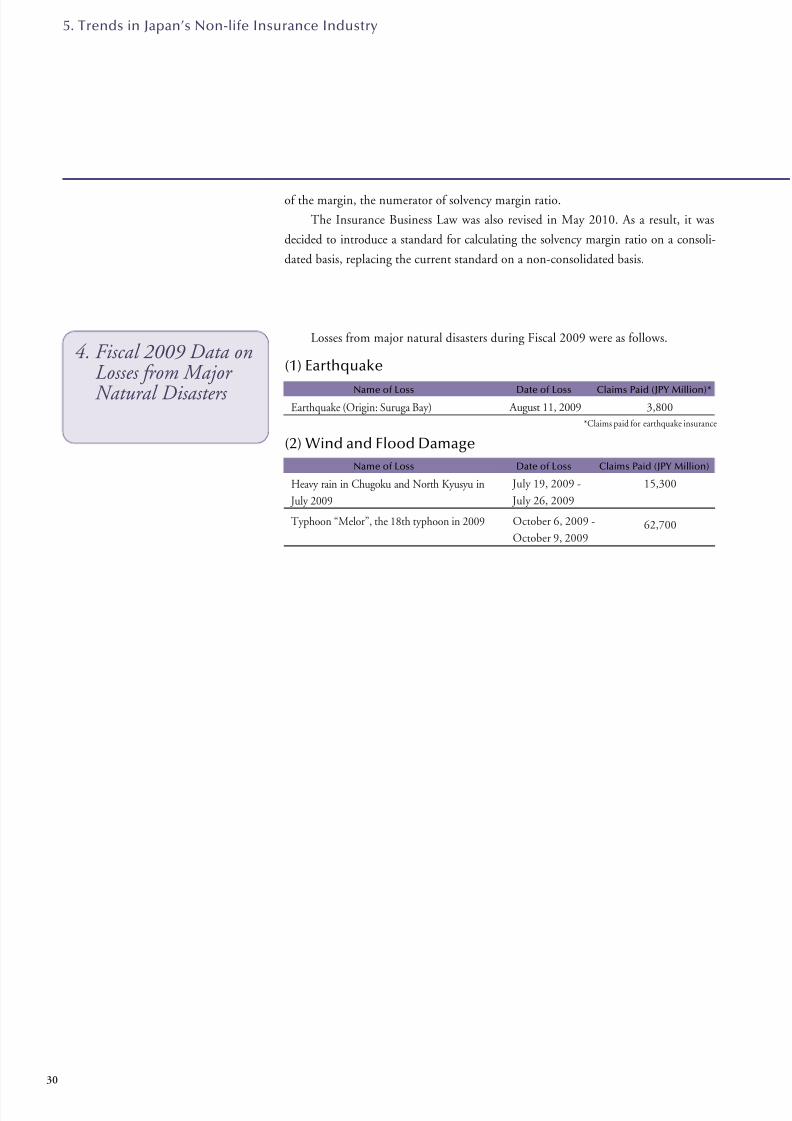

The Toa Reinsurance Company, Limited — Japan’s Insurance Market 2010

estimates that about 700 co-operatives will fall within the scope of the remedial

measures. The future position of these co-operatives will be examined as the meas-

ures are regarded as provisional until the introduction of a new law.

The 27 companies in the General Insurance Association of Japan suffered from

a fall in net premium income in Fiscal 2009 mainly due to a change in premium

rates and weak economy. Ordinary profit and net income moved into the black from

the deficit in the previous fiscal year.

Net premium income was 6,971.1 billion yen, down 190.7 billion yen on a